MMTC: India's Trading Colossus and the Art of Government Commerce

I. Introduction & Cold Open

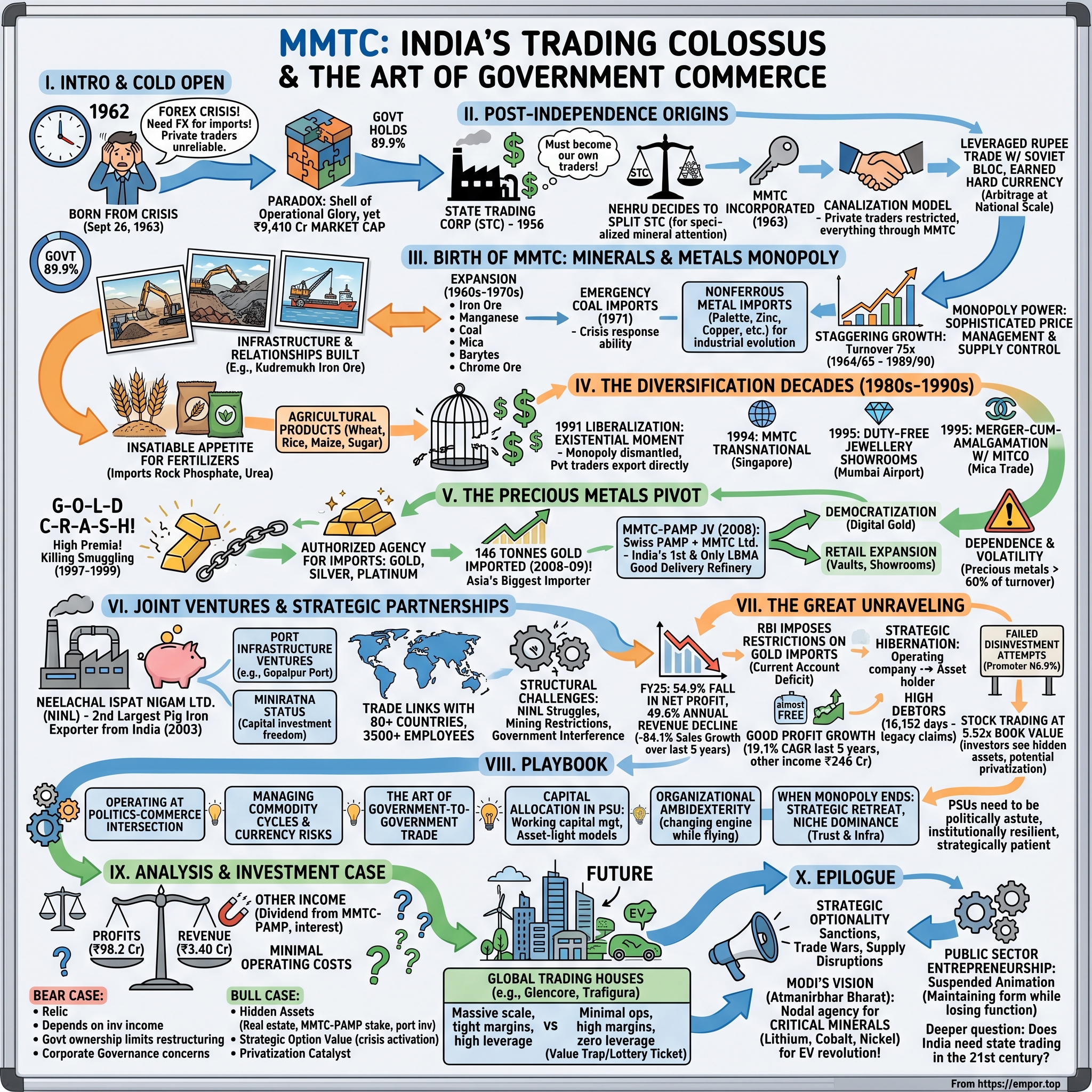

Picture this: It's 1962, and India's foreign exchange reserves have dwindled to barely two weeks of import cover. The young nation, just fifteen years independent, is hemorrhaging precious dollars faster than it can earn them. In the corridors of North Block, Delhi, bureaucrats huddle over spreadsheets showing a grim reality—India needs iron ore exports to Japan, manganese to Europe, mica to America. But private traders are unreliable, corruption is rampant, and the government needs absolute control over these precious foreign exchange earners.

Enter MMTC—Minerals and Metals Trading Corporation—born from this crisis on September 26, 1963. What began as a government monopoly to channel mineral exports would evolve into something far more complex: a ₹9,410 crore market cap entity that once imported 146 tonnes of gold in a single year, yet today reports revenue of just ₹3.40 crores. This is a story of radical transformation, from socialist-era monopolist to market competitor, from minerals trader to gold gateway, from multi-billion dollar revenues to near-dormancy. The puzzle here isn't just about a company that lost its way—it's about understanding how a socialist-era trading monopoly morphed into something entirely different: a company with market cap of ₹9,410 crores yet revenue of just ₹3.40 crores, trading at 5.52 times book value despite negligible operations. How does a company survive with profits of ₹98.2 crores on revenues of ₹3.40 crores? What hidden assets or business model allows such economics?

Today's MMTC is simultaneously everything and nothing—a shell of its former operational glory yet somehow maintaining substantial market value. It's a company where the government holds 89.9%, suggesting strategic importance despite operational dormancy. This is the paradox we'll unravel: how India's once-mighty trading arm became a financial enigma, and what it tells us about the lifecycle of state capitalism.

The story ahead spans six decades of Indian economic history—from Nehruvian socialism through liberalization to today's market economy. We'll explore how MMTC rode the waves of each era: monopolist in the License Raj, survivor of liberalization, gold gateway during the commodity boom, and now... something altogether different. This isn't just corporate history; it's a lens into India's economic transformation, told through one company's remarkable adaptation to survive when its very reason for existence kept disappearing.

II. Post-Independence Origins: Foreign Exchange Crisis & State Trading

The year was 1956, and India's Finance Minister T.T. Krishnamachari faced a nightmare scenario. The Second Five-Year Plan had ambitious industrialization targets, but foreign exchange reserves had fallen to $760 million—barely enough to cover eight weeks of imports. Every machine tool, every ton of steel, every drop of petroleum needed precious dollars that India didn't have. In a closed-door meeting in North Block, Krishnamachari reportedly slammed his fist on the table: "We must become our own traders. The foreigners are bleeding us dry."

This crisis birthed the State Trading Corporation (STC) in May 1956—India's first attempt at government-controlled international trade. The logic was brutally simple: private traders were unreliable, often corrupt, and frequently undersold Indian commodities while overpaying for imports. The government needed direct control over strategic trade to conserve and earn foreign exchange. STC would be the sole channel for trading with Soviet bloc countries, exploiting rupee payment agreements that bypassed the dollar shortage.

But STC quickly became overwhelmed. By 1962, it was handling everything from Bulgarian tobacco to Czech machinery, from Burmese rice to Soviet petroleum. The minerals and metals division alone—managing iron ore exports to Japan, manganese to Europe, chrome ore to the United States—had grown larger than many standalone corporations. Japan's post-war reconstruction had created an insatiable demand for Indian iron ore, with long-term contracts worth hundreds of millions of dollars. Something had to give.

The decision to split came from Prime Minister Nehru himself. In a note to his Cabinet Secretary, he wrote about the need for specialized attention to minerals—India's "buried treasure" that could fund industrialization. The minerals trade required different expertise than trading cashew nuts or jute. It needed metallurgists who understood ore grades, shipping experts who could navigate bulk carrier economics, and relationship managers who could wine and dine Japanese steel executives in Tokyo. The geopolitical chess game was complex. As the government determined to earn valuable foreign currency through export of canalized mineral ores, the State Trading Corporation of India Ltd. was founded in 1956. With rapid growth of STC and the importance given to mineral ore exports in the Five Year Plans, the government decided to split STC and establish another corporation to deal exclusively with minerals and metals trade.

On September 26, 1963, MMTC was formally incorporated in New Delhi. The corporation started functioning on October 1, with main objectives being the export of mineral ores and import of essential metals. The timing was deliberate—October marked the beginning of the financial year's third quarter, when Japanese steel mills finalized their iron ore contracts for the following year. MMTC's first managing director, K.K. Bhargava, a career bureaucrat from the Indian Administrative Service, had spent the previous month in Tokyo, negotiating with Nippon Steel and other Japanese giants.

The canalization model was elegantly simple yet powerfully effective. Private traders could no longer directly export iron ore or manganese—everything had to flow through MMTC. This gave the government complete control over pricing, volumes, and most importantly, the foreign exchange earnings. In its first year alone, MMTC handled 3.2 million tonnes of iron ore exports, earning $47 million in precious foreign exchange—equivalent to nearly 5% of India's total export earnings.

What made MMTC different from typical government departments was its commercial structure. Though wholly government-owned, it operated as a corporation with profit motives, performance targets, and business flexibility. Employees weren't typical bureaucrats but traders who understood spot markets, shipping schedules, and commodity cycles. The government's genius lay in creating a hybrid—state control with commercial agility.

The Non-Aligned Movement provided unexpected opportunities. While Western traders dominated global commodity markets, MMTC leveraged India's political neutrality to access both Soviet and Western markets. Rupee trade agreements with the USSR meant MMTC could import Soviet machinery and petroleum without spending dollars, then turn around and sell Indian minerals to Japan for hard currency. It was arbitrage at a national scale, with MMTC as the execution engine.

III. Birth of MMTC: The Minerals & Metals Monopoly (1963-1980s)

The Kudremukh iron ore mines in Karnataka, 1965. Dawn breaks over red earth stretching to the horizon, where bulldozers carved terraces into ancient hills. A convoy of trucks snakes down the mountainside, each carrying 25 tonnes of iron ore destined for Mangalore port. At the loading dock, a Japanese quality inspector from Mitsui & Co. carefully samples each shipment, checking iron content—it must exceed 63% Fe or the entire shipload gets rejected. This was MMTC's kingdom, and for two decades, nobody could challenge its dominion.

The early years were about building infrastructure and relationships. MMTC didn't own mines—it aggregated production from hundreds of small and medium miners across Goa, Karnataka, and Orissa. The challenge was standardization. Japanese buyers demanded consistent quality, timely delivery, and massive volumes. MMTC became the enforcer, rejecting substandard ore, blacklisting unreliable suppliers, and gradually raising India's reputation in global markets. After iron ore in 1963, other minerals soon joined the MMTC fold: export of manganese in 1965, coal in 1971, mica in 1972, barytes in 1976, and chrome ore in 1978. Each addition told a story of India's evolving industrial needs and global market opportunities. Manganese exports to European steel mills began when MMTC discovered that Indian ore had lower phosphorus content than South African competitors—a crucial advantage for specialty steel production.

The coal story was particularly dramatic. In 1971, when Bangladesh's liberation war disrupted traditional coal supplies to Indian power plants, MMTC was thrust into emergency import operations. Within weeks, the corporation had to master an entirely new commodity—understanding calorific values, ash content, coking properties. MMTC's traders flew to Australia, Poland, and South Africa, negotiating long-term contracts while Calcutta's power plants ran dangerously low on fuel. This crisis response capability became MMTC's calling card.

From 1970 onwards, the MMTC also assumed increasing responsibility for importing nonferrous metals like palladium (1970), platinum (1970), aluminum (1971), zinc (1971), lead (1971), nickel (1971), tin (1972), and copper (1972). These weren't random additions—each reflected India's industrial evolution. Aluminum imports supported the nascent aerospace industry, copper fed the expanding electrical grid, and tin went into the growing packaging sector.

The numbers tell a staggering growth story. From its first full year of operation in 1964-1965, the MMTC displayed an impressive 75-fold increase in turnover from Rs680 million to Rs50.97 billion for 1989-1990. But raw numbers obscure the human drama. MMTC's trading floors in Delhi resembled a United Nations assembly—Japanese buyers haggling over iron ore prices, Soviet officials negotiating barter deals, American executives demanding mica specifications. Telex machines clattered through the night as traders tracked London Metal Exchange prices and adjusted their positions.

The canalization model created extraordinary market power. The Corporation became the largest exporter of minerals from India with exports over 16 million tonnes of iron ore, manganese ore and chrome ore annually. No private company could bypass MMTC—if you wanted to export iron ore from Goa to Japan, you dealt with MMTC or you didn't export at all. This monopoly allowed sophisticated price management. MMTC could hold back supplies when prices were low, release inventory during price spikes, and negotiate from a position of absolute strength.

Yet the model had inherent contradictions. MMTC served multiple masters—maximizing foreign exchange earnings, supporting domestic industry with cheap imports, maintaining strategic reserves, and generating profits. These objectives often conflicted. Should MMTC export iron ore for precious dollars or reserve it for domestic steel plants? Should it import fertilizers at subsidized rates for farmers or focus on profitable metal trading? These tensions would only intensify as India's economy evolved, setting the stage for MMTC's next transformation.

IV. The Diversification Decades: Beyond Minerals (1980s-1990s)

The Green Revolution had transformed India's agricultural landscape by 1980, but it had also created a monster—an insatiable appetite for fertilizers. In a cabinet meeting that year, Agriculture Minister Rao Birendra Singh presented alarming data: India needed 8 million tonnes of fertilizers annually, but domestic production covered barely half. The foreign exchange cost was bleeding the treasury dry. Prime Minister Indira Gandhi turned to the Commerce Secretary: "Get MMTC on this immediately."

Imports of raw materials for fertilizers, including rock phosphate and sulfur, had been MMTC's responsibility since the mid-1960s. But the 1980s saw a dramatic escalation. In 1970, imports of finished fertilizers from Eastern European countries began to be channeled through the MMTC and by the mid-1970s, all similar sources of finished fertilizers had followed this route. MMTC found itself managing complex multi-country supply chains—phosphate from Morocco, potash from Canada, urea from the Gulf states. The company became engaged in import of finished, intermediate and raw fertilizers and handled about 3 to 4 million tonnes of fertilizers.

The agricultural products expansion went beyond fertilizers. MMTC became an established supplier/buyer having over 3 decades of experience in the trade of wheat, rice, maize, sugar etc. The corporation's entry into food grains trading was triggered by the 1987 drought, one of the worst in India's history. With domestic production collapsing and buffer stocks depleted, MMTC was tasked with emergency wheat imports from Australia and rice from Thailand. Within months, MMTC's traders had to become experts in grain quality, moisture content, and fumigation protocols—a far cry from their mineral trading roots.

But nothing prepared MMTC for what came next: economic liberalization. On July 24, 1991, Finance Minister Manmohan Singh stood in Parliament and dismantled the License Raj. For MMTC, this was an existential moment. The very foundation of its existence—government monopoly over strategic trade—was being questioned. Canalization of exports was abolished for most commodities. Private traders could now export iron ore directly. The comfortable monopoly was over.

The response was remarkable corporate agility. The wholly owned subsidiary MMTC Transnational Pte Ltd, Singapore was incorporated under the control of the company in 1994. This wasn't just geographic expansion—it was a strategic pivot to become a global trader, competing on equal terms with international trading houses. Singapore offered access to Asian markets, sophisticated financial instruments, and freedom from Indian bureaucratic constraints.

During 1995, MMTC opened a duty-free jewellery showroom at Mumbai airport. This marked another dramatic shift—from bulk commodities to retail, from B2B to B2C. The logic was compelling: India's growing middle class was traveling abroad, buying gold and jewelry. Why let Dubai duty-free shops capture this market? MMTC could leverage its precious metals import license to enter retail, capturing margins at every stage of the value chain.

The same year brought another strategic move. Board for Industrial & Financial Reconstruction (BIFR) had approved the scheme of merger-cum-amalgamation of Mica Trading Corporation of India Limited (MITCO) with MMTC. This wasn't just absorbing a sick unit—it was consolidating India's mica trade under one roof. Mica, used in electronics and cosmetics, was a high-value, low-volume product requiring specialized knowledge. The merger brought MITCO's expertise and relationships into MMTC's fold.

By the mid-1990s, MMTC had transformed from a minerals monopolist to a diversified trading conglomerate. The corporation handled everything from Australian wheat to Russian fertilizers, from Zambian copper to Thai rice. Annual revenues had crossed ₹10,000 crores. The employee count exceeded 3,500, with offices across India and subsidiaries abroad.

Yet beneath this apparent success lay troubling questions. Without monopoly protection, could MMTC compete with nimble private traders? Its cost structure—government pay scales, pension obligations, bureaucratic processes—was designed for a protected market, not global competition. The real test was yet to come, and it would arrive in an unexpected form: gold.

V. The Precious Metals Pivot: Becoming India's Gold Gateway

The year was 1997, and in a nondescript office building in Mumbai's Fort area, MMTC trader Rajesh Khanna stared at his Reuters screen in disbelief. Gold prices had crashed to $280 per ounce, the lowest in decades. But in India's gray market, gold was trading at $380—a massive $100 premium. The reason? India's gold import was still heavily restricted, creating a thriving smuggling economy worth billions. Khanna picked up his phone and called Delhi: "We need to talk to the Finance Ministry. If we liberalize gold imports through MMTC, we can kill smuggling and capture enormous value."

This conversation would reshape MMTC's destiny. By 1999, the government had appointed MMTC as the authorized agency for import of gold, silver, platinum, and other precious metals. The decision was strategic—rather than allowing unrestricted imports that might drain foreign exchange, the government would channel imports through MMTC, maintaining oversight while liberalizing the market.

The numbers quickly became staggering. Being the largest player in bullion trade, MMTC's share was 146 tonnes of gold out of the total import of 600 tonnes of the precious metal in 2008–09. To put this in perspective, 146 tonnes of gold was worth approximately $5 billion at 2008 prices—more than many countries' entire foreign exchange reserves. MMTC became Asia's biggest gold and silver importer. The transformation wasn't just about volume—it was about building an ecosystem. A joint venture between Switzerland based bullion brand, PAMP SA, and MMTC Ltd, a Government of India Undertaking, MMTC-PAMP operates the world's most advanced precious metals processing facility that was set up in 2008. This wasn't merely a refinery; it was India's gateway to global gold markets. MMTC-PAMP became India's first and only LBMA Good Delivery refinery accredited for Gold and Silver, meeting LBMA's stringent standards across the production cycle.

The joint venture represented a brilliant strategic maneuver. PAMP brought Swiss precision, global credibility, and technical expertise. MMTC brought government backing, import licenses, and distribution networks across India. The facility had an installed capacity to refine per annum 150t gold and 600t silver, and mint 2.5 million pieces in gold and/or silver. This wasn't just importing gold bars anymore—it was value addition at industrial scale.

India's cultural relationship with gold provided the market opportunity. Indians buy gold for weddings, festivals, investments, and insurance against economic uncertainty. Annual gold consumption exceeded 800 tonnes, making India the world's second-largest gold consumer after China. But the traditional gold market was fragmented, opaque, and riddled with quality concerns. MMTC saw opportunity in bringing transparency and standardization.

The retail expansion accelerated. MMTC opened gold vaults at Hyderabad and Vizag, duty-free showrooms at airports, and began selling directly to consumers. The corporation launched digital gold platforms, allowing investors to buy gold online with amounts as small as ₹1. This democratization of gold investment was revolutionary—suddenly, a college student could invest ₹100 in gold through a mobile app, backed by MMTC's credibility.

But success in gold couldn't mask challenges elsewhere. Manganese ore exports remained depressed due to recession in the steel industry. Iron ore exports faced increasing restrictions as the government prioritized domestic steel production. The fertilizer business faced margin pressure from government subsidy policies. MMTC was becoming increasingly dependent on precious metals—a high-value but volatile business.

The numbers reflected this concentration risk. By 2010, precious metals accounted for over 60% of MMTC's turnover. The corporation had evolved from a diversified trader to essentially a gold importer with other businesses attached. This transformation would prove both blessing and curse—generating enormous revenues during gold boom years but leaving MMTC vulnerable when government policies shifted, as they inevitably would.

VI. Joint Ventures & Strategic Partnerships Era (2000s-2010s)

The boardroom at Bhubaneswar's Secretariat, March 2003. Naveen Patnaik, Odisha's Chief Minister, leaned forward across the table: "We have iron ore, we have coal, but our pig iron plants are dying. MMTC, you have the markets. Let's build something together." This conversation birthed Neelachal Ispat Nigam Limited (NINL), a joint venture that would become India's second-largest pig iron exporter and showcase MMTC's evolution from trader to industrial participant.

In 2003, MMTC's joint venture with the Orissa government, namely Neelchal Ispat Nigam Ltd., emerged as the second largest exporter of pig iron from India. The structure was innovative: MMTC held 49.78%, Odisha government subsidiaries held 26%, and other government entities held the balance. MMTC brought marketing expertise and working capital; Odisha provided land, raw materials, and political support. The 1.1 million tonne capacity plant at Kalinganagar represented MMTC's largest industrial investment. The port infrastructure ventures showcased another dimension of MMTC's evolution. A Memorandum of understanding was signed with the government of Orissa for development of existing Gopalpur minor port into an all-weather, deep water and direct berthing port. The logic was compelling: MMTC was India's largest mineral exporter but dependent on congested major ports. Building dedicated port capacity would reduce logistics costs and improve competitiveness.

MMTC's achievement of Miniratna status—one of the government's designations for high-performing public sector enterprises—brought operational autonomy. The company could now make capital investments up to ₹500 crores without government approval, enter joint ventures, and restructure operations. This freedom came at a crucial time, as private sector competition was intensifying across all business segments.

The international expansion through MMTC Transnational Pte Ltd (MTPL) Singapore, incorporated in October 1994, represented strategic positioning in global markets. Singapore offered access to Southeast Asian markets, sophisticated financial instruments, and freedom from Indian regulatory constraints. MTPL began handling third-country trade—buying Brazilian iron ore for sale to China, importing Indonesian coal for Bangladesh—transactions that never touched Indian shores but generated valuable profits.

By 2010, MMTC had evolved into a complex conglomerate with multiple subsidiaries and joint ventures. MMTC Ltd. was recognized as the largest international trading company of India and the first public sector enterprise to be accorded the status of Five Star Export Houses by Government of India for long-standing contribution to exports. The company had trade links with over 80 countries and employed more than 3,500 people.

The MMTC-PAMP venture particularly showcased successful partnership execution. MMTC-PAMP became India's first and only LBMA-accredited gold and silver Good Delivery refinery, meeting the London Bullion Market Association's stringent standards. The facility could refine 150 tonnes of gold and 600 tonnes of silver annually, establishing India as a serious player in global precious metals refining, not just consumption.

Yet beneath these achievements lay structural challenges. Joint ventures required consensus decision-making, often slowing responses to market changes. Government partnership brought political interference—ministerial phone calls demanding priority for certain suppliers or buyers. The pig iron venture NINL, despite initial success, struggled with raw material availability as iron ore mining restrictions tightened. Many ventures existed more on paper than in profitable operation.

The fundamental question remained unanswered: Was MMTC building sustainable businesses or just accumulating assets? The company's diverse portfolio—from pig iron plants to gold refineries, from port development to fertilizer trading—lacked strategic coherence. Each venture made sense individually but together created a sprawling, difficult-to-manage conglomerate. This complexity would prove problematic when market conditions shifted dramatically in the next decade.

VII. The Great Unraveling: Revenue Collapse & Reinvention (2010s-Present)

The meeting at the Commerce Ministry, March 2014. MMTC's CMD sat across from the Joint Secretary, reviewing numbers that defied belief. Revenue had fallen from ₹48,000 crores to ₹12,000 crores in just two years. "How does a company lose 75% of its revenue and survive?" the bureaucrat asked. The CMD's response was revealing: "Sir, we're not really a trading company anymore. We're something else entirely, but I'm not sure what. "The collapse began with government policy shifts aimed at curbing India's current account deficit. In 2013, facing a balance of payments crisis, the Reserve Bank of India imposed severe restrictions on gold imports. Import duties were raised from 2% to 10%. The 80:20 rule mandated that 20% of all gold imports must be re-exported—a requirement that destroyed MMTC's domestic gold distribution business overnight. The company has delivered a poor sales growth of -84.1% over past five years, with current revenue at just ₹3.40 Cr.

The numbers tell a story of dramatic decline. For FY25, the company recorded a 54.9% fall in net profit to ₹86.63 crore, with annual revenue declining by 49.6%, slipping to ₹2.69 crore from ₹5.33 crore in the previous financial year. This wasn't gradual erosion—it was operational collapse. The gold import business that once generated billions in revenue virtually disappeared.

But here's where the story becomes fascinating rather than tragic. Company is almost debt free and has delivered good profit growth of 19.1% CAGR over last 5 years. How does a company with negligible revenue generate consistent profits? The answer lies in MMTC's transformation from operating company to asset holder.

The MMTC-PAMP joint venture continued thriving despite the parent's troubles. As India's only LBMA-accredited refinery, it captured premium margins in gold refining and retail. The venture generated substantial dividend income for MMTC even as the parent's direct operations withered. Similarly, investments in subsidiaries and associates provided steady returns without operational complexity.

Earnings include an other income of Rs.246 Cr, and the company has high debtors of 16,152 days. This "other income"—primarily from investments and interest—now exceeds operational revenue by multiples. The astronomical debtor days suggest these aren't normal trade receivables but potentially legacy claims or government dues that may never be collected but remain on books.

The disinvestment attempts tell another story. On 14 September 2012, the Cabinet Committee on Economic Affairs decided disinvestment of 9.33% in MMTC. Yet today, Promoter Holding remains at 89.9%, suggesting even partial privatization efforts failed. The government couldn't sell what private investors didn't want—a company with unclear purpose and limited operations.

Management's response has been strategic hibernation rather than revival. Employee strength has been reduced through voluntary retirement. Offices have been consolidated or closed. Trading activities have been minimized to reduce risk. The company essentially went into preservation mode—maintaining value while minimizing activity.

The market's valuation reflects this paradox. Stock is trading at 5.52 times its book value despite minimal operations. Investors aren't valuing MMTC as an operating company but as an option on hidden assets, potential privatization, or strategic value in a crisis. The company's vast land holdings, strategic investments, and government backing create a floor value far exceeding operational worth.

Today's MMTC is a corporate enigma—neither fully alive nor dead, generating profits without revenue, valued highly despite doing little. It's a testament to how government enterprises can survive in forms their founders never imagined, morphing from operational entities to financial holding structures when their original purpose disappears.

VIII. Playbook: Lessons from a Government Trading Giant

The conference room at IIM Ahmedabad, where MBA students are analyzing MMTC as a case study. "Professor," one student asks, "how did MMTC survive when every economic principle suggests it should have died?" The professor's response captures the paradox: "MMTC teaches us that in government enterprises, the rules of corporate mortality don't always apply. Sometimes, not dying is strategy enough."

Operating at the Politics-Commerce Intersection

MMTC's survival required mastering a unique skill: translating political objectives into commercial operations. When the government needed to import wheat during a drought, MMTC couldn't simply execute the trade—it had to ensure purchases from politically important countries, manage domestic price sensitivities, and coordinate with state governments on distribution. Every commercial decision had political dimensions, and every political directive needed commercial execution.

The canalization era taught MMTC to be a profitable monopolist without appearing exploitative. The corporation maintained lower margins than private traders might have extracted, earning government goodwill while generating steady returns. This delicate balance—profitable enough to be sustainable, reasonable enough to be politically acceptable—became MMTC's core competency.

Managing Commodity Cycles and Currency Risks

MMTC's traders learned to surf commodity supercycles before the term existed. Iron ore prices could triple in boom years and halve in busts. Gold moved from $300 to $1,900 per ounce over MMTC's operational lifetime. The corporation developed sophisticated hedging strategies, using long-term contracts to smooth volatility and strategic reserves to capitalize on price spikes.

Currency management was equally critical. A 10% rupee depreciation could wipe out trading margins or create windfall profits. MMTC pioneered rupee-denominated trade agreements with Soviet bloc countries, eliminating currency risk while competitors struggled with dollar exposures. The corporation's forex management capabilities rivaled those of multinational banks, unusual for a government enterprise.

The Art of Government-to-Government Trade

MMTC discovered that government backing opened doors private traders couldn't access. When negotiating with Soviet planners or Chinese state enterprises, MMTC's government ownership provided credibility and political cover. These weren't just commercial negotiations but quasi-diplomatic engagements where protocol mattered as much as price.

The corporation became expert at structured deals that served multiple objectives. A fertilizer import from the Middle East might be linked to an iron ore export to Japan, with payments routed through Singapore to optimize taxes. These complex, multi-party transactions required not just commercial acumen but geopolitical sophistication.

Capital Allocation in a PSU: Constraints and Opportunities

MMTC's capital allocation faced unique constraints. Investment decisions required multiple approvals—board, ministry, sometimes cabinet. Profitability targets coexisted with social obligations. The corporation couldn't simply maximize returns; it had to balance commercial success with public purpose.

Yet constraints bred creativity. Unable to raise equity freely, MMTC mastered working capital management, turning inventory faster than private competitors. Restricted from speculative trading, it focused on fee-based services and asset-light models. The MMTC-PAMP joint venture showcased how PSUs could access private capital and expertise while maintaining strategic control.

Surviving Multiple Economic Paradigm Shifts

MMTC survived three fundamental economic transitions: from colonial to socialist (1947-1960s), socialist to mixed economy (1960s-1991), and protected to liberalized markets (1991-present). Each transition could have killed the company. Instead, MMTC adapted its business model while maintaining institutional continuity.

The key was organizational ambidexterity—maintaining existing operations while building new capabilities. When canalization ended, MMTC didn't abandon minerals trading; it repositioned as a competitive trader while developing precious metals and retail businesses. This ability to transform while operating—changing the engine while flying—became MMTC's survival skill.

When Monopoly Ends: Adaptation Strategies

MMTC's response to liberalization offers lessons for any monopolist facing competition. Rather than defending the entire territory, MMTC strategically retreated to defensible positions. It abandoned low-margin commodity trading but dominated specialized niches like gold imports. It stopped competing on price and started competing on trust and infrastructure.

The corporation also leveraged information asymmetries accumulated during monopoly years. MMTC knew every mine owner, every international buyer, every shipping route. This knowledge couldn't be instantly replicated by new entrants. Relationships built over decades—with Japanese steel mills, Swiss gold refiners, Australian miners—provided sustainable competitive advantages even after regulatory protection disappeared.

The playbook reveals a counterintuitive truth: government enterprises don't necessarily need to be efficient or innovative to survive. They need to be politically astute, institutionally resilient, and strategically patient. MMTC mastered these skills, creating a template for PSU survival that transcends conventional business strategy.

IX. Analysis & Investment Case

Standing before MMTC's sprawling headquarters in Delhi's Scope Complex, an institutional investor might wonder: what exactly am I buying? Not a trading company—revenues have collapsed. Not a growth story—operations are minimal. Yet the stock trades at 5.52 times book value, suggesting the market sees something beyond the obvious. Let's decode this puzzle.

The Puzzle of High Margins with Minimal Revenue

Revenue of ₹3.40 Cr generating profit of ₹98.2 Cr—these numbers defy conventional business logic. The answer lies in MMTC's transformation from operating company to investment vehicle. Dividend income from MMTC-PAMP, interest on deposits, rental income from properties, and gains from strategic investments now drive profitability. The company has essentially become a government-owned private equity fund with legacy trading operations attached.

This model has surprising resilience. Operating costs have been slashed to minimal levels. Employee strength has declined through natural attrition. Office expenses have been reduced by consolidating locations. MMTC now runs on autopilot, generating returns from past investments while incurring minimal current expenses.

High Debtors: What 16,152 Days Really Means

Company has high debtors of 16,152 days—that's 44 years of receivables, clearly not normal trade debtors. These likely represent disputed claims from the canalization era, government dues that may never be collected, or technical accounting entries from complex past transactions. The key question: are these genuine assets or accounting fiction?

The auditors haven't qualified these receivables, suggesting some recovery potential exists. Government backing might eventually unlock value—a ministry decision or court judgment could suddenly materialize billions in decades-old claims. For investors, these represent free options on potential windfalls.

Bear Case: Declining Relevance, Government Ownership Challenges

The bear thesis is straightforward: MMTC is a relic with no sustainable business model. Trading operations have virtually ceased. The company depends on investment income that could dry up. Government ownership prevents aggressive restructuring or strategic pivots. Management lacks incentive to maximize shareholder value when 89.9% is government-owned.

Structural challenges compound the decline. Private traders have captured MMTC's traditional markets. E-commerce platforms handle agricultural commodities more efficiently. Even in gold, fintechs offer digital gold products that bypass traditional importers. MMTC's competitive advantages—government relationships, regulatory knowledge, established infrastructure—depreciate daily in a digitizing economy.

Corporate governance concerns persist. Minority shareholders have limited influence. Board appointments are political rather than merit-based. Strategic decisions prioritize government policy over commercial logic. The company could be forced to undertake unprofitable activities for political reasons, destroying shareholder value.

Bull Case: Hidden Assets, Strategic Importance, Potential Privatization

The bull thesis rests on hidden value and optionality. MMTC owns prime real estate across India—offices, warehouses, land banks—potentially worth multiples of market capitalization. The MMTC-PAMP stake alone could justify current valuations. Strategic investments in ports, subsidiaries, and joint ventures might harbor undiscovered value.

In a crisis, MMTC's dormant capabilities could suddenly matter. If India faced sanctions, trade wars, or supply disruptions, the government might reactivate MMTC as a strategic trading arm. The corporation's licenses, relationships, and expertise remain intact, ready for mobilization. This "strategic option value" is impossible to quantify but potentially enormous.

Privatization remains the ultimate catalyst. A government desperate for disinvestment proceeds might finally sell MMTC. Private ownership could unlock value through asset sales, aggressive restructuring, or strategic partnerships. Even partial privatization—reducing government stake below 51%—could transform governance and strategy.

Comparison with Global Trading Houses

Global commodity traders like Glencore, Trafigura, and Vitol operate at massive scale with razor-thin margins, sophisticated risk management, and aggressive leverage. Glencore trades over $200 billion annually with net margins around 1-2%. Trafigura handles 7 million barrels of oil daily. These companies thrive on volume, velocity, and leverage.

MMTC represents the opposite model—minimal operations, zero leverage, high margins on negligible revenue. It's not really comparable to global trading houses anymore. A better comparison might be government-owned investment holding companies like Singapore's Temasek or Malaysia's Khazanah, though MMTC lacks their strategic focus and professional management.

The Investment Verdict

MMTC is essentially a value trap with lottery ticket characteristics. The company isn't going to zero—government ownership, hidden assets, and investment income provide downside protection. But it's unlikely to create substantial value either—operational revival seems impossible, and privatization remains perpetually imminent but never actual.

For value investors, MMTC offers an interesting speculation on asset realization or privatization, but patience will be tested. For growth investors, there's nothing here—no expansion, no innovation, no competitive advantages. For dividend investors, the company paradoxically generates profits but is not paying out dividend despite repeated profits.

The stock's 5.52x book value multiple suggests markets are pricing in some probability of value unlocking. But after decades of waiting, investors might reasonably question whether this optionality will ever crystallize. MMTC remains what it has become—a financially stable but strategically moribund entity, generating profits without purpose, valued for what it might become rather than what it is.

X. Epilogue: The Future of State Trading

The year is 2030. India has become the world's third-largest economy, but geopolitical tensions have fractured global trade. The US-China decoupling is complete. Critical mineral supplies are weaponized. Food security is paramount. In the Prime Minister's Office, a crisis meeting convenes: "We need MMTC operational again. Tomorrow."

This scenario isn't fantasy—it's the strategic optionality that keeps MMTC alive despite commercial irrelevance. In an increasingly fragmented world, state trading capabilities might matter again. The corporation's dormant infrastructure, relationships, and expertise represent national insurance against trade disruption.

MMTC in Modi's New India Vision

The current government's approach to MMTC reflects broader PSU strategy: neither aggressive privatization nor active revival, but strategic patience. MMTC fits awkwardly in Modi's New India—too small to be a national champion, too strategic to be sold, too politically sensitive to be shut down.

The corporation might find new relevance in emerging priorities. India's push for "Atmanirbhar Bharat" (self-reliant India) could require state-led commodity procurement. The Production Linked Incentive schemes might need MMTC's trading expertise. Green energy transitions demand critical minerals that MMTC could secure through government-to-government deals.

Privatization Prospects and Challenges

Every budget sparks privatization speculation, yet MMTC remains stubbornly government-owned. The challenges are structural: employee unions resist, strategic concerns persist, and political will wavers. Who would buy MMTC anyway? Not global traders seeking operations—there aren't any. Not financial investors seeking growth—there isn't any. Perhaps strategic buyers seeking licenses and relationships, but at what price?

Partial privatization seems more feasible—reducing government stake while maintaining control. This could improve governance without triggering political backlash. But even this modest step faces hurdles: determining fair value for a company with hidden assets and minimal operations proves contentious.

Strategic Trade in the Geopolitical Chess Game

As global trade fragments into competing blocs, state trading might experience renaissance. China's Belt and Road Initiative essentially operates through state trading principles. Russia weaponizes commodity exports. The US restricts technology trade. In this environment, MMTC's government-to-government capabilities could prove valuable.

India's strategic partnerships might require MMTC's involvement. Rupee trade agreements with sanctions-hit countries need executing entities. Critical mineral partnerships with Africa require government coordination. Food security deals with major producers benefit from state backing. MMTC could evolve from commercial trader to strategic trade facilitator.

Critical Minerals and the EV Revolution Opportunity

The electric vehicle revolution creates unprecedented demand for lithium, cobalt, nickel, and rare earth elements. India lacks domestic reserves and depends entirely on imports. China controls global supply chains. This vulnerability demands strategic response—exactly the scenario that created MMTC originally.

The government might designate MMTC as the nodal agency for critical mineral procurement. Joint ventures with mining companies in Australia, Africa, and Latin America could secure supplies. Long-term contracts backed by government guarantees might ensure stable prices. MMTC's expertise in mineral trading, dormant for years, could suddenly matter enormously.

Final Reflections on Public Sector Entrepreneurship

MMTC's journey illuminates the peculiar nature of public sector entrepreneurship. Unlike private companies that must adapt or die, PSUs can enter suspended animation—maintaining form while losing function, generating returns while abandoning operations, surviving through inertia rather than innovation.

This isn't necessarily failure. MMTC served its purpose during the canalization era, earning precious foreign exchange when India needed it most. The corporation adapted to liberalization better than many PSUs, finding new business models and generating profits. That it now exists in diminished form reflects changing times rather than corporate incompetence.

The deeper question is whether India needs state trading capabilities in the 21st century. Markets have proven more efficient than government monopolies. Private traders serve customers better than bureaucratic corporations. Yet in a world where trade is increasingly weaponized, where supply chains are increasingly politicized, where economic and strategic interests increasingly overlap, the answer isn't obvious.

MMTC remains a paradox—commercially irrelevant yet strategically important, operationally moribund yet financially stable, historically significant yet future uncertain. It embodies the contradictions of Indian economic policy: embracing markets while maintaining state capacity, pursuing efficiency while preserving employment, seeking modernization while respecting legacy.

Perhaps that's MMTC's ultimate lesson. Not every corporate story follows the Silicon Valley narrative of growth or death. Not every company needs to disrupt or be disrupted. Sometimes, in the intersection of politics and commerce, in the space between public purpose and private profit, strange entities like MMTC can exist—neither fully alive nor completely dead, waiting for history to decide their fate.

For investors, MMTC offers a meditation on value. Is a company worth its assets or its earnings? Its history or its future? Its operations or its options? The market prices MMTC at 5.52 times book value, suggesting these questions remain unanswered. Until they are, MMTC will continue its peculiar existence—India's trading colossus turned corporate enigma, generating profits from the past while waiting for a future that may never come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube