Lloyds Enterprises: The Conglomerate Play on India's Industrial Renaissance

I. Introduction & Episode Roadmap

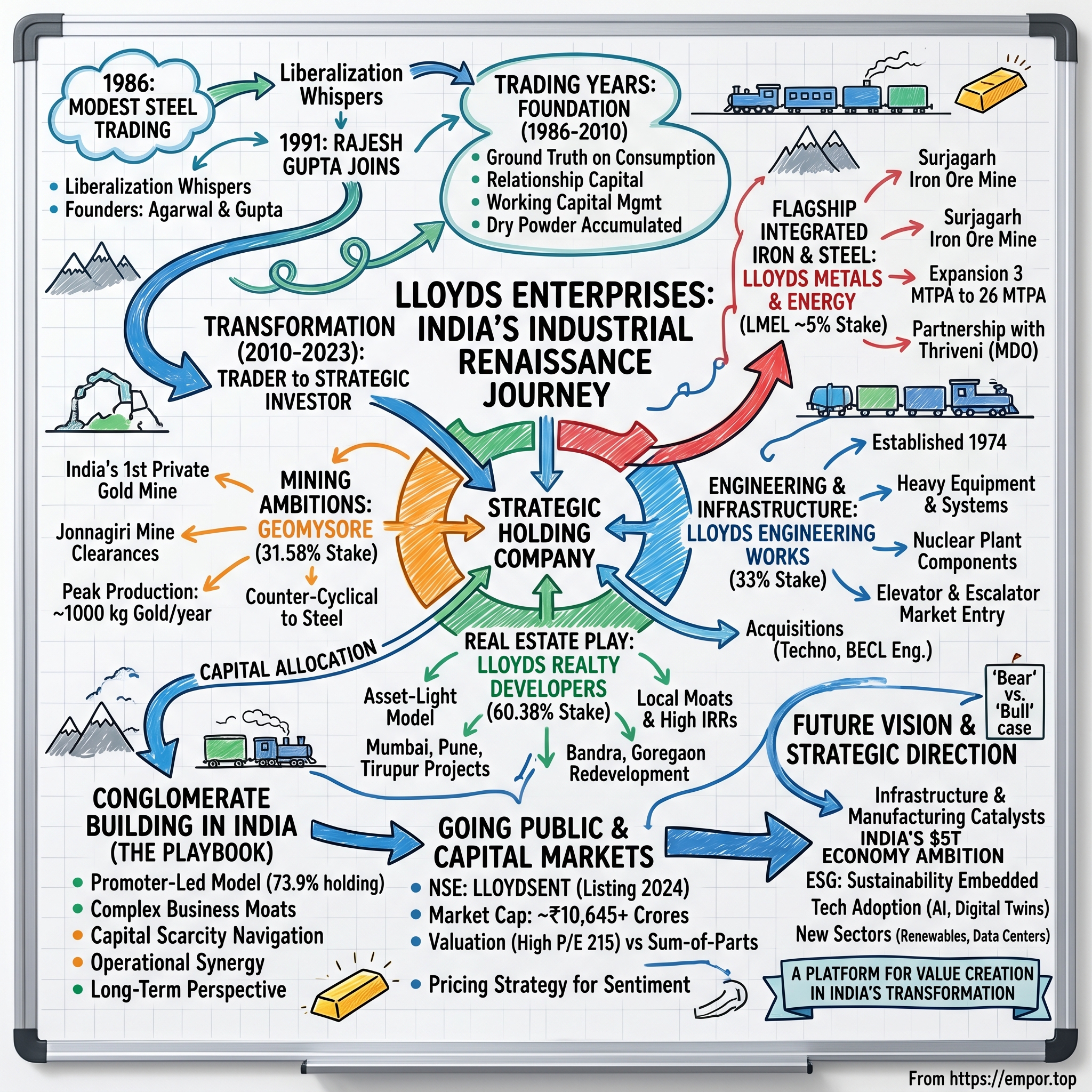

Picture this: A nondescript office building in Mumbai's Fort district, 1986. The License Raj is crumbling, economic liberalization whispers through the corridors of power, and a group of traders huddle around steel price sheets, plotting their next move. They couldn't have imagined that nearly four decades later, their modest steel trading operation would metamorphose into a strategic holding company with tentacles reaching from gold mines in Andhra Pradesh to luxury real estate in Bandra.

This is the story of Lloyds Enterprises Limited—a company that defies easy categorization. Originally incorporated as Benson Steels Ltd. in the twilight of India's socialist experiment, it underwent a dramatic rebirth in September 2023 when it shed its old skin and emerged as Lloyds Enterprises. But why does a name change matter? Because it signals something profound: the transformation from a commodity trader riding price cycles to a strategic architect of industrial assets.

The puzzle that keeps investors awake at night is this: How did a steel trading company—the kind that typically operates on wafer-thin margins and brutal competition—transform itself into a holding company with strategic bets across mining, real estate, and engineering? More intriguingly, why is the market valuing it at a P/E of 215, suggesting either irrational exuberance or recognition of something the casual observer misses?

What we're really examining here is a masterclass in conglomerate strategy adapted for the Indian context. While Western markets have largely rejected the conglomerate model—remember the dismantling of GE?—emerging markets tell a different story. In India, where capital is scarce, regulations byzantine, and relationships paramount, the conglomerate structure isn't just viable; it's often optimal.

Through this deep dive, we'll unpack three core themes that define not just Lloyds Enterprises but the broader Indian industrial renaissance: First, how commodity trading businesses can evolve into capital allocators. Second, why the promoter-led conglomerate model thrives in India's unique ecosystem. And third, how strategic positioning across multiple growth sectors creates optionality in an economy racing toward the $5 trillion mark.

You'll discover why a 31.58% stake in India's first private gold mine matters more than the percentage suggests, how an asset-light real estate model in Mumbai generates outsized returns, and why boring engineering companies suddenly become exciting when India needs to build $1.4 trillion worth of infrastructure.

But perhaps most fascinatingly, we'll explore the human dimension—the vision of founders Babulal Agarwal and Rajesh Gupta, who understood something fundamental about India's trajectory long before it became consensus. As we'll see, building a conglomerate in India isn't just about capital allocation; it's about navigating relationships, understanding political economy, and most crucially, timing the waves of liberalization that periodically wash over the Indian economy.

II. Origins & The Lloyds Group Genesis

The year is 1991. India's foreign exchange reserves have dwindled to barely three weeks of imports. Finance Minister Manmohan Singh is about to deliver a budget speech that will dismantle four decades of socialist planning. And in a modest office in Mumbai, Rajesh Gupta—then a 28-year-old with extensive experience in steel production despite his youth—joins a company called Benson Steels that would eventually become the cornerstone of an industrial empire.

Gupta didn't just stumble into Benson Steels. By November 21, 1991, when he formally joined, he already carried over a decade of hands-on experience in production and business management within the steel sector—remarkable for someone his age. His technical understanding of steel production, combined with an intuitive grasp of market dynamics, made him the perfect complement to founder Babulal Agarwal's trading acumen.

The founding vision wasn't grandiose—it was pragmatic. Agarwal and Gupta recognized that India's impending liberalization would unleash massive infrastructure demand. Steel, the backbone of any industrial economy, would be at the center of this transformation. But rather than compete with the giant integrated steel plants like Tata Steel or SAIL, they chose a different path: trading and intermediation. The 1986 founding wasn't random timing. Babulal Agarwal, a commerce and law graduate with over 54 years of experience in steel trading, founded the Lloyds Group alongside Rajesh Gupta who brought over 35 years of extensive experience in production, business management, and strategic consultancy within the steel and power sectors, joining Lloyds on November 21, 1991. What's striking is how they anticipated the economic liberalization before it formally arrived. They were positioning themselves for a wave they could see forming on the horizon.

The evolution from Benson Steels to Shree Global Tradefin in 1996 wasn't just a rebranding—it signaled an expansion of ambition. The name change coincided with India's post-liberalization trading boom, when suddenly Indian businesses could import and export with fewer restrictions. The Lloyds founders understood that in a newly liberalized economy, the intermediaries who could navigate both the old relationships and new regulations would capture enormous value.

Interestingly, Agarwal and Gupta share a maternal relationship, adding a family dimension to this business partnership—a common thread in Indian business houses where trust and blood ties intertwine. This familial bond would prove crucial in navigating the inevitable storms that any four-decade business journey encounters.

By the late 1990s, they weren't just traders anymore. They were building what would become the broader Lloyds ecosystem. The conglomerate structure made perfect sense in the Indian context for three reasons: First, capital scarcity meant that successful businesses needed to self-fund new ventures. Second, regulatory complexity favored those who had already mastered the bureaucratic maze. Third, and perhaps most importantly, relationships with banks, suppliers, and government officials were transferable across industries.

As founding members of the Group, they continued to steer the company with foresight and a strong commitment to industrial development. Their vision wasn't just about making money from steel trading—it was about using steel trading as a platform to understand India's industrial needs, build relationships, and accumulate capital for bigger bets.

The genius of their approach becomes clear in retrospect: while others were fighting brutal margin wars in commodity trading, Agarwal and Gupta were using trading as market intelligence, understanding which sectors would boom, which companies needed capital, and where the regulatory winds were blowing. They were, in essence, building an information advantage that would prove invaluable when they later pivoted to strategic investments.

III. The Trading Years: Building Foundation (1986-2010)

Mumbai's steel markets in the late 1980s operated like a bazaar crossed with a chess match. Prices changed hourly, relationships determined credit terms, and information asymmetry created fortunes. Into this chaos stepped Lloyds Enterprises (then Benson Steels), not as a manufacturer but as a master intermediary.

The business model was deceptively simple: buy steel from large producers, hold inventory when necessary, and sell to smaller consumers who lacked the scale to deal directly with steel mills. But execution required three capabilities that would later define the entire Lloyds Group: working capital management, relationship capital, and timing the commodity cycle.

Consider the environment: India's steel consumption in 1990 was barely 15 million tonnes. By 2010, it would exceed 65 million tonnes. This wasn't gradual growth—it came in waves corresponding to infrastructure pushes, real estate booms, and industrial expansion. Each wave created opportunities for traders who could anticipate demand and secure supply.

The art of commodity trading in emerging markets differs fundamentally from developed markets. In Chicago or London, you trade paper contracts backed by standardized products and clearinghouses. In 1990s Mumbai, you traded physical steel where quality varied, payment terms were negotiable, and delivery logistics could make or break a deal. Success required what traders call "ground truth"—intimate knowledge of actual supply and demand, not just published statistics.

Lloyds built this ground truth systematically. They didn't just trade steel; they became students of steel consumption patterns. When a new highway project was announced, they understood exactly what grade of reinforcement bars would be needed and when. When real estate developers broke ground, they knew the construction timeline and corresponding steel requirements.

The relationship capital accumulated during these years would prove invaluable. In India, business relationships aren't transactional—they're generational. A steel mill manager who trusted you with credit in 1995 might become a CEO by 2010. A small contractor you supported during a cash crunch might win a major government tender later. These relationships couldn't be bought; they had to be earned through decades of reliable dealing.

But perhaps most importantly, the trading years generated something more valuable than profits: they generated cash flow. In a capital-scarce economy, consistent cash generation created optionality. While other traders used their profits for consumption or dividend

distributions, Lloyds was accumulating dry powder for larger ambitions.

The 2008 financial crisis marked a turning point. While global commodity markets crashed, India's domestic demand—driven by government stimulus and infrastructure spending—remained relatively robust. Lloyds not only survived but thrived, using the crisis to strengthen relationships with suppliers facing liquidity crunches and customers needing extended credit terms.

By 2010, the writing was on the wall: pure trading would face margin compression as markets became more efficient and transparent. The next phase of growth required transformation from trader to investor, from working capital arbitrage to permanent capital allocation. The foundation was built; it was time to construct the edifice.

IV. The Transformation: From Trader to Strategic Investor (2010-2023)

The boardroom discussions in 2010 must have been intense. After nearly 25 years of successful trading, why risk transformation? The answer lay in a simple recognition: trading captures spreads, but ownership captures value creation. And India, entering its infrastructure super-cycle, was about to create enormous value.

The pivot from pure trading to strategic investments wasn't sudden—it was methodical. Today, LEL holds notable positions across the Lloyds Group—including a long-standing stake in Lloyds Metals and Energy, and partial ownership of subsidiaries such as Lloyds Realty Developers and Lloyds Engineering Works. Each investment followed a pattern: identify sectors with long-term tailwinds, acquire meaningful but not controlling stakes initially, then gradually increase ownership as understanding deepened. The crown jewel of this transformation was Lloyds Metals and Energy Ltd. (LMEL), the flagship integrated iron ore and steel company of the Lloyds Group, with operations spanning iron ore mining, DRI, power generation, and pellet production. With announced plans to expand into steel manufacturing and iron ore beneficiation, LMEL is positioned as a vital contributor to India's raw material and industrial infrastructure. LEL holds approximately 5% in LMEL—directly and indirectly—through equity and preference warrants.

What made LMEL particularly attractive was its strategic positioning. Lloyds Metals currently operates the single largest iron ore mine in India, which is in the process of ramping up dispatchable iron ore capacity to 26 MTPA. This wasn't just about owning a mine—it was about controlling a critical input in the steel value chain at a time when India's steel consumption was set to explode.

The real estate play came through Lloyds Realty Developers (LRDL), a majority-owned subsidiary of Lloyds Enterprises Limited, with LEL holding a 60.38% stake in the company. LRDL is building one of the most capital-efficient and return-optimized real estate platforms in the Mumbai Metropolitan Region (MMR). Mumbai real estate in 2015 was experiencing a correction, creating opportunities for well-capitalized players to acquire land and development rights at attractive valuations.

The engineering vertical materialized through Lloyds Engineering Works Ltd. (LEWL), a fast-evolving engineering platform with a strategic focus on infrastructure, EPC, and high-impact industrial sectors. LEL holds a 33% stake in LEWL, which is currently undergoing a major transformation to a multi-disciplinary engineering business.

Each investment reflected a different thesis but shared common threads: exposure to India's infrastructure buildout, businesses with hard assets and cash flows, and sectors where the Lloyds Group's relationships and expertise created competitive advantages.

The 2023 rebrand from Shree Global Tradefin to Lloyds Enterprises wasn't cosmetic—it was a declaration. The company was no longer a trader that happened to own some stakes; it was a strategic holding company actively managing a portfolio of industrial assets. The name change coincided with a broader reorganization that clarified the holding structure and set the stage for the next phase of growth.

What's remarkable about this transformation is its patience. Over thirteen years, Lloyds methodically built positions, never overpaying, never overleveraging, always maintaining the optionality that comes from a strong balance sheet. While other Indian conglomerates made headlines with aggressive acquisitions, Lloyds quietly assembled a portfolio that would position it perfectly for India's next growth phase.

V. The Gold Rush: Geomysore & Mining Ambitions

In the dusty plains of Andhra Pradesh's Anantapur district, 400 kilometers from Bangalore, lies something that hasn't existed in India since independence: a privately operated gold mine. The Jonnagiri Gold Mine, operated by Geomysore Services India Private Limited, represents not just a mining asset but a bet on India's evolving relationship with precious metals and private enterprise.

Geomysore's Jonnagiri Gold Mine in Andhra Pradesh is India's first privately-operated gold mine post-independence. The mine has received all critical clearances, including CTO (Consent to Operate), and is expected to commence commercial production shortly. The significance of this cannot be overstated. For seven decades after independence, gold mining in India was essentially a government monopoly. The liberalization of mining laws, particularly the 2015 amendments to the Mines and Minerals Development and Regulation Act, opened doors that had been shut since 1947.

LEL has acquired a 31.58% stake in Geomysore, a move that initially puzzled some investors. Why would a company rooted in steel and real estate suddenly pivot to gold? The answer lies in understanding gold's unique position in the Indian economy. India imports over 800 tonnes of gold annually, making it the world's second-largest consumer. Every kilogram produced domestically reduces import pressure and captures value that would otherwise flow overseas.

With a mine life valid up to 2043 and peak production visibility of 1,000 kgs of gold annually, this investment is expected to generate long-term cash flows and high strategic optionality for LEL. At current gold prices of approximately ₹75 lakh per kilogram, peak production could generate revenues exceeding ₹750 crores annually—remarkable for an investment that likely cost LEL a fraction of that amount.

The strategic rationale extends beyond simple economics. Gold mining offers several advantages that complement Lloyds' existing portfolio: counter-cyclical to steel and real estate, minimal working capital requirements compared to trading, and extremely high value-to-weight ratios that make logistics simple. Moreover, gold prices in India include import duties and GST, giving domestic producers a natural pricing advantage.

The investment is further validated by Deccan Gold Mines Ltd, another key shareholder which is also listed. Deccan Gold's involvement provides technical expertise and regulatory navigation capabilities, crucial in India's complex mining environment.

What makes the Geomysore investment particularly clever is its timing. LEL entered when the mine had already received most regulatory clearances but hadn't commenced commercial production. This sweet spot—post-approval but pre-production—typically offers the best risk-reward ratio in mining investments. The heavy lifting of exploration and permitting was complete; what remained was execution.

The broader implications are fascinating. If Jonnagiri succeeds, it could catalyze a gold mining revival in India. The country has geological potential for significant gold deposits, particularly in the Dharwar Craton that runs through Karnataka and Andhra Pradesh. Success here could position Lloyds as a first-mover in what might become a multi-billion dollar industry.

There's also an ESG angle that's often overlooked. Artisanal and small-scale gold mining in India operates in regulatory grey zones, often with environmental and safety issues. Large-scale, regulated mining like Jonnagiri could formalize the sector, improving both environmental outcomes and worker safety while generating tax revenues for state governments.

The Geomysore bet exemplifies Lloyds' evolution from trader to strategic investor. It's not just about owning a gold mine; it's about positioning for India's next phase of resource nationalism, where domestic production of critical commodities becomes a strategic imperative.

VI. The Real Estate Play: Lloyds Realty Developers

If you want to understand Mumbai real estate, stand at the Bandra-Worli Sea Link at sunset. To your left, Bandra—where one-bedroom apartments sell for more than Manhattan prices. To your right, Worli—where abandoned textile mills have transformed into India's most expensive commercial district. This seven-kilometer stretch generates more economic value than entire states. And Lloyds Realty Developers has positioned itself right in the middle of this gold rush.

LRDL has successfully delivered over 2.91 million sq. ft. of high-impact developments across Mumbai, Pune, and Tirupur, spanning luxury residential complexes, commercial offices, and mixed-use spaces. But the real story isn't what they've built—it's how they build.

Through its asset-light, high-yield development strategy, LRDL continues to focus on calibrated investments across residential, commercial, industrial, and plotted asset classes. The asset-light model is crucial to understand. Traditional real estate developers in India tie up enormous capital in land banks, betting on appreciation. LRDL takes a different approach: joint ventures, development management, and redevelopment projects where the land comes from existing owners.

Consider the economics: In a typical Mumbai redevelopment project, LRDL doesn't buy land. Instead, they convince existing residents to let them rebuild, offering new apartments in exchange for development rights. The developer funds construction (roughly ₹5,000-7,000 per square foot) and sells the surplus area at ₹20,000-40,000 per square foot. The math is staggering—300-500% gross margins, with IRRs often exceeding 30%.

Its expanding pipeline includes large-scale redevelopment projects, commercial and residential towers, and land acquisitions in strategic corridors such as Bandra, Goregaon, Thane, Khopoli, and North Mumbai. Each location tells a story about Mumbai's evolution. Bandra remains the premium market. Goregaon represents the new commercial frontier. Thane is where Mumbai's middle class is moving. Khopoli captures the warehousing boom. North Mumbai is tomorrow's growth corridor.

The Mumbai Metropolitan Region presents a unique opportunity globally. It's one of the few major cities where prime real estate still trades at significant discounts to replacement cost, a legacy of rent control and regulatory uncertainty. As these distortions unwind—and they are unwinding—the value unlocking potential is enormous.

What makes LRDL's approach particularly sophisticated is their focus on micro-markets. Mumbai isn't one real estate market; it's dozens of micro-markets, each with distinct dynamics. Bandra East differs from Bandra West. Lower Parel has different buyers than Upper Worli. LRDL's local expertise, built over decades, allows them to identify pockets of value invisible to outside investors.

The redevelopment opportunity in Mumbai is generational. The city has approximately 20,000 housing societies built before 1980, most requiring urgent redevelopment. The Slum Rehabilitation Authority estimates 60% of Mumbai's population lives in structures needing replacement. This isn't just a business opportunity; it's a social imperative.

The asset-light model also provides resilience. During downturns, traditional developers hemorrhage cash servicing land loans. LRDL can simply slow new project launches, maintaining minimal fixed costs. When markets recover—and Mumbai real estate always recovers—they can rapidly scale up.

The financial engineering is equally clever. By maintaining majority ownership (60.38%) in LRDL, LEL captures most of the upside while using project-level debt and customer advances to fund construction. This leverages returns at the project level while keeping the holding company's balance sheet clean.

There's a deeper strategic logic here. Real estate development in India isn't just about construction—it's about navigating approval processes, managing stakeholder interests, and understanding local politics. The capabilities LRDL has built are moats that money alone cannot replicate. Try getting redevelopment approval in Bandra if you're an outsider—you'll understand why relationships matter.

The Mumbai real estate story is still in early chapters. The city's GDP is projected to reach $500 billion by 2030. Every major global corporation wants presence here. The infrastructure pipeline—metro, trans-harbour link, new airport—will unlock vast land parcels. LRDL is positioned to capture this value creation, and through it, so is Lloyds Enterprises.

VII. Engineering & Infrastructure: The Industrial Backbone

In a sprawling industrial complex in Murbad, 80 kilometers from Mumbai, massive steel structures take shape. Pressure vessels for refineries. Components for nuclear plants. Equipment for steel mills. This is the heart of Lloyds Engineering Works Limited (LEWL), and its story stretches back to 1974—making it older than the holding company itself.

Engineering Business was established in 1974 at Andheri, Mumbai, a time when India was building its industrial base through import substitution. The company that would eventually become LEWL understood something fundamental: India couldn't import its way to industrialization. Someone had to build the equipment that builds the nation.

The corporate journey is complex but revealing. Our Company was incorporated as "Climan Properties Private Limited" on September 19, 1994... Pursuant to a scheme of arrangement ("Scheme") between Uttam Value Steels Limited ("UVSL") and Lloyds Steels Industries Limited, the engineering division of UVSL was demerged from UVSL into Lloyds Engineering Works Limited. This demerger, completed in 2015, brought a mature engineering business into the Lloyds fold.

Designer and Manufacturer of Heavy Equipment, Machinery and Systems for Hydro Carbon Sector, Oil & Gas, Steel Plants, Power Plants, Nuclear Plant Boilers and Turnkey Projects—the breadth is staggering. But it makes sense when you understand India's industrial landscape. The same engineering capabilities that build a refinery vessel can fabricate a nuclear component. The skills are transferable; the certifications and relationships are not.

LEL holds a 33% stake in LEWL, which is currently undergoing a major transformation to a multi-disciplinary engineering business. As part of this evolution, the company has recently entered the high-growth elevator and escalator market through its acquisition of Techno Industries and signed an MoU to acquire the engineering division of Bhilai Engineering Corporation (BECL), expanding its footprint across metallurgy, mining, railways, naval equipment, and defence.

The elevator and escalator acquisition is particularly clever. India is building more metros than any country globally—28 cities have approved metro projects. Every station needs escalators. Every commercial building over five floors needs elevators. The market is growing at 15% annually, dominated by foreign brands with local manufacturing. LEWL's engineering capabilities give it a cost advantage; its relationships open doors.

The proposed BECL acquisition adds another dimension. Bhilai Engineering Corporation's legacy in railways and defense provides entry into sectors where relationships and track records matter more than price. India's defense indigenization push and railway modernization create multi-decade opportunities.

What's fascinating about LEWL is how unsexy businesses become exciting in context. Heavy engineering sounds boring until you realize India needs to build $1.4 trillion of infrastructure. Industrial fabrication seems commoditized until you understand that qualified vendors for nuclear components can be counted on one hand.

The workshop accreditations tell the story: ISO 9001:2015 and ISO 45001:2018 and ASME U stamp certifications. That ASME U stamp—authorization to fabricate pressure vessels for nuclear applications—is a license to print money in a country building 10 new nuclear reactors.

The strategic positioning for India's infrastructure boom goes beyond just capacity. It's about being present across the value chain. When a refinery expands, LEWL supplies equipment. When a metro extends, they provide systems. When a power plant upgrades, they're there. This isn't just diversification; it's systematic positioning across India's capex cycle.

The numbers reflect the transformation: Market cap has grown to over ₹9,800 crores, with revenues of ₹846 crores generating ₹105 crores in profit. The stock trades at 16.2 times book value—expensive for old-economy engineering but perhaps cheap for a play on India's infrastructure renaissance.

The evolution from a pure mechanical engineering products company to a multi-disciplinary platform mirrors India's own industrial evolution. The country that once imported everything now exports metro coaches. The engineering capabilities built over decades servicing domestic industry now compete globally. LEWL embodies this transformation.

VIII. Going Public & Capital Markets Journey

October 17, 2024, marked a watershed moment. Lloyds Enterprises is listed on both the Bombay Stock Exchange (BSE) and the National Stock Exchange (NSE: LLOYDSENT) as of October 17, 2024. The listing wasn't just about liquidity—it was about crystallizing value that had been building for nearly four decades.

The market reception was nothing short of spectacular. Within a year of listing, the market capitalization reached ₹10,645 crores, up 121% from listing levels. The stock trades at a P/E of 215—a valuation that would make even high-flying tech stocks blush. But is this irrational exuberance or recognition of hidden value?

Understanding the valuation requires grappling with the conglomerate structure. Traditional analysis breaks down. The company's revenue of ₹1,488 crores and profit of ₹123 crores suggest a P/E ratio that seems astronomical. But this misses the point entirely. Lloyds Enterprises isn't valued on current earnings; it's valued on the sum of its parts and future optionality.

Consider what the market is actually buying: A 5% stake in LMEL, which itself has a market cap exceeding ₹40,000 crores. A 60.38% stake in LRDL, sitting on prime Mumbai real estate. A 33% stake in LEWL, transforming into a multi-sector engineering powerhouse. A 31.58% stake in Geomysore, potentially India's first successful private gold mine. The arithmetic alone justifies a significant portion of the valuation.

But there's something more subtle happening. The market is pricing in the "Lloyds Put"—the idea that the promoter group, with 73.9% holding, has both the incentive and ability to create value. High promoter holding usually concerns governance-focused investors, but in the Indian context, it often signals commitment and aligned interests.

The conglomerate discount, that persistent curse of diversified companies in developed markets, works differently in India. Here, conglomerates often trade at premiums, especially when they demonstrate capital allocation skills and have exposure to multiple growth sectors. The market recognizes that in India's relationship-driven economy, being part of a successful business group opens doors that standalone companies cannot access.

The IPO pricing strategy was clever. Rather than maximizing IPO proceeds, the company priced to ensure a successful aftermarket. This created a virtuous cycle: early investors made money, generating positive sentiment that attracted more investors, pushing valuations higher. It's financial engineering, but the kind that creates genuine stakeholder value.

The stock's volatility tells another story. Daily swings of 5-10% aren't uncommon, reflecting the battle between believers who see a multi-bagger and skeptics who see bubble valuations. This volatility creates opportunities for both traders and long-term investors, maintaining market interest and liquidity.

What's particularly interesting is the investor base evolution. Initially dominated by retail investors attracted to the "Lloyds" brand and group association, institutional ownership is gradually increasing as funds recognize the sum-of-parts value. This institutional validation provides support during market corrections.

The use of proceeds from the public listing is equally strategic. Rather than using capital for acquisitions or expansion, the company is maintaining a strong balance sheet, preserving optionality. In a rising interest rate environment, having dry powder becomes a competitive advantage.

The market's valuation implicitly recognizes something profound: Lloyds Enterprises is not just a collection of assets but a platform for value creation in India's next phase of growth. Each subsidiary and investment is a call option on different aspects of India's development story.

IX. Playbook: The Art of Conglomerate Building in India

Warren Buffett once said he tries to invest in businesses that are "so wonderful that an idiot can run them, because sooner or later, one will." In India, the opposite philosophy often works: invest in complex businesses that only sophisticated operators can run, because that sophistication becomes the moat.

The Lloyds conglomerate structure exemplifies why diversified business groups thrive in emerging markets while struggling in developed ones. In the US or Europe, capital markets are efficient, regulations transparent, and specialization rewarded. In India, capital is scarce, regulations labyrinthine, and relationships trump everything.

Consider capital allocation across diverse businesses. In developed markets, if you need capital for a real estate project, you go to real estate funds. For mining, mining funds. In India, good luck getting project finance for a first-time gold mine or a redevelopment project in Mumbai. But if you're Lloyds, with decades of credibility and cash flows from steel trading, doors open.

The promoter-led model, often criticized by Western governance advocates, makes sense in the Indian context. With 73.9% promoter holding, the Agarwal and Gupta families have skin in the game that no professional manager could match. They think in decades, not quarters. They can make bold bets—like entering gold mining—that a professionally managed company couldn't justify to quarterly earnings-focused investors. The synergies across group companies create value in subtle ways. When LRDL develops a property, LEWL might supply engineering services. When LMEL needs mining equipment, the group's relationships help. This isn't transfer pricing manipulation—it's genuine operational synergy that reduces transaction costs and accelerates execution.

The entry of Thriveni Earthmovers, a prominent mine developer and operator (MDO) joined Lloyds Metals as a co-promotor in 2021. Since then, the combined strength of Thriveni's sustainable approach coupled with Lloyds Metals' legacy has been a driving force in the industrial development of Gadchiroli, Maharashtra. This wasn't just capital infusion—it brought operational expertise that transformed a struggling iron ore mine into India's largest.

In 2021, Thriveni was appointed as the mine developer and operator for the iron ore mine in Surjagarh, Gadchiroli, Maharashtra, by Lloyds. The mine capacity was enhanced from 3 Mtpa to 10 Mtpa, with an ultimate endeavor to reach 45 Mtpa of hematite and BHQ. This dramatic capacity expansion showcases how the right partnerships can unlock value that was always there but inaccessible.

The lessons from other Indian business houses reinforce the model. Tata's century-old conglomerate structure enabled it to build India's IT industry (TCS) using profits from steel. Birla used commodity profits to build financial services. Adani leveraged infrastructure expertise across ports, power, and airports. Each proves that in emerging markets, conglomerate structures can create value that focused companies cannot.

Managing complexity becomes an art form. With businesses spanning mining to real estate, the corporate center must balance autonomy with control. Lloyds achieves this through a hybrid model: operational independence for subsidiaries but strategic decisions centralized. Capital allocation happens at the holding company level, ensuring resources flow to the highest returns.

The governance challenge is real but manageable. Independent directors on subsidiary boards provide oversight. Regular related-party transaction disclosures maintain transparency. The holding company structure actually improves governance by separating operational and investment decisions.

What makes the Lloyds playbook particularly sophisticated is its patience. Unlike private equity-style conglomerates that flip assets quickly, Lloyds builds for generations. This long-term orientation enables investments in sectors like gold mining where payoffs take years but create lasting value.

The ultimate lesson? In India, conglomerates aren't relics of an inefficient past—they're adaptive structures for an complex present. When capital markets are imperfect, regulations unpredictable, and relationships everything, the conglomerate structure provides resilience and optionality that focused companies lack.

X. Financial Analysis & Performance

The numbers tell a story, but not the one you might expect. Revenue of ₹1,488 crores generating profit of ₹123 crores suggests modest margins. The company has a low return on equity of 3.87% over the last 3 years—hardly the stuff of investment legend. Yet the market values the company at over ₹10,000 crores. This disconnect demands explanation.

The first insight is that Lloyds Enterprises' consolidated financials obscure more than they reveal. As a holding company, its revenues primarily come from steel trading and dividends from subsidiaries. The real value creation happens at the subsidiary level, where LMEL generates its own revenues exceeding ₹2,000 crores, LRDL develops multi-billion rupee real estate projects, and LEWL books engineering contracts worth hundreds of crores.

Understanding the holding company dynamics requires a sum-of-parts approach. Take LMEL: with its own market capitalization exceeding ₹40,000 crores, LEL's 5% stake is worth approximately ₹2,000 crores. The 60.38% stake in LRDL, conservatively valued at 0.5x the value of projects under development, could be worth ₹1,500-2,000 crores. The 33% stake in LEWL, based on comparable engineering company valuations, might be worth ₹3,000 crores. The Geomysore stake, though pre-revenue, has option value exceeding ₹500 crores based on comparable gold mining assets.

Add these up and you get ₹7,000-8,000 crores in identifiable value, before considering the steel trading business, other investments, or the platform value of being a Lloyds Group company. Suddenly, the ₹10,000+ crore market cap doesn't seem so irrational.

The growth trajectory tells another story. While consolidated revenues grew modestly, the value of underlying assets has exploded. LMEL's capacity expansion from 3 MTPA to planned 26 MTPA represents potential revenue growth of 8x. LRDL's project pipeline expanded from under ₹1,000 crores to over ₹5,000 crores. LEWL's transformation from pure engineering to multi-sector platform could triple its addressable market.

Margin evolution is equally important. Trading businesses operate on 2-3% margins. But as the mix shifts toward asset ownership—mining, real estate development, engineering services—margins expand. LMEL's EBITDA margins exceed 30%. LRDL's project IRRs exceed 25%. Even LEWL generates double-digit margins on specialized engineering work.

The capital efficiency deserves attention. Despite controlling assets worth tens of thousands of crores, Lloyds Enterprises maintains a relatively clean balance sheet. How? By using project-level debt at subsidiaries, customer advances in real estate, and operational leverage in trading. This financial engineering amplifies returns on equity, even if current ROE seems low due to the investment phase.

Cash flow dynamics differ from reported earnings. The steel trading business, though low-margin, generates consistent cash. Real estate projects front-load cash through customer advances. Mining and engineering require upfront investment but generate multi-year cash flows. This cash flow diversity provides stability and funding for growth.

The dividend policy reflects confidence. Despite being in investment mode, the company maintains dividends, signaling that current investments aren't straining finances. As subsidiaries mature—particularly as Geomysore begins production and LRDL completes major projects—dividend capacity should expand significantly.

What's most intriguing is the optionality embedded in the numbers. If India's infrastructure boom accelerates, LEWL benefits. If gold prices spike, Geomysore becomes a cash machine. If Mumbai real estate continues its upward trajectory, LRDL's land bank appreciates. The company isn't betting on one outcome—it's positioned for multiple scenarios.

The accounting deserves scrutiny but appears conservative. Real estate revenues are recognized on completion, not percentage completion. Mining investments are carried at cost, not market value. The conservative accounting means reported numbers likely understate economic value.

XI. Bear vs. Bull Case

The Bull Case: Riding Multiple Waves

Bulls see Lloyds Enterprises as a leveraged bet on India's entire growth story. Start with the macro: India's GDP will double from $3.7 trillion to $7+ trillion by 2030. Infrastructure spending will exceed $1.4 trillion. Real estate markets will add $1 trillion in value. Gold demand will grow 5-7% annually. Every one of these trends benefits Lloyds.

The strategic positioning across high-growth sectors creates multiple ways to win. Thriveni Earthmovers, a prominent mine developer and operator (MDO) joined Lloyds Metals as a co-promotor in 2021. Since then, the combined strength of Thriveni's sustainable approach coupled with Lloyds Metals' legacy has been a driving force in the industrial development of Gadchiroli, Maharashtra. This partnership didn't just bring capital—it brought world-class mining expertise that transformed LMEL's operations.

India's infrastructure and mining boom is just beginning. The country needs 300 million tonnes of steel by 2030, up from 120 million today. Every tonne requires iron ore that LMEL can supply. The real estate opportunity is generational—60% of buildings that will exist in 2030 haven't been built yet. LRDL is perfectly positioned in Mumbai, India's economic capital.

The management track record over 35+ years speaks volumes. Through multiple economic cycles, regulatory changes, and market crashes, the Lloyds Group has not just survived but thrived. The promoters have skin in the game with 73.9% ownership, ensuring aligned interests.

Strategic stakes in valuable assets provide downside protection. Even if growth disappoints, the company owns real assets—mines, real estate, engineering capabilities—that have intrinsic value. This isn't a tech company that could go to zero; it's backed by hard assets in critical sectors.

The sum-of-parts valuation suggests significant upside. As subsidiaries mature and get market recognition, the holding company discount should narrow. If LMEL alone justifies ₹2,000 crores of value and it doubles (not unreasonable given capacity expansion), that's ₹2,000 crores of value creation flowing to LEL shareholders.

The Bear Case: Complexity and Execution Risk

Bears worry about conglomerate complexity and opacity. With operations spanning mining to real estate to engineering, understanding the business requires analyzing multiple industries. Related-party transactions between group companies make it difficult to assess true profitability. The high promoter holding limits float and potentially governance.

The low historical ROE of 3.87% over three years raises questions. If this is such a great business, why aren't returns higher? The investment phase explanation only goes so far—at some point, investments need to generate returns commensurate with risk.

Execution risk looms large across diverse sectors. Can Geomysore actually produce 1,000 kg of gold annually? Will Mumbai real estate prices continue rising? Can LEWL successfully integrate acquisitions and enter new sectors? Each business faces its own challenges, and problems in one could affect the whole.

Regulatory risks in mining and real estate are significant. Mining licenses can be revoked. Environmental clearances can be delayed. Real estate regulations change frequently. The company operates in some of India's most regulated sectors, creating constant regulatory overhang.

The high promoter holding of 73.9% limits stock liquidity and raises governance concerns. While promoter commitment is positive, such high ownership concentration means minority shareholders have limited influence. In a dispute, minority shareholders have few options.

Valuation at 215x P/E suggests enormous expectations. Even if the sum-of-parts logic makes sense, the market is pricing in perfect execution across all businesses. Any disappointment could trigger significant multiple compression.

The conglomerate structure itself may become a liability. Global markets have consistently punished conglomerates with discounts. As Indian markets mature and become more sophisticated, they might start applying similar discounts, regardless of execution.

Concentration risk in the Indian economy is real. Unlike global conglomerates, all of Lloyds' businesses depend on India's growth. A significant economic slowdown would affect every subsidiary simultaneously, providing no diversification benefit.

The Verdict

The truth, as always, lies somewhere in between. Lloyds Enterprises is neither a guaranteed multi-bagger nor a complexity trap. It's a sophisticated play on India's structural transformation, with both significant opportunity and meaningful risks.

For believers in India's growth story who can stomach complexity and volatility, it offers diversified exposure to multiple themes through one stock. For those seeking simplicity and predictability, it's probably not the right fit.

The key question isn't whether Lloyds will succeed—it's whether the market is correctly pricing the probability of success across its various bets.

XII. Future Vision & Strategic Direction

Standing at the crossroads of 2025, Lloyds Enterprises faces choices that will define its next decade. India's $5 trillion economy ambition isn't just political rhetoric—it's driving real policy changes. Production-linked incentives, infrastructure spending, and "Make in India" initiatives create opportunities that didn't exist five years ago.

The infrastructure catalyst alone could transform the company. India needs 11,000 km of highways annually, 500 new airports, 28 metro systems, and power capacity to double. Every project needs steel (LMEL), engineering services (LEWL), and creates real estate opportunities (LRDL). The multiplication effect is staggering.

Industrial growth catalysts extend beyond infrastructure. India's manufacturing sector must grow from 15% to 25% of GDP to create jobs for its demographic dividend. This requires industrial parks (LRDL can develop), machinery (LEWL can supply), and raw materials (LMEL provides). The company sits at the intersection of multiple growth vectors.

Potential new sectors beckon. Renewable energy—where engineering capabilities meet India's 500 GW ambition. Data centers—where real estate expertise meets digital infrastructure needs. Electric vehicle components—where manufacturing capabilities meet mobility transformation. Each represents a logical extension of existing capabilities.

Capital allocation priorities will determine success. The temptation to chase every opportunity must be balanced against focus. The company seems to be following a barbell strategy: double down on proven businesses (LMEL expansion) while taking calculated bets on new opportunities (Geomysore).

The next generation leadership transition looms important but manageable. Indian family businesses often struggle with succession, but Lloyds appears to be managing it well. The involvement of next-generation family members in operations, combined with professional management at subsidiaries, suggests a smooth transition path.

Technology adoption could be a game-changer. Mining companies globally are adopting AI for exploration and autonomous equipment for operations. Real estate is being transformed by proptech. Engineering is embracing digital twins and IoT. Lloyds' traditional businesses could see step-changes in productivity.

ESG considerations increasingly matter. From establishing India's first certified green iron ore mine in the ecologically sensitive region of Gadchiroli to deploying a fully electric mining fleet and building an 87-kilometre slurry pipeline to cut emissions, the company is embedding sustainability deep into its core strategy. This isn't just compliance—it's competitive advantage as customers and investors increasingly value sustainability.

Geographic expansion remains an option. While India-focused today, the capabilities built here are exportable. Indian engineering companies win projects globally. Indian real estate developers expand to Dubai and Singapore. Indian mining companies operate in Africa and Australia. The Lloyds platform could follow.

Financial engineering opportunities abound. Individual subsidiaries could list separately, crystallizing value. Strategic investors could be brought into specific businesses. Financial investors could provide growth capital. The holding company structure provides flexibility for various capital-raising options.

The vision emerging is of Lloyds Enterprises as a platform for value creation in India's transformation. Not just a collection of businesses, but an ecosystem where capabilities, relationships, and capital combine to capture opportunities others miss.

XIII. Epilogue & Key Takeaways

After peeling back layers of complexity, several surprises emerge from the Lloyds Enterprises story. The biggest? How a steel trader became a gold miner. The conventional path would have been to vertically integrate in steel. Instead, Lloyds zagged when others zigged, recognizing that optionality matters more than optimization in rapidly evolving markets.

What makes Indian conglomerates unique isn't just their structure—it's their DNA. Built by entrepreneurs who survived socialist-era controls, liberalization chaos, and global financial crises, they possess an adaptability that spreadsheet strategies can't replicate. They understand that in India, relationships are assets, regulatory navigation is a competency, and patience is a strategy.

For investors, the lessons are clear but challenging. First, valuation frameworks designed for focused companies break down for conglomerates. Second, governance concerns are real but often overstated—high promoter ownership can align interests better than dispersed ownership. Third, complexity isn't always bad—it can be a moat that prevents easy replication.

For entrepreneurs, Lloyds demonstrates the power of platform thinking. Instead of building one great company, build a system that can create multiple companies. Use success in one area to fund experiments in others. Transform information from one business into insights for another.

The India opportunity thesis that Lloyds embodies extends beyond GDP growth rates. It's about a country transforming from informal to formal economy, from rural to urban, from services to manufacturing, from importing to producing. Each transition creates discontinuities that prepared players can exploit.

The final reflection on value creation is philosophical. Western finance theory suggests conglomerates destroy value through complexity and lack of focus. But in emerging markets, they create value through capability transfer and capital allocation. The question isn't whether conglomerates work—it's understanding when and where they work.

Looking at Lloyds Enterprises today is like looking at Berkshire Hathaway in the 1970s or Reliance in the 1990s—a platform in early stages of compounding. Whether it achieves similar success depends on execution, but the structure and strategy position it for extraordinary outcomes.

The story of Lloyds Enterprises is ultimately a story about transformation—of a company, certainly, but also of a country. As India transforms from a $3 trillion economy to a $10 trillion economy over the next decade, companies positioned across multiple growth vectors will capture disproportionate value.

For those who can navigate the complexity, tolerate the volatility, and maintain the patience, Lloyds Enterprises offers something rare: exposure to an entire country's transformation through a single stock. Whether that's brilliant or foolhardy depends on your faith in India's future. But one thing is certain—it won't be boring.

The monks at the Koyasan temple in Japan have a saying: "The pine teaches silence, the rock teaches patience, but the mountain teaches perspective." Lloyds Enterprises, built over four decades from a trading shop to an industrial conglomerate, teaches all three. In the noise of quarterly earnings, it maintains strategic silence. Through market cycles, it demonstrates patience. And in its portfolio approach, it provides perspective on India's transformation.

As we close this deep dive, remember that great businesses aren't just about numbers—they're about narratives. Lloyds Enterprises' narrative is still being written, but the plot points are in place: strategic assets in critical sectors, partnerships that multiply capabilities, and positioning for multiple futures. Whether it becomes an industrial legend or a cautionary tale depends on execution over the next decade.

The ultimate question for investors isn't whether Lloyds Enterprises is a good company—it clearly has valuable assets and capable management. The question is whether the market is correctly pricing the optionality embedded in its structure. In a world of increasing uncertainty, optionality has value. In a country transforming as rapidly as India, that value might be extraordinary.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube