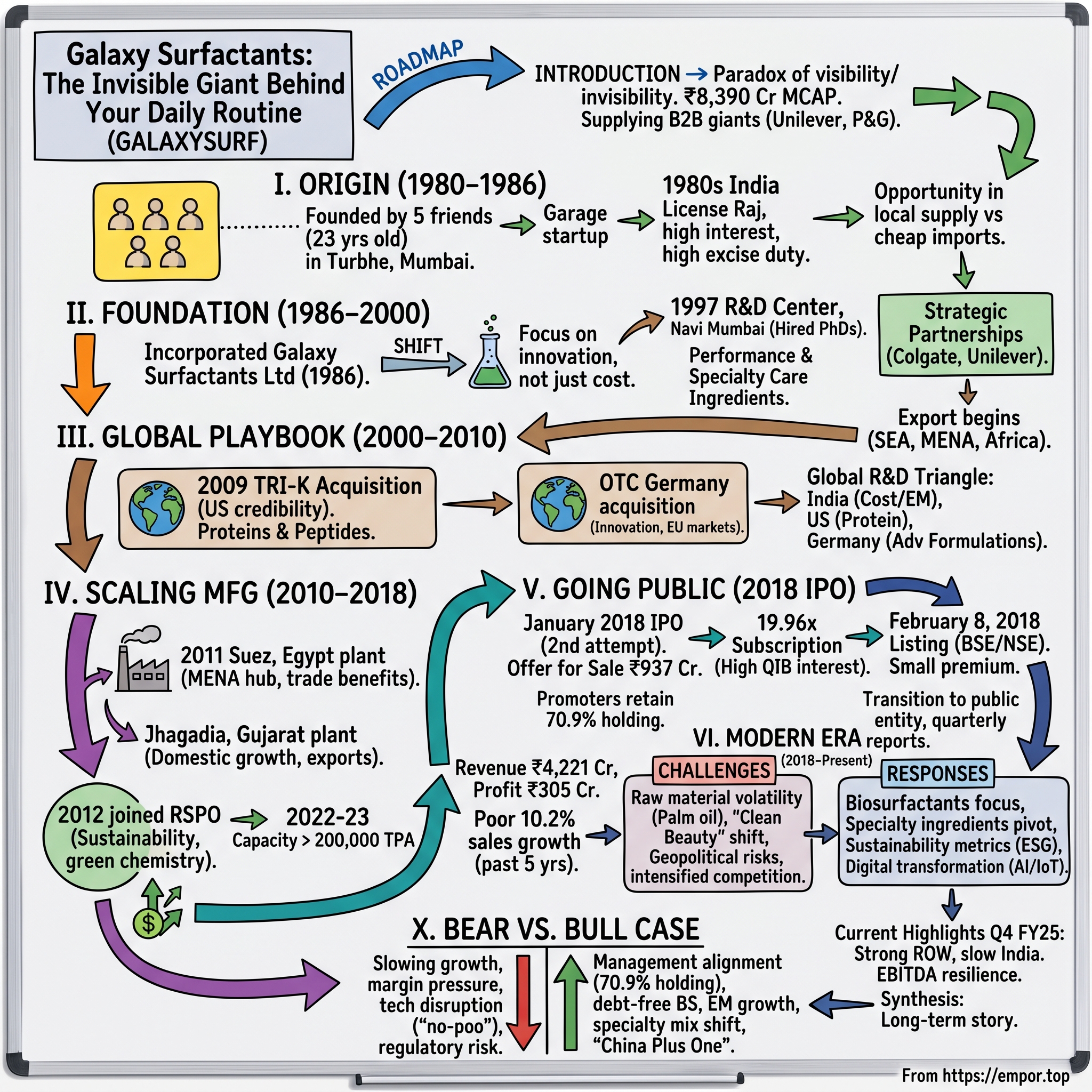

Galaxy Surfactants: The Invisible Giant Behind Your Daily Routine

I. Introduction & Episode Roadmap

Picture this: You wake up, stumble to the bathroom, squeeze toothpaste onto your brush. Later, you lather shampoo through your hair, apply sunscreen before heading out, maybe wash dishes after breakfast. In each of these mundane moments, there's a 70% chance you're touching molecules engineered by a company you've never heard of—Galaxy Surfactants.

This is the paradox of Galaxy: a ₹8,390 crore market cap company that's simultaneously everywhere and invisible. While consumer giants like Unilever, P&G, and L'Oréal dominate supermarket shelves and advertising airwaves, Galaxy operates in the shadows, supplying the critical chemistry that makes their products actually work. The surfactants—those miracle molecules that make oil and water play nice together, that create foam, that deliver actives to your skin—come from nondescript factories in Navi Mumbai, Gujarat, Egypt, and beyond.

Galaxy manufactures over 205 product grades of performance surfactants and specialty care ingredients. These aren't sexy products with Super Bowl ads. They have names like "Sodium Lauryl Ether Sulfate" and "Cocamidopropyl Betaine"—tongue-twisters that appear in tiny print on the back of bottles. Yet without them, your shampoo wouldn't clean, your toothpaste wouldn't foam, your face wash wouldn't rinse clean.

What makes Galaxy fascinating isn't just what they make, but how they built this empire. This is a story of five 23-year-old friends who started with nothing but chemical engineering degrees and ambition in 1980s India—a time when "Made in India" meant cheap knockoffs to most global buyers. They would transform their contract manufacturing startup into a trusted innovation partner for the world's pickiest customers. Today, Galaxy serves over 1,400 clients across 70+ countries, holds 62 patents, and runs R&D centers on three continents.

But here's what's truly remarkable: in an era of founder exits and private equity flips, Galaxy's original promoters still own 70.9% of the company. Forty-four years in, they're still running the show. That's either supreme confidence or supreme stubbornness—and as we'll see, probably both.

This is that story: how five friends cracked the code of B2B specialty chemicals, why the unsexy business of surfactants is actually a beautiful business model, and what Galaxy's journey teaches us about building a global champion from India. Along the way, we'll decode the chemistry (don't worry, we'll keep it simple), explore the economics of selling to giants who could crush you, and understand why boring businesses often make the best investments.

So let's dive into the molecular world of Galaxy Surfactants—where five young chemical engineers decided to build their fortune one bubble at a time.

II. The Origin Story: Five Friends, One Dream (1980–1986)

The monsoon of 1980 brought more than just rain to Mumbai. In a small garage in the industrial suburb of Turbhe, five 23-year-olds huddled around cups of cutting chai, sketching chemical formulas on the back of old newspapers. The company was founded in 1980 by Unnathan Shekhar, Geera Ramakrishnan, Shashi Shanbhag, CR Ramakrishna, and Sudhir Patil; five friends, all aged 23, who all came from different backgrounds. They had no factory, no customers, and barely any capital. What they did have was timing—and perhaps more importantly, the audacity to dream big in an India that didn't yet believe in its own potential.

Each one was pursuing different paths in life such as chemical engineering, pharmacy, accountancy, etc. But, we were all bitten by the entrepreneurial bug and had the desire to be independent. We wanted to create something of significance, but we didn't know what. Hailing from middle-class families, the only capital we had was our education. Among them, Unnathan Shekhar stood out—a Chemical Engineering graduate from the University Department of Chemical Technology, Mumbai with a Post Graduate Diploma in Business Management from IIM Kolkata, who had worked with Hindustan Unilever and Lupin Laboratories before taking the entrepreneurial plunge.

This was 1980s India—a suffocating economic environment where India's industrial and technology policy regime was among the most inward-looking and protectionist anywhere outside the socialist bloc. The infamous License Raj strangled entrepreneurship with red tape. Banks lent at interest rates of 18-19 percent. The government had made it difficult to import raw materials with strict regulations. The excise duties were 117.5 percent for shampoos because personal goods were regarded as luxuries. Starting a chemical company in this environment wasn't just ambitious—it was borderline irrational.

Yet these five friends saw opportunity where others saw obstacles. The Indian chemical industry was nascent, dominated by government-owned enterprises and a handful of established players. Foreign multinationals like Colgate-Palmolive and Unilever operated in India but struggled to find reliable local suppliers who could meet their exacting quality standards. Most Indian manufacturers were content making cheap, commoditized products. The friends sensed a gap: what if an Indian company could match global quality standards while leveraging local cost advantages?

Shekhar started Galaxy Surfactants literally in a garage in 1980 and built the company into a Rs 851 crores enterprise. But the real breakthrough came when they landed their first major contract. They began their company as contract manufacturers for Colgate-Palmolive. This wasn't glamorous work—they were essentially making fatty alcohol sulfates, the workhorses of the cleaning industry. But Colgate-Palmolive wasn't just any customer. They were notorious for their quality standards, their demanding specifications, their rigorous audits. If you could satisfy Colgate, you could satisfy anyone.

The early days were brutal. In 1980, their manufacturing capacity was just 30 metric tons—a rounding error in the global surfactants market. They operated out of cramped facilities, often working 18-hour days to meet delivery deadlines. Quality control meant Shekhar personally checking every batch. R&D was conducted on borrowed equipment after hours. Marketing consisted of showing up at customers' offices and refusing to leave until they got a meeting.

But something interesting was happening in India's broader economic landscape. While the five friends were mixing chemicals in Turbhe, policymakers in Delhi were beginning to question decades of socialist economic doctrine. The fragile but faster growth during the 1980s took place in the context of significant reforms throughout the decade but especially starting in 1985. The winds of liberalization were starting to blow, even if the storm wouldn't fully arrive until 1991.

What made Galaxy different wasn't just their technical competence—it was their mindset. While other Indian companies saw themselves as cheap alternatives to global suppliers, Galaxy positioned itself as a partner. They didn't just want to make surfactants; they wanted to understand their customers' formulations, their market challenges, their innovation roadmaps. This consultative approach was revolutionary in Indian B2B manufacturing.

By 1986, the informal partnership needed structure. Galaxy Surfactants Limited was formally incorporated, transforming from a garage startup into a proper company. The incorporation wasn't just paperwork—it was a statement of intent. These weren't five friends playing at business anymore. They were building something that could outlast them.

The timing proved fortuitous. In the 1980s and 1990s, the petrochemical industry expanded rapidly with integrated naphtha and gas crackers and downstream plants for polymers, synthetic fibers, aromatics, and other chemicals. Galaxy was perfectly positioned to ride this wave, supplying the surfactants that would go into the consumer products flooding India's newly liberalizing markets.

Looking back, what's remarkable about Galaxy's origin isn't just that five middle-class twenty-somethings started a chemical company—it's that they chose the perfect intersection of boring and essential. Surfactants aren't sexy. Nobody dreams of making sodium lauryl sulfate. But that's precisely what made it a beautiful business. While others chased glamorous opportunities, Galaxy chose to become indispensable to companies that were themselves becoming indispensable to Indian consumers.

The foundation was set. Five friends had become entrepreneurs, a garage had become a factory, and a contract manufacturer was about to become something much more significant. As the 1980s drew to a close, Galaxy stood at the threshold of transformation—both its own and India's.

III. Building the Foundation: From Contract Manufacturing to Innovation (1986–2000)

The early 1990s brought a seismic shift to India's economic landscape. As finance minister Manmohan Singh dismantled the License Raj and opened India's markets to the world, Galaxy faced a paradox: liberalization meant opportunity, but it also meant competition. Suddenly, global chemical giants could enter India freely. The protective walls were coming down. For a company that had built its early success on being a reliable local supplier, this could have been catastrophic.

Instead, Unnathan Shekhar and his team made a counterintuitive decision. Rather than hunker down and protect their existing business, they would transform Galaxy from a contract manufacturer into an innovation powerhouse. "We realized that competing on cost alone was a race to the bottom," Shekhar would later reflect. "We needed to compete on chemistry."

The transformation began with a simple observation. Galaxy's multinational customers—Colgate, Unilever, P&G—were launching increasingly sophisticated products in India. Anti-dandruff shampoos, moisturizing body washes, premium face creams. These products required specialty surfactants and ingredients that were either imported at high cost or simply unavailable. Galaxy saw its opening: become the R&D partner these companies needed in India.

In 1997, Galaxy established its first dedicated research center in Navi Mumbai. This wasn't just a quality control lab with delusions of grandeur—it was a serious commitment to innovation. The company hired PhDs in chemistry, invested in analytical equipment, and most importantly, gave its scientists freedom to experiment. The mandate was clear: don't just copy what exists, create what doesn't.

The research center's early projects revealed Galaxy's evolving strategy. Instead of developing entirely new molecules (which would require enormous investment and regulatory approval), they focused on application innovation—taking existing surfactant chemistries and optimizing them for specific uses. A surfactant that worked in European hard water might fail in Chennai's soft water. A formulation perfect for Caucasian hair might be too harsh for Indian hair. These weren't breakthrough innovations that would win Nobel prizes, but they solved real problems for real customers.

The company manufactures specialty chemicals, including surfactants, mild surfactants, rheology modifiers, pearling agents, conditioning agents, and blends based on innovative concepts, proteins, Quats for the personal care industry. This portfolio expansion wasn't random—each new product category was carefully chosen based on customer needs and market gaps.

The economics of this shift were compelling. Contract manufacturing margins ranged from 8-12%. Specialty ingredients could command 20-30% margins. More importantly, specialty products created switching costs. Any company could make sodium lauryl sulfate to specification. But a customized surfactant blend optimized for a specific shampoo formulation? That required deep technical knowledge and close customer collaboration.

Galaxy's approach to serving global giants was particularly shrewd. They embedded their technical teams within customers' R&D centers, becoming extensions of their innovation efforts. When Unilever wanted to develop a low-cost shampoo for rural India, Galaxy's scientists were in the room from day one. When Colgate needed a mild surfactant for a new toothpaste, Galaxy could prototype solutions in weeks, not months.

This technical intimacy created a powerful moat. By the late 1990s, Galaxy wasn't just a supplier to these companies—they were a strategic partner. Galaxy became Certified Preferred Supplier to Colgate, Star Status Supplier for Unilever, Strategic Mind Partner with Henkel, Green Channel Holder of Reckitt Benckiser. These weren't participation trophies. They meant Galaxy could bypass standard procurement processes, access proprietary information, and influence product development decisions.

The trust equation was critical. In the chemical industry, switching suppliers isn't like changing coffee brands. It requires requalification, stability testing, regulatory filings. A bad batch of surfactant could mean millions in recalled products. Galaxy understood this and built its entire operation around reliability. They maintained redundant supply chains, kept months of safety stock, and had never—not once—failed to deliver an order on time.

As the 1990s progressed, Galaxy's ambitions grew beyond India. They began exporting to Southeast Asia, the Middle East, and Africa—markets with similar water conditions, climate, and consumer preferences to India. The approach was surgical: they didn't try to compete with BASF in Germany or Dow in the United States. Instead, they focused on emerging markets where their cost structure and technical capabilities gave them an edge.

The numbers tell the story of this transformation. From that initial 30 metric tons capacity in 1980, Galaxy had expanded to over 20,000 tons by 2000. Revenue grew from a few crores to over ₹200 crores. But more importantly, the company's customer base had diversified from a handful of multinationals to include hundreds of regional brands across dozens of countries.

What's fascinating about this period is what Galaxy chose not to do. They didn't integrate backward into petrochemicals, despite the allure of controlling raw materials. They didn't diversify into pharmaceuticals or agrochemicals, despite having the technical capability. They didn't pursue acquisitions, despite having the cash flow. Instead, they maintained an almost obsessive focus on surfactants and personal care ingredients.

This focus might have seemed limiting, but it was actually liberating. While competitors spread themselves thin across multiple chemical segments, Galaxy became the undisputed expert in their niche. They knew every surfactant molecule, every formulation challenge, every customer preference. When a company needed a surfactant solution, Galaxy wasn't just an option—they were the option.

The foundation built during these years would prove crucial for what came next. Galaxy had evolved from contract manufacturer to innovation partner, from local supplier to regional player, from cost competitor to value creator. They had proven that an Indian company could match global quality standards while maintaining cost competitiveness. Most importantly, they had built relationships of trust with the world's most demanding customers.

As the new millennium approached, Galaxy stood at another inflection point. The Indian economy was booming, consumer spending was exploding, and global companies were viewing India not just as a production base but as a critical growth market. Galaxy had spent 20 years building capabilities. Now it was time to scale them globally.

IV. The Global Expansion Playbook (2000–2010)

The new millennium opened with Y2K anxiety and dot-com euphoria, but in Galaxy's Navi Mumbai headquarters, Unnathan Shekhar was focused on a different kind of disruption. The company had mastered the Indian market and built footholds in emerging economies. But to truly become a global player, Galaxy needed something more radical: a presence in developed markets. The problem was obvious—how does an Indian specialty chemical company compete in markets dominated by century-old giants like BASF, Clariant, and Croda?

The answer came in an unexpected form. In 2008, as the global financial crisis sent Western companies scrambling for cash, Galaxy spotted an opportunity that would transform its trajectory. In July 2009, Galaxy acquired TRI-K Industries, a distributor and producer of specialty ingredients. But this wasn't just any acquisition—it was a masterstroke of strategic thinking.

TRI-K Industries, based in New Jersey, was a 30-year-old company with something Galaxy desperately needed: credibility in the U.S. market. Founded in 1974, TRI-K had built deep relationships with American cosmetic brands, from indie startups in Brooklyn to established names in Manhattan. They specialized in proteins and peptides for hair and skin care—ingredients that commanded premium prices and required sophisticated technical knowledge.

The acquisition negotiations revealed Galaxy's evolved thinking. They weren't buying TRI-K for its assets or even its customer list. They were buying legitimacy. As one Galaxy executive later explained, "An American cosmetics company might hesitate to buy from an Indian supplier. But buy from a New Jersey company that happens to be owned by Indians? That's different."

The deal structure was clever. Galaxy didn't fully integrate TRI-K into its operations. Instead, they maintained the brand, kept the management team, and preserved the entrepreneurial culture. TRI-K continued to operate like a nimble specialty chemical company, but now with Galaxy's global supply chain and R&D capabilities behind it. The New Hampshire manufacturing facility for specialty proteins remained operational, giving Galaxy its first production footprint in North America.

But Galaxy's global ambitions extended beyond the Americas. Europe, with its sophisticated personal care market and stringent regulations, presented a different challenge. Here, Galaxy chose collaboration over acquisition. Galaxy acquired a majority shareholding in Oberhausen Technology Center (OTC) in Germany, described as a state-of-the-art R&D facility.

The German facility wasn't about manufacturing—it was about innovation and customer intimacy. European cosmetic companies, particularly in France and Germany, prided themselves on cutting-edge formulations. They wanted suppliers who could speak their language, literally and technically. The Oberhausen center gave Galaxy a seat at the European innovation table.

This created what Galaxy called its "global R&D triangle"—India for cost-effective innovation and emerging market applications, the United States for protein chemistry and American market trends, and Germany for advanced formulations and European regulatory expertise. Each center had its specialty, but they shared knowledge freely. A mild surfactant developed in Mumbai might be optimized in Oberhausen and commercialized through TRI-K.

The strategy of serving 70+ countries required more than just shipping products globally. Galaxy developed a sophisticated market segmentation approach. Mature markets like the U.S. and Europe got specialty ingredients and technical support. Emerging markets in Africa and Asia received performance surfactants and cost-optimized solutions. Middle markets like Brazil and Turkey got a hybrid offering. This wasn't one-size-fits-all globalization—it was carefully calibrated local relevance.

According to Unnathan Shekhar, two-thirds of their business comes from international customers. This wasn't an accident. Galaxy deliberately prioritized international growth, often at the expense of easier domestic opportunities. The reasoning was strategic: international customers, particularly multinationals, pushed Galaxy to maintain global quality standards. They forced continuous improvement in ways that domestic customers might not.

The company's approach to global manufacturing was equally thoughtful. Rather than building factories everywhere, Galaxy concentrated production in India and Egypt (we'll explore this in the next section) while maintaining strategic inventory and technical centers globally. This hub-and-spoke model balanced cost efficiency with customer responsiveness.

What made Galaxy's global expansion particularly impressive was its timing. The 2000s saw an explosion in natural and organic personal care products, especially in developed markets. Consumers wanted sulfate-free shampoos, paraben-free moisturizers, and naturally-derived ingredients. This trend played perfectly to Galaxy's strengths. Their amino acid-based surfactants and plant-derived ingredients were exactly what formulators needed.

Galaxy also benefited from a broader shift in global supply chains. Multinational companies were increasingly adopting "supplier rationalization" strategies—working with fewer, more capable suppliers rather than managing hundreds of small vendors. Galaxy positioned itself perfectly for this consolidation. They could supply multiple ingredients, provide technical support, and deliver globally. For a procurement manager at P&G or L'Oréal, Galaxy was a one-stop shop.

The financial metrics from this period tell a story of successful transformation. International revenue grew from under 30% of total sales in 2000 to over 65% by 2010. The company was now serving 1,400+ customers across 70+ countries. More importantly, the customer mix had shifted. While Galaxy still served large multinationals, they now also supplied hundreds of small and medium brands—the indie beauty companies that would drive the next wave of innovation in personal care.

The global expansion also changed Galaxy's internal culture. English became the working language. Young engineers were sent on international assignments. The company recruited talent from competitors and customers. This wasn't just an Indian company selling globally—it was becoming a truly global company that happened to be headquartered in India.

Yet throughout this expansion, Galaxy maintained its core discipline. They didn't chase growth for growth's sake. Every new market, every acquisition, every investment was evaluated through the lens of strategic fit. Does it strengthen our position in surfactants and specialty ingredients? Does it deepen customer relationships? Does it enhance our technical capabilities? If the answer wasn't a clear yes, Galaxy walked away.

The decade ended with Galaxy at an inflection point. They had successfully transformed from an emerging market player to a global supplier. They had proven that an Indian company could compete—and win—in developed markets. But the next challenge would be different: scaling manufacturing to meet growing global demand while maintaining the agility that had brought them success. The answer would lie in an unexpected place: the deserts of Egypt.

V. Scaling Manufacturing: The Egypt Gamble & India Expansion (2010–2018)

In 2011, as the Arab Spring convulsed the Middle East and global markets still reeled from the financial crisis aftershocks, Galaxy made one of its boldest moves yet. In 2011, Galaxy commissioned manufacturing plants at Zaghadia in Gujarat and Suez in Egypt at the cost of ₹330 crore. To understand the audacity of this decision, consider the context: Egypt was in political turmoil, having just overthrown Hosni Mubarak. Most multinational companies were pulling out, not investing hundreds of crores in new facilities.

But Unnathan Shekhar and his team saw what others missed. Egypt's strategic location offers companies a platform for their commercial activities into the Middle East and Africa. The Suez facility wasn't just about serving Egypt—it was about accessing the entire MENA region, a market with hundreds of millions of people with large consumption and importing more than 75% of its overall consumption in all areas of life.

The Egypt gamble revealed Galaxy's sophisticated understanding of global supply chains. The MENA region represented a unique opportunity: rapidly growing populations, increasing disposable incomes, and a cultural emphasis on personal grooming that drove high per-capita consumption of personal care products. But serving this market from India had limitations—shipping costs, lead times, and most importantly, the inability to respond quickly to local market needs.

Galaxy Chemicals Egypt Company, owned by Galaxy Surfactants Ltd, India, was established in 2009 for the production of surfactants and chemicals used in the personal care industry. The Suez facility, located in the Public Free Zone, offered several strategic advantages: duty-free imports of raw materials, proximity to both African and Middle Eastern markets, and access to the Mediterranean for European exports.

The technical specifications of the Egypt plant demonstrated Galaxy's evolution as a company. This wasn't a simple contract manufacturing facility—it was designed to produce specialty surfactants and sunscreen actives that met the highest global standards. The plant incorporated advanced safety systems, automated production controls, and flexibility to switch between different product grades quickly.

Meanwhile, the parallel expansion at Jhagadia in Gujarat addressed a different strategic imperative. India's domestic market was exploding. The rise of the Indian middle class, combined with the penetration of organized retail and e-commerce, was driving unprecedented demand for personal care products. The Jhagadia facility, with its proximity to Gujarat's petrochemical hub, ensured Galaxy could serve this growing domestic demand while maintaining its export commitments.

The timing of these expansions proved prescient. Between 2010 and 2018, the global personal care market underwent a fundamental shift. Natural and organic products moved from niche to mainstream. Sulfate-free became a marketing mantra. Consumers in emerging markets began demanding the same quality products as their developed market counterparts. Galaxy's expanded capacity meant they could ride these waves rather than watch them pass by.

In 2012, Galaxy became a member of Roundtable on Sustainable Palm Oil, taking a step towards creating a sustainable palm oil supply chain. This wasn't just greenwashing—it was strategic positioning. Palm oil derivatives are crucial raw materials for surfactants, and sustainable sourcing was becoming a non-negotiable requirement for global brands. By joining RSPO early, Galaxy signaled to customers that they understood where the industry was heading.

The sustainability pivot extended beyond raw materials. Galaxy invested in zero liquid discharge systems, solar power, and waste heat recovery. These weren't just compliance measures—they were competitive advantages. When L'Oréal or Unilever audited suppliers for sustainability metrics, Galaxy consistently scored at the top.

By the financial year 2022-2023, Galaxy reported a production capacity exceeding 200,000 tons per annum. This represented a massive scale-up from the 30 metric tons they started with in 1980. But what's remarkable isn't just the absolute numbers—it's how Galaxy achieved this scale while maintaining flexibility. Their plants could produce over 200 different products, switching between them with minimal downtime.

The operational excellence required to manage this complexity was staggering. Consider: Galaxy was now running manufacturing operations across three continents, serving 1,400+ customers in 70+ countries, managing 200+ product SKUs, all while maintaining 98%+ on-time delivery rates. This required sophisticated ERP systems, predictive analytics for demand planning, and a supply chain organization that could handle everything from small specialty batches for indie beauty brands to massive bulk orders for P&G.

The period also saw a subtle but important shift in Galaxy's customer mix. While they continued to serve the giants, they increasingly focused on the "long tail" of smaller, innovative brands. These companies—the ones creating sulfate-free shampoos, CBD-infused skincare, or Ayurvedic formulations—needed suppliers who could provide both standard surfactants and custom solutions. Galaxy's technical capabilities and flexible manufacturing made them the perfect partner.

Financially, the expansion paid off handsomely. Revenue grew from around ₹850 crores in 2010 to over ₹2,500 crores by 2018. More importantly, EBITDA margins improved despite the capital investments, proving that scale and specialization could coexist. The company remained virtually debt-free throughout this expansion, funding growth through internal accruals—a testament to their cash generation capabilities.

As 2018 approached, Galaxy stood at another crossroads. They had built world-class manufacturing capabilities, established a global presence, and proven their ability to compete with anyone. But to take the next leap—to truly become a global leader rather than a successful challenger—they needed something more. They needed access to capital markets, transparency in governance, and the credibility that comes with being a listed company. The time had come to go public.

VI. Going Public: The 2018 IPO Story

The boardroom at Galaxy's Navi Mumbai headquarters was unusually quiet on January 28, 2018. Tomorrow, the company would open its IPO for subscription—seven years after their first failed attempt. This was the company's second attempt to go public. Earlier in 2011, Galaxy Surfactants had tried to raise over Rs 200 crore through an IPO but withdrew due to tepid response from investors. Now, with markets at all-time highs and investor sentiment bullish, they were trying again. But this time was different—completely different.

Galaxy Surfactants IPO was a bookbuilding issue of ₹937.09 crores, entirely an offer for sale of 0.63 crore shares. No fresh capital was being raised. This wasn't about funding expansion—Galaxy was already debt-free and generating substantial cash. This was about something more strategic: liquidity for early investors, transparency for global customers, and the credibility that comes with being a listed entity.

The structure of the IPO revealed careful thinking. The promoters were selling only a small portion of their holdings, ensuring they would retain 70.9% post-listing—a clear signal that the founders weren't cashing out but rather creating a public market for the stock while maintaining control. This high promoter holding would become a key selling point to investors: the founders were betting their entire wealth on Galaxy's future.

The IPO opened on January 29, 2018, and closed on January 31, 2018, with shares listing on BSE and NSE on February 8, 2018. The price band was set at ₹1,470-₹1,480 per share, valuing the company at approximately ₹3,700 crores. By global specialty chemical standards, this wasn't expensive. But by Indian market standards, where investors were used to manufacturing companies trading at single-digit P/E ratios, Galaxy was asking for a premium valuation.

The investment banking syndicate—led by ICICI Securities, Edelweiss Financial Services, and JM Financial—had their work cut out. How do you sell a B2B chemical company to retail investors who've never heard of surfactants? The answer lay in storytelling. The pitch wasn't about molecules and manufacturing—it was about being the invisible ingredient in products used by billions of consumers daily.

The roadshow presentations painted a compelling picture. Galaxy wasn't just a chemical company; they were an innovation partner to the world's biggest brands. They weren't selling commodities; they were providing solutions. The financials backed up the narrative: consistent revenue growth, expanding margins, negligible debt, and a return on equity exceeding 20%.

But the real masterstroke was the timing. India's consumption story was reaching an inflection point. GST had been implemented, formalization of the economy was accelerating, and premium personal care products were seeing explosive growth. Galaxy was perfectly positioned to benefit from all these trends.

The response was overwhelming. Galaxy Surfactants IPO subscribed 19.96 times overall—5.92 times in the retail category, 54.27 times in the QIB category, and 6.96 times in the NII category. The institutional oversubscription was particularly telling. These were sophisticated investors who understood the specialty chemical space, and they were voting with their wallets.

On listing day, February 8, 2018, Galaxy Surfactants opened at Rs 1,525 on NSE—a 3% premium to the issue price. On BSE, the stock listed at a 2.70% premium at Rs 1,520. The modest listing gains might have disappointed momentum traders, but they reflected something more important: the IPO was fairly priced. This wasn't a pop-and-drop story—it was the beginning of a long-term value creation journey.

The stock closed its first day at 14.74% higher than the issue price, suggesting that once investors digested what Galaxy actually did, they recognized the value. The company had successfully transitioned from a closely-held private entity to a publicly-traded corporation without drama or controversy.

The post-IPO period brought immediate changes. Quarterly earnings calls became events where Unnathan Shekhar had to explain surfactant chemistry to fund managers. The company had to adapt to the 24/7 scrutiny of public markets—every raw material price movement, every customer win or loss, every margin fluctuation was now analyzed and questioned.

But public listing also brought unexpected benefits. Global customers, particularly in Europe and North America, viewed the IPO as a validation of Galaxy's governance and transparency. The ability to offer stock options helped attract talent from competitors and multinationals. The public valuation made acquisitions easier to negotiate and finance.

More subtly, being public changed Galaxy's internal culture. The quarterly reporting rhythm imposed discipline. The need to communicate strategy clearly to investors forced management to articulate their vision more precisely. The stock price became a daily scorecard that everyone from the CEO to the shop floor could track.

Looking back, the 2018 IPO wasn't just a financial event—it was a coming-of-age moment. Galaxy had spent 38 years building a world-class specialty chemical company. Now they had the platform to show the world what they had built. The premium valuation wasn't just recognition of past achievement; it was a bet on future potential.

As Unnathan Shekhar would later reflect, going public was never about the money—Galaxy didn't need capital. It was about institutionalizing the company, creating wealth for employees, and most importantly, ensuring Galaxy could outlive its founders. The high promoter retention sent a clear message: this wasn't an exit, it was a new beginning.

VII. The Business Model: B2B2C at Scale

To understand Galaxy's business model, imagine a pyramid. At the base are billions of consumers using shampoo, toothpaste, and detergent daily. At the apex are a handful of global FMCG giants—P&G, Unilever, L'Oréal. Galaxy sits invisibly in the middle, the crucial link that makes the whole system work. This B2B2C model—business to business to consumer—is deceptively simple but extraordinarily powerful when executed well.

The company offers 215+ products under Performance Surfactant and Specialty Care Products, covering hair care, oral care, home care, skin care, cosmetics, and toiletries. But these aren't just random chemicals—each product represents a solution to a specific formulation challenge. Need a sulfate-free shampoo that still foams richly? Galaxy has a mild surfactant for that. Want a face wash that cleanses without stripping natural oils? There's an amphoteric surfactant designed precisely for that pH range.

Performance surfactants account for 60% of revenue and specialty personal care products account for the rest. This 60-40 split isn't accidental—it's strategic portfolio management at its finest. Performance surfactants are the workhorses: sodium lauryl sulfate, fatty alcohol ethoxylates, the ingredients that do the heavy lifting in cleaning products. They're relatively commoditized, with pricing tied to raw material costs, but they provide steady cash flow and economies of scale.

The specialty care products—that remaining 40%—are where the magic happens. These include preservative blends optimized for specific formulations, UV filters that don't leave white residue on dark skin, proteins that actually penetrate hair shafts rather than just coating them. These products command margins 2-3x higher than performance surfactants because they solve problems that commodity ingredients can't.

Galaxy has over 1400 clients including Colgate-Palmolive, Dabur, Himalaya, L'Oréal and Unilever and more. This customer diversification is crucial. The largest customer accounts for less than 15% of revenue. Compare this to typical automotive suppliers who might have 40-50% concentration with a single OEM. Galaxy's approach reduces risk but requires managing complexity—1,400 customers means 1,400 different sets of specifications, delivery schedules, and payment terms.

According to Unnathan Shekhar, managing director of Galaxy Surfactants, two-thirds of their business comes from international customers. This international skew isn't just about market size—it's about margin structure. International customers, particularly in developed markets, are willing to pay premiums for reliability, technical support, and innovation. A specialty surfactant sold to a French cosmetics brand might generate 3x the margin of the same molecule sold to an Indian soap manufacturer.

The customer acquisition process reveals the depth of Galaxy's moat. When a potential customer approaches Galaxy, they don't just want a price quote—they want a partner who understands their entire formulation. Galaxy's technical teams will analyze the customer's existing products, identify improvement opportunities, and often develop custom solutions. This consultative selling process can take 12-18 months for a new customer, but once established, these relationships typically last decades.

Switching costs in this business are enormous—and Galaxy has engineered them to be even higher. When a customer uses a Galaxy surfactant in their shampoo, that ingredient becomes part of their regulatory filing. Changing suppliers means reformulation, stability testing, regulatory reapproval—easily a year-long process costing millions. Galaxy doesn't just sell ingredients; they become embedded in their customers' products at a molecular level.

The innovation engine is central to the model. In 2020, the company spent nearly ₹60 crore and filed for 62 patents. But these aren't breakthrough drug discoveries requiring billions in R&D. Galaxy's innovations are incremental but valuable: a surfactant that works in hard water, a preservative system that extends shelf life by three months, a pearlizing agent that creates the perfect shimmer in a premium shampoo.

The manufacturing strategy supports this complexity beautifully. Galaxy's plants are designed for flexibility, not just scale. A single reactor can produce dozens of different products by adjusting temperature, pressure, and reaction time. This allows Galaxy to offer small-batch specialty products to indie beauty brands while simultaneously fulfilling bulk orders for multinationals.

Pricing power in this business is nuanced. For performance surfactants, Galaxy is largely a price-taker—when palm oil prices rise, they pass through the costs with a lag. But for specialty products, pricing is value-based. A UV filter that enables a sunscreen brand to claim "invisible protection" might represent 5% of the formula cost but enable a 30% price premium at retail. Galaxy captures a portion of that value creation.

The working capital dynamics are fascinating. Galaxy maintains 60-90 days of inventory—seemingly high for a chemical company. But this inventory isn't idle; it's strategic. When you're serving 1,400 customers across 70 countries with 200+ products, stockouts aren't just lost sales—they're relationship breakers. The inventory is the price of reliability.

What's particularly clever about Galaxy's model is how they've avoided the commodity trap that ensnares most chemical companies. They don't make the base chemicals—fatty alcohols, ethylene oxide—that have brutal economics. Instead, they start with these commodities and add value through chemistry and application knowledge. It's the difference between selling flour and selling cake—same base ingredients, vastly different economics.

The sustainability of this model comes from alignment. Galaxy wins when their customers win. If a Galaxy ingredient helps a shampoo brand gain market share, Galaxy's volumes grow. If a new preservative system extends shelf life and reduces waste, both Galaxy and their customer benefit. This isn't a zero-sum game where Galaxy's gains come at customers' expense.

Looking at the numbers, the model's efficiency is striking. Company is almost debt free. This isn't because Galaxy doesn't have investment opportunities—it's because the business generates so much cash that external funding isn't needed. Return on capital employed consistently exceeds 20%, remarkable for a manufacturing business.

The B2B2C model also provides unique market intelligence. Galaxy sees trends before they hit retail shelves. When Korean beauty brands started ordering specific texturizing agents, Galaxy knew K-beauty was about to go global. When orders for sulfate-free surfactants spiked, they anticipated the clean beauty wave. This forward visibility allows Galaxy to position inventory and R&D ahead of trends, not behind them.

As we'll see in the next section, this powerful business model would be tested by unprecedented challenges in the modern era—raw material volatility, changing consumer preferences, and new competition. But the foundation was solid, built on four decades of trust, innovation, and an obsessive focus on making their customers successful.

VIII. Modern Era: Challenges & Opportunities (2018–Present)

The post-IPO era brought immediate reality checks. Current financials tell a sobering story: Revenue of ₹4,221 Cr and Profit of ₹305 Cr look healthy in absolute terms, but the company has delivered a poor sales growth of 10.2% over past five years. For a company that had grown at 15-20% annually for decades, this deceleration was jarring.

In Q4 FY 2024-25, the company demonstrated resilience amid a challenging market landscape, reporting a consolidated EBITDA of INR 135 crores, driven by effective cost management and a focus on volume growth over margins. While demand in regions like India and Africa remained subdued due to macroeconomic pressures and rising raw material costs, there is cautious optimism for recovery, particularly in international markets.

The challenges were multifaceted. Raw material volatility reached unprecedented levels. Palm oil derivatives, which constitute 40-50% of Galaxy's raw material costs, saw price swings of 30-40% within quarters. Fatty alcohols, another key input, faced supply disruptions as global capacity struggled to keep pace with demand. The anticipated recovery in demand remained elusive, impacted by the lingering effects of the previous quarter's slowdown and a sharp rise in fatty alcohol prices from Q2 onwards.

But the real disruption came from changing consumer preferences. The clean beauty movement, which Galaxy had anticipated and prepared for, morphed into something more radical. Consumers weren't just avoiding sulfates—they were questioning surfactants altogether. "No-poo" movements, solid shampoo bars, and waterless formulations challenged the very premise of Galaxy's business.

Galaxy's response revealed strategic maturity. Rather than fight these trends, they embraced them. The commitment to innovation is evident through recent product launches, especially in the biosurfactants segment, despite ongoing supply chain disruptions. Biosurfactants—produced by microorganisms rather than chemical synthesis—represented the future of sustainable cleaning. Galaxy invested heavily in fermentation technology, partnering with biotech startups to develop next-generation ingredients.

The specialty ingredients pivot accelerated. Galaxy launched products targeting specific consumer concerns: anti-pollution actives for urban markets, microbiome-friendly surfactants for sensitive skin, and naturally-derived preservatives for clean beauty brands. These weren't me-too products—they were genuine innovations backed by patents and clinical data.

K. Natarajan, Managing Director, Galaxy Surfactants, said: "Q3FY25 has been a slow quarter for us primarily impacted by the slowdown in India. While the festive season failed to reignite demand in India, an improving supply chain scenario supported by a stable inflationary environment ensured QoQ improvement in our AMET Volumes. Despite seasonal holidays, demand momentum remained strong in ROW markets".

The geographic performance divergence was striking. ROW continued to be the bright spot and delivered a strong performance for Q4 and FY25. This reflects our strategic focus on expanding our global footprint and meeting the growing demand for masstige specialties, particularly in Europe, APAC, North America, and Latin America. We registered volume growth of 9% and 17% for Q4 FY25 and FY25, respectively.

This international strength offset domestic weakness. India, which had been Galaxy's growth engine for decades, faced structural headwinds. Local FMCG companies, squeezed by competition from global giants and D2C startups, became increasingly price-sensitive. The shift from bar soaps to liquid cleansers, which should have benefited Galaxy, was slower than anticipated as price-conscious consumers stuck to traditional formats.

Management's strategic emphasis on customer relationships and tailored product offerings positions the company to adapt to evolving consumer preferences, particularly the shift towards liquid detergents. This wasn't just about following trends—it was about anticipating where the market would be in five years and positioning accordingly.

The operational metrics revealed both challenges and resilience. Key Highlights for Q4 FY25 were EBITDA per metric tonne (MT) stood at Rs 21,715, marking a 24% increase on QoQ. For FY25, EBITDA per MT stood at Rs 19,868, broadly in line with FY24 levels. Despite market volatility, this reflects our continued focus on operational efficiency and cost optimisation.

Supply chain disruptions added another layer of complexity. International logistics continue to face disruptions due to factors like the postponement of reciprocal tariffs by the USA and Congestion in key regions such as Europe, China, and Southeast Asia, which is impacting both export and import shipments. Despite these ongoing challenges, we are actively working to mitigate the impact on our operations by, engaging with multiple suppliers, and exploring alternative sourcing options.

Competition intensified from unexpected quarters. Chinese manufacturers, traditionally focused on commodity chemicals, began moving up the value chain into specialty ingredients. Indian competitors, backed by private equity, aggressively pursued market share with pricing strategies Galaxy couldn't match without sacrificing margins. Even customers became competitors as some large FMCG companies brought surfactant production in-house.

Yet Galaxy's response demonstrated why incumbent advantages matter in specialty chemicals. Their four decades of formulation data, customer relationships, and technical expertise couldn't be replicated overnight. When a customer needed a preservative system that worked in a specific pH range with particular actives, Galaxy could provide solutions in weeks while competitors took months.

The sustainability narrative became central to Galaxy's strategy. Beyond RSPO certification and green chemistry, Galaxy invested in lifecycle assessments, carbon footprint reduction, and circular economy initiatives. These weren't just CSR activities—they were business imperatives. European customers increasingly demanded Scope 3 emissions data. American brands wanted supply chain transparency. Galaxy's early investments in sustainability became competitive advantages.

Digital transformation, long neglected in the chemical industry, became a priority. Galaxy implemented AI-driven demand forecasting, IoT sensors for predictive maintenance, and digital twins for process optimization. The goal wasn't just efficiency—it was agility. In a world where consumer preferences changed monthly, not annually, Galaxy needed to respond faster.

Looking forward, the opportunities are as significant as the challenges. The global personal care market continues to grow at 4-5% annually. Emerging markets, particularly in Africa and Southeast Asia, are seeing explosive growth in middle-class consumption. The premiumization trend—consumers trading up to better products—benefits specialty ingredient suppliers like Galaxy.

The biosurfactants opportunity alone could transform the industry. As fermentation technology improves and costs decline, bio-based surfactants could capture 20-30% of the market by 2030. Galaxy's early investments position them to capture this shift, though success isn't guaranteed—every major chemical company is chasing the same opportunity.

However, geopolitical uncertainties and elevated freight costs continue to pose risks, necessitating a careful approach to capital expenditures and operational efficiency. The company that thrived in the stable environment of the 1990s and 2000s must now navigate a world of constant disruption.

As we transition to analyzing Galaxy's strategic playbook, it's clear that the modern era isn't about choosing between growth and profitability, innovation and efficiency, global and local. It's about achieving all simultaneously—a challenge that would test any management team, even one with four decades of experience.

IX. Playbook: Lessons in B2B Excellence

After four decades of building Galaxy from a garage startup to a global specialty chemical leader, what strategic lessons emerge? The playbook isn't about chemical formulations or manufacturing processes—it's about building a B2B champion in a market where being Indian was initially a disadvantage, not an advantage.

Lesson 1: Choose Your Niche, Then Own It Completely

Galaxy's fundamental insight was that breadth is the enemy of depth in B2B specialty chemicals. While competitors diversified into pharmaceuticals, agrochemicals, and other adjacent markets, Galaxy maintained an almost obsessive focus on surfactants for personal and home care. This wasn't limitation—it was liberation. By knowing every molecule, every application, every customer need in their specific domain, Galaxy became irreplaceable.

Consider the depth of this specialization: Galaxy doesn't just make "surfactants"—they make 215+ specific grades, each optimized for particular applications. A sulfate for shampoo isn't the same as a sulfate for body wash, which isn't the same as a sulfate for face cleanser. This granular expertise creates switching costs that go beyond commercial contracts—they're embedded in customer knowledge and trust.

Lesson 2: Manage Complexity as a Competitive Advantage

Most companies view complexity as a cost to be minimized. Galaxy turned it into a moat. Managing 200+ products for 1,400+ customers across 70+ countries is operationally nightmarish. But this complexity creates value that simple, streamlined competitors can't match.

When an indie beauty brand in California needs 50 kilograms of a specialized mild surfactant, Galaxy can deliver it. When Unilever needs 500 tons of a commodity surfactant across three continents, Galaxy can handle that too. This range—from artisanal to industrial—requires systems, processes, and culture that take decades to build.

The key is making complexity invisible to customers. Galaxy's customers don't see the supply chain orchestration, the inventory management, the quality control systems. They just see reliable delivery of quality products. This "swan principle"—graceful on the surface, furious paddling underneath—is quintessential B2B excellence.

Lesson 3: Capital Efficiency Beats Capital Intensity

Company is almost debt free—a remarkable achievement for a capital-intensive manufacturing business. This isn't about being conservative; it's about being smart. Galaxy recognized that in specialty chemicals, the highest returns come from innovation and customer intimacy, not from the biggest factories.

Rather than building massive plants that require high utilization to break even, Galaxy built flexible facilities that could switch between products quickly. This meant higher unit costs but also higher value capture. A reactor that can make 20 different products is more valuable than one that makes a single product at the lowest possible cost.

The capital efficiency extends to working capital management. Galaxy maintains higher inventory levels than pure financial logic would suggest—but this inventory is strategic. It's the buffer that ensures 98%+ on-time delivery. It's the flexibility to say yes when a customer needs an urgent order. In B2B, reliability is worth more than efficiency.

Lesson 4: Innovation in Increments, Not Breakthroughs

Galaxy's R&D philosophy challenges Silicon Valley-style disruption thinking. They don't seek breakthrough innovations that obsolete existing products. Instead, they pursue incremental improvements that solve specific customer problems. A surfactant that's 10% milder, a preservative that extends shelf life by two months, a pearlizer that creates a slightly better shimmer—these aren't revolutionary, but they create real value.

This incremental approach has two advantages. First, it's lower risk—you're building on proven chemistry rather than hoping for miracles. Second, it's harder to copy. A breakthrough innovation can be reverse-engineered. But hundreds of small improvements, embedded in customer relationships and applications knowledge? That's a much higher barrier.

Lesson 5: Build Trust Before Products

The chemical industry runs on trust. When you're supplying ingredients that go into products used on skin and hair, quality isn't negotiable. A single contamination incident can destroy decades of reputation. Galaxy understood this from day one.

Trust-building at Galaxy goes beyond quality certificates and audit compliance. It's about transparency when things go wrong, proactive communication about supply challenges, and sometimes saying no to orders they can't fulfill properly. This reputation for reliability becomes self-reinforcing—customers give Galaxy the benefit of the doubt during disruptions because history shows Galaxy will make it right.

Lesson 6: Geography as Strategy, Not Expansion

Galaxy's global footprint wasn't about planting flags on a map. Each geographic expansion served a specific strategic purpose. India for cost-effective manufacturing and emerging market proximity. Egypt for MENA market access and regulatory arbitrage. The United States for innovation credibility and customer intimacy. Germany for European technical leadership.

This selective expansion contrasts with the "go everywhere" approach of many emerging market multinationals. Galaxy recognized that presence without purpose is just cost. Every facility, every office, every technical center needs to strengthen the core value proposition or it shouldn't exist.

Lesson 7: The Trust Premium in Specialty Chemicals

In commodity chemicals, price is paramount. In specialty chemicals, trust commands a premium. Galaxy's ability to charge 10-20% premiums over Chinese competitors isn't about product superiority—often the molecules are identical. It's about everything around the molecule: technical support, regulatory documentation, supply security, and problem-solving partnership.

Building this trust premium takes decades and can be destroyed in moments. Galaxy's 70.9% promoter holding sends a powerful signal—the founders' wealth is tied to the company's reputation. This alignment creates accountability that customers value, especially when dealing with critical ingredients.

Lesson 8: Why Boring Businesses Can Be Beautiful Businesses

Surfactants will never be sexy. There's no surfactant equivalent of the iPhone launch, no TED talks about the future of foam. But this invisibility is actually an advantage. It keeps competition rational, valuations reasonable, and management focused on operations rather than optics.

Beautiful businesses share certain characteristics: predictable demand, high switching costs, rational competition, and steady cash generation. Surfactants check all these boxes. While software entrepreneurs chase unicorn valuations, Galaxy quietly compounds value at 15-20% annually—boring but beautiful.

Lesson 9: Customer Concentration vs. Customer Diversification

Galaxy's 1,400+ customer base might seem inefficient compared to businesses built on anchor clients. But this diversification is strategic risk management. No single customer can dictate terms. No single loss can crater the business. This independence allows Galaxy to walk away from bad deals and maintain pricing discipline.

Yet within this diversification, Galaxy maintains focus. They don't chase every customer—they target customers who value what Galaxy offers. A price-only buyer who switches suppliers for 2% savings isn't a Galaxy customer. A brand that needs technical partnership and supply security is.

Lesson 10: The Specialty Migration Strategy

Galaxy's journey from commodity to specialty didn't happen overnight—it was a 40-year migration. They started with basic surfactants, added technical service, developed application expertise, created custom solutions, and eventually became innovation partners. Each step up the value chain was deliberate and built on the previous level.

This migration strategy is replicable across B2B sectors. Start where you can compete, usually on cost or local presence. Add service layers that create stickiness. Develop expertise that customers value. Gradually shift mix toward higher-value products. Eventually, you're competing on capabilities, not costs.

The playbook's meta-lesson is that B2B excellence isn't about any single strategy—it's about consistency and coherence across all dimensions. Galaxy didn't always make perfect decisions, but their decisions aligned. Their focus on surfactants aligned with their R&D investments, which aligned with their customer targeting, which aligned with their geographic expansion.

This coherence creates compounding advantages. Customer relationships strengthen technical capabilities, which enable product innovation, which deepens customer relationships. It's a virtuous cycle that's hard to create and even harder to break.

X. Bear vs. Bull Case Analysis

The investment case for Galaxy Surfactants presents a fascinating study in contrasts. Bears see a company struggling with slowing growth in a commoditizing industry. Bulls see a resilient compounder with decades of runway ahead. Both perspectives have merit—the truth, as always, lies in the nuances.

The Bear Case: Storm Clouds Gathering

The bears' primary concern is growth—or rather, the lack thereof. The company has delivered a poor sales growth of 10.2% over past five years. For a company trading at premium valuations, this deceleration is troubling. The mathematics are unforgiving: if you're paying 25-30x earnings for 10% growth, you're betting on acceleration that hasn't materialized.

The margin pressure is equally concerning. Raw materials—primarily palm oil derivatives and petroleum-based feedstocks—constitute 65-70% of costs. Galaxy has limited pricing power in performance surfactants, which represent 60% of revenue. When raw material costs spike, margins compress, and the lag in price pass-through can destroy quarters of profitability.

Customer concentration risk lurks beneath the diversification narrative. Yes, Galaxy has 1,400+ customers, but the top 20 likely contribute 50-60% of revenue. These are sophisticated buyers—P&G, Unilever, L'Oréal—with enormous procurement power. As these giants face their own growth challenges, they're squeezing suppliers. Galaxy might be a preferred vendor, but preferred doesn't mean protected.

Chinese competition is intensifying. Chinese chemical companies, backed by government subsidies and massive scale, are moving up the value chain. They're offering specialty surfactants at 20-30% discounts to Galaxy's prices. While quality and reliability gaps exist, they're narrowing. In a recession, CFOs often override procurement's quality concerns.

The shift to natural and organic products threatens traditional surfactants at an existential level. Consumers increasingly want products with ingredients they can pronounce. "Sodium lauryl sulfate" doesn't pass the kitchen table test. While Galaxy is developing natural alternatives, their core expertise in synthetic chemistry becomes less relevant in a botanical world.

Technology disruption looms larger than most realize. Biotechnology companies are engineering microorganisms to produce surfactants through fermentation. Startups are creating solid formulations that eliminate surfactants entirely. Waterless products bypass the need for emulsification. Galaxy's chemical expertise might become obsolete faster than anticipated.

The end-market maturity in developed countries caps growth potential. Personal care consumption in the US, Europe, and Japan grows at GDP rates or lower. The premiumization trend has limits—there's only so much consumers will pay for shampoo. Galaxy's international revenue exposure means they're tied to slow-growth markets.

Regulatory risks are mounting globally. The EU's REACH regulations increase compliance costs and limit certain chemistries. California's Proposition 65 creates labeling nightmares. India's environmental regulations are tightening. Each new rule adds cost and complexity, particularly challenging for a company with 200+ products.

The Bull Case: Compounding Through Complexity

The bulls start with management quality and alignment. Promoter Holding: 70.9% isn't just a number—it's a statement. The founders have kept nearly three-quarters of their wealth in the business after 44 years. They've seen cycles, competition, and disruption. Their continued commitment suggests confidence in Galaxy's future.

The balance sheet provides enormous flexibility. Company is almost debt free, generating consistent cash flow, with returns on capital exceeding 20%. This financial strength allows Galaxy to weather commodity cycles, invest counter-cyclically, and pursue acquisitions without dilution. In a downturn, Galaxy can gain share while leveraged competitors struggle.

The emerging market opportunity remains massive. India's per-capita consumption of personal care products is 1/10th of developed markets. Africa's young population is entering the consumer class. Southeast Asia is premiumizing rapidly. Galaxy's established presence in these markets positions them to capture decades of growth.

The specialty product mix shift is accelerating. While overall growth has slowed, specialty care products are growing faster and carry higher margins. Each year, the mix improves slightly—a 1-2% shift annually compounds significantly over time. This isn't visible in headline numbers but drives underlying value creation.

ESG leadership creates competitive advantages. Galaxy's RSPO certification, zero discharge facilities, and renewable energy investments aren't just compliance—they're differentiators. Global brands increasingly mandate sustainability from suppliers. Galaxy's early investments make them a preferred partner for ESG-conscious customers.

The innovation pipeline suggests better days ahead. The commitment to innovation is evident through recent product launches, especially in the biosurfactants segment. Biosurfactants, natural preservatives, and microbiome-friendly ingredients represent new growth vectors. These products command premium pricing and face less commoditization pressure.

Deep customer relationships create switching costs beyond economics. Galaxy's technical teams are embedded in customers' R&D processes. They understand formulation challenges, regulatory requirements, and market dynamics. Switching to a cheaper Chinese supplier means losing this partnership value—a cost that doesn't appear in procurement spreadsheets.

The global supply chain realignment benefits Galaxy. Post-COVID, companies are diversifying away from China-only sourcing. India's manufacturing competitiveness is improving. Galaxy offers the scale, quality, and reliability that global customers need from alternative suppliers. This "China Plus One" strategy creates a multi-year tailwind.

Valuation remains reasonable for quality. While not cheap in absolute terms, Galaxy trades at a discount to global specialty chemical peers. Companies like Croda and Evonik trade at 30-40x earnings. If Galaxy successfully executes its specialty migration, multiple expansion could drive returns beyond earnings growth.

The Network effects in B2B are underappreciated. Each new customer makes Galaxy more valuable to existing customers—more R&D investment, better supply chain economies, deeper technical expertise. This isn't winner-take-all like consumer platforms, but steady accumulation of advantages that compound over time.

The Synthesis: Navigating Nuance

The reality is that both bears and bulls are partially right. Galaxy faces genuine challenges—slowing growth, margin pressure, and technological disruption are real. But they also possess durable advantages—customer relationships, technical expertise, and financial strength that shouldn't be underestimated.

The investment case ultimately depends on time horizon and belief in management execution. Short-term traders should probably avoid Galaxy—quarterly volatility from raw material costs and demand fluctuations will continue. Long-term investors might find an attractive opportunity if they believe in the specialty migration story and emerging market growth potential.

The key variables to monitor are: - Specialty product mix: If it reaches 50%+ in the next 3-5 years, the bull case strengthens significantly - Emerging market recovery: India and Africa returning to growth would reignite Galaxy's engine - Biosurfactant commercialization: Success here would validate innovation capabilities - Margin stability: Maintaining EBITDA margins at 12-13% despite headwinds would demonstrate pricing power - Capital allocation: Smart acquisitions or capacity expansions could accelerate growth

The bear-bull debate reveals a larger truth about investing in B2B companies: the exciting stuff—new products, market expansion, technological disruption—gets attention. But value creation often comes from the boring stuff—customer retention, operational efficiency, and incremental improvement. Galaxy embodies this paradox: a boring business in an exciting transition.

For potential investors, the question isn't whether Galaxy is good or bad—it's whether the current price adequately reflects both the risks and opportunities. At ₹8,390 crore market cap, you're paying for solid execution in a challenging environment. Whether that's expensive or cheap depends on your confidence in Galaxy's ability to navigate the next decade as successfully as they've navigated the last four.

The ultimate test will be whether Galaxy can maintain its relevance as the industry evolves. Surfactants will still be needed in 2035—but will they be the same surfactants made the same way? Galaxy's answer to that question will determine whether the bears or bulls are ultimately proven right.

This analysis represents a comprehensive examination of Galaxy Surfactants based on publicly available information. The complexity of the specialty chemicals industry, combined with Galaxy's unique positioning, makes this neither a simple growth story nor a value trap, but rather a study in industrial evolution and the challenges of building a global B2B champion from India.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube