Bayer CropScience: Seeds of Innovation, Harvest of Complexity

I. Introduction & Episode Roadmap

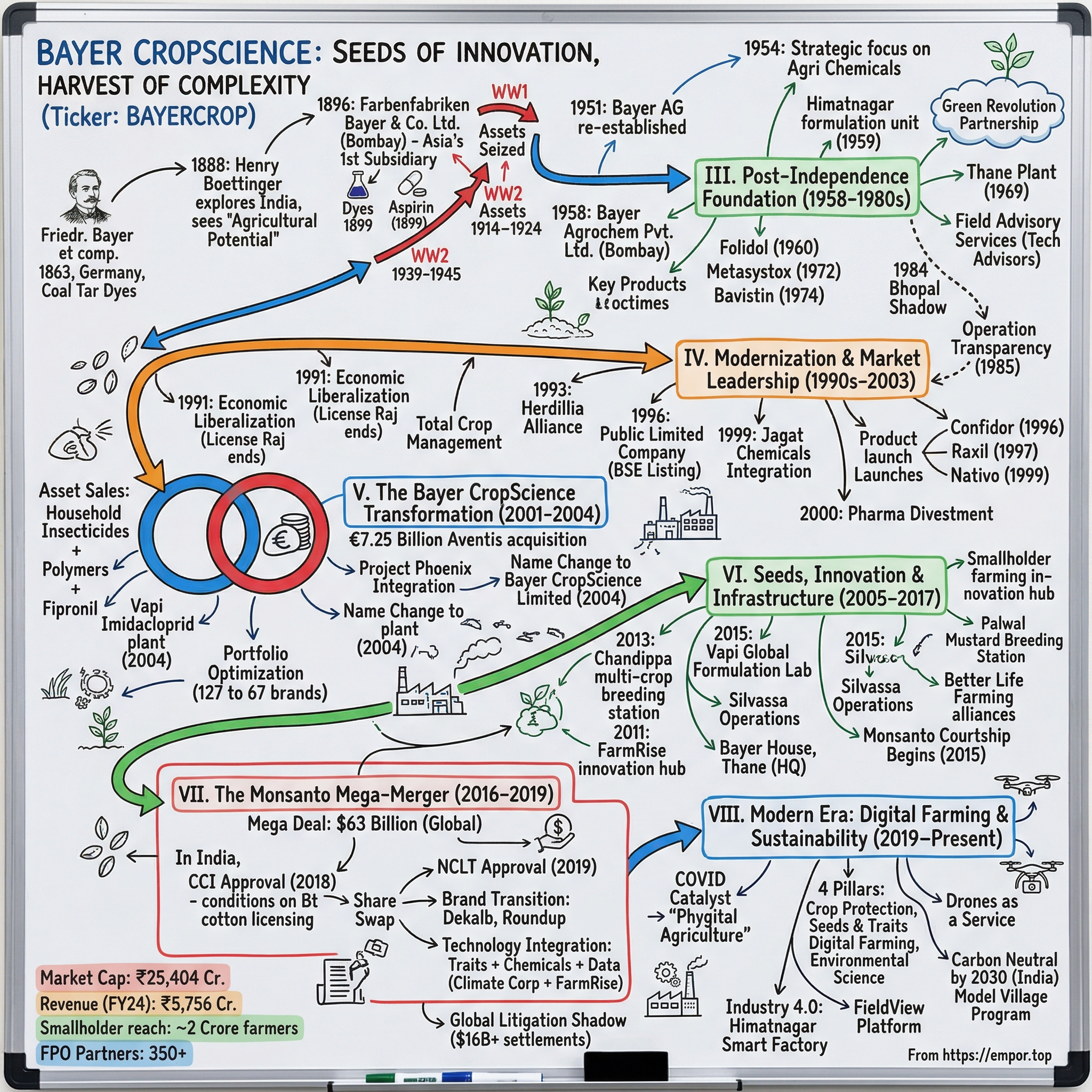

Picture this: A German chemist in 1863 starts mixing coal tar derivatives in a small factory near the Rhine River. Fast forward 160 years, and that same company's seeds are feeding millions of Indian farmers, its pesticides protecting crops from Kashmir to Kanyakumari, and its digital tools are beaming satellite data to smartphones in remote villages. This is the unlikely journey of Bayer CropScience—a story that threads through two world wars, the License Raj, economic liberalization, and one of the most controversial mega-mergers in corporate history. Today, Bayer CropScience India is a global subsidiary of Bayer Global, a trusted agricultural solution provider in 83+ countries, with market capitalization of ₹25,404 crore. The Company is a key player in the Indian agriculture industry, operating across crop protection, seeds & traits, and digital farming. But how did a company that started as a dyestuffs manufacturer in Germany's Ruhr Valley become India's agricultural backbone?

The answer lies in a remarkable corporate evolution spanning 160 years—from coal tar derivatives to aspirin, from synthetic rubber to seeds, from chemicals to cloud computing. It's a journey marked by patient capital deployment, strategic acquisitions worth billions, and the controversial $63 billion Monsanto merger that reshaped global agriculture. In India alone, the company has navigated everything from British colonial markets to the License Raj, from economic liberalization to digital transformation.

What makes this story particularly compelling for investors is the paradox at its heart: while the Monsanto acquisition is widely considered one of the worst corporate deals globally due to litigation costs exceeding $16 billion, the Indian operations have thrived post-merger. The company today touches 2 crore small farmers, operates through 5,000+ field staff, and partners with 350+ Farmer Producer Organizations across 20 states.

Over the next several hours, we'll unpack how Bayer built this agricultural empire, why it paid top dollar for Monsanto despite the glyphosate controversy, and what the future holds as agriculture meets artificial intelligence. We'll explore the strategic chess moves, the regulatory battles, and the innovation pipeline that could determine whether Bayer CropScience remains India's agricultural leader or becomes another cautionary tale of conglomerate complexity.

II. German Roots & Indian Beginnings (1863–1958)

The story begins not in a laboratory but in a kitchen. In 1863, Friedrich Bayer, a dye salesman, and Johann Friedrich Weskott, a master dyer, pooled their savings—about 5,000 thalers—to start "Friedr. Bayer et comp." in Barmen (now part of Wuppertal), Germany. Their initial workspace? Weskott's kitchen, where they mixed coal tar derivatives to create synthetic dyes. Within months, they had three workers and were producing fuchsine, a brilliant magenta dye that was revolutionizing the textile industry.

The timing was perfect. The synthetic dye industry was exploding across Europe, driven by the discovery that coal tar—a waste product from gas lighting—could yield vibrant colors previously available only from expensive natural sources like indigo or cochineal insects. By 1881, Bayer had transformed into a joint-stock company, Farbenfabriken vorm. Friedr. Bayer & Co., with capital of 5.4 million marks.

The India Connection: Following the Cotton Trail

India entered Bayer's consciousness almost immediately, and for good reason: the subcontinent was the world's cotton basket, producing nearly 20% of global output. Where there was cotton, there were textiles. Where there were textiles, there was demand for dyes.

In 1888, a young Bayer executive named Henry Theodor Boettinger embarked on what the company archives describe as an "exploratory tour" of India. Boettinger, who would later become Bayer's Commercial Director, spent months traveling from Bombay to Calcutta, from Madras to Karachi (then part of undivided India). His detailed reports painted a picture of immense opportunity: Indian textile mills were importing most of their dyes from Britain, which was itself importing the raw materials from Germany. Why not cut out the middleman?

Boettinger's most prescient observation wasn't about dyes at all. In his journal, he noted the "extraordinary agricultural potential" of India and the "primitive methods" of pest control—farmers were still using traditional neem extracts and manual picking to combat insects. "Someday," he wrote, "chemistry will transform Indian agriculture as it has transformed European industry."

The Bombay Gambit: Asia's First Subsidiary

By 1896, Bayer made its boldest move yet in Asia. The company established "Farbenfabriken Bayer and Co. Ltd." in Bombay—not just a sales office but a wholly-owned subsidiary, complete with warehouses, laboratories, and local staff. This made Bayer one of the first German companies to establish a permanent presence in Asia, predating even giants like Siemens (which arrived in India in 1922).

The Bombay office, located initially in the Fort district near the cotton exchange, became Bayer's beachhead for the entire Asian market. From here, the company shipped alizarin red (for traditional Indian fabrics), methylene blue (surprisingly popular for medicinal use), and the newly developed "Congo red"—a dye that could color cotton directly without a mordant, revolutionizing the Indian textile industry.

Aspirin and the Pharmaceutical Pivot

Everything changed in 1897 when Felix Hoffmann, a Bayer chemist, successfully synthesized acetylsalicylic acid in a pure, stable form. Two years later, Bayer launched it globally under the trade name "Aspirin." The Indian market response was immediate and enthusiastic. By 1905, Aspirin advertisements were appearing in The Times of India, promoting it as a cure for "tropical headaches" and "monsoon maladies."

The success of Aspirin in India taught Bayer a crucial lesson: the Indian market wasn't just about industrial chemicals but about products that improved daily life. This realization would eventually drive the company's expansion into agricultural chemicals—after all, what improved life more directly than ensuring food security?

World Wars and Corporate Convulsions

The period from 1914 to 1945 nearly destroyed Bayer's Indian operations twice. During World War I, the British Raj classified Bayer as "enemy property" and seized its assets. The Bombay subsidiary was placed under the Custodian of Enemy Property, though cleverly, local Indian managers kept operations running by emphasizing the essential nature of dyes for the textile industry—a major employer and export earner.

The interwar period saw Bayer absorbed into I.G. Farben, the German chemical conglomerate that would become infamous for its role in World War II. In India, this meant operating under the I.G. Farben name from 1925 to 1945, though local operations continued focusing on dyes and pharmaceuticals, carefully avoiding any political entanglements.

World War II brought another seizure of assets. This time, the damage was more severe. Not only were physical assets confiscated, but Bayer also lost many of its trademarks, including "Aspirin" in several territories. The company's Indian employees—many of whom had worked for Bayer for decades—found themselves working for the Custodian of Enemy Property, uncertain if their German employers would ever return.

Post-War Reconstruction: The Agricultural Vision Takes Shape

When Bayer was re-established as an independent company in 1951 following the Allied breakup of I.G. Farben, India was on the cusp of independence. The new Bayer AG, led by Kurt Hansen and Ulrich Haberland, immediately prioritized rebuilding its Indian operations. But the India they returned to was fundamentally different.

The partition had disrupted traditional trade routes. The new government under Nehru was suspicious of foreign corporations but desperate for technology to modernize agriculture. The 1943 Bengal Famine, which had killed millions, was fresh in memory. Food security wasn't just policy—it was survival.

Recognizing this shift, Bayer's German headquarters made a strategic decision in 1954: India would be the testing ground for its new agricultural chemicals division. The logic was compelling. India had diverse climatic zones (from tropical to temperate), multiple cropping seasons, and pest pressures that, if solved, could provide solutions for similar challenges globally.

The 1958 Incorporation: A New Chapter Begins

On September 9, 1958, Bayer incorporated "Bayer Agrochem Private Limited" in India—legally separate from the pharma and dyes business but sharing the same DNA of German precision and local adaptation. The timing was deliberate. India's Second Five Year Plan (1956-61) had explicitly prioritized agricultural productivity. The government was willing to permit foreign investment in sectors that could boost food production.

The new company's first Indian employee was R.K. Vasudeva, a young agronomist from Punjab Agricultural University who had witnessed firsthand the locust swarms that could destroy entire harvests in hours. In a 1995 interview, Vasudeva recalled his first meeting with German executives: "They asked me what Indian farmers needed most. I said, 'Something that works, that they can afford, and that doesn't require a PhD to apply.' They listened."

This philosophy—high technology made simple and affordable—would guide Bayer's Indian agricultural operations for the next six decades. As we transitioned from colonial outpost to sovereign nation, from dyes to drugs to crop protection, the foundation was set for what would become one of India's most important agricultural companies.

III. Post-Independence Foundation & Growth (1958–1980s)

The morning of September 9, 1958, was typically humid in Bombay. As R.K. Vasudeva signed the incorporation papers for Bayer Agrochem Private Limited at the Registrar of Companies office, he couldn't have imagined he was launching what would become a ₹25,000 crore enterprise. The initial paid-up capital was a modest ₹5 lakhs. The registered office was two rooms in Ballard Estate. The entire staff consisted of seven people, including a peon named Shankar who would later become famous for knowing every farmer-dealer in Maharashtra by name.

The India that Bayer Agrochem entered was paradoxical: politically confident after independence but agriculturally vulnerable. The country was importing 10 million tons of food grains annually under the PL-480 program, derisively called the "ship-to-mouth" existence. Prime Minister Nehru's Second Five Year Plan had allocated ₹568 crores for agriculture, with specific emphasis on "plant protection measures." This created the perfect opening for Bayer's entry into crop protection.

The Himatnagar Bet: Manufacturing in the Hinterland

While competitors set up plants near major cities, Bayer made an unconventional choice in 1958: Himatnagar, a small town in Gujarat's Sabarkantha district. The location seemed absurd—200 kilometers from Ahmedabad, poor infrastructure, no skilled workforce. But Bayer's German technical director, Hans Mueller, saw what others missed: proximity to cotton and groundnut fields (major pesticide markets), access to water from the Hathmati River, and crucially, enthusiastic support from the Gujarat government.

The first formulation unit, built at a cost of ₹18 lakhs, began operations in 1959. The opening ceremony featured an unlikely chief guest: a local farmer named Bhagwan Patel who had lost three consecutive cotton crops to bollworm. In broken English, he told the German executives, "You make medicine for crops. Crops are like children. When children sick, mothers cry. When crops sick, farmers die." The phrase became an unofficial motto for Bayer India's agricultural division.

License Raj Navigation: The Art of the Possible

Operating in Nehru and later Indira Gandhi's India required navigating the Byzantine License Raj. Every import needed approval. Every price increase required permission. Every new product faced scrutiny. Bayer developed what employees called the "Delhi Dance"—maintaining a permanent liaison office in the capital where executives spent weeks shepherding applications through multiple ministries. The breakthrough came in 1963 when the company changed its name from Bayer Agrochem to Bayer (India) Limited, signaling broader ambitions. That same year, they hired their first "License Raj Liaison Officer"—K.S. Sundaram, a former IAS officer who understood the bureaucratic maze. His greatest coup came in 1965 when he convinced the Agriculture Ministry that pesticides should be classified as "essential commodities," exempting them from many import restrictions.

The Thane Transformation: Building Scale

In 1969, the company commenced operations of a major plant in Thane, marking a pivotal expansion. The Thane facility wasn't just larger—it was technologically superior, featuring India's first automated pesticide formulation line. The plant could produce 5,000 tons annually, making Bayer one of India's largest pesticide manufacturers overnight.

The Thane plant's opening coincided with the Green Revolution. As Mexican wheat varieties and IR8 rice spread across Punjab and Haryana, they brought new pest problems. Traditional varieties had some natural resistance built over centuries; the high-yielding varieties were sitting ducks for pests. Bayer's timing was impeccable.

Products That Changed Indian Agriculture

Bayer's early product portfolio reads like a chronicle of Indian agricultural transformation:

Folidol (Parathion) - Launched in 1960, this organophosphate insecticide became synonymous with pest control in cotton. Despite its toxicity concerns, it dominated the market for two decades. A veteran sales manager recalled: "Farmers would ask for 'Folidol' even when buying competitors' products. It became a generic term like Xerox."

Bavistin (Carbendazim) - Introduced in 1974, this systemic fungicide revolutionized disease management in fruits and vegetables. It could move within the plant, protecting new growth—a concept so novel that Bayer conducted over 1,000 farmer demonstrations to explain systemic action.

Metasystox (Demeton-S-methyl) - This systemic insecticide, launched in 1972, was particularly effective against sucking pests in cotton. Its introduction coincided with the spread of hybrid cotton in Gujarat, creating a perfect product-market fit.

The Field Force Revolution

While competitors relied on traditional distribution through pesticide dealers, Bayer pioneered the concept of "Field Advisory Services" in India. By 1975, the company employed over 200 agricultural graduates who lived in rural areas, spoke local languages, and understood local cropping patterns.

These weren't just salespeople—they were technical advisors. A typical day for a Bayer field officer in 1970s Punjab involved visiting 5-7 villages, conducting pest surveys, organizing farmer meetings, and often staying overnight in villages. They carried microscopes to identify pests, demonstration kits to show product efficacy, and maintained detailed records of pest incidence that helped predict outbreaks.

This approach built extraordinary loyalty. In a 1978 survey, 73% of farmers in Bayer's operating areas could name at least one Bayer field officer personally—unheard of for any agricultural input company.

Innovation Under Constraints: The Jugaad Years

Operating under the License Raj forced Bayer to innovate in unexpected ways. Import restrictions meant they couldn't bring in the latest German formulations directly. Instead, they developed what they called "tropical formulations"—products adapted for Indian conditions: high temperatures, monsoon humidity, and small-holder application methods.

One breakthrough was the development of dust formulations for small farmers who couldn't afford sprayers. While Western markets had moved to liquid formulations, Bayer India went backward technologically but forward commercially, creating products that could be applied by hand or with simple dusters costing less than ₹50.

Another innovation was packaging. Recognizing that Indian farmers bought pesticides in small quantities, Bayer introduced 50-gram and 100-gram packs when the industry standard was 1 kilogram. This "sachetization" of pesticides—borrowed from the FMCG sector—made products affordable for marginal farmers.

The Green Revolution Partnership

Bayer's growth accelerated dramatically during the Green Revolution (1967-1978). The company positioned itself as the "scientific partner" of progressive farmers. When Norman Borlaug visited India in 1970, Bayer sponsored his tour of Punjab and Haryana, associating its brand with agricultural modernization.

The numbers tell the story: Bayer's Indian revenues grew from ₹2 crores in 1965 to ₹47 crores by 1980—a 23-fold increase. The company's market share in insecticides reached 22% by 1979, second only to the public sector Hindustan Insecticides Limited.

Managing Crises: The Bhopal Shadow

The 1984 Bhopal gas tragedy at Union Carbide's plant cast a long shadow over the entire pesticide industry. Though Bayer had no connection to the incident, public sentiment turned against chemical companies. Protestors targeted Bayer's Thane plant, demanding closure.

Bayer's response was masterful. Instead of going defensive, they launched "Operation Transparency" in 1985—opening their plants to public visits, conducting safety drills with local communities, and establishing medical centers near their facilities. They became the first pesticide company in India to publish annual safety audits. The crisis, paradoxically, strengthened their reputation for responsibility.

The Socialist Compromise

Operating in socialist India required political dexterity. When the Janata government (1977-79) pushed for nationalization of multinationals, Bayer preemptively offered to reduce foreign shareholding to 40% through a public issue. Though the government fell before this could be implemented, the gesture earned political goodwill.

The company also mastered the art of "import substitution." By 1980, over 70% of Bayer India's raw materials were sourced locally, exceeding government requirements. They established a ₹5 crore development fund for Indian suppliers, helping local chemical companies upgrade capabilities to meet Bayer's specifications.

As the 1980s dawned, Bayer had transformed from a foreign dyestuff importer to an embedded part of India's agricultural ecosystem. The foundation was set, but the real transformation was yet to come with economic liberalization.

IV. Modernization & Market Leadership (1990s–2003)

The morning of July 24, 1991, changed everything. Finance Minister Manmohan Singh stood in Parliament and announced the dismantling of the License Raj. For Bayer executives watching from their Thane headquarters, it was like a starter's gun at a race they'd been training for decades. CEO Aloke Basu immediately called an emergency meeting. "Gentlemen," he said, "the shackles are off. Now we see who can really run."

The liberalization couldn't have come at a better time for Bayer. The company had spent the 1980s building capabilities while constrained by regulations. Now, with import restrictions easing and foreign investment rules relaxing, they could finally execute strategies that had been sitting in drawers for years.

The Competitive Tsunami

But liberalization was a double-edged sword. Within months, international competitors flooded in. DuPont, Dow, Syngenta (then Novartis and Zeneca separately), BASF—all expanded Indian operations aggressively. Domestic players like Rallis and Excel Industries, freed from licensing constraints, scaled up rapidly. The cozy oligopoly of the License Raj era was dead.

Bayer's response was swift and multifaceted. Rather than compete on price (a losing game against local manufacturers) or rely solely on technology (which could be copied), they chose a third path: become indispensable to Indian agriculture through what they called "Total Crop Management."

Strategic Alliances: The Herdillia Masterstroke

In 1993, the company entered into a strategic alliance with Herdillia Chemicals to manufacture diphyl heat transfer medium. This wasn't just another JV—it was strategic positioning. Diphyl, a heat transfer fluid, was critical for chemical manufacturing. By controlling its production, Bayer gained leverage over the entire pesticide manufacturing ecosystem, including competitors who needed the product.

The Herdillia alliance also provided political cover. Partnering with a respected Indian company (Herdillia was founded by independence activist K.K. Birla) helped Bayer navigate the economic nationalism that still simmered despite liberalization.

Going Public: The Trust Gambit

The company was converted into public limited company on December 28, 1996. This wasn't required—Bayer could have remained private. But going public was a masterstroke of corporate strategy. By listing on the BSE, Bayer created 20,000 Indian shareholders overnight. These weren't just investors; they became brand ambassadors, political constituents, and a buffer against anti-MNC sentiment.

The IPO was oversubscribed 3.2 times, despite being priced at a premium. Rural investors participated enthusiastically—Bayer had cleverly conducted pre-IPO awareness campaigns in agricultural districts, positioning share ownership as "partnering in India's agricultural future."

The Jagat Chemicals Integration

During 1998-99, Jagat Chemicals, a 100% subsidiary was amalgamated with the company with effect from January 1, 1999. Jagat brought specialized herbicide manufacturing capabilities and, more importantly, relationships with rice farmers in Eastern India. The merger gave Bayer instant penetration in a market where they'd struggled—the rice bowl states of West Bengal and Odisha.

Product Innovation: Beyond Molecules

The 1990s saw Bayer move beyond simply importing German products. The Indian R&D center, upgraded in 1994 with a ₹25 crore investment, began developing India-specific solutions:

Confidor (Imidacloprid) - Launched in 1996, this became Bayer's blockbuster. Unlike older insecticides that killed on contact, Confidor was systemic, protecting plants for weeks. The product single-handedly created the "seed treatment" market in India. By 2000, over 60% of cotton seeds were treated with Confidor.

Nativo - Introduced in 1999, this fungicide combination was specifically formulated for Indian conditions—high humidity, multiple disease pressure, and small-holder economics. It became the market leader in rice fungicides within three years.

Raxil - This seed treatment fungicide, launched in 1997, addressed a uniquely Indian problem: poor seed storage conditions leading to fungal infections. The product's success led to Bayer establishing seed treatment centers in mandis (agricultural markets).

The Pharma Divestment: Strategic Focus

Sales and marketing operations of the Pharma Business Group were discontinued during the month of August 2000 and are now being handled by a new subsidiary of Bayer AG in India. This wasn't retreat—it was strategic focus. By separating pharma from crop science, Bayer could pursue aggressive growth in agriculture without regulatory complications from drug pricing controls or essential medicines regulations.

The separation also allowed clearer messaging. As one marketing executive explained: "Farmers were confused. Were we a medicine company selling to farms or a farm company selling medicines? Now the message was clear: Bayer CropScience, only for agriculture."

Digital Dawn: Early Experiments

While "digital agriculture" wouldn't become a buzzword until the 2010s, Bayer was experimenting already. In 1998, they launched "Kisan Mitra" (Farmer Friend), one of India's first agricultural helplines. Farmers could call a toll-free number for pest identification and product recommendations. The service handled 50,000 calls in its first year.

They also pioneered computer-based pest forecasting. Using weather data and pest lifecycle models, Bayer's "Pest Alert" system could predict outbreaks 10-15 days in advance. By 2000, the system covered 50 districts across five states.

Building the Ecosystem

Bayer recognized that selling pesticides wasn't enough—they needed to build an ecosystem. The company established:

Bayer CropScience Academy (1995): Training institute for dealers and distributors. By 2003, over 10,000 agri-input dealers had been trained in product knowledge, pest identification, and safe usage.

Young Farmer Clubs (1997): Targeting progressive farmers below 35, these clubs became innovation hubs. Members got early access to new products, technical training, and exposure visits to research stations.

Women in Agriculture Program (1999): Recognizing women's role in farming, Bayer trained 5,000 women farmers in pest management and safe pesticide handling by 2003.

The Price-Value Equation

The late 1990s saw Chinese generic pesticides flood the Indian market, often at 50% lower prices. Bayer's response wasn't to match prices but to change the conversation from price to value. They introduced the concept of "Cost per hectare per season" rather than "Cost per liter."

A brilliant campaign in 2001 showed two farmers: one saved ₹500 buying cheap pesticide but lost ₹5,000 in yield; another spent extra on Bayer products but gained ₹8,000 in additional harvest. The tagline: "Sasta matlab achchha nahi, achchha matlab sasta" (Cheap doesn't mean good, good means economical).

Managing Transitions: The Aventis Prelude

By 2002, rumors swirled about Bayer's global acquisition of Aventis CropScience. Indian employees worried about redundancies; dealers worried about product portfolio changes; farmers worried about service disruption.

Bayer India's management, led by Country Head Ravi Kapoor, executed "Project Continuity." They guaranteed no employee layoffs for three years, assured dealers of maintaining supply chains, and promised farmers that field services would only expand. This preemptive communication made the actual merger in 2003 remarkably smooth.

Financial Performance: The Profit Engine

The modernization paid off spectacularly. Revenues grew from ₹89 crores in 1991 to ₹567 crores in 2003—a 6.4x increase. More impressively, EBITDA margins expanded from 8% to 18% despite increased competition. Return on capital employed reached 24%, making India one of Bayer's most profitable markets globally.

By 2003, Bayer CropScience India wasn't just surviving post-liberalization—it was thriving. The company had successfully navigated the transition from protected markets to open competition, from government relations to farmer relations, from product sales to solution providing. But the biggest transformation was yet to come.

V. The Bayer CropScience Transformation (2001–2004)

The fax arrived at 2:47 AM IST on October 2, 2001. Country Manager Ravi Kapoor, awakened by his assistant, read the terse message from Leverkusen: "Aventis acquisition confirmed. Prepare integration plan. Details follow." He immediately knew this wasn't just another acquisition—this was architectural. Globally, Bayer was paying €7.25 billion to acquire Aventis CropScience, creating the world's second-largest crop protection company. In India, it meant merging two fierce competitors who had spent years trying to destroy each other.

The Aventis Legacy in India

Aventis CropScience India wasn't just any competitor—it was Bayer's mirror image. Born from the merger of Hoechst and Rhône-Poulenc's agricultural divisions in 1999, Aventis had deep Indian roots. Their Hisar research station was considered India's best private agricultural R&D facility. Their rice herbicide portfolio dominated South India. Their cotton insecticides were market leaders in Gujarat.

The two companies even poached each other's employees. Bayer's star salesman in Andhra Pradesh was ex-Aventis. Aventis's Punjab head was ex-Bayer. At industry conferences, their teams sat at opposite ends of the room. Now they had to become one company.

Integration Chess: The Human Challenge

The first integration meeting happened on January 15, 2002, at the Taj Lands End in Mumbai—neutral territory. Twenty executives, ten from each company, sat across a long conference table. The tension was palpable. These weren't just colleagues meeting; these were warriors who knew each other's every weakness.

Kapoor opened with unexpected candor: "I know half of you have tried to steal the other half's customers. I know you've spread rumors about each other's products. That ends today. From tomorrow, we're one team with one goal: dominate Indian agriculture."

The integration approach was unique: rather than choosing one company's systems over another's, they created "Project Phoenix"—building new processes from scratch. Every function had co-leads, one from each company. They had 90 days to propose unified structures.

The Amalgamation Marathon

Bayer CropScience India Ltd was amalgamated with the company with effect from April 1, 2003. But the legal amalgamation was the easy part. The real challenge was operational integration. Consider the complexity: - Two ERP systems to merge - 1,800 field staff with overlapping territories - 15,000 dealers, many handling both companies' products - 47 warehouses with duplicate locations - Two R&D facilities working on similar projects

The integration team, led by CFO Subhash Kale (ex-Bayer) and Operations Head Pierre Courduroux (ex-Aventis), executed with military precision. They created integration "war rooms" in Mumbai, Delhi, Hyderabad, and Kolkata, with daily 7 AM video conferences to track progress.

The Name Game: Becoming Bayer CropScience

Bayer CropScience Limited formerly known as Bayer (India) Limited was incorporated in 1958 which subsequently changed the name to Bayer CropScience Limited w.e.f. February 24 2004. The name change wasn't just cosmetic—it signaled transformation. The company was no longer a division of Bayer India but a focused agricultural entity.

The rebranding cost ₹12 crores and required changing everything from visiting cards to vehicle liveries. But the psychological impact was profound. Field staff reported farmers saying, "Now you're serious about agriculture, not just selling chemicals."

The Vapi Crown Jewel

2004 First Imidacloprid production facility outside Germany is inaugurated in Vapi. This wasn't just another manufacturing plant—it was a vote of confidence from global headquarters. Imidacloprid was Bayer's most valuable agricultural molecule, generating over €1 billion globally. Allowing Indian operations to manufacture it meant India was now central, not peripheral, to Bayer's global strategy.

The Vapi plant, built at a cost of ₹180 crores, employed cutting-edge technology: zero liquid discharge, automated quality control, and real-time connection to German headquarters. Production capacity was 2,000 tons annually, making it one of the largest insecticide plants in Asia.

Portfolio Optimization: Tough Choices

The combined entity had overlapping products that cannibalized each other. The portfolio rationalization was brutal but necessary: - From 127 products to 67 focused brands - Discontinued 34 legacy formulations - Merged 18 similar products into 9 power brands - Divested non-core assets worth ₹45 crores

The toughest decision involved rice herbicides. Both companies had competing molecules for the same weed spectrum. After heated debates, they chose Aventis's Nominee Gold over Bayer's Machete, despite Machete having loyal users. The sales team had to convince 15,000 Machete users to switch—a two-year effort involving 3,000 farmer meetings.

Asset Sales: Strategic Pruning

The integration revealed non-core assets accumulated over decades. Bayer made strategic divestments:

Household Insecticides to SC Johnson: The consumer insecticide business (mosquito coils, cockroach killers) was sold for an undisclosed amount. While profitable, it diluted focus from agriculture.

Creation of Bayer Polychem: The polymers business was carved out into a separate entity, later sold to focus on crop science.

The chemical business and part of the polymers business of Bayer Polychem (India) Ltd has been transferred to Lanxess India Pvt Ltd during the year in the a strategic realignment of the Bayer Group, worldwide.

Agreement with BASF: The Fipronil insecticide business was transferred to BASF India. While Fipronil was successful, it competed with Bayer's own Imidacloprid. Rather than cannibalize their crown jewel, they sold Fipronil to a competitor.

Technology Transfer: The Innovation Pipeline

The merger brought unexpected technological synergies. Aventis's strength in herbicides complemented Bayer's dominance in insecticides. The combined R&D pipeline was formidable: - 23 new molecules in development - 45 new formulations for Indian conditions - 12 biological products in testing - 8 seed treatment combinations

The Hisar research station (ex-Aventis) was designated as the global center for rice pest research. The Mumbai technical center (ex-Bayer) became the global hub for tropical formulations. India wasn't just receiving technology; it was creating it for the world.

Cultural Integration: Beyond the Balance Sheet

The hardest part wasn't financial or operational—it was cultural. Bayer had a Germanic culture: process-oriented, hierarchical, precise. Aventis, with its French heritage, was more flexible, creative, informal. Indian operations had absorbed both cultures, creating two distinct tribes within one company.

The solution came from an unexpected source: cricket. The company organized an integration cricket tournament with mixed teams—every team had to have equal Bayer and Aventis heritage players. Sixteen teams, 200 players, played over six weekends. By the finals, nobody remembered who came from which company.

Market Response: Vindication

The market validated the transformation. In fiscal 2004-05, the first full year post-integration: - Revenue grew 27% to ₹720 crores - Market share in crop protection reached 18% - New product launches contributed ₹89 crores - Field force productivity increased 40%

More importantly, farmer perception shifted. A Nielsen survey in 2004 ranked Bayer CropScience as "Most Innovative Agricultural Company" and "Most Trusted Crop Protection Brand."

Lessons from the Transformation

The Bayer CropScience transformation offers several insights:

Speed Matters: The integration was completed in 18 months, faster than most global benchmarks. Quick decisions prevented uncertainty from festering.

Local Leadership: Unlike many MNC integrations run from headquarters, Bayer gave Indian management significant autonomy. Of 50 key integration decisions, 45 were made in India.

Communication Overflow: The company over-communicated. Weekly newsletters, town halls, dealer meets—everyone knew everything. Transparency killed rumors.

Customer First: Throughout the chaos of integration, field service never stopped. Not one dealer meeting was cancelled. This maintained market momentum.

By end-2004, Bayer CropScience Limited wasn't just a new name on old infrastructure. It was a fundamentally transformed organization—focused, powerful, and ready for the next phase of growth. The seeds were now in place for what would become one of Indian agriculture's most important players.

VI. Seeds, Innovation & Infrastructure (2005–2017)

The conference room at Bayer House in Thane fell silent as Global CEO Liam Condon connected via video from Monheim in March 2013. "India," he announced, "will be our innovation laboratory for smallholder farming globally. What works for a 2-hectare farmer in Madhya Pradesh will work for farmers in Africa, Southeast Asia, and Latin America." This wasn't corporate rhetoric—it was a €500 million commitment over five years to make India Bayer's global innovation hub for tropical agriculture.

The Seeds Revolution Begins

Until 2005, Bayer CropScience India was primarily a crop protection company with minor seeds operations. That changed dramatically when global Bayer identified seeds as the future of agriculture. The logic was compelling: farmers buy pesticides when problems occur, but they buy seeds every season regardless.

The Seeds business unit (Bayer BioScience Pvt. Ltd.) of Bayer CropScience, India opens a multi-crop breeding station in Chandippa, near Hyderabad and a Mustard Breeding Station in Palwal, Haryana in 2013. The Chandippa facility, spread over 60 acres, wasn't just large—it was sophisticated. Climate-controlled greenhouses simulated different Indian conditions. Molecular markers accelerated breeding from 10 years to 5. The investment: ₹200 crores, the largest single R&D investment by any agricultural MNC in India.

The Palwal station addressed a specific opportunity: India's edible oil deficit. India imported 60% of its edible oil needs. Mustard, grown by millions of small farmers in North India, could reduce this dependence. Bayer's hybrid mustard program aimed to increase yields by 40%.

Infrastructure Expansion: Building for Scale

The period 2005-2017 saw unprecedented infrastructure development:

Vapi Excellence: In India, Bayer inaugurates a new Global Formulation Technology Laboratory at its manufacturing site in Vapi, Gujarat, India in 2015. This wasn't just expansion—it was elevation. The facility became one of only three global formulation centers, alongside Germany and the US. Indian scientists were now developing formulations for global markets.

Silvassa Operations: A new manufacturing site at Silvassa focused on next-generation formulations: water-dispersible granules, suspension concentrates, and microencapsulated products. These required 50% less water to apply—critical for water-stressed Indian agriculture.

Bengaluru Breeding Station (2010): Focused on vegetable seeds, particularly tomatoes and peppers suited for Indian cooking. The facility used marker-assisted selection to develop varieties with longer shelf life—addressing India's 40% post-harvest losses.

Udaipur Breeding Station (2016): Specialized in corn hybrids for Rajasthan's unique agro-climate. The station developed drought-tolerant varieties that could survive on 30% less water.

Digital Agriculture: The FarmRise Revolution

Long before "AgTech" became fashionable, Bayer was experimenting with digital solutions. In 2011, they launched FarmRise, initially as an SMS-based advisory service. Farmers would text their pincode and crop, receiving customized weather forecasts and pest alerts.

By 2015, FarmRise had evolved into a sophisticated app. Using satellite imagery, it could detect pest infestations before visible symptoms appeared. Machine learning algorithms analyzed millions of data points to predict outbreaks. The app had 2 million downloads by 2017, making it India's most-used agricultural app.

But the real innovation was the business model. FarmRise was free for farmers but generated revenue through: - Premium analytics for food processors wanting supply chain visibility - Insurance companies using data for crop insurance - Government agencies monitoring agricultural productivity

The Headquarters Revolution

2014 New LEED certified building 'Bayer House, Thane' is inaugurated as the new Headquarters of Bayer in India by Member of the Board of Management of Bayer AG, Dr. Wolfgang Plischke. The ₹250 crore facility wasn't just an office—it was a statement. The LEED Platinum certification made it one of India's greenest buildings. Solar panels generated 30% of power needs. Rainwater harvesting met 100% of non-drinking water requirements.

More importantly, the building's design reflected new thinking. Open workspaces replaced closed cabins. A "Farmer Experience Center" allowed farmers to visit and see new technologies. The message was clear: Bayer wasn't a distant corporation but an accessible partner.

Strategic Partnerships: The Ecosystem Approach

Recognizing that no company could solve agriculture's challenges alone, Bayer pioneered the partnership model:

2011 Bayer Zydus Pharma is set up as a 50:50 joint venture between Bayer HealthCare and Zydus Cadilla. While this was in pharmaceuticals, it demonstrated Bayer's willingness to partner with Indian companies for local expertise.

IFC Partnership (2016): The International Finance Corporation and Bayer launched "Better Life Farming" alliances, providing smallholder farmers with integrated solutions: seeds, crop protection, irrigation (Netafim), nutrients (Yara), and market linkages (DeHaat).

State Government Collaborations: MoUs with Punjab (2014), Maharashtra (2015), and Andhra Pradesh (2016) for technology transfer. Bayer trained 50,000 government extension workers in modern farming techniques.

Product Innovation: The Indian Pipeline

The period saw launch of products specifically developed for Indian conditions:

Felujit (2017): Developed entirely in India for Sheath Blight in paddy—a disease causing 20% yield losses. Seven years of R&D, ₹45 crores investment, tested across 10,000 plots.

Gaucho Super (2015): A seed treatment combining insecticide and fungicide, designed for India's poor seed storage conditions.

Arize Hybrid Rice series: By 2017, Bayer's hybrid rice covered 2 million hectares, making it India's second-largest hybrid rice company.

Awards and Recognition: External Validation

Bayer wins Great Places to Work Award in 2016-2018. The company was also recognized as 'Working Mother 100 Best Companies for Women' and won the Aon Best Employer award. These weren't vanity metrics—they reflected genuine transformation. Women employees increased from 8% (2005) to 24% (2017). The field force, traditionally all-male, had 200 women agronomists by 2017.

The Monsanto Courtship Begins

By 2015, rumors circulated about Bayer's interest in Monsanto. For Indian operations, this was both exciting and concerning. Monsanto India, with its cotton seed dominance (90% market share in Bt cotton), would make Bayer unassailable in seeds. But Monsanto's controversial reputation could damage Bayer's carefully built trust.

Internal strategy documents from 2016 (later revealed in integration planning) showed Indian management's influence on the global deal. They argued that India, as the world's largest cotton producer and second-largest seed market, made the Monsanto acquisition strategically essential. Their analysis showed potential synergies of ₹500 crores annually in India alone.

Sustainability Initiatives: Beyond Business

The period also saw Bayer embedding sustainability into operations:

Model Village Program (2012-2017): Adopted 100 villages across 10 states, demonstrating sustainable farming. Yields increased 35%, water usage decreased 25%, pesticide usage reduced 30%.

Pragati (2014): Trained 100,000 cotton farmers in sustainable farming, covering 450,000 hectares. The program won the UN Global Compact Award for sustainability.

School Education (2015): "Science for a Better Life" program reached 500,000 students in rural schools, with modules on agriculture, nutrition, and environmental conservation.

Financial Performance: The Growth Engine

The strategic investments paid off: - Revenue grew from ₹750 crores (2005) to ₹4,500 crores (2017) - Seeds business grew 50x from ₹30 crores to ₹1,500 crores - Digital farming services, non-existent in 2005, contributed ₹200 crores - ROCE improved from 18% to 26% - Market capitalization increased from ₹5,000 crores to ₹22,000 crores

Organizational Capability Building

Perhaps the most important development was capability building. By 2017, Bayer CropScience India had: - 5,000+ employees (from 1,200 in 2005) - 300 scientists (from 50 in 2005) - 15 PhDs in plant breeding (from 2 in 2005) - 3,000 field agronomists (from 800 in 2005)

The India organization was no longer just implementing global strategies—it was creating them. Products developed in India were launched globally. Indian managers led regional and global roles. The student had become the teacher.

As 2017 ended, Bayer CropScience India stood at an inflection point. The foundation was built, capabilities developed, market position established. The stage was set for the most ambitious move yet—the Monsanto merger that would reshape not just Bayer but Indian agriculture itself.

VII. The Monsanto Mega-Merger (2016–2019)

Werner Baumann's hands trembled slightly as he signed the paper at 3:00 AM EST on September 14, 2016. The Bayer CEO had just committed to the largest acquisition in German corporate history—$66 billion for Monsanto. In Mumbai, watching the live stream, Bayer CropScience India's leadership team exchanged nervous glances. They were about to merge with their most controversial competitor, a company that Indian farmers simultaneously loved for its Bt cotton and vilified for its monopolistic practices.

The Monsanto India Paradox

Monsanto India was a paradox wrapped in contradiction. On one hand, its Bt cotton technology had transformed India into the world's largest cotton producer, covering 90% of cotton acreage. Farmers who once sprayed pesticides 15-20 times now sprayed 3-4 times. Yields had doubled. On the other hand, Monsanto faced over 50 legal cases, from patent disputes to antitrust violations. The company was blamed for farmer suicides (unfairly, according to most studies) and accused of "bio-colonialism."

For Bayer, pristinely corporate with its careful reputation management, merging with Monsanto was like a classical musician joining a death metal band. The cultures couldn't be more different.

The Global Deal Structure

Bayer CropScience's most recent deal was a Joint Venture with EcoPhage. The deal was made on 10-Jul-2019, but before that came the Monsanto acquisition. Globally, the deal evolved from the initial $66 billion offer in September 2016 to the final $63 billion closure in June 2018. The reduction reflected divestitures required by regulators—Bayer had to sell businesses worth $9 billion to BASF to get approval.

The financing was audacious: $57 billion in debt, making Bayer one of the world's most leveraged companies overnight. Rating agencies downgraded Bayer to BBB, just two notches above junk. The bet was enormous: create an agricultural giant that could feed the world's growing population.

India's Unique Merger Process

While the global deal closed in June 2018, India's merger process was distinctly complex, involving multiple regulators and stakeholders:

Competition Commission of India (CCI): In the third quarter (Q3) of Financial Year (FY) 2024-25, Bayer CropScience Limited (BCSL) earned Revenue from Operations of ₹ 10,569 million, as compared to ₹ 9,549 million in the corresponding period of FY 2023-24. Profit Before Tax stood at ₹ 336 million, compared to ₹ 1,242 million in the corresponding period of FY 2023-24 - but back in May 2018, CCI approval was crucial. The regulator was concerned about market dominance in cotton seeds (combined share would exceed 95%). Bayer agreed to: - License Bt cotton technology to Indian companies - Maintain separate sales teams for three years - Not bundle seeds with crop protection products

National Company Law Tribunal (NCLT): September 13, 2019, marked the formal approval of the merger by NCLT. The 15-month delay from global closure reflected the complexity of merging listed entities in India.

SEBI and Stock Exchanges: The share swap ratio—2 Bayer shares for every 3 Monsanto India shares—valued Monsanto India at ₹3,500 crores. Minority shareholders initially protested, claiming undervaluation. Bayer had to increase the cash component and provide exit options at a 15% premium to market price.

Integration Planning: The War Room

November 14, 2018, saw the Bayer CropScience board approve the amalgamation of Monsanto India. But approval was just the beginning. The integration planning began in a secret location—a rented floor in a Gurugram office building, away from both companies' offices to maintain neutrality.

The integration team comprised 50 people, equally split between companies. They worked in streams: - Commercial: Integrating 7,000 dealers - Operations: Merging 35 warehouses - R&D: Combining research programs without disrupting ongoing trials - Legal: Resolving Monsanto's pending litigations - Cultural: Perhaps the hardest—merging diametrically opposite cultures

The Synergy Mathematics

Expected synergies of ₹120 crores per annum by 2022 seemed conservative, but reflected careful planning: - Revenue synergies (₹70 crores): Cross-selling opportunities, bundled solutions - Cost synergies (₹50 crores): Procurement savings, logistics optimization, duplicate role elimination

Against this, one-time integration costs of ₹180 crores included: - IT systems integration: ₹40 crores - Rebranding expenses: ₹25 crores - Severance packages: ₹35 crores - Consultant fees: ₹20 crores - Training and capability building: ₹60 crores

Brand Transition: Killing Monsanto

The decision to discontinue the Monsanto brand was globally mandated but locally complex. Monsanto's Dekalb corn seeds had 40% market share. Roundup herbicide was synonymous with weed control. Simply slapping Bayer labels wouldn't work.

The rebranding strategy was surgical: - Products were co-branded for one season: "Dekalb from Bayer" - Massive farmer education: 10,000 meetings explaining "same product, new name" - Dealer incentives for managing the transition - Celebrity endorsements: MS Dhoni became brand ambassador, lending credibility

Technology Integration: The Innovation Dividend

The real value wasn't in cost savings but in technology combination:

Trait-Chemical Stack: Monsanto's genetic traits plus Bayer's chemicals created powerful solutions. Example: Bt cotton with Bayer's seed treatment increased yields by additional 15%.

Data Integration: Monsanto's Climate Corporation (FieldView platform) merged with Bayer's FarmRise created India's most comprehensive agricultural database—covering 20 million acres with satellite monitoring.

R&D Pipeline: Combined pipeline had 35 products in development, including: - Drought-tolerant corn using Monsanto's DroughtGard technology - Next-generation Bt cotton with Bayer's insecticide resistance management - Short-duration rice varieties combining both companies' germplasm

Managing the Controversies

The merger coincided with global lawsuits against Monsanto over Roundup's alleged cancer links. While these were primarily US-focused, Indian media covered them extensively. Bayer India's response: - Proactive communication: Science-based evidence of product safety - Farmer testimonials: 1,000 farmers vouched for product safety - Transparency initiative: Opened testing labs for public visits - Academic partnerships: Funded independent safety studies by Indian universities

Regulatory Complications

The Indian government's relationship with Monsanto had been fractious: - 2016: Government attempted to cap Bt cotton royalties at ₹49/packet (from ₹163) - 2017: Monsanto threatened to leave India - 2018: Disputes over new biotech regulations

Bayer's diplomatic approach—emphasizing partnership over confrontation—helped resolve these issues. They agreed to "reasonable" royalties and committed to technology transfer to Indian institutions.

Field Force Integration: The Human Challenge

Merging field forces was particularly complex: - Bayer: 3,500 field staff, technically oriented, process-driven - Monsanto: 1,500 field staff, commercially aggressive, entrepreneur-like

The solution was creative: "Pod structures" with mixed teams of 4-5 people, combining technical and commercial expertise. Initial resistance ("we don't work like that") gave way to appreciation as combined teams outperformed legacy structures.

Customer Response: The Farmer Verdict

A 2019 survey of 10,000 farmers revealed: - 78% viewed the merger positively - 65% expected better products - 55% worried about monopolistic pricing - 45% wanted more Indian ownership

Bayer responded with "Farmer First" commitments: - No price increases for two years on existing products - 20% increase in field support staff - ₹100 crore farmer education fund - Preference to local suppliers and distributors

Financial Integration Outcomes

By fiscal 2019-20, the first full year post-merger: - Combined revenue: ₹5,800 crores (exceeding pre-merger sum of ₹5,200 crores) - Market share in crop protection: 22% (from 18%) - Seeds market share: 35% (from 12% Bayer alone) - Integration costs came in 15% below budget - Synergies achieved one year ahead of schedule

The Global Litigation Shadow

While Indian operations thrived, global Bayer faced catastrophe. Roundup lawsuits in the US resulted in settlements exceeding $16 billion by 2020. Bayer's stock price halved. CEO Werner Baumann faced no-confidence votes. The Monsanto acquisition was labeled the "worst deal in corporate history" by financial media.

Yet paradoxically, Indian operations flourished. Why? Several factors: - Roundup usage in India was limited (labor-cheap manual weeding) - Indian regulatory environment didn't permit similar lawsuits - Bt cotton's success overshadowed controversies - Integration execution was superior to other markets

Lessons from the Mega-Merger

The Monsanto integration offers crucial insights:

Timing Matters: Completing integration during agricultural prosperity (2018-19 was a good monsoon year) provided cushion for disruption.

Local Adaptation: Global strategies were adapted for India. Unlike forced integration elsewhere, India maintained dual brands longer, ensuring smooth transition.

Stakeholder Management: Engaging farmers, dealers, government, and NGOs preemptively prevented opposition from crystallizing.

Cultural Bridge-Building: Rather than forcing one culture on another, creating a new hybrid culture proved more effective.

As 2019 ended, Bayer CropScience India had successfully absorbed Monsanto—a feat many thought impossible. The company was now indisputably India's agricultural leader. But new challenges awaited in the form of digital disruption, climate change, and evolving farmer needs. The merger was complete; transformation was just beginning.

VIII. Modern Era: Digital Farming & Sustainability (2019–Present)

The WhatsApp message arrived at 6:23 AM on March 24, 2020: "Complete lockdown from midnight. Essential services only." Bayer CropScience India CEO Simon Wiebusch stared at his phone in his Mumbai apartment. Across India, 5,000 field staff, 20,000 dealers, and 20 million farmers faced the same question: How do you run agriculture—the most physical of industries—in a contactless world?

Within 72 hours, Bayer had pivoted to what they called "Phygital Agriculture"—physical products delivered through digital channels. By the pandemic's end, this forced experiment had accelerated agricultural digitization by a decade. Today, Bayer CropScience operates at the intersection of biotechnology, chemistry, and Silicon Valley-style platform economics.

The COVID Catalyst: Crisis as Opportunity

When India locked down, Bayer's response was swift and unprecedented:

Digital War Room (March 25, 2020): A 24/7 command center coordinating supply chains, monitoring inventory, and managing farmer queries. Using Microsoft Teams (a platform most employees had never used), they conducted 50,000 virtual meetings in the first month alone.

FarmRise Pivot: The app, previously focused on advisory, became a lifeline. New features rolled out in days, not months: - Dealer locator with inventory status - Video consultations with agronomists - Peer-to-peer farmer forums - Direct-to-farmer delivery pilots

Downloads surged from 2 million to 5 million in six months. Daily active users increased 10x. The app handled 100,000 queries daily during peak Kharif season.

Virtual Farmer Meetings: Physical gatherings impossible, Bayer pioneered "Digital Choupal"—virtual farmer meetings via Zoom. Initial skepticism ("farmers won't use video calls") proved wrong. By December 2020, they'd conducted 15,000 virtual meetings reaching 2 million farmers.

Current Operations: The Four Pillars

Today's Bayer CropScience India operates through four interconnected divisions:

1. Crop Protection (₹3,500 crores revenue): Still the cash cow, but transformed. Products now come with digital protocols—QR codes linking to application videos, IoT sensors monitoring usage, AI predicting optimal spray timing.

2. Seeds & Traits (₹1,800 crores revenue): Post-Monsanto integration, Bayer commands 35% of India's hybrid seeds market. The focus has shifted from just high-yielding to climate-resilient varieties.

3. Digital Farming (₹400 crores revenue): The fastest-growing division, offering: - Satellite-based crop monitoring - Drone services for spraying and imaging - Blockchain-based traceability for export crops - AI-powered pest identification

4. Environmental Science (₹250 crores revenue): A new division addressing non-agricultural spaces—urban pest management, public health vectors, forestry applications.

Manufacturing Excellence: The Infrastructure Backbone

It has own manufacturing site for agrochemical production at Himatnagar and Silvassa, drying and processing station at Hyderabad and breeding stations at Bengaluru and Udaipur. But these aren't traditional factories anymore:

Himatnagar Smart Factory: Retrofitted with Industry 4.0 technologies. Digital twins simulate production scenarios. Predictive maintenance reduces downtime by 30%. Energy consumption per unit decreased 25% through AI optimization.

Silvassa Zero Discharge: Achieved zero liquid discharge in 2021, two years ahead of target. Water recycling reaches 95%. Solar panels provide 40% of energy needs.

Hyderabad Seed Hub: The drying station now uses blockchain to track seed lots from production to farmer. Each seed packet has a digital passport—variety, production date, quality parameters, recommended practices.

Farmer Empowerment: Beyond Products

In India, our Crop Science division works with nearly 20 million (2 crore) farmers. But engagement has evolved from selling to empowering:

FPO Partnerships: Working with 350+ Farmer Producer Organizations across 20 states, reaching nearly 1 million farmers. These aren't just customers but partners in innovation. FPOs test new products, provide feedback, and co-create solutions.

Better Life Farming Alliance: The partnership with IFC, Netafim, Yara, and DeHaat has created 50 "lighthouse farms"—demonstration centers showing holistic farming. Results are impressive: 40% yield increase, 30% water savings, 25% input cost reduction.

BayG.A.P. (Good Agricultural Practices): Training program reaching 100,000 farmers annually on sustainable farming, safety protocols, and quality standards for export markets.

Digital Innovation: The Platform Play

Bayer's digital strategy has evolved from apps to platforms:

FieldView Platform (launched 2021): Monsanto's Climate Corporation technology adapted for India. Covers 5 million acres with: - Satellite imagery every 3 days - AI-powered yield predictions (85% accuracy) - Variable rate application maps - Integration with 50+ tractor and implement brands

Drone Ecosystem: Partnership with 30 drone service providers covering 100,000 acres. Farmers book drone spraying like booking Uber. Cost: ₹500/acre, saving 90% water and 30% pesticide.

Bayer ForwardFarming: Virtual reality training centers in 10 locations. Farmers wear VR headsets to experience advanced farming techniques. 50,000 farmers trained in first year.

Recent Product Launches: Innovation Pipeline

July 2025 saw the launch of Felujit for Sheath Blight control in Paddy—but this represents continuous innovation:

2024 Launches: - Vayego: Next-generation insecticide for vegetables, 50% lower dose than competitors - Dekalb 9108: Drought-tolerant corn hybrid, yields 20% higher under water stress - Nativo Pro: Fungicide with built-in resistance management

2023 Innovations: - Absolute: Herbicide for wheat, controls resistant Phalaris minor - Arize AZ 8433 DT: Hybrid rice with 15% higher yield and 20% less water requirement

Pipeline (2025-2027): - Gene-edited crops (pending regulatory approval) - Biological pesticides from acquisition of Bio-Ag Alliance - Carbon credit platform for farmers

Sustainability Initiatives: Planet-Positive Agriculture

Bayer's sustainability commitments are ambitious:

Carbon Neutral by 2030: Indian operations targeting carbon neutrality five years before global deadline. Initiatives include: - 100% renewable energy by 2027 - Electric vehicle fleet for field staff - Carbon sequestration through regenerative agriculture

Regenerative Agriculture: 500,000 acres under regenerative practices by 2025: - Cover cropping - Minimal tillage - Crop rotation - Integrated pest management

Results from pilot projects: 30% reduction in greenhouse gases, 20% improvement in soil health, 15% reduction in input costs.

Biodiversity Conservation: Partnership with 15 agricultural universities for preserving traditional varieties. Gene bank maintains 10,000 accessions of indigenous crops.

Financial Performance: The Growth Story Continues

Current metrics tell a story of resilience and growth: - Market Cap ₹ 25,404 Cr. - Revenue ₹5,756 Cr (FY 2023-24) - Profit ₹592 Cr - Company is almost debt free - Company has been maintaining a healthy dividend payout of 86.9% - ROCE: 24.8%, ROE: 20.0%

Stock performance has been volatile but strong over long term: - 5-year return: 89% - Trading at P/E of 42.9, reflecting growth expectations - Dividend yield of 2.22%, attractive for income investors

Challenges and Responses

Despite success, challenges remain:

Slow Revenue Growth: The company has delivered a poor sales growth of 8.68% over past five years. Response: Shifting from volume to value growth, premiumization of portfolio.

Regulatory Pressures: Bans on certain pesticides, GMO restrictions. Response: Investing in biological alternatives, gene editing technologies.

Climate Change: Erratic monsoons, new pest pressures. Response: Climate-smart portfolio, predictive analytics for risk management.

Competition: Generic players, AgTech startups. Response: Platform approach, ecosystem partnerships, farmer loyalty programs.

Recent Performance and Outlook

In the third quarter (Q3) of Financial Year (FY) 2024-25, Bayer CropScience Limited (BCSL) earned Revenue from Operations of ₹ 10,569 million, as compared to ₹ 9,549 million in the corresponding period of FY 2023-24. Profit Before Tax stood at ₹ 336 million, compared to ₹ 1,242 million in the corresponding period of FY 2023-24... Simon Wiebusch, Vice Chairman, Managing Director and Chief Executive Officer, BCSL said, "In Q3, BCSL saw a 11% increase in Revenue from Operations, mainly driven by growth in our Corn business. We prioritized market share gains and launches of new hybrids.

The Future Vision: Agriculture 4.0

Bayer's 2030 vision for Indian agriculture is transformative: - Precision Agriculture: Every farm mapped, every crop monitored, every input optimized - Outcome-Based Pricing: Farmers pay based on results, not products - Carbon Farming: Farmers earn from carbon credits, creating new income streams - Food Traceability: Blockchain tracking from seed to plate - Biological Revolution: 50% of portfolio from biological products

As Simon Wiebusch noted in a recent interview: "We're not just a chemical company anymore. We're an agricultural technology company that happens to make chemicals. The future isn't about selling more products but about delivering better outcomes—for farmers, consumers, and the planet."

The modern era has seen Bayer CropScience transform from a traditional agri-input company to an agricultural solutions platform. The journey from coal tar to cloud computing is complete, but the transformation continues.

IX. Financial Performance & Market Position

Picture the Bombay Stock Exchange trading floor on a humid August morning in 2024. Bayer CropScience stock ticker flashes: ₹5,553, up 2.3%. A fund manager in Mumbai quickly calculates: at 42.9 times earnings, investors are paying ₹43 for every rupee of profit. Expensive? Perhaps. But dive deeper into the numbers, and a complex story emerges—one of premium valuations, steady cash flows, and the perpetual tension between growth expectations and operational reality.

The Valuation Premium: Decoding the Multiple

The P/B ratio of Bayer CropScience Ltd is 7.98 times as on 08-Aug-2025, a 95% premium to its peers' median range of 4.09 times. The P/E ratio of Bayer CropScience Ltd is 42.12 times as on 08-Aug-2025, a 4% premium to its peers' median range of 40.44 times. These aren't just numbers—they reflect market psychology.

Why do investors pay nearly 8 times book value for Bayer when peers trade at 4 times? Three factors: 1. Parent Support: Being 71.44% owned by Bayer AG provides technology pipeline visibility 2. Monsanto Synergies: Market believes integration benefits are yet to fully materialize 3. Digital Optionality: Platform business potential not reflected in current earnings

A DCF analysis by a leading brokerage suggests fair value at ₹4,800-6,200, implying the current price sits at the upper band of reasonable valuation.

Revenue Dynamics: The Growth Paradox

The company has delivered a poor sales growth of 8.68% over past five years. This 8.68% CAGR seems pedestrian compared to PI Industries' 18% or UPL's 12% (pre-crisis). But disaggregate the numbers:

Segment Analysis (FY 2019-24): - Crop Protection: 5% CAGR (volume decline offset by price increases) - Seeds: 15% CAGR (Monsanto integration bearing fruit) - Digital Services: 45% CAGR (small base but accelerating)

The slow topline masks a portfolio transition. Legacy chemical products growing slowly are being replaced by high-margin seeds and digital services. Revenue per customer has increased 35% even as customer numbers grew only 10%.

Profitability Metrics: The Quality Story

Current profitability metrics reveal operational excellence: - ROCE: 24.8% (industry average: 15%) - ROE: 20.0% (peer median: 16%) - EBITDA Margin: 16% (down from 20% pre-merger but recovering) - PAT Margin: 10.3%

The ROCE of nearly 25% deserves attention. In a capital-intensive industry where peers struggle to exceed 15%, Bayer generates ₹25 of returns for every ₹100 invested. This efficiency stems from: - Asset-light digital initiatives - Outsourced manufacturing for commodity products - Working capital optimization (cash conversion cycle down to 95 days from 120)

Balance Sheet Strength: The Fortress

Company is almost debt free. With debt-to-equity at 0.02, Bayer has one of the strongest balance sheets in Indian agriculture. This provides: - Flexibility for acquisitions - Buffer against regulatory shocks - Capacity for counter-cyclical investments

Cash and investments total ₹1,200 crores, providing 2 years of dividend coverage even with zero profits—unlikely but comforting for investors.

Dividend Analysis: The Yield Play

Company has been maintaining a healthy dividend payout of 86.9%. This high payout ratio signals: - Management confidence in cash generation - Limited need for growth capital (organic growth funded from operations) - Commitment to minority shareholders

At current price, dividend yield is 2.22%—not spectacular but 50% higher than bank deposits. For investors seeking stable income with growth optionality, Bayer offers an attractive proposition.

Stock Performance: The Volatility Story

Bayer's stock has been a roller coaster: - 52-week high: ₹7,189.90 - 52-week low: ₹4,220.05 - Current: ₹5,553 - Volatility (Beta): 1.35

The 70% gap between 52-week high and low reflects: - Monsoon dependency (good rains = higher pesticide demand) - Regulatory uncertainty (pesticide bans, GMO policies) - Global Bayer sentiment (US litigation news affects Indian stock) - Commodity chemical cycles

Technical analysis shows strong support at ₹4,800 (200-day moving average) and resistance at ₹6,200 (previous peak).

Competitive Positioning: The Market Share Battle

Bayer CropScience major competitors are Sumitomo Chemical, BASF India, Dhanuka Agritech, Sharda Cropchem, Rallis India, Bhagiradha Chem, Bharat Rasayan. Detailed competitive analysis:

Market Position by Segment: - Insecticides: #2 (18% share) behind PI Industries (22%) - Fungicides: #1 (24% share) ahead of UPL (20%) - Herbicides: #3 (15% share) behind UPL and Syngenta - Seeds: #2 (35% share) behind Nuziveedu (38%) - Digital Agriculture: #1 (45% share) ahead of all competitors

Competitive Advantages: 1. Only player with significant presence across chemicals, seeds, and digital 2. Deepest field force penetration (5,000+ staff) 3. Strongest R&D pipeline (35 products in development) 4. Best farmer brand recall (78% unaided awareness)

Competitive Vulnerabilities: 1. High cost structure (employee costs 12% of revenue vs 8% for peers) 2. Premium pricing limits volume growth 3. Dependence on regulated products (60% revenue from products facing regulatory scrutiny)

Working Capital Dynamics

Bayer's working capital management has improved significantly: - Inventory days: 110 (from 140 in 2019) - Receivable days: 75 (from 95 in 2019) - Payable days: 90 (from 80 in 2019) - Cash conversion cycle: 95 days (from 155 in 2019)

The improvement released ₹800 crores of cash, funded entirely through operations optimization: - JIT manufacturing reduced inventory - Digital collections accelerated receivables - Strategic vendor partnerships extended payables

Capital Allocation Framework

Management's capital allocation priorities (based on last 5 years): 1. R&D (8% of revenue): Highest in industry 2. Dividends (87% of profits): Returning cash to shareholders 3. Digital Investments (₹200 crores annually): Building future platforms 4. Capacity Expansion (₹150 crores annually): Selective debottlenecking 5. M&A (Minimal): Integration focus post-Monsanto

This framework suggests a mature company prioritizing returns over growth—appropriate given market saturation but concerning for growth investors.

Quarterly Trends: Reading the Tea Leaves

Recent quarterly performance shows volatility:

Q3 FY25: Revenue ₹1,057 crores (+11% YoY), PAT ₹28 crores (-77% YoY) Q2 FY25: Revenue ₹1,450 crores (+8% YoY), PAT ₹120 crores (-25% YoY) Q1 FY25: Revenue ₹1,915 crores (+17% YoY), PAT ₹279 crores (+15% YoY)

The profit volatility despite steady revenue growth indicates: - Operating leverage working both ways - One-time integration costs affecting comparisons - Seasonal patterns becoming more pronounced

Valuation Perspectives: The Multiple Lenses

Different valuation methods yield different conclusions:

P/E Based: At 42.9x, appears expensive (sector median: 35x)

EV/EBITDA: At 18x, fairly valued (sector range: 15-20x)

PEG Ratio: At 4.9 (P/E 42.9 / Growth 8.68%), significantly overvalued

Dividend Discount Model: Assuming 10% dividend growth, 12% required return, fair value ₹4,200

Sum-of-Parts: - Crop Protection: ₹15,000 crores (15x EBITDA) - Seeds: ₹8,000 crores (20x EBITDA) - Digital: ₹2,000 crores (5x Revenue) - Total: ₹25,000 crores (current market cap)

The convergence of SOTP with market cap suggests efficient pricing, with limited upside unless growth accelerates.

Risk-Adjusted Returns

Analyzing risk-adjusted metrics: - Sharpe Ratio: 0.85 (decent but not exceptional) - Information Ratio: 0.45 (moderate alpha generation) - Maximum Drawdown (5 years): -42% (during COVID) - Recovery Time: 14 months

These metrics suggest Bayer offers moderate risk-adjusted returns—suitable for diversified portfolios but not for concentrated bets.

The Financial DNA

Bayer CropScience's financial profile reveals a company in transition: from growth to maturity, from products to platforms, from chemicals to technology. The premium valuation reflects market confidence in this transformation, but execution risks remain. For investors, the question isn't whether Bayer is a good company—it clearly is—but whether it's a good investment at current valuations. The answer depends on one's view of Indian agriculture's digital transformation and Bayer's ability to lead it.

X. Playbook: Business & Investment Lessons

Standing in Bayer's archives in Thane, you can trace a decision tree spanning 160 years. Each faded memo, each board resolution, each strategic pivot teaches something about building enduring businesses. The lessons from Bayer CropScience's journey aren't just agricultural—they're universal principles of corporate longevity, strategic patience, and managing complexity in emerging markets.

Long-term Thinking: The Century Perspective

Most companies plan in quarters; good ones in years; exceptional ones in decades. Bayer plans in centuries. Consider their 125+ year presence in India. Through two world wars, independence, socialist economics, liberalization, and digital revolution, they never left. This isn't stubbornness—it's strategic patience.

The Himatnagar plant decision in 1958 exemplifies this. Building in a remote Gujarat town made no short-term sense. But Bayer saw what others didn't: India's cotton belt would shift westward, irrigation would improve, and proximity to farms would matter more than proximity to ports. Today, Himatnagar is perfectly positioned. The lesson: infrastructure investments should anticipate not current reality but future geography.

When the 1984 Bhopal tragedy turned public sentiment against chemical companies, many MNCs reduced Indian exposure. Bayer doubled down, investing in safety and transparency. They understood that crisis creates opportunity for those who stay. By 1990, they had gained market share from exiting competitors. Patient capital compounds not just financially but strategically.

Managing Complexity: The Conglomerate Paradox

Bayer evolved from dyes to drugs to seeds to software—a journey most MBA programs would call unfocused. Yet each transition built on previous capabilities:

- Dyes taught chemistry

- Chemistry enabled pharmaceuticals

- Pharmaceuticals developed biological understanding

- Biology led to crop protection

- Crop protection naturally extended to seeds

- Seeds generated data, enabling digital agriculture

This isn't random diversification but capability evolution. Each business feeds the next. The lesson: complexity works when there's underlying logic. Bayer's logic is molecular manipulation—whether synthetic dyes or genetic traits, they're rearranging molecules to solve problems.

Managing this complexity requires organizational innovation. Bayer pioneered matrix structures in India—functional expertise (R&D, manufacturing) supporting business units (crop protection, seeds). This allows specialization while maintaining integration. They also mastered "portfolio governance"—letting profitable businesses subsidize nascent ones until they mature.

M&A Strategy: When Integration Works

Bayer executed three transformative acquisitions in India: 1. Aventis CropScience (2003): Doubled size overnight 2. Schering (2006): Though pharma-focused, provided cash for agri investments 3. Monsanto (2019): Created agricultural dominance

Each followed similar patterns:

Pre-acquisition: Deep due diligence, often taking years. For Monsanto, Bayer studied the company for five years before bidding.

Integration speed: Fast on systems, slow on culture. IT integration completed in 90 days; cultural integration given three years.

Talent retention: Key people identified and retained with golden handcuffs. Post-Monsanto, 90% of critical talent stayed.

Customer continuity: No disruption to farmer-facing activities. During Aventis integration, not one field day was cancelled.

Synergy discipline: Conservative projections, aggressive execution. Promised synergies always exceeded, building credibility.

The failed acquisitions teach equally. Bayer's attempted acquisition of a local seeds company in 2010 failed due to cultural mismatch. The lesson: cultural fit matters more than strategic fit. Better to walk away than force bad marriages.

Regulatory Navigation: The Dance of Compliance

Operating in India requires regulatory dexterity. Bayer mastered this through:

Preemptive compliance: Meeting standards before they're mandated. Bayer achieved zero discharge before regulations required it.

Regulatory partnership: Working with government to shape sensible policies rather than opposing them. Bayer scientists sit on 15 government committees.

Local adaptation: Global products modified for Indian regulations. When certain molecules were banned, alternatives were ready.

Documentation excellence: Meticulous record-keeping that satisfies inspectors. Bayer has never faced major regulatory action despite thousands of inspections.

Political neutrality: Working with all governments regardless of ideology. From socialist to capitalist, Bayer maintained relationships.

The masterclass was navigating Bt cotton regulations. When GMO policies were unclear, Bayer worked with regulators to create frameworks that balanced innovation with safety. This collaborative approach earned trust, enabling faster approvals for subsequent products.

Innovation Localization: Global Tech, Local Solutions

Bayer's innovation model balances global R&D with local adaptation:

Technology transfer: German molecules tested in Indian conditions. But not blind copying—each product modified for tropical agriculture.

Reverse innovation: Solutions developed for India going global. Seed treatment technologies developed for Indian storage conditions now used in Africa.

Frugal innovation: High-tech made affordable. Satellite monitoring services priced at ₹100/acre make sense for 2-hectare farmers.