IDFC FIRST Bank: The Audacious Retail Banking Pivot

I. Introduction & Episode Setup

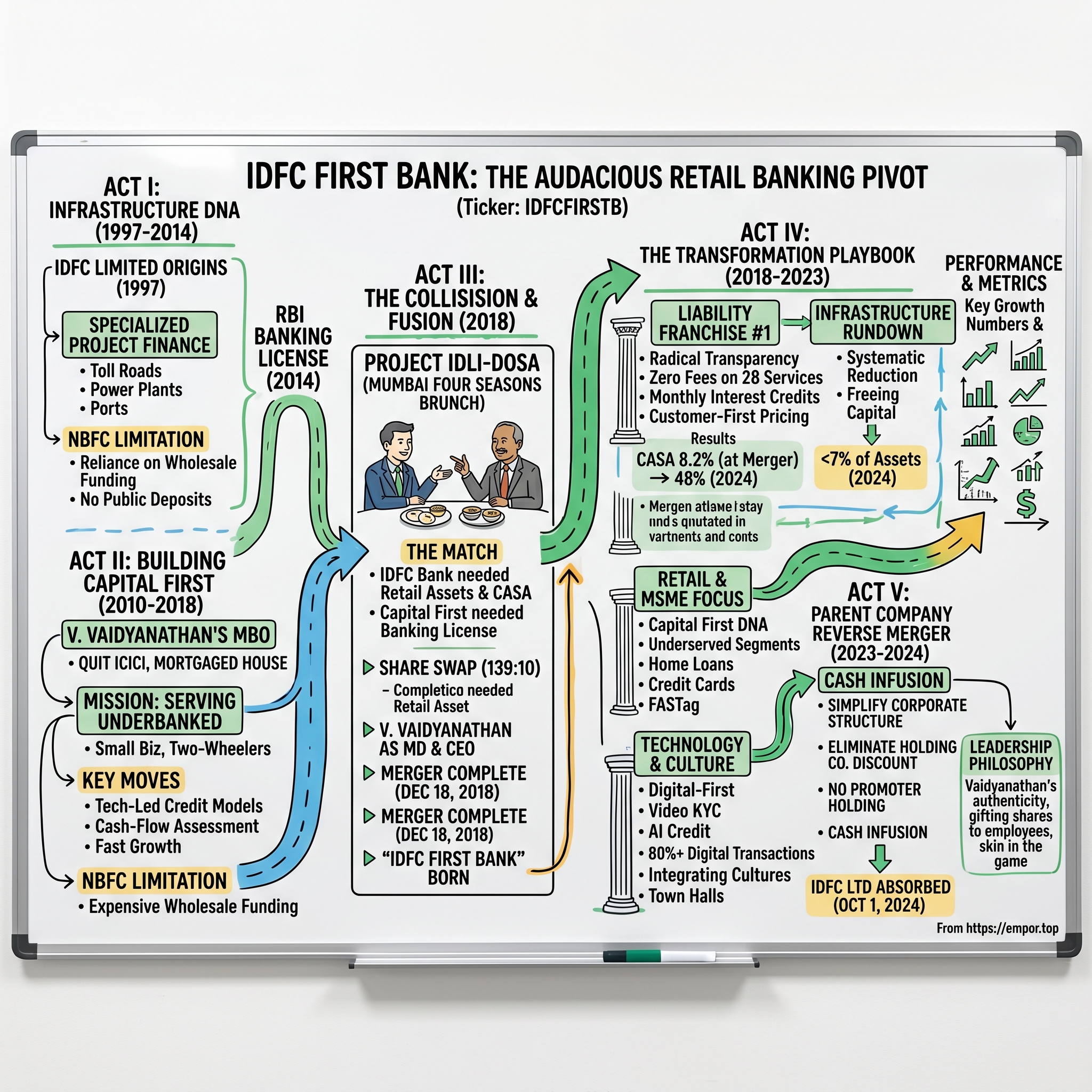

Picture this: A brunch meeting at Mumbai's Four Seasons Hotel in Worli, 2017. Two banking executives sit across from each other, negotiating the future of Indian finance over curd rice and khichdi. No investment bankers. No PowerPoint decks. Just two leaders with radically different banking philosophies, secretly code-naming their discussions "Project Idli-Dosa." One built his career financing massive infrastructure projects—bridges, power plants, highways. The other had just pulled off one of Indian banking's gutsiest moves: mortgaging his own house to buy an NBFC with borrowed money at 13% interest.

This unlikely pairing would birth IDFC FIRST Bank—a Mumbai-based private sector lender that represents one of the most dramatic pivots in Indian banking history. The central question isn't just how an infrastructure lender became a retail banking disruptor. It's how a bank with an 8.2% CASA ratio and a book full of stressed infrastructure loans transformed itself into a tech-driven retail powerhouse with 48% CASA and 7 million customers in under six years.

Founded initially as IDFC Bank in 2015 as a banking subsidiary of IDFC Limited, the institution underwent a complete metamorphosis after its 2018 merger with Capital First. Today, with a market capitalization of ₹51,179 crore and quarterly income exceeding ₹11,000 crore, IDFC FIRST Bank stands as a case study in corporate reinvention.

This is a story of three acts: First, the infrastructure DNA that gave birth to IDFC Limited in 1997. Second, the parallel universe where V. Vaidyanathan was building Capital First through sheer entrepreneurial audacity. And third, their collision and fusion into something neither could have achieved alone. It's about betting everything—literally, in Vaidyanathan's case—on the belief that India's banking system was leaving millions underserved. Let's dive into how infrastructure met retail, and why that collision changed everything.

II. The Infrastructure DNA: IDFC Limited Origins (1997–2014)

The year was 1997. India's infrastructure deficit was staggering—power cuts were routine, roads were inadequate, ports were congested. The Government of India recognized that public funding alone couldn't bridge this gap. They needed private capital, and private capital needed a specialized intermediary. Enter IDFC Limited—Infrastructure Development Finance Company—conceived not as just another financial institution, but as a catalyst for India's infrastructure transformation.

IDFC Limited was set up with a specific mandate: mobilize private sector capital for infrastructure development through project finance. This wasn't traditional banking. Project finance meant evaluating toll roads based on traffic projections, power plants on purchase agreements, ports on cargo forecasts. It required deep engineering knowledge, regulatory expertise, and most importantly, patience—infrastructure projects take years to build and decades to generate returns.

The early years were about establishing credibility. IDFC financed projects that traditional banks wouldn't touch—greenfield power plants in remote areas, toll roads through difficult terrain, ports in underdeveloped coastlines. By 2005, when Dr. Rajiv Lall joined as CEO, IDFC had already established itself as India's infrastructure financing backbone. But Lall saw beyond project finance.

Under his leadership, IDFC expanded aggressively into adjacent businesses. Asset Management came first—who better to manage infrastructure funds than those who understood the projects? Institutional Broking followed—IDFC's infrastructure expertise gave it unique insights into industrial sectors. Then came the Infrastructure Debt Fund, tapping into insurance and pension money seeking long-term yields. By 2010, IDFC wasn't just financing infrastructure; it had built an entire ecosystem around it.

Yet Lall understood a fundamental limitation: as an NBFC, IDFC couldn't accept public deposits. It relied on wholesale funding—bonds, bank loans, institutional money. This made funding expensive and volatile. During the 2008 financial crisis, when wholesale markets froze, IDFC felt the squeeze despite having solid assets. The solution was obvious: become a bank.

In 2013, when the Reserve Bank of India opened applications for new banking licenses—the first such window in a decade—Lall didn't hesitate. IDFC's application emphasized its track record, its development focus, its professional management. The pitch resonated. In April 2014, RBI granted in-principle approval to IDFC Limited to establish a new private sector bank.

The banking license represented more than regulatory approval—it was a ticket to transformation. IDFC could now access low-cost CASA deposits, expand into retail banking, and diversify beyond infrastructure. The limitations of being a specialized infrastructure financier—concentration risk, long gestation periods, limited scalability—could finally be overcome. Or so they thought. The infrastructure DNA that had been IDFC's strength would soon become its greatest challenge.

III. The V. Vaidyanathan Story: Building Capital First (2010–2018)

While IDFC was navigating boardrooms and policy corridors, V. Vaidyanathan was plotting something entirely different. In 2010, after 20 years climbing the corporate ladder—from ICICI Bank to ICICI Prudential Life Insurance where he served as CEO—Vaidyanathan did the unthinkable. He quit. Not for another corner office, but to become an entrepreneur at age 45.

His target wasn't glamorous: Future Capital Holdings, a struggling NBFC drowning in real estate loans. The company was valued at ₹780 crore, bleeding money, and desperate for direction. Vaidyanathan's vision? Transform it into a technology-driven lender serving India's underbanked millions—small businesses, truck drivers, two-wheeler buyers. The segments banks ignored because they couldn't figure out how to serve them profitably.

Here's where the story turns audacious. Vaidyanathan didn't have ₹80 crore lying around to buy his stake. So he borrowed it—every rupee—at 13% interest, securing the loan with the very shares he was buying and mortgaging his own house. His friends thought he'd lost his mind. A successful insurance CEO betting everything on a failing NBFC? The interest payments alone were ₹10 crore annually.

But Vaidyanathan saw what others missed. Traditional banks were stuck in a time warp—demanding salary slips from daily wage earners, collateral from micro-entrepreneurs, perfect credit histories from first-time borrowers. Meanwhile, 400 million Indians remained outside the formal credit system. The opportunity wasn't in competing with HDFC Bank for salaried customers; it was in building alternative credit models for everyone else.

The transformation began immediately. Out went the real estate lending team. In came data scientists, technology architects, field officers trained in cash flow assessment. Vaidyanathan rebranded the company as Capital First and rebuilt it from scratch. Instead of salary slips, they analyzed bank statements. Instead of collateral, they perfected cash-flow based lending. Instead of branch-heavy operations, they went directly to customers—financing vehicles at dealerships, machinery at industrial clusters, working capital at wholesale markets. The numbers tell the story: Capital First's retail book grew from ₹94 crore ($14m) in 2010 to ₹29,600 crore ($4b) by 2018, financing 7 million customers. The gross NPAs fell from 5.36% to under 1%. The company that was losing ₹30 crore annually became profitable, generating ₹358 crore in profits. The market capitalization jumped from ₹790 crore at the time of acquisition to ₹6,096 crore by September 2018—nearly an eight-fold increase.

By 2012, Vaidyanathan had proven the model sufficiently to attract serious institutional capital. He secured equity backing of Rs. 8.10 billion from Warburg Pincus, which included a buyout of existing shareholders through an open offer, fresh capital injection, and complete reconstitution of the board. This wasn't just funding—it was validation that alternative credit models could work at scale in India.

The technology stack Capital First built was revolutionary for its time. Automated credit scoring for micro-entrepreneurs. Mobile-based loan origination. Cash flow analysis algorithms that could assess a kirana store owner's creditworthiness without a single formal financial statement. While traditional banks were still asking for three years of ITR returns, Capital First was disbursing loans within 48 hours based on transaction patterns.

By 2017, Capital First had become everything Vaidyanathan envisioned—a profitable, fast-growing, technology-driven lender serving India's underbanked. The market capitalisation grew from $120m at the time of the MBO in 2012 to $1.2bn in five years. But there was still one problem: as an NBFC, Capital First couldn't accept deposits. It relied on expensive wholesale funding. The solution would come from an unexpected source—a struggling infrastructure bank looking for salvation.

IV. IDFC Bank's Early Struggles (2015–2018)

October 1, 2015 should have been a celebration. IDFC Bank's doors opened for business, the culmination of nearly two decades of infrastructure financing expertise. Rajiv Lall had achieved what seemed impossible—transforming an NBFC into a full-fledged bank. But the champagne stayed corked. The reality on the ground was sobering.

IDFC Bank started operations on 1 October 2015. The bank inherited IDFC Limited's infrastructure loan book—power plants, toll roads, ports—assets that looked solid on paper but were increasingly problematic in practice. India's infrastructure sector was in crisis. Projects were stuck in regulatory clearances, land acquisition battles, environmental protests. Power plants couldn't sell electricity because state distribution companies were bankrupt. Toll roads faced revenue shortfalls as traffic projections proved wildly optimistic.

IDFC Bank faced challenges due to bad loans from legacy infrastructure accounts. These weren't small hiccups—they were existential threats. A single stressed power project could wipe out an entire quarter's profits. The concentration risk that had been manageable as an NBFC became terrifying as a bank with regulatory capital requirements.

The numbers painted a stark picture. By September 2017, the bank's deposits totaled ₹38,890 crore, with a CASA ratio of just 8.2%. To put this in perspective, HDFC Bank's CASA ratio was above 40%. ICICI Bank was at 50%. IDFC Bank was essentially borrowing expensive money to lend at thin margins—a recipe for disaster.

The attempted escape route turned into another dead end. A planned merger with the Shriram Group was called off. Shriram, with its massive truck financing and SME lending portfolio, would have given IDFC Bank instant retail presence. But the complexities proved insurmountable—different cultures, overlapping businesses, regulatory hurdles. By late 2017, IDFC Bank was stuck: too small to compete with established banks, too concentrated in infrastructure to be sustainable, too expensive to fund itself profitably.

Lall knew the bank needed a dramatic pivot. Infrastructure lending, the very DNA of IDFC, had become a millstone. The bank needed retail assets, CASA deposits, technology capabilities—everything IDFC Bank didn't have. Meanwhile, 800 kilometers away in Mumbai's suburbs, V. Vaidyanathan was running a different playbook entirely. Capital First was everything IDFC Bank wasn't: retail-focused, technology-driven, profitable. What happened next would redefine both institutions.

V. The Merger: Birth of IDFC FIRST Bank (2018)

The story of how IDFC Bank and Capital First came together reads like a Mumbai business thriller. In January 2018, IDFC Bank and MSME financing company Capital First announced a merger. But the real drama happened months earlier, in a series of secret meetings that would determine the future of Indian banking.

The setting: Four Seasons Hotel, Worli. The menu: curd rice and khichdi—deliberately simple, almost ascetic. The code name: "Project Idli-Dosa." No investment bankers. No PowerPoint presentations. Just two banking leaders with radically different backgrounds but converging visions, meeting over South Indian comfort food to negotiate one of Indian banking's most consequential mergers.

When IDFC Bank boss Rajiv Lall met Vaidyanathan over that first brunch, both men knew what was at stake. Lall needed retail assets and someone who understood mass-market banking. Vaidyanathan wanted a banking license—the one thing Capital First, despite all its success, couldn't obtain as an NBFC. It was a perfect match of needs, if they could make the economics work.

The negotiations were remarkably swift—just two sittings to finalize the broad contours. 139 shares of IDFC Bank were issued for every 10 shares of Capital First as part of the merger share swap. This valued Capital First at approximately ₹15,000 crore—a remarkable premium for a company Vaidyanathan had acquired for ₹780 crore just six years earlier.

The structure was elegant in its simplicity. V Vaidyanathan, who is currently Chairman and Managing Director (CMD) of Capital First, will succeed Dr Rajiv Lall as MD and CEO of the combined entity. Dr Lall will become non-executive Chairman replacing Veena Mankar, who will remain on the Board, after the merger. It wasn't just a merger—it was a complete leadership transition.

The strategic logic was compelling. "This announcement is pursuant to IDFC Bank's stated strategy of 'retailising' its business to complete its transition from a dedicated infrastructure financier to a well-diversified universal bank, and in line with Capital First's stated intention and strategy to convert into a universal bank," the statement said. "On our part, we have always said publicly that a banking platform provides a stable diversified liability base and is hence critical for building a large franchise. We are excited about this merger because IDFC Bank provides a perfect platform for continued growth of the combined franchise, supported by low-cost funding," says Mr Vaidyanathan.

But not everyone was convinced. Analysts raised tough questions. "Retail assets can be built quickly, but the problem is, how do you garner retail liabilities (deposits)? Capital First won't be helping much in that. Besides, the kind of customers Capital First will have, I doubt the bank would want them. The bank seems to be struggling a bit," an analyst with a foreign brokerage said.

The numbers told a complex story. IDFC Bank's legacy burden creates a drag on its profit and loss accounts for two reasons: There is a legacy bad asset stock of Rs 3,700 crore for which the bank is incurring a cost of Rs 175-200 crore a year. Then, Rs 36,000 crore of bonds were contracted for a coupon of 8.9 per cent. This is a net negative drag (netted for the amount the bank would have paid if the bonds were contracted at the present rate) of around Rs 400 crore a year. This pre-tax Rs 575-600 crore of drag translates into 0.35 per cent hit on the return on assets.

"IDFC Bank and Capital First merged effective 18th December 2018. Merged entity to be called IDFC First Bank, subject to shareholders' approval," the firms said in a joint statement. The merger completed in record time—less than a year from announcement to consummation. Vaidyanathan took over as the MD and CEO of the merged entity.

The combined entity started with impressive metrics: On a combined basis, IDFC First Bank has on-book loan assets of Rs. 1,02,683 crore, as per the last reported financial results for the quarter ended September 30, 2018. The retail loan book will now contribute 32.46% to the overall loan book. It will serve 7.2 million customers through its 203 bank branches, 129 ATMs, 454 rural business correspondent centers across the country's urban and rural geographies.

An aspiration for accelerated and sustained growth had paved the way for this merger. IDFC FIRST Bank was born to be distinctly different from what either institution had been before. It combined IDFC's banking license and balance sheet strength with Capital First's retail expertise and technology platform. The infrastructure lender and the retail NBFC had become one—setting the stage for one of Indian banking's most dramatic transformations.

VI. The Transformation Playbook (2018–2023)

December 18, 2018 marked Day One of IDFC FIRST Bank. But the real work began on Day Two. Vaidyanathan inherited a bank with fundamental problems: Its CASA ratio increased from 8.6% to 49.77% and retail deposits went up from 27% to 76% of total deposits, as of March 2023. That transformation didn't happen overnight—it required a complete reimagining of what an Indian bank could be.

The bank transitioned from infrastructure financing to retail banking in four years since the merger. IDFC FIRST Bank was born to be distinctly different. It had a renewed focus on retail business with an intent to fast-forward its growth trajectory. But first, Vaidyanathan had to fix the fundamentals.

The liability franchise was priority number one. An 8.6% CASA ratio meant the bank was essentially borrowing expensive money to lend—unsustainable in any competitive environment. Traditional banks built CASA through decades of branch expansion and brand building. IDFC FIRST didn't have decades. So they took a different approach: radical transparency and customer-first pricing.

While other banks buried fees in fine print, IDFC FIRST published everything upfront. Zero fees on 28 commonly used services—savings account maintenance, debit cards, IMPS, NEFT, RTGS transfers. Monthly interest credits instead of quarterly—a small change that meant real money for customers living paycheck to paycheck. Interest rates up to 7% on savings accounts when competitors offered 3-4%. The message was clear: we're different.

The infrastructure book presented a different challenge. These weren't bad loans that could be written off quickly—they were long-term project financings with complex restructuring requirements. The strategy was surgical: run down the book systematically while avoiding fire sales. Since 2019, it has expanded its product range, including loans, deposits, and wealth management, and introduced new products like home loans, credit cards, FASTag, etc.

By December 2021, the infrastructure book had reduced by 31% year-over-year and constituted just 6.6% of total funded assets. The bank continued this rundown while redirecting capital to retail and MSME lending—segments with higher yields, better asset quality, and faster turnover.

Technology became the enabler of scale. The bank couldn't afford to build thousands of branches, so it built digital capabilities instead. Video KYC for account opening. AI-powered credit decisioning that could approve loans in minutes. A mobile app that handled everything from mutual fund investments to FASTag recharges. By 2022, over 80% of transactions happened digitally.

The retail and MSME lending playbook borrowed heavily from Capital First's DNA. Instead of competing for prime corporate loans at wafer-thin margins, IDFC FIRST focused on underserved segments. Small business loans based on GST returns. Personal loans for new-to-credit customers. Two-wheeler financing in tier-3 cities. Each segment carefully chosen for its growth potential and competitive dynamics.

Culture transformation proved as important as business transformation. The merger brought together infrastructure bankers accustomed to ₹100 crore deals and retail lenders who celebrated ₹1 lakh disbursements. Vaidyanathan's approach was deliberate integration—keeping what worked from both cultures while building something new. Town halls replaced board presentations. Customer stories replaced PowerPoints. Field visits became mandatory for senior management.

The bank, which transitioned from an infrastructure Development Finance Institution (DFI) with a net interest margin (NIM) of 1.7% to a commercial bank, faced early challenges with low retail deposits and initial losses in 2019. "Analysts back then saw this as a tough paradox—investing in growth meant more losses, but without investment, the issue would persist," Vaidyanathan explained. In FY 2024, the bank posted a profit of ₹2,947 crore and increased its CASA ratio to 47%.

The numbers validated the strategy. Customer deposits grew from ₹38,455 crore in 2019 to over ₹200,000 crore by 2023. The loan book expanded from ₹104,660 crore to ₹241,926 crore. Net interest margins improved from 1.6% to 6.0%. The bank that lost ₹1,944 crore in FY19 posted profits of ₹2,957 crore in FY24.

"Thanks to our team's dedication, we've resolved this paradox in five years. Our long-term credit rating has been upgraded to AA+ stable by four rating agencies, and we're now striving for AAA," Vaidyanathan added. The transformation wasn't complete, but the direction was clear. IDFC FIRST had successfully pivoted from infrastructure lender to retail bank. Now came the next challenge: simplifying the corporate structure.

VII. The Parent Company Reverse Merger (2023–2024)

The corporate structure of IDFC had become a puzzle within a puzzle. IDFC Limited owned 40% of IDFC FIRST Bank through a financial holding company. The bank was performing well, but investors couldn't directly benefit—they owned shares in a holding company that owned shares in the bank. Classic holding company discount. In boardrooms across Mumbai, this structure was increasingly seen as an anachronism.

In July 2023, the board of the bank approved the merger with IDFC Limited. This wasn't a typical acquisition—it was a reverse merger where the subsidiary would absorb the parent. The financial engineering was elegant: simplify the structure, eliminate the holding company discount, and create a cleaner equity story for investors.

The boards of IDFC Financial Holding Co Ltd, IDFC Ltd, and IDFC First Bank had approved the merger in July 2023. IDFC Limited and IDFC Financial Holding Company (IDFC FHCL) have received RBI's "No Objection" for the composite scheme of amalgamation on December 26, 2023. The regulatory approvals came through systematically—Competition Commission, Reserve Bank, SEBI.

The economics were carefully calibrated. Under the proposed reverse merger scheme, IDFC shareholders will get 155 shares for every 100 shares held in the bank. According to the amalgamation scheme, 264.64 crore shares of IDFC FIRST Bank held by IDFC Ltd will get extinguished, and based on the share exchange ratio mentioned above, 248 crore new shares of IDFC FIRST Bank would be issued to the shareholders of IDFC Ltd based on their respective holdings.

The strategic rationale went beyond financial engineering. The merger will lead to simplification of the corporate structure of IDFC FHCL, IDFC Limited and IDFC First Bank by consolidating them into a single entity and will help streamline the regulatory compliances of the aforesaid entities. No more regulatory arbitrage between holding company and bank. No more explaining to investors why they should value a holding company that holds a bank. Just one entity: IDFC FIRST Bank.

The majority shareholders of IDFC First Bank have approved the amalgamation of IDFC Ltd with the bank at a meeting convened by the Chennai bench of the National Company Law Tribunal (NCLT), the lender informed the stock exchanges on May 17. "We wish to inform that the resolution approving the Scheme was passed by overwhelming majority of 99.95 percent of the equity shareholders representing more than three-fourth in value of the equity shareholders of the Bank voting through remote e-voting and e-voting during the meeting, in terms of the provisions of Sections 230-232 of the Companies Act, 2013," the bank said.

The culmination came swiftly. After receiving clearance from the Competition Commission of India and the Reserve Bank of India, the merger proposal was approved by the National Company Law Tribunal in May 2024. On 1 October 2024, IDFC Limited merged with the bank. As a result of the merger, 155 equity shares of the bank were allotted for every 100 equity shares of IDFC Limited held by each shareholder in the latter.

The benefits were immediate and tangible. As a result of the proposed merger, the standalone book value per share of the bank would increase by 4.9 percent, as calculated on audited financials as of March 31, 2023, said the lender. Meanwhile, IDFC is sitting on Rs 6 bn of cash which will come into IDFC First Bank post-merger. The cash infusion strengthened an already robust capital position.

More importantly, the merger eliminated a key overhang. The merger will help create an institution with diversified public and institutional shareholders, like other large private sector banks, with no promoter holding, the IDFC First Bank said in a stock exchange filing. With the merger complete, the bank no longer has a promoter holding, aligning its structure with other major Indian private banks like ICICI Bank and HDFC Bank.

The dividend story added another dimension. IDFC First Bank has not paid dividends in recent years due to legacy losses. However, following the merger, these accumulated losses will be offset against the bank's Securities Premium Account. This paves the way for IDFC First Bank to distribute dividends in the near future—a significant positive for shareholders looking for steady returns.

In 2024, the bank took over the parent company IDFC Limited in a reverse merger. The infrastructure financier that had birthed a bank was now absorbed by its own creation. It marked the end of one era and the beginning of another—IDFC FIRST Bank was now truly independent, with no parent company, no holding structure, just a clean, simple bank ready for its next phase of growth.

VIII. Financial Performance & Business Metrics

The numbers tell a story of transformation and growing pains. IDFC FIRST Bank reported a total income of ₹11,122.86 crore in Q3 FY25, up from ₹10,684.32 crore in Q2 FY25 and ₹9,396.06 crore in Q3 FY24. Net profit stood at ₹340.17 crore, an increase from ₹211.94 crore in Q2 FY25, but a decrease from ₹732.09 crore in Q3 FY24. The year-over-year profit decline reflects the challenges of rapid growth and asset quality pressures in certain segments.

The balance sheet expansion has been remarkable. Advances grew to ₹2,23,103.93 crore, compared to ₹1,82,268.94 crore in Q3 FY24. IDFC FIRST Bank continues to grow robustly, with customer deposits increasing by 29% YoY to ₹2,27,316 crore, supported by a sustained CASA ratio of 48%. Loans and advances expanded by 22% YoY, reaching ₹2,31,074 crore. This isn't just growth—it's high-velocity expansion with maintained funding discipline.

The CASA transformation deserves special attention. From 8.6% at merger to 48% today—that's not incremental improvement, it's a complete reimagining of the liability franchise. Every percentage point of CASA improvement drops straight to the bottom line through lower funding costs. At 48%, IDFC FIRST now competes with established private banks on funding efficiency.

On the asset quality front, the bank's gross non-performing assets ratio improved to 1.94 per cent from 2.04 per cent a year ago. Similarly, net NPAs, or bad loans, came down to 0.52 per cent from 0.68 per cent at the end of the third quarter last fiscal. These are enviable metrics in Indian banking—sub-2% gross NPA and half a percent net NPA indicate strong underwriting and collection capabilities.

But the quarter also revealed challenges. Overall provisions, excluding tax doubled to Rs 1,338 crore from Rs 655 crore in the same quarter a year ago. The gross slippage for Q3-FY25 was Rs 2,192 crore as compared to Rs 2,031 crore in Q2 FY 2025, an increase of Rs 162 crore, it said. "Majority of the increase in slippage during Q3FY 25 was from the microfinance business which constituted Rs 143 crore out of the said Rs 162 crore. The microfinance segment, while strategically important for financial inclusion, presents asset quality headwinds.

Interest earned rose to ₹9,342.99 crore, reflecting growth from ₹8,957.02 crore in Q2 FY25 and ₹7,879.50 crore in Q3 FY24. The 18.5% year-over-year growth in interest income demonstrates strong lending momentum and improving yields. Net interest margins remain healthy, benefiting from the improved funding mix.

The profitability journey has been volatile but directionally positive. From losses of ₹1,944 crore in FY19 to profits approaching ₹3,000 crore in FY24, the bank has engineered a remarkable turnaround. The Q3 FY25 dip in profits reflects conservative provisioning rather than fundamental weakness—management choosing prudence over optics.

Mkt Cap: 51,179 Crore. Company has a low return on equity of 7.87% over last 3 years. The market capitalization crossing ₹50,000 crore marks a significant milestone, though the ROE remains below peer levels—a function of the infrastructure legacy and aggressive growth investments.

The infrastructure book rundown continues systematically. From over 30% of assets at merger to under 7% today, this portfolio shrinkage has freed up capital for higher-yielding retail assets. Each quarter of rundown improves the bank's risk profile and profitability metrics.

Looking at the metrics holistically, IDFC FIRST Bank presents a classic transformation story. Strong top-line growth (20%+ loan growth, 30%+ deposit growth). Improving but still sub-optimal profitability (ROE under 8%). Asset quality under control but with emerging segment-specific pressures. The trajectory is positive, but the destination—sustainable 15%+ ROE—remains several years away.

IX. The Vaidyanathan Leadership Philosophy

The guitar strums in the boardroom tell you everything. When Amitabh Bachchan visited IDFC FIRST Bank's headquarters after becoming brand ambassador, V. Vaidyanathan pulled out his guitar and sang "Wind of Change" by the Scorpions. Not a PowerPoint in sight. This isn't theatrical management—it's authenticity in a sector drowning in formality.

In February 2022, Vaidyanathan gifted shares worth ₹4 crore to five of IDFC First's employees, including help and a driver. In May 2021, he gave away 4.3 lakh shares, worth over ₹2.4 crore to three persons from IDFC First Bank to help them buy a house. The specifics matter: 3 lakh shares to his trainer Ramesh Raju, 2 lakh shares each to househelp Pranjal Narvekar and driver Algarsamy C Munapar, and 1 lakh shares each to office support staff Deepak Pathare and Santosh Jogale.

This isn't charity—it's alignment. "It is declared that the recipients are personal relationships and not related to him in any manner under the definition of related parties of the Companies Act or SEBI Regulations. These transactions are without consideration," the filing stated. By making his support staff shareholders, Vaidyanathan creates stakeholders. The driver who takes him to meetings owns a piece of the bank he's building.

The '38% given away' statistic is staggering. The 54-year-old banker, who has been named as the 'banker with a golden heart' by netizens, has gifted about 38 percent of his stake since the beginning of 2018. Most CEOs accumulate wealth; Vaidyanathan systematically distributes it. Not after retirement, not through a foundation—directly, immediately, to people who helped him build.

The mathematics teacher story encapsulates his philosophy. Vaidyanathan enrolled in the Birla Institute of Technology, Mesra, but ran out of money to buy train tickets. His mathematics teacher then lent him 500 rupees to take a train to help him appear for an interview at Birla Institute of Technology, Mesra. Decades later, he tracked down the teacher and gifted him one lakh shares. The message: debts aren't just financial, and repayment compounds.

Management style flows from personal philosophy. As a boss, he takes the call but listens to others' points of view and encourages dissent. Yes, two senior executives in the bank who had come from the NBFC—one was heading technology and operations and other retail assets—had left the bank abruptly after the merger. However, a majority have stayed put, and they swear by his leadership acumen. The attrition that matters—frontline staff—remains industry-low.

The personal investment approach defines skin in the game differently. In September 2023, Vaidyanathan sold 5.07 crore shares of IDFC First Bank for ₹478.7 crore to US-based GQG Partners through a block trade transaction. From the revenue generated, ₹229 crore was allocated for the subscription of new shares in IDFC First Bank. He's not cashing out—he's doubling down, using personal sales to fund bank growth.

Building culture through symbolism matters in banking. When Capital First employees joined him "leaving well-paying jobs, worked hard, conceptualised strategies, introduced many innovations and discovered new lines of business," the statement mentioned. Three of the giftees are no longer in the company "but their contribution cannot be forgotten," he said. Past contribution gets present recognition—unusual in corporate India.

The fitness routine speaks to discipline. Sukanto Roy, an ultramarathoner who trains Vaidyanathan for his marathon four days a week, has many stories to tell about the entrepreneur banker's behaviour. Vaidyanathan first house hunted with him, then gifted him Rs 25 lakh to pay for margin money to buy a one-bedroom flat at Lower Parel. Physical discipline mirrors financial discipline—both require daily commitment.

Long-term thinking manifests in compensation philosophy. IDFC FIRST doesn't pay highest salaries but offers widest ESOP distribution. The security guard who opens the door might own shares. The teller processing your deposit likely does. This isn't Silicon Valley equity culture transplanted—it's Indian banking reimagined as collective enterprise.

The Reserve Bank of India approved his re-appointment as IDFC First Bank's Managing Director and Chief Executive Officer for three years, effective from 19 December 2024. The regulatory confidence reflects more than financial metrics—it's validation of a leadership model that puts stakeholder capitalism into practice. Building a tech-first retail bank requires more than algorithms—it requires aligning thousands of people toward a common vision. Vaidyanathan's philosophy: make them owners, not just employees.

X. Competitive Landscape & Strategic Positioning

The Indian private banking landscape presents a David-and-Goliath narrative. At the top, four giants dominate: HDFC Bank with a market cap exceeding ₹13 trillion, ICICI Bank at ₹9.5 trillion, Kotak Mahindra at ₹3.5 trillion, and Axis Bank at ₹3 trillion. Then there's IDFC FIRST Bank at ₹511 billion—roughly 1/25th the size of HDFC Bank. The scale gap is enormous, but that's precisely the opportunity.

HDFC Bank, ICICI Bank and Kotak Mahindra Bank are the three largest and well-known private sector banks in India. These banks built their franchises over decades—HDFC Bank since 1994, ICICI since transformation in 2000s, Axis (formerly UTI Bank) since 1993. They enjoy network effects, brand recognition, and deep CASA pools that self-reinforce their dominance.

The competitive dynamics favor different strategies at different scales. HDFC Bank plays the volume game—largest loan book, most branches, highest market share. HDFC bank is #1 in terms of interest income. In terms of CAGR growth in interest income, HDFC bank is #1. HDFC bank is 2nd. In terms of CAGR growth in total income, HDFC bank is #1. In terms of interest income as % of toal income, HDFC bank is #1. HDFC bank is 2nd. In terms of net profit, HDFC bank is #1. HDFC bank is 2nd. HDFC bank is 2nd. In terms of advances, HDFC bank is #1. In terms of CAGR growth in advances, HDFC bank is #1. It's the Walmart of Indian banking—efficiency through scale.

ICICI Bank represents the conglomerate model—retail banking, corporate banking, investment banking, insurance, asset management. ICICI bank is 2nd. In terms of total income, ICICI bank is #1. ICICI bank is 2nd. ICICI bank is 2nd. They're everywhere, in everything, leveraging cross-sell across businesses.

Kotak Mahindra occupies the premium niche. As of Q1FY22, the Kotak Mahindra Bank records the highest Net Interest Margin rate of 4.60% followed by HDFC Bank- 4.10%, ICICI Bank- 3.89%, and Axis Bank- 3.46%. Among these 4 Major Private Banks, Kotak Mahindra Bank has the highest CASA ratio of 60.2% in Q1FY22 which was 56.7% in the same quarter of the previous financial year. Highest NIMs, best CASA ratios—they're the Hermès of Indian banking, prioritizing margins over volume.

Axis Bank plays the transformation card—constantly reinventing, acquiring, digitizing. India's private sector banks saw a significant rise in market capitalization in the last quarter, led by Axis Bank's 20.9% growth, with private banks outperforming their public sector counterparts. They're the most acquisitive, most experimental of the big four.

Against these giants, IDFC FIRST Bank's positioning is deliberate counter-positioning. While big banks chase corporate loans and wealth management, IDFC FIRST focuses on underserved retail and MSME segments. While others maximize fees, IDFC FIRST offers zero-fee banking. While competitors build branches in metros, IDFC FIRST goes digital-first with physical presence in tier-2/3 cities.

The fintech challenge adds another dimension. Digital-only banks like Fi, Jupiter, and Niyo target the same young, tech-savvy customers IDFC FIRST wants. PayTM Payments Bank, though restricted in lending, competes for deposits. NBFCs like Bajaj Finance offer point-of-sale credit without banking overhead. Everyone wants a piece of India's 400 million underbanked adults.

IDFC FIRST's differentiation strategy has three pillars: customer-first pricing (highest savings rates, zero fees), technology-led operations (lower cost-to-serve), and focused segmentation (new-to-credit, small business, rural). The bank isn't trying to beat HDFC at its own game—it's playing a different game entirely.

Market share aspirations must be realistic. IDFC FIRST has roughly 1% market share in deposits and advances. Getting to 3-4% over a decade would represent extraordinary success. That's still a 3-4x growth opportunity in a market growing 12-15% annually. The math works: you don't need to dethrone the kings to build a valuable franchise.

The India opportunity provides tailwind for everyone. Credit-to-GDP at 55% versus 150%+ in developed markets. Financial inclusion still expanding. Digital payments exploding. Rising incomes driving credit demand. In this environment, multiple winners can coexist—the pie is growing faster than any single player can capture it.

The top 5 private banks in India by market cap are HDFC Bank, ICICI Bank, Kotak Mahindra Bank, Axis Bank, and IDBI Bank. HDFC Bank leads with ₹1384614.97 Cr, as of March 28, 2025. IDFC FIRST Bank sits at #9, but that's not the relevant comparison. The question isn't whether IDFC FIRST can overtake HDFC Bank—it can't and doesn't need to. The question is whether it can carve out a profitable, defensible niche in India's vast banking market. The evidence suggests it can.

XI. Bear vs. Bull Case

The bear case starts with harsh reality: Company has a low return on equity of 7.87% over last 3 years. In banking, ROE is destiny. At sub-8% returns, IDFC FIRST destroys value at current valuations. The math is unforgiving—if your cost of equity is 12-14% and you're generating 7-8%, you're lighting money on fire, regardless of growth rates.

The legacy infrastructure book remains an albatross. Yes, it's down to 6-7% of assets, but that's still ₹15,000+ crore of troubled loans generating negative spreads and requiring constant provisioning. Every quarter brings another ₹100-200 crore provision surprise from some decade-old power project. Until this book runs off completely—which could take another 3-5 years—it's a permanent drag on profitability.

Intense competition in retail banking presents another challenge. Every bank in India is now "retail-focused." HDFC Bank has 8,000+ branches and unlimited capital. Bajaj Finance can approve loans in 30 seconds. Fintech players offer better UX without regulatory overhead. What's IDFC FIRST's sustainable competitive advantage? Zero fees can be copied. High savings rates compress margins. Technology can be replicated. Where's the moat?

Asset quality concerns in unsecured lending loom large. The Q3 FY25 results showed it clearly—microfinance slippages driving provisions higher. As IDFC FIRST grows its unsecured book to improve yields, credit costs will inevitably rise. The trade-off between growth and asset quality is banking's eternal dilemma, and there's no evidence IDFC FIRST has solved it better than peers.

Execution risks in transformation multiply with complexity. Cultural integration takes years. Technology migrations fail regularly. Customer acquisition costs keep rising. Management bandwidth gets stretched. One bad quarter, one failed IT implementation, one credit blow-up, and the transformation narrative crumbles. Markets have seen too many "transformation stories" become cautionary tales.

The competitive intensity will only increase. If IDFC FIRST succeeds in proving the underbanked segment is profitable, every major bank will pile in. If they fail, they're stuck with adverse selection—customers other banks rejected. It's the classic banking Catch-22: profitable segments attract competition; unprofitable segments stay that way.

The bull case rests on transformation momentum. From 8.6% to 48% CASA in five years isn't luck—it's execution. From ₹38,000 crore to ₹227,000 crore deposits isn't coincidence—it's strategy working. The trajectory matters more than current position. If CASA reaches 55% and cost of funds drops another 50bps, ROE improvement follows mathematically.

Strong retail franchise building momentum cannot be ignored. 7 million customers and growing. 30%+ deposit growth sustained for years. Digital channels handling 80%+ transactions. This isn't hypothetical—it's happening now. Network effects in banking are real: more customers bring more deposits, enabling more loans, generating more fee income, attracting more customers.

Technology-led cost advantages compound over time. IDFC FIRST's cost-to-income ratio has room for 1000bps improvement to reach peer levels. As the bank scales, fixed costs spread over larger base. Digital operations mean marginal cost of serving additional customers approaches zero. The operating leverage is enormous once scale kicks in.

The large addressable market in India changes everything. 400 million adults without formal credit. 63 million MSMEs needing working capital. Financial inclusion still in early innings. Even capturing 1-2% of incremental market growth represents massive absolute opportunity. You don't need to steal share—just participate in growth.

Proven management track record de-risks execution. Vaidyanathan built Capital First from scratch to ₹30,000 crore loans. He's done this before. The team has navigated cycles, managed credit, raised capital. This isn't their first rodeo. In banking, management quality matters more than strategy—execution is everything.

The improving financial metrics trajectory validates the thesis. NPAs declining. Margins expanding. Costs rationalizing. Profits emerging. Every quarter shows incremental progress. The direction of travel matters more than current position when transformation is underway.

The balanced view acknowledges both narratives have merit. IDFC FIRST Bank is simultaneously a risky transformation story and a compelling growth opportunity. The bear case is about what is—low ROE, legacy issues, intense competition. The bull case is about what could be—scaled retail franchise, normalized profitability, market share gains.

The key variables to watch: CASA ratio (must exceed 50%), ROE (must reach 12%+), infrastructure book rundown (must accelerate), retail asset quality (must remain stable), and cost-to-income ratio (must fall below 50%). These five metrics will determine whether bears or bulls are proven right.

For investors, the question isn't whether IDFC FIRST Bank is good or bad—it's whether risk-reward is favorable at current valuations. At ₹51,000 crore market cap, markets are pricing in partial success. Full success could mean 3-4x returns. Complete failure might mean 50% downside. The asymmetry depends on your confidence in Indian banking's growth and management's execution ability.

XII. Playbook: Key Lessons

The power of focused pivots in banking emerges as the primary lesson. IDFC FIRST didn't try incremental change—they ripped up the playbook entirely. From infrastructure to retail. From wholesale funding to CASA deposits. From corporate relationships to mass market. The lesson: in banking transformation, half-measures fail. You either commit completely or you're stuck in no-man's land. Capital First succeeded because Vaidyanathan burned the boats—there was no Plan B.

Building from scratch versus acquiring capabilities presents a fascinating trade-off. IDFC tried building retail organically—it failed. Capital First built from scratch—it worked. The merger combined both approaches. The insight: acquisitions provide instant scale but bring legacy problems. Organic building takes longer but creates cleaner culture. IDFC FIRST got both—Capital First's clean retail assets and IDFC's banking license. Sometimes 1+1 really does equal 3.

Managing legacy portfolios while building new businesses requires surgical precision. You can't just abandon old customers—regulatory and reputational damage would be severe. But you can't let legacy problems contaminate new initiatives either. IDFC FIRST's approach—systematic rundown, separate management, clear communication—provides the template. Allocate your best people to the future, competent managers to the past, and never confuse the two.

The importance of patient capital in transformation cannot be overstated. Banking transformations take 5-10 years minimum. Quarterly earnings pressure kills long-term thinking. IDFC FIRST benefited from institutional shareholders who understood the timeline. Warburg Pincus held through volatility. IDFC Limited provided stability through the merger. The lesson: choose your shareholders as carefully as your strategy. Impatient capital makes transformation impossible.

Culture as competitive advantage sounds soft but drives hard results. IDFC FIRST's zero-fee philosophy isn't just pricing—it's cultural statement. Employee stock distribution isn't just compensation—it's alignment mechanism. The guitar-playing CEO isn't just quirky—it's authenticity in a sterile industry. Banking is ultimately a trust business, and culture drives trust. You can copy products, prices, and technology. You can't copy culture.

Technology as enabler for financial inclusion flips traditional banking economics. Serving a ₹10,000 loan customer profitably was impossible with physical branches. With digital onboarding, automated underwriting, and app-based servicing, unit economics work. IDFC FIRST proved you can serve the underbanked profitably at scale. Technology didn't just improve efficiency—it opened entirely new customer segments.

The merger architecture lesson is subtle but crucial. The Capital First-IDFC Bank merger worked because roles were clear from day one. Vaidyanathan would run the bank. Lall would be chairman then exit. No ambiguity, no power struggles, no parallel organizations. Compare this to failed bank mergers with competing power centers. The lesson: in transformational mergers, leadership clarity matters more than synergy calculations.

Liability franchise first, assets second—this sequencing matters enormously. Most banks focus on loan growth and worry about funding later. IDFC FIRST obsessed over CASA deposits first, knowing cheap funding enables everything else. Building deposits is harder than building loans, takes longer, requires more investment. But once established, a strong deposit franchise becomes the moat. Assets are tactics; liabilities are strategy.

The regulatory partnership approach deserves recognition. Rather than fighting regulations or gaming the system, IDFC FIRST aligned with regulatory priorities—financial inclusion, digital banking, customer protection. This earned regulatory goodwill, smoother approvals, benefit of doubt during challenges. In Indian banking, regulatory relationship is strategic asset. Invest in it accordingly.

Counter-positioning as strategy works when done authentically. IDFC FIRST didn't try to out-HDFC HDFC Bank. They zigged when others zagged. While peers chased wealth management, they focused on mass market. While others maximized fees, they eliminated them. While competitors built branches, they went digital. The lesson: in consolidated industries, being different beats being better.

The personal stake principle—skin in the game—aligns incentives powerfully. Vaidyanathan mortgaging his house to buy Capital First. Reinvesting sale proceeds back into bank equity. Gifting shares to employees. This isn't just financial engineering—it's signaling mechanism. When the CEO bets everything, employees and investors notice. Skin in the game creates credibility that no amount of corporate communication can match.

Time horizon arbitrage remains underappreciated in public markets. Most investors focus on next quarter's earnings. IDFC FIRST is building for 2030 and beyond. This mismatch creates opportunity. If you believe in India's long-term growth, in financial inclusion's inevitability, in technology's transformation power, then short-term volatility becomes irrelevant. The playbook: identify long-term trends, find committed management, and have patience others lack.

The ecosystem approach to financial services makes particular sense in India. IDFC FIRST isn't just a bank—it's becoming a financial platform. Savings, loans, payments, investments, insurance—all integrated digitally. As customers' financial lives become more complex, single-point solutions lose to integrated platforms. The playbook: start with one product, earn trust, then systematically expand wallet share.

Finally, the India context changes everything. What works in developed markets with 100% banking penetration doesn't apply in India with 400 million unbanked adults. The playbook must be rewritten for Indian conditions—cash-heavy economy, informal income documentation, joint family structures, mobile-first digital adoption. IDFC FIRST succeeded by building an Indian solution for Indian problems, not transplanting Western models.

The ultimate lesson: in banking, transformation is possible but requires total commitment. New leadership, new culture, new strategy, new metrics, patient capital, regulatory alignment, and flawless execution. Miss any element and transformation fails. Get them all right, and you can transform an infrastructure lender into a retail banking force. The IDFC FIRST story isn't complete, but the playbook is clear for those bold enough to follow it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube