Artemis Medicare Services: India's Hospital Chain Built on Tyre Fortune

I. Introduction & Episode Roadmap

The conference room on the ninth floor of Apollo House in New Delhi carries the weight of industrial history. Photographs line the walls—black and white images of the early pipe factory, the first Apollo tyre rolling off the production line, and more recent color portraits of gleaming hospital corridors. This juxtaposition tells the story of one of India's most intriguing business diversifications: how a family that built its fortune on rubber and steel ventured into the business of healing.

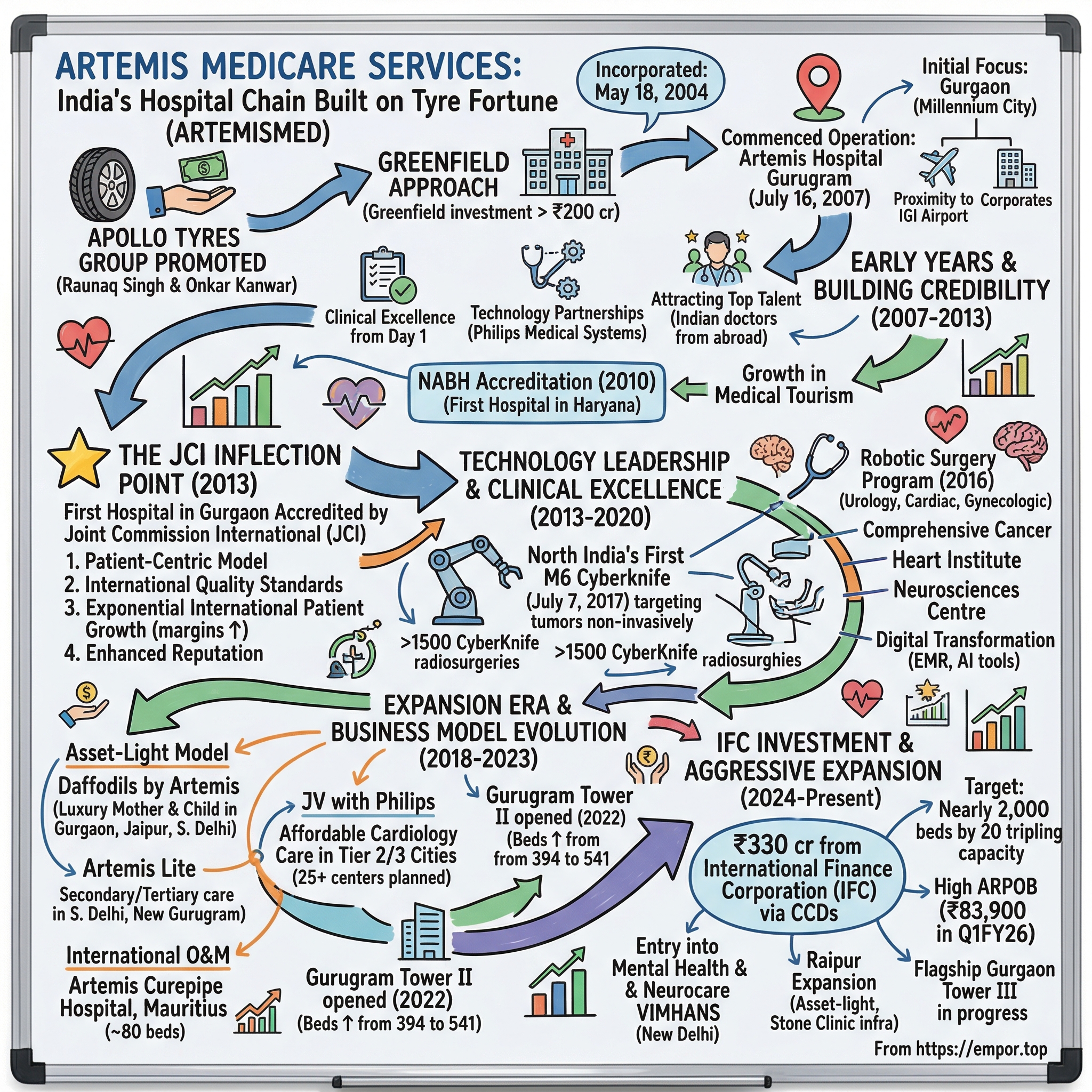

Promoted by Apollo Tyres Group, Artemis Medicare Services Ltd manages multi-specialty hospitals in Haryana under the brand Artemis Hospitals. The connection between tyres and healthcare might seem incongruous at first glance, but for the Kanwar family, it represented a natural evolution of their business philosophy—identifying critical needs in Indian society and building world-class solutions to address them. Just as Apollo Tyres had addressed India's transportation infrastructure needs in the 1970s, Artemis would tackle the healthcare infrastructure gap that became glaringly apparent as India entered the new millennium.

The timing of Artemis's entry into healthcare was no accident. In 2004, when the company was incorporated, India's healthcare sector was experiencing a fundamental shift. The country's growing middle class, with disposable incomes rising at double-digit rates, was increasingly unwilling to accept substandard medical care. Medical tourism was emerging as a significant opportunity, with international patients seeking high-quality care at fraction of Western costs. Gurgaon itself was transforming from a sleepy suburb into Millennium City, attracting multinational corporations and their employees who demanded international-standard healthcare facilities.

Artemis Hospital is spread across 9 acres, is a 395 bed state-of-the-art multispeciality hospital located in Gurugram. Artemis Health Institute is a healthcare venture launched by the Promoters of the Apollo Tyres Group. From its inception, the vision was clear: create a hospital that wouldn't just serve the local community but would become a destination for advanced medical care, attracting patients from across India and beyond.

The strategic decision to focus on Gurgaon was prescient. While established healthcare giants like Apollo Hospitals and Fortis were already present in Delhi, Gurgaon represented virgin territory with explosive growth potential. The proximity to Indira Gandhi International Airport made it accessible to international patients, while the burgeoning corporate landscape ensured a steady stream of insured patients seeking premium healthcare services.

What distinguished Artemis from other hospital ventures by industrial houses was its commitment to clinical excellence from day one. Rather than treating healthcare as just another business vertical, the Kanwar family approached it with the same engineering precision and quality obsession that had made Apollo Tyres successful. This meant significant upfront investments in technology, aggressive recruitment of top medical talent, and an unwavering focus on international accreditations that would validate their quality claims.

The company provides a comprehensive range of advanced medical and surgical services across specialties such as cardiology, oncology, orthopedics, neurology, nephrology, gastroenterology, and critical care. This wasn't about building just another multi-specialty hospital; it was about creating a healthcare ecosystem that could handle everything from routine check-ups to complex quaternary care procedures that were previously available only in a handful of institutions globally.

The financial architecture of the venture also reflected sophisticated thinking. Unlike many hospital projects that struggled with funding, Artemis leveraged the strong balance sheet and credibility of the Apollo Tyres Group while maintaining operational independence. This dual advantage—financial strength with entrepreneurial agility—would prove crucial as the hospital navigated its early years.

II. The Apollo Tyres Connection & Founding Story (2004-2007)

The boardroom at Apollo Tyres headquarters in early 2003 witnessed an unusual presentation. Onkar Kanwar has a keen interest in the field of education and health care. Artemis Health Sciences, promoted by him, is an enterprise focusing on state-of-the-art medical care and runs a cutting edge multi-specialty medical facility which focuses on holistic treatment. Rather than the usual charts showing tyre sales projections and rubber procurement costs, the slides displayed hospital bed occupancy rates, medical equipment specifications, and patient flow diagrams. For a company that had spent three decades perfecting the art of tyre manufacturing, this represented uncharted territory.

The genesis of Artemis can be traced to Onkar Kanwar's personal observations about India's healthcare landscape. Having traveled extensively across the globe for Apollo Tyres business, Kanwar had experienced world-class healthcare facilities in the US, Europe, and Singapore. The contrast with what was available in India, even in the national capital region, was stark. While India had talented doctors—many of whom had trained at prestigious international institutions—the infrastructure and systems were decades behind global standards.

Kanwar also owns speciality hospitals under the Artemis brand in northern India. The decision to enter healthcare wasn't made lightly. The Apollo Tyres board initially expressed skepticism about diversifying into such an unrelated field. Healthcare was capital-intensive, heavily regulated, and required expertise that a tyre company simply didn't possess. Yet Kanwar's vision extended beyond mere financial returns. He saw healthcare as a sector where the Apollo group could create lasting social impact while building a sustainable business.

The choice of location was strategic and deliberate. Gurgaon in 2004 was experiencing unprecedented growth. The Haryana government's pro-business policies had attracted numerous multinational corporations, creating a new urban center that desperately needed modern infrastructure—including hospitals. Land was still relatively affordable compared to South Delhi, and the proximity to the airport made it ideal for medical tourism.

The initial investment approach was conservative yet ambitious. Rather than acquiring an existing hospital—a strategy many corporate houses preferred—Artemis decided to build from scratch. This greenfield approach meant higher initial costs but offered complete control over design, technology selection, and operational philosophy. The nine-acre plot selected for the hospital was large enough to accommodate future expansion, a foresight that would prove valuable as the hospital grew.

Technology partnerships formed the backbone of Artemis's differentiation strategy. A technology tie-up with Philips Medical Systems allows Artemis early and exclusive access to the latest global imaging and monitoring equipment. This wasn't just about buying expensive machines; it was about creating an ecosystem where cutting-edge technology could be leveraged effectively. The partnership with Philips went beyond simple vendor relationships—it included training programs, maintenance support, and early access to new technologies before they were widely available in India.

The recruitment strategy was equally thoughtful. Rather than poaching entire teams from competitors—a common practice in the industry—Artemis focused on attracting Indian doctors working abroad who wanted to return home. The pitch was compelling: practice medicine at international standards without leaving India, backed by infrastructure that matched the best hospitals globally. This approach not only brought clinical expertise but also international best practices in patient care and hospital management.

Construction began in 2005 with meticulous attention to detail. The hospital design incorporated learnings from leading international facilities, with wide corridors for easy patient movement, natural lighting in patient rooms, and dedicated zones for different specialties. The infection control systems were designed to meet JCI standards from day one, even though accreditation would come years later. Every aspect, from the placement of hand sanitizer dispensers to the air handling systems in operation theaters, was planned with international benchmarks in mind.

The financial structure of the project reflected the group's commitment. While the total initial investment exceeded ₹200 crores—a significant sum in 2005—the funding came primarily from internal accruals of the Apollo Tyres Group rather than debt. This provided financial flexibility and demonstrated to stakeholders that the group was serious about the healthcare venture. It also meant that Artemis could focus on building clinical excellence without the pressure of servicing heavy debt from day one.

III. Early Years & Building Credibility (2007-2013)

It commenced the commercial operation by setting up Artemis Hospital (formerly Artemis Health Institute) at Gurugram on July 16 2007. The first patient walked through the doors on a humid July morning, but the grand opening belied the challenges that lay ahead. The Gurgaon healthcare market of 2007 was already competitive, with established players like Fortis and Max having built strong brand recognition. For Artemis, the new entrant backed by a tyre company, credibility wouldn't come easy.

The initial months were sobering. Despite state-of-the-art infrastructure and equipment, patient footfalls remained below projections. The challenge wasn't quality—early patients consistently praised the facilities and care—but awareness and trust. In healthcare, unlike consumer goods, brand building happens one patient at a time. Word-of-mouth travels slowly, and in life-or-death situations, patients naturally gravitated toward established names.

Dr. Devlina Chakravarty, who would later become Managing Director, recalled the early struggle to attract top specialists. "Doctors with established practices were reluctant to move. They would visit, appreciate our facilities, but worry about patient volumes. It was a chicken-and-egg problem—we needed renowned doctors to attract patients, but doctors wanted to see patient flow before committing." The solution came through innovative partnership models, offering doctors not just competitive compensation but equity-like participation in department growth.

It is the first Hospital in Haryana to get NABH accreditation within 3 years of start up. This early achievement in 2010 marked a turning point. NABH accreditation required demonstrating consistent adherence to over 600 quality parameters, from clinical protocols to patient safety measures. For a three-year-old hospital to achieve this was remarkable and sent a strong signal to the market about Artemis's commitment to quality.

The technology differentiation strategy began paying dividends by 2009. While competitors focused on adding beds, Artemis invested in specialized equipment that enabled complex procedures. The hospital performed Haryana's first robotic surgery in 2010, generating significant media coverage. These "firsts" became a recurring theme—first hospital in Gurgaon to perform a particular procedure, first in Haryana to install specific equipment. Each achievement built credibility incrementally.

International patient care emerged as an unexpected early success. Artemis's proximity to the airport, combined with its international-standard facilities, attracted patients from Afghanistan, Africa, and Central Asia. The hospital quickly developed specialized services for international patients, including dedicated coordinators, translation services, and customized meal plans. By 2011, international patients contributed nearly 15% of revenues, well above industry averages.

The medical outcomes during these early years were impressive. The cardiac surgery department, despite being new, achieved success rates comparable to established centers. The oncology department, leveraging advanced radiation therapy equipment, began attracting patients who would have otherwise gone to Tata Memorial Hospital in Mumbai. These clinical successes, documented and published in medical journals, helped establish academic credibility alongside commercial growth.

The company provides a comprehensive range of advanced medical and surgical services across specialties such as cardiology, oncology, orthopedics, neurology, nephrology, gastroenterology, and critical care. This comprehensive capability meant that complex cases requiring multi-disciplinary intervention could be handled in-house, a significant advantage over smaller specialty hospitals.

Financial discipline during these early years proved crucial. While the hospital wasn't profitable in the first two years—common in the healthcare industry—careful cost management ensured that losses remained manageable. The focus was on building sustainable operations rather than aggressive expansion. This meant saying no to opportunities that might have boosted short-term revenues but compromised long-term positioning.

The corporate healthcare segment became a focus area by 2010. Artemis aggressively pursued contracts with multinational corporations in Gurgaon, offering comprehensive health check-up packages and emergency care services. The hospital's location in the heart of the corporate district, combined with its international standards, made it the preferred choice for many companies. These corporate tie-ups provided steady patient flow and helped build the Artemis brand among affluent, health-conscious consumers.

Training and development initiatives set Artemis apart from competitors who often neglected nursing and paramedical staff. The hospital established comprehensive training programs, partnering with international institutions to ensure that not just doctors but the entire care team met global standards. This investment in human capital paid dividends through lower attrition rates and consistently high patient satisfaction scores.

Community engagement programs, though not immediately profitable, built crucial goodwill. Free health camps in nearby villages, subsidized treatment for economically weaker sections, and health awareness programs in schools created positive brand associations. These initiatives, personally overseen by Onkar Kanwar, reflected the group's philosophy that healthcare was about service, not just business.

IV. The JCI Accreditation Inflection Point (2013)

The assessment team from Joint Commission International arrived on a February morning in 2013, their clipboards and checklists ready to evaluate every aspect of Artemis Hospital's operations. For the next five days, they would scrutinize everything from hand hygiene compliance rates to medication error protocols, from patient identification procedures to fire safety systems. The stakes couldn't have been higher. Artemis was the first hospital in Gurgaon to be accredited by Joint Commission International (JCI) in 2013.

The journey to JCI accreditation had begun two years earlier. Unlike NABH, which focused primarily on Indian healthcare standards, JCI represented the gold standard of international healthcare quality. Fewer than 20 hospitals in India had achieved this accreditation by 2013. The process required fundamental changes in how the hospital operated, from clinical documentation to patient safety protocols. Every process had to be standardized, documented, and consistently followed.

Dr. Aditya Gupta, who would later become Director of Neurosurgery, remembered the transformation: "JCI wasn't just about meeting standards; it was about changing our DNA. We had to shift from a doctor-centric to a patient-centric model. Every decision, every protocol had to be viewed through the lens of patient safety and clinical outcomes." The cultural shift was challenging, particularly for senior doctors accustomed to autonomous decision-making.

The financial investment in JCI preparation exceeded ₹15 crores. This included upgrading information systems to ensure complete electronic medical records, installing advanced patient monitoring systems, and implementing comprehensive staff training programs. The hospital conducted over 200 training sessions in the six months leading up to the assessment, ensuring that every staff member, from senior surgeons to housekeeping staff, understood their role in maintaining JCI standards.

The accreditation's impact was immediate and transformative. International patient inquiries increased by 300% within six months of receiving JCI certification. Insurance companies that had been hesitant to partner with a relatively young hospital now actively sought tie-ups. Corporate clients, particularly multinational companies, viewed JCI accreditation as validation that Artemis met the same standards as hospitals in their home countries.

More importantly, JCI accreditation created a sustainable competitive advantage. While competitors could replicate equipment and infrastructure, building the organizational culture and systems required for JCI took years. The rigorous re-accreditation process every three years meant that standards had to be maintained consistently, not just achieved once. This created a high barrier to entry that protected Artemis's premium positioning.

The medical tourism opportunity exploded post-JCI. Artemis partnered with international facilitators, participated in global healthcare conferences, and developed specialized packages for international patients. The hospital's international patient department expanded from 3 to 25 staff members within a year. Revenue from international patients grew from ₹25 crores in 2012 to over ₹80 crores by 2014, with margins significantly higher than domestic patients.

Clinical outcomes improved measurably after JCI implementation. Hospital-acquired infection rates dropped by 60%, medication errors decreased by 75%, and patient satisfaction scores increased from 82% to 94%. These improvements weren't just statistics—they translated into real clinical benefits. The cardiac surgery department's mortality rate fell below 1%, matching the best centers globally. The oncology department's treatment protocols, standardized according to international guidelines, showed improved survival rates across cancer types.

The organizational confidence that came with JCI accreditation enabled bolder clinical initiatives. Artemis began tackling cases that would have been referred to larger centers earlier. The neurosurgery department started performing complex brain tumor surgeries, the cardiac team took on high-risk cardiac procedures, and the transplant program expanded beyond kidneys to livers. Each success built upon the last, creating a virtuous cycle of capability building.

The talent attraction dynamic shifted dramatically. Previously, Artemis had to convince doctors to join; post-JCI, leading specialists actively sought positions. The hospital received over 500 applications for 20 specialist positions advertised in 2014. Young doctors saw Artemis as a place where they could practice international-standard medicine without leaving India. This influx of talent further strengthened clinical capabilities.

This is a 600-bed hospital with systematic units designed to provide complete care. The infrastructure investments made during JCI preparation—from modular operation theaters to advanced ICUs—positioned Artemis to handle continued growth. The hospital's bed occupancy rate increased from 55% in 2012 to 75% by the end of 2013, with average revenue per occupied bed growing by 40%.

V. Technology Leadership & Clinical Excellence (2013-2020)

The unveiling ceremony in July 2017 drew an unusual crowd to Artemis Hospital. Government officials, healthcare leaders, and surprisingly, cancer patients from across North India gathered to witness something unprecedented in the region. Artemis Hospital launched the first M6 Cyberknife in North India on July 7, 2017. As the robotic arms of the M6 Cyberknife performed their demonstration, moving with balletic precision to target a tumor model, there was a palpable sense that healthcare in North India had crossed a threshold.

North India's first M6 CyberKnife at Artemis Hospitals. Transforming treatments for optimal outcomes. The ₹40 crore investment in the Cyberknife represented more than just equipment acquisition. It was a statement of intent—that Artemis would compete not just with Indian hospitals but with the best cancer centers globally. The technology enabled non-invasive treatment of tumors previously considered inoperable, particularly in the brain and spine. Patients who would have traveled to Singapore or the US for such treatment could now receive it in Gurgaon.

Dr. Aditya Gupta, Director of Neurosurgery and Cyberknife Centre, explained the transformation: "The M6 wasn't just about having advanced technology. It fundamentally changed how we approach cancer treatment. We could now offer hope to patients with tumors near critical structures, treat multiple metastases in a single session, and achieve sub-millimeter precision without opening the skull." Within the first year, Artemis performed over 500 Cyberknife procedures, with success rates exceeding 95%.

The technology acquisition strategy during this period was methodical and strategic. Rather than buying equipment for prestige, each investment was evaluated based on clinical need, competitive differentiation, and revenue potential. The 3 Tesla MRI system, installed in 2015, enabled advanced neuroimaging that supported the growing neurosurgery program. The hybrid operating room, combining surgical and imaging capabilities, positioned Artemis at the forefront of minimally invasive surgery.

Artemis has achieved a significant milestone in medical science by successfully completing over 1500 CyberKnife radiosurgeries. Artemis Hospital solidifies its position as one of the largest and most experienced centers for CyberKnife radiosurgery in India, particularly for brain-related treatments. This volume created a virtuous cycle—more cases meant more experience, leading to better outcomes, attracting more complex cases.

The robotic surgery program, launched in 2016, exemplified Artemis's approach to technology adoption. Rather than simply acquiring robots, the hospital invested heavily in surgeon training, sending teams to leading centers in the US and Europe. The program started with urology and gradually expanded to cardiac, colorectal, and gynecologic surgery. By 2019, Artemis was performing over 200 robotic procedures annually, with outcomes comparable to international benchmarks.

Digital transformation accelerated during this period. The hospital implemented a comprehensive Electronic Medical Record (EMR) system that integrated clinical, administrative, and financial data. Artificial intelligence tools were deployed for radiology, helping detect abnormalities in X-rays and CT scans. Telemedicine capabilities, established initially for follow-up consultations, proved prescient when COVID-19 struck. These digital investments improved efficiency while enhancing patient experience.

The center-of-excellence approach drove clinical specialization. Rather than trying to excel at everything, Artemis identified key areas for focused development. The Comprehensive Cancer Centre integrated medical, surgical, and radiation oncology under one roof. The Heart Institute combined interventional cardiology, cardiac surgery, and cardiac rehabilitation. The Neurosciences Centre brought together neurology, neurosurgery, and neurointervention. Each centre operated semi-autonomously, with dedicated resources and leadership, while leveraging the hospital's shared infrastructure.

International collaborations enhanced clinical capabilities. Artemis partnered with leading institutions like Johns Hopkins for second opinions, Mayo Clinic for clinical protocols, and Cleveland Clinic for cardiac surgery training. These partnerships went beyond mere MOUs—they involved regular case discussions, visiting professorships, and joint research projects. The collaborations not only improved clinical outcomes but also enhanced Artemis's credibility with international patients.

Research and academics became integral to Artemis's identity during this period. The hospital established a dedicated research department, supporting clinical trials and investigator-initiated studies. Over 50 research papers were published in peer-reviewed journals between 2015 and 2020. The DNB (Diplomate of National Board) training programs in multiple specialties attracted talented junior doctors, creating a pipeline of trained specialists while enhancing the hospital's academic reputation.

The COVID-19 pandemic in 2020 tested Artemis's resilience and adaptability. The hospital rapidly converted floors into COVID ICUs, established dedicated COVID treatment protocols, and implemented comprehensive staff safety measures. Despite the challenges, Artemis maintained non-COVID services for cancer and cardiac patients who couldn't delay treatment. The hospital's strong financial position, built over years of disciplined growth, enabled it to weather the crisis without layoffs or salary cuts, earning significant employee loyalty.

VI. Expansion Era & Business Model Evolution (2018-2023)

The architectural plans spread across the boardroom table in early 2018 told a story of ambition. Tower 2 of Artemis Hospital Gurgaon was ready to open, Tower 3 was being designed, and feasibility studies for new locations filled multiple folders. The Company commenced operations of new Tower II in Gurugram in 2022. The expansion of the Hospital Building increased bed capacity from 394 beds to 541 beds. For a hospital that had taken a decade to establish its first 400 beds, the acceleration was remarkable.

The expansion strategy reflected sophisticated thinking about healthcare delivery models. Rather than simply replicating the flagship hospital, Artemis developed differentiated formats for different market segments. The asset-light model, introduced through Artemis Lite and Daffodils brands, targeted different customer segments without the capital intensity of full-scale hospitals.

The Company opened two new units of 'Daffodils by Artemis', one each in Jaipur and South Delhi in addition to the one already operating in Gurugram in 2023. It introduced the multi-speciality hospital under the brand of 'Artemis Lite' catering to secondary/tertiary care market and opened the first centre in South Delhi. Daffodils, positioned as a luxury mother and child care brand, targeted affluent families seeking premium birthing experiences. With designer suites, gourmet meal options, and personalized care protocols, Daffodils commanded premium pricing while requiring minimal capital investment.

Artemis Lite addressed a different opportunity—the vast secondary care market underserved by both government hospitals and premium private facilities. These 25-30 bed units, located in residential neighborhoods, offered quality healthcare at accessible price points. The model leveraged Artemis's brand and clinical protocols while keeping infrastructure costs minimal. It opened a new unit under the 'Artemis Lite' brand in New Gurugram area in June, 2023.

The joint venture with Philips Medical Systems represented another innovative approach. The equipment for these centres would be provided by Philips. Through this Artemis offers comprehensive affordable cardiology care in tier 2 and 3 cities. The company's vision is to build up 25+ such centres in next 3-4 years from current 8 operational centres. Rather than Artemis investing capital in equipment, Philips provided the technology while Artemis managed operations—a win-win that enabled rapid expansion into underserved markets.

International expansion took an unexpected turn with Mauritius. The Company established the first of the two hospitals in Mauritius, a ~80-bed facility under the brand of 'Artemis Curepipe Hospital' as part of the Operations and Management agreement. This wasn't about capital investment but leveraging Artemis's operational expertise. The management contract model, common in the hospitality industry but rare in Indian healthcare, provided steady fee income without capital risk.

The doctor engagement model evolved significantly during this period. Artemis moved from a primarily full-time employment model to a hybrid approach. Senior consultants were offered flexible arrangements—practicing at Artemis while maintaining limited private practice. Younger doctors received comprehensive training and clear career progression paths. The medical education programs, including DNB and fellowship programs, created a talent pipeline while generating revenue.

Technology-enabled care delivery became a differentiator. The telemedicine platform, initially developed for follow-ups, expanded to include second opinions, international consultations, and post-operative monitoring. Home healthcare services, launched in 2019, extended Artemis's reach beyond hospital walls. These services not only generated additional revenue but also improved patient outcomes through better continuity of care.

The payer mix optimization strategy showed sophisticated revenue management. While maintaining its position in the premium segment, Artemis strategically expanded insurance partnerships. The hospital worked with TPAs (Third Party Administrators) to streamline claim processing, reducing settlement times from 45 to 15 days. Government schemes like Ayushman Bharat were selectively accepted for specific procedures where margins remained acceptable.

Supply chain optimization delivered significant cost savings. Artemis joined group purchasing organizations for commodities while maintaining direct relationships for critical supplies. Inventory management systems reduced working capital requirements by 25%. Energy efficiency initiatives, including solar panels and LED lighting, cut utility costs by 30%. These operational improvements flowed directly to the bottom line.

Clinical specialization deepened during this period. The transplant program expanded from kidneys to include liver and bone marrow transplants. The cardiac surgery team pioneered minimally invasive techniques, performing keyhole heart surgeries that reduced recovery time from weeks to days. The oncology department introduced immunotherapy and targeted therapy protocols, offering cutting-edge treatment options previously available only at specialized cancer centers.

Quality metrics continued improving, validating the expansion strategy. Patient satisfaction scores remained above 90% across all facilities. Clinical outcome indicators—surgical site infections, readmission rates, mortality rates—matched or exceeded international benchmarks. These metrics weren't just internal scorecards; they were regularly audited by insurance companies and accreditation bodies, providing external validation.

VII. The IFC Investment & Aggressive Expansion (2024-Present)

The announcement in May 2024 sent ripples through India's healthcare investment community. Artemis Medicare Services Ltd said its board approved raising Rs 330 crore from International Finance Corporation through a preferential issue of unsecured compulsorily convertible debentures. The company approved the issuance of up to 33,000 fully-paid unsecured compulsorily convertible debentures to International Finance Corporation. For the World Bank's investment arm to back a mid-sized Indian hospital chain was significant—it validated not just Artemis's track record but its future potential.

The IFC investment represented more than capital—it was a strategic partnership that would accelerate Artemis's transformation from a regional player to a potential national champion. The structure—convertible debentures rather than direct equity—provided flexibility while minimizing immediate dilution. The CCDs shall be convertible into equity shares of the company having a face value of Re 1 each, in one or more tranches, within a period of up to 18 months from the date of allotment, at a conversion price of Rs 174.03 per equity share.

The expansion plans unveiled alongside the IFC investment were audacious. ARTMSL marks its entry into mental health and expand neurocare, committing INR 60,000 Mn over the next 2–3 years. The binding MoU with VIMHANS (Vidyasagar Institute of Mental Health and Neuro & Allied Sciences) marked Artemis's entry into mental health—a severely underserved segment in India. The Company will execute a Medical Services Agreement for granting the exclusive rights to operate, manage, and provide medical services at VIMHANS located in Nehru Nagar, New Delhi. The Company is expected to incur an investment of ~ Rs. 550 - 600 crore for the project in next 2-3 years.

The Raipur expansion, announced in November 2024, showcased another innovative model. The new hospital in Raipur will be developed by Raipur Stone Clinic, which will be responsible for building the infrastructure. The Company, on the other hand, will invest approximately Rs 110 crore in medical equipment and related capital expenses. This asset-light approach—partner builds infrastructure, Artemis provides equipment and operations—enabled expansion without massive capital outlays.

The ambitious targets reflected newfound confidence. Management projected increasing bed capacity from the current 713 to nearly 2,000 beds by 2029—effectively tripling size in five years. This wasn't just about adding beds; each expansion targeted specific gaps in India's healthcare infrastructure. The VIMHANS facility would address mental health, Raipur would serve central India's underserved population, and Tower 3 in Gurgaon would handle the growing demand for quaternary care.

Financial performance validated the expansion strategy. The average revenue per occupied bed (ARPOB) went up to ₹83,900, the highest it has ever been. This industry-leading ARPOB reflected Artemis's successful positioning in high-value specialties. International patients now contributed 29% of revenues, up from 26% just two years earlier, with significantly higher margins than domestic patients.

The technology investments continued with strategic focus. India's first private Geriatrics & Longevity Department, launched in 2024, targeted the growing elderly population with specialized services. The partnership with KIMS Hyderabad for heart-lung transplants positioned Artemis among the few centers in North India capable of such complex procedures. Each addition carefully chosen to enhance clinical capabilities while generating sustainable returns.

Operational efficiency improvements funded growth without compromising margins. The flagship Gurgaon hospital achieved EBITDA margins of 20.5% in Q1 FY26, despite being in expansion mode. Cost optimization initiatives—from energy management to clinical supply chains—saved over ₹25 crores annually. These savings were reinvested in technology and talent, creating a virtuous cycle of improvement.

The competitive landscape shifted in Artemis's favor. While larger chains like Apollo and Fortis faced challenges from debt and aggressive expansion, Artemis's measured growth and strong balance sheet positioned it as a consolidator rather than a target. The company actively evaluated acquisition opportunities, looking for distressed assets that could be turned around using Artemis's operational expertise.

Digital health initiatives accelerated post-COVID. The Artemis Health app, launched in 2024, integrated appointment booking, medical records, and telemedicine consultations. AI-powered diagnostic tools improved accuracy while reducing turnaround times. These digital investments weren't just about efficiency—they created new revenue streams and improved patient stickiness.

The talent strategy evolved to support rapid expansion. Artemis established a medical college partnership for training nurses, addressing the chronic shortage of skilled nursing staff. Leadership development programs identified and groomed internal talent for new facilities. International recruitment drives brought specialized expertise in areas like robotic surgery and interventional radiology.

Sustainability initiatives, while generating positive publicity, also improved economics. Solar installations reduced energy costs, water recycling cut utility bills, and waste management programs generated revenue from medical waste processing. These initiatives resonated with ESG-focused investors while improving operational margins.

VIII. Business Model & Unit Economics Analysis

The spreadsheet on the CFO's screen told a story of transformation. In 2015, Artemis's revenue per bed was ₹40 lakhs annually—respectable but not exceptional. By 2024, this had more than doubled to over ₹85 lakhs, placing Artemis among the most productive hospital assets in India. Understanding this transformation requires dissecting the intricate mechanics of hospital economics.

ARTMSL's flagship Gurgaon hospital recorded the highest ARPOB (INR 83,900 in Q1FY26), driven by advanced clinical programs such as robotic surgery and CyberKnife. This metric—average revenue per occupied bed—is healthcare's equivalent of revenue per available room in hotels. But unlike hotels where a room is a room, hospital beds generate vastly different revenues depending on the specialty, procedure complexity, and patient profile.

The specialty mix optimization drove significant value creation. Artemis deliberately shifted toward high-value specialties—cardiac surgery, neurosurgery, oncology, and transplants—where margins exceeded 30%. General medicine and routine surgeries, while necessary for volumes, were de-emphasized. By 2024, quaternary care procedures contributed 45% of revenues despite representing only 20% of patient volumes.

The international patient strategy exemplified margin maximization. International Patients generate the highest ARPOB and strong EBITDA margin at Gurgaon. This segment's share rose from 26% in FY23 to 29% in FY25, and expected to exceed 30% after the ~600-bed South Delhi facility launch. International patients paid premium rates—often 2-3x domestic prices—while requiring minimal bad debt provisioning. The higher margins offset the costs of international patient services, including coordinators, interpreters, and premium amenities.

The asset utilization model showed sophisticated thinking. Unlike competitors who measured success by bed count, Artemis focused on asset productivity. Operation theaters ran extended hours with staggered scheduling. Diagnostic equipment operated round-the-clock with shift-based staffing. ICU beds, the most expensive assets, maintained 85%+ occupancy through careful case selection and efficient discharge planning.

Doctor compensation structures balanced multiple objectives. Senior consultants received revenue-sharing arrangements, aligning their interests with hospital profitability. Junior doctors got fixed salaries plus performance incentives based on patient satisfaction and clinical outcomes. Visiting consultants paid facility fees, generating revenue without employment costs. This hybrid model optimized costs while attracting top talent.

The procurement strategy leveraged scale while maintaining flexibility. High-volume commodities—syringes, gloves, basic medications—were sourced through group purchasing organizations achieving 15-20% cost savings. Specialized items—implants, high-end drugs—were negotiated directly with manufacturers, often securing consignment arrangements that reduced working capital. Just-in-time inventory management freed up cash while ensuring availability.

Revenue cycle management emerged as a hidden profit driver. Insurance claim denial rates dropped from 12% to 4% through better documentation and proactive authorization. Collection periods shortened from 90 to 45 days through automated follow-ups and early intervention. Bad debt provisioning decreased from 8% to 3% of revenues through better patient screening and flexible payment plans. These improvements added directly to bottom-line profitability.

The cost structure revealed operational discipline. Staff costs at 35% of revenues compared favorably to the industry average of 40%, achieved through productivity improvements rather than low wages. Material costs at 25% reflected efficient procurement without compromising quality. Administrative expenses at 12% demonstrated lean operations despite regulatory compliance requirements.

Technology investments, while requiring upfront capital, generated attractive returns. The Cyberknife, despite costing ₹40 crores, generated ₹25 crores annual revenue with 60% EBITDA margins. Robotic surgery systems, costing ₹15 crores each, paid back in under three years through premium pricing and higher volumes. Digital initiatives reduced operational costs by 10% while improving patient experience.

The network effects became increasingly apparent. As Artemis added specialties, cross-referrals increased. A cardiac patient might need nephrology consultation; a cancer patient might require pain management. Each specialty strengthened others, creating a comprehensive ecosystem that retained patients within the Artemis network. This reduced customer acquisition costs while increasing lifetime value.

Capital allocation decisions reflected strategic priorities. Growth capital focused on high-return investments—new towers at existing sites leveraging shared infrastructure. Maintenance capital ensured equipment remained cutting-edge, crucial for attracting both patients and doctors. Working capital optimization freed up cash for expansion. The result: Return on Capital Employed exceeding 20%, well above the cost of capital.

IX. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's 5 Forces Analysis

Supplier Power: Moderate to High The medical equipment industry's oligopolistic structure grants significant leverage to suppliers like GE, Siemens, and Philips. Artemis's strategic partnership with Philips partially mitigates this, providing preferential access and pricing. However, the real constraint lies in specialized medical talent. Star surgeons command premium compensation and can dictate terms. Artemis addresses this through its comprehensive talent development programs and flexible engagement models, but supplier power remains a constant pressure on margins.

Buyer Power: Segmented and Complex The buyer landscape in Indian healthcare is uniquely fragmented. Individual patients paying out-of-pocket have minimal negotiating power, accepting quoted prices for life-saving procedures. However, insurance companies and government schemes exercise considerable leverage, demanding discounted rates and questioning treatment protocols. Artemis's strategy of focusing on international patients and premium segments reduces buyer power impact. Corporate clients, while demanding, provide predictable volumes that offset their negotiating strength.

Threat of New Entrants: Moderate While capital requirements for a 500+ bed quaternary care hospital exceed ₹500 crores, creating significant barriers, the threat manifests differently. Single-specialty chains like eye or dental hospitals can enter with lower investment. International chains eye the Indian market's growth potential. However, Artemis's JCI accreditation, established clinical reputation, and prime Gurgaon location create sustainable moats. The real barrier isn't capital but the decade required to build clinical credibility and patient trust.

Substitutes: Limited but Evolving For complex procedures, substitutes remain limited—a brain tumor requires surgery, not alternative medicine. However, telemedicine platforms increasingly handle consultations and follow-ups. Wellness programs potentially reduce disease incidence. Medical tourism to Thailand or Turkey offers price competition. Artemis combats substitution by moving up the complexity chain, focusing on procedures where substitutes don't exist while embracing telemedicine as a complementary service.

Competitive Rivalry: Intense The NCR healthcare market resembles a battleground. Max Healthcare, Fortis, Medanta, and Apollo compete fiercely for patients, doctors, and corporate contracts. Price competition exists but remains secondary to clinical outcomes and doctor reputation. Artemis differentiates through technology leadership—being first with Cyberknife, robotic surgery, and specialized programs. The rivalry drives continuous improvement but also enables premium pricing for demonstrated superior outcomes.

Hamilton's 7 Powers Framework

Scale Economies: Emerging Artemis exhibits classic hospital economics where fixed costs—infrastructure, equipment, specialists—spread across growing patient volumes. The flagship Gurgaon hospital's expansion from 400 to 541 beds improved margins by 300 basis points. Shared services across facilities—centralized procurement, diagnostics, and administration—reduce per-unit costs. However, Artemis hasn't yet achieved the national scale of Apollo or Fortis that would maximize this power.

Network Effects: Strong in Specific Contexts Healthcare typically lacks traditional network effects, but Artemis creates them through clinical ecosystems. More specialties attract more complex cases requiring multi-disciplinary care. The medical education programs create alumni networks referring patients. International patient facilitators channel cases to established partners. Each additional node—doctor, specialty, or referring hospital—makes the network more valuable, though effects remain regional rather than national.

Switching Costs: Moderate to High Patients face significant switching costs—medical records, doctor relationships, and treatment continuity create stickiness. Corporate contracts involve multi-year commitments and employee familiarity. Insurance partnerships require system integration and claim history. However, switching costs work both ways—attracting patients from competitors requires overcoming similar barriers. Artemis's strategy focuses on first-time patients for complex procedures where switching costs haven't yet developed.

Branding: Building but Not Dominant The Artemis brand carries weight in Gurgaon and among international patients but lacks Apollo's national recognition. JCI accreditation provides third-party validation, while successful clinical outcomes build word-of-mouth reputation. The association with Apollo Tyres provides corporate credibility but doesn't translate directly to healthcare trust. Brand power grows slowly in healthcare, built patient by patient, outcome by outcome.

Cornered Resource: Location and Equipment Artemis's nine-acre Gurgaon campus, strategically located near the airport and corporate hub, represents an irreplaceable asset. Competitors cannot replicate this location advantage. The M6 Cyberknife, as North India's first and only such installation for several years, provided temporary resource advantage. Exclusive arrangements with certain international medical institutions create privileged access to expertise and protocols, though these advantages erode as competitors catch up.

Process Power: Developing JCI accreditation forced process standardization that competitors struggle to replicate quickly. Clinical protocols refined over thousands of cases—like the Cyberknife treatment algorithms—create superior outcomes. The international patient handling process, developed over years, provides seamless experience competitors find hard to match. However, process advantages in healthcare are vulnerable to talent poaching, as processes often reside in people rather than systems.

Counter-positioning: Limited Application Artemis doesn't fundamentally counter-position against established competitors. Unlike disruptive models challenging traditional hospitals, Artemis operates within conventional frameworks. The asset-light expansion through Artemis Lite represents mild counter-positioning—serving markets incumbents ignore—but isn't revolutionary. True counter-positioning would require challenging fundamental healthcare delivery assumptions, which Artemis hasn't attempted.

X. Bear vs. Bull Case & Financial Analysis

The Bull Case: India's Healthcare Transformation Play

The investment thesis for Artemis Medicare starts with a simple observation: India spends just 3.5% of GDP on healthcare versus 8-10% in developed nations, yet its disease burden rivals any developing economy. This spending gap represents a multi-decade growth opportunity as rising incomes, insurance penetration, and aging demographics drive healthcare consumption. Artemis, positioned in India's wealthiest region with proven execution capabilities, stands to capture disproportionate value from this transformation.

Share price moved up by 274.53% over last 3 Years. This performance reflects market recognition of Artemis's transformation from a single hospital to a scalable healthcare platform. The IFC investment provides validation from sophisticated institutional investors while funding expansion without excessive dilution. Management's target of reaching 2,000 beds by 2029 implies a 3x capacity expansion, yet seems conservative given the proven execution track record and identified projects.

The margin expansion story remains compelling. Artemis' consolidated EBITDA margin is at 15% reported in FY24. The flagship hospital's EBITDA margin stands at 19%, with clear path to 20%+ as Tower 3 reaches optimal utilization. The drag from new facilities is temporary—Daffodils and Artemis Lite approach breakeven, and established centers demonstrate 25%+ margins at maturity. Operating leverage from the high fixed cost base means incremental revenue flows disproportionately to profitability.

International patients represent an underappreciated growth driver. India's medical tourism market, valued at $9 billion, grows at 20% annually. Artemis's JCI accreditation, advanced technology, and established facilitator network position it to capture increasing share. With international patients generating 2-3x higher revenues per bed, even modest mix improvement significantly impacts profitability. The weak rupee makes Indian healthcare increasingly attractive to dollar-earning patients.

The technology leadership creates sustainable differentiation. Being first with Cyberknife, robotic surgery, and specialized programs attracts both patients and physicians. While equipment can be replicated, the expertise developed over thousands of procedures cannot. Each technology addition reinforces Artemis's position as North India's most advanced medical center, enabling premium pricing and attracting complex cases competitors cannot handle.

Consolidation opportunities could accelerate growth. India's hospital sector remains fragmented, with 70% of beds in standalone facilities. Financial stress from COVID and rising compliance costs force smaller hospitals to seek partners. Artemis's strong balance sheet and operational expertise position it as a consolidator. Acquiring distressed assets at attractive valuations and improving operations could deliver exceptional returns.

The Bear Case: Execution Risks and Structural Challenges

The skeptic's view starts with concerning financial metrics. Company has a low return on equity of 11.7% over last 3 years. Promoters have pledged or encumbered 44.5% of their holding. Low ROE in a capital-intensive business raises questions about capital allocation efficiency. Promoter pledging, while possibly for other ventures, creates overhang risk if margin calls force selling.

The aggressive expansion plans carry significant execution risk. Scaling from 713 to 2,000 beds in five years requires flawless execution across multiple projects. Construction delays, cost overruns, and slower-than-expected ramp-ups could pressure returns. The VIMHANS mental health venture enters an unfamiliar specialty with different economics and operational requirements. Raipur represents geographic expansion into a less affluent market with unproven demand for premium healthcare.

Competition intensifies rather than abates. Max Healthcare's merger with Radiant created a 3,500-bed giant with superior scale economics. Fortis, under IHH Healthcare's ownership, has deep pockets for expansion. Apollo remains the national champion with unmatched brand recognition. International chains like IHH and Ramsay eye India's growth. Artemis faces better-capitalized competitors in its core NCR market while attempting expansion elsewhere.

IFC CCD funding would dilute ~15% EPS. While providing growth capital, the convertible structure means existing shareholders face dilution when conversion occurs. At ₹174 conversion price, IFC gets upside participation while being protected on downside. Additional funding needs for the aggressive expansion could further dilute shareholders or increase debt burden.

Regulatory risks loom large. Government price caps on procedures like knee replacements and cardiac stents squeezed margins industry-wide. Increasing compliance requirements raise operational costs. Clinical establishment acts impose infrastructure mandates that increase capital intensity. Insurance regulators push for standardized treatment protocols that could commoditize healthcare. Any adverse regulatory change could significantly impact profitability.

Talent retention challenges could derail growth. Healthcare depends on star doctors who are increasingly mobile. Aggressive competition for specialized talent drives wage inflation. New facilities require experienced staff, potentially weakening established operations. The planned expansion implies hiring thousands of professionals in a tight talent market. Inability to attract and retain talent could compromise clinical quality and reputation.

Economic sensitivity remains underappreciated. While healthcare seems recession-proof, discretionary procedures—cosmetic surgery, fertility treatments, preventive check-ups—decline during downturns. Corporate healthcare spending faces pressure during economic weakness. International patients defer travel during global uncertainties. Premium positioning makes Artemis vulnerable to consumers trading down during economic stress.

Financial Trajectory & Key Metrics

The financial evolution tells the story of disciplined growth. Revenue grew from ₹450 crores in FY18 to ₹981 crores in FY24, a 14% CAGR that understates the underlying transformation. EBITDA margins expanded from 12% to 15% despite new facility investments. Working capital management improved with receivable days declining from 90 to 45. The balance sheet strengthened with debt-to-equity improving from 1.5x to 0.4x post-IFC investment.

Looking forward, analysts project revenue reaching ₹1,800 crores by FY27, implying 22% CAGR. This assumes Tower 3 completion, VIMHANS operationalization, and Raipur facility launch. EBITDA margins should reach 18-20% as new facilities mature and operating leverage kicks in. ROE should improve to 20%+ as asset utilization improves and expansion investments generate returns.

The investment case ultimately depends on execution. If management delivers on expansion plans while maintaining quality and margins, the stock could double from current levels. However, any stumble—construction delays, quality issues, talent exodus—could trigger significant correction. The risk-reward favors patient investors willing to weather near-term volatility for long-term value creation.

XI. Playbook & Key Lessons

The Artemis journey offers a masterclass in building healthcare businesses in emerging markets, with lessons that transcend industry boundaries. The playbook that emerges from their experience provides insights for entrepreneurs, investors, and established corporations considering healthcare ventures.

Lesson 1: International Accreditation as Competitive Moat It is the first and only hospital to get JCI accreditation in Gurgaon in the year 2013. This wasn't just about a certificate on the wall. JCI accreditation fundamentally transformed Artemis's market position, enabling premium pricing, attracting international patients, and creating a barrier competitors needed years to overcome. The investment in accreditation—not just financial but cultural transformation—paid returns far exceeding any equipment purchase or marketing campaign.

The key insight: in sectors where quality is hard to assess, third-party validation becomes crucial. Patients cannot evaluate clinical competence, but they trust JCI's rigorous standards. This extends beyond healthcare—any complex service business benefits from credible external certification that simplifies customer decision-making.

Lesson 2: Technology as Differentiator, Not Commodity The Cyberknife investment exemplified Artemis's technology philosophy. Rather than buying standard equipment available everywhere, Artemis invested in breakthrough technologies that enabled new treatment paradigms. Artemis has achieved a significant milestone by successfully completing over 1500 CyberKnife radiosurgeries. Being first created temporary monopoly—patients had no alternative for non-invasive brain tumor treatment in North India.

But technology alone wasn't enough. Artemis invested equally in developing expertise to utilize technology effectively. Sending teams for international training, recruiting specialized talent, and building complementary capabilities ensured technology translated into superior outcomes. The lesson: in healthcare and beyond, competitive advantage comes not from owning technology but from the organizational capability to leverage it effectively.

Lesson 3: Portfolio Approach to Growth Rather than expanding only through capital-intensive full hospitals, Artemis developed a portfolio of formats. Artemis Lite addressed the mass market with asset-light models. Daffodils targeted premium maternity through boutique facilities. Management contracts in Mauritius generated fees without capital. Each format served different segments while leveraging the core brand and clinical protocols.

This portfolio approach reduced risk while accelerating growth. Not every format needed to succeed—winners could be scaled while losers were quietly shuttered. The diversity also provided learning opportunities, with innovations in one format cross-pollinating to others. For any business, this suggests the value of controlled experimentation with different models rather than betting everything on a single approach.

Lesson 4: Timing Expansion with Capital Availability Artemis's measured expansion contrasted with competitors' aggressive growth. While others leveraged heavily during the 2010-2015 hospital building boom, Artemis grew organically, funded through internal accruals. This conservative approach meant slower initial growth but positioned Artemis strongly when the cycle turned. Post-COVID, while competitors struggled with debt, Artemis could expand opportunistically.

The IFC investment in 2024 exemplified optimal timing—securing growth capital when valuations were reasonable and expansion opportunities abundant. The convertible structure provided flexibility while minimizing immediate dilution. The lesson: in capital-intensive industries, timing matters more than speed. Expanding when capital is cheap and competition is weakened creates more value than aggressive growth during boom periods.

Lesson 5: Building Trust Through Parent Reputation Artemis Health Sciences, promoted by him, is an enterprise focusing on state-of-the-art medical care. The Apollo Tyres connection, initially seen as incongruous, became an asset. The parent company's reputation for quality and reliability transferred to the hospital venture. Corporate clients trusted Artemis partly because they knew Apollo Tyres' track record. This "reputation spillover" accelerated market acceptance.

However, Artemis was careful to establish independent identity. While leveraging parent credibility, the hospital built its own brand through clinical excellence. This balance—benefiting from parent reputation while establishing standalone credibility—offers lessons for any corporate diversification. The parent brand opens doors, but the new venture must earn its own reputation.

Lesson 6: The Hub-and-Spoke Model in Healthcare Artemis's expansion strategy created a hub-and-spoke network. The Gurgaon flagship served as the hub for complex procedures, while smaller facilities handled routine care. Patients requiring specialized treatment were referred to the hub, while follow-up care happened at convenient spoke locations. This maximized asset utilization while providing patient convenience.

The model's elegance lay in its economics. The hub's expensive equipment and specialists achieved high utilization through referrals from spokes. Spokes operated with lower costs, referring complex cases rather than attempting to handle everything. This network effect strengthened with each additional spoke. The principle applies broadly—centralize complexity and capital intensity while distributing customer touchpoints.

Lesson 7: Talent Development as Strategic Investment While competitors relied primarily on poaching talent, Artemis invested heavily in development. DNB programs, international training, and continuing medical education created a talent pipeline. This wasn't corporate social responsibility but hard-nosed strategy. Developed talent showed higher loyalty, better cultural fit, and lower total cost than hired stars.

The medical education programs created additional benefits. They enhanced academic reputation, generated revenue from training fees, and provided low-cost resident labor. Alumni became referring physicians, extending Artemis's influence beyond employed doctors. The broader lesson: in talent-constrained industries, developing rather than just buying talent creates sustainable advantage.

XII. Epilogue & Future Outlook

As dawn breaks over Gurgaon's skyline in November 2025, the cranes working on Tower 3 of Artemis Hospital symbolize both achievement and ambition. The hospital that began as an industrialist's vision has become a testament to what's possible when operational excellence meets strategic vision in Indian healthcare. Yet the journey feels far from complete.

India's healthcare infrastructure opportunity remains massive. With 1.4 billion people, India has just 0.5 hospital beds per 1,000 population compared to 3-4 in developed nations. The ₹10 trillion healthcare market grows at 15% annually, driven by epidemiological transition, rising incomes, and expanding insurance coverage. Within this ocean of opportunity, Artemis's ₹1,000 crore revenue represents a drop—suggesting enormous growth potential for well-executed expansion.

The consolidation thesis gains momentum quarterly. COVID exposed the fragility of standalone hospitals, accelerating industry consolidation. Artemis's strong balance sheet, operational expertise, and proven integration capabilities position it as a natural consolidator. The company actively evaluates acquisition targets, seeking distressed assets purchasable at attractive valuations. Each successful turnaround would not only add capacity but validate Artemis's operational model.

Yet the question persists: will Artemis be acquirer or acquired? At ₹4,500 crore market capitalization, Artemis remains sub-scale compared to national champions. International healthcare giants like IHH Healthcare, KKR-backed Asia Healthcare Holdings, or even private equity funds might view Artemis as an attractive platform for Indian expansion. The IFC investment provides some protection through board representation, but cannot prevent a generous offer that benefits all shareholders.

Technology disruption looms as both opportunity and threat. Artificial intelligence already assists in diagnosis and treatment planning. Telemedicine enables consultations without hospital visits. Wearable devices monitor patients remotely, potentially reducing hospitalization. Artemis embraces these technologies, but they could fundamentally alter hospital economics. The winners will be those who successfully integrate digital health into traditional delivery models.

The management succession question grows relevant as Onkar Kanwar approaches 84. While professional management runs daily operations, Kanwar's vision and relationships remain crucial. The next generation's commitment to healthcare versus returning focus to the core tyre business remains unclear. Institutional investors like IFC provide governance stability, but family businesses often face transition challenges that transcend governance structures.

Plans to add ~120 beds in the Gurgaon facility, plus 300 beds in Raipur and ~600 in South Delhi, effectively more than doubling the total bed capacity by FY29 to ~1,700 beds. These aren't just numbers but a transformation of scale that could fundamentally alter Artemis's competitive position. Success would establish Artemis among India's top 10 hospital chains. Failure—through execution mishaps, talent challenges, or market changes—could relegate Artemis to regional player status.

The international expansion opportunity beckons tantalizingly. India's reputation for quality healthcare at affordable costs attracts patients globally. Artemis's experience with international patients provides foundation for overseas expansion. Management contracts in Africa and Southeast Asia offer low-risk entry into growing markets. The question isn't whether to expand internationally but how quickly and in what format.

Regulatory evolution remains the wildcard. Universal health coverage, long discussed, could transform healthcare economics overnight. Price controls could squeeze margins on profitable procedures. Quality regulations could increase compliance costs. Conversely, government partnership opportunities in Ayushman Bharat or medical education could provide growth avenues. Artemis's financial strength and operational excellence position it to navigate regulatory changes better than weaker competitors.

The ESG (Environmental, Social, Governance) imperative grows stronger. Healthcare's social impact is obvious, but environmental and governance aspects gain importance. Artemis's solar installations, water recycling, and waste management demonstrate environmental commitment. Board independence, transparent reporting, and stakeholder engagement address governance concerns. Excellence in ESG could become a differentiator for attracting international capital and partnerships.

As we conclude this exploration of Artemis Medicare Services, the overwhelming impression is of a company at an inflection point. The foundation—clinical excellence, operational efficiency, strategic vision—has been laid over two decades. The growth capital, market opportunity, and execution capabilities align for potentially transformative expansion. Whether Artemis emerges as a national healthcare champion or remains a regional leader will be determined in the next five years.

For investors, Artemis represents a compelling but complex opportunity. The structural growth drivers—aging population, disease burden, insurance penetration—provide multi-decade tailwinds. The execution track record suggests management can deliver on ambitious plans. Yet the risks—execution complexity, competition intensity, regulatory uncertainty—demand careful consideration. This is not a simple growth story but a nuanced bet on India's healthcare transformation and one company's ability to capture disproportionate value from it.

For the broader healthcare industry, Artemis offers lessons in building sustainable healthcare businesses in emerging markets. The emphasis on quality over quantity, the patience in building capabilities before scaling, the balance between growth and profitability—these principles transcend specific companies or markets. As healthcare globally grapples with access, affordability, and quality challenges, models like Artemis provide templates for potential solutions.

Looking ahead, the next chapter of the Artemis story remains unwritten. Will Tower 3's completion mark the beginning of national expansion? Will the VIMHANS mental health venture open new specialty opportunities? Will international expansion transform Artemis into a regional healthcare player? These questions await answers that only time and execution will provide.

What remains certain is that Artemis Medicare Services has already achieved something remarkable—building a world-class healthcare institution in a developing market, funded by a tyre company, that competes successfully with the best hospitals globally. That achievement alone, regardless of future trajectory, deserves recognition and study. The journey from rubber to radiosurgery, from tyres to transplants, demonstrates that with vision, execution, and patience, even the most unlikely transformations are possible.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube