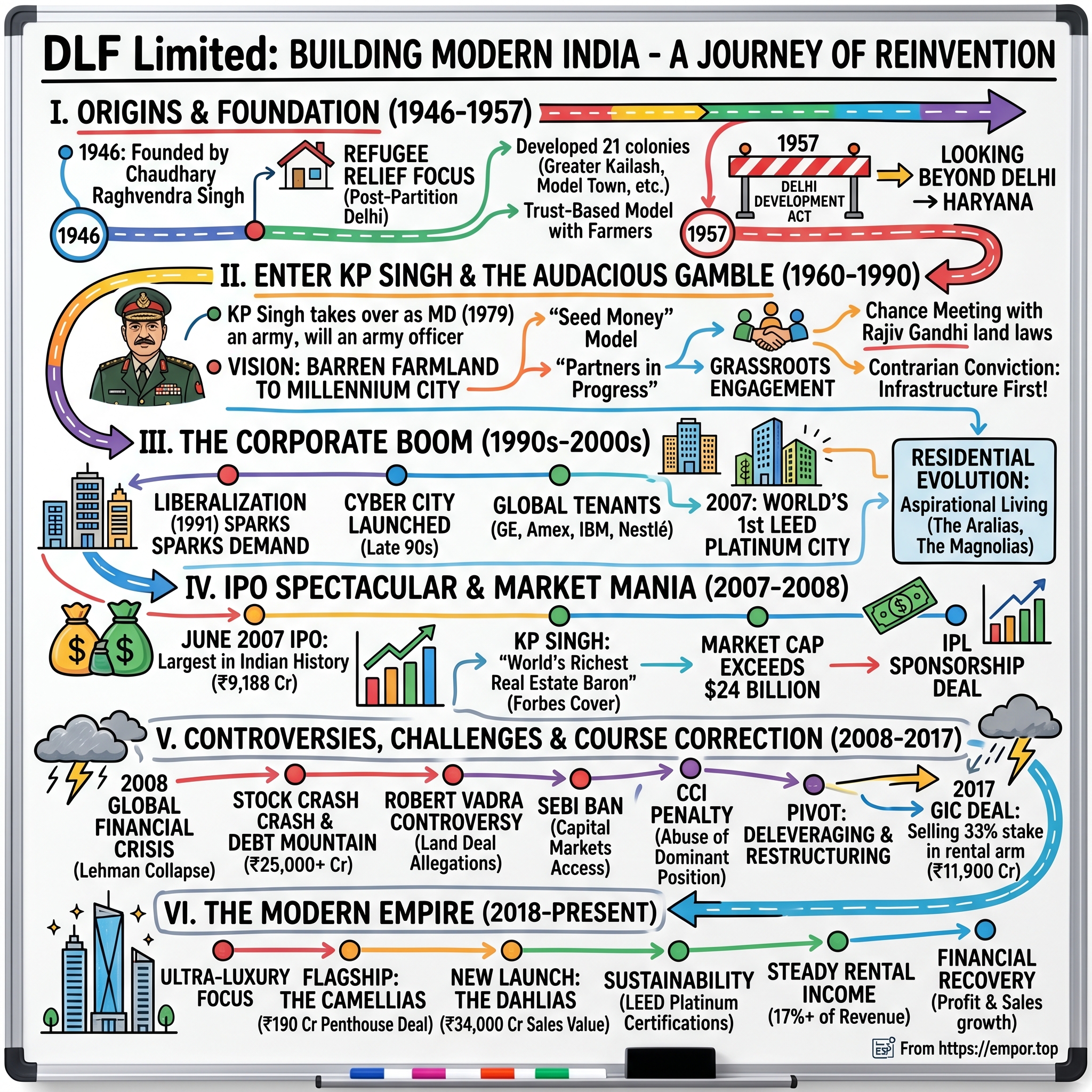

DLF Limited: Building Modern India

I. Introduction & Episode Roadmap

Picture this: April 2025, Gurugram's Golf Course Road—a gleaming tower pierces the Delhi skyline, and inside, a penthouse changes hands for Rs. 190 crore. In a historic real estate deal, a luxury penthouse at DLF Camellias, located in Gurgaon's prestigious Golf Course Road area, has been sold for Rs 190 crore. This isn't just India's most expensive apartment transaction; it's a testament to how a company born from post-Partition refugee relief evolved into the architect of modern India's urban landscape.

DLF Limited stands today as India's largest publicly listed real estate company with a market capitalization of Rs 1,87,692 crore, commanding a remarkable 74.1% promoter holding. But how did a humanitarian effort to house displaced families transform into a $25 billion real estate empire that literally built India's millennium city?

This is the story of three generations of visionaries—from Chaudhary Raghvendra Singh's compassionate foundation in 1946, through KP Singh's audacious Gurgaon gamble, to today's luxury empire helmed by Rajiv Singh. It's a saga of political navigation, controversial deals, spectacular wealth creation, and the fundamental reshaping of how India lives, works, and dreams.

We'll journey through the refugee colonies of post-Independence Delhi, witness the transformation of barren Haryana farmland into a global business hub, dissect one of India's most controversial IPOs, and explore how DLF continues to define ultra-luxury living in a rapidly evolving market. Along the way, we'll unpack the playbook that turned agricultural land into Asia's most valuable real estate, the controversies that nearly derailed an empire, and the strategic pivots that keep DLF at the apex of Indian real estate.

II. Origins: Partition, Delhi, and the Birth of DLF (1946–1957)

The year is 1946. India stands on the precipice of independence, but with freedom comes one of history's greatest human tragedies—Partition. Millions of refugees stream across newly drawn borders, many arriving in Delhi with nothing but the clothes on their backs. Into this humanitarian crisis steps Chaudhary Raghvendra Singh, a decorated army officer who would lay the foundation for what becomes India's real estate colossus.

Chaudhary Raghvendra Singh founded DLF in 1946, in pre-independent India. A born businessman, he began his real estate career by transforming the urban landscape of Delhi's National Capital Region, providing millions of homes to families displaced by partition who settled in the capital. This wasn't just business—it was nation-building at its most fundamental level.

Born on September 19, 1910 and originally a graduate of St. Stephen's College, Delhi, Chaudhary Saheb went on to join the Indian Army where he rose to the rank of Major and was decorated with an MBE for exemplary service. A philanthropist at heart, Chaudhary Saheb is remembered not only for his innovations and entrepreneurial skills but also for his association, as Board Member, with various charitable trusts and educational institutions, his role in pioneering welfare reforms for ex-servicemen, and his humanitarian work.

The early DLF model was revolutionary for its time. Starting with Krishna Nagar in East Delhi in 1949, the company embarked on an unprecedented building spree. Within a decade, DLF had developed 21 residential colonies that would become the backbone of modern Delhi's geography. These weren't just housing projects—they were entire ecosystems. Model Town, with its wide tree-lined avenues and planned infrastructure. Rajouri Garden, which would evolve into West Delhi's commercial heart. South Extension, destined to become one of the capital's most coveted addresses. Greater Kailash, synonymous with Delhi's emerging upper middle class.

He is also considered to be the father of Delhi's first co-operative movement and the founder of the Indian real estate sector. The business model was built on something rare in post-Independence India: trust. When we first began to develop residential colonies for displaced families in a post-partition India, we built on land bestowed to us by farmers on the basis of trust. Farmers would provide land based on verbal agreements and handshakes, with payments often coming after homes were built and sold. This trust-based approach would become a cornerstone of DLF's land acquisition strategy for decades to come.

But 1957 brought a seismic shift. The Delhi Development Act transferred all real estate development rights to the newly formed Delhi Development Authority (DDA). Overnight, private developers were essentially locked out of Delhi's real estate market. For most companies, this would have been a death sentence. For DLF, it became the catalyst for transformation.

Faced with the choice of dissolution or evolution, Chaudhary Raghvendra Singh made a decision that would reshape not just his company but India's urban landscape: if Delhi was closed, DLF would look beyond. The company's eyes turned to the dusty villages across the border in Haryana, where few saw opportunity but where DLF would eventually build an empire.

The foundation years established more than just a business—they created a template for large-scale urban development in India. The company had proven it could execute massive projects, build trust with stakeholders from farmers to home buyers, and most importantly, adapt to seismic regulatory changes. These lessons would prove invaluable when a young army officer married into the family and brought a vision that would transform not just DLF, but the very concept of Indian real estate.

III. Enter KP Singh: The Army Officer Who Changed Everything (1960–1979)

The transformation of DLF from a Delhi-centric developer to India's real estate titan began with an unlikely protagonist: a cavalry officer with a penchant for polo and an aeronautical engineering background. After graduating in science from Meerut College in Uttar Pradesh, Kushal Pal Singh embarked on a diverse career journey. He initially pursued aeronautical engineering in the United Kingdom and was selected to join the Indian Army by the British Officers Services Selection Board. Commissioned into the Deccan Horse in 1951, he served with distinction before transitioning to the corporate world.

Born on August 15, 1931—India's future Independence Day—Kushal Pal Singh's entry into DLF wasn't immediate or obvious. After resigning from the army, Singh, together with another retired army officer, initially entered the stud farm business. He also started a battery company; however, the venture was unsuccessful and the losses sustained from it caused Singh's creditors to take him to court. These early failures would prove formative, teaching him lessons about debt, risk, and the importance of patient capital that would guide his later real estate strategy.

In 1960, Singh joined American Universal Electric Company and, after its merger with DLF Universal Limited (DLF) in 1979, he took over as the managing director with Chaudhary Raghuvender Singh. But his connection to DLF ran deeper than business—he had married Indira Singh, the founder's daughter, binding his fate to the company's future.

The 1970s tested Singh's commitment to this future. In 1975, Singh almost sold his shares in DLF for 25 lakhs after a decision made by his father-in-law Chaudhary Raghvendra and apathy regarding the real estate sector due to bureaucratic red tape, but Singh at the last minute declined to do the transaction, keeping his shares. This near-exit moment would later seem almost incomprehensible—those shares would eventually be worth billions.

The catalyst for Singh's real estate epiphany came in 1976 with the Urban Land Ceiling Act (ULCRA). The Government of India introduced the Urban Land (Ceiling and Regulation) Act, 1976 (ULCRA) to grow low-income housing and set limits for the ownership of vacant urban land. The law received a backlash from people who had already invested in the urban land, including Singh, who took over a dormant DLF to attempt to secure exemptions for investors while studying the city's limitations. He identified the Old-Gurgaon Road as a key link between Delhi's southern area and Haryana, that had not passed the ULCRA.

While others saw regulatory constraint, Singh saw opportunity. Delhi's growth couldn't be contained forever. The city would need to expand, and when it did, it would flow south into Haryana. The Old Delhi-Gurgaon Road, a dusty highway connecting Delhi to what was then a small Haryana town, became his focus. Here was land—vast, undeveloped, and crucially, outside ULCRA's restrictions.

DLF used the relaxed land acquisition laws as Singh revitalized the company, starting with its 30 acres and rapidly acquiring land from local landowners and farmers. But Singh's approach to land acquisition was revolutionary. Rather than outright purchase, which would have required massive capital the company didn't have, he developed what he called the "seed money" model. Farmers would receive a small upfront payment with the promise of full payment once development began. More innovatively, he offered them participation in the upside—shops in future commercial developments, or developed plots they could sell at market rates.

This wasn't just financial engineering; it was social engineering. Inspired by the need to involve the farming community in building projects, his 'Partners in Progress' model for housing and urban development revolutionised land acquisition. Singh spent countless hours in Haryana's villages, drinking tea with sarpanches (village heads), attending weddings and funerals, building relationships that would span generations. He learned to speak Haryanvi, understood local customs, and most importantly, built trust.

The late 1970s saw Singh studying international models obsessively. He traveled to South Korea to understand how Seoul had expanded into satellite cities. He visited Malaysia to study Kuala Lumpur's planned townships. He analyzed Singapore's public housing model. From each, he extracted lessons: the importance of infrastructure preceding development, the need for mixed-use planning, the critical role of transportation connectivity.

By 1979, when Singh officially became Managing Director after the merger with American Universal Electric Company, he had assembled the pieces of his vision. He controlled significant land parcels along the Delhi-Gurgaon corridor. He had relationships with hundreds of farming families. He had studied global best practices. Most importantly, he had developed a contrarian conviction: that Gurgaon's farmland could become India's next great city.

But vision without execution remains merely a dream. Singh needed political support, infrastructure investment, and buyers willing to bet on his audacious vision. The 1980s would test whether an army officer turned reluctant real estate developer could transform barren fields into India's millennium city. The stage was set for one of Indian business history's greatest gambles.

IV. The Gurgaon Gamble: From Farmland to Fortune (1980–1990)

The mythology of modern Indian business has few moments as serendipitous as a car breaking down on a dusty Haryana road. During the 1980s, Singh had a chance meeting with Rajiv Gandhi, who had then just entered politics and later became Prime Minister of India, after his car engine had overheated near Singh's property in Haryana. Singh met Rajiv and spoke about business plans for Gurgaon and how certain laws were hindering his acquisition of land in the state. Singh later had meetings with Rajiv, and Rajiv convinced his mother, then Indian prime minister Indira Gandhi, to change the Haryana land laws.

This chance encounter would prove transformative. The young Gandhi scion, educated at Cambridge and comfortable with ambitious modernization projects, understood Singh's vision immediately. Here was an opportunity to create a planned city that could showcase India's development potential—a Brasília or Chandigarh for the new India.

Armed with political understanding, Singh moved quickly. In April 1981, DLF received its first license for developing 39 acres in Gurgaon. By 1983, this had expanded to 556 acres. But with opportunity came opposition. The entrenched political interests in Haryana, particularly those aligned with former Chief Minister Bansi Lal, viewed Singh's rapid land accumulation with suspicion and hostility.

The conflict with Bansi Lal's faction turned dangerous. Singh received threats, faced harassment from local authorities, and at one point, went into hiding for several weeks when intelligence sources warned of potential physical harm. His offices were raided, licenses were threatened with cancellation, and media campaigns painted him as a land shark exploiting poor farmers.

But Singh's response revealed the strategic mind behind the vision. Rather than confrontation, he chose patience and relationship-building. He continued his grassroots engagement with farming communities, ensuring that early land sellers profited visibly from their deals. When the first farmers who had sold to DLF bought cars and built pucca houses, it created a demonstration effect that no political opposition could counter.

The development strategy for what would become DLF City was revolutionary for India. Singh insisted on infrastructure first—a radical departure from the typical Indian development model where buildings came first and infrastructure followed haphazardly, if at all. DLF invested in roads, sewerage, water supply, and electrical infrastructure before selling a single plot. The company even built its own water treatment plants and power backup systems, creating an island of first-world infrastructure in rural Haryana.

The initial response was devastating. Despite roadshows in Delhi, Mumbai, and Calcutta, buyers remained skeptical. Who would invest in property 30 kilometers from Delhi, in a state known more for agriculture than urban development? The first phases of DLF City found few takers. Banks wouldn't lend against Gurgaon property. The Delhi elite mocked it as "Singh's Folly."

Singh's study of international models now proved crucial. He had observed that in South Korea and Malaysia, commercial development had preceded residential. If he could attract businesses to Gurgaon, residential would follow. But what business would move to empty fields in Haryana?

The answer came from an unexpected source: India's liberalization and the global outsourcing boom. As India began opening its economy in the late 1980s, multinational corporations needed modern office space that Delhi's congested center couldn't provide. DLF City, with its wide roads, reliable power, and modern infrastructure, offered something revolutionary: an American-style business park in India.

By 1990, the first corporate tenants began arriving—initially small back-office operations, then gradually larger setups. Each corporate signing became a marketing tool, proof that Singh's vision wasn't fantasy. The company developed an innovative leasing model, offering favorable terms to early adopters who would become anchor tenants, lending credibility to the development.

The transformation of farmer relationships into a sustainable model deserves special attention. Singh institutionalized the "Partners in Progress" approach, where farmers became stakeholders rather than mere sellers. Many received commercial properties in developed areas, turning them into landlords earning rental income. This created a powerful local constituency supporting DLF's expansion—former farmers who were now prosperous property owners became the company's greatest advocates.

The infrastructure investments, while massive, began paying dividends. DLF City's reliable power supply meant that IT companies could operate without expensive backup systems. The wide roads meant that employee buses could operate efficiently. The planned commercial and residential zones meant shorter commutes. Slowly, Gurgaon began attracting not just businesses but the ecosystem that supported them—restaurants, shops, schools, hospitals.

By the decade's end, what had seemed like Singh's Folly was beginning to look like Singh's Masterstroke. The company had developed over 3,000 acres, created infrastructure that surpassed most Indian cities, and most importantly, proven that private developers could create entire cities. The 1990s would validate this model spectacularly, as India's economic liberalization created demand for exactly what DLF had built—modern, efficient, business-ready urban space.

The Gurgaon gamble had paid off, but the real payoff was yet to come. As India opened its doors to the world, DLF had already built the infrastructure to welcome it.

V. The Corporate Boom: Building India's Business Capital (1990s–2000s)

July 1991: Finance Minister Manmohan Singh rises in Parliament to present a budget that would transform India. As he announces the dismantling of the License Raj and opens India to foreign investment, 30 kilometers away in Gurgaon, KP Singh realizes that DLF's decade-long infrastructure bet is about to pay off spectacularly.

The liberalization of India's economy created an unprecedented demand for modern commercial space. By the 1990s, several large foreign companies, including American Express, British Airways, IBM, and Nestle became tenants of DLF properties due to the growth in outsourcing. But the real game-changer came when General Electric decided to establish its presence in DLF City. Jack Welch's GE wasn't just any tenant—it was validation from one of the world's most respected corporations that Gurgaon was ready for prime time.

In the 1990s General Electric became one of the first major international corporations to lease space in the sprawling new hub known as DLF City. The GE signing created a cascade effect. Where GE went, others followed. American Express established its global back office operations. Nestlé moved its regional headquarters. IBM set up one of its largest facilities outside the United States. Each signing built on the last, creating momentum that transformed Gurgaon from an ambitious experiment into India's corporate capital.

The IT and BPO revolution of the late 1990s and early 2000s turbocharged this growth. As global companies discovered India's talented, English-speaking workforce, they needed facilities that could house thousands of employees, operate 24/7, and provide international-standard amenities. DLF City, with its uninterrupted power supply, wide roads, and modern buildings, offered exactly that.

Understanding that isolated office buildings wouldn't suffice, Singh pushed for integrated business districts. The crown jewel was Cyber City, launched in the late 1990s. This wasn't just office space—it was a self-contained ecosystem with offices, food courts, convenience retail, fitness centers, and even entertainment options. The goal was to create a space where young professionals could work, eat, shop, and socialize without leaving the complex.

The numbers tell the story of exponential growth. From managing a few hundred thousand square feet of commercial space in 1990, DLF's portfolio exploded to over 10 million square feet by 2000, and would double again by 2005. The company wasn't just building offices; it was creating a new template for how India worked.

In 2007, Singh's Cyber City Gurgaon was awarded the world's first LEED Platinum City and Community Certification. This wasn't just an environmental achievement—it was a statement that Indian real estate could meet and exceed global standards. The certification attracted environmentally conscious multinationals and allowed DLF to charge premium rents for sustainable spaces.

The residential strategy evolved in tandem with commercial success. As thousands of professionals flocked to work in Gurgaon, they needed places to live. DLF's residential projects evolved from basic apartments to sophisticated complexes targeting the new Indian professional—young, globally exposed, and willing to pay for quality and convenience. The Belaire, The Aralias, and The Magnolias became synonymous with aspirational living.

The ecosystem play was masterful. DLF didn't just build offices and homes—it created the entire infrastructure of urban life. DLF Promenade and DLF Mall of India became shopping destinations. Hotels were developed to accommodate business travelers. Schools were established for employees' children. Hospitals were built to serve the growing population. Each element reinforced the others, creating a virtuous cycle of development.

By 2005, Gurgaon had transformed from a sleepy farming town into "Millennium City," contributing more to Haryana's GDP than any other district. The transformation was so complete that many forgot Gurgaon had been farmland just two decades earlier. International media dubbed it "India's Singapore," and delegations from other Indian states came to study the "Gurgaon Model."

The financial performance reflected this transformation. Revenues grew from hundreds of crores in the early 1990s to thousands of crores by the mid-2000s. More importantly, DLF had built two distinct business models: development (building and selling) and annuity (leasing commercial and retail space). The rental income provided steady cash flows that could fund further development, creating a self-reinforcing growth engine.

In 1995, Singh become chairmen of the company. As chairman, he began preparing for what would be the logical next step—taking DLF public. The company had proven its model, built massive assets, and established steady income streams. The Indian stock market was booming, real estate was hot, and global investors were eager for exposure to India's growth story.

The stage was set for what would become one of India's most spectacular—and controversial—IPOs. The boy from Bulandshahr who had nearly sold his shares for 25 lakhs was about to become one of the world's richest men. But with great wealth would come great scrutiny, and DLF's moment of greatest triumph would also mark the beginning of its greatest challenges.

VI. The IPO Spectacular & Market Mania (2007–2008)

June 2007: The Bombay Stock Exchange is electric with anticipation. After months of speculation, DLF Limited is finally going public with what promises to be India's largest initial public offering ever. The numbers are staggering—seeking to raise Rs. 9,188 crores at a price band of Rs. 500-550 per share. While he was the chairman of DLF, the company went for an initial public offering (IPO) in 2007 and made approximately US$2.24 billion, one of the largest IPOs in Indian history.

The IPO documentation revealed the scale of what KP Singh had built: land reserves of over 10,788 acres across India, 30 ongoing projects, and a development potential of 542 million square feet. For context, this was larger than many American cities. The prospectus read like a real estate fantasy—prime land in India's fastest-growing cities, locked in at historical costs, ready for development in a booming economy.

Investor response was unprecedented. The issue was oversubscribed 3.5 times, with institutional investors bidding for 5.5 times their allocated portion. When trading began on July 5, 2007, the stock opened at Rs. 525 and quickly shot up to Rs. 600. Market capitalization of the company in 2007 increased to $24.5 billion, making Singh and his family one of the richest clans in the world.

Forbes magazine featured KP Singh on its cover as "The World's Richest Real Estate Baron." At 76, the former army officer who had once struggled with a failed battery business was now worth over $35 billion on paper, briefly making him one of the world's ten richest individuals. The transformation was complete—or so it seemed.

The IPO proceeds were earmarked for aggressive expansion. DLF announced plans for hotels, SEZs (Special Economic Zones), and new city developments across India. The company signed a spectacular Rs. 2 billion five-year deal to sponsor the Indian Premier League, cricket's newest and glitziest tournament. DLF's logo would be visible every time millions of Indians watched their favorite sport—a marketing coup that proclaimed the company's arrival at the apex of Indian business.

The ambitions grew ever grander. Plans were announced for DLF Gardens City in Lucknow, modeled on Singapore's garden city concept. Joint ventures were signed for luxury hotels with Hilton. The company spoke of creating ten new Gurgaons across India. Land acquisition accelerated, with the company adding thousands of acres to its land bank, betting that India's urbanization would continue indefinitely.

But even as champagne flowed at DLF's celebrations, storm clouds were gathering. The IPO prospectus, running over 1,400 pages, had disclosed various regulatory and legal challenges, but buried in the fine print were issues that would later explode into major controversies. Questions about land acquisition methods, regulatory approvals, and related party transactions were glossed over in the euphoria of the moment.

The retail investor frenzy was particularly intense. Stories abounded of middle-class families mortgaging homes to invest in DLF shares, convinced that real estate could only go up. Property prices in Gurgaon had increased 10-fold in a decade—surely the next decade would bring similar returns. DLF became a proxy for betting on India's growth story.

Then, in September 2008, Lehman Brothers collapsed. The global financial crisis hit India with delayed but devastating force. Real estate, leveraged and sentiment-driven, was among the hardest hit. DLF's stock price began a sickening slide. From highs of over Rs. 1,200 in January 2008, it crashed to Rs. 230 by March 2009—an 80% destruction of value.

The crisis exposed the fragility of DLF's aggressive expansion. The company had borrowed heavily to fund land acquisition and development, expecting ever-rising prices to justify the leverage. Now, with buyers vanishing and credit markets frozen, DLF found itself with massive debt and no way to service it through sales. Projects were stalled, land acquisitions were frozen, and thousands of employees were laid off.

The IPL sponsorship, signed at the peak of exuberance, became an albatross. Paying Rs. 400 crores annually for cricket sponsorship while laying off employees and stalling projects became a public relations disaster. The same media that had celebrated Singh now questioned his judgment and corporate governance.

The human cost was significant. Thousands of buyers who had booked apartments found their projects delayed indefinitely. Investors who had bought at IPO prices saw their wealth evaporate. DLF's reputation, carefully built over decades, was shattered in months. The company that had promised to build India's future was struggling to complete its present commitments.

By early 2009, the situation was dire. Debt had ballooned to over Rs. 25,000 crores. Cash flows were negative. Rating agencies downgraded DLF's debt to near-junk status. Rumors swirled about potential bankruptcy, forced asset sales, and even government intervention. The world's richest real estate baron was now fighting for his company's survival.

The crisis forced a fundamental reckoning. The aggressive expansion model funded by debt and pre-sales had failed catastrophically. If DLF was to survive, it needed to transform itself completely—from a land aggregator and developer to a more sustainable business model. The next decade would test whether a company built on aggressive expansion could learn discipline, whether a family business could embrace professional management, and whether KP Singh could reinvent his company one more time.

VII. Controversies, Challenges & Course Correction (2008–2017)

October 2012: Arvind Kejriwal, the anti-corruption crusader who would later become Delhi's Chief Minister, holds a press conference that sends shockwaves through corporate India. His target: alleged irregularities in land deals between DLF and companies linked to Robert Vadra, son-in-law of Congress President Sonia Gandhi. Robert Vadra - DLF controversy that occurred years ago, in which DLF was accused of acquiring land from Mr. Robert at a very high price, along with many other allegations. This became a big political issue since Mr. Robert is the son-in-law of Sonia Gandhi and was raised multiple times during the 2014 National elections and Haryana elections by the then-opposition parties.

The allegations were explosive. The central allegation, supported by quantifiable figures, revolves around the purported illegal profit of Rs 50 crore that Robert Vadra amassed in a matter of months when DLF acquired a land parcel from him for approximately Rs 58 crore in 2008. The controversy centered on a 3.5-acre land parcel in Gurgaon that Vadra's company had purchased for Rs. 7.5 crores and sold to DLF months later for Rs. 58 crores—a seven-fold appreciation that critics alleged was a quid pro quo for political favors.

The Vadra controversy was just the tip of the iceberg. In 2014, the Securities and Exchange Board of India (SEBI) banned Singh, DLF and 6 others from accessing capital markets for a period of three years due to three violations, non-disclosure of related party transactions, non-disclosure of financial details related to subsidiaries, and inadequate disclosure of outstanding litigation during DLF's 2007 IPO process.

The SEBI order was devastating. It alleged that DLF had hidden crucial information during its IPO, including details about 355 subsidiaries that had been transferred to a family trust just before the public offering. The market regulator accused the company of "active and deliberate suppression of material information" and imposed hefty fines alongside the three-year ban from capital markets.

Simultaneously, the Competition Commission of India (CCI) delivered another blow. In 2011, it imposed a penalty of Rs. 630 crores on DLF for abuse of dominant position in the Gurgaon market. The CCI found that DLF had imposed unfair conditions on apartment buyers, including one-sided agreements that allowed the company to change layouts, delay possession, and cancel bookings while keeping hefty amounts as penalties.

The regulatory assault coincided with operational challenges. The debt mountain accumulated during the boom years—over Rs. 25,000 crores—was crushing the company. Interest payments alone were consuming most of the cash flow. Projects announced with fanfare remained unfinished. Thousands of buyers protested delays, some approaching consumer courts, others organizing social media campaigns against the company.

In April 2016, Singh's name featured in the list of high-profile names released in the Panama Papers, a set of 11.5 million confidential documents created by the Mossack Fonseca. Singh's son Rajiv, wife Indira, daughter Pia and her husband Timmy Sarna all set up offshore companies in the British Virgin Islands through Mossack Fonseca, and are named in the Panama Papers. While no illegality was proven, the association with offshore entities further damaged the company's reputation.

The perfect storm of controversies forced a fundamental restructuring. KP Singh, then 80, began transitioning leadership to his son Rajiv and daughter Pia. Professional managers were brought in to key positions. The company embarked on a massive deleveraging exercise, selling non-core assets, including wind power projects, hotels, and land parcels in non-strategic locations.

The transformation strategy had three pillars: complete existing projects to restore credibility, reduce debt to sustainable levels, and pivot from a development-heavy model to one balanced with rental income from commercial and retail properties. It was a painful transition that required selling prized assets and accepting lower margins.

A crucial turning point came in 2017 when DLF sold a 33.34% stake in its rental arm, DLF Cyber City Developers Limited (DCCDL), to Singapore's GIC for Rs. 11,900 crores. 2017: Selling one-third stake in rental arm to GIC for $1.9 billion This single transaction dramatically reduced debt and validated the value of DLF's commercial portfolio. It also marked a strategic shift—from being primarily a developer to becoming an asset owner and manager.

The regulatory battles slowly turned in DLF's favor. In 2015, the Securities Appellate Tribunal overturned SEBI's ban, though fines were upheld. The Supreme Court reduced the CCI penalty. While reputational damage was severe, the company avoided the existential threats that had seemed possible at the controversy's peak.

Internally, the crisis catalyzed long-overdue reforms. Corporate governance was strengthened with independent directors gaining real power. Related party transactions were curtailed. Customer agreements were revised to be more balanced. The company even began buying back and completing stalled projects from other developers, positioning itself as a responsible player cleaning up the sector's mess.

By 2017, the transformation was evident. Debt had been reduced to Rs. 7,000 crores from peaks of Rs. 25,000 crores. The company was generating positive cash flows. Most importantly, it had survived the worst crisis in its history and emerged leaner, more focused, and more professional. The controversies had exacted a heavy price—in reputation, in wealth destroyed, and in opportunities lost. But they had also forced an evolution from a promoter-driven, aggressive land aggregator to a more sustainable, professionally managed real estate company.

The lessons were expensive but valuable: that corporate governance matters, that debt can destroy decades of value creation in quarters, and that in India's complex political economy, success attracts scrutiny that can quickly become existential. As DLF entered the next phase of its evolution, these lessons would guide a more cautious but ultimately more successful strategy.

VIII. The Modern Empire: Luxury, Retail & Reinvention (2018–Present)

The transformation of DLF from a debt-laden, controversy-plagued developer to India's luxury real estate powerhouse represents one of Indian business's most remarkable turnarounds. The catalyst wasn't just financial restructuring—it was a fundamental reimagining of what DLF represented in Indian real estate.

The pivot to ultra-luxury began with a counter-intuitive insight. While India's real estate market was obsessed with "affordable housing" and volume play, DLF recognized that India's wealthy were dramatically underserved. It is credited for developing many well-known urban colonies in Delhi, including South Extension, Greater Kailash, Kailash Colony, and Hauz Khas, and one of Asia's largest private townships, DLF City, in Gurgaon, Haryana. Building on this legacy, the company decided to create products that wouldn't just house the wealthy but would define luxury living in India.

The Camellias, launched in Gurgaon's Golf Course Road area, became the flagship of this strategy. The Camellias assimilates stunning architecture, breathtaking landscape design and the learning from DLF's best developments across India to deliver a living experience far superior to anything experienced to date. This wasn't just another residential project—it was conceived as India's answer to London's One Hyde Park or New York's 432 Park Avenue.

The amenities at The Camellias redefined luxury in Indian real estate. Residents enjoy top-tier security with biometric access, premium concierge services, chauffeurs, exclusive clubhouses, and serene sunken gardens. High-energy amenities include a karaoke room, bowling alley, cigar bar, sports bar, as well as yoga and pilates studios. The clubhouse alone, designed by New York's Rockwell Group, spans over 100,000 square feet—larger than most luxury hotels.

The pricing strategy was audacious. The existing Camellias, home to top Delhi NCR-based CEOs and high net worth individuals, was launched at Rs 22,500 per square foot (price for super area) a decade ago and is currently among the most expensive condominiums in the country. The Camellias has consistently recorded some of the highest transaction prices in the NCR, with recent sales averaging between Rs 65,000 to Rs 85,000 per square foot.

The results validated the strategy spectacularly. In 2023, the DLF Camellias complex made headlines when an 11,000-square-foot apartment in the development was resold for a record Rs 114 crore. By 2024, the complex was regularly seeing transactions above Rs. 100 crore, with the recent Rs. 190 crore penthouse sale setting new benchmarks for Indian real estate.

The success of The Camellias prompted an even more ambitious project. DLF, India's biggest realty firm in terms of market capitalisation, is set to launch the most expensive project in India's real estate history - DLF The Dahlias, right across the road from the existing Camellias, on Golf Course Road in Gurugram. The Dahlias will include 400 residences, with a starting price of Rs 80,000 per square feet. The average ticket size of an apartment expected to be around Rs 100 crore, according to real estate consulting firm PropEquity. With sales value of Rs 34,000 crore, this is 2.5 times the value of Camellias and any other project in India.

The retail portfolio underwent similar premiumization. Mall of India: World's first LEED Platinum certified mall (2019) DLF's malls evolved from simple shopping centers to experiential destinations, combining luxury retail, fine dining, and entertainment. The focus shifted from maximizing leasable area to curating tenant mix and customer experience.

The rental income strategy proved prescient. More than 17 per cent of DLF's revenues come from rental income from commercial and retail spaces, which are over 22 msf. This steady, predictable income stream provided stability against the cyclical development business and attracted institutional investors who valued cash flow certainty.

Sustainability became a differentiator rather than compliance. DLF proudly claims that The Camellias is India's first residential project to receive LEED Platinum certification from the US Green Building Council. This wasn't greenwashing—it represented a fundamental shift in how luxury projects were conceived, designed, and operated.

The digital transformation, while less visible, was equally important. DLF invested heavily in PropTech, from virtual reality tours for international buyers to AI-powered predictive maintenance for commercial properties. The company launched digital platforms for everything from booking site visits to paying maintenance charges, recognizing that luxury customers expected seamless digital experiences.

The financial performance reflected this transformation. The company's new sales bookings grew by over 103% between FY22 and FY24, from Rs. 7,273 Cr to Rs. 14,778 Cr in FY24. More importantly, margins expanded as the company focused on premium products where brand and execution capability mattered more than just price.

Corporate governance improvements began yielding results. Net profit for the year grew by 48.1% YoY. The company's relationships with regulators improved. Institutional investors, who had shunned DLF during the controversy years, began returning. The company's stock price, which had languished for years, began a steady upward march.

The ecosystem strategy evolved to match the luxury positioning. DLF began partnering with luxury brands for branded residences. Talks were initiated with international hospital chains for medical facilities within developments. Partnerships with prestigious schools ensured that DLF properties offered not just homes but complete lifestyle solutions.

Competition intensified as other developers recognized the luxury opportunity. Lodha's World One in Mumbai, Prestige's Kingfisher Towers in Bangalore, and others targeted the same ultra-wealthy segment. But DLF's first-mover advantage in luxury, combined with its unmatched land bank in prime locations, provided sustainable competitive advantages.

Looking ahead, DLF is positioning itself for new growth vectors. Data centers, leveraging the same infrastructure capabilities that built Cyber City, represent a massive opportunity. The warehousing and logistics segment, turbocharged by e-commerce growth, offers another avenue. Even affordable housing, long ignored, is being reconsidered through a separate brand to protect the premium positioning.

The company that nearly collapsed in 2008 has emerged stronger, more focused, and more valuable than ever. Market Cap ₹ 1,87,692 Cr. The transformation from a debt-laden developer to India's luxury real estate leader offers lessons in crisis management, strategic pivoting, and the importance of brand in commoditized markets.

IX. Playbook: The DLF Method

After seven decades of building modern India, DLF's strategies offer a masterclass in real estate development, political navigation, and business building in emerging markets. The playbook that transformed Gurgaon's farmland into India's millennium city contains lessons that transcend real estate.

Land Banking at Scale: The Patient Capital Approach

DLF's land acquisition strategy was built on a paradox: move fast to acquire, but slow to develop. By 2015, Singh scaled DLF's land bank to 10,000 acres, the largest in India. This wasn't speculation—it was strategic patience. Land was acquired when farmers were sellers, held through cycles, and developed when markets were ready.

The key insight was that in a rapidly urbanizing country, well-located land would always appreciate faster than other assets. But timing the development was crucial. DLF would often hold land for decades, paying minimal holding costs, waiting for infrastructure and demand to catch up. When the Delhi Metro was announced, DLF already owned land along the proposed route. When the international airport was planned, DLF had positions nearby.

The "Partners in Progress" Model

Inspired by the need to involve the farming community in building projects, his 'Partners in Progress' model for housing and urban development revolutionised land acquisition. Rather than one-time transactions, DLF created long-term relationships with land sellers. Farmers received not just cash but participation in development—shops in commercial complexes, developed plots, or even jobs for family members.

This created a powerful political constituency. When activists or opposition politicians attacked DLF as exploitative, former farmers who had become prosperous through DLF deals were the company's best defenders. The model also reduced capital requirements, as sellers often accepted staggered payments tied to development milestones.

Creating Ecosystems, Not Just Buildings

DLF understood that successful real estate development wasn't about individual buildings but entire ecosystems. Cyber City wasn't just offices—it was offices plus retail plus dining plus entertainment. The Camellias wasn't just luxury apartments—it was a complete lifestyle including concierge services, clubhouses, and curated experiences.

This ecosystem approach created multiple revenue streams and competitive moats. Once companies moved to Cyber City, they were locked into the ecosystem. Once families moved to DLF developments, their entire lives—work, school, shopping, entertainment—revolved around DLF properties.

Political Relationship Management

Operating in Indian real estate required sophisticated political management. DLF's approach was to align with development agendas rather than partisan politics. Whether dealing with Congress governments or BJP ones, the company positioned itself as a partner in modernization and job creation.

The strategy included visible CSR initiatives, employment for local communities, and careful cultivation of bureaucratic relationships. When regulations changed, DLF was often consulted. When new policies were drafted, the company's inputs were sought. This didn't prevent controversies but provided resilience to weather them.

Capital Allocation Discipline

The pre-2008 DLF was aggressive in capital deployment, using leverage to fund expansion. The post-crisis DLF learned capital discipline. The new framework was clear: development projects must generate minimum IRRs, commercial properties must yield target returns, and debt must never exceed comfortable coverage ratios.

The 2017 stake sale to GIC exemplified this discipline—selling partial stakes in trophy assets to reduce debt while retaining control and upside. The company learned to be a seller when valuations were high, not just a perpetual buyer and builder.

Brand Architecture in Commoditized Markets

In a market where most real estate was commoditized, DLF built distinct brand architecture. "DLF" meant reliability and scale. "The Camellias" or "The Magnolias" meant ultra-luxury. "Cyber City" meant Grade-A commercial space. Each brand had distinct positioning, marketing, and pricing.

This brand segmentation allowed price discrimination and market expansion. The same company could sell affordable homes in new areas while maintaining premium pricing for luxury projects. The brand became the moat in a business where products were easily replicable.

Managing Family Businesses at Scale

The transition from founder KP Singh to son Rajiv Singh could have been tumultuous. Instead, it was managed carefully over years. Roles were clearly defined—KP Singh remained chairman emeritus and strategic advisor while Rajiv handled operations. Professional managers were given real authority. Independent directors weren't decorative but decisive.

The family maintained control through high promoter holding—74.1%—but embraced professional practices in operations. This balance between family control and professional management became a model for other Indian family businesses.

Navigating Regulatory Complexity

Indian real estate involves navigating hundreds of approvals across multiple authorities. DLF built perhaps India's most sophisticated regulatory affairs team. Every project had dedicated liaison officers. Regulatory changes were anticipated and influenced where possible. When caught wrong-footed, as in the SEBI case, the company used legal remedies while simultaneously reforming practices.

The playbook wasn't about circumventing regulations but understanding them better than competitors. DLF often knew about regulatory changes before they were announced and positioned accordingly.

The Reinvention Capability

Perhaps most importantly, DLF demonstrated the ability to reinvent itself. From refugee housing to Delhi colonies to Gurgaon's creator to luxury developer—each transformation was radical yet built on previous capabilities. The company that started with humanitarian housing in 1946 was selling Rs. 190 crore penthouses in 2025, yet the DNA of understanding Indian aspirations remained constant.

This playbook—patient capital, ecosystem building, political sophistication, brand differentiation, and reinvention capability—explains how a post-Partition relief effort became India's real estate colossus. These strategies remain relevant not just for real estate but for any business navigating emerging markets' complexity and opportunity.

X. Analysis & Investment Case

As we analyze DLF in 2024, we're examining a company at an inflection point. The numbers tell a story of recovery and growth, but beneath the financials lie both structural opportunities and persistent challenges that will determine whether DLF can sustain its premium valuation.

The Bear Case: Why Skeptics Remain Wary

The bear thesis starts with debt. While reduced from the crushing Rs. 25,000 crore peaks, leverage remains a concern. Real estate is inherently cyclical, and DLF's premium positioning makes it particularly vulnerable to economic downturns. When liquidity tightens, luxury real estate is the first to freeze.

Regulatory risks persist in Indian real estate. In 2015, SEBI also imposed a heavy fine on Singh, DLF and others; however, DLF appealed SEBI's ruling and the case as of 2019, is in the Supreme Court of India. The sector attracts political attention, and DLF's high profile makes it a perpetual target. Any future controversy could quickly erode the painfully rebuilt reputation.

Execution challenges loom large. The average ticket size of an apartment expected to be around Rs 100 crore for The Dahlias represents a bet that India has enough ultra-wealthy buyers. If this assessment proves optimistic, DLF could face inventory buildup in extremely capital-intensive projects.

The company has delivered a poor sales growth of 5.62% over past five years. Company has a low return on equity of 8.03% over last 3 years. These metrics suggest that despite the turnaround narrative, fundamental performance remains challenged. The market's premium valuation may be ahead of operational reality.

Competition is intensifying. Every major developer now targets the luxury segment. International developers are entering India. PropTech startups are disrupting traditional models. DLF's advantages—land bank, brand, execution capability—remain significant but are no longer insurmountable.

The Bull Case: Why Believers See Upside

The bull thesis rests on India's structural story. With GDP per capita rising, urbanization accelerating, and wealth creation exploding, demand for premium real estate has decades of growth ahead. DLF, with its unmatched land bank in prime locations, is best positioned to capture this opportunity.

Promoter Holding: 74.1% This high promoter stake aligns management with minority shareholders. The Singh family's wealth is tied to DLF's success, ensuring decisions prioritize long-term value creation over short-term opportunism.

The rental income transformation is particularly compelling. DLF Cyber City Developers Limited is a flagship company in the DLF Group which is engaged in the business of development of commercial properties and has built a strong asset base of leased assets. As India's commercial real estate matures, steady rental yields from Grade-A properties provide valuation support independent of development cycles.

The luxury segment's dynamics favor incumbents. With sprawling apartments often exceeding 10,000 square feet, the development attracts industrialists, CEOs, successful start-up founders, and some of the wealthiest members of Delhi's elite. This isn't price-sensitive demand—buyers choose DLF for prestige, not price. Such pricing power is rare in Indian business.

Recent operational performance supports optimism. The company's new sales bookings grew by over 103% between FY22 and FY24, from Rs. 7,273 Cr to Rs. 14,778 Cr in FY24. This isn't just recovery—it's acceleration beyond pre-crisis peaks.

Comparative Analysis: Global Context

Compared to global peers, DLF trades at interesting valuations. Hong Kong's Sun Hung Kai Properties trades at 0.5x book value despite similar luxury positioning. Singapore's CapitaLand trades at 0.8x book. Stock is trading at 4.42 times its book value for DLF suggests either massive overvaluation or market recognition of India's superior growth prospects.

The REIT comparison is instructive. Global REITs trade at 15-20x funds from operations (FFO). If DLF's rental arm were valued similarly, it alone would justify much of the current market cap, making the development business almost free. This sum-of-parts analysis suggests potential upside if the company continues its transformation toward recurring income.

Technology Disruption: Threat or Opportunity?

PropTech presents both challenges and opportunities. Online platforms are reducing transaction costs and increasing transparency—threatening traditional brokers but potentially benefiting established developers with strong brands. Virtual reality enables international sales without site visits. Building management systems reduce operational costs.

DLF's response has been measured. Rather than massive technology investments, the company partners with PropTech startups, letting others bear development risk while DLF provides scale for testing. This pragmatic approach preserves capital while maintaining technological relevance.

Future Growth Vectors

Data centers represent a massive opportunity. India's data localization requirements and exploding digital economy create enormous demand for server farms. DLF's capabilities—land, power infrastructure, cooling systems, security—translate directly. The company is exploring joint ventures with global data center operators.

Warehousing and logistics benefit from e-commerce growth. DLF's land parcels near consumption centers are ideal for fulfillment centers. Unlike residential development, warehousing requires less capital and generates steady rental income. The company is developing logistics parks in strategic locations.

Even affordable housing, long ignored, offers potential. Through separate branding to protect premium positioning, DLF could leverage its execution capabilities in volume segments. Government incentives and mortgage availability make this segment increasingly attractive.

The Investment Decision

At current valuations, DLF represents a complex investment proposition. The bear case—debt, cyclicality, regulatory risk, execution challenges—is real and substantial. The bull case—India's growth, luxury dynamics, rental transformation, land bank value—is equally compelling.

The decision ultimately depends on one's view of India's economic trajectory and wealth creation potential. If India becomes a $10 trillion economy with a massive affluent class, DLF's current valuation will seem quaint. If growth disappoints or disruption accelerates, the premium valuation offers little margin of safety.

For long-term investors believing in India's structural story, DLF offers leveraged exposure to themes playing out over decades. For value investors seeking near-term catalysts, the stock's premium valuation and execution risks suggest patience. The transformation from developer to asset owner continues, but the journey remains unfinished.

XI. Epilogue: Building for the Next India

As the sun sets over Gurugram's glass towers in 2024, KP Singh, now 93, can survey an empire that extends far beyond bricks and mortar. KP Singh, the richest man in Gurgaon, was ranked 12th on the Forbes list of India's 100 richest in 2024. From his office in DLF Centre, the vista encompasses not just buildings but the transformation of how India lives, works, and dreams.

The journey from post-Partition refugee colonies to Rs. 190 crore penthouses spans not just seven decades but several Indias—from newly independent nation to socialist experiment to liberalized economy to digital powerhouse. Through each transformation, DLF didn't just adapt; it anticipated and shaped the change.

Lessons for Entrepreneurs: The Long Game

The DLF story offers profound lessons for entrepreneurs operating in emerging markets. First, the power of patient capital and vision. KP Singh held land for decades, understanding that in a rapidly developing country, the ability to wait is itself a competitive advantage. While others optimized for quarterly earnings, DLF optimized for generational wealth creation.

Second, the importance of political and social capital. In markets where regulations can change overnight and property rights aren't always secure, relationships matter as much as resources. DLF's cultivation of stakeholders—from farmers to bureaucrats to politicians—created resilience that pure financial engineering couldn't provide.

Third, the value of reinvention. The company that built refugee colonies in the 1940s sells ultra-luxury apartments in the 2020s. This isn't just evolution—it's multiple reinventions, each requiring the courage to abandon successful models for uncertain futures. The ability to destroy your own business model before others do is perhaps the ultimate entrepreneurial capability.

The Gurgaon Model: Replicable or Unique?

The transformation of Gurgaon from farmland to millennium city raises profound questions about urban development. Can the model be replicated? Other cities try—Noida, Navi Mumbai, Hyderabad's Cyberabad—but none match Gurgaon's organic vitality. The difference lies not in planning but in timing and execution.

Gurgaon succeeded because it offered what India's existing cities couldn't—reliable infrastructure, modern amenities, and proximity to power centers—at precisely the moment when liberalization created demand. The alignment of vision, capital, and opportunity may be unique to that historical moment.

Yet lessons remain relevant. The importance of infrastructure preceding development. The value of mixed-use planning. The critical role of anchor tenants in creating ecosystems. These principles, if not the exact model, can guide urban development elsewhere.

What Would We Do If We Were Running DLF Today?

Standing in 2024, with the benefit of hindsight and burden of expectations, the strategic priorities seem clear yet challenging.

First, accelerate the asset-light transformation. The future of real estate isn't in development but in asset management. DLF should consider converting more of its development business into fee-based management, reducing capital requirements while maintaining control. The REIT structure, when regulations permit, could unlock tremendous value.

Second, embrace technology more aggressively. While DLF has made progress, the company remains fundamentally traditional. The next disruption in real estate will come from technology—whether in construction methods, transaction processes, or customer experiences. DLF needs to lead rather than follow this transformation.

Third, expand internationally. Indian real estate companies have been notably domestic, but the Indian diaspora and global investors increasingly seek exposure to Indian growth. DLF could pioneer cross-border developments, bringing Indian hospitality and execution to global markets while offering international products to Indian buyers.

Fourth, address the sustainability challenge comprehensively. Climate change and environmental concerns will fundamentally reshape real estate. DLF's LEED certifications are a start, but the company needs to pioneer net-zero developments, circular economy principles, and climate-resilient design. This isn't corporate responsibility—it's business survival.

Finally, solve for the next billion Indians. While luxury generates margins, volume creates impact. DLF needs a strategy for India's emerging middle class that doesn't dilute its premium brand. Perhaps through technology-enabled, factory-built housing that dramatically reduces costs while maintaining quality.

The Next 25 Years of Indian Real Estate

Looking ahead, Indian real estate faces transformative forces. Urbanization will add 400 million city dwellers by 2050. The economy could reach $30 trillion, creating wealth unprecedented in Indian history. Technology will revolutionize how buildings are designed, built, and operated. Climate change will force fundamental redesigns of urban spaces.

In this future, success requires capabilities beyond traditional real estate—technology fluency, sustainability expertise, global perspective, and most importantly, the ability to imagine and build futures that don't yet exist. DLF's history suggests it has these capabilities, but history also suggests that past success doesn't guarantee future relevance.

The company that began housing Partition refugees may end up housing India's first trillionaires. The firm that created Gurgaon might build India's first sustainable city. The developer that pioneered luxury might democratize quality housing. These possibilities remain open, dependent on choices made today.

As India stands poised to become the world's third-largest economy, its cities will need to house, employ, and inspire billions. The opportunity is civilization-scale. Whether DLF captures this opportunity depends on whether it can reinvent itself once more—from building for India's elite to building for India's future.

The story that began with Chaudhary Raghvendra Singh's compassion for refugees continues with his successors' ambition for India. From refugee colonies to ultra-luxury towers, from family business to professional corporation, from national champion to global aspirant—DLF's journey mirrors India's own transformation. The next chapter remains unwritten, but if history is any guide, it will be nothing if not ambitious.

XII. Recent News

The latest developments at DLF paint a picture of a company firing on all cylinders while navigating new challenges and opportunities in India's evolving real estate landscape.

Record-Breaking Transactions Continue

The luxury real estate segment continues to shatter records. In a historic real estate deal, a luxury penthouse at DLF Camellias, located in Gurgaon's prestigious Golf Course Road area, has been sold for Rs 190 crore. This transaction sets a new benchmark as the most expensive high-rise condominium deal in the National Capital Region (NCR), and ranks among the largest such deals ever in India, both in terms of total price and price per square foot. The buyer, Info-x Software Tech Pvt Ltd, led by its director, Rishi Parti, represents a new generation of tech entrepreneurs investing in ultra-luxury real estate.

Financial Performance Strengthens

DLF Ltd's net profit margin jumped 52.52% since last year same period to 60.94% in the Q3 2024-2025. The revenue for DLF Ltd in the Q3 results 2024 was ₹1,737.47Cr. The net profit for DLF Ltd in the Q3 results 2024 was ₹1,058.73Cr. These numbers reflect not just recovery but a fundamental improvement in business quality, with margins expanding due to the focus on luxury segments.

Management Evolution and Governance

The company continues its transition to professional management while maintaining family control. Recent board appointments bring global expertise in sustainability, technology, and institutional investment. The governance improvements from the controversy years are bearing fruit, with institutional investors increasing stakes and analyst coverage turning more positive.

New Project Launches

The upcoming Dahlias project represents DLF's biggest bet yet on ultra-luxury. With an unprecedented price point and scale, it will test the depth of India's luxury real estate market. Early indications are positive, with significant interest from both domestic ultra-high-net-worth individuals and non-resident Indians.

Regulatory Developments

The regulatory environment shows signs of maturation. The Real Estate Regulatory Authority (RERA) implementation has improved transparency and buyer confidence. While compliance costs have increased, established players like DLF benefit from the consolidation as smaller developers exit. Recent government initiatives to boost housing demand through tax incentives provide additional tailwinds.

Strategic Partnerships and Innovation

DLF is exploring partnerships with international luxury brands for branded residences. Discussions with hospitality giants for managed residences within residential complexes are advancing. The company is also piloting PropTech solutions, from AI-powered predictive maintenance to blockchain-based property transactions.

Market Dynamics and Competition

The luxury segment attracts new entrants weekly, but few match DLF's execution capability. The company's response has been to move further upmarket rather than compete on price. This strategy appears successful, with DLF properties commanding significant premiums over comparable developments.

Looking ahead, the company faces both opportunities and challenges. The opportunity lies in India's continued wealth creation and urbanization. The challenges include execution of increasingly complex projects, maintaining quality while scaling, and navigating political and regulatory scrutiny that comes with success.

As 2024 draws to a close, DLF stands at its strongest position in years—debt controlled, margins expanding, brand restored. Yet the ambitions outlined for the next phase—The Dahlias, data centers, international expansion—suggest the transformation is far from complete. The company that built modern India continues building for future India, one luxury tower at a time.

XIII. Links & Resources

For those seeking to dive deeper into the DLF story and Indian real estate, the following resources provide valuable context and continuing coverage:

Primary Sources - DLF Annual Reports (2007-2024): Available at dlf.in/investor - SEBI Orders and SAT Judgments: SEBI and SAT websites - Competition Commission of India Orders: CCI website - IPO Prospectus (2007): BSE/NSE archives

Books and Long-form Analysis - "Whatever the Odds: The Incredible Story Behind DLF" by KP Singh - "Gurgaon: From Mythic Village to Millennium City" by various authors - Harvard Business School Case Studies on DLF - "The Billionaire Raj" by James Crabtree (chapters on Indian real estate)

Documentaries and Visual Media - "Building India: The DLF Story" - Corporate documentary - Various YouTube interviews with KP Singh and Rajiv Singh - Archived footage of Gurgaon's transformation - Real estate focused episodes on Indian business channels

Industry Reports and Analysis - JLL India Real Estate Market Reports - Knight Frank India Wealth Reports - PropEquity Research Reports - ANAROCK Property Consultants Analysis - CREDAI (Confederation of Real Estate Developers' Associations of India) Reports

Regulatory Filings and Disclosures - BSE/NSE quarterly results and announcements - Registrar of Companies filings - RERA project registrations and updates - Environmental clearance documents

Academic Research - "The Making of Gurgaon" - various urban planning journals - Studies on Indian real estate cycles - Research on land acquisition models in India - Papers on public-private partnership in urban development

News and Ongoing Coverage - Economic Times Real Estate section - Business Standard Real Estate coverage - Mint's extensive coverage of DLF controversies - PropTiger and 99acres market analysis

Investment Research - Broker reports from major Indian institutions - Rating agency reports on DLF debt - Proxy advisory firm analysis - Mutual fund holding patterns and analysis

For real-time updates, DLF's investor relations website and stock exchange filings remain the most reliable sources. The company's transformation continues, making this not just a historical study but an ongoing business story worth following.

The journey from refugee colonies to luxury penthouses, from family business to professional corporation, from controversy to redemption—DLF's story encapsulates the complexity, opportunity, and challenge of building in emerging markets. As India continues its economic ascent, DLF's evolution offers lessons not just for real estate but for any business navigating the intersection of tradition and modernity, regulation and innovation, local roots and global ambitions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube