Lumax Auto Technologies: The Gear Shifter King's Journey from Auto Parts to EV Components

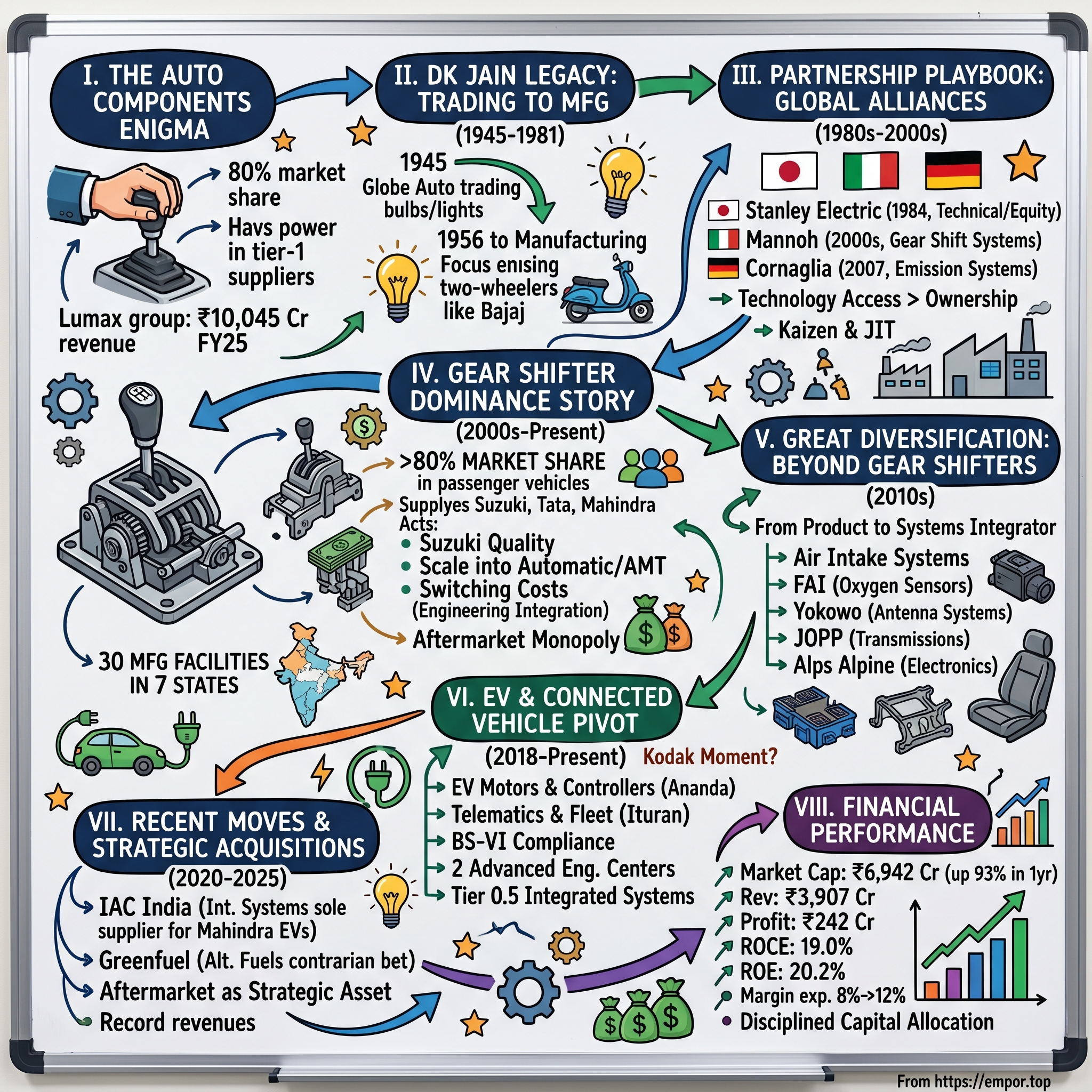

I. Introduction & The Auto Components Enigma

Picture this: You're sitting in your car, hand on the gear shifter, smoothly gliding from first to fifth as you merge onto the highway. That seemingly simple component—the one you touch hundreds of times each journey—has an 80% chance of being made by a company most investors have never heard of. Welcome to the world of Lumax Auto Technologies, India's undisputed gear shifter king with a ₹6,942 crore market cap that's quietly powering every major automobile brand in the country.

Here's the enigma: While everyone obsesses over Maruti, Tata Motors, or Mahindra—the glamorous OEMs that get all the headlines—it's the tier-1 suppliers like Lumax that hold the real pricing power and margins in India's auto ecosystem. The Lumax group clocked ₹10,045 crores in revenue for FY2025, yet remains largely invisible to retail investors mesmerized by consumer-facing brands.

The question that should intrigue any serious investor: How did a company that started as a lightbulb trader in 1945 become the monopolistic supplier of gear shifters to virtually every car manufacturer in India? And more importantly, as we hurtle toward an electric future where traditional transmissions might become obsolete, how is Lumax engineering its next act?

This is not just another auto component story. It's a masterclass in strategic partnerships, patient capital deployment, and the art of building switching costs so high that even global giants can't dislodge you. It's about a family business that understood, decades before it became fashionable, that in the auto industry, you don't need to own the technology—you just need to control the manufacturing excellence and customer relationships.

The auto components sector contributes 2.3% to India's GDP and employs over 5 million people, yet these companies trade at fraction of OEM valuations despite often having better unit economics. Lumax exemplifies this paradox: dominant market position, consistent profitability, yet flying under the radar. As we'll discover, this invisibility might be their greatest strategic advantage.

What makes this story particularly relevant now is the tectonic shift happening in automotive—electrification, connected vehicles, ADAS systems. Companies built on internal combustion engine (ICE) components face an existential question: evolve or perish. Lumax's answer? A fascinating pivot that began years before most competitors even acknowledged the threat. But we're getting ahead of ourselves. To understand where Lumax is going, we need to first understand the remarkable journey of how a trading firm in newly independent India built one of the most formidable moats in Indian manufacturing.

II. The DK Jain Legacy: From Trading to Manufacturing (1945-1981)

The year was 1945. World War II had just ended, India was two years away from independence, and in the dusty lanes of Delhi, a young entrepreneur named S.C. Jain was making a decision that would echo through generations. While others dreamed of textiles or steel—the glamour industries of that era—Jain saw opportunity in something mundane: automotive bulbs and lights. He founded Globe Auto as a trading concern, importing and distributing auto components when cars were still a luxury that only British officers and wealthy merchants could afford.

But Jain wasn't content being a middleman. By 1956, as Nehru's India embraced its tryst with destiny through industrial self-reliance, Globe Auto transformed from trader to manufacturer. The timing was perfect—India's import substitution policies meant foreign components faced massive tariffs, creating a protective moat for domestic manufacturers willing to invest in production capabilities.

The real genius of S.C. Jain wasn't just recognizing the opportunity but understanding the Indian market's unique characteristics. While western markets focused on four-wheelers, Jain realized India's mobility revolution would come on two wheels. Scooters and motorcycles—affordable, fuel-efficient, perfect for navigating narrow Indian streets—would be the real volume play. So while competitors chased prestige projects supplying to the Ambassador car (India's only passenger vehicle then), Jain built relationships with Bajaj and other two-wheeler manufacturers, supplying humble but essential headlights and tail lamps.

This wasn't sexy business. Board meetings weren't about cutting-edge technology or global expansion—they were about sourcing tungsten filaments, managing working capital during monsoon disruptions, and convincing skeptical two-wheeler manufacturers that an Indian company could match Japanese quality standards. But Jain understood something profound: in a capital-scarce economy, the unglamorous businesses that solve real problems generate the cash flows that fund future ambitions. By 1981, the pieces were in place for the next chapter. Lumax Auto Technologies Limited was formally incorporated in 1981, emerging from what had been Lumax Auto-Electricals Private Limited. The company was now part of the D.K. Jain Group, one of the pioneers in the Indian Automotive Industry. The new entity would focus initially on what the family knew best: manufacturing lighting solutions for two-wheelers from its first facility in Maharashtra.

The timing couldn't have been more fortuitous. The 1980s marked the beginning of India's two-wheeler revolution. Hero Honda had just been formed, Bajaj was ramping up production, and TVS was expanding beyond South India. Every one of these vehicles needed headlamps, tail lights, indicators—and Lumax was there, having already built the relationships and manufacturing capabilities when others were still figuring out the market.

What's remarkable about this period is how un-glamorous the strategy was. No grand visions of global dominance, no venture capital, no media coverage. Just a relentless focus on operational excellence, working capital management, and customer relationships. The Jain family understood that in India's nascent auto industry, reliability trumped innovation. OEMs didn't want cutting-edge technology—they wanted suppliers who could deliver quality parts on time, every time, at prices that made sense for a price-sensitive market.

This foundation—built on trading relationships, manufacturing discipline, and deep understanding of Indian market dynamics—would prove invaluable when global auto giants came calling in the 1980s. But that's a story for the next chapter, where we'll see how a family business from Delhi convinced some of the world's most sophisticated component manufacturers to bet on India.

III. The Partnership Playbook: Building Through Global Alliances (1980s-2000s)

The conference room at Stanley Electric's Tokyo headquarters must have been an interesting scene in 1984. On one side, executives from one of Japan's most sophisticated lighting technology companies, suppliers to Toyota and Honda globally. On the other, the Jain family from Delhi, representing a company that most Japanese executives couldn't even locate on a map. Yet by the end of those negotiations, Stanley Electric Co. Ltd., Japan entered into a technical collaboration with Lumax Industries, eventually taking a 37.5% equity stake in the company.

This wasn't just another joint venture—it was the beginning of Lumax's masterful partnership playbook that would define its trajectory for the next four decades. The genius wasn't in getting one partnership; it was in understanding that in auto components, technology access matters more than technology ownership.

Consider the context: In the 1980s, Indian manufacturing was still decades behind global standards. The choice for Indian companies was stark: spend decades and billions trying to develop proprietary technology, or partner with global leaders and leapfrog the learning curve. While others debated, the Jains acted.

The Stanley partnership transformed Lumax's lighting business overnight. Japanese manufacturing techniques—kaizen, just-in-time, total quality management—weren't just buzzwords but daily practices drilled into every worker. Stanley didn't just transfer technology; they transferred an entire manufacturing philosophy. Indian engineers were sent to Japan for months-long training programs, returning with not just technical knowledge but a fundamentally different approach to manufacturing excellence.

But the real masterstroke came with the gear shifter opportunity. Sometime in the early 2000s, as India's passenger vehicle market began its explosive growth, Lumax identified a critical gap: gear shifters were either imported (expensive) or made locally with inconsistent quality. The company partnered with Mannoh Industrial Company of Japan, creating a joint venture specifically for gear shift systems.

This wasn't a random diversification. Gear shifters sit at the intersection of mechanical precision and driver experience—you touch them constantly, they need to feel right, work flawlessly for years, yet cost almost nothing to produce once you achieve scale. It was the perfect product for Lumax's emerging strategy: find critical but unglamorous components where technology partnerships could create dominant market positions.

The Mannoh JV was structured brilliantly. The Japanese brought design capabilities and precision manufacturing knowledge. Lumax brought customer relationships, low-cost manufacturing, and deep understanding of Indian driving conditions (dusty, hot, with drivers who weren't always gentle with their gear shifts). Together, they created products specifically engineered for Indian conditions but manufactured to global quality standards.

Then came 2007, and another strategic partnership that showcased Lumax's evolving sophistication. The company formed a joint venture with Cornaglia Group of Italy for emission systems, anticipating the tightening emission norms that would sweep through India over the next decade. While competitors were still focused on current products, Lumax was positioning for regulations that wouldn't fully hit until years later.

What made these partnerships work when so many Indo-foreign JVs failed? First, the Jains understood cultural nuances. With Japanese partners, they emphasized precision, punctuality, and process—showing up to meetings minutes early, following up with detailed documentation, never surprising partners with bad news. With Italian partners, relationships came first—long dinners, family introductions, building personal trust before business trust.

Second, they never tried to be something they weren't. In every partnership, Lumax positioned itself as the local execution expert, not the technology leader. They didn't pretend to match their partners' R&D capabilities; instead, they offered something equally valuable: the ability to take sophisticated products and manufacture them at price points that made sense for India while maintaining quality standards that satisfied global partners.

Third, and perhaps most importantly, they chose partners carefully. Every partnership filled a specific capability gap or product white space. They weren't collecting joint ventures like trophies; they were assembling a portfolio of capabilities that would make them indispensable to Indian OEMs.

The philosophy was simple but powerful: why spend billions developing technology that already exists when you can partner with the best and focus on what you do best—manufacturing excellence and customer relationships? It's a lesson many Indian companies still haven't learned, burning cash on R&D for products where they have no competitive advantage.

By the late 2000s, Lumax had transformed from a family-run lighting supplier to a sophisticated multi-product component manufacturer with technology access that rivaled companies ten times its size. But the real test of this partnership model would come with their push into gear shifters—a market they would come to dominate so thoroughly that even global giants would struggle to compete. That transformation from partner to dominant player is where our story turns next.

IV. The Gear Shifter Dominance Story (2000s-Present)

In 2003, inside Maruti Suzuki's Gurgaon facility, a procurement manager faced a problem that would define Lumax's next two decades. The Swift, Maruti's ambitious global car for India, needed a gear shifter that could handle Indian conditions—extreme heat, dust, aggressive shifting by drivers used to motorcycles—while meeting Suzuki's exacting global quality standards. Imports were too expensive. Local suppliers couldn't meet the quality bar. Enter Lumax, with their Mannoh partnership and a promise: Japanese quality at Indian prices.

Fast forward to today: Lumax commands more than 80% market share in gear shifters across all passenger vehicle customers in India. Think about that dominance—eight out of every ten cars rolling off Indian assembly lines have their gear shifters made by one company. In the cutthroat world of auto components, where OEMs squeeze suppliers for every rupee, how did Lumax build such an impregnable moat?

The answer lies in understanding what a gear shifter really is. It's not just a mechanical lever—it's a complex system involving cables, bushings, joints, and increasingly, electronic sensors and actuators. It needs to work flawlessly for 15 years, in temperatures from -10°C in Ladakh to 50°C in Rajasthan, through monsoons and dust storms, while maintaining precise feel and throw. And here's the kicker: consumers notice immediately when it doesn't feel right, but it needs to cost less than a good restaurant meal.

Lumax's dominance strategy unfolded in three acts. Act One was about proving they could deliver Suzuki-level quality consistently. The Swift program became their calling card. They didn't just meet specifications; they exceeded them. Rejection rates that were industry-standard at 500 parts per million, Lumax drove down to under 50. When Maruti engineers visited the plant, they found Japanese-style visual management systems, workers who could explain statistical process control, and a quality culture that rivaled Suzuki's own suppliers in Japan.

Act Two was about scale and scope. Having proven themselves with manual transmissions, Lumax aggressively expanded into automatic, AMT (Automated Manual Transmission), and CVT (Continuously Variable Transmission) shifters. Each technology required different capabilities—AMTs needed electronic integration, automatics required hydraulic expertise, CVTs demanded precision manufacturing. Rather than developing these in-house, Lumax leveraged their partnership model, bringing in technology from Mannoh while adapting it for Indian conditions.

The masterstroke was recognizing that India's shift to automatic transmissions would be different from developed markets. While the US went straight to full automatics, India would take an intermediate step through AMTs—essentially manual gearboxes with automated clutch and shift operations. Cheaper than full automatics but offering the convenience of two-pedal driving. Lumax positioned perfectly for this transition, becoming the go-to supplier for AMT shifters just as Maruti launched the Celerio with AMT technology.

Act Three, playing out now, is about creating switching costs so high that even if competitors offered lower prices, OEMs wouldn't switch. Here's how they did it: Lumax embedded their engineers directly into OEM design centers. When Mahindra designs a new SUV or Tata develops a new sedan, Lumax engineers are there from day one, designing the shifter system in parallel with the vehicle. By the time the vehicle is ready for production, the shifter isn't just a component—it's an integral part of the vehicle architecture.

The numbers tell the dominance story. With 30 manufacturing facilities across 7 states, Lumax ensures they're always within hours of every major OEM plant. Just-in-time delivery isn't just a concept—it's a competitive weapon. When an OEM's assembly line needs shifters, Lumax delivers them in sequence, in the exact order needed for the production schedule. Miss one delivery, and you can shut down a plant costing millions per hour. This reliability, built over decades, is worth more than any price advantage a competitor might offer.

But perhaps the most underappreciated aspect of their dominance is the aftermarket. Every gear shifter that fails after warranty needs replacement. With 80% market share in OEM supply, Lumax has a natural monopoly in replacements. Mechanics trust the brand, spare parts dealers stock it by default, and the margins are significantly better than OEM supply. It's a virtuous cycle—OEM dominance drives aftermarket dominance, which provides cash flows to maintain OEM competitiveness.

The competitive dynamics are fascinating. Global giants like ZF or Magna could theoretically enter the Indian market. But the math doesn't work. The entire Indian gear shifter market is worth perhaps ₹2,000 crores annually. For a global player, that's not worth the investment in local manufacturing, supplier development, and customer relationships. For Lumax, it's a core business worth defending at any cost.

Chinese competitors pose a different threat—they have the scale and cost structure. But gear shifters aren't smartphones. You can't just ship them from China. They need local inventory, immediate engineering support, and the ability to respond to running design changes. By the time a Chinese player builds these capabilities, Lumax has moved on to the next generation of products.

The question every investor asks: What happens when EVs eliminate gear shifters entirely? It's a valid concern, but the timeline might surprise you. Even in the most aggressive EV adoption scenarios, India will have tens of millions of ICE and hybrid vehicles on the road through 2040. And here's what most miss—even EVs need selector mechanisms for park, reverse, and drive modes. The technology changes, but the need for human-machine interface remains.

With more than 80% market share, Lumax hasn't just dominated a product category—they've turned a commodity component into a strategic moat. But dominance in one product, no matter how complete, is dangerous in the fast-evolving auto industry. Which is why, even as they cemented their gear shifter monopoly, Lumax was quietly executing a diversification strategy that would transform them from a component supplier into an integrated systems provider.

V. The Great Diversification: Beyond Gear Shifters (2010s)

The boardroom discussion at Lumax headquarters in 2010 must have been intense. The company had just achieved dominant market share in gear shifters, revenues were growing steadily, and profits were healthy. The easy decision would have been to milk this cash cow. Instead, the Jain family asked a different question: "What happens when the music stops?" They saw what others missed—technological disruption wasn't a distant threat but an approaching reality. The answer? Transform from a product company to a systems integrator before disruption forced their hand.

The diversification strategy that unfolded over the next decade wasn't random expansion—it was a carefully orchestrated move into adjacent technologies that shared three characteristics: they leveraged existing customer relationships, they required similar manufacturing capabilities, and they positioned Lumax for the inevitable shift to connected and electric vehicles.

Take the expansion into air intake systems. On the surface, it seems unrelated to gear shifters. But dig deeper: both are critical powertrain components, both require precision plastic molding and assembly, both are designed in conjunction with the base vehicle platform. When Lumax approached Mahindra about supplying air intake systems, they weren't a new vendor—they were a trusted partner extending their capability set. The conversation wasn't about price; it was about reducing vendor complexity for the OEM.

The partnership strategy, refined during the gear shifter dominance years, went into overdrive. In 2016, Lumax signed with FAE, a Spanish company specializing in oxygen sensors. But this wasn't just another distribution agreement. Lumax took 51% ownership in the venture, with plans for 2 million unit capacity. Why oxygen sensors? Because every BS-VI compliant vehicle would need them. While competitors were still debating BS-VI strategies, Lumax had already locked in the technology and capacity.

Then came the Yokowo joint venture for antenna systems—a 50:50 partnership with one of Japan's leading connectivity component manufacturers. This looked like an odd move until you understood the thesis: every connected car needs multiple antennas for GPS, cellular, WiFi, and emergency calling. The Yokowo JV positioned Lumax for the connected vehicle revolution, giving them technology access that would take years to develop independently.

The JOPP partnership from Germany brought transmission components expertise—gear shift towers, AMT kits, and other drivetrain components. Alps Alpine partnership added electronic components capabilities. Each partnership was a chess move, positioning Lumax for a future where mechanical components would increasingly integrate with electronic systems.

What's remarkable is how Lumax structured these diversifications. They didn't try to be everything to everyone. Instead, they focused on what one executive called "profitable complexity"—products that were complex enough to deter new entrants but not so complex that they required massive R&D investments. Urea tanks for diesel vehicles? Not sexy, but every BS-VI diesel vehicle needs them, and once you're designed in, switching suppliers is painful. Plastic modules for interiors? Commoditized individually, but when integrated into complete cockpit systems, they become sticky.

The manufacturing footprint expansion during this period was strategic, not scattershot. New facilities were added to reach 30 plants across 7 states, but each location was chosen for proximity to customer plants or access to specific capabilities. The Pune facility focused on electronics integration. The Chennai plant specialized in plastic molding. The Gurgaon technical center became the nerve center for design and development.

The financial discipline during this diversification is worth noting. Unlike many Indian companies that funded expansion through debt, Lumax used operational cash flows and partner contributions. Each JV partner brought not just technology but also capital and customer relationships. The Spanish brought European customers. The Japanese brought quality systems. The Germans brought precision manufacturing expertise.

By 2015, a fascinating transformation had occurred. Lumax was no longer a gear shifter company that did other things. They had become an integrated interior and powertrain systems provider. When Tata Motors designed the Nexon, they didn't call Lumax for gear shifters—they called them for complete interior modules, transmission systems, and electronic components. The customer conversation had shifted from component pricing to system integration.

The product portfolio by decade-end was staggering: intake systems, integrated plastic modules, aerospace and defence engineering services, 2-wheeler chassis & lighting, gear shifters, seat structures and mechanisms, electrical and electronics components. But more important than the breadth was the interconnection. A modern vehicle interior isn't just plastic panels and metal frames—it's an integrated system of structures, electronics, and interfaces. Lumax could now offer complete solutions, not just components.

The skeptics argued this diversification would dilute focus and margins. The opposite happened. System integration commanded higher margins than individual components. Customer stickiness increased—it's one thing to replace a gear shifter supplier, quite another to replace your entire interior systems provider. And critically, the diversification created optionality for whatever future emerged—electric, autonomous, or shared.

But the real test of this strategy would come with the technology transitions of the late 2010s—BS-VI emission norms, the push toward electric vehicles, and the emergence of connected car technologies. How Lumax navigated these transitions, turning potential threats into opportunities, reveals the true genius of their diversification strategy.

VI. The EV & Connected Vehicle Pivot (2018-Present)

The auto component graveyard is littered with companies that ignored technology transitions until too late. Kodak and digital photography. Nokia and smartphones. The list goes on. In 2018, as India's auto industry grappled with BS-VI transitions and nascent EV adoption, Lumax faced their Kodak moment: evolve or become irrelevant. Their response would determine whether the company joined the graveyard or emerged stronger.

The pivot started not in India but in China, where the electric vehicle revolution was already underway. In 2019, while Indian manufacturers were still debating whether EVs were real, Lumax executives were in Changzhou, negotiating with Ananda Drive Techniques. The resulting MoU for EV motors and controllers wasn't just another partnership—it was an acknowledgment that the future had already arrived, just unevenly distributed.

But Lumax understood something crucial: the transition to EVs wouldn't be binary. India wouldn't wake up one day with all electric vehicles. Instead, there would be a long, messy transition with hybrids, mild hybrids, CNG variants, and multiple powertrain technologies coexisting. This insight shaped their strategy—not to abandon ICE components but to build capabilities for whatever mix emerged.

The connected vehicle play was equally strategic. Through their Ituran partnership, Lumax entered telematics and fleet management—seemingly far from their mechanical components heritage. But think about it: modern vehicles generate gigabytes of data daily. Someone needs to collect, transmit, and process this data. Why not the company already integrated into every major OEM's supply chain?

With advanced technologies related to safety, sensors, telematics, fleet management, auto cruise, navigation, parking assistance, infotainment and anti-theft systems expected to drive growth, Lumax positioned itself at the intersection of mechanical and digital. They weren't trying to become a software company—that would be foolish. Instead, they became the integration layer between digital systems and physical vehicles.

The BS-VI transition, which destroyed many smaller suppliers, became a growth opportunity for Lumax. The company was well-prepared to counter the challenges with the implementation of the BS-VI emission norms. Every BS-VI vehicle needed new emission control components, sensors, and systems. Lumax's earlier partnerships, particularly in oxygen sensors and emission systems, paid off handsomely. While competitors scrambled for technology access, Lumax was already shipping BS-VI compliant components.

The R&D transformation during this period deserves attention. The company established 2 advanced Engineering Centres and dramatically increased engineering headcount. But this wasn't R&D for research's sake. Every project had a customer commitment or clear market opportunity. They weren't trying to invent the next breakthrough technology—they were fast followers, taking proven technologies and adapting them for Indian conditions and price points.

The ADAS (Advanced Driver Assistance Systems) strategy exemplifies this approach. Rather than developing proprietary ADAS technology—a fool's errand given the billions being invested by global tech giants—Lumax focused on being the integration partner. When OEMs wanted to add lane departure warnings or automatic emergency braking, Lumax could integrate sensors, actuators, and control systems into vehicle platforms. They owned the integration capability, not the underlying technology.

The investment in electric vehicle components accelerated through 2020-2023. Motor controllers, battery management systems, thermal management solutions—all areas where Lumax built capabilities through partnerships rather than indigenous development. The strategy was consistent: partner for technology, own the manufacturing and integration.

What's fascinating is how Lumax managed investor expectations during this transition. The narrative could have been defensive—"we're pivoting because our core products are under threat." Instead, they positioned it as offensive expansion—"we're adding capabilities to serve our customers better." The stock market responded positively, with valuations expanding as investors saw a company managing transition rather than being managed by it.

The recent order wins validate this strategy. When Mahindra designed their BE and XEV electric platforms, they needed suppliers who could deliver both traditional components and EV-specific systems. Lumax could offer both, plus the integration capabilities to make them work together. It's one thing to supply a battery pack or motor controller; it's another to ensure they integrate seamlessly with vehicle systems you've been supplying for decades.

By 2023, Lumax had transformed from a mechanical components supplier to what industry insiders call a "tier 0.5" supplier—not quite the full vehicle integrator role of a tier 0.5 like Magna, but far beyond traditional tier-1 capabilities. They could take entire vehicle subsystems—complete interiors, integrated cockpits, powertrain modules—and deliver them ready for final assembly.

The connected vehicle capabilities deserve special mention. Through partnerships and acquisitions, Lumax built capabilities in vehicle-to-everything (V2X) communication, over-the-air updates, and predictive maintenance. These aren't products you can see or touch, but they're becoming as essential as gear shifters or headlamps. And critically, they create recurring revenue streams through software updates and services—a fundamental shift from one-time component sales.

But perhaps the most important element of the EV pivot was what Lumax didn't do. They didn't bet the company on any single technology. They didn't try to become a battery manufacturer or charging infrastructure provider—areas where they had no competitive advantage. They stayed true to their core competence: being the best manufacturing and integration partner for whatever technology emerged.

The question now isn't whether Lumax can survive the EV transition—they've already proven they can. The question is whether they can maintain their margins and market position as the industry structure fundamentally changes. And that's where their recent strategic acquisitions come into play.

VII. Recent Moves & Strategic Acquisitions (2020-2025)

The Mahindra headquarters in Mumbai, early 2024. In a closed-door meeting, senior executives are reviewing suppliers for their ambitious BE6 and XEV 9e electric vehicles—products that would define Mahindra's electric future. They needed someone who could deliver integrated cockpits combining traditional craftsmanship with cutting-edge digital interfaces. The winner? Lumax, through their strategic acquisition of IAC India, had become the sole supplier for these critical components. This wasn't just another supply contract—it was validation of Lumax's transformation from component supplier to systems integrator.

The IAC India acquisition exemplified Lumax's evolved M&A strategy. They weren't buying revenues or market share—they were acquiring capabilities that would take years to build organically. IAC brought expertise in complete interior systems, from design to manufacturing, with established relationships with global OEMs. Post-acquisition, Lumax didn't just own another factory—they owned the capability to conceptualize, design, and deliver complete vehicle interiors.

But the move that really showcased strategic foresight was the Greenfuel Energy Solutions acquisition. In 2024, while everyone obsessed over battery-electric vehicles, Lumax made a contrarian bet on alternative fuels. The logic was compelling: India's energy transition wouldn't be monolithic. Commercial vehicles would likely adopt CNG and hydrogen. Rural markets might embrace biofuels. The passenger vehicle market would fragment across multiple technologies. Greenfuel gave Lumax exposure to all these alternatives without betting everything on one.

The COVID-19 pandemic, which devastated many auto suppliers, became a catalyst for Lumax's strategic acceleration. While competitors conserved cash, Lumax went shopping—acquiring distressed assets at attractive valuations, hiring talent from struggling competitors, and investing in digitalization when others were cutting costs. The pandemic taught them that supply chain resilience mattered more than efficiency. Their response? Localize more, diversify supplier bases, and maintain higher inventory buffers—sacrificing some working capital efficiency for reliability.

The aftermarket expansion during this period deserves attention. Historically, OEM suppliers treated aftermarket as an afterthought—lower volumes, fragmented distribution, collection challenges. Lumax flipped this thinking. They recognized that every vehicle they supplied to would eventually need replacement parts. With millions of vehicles on the road containing Lumax components, the aftermarket wasn't just an opportunity—it was an annuity stream.

The financial performance during this period validated the strategy. Revenue reached ₹3,907 Cr with profit of ₹242 Cr, demonstrating that diversification hadn't come at the cost of profitability. More importantly, the revenue mix had shifted. In 2020, gear shifters and lighting dominated revenues. By 2025, integrated systems, electronic components, and aftermarket sales contributed meaningfully, reducing dependence on any single product line.

The record revenues in FY2025 tell only part of the story. The group achieved brand revenue of Rs 10,045 Crores, but the composition of these revenues had fundamentally changed. High-margin electronic components, recurring software revenues, and system integration fees now supplemented traditional component sales. The business model had evolved from selling products to selling solutions.

What's particularly impressive is how Lumax managed working capital during this expansion. Auto component businesses typically suffer from elongated working capital cycles—OEMs pay late, inventory needs are high, suppliers demand advance payments. Lumax turned this challenge into competitive advantage. They negotiated better terms with global partners (who valued India access over payment terms), implemented vendor financing programs, and used their scale to optimize inventory across facilities.

The strategic positioning for 2025 and beyond reveals long-term thinking. While others chase the latest hot trend—whether EVs, autonomous vehicles, or shared mobility—Lumax positioned for all scenarios. Their integrated cockpits work in EVs and ICE vehicles. Their sensors and electronic components are needed whether cars are human-driven or autonomous. Their aftermarket presence generates cash regardless of new vehicle sales.

The recent customer wins validate this positioning. Beyond the Mahindra EV programs, Lumax secured positions on multiple upcoming platforms across OEMs. But more importantly, they've moved up the value chain. They're no longer competing on price for commodity components—they're strategic partners in vehicle development, involved from concept to production.

The international expansion, while measured, shows ambition. With 2 overseas design centers in Taiwan and the Czech Republic, Lumax is building capabilities to serve global programs. They're not trying to compete with Bosch or Continental globally—that would be suicidal. Instead, they're positioning as the partner of choice for global OEMs' Indian operations, with the capability to support global programs where needed.

Looking at these recent moves collectively, a pattern emerges. Lumax isn't trying to predict the future—they're building optionality for multiple futures. Every acquisition, every partnership, every investment creates options that can be exercised depending on how the market evolves. It's portfolio theory applied to strategic planning, and it's why Lumax has not just survived but thrived through multiple technology transitions. But strategy without execution is hallucination. The real test is whether these moves translate into sustainable financial performance.

VIII. Financial Performance & Unit Economics

Numbers tell stories, and Lumax's financial evolution narrates a masterclass in capital allocation and operational excellence. With a market cap of ₹6,848 Crore (up 93.0% in 1 year), revenue of ₹3,907 Cr, and profit of ₹242 Cr, the headline numbers are impressive. But the real story lies in the margins, returns, and capital efficiency metrics that separate great businesses from merely good ones.

Let's start with the market cap journey. A near-doubling in one year might seem like frothy speculation, but dig deeper and it's a rerating based on fundamental business transformation. The market is no longer valuing Lumax as a cyclical auto component supplier but as a diversified systems integrator with multiple growth drivers. The P/E ratio of 37.2 might seem expensive compared to traditional auto component companies trading at 15-20x, but it's reasonable for a company with Lumax's growth profile and competitive position.

The return metrics tell the efficiency story. With ROCE of 19.0% and ROE of 20.2%, Lumax generates returns well above their cost of capital. In an industry where 12-15% returns are considered good, Lumax's 20% returns reflect pricing power, operational efficiency, and intelligent capital deployment. These aren't financial engineering tricks—they're the result of dominant market positions and disciplined execution.

The book value of ₹137 compared to the market price shows the market values Lumax at about 7.5 times book—seemingly expensive until you realize that book value dramatically understates the economic value of customer relationships, technology partnerships, and market positions built over decades. The accounting value of a 30-year relationship with Maruti? Zero. The economic value? Priceless.

The margin evolution reveals the strategic transformation. In 2015, Lumax operated with EBITDA margins around 8-9%, typical for component suppliers. Today, margins exceed 12%, approaching the 13-15% range of specialized system integrators. This margin expansion didn't come from cost cutting—it came from mix improvement, value addition, and pricing power from dominant market positions.

Working capital management deserves special attention. Auto component businesses typically struggle with working capital—OEMs demand 60-90 day payment terms while suppliers want advance payments. Lumax turned this squeeze into advantage. Their scale allows negotiation of better terms with suppliers. Their reliability earns better terms from customers. The result? Cash conversion cycles that are among the best in the industry, generating free cash flow even during rapid growth.

The capital allocation framework is remarkably disciplined. Organic growth investments focus on capacity expansion near customer plants—low risk, quick payback. Technology investments happen through partnerships, sharing both cost and risk. Acquisitions are opportunistic, buying distressed assets or strategic capabilities at attractive valuations. Dividends maintain consistency, signaling confidence without starving growth investments.

Promoter holding at 56.0% creates interesting dynamics. The Jain family's continued majority ownership aligns long-term thinking with minority shareholders' interests. They're not managing for quarterly earnings but for generational wealth creation. This shows in decisions like investing in EV capabilities before the market was ready, or maintaining R&D spending during downturns.

The segment-wise performance reveals portfolio strength. While gear shifters remain the cash cow with 40%+ EBITDA margins in a dominated market, newer segments like electronic components and integrated systems grow faster albeit at lower initial margins. The aftermarket business, often undisclosed in detail, likely generates the highest margins given minimal working capital needs and pricing power from captive demand.

Lumax's financial resilience through cycles is remarkable. During the 2019-2020 auto slowdown, when industry volumes declined 20%, Lumax maintained profitability through cost management and mix improvement. During COVID, when plants shut for months, they conserved cash without compromising strategic investments. During the semiconductor shortage of 2021-2022, their diversified supplier base and inventory buffer helped maintain supplies when competitors struggled.

The balance sheet strength enables strategic flexibility. Low debt, strong cash generation, and access to partner capital means Lumax can move quickly on opportunities. When IAC India became available, they could close quickly. When EV investments were needed, they had the resources. This financial flexibility is a competitive weapon in an industry where many players are leveraged and capital-constrained.

International revenue exposure, while limited, is growing strategically. Rather than chasing export volumes at low margins, Lumax focuses on high-value components for specific programs. The overseas design centers support these efforts, creating intellectual property that commands premium pricing. The strategy isn't to become an export powerhouse but to selectively participate in global programs where they have unique advantages.

The valuation debate is fascinating. Bears argue the P/E of 37 is excessive for an auto component company. Bulls counter that Lumax isn't just an auto component company anymore—it's a technology-enabled manufacturing platform with dominant market positions and multiple growth optionals. The truth, as always, lies somewhere in between. The valuation embeds expectations of successful EV transition, continued market share gains, and margin expansion. Possible? Yes. Guaranteed? No.

Looking forward, the financial model has interesting dynamics. Revenue growth should track vehicle production plus content per vehicle increase plus aftermarket expansion. Margins should expand with mix improvement and operating leverage. Returns should remain robust given the asset-light partnership model. The key risk? Technology disruption that makes current capabilities obsolete faster than new ones can be built.

IX. Playbook: The Tier-1 Supplier Success Formula

After decades of studying Lumax's evolution, a clear playbook emerges for building a successful tier-1 automotive supplier in emerging markets. It's not about breakthrough innovation or massive capital—it's about strategic positioning, partnership leverage, and relentless execution. This playbook, refined over 40 years, offers lessons not just for auto component companies but for any manufacturing business in a rapidly evolving industry.

Lesson 1: Technology Partnerships vs. Indigenous Development

The fundamental insight: in automotive components, being second with proven technology beats being first with unproven innovation. Lumax never tried to out-innovate Bosch or Continental. Instead, they became the best at taking proven technologies and adapting them for Indian conditions. With 9 global partnerships and 1 technical agreement, they assembled a technology portfolio that would cost billions to develop independently.

The partnership selection criteria is crucial. Choose partners who are leaders in their niche but lack India presence. Structure deals where both parties win—technology for market access. Ensure knowledge transfer, not just product supply. And critically, maintain multiple partnerships to avoid dependence while preventing partners from competing with each other.

Lesson 2: The "Fast Follower" Advantage

Lumax perfected the art of being a fast follower. When automatic transmissions emerged, they didn't try to develop proprietary technology. They partnered with Mannoh and became the manufacturing expert. When emission norms tightened, they partnered with Cornaglia. When connectivity became important, they partnered with Yokowo. Each time, they let others bear the R&D cost and risk, then executed better manufacturing and localization.

This isn't about lacking innovation—it's about intelligent capital allocation. Why spend ₹100 crores developing technology that exists when you can license it for ₹10 crores and focus on manufacturing excellence? The saved capital goes into capacity, quality systems, and customer relationships—investments that actually create competitive advantage.

Lesson 3: Building Switching Costs Through Engineering Integration

The genius of Lumax's customer stickiness strategy is making themselves indispensable at the design stage. By embedding engineers in OEM design centers, they influence specifications to leverage their capabilities. By the time production starts, switching suppliers would require redesigning entire systems. With 2 advanced Engineering Centres and hundreds of engineers, they've built technical intimacy that pure manufacturing competitors can't match.

Lesson 4: Geographic Proximity as Competitive Advantage

30 manufacturing facilities across 7 states isn't just about capacity—it's about being within hours of every customer plant. In automotive, where production lines can't stop, proximity equals reliability. Lumax understood that being 100 kilometers away with 99% quality beats being 1000 kilometers away with 99.9% quality. This distributed manufacturing also provides supply chain resilience—if one plant faces issues, others can compensate.

Lesson 5: Balancing OEM and Aftermarket

Most suppliers see aftermarket as secondary. Lumax recognized it as strategic. Every component supplied to OEMs creates future aftermarket demand. With dominant OEM market share, they have natural aftermarket advantages—brand recognition, distribution presence, and technical support infrastructure. The aftermarket provides higher margins, cash sales, and recession resilience—balancing the OEM business's cyclicality and payment terms.

Lesson 6: Managing Multiple Stakeholders

Running multiple joint ventures requires diplomatic skills rivaling international relations. Japanese partners value process and precision. European partners emphasize innovation and design. Indian customers demand cost competitiveness. Employees need growth opportunities. Investors want returns. The Jain family mastered stakeholder management, giving each what they value most while maintaining strategic control.

Lesson 7: Capital Allocation Discipline

Every rupee invested must generate returns above cost of capital. Capacity expansion happens only with confirmed customer orders. Technology investments happen through partnerships, sharing risk and cost. Acquisitions must be immediately accretive or strategically essential. Dividends maintain consistency without starving growth. This discipline, maintained over decades, compounds into superior returns.

Lesson 8: The Moat Deepening Strategy

Lumax's moat isn't one big advantage but multiple small ones that compound. Manufacturing excellence makes them reliable. Engineering integration makes them sticky. Geographic distribution makes them responsive. Technology partnerships make them capable. Scale gives them cost advantages. Together, these create a moat that's nearly impossible to replicate.

Lesson 9: Timing Technology Transitions

The key to managing disruption is moving neither too early nor too late. Move too early, and you waste capital on unproven technologies. Move too late, and you become obsolete. Lumax's timing has been masterful—entering emissions components just before BS-VI, building EV capabilities as adoption accelerates, investing in connectivity as cars become computers. They're not trying to time perfectly—they're building options to exercise when timing becomes clear.

Lesson 10: Cultural DNA

Perhaps most importantly, Lumax built a culture that balances entrepreneurial aggression with operational discipline. They move fast on opportunities but execute with precision. They embrace technology but respect manufacturing fundamentals. They think globally but act locally. This cultural DNA, embedded over generations, might be their most sustainable advantage.

The playbook sounds simple, but execution is extraordinarily difficult. It requires patient capital, long-term thinking, and the ability to manage complexity without losing focus. Most companies fail because they violate one or more principles—chasing growth without discipline, pursuing technology without advantage, or expanding without integration.

For investors, the playbook provides a framework for evaluating auto component companies. Does the company have technology access or just manufacturing capability? Are they integrated into customer design or just production? Do they have multiple growth drivers or dependence on single products? Are they building switching costs or competing on price?

The Lumax playbook isn't just history—it's a guide for navigating the industry's future. As automotive transforms with electrification, autonomy, and new mobility models, the principles remain relevant. Partner for technology, excel at execution, integrate with customers, and maintain financial discipline. Simple principles, extraordinary outcomes.

X. Bear vs. Bull Case & Future Outlook

Every investment thesis has two sides, and Lumax presents a fascinating debate between structural transformation bulls and disruption bears. The stock's near-doubling in a year has sharpened these divisions. Let's examine both cases with the rigor they deserve, because in the tension between these views lies the true investment opportunity—or trap.

The Bull Case: A Transformation Story Hidden in Plain Sight

Bulls see Lumax as a classic case of market misperception. The market still views it as a gear shifter company vulnerable to EV disruption, but bulls argue it's already transformed into a diversified systems integrator with multiple growth engines.

Start with the market position. 80%+ market share in gear shifters isn't just dominance—it's a monopolistic position that generates cash to fund transformation. Even in pessimistic EV adoption scenarios, India will produce 5+ million ICE vehicles annually through 2035. That's a 15-year cash flow stream from just the core business, ignoring growth from other segments.

The partnership portfolio is the hidden asset. 9 global partnerships provide technology access that would cost billions to develop independently. As vehicles become more complex—ADAS, connectivity, electrification—Lumax can tap partner expertise rather than making massive R&D bets. It's like having call options on multiple technologies without paying full premium.

Bulls emphasize the EV opportunity, not threat. Yes, EVs eliminate traditional gear shifters, but they need battery management systems, thermal management, electronic controls, and human-machine interfaces. Lumax is positioned for all of these through partnerships and acquisitions. The IAC acquisition making them sole supplier for Mahindra's flagship EVs validates this transition.

The financials support the transformation story. ROE of 20.2% and ROCE of 19.0% aren't achievable by commodity component suppliers. These returns reflect pricing power, competitive advantages, and intelligent capital allocation. The margin expansion from 8% to 12%+ demonstrates successful value addition, not just cost cutting.

India's auto market growth provides tailwind for decades. From 4 million vehicles annually today to potentially 10 million by 2035, driven by rising incomes, infrastructure development, and urbanization. Lumax benefits from both volume growth and content per vehicle increase as cars become more sophisticated.

The aftermarket opportunity is vastly underappreciated. With millions of vehicles on roads containing Lumax components, the replacement demand creates an annuity stream. As vehicles age and warranties expire, aftermarket margins typically exceed OEM supply by 500-1000 basis points.

Bulls point to management quality. The Jain family's patient capital approach, proven execution over decades, and successful navigation of multiple technology transitions inspire confidence. With 56% promoter holding, they're aligned with minority shareholders for long-term value creation.

The valuation, while optically expensive at 37x P/E, is reasonable for a company with Lumax's growth profile, margins, and competitive position. Compare it to global auto suppliers like Aptiv or Visteon trading at similar multiples with lower growth potential.

The Bear Case: Disruption Risk and Valuation Concerns

Bears see a different story—a company with legacy products facing existential threats, trading at valuations that assume perfect execution in an uncertain future.

The EV disruption is real and accelerating. Every EV sold is one less ICE vehicle needs gear shifters. While the transition timeline is debatable, the direction is clear. Tesla's India entry, Tata's aggressive EV push, and government mandates could accelerate adoption faster than expected. Lumax's core product could become obsolete sooner than bulls anticipate.

Customer concentration is concerning. Dependence on Indian OEMs—Maruti, Tata, Mahindra—creates vulnerability. If any major customer brings components in-house or switches suppliers, the impact would be severe. The 80% market share in gear shifters sounds impressive until you realize it means nowhere to go but down.

Chinese competition is intensifying. Chinese suppliers have scale, technology, and cost advantages. As Indian OEMs face pressure to reduce costs, especially in EVs where battery costs dominate, they might turn to Chinese suppliers despite geopolitical tensions. Lumax's margins could face severe pressure.

The partnership model has limitations. While partnerships provide technology access, they also mean sharing profits and control. As partners gain India experience, they might go direct or find other local partners. The technology dependence creates vulnerability if partnerships sour.

Execution risk in new areas is real. Transitioning from mechanical components to electronic systems isn't trivial. Software, semiconductors, and systems integration require different capabilities than metal bending and plastic molding. Many traditional suppliers have failed this transition.

The valuation leaves no room for error. At 37x earnings, the market expects perfect execution. Any disappointment—margin pressure, market share loss, execution stumbles—could trigger significant multiple compression. The risk-reward seems skewed negatively.

Bears worry about capital allocation. The recent acquisitions and expansions require significant investment. If returns don't materialize as expected, ROE and ROCE could deteriorate, destroying value despite revenue growth.

The Pragmatic View: Probabilities and Scenarios

Reality likely lies between these extremes. The transformation is real but challenging. The disruption is coming but gradually. The key is assigning probabilities to different scenarios.

Scenario 1: Successful Transformation (40% probability) Lumax successfully pivots to EVs and electronics, maintaining margins and market position. The stock doubles again over five years. This requires flawless execution, continued partnership success, and gradual EV adoption.

Scenario 2: Managed Decline (35% probability) Core business declines gradually while new businesses grow, resulting in flattish revenues but margin pressure. The stock trades sideways, providing modest returns from dividends and buybacks.

Scenario 3: Disruption Acceleration (25% probability) EV adoption accelerates, Chinese competition intensifies, and margins collapse. The stock corrects 40-50% as multiples compress to reflect a melting ice cube business.

The investment decision depends on your assessment of these probabilities and your risk tolerance. For growth investors believing in India's auto story and Lumax's execution capabilities, the risk-reward might be attractive. For value investors concerned about valuation and disruption risks, waiting for a better entry point might be prudent.

XI. Epilogue: What This Means for Indian Manufacturing

As we close this deep dive into Lumax's seven-decade journey, it's worth stepping back to consider what this story means for Indian manufacturing, capital markets, and the broader economy. Lumax isn't just another auto component supplier—it's a template for how Indian companies can build global competitiveness without global scale.

The untold story of India's auto component champions like Lumax is that they've quietly built world-class capabilities while everyone focused on IT services and consumer brands. The Lumax group's ₹10,045 crores revenue might seem modest compared to TCS or Reliance, but the manufacturing expertise, partnership management, and engineering capabilities they've built are arguably harder to replicate.

For Indian manufacturing, Lumax demonstrates that competing with China doesn't require matching their scale or cost structure. Instead, it's about finding niches where local presence, engineering integration, and customer intimacy matter more than pure cost. Lumax doesn't compete with Chinese suppliers on commodity components—they compete on integrated systems where switching costs are high and local support is critical.

The partnership model offers lessons for other industries. Rather than pursuing expensive indigenous development or accepting permanent technology dependence, Lumax shows how to use partnerships as stepping stones to capability building. Start as manufacturer, evolve to design partner, eventually become system integrator. It's a playbook relevant for everything from semiconductors to renewable energy.

The role of patient capital cannot be overstated. The Jain family's multi-generational commitment enabled long-term thinking that public markets rarely support. They invested in capabilities years before they generated returns. They maintained R&D spending during downturns. They prioritized market position over short-term margins. This patient capital approach, increasingly rare in quarterly capitalism, might be India's secret weapon against more financially engineered competitors.

For investors, Lumax illustrates the importance of looking beyond obvious narratives. The market spent years worrying about EV disruption while missing the transformation already underway. The best investments often hide in plain sight, obscured by outdated mental models and surface-level analysis.

The next decade will test whether the Lumax model is replicable and scalable. As India pushes for "Atmanirbhar Bharat" (self-reliant India), the temptation will be to pursue complete indigenous development. Lumax suggests a different path—strategic interdependence where India provides manufacturing excellence and market access while leveraging global technology. It's not as politically appealing as complete self-reliance, but it's more practical and capital efficient.

The broader implication for India's economic development is profound. If India can replicate the Lumax model across industries—pharmaceuticals, electronics, machinery—it could build a manufacturing economy that's complementary to, rather than competitive with, China. Instead of racing to the bottom on costs, India could occupy the middle ground of specialized, integrated manufacturing that requires engineering expertise and customer intimacy.

For the auto industry specifically, companies like Lumax will play a crucial role in India's EV transition. Global OEMs won't build everything locally. Chinese suppliers face trust deficits. Someone needs to bridge global technology with local manufacturing. Lumax and peers like Sona Comstar, Sandhar Technologies, and Endurance Technologies are positioning for this role.

The cultural lessons are equally important. Lumax built an organization that balances Indian jugaad (frugal innovation) with Japanese precision, German engineering with Indian cost consciousness, family values with professional management. This cultural synthesis might be harder to replicate than any technology or manufacturing capability.

Looking forward, the biggest risk isn't disruption—it's complacency. Success breeds conservatism. Market dominance reduces innovation incentives. The very factors that enabled Lumax's success could become constraints. Maintaining entrepreneurial hunger while managing a complex, multi-stakeholder organization will be the ultimate test.

For India's capital markets, Lumax represents the kind of company that deserves patient capital—not sexy but solid, not disruptive but essential, not global but deeply embedded. As markets mature, the ability to identify and value such companies will separate sophisticated investors from momentum chasers.

The Lumax story is far from over. The next chapters—navigating EV transition, managing succession, potentially consolidating the fragmented auto component industry—will be equally fascinating. But regardless of how those chapters unfold, Lumax has already provided a masterclass in building an enduring industrial enterprise in a rapidly changing world.

In the end, Lumax's greatest contribution might not be the millions of gear shifters or integrated cockpits they've produced. It might be proving that Indian manufacturing can compete not through scale or cost but through strategic positioning, partnership leverage, and relentless execution. In a world obsessed with unicorns and disruption, Lumax reminds us that building real, profitable, enduring businesses still matters.

For investors, entrepreneurs, and policymakers, the lesson is clear: look beyond the headlines, invest in capabilities not just capacity, and remember that in business, as in life, the race doesn't always go to the swift or the strong, but to those who endure and adapt.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube