MIDHANI: India's Strategic Metals Champion

I. Introduction & Cold Open

The furnace glows white-hot at 1,600 degrees Celsius. Inside, titanium slowly transforms from raw ore into an aerospace-grade alloy that will one day fly in the belly of a fighter jet. The technician monitoring the vacuum arc melting process at MIDHANI's Hyderabad facility has done this thousands of times, yet each melt remains critical—a single impurity could ground an entire squadron.

This scene plays out daily at Mishra Dhatu Nigam Limited, a company most Indians have never heard of, yet one whose products protect the nation's skies, power its nuclear submarines, and launch its satellites into space. In a world where advanced materials determine military superiority, MIDHANI stands as India's sole manufacturer of titanium alloys—a monopoly born not from market forces but from strategic necessity.

The fundamental question isn't just how a government-mandated metallurgy laboratory became a publicly-traded company worth ₹7,400 crores. It's how India, starting from virtually zero indigenous capability in special metals, built an institution that now supplies critical materials for everything from the Tejas fighter jet to the Agni missile system. This is a story of patient capital measured in decades, of learning from Soviet mentors while facing Western technology embargoes, and of the peculiar economics where paying three times the global price for domestic production makes perfect strategic sense. What makes special metals and superalloys so strategically critical? Consider that a modern fighter jet engine operates at temperatures exceeding 1,500°C—hot enough to melt most conventional metals. The turbine blades spinning at 10,000 RPM inside these infernos must maintain their structural integrity while enduring forces that would tear ordinary steel apart. Without titanium's unique strength-to-weight ratio and nickel superalloys' heat resistance, modern aerospace would simply not exist. Nations that cannot produce these materials domestically remain forever dependent on foreign suppliers—a vulnerability no serious military power can afford.

MIDHANI specializes in manufacturing a wide range of superalloys, titanium, special-purpose steels, and other special metals & alloys meeting international standards. Yet this technical capability, now taken for granted, represents five decades of painstaking development, strategic partnerships, and forced innovation born from international isolation.

The story that unfolds across the next several hours isn't just about metallurgy or defense procurement. It's about how nations build strategic capabilities from scratch, why some government enterprises succeed while others stagnate, and what happens when patient capital meets existential necessity. As we'll discover, MIDHANI's journey from a mandated laboratory to a publicly-traded company worth ₹7,400 crores offers profound lessons about industrial policy, technology absorption, and the peculiar economics of strategic autonomy.

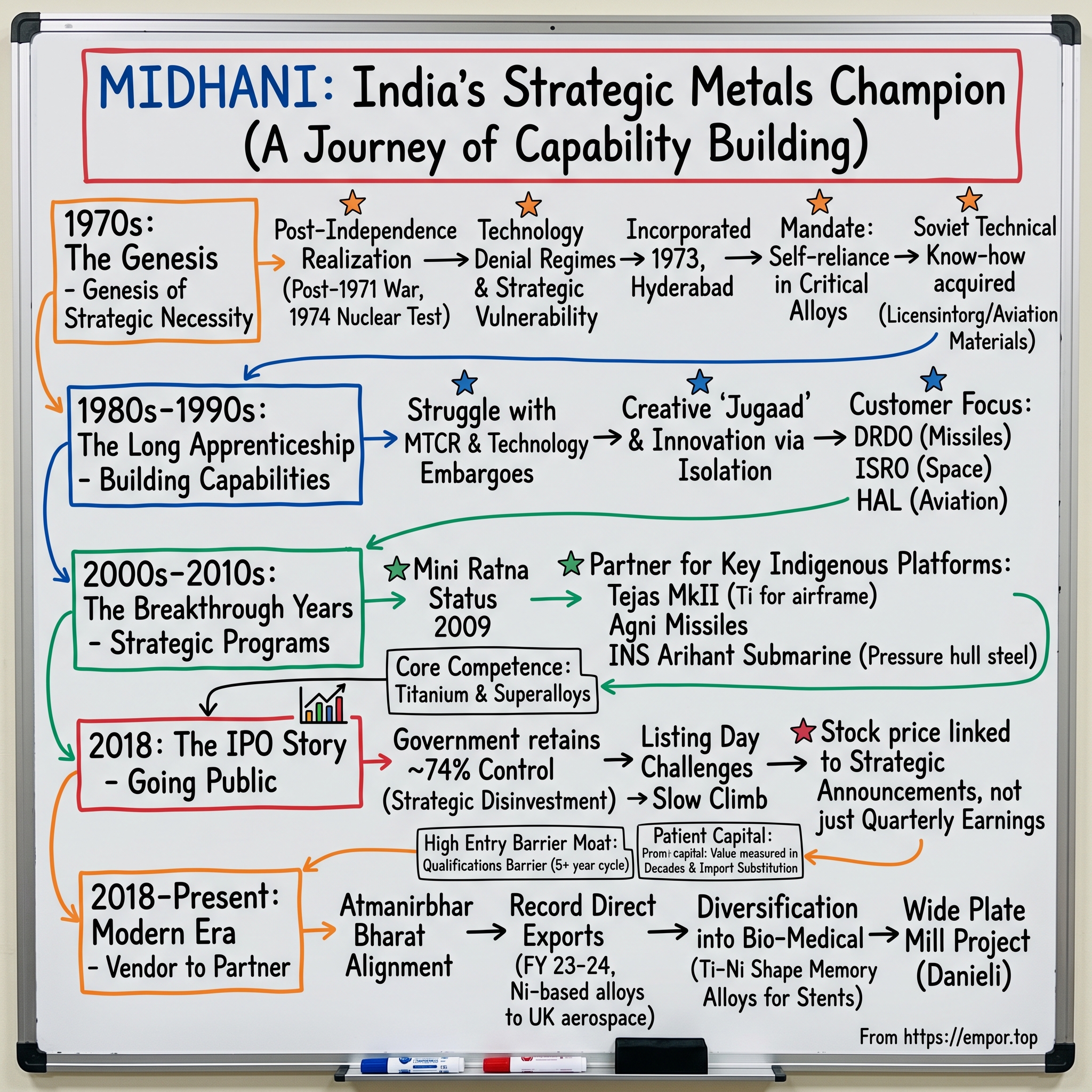

II. The Genesis: Post-Independence Strategic Imperatives (1970s)

The year is 1971. Pakistani tanks roll across the border while the Indian Air Force scrambles its Soviet-supplied MiG-21s. In the aftermath of the Bangladesh Liberation War, as India emerges victorious but diplomatically isolated, a sobering realization dawns on the defense establishment: every critical component in those aircraft engines, every high-strength alloy in the armor plating, comes from abroad. The Americans have cut off military supplies after India's tilt toward the Soviet Union. The Chinese remain hostile after the 1962 war. Even the Soviets, while friendly, extract steep prices for their technology transfers.

Three years later, on May 18, 1974, India conducts its first nuclear test—"Smiling Buddha"—in the Rajasthan desert. The international response is swift and punishing. Technology denial regimes spring up overnight. The Nuclear Suppliers Group forms explicitly to prevent countries like India from accessing dual-use technologies. Suddenly, even basic metallurgical equipment becomes impossible to import.

It's against this backdrop of strategic vulnerability that MIDHANI was incorporated in 1973 at Hyderabad as a Government of India Enterprise under the Ministry of Defence. The mandate was audacious for a nation that had barely industrialized: achieve self-reliance in the research, development, and supply of critical alloys and products of national security importance.

The choice of Hyderabad was deliberate. Far from Pakistan's border, blessed with a dry climate ideal for precision manufacturing, and home to the Defence Metallurgical Research Laboratory (DMRL), the city offered the perfect location for India's most sensitive metallurgical facility. The initial team comprised barely 50 engineers and metallurgists, many poached from the steel plants of Bhilai and Rourkela, others fresh graduates from IITs who chose patriotic duty over lucrative private sector jobs. The Soviet connection proved crucial. Technical knowhow was acquired from companies in the former Soviet Union, including Licensintorg and the Institute for Aviation Materials. But this wasn't charity—the Soviets extracted their price through complex barter arrangements and technology licensing fees that consumed precious foreign exchange. More importantly, the technology transfer came with strings: Indian engineers could learn to operate Soviet equipment, but not necessarily understand the underlying metallurgical principles.

Dr. P.R. Srinivasan, one of MIDHANI's founding metallurgists, would later recall the early days: "We had a vacuum arc melting furnace from the Soviets, but when it broke down, we couldn't get spare parts. The embargo meant we couldn't buy from the West either. So we reverse-engineered it, machined our own components, and in the process, learned more about vacuum metallurgy than any manual could teach us."

The company entered into technical collaboration agreements with Cruesot-Loire and Pechiney Ugine Kuhlmann of France and Fried Krupp GmbH of West Germany, diversifying beyond Soviet dependence. But these Western partnerships were carefully limited—the Europeans would sell equipment but not cutting-edge technology, especially anything with dual-use applications.

The technical challenges were staggering. Titanium, for instance, is notoriously difficult to work with—it burns in air at high temperatures, reacts with almost every element, and requires specialized vacuum or inert atmosphere processing. The melting point of 1,668°C meant conventional furnaces were useless. Every step, from sponge production to final forging, demanded equipment and expertise India simply didn't possess.

The early product list was modest: basic stainless steels, simple nickel alloys, materials that Western companies had mastered decades earlier. But for India's defense establishment, even these represented a revolution. The IAF's MiG-21s could now be overhauled domestically. The nuclear program had a domestic source for specialized steels. Small victories, but victories nonetheless.

By 1976, MIDHANI had commissioned its first major facility: a 2-ton vacuum induction melting furnace, the largest in South Asia at the time. The commissioning ceremony was attended by Defense Minister Jagjivan Ram, who declared: "Today we melt metal, tomorrow we forge our destiny." It was bombastic political rhetoric, yet it captured something essential—for a post-colonial nation, the ability to produce strategic materials represented more than industrial capability; it was sovereignty itself.

The Hyderabad facility expanded rapidly through the late 1970s, adding vacuum arc remelting capability, electron beam melting furnaces, and sophisticated testing equipment. Each addition represented months of negotiation with foreign suppliers, creative financing through rupee-rouble trade agreements, and occasional industrial espionage that nobody acknowledged but everyone understood was necessary.

As the decade closed, MIDHANI had established itself as more than just another public sector undertaking. It was becoming what strategic planners called a "technology absorption center"—a place where foreign equipment and limited know-how could be transformed, through persistence and ingenuity, into indigenous capability. The foundation was laid, but the real test would come in the decades ahead, when India's strategic isolation would force MIDHANI to innovate or become irrelevant.

III. The Long Apprenticeship: Building Capabilities (1980s-1990s)

The phone call came at 3 AM on a humid June night in 1985. DRDO's missile complex needed an urgent batch of maraging steel for the Prithvi missile's motor casing—a hyper-strong alloy that only five countries could produce. The Americans had explicitly banned its export to India. The Soviets claimed technical difficulties. MIDHANI's night shift supervisor knew what this meant: they would have to figure it out themselves.

This scenario repeated itself throughout the 1980s and 1990s, as India's strategic programs accelerated while technology denial regimes tightened their grip. The Missile Technology Control Regime, established in 1987, essentially quarantined India from any advanced materials technology. The Nuclear Suppliers Group expanded its restrictions. Even basic technical literature became classified as "dual-use" and disappeared from international journals that Indian scientists could access.

MIDHANI specializes in manufacturing a wide range of superalloys, titanium, special-purpose steels, and other special metals & alloys meeting international standards, but achieving those international standards without international cooperation required extraordinary creativity. Engineers would attend international conferences, memorize compositions and processing parameters discussed in hallway conversations, then return to Hyderabad to experiment. Industrial intelligence operations—never officially acknowledged—procured sample materials that MIDHANI's scientists would reverse-engineer through painstaking spectrographic analysis.

The customer base during these decades was narrow but demanding. DRDO's various laboratories needed exotic materials for everything from torpedo casings to satellite components. HAL required superalloys for the indigenous Kaveri engine program. ISRO demanded ultra-low-magnetic steels for launch vehicles. Each requirement pushed MIDHANI into uncharted territory. The Kaveri engine saga perfectly encapsulates MIDHANI's challenges during this period. The GTRE GTX-35VS Kaveri is an afterburning turbofan project under development by the Gas Turbine Research Establishment (GTRE), originally intended to power production models of the HAL Tejas. What sounds straightforward on paper—develop an indigenous jet engine—became a metallurgical nightmare. The turbine blades alone required nickel-based superalloys capable of withstanding 1,500°C while spinning at 20,000 RPM. MIDHANI had to develop these alloys from scratch, with no foreign assistance forthcoming.

The process was agonizingly slow. A typical development cycle went like this: GTRE would specify a material requirement, MIDHANI would spend months developing a prototype alloy, initial tests would reveal deficiencies, the composition would be tweaked, new samples produced, tested again—and often the entire cycle would repeat multiple times before achieving acceptable results. Each iteration consumed precious resources and time, luxuries a commercially-oriented company couldn't afford but a strategic PSU had to endure.

Indigenous technologies to produce alloys such as DMR OT4-1, GTM 900, TITAN 26A and TITAN 29A were established during this period. TITAN 26A and TITAN 29A are high-temperature titanium alloys that have been indigenously developed in India, in which MIDHANI collaborated with DMRL. These weren't mere copies of foreign alloys but genuine innovations born from necessity—when you can't import, you must invent.

The quality control challenges were particularly daunting. Aerospace materials require consistency measured in parts per million. A microscopic inclusion, an imperceptible variation in grain structure, could cause catastrophic failure. MIDHANI had to develop not just the materials but the entire quality assurance ecosystem—non-destructive testing equipment, metallographic analysis capabilities, statistical process control systems—mostly through indigenous development or creative "jugaad" when foreign equipment was unavailable.

By the early 1990s, a subtle shift occurred. MIDHANI's engineers, who had spent years reverse-engineering and problem-solving in isolation, discovered they had developed capabilities that even surprised their Soviet mentors. During a rare technical exchange in 1991, visiting Russian metallurgists were impressed by MIDHANI's novel approach to titanium processing—born not from advanced research but from making do with limited resources.

The company's workforce during this period deserves special mention. These weren't just employees but true believers in technological sovereignty. Many could have earned multiples of their government salaries in the private sector or abroad. Dr. K. Raghavan, who headed the titanium division, turned down a lucrative offer from Boeing to continue what he called "nation-building through metallurgy." This ethos permeated the organization—the canteen conversations were about phase diagrams and grain boundaries, not cricket scores.

Financial constraints added another layer of complexity. While Western companies could afford to scrap failed batches worth millions, MIDHANI had to make every melt count. This forced discipline actually became an advantage—MIDHANI developed some of the most efficient material utilization rates in the industry, with scrap recovery and recycling processes that would later be studied by international peers.

The 1998 Pokhran-II nuclear tests marked a turning point. The international sanctions that followed were harsh but also liberating—India no longer had to pretend it might gain access to advanced technologies through good behavior. The message was clear: develop everything indigenously or remain perpetually dependent. For MIDHANI, this meant accelerated investment and expanded mandates. The government finally understood that strategic autonomy required patient capital and acceptance of failures as learning investments.

By the decade's end, MIDHANI had quietly achieved several firsts: indigenous maraging steel for missile casings, specialized titanium alloys for naval applications, and nickel superalloys that could finally meet international aerospace standards. The company that had started as a metallurgical apprentice was beginning to master its craft, setting the stage for the breakthrough years ahead.

IV. The Breakthrough Years: Strategic Programs (2000s-2010s)

The Siachen Glacier, 2003. At 20,000 feet, where temperatures plunge to minus 50°C and oxygen levels are a third of sea level, Indian soldiers manning the world's highest battlefield discovered their equipment failing in ways nobody had anticipated. Standard steel became brittle as glass. Electronic components failed. Even specialty alloys showed stress fractures. The emergency request to MIDHANI was unprecedented: develop materials that could function in the most extreme environment on Earth.

This was the new reality of the 2000s—India's strategic ambitions were expanding faster than its technological capabilities, and MIDHANI found itself at the center of every critical program. The Light Combat Aircraft had moved from drawing board to prototype. The Agni missile series was advancing toward intercontinental range. The nuclear submarine program, shrouded in secrecy, demanded materials that officially didn't exist.

Hyderabad-based Mishra Dhatu Nigam (MIDHANI), a Miniratna Defence Public Sector Undertaking (PSU), has achieved a significant milestone by dispatching its first consignment of titanium and superalloy products to Hindustan Aeronautics Limited (HAL). These advanced materials are critical components for the manufacturing of the airframe and structural parts of the Tejas MkII fighter jet.

The company's technological capabilities had matured significantly. The company stands as India's sole facility for advanced vacuum-based melting and refining, employing cutting-edge technologies such as vacuum induction melting, vacuum arc remelting, and electron-beam melting. This wasn't just about having the equipment—it was about knowing how to use it, understanding the subtle interplay of temperature, pressure, and time that transforms raw materials into aerospace-grade alloys.

The breakthrough moment came in 2009 when MIDHANI achieved Mini Ratna status, recognizing its transformation from a struggling government laboratory into a profitable enterprise generating strategic value. The numbers told only part of the story—revenue had crossed ₹500 crores, but more importantly, import substitution value exceeded ₹2,000 crores annually. Every kilogram of strategic material MIDHANI produced meant foreign exchange saved and vulnerability reduced.

This is an important milestone in the development of indigenous technologies for the production and thermo-mechanical processing of high-temperature titanium alloys for aerospace applications, which DRDO is reaching along with MIDHANI and HAL. Developed by the Defence Metallurgical Research Laboratory (DMRL) of DRDO, this is a crucial technology for establishing self-reliance in aero-engine technology. With this development, India has joined the league of limited global engine developers to have the manufacturing capabilities of such critical aero-engine components.

The armor steel program showcased MIDHANI's evolution. MIDHANI has been manufacturing bulk quantities of armour steel products offering ballistic protection against a variety of weapon systems including 9mm SMC, AK-47 and 7.62mm SLR based on technologies developed by DMRL. Select few armoured products manufactured by MIDHANI are, "Rakshak" bullet-proof jackets, "Patka" (headband) for protection of head, bulletproof protection of personnel carriers for paramilitary forces & VVIP cars.

But the real revolution was happening in titanium technology. Titanium is used in aircraft spars and support and is notoriously difficult to work with, only Russians seem to have the process and methods and decades old experience in working with Ti. MIDHANI's engineers had spent two decades mastering this notoriously difficult metal, and by 2010, they weren't just matching international standards—in some specialized applications, they were setting them.

The space program provided another crucial development vector. ISRO's requirements pushed MIDHANI into exotic territories: ultra-low magnetic permeability steels for satellite launch vehicles, specialized alloys for cryogenic engines operating near absolute zero, and materials that could withstand the thermal cycling of repeated atmospheric reentry. Each success with ISRO enhanced MIDHANI's credibility and capabilities.

Hindustan Aeronautics Limited (HAL) has placed a ₹600 crore order with Mishra Dhatu Nigam Limited (MIDHANI) for the supply of advanced superalloys. MIDHANI's expertise in developing superalloys, titanium alloys, and other advanced materials has positioned it as a key player in India's defense ecosystem. The company's state-of-the-art facilities, including vacuum arc melting furnaces and precision forging units, enable it to produce superalloys that meet the stringent standards of aerospace applications.

The nuclear submarine program, INS Arihant, presented perhaps the greatest challenge. The pressure hull required special steels that could withstand crushing ocean depths while maintaining non-magnetic properties to avoid detection. The nuclear reactor needed materials that could endure decades of neutron bombardment. Every specification was classified, every material critical, and failure was not an option. MIDHANI delivered, though the details remain classified to this day.

International collaboration, limited though it was, began to shift during this period. The company entered into technical collaboration agreements with Cruesot-Loire and Pechiney Ugine Kuhlmann of France and Fried Krupp GmbH of West Germany. Later, technical knowhow was also acquired from companies in the former Soviet Union. But now, instead of being passive technology recipients, MIDHANI engineers engaged as equals, sometimes teaching as much as they learned.

The shape memory alloys program exemplified this new confidence. Under the Make in India initiative, MIDHANI has signed a transfer of technology (ToT) agreement with the National Aerospace Laboratories (CSIR-NAL) for the processing of nickel–titanium shape memory alloys (NiTi-SMAs) for engineering and bio-medical applications. The shape memory technology is a result of a decade of R&D work carried out at CSIR-NAL. MIDHANI has already ventured into development and manufacturing of titanium implants using the spin off technologies for defence applications.

Quality certifications accumulated like badges of honor: AS9100 for aerospace, ISO 14001 for environmental management, OHSAS 18001 for safety. But the real validation came from customers. When HAL chose MIDHANI materials for critical Tejas components over imported alternatives, when ISRO specified MIDHANI alloys for the Mars Orbiter Mission, when the Navy insisted on MIDHANI steel for indigenous warships—these were votes of confidence worth more than any certificate.

The financial performance during this period reflected the transformation. Revenue grew from ₹400 crores in 2000 to over ₹800 crores by 2015. More importantly, the product mix had shifted dramatically upward—from basic steels to sophisticated superalloys, from commodity materials to customized solutions. Profit margins expanded as MIDHANI moved up the value chain, validating the strategy of patient capability building.

The human capital story was equally impressive. MIDHANI had become a training ground for India's metallurgical elite. IIT graduates who once headed straight to Silicon Valley now competed for positions at MIDHANI. The company's internal research papers began appearing in international journals. Foreign delegations, once teachers, now came as students to understand how MIDHANI had achieved so much with relatively modest resources.

By 2015, as India's strategic programs accelerated—the Rafale deal, the Make in India initiative, the renewed push for indigenous defense production—MIDHANI stood ready. The apprenticeship years were over. The breakthrough had been achieved. The question now was whether this government-owned enterprise could navigate the complexities of capital markets while maintaining its strategic focus. The answer would come with one of the most interesting IPOs in Indian corporate history.

V. The IPO Story: Going Public as a Defense PSU (2018)

March 21, 2018, 10 AM. As MIDHANI's IPO opened for subscription at ₹90 per share, investment bankers in Mumbai's Nariman Point offices faced an unusual challenge: how do you value a company whose most important products are classified, whose largest customer is the government, and whose real worth lies not in profits but in national security?

The context for this IPO was the Modi government's ambitious disinvestment program—a push to unlock value from PSUs while raising capital for fiscal needs. But MIDHANI was different from selling stakes in oil companies or banks. This was about taking public a company that held some of the nation's most sensitive technological secrets.

The numbers seemed straightforward enough: the government was divesting 26% stake, looking to raise about ₹450 crores. The company's financials showed steady if unspectacular growth—revenue around ₹750 crores, profit after tax of approximately ₹100 crores. But these numbers masked the strategic complexity. How do you explain to retail investors that MIDHANI's true value isn't in its P/E ratio but in the fact that it's the only Indian company that can produce titanium alloys for fighter jets?

The IPO prospectus made for fascinating reading—heavily redacted in parts, with entire sections about strategic programs replaced with generic descriptions. Investors learned that MIDHANI served "strategic sectors" and produced "special materials" but the details of what went into the Agni missile or the Arihant submarine remained classified. It was perhaps the only IPO where ignorance about core products was a feature, not a bug.

It was incorporated in 1973 at Hyderabad as a Government of India Enterprise under the Ministry of Defence. GoI still owns ~74% stake in the company after its IPO in 2018. The government's decision to retain 74% control sent a clear message: this was strategic disinvestment, not privatization.

Institutional investors were cautiously optimistic. Defense sector analysts pointed to India's modernization plans—$250 billion in defense procurement over the next decade, the push for indigenous manufacturing, the geopolitical tensions requiring strategic autonomy. MIDHANI was positioned at the intersection of all these trends.

But retail investors were skeptical. PSU stocks had a poor track record. The company's customer concentration was extreme—over 80% revenue from government entities. The working capital cycle was long, typical of defense suppliers. And then there was the governance question: would a listed MIDHANI be more efficient, or would stock market pressures conflict with strategic imperatives?

The IPO closed on March 23, 2018, subscribed 1.3 times—modest by Indian standards where hot IPOs often see 50-100 times subscription. The institutional portion was subscribed 2.6 times, while retail was just 0.42 times. The message was clear: professionals understood MIDHANI's strategic value, but retail investors remained unconvinced.

April 4, 2018—listing day. The stock opened at ₹88, below the issue price of ₹90, and promptly fell to ₹86.05, the all-time low. Financial media had a field day: "MIDHANI Melts on Debut," screamed one headline. Short-term traders who had hoped for listing gains fled. The company that had spent 45 years building strategic capabilities saw its market value questioned within 45 minutes of trading.

But something interesting happened over the following months. As defense contracts materialized, as the Rafale deal's offset obligations became clear, as HAL's orders for indigenous programs grew, smart money began accumulating MIDHANI shares. The stock began its slow climb, crossing ₹100 in late 2018, ₹200 by 2020.

The PSU paradox became evident: MIDHANI's stock price moved not on quarterly earnings but on strategic announcements. When India tested the Agni-V missile, MIDHANI stock jumped. When tensions with China escalated in Ladakh, defense stocks including MIDHANI rallied. The market was learning to value strategic assets differently.

Being listed brought unexpected benefits. Transparency requirements forced MIDHANI to professionalize its operations. Quarterly earnings calls became forums for educating investors about materials science and strategic autonomy. The company began articulating its vision more clearly, talking about new markets like medical implants and aerospace exports.

The challenges were real too. Stock market pressure for quarterly growth conflicted with the long development cycles of strategic materials. Investors questioned R&D spending that might not generate returns for years. The company had to balance disclosure requirements with security considerations—a delicate dance that continues today.

MIDHANI reached its all-time high on February 5, 2024, touching ₹547.50, a six-fold increase from its listing price. The journey from ₹86 to ₹547 wasn't just about stock price appreciation—it reflected growing market understanding of strategic value, recognition of MIDHANI's technological moats, and appreciation for patient capital in building national capabilities.

Being a Public Sector Undertaking (PSU) under the Ministry of Defence, Midhani benefits from consistent government support, particularly in the form of defense contracts and funding for research and development projects. This government backing, once seen as a weakness implying inefficiency, was increasingly viewed as a strength ensuring steady order flow and strategic priority.

The IPO also catalyzed internal changes. Employee stock options, though limited, created new incentive structures. The discipline of quarterly reporting improved operational efficiency. The scrutiny of public markets pushed management to articulate clearer strategies and timelines.

Perhaps most importantly, the IPO demonstrated that strategic assets could access public markets while maintaining their core mission. MIDHANI proved that being listed didn't mean compromising on strategic objectives or rushing into short-term profit maximization. The market, initially skeptical, learned to value long-term strategic positioning over quarterly earnings volatility.

As the IPO chapter closed and MIDHANI entered its life as a listed entity, the company faced new challenges and opportunities. The capital raised would fund expansion, the public scrutiny would drive efficiency, and the market validation would attract talent. But the core mission remained unchanged: providing strategic materials for national security. The question now was how to balance market expectations with strategic imperatives in an increasingly complex geopolitical environment.

VI. Modern Era: From Supplier to Partner (2018-Present)

The conference room at HAL's Bangalore complex, September 2023. The agenda: finalizing specifications for materials needed for the Tejas MkII program. But this wasn't the usual customer-supplier meeting. MIDHANI's engineers weren't just taking requirements; they were proposing solutions, suggesting design modifications that could leverage new alloys they'd developed, offering to co-develop materials specifically optimized for indigenous applications. The transformation from vendor to partner was complete.

This shift represents MIDHANI's evolution in the post-IPO era. Hindustan Aeronautics Limited (HAL) has placed a ₹600 crore order with Mishra Dhatu Nigam Limited (MIDHANI) for the supply of advanced superalloys. This strategic move aligns with India's Atmanirbhar Bharat initiative, aimed at reducing dependence on foreign suppliers for critical jet engine components. The superalloys, known for their exceptional strength, heat tolerance, and durability, will be used in engines such as the Russian-origin AL-31FP, which powers the Indian Air Force's (IAF) Sukhoi Su-30 MKI fighters.

The numbers tell part of the story. Current market capitalization stands at ₹7,403 crores. Revenue has crossed ₹1,074 crores with profit after tax of ₹110 crores. But these financial metrics only hint at the strategic transformation underway. MIDHANI is no longer just filling orders; it's shaping India's defense capabilities at the design stage. The export breakthrough marks a defining shift. On exports front, MIDHANI achieved direct export of ₹6,658 Lakh during FY 23-24 reflecting a y-o-y increase of 216.17% which was highest ever. MIDHANI's share in overall Defence export by Indian Defence industry during FY 23-24 may seem insignificant, but for MIDHANI, exports were significant leap both strategically and for future growth perspective as MIDHANI catered the requirements of super alloys and special steel for Aerospace and Power Sector. By earmarking presence in global market and serving critical sectors, MIDHANI has opened avenues with vast possibilities. The company has supplied nickel-based alloys to British aerospace firms, providing critical international exposure for indigenous defense manufacturers.

The technological capabilities continue to expand. MIDHANI has already ventured into development and manufacturing of titanium implants using the spin off technologies for defence applications, and is now tapping into the huge emerging potential of nickel – titanium (NiTi) shape memory alloys in Bio-Medical Sector (medical devices), especially the stent market for which the company will manufacture shape memory alloys and market the products for the first time in India. By signing this transfer of shape memory alloy processing technology and the technological support that would be available from CSIR-NAL during the start-of-art vacuum melting and alloy processing, MIDHANI will enter into the realm of commercial production of 'smart' material and will join the band of select few shape memory alloy manufacturers in the world.

The wide plate mill project represents MIDHANI's most ambitious expansion. MIDHANI, Hyderabad, awarded a contract to Danieli for the design, manufacture, supply, and installation of a complete, modern plate mill complex consisting of a wide plate rolling mill and a modern plate treatment and finishing. The new wide plate mill will be able to process metal plates up to 3100 mm wide and from 4 mm to 20 mm in thickness in a large range of special alloys, including titanium, super-alloys, stainless steel, HSLA steels, etc. Production for the first plates is scheduled to begin by the second half of 2019.

The relationship with HAL has evolved into true partnership. Beyond the ₹600 crore order for superalloys, MIDHANI engineers now sit in HAL's design meetings, suggesting material solutions before specifications are finalized. When HAL needed materials for the AL-31FP engine overhaul program, MIDHANI didn't just supply to specifications—they proposed alternative alloys that could extend engine life while reducing maintenance intervals.

Customer diversification accelerates beyond traditional defense. The diversified sectors served by MIDHANI ranges from oil and gas, energy, naval, Aerospace etc. It is our goal to achieve initially 10% of our total revenue from export to as high as 30% in near future, so that our global presence will be further strengthened and will be step toward MIDHANI becoming a global lead supplier of aerospace grade alloys.

The medical sector emergence showcases MIDHANI's adaptability. Shape memory alloys developed for defense applications found unexpected use in medical stents and orthopedic implants. The same precision required for aerospace translates perfectly to biomedical applications, where material purity and consistency can mean life or death.

Digital transformation, though less visible, revolutionizes operations. Advanced modeling software predicts alloy properties before physical production. Machine learning algorithms optimize furnace parameters. Digital twins of production processes enable virtual experimentation. The company that once relied on trial-and-error now uses computational materials science to accelerate development cycles.

The talent equation has transformed dramatically. MIDHANI now attracts top metallurgical talent from IITs and international universities. Joint research programs with academic institutions create a pipeline of specialized expertise. The company's engineers publish in peer-reviewed journals, patent novel processes, and increasingly, get poached by global aerospace companies—a backhanded compliment to MIDHANI's training capabilities.

Strategic autonomy takes new meaning in the current geopolitical context. With supply chain disruptions and technology restrictions intensifying, MIDHANI's role becomes even more critical. The ability to produce materials domestically isn't just about cost or convenience—it's about ensuring India's defense capabilities remain uncompromised regardless of international politics.

The financial performance reflects this strategic importance. As on April 1, 2024, MIDHANI had an order book position of ₹1,57,972 Lakh vis-à-vis ₹1,33,104 Lakh as on April 1, 2023, registering a YoY growth of 18.68%. But more telling than order book growth is the shift in order composition—from commodity materials to specialized, high-margin products that only MIDHANI can produce.

Looking ahead, MIDHANI's ambitions extend beyond traditional boundaries. The planned aluminum alloy plant in Nellore, joint ventures for advanced composites, participation in global aerospace supply chains—each initiative builds on five decades of capability development while pushing into new frontiers.

The modern MIDHANI bears little resemblance to the struggling laboratory of the 1970s. It's now a sophisticated materials science company that happens to be government-owned, a strategic asset that also delivers shareholder returns, a monopoly that continuously innovates. The transformation from supplier to partner represents not just corporate evolution but national capability building at its most successful.

VII. The Technology Deep Dive: Why Metallurgy Matters

Picture a modern jet engine turbine blade. Barely larger than your hand, it operates in an environment that would vaporize most materials instantly—temperatures exceeding 1,500°C, centrifugal forces generating stress equivalent to hanging a truck from each blade, all while maintaining dimensional tolerances measured in microns. This single component embodies why metallurgy remains the hidden foundation of modern civilization and why MIDHANI's capabilities matter far beyond financial metrics.

Titanium is used in aircraft spars and support and is notoriously difficult to work with, only Russians seem to have the process and methods and decades old experience in working with Ti. So, if Midhani does really gain experience with working on it, it's a real "defense" moat. This isn't hyperbole—titanium's peculiar combination of properties makes it irreplaceable in aerospace applications. It's as strong as steel but 45% lighter. It resists corrosion better than stainless steel. It maintains strength at temperatures that would weaken aluminum. But these advantages come with extraordinary processing challenges.

Titanium's reactivity is its blessing and curse. In service, it forms a protective oxide layer that makes it nearly indestructible. During processing, this same reactivity means it will burn in air at high temperatures, absorb hydrogen and become brittle, or react with crucible materials and become contaminated. Every step—melting, forging, machining—requires specialized equipment and expertise that took MIDHANI decades to master.

The vacuum arc remelting (VAR) process illustrates this complexity. A titanium electrode is melted in a vacuum using an electric arc, with molten droplets falling into a water-cooled copper crucible. The process must be controlled precisely—too fast and you get segregation, too slow and you get excessive grain growth. The vacuum must be perfect—any air leak introduces contamination. The cooling rate determines crystal structure, which determines properties. MIDHANI's operators have developed an intuitive understanding that goes beyond procedural manuals, knowing by sound when the arc is stable, by color when the temperature is optimal.

Superalloys present different but equally daunting challenges. These nickel or cobalt-based alloys maintain strength at temperatures where most metals would be puddles. The company stands as India's sole facility for advanced vacuum-based melting and refining, employing cutting-edge technologies such as vacuum induction melting, vacuum arc remelting, and electron-beam melting. Notably, it achieved a national first by producing Hafnium metal crucial to the space sector, utilizing an innovative electron beam melting furnace. The company's diverse facilities, including air induction melting, enable the manufacturing of large nickel super-alloy-based castings. This technological prowess ensures flexibility and allows the company to deliver high-quality products meeting stringent customer requirements, positioning it as a leader in innovation and advanced materials within the industry.

The secret lies in their microstructure—a carefully controlled arrangement of different phases that provide strength through multiple mechanisms simultaneously. Gamma prime precipitates block dislocation movement. Carbides strengthen grain boundaries. Solid solution strengthening adds baseline strength. Each mechanism must be optimized without compromising others, requiring compositions controlled to 0.01% and heat treatments timed to the minute.

MIDHANI is also the only company to possess a 6000-ton forging press in India. This isn't just about size—it's about the ability to work materials that can't be shaped any other way. Titanium alloys work-harden rapidly; without sufficient force, you can't deform them uniformly. The press must apply pressure precisely, uniformly, at exactly the right temperature. Too hot and you get uncontrolled grain growth; too cold and the material cracks.

The precision forging process for turbine disks exemplifies the art hidden in the science. The starting billet must be heated uniformly to within 10°C throughout its volume. The dies must be preheated to prevent thermal shock. The forging must be completed within a temperature window that might last only minutes. The deformation must be controlled to develop the desired grain flow—radial in the bore for hoop stress resistance, circumferential in the rim for centrifugal loads. After forging, the cooling rate determines whether you get the desired microstructure or expensive scrap.

Investment casting, another MIDHANI capability, enables production of complex shapes impossible to machine. The process begins with a wax pattern, exact in every detail. This is coated with ceramic slurry, layer by layer, building a shell. The wax is melted out, leaving a cavity. Molten superalloy is poured in, filling every detail. But the devil is in the details—the ceramic must withstand 1,600°C without reacting with the metal, the pouring temperature must be exact to avoid defects, the solidification must be controlled to prevent shrinkage.

Quality control in aerospace metallurgy goes beyond simple testing. MIDHANI has acquired an in-depth understanding of the Processing–Structure–Evolution–Material Performance / Behavior interrelationships, which have contributed to solving several daunting technological problems in the field of metallurgy. Every batch undergoes chemistry analysis via optical emission spectroscopy. Mechanical properties are verified through tensile, creep, and fatigue testing. Microstructure is examined using electron microscopy. Non-destructive testing—ultrasonic, radiographic, eddy current—ensures internal integrity.

But the real quality comes from understanding failure modes. When a turbine blade fails, it's rarely from simple overload. It's from fatigue crack initiation at an inclusion, or creep rupture from incorrect heat treatment, or hot corrosion from trace contaminants. MIDHANI's metallurgists have studied thousands of failures, building an institutional knowledge base that can't be bought or transferred—only earned through experience.

The shape memory alloys program demonstrates MIDHANI's evolution from processor to innovator. These materials "remember" their original shape, returning to it when heated above a transformation temperature. The effect depends on a reversible phase transformation between martensite and austenite—crystallographic gymnastics that require precise composition and processing. MIDHANI didn't just learn to make these alloys; they're developing new compositions optimized for specific applications.

Process innovation continues behind the scenes. MIDHANI has developed proprietary techniques for grain boundary engineering in superalloys, enhancing creep resistance. They've pioneered methods for producing ultra-fine grain titanium for improved fatigue performance. They've created specialized heat treatments that optimize properties for specific applications.

The economic multiplier of these capabilities extends far beyond MIDHANI's balance sheet. Every indigenous engine that flies, every submarine that dives, every missile that protects—all depend on materials that MIDHANI produces. The technology sovereignty these capabilities provide is invaluable. In a world where advanced materials increasingly determine military and economic competitiveness, MIDHANI's metallurgical mastery represents a strategic asset whose true value transcends any financial valuation.

VIII. Competition & Strategic Positioning

The global specialty metals industry resembles a highly exclusive club where the entry fee isn't money but decades of accumulated expertise. Against titans like Allegheny Technologies (ATI) with its $3.5 billion revenue, Carpenter Technology's 130-year heritage, or Russia's VSMPO-AVISMA controlling 30% of global titanium supply, MIDHANI might seem like a marginal player. Yet this David-versus-Goliath narrative misses the profound strategic logic underlying MIDHANI's position.

It is the only manufacturer of Titanium alloys in India. This monopoly isn't accidental or temporary—it's structural. The capital requirements, technological complexity, and most importantly, the qualification cycles create insurmountable barriers for new entrants. When HAL needs titanium for the Tejas, they can't simply switch suppliers. The material qualification alone would take years, involving thousands of tests, certifications from multiple agencies, and the risk that any variation could ground an entire fleet.

Consider the economics of strategic materials. VSMPO-AVISMA can produce titanium sponge at perhaps $8 per kilogram. MIDHANI's cost might be $20 or higher. In a pure market economy, MIDHANI shouldn't exist. But when geopolitical tensions rise, when supply chains fragment, when export licenses become weapons—suddenly that premium becomes cheap insurance. The arithmetic of strategic autonomy operates on different principles than commodity economics.

The qualification barrier deserves special attention. In aerospace, changing a material supplier isn't like switching paper vendors. Every new source must undergo: initial material characterization (6 months), process qualification (12 months), component testing (18 months), flight qualification (24 months), and final certification. The total cycle can exceed five years and cost millions. Once qualified, switching becomes almost unthinkable unless forced by supply disruption or quality issues.

MIDHANI has accumulated thousands of these qualifications across India's strategic programs. Each represents years of testing, millions in costs, and irreplaceable institutional knowledge. A new entrant would need to replicate this entire qualification library—a practical impossibility given the classified nature of many applications.

The global competitive landscape is shifting in MIDHANI's favor. The Russia-Ukraine conflict has made Western aerospace companies desperately seek alternatives to Russian titanium. China's domestic consumption absorbs most of its production. Environmental regulations make new smelting capacity in developed countries prohibitively expensive. In this context, MIDHANI's expansion into international markets isn't opportunistic—it's strategic positioning for a fragmenting global supply chain.

Chinese competition presents a complex challenge. Companies like Baoji Titanium and Western Superconducting Technologies have massive scale and government support. But they face their own constraints—export restrictions on strategic materials, quality concerns in Western markets, and geopolitical tensions limiting market access. MIDHANI's democratic credentials and improving quality position it as a viable alternative for countries seeking to diversify away from Chinese suppliers.

The technology moat continues deepening. Midhani has a technological moat supported by distinct factors. Firstly, it stands as the exclusive producer of Ni and Ti alloy steel, offering a cost-effective alternative to imported materials. Secondly, Midhani's possession of patents for specific brands showcases its commitment to innovation, with an active research department tailoring materials to meet customer demands. Notably, they manufacture specialized materials for Bulletproof jackets, patka, and vehicles, utilizing formulations developed by Bhabha Atomic Center.

The customer intimacy advantage shouldn't be underestimated. MIDHANI's engineers don't just understand specifications—they understand applications. When DRDO needs materials for a classified project, MIDHANI's cleared personnel can participate in design discussions that would be impossible with foreign suppliers. This co-development capability creates switching costs that go beyond commercial considerations.

Private sector competition within India remains limited but is emerging. Companies like Mishra Dhatu Nigam Limited face potential competition from players like Bharatforge or Tata Advanced Materials, who have capabilities in certain segments. But replicating MIDHANI's full spectrum capabilities would require investments exceeding ₹5,000 crores and decades of learning. More likely, private players will focus on specific niches, potentially becoming partners rather than competitors.

The import substitution economics tell a compelling story. India imports special metals worth over $2 billion annually. Every percentage point of import substitution MIDHANI achieves represents $20 million in foreign exchange savings and reduced strategic vulnerability. At current capability levels, MIDHANI substitutes imports worth ₹2,000+ crores annually—a value that doesn't appear on the profit statement but matters enormously to national accounts.

International partnerships are evolving from technology absorption to genuine collaboration. While the passenger industry faces challenges, strategic collaborations, such as with Lockheed Martin, indicate promising prospects in the growing defense aircraft sector—a trend worth monitoring. These relationships position MIDHANI not as a low-cost alternative but as a strategic partner for global OEMs seeking supply chain resilience.

The certification advantages compound over time. Furthermore, Midhani's AS9001 certification establishes it as a qualified supplier for space and aerospace industries. Each new certification—whether Nadcap for special processes or customer-specific approvals—raises barriers for competitors while opening new markets for MIDHANI.

Looking at competitive dynamics, MIDHANI occupies a unique position: protected in domestic strategic markets, increasingly competitive in commercial segments, and positioned to benefit from global supply chain realignment. It's not trying to compete with ATI on scale or with VSMPO on cost. Instead, MIDHANI has carved out a defensible niche—strategic materials for price-insensitive applications where security of supply trumps unit economics.

The sustainable competitive advantages are clear: monopoly in domestic strategic markets, decades of accumulated qualifications, deep customer relationships in classified programs, strategic rather than commercial valuation by the government, and technology capabilities approaching global standards. These advantages don't guarantee perpetual success, but they create a moat that would take competitors decades and billions to cross—if they could cross it at all.

IX. Playbook: Lessons in Building Strategic Industrial Capacity

The MIDHANI story offers a masterclass in something unfashionable in modern business thinking: the patient construction of strategic industrial capacity. While Silicon Valley celebrates rapid scaling and quarterly growth, MIDHANI's five-decade journey demonstrates that some capabilities can't be rushed, some moats can't be bought, and some values can't be captured in financial statements.

Patient Capital: The Decade Doctrine

The first lesson is about time horizons that make even long-term investors uncomfortable. MIDHANI operated for nearly two decades before achieving basic profitability. The Kaveri engine materials program has consumed 30 years and counting. The titanium capability took 20 years to reach international standards. In each case, the temptation to abandon the effort must have been overwhelming.

Yet this patience wasn't passive waiting—it was active learning. Each failed batch taught something. Each customer rejection revealed a gap. Each import substitution attempt, successful or not, built institutional knowledge. The compound effect of this learning, invisible in annual reports, manifests in capabilities that now seem impossible to replicate.

The funding model matters enormously. MIDHANI survived because its capital came with strategic rather than financial return expectations. The government valued import substitution and strategic autonomy over ROE. This wasn't inefficiency—it was a different optimization function where national capability weighted heavier than quarterly earnings.

The Dual Mandate Navigation

MIDHANI embodies a fundamental tension: serving strategic imperatives while operating as a commercial entity. This dual mandate creates unique challenges. How do you price products for strategic programs where cost-plus ensures survival but discourages efficiency? How do you balance classified defense work with transparent public market disclosure?

The answer has been elegant compartmentalization. Strategic programs operate on different commercial terms—longer payment cycles accepted, development costs absorbed, pricing reflecting value rather than cost. Commercial products follow market discipline—competitive pricing, standard payment terms, normal business development. The surplus from strategic programs funds R&D for commercial applications, while commercial discipline improves strategic program efficiency.

This balancing act requires sophisticated management. It's not enough to be technically competent—leadership must navigate ministry bureaucracy, military procurement, public market expectations, and technological complexity simultaneously. The successful leaders at MIDHANI have been those who could speak the language of each constituency while maintaining strategic focus.

Technology Absorption Versus Indigenous Development

MIDHANI's approach to technology acquisition offers lessons for developing nations. Rather than choosing between expensive licensing and slow indigenous development, MIDHANI pursued a hybrid strategy: absorb what's available, reverse-engineer what's restricted, innovate where necessary.

The Soviet technology transfers provided initial capability but came with limitations—operational knowledge without fundamental understanding. Western partnerships offered equipment but restricted know-how. The genius was in filling gaps through indigenous development, using each partial transfer as a stepping stone rather than a destination.

This created unexpected advantages. Because MIDHANI couldn't simply copy, it had to understand. Because it had to work with inferior equipment, it developed superior processes. Because it faced embargoes, it built self-reliance. The constraints that seemed like disadvantages forced innovations that became competitive advantages.

The Ecosystem Imperative

MIDHANI's success is inseparable from India's broader strategic ecosystem. Without DRDO's research, HAL's applications, and ISRO's demands, MIDHANI would have been a capability without purpose. Each organization pushed others to improve, creating a virtuous cycle of capability development.

This ecosystem approach contrasts with attempts to build isolated centers of excellence. MIDHANI succeeded because it was embedded in a network of users, researchers, and complementary capabilities. The lesson: strategic industrial capacity requires not just individual champions but interconnected systems of innovation and application.

The government's role as ecosystem orchestrator proved crucial. By coordinating requirements across defense services, space, and atomic energy, it provided MIDHANI with diverse applications for similar technologies. This diversification reduced risk while accelerating learning through cross-application knowledge transfer.

Managing Government Ownership While Competing Globally

The conventional wisdom says government ownership breeds inefficiency. MIDHANI's journey suggests a more nuanced reality. Government ownership provided patient capital, strategic priority, and assured demand—crucial for building foundational capabilities. But it also brought bureaucratic processes, political interference, and risk aversion that could have been fatal.

The key was selective modernization. MIDHANI maintained government procedures where they added value—security clearances, audit processes, strategic alignment. But it adopted commercial practices where needed—quality systems, customer service, technology development. This selective adoption required constant negotiation and occasional conflict, but it enabled MIDHANI to retain government support while building commercial capability.

The IPO represented an evolution of this balance. Public listing brought market discipline without eliminating government control. It forced transparency without compromising security. It enabled employee incentives without full privatization. The structure—74% government ownership—maintains strategic control while allowing market participation.

When Monopolies Make Sense

MIDHANI's monopoly in titanium alloys challenges free-market orthodoxy but illustrates when monopolies serve strategic purposes. In markets where: minimum efficient scale exceeds total demand, customer qualification costs are prohibitive, strategic considerations override economics, and technology sovereignty matters more than price competition—monopolies might be not just acceptable but optimal.

The key is preventing monopolistic complacency. MIDHANI faces indirect competition from imports, pressure from customer expectations, and benchmarking against global standards. These forces substitute for direct competition in driving improvement. The government's role shifts from preventing monopoly to preventing monopolistic behavior—a subtle but crucial distinction.

The Compound Effect of Incremental Innovation

MIDHANI's innovation model differs from Silicon Valley disruption. Instead of breakthrough innovations, it pursued incremental improvements: slightly better yield rates, marginally improved properties, gradually expanded capabilities. Each improvement seemed modest, but compounded over decades, they transformed MIDHANI from a basic steel processor to an advanced materials company.

This incremental approach suited the constraints: limited R&D budgets, restricted access to global technology, and long qualification cycles that penalized radical changes. But it also built deep expertise—the kind that comes from solving thousands of small problems rather than betting on breakthrough solutions.

The Strategic Value Framework

Perhaps the most important lesson is how to value strategic capabilities. Traditional financial metrics—ROE, ROCE, P/E ratios—miss the point. MIDHANI's value lies in: import substitution worth multiples of revenue, strategic autonomy enabling independent foreign policy, technological sovereignty supporting indigenous development, knowledge spillovers benefiting the broader ecosystem, and option value for future strategic programs.

This framework suggests that certain industrial capabilities should be evaluated like infrastructure or defense—not solely on financial returns but on strategic contribution. The challenge is preventing this logic from justifying any unprofitable government enterprise. The key distinction: strategic value must be measurable, even if not in purely financial terms.

The MIDHANI playbook won't work everywhere. It requires patient government support, strategic applications that justify premium costs, technological complexity that creates barriers to entry, and an ecosystem of complementary capabilities. But where these conditions exist, the MIDHANI model offers an alternative to both pure market capitalism and traditional state socialism—a third way suited to building strategic capacity in developing nations.

X. Bear vs. Bull Case

The investment case for MIDHANI presents a fascinating study in contrasts—a company whose strategic importance seems undeniable yet whose financial metrics often disappoint, whose monopoly position appears unassailable yet whose growth remains pedestrian. Understanding both the bull and bear perspectives requires looking beyond traditional financial analysis to the intersection of geopolitics, technology, and national strategy.

Bull Case: The Strategic Necessity Premium

India's defense modernization plans read like a MIDHANI sales catalog. The country plans to spend $130 billion on defense modernization over the next decade. Every indigenous platform—from the Tejas MkII to the Advanced Medium Combat Aircraft, from the K-series submarines to the Agni-VI missile—requires specialized materials that only MIDHANI can provide. The addressable market isn't just large; it's legally mandated to buy from MIDHANI for critical materials.

Being a Public Sector Undertaking (PSU) under the Ministry of Defence, Midhani benefits from consistent government support, particularly in the form of defense contracts and funding for research and development projects. Government contracts constitute approximately 63% of MIDHANI's annual revenue, providing exceptional revenue visibility. Unlike typical government contractors who compete for each tender, MIDHANI often receives nomination basis orders—essentially sole-source contracts justified by strategic necessity.

The export opportunity is just beginning to materialize. India's defense exports have grown from $1 billion to $3 billion in five years, targeting $5 billion by 2025. As Indian defense platforms gain international acceptance—the Tejas to Argentina, BrahMos to the Philippines—MIDHANI becomes an automatic beneficiary. Every exported Indian defense system carries MIDHANI materials, creating a derivative export stream without additional business development costs.

The China factor adds urgency to MIDHANI's importance. As global supply chains decouple and "friend-shoring" accelerates, countries seek alternatives to Chinese strategic materials. MIDHANI offers democratic credentials, improving quality, and government backing—an attractive combination for nations balancing economic and strategic considerations.

Technological inflection points favor MIDHANI. The shift to hypersonic weapons requires materials that can withstand extreme temperatures. Next-generation aircraft engines demand ever-more sophisticated superalloys. Space commercialization needs specialized materials for reusable launch vehicles. MIDHANI is positioned at the intersection of all these trends, with capabilities that take decades to develop.

The replacement cycle provides steady growth. Aircraft engines require overhaul every 1,000-4,000 flight hours. Each overhaul needs replacement parts made from MIDHANI materials. As India's military aviation fleet expands from 800 to projected 1,200 aircraft, the aftermarket opportunity compounds. This installed base effect creates an annuity-like revenue stream independent of new platform development.

The qualifications moat keeps strengthening. Every new program that qualifies MIDHANI materials raises switching costs. With thousands of qualifications accumulated over five decades, replicating MIDHANI's position would require not just capital but time travel. These qualifications are like compound interest—invisible in early years but eventually becoming an insurmountable advantage.

Margin expansion potential remains untapped. As MIDHANI moves from commodity products (basic steels) to specialized solutions (single-crystal superalloys, shape memory alloys), margins should expand dramatically. The medical implants market, where MIDHANI's aerospace-grade quality commands premium pricing, exemplifies this potential.

Bear Case: The PSU Paradox

The numbers tell a sobering story. The company has delivered a poor sales growth of 8.54% over past five years. Company has a low return on equity of 9.14% over last 3 years. For a company with monopoly position in critical materials serving rapidly growing defense markets, these metrics are deeply disappointing.

The PSU culture problem runs deep. Decision-making remains bureaucratic, with simple procurement requiring multiple approvals. Innovation happens despite, not because of, organizational processes. The best talent often leaves for private sector opportunities, creating a brain drain that no amount of strategic importance can offset.

Customer concentration risk is extreme. With over 80% revenue from government entities, MIDHANI is essentially a single-customer business. Government budget constraints, payment delays, or priority shifts directly impact MIDHANI. The 18-24 month payment cycles common in defense contracts strain working capital and depress returns.

Technology gaps persist despite progress. MIDHANI's metallurgical capabilities, while impressive for India, lag global leaders by 10-15 years in critical areas. The company still cannot produce certain specialized alloys that advanced engines require. Industry experts note that while MIDHANI has made strides in producing alloys like TA (with 90-180 MPa strength) and NC (with 25-75 MPa), the absence of domestic alternatives for L-605—a cobalt-based superalloy used in extreme conditions—remains a bottleneck. The reliance on imported L-605 and specialized tubes highlights gaps in India's domestic metallurgical ecosystem, particularly for niche alloys required in high-performance jet engines.

The growth paradox frustrates investors. Despite massive defense modernization, MIDHANI's revenue growth remains single-digit. The explanation—long development cycles, extended qualification periods, gradual production ramp-ups—may be valid but doesn't change the reality of pedestrian growth in supposedly booming markets.

Scale limitations constrain potential. MIDHANI's total capacity remains tiny by global standards. Expanding capacity requires massive capital investment with uncertain returns. The specialized nature of equipment means utilization rates vary wildly across product lines, depressing overall asset efficiency.

Competition is emerging from unexpected quarters. Private players like Bharatforge are entering specialized segments. Global suppliers are establishing Indian operations through joint ventures. Even the monopoly in titanium alloys faces potential challenge as private players explore partnerships with foreign technology providers.

The valuation puzzle confounds analysis. At 5.25 times book value, MIDHANI trades at premium valuations despite pedestrian growth and modest returns. The market prices in strategic value, but strategic value doesn't pay dividends. The disconnect between strategic importance and financial performance creates valuation uncertainty that could persist indefinitely.

Working capital management remains problematic. Defense contracts require MIDHANI to maintain large inventories of expensive raw materials. Customer payment cycles stretch while supplier payments accelerate. The resulting working capital needs consume cash that could fund growth or improve returns.

The Synthesis: Strategic Value Versus Financial Returns

The MIDHANI investment case ultimately depends on how one weighs strategic positioning against financial metrics. Bulls see a company with irreplaceable capabilities serving markets with secular growth and barriers to entry that only strengthen over time. Bears see a PSU with cultural constraints, modest growth, and returns that don't justify premium valuations.

The truth, as often, lies between extremes. MIDHANI is neither the hidden gem that bulls proclaim nor the value trap that bears fear. It's a strategic asset that generates modest financial returns—a combination that makes sense for national strategy but challenges traditional investment frameworks.

For investors, the key question isn't whether MIDHANI has strategic value—it clearly does. The question is whether that strategic value will ever translate into superior financial returns. The evidence suggests a gradual improvement trajectory rather than dramatic transformation. Patient investors who value strategic positioning over near-term returns might find MIDHANI attractive. Those seeking rapid growth or high returns should look elsewhere.

The investment case ultimately reflects one's view on three critical factors: India's ability to execute defense modernization plans, MIDHANI's capacity to improve operational efficiency while maintaining strategic focus, and the market's willingness to pay premiums for strategic assets. Each investor must weigh these factors according to their own framework, timeline, and risk tolerance.

XI. Epilogue: The Future of Strategic Manufacturing

The year is 2034. India's third indigenous aircraft carrier cuts through the Indian Ocean, its hull made from MIDHANI's specialized naval steel. Overhead, sixth-generation fighters with MIDHANI superalloy engines patrol the skies. In Sriharikota, a reusable launch vehicle prepared with MIDHANI's ultra-light titanium components stands ready for its hundredth mission. This isn't fantasy—it's the logical extension of capabilities being built today.

The semiconductor parallel illuminates MIDHANI's future trajectory. Just as nations learned during COVID that semiconductor sovereignty matters more than economic efficiency, the fragmentation of global supply chains is teaching the same lesson about strategic materials. The countries that control advanced materials will shape the technologies of tomorrow—from hypersonic weapons to quantum computers, from fusion reactors to space colonies.

India's evolving defense export story creates unprecedented opportunities. As India transitions from the world's largest arms importer to an emerging exporter, MIDHANI transforms from a domestic supplier to a global player. The BrahMos success—now exported to Philippines and potentially a dozen other nations—demonstrates the model. Each exported Indian defense platform creates decades of MIDHANI material requirements for maintenance and upgrades.

The next frontiers push beyond traditional metallurgy. Advanced composites for hypersonic vehicles that must withstand 3,000°C while maintaining structural integrity. Additive manufacturing of complex geometries impossible with conventional processing—imagine turbine blades with internal cooling channels printed in single-crystal superalloy. Rare earth processing, where China's 80% global control creates vulnerabilities that MIDHANI could address.

Quantum materials represent an entirely new paradigm. Materials whose properties emerge from quantum mechanical effects rather than classical chemistry. Topological insulators for quantum computers. High-temperature superconductors for lossless power transmission. Metamaterials with properties not found in nature. MIDHANI's deep materials science capabilities position it to participate in these revolutionary developments.

The bio-materials convergence opens unexpected markets. The same precision required for aerospace translates to biomedical applications. Shape memory alloys for self-expanding stents. Titanium implants with surface modifications promoting bone integration. Drug delivery systems using MIDHANI's nano-material capabilities. The global biomedical materials market, worth $150 billion and growing at 15% annually, could become MIDHANI's second act.

Climate technology demands new materials. Wind turbines require rare earth magnets that currently depend on Chinese supply. Solar panels need specialized materials for improved efficiency. Hydrogen economy infrastructure demands materials resistant to hydrogen embrittlement. Nuclear fusion reactors require materials that can withstand neutron bombardment for decades. MIDHANI's expertise in extreme environment materials positions it for the energy transition.

The democratization of space changes everything. As launch costs plummet and space commercializes, demand for space-qualified materials explodes. Not just for rockets and satellites, but for space stations, lunar bases, asteroid mining equipment. Materials that must function in vacuum, resist radiation, survive temperature cycles from -270°C to +120°C. MIDHANI's space heritage provides first-mover advantage in this emerging market.

Artificial intelligence revolutionizes materials development. Instead of Edison's approach—trying thousands of compositions to find one that works—AI predicts optimal compositions before physical testing. MIDHANI's decades of data become training sets for machine learning models. Development cycles compress from years to months. The combination of MIDHANI's physical capabilities and AI's predictive power could leapfrog traditional development approaches.

The geopolitical chessboard favors strategic materials. As technology becomes the primary domain of great power competition, control over critical materials becomes paramount. The U.S.-China technology war extends beyond semiconductors to rare earths, specialty alloys, and advanced composites. Nations seek trusted suppliers within allied blocs. MIDHANI, representing democratic India, becomes an attractive partner for Western nations diversifying from Chinese suppliers.

Supply chain resilience trumps efficiency. COVID taught that optimized global supply chains are fragile. The Suez Canal blockage demonstrated single-point vulnerabilities. The Russia-Ukraine conflict showed how quickly supply can be weaponized. In this environment, domestic capability in strategic materials isn't inefficiency—it's insurance. MIDHANI's value transcends economics to encompass national resilience.

The industrial commons concept gains traction. Advanced manufacturing requires ecosystems—suppliers, skilled workers, research institutions, customer feedback loops. Once these commons dissolve, rebuilding them takes generations. MIDHANI anchors India's materials science commons, preventing the hollowing out that afflicted other nations that offshore

d critical capabilities. This commons effect multiplies MIDHANI's strategic value beyond its direct contribution.

What MIDHANI's journey teaches transcends the company itself. It demonstrates that some capabilities cannot be rushed or bought—only built through patient accumulation of knowledge. That strategic value and financial value operate on different timescales and metrics. That industrial policy, unfashionable though it may be, remains essential for capabilities markets won't naturally provide.

The critique of industrial policy—that governments can't pick winners—misses the point. MIDHANI wasn't picked as a winner; it was mandated as a necessity. The goal wasn't competitive advantage but strategic autonomy. Success wasn't measured in ROE but in import substitution and capability development. By these metrics, MIDHANI has exceeded expectations.

The lessons for other nations are clear but difficult to implement. Building strategic industrial capacity requires patient capital measured in decades, tolerance for financial underperformance during capability building, coordination across military, scientific, and industrial stakeholders, protection from pure market forces without enabling inefficiency, and clear strategic objectives that transcend political cycles.

For investors, MIDHANI represents a new asset class—strategic industrials whose value derives from national necessity rather than competitive advantage. These companies won't generate venture-scale returns, but they offer stability, strategic importance, and exposure to long-term technological trends. As geopolitical tensions increase and supply chains fragment, such assets might prove more valuable than financial metrics suggest.

The MIDHANI story continues to unfold. From its humble beginnings as a government laboratory to its current position as India's strategic materials champion, the journey demonstrates what's possible when national will aligns with patient capital and technological ambition. The next chapters—international expansion, new materials frontiers, potential partnerships—remain unwritten.

What is certain is that advanced materials will only become more critical. Whether for hypersonic weapons or quantum computers, for space colonies or fusion reactors, for artificial organs or climate solutions—materials determine what's possible. Nations that control advanced materials will shape humanity's technological future. In this context, MIDHANI isn't just a company or even a strategic asset—it's a cornerstone of India's technological sovereignty.

The ultimate judgment of MIDHANI's success won't come from stock price movements or quarterly earnings. It will come from history's assessment of whether India achieved strategic autonomy in critical technologies. Whether Indian fighters fly with Indian engines. Whether Indian spacecraft reach Mars with Indian materials. Whether India's nuclear submarines patrol with indigenous steel. By these measures—the ones that truly matter for national destiny—MIDHANI has already succeeded beyond what its founders could have imagined.

As we close this deep dive into MIDHANI's journey, it's worth reflecting on what makes certain businesses transcendent. It's not just about products or profits, markets or margins. It's about companies that embody national ambitions, that build capabilities others consider impossible, that measure success in generations rather than quarters. MIDHANI is such a company—imperfect, certainly; essential, absolutely; and in its own quiet way, revolutionary.

The molten titanium still glows in MIDHANI's furnaces, same as it did fifty years ago. But now it flows with confidence born from mastery, purpose derived from necessity, and ambition reaching toward frontiers yet undefined. In that glow lies not just metal, but metaphor—the transformation of raw potential into strategic capability, the alchemy of turning dependency into sovereignty, the slow-burning forge of national destiny.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube