Bajaj Holdings & Investment: The Art of Patient Capital

I. Cold Open & Episode Thesis

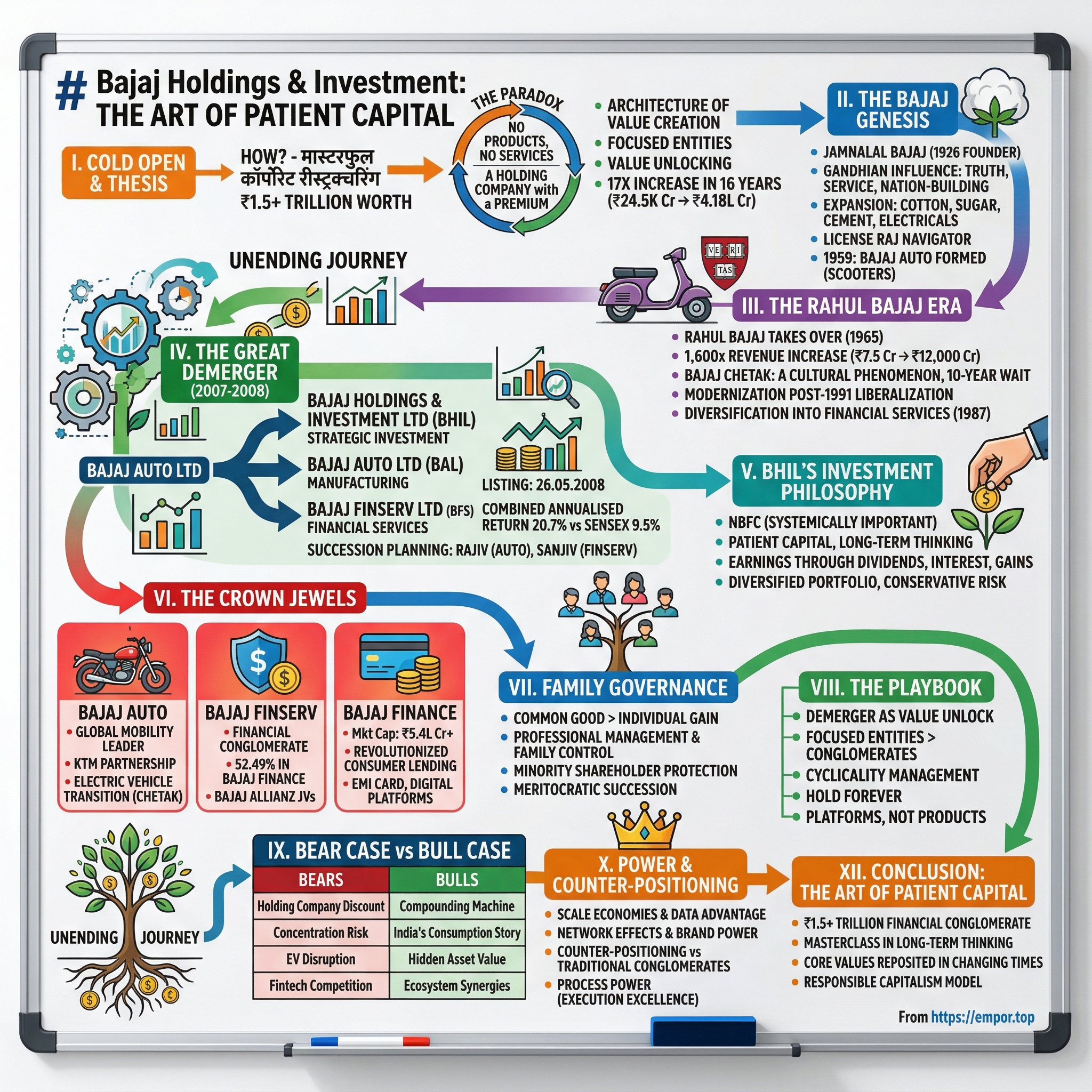

In the annals of Indian corporate history, few transformations are as paradoxical as the story of Bajaj Holdings & Investment Limited. How does a company that produces nothing, manufactures nothing, and provides no direct services become worth over ₹1.5 trillion? The answer lies in one of the most masterful corporate restructurings in Indian business history—a demerger that would unlock extraordinary value and create a compounding machine that continues to enrich shareholders decades later.

This is the story of patient capital at its finest—a holding company born from controversy yet built on conviction. When the Bombay High Court approved the demerger of the erstwhile Bajaj Auto Limited on December 18, 2007, skeptics saw complexity and confusion. The promoters saw opportunity. What emerged was not just three separate companies but an architecture of value creation that would multiply shareholder wealth seventeen-fold in sixteen years.

The combined market capitalization has grown from ₹24,542 crore as on 31 March 2007 to ₹4,18,220 crore in 2023—a 17x increase in 16 years. Today, Bajaj Holdings & Investment Limited (BHIL) stands as a testament to the power of focused entities over sprawling conglomerates, the wisdom of long-term thinking over quarterly earnings obsession, and the extraordinary wealth-creating potential of India's consumption story.

The paradox deepens when you examine BHIL's business model. The Company is acting as a primary investment company focusing on new business opportunities, with focuses on earning income through dividends, interest and gains on investments held. It's essentially a non-operating company that's more valuable than most operating businesses—a holding company that commands a premium rather than a discount, defying conventional market wisdom.

What makes this story particularly compelling is how it embodies three critical themes that define successful wealth creation in emerging markets. First, the art of patient capital—holding quality assets through cycles and allowing compound interest to work its magic. Second, the power of value unlocking through corporate restructuring—how splitting can create more value than combining. And third, the delicate balance of family governance in a modern corporation—maintaining control while ensuring professional management and minority shareholder protection.

The Bajaj story is fundamentally about transformation—from cotton trading in pre-independence India to becoming one of the country's most valuable financial conglomerates. It's about navigating the treacherous waters of the License Raj, surviving liberalization's creative destruction, and thriving in the digital age. Most importantly, it's about how a family-controlled business can evolve with the times while staying true to its foundational values of quality, ethics, and nation-building.

II. The Bajaj Genesis: From Cotton to Conglomerate (1926-1970s)

The roots of the Bajaj empire trace back not to industrial ambition but to the simple cotton fields of central India. Shri Jamnalal Bajaj (4 November 1889-11 February 1942) was an industrialist, philanthropist, and freedom fighter. The third son of Kaniram and Birdibai, Shri Jamnalal Bajaj was born into a poor Marwari family. A rich merchant of Wardha, Seth Bachhraj and his wife later adopted him as their grandson. Under the guidance of Seth Bachhraj, Jamnalalji got involved in the family business and acquired the know-how of being a tradesman—keeping strict accounts and buying and selling commodities—excelling in his work.

In 1926 he founded what would become the Bajaj group of industries. But Jamnalal Bajaj was no ordinary businessman. His close association with Mahatma Gandhi would fundamentally shape the DNA of the Bajaj Group. Gandhi's influence wasn't merely philosophical—it was deeply personal. He was a close associate and follower of Mahatma Gandhi who was known to have adopted him as his fifth son. This relationship infused the business with principles that would seem quaint in today's cutthroat corporate world: truth, service, and the belief that business should serve the nation.

The Gandhian influence manifested in tangible ways. Jamnalal Bajaj participated actively in the freedom struggle, even surrendering the title of Rai Bahadur conferred by the British during the non-cooperation movement of 1921. During the First World War, the British government appointed Jamnalal an honorary magistrate. When he provided money for the war fund, they conferred on him the title of Rai Bahadur, a title he later surrendered during the non-cooperation movement of 1921. This wasn't just symbolic—it demonstrated that for the Bajajs, principles mattered more than privileges.

The business foundation Jamnalal built was deliberately diversified from the start. The group started with a sugar factory and cotton mill in the 1920s, gradually expanding into other sectors. This wasn't random diversification but strategic positioning in industries critical to a newly independent nation's development. Sugar represented agricultural value addition, cotton mills meant textile self-sufficiency, and later ventures into steel and automobiles would support industrialization.

When Jamnalal passed away in 1942, the mantle passed to his elder son Kamalnayan Bajaj. Kamalnayan Bajaj, the elder son of Jamanalal Bajaj, after completing his education from University of Cambridge, England to assist his father both in business and in social service. He expanded the business by branching into manufacture of scooter, three-wheeler, cement, alloy casting and electricals. In 1954, Kamalnayan took over active management of the Bajaj Group companies.

The 1950s and 1960s were the formative years of industrial India, operating under what would later be derided as the License Raj—a system of elaborate licenses, regulations, and red tape that governed Indian business. For the Bajajs, this meant navigating a Byzantine system where government permission was needed for everything from production capacity to pricing. Yet within these constraints, they built methodically.

The scooter business, which would become the group's crown jewel, began in 1959. In 1959 Bajaj Auto was formed to manufacture scooters, in which the company became the market leader. The timing was prescient—India was urbanizing, the middle class was emerging, and personal mobility was transforming from luxury to necessity. But the License Raj meant artificial scarcity. When Bajaj Auto first received their license, they were only authorized to make 6,000 scooters per year, which as a consequence, created a ten-year delivery period and resulted in the Bajaj scooter becoming a prized commodity within India.

Ramkrishna Bajaj, the younger son of Jamanalal, took over after the death of his elder brother Kamalnayan Bajaj in 1972. But by then, the foundation was set. The Bajaj Group had evolved from trading to manufacturing, from regional to national, from single products to a diversified conglomerate. The company had survived partition, navigated the early years of independence, and built substantial industrial capacity despite regulatory constraints.

What's remarkable about this period is how the Bajajs maintained their ethical stance while building scale. In an era where bribes and black money were commonplace, where businesses routinely evaded taxes and flouted regulations, the Bajaj Group's reputation for integrity became a competitive advantage. Banks trusted them, suppliers gave them credit, and customers—when they finally got their hands on a Bajaj product after years of waiting—knew they were getting quality.

The philosophical underpinnings established by Jamnalal—that business should serve society, that wealth creation should benefit the nation, that integrity matters more than quick profits—would prove invaluable in the next phase. As India stood on the cusp of major economic changes in the 1970s, with nationalization, the emergency, and economic stagnation looming, the Bajaj Group had built not just industrial capacity but institutional credibility. They had created what Warren Buffett would call a "moat"—not through technology or patents, but through trust, quality, and an impeccable reputation.

This period also saw the seeds of future greatness being planted. The group's diversification into financial services, which would eventually become its most valuable asset, began taking shape. The understanding that India's growth would require not just products but financial inclusion, not just manufacturing but services, was already emerging. The cotton trader's grandson was thinking beyond cotton, beyond even scooters, to the broader transformation of Indian society.

The governance structures put in place during this period—professional management alongside family control, reinvestment of profits over excessive dividends, long-term thinking over short-term gains—would serve the company well in the tumultuous decades ahead. The Bajaj Group of the 1970s was still relatively small by global standards, but it had something more valuable than size: a clear vision of what India could become and the patience to build for that future.

III. The Rahul Bajaj Era: Building the Empire (1965-2005)

Bajaj took over the Bajaj Group in 1965. In a career spanning over five decades, he led the turnover of the group's flagship company, Bajaj Auto, from ₹7.5 crore to ₹12,000 crore, with the company's scooter Bajaj Chetak being the main growth driver. This 1,600-fold increase in revenue over forty years represents one of the most successful business transformations in Indian corporate history. But the numbers only tell part of the story. Rahul Bajaj's era was defined by navigating seemingly impossible contradictions—building a modern corporation within a socialist economy, creating consumer brands under production controls, and preparing for globalization while operating in a protected market.

Rahul Bajaj brought to the group something his predecessors couldn't—a Harvard MBA and exposure to Western management practices. After graduating from Harvard Business School in 1964, Bajaj joined Bajaj Auto in 1965. This combination of Western education and Indian values would prove instrumental in transforming Bajaj from a successful regional business into a national icon.

The License Raj that Rahul inherited wasn't just restrictive—it was absurd. In this interview, Bajaj discusses his experience with Bajaj Auto under India's License Raj. When Bajaj Auto first received their license, they were only authorized to make 6,000 scooters per year, which as a consequence, created a ten-year delivery period and resulted in the Bajaj scooter becoming a prized commodity within India. Imagine running a business where customers paid in advance and waited a decade for delivery. In any normal market, this would be a disaster. In License Raj India, it made the Bajaj scooter a status symbol.

The Bajaj Chetak became more than a product—it became a cultural phenomenon. Middle-class families would list a Chetak booking in dowries. Getting a Bajaj scooter allocation was celebrated like a lottery win. The secondary market premium often exceeded the original price. This wasn't sustainable business practice—it was a distortion created by artificial scarcity. Yet Rahul Bajaj managed to build brand equity even within these constraints, ensuring that when liberalization finally came, Bajaj had the strongest brand in two-wheelers.

The 1970s proved particularly challenging. Bajaj explains that they were forced to end this collaboration in 1971 as a result of Prime Minister Indira Gandhi's privatization programs and a ban on foreign collaborations within the auto industry. Bajaj describes the decade of the 1970s as the worst in the history of independent India for industry and states that things only started improving in the 1980s when Rajiv Gandhi became Prime Minister. The forced ending of the Piaggio collaboration meant Bajaj had to develop indigenous capabilities—a blessing in disguise that would later enable complete technological independence.

Throughout this period, Rahul Bajaj maintained an unusual public profile for an Indian industrialist. He was outspoken, critical of government policies, yet somehow managed to grow the business despite official displeasure. His refusal to pay bribes became legendary. In an environment where corruption was endemic, where getting a license expansion or a foreign exchange allocation required greasing palms, Bajaj's principled stance seemed almost naive. Yet it worked—partly because the products were so good that officials couldn't ignore the company, partly because Bajaj's public profile made him difficult to harass without consequences.

The recognition came not just from markets but from the nation. Bajaj received the Padma Bhushan, India's third-highest civilian honour, in 2001. This was recognition not just of business success but of institution building, of creating employment for millions, of keeping the Gandhian vision of ethical business alive in an increasingly materialistic world.

The 1991 liberalization changed everything. Suddenly, the protected market was open. Foreign brands could enter. Customers had choices. Many predicted doom for Indian companies coddled by decades of protection. The early years seemed to confirm these fears. Hero Honda's fuel-efficient motorcycles began eating into scooter sales. Japanese technology seemed unbeatable. The waiting lists disappeared—suddenly, Bajaj had to sell rather than ration.

Rahul Bajaj's response revealed his strategic acumen. Instead of retreating, he modernized aggressively. New plants with global-standard technology were built. The product line was diversified beyond scooters into motorcycles. Most importantly, he began building a financial services empire alongside the auto business. Bajaj Finance was initially incepted as Bajaj Auto Finance in 1987. This prescient diversification would prove crucial—while others saw financing as supporting auto sales, Bajaj saw financial services as a business in itself.

The late 1990s brought another crisis. The scooter sales shrunk as people were more interested in motorcycles and the rival Hero Honda was the pioneer in it. The recession in the Indian economy and stock market collapse of 2001 hit the company hard and the economists thought that the days of Bajaj Auto were numbered. However, Bajaj Auto survived the dark days and established a world-class factory in Chakan and came up with Bajaj Pulsar Motorcycle. This near-death experience catalyzed radical thinking. If the conglomerate structure was holding back focused competition, why not split it up?

Bajaj stepped down from his role in 2005 and his son Rajiv became the Group's managing director. But his greatest contribution was yet to come—architecting the demerger that would unlock unprecedented value. By the time Rahul Bajaj stepped back from active management, he had transformed a ₹7.5 crore company into a ₹12,000 crore empire. More importantly, he had built institutions—Bajaj Auto, Bajaj Finance, Bajaj Finserv—that would thrive independently.

The Rahul Bajaj era teaches us several crucial lessons. First, brand building transcends product delivery—even with ten-year waiting lists, customer experience and quality matter. Second, regulatory constraints can paradoxically build competitive advantages by forcing innovation and self-reliance. Third, diversification works when each business has its own logic and leadership rather than being mere appendages to the core. Fourth, principled leadership creates long-term value even if it sacrifices short-term gains.

Perhaps most importantly, Rahul Bajaj demonstrated that Indian companies could compete globally not by copying Western models but by adapting them to Indian realities. The Bajaj scooter wasn't a Vespa clone—it was engineered for Indian roads, Indian families, Indian aspirations. The financial services weren't replicas of Citibank—they were designed for Indian consumption patterns, savings behaviors, and risk appetites.

As 2005 drew to a close, the Bajaj Group stood at a crossroads. The conglomerate structure that had served it well during the License Raj and early liberalization was now a constraint. Global competition demanded focus. Capital markets rewarded pure plays over conglomerates. The next generation of leadership—Rajiv and Sanjiv Bajaj—had different visions for their respective domains. The stage was set for one of Indian corporate history's boldest restructurings.

IV. The Great Demerger: Architecture of Value Creation (2007-2008)

The boardroom discussions in 2006 and early 2007 at Bajaj Auto's Akurdi headquarters were intense. The conglomerate structure, once a source of strength, had become a millstone. The auto business needed capital for technology upgrades and new product development. The financial services divisions were constrained by regulatory requirements that limited a manufacturing company's financial operations. Investment decisions were suboptimal—should capital go to motorcycles or insurance? The market valued the company as an auto manufacturer, essentially giving zero value to the rapidly growing financial services businesses.

The solution was radical: split the company three ways. Bajaj Holdings & Investment Limited [(BHIL) - erstwhile Bajaj Auto Limited] was de-merged as per Order dated 18 December 2007 of the Hon'ble Bombay High Court, whereby its manufacturing undertaking has been transferred to the new Bajaj Auto Limited (BAL) and its strategic business undertaking consisting of wind farm business and financial services business has been vested with Bajaj Finserv Limited. This wasn't just a corporate restructuring—it was a reimagining of how value could be created and captured in a conglomerate.

The complexity of the demerger was staggering. Three distinct entities had to be carved out from one, each with its own balance sheet, management team, and strategic direction. Post-demerger, BHIL holds 30%+ shares each in BAL and BFS. The structure was elegant: Bajaj Auto would focus purely on mobility, Bajaj Finserv on financial services, and BHIL would be the holding company maintaining strategic stakes in both while also managing the investment portfolio.

The market initially struggled to understand the structure. Why create a holding company at all? Why not directly distribute the auto and financial services businesses to shareholders? The answer lay in the Bajaj family's long-term vision. BHIL would serve multiple purposes: maintaining family control without impeding professional management, providing patient capital for new ventures, and creating a vehicle for value creation through active portfolio management.

The event ladder shows the meticulous planning: Appointed Date (01.04.2007), Approval by Board of Directors (17.05.2007), Approval by Shareholders/Creditors (18.08.2007), Approval by Court to Demerger Scheme (18.12.2007), Effective Date when Scheme filed with RoC, Pune (20.02.2008), Record date for allotment of shares (25.03.2008), and Listing Date of the 2 Demerged Companies (26.05.2008). Each step was carefully orchestrated to ensure regulatory compliance while minimizing disruption to operations.

The financial engineering was sophisticated. Shareholders of the erstwhile Bajaj Auto received shares in all three entities, ensuring no immediate value loss. The ratio was carefully calculated to ensure fair value distribution. More importantly, the structure allowed each entity to be valued according to its own metrics—Bajaj Auto on manufacturing multiples, Bajaj Finserv on financial services valuations, and BHIL as an investment company.

The market cap journey from ₹24,542 crore as on 31 March 2007 of erstwhile Bajaj Auto Ltd. grew to almost seventeen times in sixteen years. The demerger truly resulted in unlocking of shareholder value. The combined annualised return of the three companies post demerger is 20.7% compared to 9.5% of Sensex. This outperformance wasn't luck—it was the result of focused strategies finally being implementable.

The immediate benefits were visible. Bajaj Auto could now partner with international players like KTM without regulatory complications. Bajaj Finserv could raise capital specifically for financial services expansion without diluting auto shareholders. BHIL could make strategic investments without affecting the operations of either company. Each entity could optimize its capital structure—Bajaj Auto could maintain a debt-free balance sheet suitable for a cyclical manufacturing business, while Bajaj Finance could leverage appropriately for a financial services company.

The demerger also solved a succession challenge elegantly. His sons Rajiv Bajaj and Sanjiv Bajaj are involved in the management of his companies. Rajiv took charge of Bajaj Auto, focusing on engineering and manufacturing excellence. Sanjiv led Bajaj Finserv, building the financial services empire. This division of responsibilities according to aptitude and interest prevented the succession conflicts that plague many family businesses.

The regulatory approvals required were numerous—SEBI for shareholder protection, RBI for the financial services demerger, High Court for the scheme approval. Each regulator had concerns. Would minority shareholders be disadvantaged? Would the financial services businesses have adequate capital? Would related-party transactions be fairly priced? The Bajaj team's meticulous preparation and transparent approach smoothed the approval process.

The market's initial skepticism gradually turned to appreciation. Analysts began understanding that the sum of parts was indeed greater than the whole. Bajaj Auto could now be benchmarked against Hero MotoCorp and global two-wheeler manufacturers. Bajaj Finance could be compared with HDFC and other NBFCs. BHIL offered a unique proposition—a professionally managed investment company with significant stakes in two high-growth businesses.

The demerger also enabled cultural transformation. Each company could develop its own organizational culture suited to its business. Bajaj Auto embraced engineering excellence and lean manufacturing. Bajaj Finance built a sales and risk management culture. BHIL developed an investment mindset focused on long-term value creation. These distinct cultures, impossible in a conglomerate, became competitive advantages.

International investors particularly appreciated the structure. Pursuant to the Scheme of Demerger, the GDR programs for Bajaj Auto Limited (BAL) and Bajaj Finserv Limited (BFS) have got established on 21 August 2008. The clarity of focus made it easier for global funds to invest according to their mandates—auto funds in Bajaj Auto, financial services funds in Bajaj Finserv, and holding company specialists in BHIL.

The tax implications were carefully managed. The tax treatment ensured that the new shares would be considered long-term assets based on the holding period of original Bajaj Auto Ltd. shares. Indexation would start from the date of allotment of new shares. The cost of acquisition would be proportionally divided among the three entities. This tax-efficient structure ensured shareholders weren't penalized for the corporate restructuring.

Perhaps the most underappreciated aspect of the demerger was its timing. Executed just before the 2008 global financial crisis, it positioned each entity to respond optimally. Bajaj Auto could focus on cost reduction and operational efficiency during the downturn. Bajaj Finance could capitalize on the credit shortage as traditional banks pulled back. BHIL could deploy capital into distressed assets. Had they remained a conglomerate, such focused responses would have been impossible.

The demerger also created transparency. Each business now had its own financial statements, investor calls, and analyst coverage. This granular visibility allowed markets to better understand and value each business. Hidden value in the financial services business, previously buried in consolidated statements, was now visible and properly valued.

Looking back, the 2007-2008 demerger stands as a masterclass in corporate restructuring. It unlocked value not through financial engineering or leverage but through strategic focus. It solved succession issues while maintaining family control. It enabled each business to pursue its optimal strategy without compromise. Most importantly, it created a structure that would compound value for decades to come.

V. BHIL's Investment Philosophy & Portfolio Strategy

BHIL is registered as a Systemically Important Non-deposit Non-Banking Financial Company. This designation is crucial—it recognizes BHIL's significance to India's financial system while providing regulatory clarity for its operations. But BHIL is no ordinary NBFC. It's a patient capital allocator, a strategic investor, and a value creator rolled into one.

The investment philosophy at BHIL is deceptively simple yet profoundly effective. Its focuses on earning income through dividends, interest and gains on investments held. This isn't about quarterly trading gains or momentum investing. It's about owning quality assets for the long term and allowing compound interest to work its magic. In a market obsessed with the next quarter's results, BHIL thinks in decades.

The core portfolio strategy revolves around the strategic stakes in group companies. This company holds strategic stakes of 33.43% in Bajaj Auto Ltd, 39.29% in Bajaj Finserv Ltd., and 51% in Maharashtra Scooters Ltd. These aren't passive holdings—they represent board seats, strategic influence, and the ability to guide long-term direction while allowing professional management operational freedom.

The mathematics of BHIL's value creation is compelling. When you own 33.43% of Bajaj Auto and 39.29% of Bajaj Finserv, you essentially own a third of India's second-largest two-wheeler manufacturer and two-fifths of one of its most successful financial services companies. Yet BHIL trades at a market capitalization that often exceeds the value of these stakes alone. This "negative holding company discount"—actually a premium—is rare globally and speaks to the market's confidence in BHIL's capital allocation abilities.

Beyond the core holdings, BHIL maintains a diversified investment portfolio. The Company's other equities portfolio comprises of its investments in listed and unlisted entities. This provides optionality—the ability to capitalize on new opportunities without diluting the core holdings. The portfolio is managed conservatively, with a focus on capital preservation and steady returns rather than aggressive risk-taking.

The dividend income stream is substantial and growing. Bajaj Auto and Bajaj Finserv have consistently paid dividends, providing BHIL with cash flows that can be reinvested or distributed to its own shareholders. This creates a virtuous cycle—as the underlying companies grow and increase dividends, BHIL's income grows, allowing for more investments or higher shareholder returns.

BHIL's approach to capital allocation deserves special attention. Unlike many holding companies that either hoard cash or make random investments, BHIL follows a disciplined approach. Excess cash is first evaluated for investment opportunities within the group—can Bajaj Finance use capital more effectively? Are there new ventures worth seeding? Only after exhausting high-return opportunities within the ecosystem does BHIL look outside.

The investment philosophy extends beyond financial returns. BHIL considers strategic value—will an investment strengthen the group's competitive position? Can it provide learning or technology that benefits other group companies? This holistic approach means investments are evaluated not just on IRR but on strategic fit and synergy potential.

Risk management at BHIL is inherently conservative. The company maintains minimal debt, ensuring it's never forced to sell assets at inopportune times. Company has reduced debt. Company is almost debt free. This financial strength provides flexibility—during market downturns, BHIL can be a buyer rather than a seller, acquiring assets when valuations are attractive.

The systematic importance designation brings both privileges and responsibilities. BHIL must maintain higher capital adequacy, follow stricter governance norms, and provide more detailed disclosures. While this increases compliance costs, it also provides credibility with institutional investors and regulators, facilitating smoother operations and better market access.

BHIL's patient capital approach has been particularly valuable for Bajaj Finance's growth. As the finance company expanded aggressively, requiring constant capital infusions, BHIL's steady support provided confidence to other investors. This patient capital, willing to accept short-term dilution for long-term value creation, is rare in public markets.

The portfolio construction philosophy follows what might be called "concentrated diversification." While the core holdings in Bajaj Auto and Bajaj Finserv represent concentration, these businesses themselves are diversified—Auto across products and geographies, Finserv across financial products and customer segments. This provides exposure to India's consumption story without excessive concentration risk.

One underappreciated aspect of BHIL's strategy is its role as a talent developer. Executives can move between group companies, gaining diverse experience. This creates a deep bench of leadership talent, reducing key person risk and ensuring continuity. The holding company structure facilitates this talent mobility in ways that would be difficult in standalone companies.

The investment philosophy also encompasses ESG considerations. BHIL's investments must meet governance standards, environmental responsibilities, and social impact criteria. This isn't just about compliance—it's recognition that sustainable businesses create more long-term value. The Bajaj Group's historical emphasis on ethical business practices provides a strong foundation for modern ESG requirements.

BHIL's approach to valuation is refreshingly long-term. While markets obsess over quarterly earnings, BHIL thinks about terminal value. What will Bajaj Finance be worth when financial inclusion is achieved? What's Bajaj Auto's value in an electric vehicle future? This long-term thinking allows BHIL to hold through volatility that might shake out shorter-term investors.

The systematic importance also means BHIL plays a role in India's financial stability. During crises, BHIL's strong balance sheet and patient capital can provide stability to group companies and, by extension, to the broader financial system. This responsibility is taken seriously—BHIL maintains higher liquidity buffers and capital reserves than strictly necessary.

Looking at the portfolio strategy holistically, BHIL represents a unique value proposition. It offers investors exposure to India's consumption story through both products (Bajaj Auto) and financing (Bajaj Finance). It provides the stability of a holding company with the growth of operating businesses. Most importantly, it offers professional management with family commitment—a rare combination that has created extraordinary value over time.

VI. The Crown Jewels: Understanding the Stakes

The true genius of BHIL lies not just in what it owns but in how these ownership stakes create a symphony of value creation. Each crown jewel—Bajaj Auto, Bajaj Finserv, and Bajaj Finance—represents a different facet of India's economic transformation, yet together they form an integrated ecosystem that captures value at multiple points in the consumption cycle.

Bajaj Auto: The Two-Wheeler Giant

Bajaj Auto is the world's third-largest manufacturer of motorcycles and the second-largest in India. It is the world's largest three-wheeler manufacturer. In December 2020, Bajaj Auto crossed a market capitalisation of ₹1 trillion (US$12 billion), making it the world's most valuable two-wheeler company. This isn't just about scale—it's about a fundamental transformation from a scooter company to a global mobility player.

The transformation under Rajiv Bajaj's leadership has been remarkable. The company made the bold decision to exit scooters entirely—the very product that built the Bajaj empire—to focus on motorcycles. He explains why his son, Rajiv, made the decision in 2009 for Bajaj Auto to stop manufacturing scooters and to only focus on motorcycles. This decision, controversial at the time, proved prescient. By focusing on motorcycles, particularly the sports and premium segments with brands like Pulsar and Dominar, Bajaj Auto carved out a profitable niche.

The international expansion strategy has been equally bold. Unlike competitors who tried to replicate their domestic models abroad, Bajaj Auto adapted to local markets. In Africa, they developed robust motorcycles for rough roads. In Latin America, they created models suited to local preferences. This localization strategy made Bajaj Auto a truly global player, with exports contributing significantly to revenues.

The partnership with KTM represents strategic brilliance. In 2007, Bajaj Auto, through its Dutch subsidiary Bajaj Auto International Holding BV, purchased a 14.5% stake of Austrian rival KTM, gradually increasing its stake to a 48% non-controlling share by 2020. This wasn't just a financial investment—it provided technology access, premium brand association, and entry into developed markets. The KTM partnership elevated Bajaj from a value player to a technology leader.

The electric vehicle transition presents both challenge and opportunity. Bajaj Auto has approached it characteristically—not through expensive bets on unproven technology but through calculated steps. The Chetak electric scooter, reviving an iconic brand for the electric age, shows how Bajaj Auto leverages heritage while embracing the future. The focus on electric three-wheelers for last-mile delivery capitalizes on India's e-commerce boom while addressing urban pollution.

Bajaj Finserv: The Financial Services Behemoth

The financial services and wind energy businesses were transferred to Bajaj Finserv Limited (BFL) as part of the concluded demerger from Bajaj Auto Limited, approved by the High Court of Judicature at Bombay by its order dated 18 December 2007. It is a financial conglomerate with stakes in the financing sector (Bajaj Finance), the life insurance business (Bajaj Life Insurance), the general insurance business (Bajaj General Insurance), and the mutual fund business (Bajaj Finserv Mutual Funds).

Bajaj Finserv is the architecture through which the Bajaj Group captures India's financial services opportunity. It's not an operating company but a holding structure for various financial services businesses. This structure provides flexibility—each business can be optimally capitalized, regulated, and managed while maintaining group synergies.

The insurance ventures with Allianz have been particularly successful. Bajaj Allianz General Insurance is a private general insurance company in India. It is another joint venture between Bajaj Finserv Limited and Allianz SE, established in 2001. These joint ventures brought global expertise to India while leveraging Bajaj's distribution and brand. The life insurance business has built significant embedded value, while general insurance has achieved scale and profitability.

De-merged in 2007, Bajaj Finserv is the holding company for financial services vertical, including insurance, wealth and consumer finance. It owns 52.49% of Bajaj Finance and promotes Bajaj Allianz Life and General Insurance, as well as mutual funds. This 52.49% stake in Bajaj Finance is the crown jewel within the crown jewel—providing majority control of one of India's most successful financial services companies.

The diversification within Bajaj Finserv provides multiple growth engines. Insurance benefits from India's under-penetration. The mutual fund business capitalizes on financialization of savings. The health-tech ventures through Bajaj Finserv Health address healthcare accessibility. Each vertical addresses a massive market opportunity while leveraging group synergies in distribution, technology, and brand.

Bajaj Finance: The NBFC Success Story

Bajaj Finance · Mkt Cap: 5,45,614 Crore (up 33.6% in 1 year) · Revenue: 73,107 Cr · Profit: 17,633 Cr. These numbers tell a story of explosive growth, but the real story is how Bajaj Finance has revolutionized consumer lending in India.

Over 17 years, Bajaj Finance has enabled India's growing mass affluent and middle-class population to fulfil aspirations by providing access to an extensive range of financial solutions. Since inception, the Company has leveraged technology to launch 26 product lines and 51 product variants for retail, MSME and commercial consumers, with major product innovations such as the EMI card and Flexi.

The innovation at Bajaj Finance goes beyond products. They've reimagined the entire lending value chain. The EMI card transformed how Indians think about purchases—from cash to credit. The digital lending platform makes loan approval instant. The cross-sell strategy means a customer acquired for one product becomes a candidate for multiple products. This isn't just lending—it's lifecycle financial services.

Bajaj Finance is mainly engaged in the business of lending. BFL has a diversified lending portfolio across retail, SME and commercial customers with a significant presence in urban and rural India. It also accepts public and corporate deposits and offers variety of financial services products to its customers. This diversification across products, customer segments, and geographies provides resilience. When urban consumption slows, rural grows. When retail faces headwinds, SME lending compensates.

The technology backbone of Bajaj Finance deserves special mention. The company is one of India's leading and most diversified financial services companies. Since its inception, it has leveraged technology to launch 26 product lines and 51 product variants for retail, MSME, and commercial consumers, with major product innovations like the EMI card and Flexi with a significant presence in both urban and rural India. This isn't just digitization of existing processes—it's fundamental reimagination of financial services delivery.

The risk management at Bajaj Finance has been tested through cycles and proven robust. Despite rapid growth, asset quality has remained superior to industry averages. This isn't luck—it's the result of sophisticated credit scoring, diversified portfolio construction, and proactive collection mechanisms. The ability to grow fast while maintaining quality is rare in financial services.

The Network Effects and Synergies

What makes these crown jewels particularly valuable is how they reinforce each other. Bajaj Auto customers become Bajaj Finance customers through two-wheeler financing. Bajaj Finance customers become Bajaj Allianz insurance customers. The data from one business informs risk assessment in another. The brand trust built in one category transfers to another.

The financial linkages are equally important. Bajaj Finance's growth is partly funded by dividends from Bajaj Auto flowing through BHIL and Bajaj Finserv. Bajaj Auto's dealers get working capital from Bajaj Finance. Insurance products are distributed through Bajaj Finance's customer base. These aren't just portfolio companies—they're an integrated ecosystem.

The strategic positioning of each crown jewel is distinctive. Bajaj Auto owns the performance motorcycle segment. Bajaj Finance dominates consumer durable financing. Bajaj Allianz has carved out profitable niches in insurance. Each business has built competitive moats that would be difficult to replicate, providing sustainable competitive advantages.

Looking ahead, the crown jewels are well-positioned for India's next phase of growth. Bajaj Auto benefits from premiumization as consumers upgrade from entry-level to performance bikes. Bajaj Finance capitalizes on financial inclusion as credit penetration increases. Bajaj Finserv's insurance businesses benefit from rising awareness and regulatory push for coverage. Each mega-trend has a Bajaj entity positioned to capture value.

VII. Family Governance & Succession Planning

The Bajaj family's approach to governance represents a fascinating study in balancing family control with professional management, traditional values with modern corporate governance, and individual ambitions with collective success. The philosophy that has guided them for nearly a century is elegantly simple yet profoundly difficult to implement: "Common good more important than individual gain."

The roots of this governance philosophy trace back to Jamnalal Bajaj and his Gandhian principles. The idea that wealth is a trusteeship, that business should serve society, that family members are stewards rather than owners—these weren't just philosophical musings but operational principles that shaped decision-making. This foundation proved crucial when navigating the complex succession and governance challenges that destroy most family businesses by the third generation.

The transition from Rahul Bajaj to the next generation—Rajiv and Sanjiv—was masterfully orchestrated through the demerger. His sons Rajiv Bajaj and Sanjiv Bajaj are involved in the management of his companies. Rather than forcing brothers to work together in a single entity, potentially creating conflict, the structure gave each their own domain. Rajiv got Bajaj Auto, where his engineering mindset and product focus could flourish. Sanjiv got Bajaj Finserv, where his financial acumen and strategic thinking could build an empire.

This separation of kingdoms prevented the succession battles that plague many Indian business families. The Ambani brothers' public feud, the Burman family disputes at Dabur, the Modi family's splitting of businesses—these cautionary tales were avoided at Bajaj through structural foresight. By giving each family member clear ownership and operational control of distinct entities, potential conflicts were preempted.

The Bajaj Group split somewhere in 2008 due to differences among the family members. Brothers Rahul Bajaj and Shishir Bajaj decided to part ways. Interestingly, first cousins Shekhar Bajaj, Madhur Bajaj, and Niraj Bajaj chose to side with Rahul Bajaj. Consequently, the combined entities managed by Rajiv Bajaj, Sanjiv Bajaj, Shekar Bajaj, Madhur Bajaj, and Niraj Bajaj are referred to as the "Bajaj Group." Even this family split was handled with characteristic Bajaj pragmatism—clean separation, fair value distribution, and continued respect despite differences.

The governance structure at BHIL exemplifies the balance between family control and professional management. The family maintains control through strategic stakes held via investment companies. These unlisted entities are fully owned by Bajaj family members and hold stakes in the listed companies. Examples: Bajaj Sevashram Private Limited, Jamnalal Sons Private Limited, Sanjiv Nayan Bajaj Sanjiv Trust etc. This pyramidal structure ensures control without excessive capital commitment, allowing family members to maintain influence while bringing in professional managers and independent directors.

The board composition across Bajaj companies reflects modern governance standards while maintaining family influence. Independent directors bring expertise and external perspective. Professional CEOs run operations. Family members focus on strategy and capital allocation. This separation of ownership, board oversight, and management execution has created accountability while maintaining long-term vision.

The approach to professional management is particularly noteworthy. Unlike many family businesses that view professionals as threats or temporary necessities, the Bajajs have embraced professional management as essential for growth. Key positions are filled based on merit rather than lineage. Performance metrics apply equally to family and non-family executives. This meritocracy has attracted top talent who might otherwise avoid family-controlled businesses.

The commitment to minority shareholder protection sets Bajaj apart. Despite family control, minority shareholders have benefited enormously. The dividend policy is consistent and generous. Related-party transactions are minimal and at arm's length. Corporate actions like the demerger were structured to benefit all shareholders, not just the family. This alignment of interests has created trust with institutional investors and earned premium valuations.

The next generation's preparation has been systematic rather than assumed. Rajiv and Sanjiv Bajaj weren't simply handed the keys—they proved themselves through performance. They worked their way up, made mistakes, learned, and earned their positions. This meritocratic succession, rare in family businesses, ensures competence alongside inheritance.

The family's approach to wealth has remained grounded despite enormous success. The Bajaj family members are known for their relatively modest lifestyles, focus on business rather than glamour, and commitment to philanthropy. This cultural foundation—wealth as responsibility rather than privilege—has prevented the decadence that often accompanies multi-generational wealth.

The governance philosophy extends to stakeholder management. Employees are treated as extended family, with many families having multi-generational associations with Bajaj companies. Dealers and suppliers are partners rather than transactions. This stakeholder capitalism, before it became fashionable, has created loyalty and stability that purely financial relationships cannot match.

The family council structure, though informal, plays a crucial role. Regular family meetings discuss strategic issues, resolve potential conflicts, and maintain alignment. These aren't board meetings but family gatherings where business and personal intersect. This forum for communication prevents misunderstandings from festering into conflicts.

The approach to family employment is pragmatic. Family members can join the business but must prove themselves. They start at operational levels, not in corner offices. Performance standards apply equally. This has prevented the nepotism that weakens many family businesses while maintaining family involvement for those genuinely interested and capable.

Succession planning for the next generation is already underway. The third generation is being groomed—some in the business, others pursuing their own paths. The structure created through the demerger provides flexibility for the next transition. Each entity can handle succession independently, preventing one problematic succession from affecting others.

The family's commitment to institutional building over personal aggrandizement is remarkable. The Bajaj name appears on companies, not on products (unlike Tata). Family members maintain relatively low public profiles despite their influence. The focus remains on building institutions that outlast individuals—a crucial factor in multi-generational success.

Risk management at the family level deserves mention. The wealth isn't concentrated in listed entities alone. Family investment companies provide diversification. Philanthropic trusts preserve wealth for social causes. This multi-layered structure ensures family wealth preservation even if individual businesses face challenges.

The handling of conflicts, when they arise, is instructive. The split with Shishir Bajaj could have been acrimonious. Instead, it was handled professionally—assets divided, businesses separated, and relationships maintained at a cordial level. This ability to separate business from personal, to disagree without destroying, is crucial for family business longevity.

Looking ahead, the Bajaj family governance model offers lessons for other business families. First, structure preempts conflicts—clear ownership and operational boundaries prevent disputes. Second, professional management enhances rather than threatens family control. Third, minority shareholder alignment creates value for all. Fourth, cultural values—ethics, service, humility—provide the foundation for multi-generational success.

VIII. The Playbook: Lessons in Value Creation

The Bajaj Holdings & Investment story offers a masterclass in value creation that transcends conventional financial engineering. This isn't about leveraged buyouts, aggressive accounting, or financial gymnastics. Instead, it's a playbook of fundamental value creation through strategic structure, patient capital, and disciplined execution. The lessons from BHIL's journey offer a template for building enduring wealth in emerging markets.

Demerger as Value Unlock Mechanism

The 2007-2008 demerger stands as perhaps the most successful corporate restructuring in Indian history. The demerger truly resulted in unlocking of shareholder value. The combined annualised return of the three companies post demerger is 20.7% compared to 9.5% of Sensex. This outperformance wasn't accidental—it was architected through careful planning and execution.

The key insight was recognizing that conglomerate structures, while valuable during capital-scarce environments, become value-destructive in developed capital markets. Investors want focused exposure. Analysts need comparable metrics. Management requires clear mandates. The demerger provided all three, allowing each entity to be valued on its own merits rather than being lost in consolidated complexity.

The lesson extends beyond just splitting companies. The architecture matters. Creating BHIL as a holding company rather than directly distributing shares to shareholders was crucial. It maintained family control while allowing professional management. It provided a vehicle for capital allocation across businesses. It created an entity that could compound value independently. This three-way split—operating company, financial services, and holding company—has become a template for other conglomerates considering restructuring.

Patient Capital and Long-term Thinking

BHIL exemplifies the power of patient capital in an impatient market. While markets obsess over quarterly earnings, BHIL thinks in decades. This long-term orientation allows for decisions that might seem suboptimal short-term but create enormous long-term value.

Consider Bajaj Finance's growth trajectory. The aggressive expansion required constant capital infusion, diluting returns in the short term. Many investors would have pushed for slower growth and higher dividends. BHIL's patient capital allowed Bajaj Finance to prioritize market share and capability building over immediate returns. The result? A company worth over ₹5 trillion, validating the patient capital approach.

The holding period for investments is measured in decades, not quarters. This allows BHIL to hold through cycles, benefiting from long-term compounding rather than trying to time markets. The stability this provides to portfolio companies is invaluable—they can plan for the long term knowing their major shareholder won't demand short-term actions that compromise long-term value.

The Power of Focused Entities vs. Conglomerates

The transformation from conglomerate to focused entities demonstrates a crucial lesson: specialization creates value. Bajaj Auto as a focused mobility company can make decisions optimized for manufacturing cycles. Bajaj Finance as a pure financial services player can leverage appropriately for its business model. Neither has to compromise for the other.

This focus extends to human capital. Each company can build its own culture, compensation structure, and talent strategy. Bajaj Auto can hire engineers and designers. Bajaj Finance can attract risk managers and data scientists. The holding company can develop capital allocators and strategic thinkers. This specialization in human capital is impossible in a conglomerate where one size must fit all.

The market valuation benefits are substantial. Focused entities trade at higher multiples than conglomerates. They attract specialist investors who understand the business deeply. They can be benchmarked against pure-play competitors. This clarity in positioning and valuation has contributed significantly to value creation.

Managing Cyclicality through Diversification

While each entity is focused, BHIL's portfolio provides diversification across cycles. Auto is cyclical, tied to economic growth and consumer sentiment. Financial services have their own cycles, influenced by credit availability and regulatory changes. The investment portfolio provides additional diversification. This multi-cylinder engine ensures some part of the portfolio is always performing.

The diversification isn't random but strategic. Each business has different capital requirements at different times. During auto downturns, capital can flow to financial services. When financial services face regulatory headwinds, auto investments can be prioritized. This dynamic capital allocation across cycles has enhanced returns while reducing risk.

Corporate Governance in Family-Controlled Businesses

BHIL demonstrates that family control and good governance aren't mutually exclusive. Promoter Holding: 51.5% Despite majority family control, minority shareholders have benefited enormously. This alignment has been achieved through multiple mechanisms.

First, the family's wealth is tied to the same shares as minority investors. There's no dual-class structure or differential voting rights. When share prices rise, everyone benefits proportionally. Second, independent directors provide genuine oversight rather than rubber-stamping family decisions. Third, professional management ensures operational decisions are merit-based rather than relationship-based.

The transparency in related-party transactions is exemplary. When transactions occur between group companies, they're at arm's length and fully disclosed. This transparency has built trust with institutional investors who might otherwise avoid family-controlled businesses.

The "Hold Forever" Investment Philosophy

BHIL's investment philosophy challenges conventional portfolio theory. Instead of diversifying across hundreds of positions, BHIL concentrates on a few high-quality assets held forever. This concentration requires deep understanding and conviction but generates superior returns.

The "hold forever" philosophy doesn't mean "hold regardless." It means holding as long as the fundamental thesis remains intact. If Bajaj Auto remains a leader in mobility, if Bajaj Finance continues growing profitably, if India's consumption story continues—the holdings make sense. This discipline in holding quality assets through volatility has been a key value driver.

The tax efficiency of this approach is significant. By not trading, BHIL avoids transaction costs and taxes. The compound effect of these savings over decades is substantial. Moreover, the stability this provides to portfolio companies—knowing their major shareholder isn't looking to exit—allows for long-term planning and investment.

Capital Allocation Excellence

Perhaps BHIL's greatest skill is capital allocation. Every rupee is evaluated for its best use. Should it be invested in existing businesses? Returned to shareholders as dividends? Held for future opportunities? This disciplined approach to capital allocation has generated superior returns.

The dividend policy exemplifies this discipline. Bajaj Holdings & Investment has fixed 27 June 2025 as record date for the purpose of determining the members eligible to receive the dividend for the financial year ended 31 March 2025. The dividend, if approved, shall be paid on or before 15 August 2025. Regular dividends provide income to shareholders while retaining sufficient capital for growth investments.

The acquisition strategy, or lack thereof, is instructive. Unlike many cash-rich companies that make expensive acquisitions for growth, BHIL has been remarkably disciplined. Organic growth through existing platforms has been prioritized over expensive acquisitions. This discipline has prevented the value destruction that often accompanies M&A activity.

Creating Platforms, Not Just Products

Each Bajaj entity has built platforms rather than just products. Bajaj Auto isn't just manufacturing motorcycles—it's building a mobility platform. Bajaj Finance isn't just lending—it's creating a financial services platform. These platforms can launch new products, enter new segments, and capture adjacent opportunities more easily than single-product companies.

The platform approach creates competitive advantages. Customer acquisition costs are amortized across multiple products. Brand investments benefit the entire portfolio. Technology infrastructure serves multiple use cases. These economies of scope, combined with economies of scale, create formidable competitive moats.

The Ecosystem Advantage

The Bajaj ecosystem creates value beyond individual companies. A customer's journey might start with a Bajaj motorcycle, financed by Bajaj Finance, insured by Bajaj Allianz. Each touchpoint reinforces brand trust and creates cross-selling opportunities. This ecosystem approach—before it became fashionable in technology companies—has been a key value driver.

The data advantage from this ecosystem is underappreciated. Customer behavior in one business informs risk assessment in another. Payment history in auto loans indicates creditworthiness for personal loans. Insurance claims data improves underwriting. This information advantage, built over decades, is nearly impossible for competitors to replicate.

Looking at the playbook holistically, BHIL's value creation hasn't come from any single brilliant move but from consistently executing multiple value-creating strategies over decades. It's the compound effect of good decisions, disciplined execution, and patient capital that has created extraordinary wealth. This playbook—focusing businesses, governing professionally, allocating capital wisely, and thinking long-term—offers a template for value creation that transcends industries and geographies.

IX. Bear Case vs. Bull Case

The investment merits of Bajaj Holdings & Investment Limited present a fascinating study in contrasts. While the bull case points to one of India's greatest compounding stories, the bear case raises legitimate concerns about structure, regulation, and disruption. Understanding both perspectives is crucial for evaluating BHIL's future trajectory.

Bear Case: The Structural and Strategic Concerns

The holding company discount remains the bears' primary argument. Globally, holding companies trade at 20-40% discounts to their net asset value, reflecting lack of control, opacity, and inefficient capital structures. While BHIL has historically defied this norm, bears argue this is unsustainable. As markets mature and investors become more sophisticated, BHIL should theoretically converge to global norms, implying significant valuation compression.

The concentration risk in financial services is alarming for conservative investors. With Bajaj Finance and Bajaj Finserv representing the majority of BHIL's value, any regulatory shock to the financial sector would devastate BHIL's valuation. The Reserve Bank of India's increasing scrutiny of NBFCs, concerns about over-leveraging, and periodic regulatory tightening create ongoing overhang. One adverse regulatory change could impair the crown jewel's value significantly.

Company has a low return on equity of 12.3% over last 3 years. This relatively low ROE for a financial holding company raises questions about capital efficiency. Bears argue that investors could achieve better returns by directly owning the underlying assets rather than holding them through BHIL's structure.

The electric vehicle disruption threatens Bajaj Auto's long-term value. While Bajaj has entered the EV space, it lacks the first-mover advantage it enjoyed in traditional motorcycles. New entrants like Ola Electric, Ather, and potential Chinese competitors could disrupt Bajaj Auto's market position. The capital requirements for EV transition—new platforms, battery technology, charging infrastructure—could pressure returns for years.

The family control structure, while historically beneficial, presents governance risks. With 51.5% promoter holding, minority shareholders have limited influence on major decisions. The next generation's capability and commitment remain untested. History is littered with third-generation failures in family businesses, and BHIL isn't immune to this risk.

The macroeconomic sensitivity is another concern. BHIL's portfolio is essentially a leveraged bet on Indian consumption. Any prolonged economic slowdown would impact both Bajaj Auto (discretionary purchase) and Bajaj Finance (credit growth) simultaneously. Unlike diversified global companies, BHIL has no geographic hedge against Indian economic volatility.

The regulatory overhang on NBFCs continues to worry bears. Recent RBI actions against various NBFCs for compliance failures, the push for lower interest rates, and potential regulations on lending practices could impact Bajaj Finance's profitability. The systematic importance designation, while prestigious, brings additional regulatory scrutiny and compliance costs.

The technological disruption in financial services poses existential questions. Fintech startups, backed by billions in venture capital, are attacking every segment Bajaj Finance operates in. Digital lending platforms offer instant loans. Buy-now-pay-later services challenge the EMI model. Neo-banks target the same customer base. While Bajaj Finance has digitalized, bears question whether a traditional NBFC can compete with digital-native competitors.

The valuation concerns are legitimate. Mkt Cap: 1,51,432 Crore At current valuations, BHIL trades at premium multiples. Bears argue this prices in perfect execution and leaves no room for error. Any disappointment in growth, margins, or asset quality could trigger significant valuation compression.

Bull Case: The Compounding Machine

The bulls see BHIL as one of the last great compounding stories in Indian markets. The track record speaks for itself—seventeen-fold growth in market cap over sixteen years, consistently outperforming indices, and creating enormous wealth for patient shareholders. This isn't luck but the result of superior business models and execution.

India's consumption story is just beginning. With per capita income still under $3,000, financial inclusion at early stages, and vehicle penetration far below global averages, the runway for growth is decades long. BHIL offers leveraged exposure to this mega-trend through best-in-class operators. As India grows from a $3.5 trillion to $10 trillion economy, BHIL's portfolio companies will capture disproportionate value.

The financial inclusion opportunity alone justifies bullishness. Credit penetration in India is still below 20% of GDP compared to 50%+ in developed markets. Bajaj Finance, with its proven execution and risk management, is perfectly positioned to capture this growth. The addressable market expansion over the next decade could drive 20%+ annual growth.

The governance track record deserves premium valuation. Despite family control, minority shareholders have been treated fairly for decades. The consistent dividend payments, value-accretive corporate actions, and professional management justify trust. In a market where corporate governance failures regularly destroy value, BHIL's track record is invaluable.

The hidden asset value provides additional upside. Earnings include an other income of Rs.8,152 Cr. Beyond the listed stakes, BHIL owns real estate, unlisted investments, and cash that aren't fully reflected in market valuations. The Maharashtra Scooters stake alone, at 51% ownership, represents hidden value.

The competitive moats are deepening, not eroding. Bajaj Auto's brand took decades to build and can't be replicated with capital alone. Bajaj Finance's data advantage from millions of customers creates underwriting capabilities competitors can't match. The distribution networks, dealer relationships, and customer trust represent intangible assets worth multiples of book value.

The execution capability sets BHIL apart. While many Indian companies struggle with execution, Bajaj companies consistently deliver. Bajaj Auto successfully transitioned from scooters to motorcycles. Bajaj Finance scaled from regional player to national giant. This execution DNA, embedded across portfolio companies, suggests future challenges will be successfully navigated.

The capital allocation optionality is valuable. With minimal debt and strong cash generation, BHIL can capitalize on opportunities others can't. During downturns, BHIL can be a buyer while leveraged competitors struggle. This counter-cyclical capability has historically created enormous value and will likely continue.

The ecosystem synergies are strengthening. As digital integration increases, the data and customer sharing across Bajaj companies becomes more valuable. A customer acquired by one company becomes a potential customer for all. This network effect, similar to technology platforms, could drive superior growth and margins.

The management pipeline is robust. Unlike many family businesses struggling with succession, Bajaj has demonstrated smooth leadership transitions. The professional management bench is deep. The next generation has been systematically groomed. This continuity reduces key person risk and ensures long-term stability.

The Balanced Perspective

The truth likely lies between extreme bear and bull cases. BHIL faces real challenges—regulatory risks, technological disruption, and valuation concerns are legitimate. However, the company's track record of navigating challenges, the quality of underlying businesses, and the long runway for growth in India provide substantial cushion.

The holding company discount concern is partially valid but overstated. While BHIL might not always trade at a premium, the quality of assets and governance should prevent deep discounts seen in other holding companies. The regulatory risks in financial services are real but manageable—Bajaj Finance has navigated multiple regulatory cycles successfully.

The EV disruption in auto is a challenge but also an opportunity. Bajaj's manufacturing expertise, distribution network, and brand remain valuable in an electric future. The financial services disruption from fintech is forcing innovation, making Bajaj Finance stronger. These challenges, while real, could catalyze transformation rather than destruction.

The valuation concerns deserve monitoring. At current levels, BHIL offers limited margin of safety. However, for long-term investors focused on compounding rather than trading, the quality of businesses and management justify patience. History suggests selling quality compounders on valuation concerns is usually a mistake.

Ultimately, the bear versus bull debate on BHIL comes down to time horizon and risk tolerance. Short-term traders might find better opportunities elsewhere. But for investors seeking to compound wealth over decades, backing India's consumption story through proven operators, BHIL remains compelling despite the risks.

X. Power & Counter-Positioning Analysis

Understanding Bajaj Holdings & Investment Limited through the lens of competitive strategy reveals multiple sources of power that create its formidable moat. Using Hamilton Helmer's 7 Powers framework and analyzing BHIL's counter-positioning against traditional conglomerates provides insights into why this holding company has defied conventional patterns and created extraordinary value.

Scale Economies: The Overwhelming Advantage

The scale economies in BHIL's portfolio companies are staggering. Bajaj Finance · Mkt Cap: 5,45,614 Crore This massive scale creates per-unit cost advantages that smaller competitors cannot match. In financial services, scale drives down cost of funds—Bajaj Finance can borrow cheaper than smaller NBFCs. In manufacturing, Bajaj Auto's volumes enable procurement advantages and R&D amortization that regional players cannot achieve.

The scale benefits extend beyond simple cost advantages. In financial services, scale enables sophisticated risk management systems, advanced analytics, and technology investments that wouldn't be viable at smaller scales. Bajaj Finance's ability to invest hundreds of crores in digital infrastructure is only possible because these costs are spread across millions of customers. Smaller competitors attempting similar investments would find the per-customer costs prohibitive.

The data advantage from scale is particularly powerful. With millions of customers across decades, Bajaj Finance has built proprietary datasets that improve underwriting, reduce fraud, and enable personalized pricing. Every additional customer makes the data moat deeper. This recursive improvement—more customers generate more data, which enables better products, which attracts more customers—creates a flywheel that accelerates with scale.

Network Effects: The Ecosystem Multiplier

While not as obvious as in technology platforms, BHIL's portfolio exhibits powerful network effects. The Bajaj ecosystem becomes more valuable to each participant as more participants join. A Bajaj Auto dealer benefits when Bajaj Finance offers financing—it increases sales. Bajaj Finance benefits from Bajaj Auto's dealer network—it provides distribution. Bajaj Allianz benefits from both—customer acquisition channels and risk assessment data.

The brand network effect is underappreciated. Each positive experience with one Bajaj company increases trust in others. A satisfied Bajaj Auto customer is more likely to choose Bajaj Finance for a personal loan. This brand transference, built over decades, creates customer acquisition advantages that new entrants cannot replicate regardless of capital invested.

The supplier and partner network effects are equally powerful. Vendors prefer working with Bajaj companies knowing they'll be paid on time and treated fairly. Regulators trust Bajaj entities based on historical compliance. International partners like KTM and Allianz chose Bajaj partly due to network reputation. These relationship networks, built over generations, create access and opportunities unavailable to competitors.

Brand Power: The Trust Premium

In markets where trust is scarce, brand becomes invaluable. The Bajaj brand, built over nearly a century, commands premium valuations and customer loyalty that transcends rational economic calculation. In financial services, where trust is the product, the Bajaj name enables lower customer acquisition costs and higher retention rates than competitors.

The brand power manifests in pricing ability. Bajaj Finance can charge slightly higher rates than competitors because customers value the certainty and service quality. Bajaj Auto commands premiums for comparable products because buyers trust the quality and resale value. This pricing power, flowing directly to margins, is the ultimate proof of brand value.

The resilience provided by brand power is crucial during crises. When IL&FS collapsed and NBFC lending froze, Bajaj Finance continued accessing capital markets. When COVID hit and auto sales plummeted, Bajaj Auto maintained dealer loyalty. Brand acts as insurance during volatility, enabling continuity when weaker brands fail.

The Berkshire Hathaway Parallel

The parallels between BHIL and Berkshire Hathaway are striking and instructive. Both are holding companies that transformed from operating businesses (textiles for Berkshire, auto for Bajaj). Both are run by families with long-term orientation. Both prioritize wholly-owned quality businesses over diversification. Both have created extraordinary wealth through patient capital allocation.

Like Berkshire, BHIL benefits from permanent capital. Unlike mutual funds facing redemptions or private equity facing exit pressures, BHIL can hold investments forever. This permanent capital structure enables long-term thinking, countercyclical investing, and compound returns that temporary capital cannot achieve.

The reputation for fair dealing, similar to Buffett's approach, has become a competitive advantage. Sellers prefer dealing with BHIL knowing they'll be treated fairly. Regulators trust BHIL's compliance. Minority investors accept family control knowing their interests are protected. This reputational capital, built over decades, enables opportunities and reduces frictions that create tangible value.

Counter-Positioning Against Traditional Conglomerates

BHIL's structure deliberately counter-positions against traditional conglomerate weaknesses. Where conglomerates suffer from complexity, BHIL maintains simplicity—clean holdings in focused entities. Where conglomerates face succession challenges, BHIL's structure enables smooth transitions. Where conglomerates trade at discounts, BHIL commands premiums.

The transparency in BHIL's structure counters the opacity typical of conglomerates. Each underlying business reports separately, enabling accurate valuation. Related-party transactions are minimal and disclosed. This transparency attracts institutional investors who avoid opaque conglomerates, enabling premium valuations.

The focused management counter-positions against conglomerate bureaucracy. Each Bajaj company has its own CEO, board, and strategy. Decisions are made quickly at the operating level rather than requiring corporate approval. This agility enables rapid response to market changes while maintaining strategic coherence through board oversight.

Capital as a Competitive Weapon

BHIL's capital strength creates strategic options unavailable to leveraged competitors. During the 2008 crisis, while others were selling assets, BHIL was investing. During COVID, while competitors conserved cash, Bajaj Finance gained market share. This ability to invest countercyclically, enabled by strong balance sheets, creates long-term advantages.

The patient capital BHIL provides to portfolio companies enables long-term investments competitors cannot make. Bajaj Auto can invest in EV platforms without immediate return pressure. Bajaj Finance can enter new segments accepting initial losses. This patient capital, rare in public markets, enables strategic moves that create lasting advantages.

The signaling effect of BHIL's capital is powerful. When BHIL invests, markets notice. Partners gain confidence. Regulators see stability. This signaling effect reduces cost of capital for portfolio companies and enables partnerships that might otherwise be unavailable.

The India Advantage: Demographics and Growth

BHIL's power is amplified by India's structural advantages. With median age of 28, India has decades of demographic dividend ahead. Rising incomes, increasing urbanization, and growing formalization create expanding addressable markets. BHIL's portfolio is perfectly positioned to capture these tailwinds.

The underpenetration in BHIL's markets creates runway for growth. Two-wheeler penetration in India is still a fraction of other Asian countries. Credit penetration is below 20% of GDP versus 50%+ in developed markets. Insurance penetration remains among the lowest globally. These gaps represent not just growth opportunity but competitive advantage for established players who can capture share as markets expand.

The regulatory evolution in India increasingly favors organized players. GST implementation advantages formal businesses. Digital payments reduce cash transactions. Credit bureaus improve risk assessment. These structural changes benefit established players like Bajaj companies while challenging informal competitors.

Process Power: The Execution Excellence

The process power in Bajaj companies is remarkable. Bajaj Auto's manufacturing excellence enables global cost competitiveness despite Indian infrastructure challenges. Bajaj Finance's risk management processes have delivered superior asset quality through multiple cycles. These processes, refined over decades, create execution advantages difficult to replicate.

The continuous improvement culture embedded in processes creates dynamic advantages. Each cycle teaches lessons that improve future performance. Each customer interaction generates data that enhances service. Each product iteration incorporates learnings. This learning organization capability, where processes continuously evolve, ensures advantages compound rather than erode.

The talent development processes deserve special mention. Bajaj companies consistently develop leaders internally rather than hiring externally. This creates cultural continuity, deep domain expertise, and loyalty that enhance execution. The ability to develop and retain talent in India's competitive market is itself a source of power.

Switching Costs: The Sticky Ecosystem

Once customers enter the Bajaj ecosystem, switching costs keep them there. A Bajaj Finance customer with multiple products faces hassle in switching. A Bajaj Auto dealer with decades of relationship has emotional and economic switching costs. These switching costs, both tangible and intangible, create customer lifetime value that exceeds acquisition costs.

The data integration creates technical switching costs. As Bajaj companies increasingly share data and provide integrated services, customers lose personalization benefits by switching. The convenience of staying within the ecosystem—seamless credit approval, insurance coverage, vehicle financing—makes switching increasingly irrational.

Looking at BHIL's sources of power holistically, it becomes clear why this holding company has created extraordinary value. Multiple reinforcing powers—scale, network effects, brand, capital strength, and process excellence—create a moat that deepens with time. The counter-positioning against traditional conglomerates ensures structural advantages. The India opportunity provides decades of runway. Together, these powers suggest BHIL's value creation journey is far from over.

XI. What Would You Do?