Corporación Financiera Alba: The Story of Spain's Patient Capital Dynasty

I. Introduction & Episode Roadmap

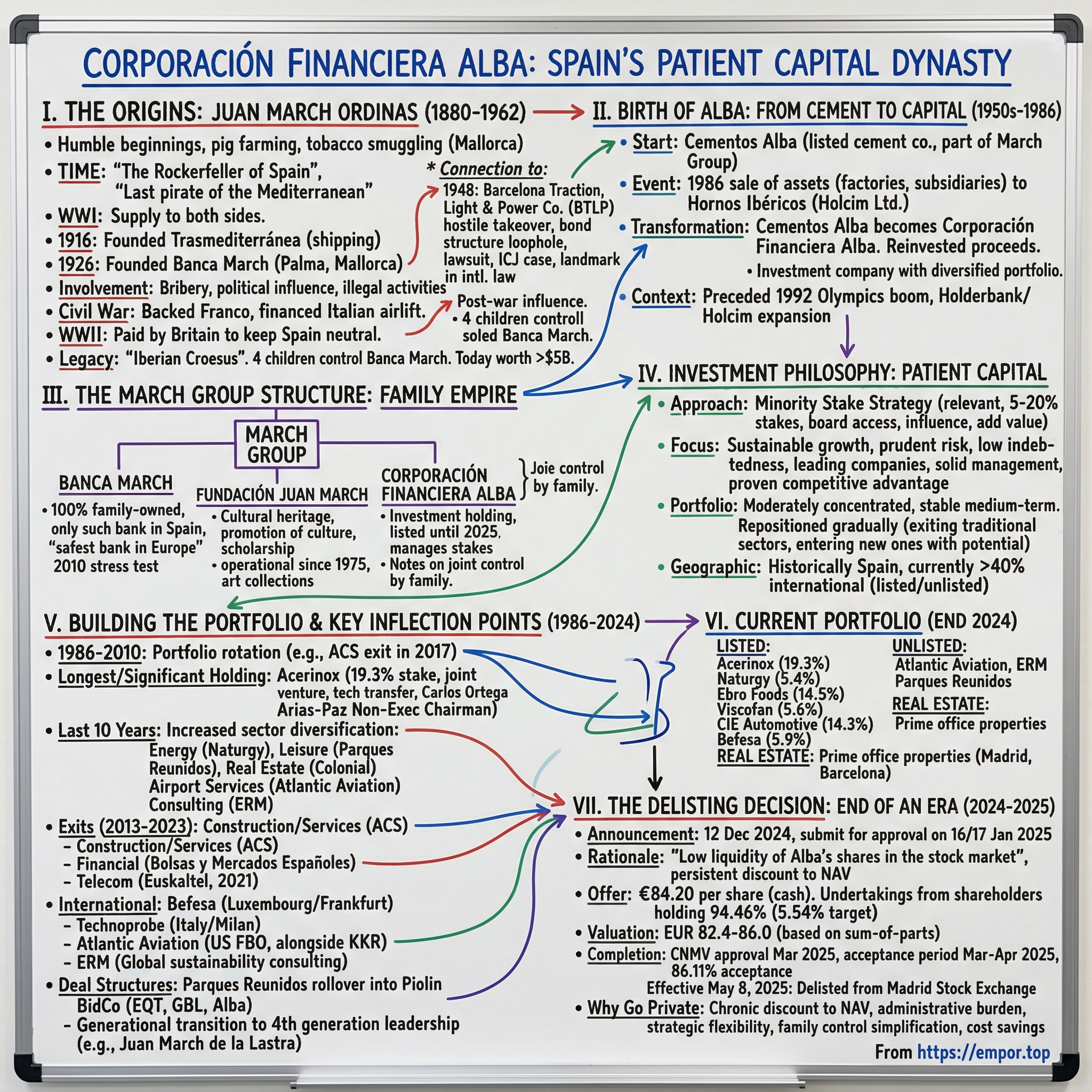

On a December morning in 2024, something remarkable happened in Spanish finance. Corporación Financiera Alba—an investment holding company that had traded on Spanish stock exchanges for nearly four decades—announced it was going private. The offer price: €84.20 per share in cash. The March family agreed to delist the Spanish holding through a takeover bid at a price of €84.20 per share in cash, which represents a premium of 79.5% compared to the closing price of €46.90 per share. This price exceeded even the historical maximum reached in 2007 of €60.70 per share.

For public market investors, this represented a windfall—nearly 80% above where the shares had been languishing. But it also marked the end of an era. Alba wasn't just any investment company. Corporación Financiera Alba is a Spanish investment holding company founded in 1986 and listed on the Continuous Market of the Spanish stock exchanges. The company is part of the March Group, one of Spain's leading private family-owned business and financial groups, which also includes Banca March and the Juan March Foundation.

The Net Asset Value (NAV) decreased by 1.1% during the year, standing at €5,733 million at December 31st, 2024, equivalent to €95.07 per share. That's over €5.7 billion in assets—a portfolio that reads like a who's who of Spanish and European industry: stainless steel giant Acerinox, energy utility Naturgy, food leaders Ebro Foods and Viscofan, plus stakes in international businesses from American FBO operations to Italian semiconductor testing firms.

The central mystery of this story: How does a cement company transform into Spain's Berkshire Hathaway, and why would one of Europe's richest families suddenly take it private at such a premium?

The delisting will be approved at the extraordinary meeting to be held in mid-January next year and is justified, according to the company itself, by "the low liquidity of Alba's shares in the stock market." The delisting was supported by both the board of directors (which represents 76.35% of the shares) and other shareholders, reaching a total of 94.46% of the capital.

The answer requires understanding the family behind Alba—the March dynasty—whose patriarch began as an illiterate tobacco smuggler in Mallorca over a century ago and became, at his peak, one of the richest men on Earth. It's a story of political influence that shaped Spain's twentieth century, a controversial hostile takeover that went to the International Court of Justice, and a patient investment philosophy refined over generations.

II. The March Dynasty: Spain's Most Controversial Fortune

The Origins: Juan March Ordinas (1880-1962)

The story begins in the rural heart of Mallorca. Juan March Ordinas was born on 4 October 1880 in Santa Margalida, on the island of Mallorca. Born into a humble family of peasants in Mallorca, he was expelled from school at an early age and began helping his father with his pig farming business while smuggling tobacco from Spanish Morocco.

From these beginnings, March would rise to extraordinary heights. Juan Alberto March Ordinas was a Spanish business magnate, arms and tobacco smuggler, banker and philanthropist. Closely associated with the Nationalist side during and after the Spanish Civil War, March was the wealthiest man in Spain and the sixth richest in the world. Throughout his life, he accumulated labels such as "the Rockefeller of Spain" or "the last pirate of the Mediterranean".

The "last pirate of the Mediterranean" was no idle moniker. During World War I, March supplied goods to both sides by evading the Allied blockade of the Central Powers and the German U-boats. This wartime profiteering laid the foundation for an empire that would prove remarkably resilient across multiple political regimes.

In 1916, March made his first major move into legitimate business. He founded Trasmediterránea, an important shipping company that strengthened March's maritime outreach. A decade later came the banking venture that would anchor the family's fortunes for the next century. Banca March was founded in Palma, Mallorca in 1926 by Juan March Ordinas. At first, the bank's area of influence was limited to Mallorca, progressively expanding throughout the 20th century and becoming an independent bank in all of the Balearic Islands.

March was never a passive figure content to accumulate wealth quietly. March was widely known for involvement in lucrative illegal activities, bribery, political influence and bending the law whenever he saw a benefit. That was exemplified in his 1948 takeover of the Barcelona Traction, Light, and Power Company (BTLP) for a small fraction of its real worth.

The Prison Escape & Post-War Influence

The Second Spanish Republic viewed March as a threat. For a short period of the Second Spanish Republic, he was jailed due to financial irregularities and illegal activities, including tobacco and arms trafficking.

What happened next became the stuff of legend. In June 1932 the Parliament voted to expel March and remove his legal immunities: he was imprisoned the following week and held for eighteen months pending trial, after the new republican finance minister announced: "Either the republic overthrows Don Juan March or the señor will overthrow the republic!" The finance minister proved prophetic.

Last week he decided that he had been in jail long enough, walked out the front door, climbed into a car full of friends and drove off, taking one of the lesser wardens with him. Pressed for an explanation, Chief Night Jailer Martinez Hernaiz said he had let his prominent prisoner escape because he said he did not feel well. Behind him Juan March left a letter for his lawyer, Tomas Perie: "I left prison because I felt my health would collapse."

He escaped from prison, and fled to Gibraltar where his influence with the British government protected him against extradition. TIME magazine captured the audacity of the moment with its characteristic wit, describing March as a "character from Cervantes" who rolled up to Gibraltar's Rock Hotel and thumbed his nose at the Spanish government.

March would exact his revenge on the Republic through financing. March was an important backer of the 1936 military rebellion against the Republic that led to the Spanish Civil War. He arranged Francisco Franco's flight from the Canary Islands to Spanish Morocco, brought the colonial troops there into the rebellion and personally financed the Italian airlift of those troops to southern Spain.

With the Nationalist victory in 1939, March regained more than his former influence and was greatly favoured in Francoist Spain. During World War II, the Allies employed him to keep Spain from joining the Axis. According to recently-declassified documents, in 1941 the British government gave him US$10,000,000 to influence the top Spanish generals.

This is one of history's great ironies: the same man who bankrolled Franco's fascist uprising was paid millions by Britain to keep Spain neutral against Hitler. March operated in the space between ideologies—his only consistent allegiance was to profit and power.

The Barcelona Traction Affair

After the war, March demonstrated his ruthlessness in business with the Barcelona Traction takeover—an affair that remains studied in international law schools today.

This was exemplified in his 1948 takeover of the Barcelona Traction, Light, and Power Company (BTLP) for a small fraction of its real worth. BTLP was a utility company which provided power and streetcar services in Barcelona; originally incorporated in Canada, it was mostly owned by Belgian investors. BTLP had come through the civil war largely undamaged, and was quite profitable. Its assets were about £10,000,000 (about $500,000,000 in 2010).

March spotted an opportunity in the company's bond structure. However, for the convenience of some of its foreign investors, BTLP had issued some bonds denominated in pounds, and the interest on these bonds was payable in pounds. The Spanish government had imposed currency restrictions: BTLP was unable to exchange its Spanish pesetas for pounds, and so could not pay the interest. This was not viewed with any great alarm by the bond-holders; BTLP had plenty of pesetas and would pay the interest arrears whenever the currency restrictions were relaxed. However, March sensed an opportunity.

In 1948, a group of bondholders, fronting for Spanish well-connected businessman Juan March, sued in Spain to declare that BTLP had defaulted on the ground that it had failed to pay the interest. The Spanish court allowed the claim.

The Belgian government appealed to the International Court of Justice but to no avail: the final resolution coming in 1970, eight years after March's death. The government of Spain under Franco in the 1960s placed restrictions on foreigners doing business in Spain. The Belgian stockholders in Barcelona Traction lost money and wanted to sue in the International Court of Justice, where their cause was defended by Belgian lawyer Henri Rolin. But in the court Judge Fornier ruled on the side of Spain, holding that only the state in which the corporation was incorporated (Canada) can sue.

The Barcelona Traction case became a landmark in international corporate law, establishing principles about shareholder rights and state espousal of claims that are still cited today.

The Modern March Dynasty

Juan March died in March 1962 from injuries sustained in a car accident in Madrid. At his death in 1961, Time called him "the Iberian Croesus". But his death marked not an ending but a transition—the March family would prove remarkably adept at intergenerational wealth preservation.

The March family under his patriarchy had a strong influence in the financial, social and cultural aspects of European affairs in the 20th century, and it played an almost equally important role as the Rothschild family. Today, the Marches are among the richest in Spain, reported to be worth over US$5 billion.

The March family is a well known banking dynasty in Spain, sometimes mentioned alongside Europe's biggest banking families, the Rothschild and von Oppenheim dynasties.

The control of Banca March, S.A. is exercised by the 4 children of Juan March y Servera: Juan (33.3%), Carlos (33.3%), Gloria (16.6%) and Leonor March y Delgado (16.6%), who jointly control 100% of its share capital, without any of them doing so individually.

The family maintained control through the third and now fourth generation, transforming controversial origins into legitimate financial empire. The transformation from smuggler patriarch to banking dynasty speaks to both the family's business acumen and their strategic rehabilitation of the March name.

III. The Birth of Alba: From Cement to Capital (1950s-1986)

The origin story of Corporación Financiera Alba defies expectations. Most investment holding companies are founded as such from the beginning—vehicles designed to deploy capital across multiple opportunities. Alba took a different path entirely.

The origin of Corporación Financiera Alba is Cementos Alba, a listed Spanish cement company founded in the 50s and participated by the March Group.

Cement may seem an unlikely starting point for what would become Spain's premier investment holding company, but in post-Civil War Spain, cement was essential infrastructure. The country was rebuilding from devastating conflict, and the March family's industrial holdings positioned them to profit from reconstruction.

The pivotal moment came in 1986, when the global cement industry was consolidating rapidly. In 1986, Hornos Ibéricos, also a cement company controlled by Holderbank (currently Holcim Ltd.), acquired all its assets, including its factories and cement mixer subsidiaries. Following the sale, Cementos Alba changed its purpose and name to Corporación Financiera Alba and reinvested the proceeds obtained, effectively becoming an investment company with a diversified portfolio of equity investments and real estate assets.

Thomas Schmidheiny took over leadership, overseeing the company as it expanded into Eastern Europe and experienced a boom in Spanish construction preceding the 1992 Summer Olympics. By 1986, Holderbank was the world's largest cement manufacturer.

This was not just opportunistic selling—it was strategic transformation. The March family recognized that Spain's economy was modernizing rapidly as the country emerged from decades of Franco-era isolation. The 1986 sale came just as Spain was joining the European Economic Community, opening new opportunities for diversified investment.

Rather than take the proceeds and deploy them elsewhere, the family used Cementos Alba's existing stock market listing as a platform. Since its inception, Alba has been an active investor, mainly in the domestic market, and shareholder of selected leading companies.

The timing proved prescient. Spain's stock market was about to embark on a remarkable growth phase driven by EU integration, the 1992 Barcelona Olympics, and broader modernization. Alba was positioned to ride this wave not as an industrial operator but as a patient capital allocator.

IV. The March Group Structure: A Family Empire

Understanding Alba requires understanding its place within the broader March Group architecture—a structure designed to separate different functions while maintaining unified family control.

Corporación Financiera Alba ("Alba") is an investment holding company owned by the March Group, one of Spain's main private family-owned financial groups, which also includes Banca March and the Juan March Foundation.

Banca March: The Private Banking Arm

Banca March was founded in 1926 by Juan March Ordinas. We are the only family‐owned bank left in Spain; 100 per cent of the bank's shares are owned by the March family. We are an unlisted bank, with a unique business model that sets us apart from the rest.

The bank earned a remarkable distinction during the European financial crisis. In 2010, March was deemed "the safest bank in Europe" by the 2010 European Union bank stress test. While Spanish banks were collapsing left and right during the 2008-2012 period—with the country eventually requiring a €100 billion EU bailout for its banking sector—Banca March emerged unscathed.

In July 2010 Banca March came on top of the European Union banking stress test exercise in terms of Tier 1 capital ratio. According to the Financial Times: While most scrutiny on Friday focused on the seven banks, of the 91 tested, that fell short of the 6 per cent tier one capital ratio pass mark, the exercise also shines the spotlight on the banks with the strongest capital positions.

Being a 100 percent family-owned bank means it adopts a prudent approach to asset management – a feature of only those who risk and manage their own money. This conservative management policy has been particularly notable during the years of the financial crisis, steering clear of risks and adventures, and allowing the bank to emerge significantly strengthened.

The bank-investment company relationship is symbiotic. Banca March, S.A. and its shareholders jointly control 66.7% of Corporación Financiera Alba. The Banca March Group holds a 15.04% stake in this corporation, which manages various stakes in leading companies to create long-term value.

The Foundation: Cultural Legacy

The Fundación Juan March is an active, family-run cultural heritage institution created by the financier Juan March Ordinas in 1955 with the mission of promoting culture in Spain, with no other commitment than the quality of its offerings and the benefit of its community.

For two decades, from 1955 to 1975, the Fundación Juan March focused its resources on covering the pressing needs of the post-war period through scholarships, prizes, pensions and sponsorships in the cultural, social, artistic and scientific fields. In 1975 the Foundation evolved into an operational organization. It applied its resources to programs designed, produced, organized and executed by its own staff. This meant a greater degree of specialization and commitment in the cultural field.

The Foundation serves multiple purposes for the family. It rehabilitates the March name—transforming the legacy of "the last pirate of the Mediterranean" into cultural patronage. It provides tax-efficient philanthropy. And it creates soft power—the kind of cultural capital that opens doors in business and politics.

They also have one of the most important art collections in Spain and two Foundations, managed independently (the Juan March and the Bartolomé March), which have ennobled their fortune and are financed with their own resources. The Foundations are the cultured image of this family saga that has become a cultural asset of the Spanish State. It is the perfect conjunction of money and culture.

The three-pillar structure—bank, investment company, foundation—represents a sophisticated approach to family wealth management. The bank provides steady income and financial services. Alba offers exposure to equity upside in leading companies. The foundation provides legitimacy and cultural capital. Together, they form an integrated ecosystem serving multiple generations.

V. The Investment Philosophy: Patient Capital Spanish Style

Alba's investment approach is distinctive in European markets—a philosophy refined over nearly four decades that blends minority stake activism with patient, long-term capital deployment.

Since its inception, Corporación Financiera Alba has oriented its investment activity towards adding value supported by a profitable growth model sustainable in the long term, with a prudent policy of risk diversification and low indebtedness. Consequently, Alba invests in leading companies, with a solid management team, a strong and flexible financial situation and a proven competitive advantage. In line with its investment strategy, Alba pursues to be a long term partner with strong commitment with the existing shareholders and the management team.

The Minority Stake Strategy

Unlike private equity firms that seek controlling stakes or activist investors that agitate for immediate change, Alba occupies a middle ground. Its shareholdings are always minority stakes but are significant enough to give it access to the management bodies of the companies in which it invests.

This approach offers distinct advantages. Minority stakes require less capital than control positions, allowing greater diversification. They avoid the operational complexity of running businesses directly. And crucially, they don't trigger the premium valuations typically required to acquire control.

Additionally, the experience and reputation gained by Alba during over 30 years of investment activity allows it to add value to its investee companies from its position as minority relevant shareholder and its active participation in the Board of Directors and other company committees.

The word "relevant" is key. Alba doesn't take 1-2% positions that would make it just another institutional investor. Its stakes typically range from 5-20%, large enough to secure board representation and influence strategic decisions, small enough to avoid triggering mandatory tender offers.

Portfolio Concentration Philosophy

The long-term investment philosophy and relevant presence in a limited number of companies, both in equity participation and in their relative weight over Alba's total assets, means that Alba's portfolio, although sectorally diversified, has a certain component of concentration and medium-term stability.

Alba's investment portfolio tends to be moderately concentrated and stable in the medium term. This is caused by Alba's long term investment philosophy and the relevant presence of a limited number of companies that represent an important portion of its NAV.

This concentrated approach differs markedly from diversified investment funds that spread capital across hundreds of positions. Alba typically holds 15-25 meaningful investments at any given time—few enough that each position receives genuine attention, diversified enough to manage risk.

However, historically, Alba has repositioned its investment portfolio gradually and non-traumatically, exiting sectors that were once traditional for the company and entering new ones with greater potential. Since its creation, Alba has been an active investor, historically largely in the domestic market and currently with a significant international presence, being a reference shareholder of highly relevant companies in their respective sectors of activity.

Geographic Evolution

However, Alba has focused on direct investment in relevant equity stakes of a relatively limited number of listed and/or unlisted companies, in which Alba has representation on their Board of Directors. Its investments have historically been focused on Spanish companies, the vast majority of which are highly international, but in recent years, the investment universe has expanded to companies headquartered outside Spain, which currently represent over 40% of its portfolio.

This international expansion represents a significant strategic evolution. Alba's early decades focused almost exclusively on Spanish companies, but as the company's NAV grew and domestic opportunities became relatively smaller, international expansion became essential.

Corporación Financiera Alba's current listed investees are all companies headquartered in Spain, with the exception of Befesa, a Luxembourg company listed on the Frankfurt Stock Exchange, and Technoprobe, an Italian company listed on the Milan Stock Exchange.

The unlisted portfolio has expanded even more internationally, with major positions in U.S. aviation services and global consulting firms.

VI. Building the Portfolio: Key Investments & Exits (1986-2010)

Alba's track record spans four decades and tells a story of disciplined capital allocation through multiple market cycles. The composition of Alba's portfolio has changed substantially over the last 10 years, with a significant increase in sector diversification. From 2013 to 2023, Alba invested in new sectors such as Energy (Naturgy), Leisure (Parques Reunidos), Real Estate (Inmobiliaria Colonial), Airport Services (Atlantic Aviation) and Consulting Services (ERM), and significantly increased the weight of Industrial sector (Acerinox, CIE Automotive and Befesa) and Food sector (Ebro Foods, Viscofan and Profand). In contrast, in this period it fully divested from the Construction and Services sector (ACS, in 2017), the Financial sector (Bolsas y Mercados Españoles, in 2020) and the Telecommunications sector (Euskaltel, in 2021) sectors.

The Acerinox Relationship

The Acerinox stake represents Alba's longest and most significant holding—a relationship that exemplifies the company's patient capital philosophy.

The company was founded in 1970. It was financed in part by Nisshin Steel. This corporation has been the only successful joint venture with Japanese investors in the steel industries in Europe. New empirical evidence from written and oral sources has revealed how significant the links between Spanish and Japanese entrepreneurs were, since the 1960s, in order to understand the formal constitution of the Joint Venture in 1970, and the successful transfer of technology and market know-how from Japan to Spain, between the 1970s and 1980s.

Alba has been invested in Acerinox for decades, and the relationship has deepened over time. The company now holds a 19.3% stake, and The Board of Directors meeting, held after the General Shareholders' Meeting, appointed Carlos Ortega Arias-Paz as Non-Executive Chairman of Acerinox. Ortega is currently Managing Director of Corporación Financiera Alba and is a member of the Board of Acerinox as a Proprietary Director.

This illustrates Alba's influence model—placing senior executives on portfolio company boards where they can contribute expertise and maintain alignment between shareholder and management interests.

The ACS Saga

The ACS relationship demonstrates Alba's willingness to exit positions when the investment thesis changes. ACS, the construction giant chaired by Florentino Pérez (better known as Real Madrid's president), was once one of Alba's largest holdings.

So too should the fact that the company's largest shareholder of yore, Alba Financial Corporation, the investment arm of Banca March, an 84-year-old family-owned bank and equity investment group that once upon a time helped bankroll Francisco Franco's reconquest of Spain, has been quietly selling its stake in the firm. Just under five years ago, the Mallorca-based private bank owned 23.3% of the construction firm; now it owns 11.7%. Another long-standing investor in ACS, Alcor, has trimmed its stake from 13% in 2012 to under 7% today.

Alba gradually reduced its position throughout the 2010s before fully exiting in 2017. The timing proved astute—construction and services businesses faced headwinds from post-financial crisis austerity and accounting controversies.

Portfolio Rotation Strategy

From 2013 to 2023, Alba invested in new sectors such as Energy (Naturgy), Leisure (Parques Reunidos), Real Estate (Inmobiliaria Colonial), Airport Services (Atlantic Aviation) and Consulting Services (ERM), and significantly increased the weight of Industrial sector (Acerinox, CIE Automotive and Befesa) and Food sector (Ebro Foods, Viscofan and Profand). In contrast, in this period it fully divested from the Construction and Services sector (ACS, in 2017), the Financial sector (Bolsas y Mercados Españoles, in 2020) and the Telecommunications sector (Euskaltel, in 2021) sectors.

This rotation tells a strategic story. Alba moved out of sectors exposed to Spanish economic cyclicality (construction, domestic telecom) and into sectors with global exposure (stainless steel, food processing) or structural growth characteristics (airport services, renewable energy).

VII. Key Inflection Points: The Last Two Decades (2010-2024)

The 2010 EU Bank Stress Test & March Family Reputation

The European sovereign debt crisis of 2010-2012 tested every Spanish financial institution. Banca March's performance provided powerful validation of the family's conservative management philosophy.

In 2010, March was deemed "the safest bank in Europe" by the 2010 European Union bank stress test. At a time when major Spanish banks were teetering and would eventually require massive bailouts, the March family's conservative approach demonstrated its value.

This reputation for prudence enhanced Alba's ability to deploy capital during the crisis. While others were distressed sellers, Alba could be a selective buyer.

The 2021 Restructuring

2021 represented a significant portfolio rotation year. The sale of Euskaltel exemplified Alba's opportunistic approach to exits.

Alba sold its entire 11.0% stake in Euskaltel for €216 million as part of the voluntary takeover bid launched by Grupo MásMóvil. This sale generated a gross book gain of €28 million—a successful exit from a position that had become less strategic as Spanish telecom consolidated.

Another notable 2021 exit came through the private equity vehicle Deyá Capital: the sale of the entire stake (16.8%) in Alvinesa's share capital for €48 million. As part of this investment, Alba obtained an IRR of 44.9% per annum over the 4.1 years it had been a shareholder—an exceptional return demonstrating Alba's ability to generate venture-like returns from private investments.

International Expansion: Atlantic Aviation

Alba's investment in Atlantic Aviation represented a significant international expansion. Alba expects to hold an indirect stake of approximately 12% in Atlantic Aviation FBO Holdings L.L.C. ("Atlantic Aviation"), upon the closing of the acquisition of Atlantic Aviation by Apple Holdings agreed with Macquarie Infrastructure Corporation (NYSE: MIC) for US$ 4.475 billion in cash and assumed debt and reorganization obligations. Atlantic Aviation is a leading fixed base operator (FBO). It manages 69 FBOs at airports across the United States and is one of the only two operators with a national footprint.

Corporacion Financiera Alba and Kohlberg Kravis Roberts have invested in Atlantic Aviation FBO. The investment positioned Alba alongside KKR, one of the world's leading private equity firms, in an essential infrastructure business serving private aviation—a sector with strong growth tailwinds.

Parques Reunidos Partnership

Alba's approach to Parques Reunidos demonstrates sophisticated deal-making. Parques Reunidos is the second largest operator of recreational infrastructure in Europe. Piolin BidCo is owned by EQT Infrastructure, Alba and GBL. Total shareholding of Piolin BidCo in Parques Reunidos reaches 86.40 percent. On 26 April 2019, the EQT Infrastructure IV fund ("EQT" or "EQT Infrastructure"), through the investment vehicle Piolin BidCo, S.A.U. ("Piolin BidCo") announced a voluntary tender offer ("the Offer") for 100 percent of the shares in Parques Reunidos Servicios Centrales, S.A. ("Parques Reunidos" or the "Company").

Alba and GBL provided hard undertakings to roll over their shares representing 44.21 percent into Piolin BidCo immediately prior to settlement of the Offer.

Rather than exit at the offer price, Alba rolled its stake into the acquiring vehicle—a structure that allowed the company to maintain exposure while partnering with EQT's infrastructure expertise and GBL's investment capabilities.

Generational Transition

Juan March Delgado (Palma de Mallorca, 1940) has a Doctorate in Industrial Engineering from Madrid's Universidad Politécnica and was Co-Chairman of Corporación Financiera Alba alongside Carlos March Delgado until 2018.

Carlos March Delgado has stepped down as the chairman of the board of Banca March at the age of 78 after serving as the longest-serving chairman of a Spanish bank (1974-2015).

We are the fourth generation of a family-owned bank with a long-term vision geared towards prudent management and sound financial ratios.

The fourth generation is now assuming leadership positions throughout the March Group. The professional career of Juan March de la Lastra, which began in 1995, has always been linked to the finance industry. After completing his Business Management degree at Carlos III University in Madrid, he joined the Capital Market division at J.P. Morgan, serving in different roles in London and Madrid. In 2000 he joined Banca March. Prior to his appointment as the bank's executive chairman, Juan March de la Lastra had served in different positions: he was the Managing Director and Chairman of March Gestión de Fondos and March Gestión de Pensiones, a director at Artá Capital, and Deputy Executive Chairman at Banca March between 2009 and 2015.

VIII. The Current Portfolio: A Deep Dive

Listed Investments Breakdown

As of the end of 2024, Alba's portfolio included stakes in nine listed companies across diverse sectors:

Stake: 19.3% Acerinox, 14.5% (Ebro Foods), 14.3% (CIE Automotive), 13.7% (Naturgy), 5.4%, 5.6%, 10.0%, 5.9%, 5.0% in various companies.

Acerinox (19.3%): The flagship holding. Founded in Spain in 1970, the Company is listed on the Continuous Market of the Spanish Stock Exchange and is a member of the selective IBEX35 index. With an international vocation since the beginning, Acerinox has now become the leader in the stainless steel market both in the United States and in the African continent.

Its production network is comprised of 15 factories distributed in three continents. The Group has 5 plants in its stainless steel division: three integrated flat product plants (Acerinox Europa, North American Stainless and Columbus Stainless) and two long product plants (Roldan and Inoxfil). The Group's High-Performance Alloys (HPA) Division (global leader in the HPA sector) is formed by VDM Metals and Haynes International, two companies that have 10 production centers throughout the United States and Germany.

The 2024 results showed the cyclical nature of the stainless steel business: Annual EBITDA amounted to €500 million, 28.9% lower than the previous year, mainly impacted by the decline in revenues in the Stainless division. For its part, the Special Alloys division obtained an EBITDA of €117 million, 33.4% lower than 2023, which registered a record in performance for the year. Net profit was €225 million (-1.4% vs. 2023).

Naturgy (5.4%): The energy utility stake provides exposure to Spain's energy transition. Naturgy's diversified infrastructure portfolio spans over more than 20 countries. Naturgy has the largest gas distribution and third-largest electricity distribution networks in Spain. It is also a major investor in renewables, with an existing portfolio of 4.6GW of capacity, including wind, solar and hydro-electric.

Ebro Foods (14.5%): A multinational food company operating in the rice and pasta sectors with presence in more than 25 countries, positioning itself as the world leader in the rice sector.

Viscofan (5.6%): The world leader in artificial casings for meat products and the only worldwide manufacturer that produces all categories of casing products (cellulose, collagen, fibrous and plastic).

CIE Automotive (14.3%): A global automotive components supplier with diversified geographic exposure.

Befesa (5.9%): One of the leading companies in waste recycling services, particularly steel dust and aluminum residue recycling, headquartered in Luxembourg.

Unlisted Investments

The private portfolio has grown increasingly significant. Corporación Financiera Alba has investments in unlisted companies both in Spain and abroad. These investments are mainly made directly, although Alba also has a number of smaller investments through holdings in Private Equity vehicles managed by Artá Capital SGEIC, S.A. and in the March P.E. Global funds of funds.

Atlantic Aviation: The U.S. FBO business remains a key holding, and values have increased substantially. KKR & Co. Inc. (NYSE:KKR) is weighing options for Atlantic Aviation FBO Inc., including a potential sale that could value the private jet fixed base operator at about $10 billion, people familiar with the matter said.

ERM: A global leading company specializing in environmental, health & safety and sustainability consulting services, with 5,500+ employees serving 3,500+ clients worldwide through 160 offices in 40 different countries.

Parques Reunidos: As of November 2025, Parques Reunidos continues as a private entity under the ownership of EQT (majority), GBL, and Alba, operating more than 30 parks primarily in Europe and Australia. Significant minority interests include Groupe Bruxelles Lambert (GBL) with 23% of the share capital and voting rights as of September 30, 2025, and Corporación Financiera Alba.

Real Estate Portfolio

Alba maintains significant real estate holdings focused on prime office properties. The company focuses on operating its own properties on a rental basis, with more than 80,000 square meters of office space in prime areas of Madrid and Barcelona.

IX. The Delisting Decision: End of an Era (2024-2025)

The Announcement

The Board of Directors of CORPORACIÓN FINANCIERA ALBA, S.A. ("Company" or "ALBA") at its meeting on 12 December 2024, unanimously agreed to submit for consideration and approval, as the case may be, to the Extraordinary General Shareholders' Meeting of the Company, to be held on 16 January 2025, at first call, and, if necessary, on 17 January 2025, at second call, a resolution for the delisting of the shares representing the Company's entire capital from the Madrid, Barcelona and Bilbao Securities Markets.

The Rationale

The delisting will be approved at the extraordinary meeting to be held in mid-January next year and is justified, according to the company itself, by "the low liquidity of Alba's shares in the stock market."

This rationale deserves scrutiny. Alba's shares had indeed been thinly traded relative to NAV—a common problem for holding company structures where the underlying value sits in portfolio companies rather than operating businesses. The discount to NAV had persisted for years, creating frustration for shareholders who could see underlying asset values but couldn't access them through the market price.

The Offer Structure

Clifford Chance is advising the Spanish investment firm Corporación Financiera Alba (Alba) on the launching of a public takeover bid for the delisting of all its shares from the Madrid, Barcelona and Bilbao Securities Markets, at a price of 84.20 euros per share.

The takeover bid is directed at all Alba shares, except for those held by shareholders who vote in favour of the delisting at the General Shareholders' Meeting (convened at first and second call for 16 and 17 January 2025) and block their shares until the end of the takeover bid acceptance period. The takeover bid has undertakings in that sense from shareholders holding a total of 94.46% of the share capital, so it will effectively be targeting a maximum number of shares representing 5.54% of the share capital.

And future cost savings due to delisting, as well as net financial debt and other assets and liabilities as at 30 June 2024, have been taken into account, resulting in a value per share of between EUR 82.4 and EUR 86.0. The Board of Directors, based on the Valuation Report, has considered the application of this method for the valuation of the Company to be the only appropriate method, as it best reflects the fair value of its shares as a sum of the different fair values of its investments, assets and liabilities.

Regulatory Approval and Completion

The Board of the National Securities Market Commission (CNMV) agreed to authorise the delisting offer for Corporación Financiera Alba (ALB) submitted by the company itself, Carlos March Delgado and Son Daviú, S.L.U. on 17 January 2025, on the understanding that its terms comply with current regulations and that the content of the explanatory brochure submitted after the latest amendments registered on 13 March 2025 is sufficient.

The acceptance period for the takeover bid for Corporación Financiera Alba begins on March 26, 2025, and runs through April 24, 2025.

Spain's National Securities Market Commission: TENDER OFFER FOR SHARES OF CORPORACION FINANCIERA ALBA BY DELISTING WAS ACCEPTED BY 86.11% OF SHARES TO WHICH OFFER WAS ADDRESSED.

Corporación Financiera Alba, S.A. has announced the exclusion of its shares from trading on the Madrid Stock Exchange, effective May 8, 2025.

And so it ended. After nearly 40 years as a public company, Alba became private. The shares that had traded on Spanish exchanges since 1986 were delisted. The March family's investment vehicle returned fully to family control.

Why Go Private?

The official rationale—low liquidity—captures only part of the story. Several factors likely drove the decision:

Chronic discount to NAV: Holding companies frequently trade at discounts to the sum of their parts, and Alba was no exception. Going private eliminates this value leakage.

Administrative burden: Public company compliance costs money and management attention. For a company that existed primarily to hold stakes in other companies, these costs provided little offsetting benefit.

Strategic flexibility: Private ownership allows longer-term thinking without quarterly earnings pressure. It enables restructuring decisions that might otherwise trigger market concerns.

Family control simplification: With the fourth generation assuming leadership, a private structure provides cleaner governance for family decision-making.

Cost savings: And future cost savings due to delisting, as well as net financial debt and other assets and liabilities as at 30 June 2024, have been taken into account, resulting in a value per share of between EUR 82.4 and EUR 86.0.

X. Investment Analysis: Bull & Bear Cases

Bull Case

Exceptional Track Record: Alba's nearly four decades of patient capital allocation have generated wealth across market cycles. The €6.4 billion in total investments and €6.7 billion in divestments since inception demonstrates disciplined capital recycling.

Structural Advantages: The March family's reputation and network provide deal flow and co-investment opportunities unavailable to typical institutional investors. The Atlantic Aviation investment alongside KKR exemplifies this access to premier deals.

Counter-Cyclical Capacity: We believe that Alba can find good investment opportunities, even in the current environment, thanks to its long-term vision, flexibility and zero debt. The zero-debt balance sheet provides crisis-era firepower.

Quality Portfolio: The current holdings represent market leaders in their respective sectors—stainless steel (Acerinox), food processing (Ebro Foods, Viscofan), automotive components (CIE Automotive), energy infrastructure (Naturgy).

Private Market Expertise: The unlisted portfolio, representing over 40% of assets, includes high-quality assets like Atlantic Aviation (potentially valued at $10 billion) and ERM. These positions may carry significant embedded value not fully reflected in NAV calculations.

Bear Case

Key Person Risk: The March family's expertise is concentrated in a small number of individuals. Generational transitions, while historically successful, always carry execution risk.

Concentration Risk: Despite sector diversification, the portfolio remains relatively concentrated in 15-25 positions. Single-company issues can materially impact NAV.

Cyclical Exposure: Major holdings in stainless steel (Acerinox) and automotive (CIE Automotive) provide significant exposure to industrial cycles. The 2024 results showed how quickly earnings can compress in these sectors.

Liquidity Lock-Up: As a now-private entity, investors have no exit mechanism other than family distributions or eventual future liquidity events.

Spain Exposure: Despite international expansion, the portfolio retains significant Spanish exposure at a time when European economic growth remains uncertain.

Porter's Five Forces Analysis

Supplier Power (Low to Moderate): As a capital provider, Alba's "suppliers" are its portfolio companies seeking investment. Alba's patient capital reputation and board-level engagement create value that attracts quality investment opportunities.

Buyer Power (Low): Alba's "buyers" are the companies seeking capital and the eventual acquirers of portfolio positions. Alba's long-term horizon and willingness to hold through cycles reduces pressure from opportunistic buyers.

Competitive Rivalry (Moderate): The European patient capital space includes other family-controlled holding companies (Exor, Wendel, GBL) and sovereign wealth funds. However, Alba's Spanish market expertise and March family network provide differentiation.

Threat of New Entrants (Low): Building the reputation, relationships, and track record required to compete with Alba takes decades. The March family's 100+ year history in Spanish finance creates barriers that new entrants cannot easily replicate.

Threat of Substitutes (Moderate): Direct investment in public markets, ETFs, and private equity funds all compete for investor capital. However, Alba's unique positioning—significant minority stakes with board influence—has few direct substitutes.

Hamilton Helmer's 7 Powers Framework

Counter-Positioning: Alba's patient capital approach contrasts with short-term-focused private equity. This positioning attracts companies and management teams seeking stable, long-term partners, creating opportunities others cannot access.

Scale Economies: Limited application—Alba's model doesn't require scale for efficiency.

Switching Costs: Portfolio companies face meaningful switching costs in replacing a supportive, long-term shareholder with potentially hostile or short-term investors.

Network Effects: The March family network creates self-reinforcing advantages—more board seats generate more deal flow, which generates more relationships.

Process Power: Decades of experience have refined Alba's due diligence, board engagement, and portfolio management processes in ways competitors cannot easily replicate.

Branding: The March name carries significant weight in Spanish finance, creating advantages in deal access and management relationships.

Cornered Resource: The March family itself represents a cornered resource—their history, relationships, and capital base cannot be duplicated.

XI. Key Metrics to Track

For investors and observers following Alba (now private) or similar holding company structures, three KPIs matter most:

1. NAV Growth Rate

The fundamental measure of Alba's success is growth in Net Asset Value per share over time. This captures both investment returns and capital allocation effectiveness.

In 2023, the Net Asset Value (NAV) increased by 9.6% to nearly €5.800 million. The following graph shows the evolution of NAV since the end of 2013, where it can be seen that Alba's NAV has grown by 79.4% over the last 10 years.

Tracking NAV growth versus relevant benchmarks (Eurostoxx 600, IBEX-35) reveals whether active management adds value versus passive index exposure.

2. Discount/Premium to NAV

For publicly-traded holding companies, the discount or premium to NAV reveals market sentiment and the effectiveness of value realization. Alba consistently traded at a discount, which ultimately drove the delisting decision.

For peers that remain public, this metric indicates whether the holding company structure creates or destroys value for shareholders.

3. Portfolio Company Performance

Alba's success ultimately depends on the performance of its portfolio companies. Key metrics include:

- Acerinox: EBITDA, production volumes, pricing, and special alloys division growth

- Naturgy: Regulated vs. liberalized business mix, renewable capacity additions, dividend sustainability

- Food sector (Ebro, Viscofan): Volume growth, margin stability, geographic expansion

- Unlisted holdings: Valuation marks, exit multiples, IRR realizations

Tracking underlying portfolio company metrics provides leading indicators of future NAV changes.

XII. Conclusion: Legacy and Future

The Alba story spans over a century—from Juan March's tobacco smuggling in Mallorca to the €5.7 billion private investment company that delisted in May 2025. It's a uniquely Spanish saga that intertwines with the nation's turbulent twentieth-century history: Civil War, dictatorship, democratic transition, European integration, and financial crisis.

For business analysts, Alba offers several enduring lessons:

Patient capital works: In an era of quarterly earnings pressure and activist hedge funds, Alba's multi-decade holding periods generated wealth through cycles. The approach requires family or institutional ownership structures willing to defer gratification.

Family businesses can perpetuate: Many family fortunes dissipate within three generations. The March family is now in its fourth generation of active management. Structures matter—the combination of bank, investment company, and foundation created distinct vehicles for different family interests while maintaining overall cohesion.

Reputation compounds: Juan March's controversial origins gave way to cultural patronage and conservative banking. The family transformed from "the last pirate of the Mediterranean" to stewards of Spain's most solvent bank. This reputational evolution took decades but created durable advantages.

Flexibility enables adaptation: Alba transformed from cement company to investment holding company when circumstances demanded. The portfolio rotation from construction to energy to international infrastructure shows continuous evolution. Rigid strategies rarely survive multiple market cycles.

The delisting raises questions about Alba's next chapter. Private ownership may accelerate portfolio repositioning, enable larger transactions, or facilitate different distribution policies. The family has navigated prior transitions successfully—from patriarch to heirs, from public to private, from Spanish to international focus.

Banca March is the only Spanish bank which is wholly family-owned and is seeking to position itself as a leading provider of private banking and corporate advisory services, with a long-term approach supported by the professionalisation of its governing bodies. Banca March boasts a unique, inimitable business model, underpinned by four pillars: shareholder commitment, exclusive products, outstanding quality service and excellent professionals.

Whatever comes next, the March family approach—patient capital, conservative finance, long-term relationships—has proven remarkably durable. From a peasant family in 1880s Mallorca to one of Europe's wealthiest dynasties in 2025, the story continues. The delisting marks not an ending but another chapter in an ongoing saga of Spanish capitalism's most distinctive family.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube