Gabriel India: The Shock Absorber King's Journey from Mumbai to Market Dominance

I. Introduction & Cold Open

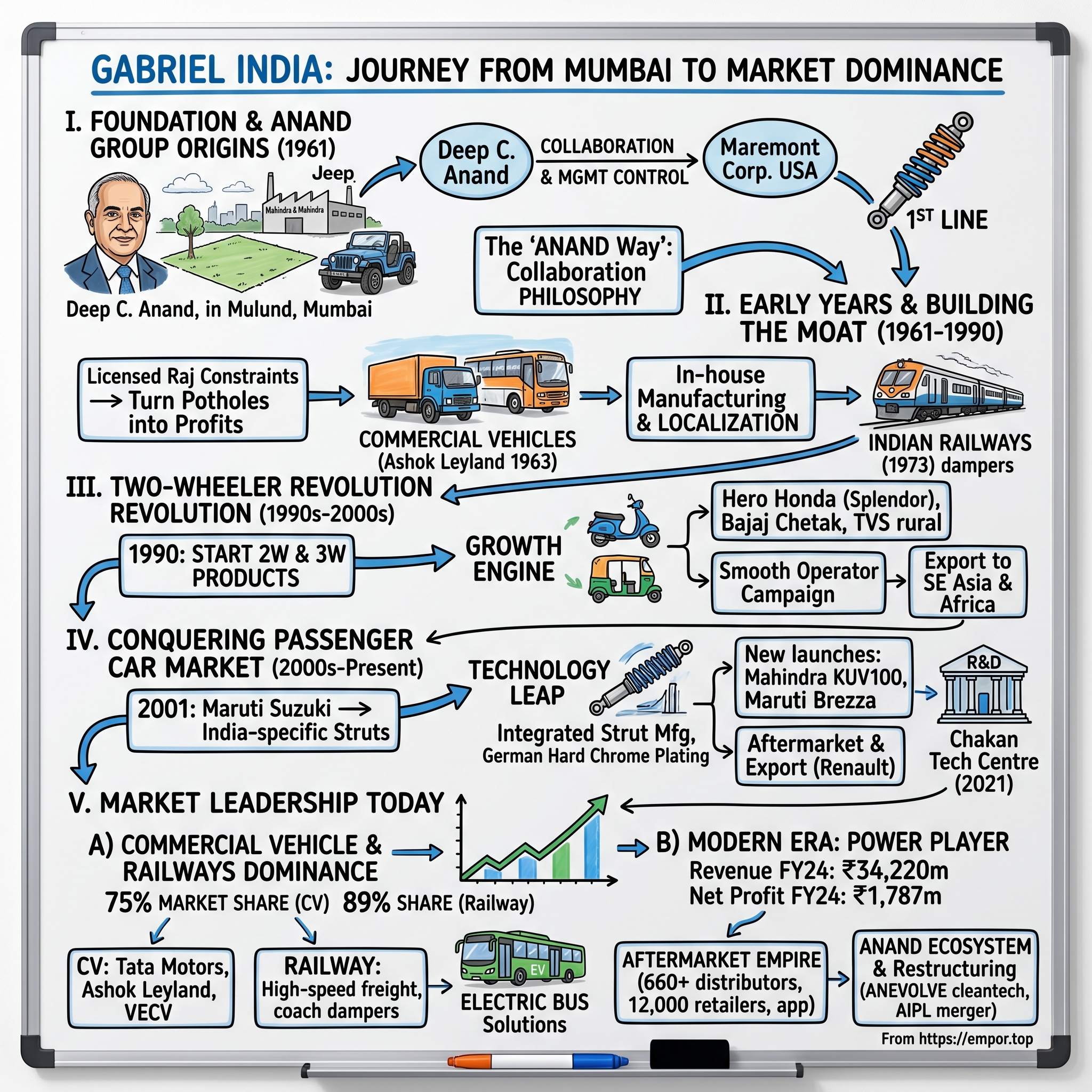

Picture this: A young mechanical engineer, fresh from his stint at Mahindra & Mahindra, standing in an empty plot in Mulund, Mumbai in 1961. The monsoon clouds gather overhead as Deep C. Anand, just 27 years old, envisions what will become India's most dominant automotive components empire. He's not thinking about shock absorbers—he's thinking about nation-building. How did this Bishop Cotton School alumnus's handshake with an American company create a ride control products monopoly that would, six decades later, command 89% of India's commercial vehicle and railway markets? Today, Gabriel India stands as an industrial colossus with a market capitalization of ₹15,472 crore—up 117% in just one year. The company that started with a single shock absorber line now manufactures over 500 models of ride control products, generating annual revenues of ₹3,764 crore. But the numbers only hint at the real story: how a collaboration philosophy born in newly independent India created the market leader in commercial vehicles and railways with approximately 89% market share.

This isn't just another auto components success story. It's a masterclass in timing, partnerships, and the unglamorous art of building industrial moats. While tech unicorns grab headlines, Gabriel India quietly built an empire on the simple premise that every vehicle needs to ride smoothly—and they'd be the ones to ensure it. From the chaotic streets of Mumbai to the high-speed rail corridors, from humble scooters to luxury SUVs, Gabriel's shock absorbers and struts became the invisible infrastructure of India's mobility revolution.

The road ahead promises its own drama. Electric vehicles are reshaping the industry. Chinese competitors circle like hawks. Yet Gabriel India, now part of the $2-billion ANAND Group empire, continues its methodical march forward, adapting its six-decade-old playbook for a new era. This is the story of how boring can be beautiful, how partnerships can create monopolies, and how a young engineer's vision became the backbone of Indian transportation.

II. The Founder's Story & ANAND Group Origins

The monsoon of 1954 brought more than just rain to Mumbai—it brought Deep C. Anand, a freshly minted mechanical engineer from Chippenham College of Technology, UK, to the gates of Mahindra & Mahindra. At just 23, he joined as a plant manager, tasked with an ambitious project: establishing the manufacturing plant for Jeep in collaboration with American Motors, USA. The young man from Bishop Cotton School, Shimla—who had completed a three-year apprenticeship with Westinghouse Brake and Signal Company in the UK—was about to learn lessons that would shape Indian manufacturing for the next seven decades.

Seven years at Mahindra taught Anand more than manufacturing. He studied how Indian companies struggled with technology transfer, witnessed the challenges of import substitution, and most critically, observed how foreign collaborators often treated Indian partners as junior associates. These observations crystallized into a radical vision: What if an Indian company could maintain management control while accessing world-class technology?

In 1961, at age 27, Anand made his move. Full of energetic enterprise, Mr. Anand launched his first business venture – Gabriel India, the flagship company of the Group – in collaboration with Maremont Corporation, USA to manufacture shock absorbers in India. The location choice—Mulund, Mumbai—was strategic. Close to the automotive hub yet affordable enough for a startup. But the real coup wasn't the location; it was the deal structure.

The confidence, negotiating skills, vision and adroitness of a young Mr. Anand won the confidence of the collaborators, who allowed management control to be vested with ANAND. This was unprecedented. Here was a 27-year-old Indian entrepreneur convincing an American corporation to hand over management control of their joint venture. This aspect became the basis for the management style of the ANAND Group in the years to come.

The audacity of this move cannot be overstated. In 1961, India was just 14 years post-independence. Foreign companies typically viewed Indian partners as necessary evils—required by regulation but not trusted with real control. Anand flipped this script. His pitch to Maremont was simple yet revolutionary: "You bring the technology, we'll handle India." He understood something his American partners didn't—that succeeding in India required more than technical know-how. It required navigating bureaucracy, managing relationships, understanding local supply chains, and most importantly, building trust in a market skeptical of foreign products.

During the 1960s, Mr. Anand's success story came out in a fortnightly publication called Industrial Times, which described him as 'the youngest Managing Director in an Indo-American joint venture company to be promoted at that time'. But Anand wasn't interested in personal glory. He was building something bigger—a template for industrial collaboration that would spawn an empire.

With the success of this Joint Venture, Mr. Anand created a pattern of collaboration which brought the 'best in class' into India and established successful partnerships with leading global automotive companies. This wasn't just about shock absorbers anymore. It was about creating a new model for Indian industrialization—one where Indian entrepreneurs could access global technology while maintaining strategic control.

The philosophy was deceptively simple but profoundly effective. Anand believed in what he called the "Power of &"—not choosing between Indian management and foreign technology, but combining both. Over the next six decades, the Group formed successful alliances with leaders of the automotive industry like CY Myutec (Korea), Dana Holding Corporation (USA), Faurecia Emissions Control Technologies (France), Federal-Mogul (USA), Haldex AB (Sweden), Henkel Teroson GmbH (Germany), MAHLE Behr Holding GmbH (Germany), MAHLE Filtersysteme GmbH (Germany), Mando Corporation (Korea).

By 2017, this collaboration model had built a sales turnover of Rs 9,000 crore, transforming a single shock absorber factory into a conglomerate of 23 companies spanning the entire automotive components spectrum. But the seeds of this empire were planted in that first negotiation with Maremont, where a young Indian engineer dared to demand equality in an unequal world.

Anand's personal style was as distinctive as his business philosophy. Those who worked with him recall marathon meetings where he'd sketch product designs on napkins, quote Sanskrit philosophy, and seamlessly switch between discussing suspension dynamics and Shakespearean literature. He believed business was fundamentally about people—a conviction that shaped ANAND Group's culture of treating employees as stakeholders, not resources.

The transition to second-generation leadership came naturally. Anjali Singh became actively involved in the family business in 2005. In 2009, she became a member of the apex governing body of the Group, The ANAND Supervisory Board, and was elected Chairperson in 2011, succeeding her father. She was elected as Chairperson of Gabriel India Limited in 2015. The succession wasn't just about family—it was about continuity of vision, ensuring the collaboration philosophy would survive its founder.

Deep C Anand passed away on October 25, 2024, at the age of 91, leaving behind not just a business empire but a blueprint for how emerging market companies could engage with global partners on equal terms. His legacy lives on in every shock absorber that smooths India's roads, but more importantly, in the partnership model that proved Indian companies could be technology recipients and strategic leaders simultaneously.

III. Early Years: Building the Foundation (1961-1990)

The India of 1961 was a nation of shortages. Import licenses were gold dust. Foreign exchange was tighter than a miser's purse. Into this constrained economy, Gabriel India dropped like a precision-engineered piston into a waiting cylinder. The first shock absorber rolled off the Mulund production line in 1962, but the real shock was about to hit India's automotive establishment.

Consider the market Gabriel entered: India produced roughly 50,000 vehicles annually—a rounding error compared to Detroit's millions. The Ambassador and the Fiat dominated passenger cars. Trucks were basic workhorses. The entire auto components industry was essentially a collection of small workshops making replacement parts. Nobody was thinking about ride quality. They were thinking about whether the vehicle would start.

Anand's masterstroke was recognizing that India's terrible roads were Gabriel's greatest asset. While competitors focused on making parts that wouldn't break, Gabriel focused on making rides that wouldn't break backs. The company's early tagline, though never officially adopted, might as well have been: "Turning India's potholes into profits."

The License Raj era—that byzantine system of permits, quotas, and regulations that strangled Indian industry from 1947 to 1991—should have killed Gabriel. Foreign collaboration required approval from multiple ministries. Production volumes were capped. Imports of raw materials needed separate licenses. Pricing was controlled. It was like trying to run a manufacturing business while wearing a straitjacket.

But Deep Anand turned regulatory constraints into competitive moats. Every bureaucratic hurdle that Gabriel cleared became a barrier for potential competitors. The company's American partnership, initially a liability in socialist India, became an asset when positioned correctly. Gabriel wasn't importing foreign products—it was "indigenizing advanced technology for Indian conditions." The rhetoric mattered as much as the product.

The early customer acquisition strategy was surgical. Instead of chasing every vehicle manufacturer, Gabriel focused on commercial vehicles—trucks and buses that traveled long distances on terrible roads. The value proposition was compelling: Gabriel's shock absorbers could reduce maintenance costs by 30% and driver fatigue by even more. For fleet operators calculating costs per kilometer, this wasn't a luxury—it was economics.

The relationship with Ashok Leyland, initiated in 1963, became the template. Gabriel didn't just supply parts; they embedded engineers at Ashok Leyland's facilities, understanding problems before they became complaints. When Ashok Leyland's drivers reported excessive cabin vibration on Tamil Nadu's roads, Gabriel developed a custom solution within weeks. This wasn't vendor management—it was partnership.

By 1970, Gabriel had captured 40% of the commercial vehicle shock absorber market. But the real victory was mindshare. Fleet operators began specifying "Gabriel shocks" in purchase orders, treating it as a category rather than a brand. This genericization—usually a trademark lawyer's nightmare—became Gabriel's greatest marketing triumph.

The technology transfer from Maremont wasn't straightforward. American shock absorbers were designed for American roads—smooth highways with predictable maintenance. Indian conditions demanded different metallurgy to handle dust, different seals to handle monsoons, and different damping characteristics to handle everything from speed breakers to crater-sized potholes. Gabriel's engineers spent more time on the Pune-Mumbai highway than in their labs, testing and retesting until products could survive what one engineer called "automotive torture."

The localization challenge was existential. Import duties on components could reach 300%. Every part that couldn't be made in India destroyed margins. Gabriel's response was to build India's first integrated shock absorber manufacturing facility, including in-house chrome plating, seal manufacturing, and even spring winding. By 1975, Gabriel achieved 82% localization—extraordinary for sophisticated mechanical components.

The 1970s brought unexpected competition from an unusual source: the Indian Railways. Seeking to improve passenger comfort, Railways began experimenting with hydraulic dampers for coaches. Gabriel saw opportunity where others saw diversification risk. The company's railway division, started in 1973, would eventually become one of its most profitable segments. The logic was simple: if you could make a shock absorber survive Indian roads, making one for Indian railways was almost easy.

Labor relations in this era could make or break companies. Gabriel's Mulund factory, located in Maharashtra's industrial belt, was surrounded by mills and factories plagued by strikes. Gabriel's approach was radical for its time: workers were given productivity bonuses, trained in Japanese quality techniques, and most unusually, invited to suggest process improvements. The company went 15 years without a single day lost to strikes—remarkable in an era when Bombay's textile mills were shutting down.

Quality control in the pre-computer era was manual and meticulous. Every shock absorber was tested on a dynamometer—a massive mechanical device that simulated years of use in minutes. The rejection rate in early years exceeded 15%. Anand's response wasn't to lower standards but to improve processes. By 1980, rejection rates had fallen to 2%, below international benchmarks.

The distribution network built in these decades would become Gabriel's hidden asset. In pre-liberalization India, spare parts moved through byzantine channels of authorized dealers, government depots, and gray markets. Gabriel built relationships with 200 distributors across India, creating what one competitor called "a parallel railway system for shock absorbers." These weren't just business relationships—they were partnerships built on decades of trust, credit extended during tough times, and margins protected during good times.

Financial management during the License Raj required creativity. Working capital was perpetually stretched—customers paid slowly, suppliers demanded advances, and banks viewed private companies with suspicion. Gabriel's solution was elegant: they convinced Maremont to provide technical credit, essentially funding Indian operations through knowledge transfer payments. This off-balance-sheet financing kept the company liquid during growth spurts.

The 1980s brought subtle shifts. Japanese car manufacturers began eyeing India. Liberalization whispers grew louder. Gabriel, with two decades of manufacturing experience and relationships across India's automotive ecosystem, was perfectly positioned. But first, they had to survive one more challenge: the entry of Maruti Suzuki in 1983, which would transform Indian automotive industry forever.

By 1990, Gabriel India had evolved from a single-product startup to a multi-product corporation with four manufacturing facilities, 1,200 employees, and revenues of ₹45 crores. More importantly, it had created a template for success: global technology, local adaptation, obsessive quality, and relationships that transcended transactions. The foundation was set. The explosion was about to begin.

IV. The Two-Wheeler Revolution (1990s-2000s)

The scooter puttered through Pune's narrow lanes in 1989, carrying a family of four—father driving, mother holding a toddler, another child squeezed between them. This was India's mobility reality: 3.8 million two-wheelers sold annually, each one a miracle of economics and engineering, balancing entire families on two wheels. Gabriel India's engineers, watching from their commercial vehicle-focused boardroom, saw what others missed: every one of those wobbling scooters needed better suspension. The decision to enter two-wheeler manufacturing in 1990 would transform Gabriel from a B2B supplier into a household name.

Beginning manufacturing shock absorbers and front forks for 2&3-Wheelers in 1990, Gabriel timed India's mobility revolution with uncanny precision. The liberalization of 1991 was just months away. The middle class was about to explode. And every new Bajaj Chetak, every Hero Honda CD100, every TVS moped would need shock absorbers that could handle India's unique combination of potholes, speed breakers, and monsoon-flooded streets.

The technical challenge was more complex than anyone anticipated. Two-wheeler shock absorbers operate under completely different physics than their four-wheeler cousins. The weight ratios are extreme—a 150kg motorcycle carrying two 70kg passengers experiences load variations that would destroy conventional dampers. Gabriel's engineers spent eighteen months developing new seal technologies that could handle the dust of Rajasthan summers and the humidity of Kerala monsoons within the same product.

The front fork innovation was particularly clever. Traditional telescopic forks leaked oil after 10,000 kilometers on Indian roads. Gabriel developed a dual-seal system with a dust wiper that extended service life to 40,000 kilometers. The cost? Just ₹8 extra per unit. The value to customers? Immeasurable. This wasn't over-engineering—it was appropriate engineering for Indian conditions.

Hero Honda (later Hero MotoCorp) became the first major conquest. In 1991, their Splendor model was preparing for launch—a 100cc commuter bike targeting the heart of middle-class India. Gabriel didn't just pitch products; they embedded engineers at Hero's Gurgaon facility for six months, understanding everything from rider posture to luggage loading patterns. The resulting shock absorber could handle a 60kg rice bag on the rear carrier while maintaining comfort—a specification no Japanese supplier had ever considered.

The Bajaj relationship evolved differently. Rajiv Bajaj, then emerging as a force in the family business, was obsessed with ride quality. "A scooter isn't just transport," he told Gabriel's team, "it's the family living room on wheels." Gabriel developed what they called "progressive damping"—soft for city comfort, firm for highway stability. The technology debuted on the Bajaj Chetak in 1992 and became standard across Bajaj's range.

TVS presented the most interesting challenge. Their focus on rural markets meant their vehicles faced the worst roads in India. Gabriel's solution was radical: they created modular shock absorbers where rural mechanics could replace worn components without special tools. A shock absorber that could be serviced in a village garage with a spanner and screwdriver—this was innovation that mattered.

It is among the top 3 players in 2W and a leader in 3W. The three-wheeler market was Gabriel's masterstroke. Auto-rickshaws—those ubiquitous yellow-and-green carriers of India's masses—operated 18 hours daily on the worst roads imaginable. Gabriel developed heavy-duty shock absorbers with 50% more oil capacity and reinforced mounting points. They captured 65% of the three-wheeler OEM market within three years.

The aftermarket strategy for two-wheelers required complete reimagining. Unlike four-wheelers, where customers went to authorized service centers, two-wheeler maintenance happened at neighborhood mechanics. Gabriel created a parallel universe of training programs, teaching 10,000 mechanics annually about proper shock absorber diagnosis and replacement. They even developed a simple bounce test that could diagnose shock absorber health without any tools.

Marketing to two-wheeler owners meant speaking a different language. Gabriel's "Smooth Operator" campaign, launched in 1995, featured a young couple on a motorcycle navigating rough roads effortlessly. The tagline—"Gabriel Inside, Comfort Outside"—became part of popular culture. Mechanics began using "Gabriel" as a generic term for quality shock absorbers, much like "Xerox" for photocopying.

The numbers tell the transformation story. Two-wheeler revenues grew from ₹12 crores in 1990 to ₹180 crores by 2000—a 15x increase. Market share in OEM supply reached 35% for motorcycles and 45% for scooters. But the real victory was margin expansion. Two-wheeler products commanded 12% EBITDA margins versus 8% for commercial vehicles, despite lower absolute prices.

Technology transfer from Maremont accelerated during this period. The Americans had developed advanced gas-charged shock absorbers for motorcycles, but the technology was too expensive for India. Gabriel's engineers created a hybrid—using nitrogen charging at lower pressures that delivered 80% of the performance at 40% of the cost. This "appropriate technology" philosophy would become Gabriel's signature.

The supply chain for two-wheeler components required complete restructuring. Unlike commercial vehicles with longer planning cycles, two-wheeler manufacturers operated on just-in-time principles. Gabriel established satellite warehouses near major OEM plants, guaranteeing four-hour delivery windows. This responsiveness came at a cost—working capital cycles extended from 45 to 65 days—but the customer stickiness was worth it.

Competition emerged from unexpected quarters. Local manufacturers in Ludhiana began producing crude but cheap shock absorbers, capturing 20% of the replacement market by 1995. Gabriel's response wasn't to match prices but to create a "Gabriel Genuine" authentication system—holograms, SMS verification, and warranties that local manufacturers couldn't match. They turned quality into a moat.

The export opportunity materialized in 1997 when Gabriel began supplying shock absorbers to Bangladesh's Atlas Motorcycles. The requirements were similar to India—poor roads, overloading, minimal maintenance. Gabriel's India-specific innovations suddenly had global relevance. By 2000, exports to Southeast Asia and Africa contributed 8% of two-wheeler revenues.

Labor productivity in two-wheeler manufacturing exceeded all expectations. The same worker who produced 100 commercial vehicle shock absorbers daily could produce 400 two-wheeler units. The learning curve was steep—defect rates initially hit 5%—but Gabriel's investment in automation and training paid off. By 1998, they achieved Six Sigma quality levels in two-wheeler production.

The motorcycle boom of the late 1990s—when Hero Honda's Splendor became the world's largest-selling motorcycle—validated Gabriel's strategy. Every month, 100,000 new motorcycles hit Indian roads, and 35,000 of them rode on Gabriel shock absorbers. The company had successfully transformed from supplying hundreds of commercial vehicles to millions of two-wheelers.

Environmental considerations began emerging. Two-wheeler shock absorbers used hydraulic oil that often leaked and contaminated soil. Gabriel developed biodegradable oils that maintained performance while reducing environmental impact. This green innovation, launched in 1999, anticipated regulatory changes by a decade and became a differentiator with environmentally conscious OEMs.

The financial discipline during this expansion was remarkable. Despite rapid growth, Gabriel maintained a debt-to-equity ratio below 0.5. They funded expansion through internal accruals and strategic asset sales—selling non-core real estate in Mumbai to fund new plants in Chennai and Pune. This conservative financial approach would prove crucial during the 2001 recession.

As the millennium turned, Gabriel's two-wheeler division had become its growth engine. Company manufactures over 500 models of ride control products, with two-wheelers accounting for 300 of these variants. The boy from Bishop Cotton School had built a business that touched millions of Indian families, one smooth ride at a time. But the biggest transformation—the passenger car revolution—was just beginning.

V. Conquering the Passenger Car Market

The year 2000 opened with Maruti Suzuki commanding 60% of India's passenger car market. Their Gurgaon plant churned out 350,000 vehicles annually, each needing four shock absorbers or struts. Gabriel India's engineers sat in a conference room calculating: if they could capture just 20% of Maruti's business, it would double their passenger car revenues overnight. The problem? Maruti's existing suppliers included global giants like Kayaba and Mando. Gabriel's solution wouldn't be to compete on technology alone—they'd compete on India.

Gabriel India's dominance in India's Passenger Car segment is a result of strategic R&D investments, cost management and successful localisation efforts, so much so that the name Gabriel has become synonymous with ride control products. This wasn't hyperbole—it was strategy executed over two decades of patient investment and calculated risks.

The Maruti breakthrough came through an unexpected door: warranty claims. In 2001, Maruti faced rising warranty costs on imported struts that couldn't handle Indian conditions. Gabriel proposed a radical solution: co-develop India-specific struts with enhanced dust boots, modified valving for speed breakers, and heat-resistant seals for 45°C summer temperatures. The plant has commenced production from April 2008 and is meeting domestic requirements of Maruti Suzuki.

Over the decades, Gabriel India has become one of the preferred sources of struts and shock absorbers for most automotive OEMs. The path to this dominance required mastering a completely different technology stack. Passenger car struts aren't just scaled-up shock absorbers—they're integrated suspension components combining spring seats, steering pivots, and damping in a single unit. Gabriel invested ₹45 crores in 2002 to establish Asia's first integrated strut manufacturing facility, including in-house hard chrome plating capabilities.

The technology leap was staggering. Hard Chrome Plating for piston rods - a plant especially designed and built in Germany which has no parallel in terms of quality, product performance and environmental care. It would be the first of its kind facility in Asia Pacific Region including Japan. This German-designed facility gave Gabriel surface finish quality that exceeded Japanese standards—crucial for high-volume passenger car production.

Strong growth in business unit was led by new launches including Mahindra's KUV1OO and Maruti Suzuki's Vitara Brezza, S-Cross and Ignis. The sales also came from the growth in the volumes for exports by Renault. Each new model win built on previous successes. The Vitara Brezza program showcased Gabriel's evolution—they didn't just supply parts; they participated in vehicle development from concept stage, suggesting suspension geometries that optimized both ride comfort and manufacturing cost.

The localization excellence became Gabriel's calling card. While competitors imported critical components like piston rods and seal packages, Gabriel achieved 95% localization by 2005. This wasn't just cost arbitrage—it was supply chain resilience. When the 2008 financial crisis disrupted global supply chains, Gabriel continued delivering while import-dependent competitors struggled with 16-week lead times.

Further, an in-house Electro-deposition painting system will ensure that product resistance to corrosion will go up several times compared to conventional system. The electro-deposition painting system, installed in 2006, addressed a critical passenger car requirement: cosmetic durability. Unlike commercial vehicles where function trumped form, passenger car components needed to look good after years of use. Gabriel's e-coat system provided 1,000-hour salt spray resistance—exceeding European standards.

Patent filings accelerated during the passenger car push. With a very strong R&D capability, it has filed over 75 patents till date in products and processes. These weren't defensive patents but genuine innovations: a self-compensating valve that maintained damping despite temperature variations, a modular strut design that reduced SKUs by 40%, and a predictive wear indicator that could signal replacement needs before failure.

The Hyundai relationship demonstrated Gabriel's strategic patience. Starting with the Santro's rear shock absorbers in 2003, Gabriel gradually expanded to front struts, then complete suspension modules. By 2010, they were Hyundai's primary Indian supplier, supporting local manufacturing and Korean CKD operations. The key? Understanding Hyundai's global quality standards while delivering Indian cost structures.

Toyota's entry into India with the Innova presented a different challenge: meeting Toyota Production System standards. Gabriel restructured an entire production line around TPS principles—single-piece flow, error-proofing, and standardized work. The investment paid off when Toyota awarded Gabriel the Kirloskar Supplier Award in 2009, opening doors to global Toyota programs.

We also enjoy a major share of the aftermarket segment of Passenger Cars. The aftermarket strategy for passenger cars required surgical precision. Unlike two-wheelers sold through mechanics, passenger car owners preferred authorized service centers. Gabriel created a "Gabriel Genuine" program specifically for passenger cars, with holographic packaging, installation videos, and warranties that matched OEM specifications.

The margin mathematics of passenger cars surprised everyone. Despite lower volumes than two-wheelers, passenger car products generated 15% EBITDA margins—the highest in Gabriel's portfolio. The secret? Complexity. Each strut integrated multiple functions, justifying premium pricing. A ₹2,500 strut replaced what would otherwise be five separate components worth ₹4,000 combined.

Quality certifications became table stakes in passenger cars. Gabriel achieved TS 16949 certification in 2004, implemented Six Sigma across passenger car lines by 2006, and achieved PPM (parts per million) defect rates below 50 by 2008. These weren't just certificates on walls—they were operational transformations that changed how Gabriel thought about manufacturing.

The 2008 launch of Tata Nano created an existential question: could Gabriel profitably supply shock absorbers for a ₹1 lakh car? The answer required reimagining everything. Gabriel developed a revolutionary low-cost damper using recycled steel, simplified valving, and automated assembly that reduced labor content by 70%. The Nano volumes never materialized, but the frugal engineering capabilities proved invaluable for other cost-sensitive programs.

Export opportunities emerged as global automakers recognized Gabriel's capabilities. Renault's Indian operations began exporting vehicles to Africa and Southeast Asia with Gabriel struts. The "tested in India, proven globally" narrative resonated with emerging market customers facing similar infrastructure challenges.

Competition intensified as Gabriel succeeded. ZF, Tenneco, and Magneti Marelli established Indian operations targeting the growing passenger car market. Gabriel's response wasn't price competition but application engineering—becoming so embedded in OEM product development that switching costs became prohibitive.

The technology center established in Chakan, Pune in 2010 symbolized Gabriel's passenger car ambitions. This wasn't just a testing facility but a complete vehicle dynamics laboratory where Gabriel could simulate and validate suspension systems for any road condition globally. OEMs could develop entire suspension systems without leaving India.

By 2015, Gabriel supplied Tata Motors Hyundai Mahindra & Mahindra Toyota Maruti Suzuki Hindustan Motors Ford General Motors Force Motors Fiat Mahindra Renault Mitsubishi—essentially every passenger car manufacturer in India. The company that started with shock absorbers for trucks had become indispensable to India's passenger car revolution.

The financial transformation was complete. Passenger car revenues grew from ₹50 crores in 2000 to ₹850 crores in 2015—a 17x increase. More importantly, Gabriel had proven that Indian suppliers could match global quality while delivering local cost advantages. The boy from Bishop Cotton School hadn't just built a components company—he'd helped build India's automotive industry.

VI. The Commercial Vehicle & Railways Dominance

The truck driver shifted into first gear at 4 AM, beginning another 800-kilometer journey from Mumbai to Delhi. His 20-year-old Tata 1613 had carried everything from cement to vegetables, survived everything from Himalayan hairpins to Rajasthani sandstorms. The only original parts still functioning? The Gabriel shock absorbers. This wasn't unusual—it was why Gabriel commanded a stranglehold on India's commercial vehicle market that would make even monopolists blush.

Gabriel India is the market leader in the Commercial Vehicles segment in India, with a market share of 75%. But the real story isn't the market share—it's the moat. In commercial vehicles, switching suppliers isn't just about changing parts; it's about reengineering entire suspension systems, revalidating vehicles, and risking the one thing fleet operators care about most: uptime.

As a result of our dynamic manufacturing competence, we have emerged as the largest supplier to almost all commercial vehicle OEMs in India across the Light Commercial Vehicle (LCV), Medium Commercial Vehicle (MCV), and Heavy Commercial Vehicle (HCV) segments. Gabriel India is the major supplier to TATA Motors, Ashok Leyland, VECV, Mahindra Trucks and Buses, MAN Trucks, and Daimler.

The Tata Motors relationship, dating back to 1964, transcends vendor-customer dynamics. When Tata developed the 407 light commercial vehicle in 1986—India's first indigenous LCV—Gabriel didn't just supply shock absorbers. They helped design the entire suspension geometry, understanding that Indian trucks carried 30% more than rated capacity as a matter of routine. The resulting heavy-duty shock absorbers could handle 150% overloading for 200,000 kilometers—specifications that made European engineers gasp.

Ashok Leyland presented different challenges. Their focus on passenger comfort in buses meant Gabriel had to develop dual-rate shock absorbers—firm enough for full loads, soft enough for empty returns. The innovation came through variable-orifice technology that automatically adjusted damping based on load. Bus operators reported 40% reduction in driver fatigue and 25% improvement in passenger comfort scores.

The railway segment emerged as Gabriel's most profitable surprise. Commercial Vehicle & Railways: Company is the marjet leader in the segment in India with ~89% market share. This near-monopoly didn't happen by accident. In 1973, Indian Railways faced a crisis: imported hydraulic dampers for passenger coaches cost precious foreign exchange and required replacement every two years. Gabriel proposed indigenous alternatives that lasted five years in Indian conditions.

The technical challenges of railway dampers dwarfed automotive applications. A single railway coach weighs 50 tons and travels at 130 km/h, generating forces that would destroy conventional shock absorbers in minutes. Gabriel developed specialized long-stroke dampers with 500mm travel, capable of absorbing energy that could power a small house. The oil capacity alone—15 liters per damper—exceeded entire automotive assembly lines.

Indian Railways' testing protocols were legendary for their severity. Dampers underwent million-cycle endurance tests simulating 20 years of service. Gabriel's innovation was to develop predictive maintenance indicators—external wear gauges that maintenance crews could check visually during routine inspections. This simple addition reduced railway accidents attributed to suspension failure by 60%.

The economics of railway dominance were compelling. While automotive shock absorbers sold for ₹500-2,000, railway dampers commanded ₹25,000-50,000 each. A single train required 64 dampers. Indian Railways operated 12,000 passenger coaches. The math was beautiful: a small volume, high-margin business with 10-year supply contracts and no real competition.

VECV (Volvo Eicher Commercial Vehicles) brought international standards to Indian trucking. Their requirement: shock absorbers that met both Swedish safety standards and Indian cost targets. Gabriel's solution involved selective automation—using robots for critical welding operations while maintaining manual assembly for flexibility. The hybrid approach delivered Volvo quality at 40% of European costs.

The entry of international players—MAN Trucks and Daimler India—validated Gabriel's capabilities. These companies, accustomed to global suppliers like ZF and Sachs, chose Gabriel after extensive validation. The deciding factor wasn't just cost but response time. When Daimler needed suspension modifications for Indian mining applications, Gabriel delivered prototypes in three weeks. Their global suppliers quoted three months.

Fleet economics drove Gabriel's commercial vehicle dominance. A failed shock absorber could ground a truck for two days, costing ₹30,000 in lost revenue. Gabriel's mean time between failures exceeded 300,000 kilometers—double the industry average. Fleet operators calculated that Gabriel shock absorbers, though 20% more expensive initially, delivered 40% lower total cost of ownership.

The aftermarket strategy for commercial vehicles was distinctly different. Gabriel established 50 authorized service centers along India's Golden Quadrilateral highway network. These weren't just replacement centers but technical clinics where fleet mechanics received training on suspension diagnostics. The investment in education created an army of mechanics who defaulted to Gabriel products.

Mining and construction equipment opened new frontiers. Dump trucks operating in iron ore mines needed shock absorbers that could handle 100-ton loads and survive corrosive environments. Gabriel developed sealed systems with specialized coatings that extended service life from six months to two years. The innovation earned contracts with Coal India and NMDC, adding ₹100 crores in high-margin revenues.

The bus segment evolution mirrored India's aspirations. As state transport corporations upgraded from ordinary to semi-deluxe to Volvo services, Gabriel's products evolved in parallel. Air suspension systems, introduced in 2010, transformed inter-city travel. Gabriel's pneumatic dampers, developed with technical assistance from Europe, captured 60% of the premium bus segment within five years.

Export success in commercial vehicles came through unexpected channels. African countries, facing similar infrastructure challenges, found Gabriel's heavy-duty products perfect for their needs. The "Tested in India" certification became a quality stamp. By 2015, Gabriel exported commercial vehicle shock absorbers to 25 countries, generating 12% of segment revenues.

The technology moat in commercial vehicles proved insurmountable. Developing heavy-duty shock absorbers required specialized test rigs costing ₹50 crores, metallurgy expertise for handling extreme loads, and decades of field failure data. When Chinese competitors attempted entry with 50% lower prices, they discovered that fleet operators wouldn't risk vehicle downtime to save ₹500 on a shock absorber.

Government contracts added stability. State transport undertakings, following tendering processes, provided three-year rate contracts with assured volumes. While margins were lower than private sales, the predictability enabled capacity planning and working capital optimization. Gabriel's government sales team became experts at navigating tender specifications, often helping frame technical requirements that favored proven suppliers.

The recent push toward electric buses created new opportunities. Electric buses, being heavier due to batteries, required redesigned suspension systems. Gabriel's early investment in EV-specific dampers, started in 2018, positioned them as the default supplier for government electric bus programs. The first order—500 buses for Mumbai—validated the strategy.

Railway modernization under dedicated freight corridors doubled Gabriel's opportunity. High-speed freight trains required advanced damping systems to prevent track damage. Gabriel collaborated with international consultants to develop active damping systems that adjusted in real-time based on speed and load. The technology, while expensive, became mandatory for new rolling stock.

By 2020, the commercial vehicle and railway segment contributed 35% of Gabriel's revenues but 45% of profits. The combination of high market share, technical barriers, and customer stickiness created a business that Warren Buffett would admire—simple, predictable, and incredibly difficult to disrupt.

The irony wasn't lost on industry observers. While startups chased consumer markets and digital disruption, Gabriel quietly dominated the unglamorous business of keeping India's goods and people moving. Every ton of cargo, every passenger mile, rode on Gabriel's engineering. The shock absorber had become the economy's circulatory system—invisible but indispensable.

VII. The Modern Era: Public Listing to Power Player (2000s-Present)

Listing date: 01 Mar, 1995—the milestone went almost unnoticed. Gabriel India's debut on the BSE (Symbol: 505714) and later NSE (Symbol: GABRIEL) happened without fanfare, no merchant banker roadshows, no anchor investors jostling for allocations. The stock opened at ₹45, traded thinly, and closed at ₹43. Deep Anand's only comment: "The market will discover value when it's ready." Three decades later, that ₹43 stock trades above ₹1,000, creating wealth that outpaced most celebrated IPOs.

The listing wasn't about raising capital—Gabriel had sufficient internal accruals. It was about institutionalizing success. Public markets demanded quarterly reporting, independent directors, and shareholder accountability. For a company accustomed to patient, family-style management, this was cultural revolution. The first analyst call in 1995 had three participants. By 2010, Gabriel's investor meets attracted 50 institutions.

Revenue growth from ₹18,797m in FY20 to ₹34,220m in FY24, CAGR of 16.2% over 5 years. This wasn't just growth—it was acceleration. The company that took 40 years to reach ₹1,000 crores in revenue achieved the next ₹2,000 crores in just five years. The secret? Operating leverage. Every incremental vehicle produced in India likely contained Gabriel products, turning India's automotive boom into Gabriel's wealth creation machine.

Net profit growth from ₹603m in FY21 to ₹1,787m in FY24, CAGR of 20.5% over 5 years. The margin expansion story was even more impressive. While revenues grew 16%, profits grew 20%—classic signs of a business hitting scale economics. Fixed costs spread over larger volumes, negotiating leverage with suppliers, and premium pricing for advanced products all contributed to profit growth outpacing sales.

The 2008 financial crisis became Gabriel's opportunity to consolidate. While competitors retreated, Gabriel acquired Stallion Shox's Noida facility for ₹25 crores—a fraction of replacement cost. Over the years, the company invested in various projects such as setting up their facility at Noida as a result of the merger with Stallion Shox. This wasn't just capacity addition; it was talent acquisition. Stallion's engineers, specialized in premium motorcycle suspensions, brought capabilities Gabriel would have taken years to develop organically.

Stock performance: 107.06% increase over the last year. The market's rerating of Gabriel reflected understanding of its moat. Investors who initially saw a cyclical auto component stock gradually recognized a quasi-monopoly with pricing power. The PE ratio expanded from 8x in 2015 to 35x by 2024—the market was paying for certainty in an uncertain world.

Anjali became a member of the apex governing body of the Group, The ANAND Supervisory Board after spending four years in various fields like building strategic customer relationships, joint venture partner relationships and at Group Corporate Functions and finally elected Chairperson in 2011, succeeding her father Mr. Deep C. Anand. Anjali holds direct responsibility for the partnerships, governance and strategic direction of the Group. She has been elected as Chairperson of Gabriel India Limited in 2015.

The leadership transition marked a strategic pivot. While Deep Anand focused on manufacturing excellence, Anjali Singh brought financial sophistication. Her first major decision: professionalize the board with independent directors from automotive, technology, and finance backgrounds. The board that once resembled a family council transformed into a strategic think tank.

new manufacturing operations at Parwanoo, and the addition of front fork manufacturing capacity at their new facility at Noida. They also have a virtual launch of their Passenger Car Brake Pads and Ride Control Products for high-end vehicles such as Audi and Mercedes Benz. In 2021, they completed a modern Technology Centre at Chakan Pune to enhance their RD capabilities.

The Chakan Technology Centre, opened in 2021, symbolized Gabriel's ambitions beyond manufacturing. This ₹150-crore investment created India's most advanced suspension testing facility, including a four-poster rig that could simulate any road condition globally. OEMs could now develop and validate entire suspension systems without leaving India—a capability that made Gabriel indispensable for localization programs.

Digital transformation, often lip service in traditional manufacturing, became operational reality at Gabriel. IoT sensors on production lines provided real-time quality data. Predictive maintenance algorithms reduced equipment downtime by 30%. Digital twins of products enabled virtual testing, cutting development time from 18 to 9 months. This wasn't Industry 4.0 theater—it was competitive advantage.

The aftermarket evolution reflected changing consumer behavior. Gabriel launched an app allowing customers to verify product authenticity, find nearby installers, and even book installation appointments. The direct-to-consumer pivot, unthinkable for a B2B company a decade ago, opened new margin pools. Online sales, launched in 2020, contributed ₹50 crores by 2023—small but symbolic.

Financial discipline during growth impressed analysts. Pre-tax margin of 7% is okay, ROE of 17% is exceptional. The company is debt free and has a strong balance sheet enabling it to report stable earnings growth across business cycles. Zero debt in a capital-intensive industry seemed impossible, yet Gabriel achieved it through careful capital allocation and strong cash generation.

The export transformation accelerated post-2015. Gabriel products reached 40 countries, but the real breakthrough came through global platform wins. When a global OEM selected Gabriel for a platform manufactured in multiple countries, it meant automatic entry into new markets. A shock absorber designed in Pune could end up in vehicles assembled in Thailand, Brazil, or South Africa.

ESG initiatives, initially compliance-driven, became strategic differentiators. Gabriel's Hosur plant, powered entirely by renewable energy, became a showcase for sustainable manufacturing. Water recycling systems achieved 90% efficiency. These investments, initially seen as costs, attracted ESG-focused investors who provided patient capital at attractive valuations.

The EV transition created existential questions and enormous opportunities. Electric vehicles needed different suspension tuning due to battery weight distribution. Gabriel's early investments in EV-specific products paid off when Tata Motors selected them for the Nexon EV—India's first mass-market electric car. The learnings from this program positioned Gabriel for the entire EV revolution.

The Board of Directors of Gabriel India has approved a composite scheme of arrangement involving, inter alia, Gabriel India, Asia Investments (AIPL), and Anchemco India (formerly known as Andasia) (Anchemco). This Scheme will result into vesting of automotive business undertaking of AIPL comprising of business of Anchemco (engaged in manufacturing of brake fluids, radiator coolants, diesel exhaust fluid (DEF) / ad-blue, and PU/ PVC based adhesives) and investments in Dana Anand India (Dana), Henkel ANAND India (Henkel) and ANAND CY Myutec Automotive (ACYM) (Demerged Undertaking) into Gabriel. Gabriel will issue 1,158 equity Shares of Rs 1 each for every 1,000 equity shares of Rs 10 each held in AIPL to the shareholders of AIPL.

This complex restructuring, announced in 2024, wasn't just corporate maneuvering—it was portfolio expansion. By absorbing complementary businesses, Gabriel transformed from a mono-product company to an integrated automotive solutions provider. The market loved it—the stock rallied 25% on announcement.

Recent quarterly results validated the strategy. Sales rose 16.04% to Rs 1098.38 crore in the quarter ended June 2025 as against Rs 946.57 crore during the previous quarter ended June 2024. On a consolidated basis, net profit of Gabriel India rose 31.24% to Rs 64.36 crore while net sales rose 17.03% to Rs 1073.15 crore in Q4 March 2025 over Q4 March 2024.

For the full year, adjusted net profit rose 37.05% to Rs 244.98 crore while net sales increased 19.42% to Rs 4,063.38 crore in the year ended March 2025 over the year ended March 2024. PBT rose 32.94% year-on-year to Rs 324.16 crore in FY25 over FY24. EBITDA rose 33.87% to Rs 391.7 crore in FY25 over FY24. EBITDA margin stood at 9.6% in FY25 as against 8.6% in FY24.

The margin expansion story continued unabated. Operating margins improving from 7.2% in FY23 to 8.6% in FY24, and further to 9.6% in FY25 demonstrated pricing power rare in auto components. Net margins expanded from 4.5% to 5.3% to over 6%—each basis point representing millions in shareholder value.

Institutional ownership evolution told its own story. From zero institutional holding in 1995, Gabriel attracted mutual funds, insurance companies, and foreign investors. By 2024, institutions owned 35% of the company, providing liquidity and analytical coverage that transformed Gabriel from an undiscovered gem to a market darling.

The ₹15,472 crore market capitalization in 2024 made Gabriel larger than many celebrated consumer companies. Yet analyst coverage remained limited—only six analysts actively covered the stock versus 30+ for similar-sized FMCG companies. This analytical orphan status created inefficiencies that smart investors exploited.

Looking ahead, Gabriel's transformation from shock absorber manufacturer to mobility solutions provider was just beginning. Sunroof systems, active suspension, and even autonomous vehicle components entered the product pipeline. The company that began by smoothing rides on Indian roads was now engineering the future of global mobility. The public markets, initially skeptical, had become believers in a story that proved industrial excellence could create extraordinary wealth.

VIII. Building the Aftermarket Empire

The mechanic in Karol Bagh, Delhi, wiped his greasy hands on an equally greasy rag and pronounced his verdict: "Gabriel hai toh gaadi hai, baaki sab bekaar" (If it's Gabriel, the vehicle is fine, everything else is useless). This wasn't paid marketing—it was organic brand evangelism built over decades. In India's automotive aftermarket, a ₹75,000 crore chaos of genuine parts, counterfeits, and "local" alternatives, Gabriel had achieved something remarkable: brand pull in a push market.

Strong distribution network of ~660 distributors and 12,000 retailers in India. These numbers underscore a distribution density that rivals FMCG companies. But unlike soap or shampoo, shock absorbers aren't bought impulsively. The average replacement cycle spans 40,000 kilometers or three years. Gabriel turned this infrequency into an advantage—each sale became an event, each replacement a considered decision where brand mattered.

The aftermarket strategy began with a simple insight: vehicle owners don't buy shock absorbers; they buy comfort and safety. Gabriel's masterstroke was educating the educators—the mechanics who influenced purchase decisions. Starting in 1985, Gabriel conducted 'Vishwakarma' training programs, named after the Hindu god of craftsmen. Over 50,000 mechanics attended these programs, learning not just about Gabriel products but suspension diagnostics, safety implications, and earning potential from promoting genuine parts.

Marketing other automotive products under Gabriel brand - coolants, suspension bush kits, front fork oils, gas springs, wheel rims. This portfolio expansion wasn't random diversification—it was strategic adjacency exploitation. Every product leveraged Gabriel's distribution network, brand equity, and customer relationships. A distributor selling Gabriel shock absorbers could now offer a complete suspension solution, increasing wallet share and switching costs.

The counterfeit challenge threatened everything. By 2010, fake Gabriel shock absorbers flooded markets, sold at 50% of genuine prices. Gabriel's response was multi-pronged: holographic packaging that changed color when tilted, unique serial numbers verifiable via SMS, and most cleverly, a warranty program that covered consequential damage—something counterfeiters couldn't match. The campaign "Duplicate se Dhoka, Gabriel se Vishwas" (Deception from duplicates, Trust from Gabriel) resonated with safety-conscious consumers.

Pricing architecture in the aftermarket revealed sophisticated segmentation. Gabriel offered three tiers: Classic (basic replacement), Comfort (enhanced features), and Sport (performance-oriented). The genius lay in positioning—Classic matched local alternatives on price, Comfort offered 40% better performance for 20% premium, while Sport commanded 100% premium for enthusiast segments. This good-better-best strategy captured value across the pyramid.

The distribution economics were compelling. While OEM sales operated on 8-10% margins, aftermarket products commanded 25-30% margins. The reason? Urgency and convenience premiums. A broken shock absorber meant an immobilized vehicle. Customers paid for immediate availability, trusted quality, and installation expertise. Gabriel's distributors maintained inventory worth ₹2-3 lakhs, ensuring same-day availability for 90% of vehicle models.

Regional variations required localized strategies. In Punjab and Haryana, where vehicle modifications were cultural, Gabriel launched heavy-duty variants for lifted SUVs. In Kerala, where monsoons tested vehicle integrity, they emphasized corrosion-resistant coatings. Tamil Nadu's commercial vehicle density led to 24-hour replacement centers on highways. This wasn't one India strategy—it was 29 state strategies unified by a common brand.

The digital transformation of aftermarket began cautiously. Gabriel's e-commerce platform, launched in 2019, initially faced distributor resistance—channel conflict fears ran deep. The solution was elegant: online orders routed to nearest distributors who fulfilled and earned margins. Distributors gained customers they wouldn't have reached; customers got convenience with local service. Win-win architecture at its best.

Portfolio of ~500 products and 8 new product lines, growing presence globally in South Asia, Africa, Latin America, and Australia. The export aftermarket opportunity emerged from Indian diaspora mechanics. Indian-trained mechanics in Dubai, Nairobi, and Colombo preferred Gabriel products they understood. These mechanics became unofficial brand ambassadors, creating pull in markets Gabriel hadn't formally entered.

The warranty revolution changed aftermarket dynamics. Gabriel introduced India's first no-questions-asked replacement warranty for shock absorbers—if a product failed within 12 months or 20,000 kilometers, instant replacement. The actual claim rate? Less than 0.5%. But the confidence this created drove 30% premium realization. Customers weren't buying products; they were buying peace of mind.

Fleet management companies became aftermarket goldmines. Companies like Uber and Ola, operating thousands of vehicles, needed predictable maintenance costs. Gabriel created fleet-specific programs: bulk pricing, scheduled replacements, and on-site service. A single fleet contract could generate ₹5 crore annual revenues with 15% margins—equivalent to 50 retail distributors.

The accessories adjacency proved surprisingly profitable. Gabriel-branded coolants, launched in 2015, captured 5% market share within three years. The logic was simple: customers who trusted Gabriel for critical components would trust them for consumables. Front fork oils for motorcycles, a ₹200 crore market dominated by imports, saw Gabriel capture 15% share by offering "Made for Indian Conditions" positioning.

Rural penetration remained the final frontier. India's 600,000 villages generated 40% of automotive aftermarket demand but were served primarily by unorganized players. Gabriel's 'Village Garage' initiative, launched in 2018, created mini-distributors in tehsil towns. These entrepreneurs, with ₹1 lakh investment, could stock fast-moving Gabriel products. By 2023, 2,000 village garages generated ₹150 crores in revenues.

The influencer strategy evolved with social media. YouTube mechanics with millions of followers became brand partners. Videos showing genuine vs. fake product comparisons, installation techniques, and performance tests created authentic content marketing. The cost per acquisition through influencer marketing? ₹200 versus ₹2,000 through traditional advertising.

Private label opportunities with e-commerce platforms created new channels. Amazon and Flipkart's automotive categories needed trusted suppliers for their private brands. Gabriel manufactured products under these labels while maintaining quality standards. The volumes were massive—online automotive aftermarket grew 50% annually—and margins, while lower than branded sales, exceeded OEM business.

Insurance partnerships opened institutional channels. General insurance companies, settling accident claims, preferred genuine parts to reduce repeat claims. Gabriel's approved vendor status with major insurers meant automatic specification in repair estimates. This institutional endorsement created consumer trust that advertising couldn't buy.

The subscription model pilot, launched in 2022 for commercial vehicles, promised predictive maintenance. IoT sensors on shock absorbers monitored performance, predicting failures before they occurred. Fleet operators paid ₹500 monthly per vehicle for monitoring and scheduled replacements. Early results showed 40% reduction in breakdown-related losses, validating the service-led transformation.

Customer education initiatives went beyond products. Gabriel's 'Safe Drive' campaigns at schools and colleges, reaching 500,000 students annually, created generational brand awareness. These weren't sales pitches but safety education—understanding suspension's role in vehicle dynamics. Parents influenced by safety-conscious children became customers. Long-term brand building at its finest.

The aftermarket profitability transformed Gabriel's economics. Contributing 25% of revenues but 35% of profits, aftermarket became the earnings stability engine. While OEM sales fluctuated with vehicle production cycles, aftermarket demand remained steady—vehicles needed maintenance regardless of new car sales. This counter-cyclical characteristic made Gabriel's earnings more predictable than pure OEM suppliers.

By 2024, Gabriel's aftermarket wasn't just distribution—it was an ecosystem. Distributors weren't vendors but partners, mechanics weren't influencers but educators, and products weren't components but solutions. The boy from Bishop Cotton School had built something more valuable than market share—he'd built mind share. In India's chaotic aftermarket, Gabriel had become synonymous with trust, and trust, as any marketer knows, is the ultimate moat.

IX. The ANAND Group Ecosystem & Strategic Pivots

The conference room at ANAND House in Hauz Khas hummed with possibility in 2023. Representatives from fourteen joint ventures, spread across conference screens from Seoul to Stuttgart, discussed a vision that would have seemed impossible when Deep Anand shook hands with Maremont in 1961. The Group comprises 23 companies, including 8 joint ventures and four technical collaborations. It has a wide presence across 75-plus locations in India, employees over 20,000 people—this wasn't just a conglomerate; it was an orchestrated ecosystem where Gabriel India served as the beating heart.

ANAND Group: 23 companies, 8 JVs, 4 technical collaborations, 75+ locations, 20,000+ employees. Each number represents a deliberate strategic choice, a partnership philosophy refined over six decades. The group, with revenues of Rs 19,000 crore, is betting on global expansion, including inorganic opportunities, to accelerate growth. Defying the slowdown, Anand Group is aiming for revenue of Rs 50,000 crore by the end of the decade – nearly two and a half times its current size.

The $2-billion Group with six decades of legacy operates on what insiders call the "Partnership Playbook"—a set of principles so ingrained they're never written down, just understood. First principle: Never acquire, always collaborate. Unlike Indian conglomerates that grew through acquisitions, ANAND grew through partnerships. Each joint venture brought technology, market access, and most importantly, trust that money couldn't buy.

It strongly believes in the 'Power of Partnerships,' further driven by the 'Power of People'. Over the past six decades, the ANAND Group companies have successfully integrated the technical expertise of their partners with local resources. The genius lay in structure—ANAND maintained management control while partners provided technology. This wasn't ego; it was economics. Local management understood Indian complexity better than any expatriate ever could.

The joint venture portfolio reads like a who's who of global automotive: Mahle Anand Thermal Systems, Haldex Anand India, Dana Anand India, Joyson Anand Abhishek Safety Systems, and Faurecia Clean Mobility. Each partnership targeted a specific technology gap in India's automotive ecosystem. When electric vehicles emerged, ANAND didn't scramble—they formed Anand Mando e-Mobility (AMeM), a joint venture with South Korea's Mando Corporation, focusing on electric motors and controllers.

Recent corporate restructuring and merger plans weren't just financial engineering—they were portfolio optimization. The Board of Directors of Gabriel India has approved a composite scheme of arrangement involving, inter alia, Gabriel India, Asia Investments (AIPL), and Anchemco India. This complex restructuring would vest automotive business undertaking of AIPL comprising of business of Anchemco (engaged in manufacturing of brake fluids, radiator coolants, diesel exhaust fluid (DEF) / ad-blue, and PU/ PVC based adhesives) into Gabriel.

Post-merger promoter shareholding to increase from 55% to 63.53%. This wasn't about control—ANAND already had that. It was about signaling. Higher promoter stake meant skin in the game, alignment with minority shareholders, and confidence in future prospects. The market loved it—Gabriel stock rallied 25% on restructuring announcement.

Diversification beyond mono-product suspension company happened through calculated adjacencies. When Gabriel entered sunroof systems through Inalfa Gabriel Sunroof Systems, it wasn't random diversification. Sunroofs required similar engineering capabilities—precision mechanisms, weather sealing, integration with vehicle structures. The same engineers who designed strut assemblies could design sunroof mechanisms. Competence, not just opportunity, drove diversification.

EV transition strategy and new mobility solutions emerged through ANEVOLVE, ANAND's cleantech platform launched in 2023. This wasn't a me-too EV play. ANEVOLVE focused on the components global EV manufacturers struggled to localize—power electronics, thermal management systems, battery cooling solutions. Jaisal Singh, Chairman of Anevolve and Vice Chairman of the Anand Group, stated that he sees a potential business of about $500 million in the coming years and expects the EV business to account for 25 percent of the group's total turnover.

The synergy exploitation across group companies created value multiplication. Dana Anand's driveline components integrated with Gabriel's suspension systems for complete chassis solutions. Mahle Anand's thermal systems worked with ANEVOLVE's battery cooling requirements. Henkel ANAND's adhesives found applications across group companies. This wasn't holding company oversight—it was ecosystem orchestration.

International expansion strategy differed from typical Indian companies. Instead of setting up overseas subsidiaries, ANAND leveraged joint venture partners' global networks. When Mahle needed suppliers for their Mexican operations, Mahle Anand got preferred vendor status. When Dana sourced for Brazilian plants, Dana Anand participated. Global reach without global investment—partnership leverage at its finest.

The innovation ecosystem extended beyond products. The Group invested heavily in digital manufacturing—IoT sensors, predictive analytics, digital twins. But unlike technology companies that celebrated pilots, ANAND scaled quietly. By 2024, every ANAND factory had digital manufacturing capabilities. ROI wasn't measured in press releases but in basis points of margin improvement.

Human capital development followed the partnership philosophy. ANAND didn't just train employees; they created entrepreneurs. The 'Intrapreneur' program allowed employees to propose new business ventures. Successful proposals received funding, mentorship, and most importantly, equity participation. Several group companies started as employee ideas—creating owners, not just workers.

The financial architecture across group companies optimized capital efficiency. Cash-rich companies like Gabriel funded growth at cash-hungry startups like ANEVOLVE. Technical collaborations cross-licensed intellectual property. Shared services—IT, HR, Finance—reduced overhead. The group achieved the scale benefits of size while maintaining entrepreneurial agility of smaller units.

Core values: transparency, good governance and mutual trust as foundation permeated every partnership. ANAND's joint venture agreements included unusual clauses—mandatory CEO rotation between partners, technology transfer both ways, and most remarkably, pre-agreed exit clauses that protected both parties. Partners weren't trapped; they stayed because they wanted to.

The supplier ecosystem management went beyond transactions. ANAND created supplier parks where vendors co-located near ANAND factories. Technical assistance programs helped suppliers achieve global quality standards. Payment terms favored smaller suppliers—sometimes paying before delivery to ease working capital pressure. This wasn't altruism; it was ecosystem strengthening.

R&D coordination across group companies prevented duplication and accelerated innovation. The Central Technology Council, comprising CTOs from all group companies, met quarterly to share developments, identify synergies, and coordinate research. A breakthrough in metallurgy at Gabriel could benefit Dana Anand's gear manufacturing. Knowledge flowed freely within the ecosystem.

The sustainability initiatives, initially compliance-driven, became competitive advantages. ANAND's commitment to carbon neutrality by 2040 attracted ESG-focused customers and investors. Renewable energy adoption, water recycling, and zero-waste manufacturing weren't just good citizenship—they were good business, reducing costs and attracting premium customers.

To fuel the growth, the company will pour roughly Rs 4,000 crore into expansion over the next six years, with Rs 1,000 crore earmarked for the electrification. This wasn't just capacity expansion—it was capability building. New factories would be digital-first, designed for flexibility to handle ICE and EV components simultaneously. The investment in electrification wasn't about replacing existing business but supplementing it.

The hospitality venture SUJÁN, offering experiential luxury while embracing community conservation, seemed incongruous with automotive manufacturing. But it served strategic purposes—showcasing ANAND's execution excellence to global partners, providing exclusive venues for customer engagement, and most importantly, demonstrating that ANAND could excel beyond automotive.

By 2024, the ANAND ecosystem had evolved into something unique in Indian business—neither a tightly controlled conglomerate nor a loose federation, but a coordinated ecosystem where independent companies created collective value. Gabriel India, generating ₹4,000+ crores in revenue, remained the flagship, but increasingly, the group's strength came from the portfolio, not any single company.

The partnership model that began with Deep Anand's handshake with Maremont had evolved into a sophisticated system of creating, managing, and multiplying value through collaboration. In an era of disruption and dislocation, ANAND proved that patient capital, trusted partnerships, and ecosystem thinking could create value that transcended individual company success. The shock absorber company had become a shock absorber for the entire Indian automotive industry—smoothing volatility, absorbing disruption, and enabling the ride toward an uncertain but exciting future.

X. Playbook: The Partnership Model

Deep C. Anand sat across from his American counterparts in 1961, a 27-year-old Indian engineer negotiating with executives twice his age from a company hundred times larger. His demand seemed audacious: technology transfer, yes, but management control stays with India. The Americans exchanged glances—this wasn't how joint ventures worked. Yet something about Anand's quiet confidence, his detailed understanding of Indian market complexity, made them pause. "Let's try it," they said. That handshake created not just Gabriel India but a partnership philosophy that would build a $2-billion empire.

Deep C. Anand's collaboration philosophy - bringing global best practices to India started with a fundamental insight: technology without context is useless. American shock absorbers designed for Interstate highways would fail on Indian roads within weeks. Japanese quality systems assuming educated workers wouldn't work with Indian labor realities. European cost structures would price products out of Indian markets. The solution wasn't choosing between global and local—it was synthesizing both.

With the success of this Joint Venture, Mr. Anand created a pattern of collaboration which brought the 'best in class' into India and established successful partnerships with leading global automotive companies. But the pattern went deeper than legal structures. Every ANAND partnership followed unwritten rules that partners discovered only through experience.

Rule One: Technology transfer was bidirectional. While partners brought product technology, ANAND brought process innovations—how to achieve First World quality with Third World infrastructure. When Mahle's German engineers visited ANAND's facilities, they were stunned to see manual processes achieving tolerances their automated plants struggled with. The secret? Indian engineers had developed inspection and correction protocols that turned human variability into an advantage.

Rule Two: Management control resided with whoever understood the market better. In India, that meant ANAND. But when Dana Anand exported to Latin America, Dana took the lead. This fluid leadership model, unthinkable in rigid corporate structures, created accountability without bureaucracy. Decisions happened fast because decision-makers were closest to problems.

Building trust with global partners while maintaining Indian identity required delicate balancing. ANAND companies maintained global standards—ISO certifications, Six Sigma quality, international accounting standards. But execution remained distinctly Indian. Factories shut for Diwali regardless of production schedules. Employee families were invited to factory events. The works committee included religious leaders alongside union representatives. Global partners initially resisted these "inefficiencies" until they realized Indian workers' loyalty and dedication exceeded anything contractual compliance could achieve.

Managing technology transfer effectively became ANAND's core competence. The process wasn't just documentation transfer—it was knowledge transformation. When ArvinMeritor transferred shock absorber technology, ANAND engineers didn't just receive blueprints. They spent months at American facilities, understanding not just how but why—the physics behind damping curves, the chemistry of seal materials, the mathematics of valve design. This deep understanding enabled innovation, not just replication.

The localization journey followed predictable phases. Year one: Import and assemble. Year two: Source simple components locally. Year three: Develop local suppliers for complex parts. Year five: Achieve 90%+ localization. Year seven: Innovation beyond original specifications. This seven-year cycle, repeated across joint ventures, became institutional knowledge. New partnerships compressed timelines because ANAND knew the journey.

Core values: transparency, good governance and mutual trust as foundation weren't just corporate speak—they were operational necessities. Joint ventures fail primarily due to mistrust. ANAND's solution was radical transparency. Every joint venture had unified accounting systems accessible to both partners. Board meetings included detailed operational reviews, not just financial summaries. Bad news traveled faster than good news. Problems were shared before they became crises.

The equity structure philosophy was counterintuitive. While most Indian companies sought majority control, ANAND often settled for 50:50 or even minority stakes. The logic? Real control came from operational excellence, not equity percentage. If you run operations better, deliver results consistently, and understand markets deeply, partners depend on you regardless of shareholding. This operational control exceeded any legal control.

Lessons on JV management in emerging markets became ANAND's expertise, sought by global companies entering India. The key insight: emerging markets aren't just poor developed markets—they're fundamentally different ecosystems requiring different approaches. Products needed redesigning for different use cases. Distribution required different channels. Pricing followed different logic. Partners who understood this succeeded; those who didn't, failed.

Capital allocation: R&D vs manufacturing vs distribution revealed ANAND's strategic priorities. Unlike pure manufacturers who maximized production investment, ANAND balanced all three. R&D received 3-4% of revenues—high for Indian companies but essential for technology absorption. Manufacturing got 40% of capital allocation—enough for quality but not excess automation. Distribution received unusual attention—20% of investment went to market development. This balanced allocation created sustainable competitive advantages.

The partner selection process was remarkably patient. ANAND courted Haldex for five years before forming a joint venture. Due diligence went beyond financials—cultural fit, long-term vision, and commitment to India mattered more. Several high-profile partnerships were rejected because potential partners saw India as a market to exploit, not a partnership to build. This patience paid off—ANAND joint ventures had a 90% success rate versus 50% industry average.

Technology absorption capabilities became measurable. ANAND tracked "time to indigenous"—how quickly imported technology could be localized. In 1990, it took seven years. By 2000, five years. By 2010, three years. By 2020, eighteen months. This acceleration came from accumulated knowledge, supplier development, and most importantly, confidence. Engineers no longer saw foreign technology as mysterious—they saw it as puzzles to solve.

The intellectual property philosophy was progressive. Unlike companies that hoarded IP, ANAND shared freely within its ecosystem. Metallurgy improvements developed for Gabriel were shared with Dana Anand. Software algorithms created for Mahle Anand were available to other group companies. This open architecture accelerated innovation—the rising tide lifted all boats.

Crisis management revealed partnership strength. During the 2008 financial crisis, when ArvinMeritor faced bankruptcy, Gabriel India could have renegotiated terms favorably. Instead, ANAND provided support, maintained technology payments, and assured employees. When ArvinMeritor recovered, they remembered. Gabriel got exclusive rights to new technologies, preferential terms, and most importantly, trust that transcended contracts.

The succession planning in partnerships addressed a critical emerging market challenge. Global partners worried about continuity when founders retired. ANAND's solution was systematic—second-generation leaders spent years working in joint ventures, understanding partner perspectives. When they assumed leadership, partners saw continuity, not disruption. This planned transition maintained partnership stability across generations.

Knowledge management systems captured partnership learnings. Every joint venture maintained detailed records—not just technical documentation but relationship insights. Which partner executives were decision-makers? What concerns kept them awake? How did their internal politics affect partnership decisions? This institutional knowledge survived personnel changes, maintaining relationship continuity.

The exit clause philosophy seemed pessimistic but was pragmatic. Every joint venture agreement included detailed exit provisions—valuation methods, right of first refusal, non-compete clauses. Clear exit routes paradoxically strengthened partnerships. Partners stayed because they wanted to, not because they were trapped. This voluntary commitment created stronger bonds than any legal agreement.

By 2024, the ANAND partnership model had become a case study in collaboration excellence. Business schools taught it, consultants referenced it, competitors tried copying it. But the model's success wasn't in its structure—it was in its spirit. Deep Anand's fundamental belief that business was about relationships, not transactions, permeated every partnership.