eClerx Services: From Mumbai Startup to Global KPO Pioneer

I. Introduction & Episode Setup

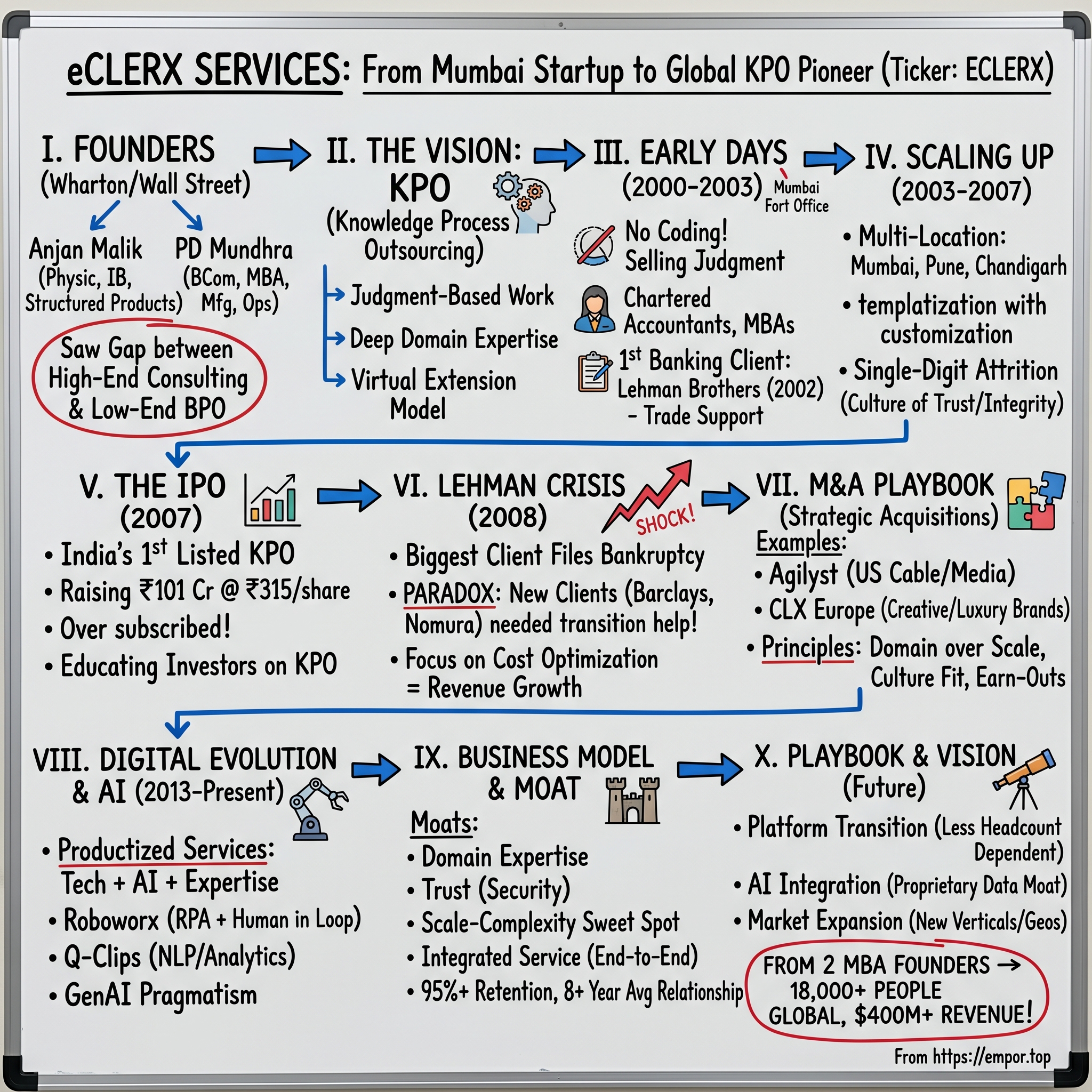

Picture this: Two Wharton MBAs, fresh from the cutthroat world of Wall Street investment banking, sitting in a cramped Fort office in Mumbai in 2000. Outside, the millennium boom is turning to bust. The dot-com bubble is deflating. Yet Anjan Malik and PD Mundhra are convinced they've spotted something everyone else has missed—a massive arbitrage opportunity not in financial markets, but in human knowledge itself.

Today, eClerx Services employs over 18,000 people across multiple continents, serves 50 of the Fortune 500, and generates over $400 million in annual revenue. But this isn't your typical Indian IT services success story. While TCS and Infosys were building armies of programmers, eClerx was pioneering something entirely different: Knowledge Process Outsourcing, or KPO—the outsourcing of complex, judgment-based work that requires deep domain expertise.

The question that drives this story isn't just how two finance guys built India's first publicly listed KPO company. It's how they identified and captured value in the most unlikely place: the messy, manual, unglamorous back-office processes that global corporations desperately needed but couldn't figure out how to fix themselves. This is a story about building trust at scale, surviving the 2008 financial crisis when your biggest client literally disappeared overnight (yes, Lehman Brothers), and creating a new category of business services that sits between traditional BPO call centers and high-end management consulting.

What makes eClerx particularly fascinating for students of business strategy is their contrarian approach. While competitors raced to automate everything, eClerx bet on human judgment augmented by technology. While others chased volume, they focused on complexity. And while the entire Indian IT industry marketed itself on cost arbitrage, eClerx sold expertise.

II. The Founders: Wharton to Wall Street to Mumbai

Anjan Malik's path to entrepreneurship reads like a classic overachiever's resume: Physics degree from Imperial College London, stints at Accenture across Europe, then seven years at Lehman Brothers where he built their global structured products business. By any measure, he'd already won the game. He was pulling down serious Wall Street money, working on cutting-edge financial engineering. But something was gnawing at him.

PD Mundhra's journey was equally impressive but more varied. After his Bachelor's in Commerce from St. Xavier's College, Kolkata, and the obligatory Wharton MBA, he'd worked at Lehman in New York and Citibank in Mumbai. But unlike Malik, Mundhra had already tasted entrepreneurship—he'd spent three years managing a capital goods manufacturing business. He understood operations, the nitty-gritty of managing people and processes, not just financial models.

The two had overlapped at Wharton in the early 1990s, part of that generation of ambitious Indians who went abroad for education but couldn't shake the feeling they were missing something back home. India was changing. The 1991 liberalization had opened doors. By 1999, when they reconnected, both were asking the same question: What if we could apply Wall Street-level analytical rigor to India's cost advantages?

But here's where their story diverges from the typical narrative. They weren't looking to build another software company or BPO call center. During their investment banking days, both had witnessed something peculiar: major financial institutions spending millions on high-end consultants for strategy, then struggling to actually implement anything because the execution required armies of people doing complex but repetitive analytical work. The consultants were too expensive for implementation. The traditional outsourcers were too unsophisticated.

"We saw this massive gap," Malik would later explain in a rare interview. "Fortune 500 companies had these incredibly complex processes—trade reconciliation, risk analytics, data management—that required deep domain knowledge but were still fundamentally repetitive. They were too complex for traditional BPO but too manual for pure technology solutions."

The insight was brilliant in its simplicity: What if you could train really smart people in India—chartered accountants, MBAs, engineers—to become domain experts in these specific processes? Not generic call center workers reading scripts, but genuine specialists who could handle complex, judgment-based work at a fraction of the cost of doing it in New York or London?

By late 1999, they had crystallized their vision. Malik would stay in London, leveraging his relationships and credibility to win clients. Mundhra would build the operation in Mumbai, creating what they called a "virtual extension" of their clients' teams. The division of labor was perfect—Malik spoke the language of Wall Street; Mundhra understood how to build and scale operations in India.

They incorporated eClerx Services Private Limited on March 24, 2000, just as the dot-com bubble was reaching its peak. The timing seemed terrible. But as we'll see, starting during a downturn would become one of their greatest advantages.

III. Founding Vision & Early Days (2000-2003)

The Fort office in Mumbai where eClerx began operations was a far cry from the glass towers of Wall Street. Mundhra started with just a handful of employees, handpicked for their analytical abilities rather than their technical credentials. The first hires weren't software engineers—they were chartered accountants, MBAs, and mathematics graduates. This was deliberate. eClerx wasn't selling coding skills; they were selling judgment.

The founding vision was elegantly simple yet radically different from anything else in the Indian outsourcing landscape. They identified that large global companies were struggling with three fundamental challenges: legacy systems that couldn't talk to each other, the explosion of e-commerce creating new data reconciliation nightmares, and constantly evolving regulatory requirements that made standardization impossible. McKinsey could diagnose these problems. Accenture could design solutions. But who would actually do the work, day in and day out, of making sense of the mess? The virtual outsourced services model that Malik and Mundhra pioneered was revolutionary for its time. Instead of requiring clients to set up captive centers in India (expensive and risky) or work with generic BPO providers (limited capabilities), eClerx offered something in between: dedicated teams that functioned as extensions of the client's own operations but were managed and trained by eClerx.

In 2002, they signed on Lehman Brothers, their first customer in the banking space. The irony of this wouldn't become apparent until 2008. Lehman wanted to outsource trade support. The trade has to get confirmed, the brokerage amounts must be reconciled and the trade has to get settled and cash exchanged. All the operational work, post the trade, was done by eClerx.

This first engagement with Lehman Brothers became the template for everything that followed. It wasn't glamorous work—reconciling trades, validating data, ensuring compliance—but it was mission-critical. A single error could cost millions. The team Mundhra built in Mumbai had to be as reliable as any team on Wall Street, just at a fraction of the cost.

The early days were brutal. The initial challenge was to find the right people to come and join the company. In 2000, people had never heard of eClerx and they weren't looked upon as a preferred industry. While Infosys and Wipro were campus recruiting stars, eClerx was an unknown startup asking people to do work they'd never heard of for clients they couldn't name (due to confidentiality agreements).

But gradually, word spread. The quality of work was exceptional. Clients who started with small pilot projects quickly expanded scope. By 2003, eClerx had proven that complex knowledge work could indeed be done remotely, reliably, and at scale. The foundation was set for explosive growth.

IV. Building the Foundation: Process Excellence & Scale (2003-2007)

Between 2003 and 2007, eClerx underwent a transformation that would make most startups dizzy. They went from dozens of employees to thousands, from one delivery center to multiple locations across India, from a handful of clients to relationships with many of the world's largest corporations. But what's remarkable isn't just the growth—it's how they maintained quality while scaling.

ESL is a data analytics and business process outsourcing company involved in the provision of management and data analytics to various industrial sectors including financial services, cable and telecom services, media and entertainment, manufacturing, travel and leisure, software and high-tech, retail, and fashion. ESL offers a suite of services including trade processing, reference data, accounting and finance, risk, and management services.

The key to their scaling strategy was what Mundhra called "templatization with customization." They would identify common patterns across client needs—say, trade reconciliation or reference data management—and build robust processes around these. But unlike traditional BPO players who forced clients into rigid frameworks, eClerx would then customize these templates for each client's specific requirements.

They opened delivery centers strategically: Mumbai for proximity to financial markets and talent, Pune for its educational institutions and growing tech ecosystem, and Chandigarh for cost advantages and untapped talent pools. Each center was designed not as a cost center but as a center of excellence, with specific domain expertise cultivated over time.

The culture Mundhra and Malik built during these years would become their secret weapon. In an industry notorious for high attrition—often 30-40% annually—eClerx maintained single-digit turnover rates. They achieved this through a combination of factors: hiring for aptitude over experience, investing heavily in training (new hires often underwent 3-6 months of intensive domain training), creating clear career paths, and most importantly, giving employees ownership of client relationships.

"All of modern society is based on trust," Malik would later say, "and as we grow, add geographies, business diversity and complexity, the thing that holds us together is a culture of trust, and it comes from one simple word—integrity. Our entire business model is built on a foundation of integrity."

This wasn't just corporate rhetoric. In an industry where data security breaches could destroy companies overnight, eClerx's track record was spotless. They handled some of the most sensitive financial data in the world—trading positions, customer information, proprietary algorithms—without a single major incident. This reliability became their calling card.

By 2007, eClerx was processing millions of transactions daily, managing petabytes of data, and had become indispensable to many of their clients' operations. Revenue had grown from virtually nothing to over $50 million. They were profitable, cash-flow positive, and growing at over 40% annually. The founders decided it was time for the next big step: going public.

V. The IPO Story: India's First Listed KPO (2007)

The Mumbai stock markets were buzzing in late 2007. The Sensex had crossed 20,000 for the first time. Global money was pouring into India. And here was eClerx, ready to make history as India's first Knowledge Process Outsourcing company to list on the public markets.

eClerx IPO bidding started from December 4, 2007 and ended on December 7, 2007. The shares got listed on BSE, NSE on December 31, 2007. The IPO was for 3,206,349 equity shares at ₹315 per share, raising approximately ₹101 crores. In a market obsessed with software companies and traditional BPO players, eClerx had to educate investors about what KPO even meant.

The roadshow presentations were fascinating exercises in storytelling. How do you explain to a retail investor in Mumbai that you're not TCS (software development) or Genpact (call centers) but something entirely different? Malik and Mundhra's pitch was elegant: "We're the knowledge workers behind the world's biggest companies. When a Fortune 500 bank needs to reconcile millions of trades, when a retailer needs to manage product data across thousands of SKUs, when a cable company needs to optimize its network operations—they call us."

Mundhra and Malik founded eClerx in 2000, and in 2007 became India's first and only publicly listed knowledge processing (KPO) company. This distinction mattered. While BPO was about cost arbitrage and scale, KPO was about expertise and trust. The margins were better, the client relationships stickier, the barriers to entry higher.

The timing seemed perfect. Global financial services were booming. Regulatory requirements were increasing, creating more demand for compliance and risk management services. Digital commerce was exploding, driving demand for data analytics. Everything pointed toward continued growth.

The IPO was oversubscribed multiple times. On December 31, 2007—New Year's Eve—eClerx shares began trading on both the Bombay Stock Exchange and National Stock Exchange. The founders, who had retained majority control, were now paper millionaires many times over. But they had no idea that in exactly nine months, their biggest client and the company that gave them their start would cease to exist.

The IPO proceeds were earmarked for expansion: new delivery centers, technology infrastructure, and potential acquisitions. The company was now under the scrutiny of public markets, required to report quarterly results and manage investor expectations. For a company built on long-term client relationships and patient capability building, this would require a delicate balance.

What's remarkable about the eClerx IPO, in hindsight, is how it marked both an ending and a beginning. It was the culmination of seven years of bootstrapped growth, proof that the KPO model worked. But it also came at the absolute peak of the global financial bubble. The real test of eClerx's model was about to begin.

VI. Surviving & Thriving Through the Financial Crisis (2008-2012)

September 15, 2008. Lehman Brothers, the 158-year-old investment bank, files for bankruptcy. For most companies, losing your first and one of your largest clients overnight would be catastrophic. For eClerx, it became a defining moment that would paradoxically strengthen their business.

The immediate impact was surreal. The eClerx team in Mumbai that had been processing Lehman trades on Friday was suddenly without work on Monday. But here's where the story takes an unexpected turn. Within days, Barclays acquired Lehman's North American operations. Nomura took over the Asian and European businesses. And both needed someone who understood Lehman's impossibly complex operations and could help with the transition.

Who better than the team that had been running these processes for six years?

Instead of losing the Lehman business, eClerx found itself working with multiple new clients, helping them untangle and integrate Lehman's operations. The crisis that should have crushed them became a massive opportunity. Revenue from financial services clients actually increased during 2008-2009.

But the real growth driver during the crisis was something else entirely: cost optimization. As global corporations faced the worst economic environment since the Great Depression, they desperately needed to cut costs without compromising operations. Suddenly, eClerx's value proposition—doing complex work at 30-40% of the cost with equal or better quality—wasn't just attractive; it was essential for survival.

The company's revenue grew from approximately $65 million in 2008 to over $100 million by 2010, even as the global economy contracted. Client concentration actually decreased as they added new relationships with banks, retailers, and cable companies all seeking efficiency. The average client relationship expanded from single processes to multiple service lines.

The crisis also validated eClerx's conservative financial management. While competitors leveraged up during the boom years, eClerx had remained debt-free with significant cash reserves. This allowed them to invest counter-cyclically, hiring top talent laid off by struggling competitors, acquiring capabilities, and expanding delivery capacity just as real estate and labor costs plummeted.

Mundhra's operational excellence shone during this period. He implemented what he called "flexible staffing models"—the ability to quickly scale teams up or down based on client needs without compromising quality. This required sophisticated workforce planning, cross-training programs, and a bench strength strategy that most BPO companies couldn't match.

The cultural DNA of integrity and trust proved invaluable during the crisis. Clients facing existential threats needed vendors they could absolutely rely on. eClerx's perfect track record on data security, consistent delivery quality, and willingness to share risk through outcome-based pricing models made them a safe harbor in the storm.

By 2012, eClerx had emerged from the financial crisis stronger than ever. Revenue had more than doubled since the IPO. They were working with over 30 Fortune 500 clients. The employee base had grown to over 7,000. And most importantly, they had proven that their model wasn't just viable in good times—it was antifragile, actually growing stronger under stress.

VII. The M&A Playbook: Strategic Acquisitions

For a decade, eClerx had grown entirely organically. But by 2013, Malik and Mundhra recognized that to reach the next level, they needed to accelerate capability building through acquisitions. Their M&A strategy would be as thoughtful and contrarian as everything else they did.

The first major move came with Agilyst Inc., a US-based KPO company specializing in cable and media operations. eClerx acquired Agilyst through its overseas subsidiary eClerx Investments Ltd. With this acquisition, eClerx gained a strong foothold in the US media industry, diversified the revenue base by addition of large Fortune 100 clients and brought on board a strong delivery team in a Tier-2 Indian location.

What made the Agilyst acquisition brilliant wasn't just the client relationships or capabilities—it was the structure. Rather than a big-bang integration that could disrupt operations, eClerx kept Agilyst as a semi-autonomous unit, preserving its culture and client relationships while gradually integrating back-office functions. The earn-out structure aligned the Agilyst founders' incentives with long-term value creation rather than short-term exit maximization.

On 31 March 2015, eClerx acquired Creative Services Agency CLX Europe, for a total purchase consideration of up to EUR 25 million. CLX brought something entirely different: creative and content management capabilities for luxury brands and retailers. This wasn't traditional eClerx territory—it was about managing product photography, creating marketing content, ensuring brand consistency across channels.

The CLX acquisition revealed the evolution in eClerx's thinking. They were no longer just a back-office processor but a company that could handle the entire data and content lifecycle for global brands. A luxury fashion house could now use eClerx to manage everything from product information management to creative asset production to online catalog management.

The M&A playbook that emerged had several key principles:

- Domain over scale: They acquired companies with deep expertise in specific verticals rather than generic BPO players

- Cultural fit over financial metrics: They walked away from financially attractive deals if the culture didn't align

- Earn-out structures: Most deals included multi-year earn-outs that kept founders engaged and aligned

- Integration patience: Rather than forced integration, they allowed acquired units to operate independently initially, then gradually integrated where it made sense

The acquisitions also brought geographic expansion. Through acquired entities, eClerx established presence in Italy, Germany, France, and other European markets. This wasn't about labor arbitrage—European operations were actually higher cost—but about being closer to clients and understanding local market nuances.

By 2018, roughly 20% of eClerx's revenue came from acquired entities, but more importantly, these acquisitions had opened entirely new verticals and service lines. The company could now credibly claim to be a full-service knowledge process partner rather than just a financial services BPO provider.

The M&A strategy also revealed something deeper about eClerx's evolution. They were building a portfolio of specialized capabilities that could be combined in unique ways for clients. A retailer might start with creative services from CLX, add data analytics from the core eClerx team, and layer on customer operations from another acquisition. This created switching costs and deepened client relationships in ways that pure organic growth couldn't achieve.

VIII. The Digital Evolution & AI Transformation (2013-Present)

The period from 2013 onward marked eClerx's most fundamental transformation since its founding. The company that had built its reputation on human expertise was now racing to integrate artificial intelligence, automation, and digital technologies into everything it did. But true to form, their approach was different from the industry's automation-everywhere mantra.

eClerx is a global leader in productized services, enhancing business outcomes through technology, Artificial Intelligence, and deep domain expertise. The key word here is "productized"—eClerx was moving from pure services to packaged solutions that combined human expertise with proprietary technology.

The shift began with Roboworx, their robotic process automation platform. But unlike generic RPA tools from UiPath or Blue Prism, Roboworx was designed specifically for the complex, exception-heavy processes eClerx specialized in. It could handle the 80% of routine work, but more importantly, it knew when to escalate to human experts for the 20% that required judgment.

They developed Q-Clips, a SaaS-based repository of customer interactions that used natural language processing to extract insights from millions of customer communications. Again, this wasn't a standalone product but part of an integrated service where eClerx analysts provided the context and actionable recommendations that pure technology couldn't deliver.

The AI integration was particularly sophisticated in their financial markets business. They built machine learning models that could predict trade breaks before they happened, identify patterns in reference data discrepancies, and flag potential compliance issues. But crucially, these models were trained on the millions of transactions eClerx had processed over two decades—a dataset competitors couldn't replicate.

For 25 years, eClerx has been delivering solutions that power processes for financial markets, automate compliance, accelerate innovation, scale digital commerce, and transform customer experiences. From the very beginning, success has been built on deep understanding of industry-specific needs and relentless focus on operational excellence at scale. As client needs evolved, eClerx continually re-engineered capabilities and integrated new ones to bring emerging technologies to help clients master rapidly changing industries. With each engagement, they deepen domain expertise, refine proprietary AI-driven tools, and pioneer innovative workflows.

What set eClerx's digital transformation apart was their "human-in-the-loop" philosophy. While competitors promised fully automated solutions, eClerx recognized that in complex knowledge work, the combination of human judgment and artificial intelligence was more powerful than either alone. Their platforms were designed to augment human capabilities, not replace them.

The productization strategy also changed their business model. Instead of purely time-and-materials or FTE-based pricing, they could now offer outcome-based pricing, subscription models, and even gain-sharing arrangements. A retailer might pay based on improvement in product data quality. A bank might pay based on reduction in trade failures.

This evolution wasn't without challenges. Building technology required different skills than managing operations. The company had to hire software engineers, data scientists, and product managers—competing with tech giants for talent. They had to balance investment in technology with maintaining margins that investors expected.

But by 2020, the strategy was clearly working. Digital services and platforms contributed over 30% of revenue. More importantly, they had changed the competitive dynamics. Pure-play BPO companies couldn't match eClerx's domain expertise. Pure technology companies couldn't provide the human insight. Management consultants couldn't operate at eClerx's price points.

The COVID-19 pandemic accelerated this digital transformation. Within weeks, eClerx moved 95% of its workforce to remote operations—something unthinkable for a company handling sensitive financial data just years earlier. Their technology investments in secure remote access, digital collaboration tools, and automated quality monitoring made this transition seamless.

Today, eClerx's technology story continues to evolve with generative AI. They're using large language models to automate report generation, extract insights from unstructured data, and even generate code for process automation. But again, their approach is pragmatic—using AI where it adds value while maintaining human oversight for critical decisions.

IX. Business Model & Competitive Moat

Understanding eClerx's business model requires appreciating the delicate balance they've struck between standardization and customization, between human expertise and technological efficiency, between growth and profitability. It's a model that has proven remarkably resilient across economic cycles and technological disruptions.

At eClerx, we serve some of the largest global companies—50 of the Fortune 500 clients. But this client concentration is actually a strength, not a weakness. The average client relationship spans over 8 years, with many dating back more than a decade. Client retention rates exceed 95% annually—extraordinary in an industry where switching vendors is common.

The economic model is compelling. Gross margins typically range from 35-40%, EBITDA margins around 25-30%—significantly higher than traditional BPO players but lower than pure software companies. This reflects their positioning: more value-add than BPO, more operational intensity than SaaS.

The company organizes itself into four geographic segments, with the United States contributing roughly 60% of revenue, followed by the United Kingdom at 20%, Continental Europe at 15%, and Asia-Pacific at 5%. This geographic mix provides natural currency hedging—rupee depreciation benefits the top line while most costs are rupee-denominated.

But the real moat isn't financial—it's operational. Consider what it would take to replicate eClerx:

Domain Expertise Moat: Twenty-plus years of handling complex processes across industries has created institutional knowledge that can't be easily replicated. An eClerx team knows not just how to reconcile trades, but why specific breaks occur with particular counterparties under certain market conditions. This tacit knowledge is embedded in their people, processes, and now their AI models.

Trust Moat: Handling sensitive financial data, customer information, and proprietary business processes requires absolute trust. eClerx's perfect security track record and deep client relationships create switching costs that go beyond economic considerations. A Fortune 500 CFO won't risk their core operations to save 10% on costs.

Scale-Complexity Sweet Spot: eClerx operates in a goldilocks zone—processes complex enough that generic BPO players can't handle them, but repetitive enough to achieve economies of scale. This is a narrow band that requires constant calibration.

Integrated Service Model: Unlike pure-play vendors that offer point solutions, eClerx can handle end-to-end processes. A cable company might start with network data management, expand to customer analytics, then add content operations. This creates a web of dependencies that makes switching vendors practically impossible.

The competitive landscape reveals eClerx's unique position. Against Indian IT giants like TCS, Infosys, and Wipro, eClerx is tiny—but these companies focus on technology services, not knowledge processes. Against global BPO players like Genpact or WNS, eClerx operates at a higher level of complexity and value-add. Against boutique KPO firms, eClerx has scale and multi-vertical capabilities.

The capital-light nature of the business is another advantage. Unlike manufacturing or even software development, eClerx doesn't require massive upfront investments. Their primary assets are people and processes—both of which can be scaled gradually based on demand. This allows them to maintain return on equity above 20% while remaining debt-free.

The pricing power dynamics are fascinating. While labor cost inflation in India averages 8-10% annually, eClerx has been able to pass through these increases and more by moving up the value chain. A process that might have been billed at $20 per hour five years ago might now include automation components, analytics, and insights—billed at $35 per hour with better margins.

X. Playbook: Lessons for Services Businesses

The eClerx story offers a masterclass in building and scaling a knowledge services business. Their playbook challenges conventional wisdom about everything from hiring to pricing to client management.

Lesson 1: Hire for Aptitude, Train for Expertise While competitors fought for experienced professionals, eClerx hired fresh graduates with strong analytical abilities and invested heavily in training. New employees often spend 3-6 months in training before touching client work. This seems inefficient but creates several advantages: lower hiring costs, better cultural fit, and most importantly, no bad habits to unlearn. The training investment also creates employee loyalty—people feel invested in rather than exploited.

Lesson 2: The Trust Equation "Our entire business model is built on a foundation of integrity," Malik has said repeatedly. In a services business where the product is intangible and quality is subjective, trust becomes the ultimate differentiator. eClerx built trust through radical transparency—sharing both successes and failures with clients, providing detailed metrics on everything from process efficiency to employee satisfaction, and sometimes even recommending against their own services when not appropriate.

Lesson 3: Geographic Arbitrage Plus The India advantage isn't just about cost—it's about talent availability, time zone coverage, and scalability. But eClerx went beyond simple arbitrage. They created centers of excellence in different locations: Mumbai for financial services, Pune for technology operations, Chandigarh for content management. This specialization created knowledge clusters that became self-reinforcing.

Lesson 4: The Power of Saying No In an industry where growth often comes from saying yes to everything, eClerx became selective. They turned down clients that wanted only cost reduction. They avoided projects outside their expertise. They walked away from acquisitions that didn't fit culturally. This discipline meant slower growth but higher quality revenue.

Lesson 5: Process as Product While everyone talked about productization, eClerx actually did it. They turned recurring processes into templated solutions, embedded best practices into technology platforms, and created intellectual property from operational experience. A trade reconciliation process became a product. A data quality framework became a platform. This allowed them to capture value beyond hourly billing.

Lesson 6: The Bench Strength Paradox In services, bench strength (unutilized employees) is typically seen as waste. eClerx maintains 10-15% bench strength deliberately. This allows them to respond quickly to client needs, provides buffer for training and innovation, and most importantly, signals to clients that they have capacity for growth. The cost of bench strength is more than offset by faster growth and higher client satisfaction.

Lesson 7: Culture as Strategy In a people business, culture isn't soft stuff—it's strategic advantage. eClerx's culture of integrity, continuous learning, and client focus became self-selecting. The right people thrived; the wrong people left quickly. This reduced management overhead and increased operational efficiency. Culture scaled better than processes.

XI. Analysis & Investment Case

Looking at eClerx as an investment proposition requires understanding both its impressive track record and the evolving challenges it faces.

As of July 25, 2025, eClerx Services's stock price is $42.18. Its current market cap is $1.98B with 47M shares. As of June 30, 2025, eClerx Services has a trailing 12-month revenue of $413M. The company has delivered impressive growth, with revenue going up 16.1% YoY in Q4 FY2025 and reporting highest-ever annual revenue at INR 3,439.6 crore for the full fiscal year.

Bull Case:

The investment thesis for eClerx rests on several compelling factors. First, the secular growth in data and process complexity isn't slowing down—it's accelerating. Every new regulation, every new digital channel, every new data source creates more work that fits perfectly into eClerx's sweet spot. The company is essentially selling shovels in a gold rush that shows no signs of ending.

Market cap of 19,572 Crore (up 66.4% in 1 year) with revenue of 3,519 Cr and profit of 571 Cr, trading at 8.49 times book value with promoter holding at 53.8%. The valuation appears reasonable for a company growing revenue at 15%+ with strong margins and no debt.

The client quality and stickiness remain exceptional. At eClerx, we serve some of the largest global companies—50 of the Fortune 500 clients. These aren't price-sensitive SMBs but large enterprises that value reliability over cost savings. The 95%+ retention rates and 8+ year average relationships create highly predictable revenue streams.

The AI opportunity is transformative rather than threatening. While automation might reduce headcount needs, it allows eClerx to move further up the value chain, charging more for insights rather than just processing. Their proprietary data sets and domain expertise create a moat that pure technology players can't replicate.

Geographic expansion provides runway. While heavily dependent on the US and UK markets, there's significant opportunity in Continental Europe, Asia-Pacific, and emerging markets. The recent Peru delivery center opening shows they're still finding new arbitrage opportunities.

Bear Case:

The risks are equally real. Labor cost inflation in India continues at 8-10% annually, and while eClerx has historically passed these through, there's a limit to pricing power. Wage pressures are particularly acute for the specialized talent eClerx needs—data scientists, domain experts, automation engineers.

Client concentration, while improving, remains a concern. The top 5 clients likely contribute 30-40% of revenue. Losing even one major client would significantly impact growth and margins. The Fortune 500 client base is consolidating through M&A, potentially reducing the customer universe.

Technology disruption is the existential threat. Generative AI and advanced automation could eventually handle much of the complex-but-repetitive work eClerx specializes in. While they're integrating AI themselves, it's unclear if they can transition fast enough from a people-leveraged to a technology-leveraged model.

Competition is intensifying from multiple directions. Indian IT giants like TCS and Infosys are moving into higher-value services. Global consulting firms are building offshore delivery capabilities. Specialist KPO players are emerging in specific verticals. Pure-play automation vendors promise to eliminate the need for human processing entirely.

The macroeconomic sensitivity can't be ignored. Despite performing well through 2008, eClerx is still tied to global corporate spending. A prolonged recession, particularly in financial services, would impact growth. The current high interest rate environment is already causing clients to scrutinize vendor spending more carefully.

Valuation Perspective:

At current levels, eClerx trades at roughly 20-25x trailing earnings—not cheap for a services business but reasonable for one growing at 15%+ with 25%+ EBITDA margins. The dividend yield is minimal as the company reinvests for growth. The promoter holding of 53.8% provides stability but limits free float.

The key question for investors is whether eClerx can successfully navigate the transition from labor arbitrage to value arbitrage, from process expertise to platform capabilities, from services to products. The early signs are encouraging, but the jury is still out.

XII. Future Vision & Conclusion

As eClerx approaches its 25th anniversary, the company stands at an inflection point. The business model that brought them from a Fort office in Mumbai to a $2 billion market cap is evolving rapidly. The future will be determined by how successfully they navigate three critical transitions.

The Platform Transition: eClerx is systematically productizing its expertise, turning processes into platforms, insights into applications, and services into subscriptions. The vision is clear: become less dependent on headcount growth for revenue growth. Early products like Roboworx and Q-Clips show promise, but they need to achieve meaningful scale to move the needle on overall growth.

The AI Integration: Generative AI represents both the greatest threat and the greatest opportunity. eClerx's approach—using AI to augment rather than replace human expertise—is pragmatic but may prove temporary. The company that built its reputation on human judgment must now prove it can thrive in an increasingly automated world. Their advantage lies in the proprietary data sets and domain knowledge accumulated over two decades, which can train AI models that generic competitors can't match.

The Market Expansion: While financial services remains the core, eClerx is systematically entering new verticals—healthcare, pharmaceuticals, technology, industrials. Each requires deep domain expertise that takes years to build. The question is whether they can replicate their financial services success in these new areas before competitors establish themselves.

Key Takeaways for Entrepreneurs and Investors:

-

Category Creation Matters: eClerx didn't compete in existing categories—they created a new one. KPO was their invention, and being first gave them a decade-long head start.

-

Trust Scales Better Than Technology: In services businesses, trust is the ultimate moat. eClerx's two-decade track record of zero security breaches and consistent delivery is irreplaceable.

-

Complexity is a Feature, Not a Bug: While others sought to simplify and standardize, eClerx embraced complexity. The messier the problem, the higher the margins.

-

Culture Compounds: The emphasis on integrity and learning created a self-reinforcing culture that attracted the right people and repelled the wrong ones. This cultural compounding is eClerx's hidden asset.

-

Patient Capital Wins: Malik and Mundhra retained majority control through the IPO and beyond, allowing them to make long-term decisions without quarterly pressure. This patience enabled investments in training, technology, and relationships that wouldn't have survived activist investors.

The Verdict:

eClerx Services is a remarkable story of vision, execution, and adaptation. From identifying the KPO opportunity before the category existed, to surviving the financial crisis, to embracing digital transformation, the company has consistently evolved ahead of the market.

The challenges ahead are real—technology disruption, talent inflation, competitive intensity. But eClerx has proven remarkably adaptable over 25 years. They've transitioned from trade processing to data analytics, from Mumbai-only to global delivery, from pure services to productized platforms.

For investors, eClerx represents a unique play on the continued growth in data and process complexity. It's not a high-growth tech stock, nor a stable utility. It's something in between—a steady compounder with option value on successful digital transformation.

For entrepreneurs, eClerx offers lessons in building sustainable competitive advantages in service businesses. Their focus on trust, expertise, and gradual capability building created a moat that pure capital or technology couldn't replicate.

As Mundhra and Malik look toward the next chapter, their creation stands as testament to a simple but powerful idea: in a world drowning in data and complexity, the companies that can make sense of the mess will always have value. Whether that value is delivered by humans, machines, or most likely some combination, eClerx has positioned itself to capitalize on the opportunity.

The Mumbai monsoons that welcomed eClerx's founding in 2000 still arrive each year, but the company they wash over has transformed beyond recognition. From a startup serving one client to a global corporation serving fifty Fortune 500 companies, from pure services to AI-powered platforms, from Mumbai to the world—eClerx's journey exemplifies the best of India's knowledge economy.

The next 25 years will undoubtedly bring challenges the founders couldn't have imagined. But if history is any guide, eClerx will adapt, evolve, and continue delivering value in ways we can't yet envision. In the end, that adaptability—more than any specific service or technology—may be their greatest asset.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube