AFCONS Infrastructure: Engineering India's Extreme Infrastructure

I. Introduction & Cold Open

Picture this: 359 meters above the Chenab River in Jammu and Kashmir, workers balance on steel girders in sub-zero temperatures, assembling what will become the world's tallest single-arch railway bridge. The structure soars 35 meters higher than the Eiffel Tower, engineered to withstand not just earthquakes and 266 km/hour winds, but also blast loads—the first bridge in the world designed for such extreme conditions. This isn't a scene from a Hollywood blockbuster. It's Tuesday morning for AFCONS Infrastructure.

Meanwhile, 33 meters beneath Kolkata's Hooghly River, another AFCONS team navigates through clay and silt, boring India's first underwater metro tunnel. The twin tunnels stretch 520 meters under the riverbed, connecting two halves of a city that has waited decades for this moment. Above them, cargo ships and ferries continue their daily routes, oblivious to the engineering marvel taking shape below.

How did a company that started in 1959 as a Swiss-Indian joint venture doing foundation work for Mumbai office buildings transform into the force that builds India's most challenging infrastructure? How did it become the 10th largest marine contractor globally while remaining virtually unknown to most Indians until its 2024 IPO?

This is the story of AFCONS Infrastructure—a 65-year journey from drilling foundation piles in Nariman Point to engineering some of the world's most extreme infrastructure projects. It's a tale of Swiss precision meeting Indian ambition, of building capabilities when others sought quick profits, and of staying private for six decades while competitors rushed to capital markets. Along the way, we'll explore how a company can dominate niches like marine construction and complex bridges, why the Shapoorji Pallonji Group saw gold where others saw a struggling contractor, and what it means to go public with promoters pledging half their stake to lenders.

The roadmap ahead takes us from foundation engineering in newly independent India through international expansion across 25 countries, from family ownership to corporate transformation, and finally to a ₹5,430 crore IPO that opened 7.99% below its issue price. Buckle up—we're about to excavate six decades of engineering excellence, financial engineering, and the occasional tunnel under a river.

II. Origins: The Swiss Connection & Early Years (1959-1976)

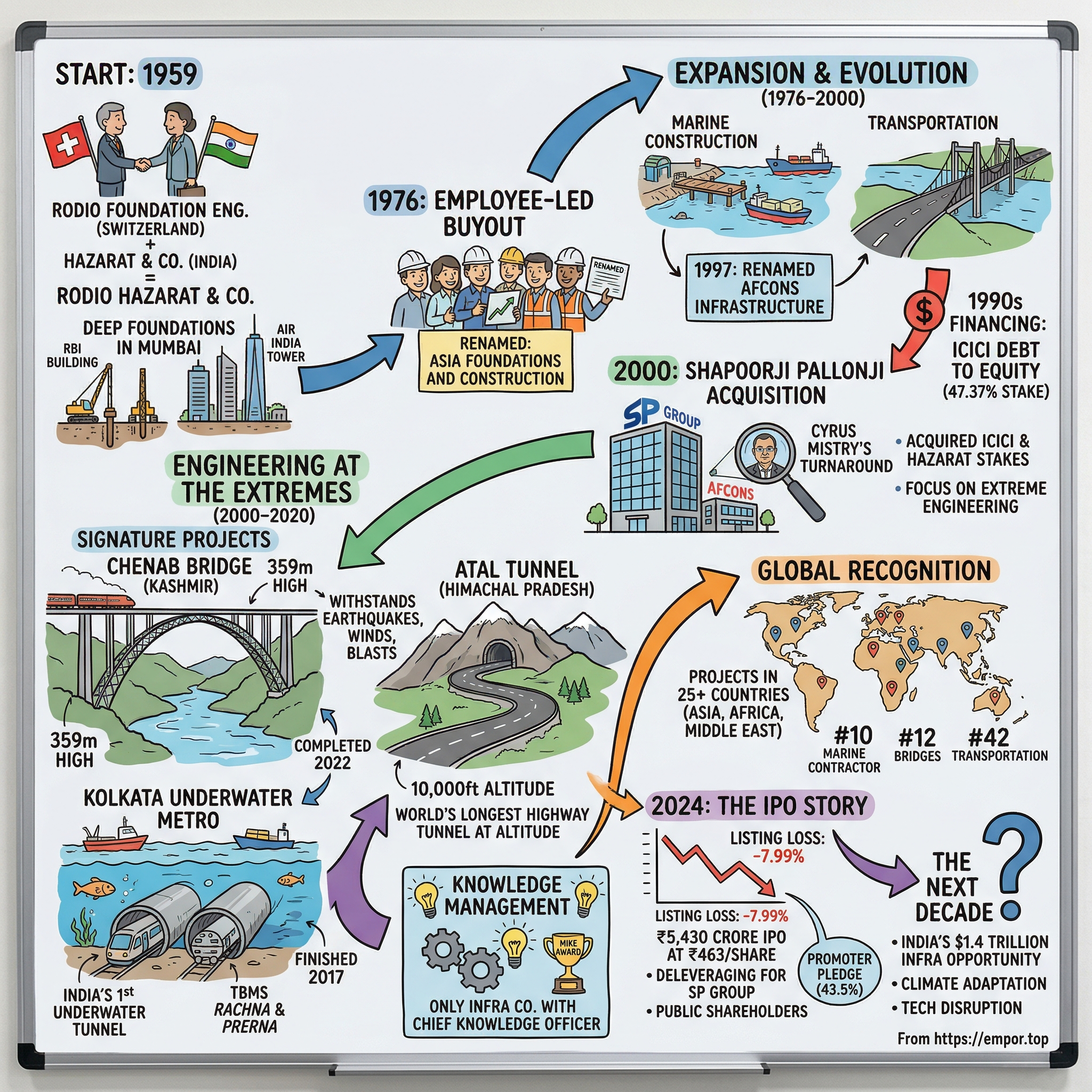

The year is 1959. Jawaharlal Nehru's India is barely a teenager, ambitious but infrastructure-poor. Mumbai's Nariman Point—today's commercial heart—is mostly reclaimed land, unstable and untested. Into this landscape arrives Rodio Foundation Engineering of Switzerland, specialists in deep foundation and ground improvement techniques that India desperately needs but doesn't possess. They find a local partner in Hazarat & Company, and together they birth Rodio Hazarat & Co.

The timing couldn't have been more perfect. Post-independence India was on a construction spree—new government buildings, commercial complexes, ports, bridges. But Indian soil presented unique challenges. Mumbai sat on reclaimed land and volcanic rock. Delhi had its Ridge, Kolkata its riverine soil. Traditional British-era construction methods weren't cutting it. The Swiss brought something revolutionary: specialized piling techniques, ground stabilization methods, and most importantly, the knowledge to build tall on difficult terrain.

Those early years in Nariman Point weren't glamorous. The company's engineers—a mix of Swiss experts and eager Indian apprentices—spent their days driving piles deep into Mumbai's uncertain ground. Each project was a classroom. The Swiss insisted on documentation, precision, measurement. "Measure twice, cut once" wasn't just a saying; it was gospel. This obsession with technical excellence would become AFCONS's DNA, but in 1959, they were just trying to keep buildings from sinking.

The company's first decade reads like a who's who of India's architectural ambitions. The Reserve Bank of India building. The Air India tower. Express Towers. If it was tall and important in 1960s Mumbai, chances are Rodio Hazarat had drilled its foundations. The Swiss partners weren't just bringing technology; they were transferring it. Young Indian engineers were sent to Switzerland for training. Technical manuals were translated. Slowly, methodically, knowledge seeped from Swiss hands to Indian minds.

But paradise rarely lasts in business. By the early 1970s, India's political climate was shifting. Indira Gandhi's government, suspicious of foreign influence and eager to assert economic sovereignty, began tightening the screws on foreign ownership. The Foreign Exchange Regulation Act (FERA) of 1973 was the death knell for many joint ventures. Foreign companies could hold no more than 40% equity in Indian operations. For Rodio Foundation Engineering, the writing was on the wall. In 1976, the inevitable happened. The Swiss partner exited the joint venture by selling its stake to an employees-led consortium, owing to the Foreign Exchange Regulation Act legislation passed in 1973 which affected its business viability. But here's where the story takes an unexpected turn. Rather than find another foreign partner or sell to a large Indian conglomerate, the company executed what might be India's first employee-led buyout in the infrastructure sector.

The company was renamed as Asia Foundations and Construction in the same year. The new name signaled ambition—not just foundations anymore, but construction across Asia. The Hazarat family retained significant ownership, but critically, employees became shareholders. This wasn't just about ownership; it was about identity. The company transformed from a foreign joint venture to an Indian enterprise with international capabilities.

This transition period reveals something profound about AFCONS's character. At a time when most Indian companies were either family fiefdoms or government enterprises, here was a company owned partially by its engineers and workers. Every project success meant personal gain. Every technical challenge overcome added to their collective equity. This alignment would prove crucial in the decades ahead, as the company tackled increasingly complex projects where technical excellence, not just cost-cutting, determined success.

III. Building Without Borders: Expansion & Evolution (1976-2000)

The employee-owned Asia Foundations and Construction of 1976 bore little resemblance to what it would become by the millennium's end. Free from Swiss oversight but armed with Swiss methods, the company embarked on a two-decade transformation that would see it evolve from a foundation specialist to a full-spectrum infrastructure contractor operating across continents.

The late 1970s and early 1980s were about proving they could survive without foreign hand-holding. India's infrastructure needs were exploding—new ports for trade, bridges across rivers that had divided communities for centuries, industrial facilities for Nehru's vision of self-reliance. Asia Foundations didn't just bid for foundation work anymore. They began expanding into marine construction—jetties, docks, and harbors. The logic was simple: if you could stabilize ground underwater for bridge piers, why not build entire port structures?

Their first major marine project came in 1982 at Kandla Port in Gujarat. The project required constructing berthing facilities in tidal conditions with currents that could sweep away incorrectly placed concrete blocks. The company's engineers spent months studying tidal patterns, developing specialized casting yards for concrete caissons, and creating installation procedures that could work within narrow tidal windows. When they successfully completed the project six months ahead of schedule, word spread. The foundation company could do marine work. By 1991, India was in crisis. The liberalisation process was prompted by a balance of payments crisis that had led to a severe recession. India's foreign exchange reserves fell to dangerously low levels, covering less than three weeks of imports. The country had to airlift gold to secure emergency loans. But for Asia Foundations, this crisis spelled opportunity. Infrastructure would be the backbone of liberalization. Ports needed modernization for increased trade. Roads required upgrading to connect newly liberalizing markets. Power plants, telecommunications towers, airports—everything needed building or rebuilding.

The company expanded its business interests beyond foundation engineering to include marine construction (jetties, docks and harbours) and transportation works (roads and bridges). This wasn't random diversification. Each new capability built on the last. Foundation engineering taught them soil mechanics and underwater work. Marine construction added experience with tides, currents, and corrosion. Transportation projects brought expertise in long linear projects and coordination with multiple stakeholders.

In 1997, the company was renamed to Afcons Infrastructure. The new name captured the transformation—from Asian ambitions to global ones (the 'Af' hinting at African projects already underway), from foundations to full infrastructure. But the name change also coincided with financial engineering that would reshape the company's destiny.

In the 1990s, the company raised debt funding from ICICI, which later converted the debt to equity, obtaining a 47.37% stake by 1998. This wasn't just a financing arrangement; it was a lifeline. ICICI, then a development financial institution, saw in AFCONS what others missed—a technically competent contractor with international potential but capital constraints. The debt-to-equity conversion gave AFCONS breathing room while giving ICICI a stake in India's infrastructure boom.

The international expansion that began in the 1980s accelerated through the 1990s. AFCONS engineers found themselves in Nigeria building ports, in Bangladesh constructing bridges, in the Middle East laying pipelines. Each international project was harder than domestic ones—unfamiliar regulations, different soil conditions, logistics nightmares. But they also paid better margins and, critically, paid in foreign currency when India desperately needed dollars.

By 2000, AFCONS had projects in over a dozen countries. The company that couldn't exist under FERA because of foreign ownership had become one of India's few infrastructure exporters. They'd built marine facilities that handled millions of tons of cargo, bridges that connected divided communities, and industrial facilities that powered economies. Revenue had grown from tens of crores to hundreds. The employee-shareholders who'd bought out the Swiss in 1976 were sitting on substantial wealth.

But success brought its own challenges. ICICI, transforming from a development institution to a commercial bank, wanted to exit. The Hazarat family, after four decades, was ready to cash out. International projects were getting larger, requiring performance guarantees and working capital that stretched the company's balance sheet. AFCONS needed a new owner—one with deep pockets, patience for long-gestation projects, and appreciation for technical excellence over financial engineering. They were about to find exactly that in India's most secretive business house.

IV. The Shapoorji Pallonji Acquisition: Finding a Home (2000)

The boardroom at Sterling Investment Corporation Limited buzzed with an energy unusual for the notoriously quiet Shapoorji Pallonji Group. It was early 2000, and executives were evaluating what would become one of their most strategic acquisitions. On the table: AFCONS Infrastructure, a company with world-class technical capabilities but ownership in flux. For the SP Group, masters of construction who'd built Mumbai's skyline and held the largest individual stake in Tata Sons, this wasn't just another deal. It was a missing piece. In 2000, the Shapoorji Pallonji Group acquired a majority stake in Afcons by buying out ICICI's entire stake and an additional 6.59% from promoter Hazarat family. According to sources, the total enterprise value of Afcons is estimated at around Rs 125 crore. For a company with world-class capabilities and international presence, this was a steal—but only if you understood what you were buying.

The SP Group understood infrastructure viscerally. Since 1865, they'd built Mumbai's landmarks—the Reserve Bank building, the Bombay Stock Exchange, the Taj Intercontinental. But their expertise was in buildings and real estate. AFCONS brought something different: complex engineering in marine, tunnels, bridges—the unsexy but essential infrastructure that made economies run. Where SP built what people saw, AFCONS built what made cities work. Cyrus Mistry is credited with the turnaround of the struggling Afcons Infrastructure in the years after its acquisition by Shapoorji Pallonji Group in 2000. The young scion, then just 32, took personal charge of the transformation. By April 2000, Shapoorji Pallonji had acquired Afcons at a market cap of USD 7 million. When the young man behind this acquisition, Cyrus Mistry, entered Afcons' office, on his first day, challenges lined up as if they were just awaiting his arrival – labour union issues, demoralized staff, mounting debt and impending losses.

In order to address varied issues like human resources, engineering, finance, corporate planning etc. Cyrus Mistry decided to have weekly meetings with the different teams. With an eye for detail, he sat on problems with senior engineers as well as junior engineers. With this approach, he was quickly able to grasp issues relating to the infrastructure business. He personally addressed problems at the project as well as at the corporate level and became their 'Solution Finder'.

This hands-on approach was revolutionary for a company used to distant ownership. Cyrus Mistry served as chairman from 2003 until 2012, when he was succeeded by his brother Shapoor Mistry. During his tenure, AFCONS transformed from a debt-laden contractor to a global infrastructure player. The cultural shift was palpable—from survival mode to excellence pursuit.

Shapoorji Pallonji Group eventually increased its stake to over 97% by acquiring shares held by employees. This wasn't a hostile takeover but a gradual consolidation. Employee-shareholders, many nearing retirement, found willing buyers in SP Group at fair valuations. The transition from employee ownership to corporate ownership was managed without disrupting operations or losing key talent.

What SP brought wasn't just capital—though that mattered enormously. They brought patience. Infrastructure projects have long gestation periods, uncertain cash flows, and massive working capital requirements. Where ICICI as a financial institution needed exits and returns, SP as a family conglomerate could wait. They understood that AFCONS's value lay not in quarterly earnings but in capabilities built over decades.

The SP acquisition also brought something intangible but crucial: prestige. Being part of the group that owned 18% of Tata Sons opened doors. Government officials took meetings. International partners saw stability. Banks extended credit lines. Young engineers joined because SP meant career security. The same technical capabilities that existed in 1999 suddenly had a platform to shine.

Under SP ownership, AFCONS began targeting projects others wouldn't touch. If it was underwater, underground, or at altitude, AFCONS was interested. This wasn't bravado; it was strategy. Complex projects had fewer bidders, better margins, and built reputational moats. Each successful extreme project made the next one easier to win. By the time Cyrus Mistry left to head Tata Sons in 2012, AFCONS had become exactly what SP had envisioned—India's extreme infrastructure specialist, ready to take on the world's most challenging projects.

V. Engineering at the Extremes: Signature Projects (2000-2020)

The Chenab river valley in Kashmir, 2004. Engineers from AFCONS stand at the proposed site of what would become the world's tallest railway bridge, staring at an impossible challenge. The bridge needed to span 467 meters across a gorge, rising 359 meters above the river—higher than the Eiffel Tower. It would face earthquakes, 266 km/hour winds, and temperature swings from -20°C to 40°C. Oh, and it needed to be blast-resistant, a first for any bridge globally. The Indian Railways officials presenting the project almost apologetically mentioned that several international firms had already declined to bid.

AFCONS took it on. The design and construction of the bridge were awarded to a joint venture comprising Afcons Infrastructure, Ultra Construction & Engineering Company of South Korea and VSL India in 2004. But AFCONS led the charge, bringing to bear everything they'd learned since 1959. The bridge is designed to withstand earthquakes up to a magnitude of eight on the Richter scale, high-intensity blasts equivalent to about 40 tonnes of TNT, temperatures up to −20 °C and wind speeds of up to 266 km/h.

The construction used about 28,660 tonnes of steel, 66,000 m³ of concrete and 84 km of bolts and cables. But numbers don't capture the human drama. AFCONS engineers worked at impossible heights beating extreme winters, torrential rains, and excruciating summers. Working at such elevations is very risky and needs specialised teams and platforms with safety measures in place. It is impossible to retrieve any HSFG bolt if it unfortunately slips and falls into the river from such height.

The project introduced several engineering firsts for Indian Railways, such as the use of Phased Array Ultrasonic Testing (PAUT) for weld inspection and the establishment of an onsite NABL-accredited testing laboratory. The bridge was fully completed and inaugurated on 13 August 2022—eighteen years after AFCONS took on the impossible. Meanwhile, 1,500 kilometers away in Kolkata, another AFCONS team was preparing to bore India's first underwater metro tunnel beneath the Hooghly River. Contract for building the underwater tunnel section from Central to Howrah Maidan awarded to Afcons in 2010. The challenges were different but equally daunting. The section under the river is at a depth of 30 metres (roof to ground distance) whereas the average roof to ground distance is 17 metres. The Howrah metro station on the west side of the river will be at a depth of 30 metres—India's deepest metro station.

Transtonnelstroy-Afcons, a joint venture between Russian engineering giant Transtonnelstroy and Afcons had bagged the Rs 938 crore contract for constructing a part of the underground stretch, including that under the Hooghly in 2010. But the project's human story transcended engineering. The two German-made tunnel boring machines were named Rachna and Prerna after the daughters of Bimal Saha, an AFCONS billing manager who died in a road accident in 2016. Everyone felt it would be appropriate if the two TBMs are named after Saha's two daughters. That would be a fitting tribute to Saha," said a senior engineer of the joint venture. This is how the two TBMs were named after Saha's two daughters.

It was Rachna who was the first to embark on the 'ground-breaking' journey from the western bank of the Hooghly river on 18 April 2017. Rachna burrowed steadily under the river and hit the eastern bank after 36 days on 23 May 2017. With that journey under the river, Rachna scripted history and nothing short of an engineering marvel in this part of the world. In 2017, the tunnelling project under the Hooghly River bed was successfully finished by construction major, Afcons Infrastructure.

These weren't isolated projects. Across India, AFCONS was building the impossible. The Atal Tunnel in Himachal Pradesh—the world's longest highway tunnel at 10,000 feet altitude, reducing the distance between Kullu and Lahaul by 48 km and travel time by four hours. Six operational LNG tanks in India, each a marvel of cryogenic engineering. Projects in over 25 countries in Asia, Africa, and the Middle East.

By 2020, AFCONS had transformed from an Indian contractor to a global infrastructure force. Afcons is ranked 14th globally in 'marine and port facilities' and is the highest-ranking Indian company in the top 25 international contractors. It ranks 12th globally in the bridge sector and is the only Indian company in the top 25 international contractors. In the transmission lines & aqueducts sector, Afcons is ranked 12th, and in water supply, 38th globally. Afcons is also the only Indian contractor in the 'Top 50 international contractors in transportation'.

What set AFCONS apart wasn't just technical capability—many firms had engineers and equipment. It was their willingness to take on projects others wouldn't touch. Each extreme project built knowledge that couldn't be bought or taught in classrooms. How do you pour concrete at -20°C? How do you ensure worker safety 359 meters above a river? How do you bore through alluvial soil under a river without flooding? AFCONS knew because they'd done it.

This knowledge became their moat. Our continuous pursuit of excellence in knowledge management is reflected in the recognition accorded to us through the MIKE (Most Innovative Knowledge Enterprise) award at Global and India levels. They were the only infrastructure company globally to win this award for nine consecutive years. While competitors chased volumes, AFCONS chased complexity. And complexity, it turned out, paid better and lasted longer.

VI. Global Recognition & Market Position (2010s-Present)

Walk into any infrastructure conference in the 2010s and mention marine construction in India. The first name you'd hear: AFCONS. Not L&T, despite its size. Not international giants like Bechtel or Fluor. AFCONS had carved out a reputation so specific, so technical, that it transcended corporate hierarchies. They weren't the biggest. They were the ones you called when biggest wasn't enough.

The numbers tell one story: 10th largest international marine and port facilities contractor globally, 12th in bridges, 42nd in transportation, 18th in transmission lines and aqueducts. But numbers miss the nuance. AFCONS wasn't competing on scale; they were competing on capability. While others built more, AFCONS built what others couldn't.The MIKE (Most Innovative Knowledge Enterprise) award story epitomizes AFCONS's approach. Afcons has received MAKE (Most Admired Knowledge Enterprise) awards for India, Asia and Global levels in 2016 and 2017. Afcons continued to receive recognition in knowledge management and won MIKE (Most Innovative Knowledge Enterprise) awards for India and Global levels from 2018 to 2023. Afcons is the only Infrastructure company to win this award at Global and India levels and is the only infrastructure company to have a Chief Knowledge Officer.

Think about that—the only infrastructure company globally with a Chief Knowledge Officer. While competitors hired more engineers, AFCONS hired someone to ensure every engineer's learning benefited every other engineer. Launched in 2012, the Knowledge Management initiative was the outcome of the realisation that completed projects could better reflect the wealth of knowledge and expertise that had gone into its creation. This is where the Knowledge Services Group (KSG) plays a crucial role. Every project that Afcons executes, generates a bounty of new knowledge. The idea of forming a dedicated group is two-fold: Firstly, to acknowledge the power of knowledge; Secondly, to capture this learning and put it back into circulation.

This wasn't corporate jargon. When an engineer in Ghana discovered a new method for underwater concreting in saline conditions, that knowledge was captured, codified, and available to a team in Bangladesh within weeks. When the Chenab bridge team developed techniques for working at extreme heights in sub-zero temperatures, those lessons informed safety protocols in African mountain projects.

The global rankings reflected this knowledge advantage. But AFCONS's market position was peculiar. They dominated niches while remaining relatively small overall. In marine construction, they were giants. In standard road construction, barely visible. This was deliberate. As one executive explained privately, "Why compete with twenty contractors for a standard highway when you can be one of three bidding for an underwater tunnel?"

Competition came from predictable quarters—L&T, India's infrastructure behemoth; KEC International and Kalpataru Projects from the RPG and Kalpataru groups respectively. But AFCONS's real competition wasn't Indian. For complex marine projects, they competed with Royal Boskalis Westminster from the Netherlands, Jan De Nul from Belgium, China Harbour Engineering Company. These were century-old firms with fleets of specialized vessels and equipment worth billions.

AFCONS couldn't match their equipment. So they matched their expertise and undercut their prices. A European firm might quote $100 million for a port project with 50% margins. AFCONS would quote $70 million with 20% margins and deliver the same quality. The Europeans had legacy costs—unionized European labor, expensive equipment financing, corporate overheads. AFCONS had Indian engineers earning a fraction of European salaries but delivering European standards.

By 2020, AFCONS faced a crossroads. They'd conquered the extremes—the highest bridge, the deepest tunnel, the most complex marine structures. But extreme projects are, by definition, limited. India plans one Chenab bridge, not ten. The underwater metros were prestigious but rare. LNG tanks paid well but how many does India need?

The answer lay in internationalization, but that brought new challenges. International projects meant political risk, currency risk, mobilization costs. The Shapoorji Pallonji Group's financial struggles added another dimension. The group had accumulated debt across ventures. AFCONS, profitable and cash-generative, was an obvious candidate for monetization. The question wasn't whether to go public, but when and at what valuation.

VII. The IPO Story: Going Public at 65 (2024)

October 25, 2024. As markets opened, AFCONS Infrastructure's IPO went live—65 years after a Swiss company shook hands with an Indian partner in Nariman Point. The ₹5,430 crore offering at ₹463 per share wasn't just another infrastructure IPO. It was the Shapoorji Pallonji Group's attempt to deleverage without losing control, AFCONS's graduation to public markets after decades of private excellence, and a test of whether Indian investors understood the value of engineering capability over financial engineering. The public issue of Afcons Infrastructure IPO was offered at ₹463.00 per share and was listed at ₹426.00, resulting in a listing loss of -7.99%. With a minimum lot size of 32 shares, the IPO incurred a loss of ₹-1184 per lot on listing. For a company with AFCONS's track record, this was a sobering moment. The backstory was complex. Shapoorji Pallonji Group began a series of divestments to reduce its debt, starting with the initial public offering of Sterling & Wilson Solar in 2019. The construction and real estate sectors, the mainstay of the SP Group, have been badly hit by the pandemic. The group needed liquidity desperately. In June 2023, the group's promoter entity Goswami Infratech raised Rs14,300 crore via zero-coupon non-convertible debentures at 18.75 per cent interest rate pledged against the shares of Tata Sons and Afcons Infrastructure.

Promoters have pledged 43.5% of their holding, indicating leverage at the promoter level, which introduces risk to Afcons' financial stability if group-level stress escalates. This wasn't a company going public from strength. It was a profitable subsidiary being monetized to shore up a struggling parent.

The market understood this. Despite AFCONS's technical excellence, global rankings, and project pipeline, investors saw the overhang. A company controlled by debt-laden promoters with pledged shares isn't the same as one with unencumbered ownership. The 7.99% listing discount reflected this reality.

Post-IPO, the shareholding structure changed but control didn't. Promoter holding at 50.2% ensured the Shapoorji Pallonji Group retained control. But now AFCONS answered to public shareholders, quarterly earnings calls, and market expectations. For a company that had thrived on patient capital and long-term thinking, this was a fundamental shift.

The IPO proceeds—Rs 80 crore for construction equipment, Rs 320 crore for working capital, Rs 600 crore for debt repayment—were sensible but unexciting. This wasn't growth capital for moonshot projects. It was housekeeping, necessary but uninspiring. The market had expected a growth story. What it got was a deleveraging exercise.

Yet beneath the disappointing debut lay unchanged fundamentals. AFCONS still had the capabilities others lacked. India's infrastructure spend was still massive. The project pipeline remained robust. The question wasn't whether AFCONS could execute—65 years had proven that. The question was whether public markets would value engineering excellence or remain fixated on financial engineering. The first day's trading suggested the latter, but as SP Group knew from building the Chenab bridge, some structures take time to reveal their strength.

VIII. Business Model & Unit Economics

Strip away the engineering marvels and global rankings, and AFCONS is fundamentally a conversion business—converting steel, concrete, and labor into infrastructure, with a spread in between. Understanding this conversion, its economics, and its constraints is key to understanding why AFCONS trades where it does despite its technical prowess.

The company operates through five business verticals: Marine & Industrial, Surface Transport, Urban Infrastructure, Oil & Gas, and Hydro & Underground. But these aren't equal contributors. Urban Infrastructure dominates at 57% of the order book as of December 2024, followed by Hydro & Underground at 25%. This concentration isn't accidental—it reflects where AFCONS's capabilities command premium pricing.

Revenue: ₹12,764 Cr, Profit: ₹533 Cr. These headline numbers look respectable until you calculate the margins: roughly 4.2% net. For context, IT services companies earn 15-20% net margins. Even manufacturing companies do better. But infrastructure is different. When your raw materials are steel and concrete, your labor is in thousands, and your customer is usually the government, margins compress.

The business model is EPC (Engineering, Procurement, and Construction) with a twist. While competitors chase volume with standard highway projects at 8-10% EBITDA margins, AFCONS targets complex projects at 12-15% EBITDA margins. The Chenab bridge might have taken 18 years, but its margins were multiples of a standard highway project. The underwater metro faced delays and cost overruns, but no one else could have built it.

Market Cap: ₹15,546 Crore, Return on equity of 13.6% over last 3 years. This ROE, while decent, reflects the capital intensity of the business. Every project requires massive upfront investment—equipment, material procurement, labor mobilization. The working capital cycle is brutal: pay suppliers in 30 days, get paid by the government in 180-360 days. Cash flow management becomes an art form.

The company has delivered a poor sales growth of 4.78% over past five years. This statistic deserves scrutiny. Why would a company with world-class capabilities in a booming infrastructure market grow so slowly? The answer lies in selectivity. AFCONS could easily double revenue by bidding aggressively for standard projects. They choose not to. Each project acceptance goes through multiple filters: technical complexity (can others do it?), margin potential (is it worth our time?), payment certainty (will we get paid?), and execution risk (can Murphy's Law destroy us?).As of 31 December 2024, the company's order book stood at Rs 38,021 crore. This order book visibility provides revenue certainty for 2-3 years but also locks in margins. Infrastructure contracts rarely have price escalation clauses that fully compensate for input cost inflation. When steel prices spike or labor costs rise, margins compress. AFCONS's Q3 FY25 results showed this dynamic: EBITDA margin improved to 13.5% from 12.3% a year earlier, but absolute profit growth lagged revenue growth.

The project execution model varies by contract type. EPC contracts transfer more risk to AFCONS but offer better margins. Item rate contracts are lower risk but also lower margin. The mix matters. Currently, about 70% of the order book is EPC, reflecting AFCONS's preference for higher-margin, higher-risk projects where technical capability matters more than price.

Working capital management remains the Achilles heel. The company's net debt was reduced to ₹2,236 crore as of March 2025, compared to ₹2,692 crore at the end of December 2024—a sign of improved financial discipline. But this is still substantial for a company with ₹533 crore in annual profit. Every project requires upfront investment that gets recovered over years. Delays in any project cascade through the system.

International projects add another layer of complexity. They typically offer 20-25% EBITDA margins versus 12-15% domestically. But they require establishing local entities, navigating foreign regulations, managing currency risk, and often partnering with local firms who may not share AFCONS's quality standards. The company has projects in over 25 countries, but international revenue remains under 20% of total—a missed opportunity or prudent risk management, depending on your perspective.

The five-year revenue CAGR of 4.78% tells a story of choice, not constraint. AFCONS could grow faster by compromising on margins, taking on riskier projects, or stretching the balance sheet. They choose not to. In a market that rewards growth over profitability, this is either admirable discipline or frustrating conservatism. The stock price suggests investors lean toward the latter interpretation.

IX. Power Dynamics: The Industry Structure

In infrastructure, the customer isn't always right—but when your customer is the government, they're always the customer. This fundamental reality shapes everything about AFCONS's business model, competitive dynamics, and future prospects. Understanding the power structure of Indian infrastructure is essential to understanding why AFCONS trades at a discount to its capabilities.

Government as the biggest customer: blessing or curse? For AFCONS, it's both. Roughly 80% of revenue comes directly or indirectly from government entities—Indian Railways, NHAI, state metro corporations, port trusts. These customers don't go bankrupt (usually), don't cancel projects (mostly), and don't negotiate post-award (technically). But they also pay slowly, change specifications midway, and award contracts to the lowest bidder who meets technical criteria.

The payment cycle is particularly brutal. A typical government project works like this: AFCONS wins a bid, mobilizes equipment and labor (cash out), procures materials (more cash out), executes work (even more cash out), submits bills (paperwork), gets bills verified (delays), receives payment (eventually). The cycle can stretch 180-360 days. Meanwhile, suppliers want payment in 30 days, workers need wages weekly. AFCONS becomes the working capital provider for India's infrastructure ambitions.

Competitive bidding dynamics create a race to the bottom that AFCONS tries to avoid. For a standard highway project, 20-30 contractors might bid. The price spread between the highest and lowest bid can be 30-40%. How? The lowest bidder either has a cost advantage, is desperate for work, or doesn't understand the project's true complexity. AFCONS rarely wins these battles and doesn't try to. They focus on projects where only 3-5 contractors globally can even submit technical bids.

But even in complex projects, margins face pressure. The Chenab bridge had only three serious contenders. The underwater metro had five. When capable contractors are few, you'd expect pricing power. But the government's procurement rules are designed to prevent "profiteering." Bids above the government's internal estimate are often rejected and re-tendered. Bids too far below raise questions about capability. The sweet spot—8-10% above the lowest technically qualified bid—becomes everyone's target.

The role of technical qualifications in creating barriers deserves attention. For the Chenab bridge, bidders needed to have built bridges above 100 meters, in seismic zones, with single spans exceeding 300 meters. How many contractors globally meet these criteria? Maybe a dozen. But the government can't award the project to the only qualifier at whatever price they quote. So they'll relax criteria slightly—maybe 80 meters is enough—until they get enough bidders for "competition." This dance between technical requirements and competitive bidding perpetually compresses margins.

International projects offer an escape from these dynamics but introduce new power imbalances. In Africa, AFCONS competes with Chinese contractors backed by state financing offering 20-year credit lines. In the Middle East, local partners are mandatory, taking their cut without adding value. In Bangladesh or Sri Lanka, political risk can nullify contracts overnight. The higher margins on international projects reflect these risks, but risk-adjusted returns might not be superior to domestic projects.

The subcontractor ecosystem represents another power dynamic. AFCONS doesn't employ 50,000 construction workers directly. They work through layers of subcontractors who provide specialized services—piling, welding, concrete work. These subcontractors have their own power dynamics. The good ones are booked years in advance. The available ones might be available for a reason. Managing this ecosystem—ensuring quality while controlling costs—becomes as important as engineering excellence.

Technology is shifting some power dynamics but slowly. Building Information Modeling (BIM) reduces design changes. Drone surveys improve monitoring. But construction remains stubbornly physical. You still need workers at height, concrete that cures properly, steel that arrives on time. Tech can optimize but can't eliminate the fundamental challenge of converting materials into infrastructure profitably.

The financial markets represent a new power center post-IPO. Previously, AFCONS answered to the Shapoorji Pallonji Group, who understood infrastructure cycles. Now they answer to quarterly earnings calls where analysts ask about margin expansion and growth acceleration. This pressure might push AFCONS toward riskier projects or aggressive bidding—exactly what they've avoided for 65 years.

ESG considerations are emerging as another power dynamic. International lenders increasingly demand environmental clearances, labor compliance, and governance standards. AFCONS's MIKE awards and systematic approach position them well here. But compliance costs money. When competing against contractors from countries with laxer standards, this becomes a disadvantage disguised as virtue.

The government's power isn't absolute—AFCONS has leverage too. When a project goes wrong, the government needs capable contractors to fix it. When a prestigious project like the Chenab bridge faces delays, reputations are at stake. AFCONS's track record of completing complex projects gives them informal power that doesn't show up in contracts but matters in practice. Still, in the infrastructure game, the house—the government—usually wins.

X. Bear vs. Bull Case

Every infrastructure stock is a bet on a story. For AFCONS, two narratives compete: the bear story of a slow-growth, capital-intensive business shackled to a debt-laden promoter, and the bull story of India's premier infrastructure specialist positioned for decades of nation-building. Both stories are true. The question is which matters more.

Bear Case:

The numbers are hard to ignore. Poor sales growth of 4.78% over past five years in an economy growing at 7% and infrastructure spending growing even faster. This isn't a sector problem—L&T's infrastructure segment grew at 15% CAGR over the same period. AFCONS is either unable or unwilling to capture growth, and neither explanation satisfies investors seeking returns.

Low return on equity of 13.6% reflects the fundamental challenge of the business model. Infrastructure contracting is inherently capital-intensive, working capital-negative, and margin-compressed. Even perfect execution yields mediocre returns. AFCONS might be best-in-class, but the class itself is unattractive. Why invest in 13.6% ROE when private banks offer 15-18% and IT services deliver 25-30%?

The capital intensity problem worsens with scale. Every new project requires equipment, mobilization costs, and working capital. Growth literally consumes cash. The recent IPO raised ₹1,250 crore fresh capital. Sounds substantial until you realize a single large project might require ₹500 crore in working capital. AFCONS faces the infrastructure contractor's paradox: the more successful you are at winning projects, the more capital you need, and the lower your returns.

Government dependency adds systemic risk. When 80% of revenue comes from government entities, you're essentially a leveraged bet on fiscal health and political priorities. If government spending slows, AFCONS has few alternatives. If payment delays worsen—as they did during COVID—AFCONS becomes an involuntary lender to the government. The company's fortunes are tied to factors entirely outside its control.

Payment delays are structural, not cyclical. Government entities pay slowly not because they're temporarily cash-strapped but because they can. No contractor sues the government—you'll never win another contract. So payment terms that would be unacceptable from private customers become business as usual with government. This isn't changing regardless of India's growth trajectory.

Execution risks in complex projects can destroy years of profits overnight. The Chenab bridge took 18 years. What if a span had collapsed during construction? The underwater metro faced multiple technical challenges. What if flooding had occurred? AFCONS takes on projects others won't touch precisely because they're risky. When risks materialize, the losses can be catastrophic. Insurance covers some risks but not reputation damage or opportunity costs.

The promoter overhang remains despite the IPO. Promoters have pledged or encumbered 53.5% of their holding. This sword of Damocles hangs over the stock. If Shapoorji Pallonji Group's financial stress worsens, forced selling could crash the stock. Even if it doesn't, the possibility constrains valuation. Why pay premium multiples for a company whose controlling shareholder might become a forced seller?

Competition is intensifying from both ends. At the premium end, international contractors are increasingly interested in India. Fluor, Bechtel, and Vinci have established Indian operations. At the commodity end, regional contractors are upgrading capabilities. The sweet spot AFCONS occupies—technically complex but not mega-scale—is shrinking.

The stock's listing at a 7.99% discount to IPO price signals market skepticism. When a company with AFCONS's track record lists below issue price in a bull market, it suggests fundamental concerns about valuation or business quality. The market's first impression matters and AFCONS failed to impress.

Bull Case:

Look beyond the numbers to the moat. AFCONS is the 10th largest international marine and port facilities contractor globally, 12th in bridges, the only Indian company in many categories. This isn't about size—it's about capability. When India needs its most critical infrastructure built, AFCONS gets the call. That positioning is irreplaceable and commands value beyond what current margins suggest.

India's infrastructure spending trajectory is extraordinary. The government has allocated ₹11.11 lakh crore for infrastructure in FY25, up from ₹10 lakh crore in FY24. This isn't a cycle—it's a structural shift. India needs to spend $1.4 trillion on infrastructure by 2030 to sustain growth. AFCONS doesn't need to capture all of it, just its fair share of the complex projects.

The technical moat in complex engineering projects is widening, not shrinking. Each successful extreme project adds to AFCONS's credentials. The Chenab bridge makes them prime candidates for other high-altitude projects. The underwater metro positions them for similar projects in other cities. Success compounds in infrastructure—reputation from one project wins the next.

Shapoorji Pallonji backing and legacy matter more than the debt overhang. Yes, the group has financial challenges. But they've been in business for 159 years, survived multiple crises, and consistently supported AFCONS. The group's construction DNA and patient capital approach align with infrastructure's long cycles. This isn't venture capital seeking quick exits—it's strategic ownership.

International diversification is reducing India risk while maintaining margins. Projects in over 25 countries provide currency diversification, exposure to different growth cycles, and higher margins. As AFCONS builds international credentials, they can be selective—choosing projects and geographies that maximize risk-adjusted returns.

The knowledge management advantage is underappreciated by markets. AFCONS is the only infrastructure company globally with nine consecutive MIKE awards. This isn't corporate fluff. It's systematic capture and deployment of learning that improves project execution, reduces risks, and enhances margins over time. While competitors rely on individual expertise, AFCONS has institutionalized excellence.

Valuation is undemanding given the quality. At current prices, AFCONS trades at about 1.2x book value and 15x P/E. For a company with global rankings, technical moats, and exposure to India's infrastructure boom, this is hardly expensive. Compare to L&T at 3x book or even regional players at 20x+ P/E. AFCONS offers better quality at lower valuations.

Operating leverage is about to kick in. As the order book of ₹38,021 crore converts to revenue, fixed costs get spread over larger revenue. The company has invested in equipment, systems, and people for larger scale. Margins should expand even with competitive pricing as utilization improves.

The infrastructure lifecycle favors established players. As projects become more complex—urban infrastructure, climate-resilient designs, smart cities—technical capabilities matter more. AFCONS's positioning at the complex end of the spectrum becomes more valuable as India's infrastructure needs sophisticate.

The bull case ultimately rests on patience. Infrastructure businesses don't deliver quarterly surprises or exponential growth. They compound steadily, building capabilities and credentials that translate to sustainable competitive advantages. For investors who can look beyond next quarter's margins to next decade's infrastructure needs, AFCONS offers exposure to India's transformation at reasonable valuations. The bears focus on today's constraints; the bulls see tomorrow's opportunities.

XI. Playbook: Lessons for Builders

AFCONS's 65-year journey from Swiss joint venture to global infrastructure player offers lessons that transcend industry boundaries. These aren't feel-good platitudes but hard-won insights from building at the intersection of engineering and economics, ambition and reality.

Building technical capabilities over decades

AFCONS didn't wake up one day capable of building the world's tallest railway bridge. The capability accumulated over decades, project by project, failure by failure. The 1959 foundation work in Nariman Point taught soil mechanics. Marine projects in the 1980s added tidal dynamics. Each project was a building block toward the next level of complexity.

The lesson: Complex capabilities can't be bought or hired—they must be built through experience. AFCONS could have remained a foundation contractor, optimizing margins in a narrow niche. Instead, they consistently chose projects slightly beyond their comfort zone. Not recklessly beyond—that leads to failure—but enough to force learning. This deliberate capability building created a moat that money alone can't replicate.

The value of patient capital (SP Group's approach)

When Shapoorji Pallonji acquired AFCONS in 2000, they didn't demand immediate returns or aggressive growth. They provided capital, connections, and most importantly, time. Infrastructure projects have long gestation periods—the Chenab bridge took 18 years. Patient capital allowed AFCONS to take on such projects without worrying about quarterly earnings.

Contrast this with private equity ownership, which typically seeks exits in 5-7 years. PE-owned infrastructure companies chase volume over value, prioritize short-term margins over long-term capabilities. SP Group's 24-year ownership before IPO let AFCONS build slowly but solidly. The lesson: Match capital structure to business characteristics. Long-cycle businesses need long-term capital.

Managing government relationships while maintaining independence

AFCONS derives 80% of revenue from government but hasn't become a government contractor in culture. They maintain private sector efficiency, invest in innovation, and critically, maintain the ability to say no to bad projects. This balance—dependent but not subservient—is delicate but essential.

The key is technical differentiation. When you can do what others can't, customers need you as much as you need them. AFCONS cultivated capabilities that made them indispensable for certain projects. The government might be slow to pay, but for underwater tunnels or high-altitude bridges, they have few alternatives. Technical excellence creates negotiating leverage even with monopolistic customers.

Knowledge management as competitive advantage

AFCONS's nine consecutive MIKE awards aren't accident or marketing. They reflect systematic investment in capturing, codifying, and disseminating learning. Every project generates knowledge—what worked, what didn't, what could be better. Most companies lose this knowledge when teams disperse. AFCONS captures it.

But capture isn't enough—knowledge must be deployed. AFCONS's knowledge management system ensures lessons from a bridge in Kashmir inform a tunnel in Kolkata. This seems obvious but is incredibly hard to execute. It requires systems, culture, and leadership commitment. The payoff: Each project stands on the shoulders of all previous projects.

When to stay private vs. go public

AFCONS stayed private for 65 years, going public only when the parent needed liquidity. This wasn't accident or inertia—it was choice. Private ownership allowed long-term thinking, patient capability building, selective project choice. The stock market would have pressured them toward quarterly growth, margin expansion, aggressive bidding.

The lesson isn't that private is always better. It's that ownership structure should align with business strategy. If your competitive advantage requires long-term thinking, patient investment, and acceptance of volatile returns, public markets might be a poor fit. AFCONS went public not because they needed growth capital but because circumstances forced it. The 7.99% listing discount suggests the market recognizes this misalignment.

International expansion without losing focus

AFCONS operates in 25+ countries but remains fundamentally an Indian company with international operations, not a global company. This distinction matters. They didn't chase international growth for its own sake but selected markets where their capabilities commanded premiums—African ports, Middle Eastern marine projects, neighboring country infrastructure.

The discipline shows in what they didn't do. No acquisitions of foreign companies. No permanent offices in dozens of countries. No trying to compete with European contractors in Europe. They exported Indian cost structures and engineering capabilities to markets that valued both. International expansion amplified strengths rather than diluting focus.

The infrastructure paradox: Success requires scale, scale destroys returns

AFCONS illustrates infrastructure's fundamental challenge: You need scale for credibility, but scale requires capital that dilutes returns. A company with ₹100 crore revenue can't bid for ₹1,000 crore projects. But growing to ₹10,000 crore revenue requires proportional working capital, equipment, and execution capacity. Returns on capital inevitably decline.

AFCONS's approach—focus on complex, high-margin projects rather than volume—represents one solution. But it limits growth. The 4.78% five-year revenue CAGR reflects this choice. They've chosen returns over growth, quality over quantity. Whether this is the right choice depends on your scorecard. For public market investors seeking growth, it's frustrating. For engineers seeking excellence, it's admirable.

Building in the physical world

In an era celebrating digital transformation, AFCONS reminds us that physical infrastructure still matters. Apps might change how we communicate, but bridges determine where we can go. Software might optimize logistics, but ports constrain trade. The digital economy runs on physical infrastructure that someone must build.

But building in the physical world is hard. Concrete doesn't scale like code. Construction workers can't work from home. Weather, geology, and physics don't care about your project timeline. AFCONS's success comes from accepting these constraints rather than fighting them. They don't pretend infrastructure is tech—they excel at what infrastructure actually is.

The compound effect of reputation

Every successful project makes the next one easier to win. Every on-time delivery builds credibility. Every technical challenge overcome adds to capability credentials. AFCONS's 65-year history is a compounding asset that new entrants can't replicate with capital alone.

But reputation is asymmetric—built over decades, destroyed in moments. One bridge collapse, one major delay, one corruption scandal could undo generations of work. This asymmetry enforces discipline. AFCONS's conservative project selection, investment in safety, and technical excellence aren't just good practice—they're existential necessities.

The playbook ultimately isn't about infrastructure. It's about building organizations that can tackle complex, long-duration challenges in regulated, capital-intensive industries where technical excellence matters more than financial engineering. These aren't the sexiest businesses, but they're the ones that literally build nations. AFCONS shows it's possible to excel in such industries, though the stock market might not always appreciate the excellence.

XII. Looking Forward: The Next Decade

The next ten years will determine whether AFCONS transforms from India's best-kept infrastructure secret into a global engineering powerhouse or remains a capable but constrained contractor in a commoditizing industry. The forces at play—India's infrastructure ambitions, climate adaptation needs, technological disruption, and succession challenges—will reshape not just AFCONS but the entire infrastructure landscape.

India's $1.4 trillion infrastructure opportunity

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube