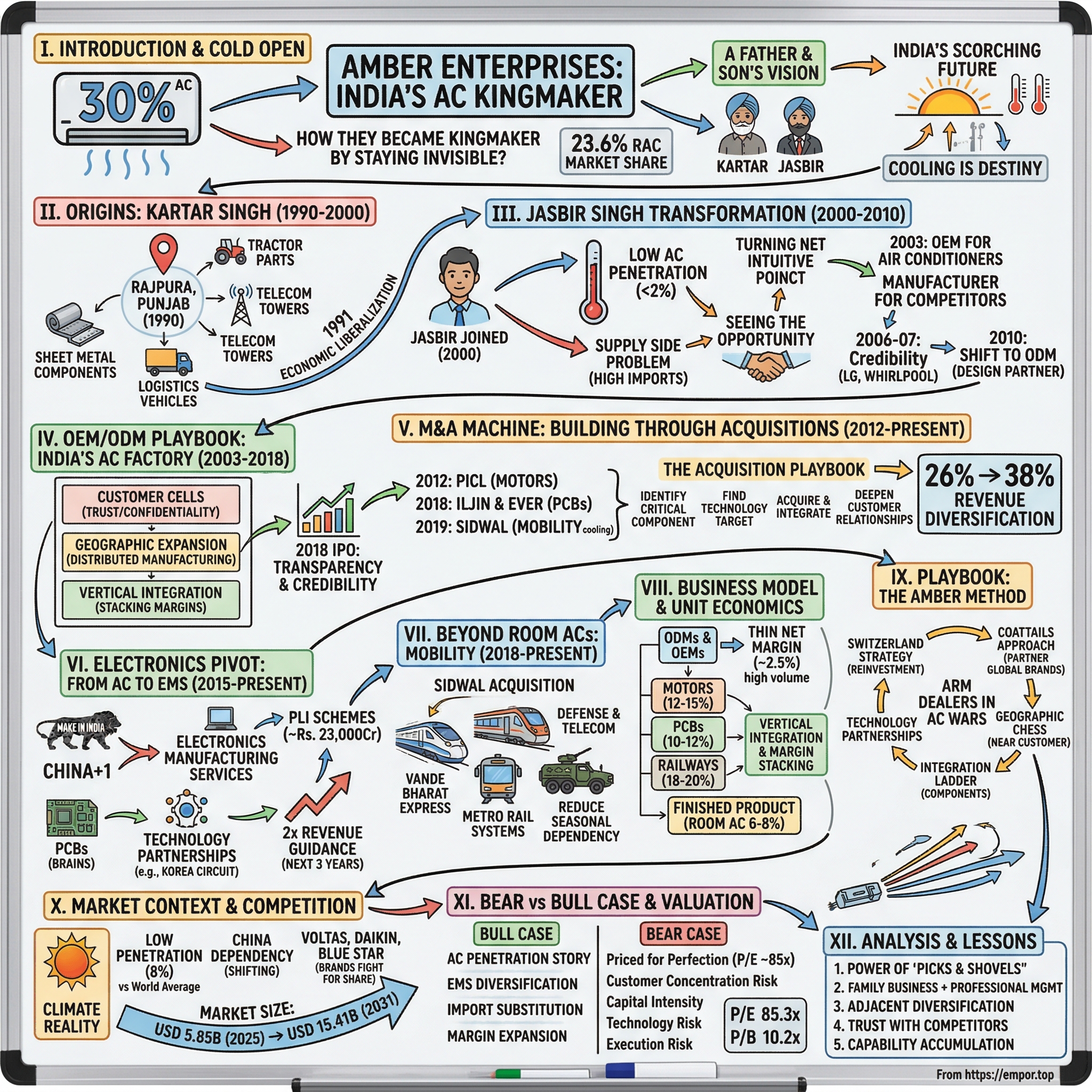

Amber Enterprises: The Air Conditioning Empire Nobody Knows About

I. Introduction & Cold Open

Picture this: You walk into an electronics store in Delhi during peak summer. The salesperson shows you air conditioners from LG, Voltas, Blue Star, Whirlpool, Panasonic. Different brands, different price points, different features. What he doesn't tell you—what he probably doesn't even know—is that there's a 30% chance that whichever brand you choose, the actual air conditioner was manufactured by the same company. A company you've never heard of.

That company is Amber Enterprises India Limited, and it's one of the most fascinating business stories in modern India. With a 23.6% share of India's total Room Air Conditioner market, Amber manufactures for virtually every major AC brand in the country. Yet walk up to any consumer and ask them about Amber—blank stares. This is by design.

How did a sheet metal component maker from Punjab become India's air conditioning kingmaker? How did a family business that started making tractor parts transform into a ₹23,475 crore market cap enterprise that's now pivoting into electronics manufacturing? And perhaps most intriguingly—in a country where brand consciousness runs deep, how did they build an empire by deliberately staying invisible?

The Amber story isn't just about air conditioners. It's about timing market transitions, the art of being everyone's supplier while competing with no one, and recognizing that in India's scorching future, cooling isn't a luxury—it's destiny. It's about a father who saw opportunity in metal sheets and a son who saw the future in rising temperatures. It's about building trust with competitors, backward integrating relentlessly, and knowing when to pivot from hardware to electronics.

This is also a story about India itself—about what happens when a country with 1.4 billion people and rising incomes meets climate change. When only 8% of households have air conditioners compared to 90% in developed nations, you're not looking at a market—you're looking at an inevitability.

What makes Amber particularly fascinating for investors is how they've positioned themselves. They're not betting on which AC brand will win. They're betting that India will need cooling, period. They're the arms dealers in the AC wars, and as any student of history knows, arms dealers tend to do quite well.

Over the next several hours, we'll trace Amber's journey from those early days in Rajpura to becoming India's largest AC original design manufacturer. We'll explore their acquisition playbook, their pivot into electronics, their expansion into mobility cooling. We'll examine why they don't pay dividends despite being profitable, why their P/E ratio sits at 85.3, and what their recent ₹2,500 crore fundraising plans tell us about their ambitions.

But first, let's go back to 1990s Punjab, where a man named Kartar Singh was about to make a decision that would eventually cool millions of Indian homes.

II. Origins: The Kartar Singh Story & Early Years (1990-2000)

The train from Delhi to Rajpura takes about four hours, winding through the agricultural heartland of Punjab. In 1990, Rajpura was the kind of place ambitious young engineers left, not where they built factories. Population: barely 80,000. Main industries: agriculture and small-scale manufacturing. Notable features: a railway junction and proximity to Chandigarh. Not exactly Silicon Valley.

But Kartar Singh saw something different. Where others saw a sleepy Punjab town, he saw strategic geography—close enough to Delhi-NCR for business, far enough for lower costs, and sitting in the heart of Punjab's emerging industrial corridor. In 1990, he incorporated what would become Amber Enterprises, though the factory wouldn't start operations until 1994.

The early 1990s were a peculiar time to start a manufacturing business in India. The country was emerging from the License Raj—that Byzantine system of permits and quotas that had strangled Indian enterprise for decades. In 1991, Finance Minister Manmohan Singh opened up the economy, but nobody quite knew what that meant yet. Foreign brands were trickling in. Indian companies were learning to compete. The rules were being rewritten in real-time.

Kartar Singh's initial vision was straightforward: make sheet metal components. Not glamorous, but essential. Every tractor needed them. Every light commercial vehicle needed them. Even the emerging telecommunications industry—those massive telecom towers sprouting across India—needed sheet metal fabrication. It was picks-and-shovels thinking before anyone called it that. The Rajpura factory that opened in 1994 wasn't much to look at—basic sheet metal fabrication equipment, a modest workforce, typical industrial shed construction. But it represented something important: Kartar Singh, a first generation entrepreneur, had founded the company in 1992 and was building something from scratch at a time when most Indian businesses were still family trading houses or government-linked enterprises.

What's particularly interesting about Kartar's approach was his focus on industrial customers rather than consumer brands. This B2B orientation would become part of Amber's DNA—even today, most consumers have never heard of them despite their massive market presence. In those early years, the customer list read like a who's who of Indian industry: tractor manufacturers who needed precision-bent metal components, telecom companies rolling out towers across rural India, light commercial vehicle makers serving the growing logistics sector.

The telecom connection is worth dwelling on. The mid-1990s saw India's telecom revolution begin—private operators entering, mobile services launching, towers sprouting everywhere. Each tower needed sheet metal work for equipment housing, cable trays, structural components. It wasn't sexy work, but it was steady, growing, and taught Amber something crucial: how to scale manufacturing quickly to meet sudden demand surges.

By the late 1990s, Amber had established itself as a reliable component supplier, but it was still essentially a job shop—taking orders, bending metal, shipping parts. The real transformation would come when Kartar's son returned from business school with fresh eyes and a very different vision. The company had survived India's economic liberalization. Now it was time to see if it could thrive in it.

III. The Jasbir Singh Transformation: Seeing the AC Opportunity (2000-2010)

Jasbir Singh joined in 2000 after completing his Master of Business Administration, and his first assignment from his father was straightforward: find new markets for their sheet metal capabilities. What he discovered would reshape not just Amber, but India's entire air conditioning industry.

One key task Jasbir received shortly after joining was to help the company expand into new verticals. As part of those efforts, he found a market for Amber's sheet metal parts in window-mounted air conditioners. It was this discovery that led him to a realisation that would totally transform the company.

The realization was stunning in its simplicity: Twenty years ago, very few people in India had air conditioning in their homes, despite the fact most of the country has a tropical climate with extremely hot summers. India had one of the lowest AC penetration rates of any major economy—less than 2% of households. In a country where summer temperatures routinely crossed 45°C, this wasn't just a market opportunity; it was an inevitability waiting to happen.

But here's where Jasbir's insight went deeper. He didn't just see the demand side of the equation. He saw the supply side problem. Most AC brands in India were either importing completely built units (expensive) or importing key components for assembly (still expensive). The sheet metal work—the housing, the structural components—was one of the few things being done locally. If Amber could move up the value chain from components to complete units, they could offer brands something revolutionary: locally manufactured ACs at price points that could unlock the mass market.

The transformation didn't happen overnight. He started out as a manager, but he quickly rose through the ranks to become General Manager before being promoted to Director, then to his current role. As he climbed the corporate ladder, he was simultaneously rebuilding the company's capabilities from the ground up.

In 2003, Amber took the leap—becoming an original equipment manufacturer (OEM) for air conditioners. This meant they weren't just supplying parts anymore; they were building complete AC units for brands to sell under their own labels. The business model was counterintuitive: become the manufacturer for your competitors. But in India's fragmented AC market, where brands were focused on marketing and distribution rather than manufacturing, it made perfect sense.

The early OEM years were about learning—understanding refrigeration cycles, managing coolant systems, dealing with compressors, ensuring quality control at a completely different level than sheet metal work required. Amber essentially ran a university inside its factories, training workers who had never seen an AC's internals to build units that would carry premium brand names.

By 2006-2007, Amber had gained enough credibility to attract serious customers. LG, the Korean giant that was rapidly gaining market share in India, became a client. Then came Videocon, Godrej, Whirlpool. Each new customer brought volume, but also knowledge—about quality standards, about design preferences, about cost optimization.

What's remarkable about this period is how Jasbir managed to convince competing brands to use the same manufacturer. The pitch was elegant: Amber would maintain complete confidentiality between clients, run separate production lines, and never launch its own consumer brand. They would be Switzerland in the AC wars—neutral, reliable, and completely trustworthy.

By 2010, Amber had developed enough expertise and confidence to start designing its own models—not to sell under an Amber brand, but to offer as ready-made designs to brands who wanted to enter the AC market quickly. This shift from OEM (Original Equipment Manufacturer) to ODM (Original Design Manufacturer) was crucial. Now Amber wasn't just a factory; it was a product development partner.

The numbers tell the transformation story: from making sheet metal components for a few thousand AC units in 2000 to manufacturing complete ACs with capacity for hundreds of thousands of units by 2010. But the real transformation was in capability—from a component supplier to a full-solution provider, from a vendor to a partner, from following specifications to setting them.

IV. The OEM/ODM Playbook: Becoming India's AC Factory (2003-2018)

The conference room at LG's Noida office in 2004 must have been an interesting scene. On one side, Korean executives from one of the world's largest electronics companies. On the other, representatives from a Punjab-based component maker nobody had heard of. LG needed local manufacturing to hit price points for the Indian market. Amber needed volume to justify its investments in AC manufacturing. What emerged from those negotiations would become the template for Amber's entire business model.

The OEM/ODM model that Amber perfected is worth understanding in detail because it's so counterintuitive. In most industries, manufacturers dream of building their own brands. Amber went the opposite direction—they would manufacture for everyone but compete with no one. As part of our journey, we saw that the air conditioners that are not being manufactured by us still need critical components like heat exchangers, motors, electronic printed circuit boards and sheet metal injection moulding. So we decided we could be a good supplier if we diversified our geographic presence for the component section.

Here's how the model worked: A brand like Voltas or Blue Star would approach Amber with requirements—capacity needs, price points, basic specifications. Amber would then either manufacture to the brand's design (OEM) or offer its own designs that the brand could customize (ODM). Amber handled everything from procurement to production to quality testing. The brand handled marketing, distribution, and after-sales service.

The genius was in the details. Amber maintained what they called "customer cells"—dedicated teams for each brand that operated almost like independent businesses within Amber. The Whirlpool team didn't know what the Godrej team was doing. Production lines were separated. Even senior management meetings had protocols about what information could be shared when.

This paranoid approach to confidentiality wasn't just about keeping customers happy—it was about building trust in a trust-deficit environment. Indian businesses, especially family-run ones, are notoriously suspicious of partners. By being almost obsessively confidential, Amber removed the biggest barrier to outsourcing.

The geographic expansion strategy during this period was equally clever. Instead of building massive centralized plants, Amber built multiple facilities near its customers' locations. A plant near Pune for the western market, facilities in the north for Delhi-NCR demand, expansion in the south as that market grew. This distributed manufacturing approach reduced logistics costs but more importantly, it made Amber indispensable. When you have a dedicated plant near a customer's warehouse, switching to another supplier becomes much harder.

Currently, the company has a market share in the RAC industry representing 29%. But this number understates Amber's true influence. Because they manufacture for multiple competing brands, Amber essentially sets the quality and cost benchmarks for the entire industry. When Amber improves its efficiency, the entire Indian AC market becomes more competitive.

The component business evolved in parallel with the OEM business, creating powerful synergies. The company also manufactures components for other consumer durables, including refrigerators, microwaves and washing machines, and it specialises in sheet metal, heat exchangers, motors, electrical and plastic injection moulding components, and vacuum forming for the automobile and metal ceiling industries. This wasn't just diversification—it was strategic vertical integration.

Consider heat exchangers—the critical component that transfers heat in an AC. By manufacturing these in-house, Amber not only captured more value but also gained supply chain control. When copper prices spiked (copper tubes are essential for heat exchangers), Amber could manage costs better than competitors who relied on external suppliers. When there were quality issues, they could fix them immediately rather than fighting with vendors.

The 2018 IPO marked the culmination of this phase. Amber went public at ₹896 per share, raising capital to fund further expansion. But more than money, the IPO brought transparency and credibility. Public market scrutiny meant better governance, audited financials, and regular disclosures—all things that made global brands more comfortable working with Amber.

By 2018, Amber had built nine production facilities across six locations. They were manufacturing for every major AC brand in India. They had integrated backward into components and forward into design. The boy from Punjab who had discovered the AC opportunity in 2000 had built India's largest AC OEM/ODM player. But Jasbir Singh wasn't done. The next phase would be about building through acquisitions.

V. The M&A Machine: Building Through Acquisitions (2012-Present)

The boardroom at Amber's Gurugram headquarters in 2012 marked a turning point. For the first time, Jasbir Singh wasn't talking about organic growth or new customers. He was talking about buying a company. The first of those acquisitions was in 2012, when Amber Enterprises bought PICL, an electrical motor manufacturing company.

PICL (now PICL India Private Limited) wasn't a random choice. Motors are the heart of any AC—they drive the compressor, power the fans, circulate the air. By acquiring PICL, Amber wasn't just buying a supplier; they were internalizing a critical technology. The integration was smooth because PICL's culture matched Amber's—engineering-focused, cost-conscious, quietly competent.

But the real acquisition spree came after the 2018 IPO, when Amber had both capital and currency (listed shares) to pursue targets. The second acquisition was of Iljin, an Indian manufacturer of printed circuit boards for home appliances, automobiles and other machines. Next, the company bought Ever Electronics, another printed circuit boards producer.

The Iljin and Ever Electronics acquisitions in 2018 were particularly strategic. Printed Circuit Boards (PCBs) are the brains of modern ACs—controlling temperature, managing power, enabling smart features. With the shift from basic ACs to inverter ACs (which adjust compressor speed for efficiency), PCB complexity and value were increasing dramatically. By acquiring these companies, Amber was positioning itself for the electronics revolution in air conditioning.

Most recently, it acquired Sidwal, which has expertise in producing air conditioners in the mobility space, meaning cooling devices for public transport. The Sidwal acquisition in 2019 deserves special attention because it represented Amber's first major diversification beyond room ACs. Sidwal was India's leader in railway and metro air conditioning—a completely different business with different customers (Indian Railways, metro corporations), different product cycles (years, not seasons), and different margins (higher, given the customization required).

With this acquisition, Amber has expanded its product offering to heating ventilation air conditioning (HVAC) solution and expanded its customer reach towards Indian Railways, Metros, Bus air-conditioning, defence, telecom and commercial refrigeration. As per the management, this brings synergies as (a) direct entry to a product segment which has high entry barrier of more than 5 years (b) reduce seasonal dependency on room air conditioning business (c) better bargaining power for outsourcing raw materials as its same for both and lastly (d) margin accretive as Sidwals EBITDA margin are 18% vs Amber's ~8%.

What made Sidwal particularly attractive was its order book visibility. Unlike room ACs, which are sold seasonally to consumers, railway ACs are ordered years in advance through government tenders. Our order book stands healthy at more than around Rs.450 Crores... with that total order book now stands at Rs. 350 crore to be executed in 24 months.

The acquisition playbook that emerged from these deals was sophisticated. First, identify a critical component or adjacent market. Second, find a company with strong technology but perhaps weak finances or limited growth capital. Third, acquire and integrate quickly, maintaining the target's technical team while applying Amber's operational excellence. Fourth, use the acquisition to deepen relationships with existing customers—"we can now offer you motors/PCBs/railway ACs too."

With this acquisition, revenue contribution of components and other business has increased from 26% (FY17) to 38% (FY20). This shift was deliberate—reducing dependence on the seasonal room AC business while maintaining the synergies of the cooling ecosystem.

The integration philosophy was equally important. Unlike many Indian conglomerates that impose their culture on acquisitions, Amber maintained subsidiary independence where it made sense. Sidwal kept its brand and customer relationships in the railway sector. Iljin maintained its technology partnerships. PICL continued serving non-AC customers. This federated structure allowed Amber to be both big (in purchasing power and financial strength) and small (in customer responsiveness and technical specialization).

Recent moves show the M&A machine isn't slowing down. The company has been exploring international acquisitions, including discussions around Unitronics in Israel for advanced electronics capabilities. They've also signed agreements to acquire stake in Resojet Private Limited for washing machine manufacturing—suggesting Amber's ambitions now extend beyond just cooling.

But perhaps the most interesting development is the potential monetization of these acquisitions. Amber Enterprises is in talks with private equity investors for a stake sale in its subsidiary ILJIN Electronics, while it may also look at a public listing of the entity along with pre-IPO placements. The monetisation strategy is being finalised for the subsidiary as it expands its electronics components manufacturing facilities, which will require significant investments.

This suggests a new phase in Amber's M&A strategy—not just acquiring and integrating, but potentially creating value through financial engineering, spinning off mature subsidiaries to fund new growth areas. The student has become the teacher in India's corporate M&A game.

VI. The Electronics Pivot: From AC to EMS (2015-Present)

The year 2015 marked an inflection point. China's manufacturing costs were rising. Global brands were rethinking their supply chains. The Indian government was launching "Make in India." And Amber, sitting on decades of manufacturing expertise and recently acquired electronics capabilities, saw an opportunity bigger than air conditioners.

Through its subsidiaries IL JIN Electronics and Ascent Circuits, Amber Group is a prominent leader in the Electronics Manufacturing Services (EMS) sector and is recognised for its solutions across industries such as consumer durables, automotive, telecom, industrials, hearable / wearable, & Defence. This wasn't a pivot away from ACs—it was a recognition that the skills needed to manufacture AC electronics could be applied to almost any electronic product.

The transformation started with printed circuit boards. After acquiring Iljin and Ever Electronics, Amber had PCB assembly capabilities. But assembly is just one part of the electronics value chain. The real value—and the real moat—comes from manufacturing the PCBs themselves. That's where the technology barriers are highest and where China had the strongest grip on global supply.

The Amber Group, through its subsidiary IL JIN Electronics, and Korea Circuit will own 70% and 30%, respectively, of the joint venture... "This collaboration will further strengthen the offering of recently acquired Ascent Circuit portfolio (and) marks the revolutionary progression of Amber Group into a leading full stack backward integrated EMS company," Jasbir Singh, Executive Chairman and CEO of Amber Group, said.

The Korea Circuit partnership announced in 2024 was particularly strategic. Korea Circuit brings 45 years of PCB manufacturing expertise—the kind of deep process knowledge that takes decades to develop. They manufacture everything from basic single-sided PCBs to complex HDI (High Density Interconnect) boards used in smartphones and semiconductor substrates.

But technology partnerships alone don't build an electronics empire. You need scale, and that requires capital. Enter the Production Linked Incentive (PLI) schemes. The Ministry of IT has finalised a Production Linked Incentive (PLI) scheme aimed at boosting the manufacturing of electronic components in India. With an allocation of ~Rs. 23,000 crores, the government was essentially subsidizing the creation of a domestic electronics manufacturing ecosystem.

Amber's response was bold. Indian company Amber Enterprises may invest 20 billion INR ($267M) in a PCB manufacturing facility in the country. But the real ambition was even larger—plans for a ₹6,000 crore electronics plant near Noida airport, targeting everything from consumer electronics to automotive applications.

The anti-dumping duties imposed by India on PCB imports from China and Hong Kong created a perfect storm of opportunity. Amber Enterprises has also gained significant traction in its electronics business, particularly due to the imposition of anti-dumping duties (ADD) on printed circuit boards (PCBs). This has allowed the company to acquire new clients and expand its customer base.

What's fascinating about Amber's EMS strategy is how it leverages their AC relationships while expanding far beyond them. Electronic division has also been consistently diversifying its product mix from only consumer durables to varied sectors like automobiles, hearables and wearables, IT and telecom, Industrial and others. A company that started with AC brands like LG and Whirlpool now manufactures for automotive companies, telecom equipment makers, even defense contractors.

The numbers tell the transformation story. Amber has set ambitious growth targets, maintaining a 2x revenue guidance for the division over the next three years. This goal is supported by a robust order book exceeding Rs 20 bn and ongoing product portfolio expansion. From being an AC company with some electronics capabilities, Amber is transforming into an EMS player that also happens to make ACs.

The strategic logic is compelling. Electronic content in products is only increasing—cars are becoming computers on wheels, appliances are getting smart, even basic products now have electronic controls. By building deep electronics capabilities, Amber isn't just serving today's market; they're positioning for a future where everything has a PCB inside.

But perhaps the most interesting aspect of the electronics pivot is what it means for margins and capital efficiency. Unlike AC manufacturing, which is seasonal and working capital intensive, EMS can provide year-round revenue with faster cash conversion. Different products, different seasons, but the same underlying manufacturing capabilities.

The recent acquisition discussions around Unitronics (Israel) and partnerships with companies like Power-One show that Amber's electronics ambitions are global. They're not content being India's EMS player; they want to be a global electronics manufacturer that happens to be based in India.

VII. Beyond Room ACs: Mobility & New Frontiers (2018-Present)

The platform at New Delhi Railway Station is a study in contrasts. In the general compartments, passengers sweat through the journey, windows open, fans struggling. In the AC coaches, it's a different world—climate-controlled comfort at 24°C, regardless of the 45°C heat outside. What most passengers don't know is that the company keeping them cool likely isn't the railways itself, but a Faridabad-based company that's been in the mobility cooling business since 1974.

THE COMPANY IS INTO THE SEGMENT OF AIR-CONDITIONING AND REFRIGERATION FOR MOBILITY APPLICATIONS SINCE 1974 AND HAS GROWN STEADILY ON ACCOUNT OF HIGH-QUALITY PRODUCTS & SERVICEs. Sidwal, acquired by Amber in 2019, brought with it something invaluable—45 years of experience cooling things that move.

The acquisition timing was perfect. India was in the midst of a railway modernization drive. The Vande Bharat trains were being rolled out. Metro systems were expanding beyond Delhi to tier-2 cities. The government was pushing for 100% electrification and air-conditioned coaches. SIDWAL pioneered the all-indigenous development of Roof Mounted Modular Compact Air Conditioner for Rail Coaches in 1991. Since then SIDWAL has supplied more than 30,000 such AC Units duly tested and approved by Research Design & Standards Organization (RDSO), Ministry of Railways, Government of India for higher speed trains like Vande Bharat Express, Shatabdi Express, Rajdhani Express for Indian Railways.

What makes mobility cooling fundamentally different from room ACs is the engineering challenge. A train compartment experiences constant vibration, extreme temperature variations, dust, and needs to cool a space that's constantly exchanging air with the outside. The power supply fluctuates. The unit needs to work at different altitudes. It's not just about cooling; it's about engineering resilience.

Pioneering indigenous development of Heating Ventilation and Air Conditioning Unit for Metro Coaches in the year 2004 we have supplied more than 3200 HVACs for metro coaches such as Delhi Metro, Jaipur Metro, Metro Railway, Kolkata, CRRC China and Mumbai Metro, RRTS etc. The metro opportunity was particularly attractive because unlike Indian Railways, which has its own manufacturing units, metro corporations prefer to outsource.

The numbers tell the story of India's urban rail explosion. In 2006, the National Urban Transport Policy had proposed the construction of a metro rail system in every city with a population of at least 20 lakh (2 million) people. From 2002 to 2014, the Indian metro infrastructure expanded by 248 km. Each kilometer of metro means multiple coaches. Each coach needs HVAC. And Sidwal-Amber was positioned to capture this demand.

But Sidwal brought more than just railway expertise. The company has a state-of-the-art manufacturing facility based in Faridabad, Haryana where it produces world class products for Railways, Metros, Buses, and Telecom application. The telecom application is particularly interesting—cooling for mobile towers and data centers, markets that are exploding as India digitizes.

The defense angle adds another dimension. Sidwal is selected for the supplies of CAB AC for Prestigious WAG 10 lR project. Military applications require even higher standards—equipment that can work in Ladakh's -40°C winters and Rajasthan's 50°C summers. The margins are higher, the contracts are longer, and once you're approved, switching costs are prohibitive.

Sidwal has entered into ToT and partners M/s. Ultimate Europe Transportation Equipment GmbH for the localization and supply of Gangway and Door System for Railway and Metro Coaches. Currently, Sidwal has been awarded for the supply of Gangway System by ALSTOM for Chennai Mero Phase II Project. This expansion beyond just HVAC into gangways (the connectors between train cars) and doors shows Amber's ambition—to become a comprehensive supplier for rolling stock, not just the cooling provider.

The bus AC market represents another frontier. As state transport corporations modernize their fleets and private operators launch premium services, the demand for bus air conditioning is surging. Unlike trains, which are ordered by government entities in large batches, the bus market is more fragmented but also more dynamic.

What's particularly clever about the mobility strategy is how it hedges against the room AC business's seasonality. Railway and metro orders are placed year-round. Defense contracts span multiple years. While room AC sales spike in summer, mobility cooling provides steady revenue through the year.

The recent partnerships with global players like Alstom (French rolling stock manufacturer) and expansion into projects like Chennai Metro Phase II show that Amber-Sidwal isn't just serving Indian demand—they're becoming part of global supply chains. When Alstom wins a metro contract anywhere in Asia, Amber could potentially supply the cooling systems.

Pioneered and supplied HVACs for first two rakes of Vande Bharat Train 18 produced by ICF—this single line captures why mobility matters. The Vande Bharat is India's indigenous semi-high-speed train, a prestige project. Being the cooling provider for such projects isn't just about revenue; it's about establishing credibility for future high-value contracts.

VIII. Business Model & Unit Economics

The conference room at a Mumbai private equity firm. Amber's CFO is explaining their business model to potential investors. "We're not in the AC business," he says. "We're in the working capital arbitrage business that happens to make ACs." It's a provocative statement, but the numbers back it up.

Let's start with the basics. Amber operates on an ODM (Original Design Manufacturer) and OEM (Original Equipment Manufacturer) model. In simple terms, they design and manufacture products that other companies sell under their own brands. The economics of this model are counterintuitive but powerful.

Revenue sits at ₹11,021 Cr with profits of ₹282 Cr, which translates to a net margin of roughly 2.5%. That might seem thin, but it's the nature of contract manufacturing. You're not capturing the brand premium; you're capturing the manufacturing efficiency premium. And when you're manufacturing at Amber's scale, even thin margins generate substantial absolute profits.

The real story is in the capital efficiency. Debtor days have improved from 80.7 to 64.0 days. This improvement might seem minor, but at Amber's scale, reducing debtor days by 16 days frees up hundreds of crores in working capital. That's capital that can be deployed for expansion rather than sitting in receivables.

Company has a low return on equity of 9.00% over last 3 years. This low ROE is actually a function of Amber's capital allocation strategy. They've been aggressively reinvesting in capacity expansion and acquisitions rather than optimizing for ROE. It's a growth-first strategy that sacrifices near-term returns for long-term market position.

The component synergies are where the model gets interesting. When Amber manufactures a complete AC, they're using their own motors (from PICL), their own PCBs (from Iljin/Ever), their own heat exchangers, their own sheet metal. Each component has its own margin, and when you aggregate them into a finished product, you're capturing value at multiple points in the value chain.

Consider the economics of a typical AC sale. The brand might sell it for ₹30,000. Amber manufactures it for them at, say, ₹20,000. Of that ₹20,000, perhaps ₹12,000 is components. If Amber makes those components in-house at a 15% margin, they're earning ₹1,800 on components plus whatever margin they make on assembly. The vertical integration isn't just about supply chain control; it's about margin stacking.

Though the company is reporting repeated profits, it is not paying out dividend. This zero-dividend policy is revealing. In India, where promoters often use dividends to extract cash from listed companies, Amber's promoters are leaving everything in the business. It signals either extreme confidence in growth opportunities or capital constraints for expansion—likely both.

The working capital dynamics deserve special attention. AC manufacturing is inherently working capital intensive. You need to buy components (copper, compressors, refrigerants) upfront, manufacture the product, ship it to brands, and then wait 60+ days for payment. During peak season (March-June), working capital requirements spike dramatically.

Amber manages this through several mechanisms. First, they've negotiated better payment terms with customers—hence the improving debtor days. Second, they've stretched payables where possible, though this is limited given the bargaining power of component suppliers. Third, and most importantly, they've diversified into non-seasonal businesses (railways, electronics) that generate cash during AC off-season.

The comparison with EBITDA is instructive. While EBITDA might look healthy, EBITDA can often be very far from cash flow. For a capital-intensive business like Amber, with significant capex requirements for new facilities and equipment, free cash flow is the real measure of economic performance. And here's where the model shows strain—aggressive expansion means much of the operating cash flow gets reinvested rather than flowing to shareholders.

The margin structure across divisions is revealing:

- Room AC OEM/ODM: 6-8% EBITDA margins

- Components: 12-15% EBITDA margins

- Sidwal (Railways): 18-20% EBITDA margins

- Electronics: 10-12% EBITDA margins

This margin differential explains Amber's strategic priorities. They're not just diversifying for growth; they're diversifying up the margin curve. Every percentage point of revenue shift from room ACs to railways or electronics improves the blended margin profile.

The capital allocation framework is aggressive but logical. Rather than returning capital to shareholders or maintaining large cash reserves, Amber consistently reinvests in capacity expansion and acquisitions. It's a strategy that assumes continued market growth and successful execution—risky, but potentially transformative if they're right about India's cooling and electronics demand.

What's particularly clever about the model is how it handles risk. By manufacturing for multiple competing brands, Amber diversifies customer risk. By backward integrating into components, they reduce supplier risk. By expanding geographically, they reduce logistics risk. It's a model built for resilience, even if it sacrifices near-term profitability for that resilience.

IX. Playbook: The Amber Method

The war room at Voltas headquarters in 2015. The air conditioning giant is debating whether to set up its own manufacturing facility. The CFO runs the numbers: ₹500 crore capex, 3-year execution, uncertain capacity utilization. Then someone mentions Amber. "Why build when they can build for us?" By year-end, Voltas had signed a multi-year manufacturing agreement with Amber. They would focus on brand and distribution; Amber would handle everything else.

This scene, repeated across boardrooms from LG to Whirlpool, encapsulates the Amber playbook: Be the arms dealer in the AC wars. It's a strategy as old as business itself—during the California Gold Rush, the real money was made selling picks and shovels, not mining gold. Amber sells the picks and shovels of India's cooling boom.

The playbook has several key elements, each refined over decades:

1. The Switzerland Strategy

Amber maintains strict walls between customers. The LG team doesn't know what Voltas is planning. Blue Star's designs don't leak to Godrej. This paranoid compartmentalization isn't just about security; it's about trust. In an industry where today's partner could be tomorrow's competitor, Amber's neutrality is its moat.

They've institutionalized this through physical separation (different production lines), information separation (separate IT systems), and even social separation (customer teams don't mingle). It's expensive and inefficient, but it's the price of being trusted by everyone.

2. The Coattails Approach

When a global brand enters India, they need local manufacturing to hit price points. Amber positions itself as the solution. They'll say: "You focus on what you're good at—brand building, distribution, service. We'll handle the manufacturing complexity." It's a compelling pitch, especially for brands that don't want to deal with India's manufacturing challenges—labor laws, supply chain complexity, seasonal demand swings.

The beauty is that once a global brand partners with Amber, switching costs become prohibitive. It's not just about finding another manufacturer; it's about transferring designs, ensuring quality standards, managing transition risk. Amber becomes embedded in their operations.

3. Geographic Chess

Amber doesn't build mega-factories. Instead, they build multiple smaller facilities near customer locations. A plant near Pune serves western India. Facilities in the north cater to Delhi-NCR. This distributed model increases capital requirements but reduces logistics costs and increases customer stickiness.

More importantly, it makes Amber indispensable. When you have a dedicated facility near a customer's distribution center, with equipment customized for their products and workers trained on their specifications, you're not just a vendor—you're infrastructure.

4. The Integration Ladder

Amber's backward integration follows a pattern: First, identify a critical component where supply is concentrated or unreliable. Second, acquire or build capability in that component. Third, supply it internally while also selling to competitors. Fourth, use the larger scale to reduce costs for everyone.

Take motors. By acquiring PICL, Amber not only secured motor supply for its own ACs but became a motor supplier to other AC manufacturers. Now they have better economies of scale than if they only produced for internal consumption. It's vertical integration that actually improves unit economics rather than destroying them.

5. The Capability Accumulation

Each acquisition isn't just about the assets or customers—it's about capabilities. PICL brought motor expertise. Iljin brought electronics knowledge. Sidwal brought railway certification and relationships. Ever brought PCB manufacturing prowess. Amber systematically acquires capabilities then cross-pollinates them across divisions.

This creates compound advantages. The electronics expertise from Iljin helps improve AC control systems. Railway cooling knowledge from Sidwal informs commercial AC development. Motor efficiency improvements benefit both room and mobility applications.

6. The Anti-Brand Strategy

Amber will never launch a consumer brand. This isn't weakness—it's strategy. The moment Amber becomes a competitor, every customer becomes suspicious. The entire business model collapses. By credibly committing to never compete downstream, Amber can serve everyone upstream.

This extends to employees. Amber's employment contracts include strict non-compete clauses. Customer-facing employees sign additional confidentiality agreements. The message is clear: we're partners, not potential competitors.

7. Technology Partnerships Over Development

Rather than trying to develop all technology internally, Amber partners with global leaders. Korea Circuit for PCBs. Siemens for PLM software. Ultimate Europe for gangway systems. These partnerships bring immediate capability while avoiding massive R&D costs.

The partnerships are structured cleverly—usually joint ventures where Amber has majority control but the partner provides technology. Amber gets technology access; partners get India market access. Both win.

8. The Margin Portfolio

Not all revenue is created equal. Room AC OEM might be lower margin but provides volume and scale. Components are higher margin but lower volume. Railways are highest margin but lumpy. Electronics is growing margin with secular growth. By managing this portfolio, Amber can optimize for growth while gradually improving margins.

The key insight is that low-margin business isn't bad if it provides scale for high-margin business. The room AC volume justifies component manufacturing scale, which improves margins across the board.

9. Capital Cycle Timing

Amber expands capacity ahead of demand, not after. This requires capital and creates short-term underutilization, but it positions them to capture growth when it comes. In a cyclical industry like ACs, being ready for the upturn matters more than optimizing utilization during the downturn.

10. The Ecosystem Play

Amber isn't just building a company; they're building an ecosystem. Training workers who might join competitors (but maintain relationships). Developing suppliers who also serve others (but give Amber priority). Creating industrial clusters that benefit everyone (but where Amber is the anchor).

This ecosystem approach creates network effects. The more players that depend on Amber's ecosystem, the stronger Amber becomes. It's a playbook for building what Warren Buffett would call a "moat"—sustainable competitive advantage that compounds over time.

X. Market Context & Competition

The thermometer at Delhi's India Gate reads 47°C. It's May 2024, and India is experiencing one of its worst heat waves on record. Churu in Rajasthan saw a maximum temperature of 50.5°C. Sadly, more than 700 heatstroke deaths were reported between March and June 2024 in 17 states. Against this backdrop, a simple truth emerges: air conditioning in India isn't about comfort anymore. It's about survival.

According to Panasonic India Business Head, Air Conditioners Group Abhishek Verma, the industry penetration level is around 7 per cent in India, though other sources cite it at 8%. Compare this to developed markets where penetration exceeds 90%, and you understand why every AC manufacturer, investor, and analyst is obsessed with India. Penetration of room air conditioners (RAC) is extremely low in India when compared to various developed economies and only one-fifth of the global average RAC penetration. Given the low RAC penetration at 8%, there is tremendous potential in the Indian market.

The numbers tell a story of explosive growth. India Air Conditioners Market size was valued at USD 5.85 Billion in 2025 and is expected to reach USD 15.41 Billion by 2031 with a CAGR of 17.57%. In unit terms, According to a study by ICRA, the Indian RAC industry is expected to witness a year-on-year (YoY) sales growth of 20-25% in FY 2024-25, reaching record levels of 12-12.5 million units.

But it's not just about raw growth. The market is undergoing fundamental shifts that benefit players like Amber:

The Climate Reality

India isn't getting cooler. The past few years have seen a steady increase in heatwave days, further accelerating the need for cooling solutions. What was once a three-month selling season (April-June) is extending. Cities like Bengaluru, historically temperate, are now AC markets. "However, due to rising temperature levels and hot summers, AC are incrementally turning out to be a necessity. For example, Bengaluru city has emerged as a new market for AC brands owing to rising temperatures"

The Competitive Landscape

The market leader tells us something important about industry dynamics. In 2023-24, Voltas achieved a milestone by selling over 2 million AC units, the highest ever sold by a single brand in a year. The company also reported selling 1 million units within just 110 days, from January to April 2024. Voltas doesn't manufacture most of these ACs itself—it relies on contract manufacturers like Amber.

Daikin has made great inroads in the market in recent years and currently occupies the second spot in the room AC market in India. In FY 2024, Daikin had a market share of 18-19% in India. Unlike Voltas, Daikin has its own manufacturing, but even they outsource to meet peak demand.

The competitive dynamics favor Amber's model. Brands are fighting for market share through marketing and distribution. Manufacturing? That's increasingly outsourced to specialists who can deliver scale, quality, and cost efficiency.

China Dependency and Shifts

India's AC industry has a China problem. Critical components—compressors, controllers, certain electronics—still largely come from China. But this is changing. Government policies including anti-dumping duties on Chinese PCBs and PLI schemes for electronics manufacturing are reshaping supply chains.

To meet this growing demand, India's domestic RAC manufacturing capacity is set to expand by over 40% in the next three years. This capacity expansion isn't just about assembling Chinese components—it's about genuine localization, and Amber with its component manufacturing capabilities is positioned to benefit.

The Technology Transition

The market is shifting from fixed-speed to inverter ACs. "We expect higher levels of rural growth in the coming years, even in the more premium categories," Godrej Appliances Business Head Kamal Nandi said, noting inverter ACs form the bulk of sales. Inverter ACs require sophisticated electronics—exactly the capability Amber has built through its Iljin and Ever acquisitions.

Beyond Residential

While residential drives volume, commercial AC is where margins lie. The India Commercial Air Conditioner Market was estimated at USD 2.4 billion in FY2024 and is forecast to reach USD 6.2 billion by FY2032, growing at a CAGR of 12.62% between FY2025-FY2032. Commercial ACs are higher value, require customization, and have longer replacement cycles—all favorable for manufacturers.

Competition: The Dixon Factor

Amber's most direct competitor is Dixon Technologies, another contract manufacturer that's expanded into ACs. But their approaches differ. Dixon is broader—mobiles, TVs, washing machines, ACs. Amber is deeper—focused on cooling and electronics. In a market growing at 15-20% annually, there's room for both, but Amber's specialization gives it an edge in AC manufacturing complexity.

Traditional AC brands like Blue Star and Voltas have manufacturing capabilities, but they're increasingly focusing on brand and distribution rather than expanding manufacturing. It's more profitable to be a brand than a manufacturer—unless you're a manufacturer at Amber's scale.

Government Support

The Indian government's approach to the AC industry reflects its importance. Despite ACs attracting the highest GST rate of 28% (treating them as luxury goods), various state governments offer subsidies for energy-efficient models. The PLI schemes for electronics and white goods manufacturing provide direct incentives for localization.

The broader "Make in India" push benefits Amber directly. Every policy that makes importing harder or more expensive strengthens the case for local manufacturing. Every subsidy for domestic production improves Amber's economics.

The Penetration Paradox

Here's the fundamental paradox of India's AC market: everyone agrees penetration will increase from 8% to something much higher. But what's that number? 30%? 50%? 90%? And over what timeframe?

The bulls point to China, where AC penetration went from under 10% to over 60% in two decades. The bears point to India's lower per capita income, higher electricity costs, and different housing stock. The reality is probably somewhere in between, but even getting to 25% penetration would triple the market size.

For Amber, the exact number matters less than the direction. Whether India reaches 30% or 60% penetration, Amber wins as long as ACs are manufactured locally rather than imported. They're not betting on a specific penetration target; they're betting on the indigenization of AC manufacturing.

XI. Bear vs Bull Case & Valuation

The analyst from a prominent mutual fund is blunt: "At 85 times earnings, Amber is priced for perfection. One stumble, and the stock gets cut in half." The company's investor relations head responds calmly: "You're not buying today's Amber. You're buying India's cooling story for the next decade." Both are right, and that's what makes Amber such a fascinating—and polarizing—investment case.

The Bull Case: Riding Multiple Megatrends

The bulls see Amber as a convergence play on several unstoppable trends:

1. The AC Penetration Story: With penetration at just 8%, the runway is enormous. Even conservative assumptions of reaching 20% penetration by 2030 imply a tripling of the market. The Indian RAC market is projected to grow at a compound annual growth rate (CAGR) of 12%, reaching an estimated value of $5.6 billion (₹50,000 crore) by FY 2028-29. Amber, with its 29% market share in manufacturing, is positioned to capture a significant portion of this growth.

2. The EMS Diversification: The electronics manufacturing services opportunity in India could be even larger than ACs. The government's PLI schemes, China+1 strategies of global companies, and India's growing electronics consumption create a multi-decade opportunity. Amber's pivot into EMS isn't just diversification—it's entering a potentially larger TAM.

3. Import Substitution: Every component Amber localizes improves its margins and strengthens its moat. With anti-dumping duties on PCBs and government pressure for localization, the trend toward domestic manufacturing is structural, not cyclical.

4. Margin Expansion Trajectory: As Amber's mix shifts from low-margin room AC OEM to higher-margin components, railways, and electronics, overall margins should expand. Sidwal's 18-20% EBITDA margins versus Amber's 8% overall margins show the potential.

5. Operating Leverage: As volumes grow, fixed costs get spread over a larger base. The investments in automation, technology partnerships, and manufacturing infrastructure create operating leverage that should drive margin expansion even without mix improvement.

6. Customer Stickiness: Once a brand outsources to Amber, switching costs are high. This isn't just about manufacturing—it's about product development, supply chain integration, quality systems. The longer the relationship, the deeper the integration.

7. Technical Capability Moat: Through acquisitions and partnerships, Amber has built capabilities that would take competitors years to replicate. Manufacturing railway ACs requires different certifications than room ACs. PCB manufacturing requires different expertise than sheet metal work. This complexity is a barrier to entry.

The Bear Case: Priced for Perfection

The bears have equally compelling arguments:

1. Customer Concentration Risk: Despite diversification, Amber remains dependent on a few large customers. If LG or Voltas decided to insource manufacturing or switch suppliers, the impact would be severe. The company's fate is tied to decisions made in boardrooms they don't control.

2. Margin Pressure: Contract manufacturing is inherently low margin. As the industry matures and competition increases, margins could compress rather than expand. The shift to higher-margin businesses might not happen as quickly as expected.

3. Capital Intensity: Company has a low return on equity of 9.00% over last 3 years. This low ROE reflects the capital-intensive nature of the business. Every expansion requires significant capex, and returns on that capital aren't spectacular.

4. Technology Risk: What if cooling technology changes dramatically? What if solid-state cooling replaces compressor-based systems? What if passive cooling technologies improve? Amber's entire business model assumes current AC technology remains dominant.

5. Execution Risk: Amber is attempting multiple transitions simultaneously—geographic expansion, product diversification, technology upgradation. Managing this complexity while maintaining quality and customer relationships is challenging. One major execution stumble could derail the growth story.

6. Commodity Exposure: Copper, aluminum, steel—Amber's raw materials are commodities with volatile prices. While they can pass through some costs, sudden spikes compress margins. In a competitive market, passing through all cost increases isn't always possible.

7. Working Capital Drain: Despite improvements, the business remains working capital intensive. Growth requires funding not just capex but also increasing working capital. This limits free cash flow generation even as profits grow.

Valuation: The Numbers Game

At current levels, Amber trades at: - P/E of 85.3x - P/B of 10.2x - EV/EBITDA of ~40x (estimated) - Market cap of ₹23,475 crores

These multiples are demanding by any measure. The market is clearly pricing in significant growth and margin expansion. The question is whether Amber can deliver.

The bulls argue these multiples are justified given: - 30% median sales growth over the last 10 years - Expansion into higher-margin businesses - Secular growth in AC penetration - Government support through PLI schemes

The bears counter that: - ROE of 9% doesn't justify such valuations - Contract manufacturers globally trade at much lower multiples - Customer concentration adds risk that should demand a discount - Capital intensity limits cash flow generation

Recent Stock Performance

Stock is up 70.5% in 1 year, significantly outperforming the broader market. This performance reflects both strong operational delivery and increasing investor enthusiasm for the India manufacturing story.

But the stock has also shown volatility, with sharp corrections on any disappointing quarterly results or concerns about demand. This volatility is likely to continue given the high valuations and growth expectations.

Institutional Views

The institutional ownership pattern is revealing. Domestic mutual funds have been buyers, attracted by the India story. Foreign institutional investors have been more selective, concerned about valuations. The promoter stake at 39.6% provides alignment but also limits float.

Analyst opinions are divided. Target prices range from ₹5,000 (bear case) to ₹10,000+ (bull case), reflecting the wide range of outcomes possible.

The Verdict

Amber's valuation makes sense only if you believe: 1. AC penetration in India will at least triple over the next decade 2. The company can successfully diversify into electronics and mobility 3. Margins will expand as the business mix improves 4. Execution will remain strong despite increasing complexity

If any of these assumptions prove wrong, the stock is vulnerable. But if they're right, current valuations might look reasonable in hindsight. It's a high-risk, high-reward proposition—exactly what you'd expect from a company trying to ride India's consumption boom.

The zero dividend policy adds another dimension. Though the company is reporting repeated profits, it is not paying out dividend. For value investors seeking income, this is a negative. For growth investors, it signals management's confidence in reinvestment opportunities.

XII. Analysis & Lessons

Sitting in Amber's Gurugram headquarters, you can see Cyber City's glass towers in the distance—monuments to India's services economy. But Amber represents something different: India's manufacturing ambition. The lessons from Amber's journey extend far beyond air conditioners.

Lesson 1: The Power of Being a "Picks and Shovels" Business

During gold rushes, selling mining equipment beats mining gold. Amber embodies this principle perfectly. They don't care which AC brand wins—Voltas, Daikin, LG, or a new entrant. They win regardless. This positioning removes market risk while maintaining market exposure.

The brilliance is in the execution. It would be tempting to launch an Amber-branded AC, capturing the full margin from manufacturing to retail. But that would destroy the entire business model. By credibly committing to never compete downstream, Amber can serve everyone upstream. It's strategic restraint at its finest.

Lesson 2: Family Business Meets Professional Management

Amber represents an interesting evolution in Indian family businesses. Kartar Singh founded it, Jasbir Singh transformed it, but they've also brought in professional management, independent directors, and institutional governance. It's not the typical promoter-driven story.

The family's continued involvement (39.6% stake) provides long-term thinking, while professional management brings operational excellence. This balance isn't easy—many Indian companies struggle with it—but when it works, it creates something powerful: entrepreneurial drive with institutional capability.

Lesson 3: When to Diversify vs When to Focus

Amber's diversification follows a pattern: it's always adjacent. From AC components to complete ACs. From room ACs to railway ACs. From AC electronics to general electronics. Each move builds on existing capabilities while opening new markets.

This is different from conglomerate diversification where a textile company enters telecom. Amber's diversification is more like concentric circles, each expansion leveraging the core while adding new dimensions. The lesson: diversification works when it's capability-driven, not opportunity-driven.

Lesson 4: Building Trust with Competitors as Customers

Imagine convincing Pepsi and Coca-Cola to use the same bottling plant. That's essentially what Amber has done with AC brands. It requires almost paranoid levels of confidentiality, operational separation, and trust-building.

The lesson extends beyond manufacturing. In any B2B business where you serve competitors, trust becomes your primary product. You're not just selling manufacturing; you're selling confidence that you won't betray secrets or play favorites.

Lesson 5: The India Manufacturing Reality

Amber's story illuminates both the promise and challenges of Indian manufacturing. The promise: huge domestic market, improving infrastructure, government support, cost advantages. The challenges: complex regulations, infrastructure gaps, skill shortages, capital constraints.

What's interesting is how Amber navigates these challenges. Multiple smaller factories instead of mega-plants (easier permits). Locations near customers (reduced infrastructure dependency). Heavy training programs (addressing skill gaps). Strategic partnerships for technology (avoiding massive R&D costs).

Lesson 6: Capital Allocation in Growth Markets

Amber's zero dividend policy and aggressive reinvestment reflect a crucial insight: in rapidly growing markets, the return on retained earnings often exceeds the cost of capital. Every rupee not paid as dividend gets reinvested at high incremental returns.

This only works if: (a) growth opportunities are real, (b) execution is strong, (c) capital allocation is disciplined. Amber seems to check these boxes, but it's a high-wire act. One bad acquisition or failed expansion, and the narrative breaks.

Lesson 7: The Vertical Integration Question

Conventional wisdom says vertical integration destroys value—companies should focus on core competencies. Amber defies this by successfully integrating backward into components. Why does it work here?

The answer lies in market structure. When component suppliers have pricing power (often true in India due to limited competition), vertical integration can make sense. When you're already the largest buyer of a component, manufacturing it yourself achieves better scale. When quality control is critical, integration ensures standards.

Lesson 8: Riding Government Policy

Amber has masterfully ridden government policy waves—PLI schemes, anti-dumping duties, Make in India. But they haven't become dependent on subsidies. The business model works without government support; policy tailwinds just accelerate growth.

This is the right balance. Companies entirely dependent on government support are vulnerable to policy changes. Companies that ignore government initiatives miss opportunities. Amber uses policy support as an accelerator, not a crutch.

Lesson 9: The Platform vs Product Debate

Is Amber a product company (making ACs) or a platform company (providing manufacturing capabilities)? Increasingly, it looks like a platform. The same capabilities that make ACs can make other electronics. The same customer relationships built on room ACs extend to commercial ACs.

Platform businesses typically deserve higher valuations than product businesses because they have more optionality. Amber's evolution toward a manufacturing platform rather than just an AC manufacturer partly justifies its premium valuation.

Lesson 10: The China+1 Opportunity

Amber is perfectly positioned for the China+1 trend—global companies diversifying supply chains away from China. But success isn't guaranteed. Vietnam, Mexico, and others are competing for the same opportunity.

What gives India (and Amber) an edge is the domestic market. Unlike Vietnam, India offers both manufacturing capability and consumption demand. Companies setting up in India can serve both local and export markets. Amber's established infrastructure and capabilities make them an obvious partner.

The Broader Implications

Amber's story is really about India's economic transition. Can India become a manufacturing powerhouse? Can Indian companies build global-scale operations? Can family businesses professionalize while maintaining entrepreneurial drive?

If Amber succeeds, it validates the India manufacturing story. If it struggles, it highlights the challenges of building industrial capabilities in a services-dominated economy. Either way, it's a bellwether for India's economic ambitions.

XIII. Looking Forward & Epilogue

The architect's rendering shows a massive facility near Noida airport—clean lines, solar panels, automated guided vehicles moving components. This is Amber's ₹6,000 crore electronics manufacturing plant, still in planning but representing the company's biggest bet yet. It's either the next chapter in an incredible growth story or an ambitious overreach. Time will tell.

The Immediate Horizon: ₹2,500 Crore Fundraise

Amber's plans to raise ₹2,500 crore signal aggressive expansion mode. The capital will likely fund: - Electronics manufacturing expansion - PCB manufacturing facilities - Potential acquisitions - Working capital for growth

The fundraising method matters. Will it be debt (increasing leverage but maintaining ownership)? Equity (diluting shareholders but strengthening the balance sheet)? Or selling stakes in subsidiaries (unlocking value but losing control)? Each choice tells us something about management's confidence and priorities.

The ILJIN IPO Possibility

Amber Enterprises is in talks with private equity investors for a stake sale in its subsidiary ILJIN Electronics, while it may also look at a public listing of the entity along with pre-IPO placements. The monetisation strategy is being finalised for the subsidiary as it expands its electronics components manufacturing facilities, which will require significant investments.

An ILJIN IPO would be fascinating. It would crystallize value, provide growth capital, and potentially rerate Amber's valuation as investors see the hidden value in subsidiaries. But it also adds complexity—managing a listed subsidiary with its own shareholders and obligations.

The EV Revolution's Impact

Electric vehicles need sophisticated thermal management—batteries need cooling, cabins need climate control, power electronics need heat dissipation. This is Amber's wheelhouse. As India's EV adoption accelerates, Amber could become a critical supplier to the EV ecosystem.

But EVs also pose risks. They're more efficient, generating less waste heat, potentially requiring less cooling. They might use different cooling technologies. Amber needs to evolve its capabilities to remain relevant in an electrified future.

Global Ambitions: From India for the World

Amber has started small exports, but the real opportunity is becoming a global supplier. If they can manufacture for Indian conditions (extreme heat, dust, voltage fluctuations), they can manufacture for anywhere. The question is whether they can compete with established global players on their home turf.

The partnership approach might be the answer. Joint ventures with global companies, technology transfers, using India as a manufacturing base for emerging markets—these strategies could globalize Amber without the risks of direct competition in developed markets.

What Could Disrupt Amber's Model

Several scenarios could derail Amber's growth story:

Technology Disruption: Solid-state cooling, passive cooling improvements, or entirely new cooling technologies could obsolete current AC technology. Amber would need to adapt quickly or become irrelevant.

Customer Insourcing: If major brands decide to bring manufacturing in-house, Amber loses volume. This seems unlikely given trends toward asset-light models, but it remains a risk.

New Competition: Chinese manufacturers setting up in India, other Indian companies entering contract manufacturing, or global EMS giants focusing on India could intensify competition.

Regulatory Changes: Environmental regulations banning certain refrigerants, energy efficiency standards Amber can't meet, or changes in import duties could disrupt the business model.

Economic Slowdown: AC demand is discretionary spending for most Indians. A prolonged economic slowdown would hit demand hard, especially for Amber's operating leverage model.

Execution Failures: Managing multiple expansions, acquisitions, and technology transitions simultaneously is complex. A major quality issue, customer loss, or failed acquisition could break investor confidence.

The 2030 Vision

Looking ahead to 2030, several scenarios are possible:

Best Case: Amber becomes India's Foxconn—a massive contract manufacturer serving multiple industries, publicly listed subsidiaries, global customers, ₹50,000+ crore market cap. AC penetration reaches 25%, electronics becomes 50% of revenue, margins expand to 12-15% EBITDA.

Base Case: Steady growth continues, AC penetration reaches 15-20%, electronics becomes a meaningful contributor, margins improve modestly. Market cap doubles to ₹50,000 crores, but ROE remains moderate. The company remains India-focused with limited global presence.

Worst Case: Growth disappoints as AC penetration stalls around 12-15%, competition intensifies, margins compress. The electronics pivot struggles, acquisitions disappoint. Stock rerates dramatically lower as growth premium evaporates.

The Entrepreneur's Dilemma

Jasbir Singh faces a classic entrepreneur's dilemma. Amber is successful but still subscale globally. Should they: - Continue organic growth, maintaining control but potentially missing opportunities? - Pursue aggressive M&A, risking execution but accelerating scale? - Partner with a global major, gaining capabilities but losing independence? - Focus on India or pursue global expansion?

These aren't just business decisions; they're existential choices about what Amber wants to become.

The India Story Writ Small

Amber encapsulates India's economic possibilities and challenges. A company that started making tractor parts in Punjab now manufactures sophisticated electronics and cooling systems for railways. It's a testament to Indian entrepreneurship, but also to the challenges of building globally competitive manufacturing in India.

The next decade will determine whether Amber becomes a global champion or remains a successful but primarily domestic player. Either outcome is acceptable, but the ambition is clearly global.

Final Thoughts: Beyond the Numbers

Walking through Amber's factory floor, you see something beyond financial metrics. Workers who joined as helpers now program CNC machines. Engineers who started in sheet metal now design complex electronics. It's human capital transformation at scale.

This might be Amber's most important contribution—not just manufacturing ACs or generating returns, but building India's manufacturing capability, one worker, one engineer, one factory at a time.

The stock price will fluctuate. Quarters will disappoint or delight. Competition will intensify. Technology will evolve. But the fundamental bet remains unchanged: India needs cooling, India needs electronics, and India needs companies that can manufacture at scale with quality.

Whether at ₹7,000 or ₹10,000 per share, whether growing at 15% or 25%, whether focused on ACs or diversified into electronics, Amber represents something important: the possibility that India can build world-class manufacturing companies.

The air conditioning empire that nobody knows about might not remain unknown much longer. As India's temperatures rise and its economy grows, Amber's invisible hand in keeping India cool becomes increasingly visible. For investors, employees, customers, and competitors, the question isn't whether Amber matters—it's how much it will matter in India's manufacturing future.

The story continues, written in sheet metal and silicon, in factory floors and boardrooms, in rising temperatures and growing aspirations. It's a story about cooling, but really, it's about India itself—its challenges, opportunities, and inexorable rise.

XIV. Recent News**

Q3 FY25: Record Performance Validates Strategy**

Amber Enterprises India Ltd (NSE:AMBER) reported a robust quarterly performance with a 65% increase in revenue, reaching INR2,133 crores. Operating EBITDA almost doubled, showing a 97% growth to INR162 crores, and PAT improved significantly to INR37 crores from a loss of INR1 crore in the previous year.

The Consumer Durable division saw a blended growth of 67%, driven by a 71% increase in the Room Air Conditioner (RAC) segment. This exceptional growth reflects the pre-season inventory stocking by brands ahead of the summer selling season, validating Amber's position as the go-to manufacturing partner.

The Electronics division experienced remarkable growth, with revenue increasing by 96% to INR472 crores and EBITDA growing by 193% to INR34 crores. This near-doubling of the electronics business shows the pivot is working faster than expected.

Amber Enterprises India Ltd (NSE:AMBER) revised its revenue growth guidance for the Electronics division from 45% to 55% for FY25, indicating strong future prospects. Management rarely raises guidance mid-year unless visibility is exceptionally strong.

However, not everything was perfect. The Railway Sub-systems & Defense division revenue witnessed a 13% decline on a YoY basis in Q3 FY25, impacted by deferral in offtake of products. However, the delay in Indian Railways offtake is more momentary, with no cancellations of orders.

Strategic Moves and Capital Allocation

Summary of 35th AGM including financials, director reappointment, remuneration hikes, and Rs. 2500 Cr fund raising. The board's approval for such significant fundraising suggests major expansion plans are imminent.

Amber Enterprises India Ltd plans to acquire a 40.24% stake in Israel's Unitronics, resulting in a 45.13% controlling interest. This strategic move aims to enhance its industrial automation capabilities and expand into global markets, valued at approximately Rs 404 crore. Unitronics brings programmable logic controllers (PLCs) and industrial automation expertise—critical for Industry 4.0 applications.

Management Commentary and Outlook

The earnings call revealed important insights. Management highlighted capacity constraints in electronics, particularly in the Accent segment, suggesting demand is exceeding their most optimistic projections. This is a good problem to have but requires urgent capacity addition.

On margins, while there was some compression in RAC gross margins due to product mix, the overall trajectory remains positive. Management expects ROCE to cross 15% by year-end, a significant improvement from historical levels.

The supply chain concern around compressors was acknowledged but deemed manageable. This transparency is refreshing—acknowledging challenges while maintaining confidence in resolution.

Analyst Actions and Market Response

Amber Enterprises India Ltd is receiving positive ratings from analysts, with Sharekhan targeting Rs 9,300 and Anand Rathi targeting Rs 10,050, highlighting strong growth in electronics and robust financial performance. Amber Enterprises Target Price Raised to Rs 9,000 - 31 Jul, 2025 Amber Enterprises shows strong performance in 1QFY26, prompting Motilal Oswal to raise the target price to Rs 9,000.

The analyst community is increasingly bullish, with target prices being revised upward following strong quarterly performances. The consensus seems to be that the electronics pivot is happening faster than expected.

Stock Performance and Technical Levels

Investment in Amber Enterprises India Ltd Shares on INDmoney has grown by 16.06% over the past 30 days, indicating increased transactional activity. Retail interest is picking up, often a sign of momentum building.

The stock has been volatile but trending upward, with each earnings report creating sharp moves. Support seems to be building around ₹6,500 levels with resistance at ₹8,000.

Key Takeaways from Recent Developments

- Core Business Strength: The 71% growth in RAC segment shows the core business remains robust

- Electronics Validation: Near 100% growth in electronics validates the diversification strategy

- Global Ambitions: The Unitronics acquisition signals serious international aspirations

- Capacity Constraints: Demand exceeding supply in electronics is a positive problem

- Railway Delays: Temporary setback in railways but order book intact

- Margin Trajectory: Some near-term pressure but long-term trajectory remains upward

- Capital Raising: ₹2,500 crore fundraise indicates aggressive expansion ahead

The recent developments suggest Amber is at an inflection point. The electronics pivot is working, the core AC business is strong, and management is confident enough to raise guidance and pursue international acquisitions. While valuations remain stretched, the operational performance is increasingly justifying the premium.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube