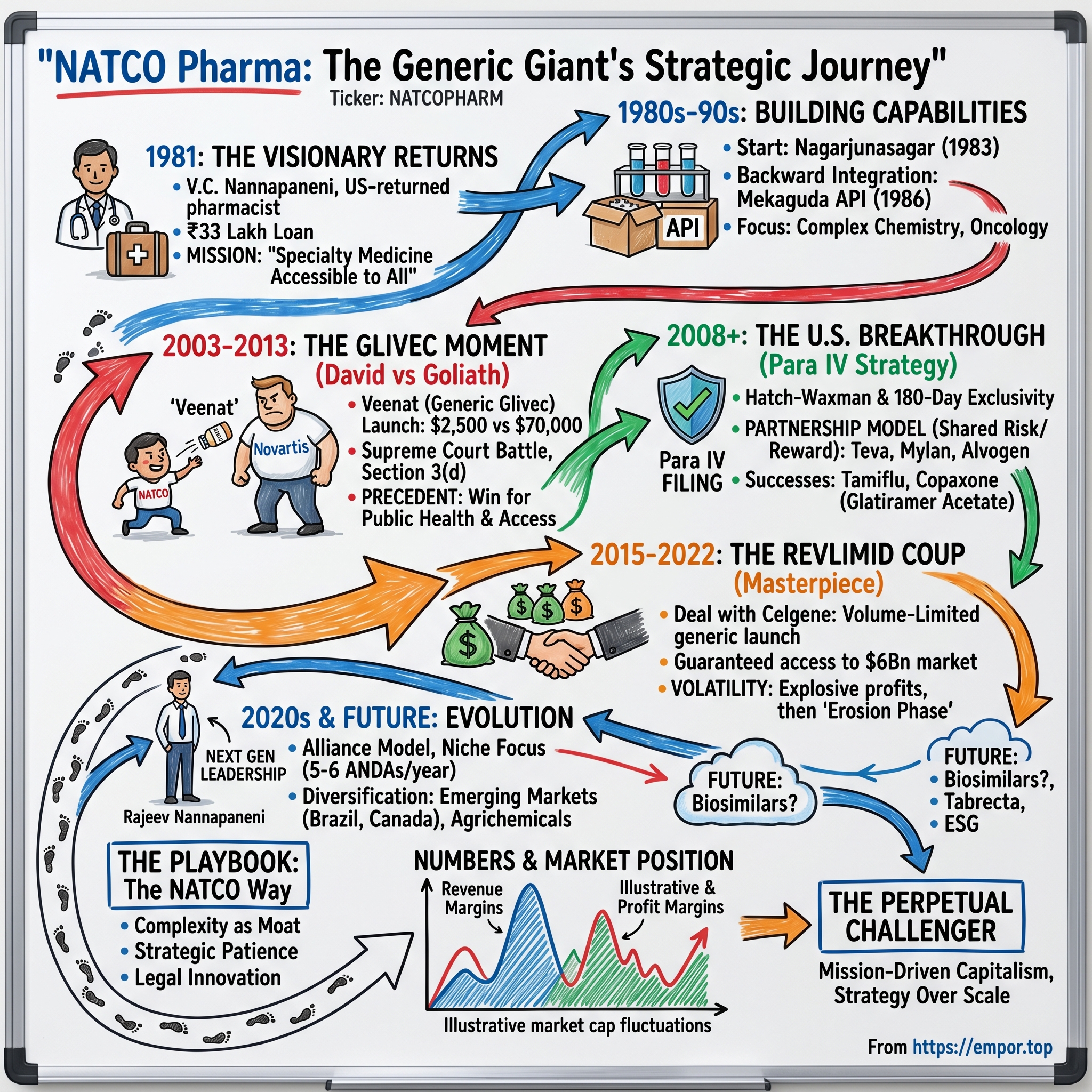

NATCO Pharma: The Generic Giant That Took on Big Pharma

I. Introduction & Episode Teaser

Picture this: March 2013, the Supreme Court of India. On one side sits Novartis, the Swiss pharmaceutical giant with $58 billion in annual revenue. On the other, NATCO Pharma, an Indian company most people had never heard of, with revenues barely crossing $100 million. The case? Whether a life-saving cancer drug that costs $70,000 per year could be sold for $2,500. When the gavel fell, David had beaten Goliath—and the reverberations would shake the global pharmaceutical industry.

This is the story of NATCO Pharma, a company that started with ₹33 lakh in 1981 and built itself into a ₹16,000 crore market cap powerhouse by systematically taking on Big Pharma's most profitable monopolies. Today, NATCO generates ₹4,396 crore in revenue with an extraordinary ₹1,695 crore in profit—a 38.5% profit margin that would make even software companies envious.

But here's what makes this story remarkable: NATCO didn't grow by playing it safe or following the conventional generic pharma playbook of volume and scale. Instead, they became masters of pharmaceutical warfare—using patent law as a weapon, turning regulatory frameworks into strategic advantages, and building a business model that thrives on complexity and risk. They've taken on Novartis over Glivec, Celgene over Revlimid, and Teva over Copaxone—and won.

The central question we're exploring today: How did a US-returned pharmacist named V.C. Nannapaneni build a pharmaceutical empire from a tiny loan that would eventually challenge the world's biggest drug companies? And more importantly, what can we learn from NATCO's playbook of turning David vs. Goliath battles into a repeatable, profitable strategy?

Over the next several hours, we'll dissect NATCO's journey from a small API manufacturer in Telangana to a global player in complex generics. We'll explore their revolutionary approach to compulsory licensing, their mastery of the Paragraph IV challenge system, and how they've built partnerships with rivals to share risks while capturing massive rewards. This isn't just a story about making medicines cheaper—it's about how strategic thinking, legal innovation, and perfect timing can build an empire.

II. V.C. Nannapaneni: The Visionary Returns Home

The monsoon of 1981 had barely passed when V.C. Nannapaneni made a decision that would alter the trajectory of Indian healthcare. After spending more than a decade working in American pharmaceutical companies, absorbing the intricacies of drug development and regulatory frameworks, this 36-year-old pharmacist from the village of Gollamudipadu in Andhra Pradesh chose to leave behind the certainties of corporate America for the uncertainties of entrepreneurial India.

Born in Gollamudipadu, Guntur District, Andhra Pradesh, Nannapaneni held Bachelor's and Master's degrees in Pharmacy from Andhra University, Visakhapatnam, and had acquired a Master's degree in Pharmaceutical Administration from Brooklyn College of Pharmacy in the US. He had worked in the US for more than a decade in various pharmaceutical companies. But unlike many of his contemporaries who saw America as the destination, Nannapaneni saw it as preparation.

The India he returned to in 1981 was a different world from today's pharmaceutical powerhouse. The country was still a year away from the Asian Games that would begin modernizing its infrastructure, still a decade away from economic liberalization. The pharmaceutical industry was dominated by multinationals, and Indian companies were largely relegated to manufacturing basic drugs under license. Patents were respected religiously, and the idea that an Indian company could challenge Big Pharma seemed absurd.

Nannapaneni was just 36 when, in 1981, he chose to return to India after working in the US. He founded NATCO with a small loan that he managed to secure and with support from family. The initial investment was modest—just ₹33 lakh (₹3.3 million)—but the vision was anything but small.

What drove this decision wasn't just entrepreneurial ambition; it was a deeply personal philosophy about healthcare accessibility. Nannapaneni believed that no patient should go without medicine or treatment due to economic constraints. This belief inspired him to start NATCO Pharma with a vision of "making specialty medicines accessible to all." It wasn't merely a business tagline—it would become the strategic North Star that would guide every major decision the company would make over the next four decades.

The name NATCO itself reflected a certain ambition—National Company—suggesting aspirations that went beyond regional boundaries. But in those early days, with just 20 employees in a single unit, such grand visions must have seemed almost delusional to outsiders.

Nannapaneni brought something unique to the Indian pharmaceutical landscape: a deep understanding of American regulatory systems combined with an intimate knowledge of Indian market realities. During his decade in the US, he hadn't just learned about drug manufacturing—he had studied the entire ecosystem: FDA regulations, patent law, the economics of drug development, and crucially, the vulnerabilities in the system that could be exploited legally and ethically.

He understood something that would become central to NATCO's strategy: the global pharmaceutical industry's Achilles' heel wasn't its science or manufacturing capabilities—it was its pricing model. Big Pharma's business model depended on charging astronomical prices in developed markets to recoup R&D investments. But what if you could legally circumvent patents? What if you could use the very legal frameworks designed to protect Big Pharma as weapons against them?

This wasn't going to be a story of competing on scale or efficiency. Nannapaneni had no interest in becoming another contract manufacturer or a me-too generic company fighting on price in commodity markets. He established NATCO Pharma with a modest investment and a grand vision—to make quality medicines accessible and affordable for all. At a time when the Indian pharmaceutical industry was still evolving, he anticipated the need for indigenous drug manufacturing to reduce dependency on costly imports. With a relentless focus on research and development, he steered the company toward producing high-quality generic drugs.

The India of 1981 offered both challenges and hidden advantages. The Patent Act of 1970 had already laid the groundwork by recognizing only process patents, not product patents, for pharmaceuticals. This meant Indian companies could reverse-engineer drugs as long as they used different manufacturing processes. But most Indian companies were content with making simple generics. Nannapaneni saw an opportunity to go after complexity—to target drugs that were difficult to manufacture, had limited competition, and served critical medical needs.

His American experience had taught him that the real money in pharmaceuticals wasn't in making the thousandth version of paracetamol—it was in complex generics, in specialized therapies, in being first to market when patents expired or could be challenged. He had seen how the Hatch-Waxman Act in the US created opportunities for generic manufacturers who were willing to take on patent challenges. He understood that regulatory knowledge could be as valuable as manufacturing capability.

Today, V.C. Nannapaneni prefers to stay in the background and lets his son and vice-chairman and CEO, Rajeev Nannapaneni, take charge, while he mentors, urging all to singularly focus on product development. He sees no reason to worry thereafter. But in 1981, he was very much in the trenches, sketching out plans, negotiating with banks, convincing talented scientists to join a company that existed more in vision than reality.

The early strategy was deliberate and methodical. Unlike companies that rushed to market with whatever they could manufacture, Nannapaneni insisted on building capabilities from the ground up. This meant starting with active pharmaceutical ingredients (APIs)—the actual drug compounds—before moving to finished formulations. It meant investing in R&D when the company could barely afford it. It meant saying no to easy opportunities in favor of building for the long term.

The journey presented numerous challenges including financial limitations, regulatory obstacles, and fierce competition from established firms. Despite these difficulties, his steadfast resolve and strategic foresight ensured that NATCO Pharma persevered. What sustained him through those early years wasn't just determination—it was a clear vision of what NATCO could become: not just another pharmaceutical company, but a force for democratizing healthcare.

By choosing to return to India at 36, at the peak of his American career, V.C. Nannapaneni wasn't just starting a company—he was initiating a revolution in how Indian pharmaceutical companies could compete globally. The boy from Gollamudipadu who had conquered Brooklyn was ready to take on Basel, New Jersey, and Cambridge. The question wasn't whether he would succeed—it was how many lives would be transformed in the process.

III. Building from Zero: The Early Years (1981–2000)

The first manufacturing facility tells you everything about a company's DNA. For NATCO, it wasn't in a bustling industrial hub or a prestigious business district—it was in Nagarjunasagar, a remote town in Telangana better known for its dam than its industry. In 1983, operations commenced at the manufacturing facility at Nagarjunasagar, Telangana. The location choice was deliberate: land was affordable, the Andhra Pradesh government was offering incentives, and being away from established pharmaceutical clusters meant NATCO could build its culture without interference.

Three years later, NATCO made a crucial strategic move that would define its competitive advantage for decades. In 1986, the company's chemical division started at Mekaguda, Telangana. While other Indian pharmaceutical companies were content with importing APIs and simply formulating them into tablets and capsules, Nannapaneni understood that true independence—and true value creation—came from backward integration. If you controlled the API, you controlled your destiny.

The 1980s were brutal for a small pharmaceutical company in India. The market was dominated by multinationals like Glaxo, Pfizer, and Hoechst, who had both the brands and the distribution networks. Indian companies that succeeded did so by playing in the margins—making cheaper versions of off-patent drugs for the price-conscious Indian market. But Nannapaneni had observed something crucial during his time in America: the real profits in pharmaceuticals came from complexity, not volume.

This insight led to NATCO's first major strategic pivot in the early 1990s. Instead of competing in crowded therapeutic areas like antibiotics or pain management, the company began focusing on complex chemistry. They started developing capabilities in oncology—a field most Indian companies avoided because of the technical challenges and smaller patient populations. Cancer drugs required sophisticated manufacturing processes, stringent quality controls, and deep technical expertise. They were exactly the kind of high-barrier, high-margin products that could differentiate NATCO.

Today, with a fortune of ₹8,600 crore, Nannapaneni is the 10th richest person of Hyderabad. But in the 1990s, he was still struggling to keep the company afloat. The R&D investments were draining cash, the complex products were taking longer to develop than anticipated, and the company was too small to attract top talent. Many nights, Nannapaneni must have wondered if his American colleagues had been right—perhaps he should have stayed in the comfortable certainty of corporate employment.

What saved NATCO during these lean years was a combination of government contracts and strategic partnerships. The company became a supplier to government hospitals, providing essential medicines at razor-thin margins but generating crucial cash flow. They also began partnering with larger Indian companies, manufacturing products on contract while building their own capabilities. It wasn't glamorous work, but it kept the lights on while the company invested in its future.

The transformation of NATCO from a struggling API manufacturer to a formulations company happened gradually through the 1990s. Each product launch was a learning experience—understanding regulatory requirements, building quality systems, establishing distribution networks. The company made mistakes, had product recalls, faced regulatory warnings. But each setback was treated as education, not failure.

A pivotal moment came in 1995 when NATCO decided to establish a dedicated R&D center. This wasn't just another laboratory—it was a statement of intent. While competitors were content with reverse engineering, NATCO began investing in novel drug delivery systems and complex formulation technologies. The R&D team, initially just a handful of scientists, was given an unusual mandate: don't just copy drugs, improve them. Make them more stable, more bioavailable, easier to manufacture.

The late 1990s brought new challenges and opportunities. India's signing of the GATT agreement meant that product patents would soon be recognized, ending the free-for-all of process patent workarounds. Many Indian companies panicked, fearing they would be reduced to contract manufacturers for Big Pharma. But Nannapaneni saw opportunity where others saw threat. If India was going to recognize product patents, it would also have to implement safeguards like compulsory licensing. If Indian companies were going to face patent challenges, they would also gain access to mechanisms like Paragraph IV certifications for the US market.

By 2000, NATCO had grown from those initial 20 employees to over 500. The company had multiple manufacturing facilities, a respectable product portfolio, and most importantly, capabilities in complex chemistry that few Indian companies could match. Revenue had grown from virtually nothing to several hundred crores. But more than the financial metrics, what mattered was the foundation that had been laid.

The company had developed three critical capabilities that would define its future success. First, it had mastered the science of complex generics—the ability to reverse-engineer and manufacture drugs that others found too difficult or too risky. Second, it had built a deep understanding of global regulatory frameworks—not just compliance, but how to use regulations strategically. Third, and perhaps most importantly, it had cultivated a culture of calculated risk-taking, where big bets on difficult products were not just tolerated but encouraged.

It was not until 2003—22 years since its founding—that NATCO got global attention when it launched Veenat, the generic version of Swiss multinational Novartis AG's anti-cancer drug Glivec. But the groundwork for that David vs. Goliath moment had been laid during these two decades of patient building.

The early years of NATCO weren't marked by headline-grabbing victories or exponential growth curves. They were characterized by something more valuable: the methodical construction of capabilities that would eventually allow a company started with ₹33 lakh to take on companies worth billions of dollars. It was during these foundational decades that NATCO developed its unique playbook—one that prioritized complexity over scale, depth over breadth, and purpose over profit.

As the millennium turned, NATCO was ready for its close-up. The small company from Telangana was about to show the world that when it came to pharmaceutical warfare, size mattered less than strategy, and conviction could triumph over capital.

IV. The Glivec Moment: Taking on Novartis (2003–2013)

The year 2003 marked a seismic shift in the global pharmaceutical landscape. NATCO launched Veenat, the generic version of Swiss multinational Novartis AG's anti-cancer drug Glivec (or Gleevec, as it is referred to in the US) in India at one-tenth the cost of the listed price. The numbers told a story of healthcare apartheid: Novartis set the price of Gleevec at USD 2666 per patient per month; generic companies were selling their versions at USD 177 to 266 per patient per month.

For patients with chronic myeloid leukemia (CML), Glivec was nothing short of miraculous—TIME magazine hailed Gleevec in 2001 as the "magic bullet" to cure cancer. But at $32,000 per year, it might as well have been made of gold for most Indian patients. Enter NATCO with Veenat, suddenly making this life-saving treatment accessible to thousands who would otherwise face certain death.

This wasn't just another generic launch. The launch of Veenat (®NATCO pharma) at a fraction of the price of the innovator drug represented a fundamental challenge to the global pharmaceutical order. NATCO wasn't simply copying an off-patent drug—they were directly confronting Novartis's attempts to extend patent protection through what critics called "evergreening."

The science behind the confrontation was complex but the ethics were simple. Novartis had originally patented imatinib in its free base form. Later, they developed and sought to patent the beta crystalline form of imatinib mesylate—essentially the same drug in a different crystalline structure that improved its stability and bioavailability. The "beta crystalline form" of the molecule is a specific polymorph of imatinib mesylate; a specific way that the individual molecules pack together to form a solid. This is the actual form of the drug sold as Gleevec/Glivec.

When India updated its patent laws in 2005 to comply with TRIPS agreements, it included a crucial provision—Section 3(d)—that would become NATCO's weapon. This section stated that mere discovery of a new form of a known substance that doesn't result in enhanced efficacy cannot be patented. It was specifically designed to prevent evergreening, and NATCO would help prove its power.

The legal battle that ensued wasn't just David versus Goliath—it was a test case for whether developing nations could balance intellectual property rights with public health needs. Novartis applied for Exclusive Marketing Rights (EMR) for Gleevec from the Indian Patent Office and the EMR was granted in November 2003. Novartis made use of the EMR to obtain orders against some generic manufacturers who had already launched Gleevec in India.

But NATCO didn't back down. They continued manufacturing and selling Veenat, arguing that the beta crystalline form wasn't sufficiently innovative to warrant patent protection under Indian law. The case wound through various courts and patent offices, with cancer patients' lives hanging in the balance.

The preparation for this battle had begun years earlier. As Nannapaneni recalled, in late 2002, when Natco was seeking niches, there was a lot of literature around on novel anti-cancer drugs like Gleevec, and his people came up with the idea of making these at affordable prices. This wasn't opportunism—it was strategic positioning at the intersection of scientific capability and social mission.

NATCO's approach was methodical. They didn't just copy the drug; they invested in understanding its chemistry, developing their own manufacturing processes, and ensuring bioequivalence. They built partnerships with cancer advocacy groups and patient organizations, turning what could have been seen as patent infringement into a moral crusade for affordable healthcare.

The international reaction was swift and polarized. Patient advocacy groups hailed NATCO as heroes. While generic manufacturers offer Glivec for roughly $175 per patient per month, Novartis sells it for about $2,600 per patient per month. The price differential wasn't just about profit margins—it was about life and death for thousands of patients.

Novartis, predictably, painted a different picture. Ranjit Shahani, vice-chairman and managing director of Novartis India Ltd is quoted as saying "This ruling is a setback for patients that will hinder medical progress for diseases without effective treatment options." He also said that companies like Novartis would invest less money in research in India as a result of the ruling.

The climax came on April 1, 2013, when the Supreme Court of India delivered its verdict. The court ruled against Novartis, holding that the beta crystalline form of imatinib mesylate failed the test of Section 3(d) as it didn't demonstrate significantly enhanced therapeutic efficacy over the known compound. Since the Court's ruling guaranteed the continued production and reasonable pricing of generic Glivec in India and other developing nations, the ruling was widely heralded as a win for public health and access to medications.

The impact was immediate and profound. Not only could NATCO continue selling Veenat in India, but the precedent emboldened generic manufacturers worldwide to challenge seemingly minor modifications to existing drugs. The case became required reading in law schools and public health programs globally, cited as an example of how developing nations could use TRIPS flexibilities to protect public health.

For NATCO, the victory was transformative. Not until 2003, or 22 years since its birth, did Natco manage to find its moment of glory and start the climb back into profits. Natco launched Veenat, a generic version of Swiss multinational Novartis AG's anticancer drug Gleevec. Veenat cost less than 1/10th that of Gleevec. The company had found its calling—complex generics that challenged patents on drugs with significant public health impact.

The financial impact was substantial, but the reputational gain was even greater. NATCO went from being an unknown Indian generic manufacturer to a company that global pharmaceutical giants had to take seriously. They had proven that with the right legal strategy, technical capabilities, and moral conviction, even the smallest player could challenge the industry's biggest names.

The introduction of generic Sorafenib (Nexavar) followed a similar playbook. A pivotal moment for Natco arrived with the introduction of generic Sorafenib, a cancer treatment that was made available at a significantly lower price than its branded counterpart. This groundbreaking decision not only transformed cancer care in India but also elevated Natco's status on the global stage.

But perhaps the most important outcome of the Glivec battle was the template it created. NATCO had shown that compulsory licensing and patent challenges weren't just theoretical possibilities—they were practical tools that could be deployed to expand access to essential medicines. The company had written the playbook for how generic manufacturers could use legal frameworks designed by developed nations to serve developing world needs.

The Glivec moment also marked a generational transition within NATCO. While V.C. Nannapaneni had laid the foundation, it was during this period that his son Rajeev began taking a more prominent role, bringing a combination of American business education and Indian market understanding to the company's strategy.

By 2013, when the Supreme Court verdict was delivered, NATCO had transformed from a company that made affordable medicines to a company that fought for the right to make medicines affordable. The distinction was crucial—they weren't just manufacturers; they were activists in lab coats, using chemistry and law as tools for social justice.

The ripple effects continue to this day. Every time a pharmaceutical company thinks twice before attempting to evergreen a patent, every time a government considers compulsory licensing for essential medicines, every time a patient advocacy group challenges drug pricing, they're building on the precedent that NATCO helped establish.

The Glivec battle had proven something fundamental: in pharmaceutical warfare, moral authority could be as powerful as market capitalization, and a company built on purpose could prevail against companies built purely for profit.

V. The U.S. Breakthrough: Paragraph IV Strategy

While NATCO was winning headlines with compulsory licensing battles in India, they were quietly preparing for an even bigger game in the world's most lucrative pharmaceutical market. In 2008, Natco Pharma filed its first paragraph IV filing in the US with the USFDA—a moment that would transform the company from an Indian generic manufacturer into a global pharmaceutical player.

To understand the significance of this move, you need to understand the genius of the Hatch-Waxman Act. Under the Drug Price Competition and Patent Term Restoration Act of 1984, also known as the Hatch-Waxman Amendments, a company can seek FDA approval to market a generic drug before the expiration of patents related to the brand-name drug that the generic seeks to copy. To seek this approval, a generic applicant must provide in its application a "certification" that a patent submitted to FDA by the brand-name drug's sponsor and listed in FDA's Approved Drug Products with Therapeutic Equivalence Evaluations (the Orange Book) is, in the generic applicant's opinion and to the best of its knowledge, invalid, unenforceable, or will not be infringed by the generic product.

The brilliance of Paragraph IV challenges lies in the risk-reward equation. The statute provides that the first applicant to file a substantially complete ANDA containing a paragraph IV certification to a listed patent will be eligible for a 180-day period of exclusivity beginning either from the date it begins commercial marketing of the generic drug product, or from the date of a court decision finding the patent invalid, unenforceable or not infringed, whichever is first. These two events - first commercial marketing and a court decision favorable to the generic - are often called "triggering" events, because under the statute they can trigger the beginning of the 180-day exclusivity period. In some circumstances, an applicant who obtains 180-day exclusivity may be the sole marketer of a generic competitor to the innovator product for 180 days.

But here's where NATCO's strategy diverged from typical generic companies. Instead of going it alone and bearing the full cost of patent litigation—which can run into tens of millions of dollars—NATCO developed a partnership model that would become its signature approach to the US market.

The first major success came with Tamiflu. Alvogen, the US-based pharmaceutical company, today announced that its India-based partner, Natco Pharma Limited, has filed an Abbreviated New Drug Application (ANDA) with the U.S. Food and Drug Administration (FDA) for the generic version of Tamiflu® (oseltamivir phosphate). Both Natco and Alvogen believe it is the first substantially completed ANDA filing containing a Paragraph IV certification and expect to qualify for 180 days of marketing exclusivity upon final FDA approval. Oseltamivir phosphate capsules are used in the treatment of bird and swine flu infections and sold by Hoffman – La Roche under the brand name Tamiflu®. According to IMS Health in 2009, Tamiflu® had U.S. sales in excess of US$1 billion.

One was the launch of the first generic version of Tamiflu (Oseltamivir oral capsules), used to treat influenza, for which Natco tied up with marketing partner Alvogen in the US. The partnership structure was elegant: NATCO would handle the complex chemistry and manufacturing, file the ANDA, and navigate the regulatory process. The partner—in this case Alvogen—would handle the expensive patent litigation, manage the marketing and distribution, and share the revenues.

Typically, Natco's strategy has been to work with a partner in markets like the US. The partners handle litigation costs and marketing and share the revenues in return. Alvogen, Mylan, Breckenridge Pharmaceuticals, Dr Reddy's and Lupin are among its many partners. This model allowed NATCO to punch far above its weight class, competing for blockbuster generics without the capital requirements that would typically exclude a company of its size.

But the real coup came with Copaxone, Teva's multiple sclerosis blockbuster. The launch of the generic version of Teva's drug Copaxone for multiple sclerosis in the US, with its partner Mylan, in the second half of 2017 was another major move. The drug represented everything NATCO had been building toward—complex chemistry, high barriers to entry, and massive market opportunity.

Glatiramer acetate, the active ingredient in Copaxone, isn't a traditional small molecule drug—it's a complex mixture of polypeptides that's notoriously difficult to characterize and manufacture. It is a mixture of random-sized peptides that are composed of the four amino acids found in myelin basic protein, namely glutamic acid, lysine, alanine, and tyrosine. Glatiramer acetate is a random polymer (average molecular mass 6.4 kDa) composed of four amino acids found in myelin basic protein.

NATCO's expertise in complex chemistry, built over decades of working with difficult oncology drugs, proved crucial. The Copaxone generic demonstrated its chemistry skills - the API (active pharmaceutical ingredient) going into the drug is made by Natco. The drug is in two formats, 20 mg and 40 mg. For 20 mg, Natco makes both the API and the formulation, and for the 40 mg, it makes the API. Analysts rate Natco's chemistry capabilities as noteworthy. Even in oncology, a key therapy area for the company, the focus has been more on chemistry than biotech.

The partnership with Mylan for Copaxone was announced with great fanfare. Mylan N.V. (NASDAQ, TASE: MYL) today confirmed that the company has launched in the U.S. the first Glatiramer Acetate Injection 40 mg/mL for 3-times-a-week injection that is an AP-rated substitutable generic version of Teva's Copaxone® 40 mg/mL, as well as Glatiramer Acetate Injection 20 mg/mL for once-daily injection, an AP-rated, substitutable generic version of Teva's Copaxone® 20 mg/mL. These products are indicated for the treatment of patients with relapsing forms of multiple sclerosis (MS), a chronic inflammatory disease of the central nervous system. Shipments to customers have commenced.

The financial implications were staggering. Copaxone® is the most prescribed MS treatment for relapsing forms of MS in the United States with brand sales for the 20 mg/mL dose of approximately $700 million and for the 40 mg/mL dose of approximately [sales data] July 31, 2017, according to QuintilesIMS. Even a small share of this market, combined with potential 180-day exclusivity, could generate hundreds of millions in revenue.

The success with Copaxone validated NATCO's US strategy. They had proven they could compete at the highest levels of generic pharmaceutical complexity. The company that had started with a ₹33 lakh investment was now partnering with billion-dollar multinationals as equals, sharing in profits from drugs with billions in sales.

In India, it was among the first to launch the hepatitis C basket of products - the drug and its combinations - under a licensing agreement with Gilead Sciences. This demonstrated NATCO's ability to work both sides of the patent system—challenging patents through Paragraph IV in the US while simultaneously licensing from innovators where it made strategic sense.

The Paragraph IV strategy wasn't without risks. In order to challenge a patent in court, the generic applicant that submitted a paragraph IV certification must notify the brand product sponsor and any patent holder of the submission of the ANDA and patent challenge. If the brand product sponsor or patent holder files an infringement suit against the generic applicant within 45 days of the ANDA notification, FDA approval to market the generic drug is generally postponed for 30 months unless the patent expires or is judged to be invalid or not infringed before that time. This 30-month postponement, commonly referred to as the "30-month stay," gives the brand product sponsor and patent holder a prescribed amount of time to assert patent rights in court before a generic competitor is approved and can market the drug.

But NATCO had developed a sophisticated approach to managing these risks. By partnering with larger companies who could bear litigation costs, by carefully selecting which drugs to challenge based on their chemistry expertise, and by building a portfolio of challenges rather than betting everything on a single drug, they had turned Paragraph IV from a high-stakes gamble into a repeatable business model.

The US breakthrough represented more than just financial success. It proved that an Indian company could compete in the world's most sophisticated pharmaceutical market not through cost advantages or volume, but through scientific excellence and strategic sophistication. NATCO had graduated from being a challenger of Big Pharma in Indian courts to being a player in the global pharmaceutical chess game.

As we'll see in the next section, all of this was merely preparation for NATCO's masterpiece—the Revlimid settlement that would generate billions in value and cement the company's reputation as one of the smartest players in generic pharmaceuticals.

VI. The Revlimid Coup: NATCO's Masterpiece

If the Glivec battle established NATCO as a fighter for affordable healthcare, and the Paragraph IV challenges proved their technical prowess, the Revlimid settlement represents something altogether different—a masterclass in pharmaceutical deal-making that would generate billions in value from a single negotiation.

Revlimid (lenalidomide) wasn't just another cancer drug—it was a financial juggernaut. It brought the price of Revlimid to $9,854 a month, or $469 a pill, and helped boost Revlimid sales for the year to $5 billion. The price of Revlimid has been hiked 26 times since it launched. For patients with multiple myeloma, it was life-saving. For Bristol Myers Squibb (which acquired Celgene), it was the crown jewel of their portfolio.

The genius of NATCO's approach to Revlimid began with recognizing a unique vulnerability in Celgene's patent strategy. Natco, leveraging its legal expertise, argued that Celgene's patents on Lenalidomide were overly broad and non-innovative. But rather than fight to the bitter end, as they had with Novartis over Glivec, NATCO played a different game—one of strategic patience and calculated compromise.

The 2015 settlement announcement shocked the industry. Celgene has agreed to provide Natco with a license to Celgene's patents required to manufacture and sell an unlimited quantity of generic lenalidomide in the United States beginning on January 31, 2026. In addition, Natco will receive a volume-limited license to sell generic lenalidomide in the United States commencing in March 2022. The volume limit is expected to be a mid-single-digit percentage of the total lenalidomide capsules dispensed in the United States during the first full year of entry. The volume limitation is expected to increase gradually each 12 months until March of 2025, and is not expected to exceed one-third of the total lenalidomide capsules dispensed in the U.S. in the final year of the volume-limited license under this agreement.

This wasn't a typical generic settlement. Celgene found a solution to the generic threat when it struck a deal to settle a lawsuit brought by generic maker NATCO Pharma in 2015. NATCO could bring a generic to market, Celgene agreed, but not for seven more years — in March 2022. Even then, the generic would be limited to less than 10% of the total market for Revlimid in the first year, with gradual increases after that. The deal set the bar for deals with other rivals for limited generic sales, and it ensured that unlimited generic competition — and lower prices — would not arrive until 2026.

The structure was brilliant for both parties. Celgene protected its blockbuster revenue stream for years while avoiding the uncertainty of litigation. NATCO, meanwhile, secured guaranteed access to one of the world's most lucrative drug markets with minimal competition. The volume limitations meant that even as a generic manufacturer, NATCO could maintain premium pricing.

The real coup came in NATCO's choice of partner for commercialization. Rather than going with a traditional generic company, they partnered with Teva—the world's largest generic manufacturer with unmatched distribution capabilities. Reports indicate that FDA approval was obtained in 2021 by two pharmaceutical companies: Natco Pharma Ltd. (working with Teva) on May 21, 2021; and Dr. Reddy's Laboratories Ltd. on October 14, 2021.

March 2022 arrived like Christmas morning for NATCO shareholders. The companies have launched four other strengths of the product in March 2022 in the US market. With today's launch the companies made available all the strengths of lenalidomide in the US market. The launch was flawless—a testament to years of preparation and NATCO's manufacturing excellence.

The financial impact was immediate and staggering. To put things into perspective, in 2019, Natco's revenue stood at ₹2,094.5 crore, with a profit of ₹642.4 crore. Fast forward to 2024, and the company's revenue has nearly doubled to ₹3,998.8 crore, with profit surging to ₹1,388.8 crore. 2023 marked a game-changing year for Natco Pharma. The launch of Revlimid, a blockbuster generic cancer drug, catapulted the company's profitability to new heights. With this breakthrough, Natco's financial performance took off like a rocket, solidifying its position as a major player in the pharmaceutical industry.

But the Revlimid story also illustrates the cyclical nature of NATCO's business model. In Q3FY25, Natco Pharma reported a profit of just ₹132 crore, a sharp 80% decline compared to the previous quarter's ₹676 crore. What makes this even more concerning is that the reported profit included a ₹90 crore one-time gain from the sale of land. If you exclude this one-time gain, the profit decline was closer to 50-60%. The primary reason behind this steep drop? A complete halt in sales of Revlimid, Natco's blockbuster drug that had been the backbone of its revenue.

This volatility wasn't a bug in NATCO's strategy—it was a feature. Natco Pharma has built its success on blockbuster generic drugs like Gleevec, Sovaldi, Copaxone, and Abilify. Once exclusivity ends, competitors flood the market with their own generics, driving prices down and eroding market share. This cyclical pattern is a familiar reality in the pharmaceutical industry, and Natco Pharma has already navigated it with Sovaldi and Abilify—both of which faced intense competition by 2021. As rival generics entered the market, price reductions followed, impacting Natco's revenue. Now, history is repeating itself with Revlimid—which has entered its erosion phase.

The Revlimid deal wasn't just about the money—though the money was certainly spectacular. It validated NATCO's entire strategic approach. They had proven that a relatively small Indian company could negotiate as an equal with Big Pharma, securing deals that balanced immediate revenue with long-term value creation.

The settlement also demonstrated NATCO's evolution as a company. This legal battle continued for years. Settlement Agreement: In 2015, after protracted negotiations, Natco and Celgene reached a settlement agreement. They had learned that sometimes the best victory isn't total defeat of your opponent, but a negotiated solution that creates value for all parties—patients get access to cheaper medicines (eventually), innovators protect their revenue streams (temporarily), and generic manufacturers secure profitable market entry (guaranteed).

The ripple effects of the Revlimid settlement extended beyond NATCO. The move follows a similar deal with Dr. Reddy's Laboratories, which settled with BMS in September to start a "volume-limited" launch of its own Revlimid generic during the same post-March 2022 timeframe. Like Sun, Dr. Reddy's deal tees up the company to sell the drug without restriction beginning in early 2026. Celgene has also forged near-identical pacts with India's Natco Pharma and New Jersey's Alvogen. For its part, Natco in March 2022 could start selling "mid-single-digit percentages" of Revlimid's total volume that month, with the figure set to gradually climb up to one-third of Revlimid's numbers. Alvogen, which has already rolled out a Revlimid copycat in some parts of Europe, has also been cleared to sell generics up to single-digit percentages of Revlimid volumes sometime after March 2022. It will be open season for both companies starting on January 31, 2026.

The Revlimid masterpiece also highlighted NATCO's sophisticated understanding of patent law and market dynamics. They recognized that in the modern pharmaceutical industry, the question isn't whether generics will enter the market, but when and how. By being first to settle, NATCO set the terms that others would follow.

According to the complaint, Celgene settled its lawsuit against first-filer Natco by entering into an anticompetitive reverse payment agreement. The agreement was structured to ensure there would not be generic competition based on price nor the launch of an authorized generic, thus inducing the first-filing generic manufacturer to accept a later date to market its generic product. This was accomplished through provisions such as volume limits on how much product Natco can sell until 2026 and both a most-favored entry clause (also referred to as an acceleration clause) and a most-favored qua[ntity clause].

Critics called it a "pay-for-delay" scheme that kept drug prices artificially high. But from NATCO's perspective, it was the art of the possible—securing guaranteed profits while navigating the complex realities of pharmaceutical patents. The volume limitations that seemed restrictive actually created a controlled market where NATCO could maintain margins that would be impossible in a free-for-all generic competition.

As 2026 approaches and volume restrictions lift, NATCO faces the challenge of what comes next. However, Natco Pharma has consistently demonstrated resilience. Its strong pipeline, strategic drug launches, and ability to capitalize on patent expirations have allowed the company to maintain steady revenue growth over the years. The key question now is: What's next for Natco Pharma? Given its track record, understanding its future portfolio and upcoming drug launches will be crucial in navigating the next phase of growth.

The Revlimid coup wasn't just NATCO's biggest financial success—it was proof that in the high-stakes world of pharmaceutical patents, sometimes the smartest move isn't to destroy your opponent's position, but to become their most valuable partner in managing its decline. It was capitalism at its most sophisticated: creating value not through innovation or efficiency, but through strategic positioning and perfect timing.

VII. Second Generation Leadership: Rajeev Takes Charge

In the pharmaceutical industry, where founders often cling to control well past their prime, the transition at NATCO represents something unusual—a carefully orchestrated passing of the torch that enhanced rather than disrupted the company's momentum. Rajeev Nannapaneni has worked at Merill Lynch and Natco Systems LL.C in USA. He joined the Company in the year 2000. He has got wide experience and exposure in General Management, New Business / New Product Development in India and for International markets. He holds B.A degree in Quantitative Economics and also B.A in History from Tufts University, Boston, USA.

The contrast between father and son couldn't be more striking. Where V.C. Nannapaneni was the quintessential scientist-entrepreneur who built NATCO through technical expertise and moral conviction, Rajeev brought the polish of Wall Street and the strategic thinking of modern business school. degree in History from Tufts University, Boston, USA. Having worked at Merill Lynch and Natco Systems LLC in USA, he has valuable international experience, which he puts to good use in his day-to-day working and strategic planning in his company.

When Rajeev joined NATCO in 2000, the company was at an inflection point. The foundational work of building manufacturing capabilities and establishing the company's reputation was complete. What NATCO needed now was someone who could navigate the increasingly complex world of global pharmaceutical partnerships, patent settlements, and capital markets. The younger Nannapaneni, fresh from Merrill Lynch, was perfectly positioned for this role.

He credits his team - led by his son, the over-six-ft-tall Rajeev Nannapaneni, who is the vice chairman and CEO of the company - for doing things right. Both analysts and industry folk see Rajeev, 40, as a professional with a sharp ability to spot opportunities and adept at keeping a pulse on the happenings within the sector. The physical description—over six feet tall—seems almost metaphorical for how Rajeev would help NATCO stand taller in global markets.

The transition wasn't abrupt. VC Nannapaneni, Chairman and Managing Director of Natco Pharma, prefers to stay in the background and lets his son and the Vice Chairman and CEO, Rajeev Nannapaneni, to take charge while he mentors, urging all to singularly focus on product development. This gradual handover allowed for knowledge transfer while giving Rajeev room to establish his own leadership style.

Rajeev's strategic philosophy represented an evolution of his father's approach. Explaining the strategy for success in the past two to three years, Rajeev says, "We never go after scale or volume or multiple filings for marketing products in the US. The strategy has always been to do limited number of things, but all niche or hard-to-do generics." The company tries to either be the first in the market or launch a product that is linked to a tricky patent litigation or have a product that is based on tough chemistry and, therefore, hard to replicate.

This wasn't just a refinement of the existing strategy—it was a distillation of NATCO's competitive advantages into a repeatable formula. Where many generic companies pursued volume, filing dozens of ANDAs annually, NATCO under Rajeev became even more selective. Focusing on making specialty medicines accessible to all, Mr. Rajeev Nannapaneni's strategy is to file only 5 to 6 abbreviated new drug applications (ANDAs) that really fit the company's core strategy.

The partnership model that would prove so successful with drugs like Copaxone and Revlimid was largely Rajeev's creation. He has also created Natco's business model as completely an alliance model, since he develops a hard-to-make niche product, and then approaches a partner to help out with the litigation and the marketing. This wasn't just about sharing costs—it was about recognizing that in the modern pharmaceutical industry, no single company could excel at everything.

Rajeev brought a sophisticated understanding of market dynamics to NATCO's strategy. Believing that the Indian market structure is shaped in such a way that no generic player would ever get to dominate it or even monopolize a big share of the market, he has concentrated on typically niche products as for every such product, 10 to 15 different generics are expected to exist and only the top 2 would do extremely well. As the market dynamics work, generally those generic products would perform well, which entered the market first, whose prices were competitive, and which followed an aggressive marketing strategy.

The risk management approach under Rajeev's leadership became more nuanced. While the upside of limited products is that you contain costs and are more focussed, the downside is that you have nothing to fall back upon for a period if you are wrong,'' says Rajeev Nannapaneni. This candid acknowledgment of risk, combined with strategies to mitigate it through partnerships and careful selection, showed a maturity beyond the company's relatively small size.

Under Rajeev's leadership, NATCO also began thinking more globally about healthcare access. Also, realizing that though the middle class in India has been growing, there is still an unequal distribution of wealth in the country, and this has a great impact on market dynamics including the healthcare market, he has been strategizing on helping new modern products enter the Indian market and create a sustainable position for his already existing products. As he feels that most Indians are still not able to afford some modern therapies, even when India's wealth is increasing, and several States have been improving their healthcare programs, his strategic move to introduce lower-priced generics in the Indian market is working.

The financial results validated the second-generation strategy. At a time when stock prices of most big players in the pharmaceutical industry have plummeted sharply on the bourses, Hyderabad-based Natco Pharma stands out - the 2,078-crore company has stood its ground despite ups and downs. Consider this: in the past three years, Sun Pharma, the biggest Indian pharma company, has seen its share price tumble from827.2 to 578.8, taking its market cap down from171,316.3 crore to 138,860 crore. Lupin's story is similar - its share price fell from1,429.7 to 899.2 and market cap slipped from64,223.8 crore to 40,644.1 crore. Analysts often refer to how most companies are currently trading at less than 50 per cent of their peak share prices two years ago. However, Natco saw its share price move up from299.5 to 998.9 - closer to the 52-week high of1,080.

The partnership strategy that Rajeev championed drew praise even from competitors. Prasad, Co-chairman and CEO of Dr Reddy's, says, "Natco is a smart company. It has been a partner and competitor. We can live with that." This ability to maintain relationships while competing—to be both partner and rival—required a diplomatic sophistication that Rajeev brought to the company.

The diversification strategy under Rajeev also showed forward thinking. The company hopes to diversify beyond the US and nearly double the revenue over the next three years from the domestic market and from markets other than the US and India. In fact, just last month, Natco initiated work on greenfield manufacturing facilities for producing niche agrichemical products in Andhra Pradesh with a total capital expenditure of Rs 100 crores.

Looking forward, Rajeev's vision for NATCO was both ambitious and realistic. The aim, says Nannapaneni, is to come up with newer products. For instance, he is upbeat about the launch of the generic version of Revlimid, expected to be launched in March 2022 in the US. The innovator product has an estimated market size of close to $6 billion in the US. It is expected to be perhaps higher by 2022. Then, the company is also excited about the generic version of Ibrutinib tablets.

The father-son dynamic at NATCO avoided the pitfalls that often plague family businesses. He says it is pointless if the focus is only on making the company big. While he is around to mentor and guide, it is Rajeev who is seen as driving Natco's operations. V.C. Nannapaneni remained engaged but not interfering, available for counsel but not control.

Focusing on building strong technological capabilities under his leadership, the company can develop any generic now. This technical confidence, combined with strategic sophistication, positioned NATCO uniquely in the global pharmaceutical landscape.

The succession at NATCO wasn't just about maintaining continuity—it was about evolution. Rajeev took his father's vision of making medicines accessible and transformed it into a sophisticated business model that could compete globally while maintaining its social mission. He proved that the second generation could honor the founding vision while adapting it for a changed world.

As NATCO navigates the post-Revlimid landscape, Rajeev's leadership will be tested. But his track record suggests he has both the strategic acumen and the operational expertise to guide the company through its next phase. The boy who left Wall Street to join his father's pharmaceutical company had become a leader who could hold his own with the industry's titans.

The transition from V.C. to Rajeev Nannapaneni represents more than just a generational change—it's a case study in how family businesses can professionalize without losing their soul, how founding visions can evolve without being abandoned, and how the next generation can build on foundations while reaching for new heights.

VIII. Business Model Deep Dive

To understand NATCO's business model, you need to think of it less as a traditional pharmaceutical company and more as a sophisticated arbitrage operation that exploits inefficiencies in global patent systems. The company has established its presence in all three business segments viz. finished dosage formulations ("FDF"), active pharmaceutical ingredients ("APIs"), Contract Manufacturing Business. The company manufactures and markets finished dosage formulations in 50+ countries, including the US, Canada, Brazil, and Europe.

The genius of NATCO's model lies in its selectivity. While competitors file dozens of ANDAs annually, chasing volume, NATCO deliberately limits itself to 5-6 filings per year. Each filing represents months of analysis—evaluating patent vulnerabilities, manufacturing complexity, market size, and competitive dynamics. They're not playing roulette; they're playing chess.

Major US partners include Sun-Ranbaxy, Aceto-Rising, Alvogen, Teva, Mylan, Actavis, Lupin, etc. Its international business focuses on Para IV and first-to-file molecules, with plans to expand into emerging markets like MENA, LATAM, and Southeast Asia. This partnership ecosystem isn't just about sharing costs—it's about creating a network effect where NATCO's technical capabilities become more valuable as they connect with more commercial partners.

The revenue breakdown tells a fascinating story of strategic evolution. Export Formulation represents 44% in Q3 FY25 vs 73% in FY23, showing how the company has diversified from export dependence while maintaining its international focus. The shift reflects both the maturation of the domestic market and the cyclical nature of blockbuster generic launches.

The API backward integration strategy that began in 1986 continues to pay dividends. By controlling the active ingredients, NATCO maintains margins that pure formulation companies can't achieve. When you manufacture both the API and the finished product, you capture value at multiple points in the chain. This vertical integration also provides strategic flexibility—they can supply APIs to competitors while maintaining their own formulation business.

But the real sophistication lies in NATCO's approach to risk management. The partnership model means they rarely bear the full cost of patent litigation, which can run $10-30 million per case. Partners handle the legal battles and marketing expenses while NATCO focuses on what they do best—complex chemistry and regulatory navigation. It's a division of labor that maximizes returns while minimizing capital requirements.

The manufacturing infrastructure reflects this focused approach. Eight facilities across India might seem modest compared to giants like Sun Pharma or Cipla, but each facility is optimized for complexity rather than volume. They're set up to handle oncology drugs, controlled substances, and products requiring special handling—the kinds of manufacturing challenges that create barriers to entry.

NATCO's approach to capacity utilization is counterintuitive but brilliant. They deliberately maintain excess capacity, knowing that when a Paragraph IV challenge succeeds or a compulsory license is granted, they need to scale rapidly. The opportunity cost of idle capacity is far less than the opportunity cost of missing a limited-exclusivity window.

The contract manufacturing segment, while smaller, serves a strategic purpose beyond revenue generation. It keeps facilities utilized during gaps between major launches, maintains relationships with potential partners, and provides intelligence on market trends. When you're manufacturing for others, you learn what's working and what's not without bearing market risk.

IX. The Numbers & Market Position

The financial trajectory of NATCO reads like a masterclass in value creation through strategic positioning rather than operational scale. From that initial ₹33 lakh investment in 1981, the company has built a market capitalization that peaked above ₹27,000 crore, though current market cap stands at 15,553 Crore (down -43.9% in 1 year) reflecting the post-Revlimid normalization.

The recent quarterly performance illustrates both the power and volatility of NATCO's model. The company's consolidated net profit surged 83.55% to Rs 677.30 crore in Q2 FY25 as against Rs 369 crore reported in Q2 FY24. Revenue from operations was at Rs 1,371.1 crore in Q2 FY25, up 32.93% from Rs 1,031.4 crore posted in Q2 FY24. These aren't the steady, predictable growth rates of a traditional pharma company—they're the explosive returns of successful patent challenges and product launches.

However, the Q3 FY25 results show the other side of this volatility. NATCO recorded consolidated total revenue of Rs 651.1 crore for Q3FY25, as against Rs 795.6 crore for Q3FY24. The net profit for the period, on a consolidated basis, was Rs 132.4 crore as against Rs 212.7 crore for Q3FY24. This dramatic quarter-to-quarter variation is a feature, not a bug, of NATCO's business model.

The profitability metrics are where NATCO truly shines. With revenue of 4,396 Cr and profit of 1,695 Cr, the company maintains profit margins that would be extraordinary in any industry, let alone in generic pharmaceuticals where many companies operate on single-digit margins. This isn't achieved through operational efficiency alone—it's the result of careful product selection and strategic timing.

The five-year performance tells the story of transformation. The company has delivered 33.4% CAGR profit growth over the last five years, a period that included both the COVID windfall from drugs like Remdesivir and the game-changing Revlimid launch. But more importantly, it demonstrates NATCO's ability to consistently find and execute on high-value opportunities.

Valuation metrics reflect the market's mixed feelings about NATCO's model. A P/E ratio of 8.55 seems absurdly low for a company with such strong profitability, but it reflects concerns about sustainability and the lumpy nature of earnings. The P/B ratio of 2.75 suggests the market values the company's strategic positioning and intellectual property beyond its tangible assets.

When compared to peers, NATCO's financial profile stands out. Sun Pharma, with revenues exceeding ₹50,000 crore, operates at net margins around 15-18%. Cipla, with revenues around ₹25,000 crore, maintains margins in the 12-15% range. NATCO, despite being a fraction of their size, consistently achieves margins above 30% during peak periods. This isn't about being better operators—it's about playing a different game entirely.

The capital allocation philosophy under the Nannapanenis has been remarkably disciplined. The Board of Directors has declared third interim dividend of Rs 1.5 per equity share, for FY25. The Board of Directors has declared second interim dividend of Rs 1.50 per equity share, for FY25. Rather than chasing growth through acquisitions or massive capex, they've focused on returning cash to shareholders while maintaining sufficient reserves for opportunistic investments.

The working capital management deserves special attention. Unlike companies that tie up capital in inventory and receivables, NATCO's partnership model means others often bear these costs. When Teva markets Revlimid or Mylan distributes Copaxone, they're handling the working capital requirements while NATCO focuses on manufacturing and collecting its share of profits.

Stock performance has been a rollercoaster that rewards timing and punishes momentum investing. The 52-week range from ₹752 to ₹1,639 reflects the binary nature of NATCO's catalyst-driven model. When products launch successfully, the stock soars. When exclusivity periods end or launches disappoint, it crashes. This isn't a buy-and-hold forever stock—it's a strategic position that requires active monitoring.

The international revenue mix provides stability amidst volatility. The company manufactures and markets finished dosage formulations in 50+ countries, creating multiple revenue streams that can offset weakness in any single market. This geographic diversification, combined with therapeutic diversity, helps smooth out some of the inherent lumpiness in the business model.

Promoter Holding stands at 49.6%, reflecting the family's continued confidence in the business while maintaining sufficient public float for liquidity. This ownership structure aligns management incentives with shareholder interests while avoiding the governance issues that plague some family-controlled businesses.

X. Playbook: The NATCO Way

If you were to distill NATCO's 43-year journey into actionable lessons, you'd have a playbook that challenges conventional wisdom about how to build a pharmaceutical empire. These aren't just tactics—they're philosophical approaches to business that have proven remarkably durable across different regulatory regimes, market conditions, and competitive landscapes.

Lesson 1: Complexity is a Moat, Not a Challenge

Where others see difficulty, NATCO sees opportunity. The company has consistently chosen products that require sophisticated chemistry, complex manufacturing processes, or challenging regulatory pathways. This isn't masochism—it's strategy. When you're one of only three companies globally that can manufacture a particular complex generic, you don't compete on price; you compete on capability. The barriers that keep you out initially become the walls that protect your profits later.

Lesson 2: Partnerships Are Force Multipliers

NATCO's partnership model turns conventional competitive dynamics on their head. By partnering with potential competitors, they transform zero-sum games into positive-sum opportunities. When NATCO partners with Teva on Revlimid, they're not splitting a pie—they're accessing Teva's distribution network while Teva accesses NATCO's technical capabilities. The result is value creation that neither could achieve alone.

Lesson 3: Legal Innovation Can Be as Valuable as Scientific Innovation

NATCO has shown that understanding legal frameworks—compulsory licensing, Paragraph IV challenges, settlement negotiations—can create as much value as discovering new molecules. They've turned regulatory processes designed to protect innovation into tools for democratizing access to medicines. This isn't about exploiting loopholes; it's about using the system as designed to balance innovation incentives with public health needs.

Lesson 4: Mission-Driven Capitalism Isn't an Oxymoron

V.C. Nannapaneni's founding vision—that no patient should go without medicine due to economic constraints—hasn't been diluted by commercial success. Instead, it's become a strategic advantage. When you're genuinely committed to expanding access, you find creative solutions that pure profit-maximizers miss. The Glivec case wasn't just about making money; it was about saving lives. That moral authority became a powerful weapon in legal and regulatory battles.

Lesson 5: Small Can Be Beautiful in Pharmaceuticals

NATCO has resisted the industry's obsession with scale. While competitors pursue blockbuster drugs and mass markets, NATCO focuses on niche products with limited competition. They've proven that in pharmaceuticals, unlike many industries, you don't need to be big to be profitable. You need to be smart, focused, and willing to take calculated risks that larger companies won't touch.

Lesson 6: Timing Beats Speed

NATCO doesn't try to be first to market with every product. Instead, they focus on being first to file for the right products. They understand that in generic pharmaceuticals, the prize often goes not to the swift but to the patient. The Revlimid settlement, where they agreed to wait until 2022 to launch, exemplifies this philosophy. Sometimes the best move is to wait for the perfect moment rather than rush to an imperfect launch.

Lesson 7: Intellectual Property Is a Tool, Not a Sacred Right

NATCO's approach to patents is pragmatic rather than ideological. They respect valid patents that represent genuine innovation, but they challenge patents that merely extend monopolies without adding therapeutic value. This balanced approach has allowed them to work within the system while challenging its excesses. They've shown that you can be both a defender and challenger of intellectual property, depending on the context.

Lesson 8: Focus Beats Diversification

While business school teaches diversification as risk management, NATCO has shown that in knowledge-intensive industries, focus can be less risky than spreading yourself thin. By concentrating on complex generics and oncology, they've built deep expertise that compounds over time. Each successful product launch makes the next one more likely to succeed, creating a virtuous cycle of capability building.

Lesson 9: Family Businesses Can Professionalize Without Losing Soul

The transition from V.C. to Rajeev Nannapaneni shows that family businesses can modernize without abandoning founding principles. By bringing in professional management practices while maintaining family values, NATCO has avoided both the stagnation that afflicts some family firms and the mission drift that affects some professionally managed companies.

Lesson 10: Volatility Is the Price of Extraordinary Returns

NATCO has embraced rather than smoothed earnings volatility. They understand that in their chosen strategy, periods of extraordinary profitability will be followed by normalization. Instead of trying to smooth earnings through diversification or financial engineering, they've educated investors to expect and accept volatility as the price of superior long-term returns.

The NATCO playbook isn't universally applicable. It requires specific capabilities—technical expertise, regulatory sophistication, legal acumen, and patient capital. It also requires a particular risk appetite—the willingness to bet big on uncertain outcomes while managing downside through partnerships and portfolio diversification. But for companies willing to embrace complexity and uncertainty, NATCO has shown a path to extraordinary value creation.

XI. Bear vs. Bull Case

The investment case for NATCO Pharma presents a fascinating study in contrasts—a company that has delivered spectacular returns but faces fundamental questions about sustainability and repeatability. Understanding both the bull and bear perspectives is crucial for anyone trying to evaluate NATCO's future.

The Bull Case: Structural Advantages in a Growing Market

Bulls argue that NATCO's best days may still be ahead. The global generic pharmaceutical market continues to grow, driven by aging populations, rising healthcare costs, and expiring patents on blockbuster drugs. NATCO's positioning at the complex end of this market means they face less competition and maintain higher margins than commodity generic manufacturers.

The pipeline remains robust, with multiple high-value opportunities in various stages of development. While specific products remain confidential for competitive reasons, NATCO's track record suggests they have several potential Revlimid-scale opportunities in their portfolio. The company's expertise in oncology positions them perfectly for the wave of cancer drug patents expiring in the next decade.

The partnership network that NATCO has built represents a sustainable competitive advantage. These aren't transactional relationships but strategic alliances built over decades. As NATCO's reputation for delivering complex products grows, they become the partner of choice for companies looking to enter difficult-to-manufacture generic markets. This network effect should strengthen over time.

Regulatory expertise keeps deepening. Each successful FDA approval, each won patent challenge, adds to NATCO's institutional knowledge. In an industry where regulatory success rates are low and declining, NATCO's accumulated expertise becomes increasingly valuable. They've shown they can navigate not just Indian and US regulations but complex international frameworks.

The financial strength to weather volatility has never been better. With minimal debt and strong cash generation during peak periods, NATCO can afford to be patient, waiting for the right opportunities rather than chasing marginal products. This financial flexibility is a luxury many competitors don't have.

Emerging market expansion offers additional growth vectors. Plans to expand into emerging markets like MENA, LATAM, and Southeast Asia could provide new revenue streams less dependent on single product launches. These markets often have less competition for complex generics and growing demand for affordable oncology treatments.

The Bear Case: Structural Challenges and Cyclical Headwinds

Bears point to fundamental vulnerabilities in NATCO's model. The dependence on a few blockbuster products creates extreme volatility. The Q3FY25 results showing revenue decline from Rs 795.6 crore to Rs 651.1 crore and profit falling from Rs 212.7 crore to Rs 132.4 crore year-over-year demonstrate how quickly fortunes can reverse when key products face competition.

The regulatory environment is becoming increasingly challenging. The U.S. Food and Drug Administration (FDA) inspected your drug manufacturing facility, Natco Pharma Limited, FEI 3004540906, at Kothur Village Rangareddy, Telangana, India, from October 9 to 18, 2023. This warning letter summarizes significant violations of Current Good Manufacturing Practice (CGMP) regulations for finished pharmaceuticals. FDA warning letters can delay product approvals and damage reputation, potentially destroying value built over years.

Patent strategies are evolving to close the loopholes NATCO has exploited. Pharmaceutical companies are becoming more sophisticated in their patent filings, making it harder to find vulnerabilities. They're also more willing to settle early with generic challengers, reducing the potential for windfall profits from successful challenges.

Competition in complex generics is intensifying. As the rewards for successful complex generic launches have become apparent, more companies are building capabilities in this space. Chinese and other Indian companies are investing heavily in complex manufacturing capabilities, potentially eroding NATCO's competitive advantages.

The partnership model, while reducing risk, also limits upside. When NATCO shares profits with partners, they capture only a fraction of the value they create. As the company matures, investors might question whether they should own NATCO or the larger partners who capture more of the economic value from successful launches.

Key person risk remains significant. While the transition from V.C. to Rajeev Nannapaneni has been successful so far, the company remains heavily dependent on a small group of decision-makers. The loss of key executives or scientists could significantly impact NATCO's ability to identify and execute on opportunities.

Market saturation in core therapeutic areas poses long-term challenges. As more oncology drugs go generic and biosimilars enter the market, the opportunity set for high-margin complex generics may shrink. NATCO will need to either expand into new therapeutic areas or accept lower returns on investment.

The cyclical nature of the business makes valuation difficult. How do you value a company whose earnings can swing 80% quarter to quarter? Traditional metrics like P/E ratios become less meaningful when earnings are so volatile. This valuation challenge may permanently constrain NATCO's multiple, regardless of operational success.

The Verdict: A Unique Risk-Reward Profile

NATCO represents neither a defensive pharmaceutical investment nor a growth story in the traditional sense. It's a specialized vehicle for investors who understand and can tolerate extreme volatility in exchange for the potential for extraordinary returns during successful product launches.

The bull case ultimately rests on NATCO's proven ability to identify and capture value from complex generic opportunities. The bear case centers on the sustainability and repeatability of this model in an evolving competitive and regulatory landscape. Both perspectives have merit, making NATCO one of the most interesting and controversial investments in the pharmaceutical sector.

XII. Looking Forward: The Next Chapter

As NATCO navigates the post-Revlimid landscape, the company stands at a critical inflection point. The next five years will determine whether NATCO's model of selective excellence can sustain itself in an increasingly competitive global pharmaceutical market, or whether the company needs to evolve its strategy for a new era.

The acquisition of Dash Pharmaceuticals LLC in the US in 2021 signals NATCO's ambition to move closer to end markets. This isn't just about having a US presence—it's about building direct relationships with customers, understanding market dynamics firsthand, and potentially capturing more value from successful launches. The question is whether NATCO can build commercial capabilities to match their technical excellence.

NATCO Pharma files FY2024-25 annual report; 42nd AGM on September 25, 2025 via VC. Launched bosentan TFOS 32mg (generic Tracleer) in US with 180-day exclusivity demonstrates the company continues to execute on its core strategy. The 180-day exclusivity on Bosentan, while not Revlimid-scale, shows NATCO still has the ability to win first-to-file positions on complex products.

The biosimilars opportunity represents both promise and peril. Biosimilars—generic versions of biological drugs—offer massive market opportunities but require different capabilities than small molecule generics. NATCO must decide whether to build these capabilities organically, acquire them, or partner with companies that already have them. The wrong choice could either constrain growth or drain resources.

The China+1 strategy beneficiary position could accelerate as global pharmaceutical companies look to diversify supply chains away from China. NATCO's established manufacturing capabilities and regulatory track record position them well to capture this business. However, they'll face competition from other Indian companies with similar aspirations.

Next-generation complex generics are becoming even more complex. As pharmaceutical innovation shifts toward personalized medicine, gene therapies, and other advanced modalities, the definition of "complex generic" is evolving. NATCO must continually upgrade its capabilities to stay at the forefront of generic pharmaceutical complexity.

Succession planning and institutionalization remain critical challenges. While Rajeev Nannapaneni has successfully taken the reins, building the next layer of leadership is essential. NATCO needs to develop institutional capabilities that transcend individual brilliance, creating systems and processes that can identify and execute opportunities regardless of who's in charge.

The regulatory landscape continues to evolve in ways that could help or hinder NATCO. Proposals for drug pricing reform in the US, changes to patent law, and evolving biosimilar regulations all create both opportunities and threats. NATCO's ability to anticipate and adapt to these changes will determine their success.

The company has applied for an Abbreviated New Drug Application (ANDA) for a generic version of Tabrecta (Capmatinib hydrochloride), a drug used to treat metastatic non-small cell lung cancer (NSCLC). Natco Pharma's recent submission to the USFDA for a generic version of Tabrecta is a bold move that could have significant financial implications for the company. This filing demonstrates NATCO continues to pursue high-value oncology opportunities, maintaining focus on their core strength.

The domestic market evolution offers untapped potential. As India's healthcare infrastructure improves and insurance coverage expands, the domestic market for complex generics should grow. NATCO's reputation and relationships position them well to capture this growth, potentially reducing dependence on export markets.

Can NATCO maintain its David vs. Goliath edge at scale? This is perhaps the most important question facing the company. The strategies that worked for a small, nimble challenger may not work for an established player. NATCO must evolve while maintaining the entrepreneurial spirit and risk-taking ability that drove their success.

The partnership model may need refinement. As NATCO's capabilities and reputation grow, they may be able to capture more value from successful launches. Renegotiating partnership terms or selectively going alone on certain products could improve economics, but would also increase risk.

Environmental, Social, and Governance (ESG) considerations are becoming increasingly important. NATCO's mission of expanding access to affordable medicines provides strong social credentials, but they'll need to articulate and demonstrate their ESG commitment more clearly to attract certain investors.

The artificial intelligence and machine learning revolution in drug discovery and development could be a game-changer. NATCO must decide how to leverage these technologies—whether for identifying patent vulnerabilities, optimizing manufacturing processes, or accelerating regulatory submissions.

XIII. Recent News & Developments

The most recent quarters have demonstrated both NATCO's continued execution excellence and the inherent volatility of their business model. Revenue stood at ₹1,371 crore, marking a 32.1% year-on-year (YoY) growth. On a quarter-on-quarter (QoQ) basis, revenue grew by 5.7% from ₹1,297.1 crore. The company posted a net profit of ₹676.5 crore, reflecting a substantial increase of 81.2% YoY. Sequentially, net profit rose by 10.6% from ₹604.9 crore in Q1 FY24-25.