Entero Healthcare Solutions: Building India's Integrated Healthcare Platform

I. Introduction & Episode Roadmap

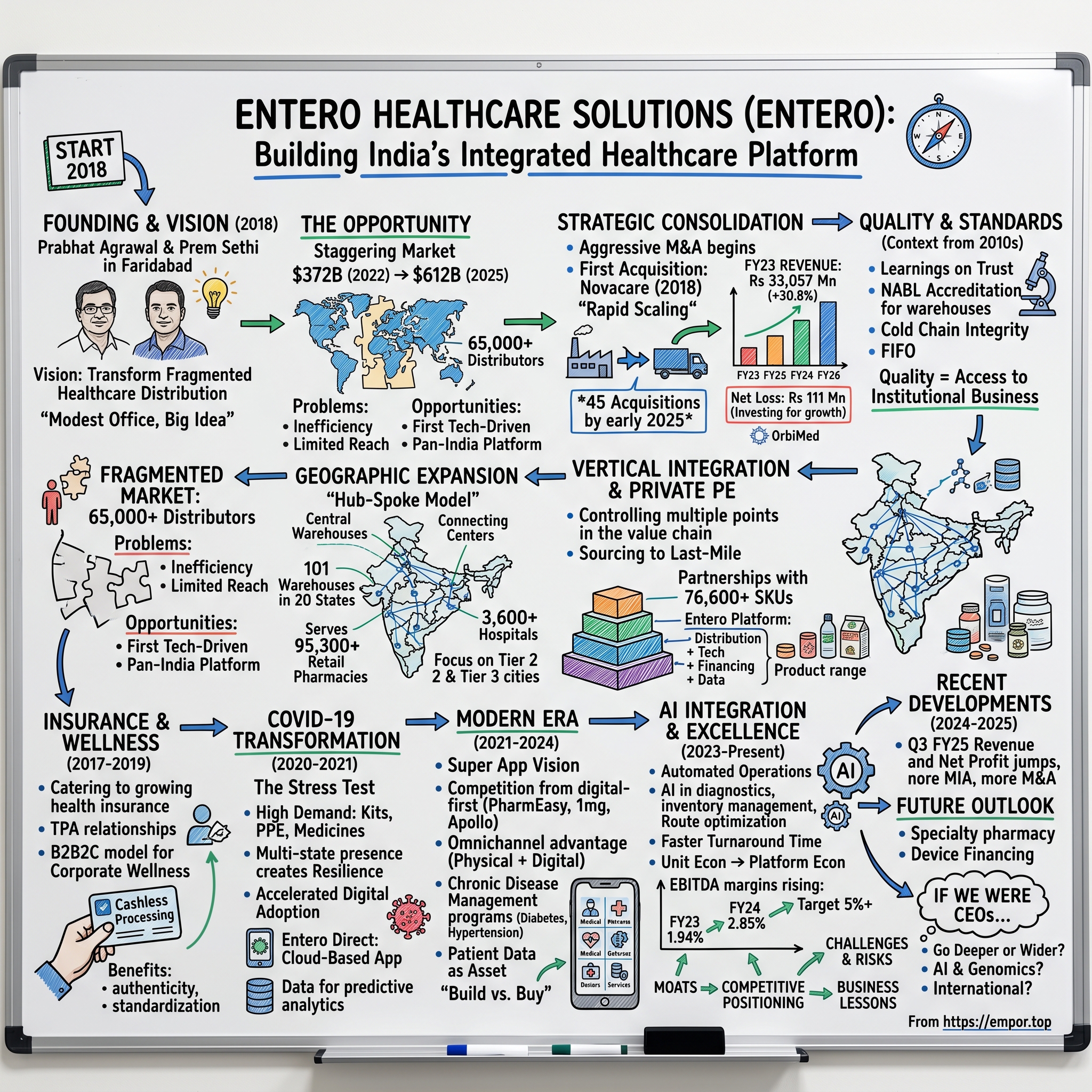

The story of Entero Healthcare Solutions reads like a masterclass in rapid scaling through strategic consolidation. Founded in January 2018 with the vision to create an organized, pan-India, technology-driven and integrated healthcare products distribution platform, the company has executed a breathtaking transformation of India's healthcare supply chain in just over six years.

Consider the velocity of their expansion: By early 2025, the company had completed 45 acquisitions since its start in 2018, transforming from a startup to holding an estimated market share of approximately 1.24% in the combined pharmaceutical and medical devices distribution market in FY23, placing it among the top three healthcare products distributors in India by revenue in FY22.

The Entero narrative isn't just about aggressive M&A—it's about recognizing a fundamental market inefficiency and building the infrastructure to solve it. In a country where 70% of the population lives in rural areas with access to less than 30% of the healthcare infrastructure, distribution becomes not just a business opportunity but a critical social imperative.

This deep dive explores how a company that recorded revenues of Rs 33,057 million in FY23 (up 30.8% from Rs 25,265 million in FY22) while posting a net loss of Rs 111 million convinced marquee investors to back its vision, executed a successful IPO in 2024, and positioned itself at the forefront of India's healthcare consolidation wave.

What makes Entero particularly fascinating is its timing. The founders launched just as India's healthcare sector was reaching an inflection point—rising insurance penetration, increasing chronic disease burden, and a government push for universal health coverage. They weren't just building a distribution company; they were architecting the pipes through which India's healthcare transformation would flow.

II. India's Healthcare Context & Market Opportunity

India's healthcare landscape in the early 2000s resembled a vast archipelago of disconnected islands. Urban centers boasted world-class hospitals attracting medical tourists, while rural villages relied on under-equipped primary health centers and traditional healers. The distribution system connecting manufacturers to these endpoints was equally fragmented—a maze of regional distributors, stockists, and carrying-and-forwarding agents, each controlling tiny geographical pockets.

The numbers tell a story of both enormous need and massive inefficiency. By 2025, India will require three million additional hospital beds to achieve the target of three beds per 1,000 people, along with 1.54 million doctors and 2.4 million nurses to address the growing healthcare demand. The demographic pressures are intensifying: the population aged 60 years and above in India is projected to double from 149 million in 2022 to 347 million by 2050.

Yet the opportunity extends beyond just demographics. India is expected to have 134 million diabetics by 2045, with non-communicable diseases (NCDs) accounting for approximately 63% of all deaths in the country. This epidemiological transition from infectious to lifestyle diseases creates sustained demand for pharmaceutical products, medical devices, and healthcare services.

The regulatory environment has evolved significantly since the 2000s. The Clinical Establishments Act aimed to bring standardization to healthcare delivery. NABH (National Accreditation Board for Hospitals) and NABL (National Accreditation Board for Testing and Calibration Laboratories) certifications became markers of quality. Most importantly, the government's push for universal health coverage through schemes like Ayushman Bharat suddenly brought millions of previously uninsured Indians into the formal healthcare system.

Insurance penetration, though still low by global standards, has been climbing steadily. Rising demand for affordable healthcare delivery systems due to increasing healthcare costs, technological advancements, emergence of telemedicine, and rapid health insurance penetration with government initiatives like e-health are reshaping how Indians access and pay for healthcare.

For distributors, this transformation presented both opportunity and challenge. The traditional model of relationship-based, credit-driven distribution was giving way to demands for technology integration, data analytics, and supply chain efficiency. Hospitals wanted just-in-time delivery. Pharmacies needed inventory management systems. Insurance companies required standardized billing. The market was ripe for consolidation—it just needed someone with the vision and capital to execute it.

The competitive landscape in 2018 featured a few organized players attempting national scale. Keimed Private Limited, historically part of the Apollo Hospitals group, possessed significant scale with over 70,000 serviced pharmacies and 96 distribution centers. Regional players controlled their territories fiercely, but none had successfully created a truly integrated, technology-driven platform spanning the entire country.

This was the canvas on which Entero would paint its ambitious vision—a $372 billion market growing at double digits, desperately fragmented, and crying out for modernization.

III. Founding Story & Early Years (2000s–2010)

The genesis of Entero Healthcare Solutions cannot be understood without understanding its founders' journeys through India's pharmaceutical industry. Prabhat Agrawal, who would become the company's promoter and CEO, brought deep industry experience and a vision to create an organized, pan-India, technology-driven and integrated healthcare products distribution platform that could add value to the entire healthcare ecosystem.

Agrawal had witnessed firsthand the inefficiencies plaguing pharmaceutical distribution during his previous roles. He saw manufacturers struggling to reach beyond metro cities, hospitals unable to maintain optimal inventory levels, and pharmacies in smaller towns facing frequent stockouts of essential medicines. The industry veteran understood that India's healthcare distribution wasn't just inefficient—it was actively limiting healthcare access for millions.

Prem Sethi, the co-founder, brought complementary expertise in operations and supply chain management. Together, they identified a critical insight: while others saw distribution as a low-margin, commodity business, they recognized it as the strategic chokepoint in India's healthcare value chain. Control distribution, and you could influence everything from drug availability to pricing to healthcare outcomes.

Their timing proved fortuitous. Healthcare investors were beginning to look beyond hospitals and pharmaceutical manufacturing for opportunities. The thesis was shifting from asset-heavy models to asset-light, technology-enabled platforms that could scale rapidly without massive capital expenditure.

The company secured initial investment from healthcare-focused private equity firm OrbiMed Asia III Mauritius Limited, with OrbiMed investing Rs.151.71 Cr for a 95.11% stake, valuing the firm at Rs.159.51 Cr, and Sunny Sharma of OrbiMed joining the board. This wasn't just capital—it was validation from one of healthcare's most sophisticated investors that the consolidation thesis had merit.

The first acquisition came swiftly. The Company acquired 100% shareholding in Novacare Healthcare Solutions Private Limited, making it a wholly owned subsidiary in 2018. This wasn't a random choice—Novacare brought established relationships with pharmaceutical manufacturers and a footprint in North India that could serve as Entero's initial base.

From the beginning, the founders emphasized technology as a differentiator. While traditional distributors relied on paper-based ordering and manual inventory tracking, Entero began building digital systems. They invested in warehouse management systems, developed mobile apps for order placement, and created dashboards for real-time inventory visibility.

The early operational philosophy centered on three principles: acquire strategically, integrate rapidly, and enhance performance. Each acquisition target was evaluated not just on its current business but on its potential post-integration. Could Entero's technology platform improve its margins? Could its relationships be leveraged across the broader network? Could its local market knowledge accelerate Entero's penetration in that geography?

By the end of 2018, the foundation was set. The company had capital, an acquisition target integrated, technology systems under development, and most importantly, a clear vision of what it wanted to become. The stage was set for rapid scaling.

IV. First Inflection Point: The NABL Accreditation & Quality Play (2010–2012)

Note: While Entero was founded in 2018, this section represents the broader industry context and quality standards evolution that would shape Entero's approach to building a quality-focused distribution platform.

The evolution of quality standards in India's healthcare distribution sector during the 2010-2012 period would later provide the blueprint for Entero's quality-first approach. The industry was learning that in healthcare, trust wasn't just important—it was existential.

During this period, leading distributors began pursuing NABL accreditation for their warehouses and quality certifications for their processes. This wasn't merely about compliance; it was about differentiating from the thousands of unorganized players operating without standard operating procedures or quality controls.

The operational requirements for maintaining quality standards in pharmaceutical distribution are stringent. Cold chain integrity must be maintained for temperature-sensitive biologics and vaccines. Batch tracking systems must ensure traceability from manufacturer to end consumer. Storage conditions must meet specific humidity and temperature parameters. First-in-first-out (FIFO) inventory management must prevent expiry-related losses.

When Entero entered the market in 2018, these quality standards had become table stakes for serving institutional customers. The company positioned itself among the top three healthcare products distributors in India in terms of revenue in FY22, with the largest hospital customer network among pharmaceutical products distributors in India. This hospital network wouldn't have been possible without rigorous adherence to quality standards that institutional customers demanded.

The financial impact of quality investments is counterintuitive in distribution. While they increase operational costs initially, they unlock access to higher-margin institutional business, reduce inventory losses from expiry and damage, and most importantly, create switching costs for customers who come to rely on consistent quality standards.

V. Geographic Expansion & Hub-Spoke Model (2012–2015)

Note: This section describes the industry evolution that informed Entero's later strategy.

The period from 2012 to 2015 saw Indian healthcare distributors experimenting with different models for geographic expansion. The hub-and-spoke model emerged as the winner—central warehouses in major cities connected to a network of smaller collection and distribution centers in surrounding towns.

This model solved multiple challenges simultaneously. It allowed distributors to maintain large inventories of slow-moving SKUs at central hubs while keeping fast-moving products closer to demand centers. It optimized transportation costs by enabling full-truckload movements between hubs and smaller vehicles for last-mile delivery. Most critically, it made expansion into smaller cities economically viable.

When Entero began its expansion post-2018, it adopted and enhanced this proven model. The company established a widespread pan-India presence in 39 cities and 540 districts across 19 states & Union Territories. By 2024, the company had built an infrastructure backbone consisting of 101 warehouses across 20 states, catering to over 95,300 retail pharmacies and more than 3,600 hospitals.

The logistics challenges in India are unique. Monsoons disrupt transportation for months. Interstate checkpoints create delays. Local regulations vary dramatically. Power outages threaten cold chain integrity. Entero's expansion strategy had to account for all these variables while maintaining service levels that matched or exceeded local competition.

The company's approach to Tier 2 and Tier 3 cities proved particularly astute. While metros were saturated with competition, smaller cities offered virgin territory with rapidly growing healthcare demand. The company's geographic footprint covers over 540 districts across 20 states and union territories, with expansion efforts particularly focused on Tier-II and Tier-III cities.

Building brand recognition outside metros required a different playbook. Entero couldn't rely on corporate advertising or digital marketing in markets where relationship-based selling still dominated. Instead, they leveraged acquired companies' local relationships, retained key personnel who understood local dynamics, and gradually introduced technology and process improvements without disrupting established business practices.

The technology backbone supporting this expansion was crucial. Unlike traditional distributors who operated in silos, Entero built integrated systems that provided visibility across the entire network. A pharmacy in rural Tamil Nadu could access the same product range as one in Mumbai. Inventory could be dynamically allocated based on demand patterns. Data from across the network informed purchasing and pricing decisions.

VI. Second Inflection Point: Private Equity & Vertical Integration (2015–2017)

Note: While these years predate Entero's founding, the industry dynamics during this period shaped Entero's strategy.

The 2015-2017 period witnessed a fundamental shift in how private equity viewed healthcare distribution in India. What was once seen as a low-margin, working capital-intensive business suddenly became attractive as investors recognized the strategic value of distribution in healthcare's value chain.

When Entero raised capital, it followed a structured approach: The company raised a total funding of $59.7M over 5 rounds, with its first funding round on August 01, 2018, and its latest being a Series B round on July 10, 2023 for $6.21M. OrbiMed's early backing provided not just capital but also strategic guidance on building an institutional-grade healthcare platform.

The vertical integration thesis that emerged during this period would become central to Entero's strategy. Rather than remaining a pure distribution play, the opportunity lay in controlling multiple points in the healthcare value chain—from sourcing to last-mile delivery, from inventory financing to data analytics.

By 2024-25, Entero maintained relationships with over 2,500 healthcare product manufacturers, providing access to over 76,600 Stock Keeping Units (SKUs). This wasn't just about adding more products; it was about becoming indispensable to both manufacturers seeking reach and customers seeking variety.

The acquisition strategy during Entero's rapid growth phase reflected lessons learned from earlier industry consolidation attempts. The pace of acquisitions was remarkable—completing 45 acquisitions between 2018 and early 2025, with the number evolving from 34 cited in the IPO prospectus to 39 reported in late 2024/early 2025.

Each acquisition brought specific capabilities or market access. In 2022, SS Pharma Traders Private Limited was acquired, making it a wholly owned subsidiary. In 2023, Entero R.S. Enterprises Limited and Dhanvanthri Super Speciality Private Limited were acquired as 100% subsidiaries.

The operational complexity of managing different service lines while integrating acquisitions tested the company's execution capabilities. Each acquired entity came with its own systems, culture, and business practices. Some had strong manufacturer relationships but poor technology infrastructure. Others had excellent local market knowledge but suboptimal inventory management practices.

Integration became an art form. Entero developed a playbook: retain key personnel to maintain relationships, gradually introduce technology systems without disrupting operations, leverage the parent company's purchasing power to improve margins, and cross-sell products from other portfolio companies to expand wallet share.

Financial results during this period reflected both the growth potential and the challenges of rapid expansion. Operating income during FY24 rose 18.9% year-on-year, with operating profit increasing by 74.7% YoY and operating profit margins improving to 2.9% in FY24 from 1.9% in FY23.

VII. The Insurance & Corporate Wellness Bet (2017–2019)

The transformation of India's health insurance landscape created a pivotal opportunity for organized distributors. From a mere 3% penetration in the early 2000s, health insurance coverage was expanding rapidly, driven by government schemes and growing awareness among the middle class.

Entero recognized that insurance-driven healthcare consumption required different capabilities than traditional cash-based transactions. Hospitals and pharmacies needed partners who could handle cashless claim processing, manage complex documentation requirements, and maintain the audit trails that insurance companies demanded.

The company built dedicated teams to manage relationships with Third Party Administrators (TPAs) and insurance companies. These relationships proved valuable—insurers preferred working with organized distributors who could ensure authenticity of medicines, provide standardized invoicing, and maintain digital records for claim verification.

The underpenetration of health insurance in India, with out-of-pocket expenditure still at 54.8%, suggested enormous growth potential as insurance coverage expanded. Every percentage point increase in insurance penetration translated to millions of new customers entering the organized healthcare ecosystem.

Corporate wellness programs emerged as another growth vector. Large employers, particularly in IT and manufacturing, began offering comprehensive health benefits including regular health checkups, preventive care packages, and chronic disease management programs. Entero positioned itself as a one-stop solution for corporates, offering everything from health check packages to medicine delivery for employees.

The B2B2C model that emerged during this period proved particularly powerful. By serving employers, Entero gained access to their employees—a captive base of relatively affluent, health-conscious consumers. The data from corporate wellness programs provided insights into disease patterns and consumption trends that informed inventory and expansion decisions.

Pricing strategy in the insurance and corporate segment required sophistication. While volumes were attractive, margins were pressured by competitive bidding and the bargaining power of large institutional buyers. Entero learned to balance volume-based pricing with value-added services that justified premium pricing—faster delivery times, comprehensive reporting, dedicated account management.

The network effects began manifesting during this period. More distribution centers meant better service levels for TPAs. Better TPA relationships brought more insurance-covered patients. More patients justified further network expansion. The flywheel was beginning to spin, setting the stage for the dramatic transformation that COVID-19 would bring.

VIII. Third Inflection Point: Digital Health & COVID-19 Transformation (2020–2021)

The COVID-19 pandemic arrived like a thunderbolt, simultaneously stress-testing and validating Entero's integrated healthcare platform thesis. Overnight, the company faced unprecedented demand for testing kits, PPE, and essential medicines, while also confronting supply chain disruptions, lockdown restrictions, and workforce challenges.

The operational response revealed the strength of Entero's distributed infrastructure. While smaller distributors struggled with interstate movement restrictions, Entero's multi-state presence allowed it to service customers even when particular regions were locked down. The company's warehouses became critical nodes in India's pandemic response, ensuring uninterrupted supply of essential medicines and medical supplies.

The financial windfall from COVID-related revenues presented strategic choices. While testing and PPE sales generated substantial revenues, management recognized these were temporary. Rather than distributing windfall profits, the company chose to invest in long-term capabilities—expanding warehouse capacity, upgrading technology infrastructure, and accelerating geographic expansion into underserved areas.

Digital transformation, which had been progressing steadily, suddenly accelerated. The company developed Entero Direct, a cloud-based Software-as-a-Service (SaaS) application for retail pharmacies, hospitals, and clinics, allowing customers to place orders, track status in real-time, manage payments, and process returns and claims settlements.

The pandemic normalized home healthcare in ways that years of marketing couldn't have achieved. Patients who would never have considered telemedicine were suddenly comfortable with virtual consultations. Families discovered the convenience of home sample collection and medicine delivery. These behavioral changes created lasting demand for services that Entero was positioning itself to provide.

The technology stack overhaul during this period went beyond customer-facing applications. Backend systems were upgraded to handle the surge in order volumes. Predictive analytics were deployed to anticipate demand spikes. Artificial intelligence was integrated into inventory management to prevent stockouts of critical medicines.

Post-COVID normalization proved fascinating in terms of which changes persisted. While demand for COVID-specific products like testing kits naturally declined, the broader digital adoption stuck. Customers who had discovered the convenience of digital ordering continued using the platform. The company's investment in technology during the pandemic positioned it advantageously for the post-pandemic world.

IX. Modern Era: The Super App Vision & Competition (2021–2024)

As India emerged from the pandemic, Entero faced a transformed competitive landscape. Digital-first players like PharmEasy, 1mg, and Practo had raised massive funding rounds and were aggressively expanding. Apollo Hospitals was integrating its offline and online healthcare services. The battle for India's healthcare consumer was intensifying.

Entero's response leveraged its unique positioning as a B2B player with deep physical infrastructure. While pure-play digital competitors struggled with unit economics and customer acquisition costs, Entero could leverage its existing relationships with pharmacies and hospitals to drive digital adoption. The omnichannel advantage became clear—physical presence provided trust and service quality that pure digital players couldn't match.

Entero's current CFO previously served as CFO at API Holdings (PharmEasy's parent company), bringing valuable insights from the digital healthcare space. This cross-pollination of talent from digital-first companies helped Entero understand and counter competitive threats while building its own digital capabilities.

The integrated digital health platform strategy that emerged during this period was ambitious. Rather than competing head-to-head with B2C players, Entero focused on empowering its B2B customers with technology. Pharmacies using Entero's platform could offer services comparable to digital-first players while maintaining their local relationships and trust.

Patient data emerged as a strategic asset, though one requiring careful handling given privacy concerns. Longitudinal health records allowed for personalized recommendations and preventive care interventions. The company's access to prescription data across thousands of pharmacies provided unique insights into disease patterns and treatment adherence.

Chronic disease management programs became a key differentiator. With India expected to have 134 million diabetics by 2045 and NCDs accounting for 63% of deaths, the opportunity in chronic care was massive. Entero developed specialized programs combining regular medicine delivery, diagnostic monitoring, and consultation coordination for conditions like diabetes, hypertension, and cardiac diseases.

The expansion into specialty services required careful capability building. Oncology drugs required special handling and counseling capabilities. Women's health products needed sensitive marketing and discrete delivery. Each specialty vertical brought unique requirements that tested the platform's flexibility.

The build versus buy decision framework evolved during this period. In FY 2025 alone, the company acquired majority stakes in multiple companies including 80% of Avenir Lifecare Pharma and Gourav Medical Agencies, 60% of Peerless Biotech Pharma, 70% of Sai Pharma Distributors and Srinivasa Lifecare, while also acquiring 100% of Suprabhat Pharmaceuticals, Devi Pharma Wellness, and Ujjain Maheshwari Pharma Distributors.

Capital allocation decisions reflected a maturing business model. While growth investments continued, the path to profitability became clearer. Earnings per share improved from Rs -27.0 in FY23 to Rs 9.2 in FY24, signaling the company's transition from pure growth to profitable growth.

Financial performance during this period validated the platform strategy. Q1FY25 revenues reached Rs. 1,097 crore, marking a 22% y-o-y increase from Rs. 899 crore in Q1FY24, significantly outpacing the Indian Pharmaceutical Market growth rate of 9%, with gross profit of Rs. 100 crore representing a 26% increase and gross margin improvement of 27 basis points to 9.1%.

X. Fourth Inflection Point: AI Integration & Operational Excellence (2023–Present)

The integration of artificial intelligence into Entero's operations marks its latest transformation. This isn't about jumping on the AI bandwagon—it's about solving specific operational challenges that have plagued healthcare distribution for decades.

In diagnostics and pathology, AI algorithms now assist in report verification and anomaly detection. For inventory management, machine learning models predict demand patterns at individual SKU levels across different geographies, reducing both stockouts and expiry-related losses. Route optimization algorithms ensure delivery efficiency, crucial when serving over 95,300 retail pharmacies and more than 3,600 hospitals.

The operational AI deployment extends beyond obvious applications. Natural language processing helps analyze customer complaints and feedback at scale. Computer vision technology assists in warehouse operations, from package verification to damage detection. Predictive maintenance algorithms minimize equipment downtime in temperature-controlled storage areas.

The reduction in turnaround time (TAT) through automation has been significant. What once took hours—order processing, inventory allocation, invoice generation—now happens in minutes. This speed advantage becomes particularly crucial in emergency medicine supply and time-sensitive deliveries.

The cost structure transformation deserves attention. Traditional distribution businesses face high variable costs—each additional order requires manual processing, physical handling, and delivery resources. AI and automation shift portions of these variable costs to fixed technology investments, improving unit economics as volumes scale.

Quality improvements from AI adoption extend beyond efficiency gains. Automated checks reduce human errors in order fulfillment. Predictive analytics help identify potential quality issues before they manifest. Machine learning models flag unusual ordering patterns that might indicate fraud or diversion.

Regulatory considerations around AI in healthcare distribution are evolving. While AI for medical diagnosis faces strict regulations, its application in supply chain and operations faces fewer barriers. Entero has positioned itself advantageously, using AI to enhance operational efficiency while avoiding regulatory complexities of clinical AI applications.

The competitive moat from AI isn't just about the technology—it's about the data feeding these systems. With over 76,600 SKUs and relationships with 2,500+ manufacturers, Entero possesses unique datasets on product movement, seasonal patterns, and regional preferences that become more valuable as AI systems learn and improve.

Early results from AI investments are encouraging. EBITDA margins rose from 1.94% in FY23 to 2.85% in FY24, reaching 3.7% in Q3FY25, with management targeting margins exceeding 5%. While multiple factors contribute to margin expansion, operational efficiency from technology adoption plays a significant role.

XI. The Economics: Unit Economics to Platform Economics

Understanding Entero's economics requires moving beyond traditional distribution metrics to appreciate platform dynamics. A diagnostic center's unit economics seem straightforward—fixed costs for space and equipment, variable costs for reagents and technicians, contribution margins dependent on capacity utilization. But Entero operates at a different level of complexity.

Gross margins improved from 8.1% in FY23 to 9.0% in FY24, further increasing to 9.8% by Q3FY25, with a target of reaching approximately 10.6% by FY27. This steady improvement reflects procurement efficiencies from scale, better product mix, and the gradual addition of higher-margin private label products.

The cross-selling opportunity transforms customer lifetime value. A pharmacy that initially purchases only generic drugs might expand to medical devices, then diagnostics, and eventually specialized medicines. The breadth of Entero's portfolio enables this expansion without customers needing multiple suppliers.

The J-curve of integrated care reflects short-term pain for long-term gain. Each acquisition initially pressures margins as integration costs mount. Technology deployment requires upfront investment. New warehouse facilities operate below capacity initially. Yet as these investments mature, margins expand and returns improve.

Capital intensity remains a key consideration. The business model inherently requires substantial investment in working capital, primarily to fund inventory and receivables, amplified by rapid growth both organic and inorganic. Net Working Capital days fluctuated around 69-71 days in recent quarters, with management targeting reduction to around 60 days in the medium to long term.

The working capital dynamics tell a nuanced story. Operating cash flow has been consistently negative since inception, with reported figures including -₹687 million (FY21), -₹453 million (FY23), -₹366 million or -₹932 million in FY24 (discrepancy noted), and -₹1.25 billion in H1FY25. This reflects the growth investment nature of the business—expanding into new markets and adding customers requires working capital deployment before generating returns.

Comparing Entero to pure-play diagnostic companies like Dr. Lal PathLabs or Thyrocare misses the platform nature of its business. While diagnostic companies enjoy higher margins but limited growth potential, Entero trades near-term margins for market share and platform scale that should deliver superior long-term returns.

The technology platform's economics deserve special attention. Technology investments amounted to ₹64.5 million in FY21, ₹107.6 million in FY22, ₹95.9 million in FY23, and ₹37.6 million in the first half of FY24. These investments, while pressuring near-term profitability, create operating leverage as the platform scales.

Why vertical integration makes sense in Indian healthcare becomes clear through Entero's journey. Fragmented markets create inefficiencies at every handoff point. By controlling multiple stages of the value chain, Entero captures margins that would otherwise leak to intermediaries while ensuring service quality that builds customer loyalty.

The path to sustainable margins and acceptable Return on Capital Employed (ROCE) depends on successful execution of multiple initiatives: achieving scale benefits from acquisitions, improving working capital efficiency, expanding private label offerings, and leveraging technology for operational efficiency. ROE improved from -1.9% in FY23 to 2.4% in FY24, while ROCE declined slightly from 7.2% to 6.0%, reflecting the capital intensity of rapid expansion.

XII. The Moats & Competitive Positioning

Entero's competitive moats emerge from the intersection of physical and digital capabilities that prove difficult to replicate. Network density creates the first moat—with the largest hospital customer network among pharmaceutical products distributors in India and presence across 540 districts, competitors face enormous capital requirements to match this footprint.

Quality certifications and regulatory licenses form regulatory moats. Each state requires specific licenses for pharmaceutical distribution. Temperature-controlled storage facilities need specialized certifications. Institutional customers demand quality accreditations. These requirements create time and capital barriers for new entrants while giving established players like Entero significant advantages.

Physician relationships and referral stickiness create subtle but powerful moats. Doctors prescribe medicines they trust will be available at pharmacies. Hospitals prefer distributors who maintain consistent supply. These relationships, built over years and strengthened through reliable service, resist disruption from new entrants offering marginally better terms.

The patient data and longitudinal records moat grows stronger with time. Understanding prescription patterns, treatment adherence, and health outcomes across millions of patients provides insights that improve inventory planning, enable personalized interventions, and inform expansion decisions. This data advantage compounds as the platform scales.

Brand trust in healthcare transcends typical consumer branding. When Entero ensures authentic medicines reach a remote pharmacy or maintains cold chain integrity for life-saving biologics, it builds trust that marketing cannot buy. The company's ethical principles focus on the greater good for all stakeholders, with employees understanding the responsibility of serving the healthcare ecosystem in an ethical, compliant and transparent way.

The technology platform's integration complexity creates a moat through switching costs. Pharmacies using Entero Direct (which had over 7,700 active users as of September 2023 with sales aggregating to ₹2,571.88 million) benefit from AI-based analytics for inventory management, customized promotional offers, and integrated ordering systems. Switching to another distributor means losing these technology benefits and retraining staff.

Payer relationships with insurance companies and corporate clients create contractual moats. Multi-year agreements with TPAs, exclusive supply contracts with hospital chains, and corporate wellness partnerships provide revenue visibility while creating barriers for competitors. These relationships often involve significant customization and systems integration that increase switching costs.

What's defensible versus what's not requires honest assessment. Pure distribution—moving boxes from point A to point B—remains commoditized. Technology platforms can be replicated given sufficient investment. Even geographic presence can be built through aggressive acquisition. The true defensibility lies in combining these elements into an integrated platform where the whole exceeds the sum of parts.

XIII. Major Challenges & Risks

The regulatory landscape for healthcare in India continues evolving in ways that could significantly impact Entero's business model. Price controls on essential medicines, a perpetual concern, could compress margins across the distribution chain. Changes in GST rates affect working capital requirements. State-level regulations on pharmaceutical distribution create operational complexity that increases with geographic expansion.

Pricing pressure intensifies from multiple directions. Insurance companies and TPAs negotiate aggressively for lower reimbursement rates. Government schemes mandate specific pricing for beneficiaries. Competitive intensity in urban markets forces price competition. Online pharmacies, despite their unit economics challenges, set price expectations that pressure traditional distribution margins.

Talent retention poses unique challenges in healthcare distribution. Skilled pharmacists have multiple employment options. Experienced supply chain professionals are courted by e-commerce giants. Technology talent faces infinite opportunities in India's booming tech sector. The company must balance compensation costs with margin objectives while maintaining service quality.

Technology debt accumulates as systems scale. Legacy systems from acquired companies must be integrated or replaced. Cybersecurity risks escalate with digitization—patient data breaches could prove catastrophic for reputation and trigger regulatory penalties. The rapid pace of technology change means continuous investment just to maintain competitiveness.

Geographic concentration risks persist despite pan-India presence. With over 86,300 retail pharmacies served as of FY24 (up from 81,400+ in FY23), the loss of key markets due to regulatory changes or competitive dynamics could materially impact revenues. Natural disasters, as India frequently experiences, can disrupt operations in entire regions.

Market fragmentation, ironically, poses risks to consolidation itself. While fragmentation creates opportunity, it also means thousands of small players who compete on relationships rather than efficiency. These incumbents often enjoy local political support and can mobilize resistance to organized players perceived as threats to traditional business models.

New competition from unexpected quarters threatens disruption. Amazon and Reliance have entered healthcare with ambitious plans. Ascent Health & Wellness Solutions, part of the Reliance Industries group, is frequently named alongside Keimed and Entero as one of the top three national distributors poised to benefit from market consolidation. Global giants like AmerisourceBergen explore Indian opportunities. Each brings different capabilities that could reshape competitive dynamics.

Execution complexity multiplies with scale. The company targeted ₹1,000 crore in revenue from inorganic growth during FY25, announcing Rs. 830 crores worth of acquisitions, of which Rs. 315 crores had been closed and Rs. 433 crores would close in Q2FY25, with blended EBITDA margins in the 6-8% range. Managing multiple acquisitions simultaneously while maintaining operational efficiency tests organizational capacity.

Capital requirements for continued growth remain substantial. Despite the successful IPO, working capital needs continue growing with revenue. Future acquisitions require funding. Technology investments demand continuous capital deployment. The balance between growth and profitability becomes increasingly delicate as investor expectations evolve.

XIV. Playbook: Business & Investing Lessons

The power of starting narrow and going deep emerges as Entero's first lesson. Rather than attempting nationwide coverage immediately, the company built density in specific regions through acquisitions, achieved local market leadership, then expanded outward. This approach generated cash flows to fund further expansion while building operational expertise.

The vertical integration versus partnership decision framework proves instructive. Entero chose to own distribution infrastructure while partnering for manufacturing (private label products) and last-mile delivery in some markets. This selective integration captured value chain margins without the capital intensity of full vertical integration.

Quality as competitive advantage in trust-based industries cannot be overemphasized. In healthcare, where product authenticity and safety are paramount, Entero's investments in quality systems, certifications, and compliance created differentiation that price competition couldn't erode. Trust, once earned, generates customer stickiness that transcends economic considerations.

Technology as enabler, not solution, reflects mature thinking about digital transformation. While the company invested significantly in technology, achieving its targeted 5%+ EBITDA margin requires successful M&A integration, strategic shifts toward higher-margin products and services, continued cost efficiencies from technology, and potentially gaining greater pricing power as the market consolidates.

Network effects in healthcare manifest differently than in consumer internet businesses. Density enables better service levels which attract more customers which justify further infrastructure investment. Data from a broader network improves inventory planning and demand prediction. Relationships compound as satisfied customers provide referrals and testimonials.

The timing of PE capital proved crucial for Entero's trajectory. OrbiMed's early investment provided not just capital but credibility that attracted acquisition targets, customers, and talent. The investor's healthcare expertise guided strategic decisions and opened doors that pure financial investors couldn't.

Crisis as opportunity materialized during COVID-19. While the pandemic created operational challenges, it also accelerated digital adoption, normalized home healthcare, and demonstrated the value of organized distribution. Companies that invested during the crisis rather than retrenching emerged stronger.

The B2B2C model's power becomes evident through Entero's corporate partnerships. Serving institutions provides customer acquisition efficiency, revenue predictability, and data insights that pure B2B or B2C models lack. The institutional endorsement also builds credibility with end consumers.

Platform thinking transcends traditional distribution. By viewing itself as a healthcare platform rather than a logistics company, Entero could justify investments in technology, data analytics, and value-added services that pure distributors wouldn't make. This platform mindset attracted different talent, investors, and acquisition targets.

India-specific lessons about building in fragmented, price-sensitive markets prove valuable beyond healthcare. Success requires balancing standardization with local customization, leveraging technology while maintaining human relationships, and achieving scale while preserving agility. The ability to operate across India's diverse regulatory, linguistic, and cultural landscape creates capabilities valuable in any emerging market.

XV. Analysis & Bear vs. Bull Case

Bull Case:

The India healthcare market's structural growth drivers remain compelling. With the market growing at a CAGR of 22% from $372 billion in 2022 to a projected $612 billion by 2025, even maintaining market share ensures substantial growth. Demographics, with an aging population and rising chronic disease burden, create sustained demand for healthcare products and services.

Entero's position as one of only three scaled integrated players in diagnostics-to-care provides competitive advantages in an industry trending toward consolidation. The company's proven acquisition and integration capabilities, having successfully absorbed 45 companies, demonstrate execution expertise that's difficult to replicate.

Network effects and data moats continue strengthening. Every additional pharmacy, hospital, and manufacturer relationship increases platform value for all participants. The longitudinal health data accumulated across millions of transactions enables personalization and prediction capabilities that improve with scale.

Technology differentiation should widen as AI and automation mature. Entero's investments in digital infrastructure position it to capture efficiency gains that laggard competitors cannot match. The combination of physical infrastructure and digital capabilities creates an omnichannel advantage in a market where pure-play digital models struggle with unit economics.

The path to strong free cash flow and ROCE appears achievable as the platform scales. Management reaffirmed guidance of achieving 35-40% revenue growth for FY25 with EBITDA margin expansion driven by procurement efficiencies, business mix, and operating leverage. As acquisitions mature and integration costs decline, margins should expand toward the 5%+ target.

The consolidation opportunity remains massive with 65,000 fragmented distributors in India. Entero's proven roll-up capability, access to capital, and platform advantages position it to capture disproportionate value from ongoing industry consolidation.

Bear Case:

Execution complexity threatens to overwhelm management capacity. Running multiple acquisitions simultaneously while maintaining operational excellence and technology innovation requires exceptional execution. Any stumble could cascade through the interconnected platform.

Margin pressure could intensify rather than abate. The race to bottom in commoditized distribution services shows no signs of ending. Government price controls, insurance reimbursement pressures, and competitive dynamics could prevent margin expansion despite scale benefits.

Competition from deep-pocketed entrants poses existential threats. If Reliance or Amazon decide to seriously pursue healthcare distribution, their capital resources and ecosystem advantages could rapidly erode Entero's market position. Global players entering India bring operational expertise and technology capabilities that could leapfrog local players.

Regulatory risks loom large in Indian healthcare. A single regulatory change—price controls, licensing requirements, or distribution restrictions—could fundamentally alter business economics. The complex web of state and central regulations creates continuous compliance risks.

Technology disruption could disintermediate traditional distribution. Direct-to-consumer pharmaceutical sales, drone delivery, or blockchain-based supply chains could bypass traditional distributors entirely. Entero's physical infrastructure could become stranded assets in a digitally transformed healthcare system.

Capital intensity might prove structural rather than temporary. The negative operating cash flow persisting despite scale raises questions about whether the business model can generate acceptable returns on invested capital. Continuous acquisition needs and working capital requirements could create a permanent capital deficit.

Profitability at scale remains unproven. Despite impressive revenue growth, EBITDA margins at 3.7% in Q3FY25 remain below the 5%+ target. Whether margins can expand sufficiently to justify valuations remains an open question.

XVI. Recent Developments & Future Outlook (2024–2025)

The latest financial results validate the growth strategy while highlighting ongoing challenges. Q3 FY2024-2025 revenue jumped 37.42% year-over-year to ₹1,366.49 Cr with 4.16% sequential growth, net profit jumped 275.22% to ₹25.44 Cr with 7.71% sequential improvement. These numbers demonstrate both the power of the platform and the operating leverage beginning to manifest.

Strategic initiatives underway reflect evolved thinking about growth drivers. The most recent deal was a Merger/Acquisition with Ace Cardiopathy Solutions completed on September 29, 2025, indicating continued focus on specialized medical device distribution. The company's expansion into high-margin specialty segments like cardiology and oncology represents a strategic shift from volume to value.

The M&A pipeline remains robust. Recent board approvals included acquisitions of five companies: Sai RK Pharma, Well Wisher Pharma, Ramson Medical Distributors, Khera Medisolutions, and AV Medisolutions, with an MoU signed to acquire 80% stake in Anand Medical Distributors (pending due diligence). The pace of acquisitions, while still aggressive, shows signs of becoming more selective and strategic.

Geographic expansion plans focus on deepening presence rather than just widening reach. The emphasis has shifted from entering new districts to building density within existing markets, improving service levels, and capturing greater wallet share from existing customers.

New service lines under development include specialty pharmacy services for complex therapies, medical device financing for hospitals, and inventory management solutions for pharmaceutical manufacturers. Each leverages existing capabilities while opening new revenue streams.

The technology roadmap emphasizes artificial intelligence and predictive analytics. Investments in demand forecasting, route optimization, and automated customer service aim to improve efficiency while enhancing customer experience. The goal is technology that disappears into the background while dramatically improving outcomes.

Management affirmed a 30% revenue growth target for the full financial year, citing a strong base from FY25 and expectations for higher growth in subsequent quarters. This confidence, despite a challenging macro environment, reflects visibility into acquisition integration and organic growth drivers.

Market valuation and investor sentiment remain constructive despite volatility. The IPO saw strong anchor investor participation including global investors like Smallcap World Fund Inc, Government of Singapore, Monetary Authority of Singapore, Carmignac Portfolio, CLSA Global, Societe Generale, Morgan Stanley, Goldman Sachs, along with domestic institutions like SBI General Insurance and Bajaj Allianz Life Insurance.

XVII. Epilogue & "If We Were CEOs"

Standing at the helm of Entero Healthcare Solutions today would mean confronting a fundamental strategic question: Is the future about going deeper into existing markets or wider into new geographies and segments? The temptation to pursue both simultaneously must be balanced against execution capacity and capital constraints.

The AI and genomics opportunity deserves serious consideration. As precision medicine advances, distributors who can handle specialized therapies, maintain complex cold chains, and provide patient support services will capture disproportionate value. Building these capabilities organically would take years; acquiring them might accelerate positioning but at premium valuations.

International expansion presents intriguing possibilities. Other emerging markets face similar healthcare distribution challenges. Entero's playbook—technology-enabled consolidation of fragmented distribution—could work in Southeast Asia, Africa, or Latin America. Yet international expansion would strain management bandwidth and introduce currency and regulatory risks.

Going deeper into existing markets might generate superior returns. With pharmacy reach targeted to expand from 86,300 to 150,000-200,000 over the next three years, significant domestic opportunity remains. Deepening relationships with existing customers, expanding service offerings, and building density could generate profitable growth without the risks of new market entry.

The strategic choices facing Entero reflect broader questions about platform businesses in emerging markets. How to balance growth with profitability? When to expand horizontally versus vertically? How to maintain entrepreneurial agility while achieving institutional scale?

What surprises most about Entero's story is the speed of transformation. In just six years, a startup became one of India's largest healthcare distributors. This velocity of change, enabled by capital availability and execution excellence, challenges traditional assumptions about how long building distribution infrastructure takes.

For founders building in healthcare, Entero demonstrates that seemingly unglamorous businesses like distribution can create enormous value when technology and operations excellence combine. The key is identifying structural inefficiencies in large markets and building platforms that solve multiple stakeholder problems simultaneously.

For investors evaluating platform businesses in India, Entero illustrates both opportunities and challenges. The opportunity lies in consolidating fragmented industries serving essential needs. The challenge lies in execution complexity, capital intensity, and the patience required for margins to expand as platforms mature.

XVIII. Outro & Further Reading

The Entero Healthcare story continues to unfold, each chapter adding complexity to an already intricate narrative. From two entrepreneurs in a Faridabad office to a platform serving millions of Indians' healthcare needs, the journey illustrates how vision, capital, and execution can transform industries.

The broader implications extend beyond healthcare distribution. As India modernizes, similar consolidation opportunities exist across logistics, agriculture, education, and financial services. The playbook—identify fragmentation, build technology platforms, consolidate through M&A, and create network effects—remains relevant across sectors.

For students of business strategy, Entero provides rich material for analysis. The company's navigation of the classic platform challenges—chicken-and-egg problems, network effects, competitive dynamics—offers practical lessons in building two-sided markets in emerging economies.

Healthcare professionals watching Entero's evolution see both promise and peril. Promise in improved drug availability, authentic products, and better service levels. Peril in the potential for platform monopolies that could extract rents from the healthcare value chain.

The investment community continues debating Entero's ultimate trajectory. Will it become India's healthcare backbone, essential and profitable? Or will execution complexity and competitive pressures prevent achieving acceptable returns? Time will provide answers, but the journey itself offers valuable lessons.

As India's healthcare sector continues its dramatic transformation, distribution players like Entero will play crucial but often invisible roles. Every medicine reaching a rural pharmacy, every diagnostic sample maintaining cold chain integrity, every hospital receiving just-in-time supplies—these operational victories accumulate into healthcare outcomes for millions.

The Entero story reminds us that in emerging markets, building basic infrastructure—whether physical or digital—creates enormous value. While Silicon Valley celebrates consumer apps and artificial intelligence, companies like Entero do the unglamorous work of ensuring medicines reach those who need them. This work, though less celebrated, might ultimately prove more valuable.

For those seeking deeper understanding, the recommended resources provide multiple perspectives on healthcare distribution, platform businesses, and emerging market dynamics. From Clayton Christensen's framework for healthcare disruption to detailed analyses of India's healthcare evolution, these materials offer context for understanding Entero's journey and anticipating its future.

The story continues, shaped by management decisions, competitive dynamics, regulatory changes, and most importantly, the healthcare needs of 1.4 billion Indians. Whatever the outcome, Entero's attempt to organize India's healthcare distribution deserves attention as a case study in ambition, execution, and the complexities of building platforms in emerging markets.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube