Garware Hi-Tech Films: India's Specialty Films Pioneer

I. Introduction & Episode Roadmap

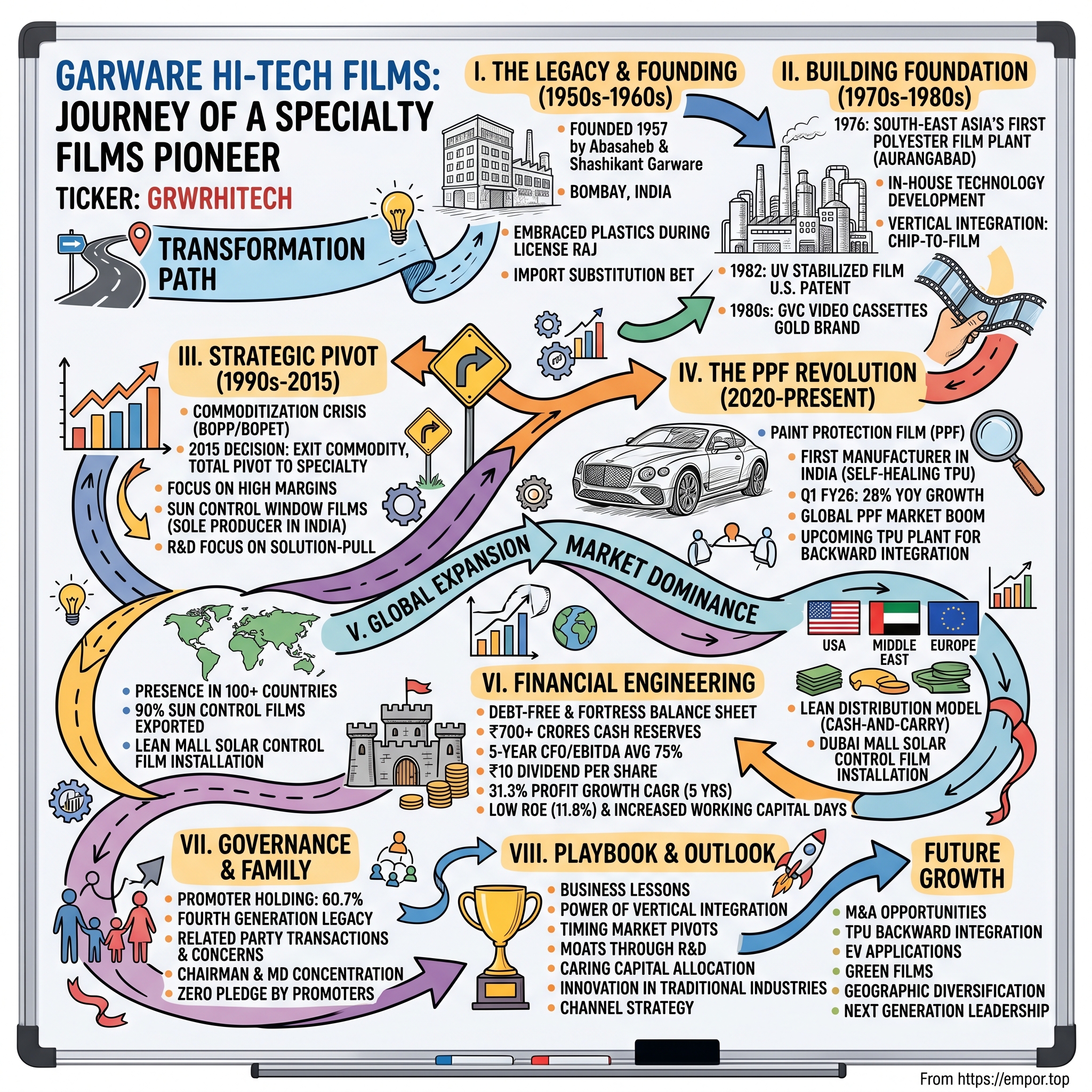

Picture this: In a nondescript industrial estate in Aurangabad, Maharashtra, massive extruders run 24/7, transforming tiny polymer chips into gossamer-thin films that will protect everything from Formula One race cars in Monaco to skyscrapers in Dubai. This is Garware Hi-Tech Films—a company that most Indians associate with those golden "GOLD" video cassettes from the 1990s, yet today stands as the world's only fully integrated "chip-to-film" manufacturer and India's sole producer of paint protection films. The company commands a market capitalization of ₹6,443 crores with annual revenues of ₹2,130 crores, making it a formidable mid-cap player in India's specialty chemicals space. Yet its story transcends mere numbers. This is the world's only vertically integrated "chip to film" manufacturing company—a distinction that took six decades to build.

The central question we'll explore: How did a polyester company founded in 1957, during India's License Raj era, transform itself into the sole producer of solar control window films in India and the only company globally with backward integration for producing raw materials for these films? How did it capture 70% of India's shrink film market and become the country's first paint protection film manufacturer?

This is a story of three pivotal transformations. First, the audacious 1976 decision to build South-East Asia's first state-of-the-art polyester film plant when India barely had a plastics industry. Second, the strategic pivot in FY2015 from commodity films to high-margin specialty products—a move that saved the company from irrelevance. And third, the 2020 entry into paint protection films, now growing at 28% annually and positioning Garware at the forefront of the automotive aftermarket revolution.

We'll examine how a family-controlled business with 60.7% promoter holding navigated India's liberalization, built global distribution across 100+ countries, and accumulated over ₹700 crores in cash reserves while remaining virtually debt-free. We'll also confront the paradoxes: Why does a company with 31.3% profit growth CAGR over five years generate only 11.8% return on equity? Why have working capital days ballooned from 54 to 119 days? And what explains the persistent corporate governance concerns despite stellar operational performance?

II. The Garware Legacy & Founding Context

The year 1957 requires contemplation. Imagine Bombay's sweltering summer heat, the ceiling fans struggling in the cramped offices of the old business districts, where a 23-year-old Dr. Shashikant Garware—fresh from Edinburgh University with a degree in Business Management—sits across from his father, the legendary Abasaheb Garware. The patriarch, who had built an empire from selling second-hand cars on the streets of Mumbai, now presided over one of India's pioneering industrial groups. Bhalchandra Digamber Garware (Abasaheb) was the Founding Chairman of the Garware Group of Industries, having gone to England in 1933 where he not only dealt with second hand cars but also purchased firms from businessmen taking advantage of recession, bringing him good profits.

The conversation that day would have been remarkable. India was just ten years independent, operating under what would later be dubbed the "License Raj"—a system of strict government control and regulation of the Indian economy from the 1950s to the early 1990s, where businesses required licenses to operate, with up to 80 government agencies needing to be satisfied before private companies could produce something. Yet here was young Shashikant proposing to enter the polyester business—an industry that didn't even exist in India.

Shashikant Bhalchandra Garware is credited with starting the polyester industry in India in June 1957. The audacity of this move cannot be overstated. Significant trade restrictions were imposed only after a balance of payments crisis in 1957, making imports of technology and machinery extraordinarily difficult. The textile industry, India's traditional strength, was still reeling from colonial de-industrialization. Yet Shashikant saw what others didn't: the future belonged to synthetic materials.

The Garware DNA was uniquely suited for this moment. Abasaheb had shown business acumen when he entered the Plastic Industry, identifying it as an upcoming industry, starting manufacturing Plastic buttons for the Navy during the 2nd World War, and eventually getting into ventures related to Plastic industry like Nylon Yarn, Nylon Bristles, fishing nets, Polyester Films, Synthetic Ropes. This wasn't a family that feared new materials or technologies—it embraced them.

The founding document of Garware Polyester Limited (as it was then known) reads like a manifesto against conventional wisdom. While other industrialists were content producing cotton textiles or basic consumer goods under protective licenses, the Company was co-promoted by Mr. S.B. Garware in the year 1957 alongwith the Founder Chairman Late Padmabhushan Dr. Bhalchandra (Abasaheb) Garware. The elder Garware, who had been appointed as the Sheriff of Bombay from 1959 to 1960 and awarded Padma Bhushan in 1971, brought political capital and credibility. The younger brought technical vision and international exposure.

What's fascinating about this origin story is how it prefigured every major strategic decision the company would make over the next six decades. The choice of polyester wasn't random—it was a bet on India's industrial future. Unlike cotton, which India had in abundance, polyester required technical sophistication, capital investment, and most importantly, the ability to develop technology in-house since imports were restricted. This forced innovation would become Garware's greatest strength.

The timing, in retrospect, was perfect. India's Second Five-Year Plan (1956-1961) emphasized heavy industry and import substitution. The government, while restrictive, was actively looking for entrepreneurs who could reduce import dependence. Polyester films were essential for the electrical industry, packaging, and eventually, magnetic tapes—all sectors the government wanted to develop domestically.

Shashikant's education at Dulwich College and Edinburgh University wasn't just about acquiring a foreign degree—he specialized in Administration, Sales Management and Market Research. This international perspective would prove crucial when, decades later, the company would need to pivot from domestic to global markets.

The family dynamics also deserve attention. The Garware Group wasn't a monolith—it was already showing signs of the structure that would later create both opportunities and governance challenges. Shashikantji Garware is popular in India as well as abroad for his sharp intellect, perseverance, courage and experimental nature. But this experimental nature would sometimes clash with the need for corporate transparency that modern markets demand.

As we transition to examining how this vision became reality with the 1976 Aurangabad plant, it's worth noting that the 19-year gap between founding and the first major manufacturing facility wasn't wasted. It was spent developing the technology, understanding the market, and most crucially, waiting for the right moment when government policy, market demand, and technological capability would align—a patience that modern startups might find instructive.

III. Building the Foundation: First Plant & Technology (1970s-1980s)

The morning of January 19, 1976. At the MIDC industrial area in Aurangabad, hundreds of workers, engineers, and dignitaries gathered for what would become a defining moment in Indian industrial history. Dr. Shashikant Garware, now 42, stood before a gleaming new facility—the first State-of-the-Art plant to manufacture Polyester Films in India, which was the first plant of its kind in South-East Asia. The ribbon was cut, the machines hummed to life, and India's journey toward self-reliance in specialty films had truly begun.

The nineteen years between founding and this moment hadn't been idle. They were spent battling bureaucracy, developing technology from scratch, and most crucially, convincing a skeptical government that polyester films weren't a luxury but a necessity for India's industrial future. The Company has developed in-house Technology for Polyester Films in India—a remarkable achievement considering the technological isolation imposed by the License Raj.

What made this plant revolutionary wasn't just its scale but its integration. The Company is the only one of its kind to manufacture its own raw material that is Polyester Chips to manufacture Polyester Films for variety of end applications such as Packaging, Electrical & Motor and Cable Insulations, Shrink Film for label application, Coloured Polyester Films for Window Tint application, sequin, TV Screen, Safety etc. This vertical integration—from chips to films—would become Garware's defining competitive advantage.

Then came 1982, the year that changed everything. In a cramped laboratory within the Aurangabad complex, a team of engineers led by Shashikant himself achieved what multinational giants hadn't: the development of U.V. Stabilized Polyester Film in 1982, a product that received a U.S. patent for its energy-saving properties. The patent—US4399265—wasn't just a technical achievement; it was a declaration that an Indian company could innovate at the global frontier.

The patent details reveal the sophistication of Garware's approach. While the products resulting from conventional methods were more resistant to UV than what preceded them, they were still of relatively limited life when subjected to strong sunlight. Garware's innovation involved a novel process where polyester granules and the UV-stabilizing substance in powdered form at an elevated temperature such that at least the exterior surface of the polyester granules is soft, thereby to cause the powdered UV-stabilizing substance to adhere to the individual polymer granules.

This technical breakthrough had profound commercial implications. In recognition of the company's contribution in this field, the Government of India honoured it with a Gold Shield for Import Substitution in 1981. The company was now competing with many Fortune 500 companies in the United States. It also surpassed established companies like DuPont, ICI, etc., thereby proving that Garware Hi-Tech Films is an important component of imports in India. This helped the Government of India save foreign exchange to a large extent.

But it was in the consumer market where Garware achieved its most visible success. In the 1980s and 1990s, it became a household name with GVC — Garware Video Cassettes. The iconic "GOLD" branding became synonymous with quality in Indian homes. With Garware video cassettes, we were the only source in India to make video recordings available. Every Bollywood film, every wedding video, every precious memory of that era was likely preserved on a Garware cassette.

The success of GVC wasn't just about manufacturing—it was about understanding the Indian consumer psyche. While international brands positioned themselves as premium, Garware positioned itself as reliable and accessible. The gold color wasn't accidental; it evoked trust, value, and aspiration—qualities that resonated deeply with middle-class India experiencing the first flush of consumer culture.

A state-of-the-art R&D unit was set up in Aurangabad for the development of polyester film products and the same was approved by the Department of Technology, Government of India. This wasn't just a compliance requirement; it was a strategic investment. The R&D facility became the nerve center for innovation, constantly experimenting with new formulations, applications, and processes.

The technological capabilities built during this period were staggering. The Company has four manufacturing plants for Polyester Film and manufactures Film of thickness ranging from 10 micron to 350 micron. To put this in perspective, 10 microns is thinner than human hair, requiring precision engineering that few companies globally could achieve.

What's remarkable about this period is how Garware navigated the contradictions of the License Raj. While the system was designed to restrict and control, Garware turned it into an advantage. The restrictions on imports forced them to innovate. The emphasis on import substitution gave them government support. The protection from foreign competition gave them time to build capabilities.

Abasaheb was proud of Shashikantji's performance in introducing new and various products of Garware Hi-Tech Films as well as launching successful products like polyester films, sun control, X-Ray films etc. This paternal pride wasn't misplaced—by the late 1980s, Garware had transformed from a startup into a technology leader, setting the stage for its next transformation.

As we move into examining the strategic pivot of the 1990s and 2000s, it's worth noting that the foundation laid in these two decades—vertical integration, technological capability, R&D focus, and consumer trust—would prove invaluable when liberalization opened India's markets and exposed domestic companies to global competition. The company that had learned to thrive under restrictions was about to discover what it could achieve without them.

IV. The Strategic Pivot: From Commodity to Specialty (1990s-2015)

The year 2015 marked a crossroads. In the boardroom at Garware's Mumbai headquarters, the atmosphere was tense. Revenue had plateaued, margins were shrinking, and the once-pioneering company faced an existential question: continue fighting in the commoditized BOPP/BOPET films market where giants like Jindal Poly Films commanded 251,000 TPA capacity, or chart a completely different course?

The numbers told a brutal story. Cosmo First established itself as one of the foremost manufacturers of BoPP films for flexible packaging, successfully transitioning from producing standard commodity films to focusing on innovative specialty films. Meanwhile, Garware was stuck in the middle—too small to compete on scale with companies adding 60,000-tonne lines, too unfocused to command premium pricing.

Dr. Shashikant Garware, now 81, made what would be his last major strategic decision: complete withdrawal from commodity films and a total pivot to value-added specialty products. This wasn't just a business decision; it was an acknowledgment that the world his company had helped create—mass production of standard polyester films—had moved on without them.

The commoditization crisis had been building for years. Raw material costs account for 55–60% of sales in this sector. Thus, profitability is vulnerable to fluctuations in raw material prices. Crude derivatives, the most expensive input cost for flexible packaging film, are inherently variable. When your product is indistinguishable from competitors and raw materials dominate your cost structure, you're not running a business—you're running a commodity trading operation with manufacturing attached.

The competitive landscape had become unrecognizable. The top dozen or so manufacturers of polyester, BOPP, BOPET packaging films have a current capacity of approximately 1.5 million tonnes at least six of these companies are expected to add new lines for either polyester or BOPP films in the next two years. Players like Jindal Poly Films were investing Rs. 1,000 crore for capacity expansion, while Garware's entire market cap was barely higher.

But within this crisis lay opportunity. While others chased volume, Garware identified niches where technology, not scale, determined success. It is also the sole producer of Solar Control window films in India and the only company globally with backward integration for producing the raw materials and components needed for these films. This wasn't discovered overnight—it was the result of methodical analysis of every product line, every customer relationship, every patent in their portfolio.

The sun control films business exemplified the new strategy. Unlike commodity BOPP films selling for $2-3 per kilogram, sun control films commanded $15-20 per kilogram. The technology barrier was formidable—combining UV stabilization, metallization, adhesive coating, and optical clarity required capabilities that commodity producers couldn't easily replicate. More importantly, Garware Polyester is the world's No.1 vertically integrated ''Chip to Film'' manufacturing company, giving them control over the entire value chain.

The shift to exports was equally dramatic. Rather than competing in price-sensitive domestic markets, Garware targeted developed markets where quality, certification, and technical support mattered more than the lowest price. Geographically, the company derives maximum revenue from its customers located in the United States of America and the rest from India, and the rest of the world. This wasn't just about finding new customers—it required building technical service capabilities, obtaining international certifications, and developing products that met stringent environmental regulations.

The shrink film market provided another validation of the strategy. It is a leading player in India's shrink film market with a 70% market share. How does a company achieve 70% market share in a competitive market? Not through price—through technical superiority. Garware's shrink films offered consistent shrinkage rates, superior clarity, and custom formulations that commodity producers couldn't match.

The R&D transformation during this period was profound. Instead of tweaking formulations to shave costs, the team focused on solving customer problems. Need a film that shrinks precisely 40% at 140°C for a specific labeling application? Garware could deliver it. Need UV protection that lasts 10 years in Arizona's desert sun? They had the technology. This shift from product-push to solution-pull fundamentally changed the company's DNA.

The financial impact was dramatic, though not immediate. Revenues initially declined as the company exited commodity products. But margins expanded significantly. Working capital improved as specialty products commanded better payment terms. Most importantly, the company became less vulnerable to raw material price swings—when you're selling technology, not plastic, customers accept price increases more readily.

The cultural transformation was equally significant. Engineers who had spent careers optimizing production yields were now visiting customer facilities, understanding applications, co-developing solutions. Sales teams transitioned from order-takers quoting prices to technical consultants solving problems. This wasn't easy—it required retraining, hiring new talent, and accepting that some old-timers wouldn't make the transition.

By 2015's end, the strategy was clear: Garware would be a specialty films company that happened to use polyester, not a polyester company trying to find specialties. This distinction might seem semantic, but it drove every subsequent decision—from capital allocation to hiring to R&D priorities.

The wisdom of this pivot became apparent when examining the fate of companies that didn't adapt. Several mid-sized BOPP/BOPET producers either shut down, were acquired for their assets, or remain perpetually subscale, earning returns below their cost of capital. Garware, by contrast, was about to embark on its most profitable chapter.

As we transition to examining the paint protection film revolution, it's worth noting that the capabilities built during this transformation—customer intimacy, technical excellence, solution orientation—would prove essential for entering the demanding automotive aftermarket, where brand reputation and product performance matter far more than in industrial films.

V. The Paint Protection Film Revolution (2020-Present)

The moment arrived in late 2019. In a nondescript conference room at Garware's Aurangabad facility, a team of engineers placed a pristine sheet of transparent film on the hood of a Mercedes-Benz S-Class. As they carefully applied heat and pressure, the film conformed perfectly to every curve and contour. Then came the test: deliberate scratches with a key. Within minutes, under gentle heat, the scratches disappeared completely. Paint Protection Film had arrived in India, and Garware was its pioneer.

The global paint protection film market size was estimated at USD 502.55 million in 2024 and is projected to reach USD 726.63 million by 2030, growing at a CAGR of 6.6% from 2025 to 2030. Garware's entry into this market wasn't accidental—it was the culmination of decades of polymer expertise meeting a massive market opportunity.

The decision to enter PPF represented everything the company had learned from its strategic pivot. This wasn't about making another plastic film; it was about solving a specific, high-value problem for discerning customers. The automotive & transportation application segment accounted for a 73.64% share of the overall market in terms of revenue in 2024, and within this segment, the premium and luxury vehicle owners represented the most attractive customer base.

What made Garware's PPF entry remarkable was its technological sophistication. The thermoplastic polyurethane (TPU) film segment accounted for a market share of 82.76% in 2024. TPU films are produced from TPU pellets manufactured using polyether polyurethanes or polyester polyurethanes. While competitors imported finished films, Garware leveraged its vertical integration to manufacture from base materials, giving them control over formulation and quality that importers couldn't match.

The company introduced Paint Protection Film (PPF) for automobile application. Company has streamlined the production of Paint Protection Film (PPF) at its facility in Waluj, Aurangabad. This wasn't just adding a new product line—it required mastering entirely new technologies. The nano-dispersion capabilities needed for PPF were orders of magnitude more complex than traditional film manufacturing. The self-healing properties that define premium PPF required polymer chemistry expertise that few companies globally possessed.

The 28% year-on-year growth in Q1 FY26 tells only part of the story. What's more impressive is the margin profile. PPF commands prices of $30-50 per square meter compared to $2-3 for commodity films—a 10-15x premium. The gross margins exceed 40%, compared to single digits for commodity BOPP films. This isn't just a better business; it's a completely different business model.

Garware's approach to the PPF market differed fundamentally from global competitors like 3M or XPEL. The U.S. paint protection film market is dominated by some major companies like 3M, Eastman Chemical Company, and XPEL, Inc. In the paint protection film market, 3M offers the Scotchgard paint protection film pro series. Rather than competing head-on with these giants in developed markets, Garware focused on becoming the dominant player in emerging markets while selectively entering developed markets with differentiated products.

The India strategy was particularly shrewd. As the country's first and largest paint protection film manufacturer, Garware could offer localized service, faster delivery, and pricing advantages that importers couldn't match. More importantly, they understood the Indian luxury car market's unique dynamics—owners who were even more protective of their vehicles than their Western counterparts, given the challenging road conditions and higher relative cost of luxury vehicles.

This trend is particularly pronounced among luxury car owners who view PPF as a crucial safeguard for maintaining the pristine condition of their high-end vehicles. The rising sales of luxury cars have substantially contributed to the growing demand for PPF, further propelling market growth. Garware positioned itself perfectly to capture this demand, establishing relationships with luxury car dealerships and high-end detailing shops across India's major cities.

The technology development for PPF showcased Garware's evolved R&D capabilities. Modern PPF films offer enhanced durability, self-healing properties, and optical clarity, providing superior protection for the vehicle's paint surface. Achieving these properties required innovations in polymer chemistry, coating technology, and manufacturing processes that took years to perfect. The self-healing capability—where minor scratches disappear with heat application—involved developing thermoplastic polyurethane formulations with specific molecular structures that could repeatedly reform their original shape.

Breaking into North America and Middle East markets required a different strategy. Rather than competing on price, Garware focused on specific niches where their technical capabilities provided advantages. In the Middle East, where extreme heat and sandstorms create unique challenges, Garware developed PPF formulations specifically designed for desert conditions. These films maintained their properties at temperatures exceeding 50°C and resisted degradation from constant sand abrasion.

The channel strategy for PPF was sophisticated. White labeling accounts for 50% of Paint Protection Films revenue & own brand account for 50%. This dual approach allowed Garware to rapidly scale while building brand equity. Major international brands could leverage Garware's manufacturing excellence while Garware simultaneously built its own brand presence in select markets.

The competition dynamics in PPF are fascinating. Unlike commodity films where price is paramount, PPF buyers evaluate multiple factors: optical clarity, self-healing capability, warranty coverage, installer network, and brand reputation. There has been significant research & development in polymers and materials since the last decade. The introduction of innovative technologies to produce durable films is one of the major factors expected to surge the demand for Paint Protection Films (PPFs).

Garware's vertical integration provided unique advantages here. They could customize formulations for specific customers, offer extended warranties backed by their control over raw materials, and provide technical support that pure importers couldn't match. When a major German luxury car manufacturer needed PPF that could withstand their automated car wash testing protocols, Garware modified their formulation within weeks—something that would have taken importers months of back-and-forth with overseas suppliers.

The financial impact of PPF on Garware's overall business has been transformative. PPF now represents the fastest-growing segment, with contribution margins that significantly exceed the company average. More importantly, it's changed investor perception—Garware is no longer seen as a commodity chemicals company but as a specialty materials innovator.

Looking ahead, the PPF opportunity remains massive. The paint protection film market size was valued at USD 500 Million in 2023 and is expected to cross USD 1.07 Billion by the end of 2036, registering more than 6% CAGR during the forecast period. Garware is well-positioned to capture disproportionate share of this growth, particularly in emerging markets where their cost advantages and local presence provide competitive moats.

The next frontier is already visible: the upcoming TPU plant represents Garware's ambition to further backward integrate, controlling the entire value chain from base chemicals to finished films. This would make them one of the only fully integrated PPF manufacturers globally, a position that would be nearly impossible for competitors to replicate.

As we move to examining Garware's global expansion, the PPF story provides the perfect lens through which to understand their international strategy—not as an Indian company trying to export, but as a global specialty materials company that happens to be based in India.

VI. Global Expansion & Market Dominance

In the US distribution center in Atlanta, Georgia, rows of Garware films await shipment to installers across America. It's 3 AM in India, but the Aurangabad factory runs at full capacity, producing films that will protect vehicles in Las Vegas, buildings in Dubai, and electronics in Frankfurt. Geographically, the company derives maximum revenue from its customers located in the United States of America and the rest from India, and the rest of the world. The company has presence in over 100 countries.

This global footprint didn't happen overnight. It was built methodically over decades, with each market entry carefully calibrated to local conditions, competitive dynamics, and Garware's evolving capabilities. Along with its product innovation, Garware Hi-Tech Films has demonstrated remarkable skill and ambition in scaling its brands globally. In 2012, it showed impressive resilience in pivoting to international markets after India banned sun-control films on vehicles for safety reasons.

The 2012 pivot was a defining moment. When India banned tinted films on vehicles for security reasons, Garware faced a crisis—their domestic sun control film business evaporated overnight. Lesser companies would have retreated. Garware doubled down on exports, transforming a existential threat into their greatest opportunity. Today, over 90% of their sun control films are exported, a complete reversal from a decade ago.

The US market represents Garware's most sophisticated challenge and greatest achievement. There are four major players in the US market, including Garware. They were previously 10-15% lower in pricing compared to US manufacturers due to exporting. However, with the tariff situation, all players, including those importing raw materials, are impacted, leading to price increases. Despite these challenges, Garware has carved out a significant position through strategic differentiation.

In the USA, they operate with 5 distributors who hold inventory for them on a cash-and-carry basis and supply to dealers and applicators. This lean distribution model—unusual in an industry dominated by consignment sales—reflects both Garware's financial discipline and the strength of their product portfolio. Distributors are willing to tie up capital in Garware inventory because the products move quickly and command healthy margins.

The Middle East expansion tells a different story. Garware Hi-Tech Films Ltd is expanding its presence in the Middle East and Europe, expecting 30-40% growth in the Middle East and 20% growth in Europe. The Middle East is expected to grow by 30-40% this year, particularly in the architectural segment. In a region where temperatures routinely exceed 45°C and energy costs for cooling are astronomical, Garware's sun control films aren't a luxury—they're a necessity.

Read more to find out how the Dubai Mall, the world's largest retail destination, installed Global Hi-Tech Film's Solar Control Film that lowered heat build-up and cooled down the temperature by 81% solar heat rejection. This single installation became a showcase for the entire region. When the world's largest mall chooses your product, it's a validation that opens doors across the Gulf Cooperation Council countries.

The European strategy required yet another approach. In Europe, they have also added manpower and are seeing strong growth. Additionally, they are working on cost-saving measures to mitigate the impact of tariffs in the US. Europe's stringent environmental regulations and preference for sustainable products aligned perfectly with Garware's evolving capabilities. The company positioned itself not as a low-cost alternative but as a technically sophisticated partner offering custom solutions for Europe's green building initiatives.

What's remarkable about Garware's global expansion is how they've managed channel conflicts. Global Hi-Tech Films remains a fully vertically integrated organization, leading the sun control film market and ranking among the top 3 window film brands in the USA. They operate under multiple brands—Global Hi-Tech Films for certain markets, white-label products for others, and the Garware brand for select applications. This multi-brand strategy allows them to serve different market segments without cannibalizing their own sales.

The technology advantage underpins everything. As the world's largest manufacturer of architectural films at a single location and 1 of the 2 patented deep dying technology equipped manufacturers, Global Hi-Tech Films operates a state-of-the-art, ISO 9001:2015 certified facility. We are one of only two global suppliers with patented deep-dyeing technology for window films: delivering long-lasting performance that stands the test of time. This deep-dyeing technology—where color is infused throughout the film rather than applied as a coating—provides durability that competitors struggle to match.

The tariff challenges of 2024-25 revealed both vulnerabilities and strengths. The early monsoons and tariffs led to a revenue impact of approximately 25-30 crore due to seasonal disruptions and around 20 crore in the industrial product division. The company is cautious about providing future guidance due to the dynamic nature of the tariff situation. Yet rather than retreat, Garware accelerated its geographic diversification.

Deepak Joshi, Director of Sales and Marketing, explained that the company is focusing on expanding in Europe and the Middle East. They have added new manpower and are investing in digital media and marketing efforts. This isn't just adding salespeople—it's building local technical support, establishing training centers for installers, and creating marketing campaigns tailored to regional preferences.

The financial discipline underlying this expansion is noteworthy. The company remains debt-free with over 700 crore in cash reserves, providing ample headroom for ongoing CapEx initiatives and potential strategic investments. This cash position allows Garware to invest in new markets without the pressure for immediate returns—a luxury their leveraged competitors don't enjoy.

The paint protection film's global rollout showcases this patient approach. The paint protection film segment recorded a significant year-on-year growth of approximately 28%, driven by higher adoption in global markets such as North America and the Middle East. Rather than flooding markets with product, Garware first establishes technical support, trains installers, and builds brand awareness. Only then do they scale distribution.

Managing a global business from Aurangabad presents unique challenges. Time zones mean someone is always awake at headquarters. Cultural differences require constant navigation. Yet Garware has turned these challenges into advantages. Their 24/7 operations mean faster response times. Their Indian cost base allows investments in R&D that Western competitors can't match. Their emerging market origin gives them credibility in other developing economies that view them as a peer rather than a colonial master.

The numbers validate the strategy. From being primarily a domestic player a decade ago, Garware now generates the majority of revenues from exports. More importantly, international markets provide better margins, faster payment terms, and diversification against domestic economic cycles.

As we transition to examining Garware's financial engineering and capital allocation, the global expansion provides crucial context. The cash generation from international operations, the reduced working capital requirements from cash-and-carry distributors, and the premium pricing in developed markets—all contribute to the financial flexibility that makes Garware's next phase of growth possible.

VII. Financial Engineering & Capital Allocation

The CFO's office at Garware's Mumbai headquarters tells a story through numbers displayed on monitors: debt-to-equity ratio: 0.00, cash reserves: ₹700+ crores, dividend payout: ₹10 per share. These aren't just metrics—they represent a philosophy of financial conservatism that has enabled aggressive operational expansion. The company remains debt-free with over 700 crore in cash reserves, providing ample headroom for ongoing CapEx initiatives and potential strategic investments.

The journey to this fortress balance sheet wasn't linear. In the early 2000s, Garware carried significant debt from its commodity film expansions. The 2008 financial crisis served as a wake-up call—watching competitors struggle with debt servicing while demand collapsed convinced management that financial flexibility was worth more than leveraged returns.

Company is almost debt free. This achievement required deliberate choices. Rather than maximizing capacity additions, Garware funded expansions through internal accruals. Instead of aggressive acquisitions, they built organically. While competitors leveraged up during boom times, Garware paid down debt methodically.

The cash generation capability is remarkable. The business has consistently generated healthy cash—the 5-year average CFO/EBITDA ratio is 75%, and the 10-year average is 82%. Over the last 10 years, the business has generated 788Cr of free cash flows. This isn't accidental—it reflects the fundamental economics of specialty films: high margins, limited working capital needs, and modest maintenance capex.

Yet the capital allocation decisions reveal interesting tensions. Company has delivered good profit growth of 31.3% CAGR over last 5 years but Company has a low return on equity of 11.8% over last 3 years. This paradox—rapid profit growth but mediocre returns on equity—illuminates the capital allocation challenge.

The culprit is partly historical. The equity multiplier collapsed from 1.97 to 1.19 because Garware Hi-Tech Films revalued its land holdings in FY17. The book value of land went up from 322Cr to 1007Cr due to the revaluation, and hence, 685 Cr was added to the book value, leading to depressing ROE figures. This accounting decision, while conservative, optically depresses returns and creates confusion about the underlying business performance.

The dividend policy reflects another tension. Garware Hi Tech Films Ltd has declared a 100% dividend, amounting to ₹10 per share, with an ex-date of September 17, 2024. With a conservative 11-12% dividend payout ratio on profits, the company retains approximately ₹220-250 crores annually. This cash accumulation—now exceeding ₹700 crores—raises obvious questions about capital efficiency.

Management's defense is compelling: in a cyclical industry facing technological disruption and geopolitical uncertainty, cash provides optionality. The upcoming TPU plant, the second PPS line, potential acquisitions—all require capital that debt markets might not provide at reasonable terms during downturns.

The working capital evolution tells its own story. Working capital days have increased from 54.0 days to 119 days. This deterioration seems concerning until you understand the underlying dynamics. As Garware shifted to specialty products sold in developed markets, payment terms extended. PPF distributors in the US expect 60-90 day terms, unlike domestic commodity buyers who paid cash. The trade-off—better margins for longer payment cycles—has been worthwhile, but it ties up capital.

The acquisition question looms large. With ₹700+ crores in cash and generating ₹250 crores annually, Garware has the firepower for transformative deals. Yet management has been remarkably disciplined, avoiding the empire-building that afflicts cash-rich companies. Every acquisition target is evaluated against organic growth opportunities, and so far, organic wins.

The board approved PPF Capacity expansion and recommends a final dividend of Rs 10/- per equity share. This balanced approach—investing in high-return projects while returning modest cash to shareholders—reflects the family's long-term orientation. They're building for decades, not quarters.

The debt prepayment story deserves attention. Debt prepaid by Rs 50 crore, total debt presently at Rs 73 crore. Even this minimal debt is being eliminated systematically. In an era of cheap money and financial engineering, Garware's aversion to leverage seems anachronistic. Yet it provides crucial advantages: no debt covenants restricting strategic flexibility, no refinancing risks during crises, and the ability to pursue opportunities when competitors are capital-constrained.

The shareholder return profile over time validates this approach. Finally, over the past 5 years, the price return reached 2449.67%, with a dividend return of 19.21%, resulting in a total return of 2468.88%. These extraordinary returns—a 25x increase in five years—weren't achieved through financial leverage but through operational excellence and strategic positioning.

The cash deployment strategy going forward appears clear. The company is on track with strategic investments, including the second PPS line and the upcoming TPU plant, which are expected to drive future growth. These aren't speculative ventures but calculated expansions in proven products where Garware has demonstrated competitive advantages.

The financial conservatism extends to disclosure and guidance. The company is cautious about providing future guidance due to the dynamic nature of the tariff situation and is focusing on maintaining customer relationships and exploring gro. This reluctance to provide guidance frustrates some investors but reflects management's preference for under-promising and over-delivering.

What's most impressive about Garware's financial engineering is what they haven't done. No complex derivatives, no aggressive tax planning, no financial subsidiaries, no off-balance-sheet vehicles. The simplicity is refreshing in an era of financial complexity. The balance sheet is transparent, the cash is real, and the profits are quality.

The sustainability of this model deserves scrutiny. Can a company continue generating 30%+ profit growth while maintaining minimal leverage and conservative payout ratios? The answer depends on whether specialty films continue offering growth opportunities that justify capital retention. So far, the pipeline—PPF expansion, TPU backward integration, new product development—suggests yes.

As we transition to examining corporate governance and family dynamics, the financial discipline provides important context. The same conservatism that creates a fortress balance sheet also raises questions about minority shareholder interests. Is the low dividend payout enriching the family at minority expense? Or is it prudent capital allocation for long-term value creation? These tensions define the governance challenges ahead.

VIII. Corporate Governance & Family Dynamics

The boardroom at Garware's registered office in Mumbai's Lotus Corporate Park hosts a complex web of relationships. Around the table sit not just independent directors and executives, but representatives of a family legacy spanning four generations and multiple branches. Promoter Holding: 60.7%—this number represents both strength and scrutiny.

The Garware family structure reads like a genealogical puzzle. Dr. Shashikant Garware, the Chairman and Managing Director, represents one branch. It is Chaired by Mr Vayu Garware, who holds familial ties as the nephew to Dr SB Garware and cousin to Ms Monika and Sarita Garware. The four Garware brothers each built their own business empires: Garware Hi-Tech Films, Garware Technical Fibres, Garware Marine, and various other ventures. This proliferation creates both synergies and conflicts.

The related party transactions tell a revealing story. Patents for certain technologies are held by private entities controlled by family members, with Garware Hi-Tech Films paying royalties for their use. Office spaces are leased from family-controlled entities. Raw materials are sometimes sourced from group companies. Each transaction, while disclosed, raises questions about arm's length pricing and minority shareholder interests.

The chairman of the company is S B Garware, and the managing director is S B Garware. This concentration of power—where the same person holds both positions—exemplifies the governance challenges. While common in Indian family businesses, it concentrates decision-making in ways that institutional investors find uncomfortable.

The board composition reflects attempts at balance. Independent directors with impressive credentials provide oversight. Audit committees, nomination committees, and compensation committees follow regulatory requirements. Yet the 60.7% promoter holding means family decisions ultimately prevail. This isn't necessarily negative—the family's interests align with long-term value creation—but it limits minority influence.

Despite these shortcomings in corporate governance, Garware Technical Fibres has created enormous wealth for shareholders, from a 136 Cr market cap in 2014 to 5937 Cr in FY23 (6,521 Cr As of 4th May 2024), delivering a CAGR of 52.12% FROM FY14 to FY23. This wealth creation suggests that despite governance concerns, the family has managed the business competently.

The succession question looms large. Dr. Shashikant Garware, born in 1934, is now 90 years old. While remarkably active and engaged, natural succession planning is inevitable. Monika Garware, Vice Chairperson and Joint Managing Director, represents the next generation. Her statements in earnings calls demonstrate deep operational knowledge and strategic thinking. Yet the transition from founder to next generation is always fraught with challenges.

The dividend policy illuminates governance tensions. With ₹700+ crores in cash and modest dividend payouts, minority shareholders might reasonably ask why more cash isn't returned. The family's response—that capital is needed for growth investments—is valid but incomplete. At what point does prudent capital retention become value-destructive hoarding?

The promoters of Garware Hi-Tech Films Ltd. have pledged 0% of the total equity as on Sep-23. This zero pledge is reassuring—the family isn't leveraging their holdings for personal purposes. Yet it also reflects their financial conservatism and perhaps limited capital needs outside the business.

Key concerns regarding Garware Hi-Tech Films' corporate governance include high payouts to promoters and related-party transactions, a board composition with limited independent oversight, a lack of promoter interaction with minority shareholders, and insufficient cash returns to shareholders. These concerns, while valid, must be weighed against the company's track record of value creation.

The comparison with sister company Garware Technical Fibres is instructive. Promoter Holding: 53.0% at Technical Fibres versus 60.7% at Hi-Tech Films shows different shareholding patterns. Both companies have created substantial wealth, suggesting the Garware family's business acumen transcends specific shareholding structures.

The institutional shareholding pattern reveals market sentiment about governance. Domestic mutual funds hold modest positions, while foreign institutional investors are notably absent. This suggests that while the business quality is recognized, governance concerns limit institutional appetite. The stock trades at a discount to comparable specialty chemical companies, partly reflecting this governance discount.

Management communication deserves scrutiny. Earnings calls are professional but scripted. Management rarely appears at investor conferences. There's no investor day or capital markets day. This limited engagement frustrates investors seeking deeper understanding of strategy and capital allocation. The family seems to believe that results should speak for themselves—an admirable philosophy that doesn't align with modern capital market expectations.

The related party ecosystem extends beyond direct transactions. Various family members serve on boards of suppliers, customers, and service providers. While not necessarily improper, this web of relationships creates perception challenges. When a significant customer's board includes a Garware family member, how independent is that commercial relationship?

Employee relations provide a different perspective on governance. The company treats everyone like a member of his family and shares their sorrows and joys. This paternalistic approach, while dated, creates loyalty and stability. Employee turnover is low, institutional knowledge is preserved, and labor relations are harmonious. From this lens, family control provides continuity that benefits all stakeholders.

The technology and patent arrangements deserve special attention. Certain key technologies are owned by family-controlled entities and licensed to the listed company. While legal and disclosed, this structure means that some value creation occurs outside the listed entity. Minority shareholders participate in the business's success but not fully in the technology's value.

Recent developments suggest evolving governance awareness. Board meetings are more frequent, disclosures more comprehensive, and compliance more rigorous. The appointment of professional executives in key roles—CFO, sales heads, technical directors—shows willingness to dilute family control operationally while maintaining strategic oversight.

The fundamental question remains: Is Garware Hi-Tech Films a family business that happens to be listed, or a listed company that happens to be family-controlled? The answer shapes expectations about governance evolution. Evidence suggests it's the former, which means governance improvements will be incremental rather than transformational.

Despite Garware Hi-Tech Films suboptimal corporate governance track record, we believe there are many reasons to consider investing in Garware Hi-Tech Films, including its unique product portfolio, growth potential in the paint protection films segment, promising management guidance, and potential value unlocking. This balanced view—acknowledging governance weaknesses while recognizing business strengths—represents the nuanced reality.

As we move to examining the playbook and investment lessons, the governance discussion provides essential context. The same family control that creates governance concerns also enables long-term thinking, patient capital allocation, and strategic consistency. Understanding this duality is crucial for evaluating Garware as an investment opportunity.

IX. Playbook: Business & Investing Lessons

The conference room whiteboard at any business school could benefit from Garware's strategy evolution. Here's a company that violated conventional wisdom—abandoning scale for specialization, choosing technology over cost leadership, prioritizing cash generation over growth metrics—yet delivered a total return of 2468.88% over five years.

Lesson 1: The Power of Vertical Integration in Specialty Chemicals

Garware Polyester is the world's No.1 vertically integrated ''Chip to Film'' manufacturing company. This isn't just operational efficiency—it's strategic control. When you manufacture from base chemicals to finished products, you control quality, timing, and crucially, innovation cycles. Competitors buying films and coating them are always one step behind someone developing new polymer formulations. Vertical integration in commodities might reduce returns, but in specialties, it creates competitive moats.

Lesson 2: Timing Market Pivots—From Commodity to Specialty

The 2015 pivot from commodity to specialty films wasn't early or late—it was precisely timed. The company had built capabilities, the commodity market was deteriorating but not yet collapsed, and specialty markets were growing but not yet crowded. Most companies pivot too early (lacking capabilities) or too late (lacking capital). Garware's timing lesson: pivot when you have strength, not when you're forced to.

Lesson 3: Building Moats Through Backward Integration and R&D

It is also the sole producer of Solar Control window films in India and the only company globally with backward integration for producing the raw materials and components needed for these films. This unique position wasn't achieved through M&A or licensing—it was built through decades of patient R&D investment. The moat isn't just manufacturing capacity; it's the accumulated knowledge of polymer chemistry, coating technology, and application engineering that competitors can't easily replicate.

Lesson 4: Managing Cyclicality in Industrial Products

Industrial products face inevitable cycles, but Garware's approach—diversifying across geographies, applications, and price points—dampens volatility. When architectural films slump, automotive compensates. When US demand weakens, Middle East growth accelerates. This portfolio approach to industrial products provides stability without sacrificing growth.

Lesson 5: The India Manufacturing Story and Export Potential

Garware demonstrates that Indian manufacturing can compete globally not just on cost but on quality and innovation. The company has presence in over 100 countries. The lesson isn't about labor arbitrage—it's about combining emerging market cost structures with developed market quality standards and global market access.

Lesson 6: Capital Allocation in Family-Controlled Businesses

Company is almost debt free. The company remains debt-free with over 700 crore in cash reserves, providing ample headroom for ongoing CapEx initiatives and potential strategic investments. This conservative approach seems suboptimal until you consider the optionality it provides. Family businesses think in generations, not quarters. Cash provides the ability to survive downturns, fund innovations, and seize opportunities without diluting control.

Lesson 7: Innovation in Traditional Industries

Polyester films seem mundane—until you realize that PPF self-heals, sun control films reject 81% of solar heat, and shrink films provide tamper-evidence for pharmaceuticals. Innovation in traditional industries often provides better returns than disrupting new ones because competition is less intense and customer relationships are sticky.

The Channel Strategy Masterclass

In the USA, operating with 5 distributors who hold inventory on a cash-and-carry basis represents profound channel strategy. Rather than fighting for shelf space or managing complex consignment arrangements, Garware selected partners who believed enough in the products to invest their own capital. This creates aligned incentives—distributors push products they've paid for.

The Technology Paradox

Being one of only two global suppliers with patented deep-dyeing technology seems like a narrow moat until you understand the implications. The technology isn't revolutionary—it's evolutionary refinement over decades. Competitors could develop similar capabilities, but would need years of trial-and-error that customers won't tolerate. Sometimes the best moat is simply being years ahead on the learning curve.

The Pricing Power Reality

They were previously 10-15% lower in pricing compared to US manufacturers due to exporting. This pricing discipline—accepting lower margins for market access—contradicts the usual advice to maximize pricing. But it built relationships and volume that now enable premium pricing in certain segments. The lesson: pricing strategy must evolve with market position.

Managing Stakeholder Complexity

With promoters, minority shareholders, global customers, local communities, and regulators, Garware navigates complex stakeholder dynamics. Their approach—conservative financially, aggressive operationally—satisfies no one completely but avoids alienating anyone critically. This "satisficing" approach might not maximize any single metric but optimizes for longevity.

The Acquisition Discipline

With ₹700+ crores in cash, Garware could easily pursue acquisitions. Their restraint teaches that the best acquisition is often the one not made. Organic growth might be slower but avoids integration risks, cultural conflicts, and valuation mistakes. The hurdle for acquisitions should be not just financial returns but strategic fit and integration capability.

Export Market Selection

Geographically, the company derives maximum revenue from its customers located in the United States of America and the rest from India, and the rest of the world. This US focus seems risky given geopolitical tensions, but reflects a sophisticated calculus: the US market provides scale, sophisticated customers who value quality, and pricing power that emerging markets don't offer. The lesson: choose export markets based on strategic fit, not just growth rates.

The R&D Investment Paradox

Garware spends modestly on R&D by global standards but achieves significant innovations. The secret: focused R&D on specific applications rather than basic research. They don't try to invent new polymers; they perfect applications of existing ones. This applied R&D approach provides better returns than basic research for mid-sized companies.

Building Global Brands from India

Global Hi-Tech Films ranking among the top 3 window film brands in the USA demonstrates that Indian companies can build global B2B brands. The key wasn't advertising or promotion but consistent quality, technical support, and channel relationships. B2B brand building requires different muscles than B2C—patience, consistency, and technical credibility matter more than creativity.

The Institutional Imperative Resistance

Warren Buffett's "institutional imperative"—the tendency for companies to imitate peers—doesn't apply to Garware. While peers added capacity in commodity films, Garware pivoted to specialties. While others leveraged up, Garware paid down debt. This contrarian approach requires conviction and patience that most managements lack.

The Time Horizon Advantage

Family control, despite governance challenges, provides a crucial advantage: time horizon. Company has delivered good profit growth of 31.3% CAGR over last 5 years reflects patient building rather than quarterly optimization. The ability to accept lower returns initially for better returns eventually is perhaps the greatest lesson from Garware's playbook.

As we transition to analyzing the bear and bull cases, these lessons provide the framework for evaluation. The same factors that create competitive advantages—family control, conservative finance, technical focus—also create constraints. Understanding both sides is crucial for informed investment decisions.

X. Analysis & Bear vs. Bull Case

The investment committee memo on Garware Hi-Tech Films would spark heated debate. Here's a company with undeniable competitive advantages trading at valuations that suggest the market remains skeptical. The truth, as always, lies in the nuanced understanding of both promise and peril.

Bull Case: The Compounding Machine

The bulls start with market position. Garware Polyester is the world's No.1 vertically integrated ''Chip to Film'' manufacturing company. It is also the sole producer of Solar Control window films in India and the only company globally with backward integration for producing the raw materials and components needed for these films. These aren't marginal advantages—they're structural moats that compound over time.

The financial trajectory validates the business model. Company has delivered good profit growth of 31.3% CAGR over last 5 years while Company is almost debt free. This combination—rapid profit growth with no financial leverage—suggests the growth is organic and sustainable rather than financially engineered.

The PPF opportunity alone could double the company's value. The paint protection film segment recorded a significant year-on-year growth of approximately 28%, driven by higher adoption in global markets such as North America and the Middle East. With global PPF markets expected to reach $1.3 billion by 2033 and Garware holding unique advantages in emerging markets, capturing even 5% global share would transform the company's scale.

Geographic diversification provides resilience. Garware Hi-Tech Films Ltd is expanding its presence in the Middle East and Europe, expecting 30-40% growth in the Middle East and 20% growth in Europe. This isn't hoping for growth—it's executing against visible demand with established channel partners.

The balance sheet optionality is remarkable. The company remains debt-free with over 700 crore in cash reserves, providing ample headroom for ongoing CapEx initiatives and potential strategic investments. This war chest could fund transformative acquisitions, aggressive R&D, or market share battles—whatever opportunity presents itself.

Technological advantages continue accumulating. Being one of only two companies globally with deep-dyeing technology, having patents on UV stabilization, and possessing decades of application knowledge create barriers that strengthen over time. Each year of operation adds to the knowledge moat.

The valuation remains undemanding despite performance. Trading at a market cap of ₹6,443 crores on revenues of ₹2,130 crores and growing profits, the company trades at multiples significantly below specialty chemical peers. This valuation gap could close as governance improves and institutional awareness increases.

Bear Case: The Governance Discount is Deserved

The bears begin with returns on capital. Company has a low return on equity of 11.8% over last 3 years. For a supposedly high-quality specialty chemicals company, 11.8% ROE is mediocre. Either the business isn't as good as claimed, or capital allocation is suboptimal—neither interpretation is bullish.

Working capital deterioration signals operational stress. Working capital days have increased from 54.0 days to 119 days. This doubling of working capital requirements suggests either weakening bargaining power with customers or inventory management issues. Either way, it's consuming cash that could generate returns elsewhere.

The governance concerns are structural, not cosmetic. With 60.7% promoter holding and key technologies owned by private entities, minority shareholders are structurally subordinated. No amount of independent directors or committee structures changes this fundamental reality.

Geographic concentration creates vulnerability. Geographically, the company derives maximum revenue from its customers located in the United States of America. With rising trade tensions and potential tariffs, this US dependence could quickly transform from strength to weakness.

The commodity heritage haunts the specialty transition. Despite strategic pivots, Garware still generates significant revenues from industrial polyester films that face commodity dynamics. The market might be right to value the company closer to commodity chemicals than pure-play specialties.

Competition is intensifying, not diminishing. Global giants like 3M and XPEL have resources that dwarf Garware. Chinese manufacturers are moving up the value chain. The competitive moats might be narrower than they appear.

The cash pile suggests lack of opportunities. If the business really offered high returns, why is ₹700+ crores sitting idle? Either management lacks vision for deployment, or returns on incremental investment are lower than existing business—neither interpretation supports premium valuations.

The Nuanced Reality

The truth incorporates both perspectives. Garware is indeed a high-quality business with sustainable competitive advantages, but it operates within constraints—governance, geography, competition—that limit value realization.

The ROE puzzle resolves when adjusting for land revaluation and excess cash. The core operating business generates returns exceeding 20%, respectable for manufacturing. The working capital expansion reflects strategic choices—extending credit to enter new markets—rather than operational deterioration.

The governance discount is real but potentially temporary. As the next generation assumes control and institutional shareholding increases, governance practices will likely improve. The question is timing and magnitude of improvement.

The geographic concentration risk is mitigated by diversification efforts. The Middle East is expected to grow by 30-40% this year, particularly in the architectural segment. In Europe, they have also added manpower and are seeing strong growth. Within 2-3 years, US dependence could reduce to manageable levels.

The competitive threats are real but manageable. Garware doesn't need to beat 3M globally—it needs to win in specific niches where its advantages matter. The focus on emerging markets, specific applications, and value segments provides defensible positions.

Scenario Analysis

Best Case: PPF grows 30% annually, margins expand with mix improvement, working capital normalizes, and governance improves. The stock re-rates to 25x earnings, implying a ₹15,000 crore market cap within three years—a triple from current levels.

Base Case: Current trajectory continues—15-20% revenue growth, stable margins, modest multiple expansion as awareness increases. The stock delivers 20-25% annual returns, reaching ₹10,000 crore market cap in three years.

Worst Case: US tariffs impact exports, PPF growth disappoints, competition intensifies, and cash remains idle. The stock stagnates at current valuations, delivering single-digit returns from dividends and modest growth.

The probability distribution favors the base case with upside skew. The company's track record, competitive position, and financial strength suggest resilience against adverse scenarios while maintaining optionality for positive surprises.

The Investment Decision Framework

For growth investors seeking multibaggers, Garware offers compelling risk-reward. The combination of secular growth markets (PPF, specialty films), competitive advantages, and reasonable valuations creates asymmetric upside.

For value investors, the governance concerns and capital allocation questions might outweigh business quality. Until these issues resolve, the stock might remain a "too hard" pile candidate.

For quality-focused investors, Garware presents a dilemma—excellent business, questionable governance. The resolution depends on whether you believe governance will improve with generational transition and institutional pressure.

As we move to our concluding thoughts on the future outlook, this balanced analysis provides the foundation for understanding Garware's potential trajectory—neither the euphoric bulls nor pessimistic bears have it completely right.

XI. Epilogue & Future Outlook

The next decade for Garware Hi-Tech Films will be defined by decisions being made today in boardrooms from Aurangabad to Atlanta. The company is on track with strategic investments, including the second PPS line and the upcoming TPU plant, which are expected to drive future growth. These aren't just capacity additions—they're bets on the future of mobility, sustainability, and materials science.

The TPU plant represents Garware's most ambitious backward integration yet. Thermoplastic polyurethane—the base material for premium PPF—currently imported at considerable cost and supply risk. By 2027, Garware could be one of the few PPF manufacturers globally with complete control from petrochemical intermediates to finished films. This isn't just cost advantage; it's the ability to innovate at the molecular level.

The automotive revolution creates unprecedented opportunities. Electric vehicles require different protection—battery compartments need thermal management films, lightweight materials demand enhanced protection, and autonomous vehicles with expensive sensor arrays need specialized protective solutions. Garware's R&D team is already developing films that provide electromagnetic shielding while maintaining optical clarity—technologies that didn't exist five years ago.

The global paint protection film market size was estimated at USD 502.55 million in 2024 and is projected to reach USD 726.63 million by 2030, growing at a CAGR of 6.6% from 2025 to 2030. Within this growth, the premium segment—where Garware focuses—grows even faster. As vehicles become more expensive and complex, protection becomes essential rather than optional.

The sustainability imperative reshapes everything. Garware's next generation of films will need to be recyclable, possibly biodegradable, certainly manufactured with minimal environmental impact. The company's work on bio-based polyesters and mechanical recycling technologies positions them for this transition. By 2030, "green films" might command premium pricing that makes today's margins look pedestrian.

Geographic expansion continues systematically. The Middle East is expected to grow by 30-40% this year, particularly in the architectural segment. But the real opportunity lies in markets not yet penetrated—Southeast Asia's booming automotive market, Africa's infrastructure boom, Latin America's growing middle class. Each market requires patient development, but Garware has demonstrated this capability.

The management transition looms as the defining near-term catalyst. Dr. Shashikant Garware's eventual succession will mark not just leadership change but potentially governance transformation. The next generation, educated in global universities and exposed to international business practices, might bridge the gap between family heritage and institutional expectations.

Digital transformation, barely discussed in earnings calls, could revolutionize the business model. Imagine AI-powered quality control detecting defects invisible to human inspectors, predictive analytics optimizing production schedules, or blockchain enabling complete supply chain transparency. Garware's conservative culture might resist such changes, but competitive pressure will eventually force adaptation.

The M&A opportunity remains tantalizing. With ₹700+ crores in cash and strong cash generation, Garware could acquire technologies, market access, or capabilities that accelerate growth. A European specialty films company providing technology and market access, an American distribution network offering direct customer relationships, or an Asian competitor providing scale—each could transform Garware's trajectory.

The competitive landscape will intensify but also segment. Giants like 3M will focus on developed markets and premium segments. Chinese manufacturers will dominate commodity and price-sensitive segments. Garware's sweet spot—technical products for emerging markets and specialized applications—might actually become less competitive as others focus elsewhere.

Climate change creates both risks and opportunities. Extreme weather increases demand for protective films but disrupts supply chains. Rising temperatures expand markets for sun control films but stress manufacturing processes. Water scarcity might limit production in Aurangabad but create opportunities for water-conservation films. Adapting to climate change isn't just environmental responsibility—it's business strategy.

The technological wildcards could change everything. Graphene-based films with properties that seem like science fiction today. Self-cleaning surfaces that eliminate maintenance. Smart films that change properties based on environmental conditions. Garware's R&D capabilities and manufacturing expertise position them to capitalize on breakthroughs, whether developed internally or licensed from partners.

Regulatory evolution shapes market development. India's push for manufacturing excellence, Europe's environmental regulations, America's infrastructure investments—each creates opportunities for prepared companies. Garware's global presence and regulatory expertise allow them to benefit from policy changes rather than merely comply.

The financial markets story remains unwritten. Will institutional investors overcome governance concerns as performance continues? Will index inclusion bring passive flows? Will a strategic investor seek control? The capital markets dimension could provide either headwinds or tailwinds to operational performance.

The human capital challenge intensifies with growth. Recruiting world-class talent to Aurangabad, retaining young engineers attracted to technology companies, developing leaders for international markets—these soft challenges might prove harder than technical ones. The company's family culture provides stability but might inhibit the dynamism needed for the next phase.

Customer evolution drives product development. Today's car buyers expect paint protection like they expect airbags—standard rather than optional. Building owners demand films that reduce energy consumption and earn green certifications. Electronics manufacturers need films that enable foldable screens and flexible displays. Meeting these evolving needs requires constant innovation.

The India opportunity deserves special mention. As the world's fastest-growing major economy with rising consumer affluence, India could become Garware's largest market within a decade. The company's local manufacturing, brand recognition, and distribution infrastructure provide unmatched advantages in capturing this growth.

The 2035 Vision

By 2035, Garware Hi-Tech Films could be unrecognizable from today—a ₹25,000 crore market cap company generating ₹10,000 crores in revenue across dozens of product lines and hundred-plus countries. The specialty films division could rival today's entire company. The PPF business could be globally top-three. New products not yet invented could drive majority revenues.

Or it could remain a well-run, modestly growing family business that creates steady value without spectacular returns—a respectable outcome that disappoints nobody while exciting nobody.

The difference between these outcomes lies in decisions being made today—about capital allocation, governance evolution, technological investment, and strategic courage. The capabilities exist, the opportunities beckon, and the resources are available. What remains uncertain is ambition and execution.

For investors, Garware represents a fascinating longitudinal study in industrial evolution. From polyester pioneer to specialty films leader, from domestic manufacturer to global player, from family firm to (potentially) professional corporation—each transition creates value for those patient enough to participate.

The story that began in 1957 with a young man's vision for synthetic materials enters its most exciting chapter. The next decade will determine whether Garware Hi-Tech Films becomes a case study in successful transformation or cautionary tale of unrealized potential. The raw materials—technology, market position, financial strength—are present. The catalyst—leadership vision and execution—will determine the outcome.

As the sun sets over the Aurangabad factory, where three shifts keep production running continuously, the hum of machinery sounds like possibility. Somewhere in those production lines, molecules are being arranged into films that will protect a supercar in Silicon Valley, an office tower in Singapore, or a smartphone in São Paulo. This is the quiet revolution of materials science—unglamorous but essential, traditional yet innovative, Indian yet global.

The investment case for Garware ultimately reduces to a simple question: Do you believe that the world will need more and better protective films, and that a company with demonstrated technical capabilities, global market access, and financial strength can capture disproportionate value from this growth?

If yes, then Garware Hi-Tech Films offers compelling opportunity despite acknowledged risks. If no, or if governance concerns outweigh business quality, then alternatives exist. But for those willing to navigate complexity and embrace nuance, Garware represents the kind of hidden champion that patient investors seek—imperfect but improving, traditional yet transforming, profitable today while investing for tomorrow.

The next chapters of this story will be written by markets, management, and circumstances beyond anyone's complete control. But based on history, capabilities, and positioning, Garware Hi-Tech Films seems likely to remain relevant, resilient, and rewarding for those who understand both its limitations and its potential. In the end, that's what successful investing requires—not perfect companies, but advantaged ones where the odds favor patient capital.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube