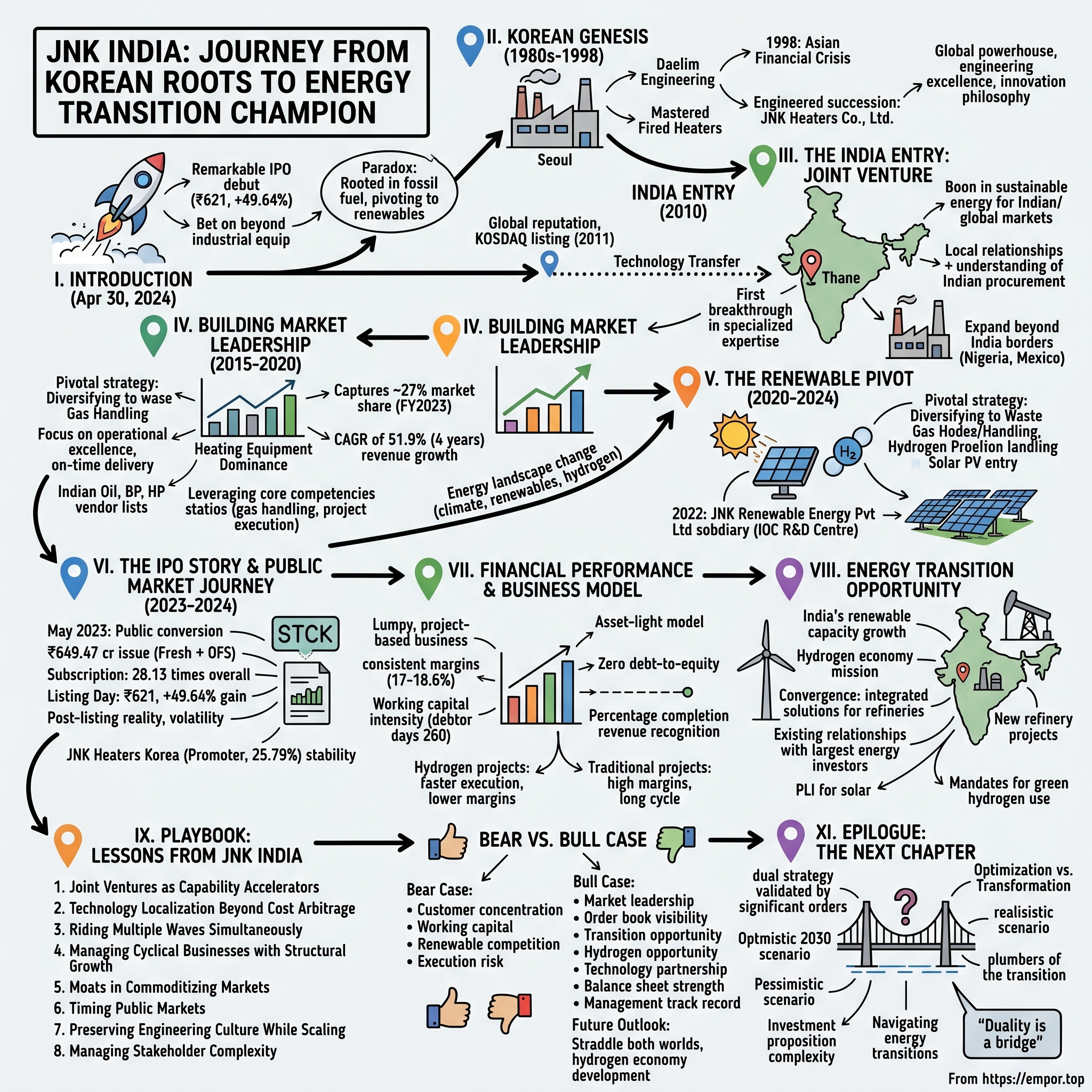

JNK India: From Korean Roots to India's Energy Transition Champion

I. Introduction & Episode Roadmap

Picture the sprawling refineries dotting India's coastline—massive steel towers reaching skyward, miles of intricate piping, and at their heart, the critical equipment that transforms crude oil into the fuels powering a nation. Among the maze of machinery, process fired heaters stand as the workhorses, operating at temperatures exceeding 1,000°C, cracking hydrocarbons into usable products. Without them, modern refineries simply cannot function.

On April 30, 2024, when JNK India's shares hit the National Stock Exchange, they opened at ₹621—a stunning 49.64% above the issue price of ₹415. For a company that most retail investors had never heard of, this was a remarkable debut. The market was betting on something bigger than just another industrial equipment manufacturer.

JNK India represents a fascinating paradox in India's capital markets: a company deeply rooted in the fossil fuel ecosystem yet pivoting aggressively toward renewable energy. With approximately 27% market share in the Indian Heating Equipment market as of Fiscal 2023, they've quietly become indispensable to India's energy infrastructure. But the real story isn't just about market dominance—it's about transformation.

How does a 2010 joint venture, born from Korean engineering excellence, become the bridge between India's fossil fuel present and its renewable future? How did a company specializing in equipment for oil refineries position itself at the forefront of India's hydrogen economy? And perhaps most intriguingly, why did the market reward this industrial player with such enthusiasm during its IPO, even as global energy markets grappled with the transition away from fossil fuels?

This is the story of JNK India—a tale that weaves through the corridors of Korean chaebols, the complexities of technology transfer, the intricacies of India's energy landscape, and the promise of a hydrogen-powered future. It's a narrative about timing, transformation, and the delicate balance between serving today's energy needs while building tomorrow's infrastructure.

II. The Korean Genesis: Daelim to JNK Heaters (1980s-1998)

The Seoul skyline of the early 1980s told the story of South Korea's economic miracle—construction cranes dotted the horizon, new petrochemical complexes rose along the coast, and Korean engineering companies were beginning to flex their muscles on the global stage. Among them was Daelim Engineering Co., Ltd., one of Korea's leading EPC contractors, which made a strategic decision that would ripple across continents: entering the fired heaters and furnaces industry.

This wasn't just another business expansion. Process fired heaters represented the confluence of metallurgy, thermodynamics, and chemical engineering—disciplines where Korean engineers were rapidly closing the gap with their Western counterparts. Daelim's engineers didn't just want to manufacture equipment; they wanted to master the science behind it. They studied heat transfer coefficients, developed proprietary burner designs, and optimized thermal efficiency in ways that caught the attention of global refineries.

By the mid-1990s, Daelim's fired heater division had become a crown jewel, winning contracts not just in Korea but across Asia and the Middle East. The division's engineers had developed something special—a deep understanding of how to design heaters that could withstand extreme conditions while maintaining optimal efficiency. They weren't just building equipment; they were solving complex engineering puzzles that directly impacted refinery economics.

Then came 1998—a year that would transform Korea's corporate landscape. The Asian Financial Crisis had forced Korean conglomerates to restructure, spinning off non-core businesses. But for Daelim's fired heater division, this crisis became an opportunity. The furnace engineers saw their chance for independence and established JNK Heaters Co., Ltd., taking with them all the accumulated experience and technology from their years at Daelim.

This wasn't a hostile breakaway—it was an engineered succession. The newly independent JNK Heaters quickly established itself as a global powerhouse in the industry, leveraging the technical expertise inherited from Daelim while embracing the agility of a focused, specialized company. The engineers who had once been employees became entrepreneurs, but their engineering-first DNA remained unchanged.

The technology they possessed was remarkable. Process fired heaters aren't simple furnaces—they're precision instruments that must heat crude oil and other feedstocks to exact temperatures while maintaining uniform heat distribution. Too hot, and you get unwanted coke formation; too cool, and conversion rates plummet. JNK's designs achieved thermal efficiencies exceeding 92%, a figure that translated directly to millions of dollars in energy savings for refineries.

By the early 2000s, JNK Heaters had established a reputation that extended far beyond Korea. Their equipment operated in Saudi Aramco refineries, in Sinopec complexes, and in facilities across Southeast Asia. The company went public on Korea's KOSDAQ market on January 31, 2011, cementing its position as a legitimate player in the global energy equipment market.

What made JNK Heaters special wasn't just their technical prowess—it was their philosophy of continuous innovation. While Western competitors often relied on decades-old designs, JNK's engineers constantly refined their products, incorporating computational fluid dynamics modeling, advanced materials, and digital monitoring systems. They understood that in the refinery business, even a 1% improvement in efficiency could justify millions in capital expenditure.

The Korean DNA of the company—the emphasis on engineering excellence, the long-term thinking, the relationship-based business model—would prove crucial as they looked beyond their home market. India, with its rapidly expanding refinery capacity and ambitious infrastructure plans, beckoned as the next frontier.

III. The India Entry: Joint Venture & Early Years (2010-2015)

Mumbai in 2010 was a city of contrasts—gleaming towers in Bandra-Kurla Complex stood alongside century-old textile mills, while the stock market touched new highs even as infrastructure struggled to keep pace with growth. India's energy sector was at an inflection point: demand was surging, new refineries were being planned, and the government was pushing for massive capacity additions. It was into this dynamic environment that JNK India Limited was incorporated in 2010 in Thane, establishing the Indian presence as "a boon in sustainable energy sources for the Indian and global markets".

The timing was no accident. India's refining capacity was set to expand from 190 million tonnes per annum to over 300 million tonnes by 2020. Every new refinery, every expansion, every modernization project needed process fired heaters. The Jamnagar complex alone—the world's largest refining hub—operated dozens of these critical units. The opportunity was massive, but so was the competition from established Western and Japanese suppliers.

JNK Heaters Korea's decision to enter through a joint venture rather than direct exports or a wholly-owned subsidiary revealed sophisticated thinking. They understood that succeeding in India required more than just technology—it needed local relationships, understanding of Indian procurement processes, and the ability to navigate the complex web of state-owned enterprises that dominated the refining sector.

The early team in Thane was small but ambitious. Korean engineers worked alongside Indian counterparts, transferring not just technology but also the methodical approach to engineering that had made JNK successful in Korea. They set up a modest facility, focusing initially on design and engineering while sourcing fabrication locally. This capital-light approach allowed them to establish credibility without massive upfront investments.

The first breakthrough came from an unexpected source—not one of India's mega-refineries, but a smaller project that needed specialized expertise. JNK India's ability to customize designs for Indian conditions—accounting for monsoons, higher ambient temperatures, and local fuel specifications—set them apart. They weren't just importing Korean designs; they were creating India-specific solutions.

As word spread about their technical capabilities, larger opportunities emerged. Indian Oil Corporation, Bharat Petroleum, and Hindustan Petroleum—the three state-owned giants that controlled over 60% of India's refining capacity—began including JNK India in their vendor lists. Each successful project became a reference for the next, creating a virtuous cycle of credibility and growth.

By 2015, the company had completed projects across India's industrial heartland—from refineries in Gujarat to fertilizer plants in Andhra Pradesh, from petrochemical complexes in Maharashtra to expansion projects in Assam. They weren't just executing projects; they were building a reputation for reliability in an industry where delays and cost overruns were endemic.

The technology transfer from Korea proved invaluable. JNK India's engineers could tap into decades of Korean experience, accessing design databases, simulation software, and troubleshooting expertise that would have taken years to develop independently. When a heater at a Paradip refinery faced operational issues, Korean experts provided remote support within hours, demonstrating the value of the partnership.

But the relationship wasn't one-sided. Indian engineers brought their own innovations—cost-engineering techniques that reduced capital costs without compromising quality, sourcing strategies that leveraged India's competitive fabrication industry, and project management approaches suited to Indian conditions. The synthesis of Korean technology and Indian execution created a unique competitive advantage.

The early years also saw JNK India expand beyond India's borders. Projects in Nigeria and Mexico demonstrated that the Indian entity wasn't just a local subsidiary but a legitimate international player. These international projects, often executed in collaboration with JNK Korea, enhanced the company's credentials and opened new revenue streams.

By 2015, JNK India had evolved from a startup joint venture to an established player in India's energy equipment sector. The foundation was set, relationships were built, and the technology transfer was complete. The company was ready for its next phase—scaling up to capture market leadership.

IV. Building Market Leadership: The Heating Equipment Dominance (2015-2020)

The conference room at Indian Oil's headquarters in New Delhi had seen many vendor presentations, but the JNK India team's 2016 pitch was different. They weren't just selling equipment; they were presenting a vision of partnership. Their proposal for the Paradip refinery expansion included not just supply but complete lifecycle support—design optimization, remote monitoring, and performance guarantees that exceeded industry standards. It was a bold move that would define their trajectory toward market leadership.

Understanding JNK India's rise requires appreciating the complexity of their market. The demand for heating equipment from Indian refineries, petrochemicals, and fertilizer segments was estimated at approximately ₹45,000 million annually between Fiscal 2024 and 2029. But this wasn't a commodity market—each heater was custom-designed, with specifications varying based on feedstock, capacity, and desired output. Success required deep technical expertise, flawless execution, and the ability to manage complex, multi-year projects.

The typical refinery operates 10-20 process fired heaters, each a critical component in units like Crude Distillation (CDU), Vacuum Distillation (VDU), delayed coker units, and catalytic reforming units. A single heater failure could shut down an entire refinery, costing millions in lost production. This criticality meant that refineries chose vendors based on track record, not just price—a dynamic that favored established players like JNK India.

By Fiscal 2023, JNK India had captured approximately 27% market share in the Indian Heating Equipment market, a remarkable achievement in a sector dominated by international giants like Lummus Technology and domestic conglomerates like Larsen & Toubro. How did they achieve this? The answer lay in their unique positioning—global technology with local execution.

The partnership model with JNK Heaters Korea proved crucial. While competitors either relied entirely on imported technology (expensive and slow) or domestic capabilities (limited in scope), JNK India offered the best of both worlds. Complex design work could be done in Korea, leveraging advanced simulation tools and decades of experience, while fabrication and assembly happened in India, taking advantage of cost competitiveness.

2019 marked a significant milestone when JNK India won its first major international order from Nigeria for erection work—not through the Korean parent but independently. This demonstrated that the Indian entity had matured beyond being just a local subsidiary. The Nigerian project, executed in challenging conditions with local content requirements, showcased JNK India's ability to operate in difficult markets.

The company's approach to capability building was methodical. Rather than trying to do everything, they focused on mastering each element of the value chain sequentially. First came design and engineering capabilities, then procurement and vendor management, followed by fabrication oversight and quality control, and finally, site execution and commissioning. By 2020, they could handle complex turnkey projects independently.

What truly set JNK India apart was their focus on operational excellence. In an industry plagued by delays and cost overruns, they developed a reputation for on-time, on-budget delivery. Their project management systems, borrowed from Korean practices but adapted for Indian conditions, included detailed risk assessments, milestone-based monitoring, and proactive communication with clients. When COVID-19 disrupted supply chains in 2020, JNK India's robust systems allowed them to minimize delays while competitors struggled.

The financial performance during this period reflected their operational success. Revenue grew at a CAGR of 51.9% over four years, but more importantly, margins remained healthy despite intense competition. This wasn't growth at any cost—it was profitable, sustainable expansion built on operational excellence and customer trust.

The relationship with the Korean parent evolved during this period from dependence to collaboration. While JNK Korea remained a crucial source of technology and expertise, the Indian entity increasingly contributed its own innovations. Cost-optimization techniques developed in India were adopted by Korean projects, while Indian engineers participated in global design teams, bringing perspectives from one of the world's most challenging operating environments.

By 2020, JNK India had established itself as the go-to partner for critical heating equipment in India. They had the technology, the track record, and the relationships. But the energy landscape was changing. Climate concerns, renewable energy mandates, and the promise of hydrogen were reshaping the industry. The company that had built its success on fossil fuel infrastructure needed to evolve.

V. The Renewable Pivot: Hydrogen & Solar (2020-2024)

The boardroom discussion in early 2021 was intense. On one side were voices advocating for doubling down on the core heating equipment business—after all, India's refining capacity was still growing. On the other were those who saw the writing on the wall—the energy transition wasn't a distant threat but an immediate opportunity. The decision they made would fundamentally reshape JNK India's trajectory.

The pivot to renewable energy wasn't born from environmental idealism but from pragmatic business logic. JNK India's leadership recognized that their core competencies—high-temperature process engineering, gas handling systems, and complex project execution—were directly transferable to the emerging hydrogen economy. The company began diversifying into Waste Gas Handling (Flares and Incinerators) and Renewable Energy Systems (Hydrogen Production/Distribution Systems and Solar PV EPC).

In 2022, JNK India took a decisive step by incorporating JNK Renewable Energy Private Limited as a subsidiary. This wasn't just a rebranding exercise—it represented a fundamental shift in capital allocation and strategic focus. The subsidiary would focus exclusively on renewable energy projects, allowing the parent to maintain its traditional business while aggressively pursuing new opportunities.

The hydrogen opportunity was particularly compelling. India's National Hydrogen Mission, announced in 2021, targeted 5 million tonnes of green hydrogen production by 2030. Every kilogram of hydrogen required specialized production equipment, storage systems, and distribution infrastructure—exactly the kind of complex engineering challenges JNK India excelled at solving.

The breakthrough moment came in 2024 when JNK India commissioned a hydrogen refueling station at Indian Oil Corporation's R&D Centre in Faridabad. This wasn't just another project—it was a proof of concept for India's hydrogen future. The facility could produce, store, and dispense hydrogen for fuel cell vehicles, demonstrating JNK India's ability to deliver complete hydrogen solutions.

The technical challenges were immense. Hydrogen, the smallest molecule in the universe, requires specialized materials and designs to prevent leakage. Storage pressures exceeding 700 bar demanded exceptional engineering precision. JNK India's engineers, working closely with their Korean counterparts who had already delivered similar projects in Korea, developed India-specific solutions that accounted for local conditions and cost constraints.

But hydrogen was just one piece of the renewable puzzle. The company also entered the solar EPC (Engineering, Procurement, and Construction) space, leveraging their project execution capabilities in a rapidly growing market. While solar panels were commoditized, the ability to deliver complete solar plants—including inverters, transformers, and grid integration—on schedule remained a differentiator.

The synergies between their traditional and renewable businesses were striking. Many of their refinery clients were also investing in renewable energy to meet carbon reduction targets. JNK India could offer integrated solutions—helping refineries reduce emissions through improved heating equipment efficiency while also building their renewable energy infrastructure. This one-stop-shop approach resonated with clients looking to simplify vendor management.

India's renewable energy sector was experiencing unprecedented growth, adding 24.5 GW of solar capacity and 3.4 GW of wind capacity in 2024 alone, pushing total non-fossil fuel capacity to 217.62 GW and targeting 500 GW by 2030. JNK India positioned itself to capture a share of this massive opportunity, particularly in the industrial and refinery segments where they had established relationships.

The financial implications of this pivot were significant. While renewable energy projects had lower margins than specialized heating equipment, they offered more predictable revenue streams and access to a rapidly growing market. The company's order book began reflecting this shift, with an increasing share coming from renewable energy projects.

Technology transfer from JNK Korea again proved crucial. The Korean parent was actively developing hydrogen refueling stations and had partnered with international technology providers for biogas refining and hydrogen production. This global expertise, combined with JNK India's local execution capabilities, created a powerful combination for the Indian market.

The market began recognizing this transformation. Investors saw JNK India not just as a traditional industrial company but as a play on India's energy transition. The company's narrative shifted from "critical equipment supplier to refineries" to "enabler of India's energy transition"—a story that would prove compelling during their IPO journey.

By early 2024, JNK India had successfully established credibility in the renewable space while maintaining leadership in traditional heating equipment. They weren't abandoning their core business but expanding their definition of what that core could be. The stage was set for their next big move—accessing public markets to fund this ambitious transformation.

VI. The IPO Story & Public Market Journey (2023-2024)

The Partners at IIFL Capital Services had seen many pitches, but JNK India's presentation in late 2022 stood out. Here was a profitable, market-leading company with a compelling growth story, riding two megatrends—India's refining capacity expansion and the renewable energy transition. The bankers saw what the company's management had been building toward: a public listing that would provide growth capital while allowing early investors to partially exit.

On May 26, 2023, JNK India converted from a private to public limited company, the first formal step toward an IPO. This wasn't just a regulatory requirement—it signaled a transformation in governance, transparency, and ambition. The company that had operated quietly in the B2B space would now face public scrutiny.

The IPO structure revealed careful thinking about stakeholder interests. The ₹649.47 crore issue combined a fresh issue of ₹300 crores with an offer for sale of ₹349.47 crores. The fresh capital would fund working capital requirements and growth investments, while the OFS allowed early investors to realize returns without completely exiting. JNK Heaters Korea, the corporate promoter, would retain 25.79% post-IPO, ensuring continued technology partnership.

Pricing the IPO required delicate balance. At ₹415 per share, the company was valued at a P/E multiple of 43x—aggressive but not unreasonable given the growth trajectory. The comparison with listed peers was favorable: Thermax traded at 113x P/E while BHEL commanded 186x, though these weren't perfect comparables given JNK India's unique positioning.

The roadshow revealed strong institutional interest. Fund managers were intrigued by the dual theme—a play on both India's immediate energy needs and its long-term transition. The order book visibility, with ₹761 crores of unexecuted orders as of February 2024, provided revenue visibility that investors craved. The debt-free balance sheet eliminated concerns about financial leverage.

April 23, 2024—the IPO opened to remarkable response. By closing on April 25, the issue was subscribed 28.13 times overall, with the QIB portion seeing 75.72 times subscription and NII category at 23.26 times. The institutional demand validated the company's narrative, while retail participation, though lower at 4.11 times, showed growing awareness.

What drove this enthusiasm? Several factors converged. First, the India infrastructure story was compelling—the government's massive capital expenditure program meant continued demand for industrial equipment. Second, the renewable energy angle resonated with ESG-focused funds. Third, the Korean parentage provided comfort on technology and governance. Finally, the company's track record of profitable growth in a sector known for working capital challenges stood out.

Listing day—April 30, 2024—delivered drama. The stock opened at ₹621, a stunning 49.64% above the issue price, giving investors who received allotment returns of ₹7,416 per lot. The grey market had indicated premiums, but the actual listing gain exceeded expectations. Trading volumes were heavy as those who received allotment booked profits while others, who missed the IPO, scrambled to buy.

But public markets are unforgiving, and the initial euphoria soon gave way to reality. The stock's journey post-listing reflected broader market volatility and sector-specific concerns. By late 2024, the stock had corrected significantly from its listing day highs, trading closer to its IPO price. The correction wasn't company-specific—the entire capital goods sector faced headwinds from rising interest rates and concerns about order execution.

The use of IPO proceeds followed the stated plan. ₹263 crores went toward working capital funding, critical given the company's growing order book, while the remainder was allocated to general corporate purposes. The company also used the enhanced profile from listing to strengthen relationships with customers and vendors—being a listed entity carried weight in India's corporate landscape.

JNK Heaters Korea's role as anchor shareholder provided stability. Unlike private equity investors who might exit quickly, the Korean parent's strategic interest ensured continued technology support and prevented excessive stock volatility. Their 25.79% stake was large enough to influence decisions but not so large as to concern minority shareholders about governance.

The quarterly results post-IPO showed both promise and challenges. Q2 FY2025 saw revenues rise 7.14% to ₹103.83 crores, but net profit declined 36.37% to ₹7.75 crores, reflecting margin pressure from competitive bidding and execution challenges. The market's reaction was swift—the stock fell sharply, reminding investors that the transition from private to public meant quarterly scrutiny.

Management's communication with investors evolved rapidly. From being a company that rarely spoke publicly, they now conducted quarterly earnings calls, investor meetings, and analyst interactions. The learning curve was steep—explaining complex engineering projects and long-term contracts to investors focused on quarterly numbers required new skills.

The IPO had achieved its primary objectives—providing growth capital, enhancing visibility, and creating a currency for future acquisitions. But it also brought new challenges—market volatility, quarterly pressure, and the need to balance long-term strategy with short-term expectations. The public market journey had just begun.

VII. Financial Performance & Business Model

The numbers tell a story of remarkable growth, but understanding JNK India's financials requires peeling back layers to reveal the underlying business dynamics. Between March 31, 2022 and March 31, 2023, revenue increased by 38.5% while profit after tax rose by 28.84%—impressive headline numbers that masked the complexity of executing multi-year projects in a volatile environment.

The growth trajectory from 2021 to 2023 was nothing short of spectacular. Revenue exploded at a CAGR of 71.97%, EBITDA grew at 68.09%, and profit after tax surged at 67.75%. These weren't the steady, predictable numbers of a utility company—they reflected the lumpy, project-based nature of the EPC business where a single large order could transform a fiscal year.

FY2024 brought continued momentum with revenues reaching ₹477 crores, though FY2025 showed more modest growth with revenues at ₹495 crores. The moderation wasn't concerning—it reflected the natural rhythm of project execution where revenue recognition followed percentage completion rather than order booking.

Operating margins told a story of consistency amid growth. Across four fiscal years leading to FY2024, margins ranged between 17% and 18.6%—remarkable stability for an EPC business where competitive bidding often erodes profitability. This margin resilience reflected JNK India's differentiation—they weren't competing purely on price but on technical capability and execution reliability.

The working capital intensity of the business was its Achilles' heel. With debtor days stretching to 260 days, cash conversion was a constant challenge. This wasn't inefficiency—it reflected the reality of working with large refineries and government entities where payment cycles were notoriously long. The IPO proceeds targeting working capital weren't for expansion but for survival in a business where you needed deep pockets to play.

Customer concentration presented both opportunity and risk. JNK Global, the Korean promoter, contributed 54% of FY2023 revenues, down from 74% in FY2022. This declining dependence was strategic—diversifying the customer base reduced risk—but the relationship remained crucial. JNK Global often brought international projects that JNK India executed, leveraging cost advantages while maintaining quality standards.

The order book dynamics revealed the lumpy nature of the business. With ₹761 crores of unexecuted orders as of February 2024, the company had visibility for roughly 1.5-2 years of revenue. But these weren't uniform orders—a single large project could represent 30-40% of the book, making execution risk concentrated.

The business model itself was elegantly simple yet operationally complex. JNK India would bid for projects, typically through competitive tendering, offering design, procurement, fabrication, and commissioning services. Contracts were usually fixed-price with milestone-based payments, putting execution risk squarely on JNK India's shoulders. Cost overruns, delays, or technical issues directly impacted profitability.

What made the model work was the blend of Korean technology and Indian execution. Design work, requiring expensive software and specialized expertise, could be done in Korea or by the growing Indian design team. Procurement leveraged global supply chains, with critical components imported and standard items sourced locally. Fabrication happened through a network of approved vendors, with JNK India maintaining strict quality control. Site execution—often the most challenging phase—relied on experienced project managers who understood local conditions.

The capital efficiency of the model was noteworthy. Unlike manufacturing businesses requiring massive fixed assets, JNK India operated with minimal capital investment. The debt-to-equity ratio stood at virtually zero, unusual for an infrastructure-related business. This asset-light approach meant that growth didn't require proportional capital investment—they could scale by taking larger projects rather than building factories.

Revenue recognition followed percentage completion methodology, creating timing differences between order booking, execution, and cash collection. A project won in Year 1 might see revenue spread over Years 2-4, with cash collection extending into Year 5. This lag meant that reported financials often reflected decisions made years earlier, making forward-looking metrics like order book more relevant than historical revenues.

The transition to renewable energy began impacting financials by FY2024. While margins in solar EPC and hydrogen projects were lower than traditional heating equipment, they offered faster execution and better working capital cycles. The strategic trade-off was clear—accept lower margins for better cash generation and exposure to a rapidly growing market.

Net profit evolution showed impressive growth—from ₹165 million in FY2021 to ₹360 million in FY2022, ₹466 million in FY2023, and ₹626 million in FY2024. But the quarterly volatility post-listing reminded investors that smooth annual numbers masked significant intra-year variation based on project milestones and execution challenges.

The financial model's sustainability depended on three factors: continued order inflow to maintain the revenue pipeline, successful execution to protect margins, and working capital management to ensure liquidity. The IPO addressed the third concern, providing a buffer that allowed the company to bid for larger projects without stretching balance sheet limits.

VIII. The Energy Transition Opportunity

Standing at the Jamnagar refinery complex—a sprawling 1,400-acre site processing 1.24 million barrels of crude daily—one appreciates the sheer scale of India's fossil fuel infrastructure. Yet just kilometers away, massive solar farms stretch across Gujarat's semi-arid landscape, their panels tracking the sun's arc. This juxtaposition captures India's energy paradox: simultaneously expanding fossil fuel capacity while aggressively building renewable infrastructure. For JNK India, this isn't a contradiction—it's the opportunity of a lifetime.

India's renewable energy statistics are staggering: 217.62 GW of non-fossil fuel capacity as of January 2025, targeting 500 GW by 2030. This isn't just government ambition—it's backed by concrete action. In 2024 alone, India added 24.5 GW of solar capacity (a twofold increase from 2023) and 3.4 GW of wind capacity, with solar now accounting for 47% of total renewable capacity.

The hydrogen opportunity is particularly compelling for JNK India. India's National Green Hydrogen Mission targets 5 million tonnes of annual production by 2030, requiring thousands of electrolyzers, reformers, and distribution systems—precisely the equipment JNK India specializes in. Unlike solar panels or wind turbines, which have become commoditized, hydrogen infrastructure requires complex engineering and customization—barriers to entry that favor established players.

The traditional heating equipment market isn't disappearing either. Demand is estimated at ₹270,890 million between FY2024-2029, approximately ₹45,000 million annually. India's refining capacity continues expanding, with new refineries planned in Rajasthan, Maharashtra, and Andhra Pradesh. Each facility needs 10-20 process fired heaters, creating steady demand for JNK India's core products.

The intersection of traditional and renewable energy creates unique opportunities. Modern refineries are investing in hydrogen production units to reduce sulfur content in fuels—these units require both traditional heating equipment and hydrogen handling systems. JNK India's ability to provide integrated solutions positions them uniquely in this converging market.

Technology transfer from Korea provides crucial advantages. JNK Global is actively developing on-site hydrogen refueling stations through natural gas and LPG reforming, working with public and private enterprises, and has partnered with international providers for biogas refining technology. This global expertise, localized for Indian conditions, gives JNK India a significant edge over purely domestic competitors.

The customer base evolution reflects this transition opportunity. Traditional clients like Indian Oil, Bharat Petroleum, and Reliance Industries are also India's largest investors in renewable energy. Indian Oil alone plans to invest ₹2 trillion by 2030, with substantial allocation to green hydrogen and renewable energy. These existing relationships provide JNK India with inside tracks to emerging opportunities.

Government policy creates powerful tailwinds. Production-linked incentives for solar manufacturing, mandates for green hydrogen use in refineries and fertilizer plants, and renewable purchase obligations for industries all drive demand for JNK India's products and services. The company's ability to navigate government tenders and comply with local content requirements—honed over years of working with PSUs—becomes a competitive advantage.

The global context amplifies the opportunity. As developed nations implement carbon border adjustments, Indian manufacturers must reduce emissions to maintain export competitiveness. This drives investment in energy efficiency (traditional JNK India strength) and renewable energy (emerging capability). The company sits at the intersection of both needs.

Competition in the renewable space is intensifying but fragmented. While numerous players have entered solar EPC, few combine engineering expertise, project execution capability, and balance sheet strength. In hydrogen, the technical barriers are even higher—designing systems that handle hydrogen's unique properties requires specialized knowledge that new entrants lack.

JNK India's approach to this opportunity is pragmatic rather than revolutionary. They're not abandoning their core business to chase renewable dreams. Instead, they're leveraging existing capabilities—high-temperature engineering, gas handling expertise, project management skills—in adjacent markets. A hydrogen reformer isn't fundamentally different from a process fired heater; both require similar engineering principles and execution capabilities.

The financial implications are significant. While renewable projects might have lower margins than specialized heating equipment, they offer larger volumes and faster execution cycles. A typical fired heater project might take 2-3 years from order to completion; a solar EPC project might finish in 12-18 months. This faster velocity means better capital efficiency even at lower margins.

Risk management in this transition is crucial. JNK India isn't betting everything on hydrogen taking off immediately or solar continuing its exponential growth. By maintaining leadership in traditional heating equipment while building renewable capabilities, they're hedged against multiple scenarios. If hydrogen adoption is slower than expected, traditional business continues. If refineries stop expanding, renewable opportunities compensate.

The timeline for this transition aligns with JNK India's capabilities. The next five years will see continued refinery investments alongside renewable scaling—perfect for a company straddling both worlds. By 2030, as India approaches its renewable targets, JNK India aims to have established leadership in hydrogen infrastructure while maintaining its heating equipment franchise.

IX. Playbook: Lessons from JNK India

The JNK India story offers a masterclass in navigating complex markets, technology transfer, and strategic pivots. Their journey from joint venture to market leader to public company reveals patterns that transcend industry boundaries—lessons for any company operating in India's infrastructure space or managing technological transitions.

Lesson 1: Joint Ventures as Capability Accelerators

The conventional wisdom suggests joint ventures often fail due to cultural misalignment and conflicting objectives. JNK India's experience proves otherwise when structured correctly. The key was clarity of roles—Korea provided technology and design expertise; India handled execution and market access. Neither party tried to dominate areas outside their competence. This wasn't just equity sharing but genuine capability complementarity.

The gradual evolution from dependence to interdependence to independence shows sophisticated relationship management. Early years saw heavy reliance on Korean technical support; middle years witnessed collaborative problem-solving; recent years show the Indian entity contributing innovations back to the parent. This progression wasn't accidental but carefully managed through personnel exchanges, joint training programs, and shared R&D initiatives.

Lesson 2: Technology Localization Beyond Cost Arbitrage

Most technology transfers focus on cost reduction—taking expensive Western or Japanese technology and producing it cheaper in India. JNK India went deeper, adapting Korean designs for Indian conditions. Heaters designed for Korean winters needed modification for Indian summers. Equipment built for Korean infrastructure quality needed ruggedization for Indian conditions. This wasn't just transplanting technology but genuine localization.

The bidirectional flow of innovation proved crucial. Indian cost-engineering techniques, developed from necessity in a price-sensitive market, found applications in Korean projects. Indian project management approaches, evolved to handle infrastructure limitations and regulatory complexity, improved execution globally. Technology transfer became technology exchange.

Lesson 3: Riding Multiple Waves Simultaneously

JNK India's growth coincided with three distinct waves—India's infrastructure boom (2010-2015), refinery modernization (2015-2020), and energy transition (2020-present). Lesser companies might have missed transitions, stuck in declining markets. JNK India anticipated each shift, positioning ahead of the curve rather than reacting to change.

This wave-riding wasn't luck but strategic planning. While executing refinery projects, they noticed clients' growing environmental concerns. While building traditional equipment, they observed global hydrogen developments. The renewable pivot wasn't a sudden revelation but gradual recognition of shifting customer needs. They didn't abandon the current wave before catching the next one—they surfed multiple waves simultaneously.

Lesson 4: Managing Cyclical Businesses with Structural Growth

The EPC business is notoriously cyclical—boom periods of excessive orders followed by bust phases of brutal competition. JNK India smoothed these cycles through diversification across end markets (refineries, petrochemicals, fertilizers), geographies (domestic and international), and now energy types (fossil and renewable). When refinery investments slowed, petrochemical projects compensated. When domestic orders declined, international opportunities emerged.

Order book management became a strategic tool. Rather than chasing every opportunity during boom periods, they maintained selective bidding, preserving margins over volumes. During downturns, strong relationships and technical differentiation allowed them to win projects even at competitive pricing. The discipline to walk away from bad deals, even when order books were thin, preserved long-term profitability.

Lesson 5: Building Moats in Commoditizing Markets

Process fired heaters could have become commoditized—standardized designs, price-based competition, declining margins. JNK India avoided this trap through continuous innovation and service expansion. They didn't just supply equipment but offered complete solutions—design optimization, lifecycle support, performance guarantees. When Chinese competitors offered cheaper heaters, JNK India sold reliability and total cost of ownership.

The expansion into renewable energy follows similar logic. Rather than entering commoditized solar panel installation, they focus on complex integration—combining solar with hydrogen production, integrating renewable energy with refinery operations. The moat isn't in any single product but in the ability to solve complex, multi-disciplinary problems.

Lesson 6: Timing Public Markets

The IPO timing revealed sophisticated understanding of market dynamics. They went public when they had proven profitability (addressing quality concerns), strong order books (providing visibility), and a renewable energy story (capturing growth narratives). Waiting longer might have meant better financials but missing the renewable energy excitement. Going earlier would have meant unproven execution in new areas.

The structure—significant fresh issue for growth capital while maintaining promoter control—balanced stakeholder interests. They raised enough to fund ambitions without excessive dilution. The Korean parent's continued stake provided technical comfort while public float ensured liquidity. Post-IPO volatility was managed through consistent communication and delivery against guidance.

Lesson 7: Preserving Engineering Culture While Scaling

Many engineering companies lose their technical edge while scaling, becoming project managers rather than problem solvers. JNK India maintained engineering focus through specific organizational choices. Senior management included engineers, not just commercial executives. Investment in R&D and training continued despite margin pressure. Technical capability, not just commercial success, determined career progression.

The balance between standardization and customization proved crucial. While developing standard modules for efficiency, they maintained flexibility for client-specific requirements. This mass customization approach—standardized components assembled in unique configurations—delivered both efficiency and differentiation.

Lesson 8: Managing Stakeholder Complexity

JNK India navigated remarkable stakeholder complexity—Korean shareholders expecting returns, Indian regulators demanding compliance, PSU customers following elaborate procedures, private clients wanting flexibility, and post-IPO, public market investors seeking quarterly performance. Each stakeholder had different expectations, timelines, and success metrics.

The key was transparent communication tailored to each audience. Korean partners received detailed technical updates; Indian regulators got compliance reports; customers saw project progress; investors heard strategic vision. This multi-stakeholder management, exhausting but essential, prevented any single group from derailing the broader agenda.

X. Bear vs. Bull Case & Future Outlook

The investment case for JNK India splits sharply between pessimists who see concentrated risks and optimists who envision transformation opportunities. Both perspectives have merit, and understanding the tension between them is crucial for evaluating the company's future.

Bear Case: The Skeptic's View

The bears start with customer concentration. Despite improvement, JNK Global still contributed 54% of FY2023 revenues. This isn't just customer concentration—it's reliance on a related party whose interests might not always align with minority shareholders. If JNK Global redirects orders to other subsidiaries or squeezes margins, JNK India has limited recourse.

Working capital intensity remains problematic. With 260 debtor days, the company essentially provides free financing to customers. In a rising rate environment, this becomes expensive even if funded through internal accruals. The IPO provided temporary relief, but structural working capital needs persist. Growth requires proportional working capital investment, limiting free cash flow generation.

Competition in renewable energy is intensifying rapidly. While JNK India brings engineering expertise, pure renewable energy players bring specialized knowledge, established relationships, and aggressive pricing. The solar EPC space is already commoditized with wafer-thin margins. Hydrogen, while promising, remains nascent with uncertain adoption timelines and evolving technology standards.

Execution risks in new business lines can't be ignored. Building fired heaters for refineries is fundamentally different from executing solar projects or hydrogen infrastructure. Technical expertise doesn't automatically translate across domains. Early mistakes in renewable projects could damage reputation and relationships built over decades in traditional business.

The stock performance post-IPO raises red flags. After the initial euphoria, reality set in—the stock corrected significantly, trading near IPO prices despite broader market strength. This suggests institutional investors, after deeper diligence, found the story less compelling than initial narratives suggested. The sharp profit decline in Q2 FY2025 validates concerns about margin sustainability.

The traditional business faces structural headwinds. Global refining capacity additions are slowing as demand growth moderates and environmental concerns intensify. Developed nations are actively reducing refining capacity. While India continues investing, the runway isn't infinite. Peak refining capacity might arrive sooner than expected, leaving JNK India exposed if renewable pivots don't compensate quickly enough.

Bull Case: The Believer's Thesis

Bulls counter with market leadership in a critical sector. 27% market share in Indian heating equipment isn't just a number—it represents deep relationships, proven expertise, and competitive moats that take decades to build. This isn't a commodity business but specialized engineering where track record matters more than price.

The order book provides concrete visibility. ₹761 crores of unexecuted orders offers 1.5-2 years of revenue visibility—rare predictability in an otherwise volatile sector. This isn't speculative demand but confirmed projects from creditworthy customers. The pipeline beyond current orders looks equally robust given India's infrastructure investments.

India's energy transition is a multi-decade opportunity with the country targeting 500 GW of renewable capacity by 2030 from 217.62 GW currently. JNK India isn't late to this party—they're arriving just as the market moves from pilots to scale. Their engineering expertise and execution capability become more valuable as projects grow in size and complexity.

The hydrogen opportunity is particularly compelling. Unlike solar or wind, hydrogen infrastructure requires specialized engineering expertise that new entrants can't easily replicate. JNK India's experience with high-pressure systems, gas handling, and process engineering provides natural advantages. Early projects like the IOC Faridabad facility establish credentials that matter in a reference-driven market.

Technology partnership with Korea remains a significant advantage. JNK Global's ongoing development of hydrogen refueling stations and partnerships with international technology providers ensures JNK India accesses cutting-edge technology without bearing full development costs. This isn't static technology transfer but dynamic capability building.

The balance sheet strength enables strategic flexibility. Near-zero debt means the company can invest in new opportunities, weather downturns, or make acquisitions without financial stress. In a capital-intensive industry, this financial strength is a competitive advantage, allowing aggressive bidding when competitors face balance sheet constraints.

Management's track record inspires confidence. Growing from startup to market leader in a decade demonstrates execution capability. Successfully managing the Korean partnership shows relationship skills. The measured approach to renewable energy—building capabilities gradually rather than betting everything—reflects strategic maturity.

Future Outlook: The Next Five Years

The most likely scenario sees JNK India successfully straddling both worlds—maintaining traditional business while scaling renewable operations. By 2030, revenue mix might be 60% traditional, 40% renewable, with margins converging as renewable operations achieve scale efficiencies.

The hydrogen economy will likely develop slower than government targets suggest but faster than skeptics expect. JNK India's early positioning means they'll capture a disproportionate share of initial projects, establishing references crucial for future growth. Success in hydrogen could transform the company from equipment supplier to infrastructure player.

International expansion presents untapped opportunity. The capabilities developed in India—cost-effective engineering, execution in challenging environments, managing infrastructure limitations—have global applications. African and Southeast Asian markets, facing similar infrastructure challenges, could become significant revenue sources.

The relationship with JNK Global will evolve toward greater independence. As the Indian entity's capabilities mature, reliance on the parent will decrease. This might initially reduce revenues but improve margins and strategic flexibility. The eventual end-state might see JNK India as an equal partner rather than subsidiary.

Stock market performance will likely remain volatile, reflecting the company's transition phase. Quarters with strong project completions will see sharp rallies; execution delays will trigger corrections. Long-term investors who understand the structural story might find opportunities in this volatility.

The key metrics to watch aren't quarterly earnings but strategic indicators: order book composition (traditional vs. renewable), customer diversification progress, hydrogen project wins, and working capital efficiency. These leading indicators will signal whether the transformation succeeds before financial results confirm it.

XI. Epilogue: The Next Chapter

The August 2025 announcement was brief but significant: JNK India received significant orders from JNK Global (Korea), with delivery by December 2027. For a company navigating the delicate balance between serving today's energy infrastructure and building tomorrow's, this order represented validation of their dual strategy—maintaining core competencies while pursuing transformation.

Standing at this inflection point, JNK India embodies the complexities of India's energy transition. They're simultaneously essential to maintaining current fossil fuel infrastructure and instrumental in building renewable alternatives. This isn't contradiction but pragmatism—recognizing that transitions take decades, not years, and success requires serving both present needs and future aspirations.

What does success look like in 2030? The optimistic scenario sees JNK India as India's leading hydrogen infrastructure company, having leveraged early-mover advantage and engineering expertise to dominate an emerging sector. Revenue might reach ₹2,000 crores, with balanced contribution from traditional and renewable segments. The company could be the partner of choice for refineries transforming into energy companies, providing integrated solutions spanning fossil and renewable energy.

The realistic scenario is more modest but still compelling. JNK India maintains market leadership in heating equipment while establishing credible presence in renewable energy. Revenue grows to ₹1,200-1,500 crores, margins stabilize around 15%, and working capital efficiency improves gradually. The company remains a solid, if unspectacular, player in India's infrastructure story.

The pessimistic scenario can't be dismissed. Renewable energy transitions often take longer than expected. Hydrogen might remain perpetually "five years away." Traditional refinery investments could dry up faster than anticipated. Competition in renewable energy could erode margins below sustainability. The company might find itself stuck between declining traditional business and unprofitable new ventures.

The key variables that will determine which scenario unfolds are partially within JNK India's control—execution excellence, strategic choices, capital allocation—and partially external—government policy, technology evolution, competitive dynamics. The company's ability to navigate this uncertainty while maintaining operational excellence will determine its trajectory.

For investors, JNK India represents a complex proposition. It's not a pure play on anything—neither traditional infrastructure nor clean energy. This complexity creates both risk and opportunity. Those who understand the nuances, appreciate the transition dynamics, and have patience for multi-year transformations might find value. Those seeking simple narratives and predictable outcomes should look elsewhere.

The broader lesson transcends JNK India. Across India's industrial landscape, companies face similar transitions—serving current needs while preparing for different futures. Success requires balance, patience, and the ability to manage contradictions. JNK India's journey, still unfolding, offers a template for navigating these transitions.

As India accelerates toward its 2030 renewable targets and 2070 net-zero commitment, companies like JNK India will play crucial but often unrecognized roles. They're the plumbers of the energy transition—not glamorous but essential. Their boring reliability and engineering excellence enable the dramatic transformations that capture headlines.

The story that began in Seoul's engineering offices in the 1980s, traveled through technology transfer and joint ventures, achieved market leadership and public listing, now enters its most crucial chapter. The next five years will determine whether JNK India becomes a footnote in India's energy transition or a foundational player in its renewable future.

For a company that has consistently defied simple categorization—Korean yet Indian, traditional yet transforming, industrial yet innovative—perhaps the most fitting conclusion is that their greatest strength lies in embracing complexity rather than simplifying it. In a world demanding binary choices, JNK India's insistence on "and" rather than "or" might be their most valuable asset.

The fired heaters that once defined them will continue operating for decades, maintaining the industrial infrastructure that powers economic growth. Simultaneously, the hydrogen systems and renewable projects they're building today will enable the cleaner future India aspires to achieve. This duality isn't a compromise—it's a bridge, connecting where we are to where we need to be.

That bridge, engineered with precision and built to last, might be JNK India's most enduring contribution to India's energy story.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube