Alembic Pharmaceuticals: From Colonial Tinctures to Global Generics

I. Introduction & Episode Roadmap

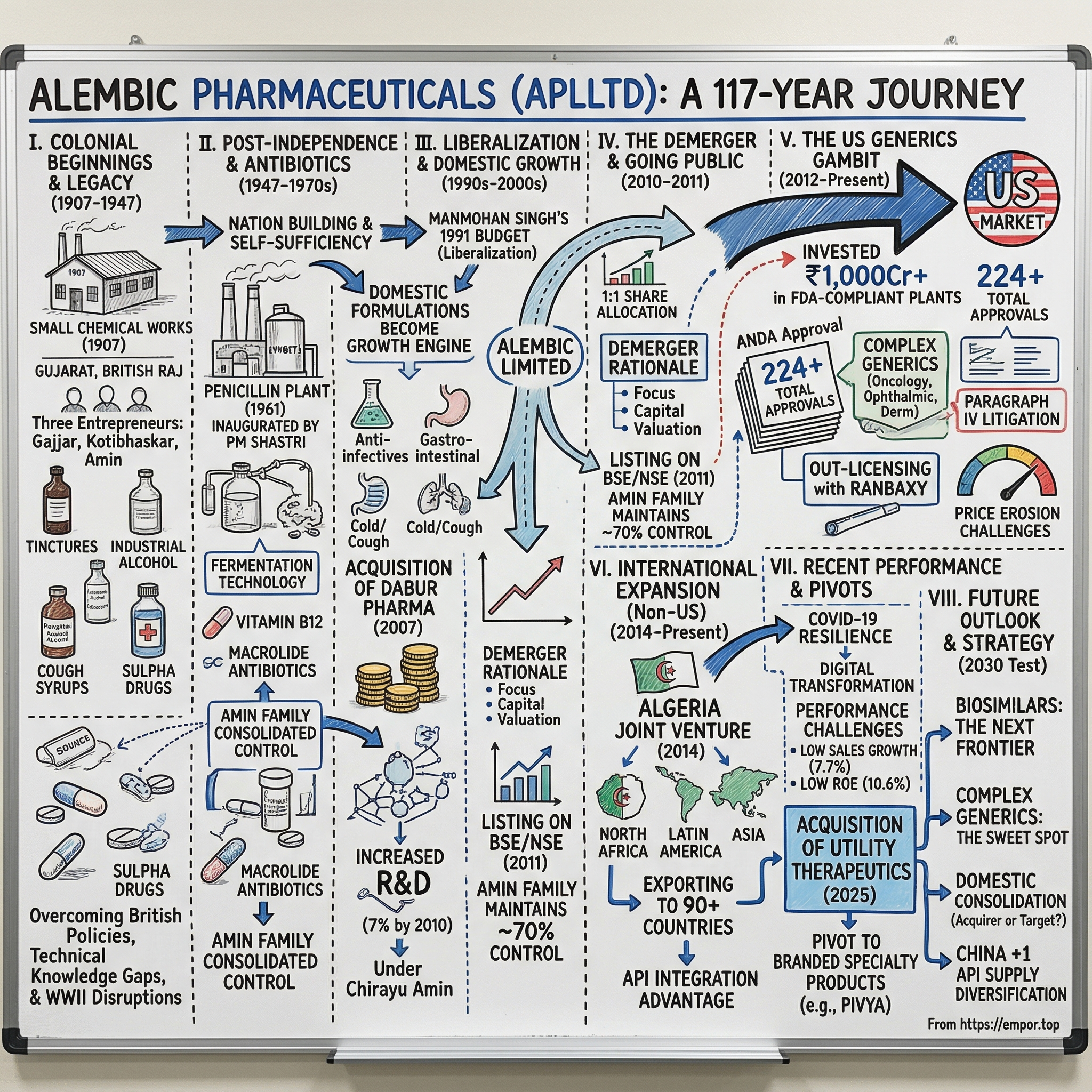

Picture this: A small chemical works in Vadodara, Gujarat, 1907. The British Raj is at its zenith. Three Indian entrepreneurs—T.K. Gajjar, A.S. Kotibhaskar, and B.D. Amin—are mixing tinctures and distilling alcohol in what would become one of India's oldest pharmaceutical companies. Fast forward 117 years, and that same company, Alembic Pharmaceuticals, commands a market capitalization exceeding ₹18,500 crores, with over 200 drug approvals from the US FDA.

The transformation is staggering. From colonial-era tinctures to complex generics competing in the world's most regulated pharmaceutical market. From family workshops to state-of-the-art R&D centers. From serving local Indian markets to exporting to 90+ countries. This is not just a business story—it's a chronicle of Indian industrial evolution itself.

At the heart of this narrative lies a fundamental question: How did a 117-year-old Indian tincture manufacturer crack the code of the US generics market while maintaining family control across four generations? The answer reveals patterns that define not just Alembic, but the entire Indian pharmaceutical miracle.

The story unfolds across distinct eras, each presenting unique challenges and opportunities. We'll witness colonial beginnings when Indian enterprise operated under severe constraints. We'll explore the post-independence antibiotic revolution when Alembic's penicillin plant was inaugurated by Prime Minister Shastri himself. We'll navigate the complexities of liberalization, the strategic demerger from parent Alembic Ltd, and the audacious push into US markets that defines the company today.

For investors, Alembic presents a fascinating paradox. Here's a company with deep technical capabilities, significant US market presence, and strong promoter backing—yet it struggles with single-digit revenue growth and returns on equity hovering around 10%. Understanding this contradiction requires diving deep into the economics of generic pharmaceuticals, the dynamics of family-controlled businesses, and the brutal realities of competing in global markets.

This isn't just Alembic's story. It's the story of Indian pharma's evolution, told through one company's century-long journey from colonial supplier to global competitor.

II. Colonial Beginnings & The Alembic Legacy (1907–1947)

The year 1907 marked a peculiar moment in Indian industrial history. The Swadeshi movement, sparked by the partition of Bengal two years earlier, had ignited nationalist fervor across the subcontinent. Indian entrepreneurs, long relegated to trading and money-lending under British economic policies, were beginning to dream of industrial enterprises. Into this charged atmosphere stepped three men with a vision that would outlast the British Empire itself.

Tribhuvandas Kalyandas Gajjar wasn't a revolutionary in the traditional sense. A pragmatist from Gujarat's merchant community, he understood that political freedom meant little without economic capability. Along with partners A.S. Kotibhaskar and B.D. Amin, Gajjar established Alembic Chemical Works in Vadodara—then Baroda—choosing a name derived from the Arabic "al-anbiq," the distillation apparatus that would become their first tool of transformation.

The initial business model was deceptively simple: manufacture tinctures and industrial alcohol. But in colonial India, even this modest ambition faced extraordinary hurdles. British policies deliberately stunted Indian manufacturing to protect metropolitan industries. Raw materials were expensive, technical knowledge restricted, and markets dominated by British imports. Yet Alembic persisted, gradually expanding from basic tinctures to more complex formulations.

The 1920s brought a crucial pivot. As Western medicine gained acceptance among India's urban middle class, Alembic began producing cough syrups, vitamins, and tonics. These weren't sophisticated drugs by today's standards, but they represented something profound: Indian-made medicines for Indian consumers, breaking the colonial monopoly on modern healthcare products.

By the 1930s, Alembic had ventured into sulpha drugs—the first effective antibiotics before penicillin. This wasn't mere business expansion; it was technological leapfrogging. While most Indian companies remained content with traditional formulations, Alembic was reverse-engineering Western pharmaceutical innovations. The company built capabilities in organic synthesis, quality control, and standardized manufacturing—foundations that would prove invaluable decades later.

The pre-independence era also established Alembic's enduring management philosophy: technical excellence combined with financial conservatism. Unlike some contemporaries who expanded aggressively on borrowed capital, Alembic grew organically, reinvesting profits into capabilities rather than capacity. This patient approach, deeply rooted in Gujarati business culture, would characterize the company through multiple generations.

World War II transformed Alembic's fortunes. With imports disrupted and demand for medicines soaring, the company's revenues multiplied. More importantly, the war forced technological self-reliance. Unable to import equipment or expertise, Alembic's engineers learned to improvise, adapt, and innovate—skills that would define Indian pharma's competitive advantage in later decades.

As independence approached in 1947, Alembic stood among a handful of Indian pharmaceutical manufacturers with genuine technical capabilities. The company had survived colonial constraints, world wars, and economic upheavals. But its greatest challenges—and opportunities—lay ahead in the task of building a self-sufficient nation.

III. Post-Independence Nation Building & The Antibiotic Era (1947–1970s)

August 15, 1947. As Nehru spoke of India's "tryst with destiny," Alembic's leadership understood their own appointment with history. The newly independent nation faced a healthcare crisis of staggering proportions: life expectancy at 32 years, infant mortality exceeding 140 per thousand births, and endemic diseases ravaging the population. For a pharmaceutical company with four decades of experience, this represented both moral imperative and commercial opportunity.

The Nehruvian state's approach to pharmaceuticals reflected broader socialist principles: self-sufficiency over imports, public health over private profit. The government established public sector units like Hindustan Antibiotics and Indian Drugs & Pharmaceuticals, while private companies like Alembic were expected to align with national priorities. This wasn't laissez-faire capitalism—it was directed development, with the state as conductor and private enterprise as orchestra.

Alembic's defining moment came in 1961. Prime Minister Lal Bahadur Shastri arrived in Vadodara to inaugurate the company's penicillin production facility. The symbolism was profound: here was India's leader, champion of the common man, blessing an indigenous capability in life-saving antibiotics. The plant represented a ₹2 crore investment—substantial for that era—but more importantly, it marked Alembic's transformation from formulator to manufacturer of active pharmaceutical ingredients.

The penicillin project revealed Alembic's evolving technical sophistication. Fermentation technology, the biological process for producing antibiotics, requires precise control of temperature, pH, oxygen levels, and sterility. Unlike chemical synthesis where reactions are predictable, fermentation involves living organisms with their own biological variability. Mastering this complexity positioned Alembic among India's pharmaceutical elite.

Simultaneously, the company initiated bulk production of Vitamin B12, another fermentation-based product. This diversification wasn't random—it leveraged the same technological platform while addressing different therapeutic needs. The strategy reflected sophisticated understanding of capability-based competition, decades before management consultants coined the term "core competencies."

During this period, the Amin family consolidated control over Alembic. The founding families had played their part, but as the business grew more complex, professional management became essential. The Amins, combining business acumen with technical understanding, emerged as the dominant shareholders. This wasn't a hostile takeover but a gradual transition, reflecting the realities of capital requirements and management bandwidth in a technology-intensive industry.

The 1960s and early 1970s witnessed Alembic building what would become enduring competitive advantages. The company established India's first indigenous capability in macrolide antibiotics—complex molecules requiring sophisticated chemistry. It developed expertise in sterile manufacturing, essential for injectable drugs. Most crucially, it created a culture of reverse engineering, taking Western innovations and finding cheaper, more efficient production methods.

This period also saw Alembic navigating India's byzantine regulatory environment. The Drug Price Control Order capped profits on essential medicines. Industrial licensing restricted capacity expansion. Foreign exchange regulations limited technology imports. Yet within these constraints, Alembic thrived, learning to optimize within boundaries—a skill that would prove invaluable when competing in regulated markets decades later.

The company's relationship with multinational pharmaceutical companies during this era was complex. Giants like Pfizer, Glaxo, and Hoechst dominated the Indian market, but government policies increasingly favored domestic manufacturers. Alembic learned from these multinationals—studying their products, hiring their trained personnel, occasionally licensing their technologies—while gradually building capabilities to compete against them.

By the mid-1970s, Alembic had established itself as a serious player in Indian pharmaceuticals. Annual revenues exceeded ₹10 crores. The company operated multiple manufacturing facilities, employed hundreds of scientists, and marketed dozens of formulations. More importantly, it had developed deep technological capabilities in fermentation, chemical synthesis, and formulation—the trinity of pharmaceutical manufacturing. The foundation was set for the next phase of growth, though few could have predicted how dramatically India's economic liberalization would transform the competitive landscape.

IV. Liberalization & Domestic Expansion (1990s–2000s)

July 24, 1991. Finance Minister Manmohan Singh rises in Parliament to present a budget that would redefine India's economic trajectory. For Alembic Pharmaceuticals, huddled in their Vadodara boardroom, Singh's words signaled both opportunity and existential threat. The protective walls that had sheltered Indian pharma for four decades were coming down. Global competition was coming.

The immediate impact was jarring. Multinationals, previously constrained by foreign investment regulations, could now expand aggressively. Patent laws were changing, threatening the reverse-engineering model that had sustained Indian companies. Import duties were falling, making foreign drugs more competitive. For a company accustomed to operating within protective barriers, this new world demanded fundamental reimagination.

Alembic's response revealed strategic sophistication. Rather than retreating or selling out—as several Indian pharma companies did—the company chose to double down on its strengths. The domestic formulations business, previously a secondary focus behind bulk drugs, became the growth engine. The logic was compelling: India's middle class was expanding, health awareness increasing, and domestic distribution networks offered defendable competitive advantages against foreign entrants.

The company systematically built therapeutic franchises. Anti-infectives, leveraging decades of antibiotic expertise. Gastrointestinal drugs, addressing India's endemic digestive disorders. Cold and cough preparations, building on historical strengths in respiratory formulations. This wasn't random portfolio expansion—each category built on existing capabilities while addressing large, growing markets.

The 2000s brought increasing professionalization under Chirayu Amin's leadership. Educated at the University of Michigan and Stanford, Chirayu represented a new generation of Indian pharmaceutical leadership—globally educated yet deeply rooted in Indian business realities. His ascension marked a crucial transition: from patriarch-led management to professional systems and processes.

Under Chirayu's watch, Alembic invested heavily in regulatory compliance and quality systems. The company understood that competing globally required meeting international standards. Manufacturing facilities were upgraded to WHO-GMP standards. Quality assurance moved from end-product testing to comprehensive process control. Documentation systems were digitized and standardized. These investments wouldn't yield immediate returns, but they were essential infrastructure for international expansion.

The 2007 acquisition of Dabur Pharma's non-oncology formulation business for ₹159 crores marked a watershed moment. This wasn't just Alembic's largest acquisition—it was one of the biggest domestic pharmaceutical deals of that year. The transaction brought 17 brands, expanding Alembic's domestic portfolio and market presence. More subtly, it signaled Alembic's evolution from organic growth to strategic consolidation.

The acquisition revealed sophisticated deal-making. Dabur Pharma, struggling with debt and strategic focus, needed to divest non-core assets. Alembic, cash-rich but seeking market share, found strategic fit. The integration was smooth—products were transferred, sales forces merged, and synergies realized within eighteen months. This execution capability would become crucial as Indian pharma entered a consolidation phase.

During this period, Alembic also established leadership in the macrolides segment of anti-infectives. Drugs like azithromycin and clarithromycin became flagship products, combining therapeutic efficacy with manufacturing complexity that deterred competition. The company's market share in macrolides exceeded 15%—remarkable in India's fragmented pharmaceutical market where hundreds of companies competed.

Investment in R&D infrastructure accelerated through the 2000s. The company established dedicated research facilities, hired doctorate-level scientists, and initiated systematic drug development programs. R&D spending increased from 2% of revenues in 2000 to over 7% by 2010—approaching international pharmaceutical industry standards. This wasn't just about creating new drugs; it was about building organizational capabilities for innovation.

The period also witnessed subtle but significant changes in corporate governance. Independent directors were inducted onto the board. Financial reporting became more transparent. Investor communications improved. While the Amin family maintained control, they recognized that accessing capital markets would require institutional-grade governance. These changes positioned Alembic for its next strategic leap: going public and expanding internationally.

By 2010, Alembic had successfully navigated India's economic liberalization. Revenues exceeded ₹1,000 crores. The company operated five manufacturing facilities, employed over 5,000 people, and marketed over 200 formulations. More importantly, it had evolved from a protected domestic player to a competitive enterprise ready for global markets. The stage was set for the most ambitious phase of its century-long journey.

V. The Demerger & Going Public (2010–2011)

The boardroom at Alembic Limited's Vadodara headquarters buzzed with tension on a humid September morning in 2010. The decision before the directors would fundamentally reshape a century-old conglomerate. After months of deliberation, investment banker presentations, and family councils, the moment had arrived: Alembic Pharmaceuticals would be carved out from its parent company, becoming an independent entity for the first time in its modern history.

The demerger architecture was elegantly complex. Alembic Limited would transfer its pharmaceutical undertaking to the newly incorporated Alembic Pharmaceuticals Limited. In exchange, pharmaceutical company shares would be allocated to Alembic Limited's shareholders in a 1:1 ratio. The transaction involved issuing 133,515,914 equity shares, with Alembic Limited's shareholding dropping from 100% to 29.18%. The Amin family, through various holding vehicles, would maintain 69.7% control—enough to drive strategy while creating liquidity for external investors.

Why demerge? The rationale went beyond financial engineering. Pharmaceutical businesses operate on fundamentally different economics than chemicals or real estate. Drug development requires patient capital, with investments taking 5-10 years to generate returns. Regulatory compliance demands specialized governance. Valuation multiples differ dramatically across sectors. Housing these disparate businesses under one roof had become increasingly untenable.

The timing was deliberate. India's capital markets were recovering from the 2008 financial crisis. Pharmaceutical stocks commanded premium valuations, driven by excitement about generic opportunities in developed markets. Investment bankers projected that a standalone pharmaceutical company could achieve valuations 40-50% higher than as a division of a conglomerate. For the Amin family, this meant crystallizing value while maintaining control.

The demerger process revealed meticulous planning. Assets were carefully segregated—manufacturing facilities, product portfolios, intellectual property, and human resources. Liabilities were allocated based on business attribution. Tax implications were structured to minimize burden on both entities. The entire transaction was executed as a court-approved scheme of arrangement, ensuring legal sanctity and shareholder protection.

March 2011 brought the next milestone: listing on the Bombay Stock Exchange and National Stock Exchange. The listing wasn't accompanied by a public issue—shares were simply admitted for trading. This approach avoided dilution while providing liquidity. On the first day of trading, Alembic Pharmaceuticals opened at ₹62 per share, valuing the company at approximately ₹1,500 crores.

The market's initial reception was lukewarm. Investors struggled to understand Alembic's positioning—was it a domestic formulations company, a bulk drug manufacturer, or an emerging global generics player? The company's financial performance was solid but unspectacular: ₹850 crores in revenues, ₹78 crores in profits. Without a clear growth narrative, the stock languished in the first few months post-listing.

Behind the scenes, however, listing had triggered fundamental changes. Quarterly earnings calls forced management to articulate strategy more clearly. Institutional investors demanded improved disclosure and governance. Analyst coverage brought scrutiny but also visibility. The discipline of public markets began shaping corporate behavior in subtle but significant ways.

The demerger also catalyzed strategic clarity. Free from conglomerate constraints, Alembic Pharmaceuticals could pursue focused expansion. Capital allocation became more transparent—every rupee invested needed justification based on pharmaceutical returns, not conglomerate considerations. Management incentives were aligned with pharmaceutical performance. The organizational energy previously dissipated across diverse businesses concentrated on a singular mission.

For Chirayu Amin, now firmly established as Managing Director, the listing represented both culmination and commencement. The culmination of a decade-long transformation from family business to professional enterprise. The commencement of an ambitious international expansion that would test every capability Alembic had built over a century.

The governance structure post-listing balanced family control with institutional oversight. The board included independent directors with pharmaceutical expertise. Audit committees ensured financial propriety. Stakeholder relationship committees managed investor concerns. While the Amin family retained decisive control through 69.7% shareholding, they operated within institutional frameworks that enhanced rather than constrained decision-making.

The financial flexibility afforded by listing proved crucial for what followed. Access to capital markets meant Alembic could fund R&D without depleting cash reserves. The ability to issue shares provided currency for acquisitions. Credit ratings improved, reducing borrowing costs. These advantages would prove essential as Alembic embarked on its most ambitious project yet: cracking the US generics market, where success required deep pockets, regulatory expertise, and tremendous patience.

VI. The US Generics Gambit (2012–Present)

The fluorescent lights of the FDA inspection room in Rockville, Maryland, cast harsh shadows as Alembic's regulatory team presented their first ANDA dossier in early 2012. Across the table sat FDA reviewers who had rejected hundreds of applications from companies worldwide. The stakes couldn't be higher: success meant entry into the world's largest pharmaceutical market; failure meant millions in wasted investment. This was Alembic's moment of truth in a decades-long preparation for US market entry.

The decision to target America wasn't obvious. The US generics market was brutally competitive, with price erosion averaging 30-40% annually. Regulatory requirements were stringent, with FDA inspections that could shut down facilities overnight. Legal battles with innovator companies could drain millions in litigation costs. Yet Chirayu Amin and his team saw opportunity where others saw obstacles: a $100 billion market growing at 8% annually, where Indian companies' cost advantages and reverse-engineering capabilities could create sustainable competitive positions.

Alembic's US strategy began with infrastructure. Between 2010 and 2015, the company invested over ₹1,000 crores in building FDA-compliant manufacturing facilities. The new plants in Panelav and Karakhadi weren't just production centers—they were statements of intent, designed from ground up to meet Current Good Manufacturing Practice (cGMP) standards. Every pipe, every air handling unit, every documentation system was configured for FDA scrutiny.

The R&D transformation was even more dramatic. Alembic established two dedicated research centers focused exclusively on the US market. Scientists were recruited from American pharmaceutical companies, bringing not just technical expertise but cultural understanding of FDA expectations. The company invested in bioequivalence facilities, analytical laboratories, and pilot plants—infrastructure costing hundreds of crores but essential for competing in regulated markets.

By 2024, the numbers told a remarkable story: 224 cumulative ANDA approvals from the FDA, including 201 final approvals and 23 tentative approvals. Each approval represented 2-3 years of development, $1-2 million in investment, and countless hours navigating regulatory complexities. But raw numbers don't capture the strategic sophistication behind Alembic's portfolio construction.

The company deliberately targeted complex generics—products requiring specialized manufacturing capabilities or presenting regulatory barriers that deterred competition. Oncology injectables, requiring sterile manufacturing and handling of cytotoxic substances. Ophthalmic solutions, demanding specialized sterilization and packaging. Dermatological preparations, involving complex formulation chemistry. These weren't commodity generics where price was the only differentiator; they were specialized products where technical capability created competitive moats.

The 2012 Paragraph IV ANDA litigation with Pfizer over desvenlafaxine revealed Alembic's appetite for calculated risks. Paragraph IV certifications challenge innovator patents, potentially allowing generic entry before patent expiry. Success means market exclusivity and extraordinary profits; failure means litigation costs and delayed entry. Alembic's willingness to engage Pfizer—one of the world's largest pharmaceutical companies—in patent litigation signaled serious ambitions in the US market.

The 2013 out-licensing agreement with Ranbaxy (later acquired by Sun Pharma) provided crucial market access. Ranbaxy's established US distribution network and customer relationships complemented Alembic's manufacturing capabilities. The partnership structure was innovative: Alembic developed and manufactured products while Ranbaxy handled commercialization, sharing profits based on pre-agreed formulas. This asset-light approach allowed Alembic to enter the US market without massive front-end investments. The regulatory journey wasn't without turbulence. FDA inspections resulted in Form 483 observations at various facilities, including procedural observations at the Panelav plant following inspections in 2018. These weren't warning letters—which would have been far more serious—but they signaled areas requiring improvement. Each observation triggered corrective actions, system upgrades, and process improvements. The ability to respond effectively to FDA observations became a core competency, distinguishing Alembic from Indian peers who stumbled at regulatory hurdles.

Price erosion in the US generics market proved more severe than anticipated. Products that launched with 70% gross margins saw prices collapse within 18-24 months as competitors entered. The consolidation of US pharmacy chains—with three buyers controlling 90% of the market—gave purchasers extraordinary negotiating leverage. Alembic learned that success in US generics required not just regulatory approvals but portfolio management, launch timing, and customer relationship sophistication.

The company's response was strategic portfolio construction. Rather than chasing every opportunity, Alembic focused on products with limited competition. First-to-file opportunities, where being first to challenge a patent meant 180-day market exclusivity. Complex formulations requiring specialized manufacturing. Niche therapeutic areas with smaller markets but sustainable pricing. This selective approach meant fewer launches but better economics per product.

Manufacturing excellence became a differentiator. While many Indian companies struggled with FDA compliance, Alembic maintained consistent quality metrics. The company's facilities passed regular FDA inspections without major observations. This reliability made Alembic an attractive partner for US distributors seeking stable supply sources. In an industry where a single quality failure could trigger multi-million dollar recalls, consistency was valuable currency.

The financial commitment to the US market was staggering. By 2024, cumulative R&D spending exceeded ₹3,000 crores, much of it directed toward US product development. Manufacturing investments totaled another ₹2,000 crores. Legal and regulatory costs added hundreds of crores more. For a company with annual revenues of ₹6,800 crores, these investments represented massive capital allocation decisions that would define Alembic's future.

Yet the results justified the gambit. US revenues grew from negligible in 2012 to over ₹2,000 crores by 2024, representing nearly 30% of total sales. More importantly, Alembic had established itself among the select group of Indian pharmaceutical companies with meaningful US presence. In a market where 90% of generic prescriptions were filled, but Indian companies captured only 40% share, Alembic had secured its foothold in the world's most lucrative pharmaceutical market.

VII. International Expansion Beyond US (2014–Present)

The conference room in Algiers hummed with nervous energy in November 2014. Across the table from Alembic's international business team sat executives from Adwiya Mami SARL, one of Algeria's established pharmaceutical distributors. The joint venture agreement they were negotiating would mark Alembic's first significant commitment to markets beyond the United States—a strategic pivot born from both opportunity and necessity. The structure revealed strategic thinking: through its wholly owned subsidiary Alembic Global Holdings, the company formed a joint venture with Adwiya Mami SARL Algeria, taking 49% equity stake. The partnership provided Alembic access to the Algerian market valued at approximately $3 billion, while leveraging local partner expertise in navigating North African regulatory and business environments.

Adwiya Mami brought critical assets to the partnership: a formulation plant with capacity of 1.2 billion oral solids per annum, designed and developed by a leading European pharmaceutical company in line with cGMP requirements. This meant Alembic could begin manufacturing immediately rather than investing years building greenfield facilities. The plant also had "enough headroom for future expansion," providing scalability as the business grew.

Algeria represented more than just another export market. The country's pharmaceutical market, estimated at $3 billion with 70% generics and 30% innovator drugs, offered attractive fundamentals: large population, improving healthcare infrastructure, government focus on reducing import dependence, and limited local manufacturing capabilities. For Alembic, accustomed to competing in hyper-competitive markets, Algeria's relatively concentrated competitive landscape offered better margins and growth potential.

The appointment of leadership revealed sophisticated cross-cultural management. Taghreed AlShunnar, a Jordanian national with over 20 years of pharmaceutical experience, was appointed as the joint venture's first CEO as Alembic's nominee. This choice—an Arab woman leading operations in a Muslim-majority country—demonstrated cultural sensitivity while ensuring professional competence.

The Algeria venture catalyzed broader international thinking. If Alembic could succeed in North Africa, why not other emerging markets? The company systematically evaluated opportunities across Asia, Africa, and Latin America, seeking markets with similar characteristics: growing middle classes, improving healthcare access, regulatory environments favoring local manufacturing, and limited competition from multinational giants.

By 2024, Alembic's international footprint had expanded dramatically. The company now exports to over 90 countries, with formulations reaching markets as diverse as Australia, South Africa, and the Middle East. Each market required unique adaptations—regulatory dossiers tailored to local requirements, packaging in multiple languages, formulations adjusted for climate conditions. This complexity demanded sophisticated supply chain management and regulatory expertise that few Indian companies possessed.

The ex-US international strategy deliberately differed from the American approach. While the US market demanded massive upfront investments with uncertain returns, emerging markets offered quicker paybacks with lower regulatory barriers. Products that were commoditized in the US could command premium pricing in Africa or Asia. Manufacturing standards that were table stakes in regulated markets became competitive advantages in semi-regulated territories.

Strategic partnerships accelerated market access. In 2015, Alembic signed an exclusive agreement with Novartis for the Swiss market, leveraging the pharmaceutical giant's distribution network while providing cost-effective manufacturing. Similar arrangements followed with regional distributors across multiple geographies, creating an asset-light expansion model that minimized capital requirements while maximizing market reach.

The API integration that had been Alembic's historical strength proved particularly valuable in international markets. Many countries imposed local content requirements or offered preferences for integrated manufacturers. Alembic's ability to produce both active ingredients and finished formulations provided flexibility in structuring deals, managing transfer pricing, and optimizing tax structures across jurisdictions.

Yet international expansion brought unexpected challenges. A fire at the Algerian joint venture plant in 2017 disrupted production, highlighting operational risks in emerging markets. Currency volatility in markets like Turkey and South Africa eroded profitability. Regulatory changes in countries like Saudi Arabia required constant adaptation. Payment delays from government tenders in African markets stressed working capital.

The company's response was portfolio diversification—both geographic and therapeutic. No single market outside India and the US would represent more than 5% of revenues. Product portfolios were tailored to local disease profiles and purchasing power. Manufacturing was distributed across multiple facilities to ensure supply continuity. This risk mitigation approach meant sacrificing some economies of scale but ensured sustainable growth.

By 2024, international markets (excluding the US) contributed approximately 25% of Alembic's revenues. While less dramatic than the US expansion, this diversification provided stability and growth optionality. More importantly, it positioned Alembic among a select group of Indian pharmaceutical companies with truly global operations—no longer just an exporter but a multinational enterprise with deep roots in multiple markets.

VIII. Recent Performance & Strategic Pivots (2020–2025)

The Excel spreadsheet glowing on CFO R.K. Baheti's laptop screen in March 2020 told a story of careful preparation meeting unprecedented crisis. As India entered its first COVID-19 lockdown, Alembic's inventory levels, cash reserves, and supply chain redundancies—built over years of conservative management—would be tested like never before. The pandemic that would devastate many businesses would paradoxically accelerate some of Alembic's most important strategic transformations.

The initial pandemic response revealed organizational resilience. Within 48 hours of lockdown announcement, Alembic had activated business continuity protocols. Manufacturing facilities were reorganized into isolated zones. Worker accommodations were arranged on-site. Raw material inventories, traditionally maintained at 3-4 months, proved prescient as global supply chains seized. While competitors scrambled for APIs from China, Alembic's integrated manufacturing continued uninterrupted.

COVID's impact on pharmaceutical demand was complex and contradictory. Acute therapy sales collapsed as patients avoided hospitals. Chronic disease medications saw panic buying followed by inventory destocking. Export markets faced logistical nightmares with container shortages and port closures. Yet certain categories—antibiotics, vitamins, immunity boosters—witnessed unprecedented demand. Alembic's diversified portfolio meant exposure to both headwinds and tailwinds, ultimately resulting in relatively stable performance through the crisis.

The pandemic accelerated digital transformation initiatives that had been percolating for years. Sales force automation, previously resisted by field teams, became essential when physical detailing stopped. E-commerce partnerships, especially for over-the-counter products, expanded rapidly. Supply chain digitization enabled real-time tracking of inventory and shipments across global operations. These weren't temporary adjustments but permanent capability upgrades that improved operational efficiency.

As markets normalized through 2021-2022, Alembic's fundamental challenges became starkly apparent. The company delivered poor sales growth of just 7.69% over five years, significantly trailing industry peers who were growing at 12-15% annually. Return on equity averaged a disappointing 10.6% over three years, well below the 15-20% that investors expected from pharmaceutical companies. The numbers demanded honest introspection about strategic choices and execution capabilities.

The US market, despite significant investments, wasn't delivering expected returns. Price erosion had accelerated beyond projections, with some products seeing 50-60% price declines within months of launch. The consolidation of US buyers—with three pharmacy chains controlling distribution—had shifted negotiating power decisively against generic manufacturers. Competition from Indian peers had intensified, with 40+ Indian companies now competing for the same opportunities. The math was sobering: Alembic had invested over ₹5,000 crores in US operations but was generating returns below cost of capital.

Domestic performance was equally concerning. Despite strong brand equity and distribution reach, Alembic was losing market share to aggressive competitors. New-age companies like Mankind and Glenmark were growing faster through innovative marketing and portfolio expansion. Multinational companies were defending positions through strategic price cuts. The domestic formulations business, traditionally Alembic's cash cow, was under pressure from all sides. The strategic response crystallized in July 2025 with the acquisition of Utility Therapeutics for $12 million through Alembic's US subsidiary. This wasn't just another asset purchase—it marked Alembic's pivot from pure generics to branded specialty products. Utility's lead product, PIVYA (pivmecillinam), had become the first antibiotic in approximately 20 years to earn FDA approval for uncomplicated urinary tract infections, targeting a market affecting millions of American women annually.

The acquisition structure revealed financial discipline: $12 million paid in staggered manner over time, depending on milestones achieved. This wasn't a desperate overpayment but a calculated bet on specialty pharmaceuticals offering better economics than commodity generics. "This acquisition gives us a strategic entry into the specialty and branded prescription products," explained Pranav Amin, Managing Director.

The move into branded specialty products represented fundamental strategic evolution. Unlike generics where price was the primary differentiator, branded products commanded premium pricing through patent protection and clinical differentiation. Alembic planned to make PIVYA available in the US in the fourth quarter of 2025, leveraging its existing commercial infrastructure while entering higher-margin market segments.

Domestic market initiatives focused on portfolio optimization rather than expansion. Underperforming brands were discontinued. Sales force productivity improved through better targeting and incentive alignment. Digital marketing initiatives, accelerated during COVID, continued expanding reach while reducing costs. Yet these incremental improvements couldn't mask fundamental challenges in India's hyper-competitive pharmaceutical market.

R&D spending remained elevated at 7-8% of revenues, but allocation shifted toward complex generics and specialty products rather than commodity ANDAs. The company recognized that competing on volume in simple generics was a losing proposition against Chinese and Indian competitors with lower cost structures. Future growth would come from products where technical complexity, regulatory expertise, or specialized manufacturing created barriers to entry.

Manufacturing excellence continued as a differentiator, but focus shifted from capacity expansion to efficiency improvement. Automation reduced labor costs. Process optimization improved yields. Quality systems prevented expensive recalls and regulatory actions. These operational improvements couldn't overcome market headwinds but prevented further margin erosion.

The financial metrics by 2024 painted a picture of a company in transition. Market capitalization at ₹18,516 crores reflected investor skepticism about growth prospects. Revenue of ₹6,821 crores and profit of ₹601 crores demonstrated solid but unspectacular performance. The stock trading at 3.57 times book value suggested market doubt about future returns on invested capital.

Yet beneath surface struggles, strategic pieces were falling into place. The US business, while facing pricing pressure, had achieved critical mass with 200+ approved products. International expansion provided geographic diversification. The move into specialty products offered paths to better economics. API integration remained a competitive advantage as supply chain resilience gained importance post-pandemic.

Management communication became increasingly candid about challenges and opportunities. Rather than promising unrealistic growth, leadership focused on sustainable profitability and strategic positioning. This honesty, while sometimes disappointing markets seeking growth stories, built credibility with long-term investors who valued execution over promises.

The company's response to recent challenges revealed both strengths and limitations. Strong technical capabilities and regulatory expertise remained valuable assets. Family control provided stability and long-term thinking. Conservative financial management ensured survival through cycles. Yet these same strengths—technical focus, family control, financial conservatism—potentially limited aggressive expansion and risk-taking necessary for breakthrough growth. The question facing Alembic as it entered its 118th year wasn't survival—that was assured—but whether it could transform from a competent player to a category leader.

IX. Playbook: Business & Investing Lessons

The conference room at Mumbai's Trident hotel buzzes with anticipation as institutional investors gather for Alembic's annual analyst meet. But this isn't just another corporate presentation—it's a masterclass in navigating the complexities of global pharmaceutical competition. Each strategic decision, each capital allocation choice, each market entry reveals patterns that transcend Alembic's specific story, offering broader lessons about building and investing in pharmaceutical businesses.

Family Control: Feature or Bug?

The Amin family's 69.7% stake in Alembic represents one of Indian pharma's enduring debates. Critics point to limited stock liquidity, potential for suboptimal capital allocation, and resistance to transformative M&A. Yet the evidence suggests nuance. Family control enabled Alembic to make decade-long bets on US market entry when quarterly earnings pressure might have forced retreat. The 2007 Dabur acquisition, executed swiftly without lengthy board debates, demonstrated decision-making advantages. Patient capital allowed R&D investments that wouldn't pay off for years.

But family control also imposed constraints. Professional managers from outside the family rarely reached top positions, potentially limiting fresh thinking. Strategic pivots happened slowly, with the company taking years to acknowledge US market challenges. Capital allocation sometimes reflected family preferences for stability over shareholder value maximization. The lesson: family control works when aligned with long-term value creation but becomes problematic when preserving control supersedes business logic.

The ANDA Game: A Casino Where the House Usually Wins

Alembic's 224 ANDA approvals represent enormous investment—roughly $250-450 million at typical development costs. Yet the economics of generic drugs in America have deteriorated dramatically. First-to-file opportunities that once guaranteed six months of duopoly pricing now face authorized generics from innovators. Portfolio products that maintained stable pricing for years now see 20-30% annual erosion. The consolidation of buyers—three pharmacy chains controlling 90% of the market—shifted power decisively against manufacturers.

The successful players in this game share characteristics: scale to spread fixed costs, portfolio breadth to manage customer relationships, manufacturing excellence to compete on cost, and regulatory expertise to avoid catastrophic failures. Alembic possesses some but not all these attributes. The company's sub-scale presence relative to Teva or Mylan limits negotiating leverage. Its portfolio depth in certain categories like ophthalmics provides some pricing power, but overall portfolio breadth remains insufficient for true bargaining strength.

Vertical Integration: When Chemistry Beats Economics

Alembic's API capabilities, dating back to 1960s penicillin production, seem anachronistic in an era of global supply chains. Why manufacture raw materials when Chinese producers offer 30-40% cost advantages? The answer emerged during COVID when supply chain disruptions crippled competitors while Alembic's integrated operations continued uninterrupted. Regulatory scrutiny of Chinese APIs following quality scandals created opportunities for reliable suppliers. Customer preferences shifted toward supply chain transparency and reliability over pure cost minimization.

Yet vertical integration isn't universally advantageous. Capital tied up in API manufacturing might generate higher returns in finished dosage development. Chinese competition continues pressuring API margins. Environmental regulations make Indian manufacturing increasingly expensive. The lesson: vertical integration works when it provides strategic control over critical inputs, quality differentiation, or regulatory advantages—not when pursued for its own sake.

Timing Market Entry: The Expensive Education

Alembic's US entry timing reveals both foresight and misfortune. Entering in 2012 meant avoiding the late-2000s quality scandals that destroyed Indian pharma's reputation. Building FDA-compliant facilities from scratch proved easier than retrofitting existing plants. Early ANDA approvals faced less competition than today's crowded pipeline.

Yet timing also worked against Alembic. The company entered just as pricing power shifted decisively to buyers. Competition from other Indian companies intensified precisely when Alembic needed to establish market position. Biosimilar opportunities emerged before Alembic had capabilities to pursue them. The lesson: market entry timing matters less than execution quality and competitive positioning. Better to enter late with differentiated capabilities than early with commodity offerings.

Capital Allocation in R&D: The Innovation Paradox

Alembic's 7-8% R&D spending approaches innovator pharma levels yet generates generic products with limited pricing power. This paradox—high innovation spending for commoditized outputs—defines generic pharmaceutical economics. Every competitor conducts similar development, creating redundant industry-wide R&D that destroys value. Yet not investing means portfolio obsolescence and market irrelevance.

Successful R&D allocation requires portfolio theory thinking. Concentrate resources on complex products where success probability is lower but returns are higher. Balance near-term launches with long-term pipeline development. Maintain optionality through platform technologies applicable across multiple products. Alembic's recent shift toward specialty products and complex generics reflects this evolution, though execution remains uncertain.

Regulatory Risk: The Sword of Damocles

FDA compliance isn't just operational necessity—it's existential requirement. A single warning letter can destroy billions in market value. Import alerts can shut down facilities for years. Data integrity violations can trigger criminal prosecution. Alembic has largely avoided catastrophic regulatory failures, but the risk remains ever-present.

Managing regulatory risk requires cultural transformation beyond mere compliance. Quality must be embedded in organizational DNA, not imposed through SOPs. Transparency with regulators builds trust that proves invaluable during inspections. Investment in quality systems and training may not generate returns but prevents catastrophic losses. The companies that survive long-term are those that treat regulatory compliance as strategic capability, not cost center.

Scale Economics: The Uncomfortable Truth

Alembic's ₹6,800 crore revenue places it in Indian pharma's middle tier—too large to be nimble, too small for global scale advantages. In commoditized generics, scale drives economics through procurement leverage, fixed cost absorption, and customer negotiations. Alembic lacks the scale of Sun Pharma or Cipla domestically, or Teva and Sandoz globally.

The response options are limited: pursue transformative M&A to achieve scale, accept niche player status with focus on specialized segments, or gradually build scale through organic growth. Alembic has chosen the third path, perhaps reflecting family control's preference for stability. Whether patience will be rewarded or markets will demand bolder action remains uncertain. The lesson for investors: in commodity businesses, scale isn't everything—it's the only thing.

X. Analysis & Bear vs. Bull Case

The spreadsheet models diverge dramatically. One shows Alembic doubling earnings within five years through US specialty products and emerging market expansion. Another projects margin compression and market share losses as competition intensifies. Both models use reasonable assumptions. Both could be right. This isn't analytical failure but reflection of genuine uncertainty facing Alembic at this strategic inflection point.

The Bull Case: Hidden Value in Plain Sight

Bulls see Alembic as a classic value play trading below intrinsic worth. Start with the fundamentals: a research-driven company with proven generic formulations platform, generating ₹600+ crores in annual profit. The company's 200+ ANDA approvals represent $250-450 million in sunk development costs—replacement value far exceeding market capitalization. API backward integration provides supply chain security increasingly valued post-COVID. Manufacturing facilities meeting FDA standards represent scarce assets as regulatory scrutiny intensifies.

The US business transformation holds particular promise. Moving from pure generics to specialty products like PIVYA could dramatically improve economics. Branded products command 50-70% gross margins versus 30-40% for generics. The $12 million Utility Therapeutics acquisition price looks modest relative to potential returns if PIVYA achieves even modest market penetration. With urinary tract infections affecting millions of American women annually, the addressable market is substantial.

Geographic diversification provides multiple growth vectors. The Algerian joint venture offers entry into North Africa's rapidly growing pharmaceutical market. Presence in 90+ countries reduces dependence on any single geography. Emerging markets offer better pricing dynamics than developed markets' commoditized generics. As these economies grow and healthcare spending increases, Alembic's early positioning could yield substantial returns.

The promoter holding at 69.7% ensures alignment between management and shareholders. The Amin family's century-long commitment to the business suggests patient capital willing to invest through cycles. No corporate governance scandals or related-party transactions concern. Management has demonstrated willingness to make bold moves like the 2011 demerger when strategically necessary.

Valuation metrics suggest opportunity. Trading at 3.57 times book value for a profitable company with global operations seems undemanding. Price-to-earnings ratios below industry averages despite superior regulatory track record. If margins improve even modestly through mix shift toward specialty products, earnings could surprise significantly upward.

The Bear Case: Structural Challenges Without Easy Solutions

Bears paint a darker picture of structural headwinds overwhelming any strategic initiatives. The 7.69% five-year revenue CAGR tells the story—a company struggling to grow despite massive R&D investments and geographic expansion. When inflation-adjusted, real growth turns negative. This isn't temporary weakness but reflection of fundamental competitive disadvantages.

The US generics market has become a value trap. Pricing erosion accelerates as more Indian and Chinese competitors enter. Buyer consolidation means manufacturers have zero negotiating leverage. Even successful products see margins evaporate within 18-24 months of launch. The 200+ ANDA approvals represent sunk costs unlikely to generate acceptable returns. Moving to specialty products sounds attractive but requires capabilities Alembic hasn't demonstrated—brand building, physician detailing, payer negotiations.

Domestic market challenges are equally daunting. Despite decades of presence, Alembic remains subscale relative to leaders like Sun Pharma or Cipla. New-age companies like Mankind leverage innovative marketing to capture share. MNCs defend positions through strategic pricing. Government price controls limit upside while input cost inflation pressures margins. The domestic business—traditionally Alembic's cash cow—faces structural profitability challenges.

Return on equity averaging 10.6% over three years signals capital allocation problems. With cost of equity around 12-14% for Indian pharma, Alembic destroys value with every rupee invested. High R&D spending without commensurate returns suggests poor project selection or execution. Manufacturing investments in commoditized products unlikely to generate acceptable returns. The company needs not more investment but better investment.

International expansion beyond the US offers limited salvation. Emerging markets are attractive in theory but challenging in practice. Regulatory requirements vary dramatically across countries, increasing complexity costs. Currency volatility erodes returns when converted to rupees. Payment delays from government tenders stress working capital. Competition from Chinese companies with state support makes pricing difficult. The Algeria venture, while promising, remains subscale to move overall numbers.

Management's strategic pivots come slowly, perhaps reflecting family control's inherent conservatism. Years passed before acknowledging US market challenges. Domestic portfolio rationalization should have happened earlier. The move to specialty products, while directionally correct, may be too little too late. In rapidly evolving pharmaceutical markets, speed matters—and Alembic lacks urgency.

The Verdict: A Company at Crossroads

Neither bulls nor bears are entirely wrong. Alembic possesses genuine strengths—technical capabilities, regulatory expertise, global presence—that could drive value creation under the right circumstances. Yet structural challenges in both domestic and international markets limit near-term growth potential. The company's future likely lies somewhere between dramatic success and catastrophic failure—a steady but unspectacular business generating acceptable but not exceptional returns.

For investors, Alembic represents a complex bet on multiple variables: success of specialty product initiatives, emerging market growth trajectories, competitive dynamics in global generics, and management's ability to execute strategic transformation. The risk-reward depends entirely on entry price and investment horizon. At current valuations, the market seems to be pricing in continued challenges with limited credit for transformation potential—creating opportunity for contrarians willing to bet on long-term execution.

XI. Epilogue & Future Outlook

Imagine Alembic Pharmaceuticals in 2030. The optimistic scenario envisions a transformed company: specialty products contributing 40% of US revenues with superior margins, biosimilars providing new growth avenues, emerging markets delivering consistent mid-teens growth, and domestic operations regaining market share through focused therapeutic leadership. Market capitalization exceeds ₹50,000 crores as investors recognize successful transformation.

The pessimistic scenario paints continued struggle: US generics margins compressed to single digits, specialty product initiatives failing to achieve scale, emerging markets proving more challenging than anticipated, and domestic business losing share to nimbler competitors. The company remains profitable but uninspiring, a value trap for investors seeking growth.

Reality will likely fall between extremes. Alembic's century-long survival demonstrates resilience that shouldn't be underestimated. The company has navigated colonial constraints, socialist economics, liberalization upheaval, and global competition. Each challenge forced adaptation that built capabilities. Current headwinds, while serious, aren't existential threats to a company with Alembic's technical depth and financial strength.

Biosimilars: The Next Frontier

Biosimilars represent Alembic's most intriguing opportunity. These complex biological drugs offer better economics than chemical generics—fewer competitors due to technical barriers, longer development timelines deterring opportunistic entry, and switching costs that provide some pricing stability. Alembic's fermentation expertise from decades of antibiotic production provides foundational capabilities for biological manufacturing.

Yet biosimilar success requires massive capital investment, regulatory expertise beyond small molecules, and commercial capabilities to compete against originator companies. Alembic must decide whether to pursue biosimilars independently, requiring billions in investment, or through partnerships that dilute returns but reduce risk. The choice will define the company's next decade.

Complex Generics: The Sweet Spot

Alembic's focus on complex generics—products requiring specialized manufacturing or presenting regulatory barriers—offers more immediate opportunity. Oncology injectables, ophthalmic solutions, and dermatological preparations provide better margins than oral solids. The company's existing infrastructure and expertise support this strategy without massive incremental investment.

Success requires careful portfolio selection, focusing on products with limited competition rather than chasing every opportunity. Manufacturing excellence becomes even more critical as complex products leave no room for error. Regulatory expertise must evolve as FDA scrutiny of complex generics intensifies. The companies winning in complex generics combine technical capabilities with commercial sophistication—a combination Alembic is still developing.

Domestic Consolidation: Inevitable Reality

India's pharmaceutical market will consolidate over the next decade as subscale players struggle with compliance costs and competition. Alembic could be acquirer or acquired, depending on strategic choices and market dynamics. As acquirer, the company's strong balance sheet and operational expertise position it to integrate struggling competitors. As target, Alembic's US presence and manufacturing capabilities would attract global generic companies seeking Indian footprint.

The family's 69.7% stake complicates consolidation scenarios. Any transaction requires Amin family agreement, limiting hostile approaches. Yet generational transitions often catalyze strategic changes as new leadership brings different perspectives. Whether the next generation maintains family control or monetizes holdings will significantly impact Alembic's strategic direction.

China +1: Opportunity and Challenge

Global pharmaceutical supply chains are diversifying away from Chinese concentration, creating opportunities for Indian API manufacturers. Alembic's integrated capabilities and regulatory track record position it well for this shift. Western companies seeking supply chain resilience might pay premiums for reliable non-Chinese sources. Government initiatives supporting API manufacturing could provide additional tailwinds.

Yet Chinese competitors won't cede market share easily. State support enables Chinese companies to compete at losses that would bankrupt private competitors. Technology transfer and automation give Chinese manufacturers cost advantages difficult to overcome. Environmental regulations make Indian manufacturing increasingly expensive. Alembic must find niches where reliability and quality trump pure cost—a challenging but not impossible task.

The 2030 Test

Success in 2030 won't be measured by size alone but by strategic positioning and return on capital. A successful Alembic might be smaller but more profitable, having exited commoditized segments while dominating specialized niches. The company might have merged with peers to achieve global scale. Or it might have been acquired by global players seeking Indian capabilities.

What seems certain is that status quo isn't sustainable. The comfortable middle ground Alembic has occupied for decades—large enough to matter but not large enough to lead—is disappearing as markets bifurcate between scale players and specialists. Alembic must choose its path and execute with conviction. The company's history suggests it will adapt and survive. Whether it will thrive remains an open question.

For investors, Alembic represents a bet on transformation potential versus execution risk. The company possesses ingredients for success—technical capabilities, regulatory expertise, financial strength—but must combine them effectively while navigating intensifying competition. The next five years will determine whether Alembic's second century mirrors its first—steady progress through patient effort—or marks dramatic departure toward either breakthrough success or marginalized survival.

The story of Alembic Pharmaceuticals is far from over. From colonial tinctures to global generics, the company has demonstrated remarkable adaptability. As it faces perhaps its greatest challenges yet, that adaptability will be tested again. The outcome matters not just for shareholders but for understanding how traditional companies transform in rapidly evolving industries. Whether Alembic succeeds or struggles, its journey offers lessons about building, managing, and investing in businesses navigating technological and competitive disruption.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube