NESCO: The Engineering Company That Became Mumbai's Real Estate Goldmine

I. Introduction & Episode Roadmap

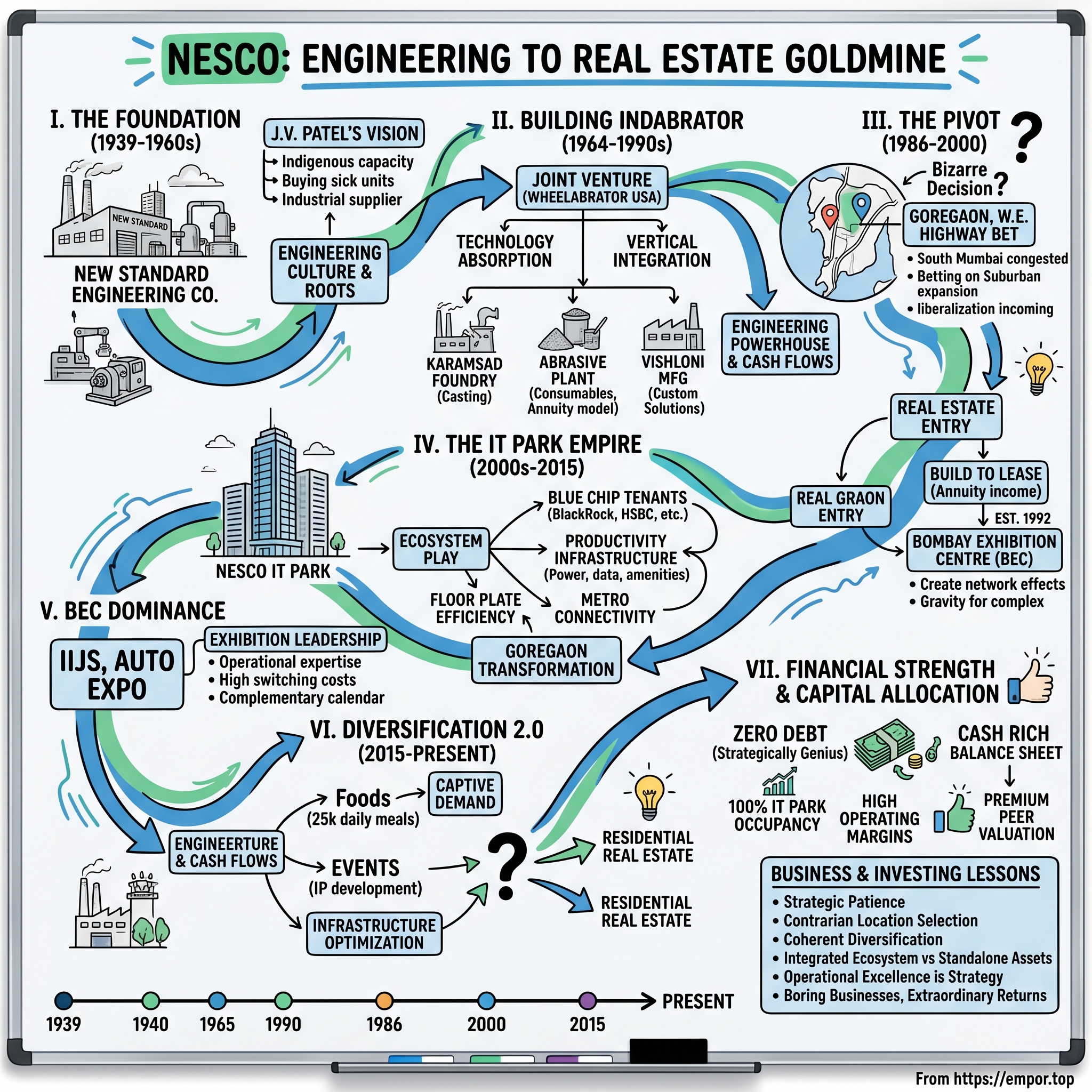

Picture this: It's 1986, and the western suburbs of Mumbai are still considered the outskirts. Goregaon is a sleepy neighborhood known more for its film studios than commercial potential. A 47-year-old engineering company that makes shot-blasting equipment—machines that clean metal surfaces—makes what seems like an inexplicable decision. They're going to build office spaces. Not in Nariman Point where the action is, not in Bandra-Kurla Complex where planners envision the future, but in Goregaon, on a stretch of land along the yet-to-be-completed Western Express Highway.

Fast forward to today. That same company, NESCO Ltd, commands a market capitalization of ₹9,664 crore. Their IT parks house the who's who of global finance—BlackRock, HSBC, KPMG, PwC. The Bombay Exhibition Centre they built has become India's largest private exhibition venue. And here's the kicker: they're completely debt-free in a business where leverage is considered oxygen.

This is the story of how the New Standard Engineering Company—founded in 1939 to build industrial equipment for a pre-independence India—transformed into one of Mumbai's most valuable real estate plays. It's a tale of three generations of the Patel family, of betting on locations before they're fashionable, and of understanding that sometimes the best pivots aren't about abandoning your past but building on top of it.

The central question we're exploring isn't just how an engineering company became a real estate powerhouse. It's about something more fundamental: In a country where conglomerates often destroy value through unrelated diversification, how did NESCO build a portfolio of businesses that actually reinforce each other? Why does a company with 68.5% promoter holding and limited float trade at such rich valuations? And what can we learn from their patient, multi-generational approach to capital allocation?

We'll journey through four major inflection points: the founding vision of J.V. Patel in 1939, the establishment of Indabrator in 1964 that created their engineering moat, the prescient real estate pivot in 1986, and the creation of an integrated business ecosystem from 2000 onwards. Along the way, we'll uncover why being early to Goregaon mattered more than anyone imagined, how exhibitions create network effects, and why running a debt-free operation in cyclical businesses might be the ultimate competitive advantage.

II. The Founding Story & J.V. Patel's Vision (1939–1960s)

The year is 1939. World War II is erupting across Europe, and India remains under British colonial rule. In this environment of global upheaval and local subjugation, a young Gujarati entrepreneur named Jethabhai V. Patel sees an opportunity that others miss. While the British control India's major industries and imports dominate the market, Patel believes in something radical for its time: indigenous industrial capability.

Shri J.V. Patel didn't come from privilege. Growing up in a Gujarat that was primarily agricultural, he witnessed firsthand how India's lack of industrial infrastructure kept it dependent on foreign powers. His response wasn't political activism—it was entrepreneurial action. He founded the New Standard Engineering Company with a mission that sounds simple today but was revolutionary then: build equipment that Indian industries needed, using Indian hands and Indian minds.

What made Patel different wasn't just his vision—it was his approach to failure. In the 1940s and 1950s, as India gained independence and struggled to build its industrial base, numerous companies failed. Banks were reluctant to lend, technical expertise was scarce, and market demand was uncertain. While others saw these "sick units" as toxic assets, Patel saw opportunity. He began acquiring struggling companies, earning a reputation as the "Doctor of Sick Units."

Think about the audacity of this approach. In a newly independent nation with limited capital markets, no venture capital ecosystem, and minimal industrial infrastructure, Patel was essentially running a private equity turnaround fund before such concepts existed in India. He would acquire distressed assets, inject not just capital but technical expertise and management discipline, and transform them into viable businesses.

The post-independence context is crucial here. Nehru's India was pursuing a socialist model with heavy state involvement, but there was space for private enterprise in certain sectors. The government's import substitution policies, while often criticized for creating inefficiencies, actually created a protective moat for companies like New Standard Engineering. If you wanted surface preparation equipment—essential for any manufacturing process involving metal—importing was expensive and time-consuming. Patel's company could provide it locally.

But why surface preparation equipment? This wasn't glamorous technology. Shot-blasting machines essentially fire small metal pellets at high velocity to clean or strengthen metal surfaces. Boring? Perhaps. Essential? Absolutely. Every piece of industrial equipment, every steel structure, every manufactured metal component needs surface preparation. Patel understood something fundamental: in a industrializing economy, selling the picks and shovels is often more profitable than mining for gold.

By the 1950s, New Standard Engineering had established itself as a reliable supplier to India's nascent industrial sector. They weren't just importing and assembling—they were designing and manufacturing. This technical capability would become crucial for what came next. Patel was building more than a company; he was building an engineering culture that could adapt and evolve.

The company's early clients included the Indian Railways, defense establishments, and the emerging steel plants in Bhilai and Rourkela. Each relationship wasn't just a transaction—it was a learning opportunity. How do you descale massive steel plates? How do you prepare surfaces for critical defense equipment? How do you ensure consistency across thousands of components? New Standard Engineering was essentially enrolled in India's industrial university, with each client teaching them something new.

Patel's management philosophy, radical for its time, was built on three principles. First, complete backward integration—control your supply chain to control your quality. Second, patient capital—don't chase quick profits at the expense of long-term capability building. Third, and most importantly, succession planning—ensure the next generation understands not just the business but the mission.

This last point would prove prophetic. As the 1960s dawned, India was changing. The economy was growing, albeit slowly. Industrial capacity was expanding. And New Standard Engineering was about to make a move that would transform it from a local equipment manufacturer into a technology leader. The foundation that J.V. Patel built—technical expertise, financial discipline, and a reputation for reliability—would enable the company's next chapter: the creation of Indabrator.

III. Building Indabrator: The Engineering Powerhouse (1964–1990s)

The invitation arrived at New Standard Engineering's modest Mumbai office in 1963, typed on thin aerogram paper. Wheelabrator Corporation of USA, one of the world's leading surface preparation technology companies, was looking for an Indian partner. For most Indian companies at the time, this would have been seen as winning the lottery—access to American technology, global best practices, and instant credibility. But J.V. Patel saw it differently. This wasn't just about importing technology; it was about absorbing it, improving it, and eventually owning it.

The joint venture that created Indabrator in 1964 was structured unlike typical foreign collaborations of that era. While most Indian companies were content being perpetual licensees, paying royalties indefinitely, Patel negotiated something different. The agreement included technology transfer provisions, training for Indian engineers, and crucially, a path to complete ownership. When Wheelabrator Corporation was acquired by Waste Management Inc. years later and decided to exit non-core international ventures, Patel was ready. He bought them out, making Indabrator fully Indian-owned.

But ownership was just the beginning. What Patel and his team built next was remarkable in its scope and ambition. Instead of just assembling imported components, they went completely vertical. First came the foundry in Karamsad, Gujarat—60 acres of land transformed into a state-of-the-art casting facility. Why did this matter? Because the heart of any shot-blasting machine is its blast wheel, and the quality of the casting determines everything—durability, efficiency, maintenance cycles. By controlling the foundry, Indabrator controlled its destiny.

Then came the abrasive plant, also in Karamsad. This might seem like overkill—why manufacture the steel shots and grits that the machines fire? But consider the economics: abrasives are consumables. Every customer needs continuous supply. By manufacturing both the machines and the consumables, Indabrator created an annuity business model decades before SaaS companies made it fashionable. Sell the printer, then sell the ink—except here it was sell the blasting machine, then sell the abrasives.

The Vishnoli manufacturing facility, spread across 12 acres, became the nerve center of operations. By the 1970s, it wasn't just producing standard machines—it was customizing solutions for specific industries. The Indian Railways needed equipment to descale kilometer-long rails. Defense establishments required precision surface preparation for aerospace components. Steel plants wanted massive tunnel-type machines that could handle continuous production. Each custom order pushed Indabrator's engineering capabilities further.

The numbers tell only part of the story. Over 5,000 machines supplied in India and abroad—impressive, certainly. But what those numbers don't capture is the institutional knowledge being accumulated. Every machine failure was a learning opportunity. Every customer complaint led to a design improvement. Every export order (and Indabrator was exporting to Southeast Asia and Africa by the 1980s) provided exposure to different operating conditions and requirements.

The competitive moat that emerged wasn't just about scale or technology—it was about ecosystem control. Imagine you're a large industrial customer in 1985 India. You need surface preparation equipment for your new plant. You could import from Europe or America—expensive, long lead times, uncertain service support. Or you could buy from Indabrator. They'd customize the equipment for your needs, manufacture it locally (meaning faster delivery and lower costs), supply the consumables, and provide service support with engineers who spoke your language and understood your constraints. The choice was obvious.

But Indabrator's real strategic masterstroke was recognizing that surface preparation was becoming more sophisticated. Environmental regulations were tightening globally. Dust-free, enclosed blasting systems were becoming mandatory. Recovery and recycling of abrasives was now essential. While competitors were still selling basic equipment, Indabrator was investing in next-generation technology. They introduced dust collectors, abrasive recovery systems, and automated controls—features that weren't just nice-to-have but would soon become regulatory requirements.

The 1980s brought new challenges and opportunities. India's economy was slowly liberalizing. Foreign competition was increasing. But Indabrator had spent two decades building something that couldn't be easily replicated—deep technical expertise combined with local manufacturing capability and established customer relationships. They weren't just equipment suppliers; they were solution partners to India's industrial sector.

By 1986, Indabrator was generating steady cash flows, had dominant market share, and faced an interesting problem—what to do with the profits? The surface preparation market, while stable, wasn't growing exponentially. Reinvesting everything back into the same business would yield diminishing returns. The Patel family, now in its second generation of leadership, faced a crucial decision. Do they expand internationally, acquire competitors, or do something completely different?

The answer they chose would seem bizarre to any management consultant. They decided to go into real estate. Not industrial real estate that might complement their engineering business, but commercial office space. In Goregaon. In 1986. This wasn't diversification—this was transformation. And it would prove to be one of the most prescient business decisions in Indian corporate history.

IV. The Pivot: From Manufacturing to Real Estate (1986–2000)

The board meeting in 1986 must have been interesting. Here's NESCO, a successful engineering company with steady cash flows from Indabrator, and someone proposes: "Let's build offices in Goregaon." To understand how radical this was, you need to understand Mumbai's geography of the 1980s. Nariman Point was the undisputed business district. Bandra-Kurla Complex was emerging as the planned alternative. Goregaon? That was where Filmistan and Film City were located. It was where you went to shoot movies, not conduct business.

But NESCO's leadership saw something others missed. The company already owned land along what would become the Western Express Highway—a massive infrastructure project that would transform Mumbai's suburban connectivity. They understood that Mumbai's island geography meant one thing: expansion could only happen northward. And they recognized that the liberalization winds beginning to blow would eventually bring multinational corporations needing modern office space—something Mumbai's traditional business districts, constrained by old buildings and impossible traffic, couldn't provide.

The decision to diversify into real estate wasn't made in isolation. It was informed by a careful reading of global trends. Singapore and Hong Kong were building modern business parks. Technology companies in California's Silicon Valley were demanding campus-style offices rather than traditional downtown high-rises. India might have been a closed economy in 1986, but the Patels were betting it wouldn't remain one forever.

The first phase was modest—developing basic commercial spaces that could be leased to Indian companies looking for affordable alternatives to expensive South Mumbai real estate. But even in this early phase, NESCO did something different. Instead of building and selling (the traditional developer model), they built to lease. This meant lower immediate returns but created an annuity income stream—similar to what they'd learned from the abrasives business at Indabrator.

Then came 1991. India's economic liberalization changed everything. Suddenly, multinational corporations were setting up Indian operations. They needed offices—modern, air-conditioned, with parking and amenities their employees expected. South Mumbai was too expensive and too congested. Bandra-Kurla Complex was still developing. NESCO's Goregaon location, once considered too far, was now perfectly positioned—accessible from both the western and central suburbs where employees lived, right on the Western Express Highway, with space for expansion.

The masterstroke came in 1992 with the establishment of the Bombay Exhibition Centre (BEC). This wasn't just about adding another revenue stream—it was about creating an ecosystem. Exhibitions bring thousands of visitors. These visitors need food, parking, and sometimes accommodation. The exhibition organizers need offices. The companies exhibiting often decide they want a permanent presence nearby. By building BEC, NESCO wasn't just developing real estate; they were creating gravity—a reason for businesses to locate specifically in their complex.

Consider the psychology of this move. Exhibition centers are typically built by governments or trade associations—they're seen as infrastructure, not profit centers. But NESCO recognized something others missed: exhibitions create network effects. The more exhibitions you host, the more organizers want to use your venue (because that's where attendees expect to go). The more successful exhibitions, the more companies want to exhibit. The more companies exhibit, the more they consider permanent offices nearby. It's a virtuous cycle that compounds over time.

The timing was perfect. The 1990s saw an explosion in trade exhibitions as India's economy opened up. Auto Expo, Acetech (architecture and construction), ChemTech (chemicals), IIJS (jewelry)—every industry wanted to showcase products and connect with customers. BEC became the default venue not because it was the only option, but because it offered something unique: a private, professionally managed space with flexibility government-run venues couldn't match.

By the late 1990s, NESCO's transformation was becoming apparent. Revenue from real estate was beginning to match and would soon exceed the engineering business. But this wasn't a conglomerate randomly acquiring unrelated businesses. The real estate wasn't just generating rental income—it was creating a platform for further expansion. The engineering business wasn't abandoned—it continued generating steady cash flows that funded real estate development without requiring debt.

The year 2001 marked a symbolic transition. The company formally changed its name from New Standard Engineering Company Limited to NESCO Limited. This wasn't just rebranding—it was acknowledgment of a fundamental transformation. The engineering company founded in 1939 had evolved into something entirely different yet somehow entirely logical—a creator and operator of business infrastructure for modern India.

But the real transformation was yet to come. As the new millennium dawned, India was about to experience its IT boom. Y2K had put Indian technology services on the global map. Companies like Infosys, TCS, and Wipro were growing exponentially. And they all needed one thing: modern office space for thousands of engineers. NESCO, with its land bank in Goregaon and experience in commercial real estate, was perfectly positioned to capitalize. The next phase wouldn't just be about building offices—it would be about creating an IT ecosystem that would define Goregaon's transformation from suburban outpost to business hub.

V. Creating the IT Park Empire (2000s–2015)

The story of NESCO IT Park begins with a parking lot. In 2003, as NESCO's management surveyed their Goregaon complex, they saw vast stretches of open parking spaces that remained empty except during major exhibitions. Meanwhile, a few kilometers away in Mindspace, Malad, they watched as IT companies scrambled for office space, willing to pay premium rents for modern facilities. The opportunity was obvious, but the execution would require something special—not just building offices, but creating an ecosystem that IT companies and their employees would actually want.

The first challenge was understanding what made IT real estate different. Traditional offices measured success by cost per square foot. IT companies cared about different metrics: power backup capacity (100% backup wasn't negotiable), internet redundancy, floor plate efficiency (those vast open floors for hundreds of programmers), and surprisingly, lifestyle amenities. These weren't your father's government clerks who'd tolerate any conditions—these were young engineers being wooed by global companies, people who had options.

NESCO's approach was methodical. Instead of rushing to build maximum square footage, they started with infrastructure. Dedicated electrical substations with N+1 redundancy. Multiple internet service provider connections with automatic failover. Central air conditioning that could handle Mumbai's humidity and the heat generated by thousands of computers. Sewage treatment plants and rainwater harvesting—not because regulations required them (yet), but because they understood sustainability would eventually become a differentiator.

The design philosophy was borrowed from Silicon Valley but adapted for Mumbai. Wide corridors that could handle rush-hour foot traffic when thousands of employees arrived or left simultaneously. Food courts designed like university campuses rather than office cafeterias. Abundant parking—a rarity in Mumbai—with separate sections for cars and two-wheelers (because many young engineers still rode motorcycles). Every decision reflected deep observation of how IT companies actually operated versus how traditional offices assumed they should.

Tower 3 came first, spanning 62,315 square meters with 24 floors. But the real innovation was in the details. Floor plates were designed to be subdividable—a startup could take 5,000 square feet, then expand to 15,000 without relocating. Pre-installed cable trays meant companies could set up IT infrastructure in weeks, not months. The building management system was computerized when most Mumbai buildings still relied on manual logs. These weren't revolutionary innovations individually, but together they created something Mumbai's IT sector desperately needed—plug-and-play office space.

The tenant acquisition strategy was surgical. Instead of casting a wide net, NESCO targeted specific anchor tenants who would establish credibility. When HSBC's global in-house center signed up, it sent a signal—if one of the world's most conservative banks trusted NESCO IT Park for critical operations, others could too. KPMG followed, then PwC. Each blue-chip tenant made the next acquisition easier. By the time BlackRock and MSCI signed leases, NESCO IT Park wasn't just an option—it was the destination for serious financial services and IT operations.

Tower 4, completed later, took the learning from Tower 3 and amplified it. At 104,515 square meters, it was massive, but the real innovation was the floor plates—at 88,500 square feet each, they were among the largest in Mumbai. Why did this matter? Large IT companies wanted entire floors for security and operational efficiency. A single floor at Tower 4 could accommodate 800-1,000 employees—an entire division under one roof. No other building in the western suburbs offered this.

But buildings alone don't create ecosystems. NESCO understood they were really in the productivity business. Every amenity was designed to keep employees on campus and productive. Fine dining restaurants for client meetings (because not every discussion happens in conference rooms). Food courts with enough variety that employees wouldn't get bored eating there daily. Convenience stores for last-minute necessities. Even crèches—because many IT employees were young parents who valued on-site childcare over slightly higher salaries.

The LEED Platinum certification achieved by the complex wasn't just about environmental brownie points. It translated into lower operating costs—30% reduction in energy consumption, 40% reduction in water usage. For IT companies signing 5-10 year leases, these savings compounded into millions. More importantly, it allowed them to meet their own global sustainability commitments. When Microsoft or Goldman Sachs audited their vendors' environmental practices, NESCO IT Park passed with flying colors.

By 2010, something remarkable was happening. NESCO IT Park wasn't just achieving high occupancy—it was maintaining 98%+ occupancy while commanding premium rents. The wait list for space was growing. Companies were signing leases for floors that hadn't been built yet. The complex was housing over 25,000 employees daily—equivalent to a small town—all functioning smoothly within a few acres in Goregaon.

The network effects were powerful. When MSCI employees wanted to switch jobs, they often looked first at other companies within NESCO IT Park—no commute change required. When companies needed to collaborate with vendors or partners, physical proximity in the same complex made coordination easier. When international clients visited, the professional environment and amenities impressed them—crucial for Indian IT companies trying to move up the value chain from cost arbitrage to strategic partnerships.

The financial performance validated the strategy. IT Park revenues grew 49% between FY20 and FY24, even through a pandemic that supposedly killed office demand. While competitors struggled with vacancy rates as companies embraced remote work, NESCO maintained near-full occupancy. Why? Because their tenants weren't just renting space—they were buying into an ecosystem that enabled their business models.

By 2015, NESCO IT Park had achieved something remarkable—it had transformed Goregaon from a suburb known for film studios into a legitimate business district. Property values in the surrounding area had multiplied. The Western Express Highway metro station, when it finally opened, was strategically located to serve the complex. The company that had bet on Goregaon in 1986 when it was nowhere had helped turn it into somewhere.

But NESCO wasn't done evolving. With IT Park established and generating steady cash flows, with the exhibition business humming, the company began looking for the next growth opportunity. The answer would come from an unexpected source—not another industrial pivot, but from going deeper into the ecosystem they'd already created. If you have 25,000 people coming to your complex daily, plus thousands more for exhibitions, what else do they need? The answer would lead to NESCO's next phase of diversification.

VI. The Exhibition Business & BEC Dominance

Every January, something remarkable happens at the Bombay Exhibition Centre. Over 800 jewelry manufacturers from across India converge for the India International Jewellery Show (IIJS). Buyers fly in from Dubai, Singapore, New York. Millions of dollars in loose diamonds and gold jewelry change hands. Security rivals that of international airports. For one week, a corner of Goregaon becomes the global center of the jewelry trade. This scene repeats throughout the year—automobiles, chemicals, architecture, textiles—each industry taking its turn. BEC isn't just hosting exhibitions; it's facilitating entire industries.

To understand BEC's dominance, you need to understand what an exhibition actually is. It's not just a large hall where companies set up booths. It's a carefully orchestrated collision of supply and demand, a physical manifestation of market forces that even in our digital age cannot be fully replicated online. When a textile manufacturer from Surat meets a buyer from Walmart at BEC, they're not just exchanging business cards—they're touching fabrics, negotiating prices, building relationships that will generate millions in trade.

NESCO understood this from the beginning. When they established BEC in 1992, they didn't just build exhibition halls—they built infrastructure for deal-making. The 60,000 square meters of exhibition space is just the visible part. Behind the scenes: dedicated loading bays that can handle everything from automobiles to industrial machinery, customizable power supplies for different exhibition needs, modular spaces that can be configured differently for each event, storage facilities for exhibitors who participate in multiple shows annually.

The competitive advantage wasn't just physical infrastructure—it was operational expertise accumulated over decades. Consider the complexity of hosting Auto Expo: cars need to be driven in and positioned precisely, electrical connections for elaborate displays, safety protocols for thousands of visitors walking around expensive vehicles. Now contrast that with ACETECH: heavy marble slabs and construction equipment requiring reinforced flooring, dust management for stone cutting demonstrations, specialized ventilation for chemical displays. Each exhibition is essentially a different business, and BEC had mastered them all.

The network effects in the exhibition business are even stronger than in real estate. Exhibitors go where buyers go. Buyers go where exhibitors go. Once an exhibition establishes itself at a venue, moving it risks breaking this delicate equilibrium. IIJS didn't stay at BEC for 30 years because of inertia—it stayed because every participant knew that's where everyone else would be. This predictability is valuable. International buyers can plan annual trips knowing exactly where and when to find Indian suppliers.

The economics of exhibitions are fascinating and often misunderstood. Revenue comes not just from renting space but from multiple streams: booth construction, electrical connections, parking, food concessions, advertising opportunities. A large exhibition might generate ₹50-100 crore in economic activity over a week, with NESCO capturing value at multiple points. More importantly, exhibitions are largely recession-proof—companies might cut advertising budgets during downturns, but they can't afford to miss the one annual event where their entire industry gathers.

BEC's calendar management is a strategic art form. Each exhibition needs setup and teardown time, meaning the venue can't be utilized 365 days a year. But NESCO optimized this constraint beautifully. They scheduled complementary exhibitions back-to-back—ACETECH (construction) followed by a real estate expo, leveraging visitor overlap. They reserved certain periods for private events—corporate gatherings, weddings, concerts—which offered higher margins and different revenue characteristics. The result: a utilization rate that maximizes revenue while maintaining the venue's premium positioning.

The symbiosis with NESCO IT Park is subtle but powerful. Many IT Park tenants are involved in industries that exhibit at BEC—BFSI companies attending fintech exhibitions, consulting firms participating in industry conferences, technology companies showcasing at IT expos. The physical proximity means executives can attend important sessions without losing entire days to travel. Some companies specifically chose NESCO IT Park offices to be close to BEC's exhibition ecosystem.

The private ownership of BEC provides advantages government-run venues can't match. Decision-making is quick—if an organizer needs a configuration change, it happens. Pricing is flexible—NESCO can offer volume discounts to organizers who book multiple exhibitions. Investment is continuous—regular upgrades keep facilities modern. Customer service is paramount—organizers have dedicated relationship managers who understand their specific needs. These soft factors matter enormously in an industry built on relationships and trust.

By 2015, BEC had achieved something remarkable: it had become infrastructure as essential to certain industries as ports or highways. The jewelry industry couldn't imagine IIJS anywhere else. The construction industry had built its annual calendar around ACETECH at BEC. The automobile industry's marketing plans assumed Auto Expo at this venue. NESCO had created switching costs so high that even if competitors built superior facilities, exhibitions wouldn't move.

The COVID-19 pandemic tested this model severely. Exhibitions were among the last businesses to reopen. Virtual exhibitions were attempted but proved poor substitutes—you can't assess diamond quality on Zoom or test-drive a car virtually. When exhibitions resumed, pent-up demand was explosive. BEC's 2021-2022 calendar was booked solid as industries rushed to reconnect physically. The pandemic had proven something counterintuitive: in an increasingly digital world, the value of physical gathering spaces had actually increased.

The exhibition business also provided NESCO with valuable optionality. Every exhibition brought thousands of industry participants to Goregaon. Many discovered NESCO IT Park and became tenants. Some decided they needed permanent presence near this industry hub. The exhibition business wasn't just generating direct revenue—it was a customer acquisition engine for the real estate business, a marketing platform that brought potential tenants directly to NESCO's doorstep.

As NESCO entered the mid-2010s, the exhibition business was generating steady cash flows with minimal capital requirements—the infrastructure was already built. This cash generation, combined with IT Park revenues, gave NESCO the financial flexibility to explore new opportunities. The question was: where next? The answer would come from looking not outward for new industries to enter, but inward at the ecosystem they'd already created. With 25,000+ daily office workers and thousands of exhibition visitors, what services could NESCO provide that others couldn't or wouldn't?

VII. Diversification 2.0: Foods, Events & Beyond (2015–Present)

The insight came from a complaint. In 2014, a senior executive from one of NESCO IT Park's anchor tenants mentioned casually that their biggest employee satisfaction issue wasn't salary or work-life balance—it was food. The food courts were decent but repetitive. Outside options required leaving the complex. Catering for corporate events was inconsistent. NESCO's management realized they had 25,000 people eating 2-3 meals daily within their complex, plus thousands more during exhibitions. They were sitting on a food services opportunity hiding in plain sight.

But NESCO Foods, launched in 2015, wasn't conceived as just another corporate cafeteria operator. The vision was grander: become Mumbai's largest non-flight kitchen, leveraging the captive demand to build scale, then use that scale to serve external clients. The strategy was classic NESCO—start with guaranteed internal demand, build operational excellence, then expand outward.

The numbers were compelling. Those 25,000 IT Park employees represented 50,000-75,000 meals daily. Exhibition days could add another 10,000-20,000 meals. Corporate events needed specialized catering. The guaranteed base load meant NESCO could invest in industrial-grade infrastructure that standalone catering companies couldn't justify—automated cooking equipment, blast chillers, sophisticated inventory management systems. This infrastructure, once built, had massive operating leverage.

The execution was meticulous. Different cuisines for different days to prevent monotony. Price points calibrated to IT salaries—affordable enough for daily consumption but quality that justified slight premiums. Separate facilities for vegetarian and non-vegetarian food, crucial in India's dietary landscape. Health-conscious options as wellness became a corporate priority. The goal wasn't just feeding people—it was becoming integral to the daily experience of working at NESCO IT Park.

Within three years, NESCO Foods was serving 50,000 meals daily, making it one of Mumbai's largest food production facilities outside the airport. But the real innovation was in diversification within food services. Corporate catering for IT Park tenants' events. Exhibition catering with customized menus for different industries (light snacks for jewelry shows where security is paramount, hearty meals for construction exhibitions with physical laborers). Even home delivery for employees working late, leveraging the kitchen infrastructure during off-peak hours.

The synergies were powerful. Food quality became a selling point for new IT Park tenants—companies could promise employees varied, quality meals without managing vendors. Exhibition organizers could guarantee participants consistent food experiences. The food business wasn't just generating revenue; it was enhancing the value proposition of the core real estate and exhibition businesses.

Parallel to foods, NESCO Events emerged from another observation. The BEC infrastructure sat partially idle between major exhibitions. Corporate India was spending billions on events—product launches, dealer meets, annual gatherings—often struggling to find appropriate venues. NESCO had the infrastructure, the operational expertise, and crucially, the ability to provide integrated services—venue, food, logistics—under one roof.

The events business started with corporate gatherings but quickly expanded. Cultural events during festivals. Concerts leveraging Goregaon's entertainment industry connections. Even weddings—the ultimate high-margin event business. Each event type taught NESCO something new about customer needs, operational challenges, and revenue optimization. The learnings from managing 5,000-person exhibitions scaled down nicely to 500-person corporate events.

The intellectual property development was particularly clever. Instead of just renting space, NESCO began creating and owning events. Trade shows in emerging sectors without established exhibitions. Cultural festivals that became annual fixtures. By owning the IP, NESCO captured value not just as venue provider but as organizer—a much more lucrative position in the value chain.

The pandemic accelerated certain innovations. Hybrid events combining physical and virtual attendance. Biosecure protocols that became selling points. Flexible cancellation policies that reduced customer risk. While competitors retreated, NESCO invested, betting correctly that physical events would return with vengeance. When they did, NESCO had enhanced capabilities and weakened competition.

Looking forward, NESCO's latest diversification might be its boldest yet—entering the residential real estate market. The logic is compelling: they own prime land in Goregaon, understand real estate development, and have watched property values around their complex soar. But residential is different from commercial—customers are individuals not corporations, decision-making is emotional not rational, and execution risks are different.

The residential strategy appears characteristically thoughtful. Target middle and premium segments—not luxury where competition is fierce, not affordable where margins are thin. Leverage the NESCO brand which now carries premium connotations in Mumbai. Focus on locations near the existing complex where infrastructure and amenities are already established. Most importantly, maintain the capital discipline—no aggressive leverage, no speculative land banking.

The beauty of NESCO's diversification is its coherence. Foods serves real estate tenants and exhibition visitors. Events leverage exhibition infrastructure and relationships. Residential capitalizes on the neighborhood transformation NESCO itself created. Each business reinforces others. A company attending an exhibition might become an IT Park tenant, use NESCO Foods for catering, host events at BEC, and its executives might buy NESCO residential properties. It's an ecosystem play executed with unusual patience and discipline.

This integrated approach has created multiple competitive advantages. Customer acquisition costs are lower when businesses share customers. Operational expertise transfers across businesses. Capital allocation is optimized—cash from mature businesses funds new ventures without external capital. Risk is diversified but manageable—if exhibitions slow, IT rentals continue; if IT demand softens, foods and events provide cushion.

As NESCO enters its ninth decade, the company J.V. Patel founded to build industrial equipment has evolved into something uniquely positioned for India's service economy. It's not just a real estate company with some side businesses, nor a random conglomerate of unrelated ventures. It's an infrastructure platform for modern business—providing the spaces, services, and ecosystems that enable India's economic transformation. The question now isn't whether NESCO can continue growing, but how it will deploy its substantial cash flows and prime real estate assets in an India that's changing faster than ever.

VIII. Financial Performance & Capital Allocation

The spreadsheet reads like poetry to value investors. ₹9,664 crore market capitalization. ₹784 crore in revenue. ₹402 crore in profit. 68.5% promoter holding. And the number that makes CFOs of capital-intensive businesses weep with envy: zero debt.

In an industry where leverage is considered essential—real estate developers routinely run debt-to-equity ratios above 2x—NESCO operates completely debt-free. This isn't financial conservatism; it's strategic genius. When your competitors are paying 10-12% interest on massive debt loads, every rupee of your operating profit flows straight to the bottom line. When credit markets freeze, as they did in 2008 and 2020, you're buying distressed assets while others are selling to survive.

Let's break down the revenue architecture. IT Parks Division contributed 41% of revenue in FY24, down from 45% in FY20—not because IT Parks are shrinking but because other segments are growing faster. The IT Park segment revenue grew by 49% between FY20 and FY24, even through a pandemic that supposedly killed office demand. That's not growth; that's validation of irreplaceability.

The margin profile is even more impressive. Operating profit margins stood at 62.4% in FY24, while net profit margins reached 53.5%. Think about what this means: for every ₹100 of revenue, ₹53.50 flows to net profit. These aren't software company margins achieved through intellectual property; these are margins from physical real estate and exhibitions. How? Because when you own the land outright, have no interest payments, and operate at 98%+ occupancy, your only real costs are maintenance and staff.

Return on Equity improved to 15.8% in FY24 from 14.8% in FY23. Return on Capital Employed reached 20.8%. Return on Assets stood at 14.2%. These returns might seem modest compared to asset-light businesses, but for a capital-intensive real estate company, they're exceptional. More importantly, they're achieved without leverage. A leveraged competitor might show higher ROE, but that's financial engineering. NESCO's returns are operational excellence.

The cash flow statement tells the real story. Cash flow from operating activities during FY24 stood at ₹4 billion, an improvement of 26.6% year-on-year. This isn't accounting profit that might reverse; this is actual cash that can be deployed. The company generates so much cash that its biggest challenge is finding productive uses for it—a problem most Indian real estate companies would love to have.

The capital allocation framework is disciplined to the point of being boring—which is exactly what you want. No expensive acquisitions justified by "synergies." No ventures into unrelated businesses because management got bored. No financial engineering to juice returns. Just patient, methodical investment in businesses they understand, in locations they control, serving customers they've served for decades.

Operating income rose 24.2% year-on-year in FY24. Operating profit increased by 21.8%. Net profit grew by 24.8%. This is a company firing on all cylinders—every division contributing, margins expanding despite inflation, cash generation accelerating.

The dividend policy reflects confidence without aggression. Recent 325% dividend announcement signals two things: the business is generating more cash than it can immediately deploy, and management is shareholder-friendly enough to return excess capital rather than empire-build. Yet they retain enough to fund growth without ever needing external capital.

What makes NESCO particularly interesting from a financial perspective is the optionality embedded in the balance sheet. Fixed assets rose 26% to ₹22 billion in FY24. These aren't depreciated book values; these are prime Mumbai real estate assets carried at historical cost. The market value of their Goregaon land alone could be multiples of book value. They're sitting on one of Mumbai's most valuable land banks, and it's barely reflected in the financials.

The revenue growth trajectory—13.5% CAGR over the past 5 years—might seem pedestrian compared to new-age companies. But this is real, profitable growth. No customer acquisition costs bleeding the bottom line. No "growth at any cost" mentality. Just steady, compound growth that translates directly to shareholder value.

The pandemic stress test was revealing. While leveraged real estate companies negotiated with lenders and offered massive rent concessions, NESCO maintained near-full occupancy and continued generating cash. 100% occupancy in Towers 3 and 4 isn't just a post-pandemic recovery story; it's validation that their tenants literally cannot afford to leave.

The segmental performance shows intelligent portfolio management. IT Parks remains the crown jewel, but the exhibition business provides stability, foods generates daily cash, and events offer high-margin opportunities. Each segment hedges the others—if IT companies reduce office space, exhibitions continue; if exhibitions slow, food services to existing tenants continue; if everything slows, you're debt-free and can wait.

Looking at peer comparison, NESCO trades at premiums to most real estate companies—justifiably so. This isn't a developer dependent on the next project launch. It's an annuity business disguised as a real estate company. The revenue visibility, margin stability, and balance sheet strength justify valuation premiums that would seem absurd for typical developers.

The capital intensity that would terrify most investors—₹22 billion in fixed assets—is actually the moat. Try replicating NESCO's position today. You'd need to acquire prime Mumbai land (good luck), build IT parks (5-7 year process), achieve 98% occupancy (without the reputation), create exhibition infrastructure (enormous upfront investment), and do it all without debt (impossible for most). The replacement cost of NESCO's assets would be multiples of its market cap.

Pre-tax margins of 67% deserve emphasis. In a country where corporate tax rates are around 30%, maintaining such high pre-tax margins means the effective tax rate becomes almost irrelevant to returns. Every operational efficiency flows directly to shareholders.

The working capital management is another hidden strength. Real estate companies typically have massive working capital needs—construction costs, land payments, development expenses. NESCO's model—built assets generating rental income—means negative working capital cycles. Tenants pay rent in advance; exhibitions pay before events; food services generate daily cash. The business funds itself.

This financial profile—debt-free, cash-generative, high-margin, stable-growth—is why NESCO trades more like a bond than a stock. In a world of zero interest rates and volatile markets, a company generating 15%+ returns on equity with minimal risk becomes incredibly valuable. It's not exciting, but it's exactly the kind of boring that compounds wealth over decades.

IX. Playbook: Business & Investing Lessons

The NESCO story offers a masterclass in strategic patience that contradicts everything modern business schools teach about growth and capital allocation. While contemporaries leveraged up to chase growth, pivoted to trending sectors, or pursued aggressive M&A, NESCO did something radical: they waited. They built slowly. They stayed disciplined. And they created more value than almost any of their more "dynamic" peers.

The Power of Patient Capital and Multi-Generational Thinking

Three generations of the Patel family have run NESCO, and this continuity shows in every strategic decision. When they bought land in Goregaon in the 1960s, they weren't thinking about quarterly earnings; they were thinking about where Mumbai would grow over decades. When they invested in shot-blasting technology, they weren't chasing quick returns; they were building capabilities that would compound over time. This isn't just long-term thinking—it's generational thinking, where success is measured not in years but in decades.

The patience extends to capital deployment. NESCO could have leveraged their Goregaon land ten times over, built massive developments, and shown spectacular near-term growth. Instead, they developed gradually, ensuring each phase was cash-flow positive before moving to the next. This patience meant slower initial growth but created an anti-fragile business model that actually strengthened during downturns while leveraged competitors collapsed.

Location, Location, Location: Being Early to Goregaon

NESCO's Goregaon bet teaches a profound lesson about contrarian location selection. In 1986, choosing Goregaon over established business districts seemed foolish. But NESCO understood something crucial: established districts are established precisely because they can't grow much further. The value creation happens in transitions—when an area transforms from nowhere to somewhere.

But being early isn't enough; you need staying power. Goregaon didn't transform overnight. For years, NESCO operated in what seemed like a remote location, accepting lower rents and struggling to attract tenants. Lesser companies would have sold out when land prices first appreciated. NESCO held on, continued investing, and essentially created the transformation they had bet on. They didn't just benefit from Goregaon's rise; they caused it.

Diversification Done Right: Related Businesses with Synergies

Business schools teach that diversification reduces risk. Markets teach that conglomerates trade at discounts. NESCO squares this circle through what might be called "coherent diversification"—every business reinforces the others without requiring entirely different capabilities.

The IT Park creates demand for food services. Exhibitions bring potential IT Park tenants. Events utilize exhibition infrastructure during off-peak times. Each business makes the others more valuable. This isn't the random diversification of a typical Indian conglomerate; it's ecosystem construction where the whole genuinely exceeds the sum of parts.

More importantly, NESCO diversified into businesses they could understand and control. They didn't venture into financial services because it was profitable or technology because it was trendy. They stuck to physical infrastructure and services—businesses where their operational expertise created genuine competitive advantages.

The Moat of Integrated Ecosystems vs Standalone Assets

Most real estate companies think in terms of projects—build, sell, move on. NESCO thinks in terms of ecosystems—create gravitational pull that becomes self-reinforcing. A standalone office building is a commodity; an IT Park with food services, exhibition centers, and event spaces is an ecosystem.

This ecosystem approach creates switching costs that pure financial analysis misses. A company in NESCO IT Park isn't just renting office space; they're buying into an infrastructure that enables their business. Their employees know the commute, like the food options, have routines established. Leaving means disrupting all of this—a hidden cost that keeps occupancy at 98%+ even when competitors offer lower rents.

Why Being Debt-Free Matters in Cyclical Businesses

Real estate is cyclical. Exhibitions are cyclical. Even IT services face cycles. Operating in cyclical businesses without debt is like wearing a seatbelt—it seems unnecessary until it's critical. NESCO's debt-free status isn't just about avoiding interest payments; it's about optionality.

In 2008, when credit markets froze, NESCO could have bought distressed assets but chose not to—discipline again. In 2020, when COVID shut everything down, NESCO didn't negotiate with lenders or fire-sale assets; they simply waited. This financial flexibility means they can play offense during downturns while competitors play defense—the source of extraordinary long-term returns.

The debt-free approach also enables true long-term thinking. Leveraged companies must optimize for cash flow to service debt. NESCO can optimize for value creation, even if it means accepting lower near-term returns. They can keep rents reasonable to maintain 98% occupancy rather than pushing for maximum rates that might trigger tenant departures.

Managing Complexity While Maintaining Focus

NESCO operates in four distinct businesses, each with different dynamics, customer bases, and operational requirements. Managing this complexity while maintaining the operational excellence that defines the company requires unusual organizational capability.

The secret seems to be treating each business as distinct while leveraging shared resources intelligently. IT Parks has dedicated management focused on tenant relations. Exhibitions has specialists who understand event logistics. Foods has culinary and service expertise. But all share common infrastructure, maintenance teams, and strategic oversight. It's federated autonomy—independent operations within a unified strategy.

This structure avoids both the inefficiencies of complete separation and the confusion of complete integration. Each business maintains its identity and excellence while benefiting from the parent's resources and reputation. It's complexity managed through clarity rather than control.

The Hidden Value of Operational Excellence

In glamorous businesses, strategy matters more than operations. In commodity businesses like real estate, operational excellence is strategy. NESCO's 98% occupancy isn't achieved through financial engineering or marketing brilliance; it's achieved through thousands of small operational decisions executed well daily.

The elevator that's never broken. The parking spot that's always available. The food court that maintains quality despite serving 50,000 meals daily. The exhibition setup that happens flawlessly despite complexity. These operational details seem trivial individually but compound into competitive advantage that's nearly impossible to replicate.

Understanding Your Cost of Capital Advantage

Most companies think about cost of capital in terms of interest rates or equity returns. NESCO understands something deeper: when you're funded entirely by patient family capital and retained earnings, your cost of capital isn't just lower—it's different in kind.

They can invest in projects with 10-year paybacks that public market investors would never tolerate. They can maintain assets that aren't currently profitable but might become valuable. They can say no to opportunities that would boost near-term earnings but compromise long-term value. This patient capital structure is as much a competitive advantage as their physical assets.

The Compound Effect of Reputation

NESCO's reputation took decades to build but now generates returns that don't appear on financial statements. When a multinational needs office space in Mumbai, NESCO is on the shortlist not through marketing but through reputation. When an exhibition organizer plans a new event, BEC is the default choice through reputation. When companies need reliable catering for important events, NESCO Foods gets the call through reputation.

This reputation compounds like interest. Every successful tenant becomes a reference. Every well-run exhibition attracts the next organizer. Every satisfied customer reduces the cost of acquiring the next one. After 85 years, NESCO's reputation is worth billions but carried on the books at zero.

The Ultimate Lesson: Boring Businesses, Extraordinary Returns

NESCO proves that you don't need to be in exciting businesses to generate exciting returns. Shot-blasting equipment is boring. Office rentals are boring. Exhibition centers are boring. Food services are boring. But boring businesses done exceptionally well over long periods create extraordinary value.

The paradox is that boring businesses often have better economics than exciting ones. Less competition (who dreams of running exhibition centers?). More stable cash flows (companies always need offices). Higher barriers to entry (try building an exhibition center). Lower disruption risk (virtual exhibitions failed; physical ones thrived).

For investors, the NESCO playbook suggests looking for boring businesses with great execution, patient capital, and long runways. For operators, it suggests that sustainable competitive advantage comes not from being in the right business but from being right in your business—whatever that business might be.

X. Analysis & Bear vs. Bull Case

The investment case for NESCO creates fascinating tension. Bulls see a Mumbai real estate crown jewel trading at a fraction of replacement cost. Bears see a low-float, family-controlled company vulnerable to technological disruption. Both are right, which makes NESCO one of the more interesting risk-reward equations in Indian markets.

Bull Case: The Irreplaceable Asset Thesis

The bull case starts with a simple question: what would it cost to replicate NESCO today? You'd need to acquire prime land in Goregaon (probably impossible at any price), build IT parks and exhibition centers (₹2,000+ crore), achieve 98% occupancy (minimum 5-10 years), and create the ecosystem effects (decades). The replacement cost would likely exceed ₹15,000-20,000 crore—double the current market cap.

The 98%+ occupancy rate isn't just a number; it's validation of irreplaceability. In a world where remote work supposedly killed office demand, NESCO maintained full occupancy through the pandemic. Why? Because their tenants—BlackRock, HSBC, KPMG—need more than just office space. They need the ecosystem, the location, the infrastructure that enables their business models.

The debt-free balance sheet provides enormous optionality in a rising rate environment. While competitors struggle with refinancing, NESCO can invest counter-cyclically. They could literally buy distressed assets for cash while others are selling to survive. This financial flexibility is worth billions in optionality value that traditional metrics don't capture.

Mumbai's geographic constraints create natural supply limits that benefit NESCO enormously. The city can only expand northward, and NESCO owns prime land along the expansion corridor. Every infrastructure improvement—metro extensions, highway expansions, airport connections—increases the value of their Goregaon holdings. They're essentially long Mumbai's economic growth with leverage to infrastructure development.

The business mix provides multiple growth engines beyond just IT parks. The exhibition business should grow with India's economy—more industries, more trade, more exhibitions. Food services can expand beyond the current complex. Events represent high-margin opportunities. Residential development could unlock massive land value. The current valuation arguably reflects only the IT Park business, making everything else free optionality.

The promoter holding of 68.5% might seem like a governance negative, but it ensures aligned interests. The Patel family's wealth is tied to NESCO's long-term value, not quarterly earnings. They can make decisions that might hurt near-term stock price but create long-term value—a luxury most publicly traded companies don't have.

Bear Case: The Disruption and Concentration Risk Thesis

The bear case begins with concentration risk that bulls conveniently ignore. NESCO is essentially a bet on one location—Goregaon—in one city—Mumbai. Any shock to Mumbai's economy or Goregaon's attractiveness devastates the investment thesis. A major earthquake, flooding from climate change, or even significant infrastructure failure could impair value permanently.

The work-from-home revolution might be paused, not reversed. Yes, companies maintained leases through COVID, but that might reflect lease terms rather than preference. As leases expire over the next 5-10 years, companies might reduce office footprints dramatically. NESCO's 98% occupancy could be yesterday's equilibrium, not tomorrow's.

Technology disruption threatens multiple business lines simultaneously. Virtual exhibitions gained traction during COVID and might permanently capture share. AI and automation reduce the number of employees needing office space. Food delivery apps make captive food services less valuable. NESCO's physical infrastructure advantages could become liabilities in an increasingly digital world.

The limited float creates serious liquidity concerns for institutional investors. With promoters holding 68.5%, the free float is thin. Any significant selling pressure could cause disproportionate price declines. More concerningly, the thin float might prevent institutional ownership, keeping valuations permanently depressed regardless of fundamental performance.

Execution risk in new ventures shouldn't be dismissed. Residential real estate is fundamentally different from commercial—emotional purchases versus rational, individual buyers versus institutional, high marketing costs versus relationship sales. NESCO's operational excellence in commercial might not translate. Failed diversification could destroy value and management credibility.

The valuation already embeds significant growth expectations. Trading at premium multiples to other real estate companies assumes continued exceptional execution. Any disappointment—occupancy dropping to 95%, exhibition growth slowing, food services struggling—could trigger multiple compression that overwhelms operational performance.

Regulatory risks lurk beneath the surface. Changes in FSI regulations could allow competitors to build competing supply. Property tax disputes—NESCO already faces some—could escalate. Environmental regulations might require expensive retrofitting. Labor law changes could impact the large service workforce. Each regulatory change is a potential hit to margins or growth.

The Nuanced Reality

The truth, as always, lies between extremes. NESCO is neither as bulletproof as bulls suggest nor as vulnerable as bears fear. It's a high-quality business with genuine competitive advantages, trading at valuations that reflect those advantages. The investment case depends largely on time horizon and risk tolerance.

For long-term investors, NESCO offers exposure to Mumbai's continued economic growth with downside protection from the debt-free balance sheet and diversified revenue streams. The replacement cost argument provides valuation support, while operational excellence suggests continued market share gains. Patient capital might be rewarded as land values appreciate and new businesses mature.

For shorter-term investors, the risks are more pronounced. Limited float means volatility. Technology disruption could impact sentiment before affecting fundamentals. Any occupancy decline or exhibition weakness might trigger selling regardless of long-term prospects. The stock could remain "dead money" for extended periods despite strong operational performance.

The key variables to monitor aren't the obvious ones. Everyone watches occupancy rates and rental prices. The critical factors are subtler: tenant renewal rates (not just occupancy), exhibition organizer satisfaction (not just event count), food service margins (indicating pricing power), and especially capital allocation decisions (disciplined or empire building?).

Climate change represents an underappreciated long-term risk. Mumbai's coastal location and monsoon exposure create physical risks that insurance might not fully cover. More subtly, if climate concerns drive businesses from Mumbai to inland cities, NESCO's location advantage inverts to disadvantage. This isn't next year's risk, but it might be next decade's.

The family control that provides patient capital also creates succession risk. Three generations of successful management doesn't guarantee a fourth. Family disputes, succession struggles, or simply regression to the mean in management quality could erode the operational excellence that justifies premium valuations.

XI. Recent News

The recent developments at NESCO read like a carefully orchestrated expansion without drama—exactly what you'd expect from this management team.

In August 2024, NESCO reported 8% revenue growth to Rs.845 Cr, declared a 325% dividend, and maintained 100% occupancy in Towers 3 and 4. The occupancy metric is particularly significant—while global companies debate return-to-office policies, NESCO's tenants have voted with their leases.

The most intriguing development is NESCO's winning bid for highway amenities. The National Highways Logistics Management declared NESCO as the highest bidder for developing, operating, and maintaining wayside amenities on the Raipur-Visakhapatnam Expressway for a 30-year period. The project involves 4 sites with an estimated development cost of Rs. 50 crore each, expected to generate annualized revenue of Rs. 300 crore from year 4 of operations, with annual lease rent of Rs. 3.34 crores.

This highway project represents classic NESCO thinking—long-term infrastructure play with annuity-like returns. Highway amenities might seem far from IT parks and exhibitions, but the operational DNA is identical: manage physical infrastructure, provide services, generate steady cash flows.

In February 2025, NESCO incorporated a wholly-owned subsidiary named Nesco Retail, suggesting potential expansion into retail operations—likely leveraging their existing foot traffic and locations.

The quarterly performance shows remarkable consistency. Q4 FY25 saw net profit decline 15.71% to Rs 88.61 crore year-on-year, though sales rose 1.61% to Rs 192.01 crore. For the full year, net profit rose 3.43% to Rs 375.21 crore while sales increased 7.94% to Rs 732.01 crore. The profit decline likely reflects investments in new ventures rather than operational weakness.

Q3 FY25 showed stronger momentum with net profit rising 17.27% to Rs 109.94 crore and sales jumping 16.19% to Rs 206.54 crore year-on-year, demonstrating the underlying business strength.

The company launched a 100-day 'Saksham Niveshak' campaign for unclaimed dividend claims and KYC updates, reflecting attention to shareholder services and regulatory compliance.

A minor hiccup appeared with BMC (Brihanmumbai Municipal Corporation) issuing a notice for Rs.2.59 crore penalty on property tax, which NESCO has denied and is seeking clarifications—typical of the regulatory frictions that come with substantial real estate holdings in Mumbai.

Stock performance has been robust. Over the last month, NESCO shares moved up 13.19%, over three months up 49.40%, over 12 months up 50.02%, and over three years up 136.40%. This performance significantly outpaced broader market indices, reflecting growing investor appreciation for the NESCO model.

NESCO's Q4 FY25 net profit fell 15.71% year-on-year to ₹88.61Cr, with a 19.4% quarter-on-quarter decline, though this appears to be timing-related rather than structural given the full-year growth.

The corporate governance updates show continued professionalization. The 66th Annual General Meeting was held on July 30, 2025, with proper voting results and scrutinizer's reports published, maintaining transparency standards expected of listed companies.

What's absent from recent news is equally telling—no debt issuances, no emergency fundraising, no asset sales, no management turmoil. In an Indian real estate sector often characterized by financial engineering and corporate drama, NESCO's news flow is refreshingly operational.

XII. Links & Resources

For deeper exploration of NESCO's business model and Indian real estate dynamics, consider these resources:

Company Resources: - NESCO Official Website - Annual reports, investor presentations, and official announcements - NESCO Financials Section - Detailed quarterly and annual financial statements - BSE Company Page - Exchange filings and corporate announcements - NSE Company Page - Real-time quotes and historical data

Industry Analysis: - "The Evolution of Mumbai's Commercial Real Estate" - JLL India Research Reports - "India's Exhibition Industry: Growth Drivers and Challenges" - India Exposition Mart Studies - "From Manufacturing to Services: India's Economic Transformation" - Economic & Political Weekly Archives - "Family-Owned Businesses in India: Governance and Performance" - IIM Bangalore Working Papers

Mumbai Real Estate Context: - "Mumbai Metropolitan Region Development Plan 2036" - MMRDA Official Documents - "The Northward Expansion of Mumbai: Infrastructure and Real Estate" - Knight Frank India Reports - "Goregaon: From Suburb to Business District" - Times Property Special Reports - "Impact of Metro Connectivity on Mumbai Real Estate Values" - CBRE Research

Historical Business Context: - "Industrial Policy in Post-Independence India" - Planning Commission Archives - "The Patel Business Community: Entrepreneurship and Networks" - Economic History Review - "Surface Preparation Industry in India: Technology Evolution" - Indian Foundry Journal Archives - "Mumbai's Transformation: 1980-2020" - Bombay Chamber of Commerce Publications

Investment Analysis: - Screener.in NESCO Page - Comprehensive financial metrics and peer comparison - Tijori Finance NESCO Analysis - Detailed fundamental analysis - ValueResearch NESCO Profile - Mutual fund holdings and analyst views - Trendlyne NESCO Dashboard - Technical and fundamental indicators

Broader Reading on Business Strategy: - "The Outsiders" by William Thorndike - Capital allocation by exceptional CEOs - "Good to Great" by Jim Collins - Why some companies make the leap - "Competitive Strategy" by Michael Porter - Framework for analyzing industries - "The Essays of Warren Buffett" - Lessons on long-term value creation

Indian Conglomerate Studies: - "India's Business Houses: Growth and Transformation" - Oxford University Press - "The Tata Group: From Torchbearers to Trailblazers" - Portfolio Penguin - "Business Maharajas" by Gita Piramal - Profiles of India's business leaders - "The Billionaire Raj" by James Crabtree - Modern Indian capitalism

Real Estate Investment Insights: - "The Real Estate Game" by William Poorvu - Fundamentals of property investment - "Emerging Market Real Estate Investment" by David Lynn - Framework for analysis - REITs and Real Estate Investment Trusts research - NAREIT publications - Indian Real Estate: Opportunities and Challenges - McKinsey India Reports

These resources provide context for understanding NESCO's journey from engineering company to diversified conglomerate, the Mumbai real estate market dynamics, and the broader themes of patient capital allocation and ecosystem building that define the company's strategy.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube