Anthem Biosciences: From Bangalore Startup to India's CRDMO Unicorn

I. Introduction & Cold Open

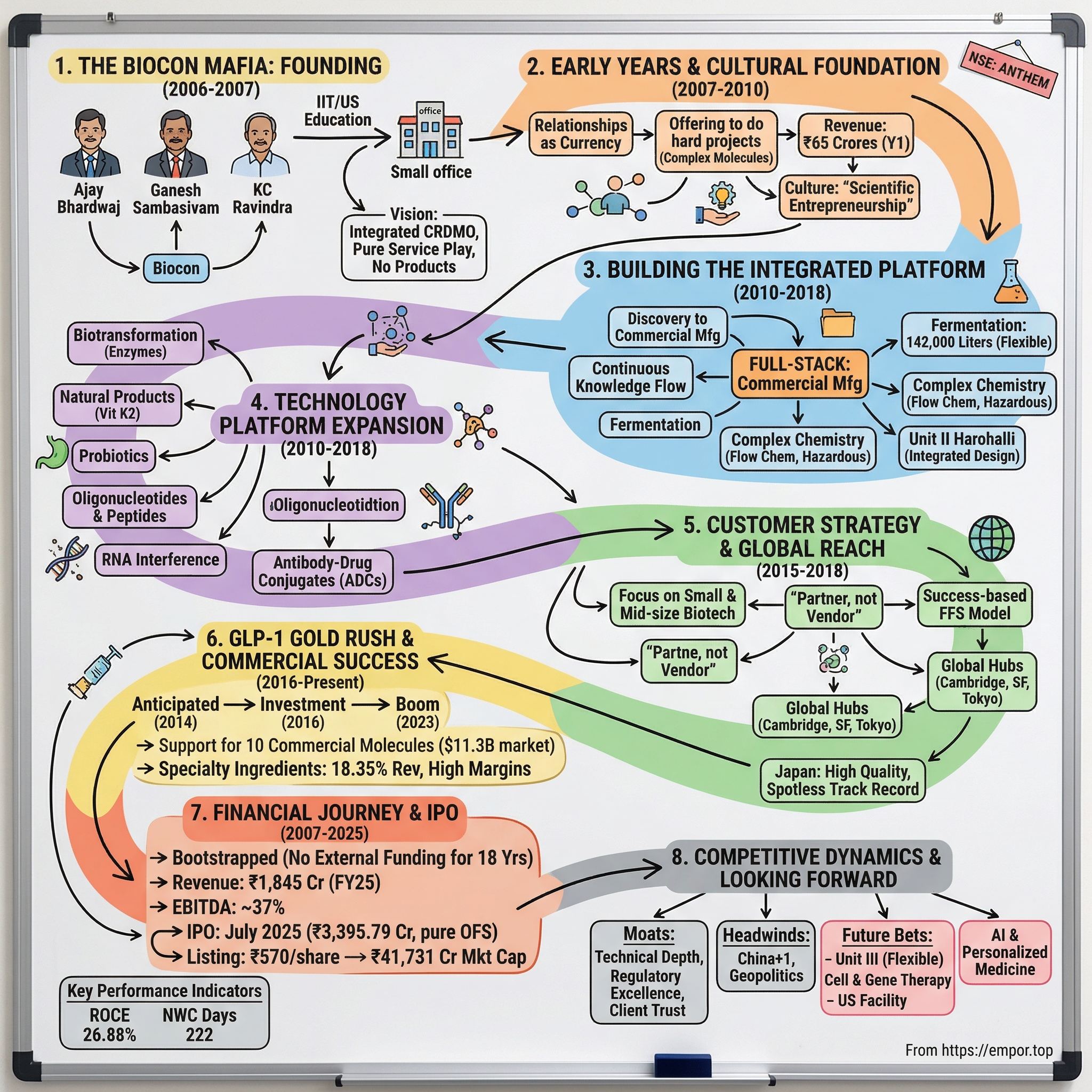

The conference room at Anthem Biosciences' Bommasandra facility overlooks a sprawling complex of laboratories and manufacturing units—142,000 liters of fermentation capacity humming quietly in the distance. It's July 2025, and the company has just listed on the NSE at ₹570 per share, commanding a market capitalization of ₹41,731 crores. Not bad for three ex-Biocon executives who started with a vision and a borrowed conference room eighteen years ago.

Here's the hook that should grab any serious investor: Anthem reached ₹1,000 crores in revenue within just 14 years of operations—the fastest among all Indian CRDMOs. Today, with revenues of ₹1,845 crores and profits of ₹451 crores, it's become something far more intriguing than just another contract manufacturer. It's a fully integrated platform spanning drug discovery to commercial manufacturing, serving over 550 customers across 44 countries, with capabilities in both small molecules and large biologics that most competitors can only dream of.

But the real story isn't in these numbers. It's in how three professionals walked away from one of India's most successful biotech companies at its peak, bet everything on a contrarian vision of what Indian pharma could become, and somehow managed to build the country's most comprehensive CRDMO without taking significant external funding until their IPO. They didn't just ride the outsourcing wave—they anticipated where the pharmaceutical industry would need help a decade before those needs became obvious.

Consider this: while most Indian pharma companies were racing to become the next generic giant, Anthem's founders were quietly building capabilities in RNA interference, antibody-drug conjugates, and peptide synthesis. When the GLP-1 revolution hit and Ozempic became a household name, Anthem was already there, manufacturing critical components for what would become an $11.3 billion market. That's not luck—that's the kind of strategic foresight that separates platforms from service providers.

This is a story about timing, certainly, but more fundamentally about building for a future that hasn't arrived yet. It's about why being "full-stack" matters in an industry where everyone else was picking lanes. And it's about how a Bangalore startup became the backbone for some of the world's most innovative drug development programs, all while maintaining EBITDA margins north of 36%.

The journey from zero to unicorn status reveals lessons about founder-led businesses, the power of technical depth, and why sometimes the best investment opportunities come from companies solving problems their customers don't even know they have yet. As we'll see, Anthem didn't just build a business—they built an essential piece of infrastructure for the global pharmaceutical innovation ecosystem.

II. The Biocon Mafia: Origins & Pre-founding Context

Picture Biocon in 2006: Kiran Mazumdar-Shaw's pioneering biotechnology company had just crossed $600 million in market capitalization, making it one of India's most celebrated entrepreneurial success stories. The company was firing on all cylinders—biosimilars were taking off, the contract research division was growing rapidly, and international partnerships were materializing left and right. For any ambitious executive, leaving Biocon at this moment would seem like career suicide.

Yet that's exactly what Ajay Bhardwaj decided to do.

Bhardwaj wasn't just any Biocon employee—he was employee number eight, one of the founding team members who had helped build the company from a garage startup in 1978 to a biotechnology powerhouse. As President of Marketing, he had been instrumental in Biocon's transformation, spearheading the company's expansion into contract research, clinical trials, and international markets. His fingerprints were on virtually every major strategic initiative that had driven Biocon's meteoric rise.

His journey to Biocon had been anything but linear. After completing his Bachelor of Technology in Chemical Engineering from IIT Delhi—that breeding ground of Indian entrepreneurship—Bhardwaj had crossed the Atlantic to Louisiana State University for his Master's in Chemical Engineering. The combination of IIT rigor and American research exposure would prove formative. He started his career at Max India, but it was at Biocon where he found his calling, spending nearly two decades helping Mazumdar-Shaw build her vision of an Indian biotech giant.

By 2006, Bhardwaj had assembled around him two equally impressive colleagues: Dr. Ganesh Sambasivam, a brilliant scientist with deep expertise in organic chemistry and process development, and KC Ravindra, who brought operational excellence and a keen understanding of manufacturing scale-up. The three of them had worked together on numerous projects at Biocon, developing an almost telepathic understanding of each other's strengths and working styles.

The Indian pharmaceutical landscape they surveyed in 2006 was undergoing a tectonic shift. The country had become the pharmacy of the developing world, with generic manufacturers like Ranbaxy, Dr. Reddy's, and Cipla dominating global markets for affordable medicines. But Bhardwaj and his co-founders saw something others missed: while everyone was focused on the generic gold rush, a quieter revolution was brewing in contract research and development.

Big Pharma was beginning to question its fully integrated model. The blockbuster era was ending, R&D productivity was plummeting, and companies were looking to externalize non-core activities. India had proven it could manufacture drugs cheaply and reliably—but could it move up the value chain into discovery and development? Most industry observers were skeptical. The conventional wisdom held that innovation happened in Boston and Basel, not Bangalore.

Bhardwaj disagreed. His years at Biocon had shown him that Indian scientists were every bit as capable as their Western counterparts—they just needed the right platform and opportunity. More importantly, he understood that the future of pharmaceutical development wouldn't be about choosing between chemistry or biology, small molecules or large molecules, discovery or manufacturing. It would be about integration—providing end-to-end solutions that could take a molecule from concept to commercial production.

"Why leave Biocon at its peak?" colleagues asked him repeatedly. His answer was both simple and audacious: Biocon had proven what was possible, but it was still fundamentally a product company that did services on the side. What if you built something from the ground up as a pure platform—no products, no conflicts of interest, just complete dedication to helping other companies bring their innovations to life?

The timing seemed almost suicidal. Starting a CRDMO in 2006 meant competing not just with established Indian players but with global giants like Lonza and WuXi. It meant convincing pharmaceutical companies to trust critical development work to a company with no track record, no facilities, and no proven capabilities. Most venture capitalists they approached couldn't understand why anyone would want to be a services company in an industry obsessed with product margins.

But Bhardwaj had seen something during his final years at Biocon that convinced him the timing was perfect. Small biotech companies were proliferating, funded by venture capital and focused on novel mechanisms and breakthrough therapies. These companies had brilliant science but lacked the infrastructure and expertise to develop and manufacture their discoveries. They needed partners, not vendors—companies that could think strategically about their entire development pathway, not just execute discrete tasks.

The decision to leave wasn't made lightly. The three founders spent months discussing their vision, sketching out capabilities they would need, identifying gaps in the market. They studied successful CRDMOs globally, analyzed why some thrived while others remained perpetual also-rans. They realized that most contract organizations were either too specialized (only discovery, only manufacturing) or too broad (trying to be everything to everyone). Their insight: build deep, integrated capabilities in specific areas where complexity created value.

By late 2006, the die was cast. Bhardwaj, Sambasivam, and Ravindra submitted their resignations to a shocked Biocon management team. The "Biocon Mafia"—as they would later be known in Indian pharma circles—was born. They had no funding, no facilities, and no customers. What they had was a contrarian vision of where pharmaceutical development was heading and the technical chops to build something unprecedented in Indian pharma: a fully integrated CRDMO that could compete globally from day one.

The biotech ecosystem in Bangalore would never be quite the same. And as we'll see, neither would the global CRDMO landscape.

III. The Founding & Early Years (2006–2010)

The first Anthem Biosciences "office" was actually a borrowed conference room in a Bangalore business center, where Ajay Bhardwaj and his co-founders would meet potential clients and partners, projecting confidence while their actual laboratory was still under construction. It was 2007, and they had just incorporated the company with minimal capital—no venture funding, no private equity, just personal savings and an unshakeable belief in their vision.

The name "Anthem" itself was carefully chosen. Unlike the Sanskrit-derived names favored by many Indian pharma companies, they wanted something that would resonate globally, suggesting both celebration and unity—a platform where different capabilities would come together in harmony. The logo, with its interconnected elements, symbolized their integrated approach to drug development.

Starting operations in 2007 meant entering a market where trust was everything and track records were currency. Pharmaceutical companies don't switch CRDMOs lightly—a failed project can set drug development back years and cost millions. For a startup with no completed projects, no regulatory inspections, and no reference customers, the challenge seemed insurmountable.

But Bhardwaj had an ace up his sleeve: relationships. His two decades at Biocon had given him deep connections across the global pharmaceutical industry. More importantly, he understood the pain points of both big pharma and emerging biotech. He knew that many companies were frustrated with the existing CRDMO landscape—providers who were either too rigid, too slow, or too focused on their own product pipelines to give client projects proper attention.

The founding team made a crucial early decision that would define Anthem's trajectory: they would never develop their own products. This "pure-play" CRDMO model meant forsaking the higher margins that came with proprietary drugs, but it eliminated conflicts of interest. Clients could share their most sensitive intellectual property without worrying that Anthem might become a competitor. In an industry rife with paranoia about IP theft, this commitment to being a pure service provider became a powerful differentiator.

The early pitch was audacious. While established CRDMOs were telling clients to choose specific services from a menu, Anthem promised to be a strategic partner across the entire development continuum. Need early-stage discovery work? They would do it. Want to scale up manufacturing? They could handle that too. Require regulatory support for global filings? Consider it done. It sounded too good to be true—and for the first year, it largely was.

Building credibility without a track record required creative approaches. Bhardwaj and his team offered to take on challenging projects that established players had rejected—complex molecules, difficult syntheses, tight timelines. They positioned themselves as problem-solvers, not just service providers. When a small US biotech came to them with a particularly challenging peptide synthesis that three other CRDMOs had failed to deliver, Anthem's scientists worked around the clock to crack it. Word spread quickly in the tight-knit biotech community.

By the end of their first operational year, they had crossed ₹65 crores in revenue—a remarkable achievement for a startup in the conservative pharmaceutical industry. But revenue was just one metric. More importantly, they were building capabilities at a breakneck pace. The initial team of 50 scientists and engineers grew to over 200 by 2009. They weren't just hiring; they were building a culture of innovation that would become Anthem's secret weapon.

The culture Bhardwaj fostered was unique in Indian pharma. While most companies operated on strict hierarchies inherited from traditional Indian corporate structures, Anthem adopted a more egalitarian approach. Young scientists could directly approach senior management with ideas. Failure was tolerated if it came from pushing boundaries. The company instituted "Science Fridays" where teams would present challenging problems and brainstorm solutions collectively.

Dr. Sambasivam, the chief scientific officer, insisted on building capabilities before market demand materialized. While competitors focused on proven technologies, Anthem began investing in emerging areas like biocatalysis and continuous flow chemistry. "We wanted to be ready when the market turned," he would later explain. This forward-thinking approach meant lower margins in the short term but positioned them perfectly for future opportunities.

The decision to focus equally on both chemistry and biology from day one was controversial. Most Indian CRDMOs picked one lane—either small molecule chemistry or large molecule biologics. Building capabilities in both required different equipment, different expertise, and different regulatory frameworks. It was expensive and complex. But Bhardwaj believed that the future of drug development would increasingly blur the lines between small and large molecules. Antibody-drug conjugates, for instance, required expertise in both domains.

The global financial crisis of 2008-2009 could have killed the young company. Pharmaceutical companies slashed R&D budgets, biotechs struggled to raise funding, and outsourcing decisions were postponed indefinitely. Anthem's order book shrank dramatically. But instead of retrenching, Bhardwaj made a counterintuitive decision: accelerate investment in infrastructure and capabilities.

While competitors were laying off scientists, Anthem was hiring. While others delayed expansion plans, Anthem pushed ahead with its facility buildout. The logic was simple but risky: when the recovery came, they wanted to be positioned to capture disproportionate share. They used the downturn to build capabilities that would have been impossible to develop during boom times when everyone was running at full capacity.

By 2010, Anthem had completed over 500 projects for more than 100 clients globally. They had built state-of-the-art facilities in Bommasandra and were planning their second site in Harohalli. Revenue had grown at a compound annual rate exceeding 40%. More importantly, they had begun to develop a reputation as the CRDMO that could handle the projects others couldn't or wouldn't take on.

The foundation was set. The question now was whether they could scale their boutique, high-touch model without losing what made them special. As the pharmaceutical industry emerged from the financial crisis, a new era of drug development was dawning—one focused on biologics, personalized medicine, and novel modalities. Anthem's bet on being full-stack was about to be tested in ways the founders could never have imagined.

IV. The CRDMO Playbook: Discovery to Manufacturing

Inside Anthem's Bommasandra facility, a visitor in 2011 would have witnessed something unusual for an Indian CRDMO: chemists and biologists working literally side by side, sharing not just cafeteria space but actual project teams. This physical manifestation of integration wasn't just symbolic—it represented a fundamental rethinking of how contract development should work.

The decision to be "full-stack" went against every piece of conventional wisdom in the CRDMO industry. Specialization was supposed to be the path to excellence. Focus on one thing, do it better than anyone else, and dominate that niche. Lonza focused on biologics manufacturing. Albany Molecular Research (AMR) concentrated on complex chemistry. ChemPartner specialized in discovery. Everyone had their lane.

But Bhardwaj and his team had observed something critical: drug development doesn't happen in lanes. It's a complex, iterative process where discovery insights inform development decisions, where manufacturing constraints shape formulation choices, where regulatory requirements influence analytical methods. When these activities happen in different organizations—or even different departments—critical information gets lost in translation. Timelines stretch. Costs balloon. Projects fail.

Anthem's integrated model meant that when a biotech company came to them with a promising molecule, the same team that conducted the initial feasibility assessment would shepherd it through scale-up, process optimization, and eventually commercial manufacturing. This continuity created tremendous efficiencies. Knowledge accumulated rather than dissipated. Relationships deepened rather than reset with each phase transition.

Building these capabilities required massive investment. The Bommasandra facility, spread across 8 acres, housed one of India's most sophisticated analytical laboratories. High-resolution mass spectrometers sat next to nuclear magnetic resonance machines. The quality control lab alone represented an investment of over ₹50 crores—money that could have gone toward capacity expansion but instead went toward capability building.

The fermentation capacity decision was particularly bold. By 2012, Anthem had installed 142,000 liters of fermentation capacity—the largest of any Indian CRDMO, six times larger than their nearest competitor. This wasn't just about scale; it was about flexibility. They configured their fermenters to handle everything from E. coli to mammalian cell cultures, from small-scale process development to commercial production. The distributed control systems (DCS) they implemented were typically found only in big pharma facilities, allowing for precise control and documentation that would prove critical for regulatory compliance.

The chemistry capabilities were equally impressive. While most Indian CRDMOs focused on straightforward reactions that could be easily scaled, Anthem invested in complex chemistry—organometallic reactions, asymmetric synthesis, hazardous chemistry involving reagents like azides and diazomethane. They built specialized facilities with blast walls and sophisticated safety systems. It was expensive and risky, but it allowed them to take on projects others couldn't handle.

The flow chemistry investment exemplified their forward-thinking approach. In 2011, continuous flow chemistry was still largely academic. Most pharmaceutical companies were skeptical about its commercial viability. But Dr. Sambasivam had seen presentations at conferences suggesting flow chemistry could revolutionize pharmaceutical manufacturing—better yields, improved safety, smaller footprints, easier scale-up. Anthem built one of India's first commercial-scale flow chemistry units, years before market demand materialized.

The regulatory framework they built was perhaps their most underappreciated asset. Unlike product companies that only need to navigate regulations for their own portfolio, Anthem had to be fluent in the requirements of multiple regulatory agencies—FDA, EMA, PMDA, and others. They built quality systems that could satisfy the most stringent inspector from any agency. The documentation systems they implemented generated an average of 10,000 pages per project—a paper trail that provided complete transparency and traceability.

But integration meant more than just having diverse capabilities under one roof. It meant creating systems and processes that allowed these capabilities to work together seamlessly. They developed proprietary project management software that allowed real-time tracking across different departments. A discovery chemist could see how their synthetic route was performing in scale-up. A manufacturing engineer could flag potential issues back to the development team before they became problems.

The success-based fee-for-service (FFS) model they pioneered was another differentiator. Unlike traditional fee-for-service arrangements where CRDMOs got paid regardless of outcome, Anthem tied part of their compensation to project success. If they delivered on time and met specifications, they earned bonuses. If they failed, they absorbed some of the cost. This skin-in-the-game approach aligned their interests with clients and drove a culture of accountability that permeated the organization.

The results spoke for themselves. By 2013, Anthem boasted a 96.76% project success rate—extraordinary in an industry where a 70% success rate was considered good. Their on-time delivery rate exceeded 90%. Perhaps most importantly, over 80% of clients who completed one project with them came back for additional work—a repeat rate that suggested they were delivering value beyond just technical execution.

The Unit II expansion in Harohalli, completed in 2014, represented the full flowering of their integrated vision. Unlike Unit I, which had grown organically as capabilities were added, Unit II was designed from the ground up as an integrated facility. The layout minimized material movement between departments. The utilities were sized for future expansion. The automation systems were state-of-the-art. It was a physical manifestation of everything they had learned about efficient, integrated drug development.

What made this integration work wasn't just infrastructure or systems—it was culture. Anthem cultivated what they called "scientific entrepreneurship" among their staff. Scientists weren't just expected to execute protocols; they were encouraged to suggest improvements, challenge assumptions, and think holistically about projects. This culture of innovation meant that even routine projects often yielded process improvements or novel approaches that benefited future work.

The full-stack model also created unexpected synergies. Insights from biologics projects informed small molecule development. Analytical methods developed for one project found applications in others. The deep expertise in fermentation positioned them perfectly when the industry's interest in biosimilars exploded. Being full-stack wasn't just about offering comprehensive services—it was about building a platform where knowledge and capabilities compound over time.

By 2015, Anthem had become something unique in the global CRDMO landscape: a company with the comprehensive capabilities of a major pharmaceutical company but the agility and customer focus of a boutique service provider. They could take a project from earliest discovery through commercial manufacturing, but they could also plug into any point in the development continuum where clients needed help. This flexibility, combined with their technical depth, made them an ideal partner for the emerging biotech companies that would drive the next wave of pharmaceutical innovation.

V. The Technology Platform Build (2010–2018)

The conference room walls at Anthem's R&D center in 2012 were covered with molecular structures that looked like abstract art to outsiders but represented the future of medicine to those who could read them: RNA interference molecules, antibody-drug conjugates, GLP-1 agonists. While the rest of Indian pharma was perfecting generic statins and antibiotics, Anthem was quietly building capabilities for drugs that didn't exist yet.

This wasn't speculative investment—it was calculated anticipation. Bhardwaj and Dr. Sambasivam had spent years attending scientific conferences, reading journals, and talking to researchers at the cutting edge of drug discovery. They saw patterns that others missed. They noticed which academic discoveries were attracting venture funding. They tracked which big pharma companies were making strategic acquisitions. And they placed bets accordingly.

The biotransformation platform was their first major technology investment. Traditional chemical synthesis often required harsh conditions, toxic reagents, and generated substantial waste. Biotransformation—using enzymes or whole cells to catalyze chemical reactions—offered a greener, often more efficient alternative. But it required entirely different expertise and infrastructure than traditional chemistry.

Anthem didn't just buy some fermenters and hire a few microbiologists. They built comprehensive capabilities: enzyme engineering to create novel biocatalysts, fermentation expertise to produce them at scale, and downstream processing to purify the products. They developed proprietary enzyme libraries and screening methods. By 2014, they could perform transformations that were impossible through traditional chemistry—selective modifications of complex molecules that would otherwise require multiple protection and deprotection steps.

The natural products division exemplified their strategy of building platforms before markets. In 2013, natural Vitamin K2 was a niche product with limited demand. But Anthem's scientists had noticed increasing research linking K2 deficiency to osteoporosis and cardiovascular disease. They developed a fermentation-based production process that was more efficient and sustainable than chemical synthesis. When demand exploded in 2016-2017, driven by aging populations and increased health consciousness, Anthem was one of the few companies globally that could supply high-quality K2 at scale.

The probiotics platform followed a similar trajectory. While others saw probiotics as a simple supplement business, Anthem recognized them as sophisticated biological products requiring careful strain selection, controlled fermentation, and specialized formulation. They built capabilities to produce spores, live bacteria, and even engineered probiotics for therapeutic applications. The same fermentation expertise that produced small molecule intermediates could be leveraged for these biological products.

But the real technological leap came with their investment in oligonucleotide and peptide synthesis. These were complex molecules sitting at the intersection of chemistry and biology—too large for traditional small molecule approaches but synthesized chemically rather than biologically. The equipment was expensive, the chemistry was difficult, and the market in 2014 was still nascent. Most Indian CRDMOs wouldn't touch these molecules.

Anthem built one of Asia's most sophisticated oligonucleotide synthesis facilities. They invested in high-throughput synthesizers that could produce multiple sequences in parallel. They developed purification methods that could achieve the extraordinary purity levels required for therapeutic applications. They created analytical methods that could detect impurities at parts-per-billion levels. It was a massive investment in a market that barely existed.

The RNA interference (RNAi) platform represented perhaps their boldest bet. In 2014, RNAi therapeutics were still recovering from the "valley of death" period when many had written off the technology as too difficult to deliver in vivo. But Anthem's scientists believed the delivery problems would eventually be solved, and when they were, demand for high-quality oligonucleotides would soar. They were right—by 2018, the FDA approval of Patisiran validated RNAi as a therapeutic modality, and Anthem was perfectly positioned to supply the complex lipids and oligonucleotides these drugs required.

The antibody-drug conjugate (ADC) platform showcased their integrated capabilities better than anything else. ADCs required expertise in three distinct areas: antibody production and modification, cytotoxic payload synthesis, and linker chemistry to connect them. Most CRDMOs could handle one, maybe two of these components. Anthem could do all three, and more importantly, they could optimize the entire conjugate as a system rather than individual parts.

The technology build wasn't just about adding new capabilities—it was about creating interconnections between them. The same mass spectrometry expertise used for small molecule analysis was adapted for oligonucleotide sequencing. Purification methods developed for peptides found applications in ADC payloads. The quality systems built for biologics manufacturing ensured the consistency required for complex chemical synthesis.

By 2016, Anthem had built something unique: a technology platform that spanned the entire spectrum of pharmaceutical modalities. They could handle traditional small molecules, complex biologics, and everything in between. But more than just breadth, they had depth—the ability to tackle the most challenging projects in each area.

The fermentation capacity expansion to 182,000 liters, announced in 2017, wasn't just about scale—it was about flexibility. The new fermenters were designed to handle an even wider range of organisms and conditions. They could switch from bacterial fermentation for small molecules to mammalian cell culture for antibodies with minimal downtime. This flexibility would prove crucial as the industry increasingly moved toward smaller batch sizes and more diverse product portfolios.

The numbers validated the strategy. By 2018, Anthem had completed over 5,000 projects across their various technology platforms. Their specialty ingredients business, built on these advanced capabilities, was generating 18.35% of revenue with significantly higher margins than traditional service work. More importantly, they had become a go-to partner for some of the most innovative biotechnology companies in the world.

But the real validation came from an unexpected source: the obesity drug revolution that was about to transform pharmaceuticals. All those years of investing in peptide synthesis, all that expertise in complex molecules, all those capabilities that seemed excessive for the market—they were about to pay off in ways even Bhardwaj hadn't fully anticipated. The GLP-1 gold rush was coming, and Anthem had already staked their claim.

VI. The Customer Strategy & Global Expansion

The small biotech CEO sat across from Ajay Bhardwaj in 2015, visibly frustrated. His company had a promising drug candidate but had just been burned by their third CRDMO—delays, quality issues, and worst of all, a sudden deprioritization when the contractor landed a bigger client. "We need a partner, not a vendor," he said. It was a sentence Bhardwaj had heard dozens of times, and it perfectly captured Anthem's strategic opportunity.

While large CRDMOs chased big pharma contracts worth hundreds of millions, Anthem made a contrarian bet: focus on small and mid-size biotechnology companies. These companies, typically with fewer than 500 employees and often pre-revenue, were the ugly ducklings of the CRDMO world. They had limited budgets, complex molecules, aggressive timelines, and no room for error. A single failed project could kill the company. Most established CRDMOs treated them as second-tier clients.

Anthem saw them differently. These companies were where innovation happened—novel mechanisms, breakthrough technologies, first-in-class drugs. They were run by scientists who understood the technical challenges and appreciated sophisticated solutions. Most importantly, they needed true partners who would treat their projects with the urgency of survival, because for many of them, it was.

The customer acquisition strategy was surgical. Instead of casting a wide net, Anthem focused on biotech hubs: Cambridge, San Francisco, San Diego, and increasingly, Shanghai and Tokyo. They didn't send traditional sales representatives; they sent senior scientists who could engage in deep technical discussions. Dr. Sambasivam himself would often fly to meet potential clients, sketching synthetic routes on whiteboards and suggesting alternative approaches.

The success-based pricing model was particularly attractive to cash-strapped biotechs. Traditional CRDMOs demanded payment regardless of outcome—if a synthesis failed, the client still paid for the attempt. Anthem's model shared the risk. They would invest their own resources upfront, betting on their ability to deliver. This skin-in-the-game approach resonated with entrepreneurs who were betting everything on their science.

By 2016, Anthem was working with over 350 customers across 30 countries. But the geographic expansion was strategic, not scattershot. They focused on markets with strong intellectual property protection, sophisticated regulatory frameworks, and robust venture funding for biotechnology. The U.S. represented 40% of revenue, Europe 30%, and Japan—notoriously difficult for Indian companies to penetrate—a remarkable 15%.

The Japan success story deserves special attention. Japanese pharmaceutical companies are famously conservative, preferring to work with established partners and placing enormous emphasis on quality and reliability. Breaking into this market typically took decades. Anthem cracked it in less than five years through a combination of technical excellence and cultural sensitivity. They hired Japanese-speaking project managers, adapted their documentation to Japanese preferences, and most importantly, never missed a deadline—ever.

Building trust with global pharma required more than just technical competence. It required demonstrating stability and sustainability. The fact that Anthem was founder-led and hadn't taken external funding was actually an advantage. Clients didn't have to worry about private equity owners pushing for short-term profits or strategic pivots. The founders were in it for the long haul.

The quality and compliance infrastructure Anthem built was world-class. They didn't just meet regulatory requirements; they exceeded them. FDA inspections resulted in zero critical observations. European authorities praised their documentation systems. Japanese inspectors—known for their meticulousness—found nothing significant to criticize. This spotless regulatory track record became a powerful marketing tool.

But perhaps the most innovative aspect of their customer strategy was the "scientific collaboration" model. Rather than just executing prescribed protocols, Anthem's scientists actively contributed to project design. They would suggest alternative synthetic routes, recommend analytical methods, propose formulation improvements. Many clients found that Anthem scientists knew more about certain aspects of their molecules than they did themselves.

This deep engagement created switching costs that went beyond the typical CRDMO relationship. When a client had worked with Anthem through discovery and development, the institutional knowledge accumulated was irreplaceable. The idea of transferring to another provider and having to re-educate them on years of project history was daunting. This stickiness showed in the numbers: client retention rates exceeded 85%, and average relationship duration was over seven years.

The customer concentration that would later concern some investors was actually a sign of strength. By FY25, five customers represented over 70% of revenue. But these weren't dependent relationships—they were deep partnerships. These clients weren't just buying services; they were accessing capabilities they couldn't build internally. The concentration reflected the depth of value Anthem provided rather than customer dependence.

The global expansion strategy also involved careful capability matching. They didn't try to be everything to everyone everywhere. In the U.S., they focused on complex chemistry and integrated projects. In Europe, they emphasized their biologics capabilities and regulatory expertise. In Japan, they led with quality and reliability. This targeted approach allowed them to compete effectively against much larger CRDMOs.

By 2018, Anthem had completed over 8,000 unique projects. But more impressive than the quantity was the diversity—from simple intermediates to complex biologics, from microgram-scale synthesis to ton-scale manufacturing. This breadth of experience created a virtuous cycle: each project added to their knowledge base, making them more capable for the next challenge.

The decision to remain a pure service provider, never developing their own products, continued to pay dividends. In an industry rife with conflicts of interest—CRDMOs abandoning client projects to focus on their own pipelines—Anthem's commitment to being conflict-free was increasingly valuable. Clients could share their most sensitive data, their most innovative ideas, without fear of creating a future competitor.

Looking at the customer base in 2018, a pattern emerged: Anthem had become the preferred partner for the most innovative companies in biotechnology. Their client list read like a who's who of breakthrough drug development. And as these companies succeeded—getting drugs approved, going public, getting acquired—Anthem grew with them. The small biotechs they had supported through lean years became major customers as their drugs reached commercialization.

This customer strategy—focusing on innovation over size, partnership over transaction, quality over quantity—had created something remarkable: a network effect in drug development. The more innovative companies Anthem worked with, the more they learned about cutting-edge science. The more they learned, the better they became at solving complex problems. The better they became, the more innovative companies wanted to work with them. It was a flywheel that would accelerate dramatically with the coming revolution in obesity drugs and novel therapeutics.

VII. The GLP-1 Gold Rush & Commercial Success

The Ozempic phenomenon of 2023 seemed to catch the world by surprise—suddenly, everyone from Hollywood celebrities to suburban mothers was talking about semaglutide and tirzepatide. But in Anthem's peptide synthesis labs, the champagne had been on ice since 2016. They had been manufacturing GLP-1 receptor agonists and their intermediates for years, quietly building capacity while the rest of the industry focused elsewhere.

The story of how Anthem positioned itself for the GLP-1 gold rush goes back to 2014, when diabetes drugs were a steady but unspectacular market. GLP-1 agonists existed—exenatide had been approved in 2005—but they were seen as niche products for Type 2 diabetes. The weekly formulations were still in development, and the idea that these drugs could transform obesity treatment was confined to academic conferences and pharmaceutical R&D departments.

But Anthem's scientists noticed something interesting in the scientific literature and patent filings: an unusual amount of activity around longer-acting GLP-1 formulations and dual agonists targeting multiple receptors. More tellingly, several small biotechs were raising significant funding for next-generation metabolic drugs. The synthesis of these peptides was complex—long sequences, difficult modifications, challenging purification requirements. It was exactly the kind of high-barrier chemistry Anthem had been building toward.

The decision to invest heavily in peptide manufacturing capacity in 2015-2016 raised eyebrows internally. Peptides were a small market, the equipment was expensive, and the expertise was specialized. But Bhardwaj pushed forward, authorizing the construction of dedicated peptide synthesis suites with solid-phase synthesis capability, preparative HPLC systems for purification, and analytical tools that could characterize these complex molecules down to individual amino acid modifications.

By 2018, Anthem wasn't just making peptides—they were innovating in peptide manufacturing. They developed proprietary methods for difficult couplings, created novel purification strategies that improved yields, and built analytical methods that could detect impurities other manufacturers missed. When pharmaceutical companies came to them with challenging peptide projects, Anthem often knew more about manufacturing these molecules than the companies developing them.

The specialty ingredients division, which included these peptide capabilities, was generating ₹338 crores by FY24—18.35% of total revenue but with significantly higher margins than traditional fee-for-service work. The business model was elegant: develop manufacturing processes for innovative molecules, capture value through both service fees and supply agreements, and leverage the same capabilities across multiple clients.

Then came 2023, and the world discovered what Anthem had been preparing for: GLP-1 drugs weren't just for diabetes anymore. The STEP trials had shown remarkable weight loss results. The SURMOUNT trials for tirzepatide were even more impressive. Suddenly, analysts were projecting the GLP-1 market would reach $100 billion by 2030. Every pharmaceutical company wanted in on the action.

Anthem found itself in an enviable position. They had the capacity, the expertise, and most importantly, the regulatory approvals already in place. While competitors scrambled to build peptide capabilities, Anthem was already manufacturing. They supported 10 commercialized molecules, including 5 with collective end-market sales of $11.3 billion in 2024, projected to grow to $21.4 billion by 2029.

But the real value wasn't just in manufacturing the blockbuster drugs. It was in supporting the next generation. By 2024, over 100 companies were developing GLP-1 variants, dual agonists, and oral formulations. Each needed partners for synthesis, scale-up, and manufacturing. Anthem's phones didn't stop ringing. They were careful not to over-commit, maintaining their quality standards even as demand soared.

The numbers tell the story of explosive growth. Revenue jumped from ₹1,057 crores in FY23 to ₹1,419 crores in FY24 and then to ₹1,845 crores in FY25—a 30% annual growth rate that outpaced every peer. More impressively, they maintained EBITDA margins of 36.81% even while scaling rapidly, suggesting strong pricing power and operational efficiency.

The GLP-1 boom also validated Anthem's integrated model in unexpected ways. These drugs didn't just need peptide synthesis—they needed formulation development for long-acting depots, analytical methods for complex characterization, and manufacturing capabilities for commercial supply. Companies that came to Anthem for peptide synthesis stayed for the full development program.

The success in GLP-1 had spillover effects across the business. The same capabilities that produced GLP-1 peptides could manufacture other complex peptides—oncology drugs, rare disease treatments, diagnostic agents. The analytical methods developed for GLP-1 characterization found applications in other projects. The quality systems built to satisfy regulatory requirements for these high-profile drugs elevated standards across the organization.

But Anthem was careful not to become over-dependent on the GLP-1 boom. They used the profits to invest in other emerging areas—oligonucleotides for rare diseases, antibody-drug conjugates for oncology, cell therapy components. The GLP-1 windfall was funding the next generation of capabilities, continuing the pattern of building for the future that had defined the company since its founding.

The commercial success went beyond just financial metrics. Anthem had become a critical part of the global pharmaceutical supply chain for one of the most important drug classes of the decade. They were enabling innovation, helping companies bring life-changing treatments to patients. It was the validation of everything Bhardwaj and his co-founders had envisioned when they left Biocon eighteen years earlier.

Looking at the order book in early 2025, the GLP-1 story was far from over. Oral formulations were in development. Combination therapies were being explored. Next-generation agonists with better efficacy and fewer side effects were in the pipeline. And Anthem was involved in many of these programs, not just as a manufacturer but as a strategic partner helping to solve the technical challenges that stood between promising molecules and patient benefit.

The specialty ingredients business had grown to represent nearly 20% of revenue, with margins that made it disproportionately profitable. But more than just a financial success, it represented the power of anticipation—of building capabilities before markets materialized, of investing in complexity when others sought simplicity, of betting on innovation when others played it safe. The GLP-1 gold rush hadn't made Anthem successful; it had revealed the success they had been building toward all along.

VIII. Financial Journey & The Path to IPO

The spreadsheet on the investment banker's laptop in early 2025 told a story that seemed almost too good to be true: compound annual revenue growth of 30% over three years, EBITDA margins approaching 37%, and return on equity exceeding 20%—all achieved without a single rupee of external funding until the IPO. In the conference room of Kotak Mahindra Capital, the lead bankers were preparing what would become one of the most successful CRDMO listings in Indian capital markets history.

The financial journey of Anthem Biosciences breaks conventional wisdom about capital-intensive businesses. From 2007 to 2024, the company had funded its entire growth—from zero to ₹1,845 crores in revenue—through internal accruals and modest debt. No venture capital, no private equity, just reinvested profits and the founders' conviction that patient capital creates lasting value.

The numbers from FY23 to FY25 tell the story of acceleration. Revenue grew from ₹1,057 crores to ₹1,845 crores. Profit after tax rose from ₹367 crores to ₹451 crores. But the real story was in the composition of this growth. It wasn't just more of the same—it was a fundamental shift toward higher-value services. The integrated projects business, where Anthem handled multiple stages of development, grew from 60% to 72% of revenue. These projects commanded premium pricing and created stickier customer relationships.

The margin profile was particularly impressive. While most Indian CRDMOs operated at EBITDA margins in the 20-25% range, Anthem consistently delivered 35%+. This wasn't through cost-cutting—employee costs and R&D spending remained robust. Instead, it reflected pricing power that came from technical differentiation. When you're one of the few companies globally that can synthesize a complex peptide or manufacture a difficult ADC payload, customers pay premium prices.

Return ratios told another story of efficiency. Return on equity of 20.82% and return on capital employed of 26.88% in FY25 suggested a business that was generating substantial value from its asset base. The comparison with peers was stark—Syngene's ROE was 11.9%, Sai Life Sciences was at 9.2%. This efficiency came from the integrated model: the same assets could serve multiple purposes, the same expertise could be leveraged across projects, the same customer relationships could generate multiple revenue streams.

But there was one metric that concerned analysts: working capital. Net working capital days stood at 222 in FY25, compared to Syngene's 34 days. This meant Anthem had significant money tied up in inventory and receivables. The company's explanation was reasonable—complex projects required purchasing specialized raw materials upfront, and blue-chip customers often negotiated extended payment terms. Still, it was capital that couldn't be deployed elsewhere.

The decision to go public in 2025 wasn't driven by capital needs—the company was generating enough cash to fund its expansion. Instead, it was about liquidity for early investors and employees, brand building in global markets, and creating currency for potential acquisitions. The timing was deliberate: the GLP-1 boom had demonstrated Anthem's capabilities, the order book was strong, and Indian capital markets were receptive to quality stories.

The IPO structure was unusual—it was a pure offer for sale (OFS) with no fresh capital raise. Existing shareholders, including the founders and early employees, were selling ₹3,395.79 crores worth of shares at ₹570 per share. The fact that the company didn't need capital even for its ambitious expansion plans was a powerful signal about cash generation capabilities.

The roadshow revealed strong investor interest. The institutional portion was subscribed 15 times, with participation from marquee global funds. The story resonated: a founder-led business with demonstrated execution, exposure to secular growth trends in pharmaceutical outsourcing, and a differentiated positioning in complex chemistry and biology. The July 2025 listing saw the stock price jump 20% on day one, valuing the company at over ₹41,000 crores.

Post-IPO, Anthem's valuation metrics sparked debate. At 23x FY25 earnings, it was trading at a premium to established players like Divi's Laboratories (18x) and Syngene (19x). The bulls argued this was justified given superior growth rates and margins. The bears worried about customer concentration and working capital requirements. Both had valid points.

The capital allocation strategy post-IPO was conservative but strategic. Despite having no immediate capital needs, the company announced a ₹500 crore capex plan focused on three areas: expanding fermentation capacity to 250,000 liters, building dedicated facilities for cell and gene therapy components, and creating a U.S. finishing facility to serve American customers directly. Each investment extended existing capabilities rather than venturing into entirely new areas.

Financial discipline remained paramount even after becoming public. The company maintained its policy of not providing quarterly guidance, arguing that the project-based nature of their business made short-term predictions meaningless. They focused instead on long-term metrics: customer additions, capability development, and capacity utilization. This approach frustrated some analysts but reinforced the company's long-term orientation.

The cash flow characteristics of the business were unique. Unlike product companies that needed continuous investment in R&D with uncertain returns, Anthem's investment in capabilities had predictable payoffs. Once they built expertise in a particular area—say, oligonucleotide synthesis—they could leverage it across multiple clients and projects. This created a compounding effect where returns on invested capital improved over time.

By early 2025, institutional ownership had risen to 45%, with several global pharmaceutical-focused funds taking substantial positions. The smart money recognized what Anthem represented: not just exposure to the CRDMO sector, but a play on the increasing complexity of drug development. As pharmaceuticals moved toward more sophisticated modalities—cell therapies, gene editing, personalized medicine—companies with Anthem's integrated capabilities would become increasingly valuable.

The founder ownership structure post-IPO remained substantial, with the three co-founders retaining 35% of the company. This alignment of interests reassured long-term investors. The founders weren't cashing out; they were creating liquidity while remaining committed to the business they had built.

Looking at the financial trajectory from startup to ₹41,000 crore market cap, several lessons emerge. First, patient capital and reinvestment can create extraordinary value without dilution. Second, technical differentiation translates directly to financial performance through pricing power and customer stickiness. Third, the integrated model, while capital-intensive upfront, creates superior returns over time through operational leverage and synergies.

The IPO marked not an end but a transition. From bootstrapped startup to public company, Anthem had maintained its culture of innovation and customer focus while building world-class financial performance. The question now was whether they could maintain this trajectory as a public company with quarterly scrutiny and investor expectations. As we'll see in examining the competitive landscape, the challenges ahead were as significant as those behind.

IX. Competitive Dynamics & Industry Analysis

The global CRDMO industry in 2025 resembles a massive chess board with over 1,000 players, each maneuvering for position in a $150 billion market growing at 8% annually. At the top sit giants like Lonza and Catalent with revenues exceeding $5 billion. In the middle tier, companies like WuXi AppTec and Samsung Biologics leverage scale and geographic advantages. And then there's Anthem—smaller in absolute terms but punching far above its weight in complexity and capability.

Understanding Anthem's competitive position requires appreciating how the CRDMO industry has evolved. Twenty years ago, contract manufacturing was largely about labor arbitrage—Western companies outsourcing to Asia for cost savings. Today, it's about accessing capabilities that pharmaceutical companies can't or won't build internally. The game has shifted from cost to complexity, from scale to specialization, from transaction to partnership.

In India, Anthem competes with several formidable players. Syngene International, spun out of Biocon in 2015, brings similar parentage but a different strategy—they maintain discovery research as their core while Anthem emphasizes integrated development and manufacturing. With revenues of ₹3,614 crores, Syngene is larger, but Anthem's 36.81% EBITDA margins significantly exceed Syngene's 28%.

Sai Life Sciences, backed by private equity, has pursued an aggressive acquisition strategy, buying capabilities rather than building them. They've assembled an impressive portfolio, but integration challenges have kept their margins below 25%. Their focus on small molecules contrasts with Anthem's balanced approach across modalities.

Divi's Laboratories represents a different model—primarily a contract manufacturer of generic APIs with some custom synthesis. Their scale is impressive—₹7,970 crores in revenue—but their capabilities in complex chemistry and biologics lag Anthem's. They're playing a volume game while Anthem pursues value.

The Chinese competition looms large. WuXi AppTec, with revenues exceeding $3 billion, offers similar integrated capabilities but faces increasing geopolitical headwinds. The U.S. BIOSECURE Act, aimed at reducing dependence on Chinese biotechnology companies, has created uncertainty about WuXi's future in American markets. This "China+1" dynamic has been a tailwind for Indian CRDMOs, with Anthem particularly well-positioned given its established U.S. relationships and regulatory track record.

Globally, Anthem's true peers are companies like Cambrex and Recipharm—mid-sized CRDMOs with specialized capabilities. But even here, Anthem's breadth is unusual. Cambrex focuses on small molecules, Recipharm on formulation and finished dosage forms. Anthem's ability to handle everything from discovery to commercial manufacturing across multiple modalities makes direct comparison difficult.

The competitive moat Anthem has built has several layers. First is technical capability—the fermentation capacity, the peptide expertise, the oligonucleotide synthesis. These aren't easily replicated; they require not just equipment but years of accumulated knowledge. When a client needs a complex biotransformation or a difficult peptide synthesis, the list of capable providers globally might be five companies. Being on that shortlist creates pricing power.

Second is regulatory excellence. FDA approval isn't just a checkbox—it's an ongoing commitment to quality systems, documentation, and continuous improvement. Anthem's spotless inspection record over 18 years isn't luck; it's the result of systematic investment in quality infrastructure. New entrants can build facilities, but building this regulatory credibility takes decades.

Third is the customer relationship moat. When Anthem has worked with a biotech from preclinical through Phase III, the switching costs are enormous. The institutional knowledge—every synthetic route attempted, every analytical method developed, every scale-up challenge overcome—can't be transferred to a new provider without significant risk and delay. This stickiness is reflected in their 85%+ customer retention rate.

The industry structure favors incumbents like Anthem. Pharmaceutical companies are reducing their supplier base, preferring to work with fewer, more capable partners rather than managing multiple vendors. This consolidation dynamic benefits integrated players who can handle entire projects rather than specialists who only do piece parts.

But competition is intensifying from unexpected directions. Large pharmaceutical companies, facing patent cliffs and pipeline challenges, are entering the CRDMO space themselves. Novartis's Sandoz division, Sanofi's EUROAPI—these aren't traditional competitors, but they're competing for the same projects. Their advantage is scale and resources; Anthem's is focus and agility.

Technology is also reshaping competition. AI-driven drug discovery companies like Insilico Medicine and Atomwise are developing their own synthesis capabilities. Laboratory automation is reducing the labor advantage that countries like India traditionally enjoyed. Continuous manufacturing is changing the economics of production. Anthem has responded by investing in these technologies themselves, but the landscape is shifting rapidly.

The pricing dynamics in the industry are complex. Unlike generic pharmaceuticals where prices consistently decline, CRDMO pricing for complex projects has remained stable or even increased. This reflects the value of expertise and the cost of failure—when a delayed project can cost hundreds of millions in lost revenue, paying premium prices for reliable execution makes sense.

Anthem's market share in specific segments tells the competitive story. In peptide synthesis for innovative drugs, they're among the top five globally. In integrated projects for small biotechs, they consistently win against much larger competitors. In fermentation-based manufacturing, their capacity leadership in India is unchallenged. They've found profitable niches within the broader market.

The geographic dimension of competition is evolving. While India and China have dominated CRDMO growth for two decades, new locations are emerging. Eastern Europe offers cost advantages and proximity to European markets. Singapore provides regulatory sophistication and government support. The U.S. is even experiencing some reshoring of critical capabilities. Anthem's response has been to double down on India while building commercial presence in key markets.

Looking forward, the competitive landscape will likely consolidate. The increasing complexity of drug development favors players with broad capabilities. The capital requirements for next-generation technologies—cell therapy, gene editing, personalized medicine—will challenge subscale players. Regulatory requirements continue to increase, raising the bar for participation.

Anthem's position in this evolving landscape is strong but not unassailable. Their integrated model and technical capabilities provide differentiation. Their customer relationships and regulatory track record create switching costs. Their capital efficiency and founder leadership enable long-term thinking. But maintaining this position will require continuous investment, constant innovation, and careful navigation of an industry where yesterday's differentiation becomes tomorrow's table stakes.

The ultimate competitive question isn't whether Anthem can compete—they've proven they can. It's whether they can maintain their differentiation as the industry evolves, technologies advance, and competitors adapt. As we'll explore in the playbook section, the lessons from their success so far provide clues to their future trajectory.

X. Playbook: Key Business Lessons

The Anthem story offers a masterclass in building a platform business in a complex, regulated industry. The key lessons transcend pharmaceuticals, providing insights for any entrepreneur or investor thinking about specialized B2B services.

Lesson 1: Full-Stack Integration in Specialized Industries Creates Compound Advantages

The decision to be "full-stack" went against conventional wisdom about focus and specialization. But in industries where projects are complex and iterative, integration creates value that exceeds the sum of parts. When Anthem handles a project from discovery through manufacturing, knowledge accumulates rather than dissipates. Problems solved in development inform manufacturing optimization. Analytical methods created for one phase serve subsequent phases. This isn't just operational efficiency—it's compound learning that makes each subsequent project better than the last.

The integration also changes the customer relationship from vendor to partner. When you own the entire process, you own the outcome. This accountability creates trust, which enables deeper collaboration, which generates better results, which strengthens the relationship further. It's a virtuous cycle that transaction-based models can't replicate.

Lesson 2: Build Platform Capabilities Before Market Demand

Anthem's investment in oligonucleotides, ADCs, and peptides years before these markets materialized seems prescient in retrospect. But it wasn't lucky timing—it was systematic anticipation. They studied academic literature, tracked venture funding, attended conferences, and placed calculated bets on where pharmaceutical development was heading.

This anticipatory building requires patient capital and conviction. The oligonucleotide facility sat underutilized for years. The peptide synthesis capabilities were a drag on margins initially. But when markets turned, Anthem wasn't scrambling to build capabilities—they were ready to capture demand. In platform businesses, being early is expensive but being late is fatal.

Lesson 3: Founder-Led Businesses Navigate Complexity Better

The pharmaceutical industry is Byzantine in its complexity—scientific, regulatory, commercial. Navigating this requires not just expertise but judgment, not just intelligence but wisdom. Founder-leaders bring several advantages: they can make long-term bets without quarterly pressure, they have the credibility to make bold decisions, and they create cultures that reflect their values rather than generic corporate templates.

Bhardwaj's continued involvement 18 years after founding allowed Anthem to maintain strategic consistency while adapting tactically. When others pivoted to follow trends, Anthem stayed the course. When short-term profits beckoned, they invested for the long term. This isn't an argument against professional management—it's recognition that in complex industries, founder wisdom is irreplaceable.

Lesson 4: Customer Concentration Can Signal Value Creation, Not Just Risk

The fact that five customers represent 70% of Anthem's revenue makes some investors nervous. But this concentration reflects the depth of value creation rather than customer dependence. These aren't transactional relationships where customers could easily switch providers. They're deep partnerships where Anthem has become embedded in the customer's development process.

The concentration also enables efficiency. Serving five deep relationships is more profitable than serving fifty shallow ones. The learning from one project with a customer accelerates the next. The trust built over years enables more ambitious collaborations. In B2B platforms, customer concentration done right is a feature, not a bug.

Lesson 5: Timing Markets Requires Preparation Plus Recognition

The GLP-1 boom made Anthem look prescient, but the real lesson is about prepared opportunism. They didn't predict that obesity drugs would become a cultural phenomenon. They recognized that peptides were becoming increasingly important in drug development and built capabilities accordingly. When the market exploded, they were positioned to capitalize not through luck but through preparation.

This pattern—building capabilities for unclear future demand—requires a different mental model than traditional ROI calculations. You're not betting on specific outcomes but on general directions. You're creating options, not obligations. And when those options become valuable, the returns justify all the failed bets you made along the way.

Lesson 6: Capital Efficiency Comes From Leverage, Not Starvation

Anthem reached unicorn status without external funding, but this wasn't through extreme frugality. They invested heavily in infrastructure, technology, and people. The efficiency came from leverage—using the same capabilities across multiple customers, the same infrastructure for different modalities, the same expertise for various projects.

This is different from the blitzscaling model of throwing capital at growth. It's about finding the minimum viable investment that creates maximum optionality. The fermentation capacity serves both small molecules and biologics. The analytical lab supports all projects. The quality systems apply everywhere. Every investment does double or triple duty.

Lesson 7: Technical Depth Trumps Breadth in Complex Industries

While Anthem built broad capabilities, they went deep in specific areas. Their fermentation capacity isn't just large—it's flexible and sophisticated. Their peptide synthesis isn't just available—it's world-class. This depth creates defensibility that breadth alone cannot.

In complex B2B services, customers don't just want capability—they want expertise. They want partners who know more about specific aspects than they do themselves. This requires choosing battles carefully. Anthem couldn't be world-class at everything, so they picked areas where complexity created value and went deeper than anyone else.

Lesson 8: Culture Is Strategy in Knowledge Businesses

The "scientific entrepreneurship" culture Anthem cultivated wasn't just about employee satisfaction—it was strategic. When scientists feel ownership over projects, quality improves. When they're encouraged to innovate, processes get better. When knowledge is shared freely, capabilities compound.

This culture can't be copied through corporate initiatives or consultant frameworks. It emerges from founder values, gets reinforced through hiring, and becomes self-sustaining through success. In knowledge-intensive businesses, culture isn't soft stuff—it's the hardest competitive advantage to replicate.

Lesson 9: Regulatory Excellence Is a Moat, Not a Cost

Most companies view regulatory compliance as a necessary evil—cost to be minimized. Anthem viewed it as competitive advantage to be maximized. Their spotless FDA record wasn't just about avoiding problems—it became a selling point that justified premium pricing.

In regulated industries, the temptation is to do the minimum required. But excellence in regulatory matters creates trust with both regulators and customers. It reduces friction in every interaction. It enables faster approvals and smoother inspections. Over time, this compounds into a reputation that becomes invaluable.

Lesson 10: Platform Effects Emerge at System Level

The real power of Anthem's model isn't in any individual capability but in how they work together. The knowledge from one project improves the next. The customer won through peptide synthesis stays for oligonucleotides. The analytical method developed for one molecule finds application in another.

These platform effects weren't designed—they emerged. But once recognized, they can be cultivated. Hiring decisions consider not just project needs but knowledge building. Investments evaluate not just direct returns but spillover benefits. Customer relationships focus not just on current projects but future possibilities.

Looking at these lessons collectively, a meta-principle emerges: in complex industries, winning requires playing a different game than competitors. While others optimized for efficiency, Anthem optimized for capability. While others focused on execution, Anthem emphasized innovation. While others managed transactions, Anthem built relationships. The playbook isn't about doing the same things better—it's about doing fundamentally different things.

XI. Bull vs. Bear Case

The Bull Case: A Platform for the Future of Pharma

The optimistic view on Anthem starts with secular tailwinds that seem almost too good to be true. Global pharmaceutical R&D spending is approaching $250 billion annually and growing at 5-6% per year. More importantly, the share of this spending going to outsourced partners is increasing from 30% today to an estimated 45% by 2030. That's roughly $50 billion in incremental outsourcing opportunity, and Anthem is perfectly positioned to capture disproportionate share.

The shift toward complex modalities plays directly to Anthem's strengths. Traditional small molecule drugs are giving way to biologics, cell therapies, gene therapies, and other sophisticated approaches. These require exactly the kind of integrated capabilities Anthem has built. While competitors scramble to add biologics to their chemistry capabilities or vice versa, Anthem already operates seamlessly across modalities.

The small biotech focus that seemed risky a decade ago now looks prescient. These companies, funded by increasingly sophisticated venture capital, are driving pharmaceutical innovation. They need partners who can handle their entire development program, not just discrete tasks. Anthem's success-based model and technical depth make them the ideal partner for these innovation engines.

Geopolitical dynamics create additional opportunity. The U.S.-China tensions have made American companies wary of Chinese CRDMOs. The BIOSECURE Act could force wholesale shifts in supply chains. European companies are similarly seeking to diversify away from China. India, with its democratic governance, English-speaking workforce, and established pharmaceutical industry, is the natural beneficiary. And within India, Anthem's regulatory track record and customer relationships position them to capture more than their fair share.

The GLP-1 opportunity is still in early innings. Current drugs are just first-generation—the pipeline includes oral formulations, combination therapies, and next-generation agonists with better efficacy and fewer side effects. The market could reach $150 billion by 2032. Even a small share of manufacturing and development for these drugs represents massive revenue opportunity for Anthem.

Financial metrics support the bullish outlook. Revenue growth of 30% annually is exceptional for a company of Anthem's size. EBITDA margins approaching 37% suggest pricing power that comes from true differentiation. Return on equity exceeding 20% indicates efficient capital deployment. These aren't metrics of a commodity service provider—they're the hallmarks of a differentiated platform.

The capacity expansion underway extends the growth runway. Adding 40,000 liters of fermentation capacity, building dedicated facilities for cell and gene therapy, establishing U.S. operations—each investment opens new markets and customers. The company could double revenue over the next 3-4 years without stretching operational capabilities.

Perhaps most compelling is the platform nature of the business. Each new capability enables others. Each customer relationship deepens over time. Each project adds to institutional knowledge. This isn't linear growth—it's compound expansion where the business gets stronger as it gets larger.

The Bear Case: Concentration, Competition, and Cycles

The skeptical view starts with customer concentration. Five customers representing 70% of revenue is precarious regardless of relationship depth. If even one of these customers faces clinical trial failures, funding challenges, or strategic changes, Anthem's revenue could drop precipitously. The biotech industry is inherently volatile—companies fail, get acquired, or pivot strategies regularly.

Working capital requirements are concerning. At 222 days, Anthem has significant capital tied up in operations. This limits flexibility and could become problematic if growth slows or customers delay payments. The comparison with Syngene's 34 days is stark and suggests operational inefficiencies that margin metrics don't capture.

Competition is intensifying from multiple directions. Chinese CRDMOs, despite geopolitical challenges, aren't disappearing—they're adapting, building facilities in other countries, and offering aggressive pricing. Other Indian players are copying Anthem's integrated model. Global giants have resources to build whatever capabilities they lack. The moats that seem strong today could erode quickly.

The valuation multiple of 23x earnings seems stretched for a services business, regardless of growth rates. If growth slows even modestly, multiple compression could drive significant stock price declines. The post-IPO run-up may have pulled forward years of appreciation, leaving limited upside for new investors.

Technological disruption poses medium-term risks. AI-driven drug discovery could reduce the need for traditional development services. Continuous manufacturing could obsolete batch production infrastructure. Laboratory automation could eliminate the labor arbitrage that benefits Indian companies. Anthem is investing in these technologies, but they're playing catch-up rather than leading.

The founder dependence is a double-edged sword. While Bhardwaj's leadership has been instrumental in building Anthem, the company's trajectory seems inseparable from his involvement. He's 68 years old. Succession planning hasn't been clearly articulated. The transition from founder-led to professionally managed could be rocky.

Regulatory risks lurk beneath the surface. A single FDA warning letter could damage the pristine reputation Anthem has built over 18 years. As they handle more complex projects with higher stakes, the probability of something going wrong increases. The pharmaceutical industry is littered with CRDMOs that stumbled on regulatory issues and never fully recovered.

Market cycles are inevitable. Pharmaceutical R&D spending, while growing long-term, goes through periods of retrenchment. Biotech funding is notoriously cyclical. A prolonged downturn in venture funding could devastate the small biotech customers that drive Anthem's growth. The company hasn't been tested through a severe industry downturn.

The GLP-1 tailwind could reverse. Safety concerns, though unlikely, could emerge. Competitive dynamics could drive pricing pressure. The gold rush mentality could lead to overcapacity across the industry. Anthem's success in this area could become a liability if the market dynamics shift.

The Balanced View

Reality likely lies between these extremes. Anthem has built something genuinely differentiated in the CRDMO space, with capabilities, relationships, and culture that create sustainable competitive advantages. The secular trends toward outsourcing and complex modalities provide multi-year growth tailwinds.

But the risks are real. Customer concentration needs to be reduced. Working capital management must improve. Competition will intensify. Valuation multiples will likely compress from current levels.

For investors, the question isn't whether Anthem is a good company—it clearly is. The question is whether it's a good investment at current valuations given the risk profile. The answer depends on time horizon, risk tolerance, and belief in the sustainability of Anthem's differentiation.

The bull case requires everything to go right—continued innovation, flawless execution, favorable industry dynamics. The bear case needs just one or two things to go wrong—a major customer loss, a regulatory stumble, a funding drought in biotech. As with most investments, the outcome will likely be determined by factors that aren't yet visible.

XII. Looking Forward: The Next Decade

Standing at the construction site of Anthem's Unit III facility in early 2025, watching steel beams rise against the Bangalore skyline, it's hard not to wonder what this complex will be manufacturing in 2035. Will it be producing components for CRISPR therapies that edit genes in vivo? Manufacturing the lipid nanoparticles that deliver mRNA vaccines for cancer? Or synthesizing molecules we can't yet imagine for diseases we haven't yet characterized?

The next decade in pharmaceuticals promises to be more transformative than the last three combined. The convergence of artificial intelligence, genomics, and advanced manufacturing technologies is creating possibilities that sound like science fiction. For Anthem, this represents both extraordinary opportunity and existential challenge—how do you prepare for a future that's accelerating beyond prediction?

The immediate expansion plans are concrete and strategic. Unit III will add 50,000 liters of fermentation capacity, but more importantly, it's designed for flexibility—able to switch between bacterial, yeast, and mammalian cell culture with minimal downtime. The facility incorporates single-use technologies that reduce contamination risk and enable rapid changeovers. It's not just more capacity; it's more adaptable capacity.

The cell and gene therapy initiative represents Anthem's biggest bet yet. These therapies require entirely different manufacturing paradigms—working with living cells rather than chemical reactions, managing chain-of-custody for patient-specific treatments, maintaining ultra-cold supply chains. The infrastructure investment exceeds ₹200 crores, but the real investment is in expertise—hiring scientists from leading cell therapy companies, partnering with academic institutions, building knowledge in an entirely new domain.

The U.S. facility, planned for 2026, isn't about manufacturing—it's about proximity. American biotech companies increasingly want partners who can provide local support, attend meetings in person, and respond to urgent requests in real-time. The facility will house development laboratories, analytical capabilities, and crucially, regulatory and project management teams who understand the FDA intimately.