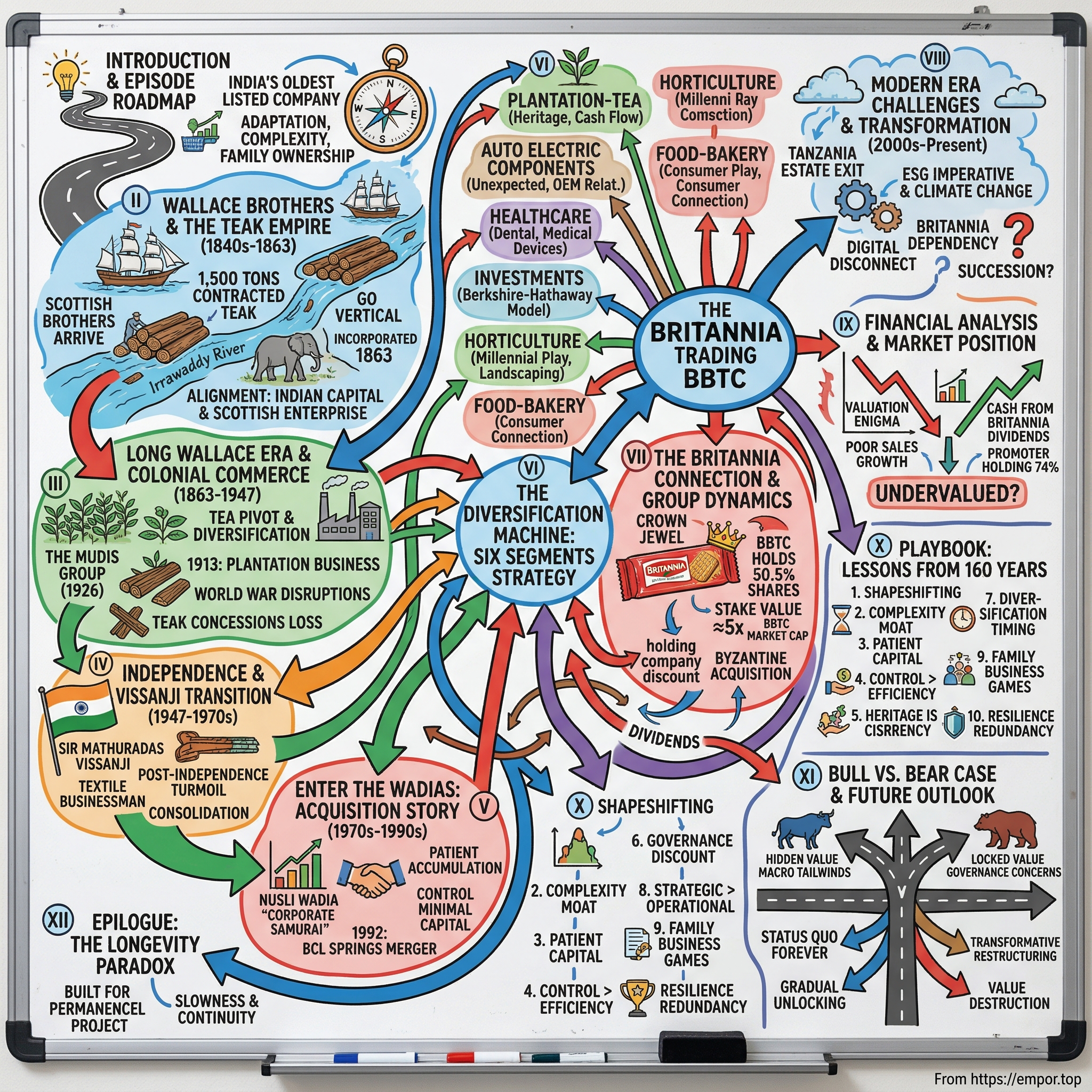

Bombay Burmah Trading Corporation: From Teak to Conglomerate - India's Oldest Listed Company

I. Introduction & Episode Roadmap

Picture this: It's 1863, the American Civil War rages across the Atlantic, Japan's Meiji Restoration is five years away, and in colonial Bombay, six Scottish brothers are about to float what would become India's second-oldest publicly traded company. The Bombay Burmah Trading Corporation—a name that sounds like it belongs in a Somerset Maugham novel—would somehow survive the British Raj, two world wars, Indian independence, socialist economics, and market liberalization to stand today as a ₹13,000+ crore conglomerate.

Here's the puzzle that keeps us up at night: How does a company that started by floating teak logs down Burmese rivers end up manufacturing solenoids for Maruti Suzuki, owning half of Britannia Industries, and running tea plantations across three countries? More importantly, what can modern entrepreneurs learn from a business that has outlived empires, currencies, and entire economic systems?

This isn't just another corporate history. It's a masterclass in adaptation, a case study in conglomerate complexity, and perhaps most fascinatingly, a window into how family-controlled businesses in emerging markets create—or destroy—value across centuries. We're going to unpack how BBTC transformed from a colonial trading house into a diversified industrial group, why it trades at a persistent conglomerate discount despite owning crown jewels like Britannia, and what its 160-year journey teaches us about building enduring businesses.

The themes we'll explore resonate far beyond BBTC: the art of surviving regime changes, the challenge of managing unrelated businesses, the dynamics of family ownership across generations, and the eternal tension between heritage and innovation. Whether you're a founder thinking about your company's next decade or an investor evaluating conglomerates, BBTC's story offers lessons you won't find in any MBA textbook.

II. Wallace Brothers & The Teak Empire (1840s-1863)

The rain hammered Rangoon's docks in 1855 as William Wallace watched elephants drag massive teak logs through the mud. The eldest of six Scottish brothers, William had been sent from Bombay to solve a delivery problem—1,500 tons of contracted teak that threatened to derail their fledgling partnership. But standing there in the monsoon, watching the ancient dance of mahouts and elephants moving timber worth fortunes, William didn't see a problem to solve. He saw an empire to build.

The Wallace brothers—all six of them—had arrived in Bombay in the 1840s from Edinburgh, establishing "Wallace Bros & Co" as a partnership in 1848, and by the mid-1850s had set up operations in Rangoon. They weren't the first Scots to seek fortune in the East, but they brought something different: a combination of merchant acumen, family cohesion, and an almost mystical ability to navigate the treacherous waters between colonial power and local commerce.

The brothers' origin story reads like a Victorian novel. Sons of Edinburgh architect and builder Lewis Alexander Wallace, the six brothers were born between 1818 and 1836. Rather than follow their father into Scottish construction, they looked east to the jewel of the British Empire. The timing was perfect—the expansion of Indian railways created insatiable demand for Burmese teak, prized for its durability and resistance to the subcontinent's punishing climate.

William's fateful trip to oversee that 1,500-ton teak shipment destined for Bombay railway construction opened his eyes to the scale of opportunity in Burma's forests, where the British-controlled southern provinces of Arakan, Pegu and Tenasserim harbored a brisk trade in teak along the Irrawaddy, Sittang and Salween rivers. The numbers were staggering: Between 1857 and 1864, approximately 85,000 tons of teakwood was exported annually from Burma.

But here's where the Wallace brothers showed their genius. Rather than simply acting as middlemen, they decided to go vertical. The partners at Wallace & Co in Bombay viewed William's Upper Burmese concessions as risky—the totalitarian kingdom could rescind contracts on a whim, and tensions with British-ruled southern Burma made large investments financially dangerous. To minimize risk, they floated a new company: The Bombay Burmah Trading Corporation.

The 1863 incorporation was a masterpiece of colonial-era financial engineering. The business was floated as "The Bombay Burmah Trading Corporation" with equity held by both Indian merchants and the Wallace Brothers, who maintained controlling interests. This structure was revolutionary—it brought Indian capital into a Scottish enterprise while maintaining Wallace control, creating alignment between colonial merchants and local financiers.

Think about the audacity of this move. In an era when most British enterprises in India operated as pure extractive operations, the Wallaces created a hybrid structure that would prove remarkably resilient. Indian merchants got access to the lucrative teak trade; the Wallaces got local capital and political cover. It was capitalism with a multicultural twist, decades before anyone coined the term "stakeholder alignment."

By the 1870s, BBTC had become a leading producer of teak in Burma and Siam, with interests expanding into cotton, oil exploration and shipping. The company wasn't just trading timber—it was building an integrated supply chain from forest to port. Until the 1880s, forests were worked by contractors with Wallace doing the financing, marketing and shipping, but after receiving extensive new teak leases from the Burmese King in 1880, Bombay Burmah expanded operations to do timber extraction itself.

The scale of this transformation cannot be overstated. For eighty years, Bombay Burmah would be the single largest teak company in the industry, marketing over a third of the world's teak supplies. They weren't just participating in the market—they were the market.

But the story takes a geopolitical turn that would make modern risk managers shudder. British motivations for the third Anglo-Burmese War were partly influenced by BBTC's concerns, with the Burmese state's conflict with the company furnishing British leaders with a pretext for conquest. By the mid-1880s, French interests had become close to the Burmese King, culminating in court action against Bombay Burmah, which indirectly precipitated the Third Anglo-Burmese War in 1886 and the deposing of the King.

Winston Churchill's father would later call it a "lucky incident"—the contentious claim that gave Great Britain the excuse to invade Upper Burma. For BBTC, it meant their long-term future in Burma was secured under British administration. The exiled King Theebaw would spend his final days in Ratnagiri, south of Bombay, watching through his telescope as ships passed the coast—many likely carrying the teak that had once been his kingdom's treasure.

The financial architecture supporting this empire was equally impressive. Until the 1950s, Wallace Brothers had the power to exercise control over Bombay Burmah's policy and operations, with dividends and staff pay decided in London, and senior European staff selected and appointed there until around 1960. Alexander Wallace had become Chairman of the Commercial Bank of India in 1864, with three of his brothers also serving as directors—Alexander would later become Governor of the Bank of England.

This wasn't just a trading company; it was a node in the global financial system, with tentacles reaching from Edinburgh to London to Bombay to Rangoon to Bangkok. Competition for teak supplies led them to Siam (now Thailand), where Bombay Burmah opened an office in Bangkok in 1884. They were building what we'd now call a "platform business"—controlling the key resource, the logistics, the financing, and increasingly, the political framework within which trade occurred.

The genius of the Wallace brothers wasn't just in recognizing the value of Burmese teak. It was in understanding that in the colonial economy, the real money wasn't in trading commodities—it was in controlling the entire value chain from forest to final customer, and embedding that control within the political and financial architecture of empire. They had created something that would outlast the British Raj itself: a business model so deeply rooted in the economic geography of South and Southeast Asia that it would survive every subsequent upheaval. As we'll see, this foundation would prove both a blessing and a curse as the company navigated from colonial commerce into the complexities of the modern era.

III. The Long Wallace Era & Colonial Commerce (1863-1947)

For 85 years—from 1863 to 1947—the Wallace brothers and their descendants presided over an empire that stretched from London to Bangkok, built on teak but increasingly diversified into what would become a sprawling conglomerate. This wasn't merely business longevity; it was dynasty-building on a scale that would make the Medicis envious.

The real genius of the Wallace era wasn't in maintaining the teak monopoly—though they did that brilliantly—but in recognizing when to pivot. In 1913, the company entered the plantation business, turning their attention to tea estates in South India just as global teak markets were beginning to shift. The timing was prescient: World War I was about to disrupt global trade patterns, and having a domestic Indian agricultural business would prove invaluable.

After learning about suitable areas for tea plantations in South India, they opened their first estates in the Anamallai hills of Coimbatore District in Tamil Nadu, and by 1926 had established "The Mudis Group of estates," which today comprises five estates and four factories with 1,863 hectares. They also founded "The Singampatti Group" in the south, which today has three estates covering 804 hectares with three factories.

Think about the audacity of this diversification. In 1913, Europe was hurtling toward the Great War, colonial economics were about to be fundamentally disrupted, and the Wallaces decided to invest heavily in an entirely new industry requiring massive capital outlays, decades-long cultivation cycles, and expertise in a completely different agricultural product. It was the corporate equivalent of a chess grandmaster positioning pieces for an endgame still decades away.

The tea pivot reveals something profound about colonial-era business strategy. Unlike modern Silicon Valley's "move fast and break things" ethos, the Wallaces thought in generational timescales. Tea plantations take seven years to mature, require massive infrastructure investments in processing facilities, and depend on stable labor forces numbering in the thousands. This wasn't a hedge—it was a second empire.

By the 1920s, BBTC had become something far more complex than a teak trading company. Their plantations in the hills of South India covered 2,822 hectares under tea, located in prime plantation areas producing 8 million kgs of tea annually. They had evolved from resource extractors to agricultural industrialists, managing not just commodities but entire communities of workers, processing facilities, and supply chains.

The social architecture of these plantations was as complex as the business model. Unlike the teak operations which relied on contractors and seasonal labor, tea plantations required permanent settlements, schools, medical facilities, and intricate social hierarchies. The Wallaces weren't just running businesses—they were governing small principalities within the Raj, complete with their own systems of justice, welfare, and social organization.

World War I brought the expected disruptions but also unexpected opportunities. With European markets in chaos and shipping routes compromised, BBTC's diversified portfolio—spanning teak in Burma and Siam, tea in South India, and various trading operations—provided resilience that pure-play competitors lacked. The company's London connections, particularly through Wallace Brothers' position as a leading financial house, enabled them to navigate wartime restrictions and capital controls that destroyed lesser firms.

The interwar period saw BBTC consolidate its position as one of the premier trading houses of the British Empire. But beneath the surface, tectonic shifts were occurring. The rise of Burmese nationalism, Indian independence movements, and changing global economics meant the colonial model was living on borrowed time. The Wallaces, comfortable in their Edinburgh drawing rooms and Bombay clubs, seemed oddly oblivious to these undercurrents.

The Great Depression tested the model but didn't break it. While global trade collapsed and commodity prices plummeted, BBTC's integrated structure—controlling everything from production to shipping to financing—provided buffers that independent operators lacked. They could absorb losses in one division while maintaining cash flow from others, a luxury that would prove critical as the world economy spiraled.

World War II, however, was different. The Japanese invasion of Burma in 1942 was catastrophic for BBTC's core business. Overnight, their teak operations—the foundation upon which everything else had been built—vanished behind enemy lines. Rangoon fell, Bangkok was occupied, and decades of carefully cultivated forest concessions became worthless paper. For a company that had weathered every storm since 1863, this was existential.

Yet somehow, they survived. The tea operations in South India, once a diversification play, became the lifeline. The plantations kept producing, Indian domestic consumption remained stable, and the sterling area's need for dollar-earning exports made tea more valuable than ever. What had begun as a hedge in 1913 had become, by 1945, the company's salvation.

As India moved toward independence in 1947, the Wallace brothers faced a reckoning. The company they had built was fundamentally a creature of empire—Scottish ownership, London control, Indian operations, Burmese resources. In a world of nascent nation-states and economic nationalism, this structure was untenable. The handwriting wasn't just on the wall; it was in Gandhi's speeches and Nehru's economic plans.

The Wallace era ended not with bankruptcy or nationalization but with a negotiated transition—itself a testament to eight decades of relationship-building and political navigation. The sale to the Vissanji family around independence represented both an ending and a beginning: the end of colonial commerce as the Wallaces had known it, and the beginning of BBTC's transformation into an Indian company.

Looking back, the Wallace era's most lasting contribution wasn't the wealth extracted or the tea planted, but the institutional DNA they embedded in BBTC: patience in the face of volatility, diversification as a survival strategy, and the ability to navigate political upheaval while maintaining business continuity. These traits, forged in the crucible of empire, would prove invaluable as BBTC entered its next chapter under Indian ownership in an independent nation.

IV. Independence & The Vissanji Transition (1947-1970s)

On August 15, 1947, as Nehru proclaimed India's "tryst with destiny" from the Red Fort, the fate of a 84-year-old Scottish trading company hung in the balance. The Vissanji family purchased the company from the Wallace brothers around the time of Indian independence, a transaction that represented far more than a simple change of ownership—it was a microcosm of the massive economic realignment happening across the subcontinent.

The Vissanjis weren't strangers to big business. Sir Mathuradas Vissanji (1916-1949) was an Indian businessman and politician, born on 18 March 1916 in Mumbai, who founded the Wallace Mills Company, a family owned textile business. He was the first president of the Cotton Corporation of India and was elected to the Bombay Legislative Assembly in 1935. This was a family that understood both commerce and politics—essential qualifications for navigating the turbulent waters of post-independence India.

The timing of the acquisition was extraordinary. Burma had gained independence in January 1948, effectively ending BBTC's access to its historical teak concessions. The partition of India had disrupted supply chains, created massive refugee movements, and fundamentally altered the business landscape. Socialist rhetoric dominated political discourse, with talk of nationalization sending shivers through boardrooms across Bombay. Yet the Vissanjis saw opportunity where others saw only risk.

Consider what they were buying: a company whose very name—Bombay Burmah—referenced two places undergoing fundamental transformation. Bombay was evolving from colonial port to Indian commercial capital. Burma was no longer accessible. The company's Scottish management structure was an anachronism in Nehru's India. Most rational investors would have run for the hills. The Vissanjis doubled down.

Their strategy was brilliantly counterintuitive. Rather than dismantling the colonial structure, they preserved what worked while adapting to new realities. The tea plantations in South India, which had saved the company during World War II, became the foundation for the future. The Vissanji era would be defined not by expansion but by consolidation—turning a far-flung empire into a focused Indian enterprise.

The challenges were immense. The License Raj, that Byzantine system of permits and quotas that defined Indian economic policy from the 1950s through the 1980s, made every business decision a bureaucratic marathon. Foreign exchange was scarce and strictly controlled. Import substitution policies meant sourcing equipment and technology became increasingly difficult. The very idea of a private company controlling vast plantation lands seemed incompatible with socialist land reform agendas.

Yet BBTC survived, even thrived, during this period. The key was understanding that in post-independence India, business success required more than commercial acumen—it required political navigation skills that would make Machiavelli proud. The Vissanjis had to transform BBTC from a symbol of colonial exploitation into a contributor to national development, all while maintaining profitability in an increasingly controlled economy.

The company's workforce transformation during this period is particularly noteworthy. From a hierarchical structure with European managers and Indian workers, BBTC had to evolve into an Indian company with Indian management. This wasn't just about replacing Scottish supervisors with Indian ones—it required reimagining the entire organizational culture, from the clubs and bungalows of the plantation raj to something more aligned with independent India's egalitarian aspirations.

Labor relations became increasingly complex. The plantation workers, many of whom were descendants of indentured laborers brought from other parts of India, began asserting their rights through unions and political movements. The Vissanjis had to balance worker demands with economic viability, all while operating under increasingly stringent labor laws. It was a delicate dance that required both firmness and flexibility.

The 1960s brought new challenges. The Indo-China war of 1962 and the Indo-Pakistan wars of 1965 and 1971 created economic disruptions and security concerns, particularly for estates near border areas. The Green Revolution was transforming Indian agriculture, raising questions about the relevance of colonial-era plantation models. Meanwhile, a new generation of Indian businesses—the Ambanis, the Hindujas—were emerging with different models and ambitions.

By the 1970s, it was clear that the Vissanji model, successful as it had been in navigating the transition from colonial to independent India, needed evolution. The company required capital for modernization, political connections to navigate the License Raj, and strategic vision to compete in an evolving economy. The stage was set for BBTC's next transformation.

The Vissanji era deserves recognition for what it achieved: preserving a colonial-era company through one of history's most tumultuous political and economic transitions. They maintained operations when many British companies fled, preserved jobs when unemployment was rampant, and kept BBTC viable when nationalization seemed inevitable. But by the 1970s, maintaining the status quo was no longer enough. BBTC needed not just survival skills but growth strategies. Enter the Wadias.

V. Enter the Wadias: The Acquisition Story (1970s-1990s)

The acquisition of BBTC by the Wadia Group wasn't a sudden corporate raid—it was a patient, decades-long culmination of history, opportunity, and strategic vision. Around 1913, the Wadia Group acquired BBTC, but this early connection lay dormant for decades, like a seed waiting for the right conditions to germinate. It would take another sixty years and a generational change before the Wadias would fully control this colonial-era jewel.

To understand the significance of this acquisition, you must first understand the Wadias themselves. Founded by Lovji Nusserwanjee Wadia in 1736, the Wadia Group is the oldest company in India, predating even the formal establishment of British rule. The family built ships for the British Navy, including HMS Minden, on which the words of the American national anthem were penned. By the time they fully acquired BBTC, the Wadias weren't just buying a company—they were adding another chapter to a 250-year corporate saga.

The modern acquisition story begins with Neville Wadia, who joined the business in 1952 after the demise of his father Ness Wadia. But the real protagonist of this tale is his son, Nusli Neville Wadia, who entered the business in 1977 and would earn the moniker "corporate samurai" for his legendary boardroom battles.

Nusli Wadia's approach to BBTC was emblematic of his broader business philosophy: patient accumulation of control, strategic positioning, and ruthless execution when the moment arrived. The Vissanji era had preserved BBTC through independence, but by the 1970s, the company needed more than preservation—it needed transformation. The Wadias offered not just capital but something more valuable: a place within one of India's most powerful business ecosystems.

The formal takeover wasn't a single transaction but a gradual consolidation. In 1992, the Wadia group bought the controlling stakes in the company, cementing their control after years of increasing influence. But the real masterstroke came with the 1992 acquisition and merger of BCL Springs, which expanded BBTC's manufacturing capabilities and diversified its portfolio beyond plantations.

Think about the strategic brilliance here. The Wadias weren't just acquiring a tea company or a trading house—they were acquiring a platform. BBTC's diversified structure, built over 130 years, provided multiple avenues for value creation. The plantations generated steady cash flows, the manufacturing operations offered growth potential, and most intriguingly, the company's various investments provided optionality in an evolving Indian economy.

The integration of BBTC into the Wadia ecosystem created powerful synergies. Bombay Dyeing, established in 1879, was the group's textile flagship. Britannia Industries, which the Wadias would later control through BBTC, was a growing FMCG player. National Peroxide provided a chemicals angle. Together, these companies formed a conglomerate that touched multiple aspects of Indian consumer and industrial life.

Nusli Wadia's management philosophy for BBTC was distinctive. Rather than dismantling the colonial-era structure entirely, he modernized it selectively. The plantation operations continued but with improved practices. The manufacturing divisions were upgraded with new technology. Most importantly, the company's investment philosophy evolved from passive holdings to strategic stakes in high-growth businesses.

The cultural transformation was equally significant. Under the Wadias, BBTC evolved from a company with colonial hangovers to one embracing Indian business practices while maintaining global standards. The head office remained at 9 Wallace Street in Fort, Mumbai—a symbolic retention of heritage—but the mindset shifted from preservation to growth.

The Wadia era also brought sophisticated financial engineering. The group structure allowed for complex cross-holdings and inter-company transactions that optimized tax efficiency and capital allocation. While critics would later point to governance concerns—as evidenced by Bombay Burmah Trading Corporation, its promoters including Nusli Wadia, his sons Ness and Jehangir, settling a disclosure lapses case with markets regulator Sebi after paying Rs 2.12 crore—the structure enabled the Wadias to maintain control with minimal capital.

The appointment of family members to key positions solidified control. Ness Nusli Wadia became managing director of Bombay Burmah Trading Corporation, ensuring continuity of the Wadia vision. This wasn't mere nepotism—it was strategic succession planning in a business environment where trust and long-term thinking were paramount.

Perhaps the most significant achievement of the Wadia era was maintaining BBTC's relevance in a rapidly liberalizing economy. As India opened up in 1991, many old economy companies struggled to adapt. BBTC, under Wadia stewardship, not only survived but positioned itself to benefit from new opportunities. The diversified structure that might have seemed anachronistic became an advantage, providing multiple engines of growth.

The transformation from Vissanji caretaking to Wadia dynamism marked BBTC's evolution from a colonial relic to a modern conglomerate. The Wadias brought not just capital and management expertise but something more valuable: a vision for how a 19th-century company could thrive in the 21st century. As we'll see, this vision would be most powerfully expressed through BBTC's crown jewel acquisition—Britannia Industries.

VI. The Diversification Machine: Six Segments Strategy

Walk through BBTC's Mumbai headquarters today and you'll encounter a bewildering array of businesses that would make any focused strategist weep: tea plantations, dental products, automotive solenoids, weighing scales, decorative plants, and bakery products. It's as if someone took six different companies and forced them to share a parent. Yet this seemingly random collection of businesses represents something profound about emerging market conglomerates—the art of finding value in complexity.

BBTC operates through six segments: Plantation-Tea, Health Care, Auto Electric Components, Investments, Horticulture, Food-Bakery & Dairy Products, and Others. Each segment tells a story of opportunistic expansion, strategic positioning, or historical accident that somehow cohered into a functioning whole.

Plantation-Tea: The Heritage Crown Jewel

The plantation segment remains BBTC's historical heart. The company produces and trades in tea, coffee, timber, cardamom, and pepper. With 2,822 hectares under tea cultivation producing 8 million kgs annually, this isn't just a business—it's an agricultural empire spanning multiple states and employing thousands.

But here's what makes it interesting from an investment perspective: while global tea consumption grows at 2-3% annually, BBTC's plantation operations provide something more valuable than growth—they provide predictable cash flows and real asset backing. In an era of asset-light business models, owning thousands of hectares of prime agricultural land in South India is like holding a massive real estate option that happens to produce tea.

The segment has evolved far beyond simple commodity production. BBTC pioneered organic farming of tea in 1988, years before organic became a premium category. They've developed proprietary varietals, implemented precision agriculture, and created direct relationships with global buyers. This isn't your grandfather's tea plantation—though ironically, it might literally be on your grandfather's tea plantation land.

Auto Electric Components: The Unexpected Industrial Play

The company manufactures solenoids, switches, valves, and slip rings for automobile and other industries. How does a tea company end up making critical components for Maruti Suzuki and other automotive giants? The answer reveals the opportunistic genius of conglomerate building in protected markets.

During the License Raj, getting permission to manufacture anything was like winning a lottery. When BBTC acquired BCL Springs in 1992, they didn't just get a springs manufacturer—they got licenses, relationships, and most importantly, a foothold in India's nascent automotive component industry. Today, as India emerges as a global automotive hub, these seemingly random industrial assets have become strategically valuable.

The segment faces an existential question with the EV transition. Solenoids and valves designed for internal combustion engines may become obsolete, but BBTC's manufacturing capabilities and OEM relationships provide optionality for pivoting to EV components. It's a classic conglomerate hedge—even if the product becomes obsolete, the capabilities and relationships remain valuable.

Healthcare: From Dental Chairs to Medical Devices

The company manufactures and trades in dental products. Healthcare products include dental, orthopaedic and ophthalmic products. This segment emerged from another historical accident—a 1960s partnership with a European dental equipment manufacturer that needed an Indian partner to navigate import substitution policies.

Today, BBTC manufactures everything from dental chairs to surgical instruments, serving both domestic and export markets. In a country where healthcare spending is growing at 15% annually and medical device imports exceed $15 billion, being an established domestic manufacturer with decades of regulatory compliance history is incredibly valuable.

The healthcare segment exemplifies conglomerate optionality. As India's healthcare infrastructure expands and the government pushes for domestic manufacturing through PLI schemes, BBTC's existing manufacturing facilities and regulatory approvals become platforms for expansion rather than legacy burdens.

Investments: The Hidden Value Driver

The company invests in various listed and unlisted securities primarily on a long-term basis. This segment is where BBTC transforms from operating company to investment vehicle. Beyond the crown jewel Britannia stake, BBTC holds a portfolio of strategic investments accumulated over decades.

Think of this as Warren Buffett's Berkshire Hathaway model in miniature—using steady cash flows from operating businesses to make long-term investments. The investment philosophy is distinctly old-school: buy and hold forever, preferring control to liquidity, and viewing investments as relationships rather than trades.

Horticulture: The Millennial Play

The company deals with decorative plants and landscaping services. Started in the 1990s when India's IT boom created demand for corporate landscaping, this segment seems almost whimsical compared to BBTC's industrial operations. Yet it represents something important: the ability to identify and capture emerging consumer trends.

As urban India discovers gardening and companies invest in green campuses, BBTC's horticulture division has evolved from supplying office plants to designing entire corporate landscapes. It's a high-margin, asset-light business that leverages BBTC's agricultural expertise in an entirely different market.

Food-Bakery & Dairy Products: The Consumer Connection

The company offers bakery and dairy products. This newest segment represents BBTC's attempt to move closer to the consumer, leveraging both its agricultural inputs and its Britannia connection. While still subscale, it provides a testing ground for consumer products that could eventually be scaled through the Britannia distribution network.

The Conglomerate Paradox

The company has delivered a poor sales growth of 9.01% over past five years and has a low return on equity of -10.9% over last 3 years. These numbers tell a story that every conglomerate investor knows: diversification often destroys more value than it creates. The question is whether BBTC's seemingly random collection of businesses contains hidden synergies or represents accumulated corporate debris.

The bear case is straightforward: BBTC is an unfocused conglomerate in an era that rewards specialization. Management attention is divided, capital allocation is suboptimal, and the market applies a deserved discount to this complexity.

The bull case is more nuanced: In emerging markets, conglomerate structures provide resilience, regulatory arbitrage, and optionality that focused companies lack. Each seemingly unrelated business provides options for future growth, hedges against sector-specific risks, and platforms for opportunistic expansion.

What's undeniable is that BBTC's six-segment strategy reflects a fundamentally different philosophy from Western corporate strategy. It's not about focus, efficiency, or optimization. It's about survival, optionality, and patient capital allocation across multiple time horizons. Whether this creates or destroys value depends entirely on execution—and as we'll see in examining the Britannia connection, sometimes one brilliant investment can justify an entire conglomerate structure.

VII. The Britannia Connection & Group Dynamics

Here's the most astonishing fact about BBTC: Bombay Burmah holds a majority share of 50.5 per cent in Britannia Industries, amounting to a total of 12.17 crore equity shares. At Britannia's current market cap of approximately ₹1,28,500 crores, BBTC's stake is worth over ₹64,000 crores—nearly five times BBTC's own market capitalization of ₹13,000 crores. It's like finding a Rembrandt in your attic, except everyone knows it's there and still values your house at less than the painting.

This valuation anomaly represents one of the most extreme holding company discounts in Indian markets. BBTC's stake in Britannia is currently worth more than Rs 40,000 crore i.e., almost 5 times of it's total current market cap. However, what is unusual is the quantum of discount. Most holding companies trade at 20-40% discounts to their underlying assets. BBTC trades at an 80% discount.

The Britannia Acquisition Saga

The story of how BBTC came to control India's leading biscuit company is a masterclass in patient capital and strategic maneuvering. Britannia, established in 1892 by British businessmen, had passed through multiple hands—from British ownership to American conglomerate RJR Nabisco. The Wadias' acquisition in the early 1990s wasn't just buying a biscuit company; it was acquiring a piece of Indian consumer culture.

The acquisition itself was byzantine in its complexity. Nusli Wadia first attempted to buy Britannia through his friend K. Rajan Pillai, who had connections with RJR Nabisco's management. The plan backfired spectacularly when Pillai was appointed chairman of Britannia and then allegedly defrauded the company. After a bitter boardroom battle, Pillai was ousted, imprisoned, and died in custody. Wadia eventually partnered with French food giant Danone to complete the acquisition.

What followed was equally dramatic. The Wadia-Danone partnership, initially harmonious, devolved into one of India's most acrimonious corporate battles. Danone wanted management control; Wadia wanted to maintain his family's dominance. The dispute lasted years, involved multiple legal proceedings, and ended with Danone's exit in 2009, leaving the Wadias through BBTC as the undisputed controllers of Britannia.

The Strategic Value Beyond Numbers

Britannia isn't just an investment for BBTC—it's the crown jewel that justifies the entire conglomerate structure. Britannia Industries belongs to the Wadia Group, a reputed Indian Business house who has presence in wide range of business segments like Airlines (Go Air), Realty ( Bombay Realty), Textiles ( Bombay Dyeing) and Plantations and other business (Bombay Burmah trading Corporation which is also the Ultimate holding company of Britannia Industries).

Consider what Britannia brings to the table: ₹18,000+ crores in revenue, presence in over 60 countries, market leadership in multiple categories, and most importantly, direct access to Indian consumers through 5 million retail outlets. For a conglomerate with industrial and plantation heritage, Britannia provides the consumer connection that transforms BBTC from a holding company into a strategic platform.

The synergies, while not immediately obvious, are profound. BBTC's plantation operations could theoretically supply raw materials (though they don't currently). The healthcare division's quality control expertise applies to food manufacturing. The investment philosophy of patient capital perfectly suits Britannia's long-term brand building. Even the seemingly unrelated auto components business provides manufacturing excellence that translates to operational efficiency.

The Governance Labyrinth

The ownership structure creates a governance puzzle that would challenge even the most sophisticated investors. BBTC owns 50.5% of Britannia. The Wadia family controls BBTC with approximately 74% ownership. This creates a cascade of control where the Wadias effectively control Britannia with an economic interest of only about 37% (74% of 50.5%).

This structure has attracted regulatory scrutiny. Bombay Burmah Trading Corporation, its promoters including Nusli Wadia, his sons Ness and Jehangir, and others on Friday settled a disclosure lapses case with markets regulator Sebi after paying Rs 2.12 crore towards settlement amount. The complexity creates opacity that the market penalizes through valuation discounts.

Yet from the Wadias' perspective, this structure is optimal. They control a ₹1,28,000 crore company (Britannia) through a ₹13,000 crore company (BBTC) with an actual economic investment of less than ₹10,000 crores. It's leverage without debt, control without proportional capital—a structure that would make private equity firms envious.

The Value Unlock Question

The elephant in the room is obvious: Why doesn't BBTC simply distribute its Britannia shares to shareholders, unlocking the massive discount? The answer reveals the fundamental tension in family-controlled conglomerates.

First, distribution would trigger massive tax liabilities. Second, it would dilute the Wadias' control over Britannia. Third, and perhaps most importantly, it would destroy the strategic value of the integrated structure. BBTC isn't just a holding company—it's the architecture through which the Wadias control their empire. Dismantling it for short-term value realization would be killing the golden goose.

BBTC for periods maybe under performing Britannia. However, then it catches up sharply. BBTC moved very quickly from 2016 to 2018 and then went into technical correction followed by covid related concerns related to the group's aviation business (Go Air). This pattern suggests the market occasionally recognizes the value, creating opportunities for patient investors.

The Dividend Paradox

Here's another puzzle: Britannia, with its consistent profitability and cash generation, pays healthy dividends. Britannia's 106th AGM: All resolutions including Rs.75 dividend approved on 11 Aug 2025. BBTC receives approximately ₹900 crores annually in dividends from its Britannia stake alone. Yet BBTC's own dividend policy doesn't fully reflect this cash flow, creating another layer of value leakage.

This dividend paradox exemplifies the agency problems in complex holding structures. Cash flows from Britannia to BBTC, but not proportionally from BBTC to its minority shareholders. The money funds other ventures, covers corporate expenses, or simply accumulates—everything except flowing through to ultimate shareholders.

The Future of the Connection

The Britannia-BBTC relationship faces several inflection points. Britannia's growth trajectory in India's FMCG sector remains robust, with premiumization and distribution expansion driving value. But BBTC's other businesses face headwinds—tea plantations are capital intensive with limited growth, auto components face EV disruption, and healthcare remains subscale.

The strategic question isn't whether to separate Britannia from BBTC, but how to better leverage this connection. Could BBTC's other food ventures (bakery and dairy) be integrated with Britannia? Could the plantation products be branded and distributed through Britannia's network? Could the healthcare division pivot to nutraceuticals under the Britannia brand?

The Britannia connection makes BBTC simultaneously one of the most undervalued and most complex investments in Indian markets. It's a value trap and a value opportunity, depending on your time horizon and tolerance for complexity. What's undeniable is that understanding BBTC requires understanding that it's not really a conglomerate with a Britannia stake—it's a Britannia controlling vehicle with some additional businesses attached. Everything else is just noise around this central reality.

VIII. Modern Era Challenges & Transformation (2000s-Present)

The millennium brought a reckoning that even a 160-year-old company couldn't avoid. Global supply chains, digital disruption, ESG pressures, and changing consumer preferences converged to challenge every assumption BBTC had operated under since independence. The company's response—a mix of strategic retreats, tentative modernization, and stubborn traditionalism—reveals both the limitations and surprising resilience of legacy conglomerates in the modern era.

The Great Plantation Retreat

In 2023, the company announced that it will be divesting 3 tea estates in Tanzania, measuring around 3,957 acres, to Udongo Wetu, Dar es Salaam, Tanzania. Orange County Resorts acquired eight coffee estates from Bombay Burmah for Rs 291 crore. These divestments weren't just asset sales—they represented a fundamental rethinking of BBTC's plantation strategy.

The Tanzania exit was particularly symbolic. These estates, acquired during the expansion era when geographic diversification seemed prudent, had become liabilities. Tanzania's tea industry, once dominated by large estates, had shifted to smallholder production. The government's nationalization and subsequent privatization cycles had created an unstable operating environment. For BBTC, maintaining estates thousands of miles from Mumbai headquarters in a volatile regulatory environment no longer made strategic sense.

The coffee estate sale to Orange County Resorts was even more telling. Here was BBTC selling productive agricultural assets to a hospitality company that would convert them into luxury resorts. The buyer saw more value in the land as tourist destinations than as agricultural operations—a sobering commentary on the economics of traditional plantation businesses.

The ESG Imperative

Modern stakeholders demand more than profits, and BBTC's plantation heritage became both an asset and a liability in the ESG era. The company's initiatives in generating non-conventional, environment-friendly energy sources such as wind mills, are an expression of this dedication. BBTC's tea factories run on this eco-friendly energy. The company supplements this with other renewable fuel sources which possibly makes BBTC Teas as one of the 'greenest teas' available to the consumer.

The Bombay Burmah Trading corportation Limited, first obtained Fair Trade Certificate for the Singampatti group of Estates in 1995 under the name"Singampatti Foundation". This early adoption of Fair Trade certification—years before it became mainstream—demonstrated surprising foresight. Yet the company struggled to monetize this ESG leadership, trapped between commodity pricing in bulk markets and inability to build consumer-facing premium brands.

The environmental challenges were equally complex. Climate change directly threatens tea cultivation, with changing rainfall patterns and rising temperatures affecting yield and quality. BBTC's response—investing in drought-resistant varietals and precision agriculture—required capital that competed with other investment priorities. The question became: Is BBTC a plantation company investing in technology, or a technology-enabled agriculture company? The answer remained frustratingly unclear.

The Digital Disconnect

While Britannia built e-commerce capabilities and direct-to-consumer channels, BBTC remained stubbornly analog. The company's website, unchanged for years, epitomizes this digital reluctance. In an era when D2C brands achieve billion-dollar valuations, BBTC continued selling through traditional B2B channels, leaving value on the table.

The auto components division faced its own digital disruption. The shift to electric vehicles threatens the relevance of solenoids and valves designed for internal combustion engines. While management speaks of pivoting to EV components, concrete progress remains minimal. The division operates like it's still 1992, when the BCL Springs acquisition seemed transformative.

Even the healthcare division, which should benefit from India's medical device boom, struggles with scale and focus. In a market where specialized medical device companies command premium valuations, BBTC's subscale, unfocused healthcare operations destroy rather than create value.

The Governance Evolution

The company has delivered a poor sales growth of 9.01% over past five years. Company has a low return on equity of -10.9% over last 3 years. These numbers tell a story of stagnation that no amount of financial engineering can hide. The modern era demanded operational excellence, not just patient capital allocation.

Corporate governance emerged as a persistent concern. The complex cross-holdings, related-party transactions, and opacity around capital allocation decisions created a trust deficit with minority shareholders. The 2025 settlement with SEBI over disclosure lapses, while resolved, reinforced perceptions of governance weakness that the market penalized through valuation discounts.

The Britannia Dependency

BBTC's modern era is increasingly defined by a single reality: its value derives almost entirely from Britannia. The other businesses—tea, auto components, healthcare—have become almost incidental to the Britannia stake's appreciation. This creates a peculiar dynamic where BBTC management's actions in the operating businesses matter less than Britannia's quarterly results.

This dependency creates strategic paralysis. Major capital allocation decisions must consider impact on Britannia control. Aggressive expansion might require equity dilution that threatens the Wadia family's cascade of control. Conservative management preserves control but sacrifices growth. BBTC exists in strategic purgatory—unable to grow aggressively, unwilling to shrink strategically.

The Succession Question

As Nusli Wadia approaches his eighties, succession looms large. Ness and Jehangir Wadia are involved in the business, but their vision for BBTC remains opaque. Will they maintain the conglomerate structure their father fought to control? Will they unlock value through simplification? Or will they double down on diversification?

The generational transition coincides with fundamental questions about BBTC's relevance. In a market that rewards focused execution and punishes complexity, does a six-segment conglomerate make sense? Can a company founded to export Burmese teak reinvent itself for the AI age?

The Path Forward

BBTC's modern challenges aren't unique—every legacy conglomerate faces similar pressures. What makes BBTC distinctive is the extreme disconnect between its market value and asset value, driven primarily by the Britannia stake. This creates both opportunity and constraint.

The opportunity is clear: even modest operational improvements in the non-Britannia businesses could significantly reduce the holding company discount. A focused strategy to divest subscale operations, modernize core businesses, and improve governance could unlock billions in value.

The constraint is equally clear: any strategy must preserve Britannia control. This non-negotiable requirement eliminates many value-creation options and forces suboptimal capital allocation. BBTC is condemned to complexity by its own success in acquiring Britannia.

The modern era has exposed BBTC's fundamental contradiction: it's simultaneously one of India's most valuable and most poorly managed companies. The Britannia stake ensures value; the conglomerate structure ensures that value remains locked. Breaking this paradox requires either a revolutionary restructuring or generations of patient investors willing to accept complexity for indirect Britannia exposure. Neither seems imminent, suggesting BBTC will continue its strange dance—a 19th-century company controlling a 21st-century brand, creating value it cannot unlock, persisting through sheer institutional inertia. The modern era hasn't transformed BBTC; it has simply made its anachronisms more visible.

IX. Financial Analysis & Market Position

The numbers tell a story of spectacular undervaluation wrapped in operational mediocrity. Mkt Cap: 12,945 Crore (down -18.4% in 1 year) · Revenue: 18,676 Cr · Profit: 2,225 Cr. With NSE:BBTC has a market cap or net worth of INR 140.96 billion and considering its Britannia stake alone is worth over ₹64,000 crores, the mathematics of BBTC's valuation defies conventional finance theory.

The Valuation Enigma

The intrinsic value of one BBTC stock under the Base Case scenario is 3 868.72 INR. Compared to the current market price of 1 850.3 INR, Bombay Burmah Trading Corporation Ltd is Undervalued by 52%. Even conservative valuation models suggest massive undervaluation, yet the market stubbornly refuses to close this gap.

The key metrics paint a picture of a company trading at distressed valuations despite solid fundamentals: - The trailing PE ratio is 12.56 - The P/B (price-to-book) ratio is 1.64 - The stock's EV/EBITDA ratio is 4.56, with an EV/FCF ratio of 8.32

These are the valuations you'd expect for a declining industrial company, not one controlling India's leading biscuit brand. The disconnect between price and value has persisted for years, suggesting structural rather than temporary factors.

Revenue and Profitability Dynamics

In the last 12 months, NSE:BBTC had revenue of INR 185.67 billion and earned 11.23 billion in profits. Earnings per share was 160.90. The consolidated numbers include Britannia's contribution, making BBTC appear more profitable than its standalone operations suggest.

The revenue breakdown reveals the dominance of Britannia in the consolidated numbers. Stripping out Britannia's contribution, BBTC's other businesses generate modest revenues with even more modest margins. The plantation business, despite its vast land holdings, contributes marginally to profits. The auto components division operates at commodity margins. Healthcare remains subscale.

The company has delivered a poor sales growth of 9.01% over past five years. Company has a low return on equity of -10.9% over last 3 years. These growth metrics would be concerning for any company but are particularly damning for one operating in India's high-growth economy.

Capital Structure and Financial Health

The company has 16.58 billion in cash and 15.74 billion in debt, giving a net cash position of 834.27 million. The near-neutral net cash position seems conservative given the asset base, but it reflects the capital intensity of plantation and manufacturing operations.

The company has a current ratio of 1.07, with a Debt / Equity ratio of 0.20. Return on equity (ROE) is 30.41% and return on invested capital (ROIC) is 21.14%. The high ROE is misleading—it's inflated by the Britannia stake's appreciation rather than operational excellence.

Cash Flow Generation

In the last 12 months, operating cash flow was 22.78 billion and capital expenditures -3.32 billion, giving a free cash flow of 19.46 billion. The strong free cash flow generation is primarily driven by dividend income from Britannia, highlighting BBTC's dependence on its crown jewel investment.

The capital allocation reveals management priorities—or lack thereof. Despite generating substantial free cash flow, BBTC hasn't meaningfully increased dividends, made transformative acquisitions, or bought back stock at these discounted valuations. Cash accumulates without clear purpose, another source of value destruction.

Ownership and Market Dynamics

Promoter Holding: 74.0%. The high promoter holding creates low float, which theoretically should amplify price movements but in practice contributes to the illiquidity discount. With limited shares available for trading, institutional investors avoid the stock, perpetuating undervaluation.

The shareholding pattern reveals another issue: minimal institutional ownership. Quality institutional investors who might advocate for value unlocking are absent. The investor base consists primarily of retail investors attracted by the Britannia angle but lacking the influence to drive corporate change.

Peer Comparison and Relative Valuation

Comparing BBTC to pure-play companies in its operating segments reveals the conglomerate discount starkly:

- Tea companies like Tata Consumer trade at 35-40x P/E

- Auto component companies average 20-25x P/E

- Medical device companies command 30-40x P/E

- Britannia itself trades at 60x P/E

Yet BBTC, with exposure to all these sectors plus its Britannia stake, trades at just 12x P/E. The market essentially values BBTC's operating businesses at negative value after accounting for the Britannia stake.

The Dividend Policy Puzzle

In the quarter ending December 2024, Bombay Burmah Trading Corporation Ltd has declared dividend of ₹4 - translating a dividend yield of 0.94%. Given the substantial dividend income from Britannia, BBTC's own parsimonious dividend policy seems inexplicable. The company receives approximately ₹900 crores annually from Britannia but distributes only a fraction to its own shareholders.

Recent Performance Trends

Bombay Burmah Trading Corporation Ltd's net profit jumped 8.62% since last year same period to ₹308.65Cr in the Q4 2024-2025. While profit growth appears healthy, it's largely driven by Britannia's performance rather than improvement in BBTC's operating businesses.

The stock price has increased by +38.31% in the last 52 weeks. The beta is 0.71, so NSE:BBTC's price volatility has been lower than the market average. The recent appreciation suggests growing investor recognition of the value gap, but from such a low base that substantial undervaluation persists.

The Analyst Perspective

Wall Street analysts forecast BBTC stock price to rise over the next 12 months. According to Wall Street analysts, the average 1-year price target for BBTC is 3 570 INR with a low forecast of 3 535 INR and a high forecast of 3 675 INR. Even analyst targets, typically optimistic, suggest nearly 100% upside from current levels.

The Financial Reality

BBTC's financial analysis reveals a fundamental paradox: it's simultaneously one of India's most undervalued stocks and one of its worst capital allocators. The company sits on valuable assets—prime plantation land, a controlling stake in Britannia, established manufacturing operations—yet generates returns that barely exceed the cost of capital.

The financial statements read like a case study in value destruction through complexity. Segmental reporting is opaque, related-party transactions are numerous, and capital allocation lacks strategic coherence. The market's response—a massive conglomerate discount—is entirely rational given these governance and strategic shortcomings.

What makes BBTC fascinating from a financial perspective is that the value gap is so extreme that even modest improvements could generate substantial returns. If management simply distributed Britannia dividends more generously, improved transparency, or divested underperforming assets, the stock could double without any operational improvement.

The financial analysis ultimately points to a simple conclusion: BBTC is a value trap that might also be a value opportunity, depending entirely on whether the Wadia family decides to unlock value for all shareholders or continue using it as a private vehicle for controlling Britannia. Until that strategic question is resolved, BBTC will remain one of Indian markets' most frustrating investments—obviously undervalued, stubbornly stuck, perpetually promising but never delivering.

X. Playbook: Lessons from 160 Years

After examining BBTC's journey from Victorian teak trader to modern conglomerate, certain patterns emerge that transcend industry, geography, and time. These aren't just historical curiosities—they're actionable insights for anyone building or investing in long-term businesses.

Lesson 1: Survival Requires Shapeshifting

BBTC has been at least four different companies: a colonial resource extractor (1863-1913), an agricultural enterprise (1913-1970s), a diversified industrial conglomerate (1970s-2000s), and now essentially an investment holding company with operating subsidiaries. Each transformation wasn't planned—it was forced by external disruption.

The lesson isn't that you should randomly diversify. It's that organizational identity must be fluid enough to survive regime changes. The Wallace brothers didn't set out to become tea planters; they pivoted when their core business faced existential threat. The Wadias didn't plan to control Britannia through BBTC; they seized an opportunity when it appeared.

Modern founders obsess over focus and core competency. BBTC suggests the opposite lesson: in emerging markets with volatile regulatory environments, the ability to completely reinvent yourself while maintaining institutional continuity is the ultimate competitive advantage.

Lesson 2: Complexity Can Be a Moat

Conventional wisdom says conglomerates destroy value through complexity. BBTC's structure—six unrelated segments, multiple subsidiaries, byzantine ownership—should be a disaster. Yet this complexity has enabled the company to survive when focused competitors disappeared.

During the License Raj, having multiple businesses meant multiple licenses—optionality when regulations changed. During liberalization, diverse revenue streams provided stability as sectors opened at different paces. Today, the complex structure enables tax efficiency and regulatory arbitrage that focused companies can't achieve.

The playbook insight: In uncertain environments, complexity that seems inefficient in steady state becomes invaluable during transitions. It's expensive insurance that pays off during regime changes.

Lesson 3: Patient Capital Beats Smart Capital

BBTC's investment philosophy—buy and hold forever—seems anachronistic in an era of quarterly earnings and activist investors. Yet their patient approach to Britannia, held through decades of underperformance before eventual value creation, validates the strategy.

Consider the counterfactual: If BBTC had been run by financial engineers optimizing quarterly returns, they would have sold Britannia during its struggles with Danone, divested the plantations during commodity downturns, and exited auto components when margins compressed. They would have been wrong every time.

The lesson: In emerging markets, the ability to hold assets through cycles, ignoring market volatility and temporary underperformance, creates more value than any amount of strategic brilliance. Time arbitrage—being able to wait when others cannot—is the ultimate edge.

Lesson 4: Control Premium > Economic Efficiency

BBTC's structure makes no economic sense. The Wadias control Britannia through a cascade of holdings that destroys value at every level through taxes, administrative costs, and market discounts. Any MBA student could design a more efficient structure.

But efficiency misses the point. The structure optimizes for control, not returns. In markets where minority shareholders have limited rights and regulatory capture is possible, control is worth more than any amount of economic efficiency. The Wadias would rather own 37% of Britannia with control than 60% without it.

For founders, the lesson is uncomfortable but important: maintaining control through suboptimal structures might be rational if it enables long-term value creation that wouldn't be possible with distributed ownership.

Lesson 5: Heritage Is Currency

BBTC trades on its history. The company's 160-year legacy provides intangible benefits: regulatory forbearance, banking relationships, supplier trust, and brand recognition that money can't buy. When BBTC enters a new business, counterparties assume stability and longevity that startups can't match.

This heritage premium is particularly valuable in relationship-driven markets. A tea buyer in London trusts BBTC not because of its financials but because his grandfather bought from them. A bank extends credit not based on ratios but on 160 years of repayment history.

The playbook: In emerging markets, institutional age provides competitive advantages that no amount of venture capital can replicate. Building hundred-year companies requires thinking in hundred-year timescales from day one.

Lesson 6: Governance Discount Is Forever

Despite its survival skills, BBTC trades at a persistent discount to asset value. The market has learned that complex structures with concentrated ownership and opaque governance never fully unlock value for minorities. This discount is the price of the control structure that enables survival.

The lesson for investors: Companies that survive centuries do so by prioritizing institutional continuity over shareholder returns. They're great businesses but mediocre investments. The governance discount isn't a bug—it's a feature that enables longevity.

Lesson 7: Diversification Timing Matters

BBTC's diversifications weren't random—they followed a pattern. Major pivots occurred during external disruptions when asset prices were depressed and competition was distracted. The tea plantation entry in 1913 preceded World War I. The industrial diversification followed independence uncertainty. The Britannia acquisition exploited 1990s liberalization chaos.

The playbook: Diversify during disruption, not stability. When markets are calm, focus on operational excellence. When regimes change, regulations shift, or crises hit, that's when conglomerate-building creates value.

Lesson 8: Operating Mediocrity Can Coexist with Strategic Brilliance

BBTC's operating businesses are unremarkable. The tea estates aren't particularly efficient. The auto components business lacks scale. Healthcare is subscale. Yet the strategic decision to acquire and hold Britannia created more value than decades of operational excellence could have achieved.

This challenges the cult of operational excellence. Sometimes one brilliant strategic decision matters more than thousands of operational improvements. The playbook: Allocate talent accordingly—put your best people on strategic capital allocation, not operational optimization.

Lesson 9: Family Businesses Play Different Games

BBTC makes decisions that would get public company CEOs fired. Holding underperforming assets for decades, maintaining inefficient structures for control, prioritizing family harmony over shareholder returns—these seem irrational until you realize the game being played.

Family businesses optimize for multi-generational wealth preservation, not quarterly earnings. They'd rather own a smaller piece of something that lasts centuries than a larger piece of something that might not survive the next recession. Public market investors who don't understand this game will always be frustrated.

Lesson 10: Resilience Requires Redundancy

BBTC maintains what seems like inefficient redundancy—multiple business lines, excess cash, conservative leverage. This redundancy is expensive but has enabled survival through wars, independence, socialism, and liberalization.

Modern businesses optimize for efficiency, eliminating redundancy to maximize returns. BBTC's playbook suggests the opposite: in volatile environments, redundancy that seems wasteful in good times becomes essential for survival in bad times.

The Meta-Lesson

BBTC's ultimate lesson is that building centennial businesses requires accepting paradoxes. You must be focused yet diversified, efficient yet redundant, innovative yet traditional, global yet local. These contradictions aren't bugs to be fixed but tensions to be managed.

The company's 160-year journey suggests that longevity comes not from having the right strategy but from having the capacity to completely change strategy when circumstances demand. It's not about being right—it's about being able to become right, again and again, across decades and centuries.

For modern entrepreneurs intoxicated with disruption and creative destruction, BBTC offers a sobering reminder: the companies that last aren't always the most innovative or efficient. They're the ones that master the mundane art of survival, playing games measured in generations while others chase quarterly targets. In the end, simply surviving is the ultimate victory.

XI. Bull vs. Bear Case & Future Outlook

The Bull Case: Hidden Value Waiting for Catalyst

The bull case for BBTC starts with simple arithmetic. The company trades at ₹13,000 crores market cap while owning ₹64,000+ crores of Britannia stock. Even assigning zero value to all other assets, BBTC trades at an 80% discount. This isn't a small mispricing—it's a gaping valuation anomaly that markets eventually correct.

Beyond Britannia, bulls point to hidden assets. The 2,822 hectares of plantation land in prime South Indian locations could be worth ₹2,000-3,000 crores at current real estate valuations. The auto components business, while facing headwinds, generates steady cash flows worth at least ₹500 crores. The healthcare division, though subscale, has regulatory approvals and manufacturing capabilities valuable in India's medical device import substitution push.

The governance catalyst argument is compelling. Nusli Wadia is approaching 80. The next generation—Ness and Jehangir—might be more receptive to unlocking value. Even minor improvements like better disclosure, higher dividend payouts, or strategic asset sales could trigger rerating. History shows that conglomerate discounts can close rapidly when management signals change.

The macroeconomic tailwinds favor BBTC's segments. India's tea consumption grows steadily. The auto component industry benefits from production-linked incentives. Healthcare spending expands at 15% annually. Even without operational improvements, sectoral growth should drive value creation.

The special situations angle is intriguing. BBTC could become an acquisition target—any buyer getting Britannia control at these valuations would instantly create value. Alternatively, activists might target BBTC as India's governance standards improve. The asymmetry is attractive: limited downside given asset backing, massive upside if the discount narrows.

Bulls also note technical factors. The low float creates potential for explosive moves if sentiment shifts. Promoter holding at 74% means any accumulation quickly impacts price. BBTC has historically moved in sudden bursts—staying dormant for years then doubling in months.

The Bear Case: Permanent Capital Destruction Machine

Bears see BBTC as a value trap par excellence—obviously cheap for good reasons that won't change. The conglomerate discount isn't temporary market inefficiency but permanent punishment for structural problems.

The Britannia stake, bears argue, is effectively locked forever. Selling would trigger massive taxes and lose control premium. The Wadias will never distribute it to shareholders. It's phantom value—real on paper, inaccessible in practice. Paying for something you'll never receive is foolish, regardless of discount.

The operating businesses are melting ice cubes. Tea plantations face climate change, labor issues, and commodity pricing pressure. Auto components confront EV disruption without clear transition strategy. Healthcare remains subscale in a business requiring scale. These aren't temporarily underperforming assets—they're structurally challenged businesses in secular decline.

Governance concerns run deeper than disclosure lapses. The complex structure enables value extraction through related-party transactions. Management compensates itself for running a ₹13,000 crore company while sitting on ₹64,000 crores of assets. The interests of controlling shareholders and minorities are permanently misaligned.

The opportunity cost argument is powerful. While waiting for BBTC to unlock value, investors miss opportunities in focused companies with aligned management. India offers numerous growth stories without governance baggage. Why accept complexity and conflicts when cleaner alternatives exist?

Bears note that catalysts have repeatedly failed to materialize. Generations of investors have waited for value unlocking that never comes. The Vissanjis didn't unlock value. The Wadias haven't for 50 years. Why would the next generation be different? The structure serves the family's purposes—control with minimal capital—and won't change.

The market has rendered its verdict through persistent discount. If sophisticated investors saw unlocking potential, they'd arbitrage it away. The discount persists because the market correctly assesses that value will never be released. Fighting the market's collective wisdom is hubris.

Future Scenarios

Scenario 1: Status Quo Forever (60% probability) BBTC continues exactly as it has—generating modest returns, maintaining the structure, trading at deep discounts. Britannia grows steadily, providing increasing NAV that's never realized. Operating businesses muddle through without major investment or divestment. The stock delivers 8-10% annual returns from NAV growth, underperforming markets but not catastrophically. Investors wait another generation for change that doesn't come.

Scenario 2: Gradual Value Unlocking (25% probability) Next-generation leadership implements incremental improvements. Better disclosure reduces information asymmetry. Higher dividend payouts return cash to shareholders. Non-core assets are divested, focusing the portfolio. The conglomerate discount narrows from 80% to 50%—still substantial but offering 60% returns to patient investors. This scenario requires family philosophy evolution without revolution.

Scenario 3: Transformative Restructuring (10% probability) A major catalyst—regulatory pressure, family split, or hostile approach—forces dramatic restructuring. Britannia stake is distributed to shareholders through tax-efficient structure. Operating businesses are spun off or sold. BBTC becomes a focused entity or liquidates entirely. The discount collapses, delivering 200-300% returns. This requires external pressure overwhelming family resistance.

Scenario 4: Value Destruction (5% probability) Something goes seriously wrong—Britannia faces major disruption, key assets are impaired, or governance failures escalate. The Wadia empire faces stress, forcing asset sales at distressed valuations. BBTC's complexity becomes liability in crisis. The stock falls 50% despite appearing cheap today. This tail risk reflects conglomerate fragility during systemic stress.

Investment Implications

BBTC represents a fascinating investment paradox—mathematically undervalued yet practically uninvestable for many. It suits specific investor types:

Perfect for: - Patient value investors with 5+ year horizons - Special situations funds seeking asymmetric risk-reward - Family offices comfortable with complexity - Contrarians betting on mean reversion

Avoid if you need: - Predictable returns or clear catalysts - Strong governance and alignment - Growth or momentum characteristics - Liquidity or easy exit options

The Verdict

BBTC embodies the classical value investing dilemma: the gap between price and value is obvious, but the path to closing it is obscure. Bulls and bears aren't disagreeing about facts—they're disagreeing about whether those facts will ever change.

The future likely holds more of the same—a company too valuable to ignore yet too complex to love, generating returns that disappoint growth investors while tantalizing value investors, surviving everything while thriving at nothing. BBTC will probably outlive everyone reading this analysis, still trading at a discount, still promising value that's always just out of reach.

For investors, BBTC offers a philosophical question disguised as an investment decision: Is obvious value worth pursuing if it might never be realized? The answer depends less on financial analysis than on faith—faith that markets eventually recognize value, that governance eventually improves, that patience eventually pays.

Those who buy BBTC aren't really buying a conglomerate—they're buying a belief that even in complex, conflicted, compromised situations, value eventually finds a way. Whether that belief is wisdom or folly, only time—probably lots of it—will tell.

XII. Epilogue: The Longevity Paradox

Standing in BBTC's Mumbai headquarters at 9 Wallace Street—the address itself a monument to continuity—you can almost feel the weight of 160 years pressing down from the colonial-era beams. This building has witnessed the Raj, independence, wars, liberalization, and digitalization. The company that operates within has shapeshifted through each era, yet somehow remained essentially itself: cautious, complex, and curiously eternal.

BBTC presents us with the longevity paradox: the very characteristics that enable century-spanning survival—diversification, conservatism, complexity, family control—are precisely what prevent excellence in any given decade. It's as if there's an inverse relationship between longevity and performance, between surviving forever and thriving today.

Consider what it actually means to build a business that lasts 160 years. You must survive multiple complete transformations of your core market. Your original customers, suppliers, and competitors will all disappear. The political system will change completely—BBTC has operated under British colonial rule, socialist democracy, and liberalized markets. Currency itself changes—BBTC has conducted business in pounds sterling, Indian rupees, Burmese kyat, and now digital payments. Technology cycles multiple times—from sailing ships to steamships to aircraft to video calls.

Most businesses optimize for the present. They build lean operations, focus on core competencies, maximize returns on capital. BBTC optimizes for permanence. It maintains redundancies that seem wasteful, diversifications that seem random, structures that seem inefficient. But these apparent weaknesses become strengths across longer timescales.

The modern cult of disruption celebrates companies that grow fast and break things. BBTC represents the opposite philosophy: grow slowly and preserve things. In a world obsessed with unicorns—companies that reach billion-dollar valuations in years—BBTC is something rarer: a survivor that measures success in centuries.

This isn't to romanticize BBTC's approach. The company has destroyed enormous value through poor capital allocation, governance failures, and operational mediocrity. Minority shareholders have suffered while watching obvious value remain locked away. Employees in struggling divisions have seen underinvestment while cash piles accumulate. The social cost of this inefficiency—capital that could fund innovation instead maintaining redundancy—is real.

Yet BBTC's survival contains lessons that transcend its specific failures. In an era when the average S&P 500 company lifespan has declined from 60 years in the 1950s to less than 20 years today, understanding longevity becomes crucial. What allows some organizations to persist while most perish?

The answer isn't strategic brilliance—BBTC has made numerous strategic errors. It isn't operational excellence—the company consistently underperforms peers. It isn't even financial strength—BBTC has faced near-bankruptcy multiple times. Instead, longevity seems to emerge from a particular organizational character: the ability to absorb change without losing identity, to bend without breaking, to fail without dying.

This character manifests in specific capabilities. The ability to completely change business models while maintaining stakeholder relationships. The patience to hold assets through decades of underperformance. The wisdom to maintain reserves that seem excessive until crisis makes them essential. The humility to survive rather than dominate.

Modern entrepreneurs could learn from this, though the lessons are uncomfortable. Building for centuries requires accepting lower returns for higher resilience. It means maintaining structures that seem inefficient but provide optionality. It requires thinking about stakeholders who don't yet exist—employees not yet born, customers in markets not yet created, societies facing challenges not yet imagined.

The Wadia family's stewardship of BBTC, whatever its flaws, represents something increasingly rare: business as multi-generational project rather than quarterly optimization exercise. They've preserved an institution that provides employment, generates taxes, and maintains capabilities across economic cycles. This isn't heroic, but it isn't trivial either.

Looking forward, BBTC faces an existential question: Can organizations built for one epoch adapt to another? The company thrived in an era of patient capital, relationship-based business, and information opacity. Today's world demands transparency, efficiency, and constant innovation. Can BBTC evolve without losing the characteristics that enabled its survival?