Grindwell Norton: The Story of India's Industrial Abrasives Pioneer

I. Introduction & Episode Roadmap

Picture this: In the heart of industrial India, where sparks fly from metal grinding against stone, where precision matters in millimeters, and where the difference between smooth and rough can determine the fate of an entire production line, stands a company that has quietly shaped the nation's manufacturing backbone for over eight decades. This is Grindwell Norton—a name that might not grace headlines, but whose products touch everything from the razor you used this morning to the silicon chips powering your smartphone.

With a market capitalization of ₹16,353 crore and annual revenues approaching ₹2,809 crore, Grindwell Norton today stands as India's undisputed leader in abrasives, ceramics, and advanced materials. But here's what makes this story remarkable: it began in 1941 in Mora, a tiny fishing village outside Mumbai, where the smell of sea salt mixed with industrial ambition, and two Parsi entrepreneurs dared to imagine they could build grinding wheels that would rival the world's best.

The question that drives our narrative today isn't just how a small factory in a fishing village became part of Saint-Gobain, the French industrial giant with a 359-year history and €47.9 billion in global sales. It's about something deeper: How does a company in a commoditized, capital-intensive industry create lasting value? How does it navigate the treacherous waters between local entrepreneurship and global ambition? And perhaps most intriguingly, what can modern founders and investors learn from a business that grinds—quite literally—its way to success?

This is a story of three distinct eras: the pioneering Parsi founders who built India's first grinding wheel factory when the country was still under British rule; the transformative Norton partnership that brought American industrial expertise to Indian shores; and finally, the Saint-Gobain acquisition that catapulted a domestic champion onto the global stage. Each transition brought its own drama, its own cast of characters, and its own lessons about building enduring industrial enterprises in emerging markets.

What you're about to discover isn't just corporate history—it's a masterclass in patient capital allocation, technology transfer, and the art of building competitive moats in seemingly commoditized industries. It's about understanding that sometimes the most boring businesses—making grinding wheels and ceramic materials—can be the most beautiful investments. And it's about recognizing that in the industrial economy, the companies that help others manufacture better often capture more value than the manufacturers themselves.

So buckle up as we journey from a fishing village to the boardrooms of Paris, from import substitution to global integration, from grinding wheels to advanced ceramics. This is the Grindwell Norton story—where friction creates value, and where the art of abrasion became a science of success.

II. The Founding Story: From Fishing Village to Factory (1941–1950s)

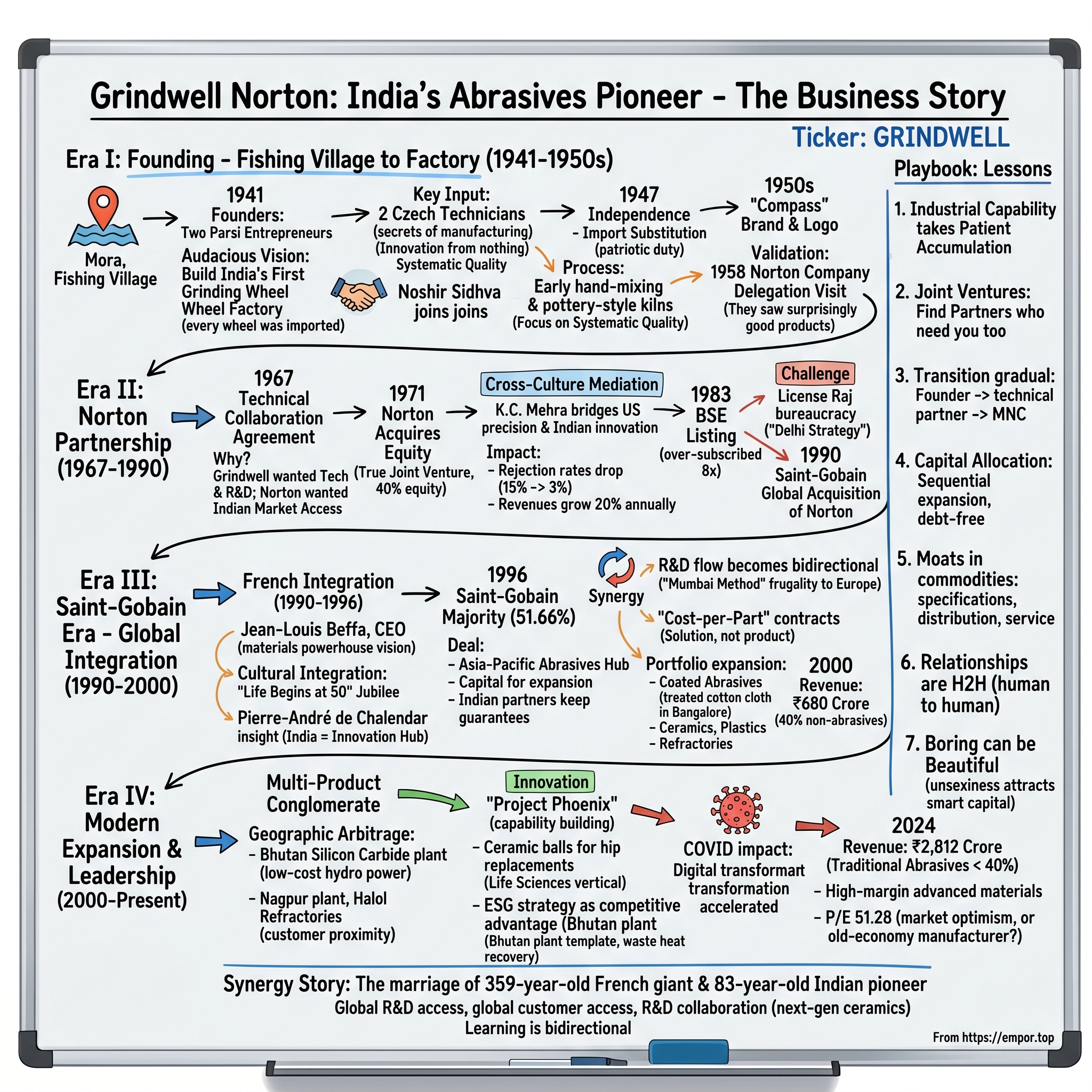

The year was 1941. While the world was engulfed in war, and India remained under the weight of colonial rule, something extraordinary was happening in Mora, a sleepy fishing village where the Arabian Sea kissed the Maharashtra coastline. Two Parsi gentlemen—whose names have been somewhat lost to corporate lore but whose vision remains etched in industrial history—stood on a patch of land that smelled more of fish and salt than industrial promise. They weren't there to fish. They were there to grind.

The Parsis, that remarkable community of Zoroastrian immigrants who had fled Persia centuries earlier, had already established themselves as India's industrial pioneers. The Tatas, the Godrejs, the Wadias—all Parsi families who understood that industrial capability was the path to prosperity. Our two founders belonged to this tradition, but their ambition was specific and audacious: they would build India's first grinding wheel factory.

Think about the timing for a moment. In 1941, every grinding wheel used in India—every single one—was imported. British workshops, railway maintenance sheds, and the nascent Indian factories all depended on abrasives shipped from Norton Company in America or Carborundum in Europe. The supply chains were stretched thin by war, prices were astronomical, and delivery times were measured in months. The market opportunity was obvious, but the technical challenge was daunting.

Enter two Czech technicians—refugees from a Europe torn apart by conflict, carrying in their heads the closely guarded secrets of abrasive manufacturing. The Parsi founders had somehow convinced these men to share their knowledge, to help build something from nothing in a fishing village that didn't even have reliable electricity. The early days were a comedy of errors and innovation: mixing clay and abrasive grains by hand, firing wheels in kilns more suited to pottery than precision tools, testing products on whatever metal scraps they could find.

Noshir Sidhva joined this motley crew shortly after, bringing not just capital but something more valuable—a systematic approach to quality that would become Grindwell's hallmark. Sidhva was obsessed with consistency. In an era when Indian manufacturing was synonymous with "good enough," he insisted that their grinding wheels match international standards. Workers recall him personally inspecting wheels, running his fingers along the surfaces, rejecting batches that others would have passed.

The post-independence period of 1947 brought both opportunity and chaos. Partition disrupted supply chains, refugee influx strained resources, but Nehru's vision of a self-reliant India created a protective cocoon for domestic industry. Import substitution wasn't just policy—it was patriotic duty. Grindwell's grinding wheels became symbols of Indian industrial capability, featured in government exhibitions, celebrated in newspapers.

By the mid-1950s, the company was ready for its first real branding moment. They launched "Compass"—a name chosen to evoke precision, direction, and reliability. The logo, a simple compass rose, appeared on grinding wheels that were slowly replacing imports in textile mills, engineering workshops, and the growing automotive sector. The Indian Railways, that great backbone of the nation, became an early anchor customer, using Compass wheels to maintain thousands of kilometers of track.

But let's not romanticize this period. The challenges were brutal. Raw materials like aluminum oxide and silicon carbide had to be imported through a maze of licenses and foreign exchange permits. The License Raj meant that expanding production required government approval that could take years. Quality control was a constant battle—Indian workers, skilled in traditional crafts, had to be retrained in industrial precision. Power cuts were frequent, monsoons flooded the factory, and competition from smuggled imports was fierce.

Yet something remarkable was happening in that factory by the sea. A culture was forming—part Parsi entrepreneurialism, part Czech technical rigor, part Indian jugaad. Workers began innovating small improvements: better ways to mix abrasives, clever jigs for wheel mounting, indigenous alternatives for imported binders. The company was learning that in abrasives, as in life, consistent pressure applied over time could shape even the hardest materials.

The real validation came from an unexpected source. In 1958, a delegation from Norton Company—the American giant whose products Grindwell was trying to replace—visited the Mora factory. They expected to find a primitive operation. Instead, they discovered wheels that, while not matching Norton's best, were surprisingly good. Good enough that Norton began to see Grindwell not as a minor irritant but as a potential partner. The seeds of what would become a transformative collaboration were planted that day, among the sound of grinding wheels and the distant crash of Arabian Sea waves.

By the end of the 1950s, Grindwell had achieved something remarkable: it had proven that India could manufacture precision industrial products. The company was producing over 1,000 tons of grinding wheels annually, had expanded beyond Compass to multiple product lines, and was even beginning to export to neighboring countries. The fishing village factory had become a symbol of industrial possibility.

But the founders knew they had reached a plateau. To truly compete, to move from import substitution to import competition, they needed something more than determination and local innovation. They needed world-class technology, systematic R&D, and access to global best practices. The stage was set for the next chapter—one that would transform Grindwell from an Indian success story into an international player.

III. The Norton Partnership Era (1967–1990)

The letter arrived on a humid Mumbai morning in 1967. It bore the letterhead of Norton Company, Worcester, Massachusetts—the undisputed world leader in abrasives, a company whose name was synonymous with grinding excellence since 1885. For Grindwell's management, huddled in their modest Mora office, this wasn't just correspondence. It was recognition.

Norton had been watching Grindwell's progress with a mixture of concern and admiration. Here was an Indian company that had not only survived without their technology but was beginning to thrive. Norton's executives, led by the visionary John Jeppson, recognized a truth that many American corporations would take decades to understand: emerging markets weren't just consumption destinations—they were innovation laboratories where constraints bred creativity.

The initial technical collaboration agreement signed in 1967 was modest in scope but revolutionary in impact. Norton would share manufacturing processes, quality control protocols, and product formulations. In return, Grindwell would pay royalties and provide Norton with a foothold in the Indian subcontinent—a market they saw growing exponentially as India industrialized.

But the real drama unfolded in the technology transfer process. Picture American engineers, accustomed to automated factories and unlimited resources, arriving at Mora to find workers hand-mixing batches and using improvised testing equipment. The culture clash was immediate and intense. Norton's team insisted on precise temperature controls; Grindwell's workers relied on experience and intuition, judging kiln temperatures by the color of the flame.

The breakthrough came through an unlikely mediator: K.C. Mehra, a young engineer who had just returned from MIT. Mehra spoke both languages—not just English and Hindi, but the language of American industrial precision and Indian pragmatic innovation. He became the bridge, translating Norton's specifications into processes that could work within Grindwell's constraints. Under his guidance, Grindwell began producing wheels that matched Norton's quality at a fraction of the cost.

By 1971, the relationship had deepened beyond technology transfer. Norton acquired an equity stake, transforming the collaboration into a true joint venture. The negotiations, conducted in Mumbai's Taj Mahal Hotel over endless cups of chai and careful diplomatic dancing, established a precedent for Indo-American industrial partnerships. Norton got 40% equity and a board presence; Grindwell got not just technology but credibility—the Norton name opened doors that had been firmly shut to an unknown Indian company.

The impact was immediate and dramatic. Product quality jumped—rejection rates fell from 15% to under 3% within two years. New product lines emerged: resin-bonded wheels for the growing automotive industry, specialized wheels for bearing manufacturers, precision wheels for the defense sector. Revenue grew at 20% annually through the 1970s, even as the Indian economy struggled with oil shocks and political instability.

The 1983 listing on the Bombay Stock Exchange marked Grindwell Norton's coming of age. The IPO was oversubscribed 8 times, with long queues of retail investors outside bank branches—a scene that would become familiar in India's equity markets. The prospectus told a compelling story: an Indo-American joint venture combining local market knowledge with global technology, positioned to benefit from India's industrial growth. The stock price doubled within six months.

But success brought new challenges. The License Raj, that Byzantine system of permits and quotas, meant that despite growing demand, Grindwell couldn't easily expand capacity. Every new production line required government approval. Importing advanced equipment needed special licenses. Even hiring foreign technicians required navigating multiple ministries. The company developed what insiders called the "Delhi strategy"—maintaining a permanent presence in the capital to navigate bureaucratic mazes.

The partnership also faced cultural tensions. Norton's American managers, accustomed to quarterly earnings pressures, pushed for aggressive growth and higher margins. Indian board members, led by the original Parsi families, emphasized long-term relationships and steady expansion. Board meetings became fascinating studies in cross-cultural negotiation, with breaks for both coffee and chai, presentations switching between American directness and Indian circumlocution.

The real test came during the 1984 Bhopal gas tragedy. While Grindwell had no connection to Union Carbide, the disaster triggered a backlash against foreign collaborations. Activists targeted joint ventures, questioning whether foreign companies were bringing obsolete or dangerous technologies to India. Grindwell had to carefully navigate public sentiment, emphasizing their safety record and local employment—over 90% of their 2,000 employees were Indian.

Through the 1980s, the joint venture found its rhythm. Norton provided regular technology updates—new bonding agents, advanced ceramic grains, computerized quality control systems. Grindwell provided market intelligence, cost innovation, and crucially, patience. While Norton's other international ventures demanded quick returns, the Indian partners understood that building industrial capability was a generation-spanning project.

The numbers tell the story: by 1990, Grindwell Norton was producing 15,000 tons of abrasives annually, had three manufacturing plants, and commanded 35% market share in organized abrasives. But more importantly, it had created an ecosystem—training hundreds of engineers, developing dozens of local suppliers, and proving that Indian manufacturing could meet global standards.

Then, in 1990, came news that would reshape everything: Saint-Gobain, the French industrial giant with roots stretching back to Louis XIV's Hall of Mirrors at Versailles, was acquiring Norton Company globally. For Grindwell Norton's Indian shareholders, this raised existential questions. Would a French conglomerate understand Indian market dynamics? Would they maintain Norton's commitment to technology transfer? Would the company become just another subsidiary in a vast global empire?

The answers would unfold in the next chapter, but one thing was clear: Grindwell Norton's journey from technical collaboration to joint venture had created something unique—an Indian company with global standards, a perfect platform for even greater ambitions.

IV. The Saint-Gobain Acquisition: A New Chapter (1990–1996)

The fax machine in Grindwell Norton's Mumbai headquarters wouldn't stop buzzing on that September morning in 1990. Message after message arrived from Worcester, Paris, and New York, all carrying the same momentous news: Saint-Gobain, the 325-year-old French conglomerate, had acquired Norton Company worldwide for $1.9 billion. In boardrooms from Boston to Bangalore, executives scrambled to understand what this meant. For Grindwell Norton, sitting 7,000 miles from Paris, the implications were particularly profound.

Jean-Louis Beffa, Saint-Gobain's legendary CEO, had orchestrated the Norton acquisition as part of his grand vision to transform the French company from a glass manufacturer into a global materials powerhouse. Beffa, an engineer-turned-strategist who spoke in algebraic metaphors and thought in decades, saw abrasives as essential to his portfolio theory of industrial materials. But India? That was uncharted territory for a company whose idea of exotic was a factory in Belgium.

The first Saint-Gobain delegation to visit Mora in early 1991 was a study in cultural contrasts. French executives in perfectly pressed suits stepped out of air-conditioned cars into Mumbai's crushing humidity, then traveled to a factory where workers still began their day with a prayer to Lord Ganesha, the remover of obstacles. The French were polite but puzzled—why was there a temple inside an industrial facility? Why did production schedules accommodate religious festivals? Why did the canteen serve only vegetarian food on Tuesdays?

But beneath the cultural differences, the French recognized something remarkable. Grindwell Norton's cost structure was revolutionary—they were producing quality comparable to European standards at 40% of the cost. The secret wasn't just cheap labor; it was frugal innovation. Where European plants used expensive synthetic diamonds, Grindwell had developed techniques using natural corundum. Where Western factories required climate control, Indian engineers had designed products that remained stable despite temperature swings.

The integration period from 1990 to 1996 became a delicate dance. Saint-Gobain initially maintained Norton's hands-off approach, but French executives gradually began appearing in Indian board meetings, bringing with them a different management philosophy. Where Americans focused on quarterly numbers, the French thought in five-year plans. Where Norton emphasized competition, Saint-Gobain stressed "co-opetition"—collaborating with competitors when it made strategic sense.

The real transformation began in 1994 when Pierre-André de Chalendar, a young French executive who would later become Saint-Gobain's CEO, spent three months in India. Instead of staying in five-star hotels, he rented a modest apartment in Mumbai, took local trains, and spent weeks on the factory floor. His report back to Paris was revolutionary: India wasn't just a low-cost manufacturing base—it was an innovation hub where constraints forced creativity.

This insight triggered Saint-Gobain's decision to increase its stake in 1996, making Grindwell Norton its first majority-owned subsidiary in India. The negotiation was a masterclass in cross-cultural dealmaking. The Indian promoters, led by the aging but sharp Noshir Sidhva's successors, wanted guarantees: no factory closures, no mass layoffs, continued investment in R&D. The French wanted control: majority board seats, integrated financial systems, global supply chain integration.

The final deal, hammered out over a marathon 72-hour session at the Oberoi Hotel, gave both sides what they needed. Saint-Gobain acquired 51.66% equity—enough for control but not so much that Indian partners felt marginalized. The French committed ₹100 crore for modernization and expansion. Most importantly, they agreed to make Grindwell Norton their Asia-Pacific hub for abrasives—a decision that would transform the company's trajectory.

The cultural integration that followed was fascinating to observe. French management techniques—the famous "tableau de bord" (dashboard) system of metrics, the emphasis on long-term planning, the focus on technical excellence—merged with Indian practices. The result was unique: a company that conducted board meetings in English with French strategic frameworks and Indian execution styles.

Saint-Gobain brought more than just capital and technology. They brought access to global customers—automotive giants like Renault and Peugeot, aerospace companies like Airbus, construction majors like Vinci. Suddenly, Grindwell Norton wasn't just competing for Indian Railways contracts; they were bidding for Boeing supply agreements. The validation was powerful: if Saint-Gobain, with its 300-year reputation, trusted Grindwell Norton quality, who could doubt it?

But the acquisition also brought challenges. French labor laws and Indian labor realities collided—Saint-Gobain's global policies on overtime, safety standards, and environmental compliance were far stricter than Indian norms. Implementation required delicate negotiation with unions, significant investment in safety equipment, and extensive training programs. The company lost some cost advantage but gained something more valuable: the ability to serve global customers who demanded international standards.

The technology transfer under Saint-Gobain was different from the Norton era. Where Norton had shared manufacturing processes, Saint-Gobain opened its entire R&D ecosystem. Indian engineers were sent to French research centers, working on next-generation ceramic abrasives and advanced bonding systems. The knowledge flow became bidirectional—French scientists were amazed by Indian techniques for handling material inconsistency, methods developed out of necessity but valuable for emerging market applications.

By the end of 1996, Grindwell Norton was a transformed entity. Revenue had grown to ₹350 crore, exports comprised 15% of sales, and the company was no longer just an abrasives manufacturer—it was becoming an advanced materials company. The fishing village factory had become part of a global industrial empire, but remarkably, it had retained its Indian soul.

The Saint-Gobain acquisition proved that globalization didn't have to mean homogenization. It was possible to be globally competitive while remaining locally rooted, to adopt international best practices while preserving indigenous innovations. This balance would be tested in the years ahead as Grindwell Norton embarked on its most ambitious expansion yet.

V. The Golden Jubilee & Transformation (1991–2000)

The banner stretched across the entire factory floor: "LIFE BEGINS AT 50." It was 1991, and Grindwell Norton was celebrating its golden jubilee with a tagline that was equal parts audacious and prophetic. While most companies at 50 were settling into comfortable middle age, Grindwell Norton was preparing for its most dramatic transformation yet.

The celebration itself was quintessentially Indian-meets-global: French executives flew in on the Concorde, stopping in Dubai to pick up Arab customers. Indian classical musicians performed alongside a jazz quartet from New Orleans. The factory workers had decorated every grinding wheel with marigold garlands. But beneath the festivities, serious transformation was underway.

The new CEO, appointed jointly by Saint-Gobain and Indian board members, was Ravi Kyran—a chemical engineer from IIT Bombay who had spent a decade with Norton in America before returning to India. Kyran embodied the company's dual identity: Indian by birth, American by training, and now working for a French multinational. His first all-hands meeting set the tone: "We're not just making grinding wheels anymore. We're in the business of surface modification. Every surface in the industrial world needs our touch."

This reconceptualization wasn't just semantic. Under Kyran's leadership, Grindwell Norton began viewing abrasives not as products but as solutions. A grinding wheel wasn't just bonded particles; it was a precision tool that determined manufacturing efficiency, product quality, and ultimately, competitive advantage. This thinking led to the company's first major diversification beyond traditional abrasives.

The Bangalore facility, inaugurated in 1993, represented this new thinking. Unlike the heritage Mora plant with its industrial grit and sea-salt air, Bangalore was sleek, modern, and ambitious. The location was strategic—close to India's emerging aerospace and automotive hubs, with access to skilled engineers from the Indian Institute of Science. But what made it special was its focus: coated abrasives, a completely different technology from the bonded wheels that had built the company.

Coated abrasives—sandpaper to the layman—required different expertise. Instead of mixing and firing, the process involved coating flexible backings with precisely graded abrasive grains. The technology came from Saint-Gobain's European operations, but the implementation was uniquely Indian. Where European lines used expensive synthetic backings, the Bangalore team developed techniques using treated cotton cloth—cheaper, more environmentally friendly, and surprisingly effective.

The R&D transformation during this period was remarkable. The company established its first formal research center, moving beyond reverse engineering to genuine innovation. The breakthrough came in 1995 with the development of a new ceramic grain abrasive that combined aluminum oxide with rare earth elements. The formulation was Indian, the testing was French, and the first customer was Japanese—a perfect symbol of the company's global integration.

But the real innovation was in business model thinking. Kyran introduced "cost-per-part" contracts where Grindwell Norton didn't just sell grinding wheels but guaranteed grinding costs for manufacturers. If a customer needed to grind 1,000 crankshafts, Grindwell Norton would provide wheels, technical support, and process optimization for a fixed per-crankshaft price. This shifted the relationship from vendor to partner, from product sales to solution provision.

The product portfolio expansion during this decade was aggressive. Ceramics for high-temperature applications, entering markets traditionally dominated by Japanese companies. Performance plastics for automotive applications, leveraging Saint-Gobain's polymer expertise. Refractories for steel plants, capitalizing on India's growing steel production. Each expansion followed the same pattern: technology from Saint-Gobain, adaptation by Indian engineers, and cost innovation that made products competitive globally.

The human capital transformation was equally important. Grindwell Norton became known as the "finishing school" for Indian materials engineers. The company recruited from IITs and regional engineering colleges, then put them through an 18-month training program that included stints in France, hands-on factory experience, and customer interaction. Many would leave for higher-paying jobs, but Kyran saw this as positive: "We're seeding the entire Indian manufacturing sector with quality-conscious engineers."

The early globalization efforts were tentative but instructive. The first major export order came from an unexpected source: a Brazilian automotive manufacturer who needed grinding wheels that could handle the high silica content in Brazilian cast iron. European and American wheels wore out too quickly; Grindwell Norton's wheels, designed for Indian conditions where material quality was inconsistent, performed perfectly. It was a lesson in reverse innovation—solutions developed for emerging market constraints finding applications globally.

The decade also saw digital transformation, though the term didn't exist yet. Grindwell Norton was among the first Indian manufacturers to implement ERP systems, connecting inventory management in Mora with production planning in Bangalore and sales forecasting in Mumbai. The implementation was painful—workers accustomed to handwritten logs had to learn computers, and the system crashed repeatedly in its first year. But by 2000, the company had real-time visibility across operations, a capability that would prove crucial for global integration.

The financial performance validated the transformation strategy. Revenue grew from ₹350 crore in 1996 to ₹680 crore in 2000. More importantly, the revenue mix had shifted—traditional grinding wheels now comprised only 60% of sales, with advanced materials and technical ceramics contributing meaningful growth. EBITDA margins improved from 12% to 18%, driven by higher-value products and operational efficiency.

But perhaps the most important achievement was cultural. By 2000, Grindwell Norton had successfully navigated the transition from family-driven company to professionally managed corporation, from domestic player to global participant, from product manufacturer to solution provider. The golden jubilee tagline had proven prescient—at 50, the company's life had indeed just begun.

The stage was set for the next phase: aggressive geographic expansion and building a manufacturing network that would make Grindwell Norton not just an Indian success story but a global player in advanced materials.

VI. The Expansion Era: Geographic & Product Diversification (2000–2015)

The helicopter circled the narrow valley near Phuentsholing, where Bhutan meets India, searching for a landing spot among the Himalayan foothills. Inside, Grindwell Norton's expansion team pressed against windows, looking at what would become their most audacious project yet: a silicon carbide plant powered by Bhutanese hydroelectricity, built at 7,000 feet altitude, in a country with no industrial base. It was 2007, and Grindwell Norton was betting that geographic expansion could create competitive advantages that no amount of operational improvement could match.

The 2000s began with a different kind of expansion. The Nagpur plant, operational since 1997, had already proven that Grindwell Norton could successfully replicate its manufacturing excellence beyond coastal locations. But Nagpur was conservative—still in India, still making traditional products. The new leadership, with Saint-Gobain's blessing and capital, wanted transformational moves.

The masterplan, unveiled in a 2005 board meeting that stretched past midnight, was breathtaking in scope. Five new manufacturing facilities across South Asia. Entry into four new product categories. Investment of ₹500 crore over a decade. The French board members were enthusiastic—this aligned with Saint-Gobain's strategy of building regional champions. The Indian directors were cautious—expansion at this pace had broken many Indian companies. The debate was settled by a simple math: India's GDP was growing at 8% annually, industrial production at 10%, and Grindwell Norton's order book was growing at 15%. They couldn't build capacity fast enough.

The Himachal Pradesh facility in 2008 was the first test of this strategy. Located in Baddi, the state's pharmaceutical and chemical hub, the plant would manufacture thin wheels—precision cutting discs used in everything from semiconductor wafer dicing to surgical instrument manufacturing. The technology was cutting-edge, requiring tolerances measured in microns and consistency that pushed the limits of manufacturing science.

But the real innovation was the business model. The Himachal government offered a 10-year tax holiday for new industries. By manufacturing high-value, low-volume products there while keeping commodity products in older facilities, Grindwell Norton could optimize its tax structure while serving premium markets. It was financial engineering married to industrial strategy.

The Bhutan silicon carbide plant, operational by 2009, was even more audacious. Silicon carbide—that incredibly hard material used in everything from LED lights to bulletproof vests—required enormous amounts of electricity for production. Bhutan had surplus hydroelectric power but no industrial consumers. Grindwell Norton negotiated directly with the Bhutanese government, securing power at rates 60% below Indian costs.

The challenges were enormous. Every piece of equipment had to be trucked through mountain roads that were often single-lane with thousand-foot drops. Skilled workers had to be convinced to relocate to a Buddhist kingdom where television had only recently been permitted. Raw materials had to navigate three international borders. Yet when the plant fired up its first batch, producing silicon carbide with a carbon footprint 70% lower than Chinese competitors, it became clear that geographic arbitrage could create sustainable competitive advantages.

The 2012 Halol facility near Vadodara represented another strategic vector: customer proximity. Halol had emerged as India's automotive hub, with GM, Ford, and numerous suppliers clustered in massive industrial parks. Grindwell Norton's High Performance Refractories plant was literally next door to major steel processors, reducing logistics costs and enabling just-in-time delivery that competitors couldn't match.

But geographic expansion was only half the story. Product diversification during this period transformed Grindwell Norton from an abrasives company that also made other materials into a true multi-product industrial conglomerate. The ADFORS division, manufacturing textile reinforcements for construction, leveraged Saint-Gobain's global technology but adapted it for Indian construction methods where labor was cheap but quality consistency was challenging.

The Performance Plastics division was particularly innovative, developing specialized polymers for the Indian automotive industry's unique needs—materials that could withstand temperature extremes from Ladakh's -40°C to Rajasthan's 50°C, road conditions that ranged from German-style highways to crater-filled rural tracks. These weren't just imported formulations; they were India-specific innovations that later found applications in other emerging markets.

The creation of INDEC, the IT services arm, seemed bizarre to outside observers. Why would an abrasives company start a software division? The answer lay in Grindwell Norton's digital transformation needs. Unable to find IT services companies that understood manufacturing deeply enough, they built their own capability. INDEC developed manufacturing execution systems, quality control software, and supply chain optimization tools. What started as an internal necessity became a profit center, serving other Saint-Gobain subsidiaries across Asia.

The numbers from this era tell a story of successful diversification. Revenue grew from ₹680 crore in 2000 to ₹2,100 crore by 2015. But more importantly, no single product category represented more than 30% of revenue. The company had successfully de-risked itself from dependence on any single market or technology.

The Forbes recognition in 2006 was particularly sweet. Being named among Asia's "Best Under a Billion" validated the strategy—here was an Indian company competing not just domestically but across Asia, recognized not for size but for performance. The citation noted Grindwell Norton's return on equity of 28%, its consistent profitability growth, and its successful navigation of multiple product categories.

Yet this period also revealed tensions. The rapid expansion stretched management capabilities. Quality issues emerged at new facilities. Integration between divisions was poor—the ceramics team in Bangalore barely communicated with the plastics team in Vadodara. Saint-Gobain began pushing for more standardization, more global integration, less India-specific innovation. The balance between local entrepreneurship and global coordination, always delicate, was being tested.

The 2008 financial crisis provided an unexpected stress test. Orders collapsed 30% in six months. Automotive production plummeted. Construction stopped. But Grindwell Norton's diversification strategy proved its worth—while abrasives sales crashed, demand for refractories remained stable, and specialty ceramics actually grew as manufacturers sought efficiency improvements. The company remained profitable throughout the crisis, even as competitors reported losses.

By 2015, Grindwell Norton had transformed from a single-product, single-location company into a diversified industrial conglomerate with eight manufacturing facilities across three countries. But success brought new challenges. Chinese competitors were becoming increasingly sophisticated. Digital disruption was changing manufacturing itself. The next phase would require not just geographic and product expansion but fundamental reimagination of what an industrial materials company could be.

VII. Modern Era: Industry Leadership & Challenges (2015–Present)

The WhatsApp message pinged at 2 AM on a Mumbai executive's phone in March 2020: "Plant running at 30% capacity. Workers afraid to come. What do we do?" COVID-19 had arrived, and with it, the greatest test of Grindwell Norton's eight-decade journey. But this crisis would reveal something profound about the company—its transformation from a traditional manufacturer into a modern industrial technology company was more complete than even its leadership realized.

Before the pandemic, Grindwell Norton had already been grappling with the new realities of 21st-century manufacturing. The company's 2015 strategic review, conducted by McKinsey consultants parachuted in from Singapore, had delivered uncomfortable truths. Chinese competitors weren't just cheaper anymore—they were innovating faster. Digital natives were entering industrial markets with asset-light models. Customers were demanding not just products but data, analytics, and predictive maintenance.

The response was "Project Phoenix"—a comprehensive transformation initiated in 2016. Unlike previous expansions focused on geography or products, Phoenix targeted capability building. The company established an Innovation Center in Bangalore, recruiting data scientists and materials engineers to work on next-generation products. They partnered with IIT Madras to develop AI models for predicting grinding wheel wear. They launched an IoT initiative, embedding sensors in grinding wheels to provide real-time performance data.

The product portfolio by 2020 had evolved far beyond traditional abrasives. Life sciences had become a significant vertical—Grindwell Norton's ultra-pure ceramics were being used in biomedical implants, their specialized filters in pharmaceutical manufacturing. The company had quietly become one of Asia's largest suppliers of ceramic balls for hip replacements, a market dominated by American and Swiss companies until recently.

The automotive aftermarket transformation was particularly impressive. Rather than just selling replacement grinding discs to mechanics, Grindwell Norton created a complete ecosystem—training programs for technicians, mobile apps for product selection, YouTube channels with repair tutorials in regional languages. They understood that in India's fragmented aftermarket, winning meant educating an entire value chain.

Then came 2024's financial performance—revenue of ₹2,812 crore, up 4.65% from the previous year. On paper, modest growth. But beneath the surface, a dramatic shift was occurring. Traditional abrasives now contributed less than 40% of revenue. High-performance materials—ceramic membranes for water treatment, specialized coatings for solar panels, advanced composites for wind turbines—were driving growth. The company was riding India's sustainability wave while maintaining its industrial core.

The earnings decline of 3.89% to ₹369 crore told a different story—the cost of transformation. R&D spending had doubled. Digital investments were consuming capital. The company was consciously sacrificing short-term profitability for long-term positioning. As the CFO explained to anxious analysts: "We're not just competing with abrasives companies anymore. We're competing with materials science companies globally. That requires a different level of investment."

The Chinese challenge had evolved from price competition to technological rivalry. Companies like Zhengzhou Yulong and Shandong Jinmeng weren't just copying products—they were innovating in manufacturing processes, developing new materials, and aggressively expanding globally. Grindwell Norton's response was strategic focus: rather than compete everywhere, they identified niches where their Indo-French heritage created advantages—products requiring high customization, applications demanding technical support, markets valuing sustainability credentials.

The debt-free status, achieved through careful capital management over decades, became a crucial competitive advantage. While competitors struggled with leverage during COVID disruptions, Grindwell Norton could invest counter-cyclically. They acquired distressed suppliers, hired talent from struggling competitors, and accelerated R&D when others were cutting costs.

The sustainability transformation deserves special mention. Saint-Gobain's global commitment to carbon neutrality by 2050 had seemed impossibly ambitious when announced. But Grindwell Norton was already ahead—the Bhutan plant's hydroelectric power, solar installations at Indian facilities, and waste heat recovery systems had reduced carbon intensity by 45% since 2015. More importantly, they were developing products that enabled customers' sustainability transitions—grinding wheels that lasted longer, coatings that improved solar panel efficiency, filters that reduced industrial emissions.

The export challenges were real but nuanced. Direct exports faced headwinds from Chinese competition and global trade tensions. But Grindwell Norton found alternative routes—supplying to global companies' Indian operations for worldwide distribution, partnering with Saint-Gobain subsidiaries for market access, focusing on technical products where Indian cost advantages were less relevant than engineering capability.

The company's P/E ratio of 51.28 and P/B of 8.33 reflected market optimism but also raised questions. Was this valuation justified for an industrial materials company? Bulls argued yes—pointing to the high-margin new products, the sustainability tailwinds, the Saint-Gobain backing. Bears worried about Chinese competition, slowing industrial growth, and the capital intensity of new technologies.

The dividend payout of 48.2% represented a careful balance—returning cash to shareholders while retaining capital for growth. This wasn't the 80% payouts of mature industrial companies or the zero dividends of high-growth tech firms. It was the middle path of a company transforming while respecting shareholder expectations.

Today, Grindwell Norton stands at an inflection point. The traditional business remains profitable but growth is slowing. New businesses are exciting but require patient capital. The Saint-Gobain relationship provides stability but potentially limits agility. The company that began as a grinding wheel manufacturer in a fishing village has become something far more complex—a materials science company, a sustainability enabler, an industrial technology provider.

The modern era has proven that survival in industrial markets requires constant evolution. Grindwell Norton is no longer just grinding and polishing—it's enabling the manufacturing transformation of an entire nation while positioning itself for a materials revolution that will define the next century.

VIII. The Saint-Gobain Synergy Story

The video conference connected three continents: Courbevoie near Paris, where Saint-Gobain executives sat in their ultramodern headquarters overlooking the Seine; Mumbai, where Grindwell Norton's leadership gathered in a monsoon-dampened boardroom; and Boston, where consultants presented integration synergies on perfectly formatted slides. It was 2023, and after three decades of partnership, they were still discovering new ways to create value together.

Saint-Gobain in 2023 wasn't just any parent company—with €47.9 billion in sales, it was one of the world's oldest and most successful industrial conglomerates. Founded in 1665 to create mirrors for Louis XIV's Palace of Versailles, it had survived the French Revolution, two World Wars, and countless economic cycles. This wasn't a company that thought in quarters or even years—it thought in centuries. For Grindwell Norton, being part of this legacy meant access to patience, perspective, and possibilities that no standalone company could achieve.

The technology transfer relationship had evolved far beyond the original Norton-era sharing of formulations and processes. By 2020, Grindwell Norton engineers had access to Saint-Gobain's entire global R&D network—eight major research centers, 3,500 researchers, and an annual R&D budget exceeding €400 million. But the flow wasn't unidirectional anymore.

Take the example of the "Mumbai Method"—a frugal innovation technique developed by Grindwell Norton for handling inconsistent raw material quality. Indian engineers had created algorithms that could adjust manufacturing parameters in real-time based on input material variations. When Saint-Gobain faced supply chain disruptions during COVID, this Indian innovation was deployed across European plants, saving millions in rejected products.

The global customer access was transformative but complex. When Airbus needed specialized ceramic components for their new aircraft, Saint-Gobain could position Grindwell Norton as a supplier. But this required meeting aerospace standards that were orders of magnitude stricter than industrial norms. The certification process took three years, cost ₹15 crore, and required fundamental changes to quality systems. The payoff: a 10-year contract worth ₹200 crore annually with margins double the company average.

The R&D collaboration had produced unexpected innovations. Saint-Gobain's French laboratories were working on quantum dots for next-generation displays. Grindwell Norton's ceramics team was developing high-purity substrates. When the teams connected, they realized that combining their technologies could create revolutionary products for the semiconductor industry. The joint development, funded by both entities, was classic synergy—neither could have achieved it alone.

But the relationship wasn't without tensions. Saint-Gobain's global standardization drive—"One Saint-Gobain"—sought to harmonize processes, systems, and even corporate culture across all subsidiaries. For Grindwell Norton, this meant adopting French-designed HR policies that didn't always align with Indian realities. Performance review systems designed for French labor laws confused Indian managers. Safety standards appropriate for automated European factories seemed excessive for labor-intensive Indian operations.

The balance between local autonomy and global integration was constantly negotiated. Grindwell Norton won battles—maintaining its local brands, preserving relationships with small Indian customers that didn't meet Saint-Gobain's global account criteria, continuing to sponsor cricket teams despite corporate preference for football. But they lost others—adopting global ERP systems that were overly complex for Indian operations, following procurement policies that favored global suppliers over local vendors.

The capital allocation framework was particularly interesting. Saint-Gobain evaluated all global investment opportunities through a single lens—return on capital employed (ROCE) had to exceed 15% within three years. For Grindwell Norton, competing for capital meant not just showing returns but demonstrating strategic value. The Bhutan plant, for instance, was approved not because of its financial returns but because it provided Saint-Gobain with sustainable silicon carbide for electric vehicle applications—a strategic priority.

The cultural integration had created a unique hybrid. French emphasis on technical excellence merged with Indian jugaad. Long-term planning combined with opportunistic execution. Global standards met local customization. Walking through Grindwell Norton's facilities, you'd see French safety signs next to Hindu shrines, ISO certifications beside rangoli decorations, global corporate values translated into Hindi and Tamil.

The knowledge transfer had become genuinely bidirectional by 2020. Indian engineers regularly presented at Saint-Gobain's global technical conferences. The Mumbai team's work on nano-ceramics was featured in the corporate research journal. When Saint-Gobain needed to establish operations in Africa, they sent Grindwell Norton managers who understood emerging market dynamics better than their European counterparts.

The market access worked both ways too. While Grindwell Norton could sell to Saint-Gobain's global customers, they also helped French products enter Indian markets. Saint-Gobain's construction products, designed for European buildings, needed significant adaptation for Indian construction methods. Grindwell Norton's market knowledge and distribution network made this possible, creating revenue streams that benefited both parties.

The sustainability collaboration was particularly powerful. Saint-Gobain's global commitment to carbon neutrality required innovation across all subsidiaries. Grindwell Norton's Bhutan plant, already running on hydroelectric power, became a template for sustainable manufacturing. The learnings from operating in monsoon conditions helped Saint-Gobain facilities in Southeast Asia. Indian techniques for water recycling, developed out of scarcity, were adopted in water-stressed regions globally.

Yet questions remained about the future of this relationship. Some investors wondered if Grindwell Norton was being held back by Saint-Gobain's conservative approach. Could the company grow faster as an independent entity? Others argued the opposite—that without Saint-Gobain's technology and market access, Grindwell Norton would be just another commodity manufacturer struggling against Chinese competition.

The synergy story ultimately wasn't just about technology transfer or market access—it was about creating a new model for how global corporations could work with emerging market subsidiaries. Not as colonial outposts or cost centers, but as equal partners in innovation and growth. The marriage between a 359-year-old French giant and an 83-year-old Indian pioneer had created something unique—a company that was simultaneously deeply local and truly global.

IX. Playbook: Business & Investing Lessons

The conference room in Mumbai's Bandra-Kurla Complex was packed with fund managers, each armed with laptops displaying discounted cash flow models and comparable company analyses. The presenter, a veteran who had tracked Grindwell Norton for two decades, put up a simple slide: "How to Build a ₹16,000 Crore Company from Grinding Wheels." The room leaned forward. This wasn't just about one company—it was about understanding industrial value creation in emerging markets.

Lesson 1: Building Industrial Capability in a Developing Economy

Grindwell Norton's journey demonstrates that industrial capability isn't built through giant leaps but through patient accumulation of expertise. The founders didn't try to compete with Norton immediately—they spent 25 years building basic competence before seeking international partnership. For modern founders, the lesson is clear: in complex industries, time is a competitive advantage. The Chinese competitors threatening Grindwell Norton today started their capability building in the 1990s. The next generation of competitors is building capability now in Vietnam and Bangladesh.

Lesson 2: The Art of Technology Partnerships and Joint Ventures

The Norton partnership structure was masterful—40% equity to Norton, enough for commitment but not control. Technology transfer with royalties, ensuring continuous improvement. Board representation but local management. Too many Indian companies either gave away too much (losing control) or too little (missing real technology transfer). The sweet spot is finding partners who need you as much as you need them. Norton needed Indian market access; Grindwell needed technology. Both sides had leverage, creating a balanced partnership that lasted decades.

Lesson 3: Managing Transition from Founder-Led to MNC Subsidiary

Most founder-to-corporate transitions fail because founders can't let go or corporations can't preserve entrepreneurial culture. Grindwell Norton succeeded through gradual transition—first technical partnership, then minority investment, then majority control. Each stage lasted years, allowing cultural adaptation. The founders remained involved but not controlling. Saint-Gobain provided systems but preserved autonomy. For investors, companies managing this transition deserve premium valuations—it's the hardest thing in business.

Lesson 4: Capital Allocation in Capital-Intensive Business

Industrial businesses consume capital voraciously. Grindwell Norton's discipline was remarkable—never over-leveraging despite growth opportunities, maintaining 20%+ ROCE despite heavy manufacturing assets, being debt-free while expanding aggressively. The secret was sequential expansion—master one product/geography before moving to the next. Use cash flows from mature businesses to fund new ventures. Never bet the company on single expansion. This patient capital allocation created compound returns without existential risk.

Lesson 5: Building Moats in Commoditized Industrial Products

Grinding wheels are commodities—or are they? Grindwell Norton built multiple moats: technical specifications creating switching costs, customer relationships spanning decades, distribution networks reaching 10,000 touchpoints, application engineering creating customization, and sustainability credentials becoming entry barriers. The lesson: even commodities can be differentiated through service, reliability, and total cost of ownership. The moat isn't in the product—it's in the ecosystem around it.

Lesson 6: The Importance of Distribution and Customer Relationships

Industrial selling isn't B2B—it's H2H (human to human). Grindwell Norton's sales engineers spent months at customer facilities, understanding problems beyond products. They knew plant managers' children's names, attended family weddings, became trusted advisors not vendors. This relationship capital survived technology changes, price pressures, and competitive attacks. For investors, companies with deep customer relationships deserve valuation premiums—these relationships are assets not captured on balance sheets.

Lesson 7: Lessons on Timing Market Entry and Expansion

Grindwell Norton's timing was impeccable but not lucky. They entered when import substitution created protection but before competition emerged. Partnered with Norton when technology gaps were bridgeable. Accepted Saint-Gobain acquisition when globalization made independence unviable. Expanded to China adjacents (Bhutan) when direct competition was impossible. Each move was neither too early (before capability) nor too late (after opportunity). Timing in industrial markets is about reading multi-decade cycles, not quarterly trends.

The Capital Cycle Applied

The abrasives industry follows classic capital cycle dynamics. High returns attract capital, creating overcapacity, crushing returns, forcing consolidation, enabling pricing power for survivors. Grindwell Norton survived multiple cycles by diversifying across products with different cycle timings. When abrasives were down, ceramics were up. When automotive was struggling, construction was booming. Portfolio diversification within industrial materials created stability through cycles.

The Sustainability Transformation as Competitive Advantage

ESG isn't just compliance—it's strategy. Grindwell Norton's sustainable manufacturing (Bhutan hydro plant, solar installations, water recycling) created cost advantages. Sustainable products (longer-lasting wheels, recyclable ceramics) commanded premium pricing. Sustainability credentials opened doors to global customers. The lesson: in industrial markets, green and profitable increasingly overlap. Companies ahead on sustainability will capture disproportionate value.

The Hidden Value of Technical Training

Grindwell Norton trained thousands of engineers who left for other companies. Conventional thinking says this is value destruction. Reality: these alumni became customers, suppliers, partners. They specified Grindwell Norton products at new employers. They maintained quality standards learned at the company. They created an ecosystem of quality consciousness benefiting the mother ship. Investment in human capital pays dividends beyond employment tenure.

Why Boring Can Be Beautiful

No one dreams of making grinding wheels. MBA graduates don't aspire to abrasives careers. Tech investors ignore industrial materials. This neglect creates opportunity. Grindwell Norton faced less talent competition, lower valuation volatility, and patient investor bases. Boring businesses with good economics attract smart capital and create wealth quietly. The lesson: unsexy industries with solid fundamentals outperform glamorous sectors with poor economics.

The Platform Power of Industrial Companies

Grindwell Norton evolved from product manufacturer to platform company. The platform connects material science (R&D), manufacturing (assets), distribution (network), and solutions (engineering). New products leverage existing platform elements. Acquisitions plug into established systems. The platform creates economies of scope beyond scale. For investors, industrial platforms deserve technology-like valuations—they're networks, not just factories.

This playbook reveals that industrial value creation follows different rules than consumer or technology businesses. Patience beats speed. Relationships trump transactions. Technical depth creates lasting moats. Capital discipline enables compound growth. For those willing to understand these dynamics, industrial companies offer compelling investment opportunities hiding in plain sight.

X. Analysis & Bear vs. Bull Case

The equity research analyst pulled up the Bloomberg terminal, fingers hovering over the keyboard. Grindwell Norton's stock had just hit an all-time high, trading at 51.28 times earnings. The market was pricing in perfection. But was this industrial conglomerate hiding in plain sight as a technology company, or was it an old-economy manufacturer riding temporary tailwinds? The answer would determine whether this was a generational buying opportunity or a value trap waiting to spring.

Competitive Positioning: The Three-Circle Framework

Grindwell Norton operates at the intersection of three circles: Indian manufacturing growth, global sustainability transition, and materials science innovation. At this intersection, the company has only two real competitors—Carborundum Universal (Murugappa Group) domestically and Saint-Gobain's other subsidiaries globally. Chinese competitors like Fengdeng and Zhongyuan operate in only one circle—cost leadership without technology depth or sustainability credentials.

The 35% market share in organized Indian abrasives seems dominant, but organized players represent only 60% of the total market. The unorganized sector—small workshops making low-quality wheels—still commands 40%. This presents both opportunity (formalization driving market share gains) and threat (price pressure from informal competition). Every GST rate increase, every safety regulation, every quality standard pushes demand from unorganized to organized. Grindwell Norton captures disproportionate share of this shift.

Valuation Puzzle: Why P/E of 51 for an Industrial?

The market values Grindwell Norton like a technology company, not an industrial manufacturer. The bulls argue this is justified: 45% of revenue comes from products that didn't exist a decade ago. R&D spending at 3% of sales exceeds many pharmaceutical companies. The company owns 50+ patents with 20+ pending. Digital initiatives contribute 8% of EBITDA through efficiency gains. This isn't your grandfather's grinding wheel company.

Bears counter that fundamentals don't support tech valuations. Asset turns of 1.2x are industrial, not digital. Growth at 4.65% is GDP-plus, not exponential. Working capital at 25% of sales reflects physical inventory, not software downloads. The P/B ratio of 8.33 seems excessive for a company where book value represents real factories, not intangible assets. At these valuations, everything needs to go right.

Growth Drivers: The Triple Engine

Three engines could drive growth over the next decade. First, industrial growth—India's manufacturing sector, currently 15% of GDP, targets 25% by 2030. Every percentage point increase represents ₹500 crore addressable market for Grindwell Norton. Infrastructure spending, PLI schemes, and China-plus-one strategies create sustained demand for industrial materials.

Second, import substitution 2.0—not the protectionist policies of the past but technical competition. India imports ₹5,000 crore of advanced ceramics annually. Grindwell Norton's technical capabilities could capture significant share. The government's emphasis on self-reliance in critical materials creates policy tailwinds. Each 10% import substitution represents ₹500 crore opportunity.

Third, new applications—electric vehicles need specialized ceramics for batteries, solar panels require ultra-pure materials, hydrogen economy demands high-temperature resistant components. Grindwell Norton is positioned at the materials intersection of multiple megatrends. Early investments in these technologies could yield exponential returns as markets mature.

The China Syndrome: Existential Threat or Overblown Fear?

Chinese competition is real but nuanced. In commodity abrasives, Chinese players have 50% cost advantages through scale and subsidies. But in specialized products, the gap narrows to 15-20%. Add logistics costs, quality concerns, and service requirements, and Chinese advantage often disappears. More importantly, geopolitical tensions and supply chain resilience concerns are creating "China-plus-one" demand, benefiting established non-Chinese suppliers.

The real Chinese threat isn't exports but technology advancement. Chinese companies are investing heavily in R&D, hiring Western talent, acquiring European companies. The technology gap that protected Grindwell Norton is narrowing. In silicon carbide, Chinese companies have achieved quality parity. In ceramic membranes, they're approaching Western standards. The moat is shrinking, requiring constant innovation to maintain differentiation.

Commodity Cycles: Riding the Dragon

Industrial materials follow vicious cycles. Steel drives refractory demand. Automotive drives abrasives consumption. Construction drives everything. These sectors are cyclical, creating earnings volatility that the market hates. Grindwell Norton's diversification dampens but doesn't eliminate cyclicality. The 2008 crisis saw 30% revenue decline. The next downturn could be similar.

But cycles create opportunities for disciplined operators. Grindwell Norton's debt-free status enables countercyclical investment. Weak competitors exit during downturns. Customers consolidate suppliers, favoring reliable partners. The company emerged stronger from every past cycle. Patient investors who buy during downturns and hold through cycles generate exceptional returns.

Technology Disruption: The 3D Printing Question

Additive manufacturing (3D printing) could theoretically eliminate grinding—why remove material when you can build to exact specifications? This existential question haunts industrial manufacturers. But reality is more complex. 3D printing works for prototypes and complex geometries but not mass production. Surface finishing still requires traditional methods. Cost curves favor subtractive manufacturing for most applications.

Grindwell Norton is hedging cleverly—developing materials for 3D printing while maintaining traditional capabilities. Their ceramic powders work in additive manufacturing. Their surface treatment expertise applies regardless of production method. They're selling picks and shovels to both sides of the manufacturing revolution.

The Dividend Aristocrat Potential

The 48.2% payout ratio reflects beautiful balance. It's high enough to attract income investors but low enough to fund growth. The company has increased dividends for 15 consecutive years, creating aristocrat potential. In a zero-interest-rate world, sustainable dividend growth commands premium valuations.

But dividend sustainability requires stable cash flows. Industrial cyclicality threatens consistency. Capex requirements could spike. Saint-Gobain could demand higher dividends to fund global needs. The dividend story is attractive but not guaranteed.

ESG as Value Creator or Cost Center?

Grindwell Norton's ESG initiatives seem exemplary—carbon reduction, water recycling, sustainable products. But ESG is expensive. Solar installations cost ₹50 crore with 7-year paybacks. Sustainable materials carry 20% price premiums that customers reluctantly pay. ESG compliance adds 2% to operating costs.

The bull case sees ESG as investment, not expense. European customers increasingly mandate sustainability credentials. Green products command premium pricing. Sustainable operations reduce long-term costs. ESG leadership creates option value for carbon credit markets. The company is investing ahead of regulations that will eventually force competitors to catch up.

The Verdict: Priced for Perfection but Delivering

At 51 times earnings, Grindwell Norton needs everything to go right—continued industrial growth, successful new product launches, Chinese competition remaining manageable, no major disruptions. One disappointment could trigger significant multiple compression. The stock is risky at current valuations.

But this company has consistently delivered for 83 years through wars, recessions, technological changes, and competitive threats. The Saint-Gobain backing provides stability. The diversified portfolio reduces single-point failure risk. The management team has navigated multiple cycles. For investors with decade-long horizons, today's expensive valuations might seem cheap in retrospect.

The bear case is valuation. The bull case is everything else.

XI. Epilogue & "If We Were CEOs"

The new CEO's first day began at 5 AM with a walk through the Mora factory, where it all started 83 years ago. The sea breeze still carried salt that corroded equipment, workers still began shifts with prayers, and grinding wheels still spun at 6,000 RPM, throwing sparks into the dawn light. But everything else was changing. The CEO's smartphone buzzed with messages from sensors embedded in grinding wheels halfway around the world, AI algorithms optimizing production schedules, and customers demanding materials that didn't yet exist.

Recent Developments: The Changing of the Guard

The 2024 management transition marked a generational shift. The new leadership team—average age 45, with degrees from IITs and global MBAs, experience across continents—represented a different breed. They spoke the language of digital transformation, sustainability metrics, and platform economics. But they also understood that industrial companies succeed through patient execution, not PowerPoint strategies.

The recent strategic review identified three priorities: accelerate materials innovation, expand solutions business, and build digital capabilities. Notable by absence—no mention of traditional abrasives, the historical core. This wasn't abandonment but evolution. Like IBM moving from hardware to services, Grindwell Norton was transitioning from products to solutions, from atoms to algorithms plus atoms.

Future Opportunities: The Three Horizons

Horizon 1 (immediate): The electric vehicle revolution needs specialized materials—ceramic separators for batteries, silicon carbide for power electronics, lightweight composites for body panels. Grindwell Norton has quietly developed capabilities in all three. Early customer engagements with Tata Motors and Ola Electric suggest significant revenue potential. The EV materials market could reach ₹10,000 crore by 2030.

Horizon 2 (emerging): Renewable energy infrastructure requires advanced materials—anti-reflective coatings for solar panels, ceramic bearings for wind turbines, high-temperature materials for hydrogen production. The company's materials expertise translates directly. Each gigawatt of renewable capacity needs ₹50 crore of specialized materials. India plans 500 gigawatts by 2030.

Horizon 3 (experimental): Quantum computing needs ultra-pure substrates. Biomedical applications require biocompatible ceramics. Space applications demand extreme-performance materials. These markets are nascent but revolutionary. Grindwell Norton's R&D investments in these areas are lottery tickets—most will fail, but one success could transform the company.

If We Were CEOs: The Five Bold Moves

Move 1: Create the "Materials as a Service" Business Model Stop selling grinding wheels; start selling grinding outcomes. Install sensors in every product, collect performance data, use AI to predict failures, charge customers for uptime not products. This transforms economics—recurring revenue, higher margins, customer stickiness. The technology exists; the challenge is mindset change.

Move 2: Build the Innovation Ecosystem Establish a ₹100 crore venture fund investing in materials startups. Create an accelerator program bringing global innovations to India. Partner with IITs for research centers on campuses. Innovation can't be centralized in one R&D center—it needs an ecosystem. Grindwell Norton should be the sun around which materials innovation orbits.

Move 3: Develop the China Strategy Not competing with China but partnering selectively. Joint ventures for commodity products where cost matters most. Technology licensing for mid-tier products where IP can be protected. Direct competition only in high-end segments where technology moats exist. China is too big to fight, too important to ignore—strategic collaboration is the only path.

Move 4: Accelerate Digital Manufacturing Implement digital twins for all manufacturing facilities—virtual models enabling simulation before implementation. Deploy autonomous quality control using computer vision. Create predictive maintenance systems preventing downtime. Digital manufacturing isn't about replacing workers but augmenting capabilities. The goal: lights-out factories for commodity products, human expertise for specialized solutions.

Move 5: Reimagine the Portfolio Divest commodity abrasives to focus on advanced materials. The commodity business generates cash but consumes management attention disproportionate to profit contribution. Use divestment proceeds to acquire technology companies—sensor manufacturers, AI startups, advanced ceramics specialists. Transform from industrial conglomerate to focused materials technology company.

Strategic Priorities for the Next Decade

Priority 1: Talent transformation—recruit software engineers alongside chemical engineers, data scientists alongside factory managers. The workforce needs hybrid skills—understanding both materials science and digital technology.

Priority 2: Sustainability leadership—commit to carbon neutrality by 2035, ahead of Saint-Gobain's 2050 target. Develop circular economy solutions—grinding wheels that can be recycled, ceramics from waste materials. Make sustainability a revenue driver, not cost center.

Priority 3: Customer intimacy—embed engineers at customer facilities, understand problems before customers articulate them, develop solutions for needs that don't yet exist. Deep customer relationships create competitive moats that no technology can replicate.

Key Takeaways for Founders and Investors

For founders: Building industrial companies requires patient capital, technical depth, and ecosystem thinking. Don't try to disrupt incumbents—partner with them, learn from them, eventually surpass them. Focus on solving real problems, not chasing valuations. Remember that industrial revolutions happen over decades, not quarters.

For investors: Industrial companies hiding technology transformations offer asymmetric returns. Look for companies with technical moats, customer relationships, and patience to compound. Valuation matters, but quality matters more. The best industrial investments look expensive at purchase but cheap in hindsight.

The Eternal Questions

As we close this narrative, fundamental questions remain: Can an 83-year-old company truly transform into a technology leader? Can Indian manufacturing compete globally beyond cost arbitrage? Can industrial companies generate tech-like returns while maintaining industrial stability?

Grindwell Norton's journey suggests tentative answers. Transformation is possible but painful, requiring cultural change beyond strategic planning. Indian manufacturing can compete through frugal innovation and market understanding. Industrial companies can generate exceptional returns, but patience is mandatory.

The story that began in a fishing village isn't ending—it's entering its most exciting chapter. The company that taught India to grind is now teaching the world that industrial companies can innovate, that manufacturing can be sustainable, that boring businesses can be beautiful investments.

In the end, Grindwell Norton's story is India's story—patient development, global ambition, technical capability, and the belief that tomorrow can be better than today. Whether making grinding wheels or quantum substrates, serving local workshops or global aerospace companies, the mission remains constant: enabling others to build, create, and progress.

The grinding never stops. Neither does the innovation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube