Kaynes Technology: From PCB Workshop to India's EMS Giant

I. Introduction & Episode Roadmap

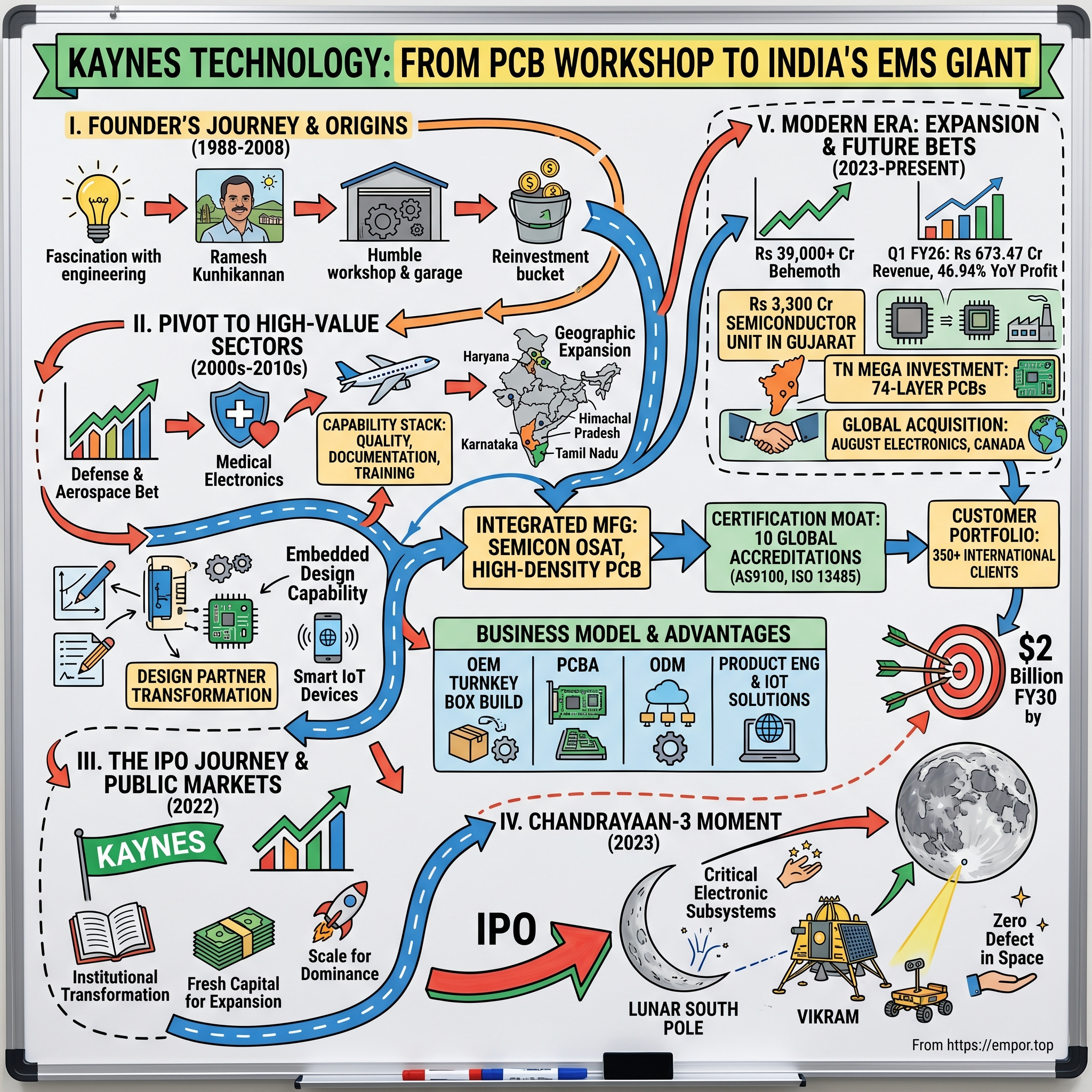

Picture this: August 23, 2023. As India held its collective breath, Chandrayaan-3's Vikram lander touched down near the Moon's south pole—a feat no nation had achieved before. In mission control, alongside ISRO scientists, stood a 59-year-old entrepreneur from Mysore whose company's electronic systems powered both the rover and lander. That man was Ramesh Kunhikannan, and his journey from a small workshop assembling circuit boards to enabling India's space ambitions encapsulates one of the most remarkable transformations in Indian manufacturing.

Kaynes Technology India isn't just another electronics manufacturer. It's a Rs 39,000+ crore behemoth that has quietly positioned itself at the intersection of India's most critical technological frontiers—from the circuits in your car's infotainment system to the electronics guiding nuclear reactors, from IoT sensors in smart cities to components in defense systems. The company spans automotive, industrial, aerospace and defense, outer-space, nuclear, medical, railways, IoT, and IT segments—a breadth that would make most conglomerates dizzy.

But here's the central question that makes this story worth telling: How does a 24-year-old with no family connections, no venture capital, and no ties to the technology industry build a company that becomes indispensable to India's space program? How does a Mysore workshop evolve into an integrated electronics manufacturer with 10 global accreditations—the most certified ESDM (Electronic System Design & Manufacturing) company in India?

This is a story about timing, patience, and the power of compound capabilities. It's about recognizing that India's manufacturing renaissance wouldn't happen overnight but betting your entire career that it would eventually arrive. It's about the unglamorous work of building standards, acquiring certifications, and creating trust in sectors where failure isn't an option. And perhaps most importantly, it's about how a family business can professionalize without losing its entrepreneurial soul.

Over the next few hours, we'll trace Kaynes' evolution through five distinct phases: the bootstrap years when survival meant taking any PCB assembly job; the strategic pivot to high-value sectors that required betting the company on certifications; the transformation from contractor to design partner; the public markets debut that coincided with India's manufacturing moment; and the current era where semiconductor ambitions meet space-age achievements.

We'll examine the playbook that allowed Kaynes to compound at extraordinary rates—from workshop to Rs 39,000 crore in 36 years. We'll dissect the business model that makes it both a picks-and-shovels play on India's electronics boom and a direct beneficiary of the China+1 narrative. And we'll wrestle with the fundamental question facing the company today: Can Kaynes maintain its innovation edge as it scales from David to Goliath?

The stakes couldn't be higher. India's ESDM market is projected to grow four-fold to $73 billion by 2027. The government's PLI schemes are pumping billions into domestic manufacturing. Global supply chains are being redrawn in real-time. And at the center of it all sits a company that most investors discovered only when its rockets literally shot to the moon.

So buckle up. This isn't just a business story—it's a masterclass in how emerging market companies can leverage constraints as catalysts, how patient capital can outmaneuver fast money, and how sometimes the best strategy is simply to be ready when your country's moment arrives. Welcome to the Kaynes Technology story.

II. The Founder's Journey & Company Origins (1988–2008)

The Making of an Engineer

Ramesh Kunhikannan's childhood in 1960s Mysore bore no resemblance to the typical Silicon Valley founder mythology. Born in 1964 into a modest family with zero connections to technology or business, young Ramesh's fascination with engineering manifested in the most analog ways—dismantling household radios, attempting to fix neighbors' appliances, sketching circuit diagrams in school notebooks. His father worked a government job; his mother managed the household. The idea that their son would one day power India's moon mission would have seemed like fantasy.

But Mysore in the 1970s and 80s wasn't just any Indian city. Known as the "City of Palaces," it had a unique duality—ancient royal heritage coexisting with pockets of industrial activity. The city housed companies like BEML and Rail Wheel Factory, creating an ecosystem where engineering wasn't just theoretical but tangible. For a curious teenager like Ramesh, this meant exposure to real manufacturing, real problems, and real solutions.

At the National Institute of Engineering in Mysore, Ramesh pursued electrical engineering with an intensity that stood out even among ambitious peers. While classmates dreamed of government jobs or positions in established companies, Ramesh spent nights in the lab, not just completing assignments but understanding the why behind every circuit. Professors recall a student who asked uncomfortable questions—why were Indian companies importing simple electronic components? Why couldn't India manufacture its own printed circuit boards at scale?

The Workshop That Started Everything

In 1988, armed with an engineering degree and little else, 24-year-old Ramesh made a decision that seemed either courageous or foolish depending on who you asked. Instead of joining an established firm, he pooled together his meager savings—reports suggest it was less than Rs 50,000—and set up a small workshop in Mysore. The "company" was generous terminology for what was essentially a garage operation with second-hand equipment, a handful of local workers, and a single-minded focus: assembling printed circuit boards for whoever would pay.

The timing was both terrible and perfect. India in 1988 was still largely a closed economy—liberalization was three years away. Import licenses were gold dust. Foreign technology was virtually inaccessible. Capital was scarce and expensive. But these constraints forced innovation. Unable to import sophisticated equipment, Ramesh reverse-engineered processes. Unable to afford specialized workers, he trained local youth himself. Unable to access modern designs, he studied whatever technical manuals he could find in libraries and adapted them to Indian conditions.

The early clients were unglamorous—local industrial units needing basic PCB assemblies for control panels, small-scale manufacturers requiring simple electronic components. Each order was a lifeline. Ramesh personally oversaw every assembly, every solder joint, every quality check. The workshop operated on a simple principle that would later become company DNA: reliability at competitive prices. Not the cheapest, not the most sophisticated, but consistently dependable.

The Capital Constraint Innovation

What separates successful emerging market entrepreneurs from their developed market counterparts isn't access to resources—it's resourcefulness with constraints. Ramesh's approach to capital scarcity became a masterclass in this principle. Instead of seeking external funding (which was virtually non-existent for small-scale electronics manufacturing in 1990s India), he developed what he called the "reinvestment religion."

Every rupee of profit went back into the business. When a large order came in, instead of upgrading his personal life, Ramesh would buy slightly better equipment. When payments cleared, instead of expanding prematurely, he'd invest in training workers on new techniques. This wasn't patient capital by choice—it was patient capital by necessity. But it created something powerful: a company with zero debt, complete founder control, and an intimate understanding of unit economics.

By the mid-1990s, this approach started paying dividends. The workshop had evolved into a small factory. The client base expanded from local to regional. Orders grew from dozens of PCBs to hundreds, then thousands. But Ramesh understood that incremental growth wouldn't create a breakthrough. He needed a catalyst.

Enter Savitha: The Strategic Partnership

In 1996, Ramesh made perhaps his most important strategic decision—bringing his wife Savitha into the business. This wasn't nepotism; it was recognition that the company needed complementary skills. While Ramesh obsessed over technical perfection and customer relationships, Savitha brought financial discipline and operational efficiency. She restructured cost systems, negotiated with suppliers, and most critically, professionalized documentation and processes that would later prove essential for certifications.

The husband-wife dynamic created an interesting management structure. Board meetings happened at the dinner table. Strategic planning occurred during morning walks. This intimacy allowed for rapid decision-making but also created accountability—there was no separation between personal and professional stakes. When the company struggled, it affected family finances directly. When it succeeded, the joy was shared at home.

Savitha's entry coincided with India's growing electronics consumption. The late 1990s saw expansion in telecommunications, consumer electronics, and industrial automation. Each sector needed PCBs, and Kaynes was positioning itself to capture this demand. But they recognized a crucial limitation: remaining a pure assembly player meant competing on cost alone—a race to the bottom in a country where someone could always do it cheaper.

The Incorporation Moment

By 2008, twenty years after that first workshop, Kaynes had grown into something substantial yet still informal. The decision to formally incorporate as a private limited company wasn't just legal structuring—it was a declaration of ambition. The global financial crisis was unfolding, markets were in turmoil, but Ramesh and Savitha saw opportunity in chaos.

The incorporation brought discipline that the informal structure lacked. Proper books of accounts, formal employment contracts, systematic vendor agreements—the boring stuff that separates real companies from extended workshops. Revenue had crossed several crores, employees numbered in the dozens, and clients included recognized industrial names. But more importantly, incorporation was preparation for what Ramesh saw coming: the high-value pivot that would transform Kaynes from a vendor to a partner.

Looking back, these first twenty years seem almost quaint compared to what followed. But they established principles that would prove invaluable: technical excellence over marketing flash, reinvestment over consumption, relationships over transactions, and most importantly, the patience to build capabilities before chasing opportunities. The workshop kid from Mysore had built a real company. Now it was time to build an empire.

III. The Pivot to High-Value Sectors (2000s–2010s)

The Bet-the-Company Decision

By 2000, Kaynes faced an existential choice. The company could continue as a reliable but unremarkable PCB assembler, competing with hundreds of similar firms on price and delivery times. Or it could attempt something audacious: pivot into aerospace, defense, and medical electronics—sectors where entry barriers weren't just high, they were Mount Everest.

Ramesh's decision to pursue high-value sectors wasn't driven by spreadsheet analysis or consultant recommendations. It came from a simple observation during a client visit to HAL (Hindustan Aeronautics Limited) in nearby Bangalore. He noticed that critical electronic components for aircraft were being imported at astronomical costs, with lead times stretching months. India was assembling fighter jets but importing circuit boards. The irony was painful, the opportunity obvious.

But entering aerospace and defense wasn't like adding a new product line. These sectors demanded certifications that cost more than Kaynes' annual revenue. AS9100 for aerospace, ISO 13485 for medical devices, NADCAP for special processes—each certification required not just money but fundamental reorganization of operations. Quality control had to shift from "good enough" to "zero defects." Documentation had to evolve from basic records to complete traceability. Workers needed training not just in assembly but in understanding why a single failed component could cost lives.

The certification journey nearly broke the company. The first AS9100 audit failed spectacularly. Auditors found gaps in everything from environmental controls to process documentation. Ramesh recalls spending eighteen-hour days rewriting procedures, installing new equipment, retraining every single employee. Savitha managed cash flows down to the daily level, juggling vendor payments to keep certification consultants engaged while maintaining regular operations.

Building the Capability Stack

What emerged from this crucible was something remarkable: a company that didn't just have certifications but had internalized their philosophy. Kaynes developed what Ramesh called the "capability stack"—layered competencies that competitors couldn't easily replicate.

At the bottom was manufacturing excellence: clean rooms, automated optical inspection, X-ray inspection systems, environmental stress screening chambers. Equipment that cost crores but was essential for high-reliability electronics. The middle layer was process excellence: statistical process control, failure mode analysis, corrective action systems that actually worked. The top layer was design capability: engineers who didn't just assemble to specifications but could suggest improvements, identify potential failures, optimize for manufacturability.

This stack approach created compound advantages. Aerospace certification made medical device entry easier. Medical quality systems improved automotive processes. Each new sector didn't require starting from zero but building on existing capabilities. By 2010, Kaynes had accumulated competencies that would take new entrants a decade to replicate.

The numbers tell the story: from 2005 to 2010, despite the global financial crisis, Kaynes grew revenue at 35% CAGR. But more importantly, margins expanded from single digits to mid-teens as the company moved from commodity assembly to specialized manufacturing. A PCB for a washing machine might earn 5% margin; the same size board for an aircraft flight control system commanded 20%.

The Geographic Expansion Chess Game

With capabilities established, Kaynes faced a new challenge: customers wanted local presence. Aerospace companies in Hyderabad, automotive firms in Chennai, medical device makers in NCR—each demanded proximity for quick turnarounds and engineering collaboration. This triggered a geographic expansion that was more strategic chess than simple growth.

The first move outside Mysore came in Haryana, targeting the automotive and industrial corridor. But this wasn't just opening a factory; it was creating a complete ecosystem. Local hiring, supplier development, customer application centers where clients could test prototypes. Each facility became a hub for specific sectors, developing specialized expertise while leveraging common systems and processes.

By 2015, Kaynes operated eight strategically located facilities across Karnataka, Haryana, Himachal Pradesh, Tamil Nadu, and Uttarakhand. The Himachal facility focused on high-volume consumer electronics, leveraging tax benefits. The Tamil Nadu plant specialized in automotive electronics, sitting within driving distance of major OEM plants. The Uttarakhand facility handled industrial electronics, close to the northern industrial belt.

This wasn't empire building—it was calculated positioning. Each facility could serve as backup for others, providing supply chain resilience that customers valued. During the 2013 Uttarakhand floods, production seamlessly shifted to other plants without missing customer deadlines. This reliability in crisis became a selling point worth more than any marketing campaign.

From Vendor to Design Partner

The most profound transformation during this period wasn't physical expansion but intellectual evolution. Kaynes shifted from being a contract manufacturer executing customer designs to a design partner creating solutions. This transition, subtle from outside but revolutionary internally, redefined the company's value proposition.

It started with small suggestions—pointing out that a customer's design could be optimized for better thermal management or that component placement could reduce electromagnetic interference. Customers initially resisted ("just build what we designed"), but when Kaynes' suggestions reduced costs by 15% or improved reliability by 30%, resistance turned to reliance.

By 2012, Kaynes had formalized this into design-led manufacturing services. The company employed over 200 engineers focused not on production but on design optimization, value engineering, and product development. They developed specialized expertise in embedded systems, particularly for harsh environments—electronics that could function in the temperature extremes of space, the vibration of aircraft, the electromagnetic noise of industrial plants.

The business model implications were profound. Design services commanded premium pricing, created customer stickiness (switching costs increased dramatically when Kaynes co-owned the design), and generated intellectual property. By 2015, over 30% of revenue came from products where Kaynes had contributed to design, up from zero a decade earlier.

The Mature Embedded Capability

What truly distinguished Kaynes during this period was its embedded design capability—the ability to not just manufacture electronics but embed intelligence into products. This wasn't about making circuit boards; it was about creating smart systems that could sense, process, and respond.

The company developed expertise in real-time operating systems, communication protocols, sensor integration—the building blocks of intelligent devices. An automotive client wanting to add telematics to their vehicles didn't need to find separate hardware and software vendors; Kaynes could design the hardware, develop the firmware, integrate the communications, and manufacture at scale.

This capability positioned Kaynes perfectly for the IoT revolution that everyone talked about but few could execute. While competitors focused on either hardware or software, Kaynes straddled both worlds. A water meter manufacturer could come with a mechanical product and leave with a smart meter capable of remote reading, leak detection, and predictive maintenance.

By 2015, Kaynes wasn't just among the first companies in India to offer design-led electronics manufacturing—it was defining what that meant. The evolution from electronics manufacturing services provider to design-led manufacturer providing value-add services and ODM solutions was complete. The workshop had become a technology company that happened to manufacture, rather than a manufacturer trying to add technology.

IV. The IPO Journey & Public Markets (2022)

The Perfect Storm of Timing

In early 2022, Ramesh and Savitha faced a decision they'd deliberately avoided for decades: going public. The company was profitable, debt-free, and growing at 30%+ annually. They didn't need capital. But three forces converged to make an IPO not just attractive but almost inevitable.

First, the macro environment had shifted dramatically. Post-COVID supply chain disruptions had made "China+1" a boardroom priority globally. Apple was moving production to India. Tesla was scouting locations. Every global OEM wanted Indian manufacturing partners, and they preferred working with listed companies that offered transparency and governance standards.

Second, the Indian government had launched the PLI (Production Linked Incentive) scheme with Rs 2 lakh crore allocated for electronics manufacturing. But accessing these incentives effectively required scale, and scale required capital. Not for survival but for dominance—to build facilities that could handle billion-dollar orders, to invest in capabilities that would take years to generate returns.

Third, and perhaps most personally, Ramesh at 58 understood succession planning. A public listing would institutionalize the company, create wealth for employees who'd built Kaynes, and ensure continuity beyond the founders. The IPO wasn't an exit—the family would retain majority control—but it was evolution from family business to institution.

The Roadshow Reality Check

The IPO process revealed something fascinating: the gap between Kaynes' actual business and market perception. Investment bankers initially positioned it as "India's Foxconn," but Ramesh pushed back. Kaynes wasn't about scale manufacturing of consumer electronics; it was about complex, high-reliability electronics where India had genuine competitive advantage.

During roadshows, institutional investors asked predictable questions about competition with Dixon Technologies or global EMS giants. But when Ramesh explained that Kaynes made electronics for nuclear reactors, satellite systems, and submarine components—products where trust mattered more than cost—the narrative shifted. This wasn't a commodity play on Indian manufacturing; it was a strategic capability play on sectors where India was becoming self-reliant.

The IPO structure reflected founder confidence: Rs 857.82 crores total, with Rs 530 crores in fresh capital for expansion and Rs 327.82 crores as offer for sale, primarily for early investors and employees. The price band of Rs 587 per share valued the company at roughly Rs 3,600 crores—expensive by traditional metrics but reasonable for a company positioned at the intersection of multiple secular trends.

The Subscription Frenzy

When the IPO opened for bidding on November 10, 2022, the response exceeded all expectations. The issue was subscribed over 30 times, with qualified institutional buyers leading the charge at 65x subscription. This wasn't just enthusiasm; it was recognition that India's electronics manufacturing story needed pure-play proxies, and Kaynes was one of the few with actual capabilities rather than just ambitions.

The retail participation was particularly interesting. Unlike typical IPOs dominated by HNIs flipping for listing gains, Kaynes attracted long-term retail investors who understood the business. Many were engineers who'd worked in the electronics industry, investors who'd tracked the company's journey, or simply believers in India's manufacturing renaissance.

On November 22, 2022, when Kaynes listed on NSE and BSE, it opened at Rs 892—a 52% premium to the issue price. But this was just the beginning. What followed would make the IPO pricing look like a bargain.

The Use of Proceeds: Building for the Future

Post-IPO capital deployment revealed the strategic thinking that had built Kaynes. Instead of splurging on acquisitions or unrelated diversification, the company stuck to its knitting—but at an accelerated pace.

The largest chunk went toward capacity expansion, but not generic capacity. Kaynes invested in specialized capabilities: high-layer count PCB manufacturing for 5G applications, automated assembly lines for automotive electronics with sub-PPM defect rates, and critically, infrastructure for semiconductor assembly and testing. This wasn't following the herd into commodity manufacturing but building moats in complex electronics.

Debt reduction, though a smaller component, was strategic. While Kaynes had minimal debt, clearing it completely sent a signal: this company would grow through internal accruals and equity, not leverage. In a capital-intensive industry where competitors carried debt-to-equity ratios exceeding 1x, Kaynes' zero-debt status became a competitive advantage, allowing aggressive bidding for large contracts without balance sheet concerns.

The company also invested heavily in talent—not just technical but managerial. Post-IPO, Kaynes hired senior executives from global EMS companies, semiconductor firms, and automotive suppliers. The organization chart evolved from family-and-loyalists to professional management with domain expertise, though Ramesh and Savitha retained strategic control.

The Institutional Transformation

Going public forced changes that private Kaynes had resisted. Quarterly earnings calls replaced annual informal updates. Detailed segment reporting exposed previously opaque business lines. Independent directors brought questions that family members wouldn't ask. This transparency initially felt constraining but ultimately strengthened the company.

The discipline of public markets forced clearer capital allocation frameworks. Each new investment now required IRR calculations, not just strategic logic. The company developed formal policies for everything from related-party transactions to dividend distribution. What seemed like compliance burden actually improved decision-making speed—clear frameworks meant less debate, more execution.

Employee stock options, now liquid, transformed talent retention. Key engineers who'd considered joining startups stayed because their Kaynes equity had real value. The company could attract talent from MNCs by offering equity upside alongside competitive salaries. The IPO didn't just raise capital; it created currency for talent acquisition.

By early 2023, Kaynes had successfully transitioned from family enterprise to public company without losing entrepreneurial agility. Quarterly results showed consistent growth, margins expanded despite inflation, and the order book grew to unprecedented levels. The stock price reflected this execution, but the real transformation was yet to come. A mission to the moon would change everything.

V. The Chandrayaan-3 Moment: From Contractor to National Hero (2023)

The Call That Changed Everything

In 2019, four years before Chandrayaan-3 captured global attention, Kaynes received a cryptic inquiry from ISRO. The requirements were specific yet vague: electronic systems capable of functioning in extreme temperature variations (-200°C to +125°C), surviving radiation levels that would fry normal circuits, and maintaining precision despite vibrations that could shake apart conventional assemblies. Most critically, these systems needed to be light—every gram mattered when fuel costs Rs 1 crore per kilogram to launch.

Ramesh personally led the team responding to ISRO. This wasn't just another contract; it was validation of everything Kaynes had built over three decades. The certifications accumulated, the zero-defect manufacturing culture, the harsh-environment expertise—all culminated in this moment. But ISRO's requirements pushed even Kaynes' capabilities. They needed electronics that could work in vacuum, resist cosmic radiation, and operate autonomously 384,000 kilometers from Earth.

The development process was unlike any commercial project. ISRO engineers practically lived at Kaynes facilities, reviewing every design decision, questioning every component choice, testing beyond normal breaking points. Failure modes that had 0.0001% probability in terrestrial applications became unacceptable risks in space. The company developed new testing protocols, invested in specialized equipment, and most importantly, created a dedicated team that thought in space-grade reliability.

The Technical Mastery Behind the Mission

What Kaynes actually delivered for Chandrayaan-3 reveals the depth of capability required. The company provided critical electronic systems for both the Vikram lander and Pragyan rover—not just circuit boards but complete electronic subsystems that controlled navigation, communication, and scientific instruments.

The navigation electronics had to guide Vikram through the "15 minutes of terror"—the powered descent to the lunar surface where split-second decisions determined success or failure. The systems processed data from multiple sensors, calculated trajectory corrections, and controlled thrusters, all while maintaining redundancy. If one circuit failed, backups had to activate instantly without ground intervention.

For the Pragyan rover, Kaynes developed motor control electronics that would drive the six wheels across lunar regolith, camera systems that would capture and transmit images, and power management systems that would preserve battery life in the harsh lunar environment. Each system was manufactured in duplicate or triplicate—redundancy was religion when repair was impossible.

The manufacturing process itself was extraordinary. Clean rooms were upgraded to Class 100 standards. Components were individually tested and tracked. Each solder joint was X-rayed. Thermal cycling pushed assemblies through temperature ranges they'd never experience on Earth. Vibration testing simulated launch conditions that would destroy consumer electronics in seconds. Only after months of testing did ISRO accept the systems for integration.

August 23, 2023: The Moon Landing

When Vikram touched down near the lunar south pole at 6:04 PM IST, making India the fourth nation to soft-land on the moon and the first to reach the south pole region, Ramesh watched from Kaynes' Mysore facility with hundreds of employees. Many had worked on the project without knowing its ultimate purpose—ISRO contracts came with strict confidentiality requirements.

The landing was flawless, but for Kaynes engineers, the real validation came over the following days. Every system functioned perfectly. The rover rolled out, instruments activated, communications remained stable. In the extreme cold of lunar night and scorching heat of lunar day, Kaynes' electronics performed exactly as designed. This wasn't just technical success; it was proof that Indian manufacturing could meet the highest global standards.

The immediate aftermath was subdued. ISRO's success was celebrated nationally, but Kaynes' role remained largely unknown outside industry circles. The company had signed NDAs preventing publicity, and Ramesh, ever understated, saw no need for chest-thumping. But markets have their own intelligence networks.

The Market Discovery and Wealth Explosion

Within days of the landing, research analysts began connecting dots. Supply chain experts identified Kaynes components in mission photographs. Former ISRO scientists confirmed the company's involvement in interviews. By August 28, five days after landing, the secret was out: the same company that made automotive electronics had powered India's moon mission.

The market reaction was volcanic. On August 29, Kaynes stock opened 10% higher and kept climbing. By September end, shares had surged 40% from pre-landing levels. The logic was simple but powerful: if Kaynes could meet ISRO's standards, every commercial customer would want their capabilities. The space qualification became the ultimate quality stamp, worth more than any marketing campaign.

But the real transformation was in Ramesh's personal wealth. The stock surge pushed his net worth past $1 billion by November 2023, making him one of the few first-generation Indian entrepreneurs to achieve billionaire status through manufacturing rather than software or services. The boy from modest Mysore family had joined India's billionaire club, not through financial engineering or market speculation, but by building capabilities that put India on the moon.

The Strategic Implications

Chandrayaan-3 wasn't just a financial windfall; it fundamentally repositioned Kaynes in global supply chains. International aerospace companies that had hesitated to source from India now actively sought partnerships. The European Space Agency inquired about collaboration. NASA contractors explored supply agreements. The moon landing had provided third-party validation that no amount of marketing could achieve.

Domestically, the impact was even more profound. The Department of Space increased procurement budgets for indigenous suppliers. DRDO expanded vendor development programs. The Indian Navy, Army, and Air Force—all seeking to reduce import dependence—viewed Kaynes differently. From one of many vendors, the company became a strategic partner in India's self-reliance journey.

The talent impact was equally significant. Top engineers from ISRO, many nearing retirement, joined Kaynes to build commercial space capabilities. Young graduates who might have chosen software companies now saw hardware and space technology as exciting career paths. IIT placement cells, which hadn't previously featured Kaynes prominently, now highlighted the company alongside tech giants.

Building the Space Vertical

Post-Chandrayaan, Kaynes didn't rest on laurels but doubled down on space capabilities. The company established a dedicated aerospace and defense vertical with separate P&L responsibility, specialized facilities, and autonomous decision-making. This wasn't opportunistic pivoting but systematic capability building.

The company began developing components for satellite constellations—the hundreds of small satellites that would enable global broadband, earth observation, and IoT connectivity. Each satellite needed electronics for power management, communication, attitude control, and payload operation. With Indian companies like OneWeb and international players like SpaceX planning mega-constellations, the addressable market was massive.

Kaynes also entered adjacent areas: ground station equipment for satellite communication, testing equipment for space components, and even early-stage development of electronic systems for launch vehicles. The vision was clear: as India's space industry evolved from government-led to commercial, Kaynes would be the essential electronics partner.

By early 2024, space and defense contributed over 15% of revenue, up from single digits pre-Chandrayaan. More importantly, these segments commanded the highest margins and created a halo effect on other businesses. Automotive customers valued space-grade quality processes. Medical device companies appreciated the reliability culture. The moon mission hadn't just created wealth; it had transformed Kaynes from vendor to technology partner.

The Chandrayaan success story embodied everything remarkable about India's manufacturing potential: patient capability building meeting momentous opportunity. But it also raised the stakes. Having proven it could reach the moon, Kaynes now faced expectations of reaching the stars.

VI. Business Model & Competitive Advantages

The Four Pillars of Value Creation

At its core, Kaynes operates through four distinct but synergistic business verticals that create multiple touchpoints with customers and compound competitive advantages. Understanding how these pieces fit together reveals why the company commands premium valuations despite being in the supposedly commoditized EMS sector.

The first pillar, OEM-Turnkey Solutions for Box Build, represents complete product assembly—taking individual components and delivering finished electronic products ready for market. This isn't just putting pieces together; it's managing entire supply chains, ensuring quality across hundreds of components, and delivering just-in-time to customer production lines. When an automotive OEM needs dashboard assemblies or a medical device company requires patient monitoring systems, Kaynes handles everything from procurement to final testing.

The second pillar, PCBA (Printed Circuit Board Assembly) services, might seem like the commodity end, but Kaynes has systematically premiumized this segment. The company doesn't compete for simple, high-volume PCBAs that race to bottom on price. Instead, it focuses on complex, multi-layer boards for mission-critical applications—the kind where failure costs aren't measured in warranty claims but in human lives or mission failures.

The third pillar, ODM (Original Design Manufacturing), is where Kaynes transcends typical EMS players. Here, customers arrive with problems, not products. A railway company needs a signaling system that works in extreme weather. A nuclear power plant requires radiation-hardened control systems. Kaynes designs, prototypes, tests, and manufactures solutions, owning intellectual property and creating switching costs that lock in relationships for decades.

The fourth pillar, Product Engineering and IoT Solutions, positions Kaynes for the future. The company doesn't just add connectivity to products; it reimagines them for the connected age. A traditional energy meter becomes a smart grid node. An industrial motor becomes a predictive maintenance system. This isn't about chips and circuits; it's about data, analytics, and recurring revenue streams from software and services.

The Integrated Manufacturing Advantage

What truly distinguishes Kaynes from typical EMS players is its integrated manufacturing approach—a strategy that required decades of patient investment but now creates formidable competitive moats. The company has ventured into semiconductor assembly and testing (OSAT) and high-density interconnect PCBs (HDI PCBs), positioning itself as one of the few Indian companies capable of handling the entire electronics value chain.

The OSAT capability deserves special attention. Kaynes Technology plans to set up a subsidiary for outsourced semiconductor assembly and testing (OSAT) business, with 12 lines planned at its upcoming OSAT and Compound Semiconductor facility near Hyderabad, Telangana, with investment exceeding Rs 2800 crore. This isn't just capacity addition; it's strategic positioning for the semiconductor age. "This is the first paying OSAT customer in India," as announced during the collaboration with Lightspeed Photonics, marking a historic milestone for Indian semiconductor manufacturing.

The vertical integration philosophy extends beyond semiconductors. Kaynes possesses build-capabilities for custom designing of testing hardware for automated test equipment, with test equipment designed and built in-house including custom firmware supporting various platforms, processors and microcontrollers, along with test application software for automated testing, analysis, report generation, alert generation and data push to server. This means customers don't need separate vendors for design, manufacturing, and testing—Kaynes handles the entire value chain.

The Certification Moat

While competitors scramble for individual certifications, Kaynes has built what might be India's most comprehensive quality certification portfolio—10 global accreditations making it the most certified ESDM company in the country. But these aren't vanity metrics; each certification opens doors to sectors where others cannot compete.

The AS9100 certification for aerospace didn't just allow Kaynes to make aircraft components; it forced the company to implement quality systems that improved every other vertical. The ISO 13485 for medical devices created documentation standards that automotive customers appreciated. The EN 9110/AS 9110 certification for avionics repairs allows for critical electronics repair and maintenance of commercial, private, and military aircraft, capabilities that took years to develop but now generate recurring revenue from maintenance contracts.

This certification stack creates a virtuous cycle. New customers are attracted by existing certifications, their requirements drive new certifications, which in turn attract more sophisticated customers. A competitor trying to replicate this would need not just money but years of operational transformation.

The Customer Portfolio Power

With over 350 international customers, Kaynes has achieved something rare in manufacturing: customer diversification without operational complexity. The company doesn't serve 350 different industries with 350 different processes. Instead, it focuses on customers whose needs overlap—an automotive ECU manufacturer and an aerospace avionics company both need high-reliability electronics, just with different specifications.

This customer overlap creates knowledge spillovers. Techniques developed for automotive functional safety help improve medical device reliability. Aerospace traceability requirements enhance nuclear component documentation. Each customer makes every other customer's products better—a network effect in manufacturing that's difficult to replicate.

The customer mix also provides recession resilience. When automotive spending declined during COVID, defense and medical segments grew. When consumer electronics slowed, industrial automation accelerated. This isn't luck; it's deliberate portfolio construction over decades.

The IoT and Smart Device Revolution

Kaynes has gained technological expertise and evolved from an electronics manufacturing services provider into a design-led manufacturer providing value-add electronics manufacturing services and ODM solutions in fields of dispensing solutions, smart devices, connectivity technologies, IoT solutions, brushless drive technology, and Gallium Nitride technology. This evolution positions the company perfectly for the IoT revolution.

The value proposition here transcends traditional manufacturing. The company operates canvas-to-cloud industrial internet of things (IIoT) solutions, meaning it doesn't just make IoT devices but provides complete ecosystems—hardware, firmware, connectivity, cloud infrastructure, and analytics. A utility company wanting smart meters doesn't need to coordinate multiple vendors; Kaynes delivers an end-to-end solution.

This IoT capability is particularly powerful in industrial applications. Legacy industrial equipment worth billions needs retrofitting for Industry 4.0, but original manufacturers often lack IoT expertise. Kaynes bridges this gap, transforming "dumb" machines into intelligent assets that provide predictive maintenance, energy optimization, and operational insights.

The Services Layer

Beyond manufacturing, Kaynes has built a high-margin services business that deepens customer relationships and provides recurring revenue. The company undertakes repairs and provides rehabilitation of electronic cards in railways, aerospace and defense and industrial verticals at its servicing and maintenance business unit at Navi Mumbai, specializing in re-engineering at component and PCBA level to meet obsolescence and discontinuance issues, with third-party service support extended in electronics repair for railways, and aerospace and defence establishments.

This services capability is strategic gold. Military equipment designed decades ago needs maintenance, but original components are obsolete. Kaynes reverse-engineers replacements, ensuring compatibility while upgrading performance. Railway signaling systems installed in the 1990s need modernization without complete replacement. The company provides upgrade paths that preserve existing investments while adding new capabilities.

The services business also provides market intelligence. By maintaining equipment, Kaynes understands failure modes, improvement opportunities, and replacement cycles. This knowledge feeds back into design and manufacturing, creating products that address real-world problems competitors don't even know exist.

VII. Modern Era: Expansion & Future Bets (2023–Present)

The Financial Transformation Story

The financial transformation at Kaynes in the modern era tells a story of exceptional execution meeting favorable market conditions. With a market cap of Rs 39,108 Crore, Revenue of Rs 2,891 Cr, and Profit of Rs 317 Cr, the company has evolved from a successful mid-cap to a legitimate large-cap player in India's EMS space.

The Q1 FY26 results released in July 2025 showcased the acceleration in progress. Consolidated revenue jumped to ₹673.47 crores vs ₹503.98 crores year-over-year, while consolidated PAT reached ₹74.61 crore in Q1 FY26, representing a 46.94% YoY increase. But what's more impressive than the absolute numbers is the quality of growth—margins expanding despite inflation, order book swelling despite global uncertainty.

The orderbook stood at Rs 74,011 million as of June 30, 2025, representing a 47% YoY growth. This isn't just backlog; it's validation that customers are committing to long-term partnerships. The order composition reveals the strategic positioning—aerospace contracts with multi-year visibility, EV components for global OEMs, smart infrastructure projects backed by government spending.

The Semiconductor Ambition

The semiconductor ambition represents Kaynes' boldest bet yet. Homegrown electronics manufacturer Kaynes Technology is investing ₹2,850 crore ($342 million) to set up an outsourced semiconductor assembly and test (OSAT) and compound semiconductor facility near Hyderabad in Telangana. But the story evolved further when the Union Cabinet approved the proposal of Kaynes Semicon Pvt Ltd, a wholly owned subsidiary of the company, to set up a semiconductor unit in Sanand, Gujarat. The proposed unit will be set up with an investment of Rs 3,300 crore.

This isn't just capacity expansion; it's positioning for the next decade of electronics evolution. The fabrication unit will have the capacity to produce six million chips per day. The chips produced in this unit will cater to a wide variety of applications which include segments such as industrial, automotive, electric vehicles, consumer electronics, telecom and mobile phones, among others. The dual-location strategy—Hyderabad for initial capabilities, Gujarat for scaled production—shows sophisticated planning.

The government support is crucial. The investment will be funded by a mix of contributions: 50 percent or Rs1,653.5 crore from the central government, 20 percent or Rs661.4 crore from the Gujarat state government, and the remaining 30 percent or Rs992.1 crore will be invested by Kaynes Semicon. This isn't subsidy; it's strategic partnership where government and private capital align for national capability building.

The Tamil Nadu Mega Investment

In August 2025, Kaynes announced another game-changing investment. MoU signed for ₹4,995 Cr investment in Tamil Nadu manufacturing over 6 years. The new plant aims to produce high-tech components such as 74-layer printed circuit boards (PCBs), high-density interconnect (HDI) PCBs, flexible PCBs, high-performance laminates, camera module assemblies, and wire harness assemblies.

This initiative marks a significant milestone as the first large-scale PCB manufacturing investment in Tamil Nadu, positioning the state as a new electronics hub beyond traditional centers. The facility is expected to generate approximately 4,700 jobs, contributing to economic growth and technological advancement in Thoothukudi and surrounding regions.

The strategic logic is compelling. PCBs are the backbone of every electronic device, yet India imports most high-complexity boards. By manufacturing 74-layer PCBs domestically—complexity levels typically reserved for aerospace and high-performance computing—Kaynes isn't just import substituting; it's capability building that enables entire ecosystems.

Global Expansion Through Acquisition

The modern era also saw Kaynes' first significant international move. The recent acquisition of August Electronics in Canada aligns with the strategy to enhance North American presence and capitalize on opportunities amid increasing geopolitical trade shifts, with expected growth from this acquisition projected at around 20% over the next 5 years.

This isn't empire building but strategic positioning. North American customers increasingly want supply chain diversification but need suppliers who understand their quality requirements, certification needs, and business culture. An acquired Canadian presence provides the beachhead for serving these customers while manufacturing in India—the best of both worlds.

The China+1 Positioning

Perhaps no trend benefits Kaynes more than the global supply chain reconfiguration away from China concentration. But unlike many Indian companies that simply tout "China+1" in investor presentations, Kaynes has systematically built the capabilities that global customers actually need when diversifying.

The company doesn't compete on labor cost—those days are gone. Instead, it offers integrated capabilities that Chinese suppliers built over decades: design support, rapid prototyping, volume manufacturing, and entire ecosystem management. When a global automotive Tier-1 wants to diversify from China, they need a partner who can handle everything from initial design to volume production to after-sales support. Kaynes is one of the few Indian companies that can credibly make that claim.

The numbers validate the strategy. Order book grew from Rs 50,386 million in Q1FY25 to Rs 74,011 million by Q1FY26. Much of this growth comes from global customers establishing India footprints, whether driven by supply chain risk, government incentives, or market access. Each new customer relationship tends to expand—starting with one product line, then expanding as trust builds.

The Vision Articulated

Management's vision is ambitious but grounded. The company targets USD 1 billion revenue by FY28, with a projected CAGR of 57% in revenue over FY25-FY27. Beyond that, the target is $2 billion by FY30. These aren't random numbers but careful calculations based on capacity additions, customer commitments, and market growth.

The margin story is equally important. Q1 EBITDA margin of 16.8% exceeded the earlier full-year guidance of 15.6%, driven by higher share of ODM and advanced technology products. As semiconductor and PCB facilities come online, margins should expand further—these are inherently higher-value activities than traditional EMS.

But perhaps most importantly, Kaynes is building for a future where electronics isn't a sector but the substrate of every sector. Cars are becoming computers on wheels. Medical devices are becoming connected diagnostic platforms. Industrial equipment is becoming intelligent. In this future, companies that can integrate hardware, software, and connectivity will capture disproportionate value. Kaynes is positioning to be that company for India and increasingly, the world.

VIII. Playbook: Business & Investing Lessons

Capital Constraints as Innovation Catalyst

The Kaynes story demolishes a persistent myth about emerging market companies—that they need abundant capital to compete globally. Ramesh's journey proves the opposite: constraints force innovation in ways abundance never could. Unable to import expensive equipment in the 1990s, Kaynes developed in-house capabilities that later became competitive advantages. Unable to access venture capital, the company learned unit economics discipline that now allows it to grow profitably while competitors burn cash.

This constraint-driven innovation extends beyond equipment to entire business models. Take the geographic expansion strategy. Instead of building massive centralized facilities like Chinese competitors, Kaynes created distributed manufacturing nodes, each specialized for local markets. This wasn't just making virtue of necessity—it created supply chain resilience that customers now pay premiums for. During COVID, when single-location manufacturers faced shutdowns, Kaynes shifted production between facilities seamlessly.

The lesson for investors is counterintuitive: look for companies that succeeded despite constraints, not because of abundance. These companies develop muscles that privileged competitors never need. When external capital finally arrives—as it did post-IPO for Kaynes—these companies deploy it with surgical precision rather than spraying money at problems.

The Compound Power of Reinvestment

For over three decades, Kaynes practiced what might be called "radical reinvestment"—virtually every rupee of profit went back into the business. This wasn't financial engineering or tax optimization; it was conviction that compound capabilities beat compound returns. Each piece of equipment purchased enabled slightly more complex products. Each certification achieved opened slightly more lucrative markets. Each engineer hired created slightly more customer value.

The mathematics of this approach are staggering. A 30% annual reinvestment rate compounds to 13,000% over 30 years. But the real compounding happened in capabilities, not just capital. The ability to do 4-layer PCBs enabled 8-layer capabilities, which enabled 16-layer expertise, ultimately reaching today's 74-layer complexity. Each step seemed incremental, but the cumulative effect created moats that would take competitors decades to cross.

Modern investors obsessed with capital efficiency metrics might have passed on early Kaynes—the company consistently chose capability building over margin optimization. But this patient approach created something more valuable than high ROCE: customer relationships where switching costs approach infinity. When you're making electronics for nuclear reactors or satellites, customers don't switch for 50 basis points of cost savings.

Timing Market Transitions

Kaynes' history reads like a masterclass in timing structural transitions. The company didn't try to time cycles or predict quarterly demand. Instead, it positioned for secular shifts years before they materialized. The aerospace pivot in 2000 preceded India's defense modernization by a decade. The IoT investments in 2015 came before smart cities became government priority. The semiconductor plans in 2020 anticipated the global chip shortage and India's semiconductor mission.

This isn't luck or prescience—it's pattern recognition combined with patience. Ramesh understood that India's development would follow predictable phases: first, basic manufacturing; then, complex assembly; then, design integration; finally, cutting-edge technology. By building capabilities one stage ahead of market demand, Kaynes could capture premium economics when transitions occurred.

The "Make in India" program launched by PM Modi in 2014 exemplifies this dynamic. While competitors scrambled to build capabilities post-announcement, Kaynes had spent the previous decade preparing. When government incentives arrived, when global customers started sourcing, when local content requirements kicked in, Kaynes was ready. The company didn't benefit from Make in India—Make in India benefited from companies like Kaynes that had already built the capabilities.

Family Business, Professional Management

The evolution of Kaynes' governance structure offers lessons for family businesses worldwide. Ramesh and Savitha maintained majority control (53.5% promoter holding) while progressively professionalizing management. This wasn't the typical family business narrative of resistance to outside talent or governance structures. Instead, the founders actively recruited senior executives from global companies, implemented institutional processes, and created genuine accountability.

The key was separating strategic control from operational management. The founders retained veto rights on major capital allocation and strategic direction while delegating day-to-day operations to professional managers. Board meetings evolved from family discussions to structured governance with independent directors asking tough questions. This hybrid model—entrepreneurial vision with professional execution—proved more powerful than either pure family or pure professional management.

The succession planning, still evolving, shows similar thoughtfulness. Rather than automatic family succession or complete professionalization, Kaynes is building a bench of both family and non-family leaders, letting capability rather than bloodline determine roles. This pragmatic approach ensures continuity without sacrificing competence.

The Certification-Standard Arbitrage

One of Kaynes' most underappreciated strategies was what might be called "certification arbitrage." The company understood that in B2B manufacturing, certifications aren't just quality stamps—they're exclusion mechanisms that limit competition. Every certification required—AS9100, NADCAP, ISO 13485—eliminated dozens of potential competitors who couldn't afford or wouldn't endure the certification process.

But Kaynes went further, accumulating certifications across sectors to create combination advantages. A competitor might match Kaynes' aerospace certifications or medical certifications, but matching all 10 global accreditations while maintaining operational efficiency? Nearly impossible. This certification stack became like compound interest—each new certification made the next one easier to obtain (shared quality systems) while making the total package harder to replicate.

The financial impact is striking. Products requiring multiple certifications command 25-40% gross margins versus 10-15% for single-certification products. More importantly, customer acquisition costs approach zero—customers needing specific certification combinations have few alternatives. Kaynes doesn't win on price; it wins by being the only qualified option.

Vertical Integration as Strategic Choice

While the tech world preaches asset-light models and outsourcing everything non-core, Kaynes systematically integrated vertically—but with strategic logic. The company didn't integrate for control or size but for capability gaps in the ecosystem. When reliable PCB suppliers didn't exist, Kaynes built PCB capabilities. When semiconductor assembly became a bottleneck, Kaynes entered OSAT. When customers needed IoT solutions, Kaynes developed software capabilities.

This selective vertical integration created three advantages. First, it eliminated ecosystem dependencies that constrained growth. Second, it captured margin pools that would otherwise go to suppliers. Third, and most importantly, it created integrated solutions that competitors assembling third-party components couldn't match.

The upcoming semiconductor and PCB facilities exemplify this philosophy. Kaynes isn't trying to compete with TSMC in logic chips or with Chinese manufacturers in commodity PCBs. Instead, it's filling specific gaps—advanced packaging for power electronics, high-layer PCBs for 5G infrastructure—where integration with existing capabilities creates unique value.

The Trust Premium in Critical Electronics

Perhaps the most important lesson from Kaynes is that in critical electronics, trust trumps everything—price, features, even performance. When you're making electronics for nuclear reactors, spacecraft, or medical devices, failure isn't measured in warranty claims but in human lives and national security. In these markets, three decades of zero-defect delivery is worth more than any cost advantage.

Kaynes systematically built this trust through radical transparency, conservative promises, and consistent delivery. The company under-promised and over-delivered so consistently that customers learned to rely on Kaynes' commitments for their own planning. This trust compounds—each successful project makes the next sale easier, each crisis handled well deepens relationships.

The financial value of trust is enormous but hidden in traditional metrics. It appears as customer concentration that doesn't create risk (because switching is unthinkable), as pricing power that doesn't erode with competition, as growth that doesn't require marketing spend. When India needed electronics for Chandrayaan-3, the trust Kaynes had built over decades was worth more than any capability presentation.

IX. Analysis & Bear vs. Bull Case

Bull Case: The Convergence of Megatrends

The optimistic view on Kaynes rests on multiple structural tailwinds converging simultaneously. India's ESDM market projected to grow four-fold to $73 billion by 2027 isn't just growth—it's a generational transformation. Unlike previous cycles driven by single factors, this expansion has multiple independent drivers: government policy, global supply chain shifts, domestic consumption growth, and technology transitions. Even if one driver disappoints, others can sustain momentum.

The strong order book visibility deserves special attention. At Rs 74,011 million as of June 30, 2025, representing roughly 2.5x annual revenue, this isn't just backlog—it's contracted future revenue with established customers. Unlike consumer businesses where demand can evaporate overnight, these orders represent multi-year commitments for critical components. The order book composition—aerospace, defense, industrial—suggests recession-resistant demand that could actually strengthen during downturns as governments increase strategic spending.

Kaynes' first-mover advantage in integrated EMS with design capabilities positions it uniquely for value capture. While competitors fight for commodity assembly work, Kaynes owns customer relationships at the design phase. This means higher margins, deeper moats, and earlier visibility into technology trends. As products become more complex—74-layer PCBs, advanced semiconductor packaging—the gap between Kaynes and subscale competitors widens exponentially.

Government support through PLI schemes and strategic sector focus provides unprecedented tailwinds. Unlike previous industrial policies that created inefficient national champions, current schemes reward performance and capability building. Kaynes' alignment with strategic sectors—space, defense, nuclear—ensures continued policy support regardless of political changes. The company isn't dependent on subsidies but benefits from them—a crucial distinction.

The valuation math, while optically expensive, makes sense for fundamental growth. If Kaynes achieves its $1 billion revenue target by FY28 with 15% EBITDA margins, at a conservative 25x EV/EBITDA multiple (versus current 60x), the market cap could triple. Add successful semiconductor/PCB ventures, and the upside becomes asymmetric. This isn't speculative hope but extrapolation of current trajectory.

Bear Case: The Execution and Competition Challenges

The skeptical view starts with return metrics that raise questions. Low return on equity of 11.5% over last 3 years in a supposedly high-growth, high-margin business suggests either capital inefficiency or margin pressure. While management explains this as investment for future growth, sustained low returns could indicate structural challenges in achieving targeted economics.

Capital intensity presents ongoing challenges. Unlike software or asset-light businesses, electronics manufacturing requires continuous capital investment just to maintain competitiveness. The Rs 3,300 crore semiconductor investment, Rs 4,995 crore Tamil Nadu expansion—these aren't one-time investments but the beginning of perpetual capital needs. Each technology generation requires new equipment, threatening returns.

Competition from global EMS giants remains a persistent threat. Foxconn, Flex, Jabil—these companies have scale, relationships, and capabilities that dwarf Kaynes. As India becomes more attractive, these giants are establishing local operations. While Kaynes has local advantages, global customers might prefer working with known partners who can serve them worldwide. The question isn't whether Kaynes can compete but at what cost.

Execution risks in rapid expansion could derail growth narratives. Managing multiple facility expansions, integrating acquisitions, entering new technologies—each carries execution risk. The semiconductor venture is particularly concerning; even established players struggle with yield rates and technology transitions. One major execution failure could damage the trust premium that took decades to build.

The valuation leaves zero room for disappointment. Stock trading at 13.2 times book value prices in flawless execution. Any delay in semiconductor production, margin compression from competition, or customer concentration issues could trigger violent derating. The stock's 234% return since IPO has created expectations that become increasingly difficult to meet.

The Competitive Landscape Reality

The competition analysis reveals nuanced dynamics. Dixon Technologies, often cited as Kaynes' primary competitor, actually operates in largely different segments—consumer electronics versus Kaynes' industrial focus. This isn't direct competition but category expansion risk if Dixon enters Kaynes' segments or vice versa.

Syrma SGS represents a more direct competitor with similar capabilities and certifications. But the market is growing fast enough to accommodate multiple winners. The real competition isn't for existing business but for new global customers establishing India operations. Here, execution track record, certification stack, and trust premium matter more than marginal cost differences.

Global players present different challenges. They bring scale and customer relationships but also bureaucracy and global cost structures. Kaynes' advantage lies in entrepreneurial agility—the ability to customize solutions, make quick decisions, and provide CEO-level attention to strategic customers. This David versus Goliath dynamic has historically favored focused local champions in complex manufacturing.

Valuation Framework for Long-term Investors

At current levels, the valuation mathematics require careful consideration. The forward P/E of ~79x for FY26 seems astronomical, but examining the trajectory reveals a different story. If the company delivers 57% revenue CAGR through FY27 as projected, with margins expanding from operational leverage, the FY28 P/E could compress to 25-30x—expensive but not irrational for a company growing at 30%+ with strategic positioning.

The key is understanding what you're paying for: not just current earnings but option value on India's electronics manufacturing future. If India captures even 10% of global electronics manufacturing by 2030 (from 3% currently), and Kaynes maintains its ~2% share of Indian ESDM, the revenue opportunity exceeds $5 billion. Current valuation at Rs 39,000 crore ($4.5 billion) doesn't seem unreasonable against this potential.

The margin of safety, paradoxically, comes from diversification—not portfolio diversification but business model diversification. Unlike single-product or single-customer companies, Kaynes has multiple ways to win: semiconductor success, PCB dominance, IoT solutions adoption, defense indigenization, space commercialization. Each path alone could justify current valuation; multiple successes create substantial upside.

The Structural versus Cyclical Debate

The crucial analytical question is whether Kaynes' growth is structural or cyclical. Bears argue that electronics manufacturing is inherently cyclical, subject to inventory cycles, technology transitions, and global economic swings. The current boom, they suggest, reflects post-COVID restocking and government stimulus that will inevitably reverse.

Bulls counter that India's electronics manufacturing is in structural transformation similar to China in the 2000s. The shift from import dependence to domestic manufacturing, from assembly to design, from low-value to high-value products—these are decade-long transitions, not cycles. Government commitment through PLI schemes, infrastructure investment, and strategic sector focus suggests sustained support regardless of global cycles.

The truth likely combines both perspectives. Short-term volatility is inevitable—order flow will fluctuate, margins will compress and expand, growth will accelerate and decelerate. But the structural direction seems clear: India will manufacture more electronics, complex products will proliferate, and companies with capabilities will capture value. Kaynes is positioned for this structural shift while remaining vulnerable to cyclical swings—a reality investors must accept.

X. Epilogue & "If We Were CEOs"

The International Expansion Dilemma

If we were running Kaynes today, the most pressing strategic question would be the pace and pattern of international expansion. The Canadian acquisition opens North American possibilities, but should Kaynes double down on India or aggressively expand globally? The answer isn't obvious.

The case for domestic focus is compelling. India's electronics market will grow from $75 billion to $300 billion by 2030—enough opportunity for decades of growth. Kaynes understands Indian customers, regulations, and ecosystems better than any global competitor. Capital deployed in India generates higher returns than unfamiliar markets. Why chase global complexity when domestic opportunity abounds?

But the global expansion argument has merit. Large customers increasingly demand global supply chains—serving them only from India limits relationship depth. International presence provides natural currency hedges and market diversification. Most critically, global operations accelerate capability learning—exposure to different standards, technologies, and competitors makes the entire organization stronger.

The optimal strategy might be selective globalization—not trying to be everywhere but establishing presence in strategic nodes. A European facility for aerospace customers, a Southeast Asian plant for consumer electronics, a Mexico operation for North American automotive. Each expansion would be capability-driven rather than volume-driven, enhancing rather than diluting core competencies.

The Semiconductor Depth Decision

The semiconductor venture represents a defining bet. The question isn't whether to enter—that decision is made—but how deep to go. Should Kaynes focus on packaging and testing where investment is manageable, or eventually move toward front-end fabrication where real value creation happens?

The conservative approach would limit semiconductor ambitions to OSAT—already capital intensive but manageable with government support. This provides sufficient value capture without existential risk. Focus on becoming India's best OSAT player rather than chasing fabrication dreams that have bankrupted better-capitalized companies.

Yet the aggressive approach has logic. India needs domestic fabrication capability for strategic autonomy. Government support will be maximum for early movers. Technology partnerships are available now that might not exist later. Most importantly, fabrication capability would make Kaynes indispensable to India's technology ambitions—a position worth almost any investment.

The pragmatic path might be progressive deepening—master OSAT first, then advanced packaging, then compound semiconductors, eventually logic chips. Each stage funds the next, reduces risk, and builds capabilities. This isn't lack of ambition but recognition that semiconductor manufacturing is perhaps humanity's most complex endeavor.

Software and Hardware Integration

The convergence of hardware and software presents both opportunity and challenge. Pure hardware margins are compressing globally; value increasingly comes from software and services. Should Kaynes build serious software capabilities or partner for them?

Building software capabilities internally seems necessary. IoT solutions require firmware, embedded software, cloud platforms, and analytics—outsourcing these means giving away value and customer relationships. The company needs thousands of software engineers, not dozens. This means cultural transformation—attracting different talent, managing different processes, accepting different economics.

But wholesale transformation into a software company would be a mistake. Kaynes' advantage is making physical products that work in harsh environments with zero failure tolerance. Software should enhance this capability, not replace it. The goal isn't becoming Infosys but creating hardware-software solutions that neither pure hardware nor pure software companies can match.

Institutionalization Without Bureaucratization

As Kaynes scales toward $1 billion revenue, maintaining entrepreneurial agility becomes exponentially harder. The company needs institutional processes for quality, compliance, and risk management. But excessive bureaucracy could destroy the responsiveness that customers value.

The solution might be federated autonomy—business units operating as mini-companies with P&L responsibility and decision authority. Central functions provide platforms and standards but don't control operations. This preserves entrepreneurial energy while ensuring institutional consistency.

Leadership development becomes critical. Kaynes needs hundreds of leaders who think like owners, not employees. This requires genuine empowerment, equity participation, and tolerance for failure. The ESOP expansion post-IPO was a start, but cultural transformation takes years.

The Succession Question

While premature to discuss immediate succession, building institutional continuity is essential. The company's dependence on founder vision, while currently a strength, could become vulnerability. The transition from founder-led to institution needs careful orchestration.

The optimal approach might be gradual transition—founders remaining as strategic architects while operational leadership transfers to next generation. This could include both family members who've proven capability and professional managers who've internalized company values. The key is meritocracy—leadership based on capability rather than lineage or tenure.

Capital Allocation in the Age of Abundance

After decades of capital scarcity, Kaynes now has access to abundant capital—from operations, government support, and capital markets. Managing abundance is paradoxically harder than managing scarcity. How should the company deploy capital for maximum long-term value?

The framework should prioritize capability building over capacity addition. New facilities should enhance technological capabilities, not just add production volume. Acquisitions should bring new competencies, not just revenue. R&D investment should create proprietary advantages, not just match competitor offerings.

Dividend policy needs reconsideration. While reinvestment has driven growth, at some scale, returning capital to shareholders becomes optimal. A progressive dividend policy—paying out excess capital while retaining growth needs—would signal confidence and maturity.

Final Reflections on India's Manufacturing Renaissance

Kaynes' journey from Mysore workshop to semiconductor ambitions mirrors India's own transformation. The company embodies what's possible when patient capital meets persistent execution, when constraints catalyze innovation, when trust compounds over decades.

But Kaynes also represents something larger—the promise that India can manufacture products requiring highest precision, reliability, and innovation. This isn't about labor arbitrage or cost advantage but genuine capability building. When Indian electronics power moon missions, nuclear reactors, and defense systems, it demonstrates manufacturing prowess that transcends economics.

The next decade will determine whether Kaynes becomes India's TSMC, its Foxconn, or something uniquely Indian that doesn't yet have a comparison. The building blocks are in place—capabilities, capital, customers, and catalytic government support. Execution will determine outcome, but the opportunity is generational.

For investors, Kaynes represents a complex proposition—expensive valuation on near-term metrics but potentially cheap on long-term value creation. For India, Kaynes represents something more—proof that domestic companies can compete globally in humanity's most complex industry. That alone makes this story worth following, regardless of stock price movements.

The workshop in Mysore has come far, but the real journey is just beginning.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube