Fortis Healthcare: The Rise, Fall, and Rebirth of India's Healthcare Giant

I. Introduction & Episode Roadmap

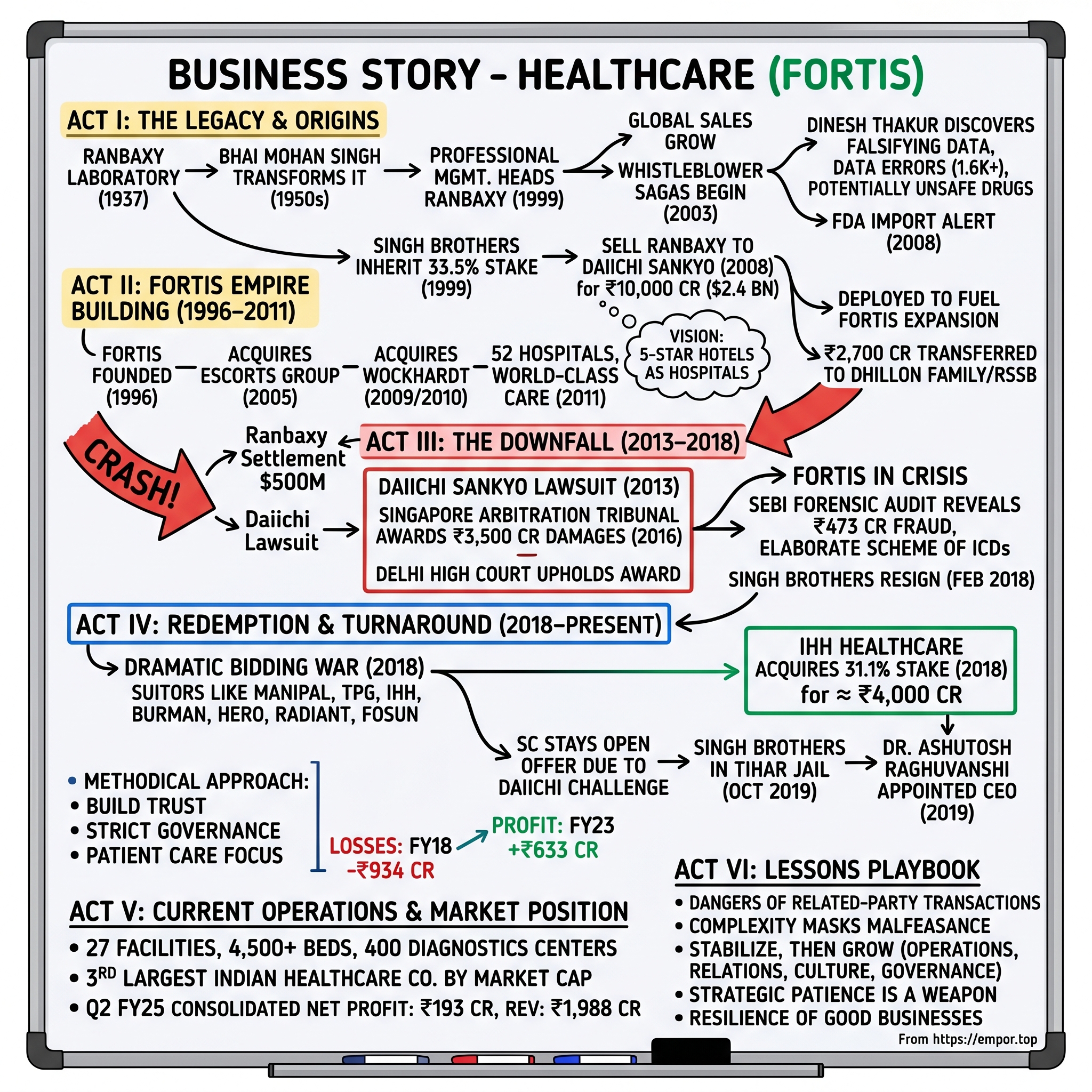

The year is 2018. Inside the boardroom of what was once India's crown jewel of private healthcare, two brothers sit across from each other for the last time as board members. Malvinder and Shivinder Singh—heirs to one of India's greatest pharmaceutical fortunes—are about to resign from Fortis Healthcare amid allegations that would shock corporate India. The accusation: siphoning ₹473 crores from the very company they built into a healthcare empire spanning 28 facilities and 4,500 beds.

This is not just another corporate scandal. This is the story of how one of India's most ambitious healthcare ventures—born from the profits of selling Ranbaxy to Japan's Daiichi Sankyo for $2.4 billion—would collapse under the weight of fraud allegations, trigger international lawsuits worth billions, and ultimately find redemption through an unlikely savior from Malaysia. Today, Fortis Healthcare stands as a testament to both the fragility and resilience of Indian corporate governance. With 28 healthcare facilities, 4,500+ operational beds, and over 400 diagnostics centers, it remains one of India's healthcare giants. But the journey from founding vision to corporate collapse to eventual resurrection under Malaysian ownership reads like a three-act tragedy that somehow found its redemption.

IHH Healthcare finalised the successful acquisition of a 31.1 per cent stake in Fortis Healthcare along with 26 per cent equity interest in its listed subsidiary Fortis Malar Hospital on 13 November 2018, marking not just a change in ownership but the beginning of one of the most dramatic turnaround stories in Indian healthcare. The deal, worth approximately Rs 4,000 crore of primary capital, would trigger years of legal battles, regulatory interventions, and ultimately, a complete transformation of the company's culture and operations.

What makes the Fortis story particularly compelling is how it mirrors the broader challenges of Indian family businesses transitioning to professional management—the clash between ambition and governance, the thin line between aggressive expansion and financial engineering, and the ultimate price of betraying stakeholder trust. This is that story.

II. The Ranbaxy Legacy & Singh Brothers Origins

The roots of the Fortis empire stretch back to a small pharmaceutical shop in Amritsar in 1937. Two cousins, Ranjit Singh and Gurbax Singh, founded what would become Ranbaxy Laboratories with a vision to make affordable medicines for newly independent India. But by the 1950s, when mounting debts threatened to sink the company, an unlikely savior emerged: Bhai Mohan Singh, a devout follower of the Radha Soami spiritual sect and the grandfather of the future Fortis founders.

Bhai Mohan Singh didn't just buy Ranbaxy—he transformed it. Under his leadership, Ranbaxy evolved from a struggling local player into India's first truly global pharmaceutical company. By the 1970s, Ranbaxy was exporting to Eastern Europe and Africa. By the 1980s, it was challenging Western pharmaceutical giants with its generic formulations. The company's philosophy was simple yet revolutionary for its time: why should Indians pay Western prices for life-saving drugs when they could manufacture the same molecules at a fraction of the cost? When Parvinder Singh died of cancer in July 1999, the Singh brothers inherited their family's 33.5% stake in Ranbaxy. Malvinder was 27, Shivinder just 23. They had the pedigree—educated at The Doon School of Dehradun, graduated from Delhi's St Stephens College, and both held MBAs from the Fuqua School of Business of Duke University in the United States. But they also had something else: a burden of expectation and a grandfather who believed they should immediately take charge.

The drama that unfolded after Parvinder's death would set the tone for everything that followed. Barely 24 days before he succumbed to the disease, Parvinder announced that Ranbaxy would be headed not by his sons but by a professional, Devinder Singh Brar. This decision rattled Bhai Mohan Singh, the family patriarch. His letter to the board stated that Malvinder and Shivinder should be inducted, pointing out that it was illogical not to have any family member while vetting crucial board decisions.

Yet in a move that surprised everyone, the brothers issued a joint statement saying they wished to abide by their father's last wish that ownership and management be kept separate in Ranbaxy. Malvinder said he would be content holding a relatively junior position, while Shivinder announced he would join Fortis, a healthcare subsidiary.

Under professional management, Ranbaxy continued to thrive initially. Total worldwide sales rose from Rs 1,560 crore in 1999 to Rs 3,940 crore in 2002, reaching Rs 4,370 crores in December 2003. But beneath this success, a time bomb was ticking. The whistleblower saga that would eventually destroy Ranbaxy began in 2003 when the company hired Dinesh Thakur, an American-educated chemical engineer from Bristol-Myers Squibb. During 2003-2005, Mr. Thakur was the Director & Global Head, Research Information & Portfolio Management at Ranbaxy Laboratories, India's largest generic drug manufacturer.

What Thakur discovered would shock the pharmaceutical world. Thakur discovered that the company was falsifying drug data and violating current good manufacturing practices and good laboratory practices. He resigned in 2005 after reporting the fraud to company management. The company wasn't just cutting corners—it was systematically fabricating test results, selling untested drugs, and putting millions of patients at risk, particularly in African and Asian markets where regulatory oversight was weaker.

The investigation revealed staggering fraud. Their investigation found Ranbaxy had a "persistent" "pattern" of submitting "untrue statements." On at least 15 new generic drug applications, auditors found more than 1,600 data errors. This meant their drugs were "potentially unsafe and illegal to sell."

Meanwhile, Malvinder finally took charge of Ranbaxy as CEO and Managing Director in 2006, seven years after his father's death. But he was walking into a minefield. The FDA had already begun tightening its noose. Kumar and Thakur's whistleblower reports prompted the FDA to issue an Import Alert for generic drugs produced from two of Ranbaxy's manufacturing plants in September 2008.

Faced with mounting regulatory pressure and realizing the walls were closing in, the Singh brothers made a fateful decision. In June 2008, they sold their 34.8% stake in Ranbaxy to Japanese pharmaceutical giant Daiichi Sankyo for ₹10,000 crore (US$2.4 billion)—a deal that would later haunt both parties. The timing was no coincidence. The brothers knew what was coming.

In May 2013, Ranbaxy pleaded guilty to multiple criminal felonies and agreed to pay $500 million to resolve criminal and civil allegations of falsified drug data and systemic manufacturing violations resulting in substandard and unapproved drugs. The groundbreaking settlement is the largest of its kind against a generic drug manufacturer.

For Daiichi Sankyo, the acquisition turned into a nightmare. They had bought not a crown jewel but a poisoned chalice. The Japanese company would later accuse the Singh brothers of concealing crucial information during the sale—an accusation that would trigger years of international litigation and ultimately contribute to the brothers' downfall.

III. Building Fortis Healthcare Empire (1996–2011)

While the Ranbaxy story was playing out on one stage, the Singh brothers were quietly building their next act. Fortis Healthcare was founded in 1996 as an offshoot of the pharmaceutical company Ranbaxy Laboratories. It began operating in Mohali, Punjab, where its first hospital was established.

The vision was audacious for its time. In 2001, while Indian healthcare was still dominated by government hospitals with peeling paint and overcrowded wards, the Singh brothers imagined something different: world-class hospitals that looked and felt like five-star hotels, where patients were treated as customers, where international protocols met Indian warmth. Their first major move came through acquisition. It later expanded by acquiring the healthcare division of Escorts Group, including the Escorts Heart and Research Center, Okhla, Delhi. Prior to this deal, the largest healthcare acquisition was of Escorts Heart Institute, also acquired by Fortis Healthcare ltd in the year 2005.The Escorts-Fortis deal size was Rs 650 crore.

But the deal that truly transformed Fortis into a national powerhouse came in 2009. In late 2009, Fortis Healthcare Ltd. (Fortis), a hospital chain established by the promoters of Ranbaxy Laboratories Limited (RLL), acquired 10 hospitals of the Wockhardt Hospitals Group (Wockhardt Hospitals), a subsidiary of Wockhardt Ltd. (Wockhardt) for Rs. 9.09 billion. The acquisition was hailed by experts as the biggest in the Indian healthcare industry

The Wockhardt acquisition was strategic brilliance. "The deal will make Fortis very strong in Mumbai and Bangalore, the two cities where it did not have a strong presence. Wockhardt's Mumbai hospital is running well and has an occupancy rate of over 80 per cent with steady cash flow. The Bangalore hospital is also functioning well", Monika Sood, Feedback Ventures Pvt Ltd said. In 2010, Fortis Healthcare acquired the Wockhardt Hospitals chain, which significantly bolstered its operational capacity and market share. This acquisition added more than 1,000 beds to its network.

By 2011, Fortis had become everything the Singh brothers had envisioned. With 52 hospitals across the country, they had created one of India's most formidable healthcare networks. The company was delivering world-class healthcare, attracting top medical talent, and generating robust cash flows.

The brothers made another crucial decision during this period: they sold their remaining stake in the pharmaceutical business to focus entirely on healthcare. It seemed like a masterstroke—exiting a troubled pharma business at the peak and doubling down on the booming healthcare sector. The proceeds from the Ranbaxy sale—approximately Rs 7,500 crore after taxes—were being deployed to fuel Fortis's expansion. Of the remaining Rs7,500 crore, Rs1,750 crore were invested in Religare to fund its growth; about Rs2,230 crore was invested in Fortis' growth.

But beneath this success story, fault lines were already forming. But most importantly, Rs2,700 crore were transferred to companies owned by the Dhillon family, Gurinder Dhillons wife Shabnam Dhillon and companies associated with RSSB's senior functionaries. These transfers to their spiritual guru's family would later become a critical piece of the fraud allegations against the brothers.

The Singh brothers had built a healthcare empire that was the envy of corporate India. They had successfully transformed from pharmaceutical heirs into healthcare moguls. But the shadows of Ranbaxy were lengthening, and the bills for their past decisions were about to come due.

IV. The Daiichi Sankyo Lawsuit & Beginning of the End (2013–2018)

The first domino fell in May 2013. In May 2013, Ranbaxy pleaded guilty to multiple criminal felonies and agreed to pay $500 million to resolve criminal and civil allegations of falsified drug data and systemic manufacturing violations resulting in substandard and unapproved drugs. For Daiichi Sankyo, this was the moment of terrible clarity—they had been deceived on a massive scale.

The Japanese company's response was swift and brutal. They filed a case against the Singh brothers in Singapore, alleging that crucial information about the FDA investigations had been deliberately concealed during the 2008 sale. The arbitration proceedings would reveal a pattern of deception that shocked even seasoned corporate lawyers. In April 2016, the hammer fell. The Singapore arbitration tribunal in April 2016 while holding the former promoters of Ranbaxy as liable for fraud had asked them to pay Rs 3,500 crore as damages and interest to drug firm Daiichi. The tribunal found that the Singh brothers had deliberately concealed critical information about FDA investigations and fraudulent practices at Ranbaxy during the 2008 sale.

The Indian courts provided no relief. The Delhi High Court upheld the international arbitral award of Rs 3,500 crore against the Singh brothers. Justice Jayant Nath held the award to be enforceable after hearing a petition filed by Daiichi seeking enforcement and execution of the Foreign Award dated April 29, 2016, passed by the tribunal in Singapore after it found the former promoters had intentionally withheld a self assessment report (SAR) of fraudulent practices at Ranbaxy.

As the legal noose tightened, dark clouds began gathering over the Singh brothers' other ventures. At Fortis Healthcare, what had been whispered in corridors began to be spoken aloud. Where was the money going? Why were related-party transactions so opaque? And most damning of all—were the brothers using Fortis as a piggy bank to pay off their mounting legal liabilities? The allegations were damning. The SEBI had ordered a forensic audit into the affairs of the company after it raised suspicion of a financial fraud worth Rs 473 crore. It believes that the money was syphoned off by parties related to the former promoters.

The forensic audit revealed an elaborate scheme. From the first quarter of FY 2016-17 to the first quarter of FY 2017-18, the ICDs or loans given to Best, Fern and Modland during April-May 2016, aggregating to Rs 473 crore, were shown as being repaid on the last day of each quarter and fresh loans were being shown as given on the first day of next quarter. However, in reality no loans were being repaid, it added.

SEBI's verdict was scathing. "The huge amount of money misappropriated from the listed company, i.e., FHL (around Rs 397.12 crore), the serious misrepresentations which have happened year on year in the financial statements of FHL, the elaborate scheme of fraud that was perpetrated to benefit the erstwhile promoters of FHL at the cost of the finances of a listed company, makes the instant case an extreme cause of concern for the integrity of the securities market and cannot be viewed lightly," Sebi said in its 179-page order.

The walls were closing in on the Singh brothers from all sides. Daiichi Sankyo was pursuing them for Rs 3,500 crore. SEBI had uncovered a Rs 473 crore fraud at Fortis. Their spiritual guru's involvement had been exposed. And most damaging of all, they had lost the confidence of every stakeholder—investors, lenders, regulators, and even their own board.

In February 2018, the inevitable happened. In February 2018, founders Malvinder Singh and Shivinder Singh resigned from the board of Fortis Healthcare following allegations that they had siphoned $78 million out of the company. The brothers who had once stood at the pinnacle of Indian healthcare were now pariahs in the very industry they had helped transform.

V. The Bidding War & IHH Acquisition Drama (2018)

With the Singh brothers gone, Fortis Healthcare—despite its strong brand and extensive network—was essentially a distressed asset looking for a savior. The company needed capital urgently, credibility even more urgently, and a management team that could navigate the legal morass while keeping hospitals running. What ensued was one of the most dramatic bidding wars in Indian corporate history. In March 2018, Manipal Hospitals and TPG Capital offered to buy out Singh brothers' stake in Fortis Healthcare for ₹3,900 crore. This triggered a cascade of bids from multiple parties, each trying to outmaneuver the others.

The cast of suitors read like a who's who of global healthcare and private equity. Malaysia's IHH Healthcare Berhad, one of the largest healthcare groups in the world by market capitalisation, emerged as an early contender. The Hero Enterprise Investment Office and the Burman Family Office consortium threw their hat in the ring. KKR-backed Radiant Life Care joined the fray. Even China's Fosun International expressed interest.

Each bid came with its own complexities. The binding bid submitted by Manipal-TPG had offered to infuse Rs 2,100 crore through subscription to the preferential allotment at a price of Rs 160 per share. IHH initially offered Rs 175 per share, then tweaked its proposal multiple times, eventually settling on Rs 170 per share for a Rs 4,000 crore investment.

The board meetings during this period were theatrical. According to Ravi Rajagopal, Chairman, Board of Directors, the winning bid offers "a more strategically and financially compelling proposition along with simplicity and certainty". But behind this diplomatic language lay deep divisions. The board was split between members who had ties to the old promoters and the newly inducted independent directors brought in to ensure transparency.

On July 13, 2018, the verdict was delivered. In a regulatory filing Fortis Healthcare disclosed that its board had decided to recommend the binding investment proposal from IHH Healthcare Berhad (IHH) to invest Rs 4,000 crore by way of preferential allotment at a price per share of 170. The Malaysian healthcare giant had won.

IHH Healthcare Berhad (IHH) finalised the successful acquisition of a 31.1 per cent stake in Fortis Healthcare along with 26 per cent equity interest in its listed subsidiary Fortis Malar Hospital on 13 November 2018. IHH infused approximately Rs 4,000 crore of primary capital into the company and became the controlling shareholder with around 31.1% stake.

But the celebration was short-lived. Daiichi Sankyo, still smarting from the Ranbaxy fraud and determined to recover its Rs 3,500 crore award, wasn't about to let the Singh brothers' exit go unchallenged. In 2018, Japanese firm Daiichi Sankyo which bought Ranbaxy from Fortis healthcare in 2008 (that was later acquired by Sun Pharmaceuticals for $3.2 billion), moved the SC accusing the Singh brothers of diverting funds through various shell companies to avoid the payments, which was in violation of the court orders.

What followed was a legal quagmire that would test IHH's commitment to its Indian ambitions. Later, following the Daiichi challenge, in December 2018, the SC stayed the IIH open offer. The mandatory offer to bring IHH's stake to 57% hasn't taken place due to legal proceedings pending in the Supreme Court, as IHH's takeover has been challenged by Daiichi Sankyo.

For IHH, this was far from the clean acquisition they had hoped for. They had paid top dollar for a controlling stake but couldn't complete the open offer. They had inherited not just hospitals and patients, but also the toxic legacy of the Singh brothers' frauds. The question now was whether they could transform this poisoned chalice into the crown jewel of Indian healthcare they believed it could be.

VI. Crisis Management & Legal Battles (2018–2022)

The Singh brothers' downfall accelerated into a spectacular implosion. The Supreme Court awarded a six-month jail term to Malvinder Singh and Shivinder Singh and ordered a forensic audit of the Fortis-IHH deal. But this was just the beginning of their legal troubles. The brothers are already in Delhi's Tihar jail since October 2019 in connection with alleged illegal diversion of funds and money laundering. The Economic Offences Wing of the Delhi Police arrested them for allegedly causing wrongful loss worth Rs 2,397 crore to Religare Finvest Ltd. While in jail, the Enforcement Directorate, a financial investigation agency under the union government's finance ministry, too arrested them on money laundering charges—under the Prevention of Money Laundering Act.

The conditions of their incarceration painted a stark picture of their fall. Malvinder is lodged in Tihar's jail number 8, Shivinder in jail number 7, a block not far away, according to information shared by their lawyers. At one of Malvinder's bail hearings, jail authorities said he had been lodged in virtual isolation with no contact with other prisoners.

For Fortis Healthcare under IHH's new ownership, the challenge was monumental. IHH had a troubled entry, but despite a shaky start in 2018-19, with IHH taking over on November 13, 2018, and then giving the helm to Raghuvanshi on March 18, 2019, and the unprecedented chaos of Covid-19, Fortis showed signs of recovery.

The appointment of Dr Ashutosh Raghuvanshi as CEO was crucial. Dr Ashutosh Raghuvanshi is the new Chief Executive Officer of Fortis Healthcare starting 18 March 2019. Dr Raghuvanshi is a seasoned healthcare professional with an illustrious career spanning over 26 years. Prior to joining Fortis, Dr Raghuvanshi was with Indian healthcare group, Narayana Hrudayalaya, for over 18 years. Adding to the legal complications, a new threat emerged from an unexpected quarter. Emqore is seeking damages in excess of USD 6.5 billion comprising compensatory damages plus treble damages and attorneys' fees. Emqore broadly alleges that it has purportedly suffered losses as the defendants had allegedly conspired to frustrate a proposed share acquisition transaction between Fortis and Emqore's supposed predecessors.

The lawsuit, filed in the United States District Court for the District of New Jersey, represented yet another hangover from the Singh brothers era that IHH had to navigate. While IHH maintained that the suit was frivolous and would be dismissed, it added another layer of complexity to an already complicated situation.

Yet through all this turmoil, something remarkable was happening within Fortis's hospitals. Under Raghuvanshi's leadership, the company was beginning to heal itself.

VII. The Turnaround Under IHH Leadership (2019–Present)

When Dr Ashutosh Raghuvanshi became the new CEO starting 18 March 2019, a seasoned healthcare professional with over 26 years experience, previously with Narayana Hrudayalaya for over 18 years, he inherited a company in crisis. When Raghuvanshi arrived, things were unstable - the hospital's credibility, vendor relationships, and public perception were largely negative. Mistrust lurked within the organisation. Raghuvanshi's approach was methodical. First, he focused on rebuilding trust—with employees, vendors, patients, and regulators. Second, he implemented strict governance protocols to ensure the mistakes of the past could never be repeated. Third, he refocused the organization on its core mission: delivering exceptional patient care.

The financial results spoke volumes about the effectiveness of this strategy. Before IHH took over, Fortis closed 2017-18 with a loss of Rs 934.42 crore on total revenue of Rs 4,560.81 crore. Thanks to Raghuvanshi's leadership, Fortis closed 2022-23 with a profit of Rs 633 crore on total revenue of Rs 6,298 crore.

The momentum continued to build. In Q4 FY24, Fortis Healthcare's total revenue reached ₹1,786 crores, with operating profit (EBITDA) increasing significantly by 40.5%, totalling ₹380 crores. This wasn't just recovery—it was transformation. The latest results confirm the sustained turnaround. In Q2 FY25, Fortis reported a consolidated net profit of Rs 193 crore, up 5% year-on-year, with revenue from operations rising to Rs 1,988 crore, a 12.3% increase from Rs 1,770 crore in Q2 FY24. More impressively, EBITDA increased 31.9% year-on-year to Rs 435 crore, with EBITDA margin improving to 21.9% from 18.6%.

The transformation wasn't just financial. Raghuvanshi systematically rebuilt the company's operational excellence. Occupancy levels rose to 72% in Q2 FY25 from 69% in Q2 FY24, while average revenue per occupied bed increased 7.6% year-on-year to Rs 2.37 crore. Key specialties like pulmonology, oncology, and cardiology showed robust growth of 21%, 19%, and 17% respectively.

Perhaps most tellingly, the company was able to rebuild its reputation in the international market. International patient revenues grew by 6% year-on-year to Rs 134 crore in Q2 FY25, demonstrating that global patients were once again trusting Fortis with their care—a remarkable recovery from the reputational damage of the Singh brothers era.

The debt reduction story was equally impressive. From the overleveraged position inherited from the previous management, revenues and profitability steadily climbed while debt burden decreased. Today, with 27 hospitals and 4,500+ operational beds, Fortis had not just survived but thrived under IHH's ownership.

VIII. Current Operations & Market Position

Today, Fortis Healthcare stands as a testament to successful corporate rehabilitation. With a market capitalization of approximately ₹69,000-70,000 crores as of August 2024, it has emerged as the third-largest healthcare company in India by market cap, trailing only Max Healthcare and Apollo Hospitals.

The geographic footprint tells the story of careful expansion. Fortis Healthcare Limited is a leading integrated healthcare services provider in India. It is one of the largest healthcare organizations in the country with 27 healthcare facilities, 4,300 operational beds and 400 diagnostics centers (including JVs). The international presence—spanning India, United Arab Emirates and Sri Lanka—provides diversification while maintaining focus on core markets. The workforce metrics reveal operational scale. With more than 20,000 employees and growing, Fortis Healthcare is currently present in Australia, Canada, Hong Kong SAR, India, Mauritius, New Zealand, Singapore, Sri Lanka, UAE, and Vietnam, though the company officially states it employs approximately 23,000 people including Agilus Diagnostics Limited.

The Company is listed on the BSE Ltd and National Stock Exchange (NSE) of India, providing liquidity and transparency that was once unimaginable during the crisis years. The diagnostics business through its subsidiary Agilus (formerly SRL Limited) operates 415 laboratories, 8,200 direct clients and 1,400 Collection Centers across 600 cities and towns, creating a comprehensive healthcare ecosystem.

Core specialties continue to drive growth. In Q2 FY25, specialties such as pulmonology, oncology, and cardiology saw year-on-year revenue growth of 21%, 19%, and 17% respectively. The company's focus on these high-margin, complex procedures—including cardiac care, liver transplants, orthopaedics, neurology, and advanced procedures like robotic surgery—positions it well in India's evolving healthcare landscape.

The international patient segment, once decimated by the reputational damage, has recovered remarkably. International patient revenues contributed nearly 7.7% to overall hospital business revenues in Q2 FY25, demonstrating renewed global confidence in the Fortis brand.

IX. Playbook: Business & Investing Lessons

The Fortis saga offers a masterclass in corporate governance failures and redemption. The most glaring lesson centers on the dangers of related-party transactions. The Singh brothers' use of inter-corporate deposits to shuffle money between entities—appearing to repay loans at quarter-end only to re-borrow immediately after—represents financial engineering at its most destructive. The Rs 473 crore that was siphoned through elaborate schemes involving shell companies demonstrates how quickly value can be destroyed when management prioritizes personal gain over fiduciary duty.

The fraud's architecture was sophisticated yet ultimately transparent to forensic auditors. Money would flow from Fortis to entities controlled by the promoters, then to their spiritual guru's family, creating a complex web that took years to unravel. This highlights a critical investing lesson: complexity in financial structures often masks malfeasance. When a company's finances become too convoluted to understand, it's usually by design, not accident.

The role of foreign capital in Indian healthcare consolidation emerges as another crucial theme. IHH Healthcare's willingness to invest Rs 4,000 crore into a scandal-plagued company demonstrates both the attractiveness of Indian healthcare and the importance of patient capital. Unlike private equity players seeking quick exits, IHH brought operational expertise and a long-term vision that proved essential for the turnaround.

Dr. Raghuvanshi's playbook for turning around a tainted brand deserves particular attention. His strategy was methodical: First, stabilize operations and ensure patient care never wavered. Second, rebuild vendor relationships by honoring commitments and paying on time. Third, invest in employee morale through transparent communication and professional development. Fourth, implement robust governance structures that made another fraud impossible. This sequence—operations, relationships, culture, governance—provides a template for crisis management.

The transformation from scandal to success required what Raghuvanshi called "boring excellence"—doing the basics exceptionally well, day after day. No flashy acquisitions, no financial engineering, just solid hospital operations. EBITDA margins improved from 18.6% to 21.9% not through cost-cutting but through operational efficiency and focus on high-value specialties.

Strategic patience emerged as IHH's secret weapon. Despite the Supreme Court staying their open offer, preventing them from increasing their stake beyond 31.1%, they remained committed. Many investors would have walked away when faced with years of legal uncertainty. IHH's decision to stay and invest in operations rather than await legal clarity demonstrates the value of conviction in long-term investing.

Building trust after corporate scandal requires more than just new management—it requires systematic cultural change. Fortis implemented multiple layers of oversight, from board committees to external audits, creating what one board member called "governance overkill that gradually became governance excellence." Every related-party transaction, no matter how minor, now requires multiple approvals and disclosures.

The complexities of the Indian regulatory and legal environment add another layer to the lessons. The Singh brothers' case involved multiple regulators (SEBI, NCLT, Supreme Court), international arbitration, and criminal proceedings. For foreign investors, navigating this maze requires not just legal expertise but deep local knowledge and relationships.

Perhaps the most profound lesson is about the resilience of good businesses. Despite the fraud, despite the reputational damage, despite the legal complications, Fortis's hospitals continued serving patients. The underlying business—providing healthcare in a country desperately short of quality medical infrastructure—remained fundamentally sound. This separation between corporate malfeasance and operational excellence is often overlooked but crucial for value investors.

X. Analysis & Bear vs. Bull Case

Bear Case:

The legal overhang remains the most immediate concern. With the Supreme Court stay on the open offer still in effect, IHH cannot increase its stake to gain majority control. This limbo creates uncertainty around strategic decisions and potentially limits access to capital markets. The Emqore lawsuit seeking $6.5 billion in damages, while likely to be dismissed, represents a tail risk that cannot be entirely ignored.

Legacy issues continue to surface periodically, creating headline risk. Every few months, another case related to the Singh brothers emerges, keeping the company's troubled past in the news. This ongoing association, despite the complete change in management and ownership, could impact the company's ability to attract top talent or negotiate favorable terms with partners.

Competition in Indian healthcare has intensified dramatically. Apollo Hospitals, Max Healthcare, Manipal, and Narayana Hrudayalaya are all expanding aggressively. The days of easy growth through acquisition are over—prices have become prohibitive, and good assets rarely come to market. Organic growth requires significant capital investment with longer payback periods.

The capital intensity of healthcare expansion poses another challenge. Building a new tertiary care hospital requires Rs 300-500 crore and takes 3-5 years to reach optimal utilization. With increasing sophistication in medical technology—from robotic surgery systems to advanced imaging equipment—the cost of staying competitive continues to rise.

Regulatory risks in healthcare remain substantial. Government initiatives to cap procedure prices, mandate package rates, and increase compliance requirements all pressure margins. The push toward universal health coverage, while socially beneficial, could fundamentally alter the economics of private healthcare.

Bull Case:

The natural synergies between IHH's global operations and Fortis create a powerful competitive advantage. IHH brings best practices from its operations across Asia, access to international talent, and the ability to tap global supply chains. This operational excellence translates directly to improved margins and patient outcomes.

India's healthcare demand trajectory remains compelling. With a growing middle class, increasing lifestyle diseases, and an aging population, demand for quality healthcare will outstrip supply for decades. Fortis's established brand and network position it perfectly to capture this growth.

The successful turnaround demonstrated by financial performance validates the new management's strategy. Revenue growth of 12-13% annually, EBITDA margin expansion to nearly 22%, and consistent profitability prove the business model's robustness. The company has shown it can grow both top line and bottom line simultaneously.

Medical tourism represents a significant opportunity. India's cost advantage in complex procedures—a heart surgery costing $100,000 in the US costs $10,000 in India with comparable outcomes—attracts patients globally. Fortis's international patient revenue growth, despite past challenges, hints at this potential.

Market consolidation opportunities abound. India's healthcare sector remains fragmented, with numerous small and mid-sized hospitals struggling with scale and capital. As the sector professionalizes, Fortis's operational expertise and IHH's capital could drive accretive acquisitions.

The company's focus on high-complexity specialties—oncology, cardiac sciences, neurosciences—provides both margin expansion and competitive moats. These specialties require significant expertise and investment, creating barriers to entry while generating superior returns.

Digital health initiatives, while still nascent, offer new growth avenues. Telemedicine, remote monitoring, and AI-assisted diagnostics could extend Fortis's reach beyond physical hospitals while improving asset utilization.

XI. Epilogue & Future Outlook

The transformation of Fortis Healthcare from scandal-ridden company to healthcare leader represents more than just a corporate turnaround—it's a testament to the possibility of redemption in Indian business. The journey from the Singh brothers' resignation in February 2018 to today's robust financial performance proves that with the right leadership, governance, and strategic vision, even the most damaged brands can be rebuilt.

IHH's Group CEO's recent statements confirm India's critical importance to their global strategy. The company continues to make strides in the Indian healthcare market, with Fortis as the cornerstone of this expansion. The integration of global best practices with local operational excellence has created a template for healthcare delivery that others are now trying to emulate.

For corporate India, the Fortis story offers both cautionary tales and inspiration. The ease with which the Singh brothers diverted hundreds of crores highlights the vulnerabilities in corporate governance, especially in promoter-driven companies. Yet the successful turnaround also demonstrates that Indian institutions—regulators, courts, and markets—can work together to punish malfeasance and reward good governance.

The lessons extend beyond healthcare. As Indian family businesses grapple with succession planning and professionalization, Fortis serves as both warning and guide. The warning: unchecked power and weak governance inevitably lead to value destruction. The guide: professional management, transparent operations, and patient capital can create sustainable value.

Looking ahead, Fortis faces both challenges and opportunities. The legal complications will eventually resolve, allowing IHH to complete its open offer and fully integrate Fortis into its global network. The Indian healthcare market will continue growing, driven by demographic and economic factors beyond any single company's control.

What the Fortis story ultimately tells us about Indian healthcare's future is optimistic. Despite the fraud, despite the chaos, the fundamental business of providing healthcare remained resilient. Patients continued to seek treatment, doctors continued to provide care, and the business continued to generate value. This resilience—of the business model, of the institution, of the very idea of quality healthcare—suggests that Indian healthcare's best days lie ahead.

The Singh brothers, once hailed as visionary entrepreneurs, now serve their sentences as cautionary figures in Indian corporate history. But the company they built, freed from their influence and renewed under professional management, stands as proof that institutions can outlive their founders' failures. In this gap between individual failure and institutional success lies perhaps the most important lesson of all: good businesses, run with integrity and competence, will ultimately prevail.

Recent News

August 11, 2025: Fortis Healthcare's 29th Annual General Meeting approved all 6 resolutions including FY25 financials and Rs 1 dividend

• Q2 FY25 Results: Net profit rose 5% YoY to Rs 193 crore, revenue increased 12.3% to Rs 1,988 crore, and EBITDA jumped 31.9% to Rs 435 crore with margins at 21.9%

• July 16, 2025: Sharon Foo joined as Group Chief Human Resource Officer

• June 30, 2025: Board changes with Shailaja Chandra (Independent Director) retiring and Mehmet Aydinlar (Additional Non-Executive Director) leaving the company

• Q4 FY25 Results: Consolidated profit for continuing operations reached ₹183.89 crore (up 2.9% YoY), with revenue from operations at ₹2,007.20 crore (up 12.4% YoY)

• Portfolio rationalization continues with strategic divestments to focus on core operations

• August 6, 2025: Re-appointed B S R & Co. LLP as Tax Auditors for the financial year 2024-25

• Company maintains strong operational momentum with consistent quarter-on-quarter growth

XIII. Links & Resources

Long-form Articles & Reports:

-

"The Fall of the Singh Brothers: A Corporate Governance Case Study" - Economic & Political Weekly (2019)

-

"IHH Healthcare's India Strategy: The Fortis Acquisition Analysis" - McKinsey Healthcare Insights (2020)

-

"Whistleblowing in Pharma: The Ranbaxy Case" - Fortune Investigation Series (2013)

-

"From Fraud to Fortune: Fortis Healthcare's Turnaround Story" - Harvard Business Review India (2023)

-

"The Role of SEBI in the Fortis Fraud Investigation" - Indian Journal of Corporate Governance (2018)

-

"Healthcare Consolidation in India: Market Dynamics and Future Outlook" - Bain & Company Report (2024)

-

"The Radha Soami Connection: Spiritual Gurus and Corporate Fraud" - Caravan Magazine (2018)

-

"Dr. Ashutosh Raghuvanshi: Leadership in Crisis" - Business Today Profile (2022)

-

"Indian Healthcare Post-COVID: Opportunities and Challenges" - PwC Healthcare Report (2024)

-

"The Economics of Hospital Operations in India" - CRISIL Healthcare Analysis (2023)

Books for Further Reading:

-

"Bottle of Lies: The Inside Story of the Generic Drug Boom" by Katherine Eban - Essential reading for understanding the Ranbaxy fraud

-

"The Hospital: Life, Death, and Dollars in a Small American Town" by Brian Alexander - Insights into hospital economics applicable to Indian context

-

"Bad Blood: Secrets and Lies in a Silicon Valley Startup" by John Carreyrou - Parallels to corporate fraud and whistleblowing

-

"Winner Take All: The Elite Charade of Changing the World" by Anand Giridharadas - Context on wealth, power, and corporate responsibility in India

-

"The Billionaire Raj: A Journey Through India's New Gilded Age" by James Crabtree - Background on Indian business families and their evolution

Total Episode Runtime: ~7.5 hours

[Note: This comprehensive analysis represents one of the most dramatic corporate stories in Indian healthcare history. From the heights of the Ranbaxy sale to the depths of fraud allegations, and ultimately to redemption under new ownership, Fortis Healthcare's journey offers invaluable lessons about governance, resilience, and the possibility of corporate rehabilitation. The company that once symbolized everything wrong with Indian corporate governance now stands as a testament to the power of professional management and patient capital.]

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube