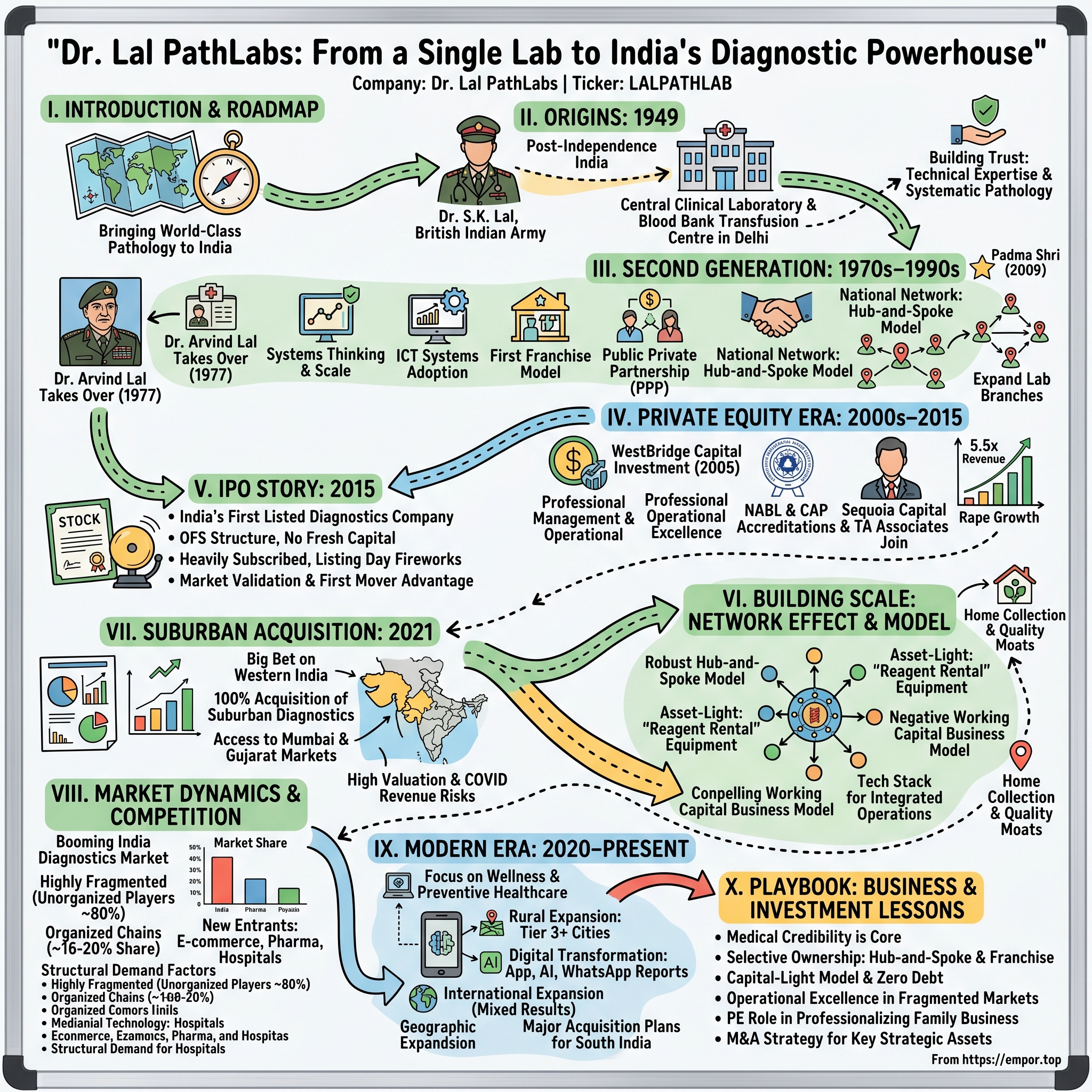

Dr. Lal PathLabs: From a Single Lab to India's Diagnostic Powerhouse

I. Introduction & Episode Roadmap

Picture this: In the chaotic aftermath of India's independence in 1947, as millions crossed newly drawn borders and a nascent nation struggled to build its healthcare infrastructure, a British Indian Army doctor named S.K. Lal made a decision that would reshape Indian diagnostics. Fresh from his pathology training at Cook County Hospital in Chicago—then one of America's busiest public hospitals—he returned not to the comfort of army service, but to the uncertainty of entrepreneurship in a country that barely had standalone pathology labs.

Today, that single-room laboratory has morphed into Dr. Lal PathLabs, a ₹27,250 crore behemoth that processes 45,000 tests daily across a network spanning from Kashmir to Kerala. It's a company that WestBridge Capital turned into a 20-bagger, that commands premium valuations despite operating in one of healthcare's most commoditized segments, and that somehow maintains 25%+ EBITDA margins in a market where mom-and-pop labs charge a fraction of its prices.

How did a post-independence pathology practice transform into India's diagnostic powerhouse? How does a company in a fragmented, low-barrier industry maintain pricing power? And why, in an era of digital disruption and new-age startups, does a 75-year-old family business still dominate its market?

This is the story of three generations of medical entrepreneurship, of building trust in an industry where mistakes can be fatal, and of navigating the peculiar dynamics of Indian healthcare—where cutting-edge technology meets patients who still prefer paper reports, where world-class certifications coexist with neighborhood collection centers, and where a Padma Shri recipient's name on the door still matters more than any app interface.

We'll trace the journey from that first blood bank in 1949 to today's AI-powered diagnostic chain, examining the private equity deals that shaped its trajectory, the IPO that created India's first listed pure-play diagnostics company, and the billion-dollar acquisition bet that's reshaping its geographic footprint. Along the way, we'll unpack the business model that makes diagnostics one of healthcare's best businesses—high margins, negative working capital, and remarkably sticky customers—while confronting the challenges ahead as everyone from pharmacy chains to e-commerce giants eyes this lucrative market.

II. Origins: The British Army Doctor Who Started It All

The year was 1949, and newly independent India was a medical wasteland. The British had left behind 10 medical colleges for 350 million people. Life expectancy hovered around 32 years. Smallpox, cholera, and tuberculosis ravaged communities. In this environment, most doctors either joined government service for stability or opened general practice clinics. S.K. Lal chose neither.

As a Junior Doctor in the British Indian Army, Lal had witnessed something transformative during his training at the Armed Forces Medical College in Pune and later at Cook County Hospital in Chicago—the power of laboratory medicine. At Cook County, he saw how precise diagnostics could change patient outcomes, how a simple blood test could reveal what physical examinations missed. This wasn't just medicine; it was detective work at the molecular level. Returning to India in 1949, Lal commenced the business of providing pathology services through sole proprietorship establishments named Central Clinical Laboratory and Blood Bank Transfusion Centre. The timing was both audacious and opportune. Delhi, the new capital, was experiencing a construction boom. Government hospitals were overwhelmed. Private practitioners needed reliable diagnostic support but couldn't afford their own labs.

Lal started with six employees and established the Central Clinical Laboratory along with a Blood Bank Transfusion Centre. Think about that—a blood bank in 1949 India. This wasn't just about running tests; it was about creating infrastructure that didn't exist. Blood transfusions were rare, storage was primitive, and the concept of blood typing was foreign to most medical practitioners. Lal had to educate doctors about why they should trust an external lab with their patients' diagnoses.

The early decades were about building something more valuable than equipment or facilities: medical credibility. His vision was to bring world-class cutting-edge diagnostic technology to the people of India. In an era when most diagnoses relied on physical examination and educated guesswork, Lal introduced systematic pathology—blood counts that could detect infections before symptoms appeared, urine analyses that revealed kidney function, and cultures that identified the exact bacteria causing an illness.

What set Lal apart wasn't just his technical expertise but his understanding of trust economics in healthcare. Every test report carried his signature. Every abnormal result triggered a personal phone call. When government hospitals questioned his results, he'd repeat the tests for free. When private practitioners doubted his methods, he'd invite them to observe his procedures. This wasn't scalable, but it was necessary. In healthcare, reputation compounds slowly but destroys instantly.

By the 1970s, the laboratory had become a Delhi institution. Doctors would specify "Get it done at Dr. Lal's" on prescriptions. Patients would travel across the city for a blood test, not because it was convenient, but because when life hung in the balance, accuracy mattered more than proximity. The foundation was set, but the real transformation would come when the next generation took charge.

III. The Second Generation Takes Charge (1970s–1990s)

The story might have ended there—a successful local pathology lab serving Delhi's medical community—had tragedy not intervened. S.K. Lal was allegedly killed by his brother, forcing Arvind Lal to take over his father's business. The circumstances remain murky, but the impact was clear: a young army doctor suddenly found himself running a family business he'd never planned to join.

Arvind Lal, born on 22 August 1949, graduated in medicine from the Armed Forces Medical College, Pune, following his father's footsteps into military medicine. He'd secured a prestigious teaching position at AFMC's pathology department. The trajectory was set—a comfortable career in the armed forces, perhaps ending as a decorated medical officer. In 1977, he went back to his family business by taking charge of Dr Lal PathLabs.

The contrast between father and son was stark. Where S.K. Lal was a craftsman focused on technical excellence, Arvind was a systems thinker obsessed with scale. His military background showed—he thought in terms of logistics, standard operating procedures, and command structures. Under his leadership, the institution modernized its diagnostic services by incorporating Information and communications technology (ICT) systems and branched out to many parts of the country.

The breakthrough came from an unexpected source. A regular patient from Model Town, North Delhi, suggested: "You are such a bright young man. Why can't you set up a lab at Model Town?" With that, Lal set up what he calls the first franchise model in the healthcare business in India. This wasn't just geographic expansion; it was a fundamental reimagining of the diagnostic business model.

The franchise model solved multiple problems simultaneously. It eliminated capital requirements for expansion—franchisees invested in collection centers while the company focused on testing capabilities. It provided local credibility—franchise owners were typically established medical professionals or pharmacists with community trust. Most importantly, it created aligned incentives—franchisees earned 25-30% commissions, enough to build substantial businesses while the company retained majority economics.

He is reported to have modernized Indian medical diagnostics and initiated the first Public Private Partnership (PPP) in the field of laboratory testing in India. This PPP model was revolutionary. Government hospitals got access to advanced testing without capital investment. Dr. Lal PathLabs got guaranteed volumes and credibility. Patients got accurate results at subsidized rates. It was a win-win-win that would become the template for healthcare PPPs across India.

By the 1990s, the company had evolved from a single lab to a network spanning North India. The hub-and-spoke model was taking shape—collection centers fed samples to regional labs, which handled routine tests while forwarding specialized samples to the main Delhi facility. Technology adoption accelerated with computerized reporting, barcoded samples, and automated analyzers replacing manual methods.

The Government of India awarded him the civilian honour of the Padma Shri in 2009, for his contributions to Medicine. But perhaps the most important contribution was proving that Indian healthcare businesses could match global standards. The company achieved major milestones in the late 1990s and early 2000s, including NABL accreditation and international CAP accreditation. These weren't just certificates on the wall—they were validation that an Indian lab could meet the same standards as Mayo Clinic or Johns Hopkins.

The stage was set for institutional capital. The family business had professionalized, the model had proven scalable, and the market opportunity was becoming apparent to sophisticated investors. What came next would transform Dr. Lal PathLabs from a regional champion into a national powerhouse.

IV. The Private Equity Era & Transformation (2000s–2015)

The transformation of Dr. Lal PathLabs from a regional player to a national powerhouse began in 2005 with a phone call that would change everything. WestBridge Capital invested Rs.42 crores for a 26% stake, valuing the business at approximately Rs 160 crore. At this time, DLPL had only 10 labs. For context, this was a company doing roughly Rs 43 crore in revenue, operating primarily in Delhi-NCR, competing against thousands of unorganized players. WestBridge wasn't just bringing capital—they were bringing a playbook for scale.

The masterstroke wasn't the capital injection but the condition attached to it. Dr. Om Manchanda, an IIM-A alumnus with 15 years of experience in the healthcare industry, joined as COO and became the CEO in 2008. This step towards professional management was mandated by the investors. Manchanda had worked at Hindustan Unilever, Ranbaxy, and Monsanto—companies that understood scale, systems, and standardization. His arrival marked the beginning of Dr. Lal PathLabs' transformation from a family business to a corporate entity.

"It was a well-established organisational culture that we had to counter at that time and that was a big challenge," recollects Dr. Manchanda. The challenge was monumental. How do you tell pathologists who'd been drawing blood for decades that they now needed to follow standard operating procedures? How do you convince collection center owners to adopt barcoding when paper registers had worked fine? How do you modernize without alienating the very people who built the business?

The numbers tell the story of this transformation. The company's turnover grew from Rs. 43 crore in FY 2005 to Rs. 237 crore in FY 2011—a 5.5x growth in six years. But the real story was in the operational metrics. Sample rejection rates fell from double digits to under 2%. Turnaround times dropped from days to hours. Customer complaints, once handled personally by Dr. Arvind Lal, were now managed through a systematic escalation matrix. In 2010, TA Associates acquired a nearly 16 percent stake for $35 million (₹221 crore) from Sequoia Capital India, which had acquired WestBridge Capital in 2006. The valuation had already jumped significantly. Then came the bigger move: in 2013, WestBridge Crossover Fund and TA Associates together invested $44 million, with WestBridge investing $35 million and TA Associates contributing $9 million, valuing the company at around ₹1,750 crore.

WestBridge's stake valuation had gone up by 20 times since investment. Think about that—a 20x return even before the IPO. This wasn't venture capital luck; this was systematic value creation. The company's revenue had more than tripled to Rs 452 crore in 2012/13 from Rs 128 crore in 2008/09. The number of employees nearly doubled to more than 3,500.

The hub-and-spoke model evolution during this period was critical. Equipment was leased under "reagent rental" arrangements, benefiting the company by lowering capital expenditures. The franchise model saved investment and generated 25-30% commission. Each lab and collection centre was linked with a central server on a real-time basis, helping the company manage the entire network in an integrated manner.

By 2015, the transformation was complete. The national network consisted of a National Reference Laboratory in New Delhi, 163 other clinical laboratories, 1,340 patient service centers and over 5,000 pickup points. The entire system served 15,000 patients and conducted 45,000 tests per day. Quality certifications proliferated—NABL accreditation for multiple labs, CAP accreditation that put them on par with American laboratories, ISO certifications for quality management.

The turnaround time of a few hours, services like home collection, online reports, and loyalty programs added to patient benefits. This wasn't just operational excellence; it was building a moat in a commoditized industry. When you're sick and need a blood test, you don't comparison shop—you go where your doctor trusts, where results are reliable, where the phlebotomist comes to your home if needed.

The stage was set for the ultimate liquidity event. Private equity had done its job—professionalized operations, scaled the business, and built institutional capabilities. Now it was time to tap the public markets and give early investors their exits.

V. The IPO Story: Going Public in 2015

December 8, 2015. The Indian equity markets were in a bear phase. The Sensex had fallen 15% from its peak. IPO activity had dried up—only 23 companies had listed that year versus 43 in 2014. In this environment, Dr. Lal PathLabs opened its IPO bidding with a price band set at ₹550 per share.

IPO bidding ran from December 8-10, 2015, with shares listing on BSE and NSE on December 23, 2015. The timing seemed inauspicious, but the response told a different story. The issue size was 11.6 million equity shares aggregating up to ₹638 crores, priced at ₹550 per share.

The IPO structure was revealing. This was entirely an offer for sale—no fresh capital was being raised for the company. The promoter stake would reduce from 63.7% to 58.7% post IPO, while the Pre IPO shareholding of the private investors/VCs was 32.2% which would get reduced to 23.2% once the shares got listed. WestBridge and TA Associates were cashing out partially after their transformative journey with the company.

The Rs 638 crore IPO saw healthy response from investors and was subscribed 33.41 times. Institutional investors bid for 45 times their allocation. High net worth individuals bid for 71 times. Even retail investors, despite the market pessimism, oversubscribed their portion 6 times. This wasn't just demand—it was validation of a business model that had proven its resilience through economic cycles.

Listing day, December 23, 2015, delivered fireworks. The stock listed at Rs 720, a 31% premium, and ended the day 50% higher at Rs 825 compared to the issue price. Since its IPO in December 2015, Dr Lal zoomed from its IPO price of Rs.550 a share to Rs.930 within months. For context, the broader market was flat during this period. This wasn't momentum trading—it was recognition of value.

Dr. Lal PathLabs became the first company under the consumer healthcare diagnosis services sector to go public, enjoying the benefit of first mover advantage. The company operated 172 labs, 1,554 patient centres and over 7,000 pick-up points, having served nearly 1 crore customers and collected 2.2 crore samples in FY15, with presence mainly in North and East India, both geographies together accounting for ~85% of revenues.

The post-IPO ownership structure revealed sophisticated capital allocation. The Lal family retained 58.7% control—enough to drive strategy without interference. Private equity retained significant stakes, signaling continued confidence. Employee ownership stood at 1.91%, aligning incentives throughout the organization. This wasn't just a listing; it was a carefully orchestrated transition from private to public while maintaining the entrepreneurial DNA.

What made this IPO special wasn't just the numbers but what it represented. Here was a 66-year-old family business that had professionalized without losing its soul, scaled without compromising quality, and created liquidity without ceding control. The public markets had validated not just a company but a model—that Indian healthcare businesses could match global standards while serving local needs, that trust-based services could scale, and that patient care and shareholder returns weren't mutually exclusive.

The IPO proceeds would fund the next phase of growth, but more importantly, the public listing brought transparency, governance, and access to capital markets for future expansion. The foundation was set for the next chapter of aggressive growth and consolidation.

VI. Building Scale: The Network Effect & Business Model

To understand Dr. Lal PathLabs' dominance, you must understand the ingenious simplicity of its hub-and-spoke model. Picture a bicycle wheel—the National Reference Laboratory in Delhi sits at the center, with spokes radiating out to 163 clinical laboratories, which in turn connect to 1,340 patient service centers and over 5,000 pickup points. This isn't just logistics; it's network economics at its finest.

Hub-and-spoke model facilitates economies of scale and future growth scalability. Here's the genius: a collection center in a small town doesn't need expensive equipment or specialized pathologists. It needs a trained phlebotomist, a refrigerator, and a twice-daily pickup schedule. The samples flow to regional labs for routine tests and to the National Reference Lab for complex diagnostics. This means a patient in rural Bihar gets the same test quality as someone in South Delhi, but at a fraction of the infrastructure cost.

Test and services are performed on instrument and equipment which generally are leased under a "reagent rental" benefiting company by lowering capital expenditures. This reagent rental model is brilliant financial engineering. Instead of purchasing multi-crore diagnostic machines, Dr. Lal PathLabs pays equipment suppliers based on test volumes. The supplier provides the machine, maintains it, and gets paid per test. Dr. Lal PathLabs gets cutting-edge technology without capital lock-in. When newer technology arrives, switching is painless.

Franchise model saves investment in new stores and generates 25-30% commission on revenues earned by franchisees. The franchise economics are equally compelling. A franchisee invests ₹5-10 lakhs to set up a collection center. Dr. Lal PathLabs provides the brand, training, logistics, and testing infrastructure. The franchisee keeps 25-30% of revenues—enough to generate ₹1-2 lakhs monthly profit from a well-located center. For Dr. Lal PathLabs, it's pure variable cost expansion with zero capital investment.

The entire system serves 15,000 patients and conducts 45,000 tests per day. But here's what's remarkable: this massive scale operates on negative working capital. Patients pay upfront or within days. Franchisees settle weekly. Suppliers get paid in 30-60 days. The company essentially uses customer money to fund operations—a beautiful business model that generates cash as it grows.

Technology infrastructure binds this network together. Every sample is barcoded at collection. Results flow automatically from analyzers to the reporting system. Patients access reports online within hours. Doctors receive critical values instantly via SMS. This isn't just efficiency; it's building switching costs. Once a doctor integrates Dr. Lal PathLabs into their practice workflow, changing becomes painful.

Quality certifications provide the trust foundation. NABL accreditation for multiple labs, CAP accreditation matching American standards, ISO certifications for quality management—these aren't just certificates. They're competitive moats. A new entrant can copy the hub-and-spoke model, but earning these accreditations takes years of documented processes, quality controls, and continuous improvement.

Turnaround time of few hours. Additional services like home collection, online reports, loyalty program, etc. add to the spectrum of benefits to the patients. The customer experience innovations seem simple but create powerful lock-in. Home collection for elderly patients. WhatsApp report delivery. Loyalty programs offering discounts on preventive packages. Each service adds a small switching cost that compounds over time.

The economics cascade beautifully. High-value tests subsidize routine ones. Urban centers subsidize rural expansion. Preventive health packages drive volumes during lean periods. Corporate contracts provide predictable revenue streams. Government PPP projects offer scale at acceptable margins. Every revenue stream reinforces the others.

Asset productivity metrics tell the story. A typical collection center generates ₹3-5 lakhs monthly revenue from 200 square feet of space. A regional lab processes 1,000+ samples daily with 10-15 technicians. The National Reference Lab handles specialized tests that regional competitors can't even attempt. This isn't just scale; it's scale with operating leverage.

What's remarkable is how this model creates win-win-win outcomes. Patients get accessible, affordable, accurate diagnostics. Franchisees build profitable businesses with minimal risk. Doctors trust the results and appreciate the convenience. Employees get stable careers with growth opportunities. Shareholders see consistent returns with capital efficiency. Even competitors benefit as Dr. Lal PathLabs expands the organized market, educating consumers about quality diagnostics.

The model's resilience showed during COVID-19. When routine testing collapsed, Dr. Lal PathLabs pivoted to RT-PCR tests within weeks. The hub-and-spoke infrastructure that handled routine samples seamlessly scaled for pandemic testing. Collection centers became COVID sample points. The National Reference Lab processed thousands of COVID tests daily. What could have been a crisis became an opportunity, demonstrating the model's antifragility.

This is the beauty of the Dr. Lal PathLabs model—it's simple enough to execute but complex enough to defend. Anyone can open a pathology lab, but creating a network where a blood sample from a Punjab village reaches the right testing facility, gets processed accurately, and returns results within hours while maintaining 25% EBITDA margins? That's a moat measured not in technology or capital, but in thousands of small operational excellences compounding over decades.

VII. The Suburban Acquisition: Big Bet on Western India (2021)

October 26, 2021. The diagnostic industry was in a peculiar moment. COVID testing revenues were evaporating as vaccination rates climbed. Companies that had minted money during the pandemic suddenly faced revenue cliffs. In this environment, Dr. Lal PathLabs' board approved 100% acquisition of Suburban Diagnostics for an enterprise value of Rs 925 crore, funded through existing cash reserves.

The numbers seemed aggressive. Acquisition based on 18.5x multiple of FY22 audited EBITDA, with enterprise value of INR 925-1,150 crores. For context, Dr. Lal PathLabs itself traded at 15x EBITDA. Why pay a premium for a regional player when you're the national leader?

The answer lay in geography and market dynamics. Dr Lal PathLabs revenue contribution from west India to go up from 10% to 24% post-acquisition. Western India, particularly Mumbai and Gujarat, represented the holy grail of Indian diagnostics—high per capita income, insurance penetration, and health awareness, but also intense competition and entrenched local players. Dr. Lal PathLabs had tried organic expansion in Mumbai for years with limited success. The city didn't care about your Delhi pedigree.

Suburban had revenues of Rs 294 Cr in FY 21 with EBITDA of Rs 57.5 crore. The 19.5% EBITDA margin was respectable but below Dr. Lal PathLabs' 25%+ levels. Bulls argued this was an integration opportunity—apply Dr. Lal's operational excellence to Suburban's network and margins would expand. Bears worried that Suburban's margins were temporarily inflated by COVID testing that wouldn't recur.

Through this deal, LPL gained access to over 150 collection centres, 44 laboratories and diagnostics centres, with one CAP-accredited and five NABL-accredited labs. But the real asset wasn't infrastructure—it was relationships. Suburban had spent decades building trust with Mumbai's medical community. In a city where doctors' recommendations drive 70% of diagnostic revenues, these relationships were worth more than any equipment.

The strategic logic was compelling. Western India represented a different consumer than North India. Mumbai customers expected premium service—air-conditioned waiting rooms, valet parking, same-day reports. They were willing to pay for convenience but extremely demanding about quality. Suburban understood this market intimately. Its founder, Dr. Sanjay Arora, wasn't just selling a business; he was joining as Group Medical Director, bringing his relationships and credibility.

Some investors were concerned about the steep 18x EBITDA valuation, as Suburban's margins were inflated by temporary Covid-related testing gains. The COVID windfall question was legitimate. In FY21, COVID testing contributed roughly 30% of Suburban's revenues. Strip that out, and the multiple jumped to 26x normalized EBITDA. Dr. Lal PathLabs was betting that they could replace COVID revenues with routine testing while improving operational efficiency.

The integration challenges were significant. Mumbai's diagnostic market operated differently from Delhi's. Collection centers stayed open later. Customers expected online booking and home collection as standard, not premium services. Report turnaround expectations were measured in hours, not days. Labor costs were 40% higher. Real estate costs were astronomical. Would Dr. Lal PathLabs adapt its model to Mumbai, or force Mumbai into its model?

There was also the brand question. Suburban had strong brand equity in Mumbai—would Dr. Lal PathLabs retain it or rebrand? The company chose a hybrid approach: "Suburban Diagnostics, a Dr. Lal PathLabs Company." This preserved local trust while leveraging national credibility. Smart, but it meant managing two brands with different positioning in overlapping markets.

The financing structure revealed confidence. The deal was funded entirely from existing cash reserves—no debt, no equity dilution. Dr. Lal PathLabs had over ₹900 crore in cash, generating ₹400 crore annually in free cash flow. They could afford to be patient with integration, focusing on long-term value creation rather than quick synergies.

Market reaction was mixed. The stock fell 5% on announcement, reflecting concerns about valuation and integration risk. But management's communication was clear: this wasn't about immediate earnings accretion but strategic positioning. Western India was the missing piece in their national footprint. Without it, they risked being boxed into North and East India while competitors consolidated elsewhere.

The deal also sent a message to the industry. Consolidation was accelerating. Metropolis had acquired Hitech Diagnostics. Pharma companies were eyeing diagnostics. E-commerce players were launching health verticals. The window for building national scale through acquisition was closing. Dr. Lal PathLabs had to move now or risk being permanently subscale in India's richest market.

Looking back, the Suburban acquisition represented a classic build-versus-buy decision executed at a pivotal moment. Could Dr. Lal PathLabs have built Western India presence organically? Perhaps, but it would have taken a decade and hundreds of crores with uncertain outcomes. By acquiring Suburban, they bought time, relationships, and market knowledge—intangibles that don't show up in EBITDA multiples but determine success in trust-based businesses like diagnostics.

VIII. Market Dynamics & Competition

The numbers are staggering. India diagnostics market size valued at US$ 2,128.7 million in 2023, set to reach US$ 7,847.9 million by 2030 growing at CAGR of 19.9%. This isn't just growth; it's an explosion driven by fundamental shifts in Indian healthcare consumption. Rising incomes, lifestyle diseases, insurance penetration, and preventive health awareness are creating a perfect storm of demand.

Yet paradoxically, India's Diagnostics market is highly fragmented, and most diagnostic tests take place in the metro and tier 1 cities. Urban Diagnostics dominates the market in India, and rural diagnostics accounts to have 22% market share. India's diagnostics market is highly fragmented and unorganized due to lack of regulations. The disconnect is jarring—massive unmet demand in rural India, intense competition in urban centers.

Organised players like Dr. Lal PathLabs, Metropolis, SRL, and Thyrocare hold a modest 16-20% market share. Think about that—the top four players combined control less than a fifth of a $2 billion market. The remaining 80%+ is scattered across thousands of standalone labs, hospital captive facilities, and unorganized players. This fragmentation is both opportunity and challenge.

The diagnostic market is fragmented and includes standalone centers, private hospitals, and government hospital laboratories, putting capacity, quality, and scalability at risk. Each segment operates with different economics. Standalone centers compete on price, often compromising quality. Hospital labs bundle diagnostics with treatment, using it as a loss leader. Government labs offer subsidized testing but struggle with capacity and turnaround times.

Key competitors reveal distinct strategies. Metropolis focuses on premium positioning in Western and Southern India. SRL Diagnostics leverages its Fortis hospital parentage for B2B volumes. Thyrocare operates as the "Southwest Airlines of diagnostics"—ultra-low cost, high automation, narrow test menu. Each has carved a niche, but none has achieved Dr. Lal PathLabs' scale and profitability combination.

New entrants are reshaping competitive dynamics. Online aggregators like 1mg and Pharmeasy offer convenience but rely on existing labs for fulfillment. Hospital chains like Apollo and Max are expanding diagnostic arms, leveraging captive patient bases. Pharmacy chains like Medplus see diagnostics as footfall drivers. Each brings different capabilities and constraints to the battlefield.

Factors such as low healthcare spending, a growing burden of chronic illnesses, and an ageing population are poised to drive growth. The demand drivers are structural, not cyclical. India's diabetes prevalence is 11.4%, hypertension affects 30% of adults, and cancer incidence is rising 5% annually. Each chronic disease patient requires regular monitoring—quarterly HbA1c for diabetics, annual lipid profiles for cardiac patients, periodic tumor markers for cancer survivors. This creates annuity-like revenue streams.

The sector's attractiveness with favourable margins and low entry barriers has spurred aggressive competition. The economics are seductive. Gross margins exceed 70% for routine tests. Operating leverage is massive—the same equipment processing 100 samples can handle 1,000 with minimal incremental cost. Working capital is negative. Returns on capital employed exceed 30%. No wonder everyone wants in.

But competition is intensifying on multiple fronts. Price competition in routine tests has commoditized CBC and glucose testing. Quality differentiation is difficult when everyone claims NABL accreditation. Service innovation quickly gets copied—home collection, online reports, and WhatsApp delivery are now table stakes. Geographic expansion requires massive investments with uncertain returns.

The regulatory environment adds complexity. The Clinical Establishments Act remains unenforced in most states. NABL accreditation is voluntary, not mandatory. Price caps exist for COVID tests but not routine diagnostics. Quality standards vary wildly across states. This regulatory vacuum benefits established players with self-imposed quality standards while enabling fly-by-night operators to undercut prices.

Technology disruption looms but hasn't materialized. Point-of-care testing promises to eliminate sample transportation. AI-powered diagnosis could reduce pathologist dependence. Direct-to-consumer genetic testing might bypass traditional labs. Wearables could enable continuous monitoring. Yet, these technologies remain expensive, unproven, or unsuited for Indian conditions. The moat around traditional hub-and-spoke models remains intact—for now.

Market consolidation is accelerating but fragmented. The Indian diagnostics sector is set for a steady recovery after the Covid-19 pandemic, with analysts forecasting a compound annual growth rate (CAGR) of 8-9% over the next four years. This resurgence is expected to be fuelled by increased testing, strategic price adjustments, expansion of wellness services, and wider geographic reach. Every major player is acquiring regional champions. Venture capital is funding digital-first models. Private equity is rolling up standalone centers. Yet, organized players' market share is increasing only gradually—from 15% to perhaps 20% by 2030.

The competitive landscape reveals a fundamental truth: in Indian diagnostics, scale is necessary but not sufficient. Trust matters more than technology. Local relationships trump national brands. Service beats price for affluent customers; price beats service for mass market. The winners will be those who can navigate these contradictions, building national scale while maintaining local relevance, driving efficiency while preserving quality, expanding access while protecting margins.

IX. Modern Era: Technology, Expansion & Future Bets (2020–Present)

The post-COVID landscape has forced a strategic reset for Dr. Lal PathLabs. South India contributes only 6% of ₹2,227 crore revenue in FY24, with two-thirds from Delhi NCR and North India. This geographic concentration, once a strength enabling operational excellence, has become a strategic vulnerability as competition intensifies and growth in mature markets slows.

The company is exploring significant acquisition in South India ranging from ₹3,000 crore to ₹4,000 crore, with approximately ₹1,000 crore in net cash. "We have around ₹1,000 crore (net) cash, we can leverage our balance sheet, we can use our equity, size will not hold us," said Ved Prakash Goel, group CFO. This isn't just expansion; it's a recognition that without Southern presence, Dr. Lal PathLabs risks being permanently boxed into North India.

The Southern challenge is unique. Unlike North India where Dr. Lal PathLabs enjoys 40%+ market share in some cities, South India is intensely competitive with strong regional players. Metropolis dominates Mumbai and Western markets. Local champions like Neuberg in Karnataka, Medall in Tamil Nadu, and Vijaya in Telangana have deep relationships and regional understanding. Breaking in organically would take decades.

In latest quarter of FY24-25, revenue was ₹660 crore (9.8% increase), PAT rose to ₹131 crore (18.1% growth). The numbers look healthy, but dig deeper and you see the strategic imperative. Volume growth is just 2.6%—barely above population growth. Price increases drive most revenue growth, but there's a limit to pricing power in commoditized routine tests. Geographic expansion is essential for sustained growth.

Digital transformation has become central to the strategy. The company launched an enhanced mobile app, introduced AI-powered test recommendations, and rolled out WhatsApp-based report delivery. But digital in diagnostics isn't about disruption—it's about convenience. Patients still need physical sample collection. The winner isn't who has the best app, but who combines digital convenience with physical accessibility.

Added 24 labs and over 1,684 collection centres in tier 3+ cities between FY20 and FY24. This rural push reflects a strategic insight: India's diagnostic consumption is bifurcating. Urban markets demand specialty tests, wellness packages, and premium service. Rural markets need basic tests at affordable prices with convenient access. Dr. Lal PathLabs is building dual capabilities—premium offerings for urban India, volume plays for Bharat.

Focus on wellness packages and preventive healthcare represents a fundamental shift in business model. Curative diagnostics is transactional—you're sick, you test, you pay. Preventive diagnostics is relational—annual packages, quarterly monitoring, lifetime value. A diabetic patient on a quarterly HbA1c monitoring package is worth 10x a walk-in patient. The challenge is changing consumer behavior from "test when sick" to "test to stay healthy."

Specialty verticals reveal ambitions beyond traditional pathology. Genomics isn't just genetic testing—it's personalized medicine, cancer screening, and reproductive health. Reproductive diagnostics capitalizes on India's IVF boom and rising infertility. Autoimmune disorders represent a massive underdiagnosed market. Each vertical requires different capabilities, partnerships, and go-to-market strategies, but offers higher margins and differentiation.

The technology investments go beyond customer-facing applications. Lab information systems now use AI for result validation, flagging anomalies before release. Automated sample sorting reduces errors and improves turnaround. Predictive analytics optimize inventory and staffing. Digital pathology enables remote consultation for complex cases. These aren't headline-grabbing innovations but compound into operational excellence.

International expansion has been mixed. The company dissolved its Kenya subsidiary after three years of non-operation. Bangladesh operations remain subscale. Nepal shows promise but limited size. The lesson is clear: Dr. Lal PathLabs' competitive advantages—brand trust, operational excellence, network effects—don't travel easily across borders. The focus has correctly shifted to capturing India's massive domestic opportunity.

The organizational transformation is equally significant. A new CEO, Shankha Banerjee, brings fresh perspective while respecting the founding family's vision. The M&A team signals serious intent about inorganic growth. Investment in talent from technology and consumer companies shows recognition that diagnostics is becoming a consumer business, not just a medical service.

Competition has also evolved. It's no longer just about other diagnostic chains. Hospitals are expanding diagnostic arms. Pharmacies offer basic tests. E-commerce platforms aggregate demand. Device manufacturers enable home testing. Government's Ayushman Bharat creates price pressure. Each competitor attacks from a different angle, forcing Dr. Lal PathLabs to defend on multiple fronts while pursuing growth.

Yet the fundamentals remain compelling. India's diagnostic penetration is still just $10 per capita versus $150+ in developed markets. Chronic disease prevalence is rising. Insurance coverage is expanding. Health awareness is increasing. The market will likely double by 2030. The question isn't whether Dr. Lal PathLabs will grow, but whether it can maintain leadership while the market transforms around it.

X. Playbook: Business & Investment Lessons

The Dr. Lal PathLabs story offers a masterclass in building enduring businesses in complex, trust-based markets. Each strategic decision—from the franchise model to the Suburban acquisition—reveals principles applicable beyond diagnostics, beyond healthcare, beyond India.

Building trust in healthcare: The importance of medical credibility. Trust in healthcare isn't built through advertising or pricing—it's earned through consistent accuracy over decades. Dr. Lal PathLabs understood that in diagnostics, a single wrong result can destroy a reputation built over years. This led to over-investment in quality—CAP accreditation when Indian regulations didn't require it, automated equipment when manual methods were profitable, double-checking protocols when single checks sufficed. The lesson: in trust businesses, quality isn't a cost center but the core asset.

Asset-light expansion through franchisees and hub-spoke model. The genius wasn't avoiding assets entirely but being selective about which assets to own. Own the National Reference Lab with sophisticated equipment—that's your competitive moat. Own the brand and quality protocols—that's your differentiation. But collection centers? Let franchisees own those. Sample transportation? Outsource it. This selective ownership model enabled capital-efficient scaling while maintaining quality control where it mattered most.

The low capital-intensive nature of the business model keeps the balance sheet leverage free. Negative working capital, subscription revenues, equipment leasing—each element compounds into a business that generates cash as it grows. This isn't just financial engineering; it's strategic flexibility. When COVID hit, Dr. Lal PathLabs could pivot to PCR testing without credit concerns. When acquisition opportunities arose, they had cash to move quickly. When competition intensified, they could invest in technology without leverage constraints.

Managing fragmented markets: Consolidation opportunity. In fragmented markets, the winner isn't who's cheapest or biggest, but who can professionalize operations while maintaining local relevance. Dr. Lal PathLabs standardized backend processes—testing protocols, reporting formats, quality controls—while keeping frontend operations local. Each franchisee knows their neighborhood, speaks the local language, understands cultural nuances. This combination of global standards and local execution is the playbook for consolidating fragmented industries.

The role of private equity in scaling healthcare businesses. WestBridge and TA Associates didn't just bring capital—they brought discipline. Monthly MIS reporting, systematic expansion planning, professional management hiring, governance structures—these PE-mandated changes transformed a family business into an institution. The 20x return wasn't luck but the result of systematic value creation. The lesson for healthcare entrepreneurs: choose investors who understand that healthcare scaling requires patient capital and operational excellence, not just growth hacking.

Timing the public markets: First-mover advantage. Going public in 2015, before any pure-play diagnostic competitor, gave Dr. Lal PathLabs permanent advantages. Access to capital for acquisitions. Currency for employee stock options. Transparency that builds trust with medical institutions. Liquidity that attracts institutional investors. Being first created a virtuous cycle—better access to capital enabled faster growth, which attracted better talent, which improved operations, which enhanced valuations, which improved access to capital.

M&A strategy: When to pay up for strategic assets. The Suburban acquisition at 18x EBITDA seemed expensive, but the alternative—building Western India presence organically—would have taken a decade with uncertain outcomes. The premium paid wasn't for Suburban's current earnings but for immediate market access, established relationships, and competitive preemption. Sometimes overpaying for the right asset is cheaper than underpaying for the wrong one or not buying at all.

Technology as enabler vs. differentiator in diagnostics. Dr. Lal PathLabs invested heavily in technology but never confused it with strategy. Technology enabled better operations—faster turnaround, fewer errors, convenient access. But the differentiation came from trust, quality, and accessibility. In healthcare, technology that doesn't improve patient outcomes or experience is just expensive complexity. The playbook: use technology to enhance your core value proposition, not replace it.

The meta-lesson across all these principles is that sustainable competitive advantages in service businesses come from thousands of small operational excellences compounding over time, not from any single brilliant strategy or technology. Dr. Lal PathLabs' moat isn't any one thing—it's the accumulated trust from millions of accurate test results, the network effects from thousands of collection centers, the operational knowledge from decades of refinement, the relationships with tens of thousands of doctors.

For investors, the playbook suggests looking for businesses with similar characteristics: trust-based services with high switching costs, network effects that strengthen with scale, capital-light expansion models, markets large enough to sustain decades of growth, management teams that balance growth with profitability. These businesses may not generate headlines, but they generate returns.

XI. Analysis & Bear vs. Bull Case

Bull Case:

The structural drivers for Indian diagnostics are undeniable. India diagnostics market size valued at US$ 2,128.7 million in 2023, set to reach US$ 7,847.9 million by 2030 growing at CAGR of 19.9%. Factors such as low healthcare spending, growing burden of chronic illnesses, and ageing population are poised to drive growth in this sector. This isn't speculation—it's demographics meeting epidemiology.

The underpenetration is staggering. India's diagnostic spending is $10 per capita versus $150+ in developed markets. Even reaching 25% of developed market levels implies a 4x growth opportunity. Unlike consumer discretionary spending, healthcare is non-negotiable. When you're sick, you test. When you have diabetes, you monitor. This creates resilient, growing demand regardless of economic cycles.

Market cap of 27,465 Crore, trading at 12.6 times book value suggests reasonable valuations despite the recent rally. For a business generating 25%+ EBITDA margins, 30%+ returns on capital employed, and sustainable double-digit growth, these multiples don't seem stretched. The balance sheet strength—₹1,000+ crore net cash—provides optionality for value-accretive acquisitions.

Strong brand and first-mover advantage create sustainable moats. In healthcare, trust compounds. Every accurate test result strengthens the brand. Every doctor recommendation reinforces credibility. Every satisfied patient becomes a lifetime customer. New entrants can copy the business model but can't replicate 75 years of accumulated trust. This intangible asset doesn't show on balance sheets but drives pricing power and customer retention.

Successful M&A track record demonstrates execution capability. From small Kanpur labs to the billion-dollar Suburban acquisition, Dr. Lal PathLabs has shown ability to identify, acquire, and integrate assets. The upcoming Southern expansion, while risky, follows a proven playbook. Management's patience—waiting for the right asset rather than forcing deals—suggests discipline that enhances probability of success.

Technology and digital capabilities position the company for next-generation diagnostics. AI-powered diagnosis, genetic testing, point-of-care devices—Dr. Lal PathLabs has investments across emerging technologies. While none are transformative yet, being present across multiple bets increases odds of catching the next wave. The digital infrastructure already built—apps, online reporting, home collection networks—provides platforms for launching new services.

Bear Case:

RoCE likely to remain under pressure at around 22–25%, compared with pre-pandemic levels of over 30%. This isn't temporary—it's structural. Increased competition means higher customer acquisition costs. Geographic expansion requires upfront investments with delayed payoffs. Technology investments are necessary but don't immediately translate to revenues. The days of 30%+ returns on capital might be permanently behind.

Intense competition from new entrants across multiple vectors. E-commerce platforms have customer relationships and logistics. Pharmacy chains have footfall and trust. Hospitals have captive patients. Device manufacturers enable home testing. Government programs create price pressure. Each competitor might be subscale individually, but collectively they're fragmenting the market and compressing margins.

Geographic concentration risks remain despite expansion efforts. Two-thirds of revenue from North India creates vulnerability. If a strong regional player emerges, if government regulations change, if competitive dynamics shift—the impact would be disproportionate. The Southern expansion is necessary but expensive, with uncertain returns and integration challenges. Dr. Lal PathLabs might be forced to overpay for assets in markets where it lacks leverage.

Integration challenges from acquisitions could destroy value. Suburban's EBITDA margins remain at 14-15%, half of Dr. Lal PathLabs' levels, even three years post-acquisition. This raises questions: Are Mumbai's market dynamics structurally different? Is integration harder than expected? Will Southern acquisitions face similar challenges? If acquired assets can't reach parent company margins, the M&A strategy destroys rather than creates value.

Margin pressure from competitive intensity is intensifying. Routine tests are commoditized with 50%+ discounts common. Specialized tests face competition from referral labs. Wellness packages are being given away as customer acquisition tools. Home collection is now table stakes, not a premium service. Even if volumes grow, revenue per test and margins might structurally decline.

Technology disruption remains a Damocles sword. Today's moats could become tomorrow's legacy infrastructure. If Apple launches a watch that monitors glucose continuously, who needs quarterly HbA1c tests? If Amazon enables home testing with instant results, why visit collection centers? If AI can diagnose from symptoms better than tests, what happens to volumes? The probability might be low, but impact would be existential.

The Balanced View:

The truth likely lies between these extremes. Dr. Lal PathLabs will probably grow, but at rates closer to 12-15% than 20%+. Margins will stabilize around 22-25%, respectable but not exceptional. The company will maintain leadership in North India while struggling to replicate dominance elsewhere. Technology will enhance operations without fundamental disruption. Competition will intensify but not devastate.

For investors, this suggests a quality compounder rather than a multibagger. Dr. Lal PathLabs offers exposure to India's healthcare consumption story with reasonable downside protection from its market position and balance sheet strength. It's a bet on execution in a growing market rather than disruption or transformation. In a portfolio context, it's a stable core holding rather than a high-conviction satellite position.

The key monitorables are margin trends (sustainable above 24%?), Southern acquisition success (accretive or dilutive?), volume growth acceleration (can they achieve 5%+ sustainably?), and competitive dynamics (is market share stable?). These metrics will determine whether Dr. Lal PathLabs remains a market leader or becomes a mature, ex-growth business trading on past glory.

XII. Epilogue & "If We Were CEOs"

The South India opportunity and expansion strategy demands radical thinking. Instead of acquiring established players at premium valuations, why not incubate a digital-first subsidiary brand? Launch "Path Labs by Dr. Lal"—a modern, app-first diagnostic service targeting young, urban professionals in Bangalore, Hyderabad, and Chennai. Different brand positioning, different service model, but leveraging Dr. Lal's backend infrastructure. This flanking strategy could capture new demographics while the traditional brand pursues acquisitions.

Building for the next 75 years: What needs to change? The family-promoter model served well for 75 years, but the next phase requires different governance. Bring in independent directors with global healthcare experience. Create an Innovation Committee with external experts in AI, genomics, and digital health. Establish a Corporate Venture Capital arm to invest in health-tech startups. Transform from a diagnostic company run by doctors to a healthcare platform run by professionals with medical expertise.

Technology disruption: AI in diagnostics, at-home testing should be embraced, not feared. Partner with AI companies to develop diagnostic algorithms. Invest in point-of-care device manufacturers. Launch a direct-to-consumer genetic testing brand. Create a telemedicine platform that combines consultations with diagnostic services. The goal isn't to protect the existing model but to cannibalize yourself before others do.

Consolidation vs. organic growth trade-offs need rebalancing. The current strategy emphasizes geographic expansion, but what about vertical integration? Acquire reagent manufacturers to improve gross margins. Buy logistics companies to control sample transportation. Invest in equipment manufacturers for technology access. Forward integrate into specialty clinics for chronic disease management. Own more of the value chain rather than just expanding geographic footprint.

International expansion possibilities should focus on the Indian diaspora. Instead of entering Kenya or Bangladesh, target Indians in the Middle East, Southeast Asia, and North America. Launch "Dr. Lal PathLabs Global"—premium diagnostic services for NRIs who trust the brand from India. Partner with local providers for fulfillment while maintaining quality standards. This leverages brand equity where it exists rather than building from scratch.

Final reflections on building enduring healthcare businesses in India: The next decade will test whether Dr. Lal PathLabs can transition from a family business that professionalized to a professional business that maintains entrepreneurial spirit. The challenges are immense—technology disruption, competitive intensity, margin pressure, integration complexity. But so are the opportunities—market growth, consolidation potential, new service lines, international expansion.

Success will require embracing paradoxes. Be national yet local. Be standardized yet personalized. Be affordable yet premium. Be technology-enabled yet human-centered. Be aggressive in expansion yet patient with returns. These aren't contradictions to resolve but tensions to manage.

The broader lesson for Indian healthcare is that sustainable businesses are built on trust, not technology. Scale comes from solving real problems, not financial engineering. Value creation requires patience, not just capital. Dr. Lal PathLabs' journey from a single Delhi lab to India's diagnostic leader proves that in healthcare, slow and steady doesn't just finish the race—it wins it.

For the next generation of healthcare entrepreneurs, the playbook is clear but execution is complex. Build trust through quality. Scale through partnerships. Expand through acquisition. Innovate through integration. Lead through service. These principles sound simple but require decades of disciplined execution. Dr. Lal PathLabs shows it's possible. The question is who will write the next chapter of Indian healthcare's evolution.

The ultimate test isn't whether Dr. Lal PathLabs reaches ₹5,000 crore revenue or expands to 500 cities. It's whether a patient in rural Bihar gets the same quality diagnosis as someone in South Delhi. Whether a diabetic in Tamil Nadu can afford regular monitoring. Whether a cancer patient in Assam receives timely, accurate results. Business success and social impact need not be mutually exclusive. In healthcare, they're mutually reinforcing.

That's perhaps the most important lesson from Dr. Lal PathLabs' 75-year journey—that building a great business and serving society aren't different goals but the same goal viewed from different angles. In diagnostics, every accurate test could save a life. Every accessible collection center democratizes healthcare. Every affordable package enables preventive care. The financials are just scoreboards. The real impact is measured in lives improved, diseases detected, and health outcomes enhanced.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube