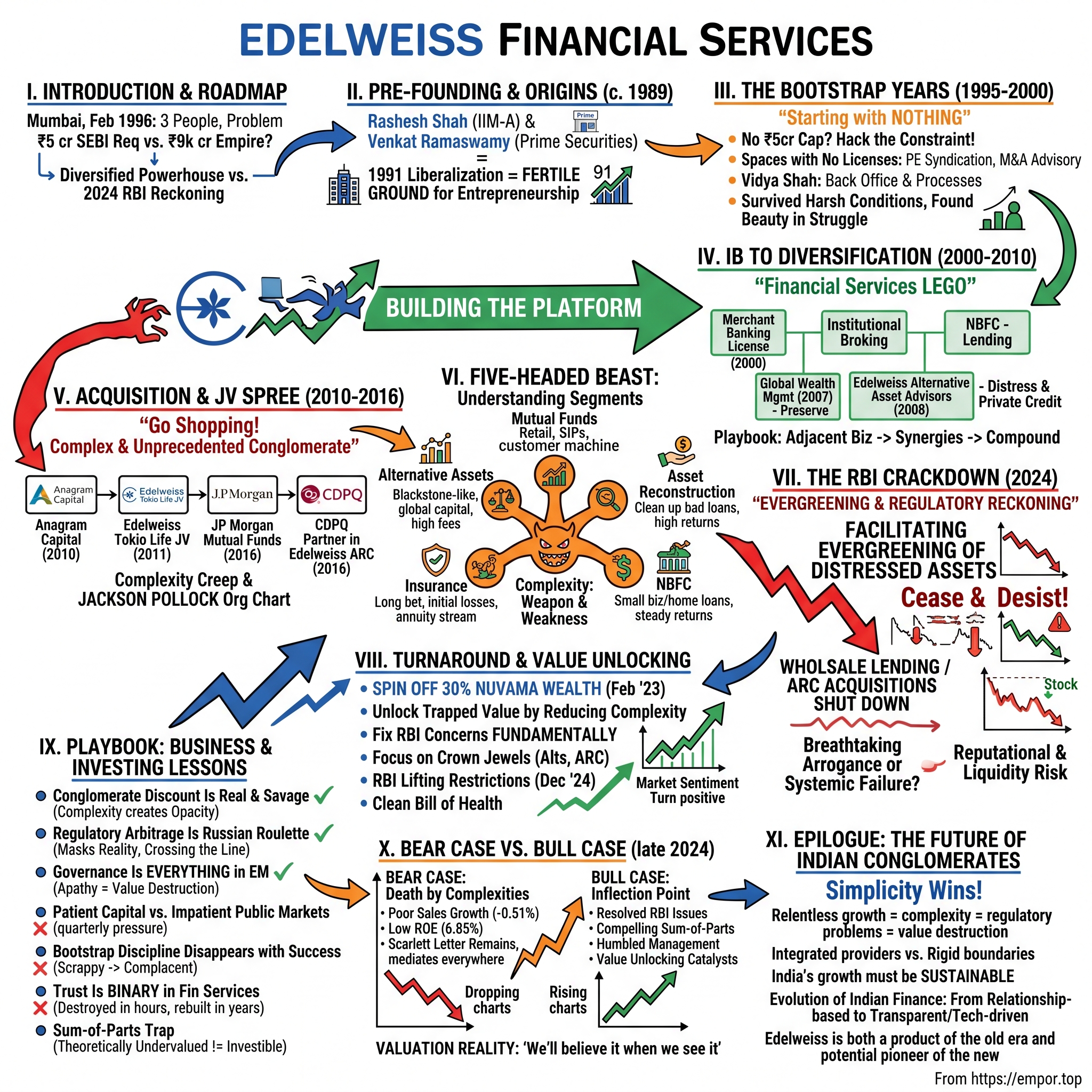

Edelweiss Financial Services: From Investment Banking Boutique to Conglomerate Controversy

I. Introduction & Episode Roadmap

Picture this: It's February 1996, and in a cramped office in Mumbai's Fountain area, three people are staring at a problem. They'd quit their jobs to start an investment bank, but they don't have the ₹5 crore required by SEBI to actually be an investment bank. Most founders would pack it in. These three would build a ₹9,000 crore empire instead.

Today, Edelweiss Financial Services stands as one of India's most complex financial conglomerates—a five-headed beast spanning everything from alternative assets to insurance, from mutual funds to distressed debt. With a market cap hovering around $1.1 billion, it's simultaneously one of India's most ambitious financial services plays and one of its most controversial.

The paradox at the heart of this story: How did Rashesh Shah and Venkat Ramaswamy transform their bootstrap operation into a diversified financial powerhouse, only to find themselves in the crosshairs of India's banking regulator nearly three decades later? And more importantly—what does their journey tell us about building financial services businesses in emerging markets?

This is a story of regulatory arbitrage and redemption, of complexity as both weapon and weakness, of how the very strategies that fuel growth can become the seeds of near-destruction. It's about navigating the tension between innovation and compliance in one of the world's most dynamic yet tightly regulated financial markets.

We'll trace Edelweiss from its origins in the heady days of India's 1991 liberalization, through its methodical platform-building phase, into its aggressive acquisition spree, and finally to its 2024 regulatory reckoning with the Reserve Bank of India. Along the way, we'll unpack how a company can be simultaneously undervalued and overextended, why conglomerates trade at discounts even when their parts are valuable, and what happens when financial engineering meets regulatory reality.

II. Pre-founding & Origins Story

The year is 1989, and at IIM Ahmedabad—India's equivalent of Harvard Business School—a Gujarati student named Rashesh Shah is having an existential crisis. Born into a traditional business family where everyone traded commodities and textiles, Shah had deliberately chosen the MBA path to avoid following his father and uncles into the family business. The irony wasn't lost on him: here he was at India's premier business school, trying to escape business.

Shah's background was a study in contradictions. He was the first in his family to attend an English-medium school—Bharatiya Vidya Bhavan and Manav Mandir High School in Mumbai. While his cousins were learning the ropes of traditional trading, he was studying statistics at KC College and spending a year at the Indian Institute of Foreign Trade in Delhi, diving deep into the mechanics of exports. The family saw education as nice-to-have; Shah saw it as his ticket to something different.

At IIM-A, Shah found his tribe—including Vidya, who would become his wife and later play a pivotal role in Edelweiss's early survival. But more importantly, he found his moment. India was transforming before his eyes. In 1991, facing a balance-of-payments crisis, Finance Minister Manmohan Singh (later Prime Minister) had unleashed sweeping economic reforms. License Raj was crumbling. Foreign investment was flowing in. Capital markets were awakening from decades of socialist slumber.

"The 1991-96 period was extraordinarily fertile for entrepreneurship," Shah would later reflect. "You could feel the energy—India opening up, global capital interested, domestic businesses hungry for advisory." After graduation, he joined Prime Securities, one of the early investment banks riding this wave. There he met Venkat Ramaswamy, a kindred spirit who shared his vision of what Indian finance could become.

By 1995, both men had seen enough. Prime Securities had shown them what was possible, but they wanted to build something of their own. The timing seemed perfect—India's capital markets were booming, companies needed sophisticated financial advice, and the regulatory environment was still forming. They quit their jobs, pooled their savings, and in November 1995, incorporated Edelweiss Financial Services.

The name itself was telling. Edelweiss—the mountain flower that grows in harsh Alpine conditions, symbol of rugged beauty and rare achievement. Perhaps they sensed what was coming: that building a financial services firm in India would require surviving in harsh conditions, finding beauty in struggle, achieving the rare. Or perhaps they just liked how it sounded—European, sophisticated, different from the alphabet soup of Indian financial firms.

What they didn't know was that within months, they'd face their first existential crisis—one that would force them to completely reimagine their business before it had even properly begun.

III. The Bootstrap Years: Starting with Nothing (1995–2000)

February 1996 should have been a celebration. After three months of preparation, Edelweiss was ready to launch operations. The office in Fountain—Mumbai's old business district—was modest but respectable. The three-person team (Shah, Ramaswamy, and one analyst) was lean but capable. The business plan was clear: investment banking and advisory for India's emerging corporate sector.

Then came the gut punch. SEBI's capital requirement for a Category-1 merchant bank: ₹5 crore. Shah and Ramaswamy had scraped together everything they had, convinced friends and family to invest, and they were still short. Way short. The kind of short that usually ends entrepreneurial dreams.

This is where most founder stories would pivot to the magical angel investor or the venture capitalist who believed. But this was India in 1996. There were no VCs. Angel investors were actual angels—mythical creatures nobody had seen. Banks wouldn't lend to startups. The capital simply didn't exist.

So Shah and Ramaswamy did something that would define Edelweiss's DNA for decades: they hacked around the constraint. Can't be a merchant bank? Fine. They'd operate in the spaces that didn't require licenses. Private equity syndication—connecting Indian companies with foreign investors—needed relationships, not regulatory approval. M&A advisory required expertise, not capital adequacy. Structured finance solutions demanded creativity, not compliance certificates.

The numbers from this period are almost comically small by today's standards. First year revenue: ₹20 lakh (about $27,000 at current exchange rates). The entire operation could have fit in a Mumbai local train compartment. But something crucial was happening—they were learning how to survive without capital in a capital-intensive business.

Vidya Shah, Rashesh's wife and IIM-A batchmate, played a role that's often understated in official histories. While Rashesh and Venkat pitched deals, she built the back office—operations, compliance, accounting. "We couldn't afford to hire professionals," she'd later say. "So we became professionals at everything." She standardized processes that would scale, created documentation systems that would later impress regulators, built a culture of precision that would matter when the stakes got higher.

The client wins were small but symbolic. A cross-border acquisition advisory here, a private placement there. Each deal taught them something: how to navigate India's byzantine regulations, how to bridge the gap between global capital and Indian opportunity, how to build trust without a brand. They were earning degrees from the university of survival.

By 1998, something shifted. The Asian Financial Crisis had scared away fair-weather players, but Edelweiss kept growing. They'd figured out a crucial insight: in a market where everyone was chasing the same large deals, there was value in complexity. Structured products that others wouldn't touch. Small cross-border transactions that big banks ignored. Financial engineering that required more creativity than capital.

The team grew to ten people. Revenue crossed ₹1 crore. Still tiny, but the trajectory was clear. More importantly, they'd accumulated something money couldn't buy: five years of relationships, reputation, and most crucially, the ₹5 crore they'd originally needed.

In 2000, Edelweiss finally became what it had always claimed to be—a Category-1 merchant bank, fully licensed and regulated. The bootstrap phase was over. But the lessons learned—frugality as strategy, complexity as moat, regulation as both constraint and opportunity—would shape everything that came next.

IV. Building the Platform: Investment Banking to Diversification (2000–2010)

The morning Edelweiss received its merchant banking license in 2000 should have been pure celebration. Instead, Rashesh Shah was in his office, staring at a whiteboard covered with arrows and boxes. The question wasn't whether they'd made it—it was what to build next.

"Getting the license was like getting admitted to the game," Shah would later tell colleagues. "But we were still playing with a tennis ball while others had cricket equipment." The Indian financial services landscape of 2000 was dominated by two forces: the old public sector banks with their massive balance sheets and government backing, and the foreign banks—Merrill Lynch, Morgan Stanley, Goldman Sachs—with their global expertise and deep pockets. Edelweiss was neither.

The strategic choice they made would define the next decade: instead of competing head-on in investment banking, they would build adjacencies. Think of it as financial services Lego—each piece individually small, but collectively forming something substantial and unique.

The first addition came almost immediately. Institutional broking—providing research and trading services to mutual funds, insurance companies, and foreign institutional investors. This wasn't random. Shah had noticed that foreign investors flooding into India post-liberalization needed local intelligence. Not just data, but interpretation. What did it mean when a Karnataka politician made a statement about infrastructure? How would monsoon patterns affect consumer companies? Edelweiss hired analysts who could bridge this gap—people who understood both Excel and elections, both P&L statements and panchayat politics.

By 2003, the institutional broking desk was generating more revenue than the original investment banking business. But this created a new problem: clients wanted to trade, but Edelweiss needed capital to facilitate trades. Enter the next Lego block: becoming a Non-Banking Financial Company (NBFC). This allowed them to lend, to provide margin funding, to warehouse securities. It was also their first dance with serious regulation—RBI oversight, capital adequacy norms, asset-liability management. The compliance costs alone would have killed the 1996 version of Edelweiss.

The 2003-2007 period was India's first real bull market, and Edelweiss surfed it brilliantly. But while everyone else was drunk on growth, Shah and Ramaswamy were thinking about sustainability. They'd seen enough cycles to know this wouldn't last. The question was: what would clients need when the music stopped?

The answer came in 2007 with the launch of Edelweiss Global Wealth Management. The timing seems prescient in hindsight—launching a wealth management business just before the global financial crisis. But it wasn't luck. They'd noticed that India's entrepreneurs, who'd created massive wealth during the bull run, had no idea how to preserve it. These weren't inherited-wealth families with generations of experience. These were first-generation creators who'd built software companies, pharmaceutical firms, manufacturing businesses. They needed what Edelweiss had learned to do during its bootstrap years: structure complexity, navigate regulation, optimize without breaking rules.

The wealth management pitch was sophisticated: asset protection strategies using trusts, tax optimization through legal structures, succession planning using holding companies. This wasn't about picking stocks—it was about architectural finance, building frameworks that could weather storms.

Then came 2008, and two things happened that would prove crucial. First, the global financial crisis hit, validating every conservative decision Edelweiss had made. While overleveraged players collapsed, Edelweiss survived with minimal damage. Their clients in wealth management, protected by the structures they'd built, became evangelists.

Second, they launched EdelGive Foundation, focusing on education and livelihoods. This might seem like corporate tokenism, but it served a strategic purpose. In India, financial services is as much about social license as regulatory license. The foundation gave Edelweiss something money couldn't buy: moral authority in a business often seen as morally ambiguous.

The masterstroke came in mid-2008 with Edelweiss Alternative Asset Advisors (EAAA). While the world was deleveraging, they saw opportunity in alternatives—private credit for companies banks wouldn't touch, real estate debt for projects stuck mid-construction, infrastructure yield strategies for pension funds seeking stable returns. This wasn't contrarian investing; it was recognizing that in a crisis, the conventional pipes of finance freeze, but the need for capital remains.

By 2010, Edelweiss had transformed from a one-trick investment banking pony into a diversified platform. Investment banking, institutional broking, wealth management, NBFC lending, alternative assets—each business supporting and feeding the others. Revenue had grown from ₹20 lakh in 1996 to over ₹1,000 crore. The employee count had exploded from 3 to over 2,000.

But the real transformation was in capability. They'd built the infrastructure—technology systems, risk management frameworks, compliance processes—to operate at scale. They'd assembled talent that could compete with anyone. Most importantly, they'd developed a playbook: enter adjacent businesses, build organically, create synergies, compound.

The platform was built. Now it was time to go shopping.

V. The Acquisition & JV Spree (2010–2016)

October 2010, Edelweiss headquarters, and the M&A team that had spent a decade advising others on acquisitions was about to pull the trigger on its first major deal. Anagram Capital—₹164 crore. For a company that had started with barely ₹20 lakh, this was like a teenager buying their first car with cash.

But Anagram wasn't just any acquisition. It was a statement of intent. Founded by former Enam Securities executives, Anagram brought institutional credibility and a book of blue-chip clients. More importantly, it brought a culture of research excellence that would mesh perfectly with Edelweiss's analytical DNA. This wasn't financial engineering—it was cultural engineering.

The integration went so smoothly that Shah and Ramaswamy immediately started hunting for more. But their next move would surprise everyone. In 2011, instead of another acquisition, they announced a joint venture with Tokio Marine, one of Japan's oldest insurers. Edelweiss Tokio Life Insurance—74% Edelweiss, 26% Tokio Marine.

Insurance? The business that requires massive capital, operates on 20-year time horizons, and bleeds money for the first decade? It seemed antithetical to everything Edelweiss had built—asset-light, fee-based, quick returns. But Shah saw something others missed. Insurance wasn't just about underwriting risk; it was about distribution, data, and trust. Every insurance policy sold created a customer relationship that could be leveraged across the platform. Every claim settled built trust that money couldn't buy.

The 2014 acquisition of Forefront Capital Management was different—almost surgical in its precision. Forefront was tiny but had something Edelweiss needed: expertise in quantitative strategies and systematic trading. As markets became more algorithmic, Edelweiss was essentially acquiring the future, packaged in a small Mumbai firm most people had never heard of.

Then came 2016, the year of the double play that would reshape Edelweiss's trajectory. First, the acquisition of JP Morgan's mutual fund schemes in India. This wasn't just buying assets under management; it was buying legitimacy. JP Morgan's exit from Indian mutual funds was Edelweiss's entry into the big leagues. Overnight, they went from nobody to somebody in asset management.

The second move was more complex: bringing in Caisse de dépôt et placement du Québec (CDPQ), one of North America's largest pension funds, as a 20% partner in Edelweiss Asset Reconstruction Company (EARC). This needs context. Asset reconstruction in India—buying and resolving bad loans—was seen as a dirty business, the financial equivalent of waste management. But it was also incredibly lucrative if done right. CDPQ's investment wasn't just capital; it was validation from one of the world's most sophisticated institutional investors.

September 2016 brought the final piece: Ambit Alpha Fund, a long-short hedge fund that most retail investors had never heard of but every institutional investor respected. Ambit's quantitative strategies were the opposite of Edelweiss's relationship-driven approach, and that was exactly the point. Edelweiss was building a platform that could serve every client need, from vanilla to exotic, from rural to sophisticated.

By the end of 2016, Edelweiss had transformed through acquisition and partnership. The company that had organically built its first billion in revenue had inorganically built its second. But something else had happened—complexity had crept in like fog. The organizational chart looked like a Jackson Pollock painting. The regulatory requirements spanned multiple agencies—RBI, SEBI, IRDAI, NHB. The synergies that looked obvious on PowerPoint were proving elusive in practice.

Each acquisition had made strategic sense in isolation. Together, they'd created something unprecedented in Indian financial services—a true conglomerate spanning every aspect of finance. But as any student of history knows, conglomerates are either empires or houses of cards. The next few years would determine which one Edelweiss had built.

VI. The Five-Headed Beast: Understanding the Business Segments

To understand what Edelweiss had become by 2016, imagine walking into a financial department store where every floor offers a completely different service, each with its own economics, regulations, and customers. The elevator buttons read like a financial services textbook: Agency, Capital, Insurance, Asset Reconstruction, Treasury. Five heads, one body, infinite complexity.

Let's start with Alternative Assets (EAAA), the crown jewel that most retail investors completely misunderstand. This isn't your grandfather's mutual fund. EAAA raises capital for investments in everything from early-stage startups to distressed debt, from real estate projects to infrastructure yields. Think of it as India's answer to Blackstone or Brookfield—raising funds from global institutions and deploying them in opportunities that traditional finance won't touch.

The numbers tell the story: by 2016, EAAA was managing over $5 billion across multiple strategies. The fee structure was enviable—2% management fees plus 20% carry (profit share) on successful exits. This is the business that Silicon Valley venture capitalists dream about—scalable, asset-light, with operating leverage that would make a software company jealous. Every additional billion under management dropped almost directly to the bottom line.

The Mutual Funds business (EAMC) operated on entirely different physics. Where EAAA served institutions with $100 million checks, EAMC served retail investors with ₹5,000 SIPs (Systematic Investment Plans). The margins were thinner—maybe 50 basis points versus EAAA's 200—but the scale potential was massive. India had 1.3 billion people, but only 20 million mutual fund investors. The headroom for growth was essentially infinite.

But here's where it gets interesting: the mutual fund business was also a feeder for everything else. That retail investor who starts with a small SIP? Three years later, they might need a home loan (Housing Finance). Five years later, wealth management. Ten years later, their company might need investment banking. EAMC wasn't just a business—it was a customer acquisition engine disguised as an asset manager.

The Asset Reconstruction business (EARC) was Edelweiss's profitable dark horse. Created under RBI's mandate to clean up India's banking system, ARCs buy non-performing assets from banks at a discount and try to recover value. It's unglamorous work—chasing defaulted borrowers, restructuring failed projects, sometimes literally taking possession of half-built factories. But the economics were spectacular when done right.

Here's how it worked: Buy a ₹100 crore bad loan for ₹30 crore. Recover ₹50 crore through restructuring or sale. That's a 66% return, plus management fees along the way. EARC had perfected this alchemy, becoming India's largest ARC with over ₹40,000 crore in assets under management. The CDPQ partnership had given them not just capital but also global best practices in distressed investing.

The Insurance business was the long bet, the one that made quarterly-focused analysts tear their hair out. Both life and general insurance were bleeding money—₹200 crore in annual losses—but this was by design. Insurance in India follows a J-curve: massive losses in early years due to customer acquisition costs and regulatory provisioning, then exponential profitability as the book matures.

Edelweiss was essentially building an annuity stream for the 2030s. Every policy sold today would pay premiums for decades. The distribution synergies with other businesses made customer acquisition cheaper. The data from insurance customers informed credit decisions in the NBFC. It was patient capital at work, but patience isn't a virtue markets typically reward.

The NBFC and Housing Finance segments were the workhorses—unglamorous but essential. The NBFC provided working capital to SMEs, structured credit to corporations, margin funding to traders. Housing Finance partnered with banks to originate home loans, earning fees without taking balance sheet risk. Together, they generated steady returns, though nothing spectacular—8-10% ROE versus the 15-20% that investors expected.

Finally, Treasury acted as the circulatory system, managing liquidity across all businesses, optimizing capital allocation, ensuring that money flowed where it was needed. In a conglomerate this complex, treasury wasn't just about parking surplus funds—it was about orchestrating a financial symphony where every instrument played at different tempos.

The beauty of this five-headed structure was the optionality it created. When credit markets tightened, alternative assets thrived. When equity markets boomed, mutual funds and broking exploded. When banks pulled back, the NBFC stepped in. It was portfolio theory applied to business models—diversification reducing risk while maintaining return potential.

But this complexity came with a cost that wouldn't become apparent until 2024, when the Reserve Bank of India would look at these interconnected businesses and see not synergy but systemic risk.

VII. The RBI Crackdown: Evergreening & Regulatory Reckoning (2024)

May 29, 2024, started like any other day at Edelweiss's Mumbai headquarters. By noon, it had become the darkest day in the company's 29-year history. The Reserve Bank of India didn't just slap them on the wrist—it essentially paralyzed two of their most important businesses with immediate effect.

The language in the RBI's order was devastating in its precision. Some Indian ARCs were bypassing regulations and facilitating the evergreening of distressed assets, Deputy Governor Swaminathan J had warned just days earlier. Now Edelweiss was in the crosshairs. The group entities were acting in concert, entering into a series of structured transactions for evergreening stressed exposures of ECL, using the platform of EARCL and connected AIFs, thereby circumventing applicable regulations.

Let's decode what "evergreening" means and why it's the financial equivalent of a cardinal sin. Evergreening involves extending fresh loans to stressed borrowers to repay existing ones, a practice the RBI has warned against for masking financial realities. Imagine you owe me ₹100 and can't pay. Instead of declaring it a bad loan, I lend you another ₹100 through my cousin's company to pay me back. On paper, the loan looks healthy. In reality, it's zombie debt walking around pretending to be alive.

The specific violations read like a masterclass in how not to run a financial conglomerate. ECL had indulged in submission of incorrect details of its eligible book debts to its lenders for computation of drawing power, non-compliance with loan to value norms for lending against shares. They were essentially telling their lenders they had more collateral than they actually did—financial fiction at its finest.

But the most damning finding was the interconnectedness. ECL has been accused of not maintaining arm's length with other group companies. The NBFC would take over loans from other group entities, then sell them to the group's ARC. It was financial hot potato, with bad assets being passed around until nobody knew where they originated or how toxic they really were.

Some of the violations by Edelweiss ARC included not placing the RBI's supervisory letter issued after the previous inspection for 2021-22 before the board. Think about that—the regulator sends you a warning letter, and you don't even show it to your board of directors. It's either breathtaking arrogance or systemic governance failure.

The RBI's response was swift and severe. ECL Finance was asked to cease and desist from undertaking any structured transactions in respect of its wholesale exposures, other than repayment and/or closure of accounts. For a wholesale lending business, this is like telling a restaurant it can only serve water.

Edelweiss Asset Reconstruction Company was asked to cease and desist from acquisition of financial assets, including security receipts and reorganising the existing SRs into senior and subordinate tranches. An ARC that can't acquire distressed assets is like a hospital that can't admit patients.

The market reaction was brutal but predictable. Edelweiss was trading 11 per cent lower at Rs 68.56 within hours of the announcement. But the stock price was the least of their problems. Reputational risk leading to liquidity risk was going to be a major issue for the Edelweiss group. When the regulator states that the group was "evergreening stressed assets", it raises serious concerns for the group's lenders.

What made this particularly painful was the pattern of defiance. Even after the deficiencies were pointed out, instead of taking remedial action, the group entities were resorting to new ways to circumvent regulations. It wasn't just non-compliance; it was active resistance to regulatory oversight.

The Reserve Bank had been engaging with the senior management and their statutory auditors, but no meaningful corrective action had been evidenced, necessitating the imposition of business restrictions. The RBI had tried the carrot; now it was using the stick.

The timing couldn't have been worse. Indian financial markets were already nervous about regulatory tightening. IIFL Finance had been barred from gold loans. JM Financial faced restrictions. Paytm Payments Bank had been essentially shut down. Edelweiss wasn't just another name on this list—it was proof that even the biggest, most sophisticated players weren't immune.

For Rashesh Shah, who'd spent three decades building Edelweiss from nothing, this was more than a regulatory action. It was a repudiation of the very complexity that had been their competitive advantage. The interconnected businesses that created synergies had become channels for systemic risk. The financial engineering that generated returns had crossed into regulatory arbitrage.

But buried in the disaster was a glimmer of hope. The restrictions would be reviewed after the rectification of the supervisory observations by the group to the satisfaction of the Reserve Bank. This wasn't a death sentence—it was a chance at redemption. The question was whether Edelweiss could transform itself quickly enough to earn back the RBI's trust.

VIII. The Turnaround & Value Unlocking Strategy

Six months after the RBI's devastating regulatory action, something remarkable was happening at Edelweiss. While the media focused on the restrictions and the compliance failures, Shah and his team were quietly engineering one of the most significant value-unlocking exercises in Indian financial services history.

The masterstroke had actually begun a year before the RBI crisis. The Board of Edelweiss Financial Services Limited announced the spin off of 30% stake of Nuvama Wealth Management on February 24, 2023. This wasn't crisis management—it was strategic foresight. Shah had recognized that the conglomerate structure, while creating operational synergies, was destroying market value. Investors couldn't properly value a company that was simultaneously a wealth manager, an ARC, an insurer, and a lender.

Friday was also the record date for the purpose of determining the shareholders of Edelweiss Financial Services, who would be allotted equity shares by Nuvama Wealth Management pursuant to the scheme of arrangement. The mechanics were elegant: every Edelweiss shareholder would receive Nuvama shares proportionate to their holding. After listing, the shareholders of Edelweiss Financial Services would hold 30 per cent of the paid‐share capital of Nuvama Wealth Management.

The market's initial reaction was confused. Following the development, the stock (ex-spin off) traded at Rs 41.37 a piece on BSE, up 5 per cent over its adjusted price of Rs 39.40 for Thursday. The stock, on the other hand, was down 37.86 per cent over its unadjusted price of Rs 66.59 per share for Thursday. But this apparent decline was an optical illusion—value hadn't been destroyed, just redistributed across two entities.

The listing of Nuvama Wealth Management followed a significant restructuring process that began in 2020, when PAG, an Asia-focused alternative investment firm, acquired a stake in the wealth management business of Edelweiss Financial Services. PAG wasn't just any investor—they were one of Asia's most sophisticated alternative asset managers, and their involvement validated the wealth management business's standalone potential.

By September 2023, as Nuvama began trading independently, the value creation became apparent. Despite a decline on Wednesday, the stock has surged by 31 per cent in the past month. The wealth management business, freed from the conglomerate discount, was being valued on its own merits—high-growth, asset-light, with sticky customer relationships.

But the Nuvama spinoff was just the beginning of Shah's value-unlocking playbook. With the wealth management business separated, Edelweiss could now be valued more clearly as a focused financial services player. The market cap of 12,000 crores began to look increasingly disconnected from the sum of its parts.

The strategy going forward was surgical in its precision. First, satisfy the RBI's concerns completely—not just cosmetically, but fundamentally restructuring processes to ensure no repeat of the evergreening issues. Both entities implemented corrective measures, addressing issues related to structured transactions and distressed loan evergreening.

Second, simplify the business structure. The wholesale lending business that had caused so much trouble? Wind it down systematically. The complex inter-company transactions that had raised regulatory eyebrows? Eliminate them entirely. Each business would stand on its own, with clear boundaries and transparent operations.

Third, focus on the crown jewels. The Alternative Asset business, with its Blackstone-like economics, would be the growth engine. The Asset Reconstruction business, despite being mature, still generated substantial cash flows that could be redeployed. The insurance business, though still loss-making, represented optionality for the future.

The December 2024 vindication came faster than anyone expected. After significant engagement and corrective actions by the companies, the RBI is satisfied with their adherence to regulatory norms and has allowed their normal operations to resume. The lifting of restrictions wasn't just regulatory relief—it was a clean bill of health that removed the biggest overhang on the stock.

As a result, market sentiment turned positive, with Edelweiss Financial Services Ltd's share price rising by 7.76% to ₹138.80 on the Bombay Stock Exchange (BSE), signaling increased investor confidence. But this was still just the beginning. With a clean regulatory slate and simplified structure, Edelweiss was positioned for what Shah called "60% growth via value unlocking, debt reduction, and strong core business performance."

The turnaround strategy wasn't about grand gestures or dramatic pivots. It was about methodical execution: fix the problems, simplify the structure, unlock trapped value, and let each business perform to its potential. Sometimes the best strategy after a crisis isn't to rebuild—it's to reveal what was always there, hidden beneath layers of complexity.

IX. Playbook: Business & Investing Lessons

After spending years analyzing Edelweiss's journey from a three-person startup to a controversial conglomerate and back to redemption, several profound lessons emerge—not just about Indian finance, but about the nature of building complex businesses in emerging markets.

The Conglomerate Discount Is Real and Brutal

Edelweiss proved definitively that in financial services, 2+2 often equals 3 in market valuation terms. Despite each business unit potentially being valuable independently, the market applied a savage discount to the combined entity. Why? Complexity creates opacity. When investors can't clearly understand how you make money, they assume the worst. The Nuvama spinoff unlocked immediate value not by creating anything new, but simply by reducing complexity. The lesson: in public markets, clarity trumps synergy.

Regulatory Arbitrage Is Russian Roulette

The interconnected transactions between ECL Finance and Edelweiss ARC might have seemed clever—using internal synergies to optimize returns. But this is precisely what regulators fear most: systemic risk hiding in complexity. The RBI's crackdown wasn't just about rule violations; it was about pattern recognition. When you build a business model that depends on regulatory blind spots, you're not building a moat—you're digging a grave. Every regulatory arbitrage eventually gets arbitraged away by the regulator.

In Emerging Markets, Governance Is Everything

The most damning finding in the RBI's investigation wasn't the evergreening—it was that Edelweiss ARC didn't even present the regulator's warning letter to its board. This speaks to a deeper truth about emerging market investing: when institutional frameworks are still developing, corporate governance becomes the primary determinant of long-term value. A company can survive bad strategy, tough competition, even temporary losses. It cannot survive a governance failure in a market where trust is already scarce.

Complexity Can Be Both Weapon and Weakness

Edelweiss's early success came from tackling complex transactions others wouldn't touch—structured products, cross-border deals, regulatory navigation. This complexity was their competitive advantage when they were small. But as they scaled, the same complexity became their vulnerability. Complex organizations are harder to manage, harder to regulate, and harder to value. The lesson: complexity should be at the edge of your business, not at its core.

Patient Capital Requires Patient Markets

The insurance business bleeding ₹200 crore annually was strategically sound—insurance always follows a J-curve. But public markets aren't patient. Every quarterly loss was punished, even though the long-term logic was impeccable. This creates a fundamental tension: the best long-term strategies often require accepting short-term pain, but public markets price on quarterly performance. Edelweiss learned this the hard way—you can't build a 20-year business with 3-month shareholders.

The Cost of Aggressive Growth in Regulated Industries

Every acquisition Edelweiss made between 2010-2016 made strategic sense. Anagram brought clients. Tokio Marine brought credibility. JP Morgan's funds brought scale. But each acquisition also brought complexity, and in regulated industries, complexity multiplies compliance costs exponentially. The formula is brutal: as you grow linearly, regulatory scrutiny grows geometrically, and compliance costs grow exponentially.

Bootstrap Discipline Disappears with Success

The company that survived on ₹20 lakh in revenue in 1996 by being scrappy and creative had, by 2024, forgotten those lessons. Success bred complexity, which bred complacency, which bred regulatory violation. The very constraints that forced innovation in the early years—lack of capital, lack of licenses—had actually been protecting them from themselves. Once those constraints were removed, discipline disappeared.

Financial Engineering Has Limits

Edelweiss mastered the art of financial engineering—creating structures, optimizing capital, navigating regulations. But the RBI action proved that there's a line between optimization and manipulation, and that line is wherever the regulator decides to draw it. In finance, unlike technology, innovation that looks too clever eventually gets shut down. The sustainable innovations in finance are boring—better service, lower costs, wider access. Everything else is temporary arbitrage.

Trust Is Binary in Financial Services

When the RBI announced its restrictions, Edelweiss lost 11% of its value in hours. When restrictions were lifted, it gained 7.76% in a day. This binary nature of trust in financial services is unique—you either have it completely or you don't have it at all. One regulatory action can destroy decades of reputation building. This makes financial services fundamentally different from other businesses where trust can be partially maintained or gradually rebuilt.

The Sum-of-Parts Trap

Every analyst covering Edelweiss could prove it was undervalued by doing a sum-of-parts analysis. The ARC alone was worth X, the alternatives business worth Y, the insurance option value worth Z. Add them up and you got a number well above market cap. But markets aren't calculators—they're voting machines that hate what they don't understand. The lesson: being theoretically undervalued and being investible are entirely different things.

These lessons extend beyond Edelweiss to any company operating in emerging markets, especially in financial services. The path from startup to scale is littered with companies that grew too fast, became too complex, or pushed regulatory boundaries too far. Edelweiss survived because, ultimately, the underlying businesses were real and valuable. But survival and success are different things, and the cost of learning these lessons—in reputation, opportunity, and market value—was enormous.

X. Bear vs. Bull Case & Valuation Analysis

As we sit in late 2024, with Edelweiss trading around ₹140 and the RBI restrictions lifted, investors face a classic dilemma: is this a transformed company trading at a discount to its potential, or a permanently impaired conglomerate that will never escape its history?

The Bear Case: Death by a Thousand Complexities

Bears point to the brutal numbers first. The company has delivered a poor sales growth of -0.51% over past five years. While peers like Bajaj Finance and HDFC Bank were compounding at 15-20%, Edelweiss was shrinking. This isn't just underperformance—it's value destruction during one of India's greatest bull markets.

The return on equity tells an equally grim story. Company has a low return on equity of 6.85% over last 3 years, when any decent financial services business should be generating 15%+. This isn't just about one bad year—it's about a structurally unprofitable business model where complexity costs exceed synergy benefits.

The regulatory overhang may be officially lifted, but bears argue the scarlet letter remains. Which bank wants to lend to a company that was caught evergreening? Which institutional investor wants to explain why they own a stock that was publicly censured for regulatory violations? The reputational damage is like radiation—invisible but persistent, affecting every interaction, every negotiation, every transaction.

Competition is another bear argument. In every single segment, Edelweiss faces better-capitalized, more focused competitors. In alternatives, they're up against global giants like Blackstone and KKR entering India. In mutual funds, they're competing with HDFC and ICICI who have 10x the distribution. In insurance, they're a subscale player in a business that requires massive scale. Being mediocre at everything isn't a strategy—it's a recipe for permanent underperformance.

The conglomerate structure itself is perhaps the biggest bear argument. Even after the Nuvama spinoff, Edelweiss remains a complex holding company with multiple regulated entities, each with different capital requirements, regulatory overseers, and business cycles. The market has consistently shown it will not pay full value for such structures. Why should that change now?

Finally, bears point to management credibility. The same team that built the complexity, violated regulations, and destroyed shareholder value is still in charge. Yes, they've apologized and reformed, but can leopards really change their spots? The incentive structures that led to aggressive financial engineering haven't fundamentally changed.

The Bull Case: Misunderstood Value at an Inflection Point

Bulls see a completely different picture. They argue Edelweiss has successfully resolved RBI issues and is positioned for 60% growth via value unlocking, debt reduction, and strong core business performance. The regulatory clearance isn't just a relief—it's a rebirth.

The sum-of-parts valuation is compelling. The ARC business alone, with ₹40,000 crore in AUM and steady cash flows, could be worth ₹5,000-6,000 crore. The alternatives business, managing $5+ billion with private equity economics, could easily be worth another ₹4,000-5,000 crore. The mutual fund business, even at a discount to peers, is worth ₹2,000-3,000 crore. Add in the insurance optionality and housing finance book, and you get to ₹15,000+ crore in value against a market cap of ₹9,000 crore.

Bulls argue the cleanup is real and permanent. Management has learned its lesson, simplified the structure, and eliminated the interconnected transactions that caused problems. The businesses that remain are fundamentally good businesses temporarily masked by past mistakes. As the stench of regulatory action fades, fundamental value will reassert itself.

The macro tailwind is another bull argument. India's financial services penetration remains among the lowest in major economies. Credit to GDP, insurance penetration, mutual fund adoption—all have massive headroom. Edelweiss doesn't need to gain share; it just needs to participate in the natural market growth to generate substantial returns.

The value unlocking isn't complete. Beyond Nuvama, there are multiple catalysts: potential stake sales in the ARC business to global investors, IPO of the alternatives platform once it reaches scale, strategic partnerships in insurance. Each of these could re-rate the stock significantly.

Finally, bulls point to management alignment. The promoters still own significant stakes and have their reputation tied to the company's recovery. The pain of the last few years has created a hunger to prove doubters wrong. Sometimes the best investments are in humbled management teams with something to prove.

The Valuation Reality

The truth, as always, lies somewhere in between. Edelweiss is neither uninvestible toxic waste nor undiscovered treasure. It's a complex financial services company with some good businesses, some mediocre ones, and a complicated history, trading at a discount that reflects both its potential and its problems.

At current valuations, the market is essentially saying: "We'll believe it when we see it." The stock is priced for modest recovery, not dramatic success. This creates an asymmetric risk-reward—if management executes even moderately well, the stock could re-rate significantly. If they stumble again, the downside is probably limited given the already-depressed valuations.

The key monitorables for investors are clear: simplification progress (are they actually reducing complexity?), ROE improvement (can they get to even 12-15%?), regulatory compliance (any new issues?), and value unlocking (are the sum-of-parts gaps closing?).

For value investors with patience and stomach for complexity, Edelweiss represents a classic contrarian opportunity—a decent business at a distressed price. For quality-focused investors, it remains uninvestible until proven otherwise. For traders, it's a volatility machine that will swing wildly on every quarterly result and regulatory announcement.

The investment decision ultimately comes down to a simple question: Do you believe complex financial conglomerates can successfully transform into focused, valuable businesses? History suggests it's possible but rare. Edelweiss is running that experiment in real-time, with public shareholders along for the ride.

XI. Epilogue: The Future of Indian Financial Conglomerates

As Edelweiss enters 2025, its story has become a cautionary tale and potential redemption arc that speaks to larger questions about Indian finance. Can financial conglomerates survive in an era of increasing regulatory scrutiny? Is complexity always a bug, never a feature? And what does the Edelweiss saga mean for the dozens of other financial groups pursuing similar multi-business strategies?

The regulatory environment has fundamentally shifted. The RBI's actions against Edelweiss, IIFL, JM Financial, and others signal a new era where regulators are willing to use harsh medicine to prevent systemic risks. The days of "feather touch" regulation are over. This isn't just about compliance—it's about a philosophical shift in how Indian regulators view financial innovation. Complexity is now presumed guilty until proven innocent.

This creates an existential challenge for conglomerates. The entire premise of companies like Edelweiss was that India needed integrated financial services providers who could offer everything from a loan to insurance to wealth management. The synergies were supposed to be obvious—cross-sell to customers, share infrastructure, optimize capital allocation across businesses. But if regulators force rigid boundaries between businesses, if they prevent the very interconnections that create synergies, then what's the point of the conglomerate structure?

We're likely to see more breakups. Just as Edelweiss spun off Nuvama, other financial conglomerates will be forced to choose: simplify voluntarily or have simplicity imposed by regulators. The market is already voting with its valuations—pure-play companies trade at premiums while conglomerates languish at discounts. The age of the financial supermarket might be ending before it really began in India.

Yet there's a contrarian view worth considering. India is not the US or Europe. It's a market where relationships matter more than products, where trust is local and personal, where customers often need bundled solutions because they lack the sophistication to assemble components themselves. In this context, integrated financial services providers might actually serve a crucial role—if they can figure out how to maintain integration while satisfying regulators' demands for separation.

The technology angle adds another dimension. While traditional conglomerates like Edelweiss struggle with legacy complexity, new-age fintech players are building integrated offerings on modern technology stacks. Companies like Paytm (before its regulatory troubles) or Razorpay are essentially pursuing the same multi-product strategy, just with better technology and less regulatory baggage. The question is whether they'll face the same regulatory pushback once they reach scale.

For investors, the Edelweiss story offers crucial lessons about emerging market financials. First, regulatory risk is not a tail risk—it's a central risk that must be constantly monitored and priced. Second, corporate governance in emerging markets requires active vigilance, not passive trust. Third, complexity discounts in public markets are permanent features, not temporary aberrations.

The path forward for Edelweiss itself remains uncertain but interesting. If management can execute the simplification strategy, improve ROE to respectable levels, and avoid any new regulatory issues, the stock could re-rate dramatically. The businesses underneath the complexity are real and valuable. But trust, once broken, takes years to rebuild. The company will need to demonstrate consistent execution over multiple quarters before the market believes the transformation is real.

The broader implications extend beyond finance. As India develops, it will face this tension repeatedly: the desire for sophisticated, integrated solutions versus the need for simple, transparent, easily regulated structures. The Edelweiss story suggests that, at least in financial services, simplicity will win. Regulators will force it, markets will reward it, and companies will eventually embrace it—voluntarily or otherwise.

Perhaps the most important lesson is about the nature of growth itself. Edelweiss's journey from ₹20 lakh to ₹9,000 crore market cap is impressive, but it came at a cost. The relentless pursuit of growth led to complexity, which led to regulatory problems, which led to value destruction. Sometimes the most valuable thing a company can do is not grow faster but grow more sustainably.

As we watch Edelweiss navigate its next chapter, we're watching more than one company's recovery. We're watching the evolution of Indian finance itself—from an era of relationship-based, complex, sometimes opaque practices to a future of transparent, technology-driven, strictly regulated financial services. Edelweiss is both a product of the old era and a potential pioneer of the new. Whether it successfully makes that transition will determine not just its own fate, but provide a template for dozens of other financial institutions facing similar challenges.

The story of Edelweiss Financial Services is far from over. But the chapters written so far—from bootstrap startup to regulatory crisis to potential redemption—already offer enough lessons to fill a business school curriculum. It's a reminder that in finance, unlike technology, innovation that runs too far ahead of regulation doesn't disrupt the industry—it disrupts itself.

For India's financial sector, the message is clear: the future belongs to those who can balance innovation with compliance, growth with governance, complexity with clarity. Edelweiss learned these lessons the hard way. The question now is whether they—and others—can apply them before it's too late.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube