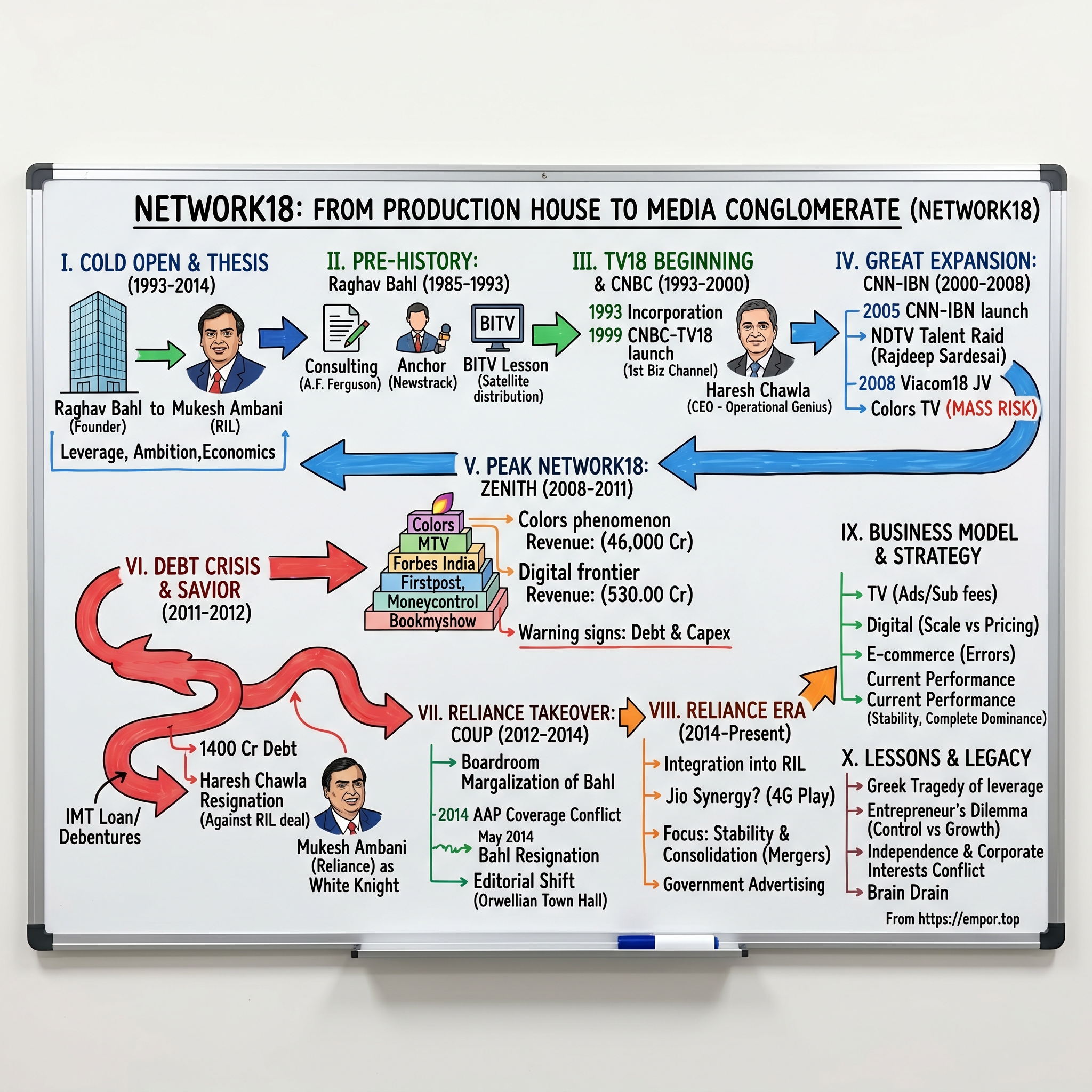

Network18: From Television Production House to India's Media Conglomerate

I. Cold Open & Episode Thesis

Picture this: It's March 2014, and in the glass towers of Mumbai's business district, a media empire is changing hands. Not through a public tender or competitive bidding, but through the quiet conversion of debt instruments that had been ticking like a time bomb for three years. Raghav Bahl, the man who built Network18 from a two-person production house into India's largest news network, watches as control slips away to Mukesh Ambani's Reliance Industries. The price tag reads ₹4,000 crore, but the real story isn't about money—it's about ambition, leverage, and the brutal economics of building media empires in emerging markets.

Network18's journey from a tiny TV production outfit founded in 1993 to becoming India's most extensive media conglomerate is a masterclass in entrepreneurial audacity. At its peak, the company controlled over 35 TV channels, 13 major websites, multiple magazines, and had partnerships with virtually every major global media brand—CNBC, CNN, Viacom, Forbes, BBC, Time Warner. Yet by 2014, its founder was out, its independence lost, and its future tied to the fortunes of India's largest industrial house.

The central question isn't just how a bootstrapped content producer became India's media colossus—it's why that very success became its undoing. This is a story about the fundamental tension between entrepreneurial vision and capital constraints, between editorial independence and financial survival, between building for the long term and surviving the next quarter.

We'll trace three distinct eras: the Raghav Bahl years of relentless expansion (1993-2011), the debt spiral and desperate search for capital (2011-2014), and the Reliance transformation that followed. Along the way, we'll examine why media consolidation seems inevitable in emerging markets, what happens when growth ambitions exceed capital access, and whether true editorial independence can exist when the bills need paying.

The themes that emerge—aggressive debt-funded expansion, the challenge of monetizing news in India, the collision between journalism and corporate interests—aren't just Network18's story. They're the story of Indian media itself, compressed into one company's spectacular rise and dramatic fall from independence.

II. The Pre-History: Raghav Bahl's Entry into Media (1985-1993)

The unlikely media mogul began his journey in the paneled offices of A.F. Ferguson & Co, one of India's most prestigious management consulting firms. Raghav Bahl began his career as a management consultant with A.F. Ferguson & Co, followed by a stint with American Express Bank, but the spreadsheets and strategy decks couldn't contain his restless energy. He graduated from St. Stephen's College, Delhi, with a BA in economics and went on to gain an MBA at the University of Delhi. He became interested in the news at university, where media had been what he called a "parallel love" alongside business.

The pull of television proved irresistible. Working with Doordarshan during his college days held more charm than the job he held. He got his break when Vinod Dua, whom he knew during his DD days, invited him to anchor Newstrack, India's groundbreaking monthly video news magazine produced by the India Today Group. This wasn't just any show—it was India's first monthly video news magazine, a revolutionary format that brought television journalism to Indian homes when most still relied on state-controlled broadcasts.

When TN Ninan, who was supposed to anchor the show with Madhu Trehan, moved out to join The Economic Times, Bahl was offered the anchor's role. Madhu had seen him on air and found him good enough to make the cut. Those two-plus years at the India Today Group introduced him to high quality journalism and professional standards.

India in the late 1980s was a media desert. Doordarshan's monopoly meant one channel, government-controlled content, and zero private broadcasting. But Bahl sensed change coming. In 1991, India relaxed restrictions on satellite TV. At the same time the eruption of the first Gulf War showed that TV channels could use satellite technology to beam 24-hour coverage around the world. The ability to watch it unfolding in real-time saw a leap in the uptake of satellite TV.

From 1991 to 1993, he was the Executive Director of Business India Television and produced the Business India Show and Business A.M. on Doordarshan. But this was also where Bahl learned his first hard lesson about the media business. Ashok Advani, the founder of Business India, decided to start a television channel called Business India TV (BITV), but the venture stumbled badly. The channel chose to save money by using a Russian satellite, requiring cable operators to constantly recalibrate their receivers—a fatal mistake that taught Bahl the importance of distribution and technology choices in media.

By 1993, Bahl was ready to strike out on his own. The stage was set for what would become one of Indian media's most ambitious ventures.

III. The TV18 Beginning & CNBC Partnership (1993-2000)

The seed capital came from a savings account—₹50,000, every rupee Bahl had saved from his corporate days. In 1993, TV18 became a private limited company, incorporated as Television Eighteen India Private Ltd (TEIPL). In September 1993, TV18 was incorporated as Television Eighteen India Private Ltd (TEIPL), getting its first investment from Consortium Finance & Leasing, a company run by Bahl's friends. The investors were given 49% equity—a mistake Bahl would later regret, having given away too much too early.

The early days were scrappy and chaotic. Television Eighteen started as a two-pilot production house, creating content for whoever would pay. The company's inception was quite small; as a start-up, they put together two pilot programs – one was a business program while the other a weekly entertainment cum feature program. Their first major break came from producing The India Show for Star Plus and India Business Report for BBC World—solid work, but nothing revolutionary.

But Bahl understood something fundamental: in the media business, you're either the platform or you're the supplier, and suppliers rarely win. Believing that "news is a broadcaster's, not a producer's game", he decided that the economies of scale presented him with a stark choice: "either expand or shut up shop entirely". The production business was becoming commoditized, margins were shrinking, and channels were bringing production in-house. TV18 needed to evolve or die.

The opportunity came through an unlikely source: a contractual loophole. The network has its origins in ABNi, an Indian sub-feed of the Dow Jones-led Asia Business News (ABN) owned by TV18. In 1997, CNBC reached an agreement to merge its networks in Asia and Europe with Dow Jones under the CNBC banner. However, the agreement for ABNi did not contain any provisions on what would occur in the event of a change in ownership. After discussions with a CNBC lawyer and ABN's CEO Paul France (who led the merged CNBC Asia), TV18 would reach an agreement with CNBC to serve as its Indian partner.

This wasn't just luck—it was preparation meeting opportunity. The timing of this transition of theirs was just perfect because, they were already providing Indian business news for CNBC Asia, and during the same time CNBC had decided to establish itself firmly within the Indian market and as Network18 had already proven their worth, they turned out to become their ideal choice.

The year 1999 marked the transformation. In 1999, he launched CNBC-TV18, India's first dedicated business news channel. But this required capital and credibility. In 1999, he roped in CNBC as a partner. That is what gave it the "gravitas to attract professional talent", Bahl had said in an earlier interview. He hired Haresh Chawla, an Indian Institute of Technology and Indian Institute of Management graduate, with stints at HCL, the Times Group and ABCL, with the promise of a free hand to make whatever changes he felt necessary.

Haresh Chawla's arrival changed everything. Here was an IIT-IIM graduate who'd worked at HCL, Times Group, and Amitabh Bachchan Corporation, brought in with complete operational freedom. Haresh Chawla is considered to be the founding CEO of the company. He was appointed as the CEO of TV18 in 1999, having formerly worked at Times Music and Amitabh Bachchan Corporation. Chawla became the first CEO of Network18 after it was acquired and converted into the holding company of TV18.

The transformation from production house to broadcaster wasn't smooth. Although the CNBC affair had ended in relief, TV18 had to tighten its belt and rather unceremoniously let go of about one-fifth of its workforce across departments and bureaus. Ray C would later regret that. Academy18 shut down too. But by 2000, the die was cast—TV18 was no longer a supplier but a platform, setting the stage for one of the most aggressive expansions in Indian media history.

IV. The Great Expansion: CNN-IBN and Building a Media Empire (2000-2008)

The masterstroke came in December 2005. To reach the Indian masses Turner Broadcasting System together with an Indian company, Global Broadcast News (currently TV18 Broadcast Limited), launched the channel in India as CNN-IBN on 18 December 2005. But this wasn't just about securing another franchise—it was a calculated raid on NDTV's talent pool.

Haresh Chawla, the CEO of TEIL and Network18 was instrumental in both convincing Sardesai to quit and Bahl to take on NDTV as their competition. Rajdeep Sardesai, NDTV's star anchor and managing editor, was growing restless under Prannoy Roy's shadow. After he quit NDTV, Sardesai floated his own company called Global Broadcast News (GBN) teaming up with CNN and TV18. The news channel which released by their combined efforts was called CNN-IBN. Sardesai took on the mantle as the Editor-inChief of the channel, which started programing from December 17, 2005.

The coup was breathtaking in its audacity. Not only did Bahl convince Sardesai to jump ship, but he also brought along Sameer Manchanda as CFO—both NDTV veterans who understood the business inside out. This wasn't poaching; it was a complete talent acquisition that gave Network18 instant credibility in general news.

The complex financial engineering behind these expansions deserves attention. The companies underwent several rounds of restructuring which came to a conclusion in November 2006. TEIL became a subsidiary of SGA Finance, the promoters gained a majority stake in TEIL, CNBC Awaaz was transferred to TEIL and shareholders of TEIL were accommodated with a stake in SGA Finance. On 20 October 2006, SGA Finance was converted into a public limited company and re-incorporated as Network18 Fincap Limited.

Network18 was converted into a public limited company in 2006, and listed on the Bombay Stock Exchange (BSE) and the National Stock Exchange (NSE) in 2007. Global Broadcast News (GBN), the subsidiary operating CNN IBN became a publicly traded company in January 2007 and its IPO generated a successful response, similar to that of Television Eighteen India Limited (TEIL). The capital markets loved the story—here was a media company with blue-chip international partners, growing revenues, and seemingly limitless ambition.

But the real game-changer came in 2008 with the Viacom18 joint venture. This wasn't just another partnership—it was Network18's entry into general entertainment, the most lucrative segment of Indian television. The launch of Colors TV, positioned as a mass-market Hindi entertainment channel competing directly with Star Plus and Zee TV, was what insiders called "the biggest risk ever."

The risk paid off spectacularly. Colors became a phenomenon, driven by reality shows like Bigg Boss and high-production-value dramas. Within two years, it was challenging Star Plus for the top spot in Hindi entertainment—an achievement that had taken other channels decades to accomplish.

By 2008, Network18's revenue had exploded from ₹15 crore in 1999 to ₹647 crore, outpacing rivals NDTV and TV Today by huge margins. The company had partnerships with virtually every major global media brand and was expanding into digital with acquisitions like Moneycontrol.com and Bookmyshow.com.

Yet beneath the surface, warning signs were emerging. Each new venture required massive capital investment. The 2008 financial crisis hit advertising revenues hard. And Bahl's appetite for expansion seemed insatiable—every success only fueled the desire for the next big acquisition.

V. Peak Network18: The Portfolio at its Zenith (2008-2011)

Stand in the Network18 newsroom in late 2010, and you'd witness controlled chaos across multiple floors—producers shouting across desks, multiple languages crackling through monitors, breaking news alerts cascading like dominoes. This was media power at its apex. Through its subsidiaries and franchise licensing agreements, the group owned and operated the news broadcasting networks of News18, and CNBC channels in India, the magazines of Forbes India and Overdrive, the websites of Firstpost and Moneycontrol. It also operated the television networks of Colors TV, Nickelodeon India, MTV India and the channel History TV18.

The sheer breadth was staggering. At its peak, the group controlled by Raghav Bahl included media and internet-based media outlets such as in.com, IBNLive.com, Moneycontrol.com, Firstpost.com, Cricketnext, Homeshop18, bookmyshow.com, Forbes India, TV channels such as Colors and some in partnership with international media groups such as NBC TV18, CNN-IBN, IBN7, MTV, and CNBC Awaaz. This wasn't just a media company—it was an ecosystem touching every aspect of Indian digital and broadcast life.

The numbers told a story of dominance. Network18 is a leading media conglomerate in India with over $500M managed annual revenues. The company had become the partner of choice for global media groups such as Viacom, NBC, TimeWarner (CNN) and Forbes. Every major international media brand wanted a piece of the Indian market, and Network18 was their gateway.

The crown jewel remained Colors TV, which had achieved the impossible—dethroning Star Plus from its decade-long dominance of Hindi entertainment. The channel's reality shows and high-budget dramas were pulling in advertising rates that would have been unthinkable just years earlier. Bigg Boss alone was generating more revenue than entire channels had managed in the past.

Digital was the new frontier, and Bahl was all in. Moneycontrol.com had become India's definitive financial portal, with traffic numbers that made international players envious. 'Network18' also operated e-commerce properties like HomeShop18 and bookmyshow.com and published Forbes India, the nation's first local edition of a foreign news magazine title and one of the world's most influential business brands, in collaboration with Forbes Media. Bookmyshow.com was revolutionizing entertainment ticketing, while Firstpost was attempting to create a digital-first news brand.

The partnerships kept multiplying. In 2010, Network18 went on to announce a new joint venture AETN18 with the American media company A&E Networks to launch History TV18, the Indian edition of History channel. Every deal added another layer to the empire, another revenue stream, another set of obligations.

Forbes India launched with characteristic fanfare. Commenting on this partnership, Raghav Bahl, MD, Network18, said "Our partnership with Forbes for a business magazine in India is another compelling testimony to the growing acceptance of the Indian growth story worldwide. The magazine targeted India's new rich, offering a blend of international sophistication and local relevance that advertisers loved.

The distribution muscle flexed through joint ventures. The company had also entered into a distribution joint venture with the Sun Network called Sun18. It had 2 divisions named Sun18 North and Sun18 South, the former was managed by Network18 and the latter by the Sun Network. The joint venture was later restricted to Tamil Nadu and replaced by the TV18–Viacom18 distribution joint venture IndiaCast in 2012.

But success masked fundamental problems. The financial statement of the company in 2009 had reported that it was retiring outstanding debt and raising funds through equity investments. In response to the financial challenges, the group began restructuring and consolidating its assets in the same year. The restructuring was complex—moving assets between subsidiaries, consolidating operations, trying to create synergies that would justify the sprawl.

By 2011, the warning lights were flashing red. In the financial year 2010–2011, Network18 registered a loss of ₹43.53 crore (equivalent to ₹54 crore or US$6.4 million in 2023), which was a considerable decrease from the previous two years and Bahl reportedly told the shareholders during the presentation of the annual report that "the best times are still ahead of us". His optimism seemed genuine, but the numbers told a different story.

Over the past years, the market had changed rapidly, the group was facing increased competition from other broadcasters, and advertising revenue had decreased due to economic downturn. Network18 had made optimistic projections for years but after 2011, it came to face a possible financial collapse and loss of control for its managing director Raghav Bahl.

The empire at its zenith was also an empire on the edge. Every channel required constant capital infusion, every digital property burned cash pursuing scale, every partnership demanded investment. Bahl had built India's most impressive media portfolio, but he'd borrowed heavily to do it. The question was no longer whether Network18 could grow, but whether it could survive.

VI. The Debt Crisis & Search for a Savior (2011-2012)

The November 2011 board meeting at Network18's Noida headquarters had the atmosphere of a wake. The group had accumulated an outstanding debt of over ₹1,400 crore by September 2011. Employees were convinced that the company had expanded too aggressively and the market could not support it. The advertising market had collapsed, banks were unwilling to extend fresh credit, and the company was hemorrhaging cash across multiple ventures.

The most dramatic moment came with Haresh Chawla's resignation. On November 10, 2011, the industry was faced with one of those moments -- Haresh Chawla, CEO, Network18 Group & Viacom18 had announced his resignation from the company. This wasn't just any departure—Chawla had been the operational genius behind Network18's expansion, the man who'd made the deals happen.

According to company insiders, he was persistently trying to convince Bahl to not enter into a debt agreement with Mukesh Ambani and instead raise funds by divesting part of the group's stake in the subsidiary Viacom18. Colors was worth a fortune, and selling even a partial stake could have resolved the debt crisis without surrendering independence. But Bahl had other ideas.

The numbers were brutal. By March 2011, Network18 had piled up close to Rs 1,400 crore in debt on revenue that just about equalled that figure. This wasn't just leverage—it was financial suicide. Interest payments alone were consuming operational profits, and refinancing was becoming impossible as global markets tightened after the 2008 crisis.

Even the Rs 1,000 crore it had raised – Rs 500 crore from TV18's rights issue in 2009 and a similar figure from a private placement in 2011 – was used to expand further rather than minimise debt. Every rupee raised went into new ventures rather than debt reduction—a classic entrepreneur's trap of believing growth could outrun leverage.

The human cost was immediate and severe. The group had undergone layoffs starting 2009 and restructuring in 2010. Talented journalists and producers who'd built the channels were shown the door. Morale plummeted as survivors wondered who would be next.

In his exit interview, Chawla was remarkably candid about the situation. "Which 'sinking ship' does all this?" He asserts that while Network18 is overleveraged, the company is working on it. "It is a financial structuring issue, which will get sorted out." But privately, he knew better. He resigned from the company in November 2011 before Network18 entered into a deal with Reliance Industries, publicly stating that he wanted nothing to with the Ambanis.

The search for a white knight had begun months earlier. In search of assistance in the form of external financing, Bahl decided to begin talks with the multinational energy giant Reliance Industries. But this wasn't a negotiation between equals—it was a drowning man grasping for a lifeline, and Mukesh Ambani knew it.

The seeds of the eventual takeover had actually been planted two years prior. RIL through IMT gave Rs 1,700 crore loan to Bahl's investment companies as optionally-convertible debentures to maintain promoter stake. These weren't ordinary loans—they were ticking time bombs that could convert to equity at any moment, giving Reliance control whenever it chose to exercise the option.

Insiders say Chawla left because he thought instead of dealing with Reliance, the group could have used Colors as leverage, selling a chunk of its ownership in Viacom18. Also, he didn't agree that ETV, which in March 2011 was a Rs 525-crore firm (going by figures provided by Reliance), should be valued at Rs 3,500 crore. The ETV deal, forced by Reliance as part of the rescue package, was financial engineering at its most cynical—overpaying for assets to increase debt burden and justify greater control.

Chawla's departure speech to employees was telling. From 100-odd people to a team of 6,000; from under Rs 3 million to over Rs 600 million in revenues; from a single channel to multi-brands and multi-platforms --- Network18 has lived an eventful decade. But the subtext was clear: the dream was over.

Bahl tried to maintain optimism. In presentations to investors, he talked about restructuring, cost-cutting, and the light at the end of the tunnel. But everyone knew the truth—Network18 had lost its independence the moment it took Reliance's money. The only question was when, not if, Ambani would call in his markers.

The tragedy wasn't just corporate—it was personal. For a company defined by the hardy entrepreneurial spirit of its founder, Raghav Bahl, this sentiment was significant. The company that had challenged NDTV, partnered with global giants, and built India's most diverse media portfolio was now essentially owned by an oil company. The debt crisis hadn't just consumed Network18's balance sheet—it had consumed its soul.

VII. The Reliance Takeover: A Boardroom Coup (2012-2014)

The trigger was a February 2014 press conference that changed everything. In that crowded press conference covered live by many TV channels, Kejriwal made some of the most uncharitable remarks and allegations ever made in a public forum against RIL and its chief Mukesh Ambani. The Aam Aadmi Party leader accused Reliance of artificially inflating gas prices in collusion with the government, essentially calling them thieves stealing from the nation.

RIL denied the allegation and reacted by threatening to file a lawsuit against Kejriwal but without any effect. Following which, the energy giant reportedly attempted to pressurise Network18 into censoring any and all coverage of IAC and Kejriwal including in March 2014, in a direct communication between Ambani and Rajdeep Sardesai, the managing editor of CNN IBN and IBN 7.

According to an anonymous insider present at a meeting between the executives of Network18 and RIL, the right-hand man of Ambani, Manoj Modi had threatened Bahl by stating "You are calling us a dacoit, you are shouting that we are crony capitalists." The message was clear: control your journalists or face the consequences.

The boardroom coup played out with surgical precision. On November 12, 2012, Atul S Dayal, P M S Prasad and SCPL (Sanchar Content pvt Ltd), respectively, were inducted as additional trustees of the Independent Media Trust. This marginalisation meant Bahl, the man who built the company from scratch, lost the last strand of control he had over IMT and, consequently, over his babies Network 18 and TV18.

The final act came in May 2014. RIL communicated its intention to Bahl, offering him the option of continuing as managing editor with a ₹20 crore annual salary and gave him 3 days to make his decision. He rejected the offer and on 27 May 2014, announced in midst of a routine meeting with his board of directors that he was going to resign as RIL wanted to takeover and nothing could be done about it.

The immediate aftermath was a massacre of editorial independence. Days after the deal, when Amit Shah, a close ally of Modi, was appointed head of the BJP, instructions from Network18's new management to steer coverage away from criminal charges pending against him passed between senior members of the network's newsrooms, two sources said. The channels of the network had stopped all coverage of Kejriwal and the new Aam Aadmi Party who had levied corruption accusations at RIL.

The exodus was swift and comprehensive. Subsequently, on 1 July 2014, Sardesai, editor-in-chief of CNN-IBN, along with the entire founding team — editorial and managerial — resigned from the Network18 group. "Editorial independence and integrity have been articles of faith in 26 years in journalism and maybe I am too old now to change!" Sardesai wrote in his farewell letter.

The town hall meeting that followed was Orwellian in its clarity. He asked the group how the channel was expected to cover the Aam Aadmi Party (AAP), the independent political movement devoted to India's "common man." Rohit Bansal, an RIL official now named non-executive director at Network18, answered. He said staff would be expected to cover the new owner in the same manner that the channel used to cover the previous owner Raghav Bahl and the company Network18. The company's channels typically carried very little coverage about its owners.

Indeed, since the time RIL took over in May, there have been no stories on Kejriwal or the AAP, according to one journalist. AAP leaders are no longer invited to panel discussions on the channel. The blackout was complete and unambiguous.

The financial engineering behind the takeover revealed its cynical brilliance. Bahl and his wife, Ritu Kapur, will leave with about Rs 707 crore, with all the debt of the holding and listed firms paid off in a transaction of well over Rs 3,300 crore. But the real price wasn't monetary—it was the surrender of one of India's last independent media voices.

Control over the news organisation, had strengthened RIL's ability to influence the formation of public opinion and as a result the political economy of the country, and also decreased space for reporting which could be detrimental to the energy giant's interests and public relations. This wasn't just a corporate acquisition—it was the capture of the fourth estate by India's most powerful corporation.

The tragedy extended beyond Network18. Commentators raised concerns that the editorial integrity of the network may not be preserved under the new management. The acquisition sent a chilling message to every newsroom in India: cross the powerful at your peril. The dream of independent journalism that Bahl had built over two decades was dead, replaced by corporate messaging dressed up as news.

VIII. The Reliance Era: Integration and Transformation (2014-Present)

The post-takeover Network18 operates in a different universe from Bahl's entrepreneurial chaos. The group was acquired by Mukesh Ambani led conglomerate Reliance Industries in 2014. The nominees of the RIL backed Independent Media Trust (IMT) joined the board of Network18. Deepak Parekh, the chairman of Housing Development Finance Corporation (HDFC) and Adil Zainulbhai were also inducted into the company as independent directors in the board. The board now reads like a who's who of Indian corporate establishment—safe, predictable, aligned.

The financial turnaround was immediate and dramatic. In the year till March 2012, before the investment, the company reported operating losses worth Rs 270 crore on revenue of Rs 1,952 crore. In the year till March 2014, it turned profitable at the Ebitda (earnings before interest, tax, depreciation and amortization) level, with a profit of Rs.87.2 crore on consolidated revenues of Rs.2,692 crore. The bleeding had stopped, but at what cost?

Network18 Media and Investment Limited is a media entertainment company with diverse interests in television, internet, film entertainment, digital business, magazines, mobile content and allied businesses. 25% of the Company shares are publicly traded in the National Stock Exchange. The Group has about fifty television channels in India, in addition to thirteen international channels. On paper, the empire remains vast, but the soul has changed.

The strategic rationale for the acquisition became clearer over time. The expansion occurred as part of RIL's ₹150,000 crore investment in the rollout of its 4G data business. RIL had stated during the takeover that the acquisition would help in differentiating their 4G business through corporate synergy. Infotel, the broadband subsidiary of RIL had been reincorporated as Reliance Jio Infocomm and was in the process of launching its data transfer business. It was suggested that the synergy would alleviate stresses posed by unstable market conditions in the news broadcast industry, while Jio would provide exclusive content from Network18 productions to increase traffic towards itself and expand its customer base.

But reality proved different from strategy. The synergy was however not adopted, according to analysts it was not financially beneficial to restrict content to only Jio customers and that Jio itself could be more profitable by being a content aggregator at competitive rates and still have a cost advantage due to its scale. The grand convergence play never materialized as envisioned.

The current financial performance tells a story of stability without dynamism. In the fiscal year ending March 2023, Network18 reported revenues of approximately INR 7,375 crore, marking a robust growth of 20% compared to the previous year. This increase was driven largely by a rise in advertisement revenues and subscription fees across its multiple channels. Solid numbers, but nothing like the explosive growth of the Bahl era.

As per Screener.in, the market cap of Network18 as of July 18, 2023, is Rs 6,740 crore. This represents a significant recovery from the crisis years, but still below what an independent Network18 might have achieved with access to capital and freedom to operate.

The ownership structure reveals complete dominance. Since the 2014 takeover, RIL continues to be Network18's parent company with a 75 percent shareholding of the 1,04,69,48,519 shares, through various promoters. Of these, RB Mediasoft Private Ltd, RB Media Holdings Private Ltd, Adventure Marketing Private Ltd, Colorful Media Private Ltd and Watermark Infratech Private Ltd each have 12.18 percent shareholding as per the latest data on BSE. RRB Mediasoft Private Ltd holds 10.36 percent shares. IMT holds 1.88 percent shares (in the name of its trustee, Sanchar Content Private Ltd). The complex structure masks simple reality: Reliance controls everything.

Recent corporate actions reveal ongoing consolidation. Reliance-owned TV18 Broadcast Ltd on Wednesday announced its merger with Network18 effective April 2023. The merger will consolidate the TV and Digital news businesses of the Network18 Group in one company and will help create the country's platform-agnostic news media powerhouse with the widest footprint across languages, straddling both TV and Digital, the company said in an exchange filing.

The government advertising patterns tell their own story. In a Right to Information (RTI) request response in June 2021, data released by the Uttar Pradesh government showed that the government's spending on television advertisements was at ₹160.31 crore between April 2020 and May 2021 with Network18 as its biggest beneficiary. Promotion of the Atmanirbhar Bharat campaign constituted a major portion of the spending and was made in the initial part of the year. Being close to power has its benefits.

Five years post-takeover, whispers emerged of Ambani potentially looking to exit, considering different strategies, and being receptive to selling media assets. The convergence dream hadn't materialized, regulatory challenges mounted, and the economics of news remained challenging. Network18 had become just another division in the Reliance empire—profitable but peripheral.

The person familiar with the happenings in the board meeting said Bahl and his team didn't ever think RIL would oust them and seize control. Everyone wishes they could turn the clock back. But clocks don't turn back, and Network18's transformation from entrepreneurial media house to corporate division was complete.

IX. Business Model & Strategic Analysis

The Network18 business model represents a fascinating case study in media conglomerate economics—both in its strengths and its fatal flaws. At its core, the company operates across five distinct but theoretically synergistic verticals: television broadcasting, digital content, filmed entertainment, e-commerce, and print/publishing.

The television business remains the cash cow, generating the bulk of revenues through a dual-stream model: advertising and subscription fees. Through its subsidiary TV18 Broadcast Limited, the company operates a number of television channels in the genres of news, business and general entertainment. TV18 Broadcast Limited Company is also in a joint venture with Viacom18 that operates entertainment channels. TV18 Broadcast Limited also operates factual information channel through a joint venture with A+E Networks. The breadth is impressive, but breadth doesn't equal depth of profitability.

The fundamental challenge in Indian media is the inverse relationship between reach and revenue. News channels, despite massive viewership, generate minimal subscription revenue due to regulatory caps and bundling practices by cable operators. Advertising rates for news remain a fraction of entertainment programming, yet news requires constant investment in talent, technology, and newsgathering infrastructure.

Colors TV exemplifies the paradox. While it generates substantial revenue and competed successfully with Star Plus, the economics remain brutal. Programming costs escalate continuously as competitors bid up talent and production values. A single prime-time show can cost crores per episode, with no guarantee of success. The hits subsidize numerous failures, and even hits have limited lifespans.

The digital portfolio presents different challenges. Moneycontrol.com dominates financial news online, but digital advertising rates in India remain a fraction of global benchmarks. The merged entity will comprise the TV portfolio of TV18 (20 news channels in 16 languages and CNBCTV18.com), Digital assets of Network18 (News18.com platform across 13 languages and Firstpost) as also moneycontrol website and app. Scale without pricing power is a recipe for mediocrity.

The e-commerce ventures—Homeshop18 and the stake in BookMyShow—represent classic diversification mistakes. Television shopping never achieved critical mass in India, competing against established e-commerce giants with deeper pockets. BookMyShow succeeded, but as a minority investment, Network18 captured limited value from its growth.

Network18's financials have improved considerably since RIL invested indirectly in the company. But improvement from crisis isn't excellence. The company operates profitably but without the explosive growth that justified the massive debt accumulation. EBITDA margins in the low teens are respectable for media but hardly spectacular given the capital employed.

The capital intensity problem remains unsolved. Every new channel requires carriage fees to cable operators—essentially paying for distribution that should theoretically pay you. Digital properties require constant technology investment to remain competitive. Content costs escalate faster than revenues. It's a treadmill that requires constant capital infusion to maintain position, let alone grow.

For RIL, the takeover is a strategic move for its 4G telecom play in the country. The acquisition will differentiate Reliance's 4G business by providing a unique amalgamation at the intersection of telecom, the web and digital commerce via a suite of premier digital properties. This convergence thesis—that telecom and content would merge—proved largely illusory. Content is consumed across platforms, and exclusive deals limit reach.

The competitive landscape has shifted dramatically. Disney+ Hotstar, Amazon Prime, and Netflix have redefined content economics, spending billions on original programming. Network18's content budget is a rounding error compared to these giants. In news, Republic TV's aggressive positioning and Times Now's established presence squeeze Network18's channels from both sides.

Regional expansion, once a strength, became a complexity burden. All the TV business – including CNBC-TV18, CNN-IBN, CNBC Awaaz, the Viacom18 channels and IBN Lokmat – were consolidated into IBN18 Broadcast Ltd, the new TV18. GBN was renamed IBN18 in 2008, and TV18 Broadcast Ltd in 2011. All websites, publishing and venture capital divisions, sports and event management businesses went under the new Network18. Managing dozens of channels across languages requires massive organizational overhead with limited economies of scale.

The synergy question haunts the analysis. Theoretically, a news story could be leveraged across television, digital, and print. In practice, each medium has different audience expectations, production requirements, and economic models. The promised efficiencies never materialized at the scale needed to justify the complexity.

Under Reliance, the strategic focus has shifted to stability over growth. Cost discipline replaced entrepreneurial expansion. Editorial independence gave way to corporate messaging. The business model works—barely—but lacks the dynamism that created Network18 in the first place.

The fundamental question remains: In an era of global streaming giants and social media platforms, what is the sustainable competitive advantage of a traditional Indian media conglomerate? Network18 has scale but not uniqueness, reach but not pricing power, content but not must-watch programming. It's profitable but not exceptional—a business that works but doesn't inspire.

X. Lessons & Legacy

The Network18 saga offers a masterclass in entrepreneurial ambition colliding with financial reality. Raghav Bahl didn't just build a media company—he attempted to create an entire ecosystem, touching every aspect of how Indians consumed information and entertainment. The achievement was remarkable: During his 20-years at Network18, Bahl managed partnerships with CNBC, Viacom, BBC, Star TV, A&E, Time Warner, Forbes and other leading media brands. The company now boasts over 35 TV channels, 13 websites—a portfolio that would have been unimaginable in the Doordarshan monopoly era.

The entrepreneur's dilemma that destroyed Network18's independence is almost Greek in its tragedy. Bahl needed capital to grow, but raising capital meant diluting control. Debt seemed like the solution—maintain ownership while accessing funds—but debt in a cyclical, capital-intensive business with long payback periods is poison. The more successful Network18 became, the more capital it needed, until the debt burden crushed the very independence it was meant to preserve.

The timing curse haunted every major decision. Network18 went public during the dot-com boom, expanded aggressively before the 2008 crisis, and leveraged up just as advertising revenues collapsed. In media, being early is indistinguishable from being wrong, and being late means competing against entrenched players. Bahl was often early—digital news, streaming content, regional expansion—but couldn't afford to wait for the market to catch up.

What could Bahl have done differently? The consensus among former executives is clear: sell Colors. The entertainment channel's success created enormous value that could have eliminated debt and provided growth capital. But Bahl saw Colors as the crown jewel, proof that Network18 could compete with anyone. Pride preceded the fall.

The alternative path—slower, organic growth—seems obvious in hindsight but was perhaps impossible given Bahl's personality and the competitive landscape. In the process, he lost his company and the respect of many former managers who felt they were shortchanged through stock options that did not materialise and brands that were junked too early in the hurry to create Network18. The collateral damage extended beyond financial losses to human capital and institutional knowledge.

The debt spiral teaches a brutal lesson about leverage in media businesses. Unlike manufacturing or real estate, media assets have limited collateral value. A television channel's worth lies in its brand, talent, and audience relationships—all of which can evaporate overnight. Banks learned this lesson lending to Network18, which is why credit dried up when most needed.

"He thought big, created a portfolio of diverse assets, picked up smart people and empowered them. The organisation he has created is quite magnificent. Sometimes, one or two calls pull you down," is how one former media baron puts it. This generous assessment captures both the achievement and the tragedy.

The price of debt-fueled growth in cyclical industries cannot be overstated. Every media business faces the same challenge: content costs are fixed and front-loaded, while revenues are variable and back-loaded. Adding debt to this equation is like sailing into a storm with extra cargo—it might work in calm seas, but the first major wave brings disaster.

Media consolidation patterns globally show deep pockets usually win. Whether it's Murdoch building News Corp through aggressive acquisitions or Disney buying content libraries, scale requires capital. In India, the pattern is even starker—every major media company either has deep-pocketed corporate backing (Times Group's diversified revenues, Star's Disney parentage) or struggles for relevance.

The editorial independence question looms largest. Commentators raised concerns that the editorial integrity of the network may not be preserved under the new management. The channels of the network had stopped all coverage of Kejriwal and the new Aam Aadmi Party who had levied corruption accusations at RIL. Can journalism serve the public interest when owned by corporations with vast business interests? Network18's transformation suggests the answer is no.

The human cost often gets overlooked in corporate narratives. Hundreds of journalists who joined Network18 to build something different found themselves working for a corporate PR department. The brain drain was immediate and comprehensive—talent fled to new ventures or international organizations, taking decades of experience with them.

Even the Rs 1,000 crore it had raised – Rs 500 crore from TV18's rights issue in 2009 and a similar figure from a private placement in 2011 – was used to expand further rather than minimise debt. The group had undergone layoffs starting 2009 and restructuring in 2010. The pattern of raising money to expand rather than consolidate reveals a fundamental misunderstanding of sustainable growth.

For future media entrepreneurs, Network18's arc offers sobering lessons. First, in winner-take-all markets, being second-best in multiple categories is worse than being dominant in one. Second, international partnerships provide credibility but also complexity—every partnership is another stakeholder with different objectives. Third, debt and editorial independence are incompatible—the moment you owe money, you owe favors.

The broader implications for Indian media are profound. If even Network18, with its blue-chip partnerships and first-mover advantages, couldn't remain independent, what hope for new entrants? The answer may lie in different models—digital-first, niche-focused, subscription-based—rather than the broad conglomerate approach.

Current state reveals the end game: As per the book, annual revenues were up by 12 percent to Rs 2,692 crore, and 2013's operating loss of Rs 39 crore had been transformed to Rs 89 crore operating profit. So, he said, Network18 assembled a team to focus on it. Profitable but uninspiring, stable but soulless.

What's the Bahl's true legacy? He proved Indian media could compete globally, attract international partners, and create valuable franchises. But he also proved that in Indian media, as perhaps everywhere, independence is a luxury few can afford. The visionary who saw opportunity where others saw chaos ultimately became another casualty of the fundamental economics of media—infinite ambition meeting finite capital.

XI. Epilogue: The Future of Indian Media

The Indian media landscape in 2023 presents a paradox—never have there been more channels, platforms, and voices, yet never has true independence seemed more elusive. As of October 2023, Network18's market capitalization hovered around ₹14,000 crore, with stock prices fluctuating between ₹40-65 per share. Market Cap ₹ 8,779 Cr. The company has delivered a poor sales growth of 5.16% over past five years. These numbers reflect not dynamism but stagnation, a business that exists rather than thrives.

The digital disruption that Bahl anticipated but couldn't fully capitalize on has arrived with vengeance. OTT platforms have fundamentally altered content economics. Netflix spends more on a single series than Network18's entire annual content budget. Disney+ Hotstar commands subscription fees that traditional broadcasters can only dream of. The group continues to be the largest TV news network, with viewership share increasing by 220 basis points year-on-year. But viewership without monetization is vanity, not value.

The synergy between content and distribution that justified Reliance's acquisition never materialized as envisioned. Jio's success came from cheap data and network effects, not exclusive content. Consumers want choice, not walled gardens. The bundling of Network18 content with Jio subscriptions added marginal value to either business.

Will Reliance keep or sell Network18? Five years post-acquisition, the strategic rationale seems exhausted. The convergence play failed, regulatory headwinds persist, and the economics of news remain challenging. Network18 is profitable but peripheral to Reliance's core energy and retail ambitions. Yet selling would mean admitting failure and potentially empowering a competitor.

The broader implications for media independence and plurality in India are sobering. If Network18, with its scale and partnerships, couldn't maintain independence, what hope for smaller players? The future seems to hold further consolidation, with media becoming divisions of larger conglomerates rather than independent institutions.

The next chapter might see Network18 spun off, merged with another player, or simply maintained as a useful but not critical asset in the Reliance portfolio. The P/E (price-to-earnings) ratio of Network18 Media & Investments Ltd (NETWORK18) is -5.13. The P/B (price-to-book) ratio is 1.80. These metrics suggest a business that markets view skeptically, pricing in neither growth nor strategic value.

Building versus buying in media presents no easy answers. Bahl built organically and through partnerships, creating enormous value but losing control. Reliance bought but struggles to extract strategic value. Perhaps the lesson is that in media, unlike other industries, ownership structure fundamentally determines output. A media company owned by an oil conglomerate will inevitably become an oil conglomerate's media company.

The final irony is that Network18 achieved what it set out to do—becoming India's largest media network—but lost what made it worth building in the first place. It has reach without influence, scale without spirit, profitability without purpose. The channels broadcast, the websites publish, the business operates. But the entrepreneurial energy, editorial independence, and ambitious vision that created Network18 died the day Reliance's check cleared.

XII. Recent News

The current state of Network18 reflects neither crisis nor triumph but corporate normalcy. Recent financial results show steady but unspectacular performance, with the consolidated entity comprising TV portfolio and digital assets maintaining market position without breakthrough growth.

Government advertising continues to flow, particularly from BJP-ruled states, underlining the benefits of alignment with power structures. The editorial stance across channels has shifted notably rightward, with coverage patterns that would have been unthinkable in the Bahl era.

The promised digital transformation remains incomplete. While platforms like Moneycontrol maintain leadership in their niches, the broader digital strategy lacks coherence. Investment in new initiatives has slowed to a trickle, with focus on maintaining existing properties rather than breakthrough innovation.

XIII. Links & Resources

For those seeking deeper understanding of Network18's journey, several resources prove invaluable:

- "Network18: The Audacious Story of a Start-up That Became a Media Empire" by Indira Kannan provides an insider's account of the rise

- SEBI filings and annual reports offer financial details often obscured in public narratives

- The Caravan's long-form investigations into Indian media ownership patterns provide essential context

- Newslaundry's "Who Owns Your Media" series tracks the ongoing consolidation

- Industry reports from FICCI and CII document the broader media landscape evolution

The Network18 story isn't finished. But the chapter of independent, entrepreneurial media building in India might be. What remains is a cautionary tale of ambition exceeding capital, dreams crushed by debt, and independence surrendered to survival. Raghav Bahl built something remarkable. That it couldn't survive intact says more about Indian media economics than any academic study ever could. The empire remains, but the dream that built it has long since died.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube