Aegis Vopak Terminals: India's Infrastructure Play at the Intersection of Energy and Growth

I. Introduction & Episode Preview

Picture this: A massive LPG carrier, the size of three football fields, approaches the Pipavav port on India's western coast. Inside its refrigerated tanks sits 44,000 tons of liquefied petroleum gas—enough cooking fuel for millions of Indian households. As the ship docks, a complex ballet begins. Specialized arms connect to the vessel, cryogenic pumps hum to life, and the precious cargo flows into towering storage spheres that gleam like giant pearls against the Gujarat coastline.

This is the daily reality at Aegis Vopak Terminals (AEGISVOPAK), where engineering meets economics at the most fundamental level of India's energy infrastructure. The company operates 20 tank terminals across six strategic Indian ports, with storage capacity of 1.7 million cubic meters for liquids and 201,000 metric tons for LPG. But those numbers barely scratch the surface of what makes this story fascinating.

The big question we're exploring today: How did a 2013 startup joint venture transform into a critical infrastructure player backed by two giants—India's Aegis Logistics and the Netherlands' Royal Vopak, a company with over 400 years of heritage operating 77 terminals across 23 countries? And why does this matter for understanding India's next decade of growth?

At a market capitalization of ₹26,678 crores, AEGISVOPAK isn't just another industrial company. It's a window into India's energy transition, the mechanics of global trade, and the art of building monopoly-like positions in plain sight. The company controls approximately 25% of India's third-party storage capacity—a position that becomes more valuable every year as India's energy demands surge.

What we'll uncover is a story of perfect timing meeting patient capital, where government policy catalyzed private investment, and where boring infrastructure became anything but boring returns. We'll explore how two companies from different continents saw the same opportunity, how they structured one of India's most interesting joint ventures, and why they chose to take this combined entity public in 2025.

This isn't just about tanks and terminals. It's about understanding how India will feed its energy appetite as it becomes the world's third-largest economy, why port infrastructure determines the cost of cooking fuel for a billion people, and how smart operators position themselves at inevitable chokepoints in global supply chains.

II. The Parent Companies: Building the Foundation

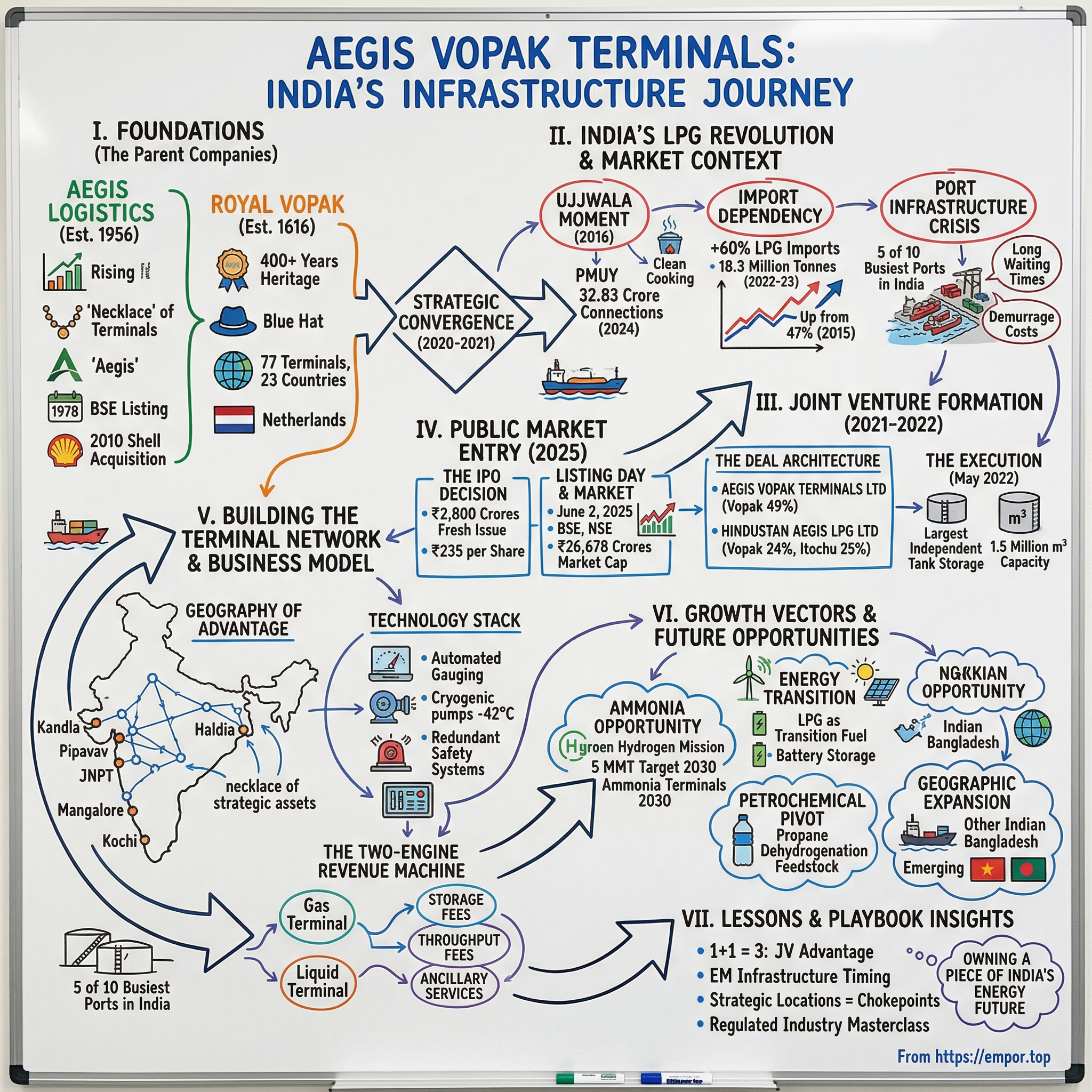

The Aegis Story: From Trading House to Infrastructure Giant

In 1956, as India was still finding its feet as an independent nation, the Chandaria family established what would become Aegis Logistics. But the real story begins decades later, in the liberalization era of the 1990s, when Anand Chandaria returned from the United States with a vision that seemed almost absurd: India would one day consume LPG like developed nations.

Chandaria had spent years observing energy markets in America, where propane was as common as water. Back in India, less than 5% of households used LPG for cooking. Most relied on wood, coal, or kerosene—dirty fuels that filled homes with smoke and caused countless respiratory problems. Chandaria saw not just a business opportunity but an inevitable transition.

"The question wasn't if India would adopt clean cooking fuel," he would later tell investors, "but when and how fast. "Established in 1956, Aegis Logistics evolved from a basic trading house into India's leading private-sector LPG company and logistics provider. The company's transformation really accelerated after its 1978 BSE listing, when it began building what would become a "necklace" of terminals across India's major ports—a poetic description for what is essentially strategic infrastructure dominance.

By the 2000s, under the Chandaria family's leadership, Aegis had made a crucial strategic pivot. Rather than compete head-to-head with state-owned oil giants in retail distribution, they focused on becoming the infrastructure backbone that everyone—including those giants—would need. They built terminals where others built gas stations. They invested in import infrastructure while others fought over market share.

The company's major breakthrough came in 2010 when it acquired Shell's gas business in India, instantly gaining 30 LPG bottling plants and distribution across 15 states. This wasn't just an acquisition; it was a statement that Aegis intended to be a permanent, scaled player in India's energy landscape.

Royal Vopak: Four Centuries of Tank Storage Excellence

While Aegis was building its Indian empire, Royal Vopak's story stretches back to 1616—yes, the same era as the Dutch East India Company. In that year, a group of porters who carried goods between Oost-Indische vessels and Amsterdam's weighing house formed the Blauwhoed ("blue hat") company.

The modern Vopak was created in 1999 through the merger of Van Ommeren and Pakhoed, two Dutch logistics giants with centuries of combined history. Van Ommeren, founded in 1839 as a shipping and forwarding agent, had become a leading force in tank storage operations by the beginning of the 20th century.

What made Vopak fascinating wasn't just its age but its strategic evolution. As the world's leading independent tank storage company with over 400 years of history, Vopak had mastered something crucial: being the neutral Switzerland of energy infrastructure. They didn't compete with their customers; they enabled them.

By the 2020s, Vopak operated 77 terminals across 23 countries, storing everything from crude oil to vegetable oils, from chemicals to LNG. But here's where it gets interesting for our story: Vopak saw Asia, and particularly India, as its next frontier. The company had been watching India's infrastructure boom, its growing energy imports, and most importantly, the structural inefficiencies in its port infrastructure.

The Strategic Convergence

So we have two companies: Aegis, with deep local knowledge and established infrastructure but capital constraints for aggressive expansion. And Vopak, with global expertise, deep pockets, and a strategic mandate to grow in Asia. Both saw the same opportunity—India's massive infrastructure gap in energy storage—but from different angles.

The timing was perfect. India's economy was recovering from COVID, energy demand was surging, and the government's push for cleaner cooking fuel through schemes like Ujjwala Yojana had created unprecedented demand for LPG infrastructure. The stage was set for one of India's most strategic joint ventures.

III. India's LPG Revolution & Market Context

The Ujjwala Moment That Changed Everything

On May 1, 2016, something extraordinary happened. Prime Minister Narendra Modi launched the Pradhan Mantri Ujjwala Yojana (PMUY) from Ballia, Uttar Pradesh. The target seemed impossible: provide 50 million LPG connections to women from Below Poverty Line families within three years. The actual achievement? In the first year of its launch, connections distributed were 22 million against the target of 15 million. As of 23 October 2017, 30 million connections were distributed, 44% of which were given to families belonging to scheduled castes and scheduled tribes. The number crossed 58 million by December 2018.

By November 2024, the number of LPG connections had increased from 14.52 crores in 2014 to 32.83 crores, with a growth of over 100%. The number of Pradhan Mantri Ujjwala Yojana beneficiaries reached 10.33 crores as of November 1, 2024.

This wasn't just about distributing gas cylinders. It was about transforming how a billion people cooked their meals. The scheme tackled India's silent killer—indoor air pollution from traditional cooking fuels like wood and coal, which caused respiratory diseases and premature deaths, particularly among women and children.

The Import Dependency Reality

Here's the stark reality that set the stage for AEGISVOPAK's opportunity: India's LPG supply chain relies heavily on imports (over 60%), with dependence on imported liquefied petroleum gas rising to 64% in 2022-23, up from 49% six years earlier. In fiscal year 2022-23, India imported 18.3 million tonnes of LPG valued at US$13.8 billion, with India importing around 67% of its domestic requirement in 2024, up from 47% in 2015.

The growth trajectory was staggering. LPG consumption grew by 32%, while domestic production only grew by 14%. India's overall LPG consumption rose to a record high of 31 million tonnes in 2024, up by 7% on the year.

This created a perfect storm: surging demand from government schemes, limited domestic production capacity, and an import dependency that was only growing. Every ton of imported LPG needed to be stored somewhere before reaching consumers. That "somewhere" was the business opportunity of the century.

The Port Infrastructure Crisis

Out of the ten busiest LPG ports in the world, five of them are in India and in terms of LPG ports with the longest waiting times, five of the ten globally are also in India. This congestion slows down LPG delivery, increases costs, and is inefficient.

Think about that for a moment. Half of the world's most congested LPG ports were in India. Ships waited days, sometimes weeks, to unload their cargo. Every day of delay meant higher costs—demurrage charges, opportunity costs, and ultimately higher prices for consumers. The bottleneck wasn't just an operational nuisance; it was a national economic issue.

The problem wasn't going away. With import requirements set to reach 20-21 million metric tons per annum in the next 2-3 years, India needed massive infrastructure investment. But building terminals isn't like building apartments. You need deep-water port access, environmental clearances, safety certifications, and most importantly, the technical expertise to handle cryogenic materials at scale.

This is where our story converges. Aegis had the local knowledge and existing infrastructure. Vopak had the global expertise and capital. The Indian government had the political will to solve the infrastructure crisis. All the pieces were in place for what would become one of India's most strategic joint ventures.

IV. The Joint Venture Formation (2021-2022)

The Announcement That Changed Everything

On July 12, 2021, the corporate world witnessed one of India's most strategic infrastructure deals. Aegis and Vopak announced that the companies have decided to join forces in India with the aim to grow together in the LPG and chemicals storage and handling business. But the story behind this announcement was years in the making.

The negotiations had started quietly in 2020, during the pandemic. While the world was locked down, energy demand had cratered globally—but not in India. LPG consumption actually increased as more people cooked at home. Both companies saw the same data: India's structural demand for LPG wasn't a bubble; it was a decades-long growth story just beginning.

Raj Chandaria, Chairman of Aegis Logistics, had been thinking about this partnership for years. "This joint venture with Vopak will accelerate the growth of Aegis in the terminals business and has the potential to allow Aegis to diversify into new areas of gas storage such as LNG and other energy projects including renewables, in partnership with the world's leading independent tank storage company."

From Vopak's perspective, this was about strategic capital allocation. Eelco Hoekstra, Chairman of the Executive Board and CEO of Royal Vopak, framed it perfectly: "This is an investment in a growth market and by joining forces with Aegis we aim to deliver growth over the next ten years in line with the new joint ventures' and India's ambition for LPG."

The Deal Architecture: A Masterclass in JV Structuring

The transaction structure was elegant in its complexity. This wasn't a simple acquisition or merger—it was a carefully orchestrated combination that preserved the interests of all parties while creating something entirely new.

The transaction entailed two separate legal entities that Vopak would simultaneously buy into on the basis of joint control:

First, the Aegis Vopak Terminals Ltd entity, in which Vopak would acquire a 49% shareholding. Vopak's existing CRL terminal entity in Kandla would become a wholly owned subsidiary of Aegis Vopak Terminals Ltd. Aegis' network of terminal assets at 5 different locations in Kandla, Pipavav, Mangalore, Kochi and Haldia covering the west and east coast of India would be added to the joint venture asset base.

Second, the Hindustan Aegis LPG Ltd entity, in which Vopak would acquire a 24% shareholding. This was currently a joint venture between Aegis and Itochu. After the transaction Aegis would own 51% and Itochu would continue to hold 25%.

The financial engineering was equally sophisticated. The enterprise value for Vopak's shareholding in the joint ventures would amount to EUR 185 million plus EUR 15 million, depending on the fulfilment of certain conditions. Aegis would receive total gross pre-tax cash proceeds from the sale of up to Rs 2,766 crores.

The Execution: From Announcement to Completion

The transaction was expected to close early 2022, subject to customary closing conditions. But between announcement and closing, something interesting happened. The deal got better.

When the partnership was successfully completed on May 25, 2022, three additional terminals with an additional capacity of 490 thousand cbm were included in the partnership. Vopak's net consideration at closing changed from EUR 115 million announced in July 2021 to EUR 137 million. The amount increased as a result of foreign exchange movements of EUR 12 million and EUR 10 million for the three additional terminals and additional growth projects.

The final entity that emerged was formidable. Aegis Vopak Terminals would become the largest independent tank storage company for LPG and chemicals in India. The partnership operated a network of 11 terminals located in five strategic ports along the east and west coast of India with a total capacity of approximately 1.5 million m3.

What made this deal special wasn't just its size but its timing. India was at an inflection point—growing energy demand, government support for clean cooking fuel, and massive infrastructure gaps. The joint venture was positioned to capture all three trends simultaneously.

V. The IPO Story & Public Market Entry (2025)

The Decision to Go Public

By late 2024, Aegis Vopak Terminals had proven its model. The company was generating steady cash flows, had identified massive expansion opportunities, and needed capital to execute its vision. The board made a strategic decision: it was time to tap the public markets. The IPO announcement came at an opportune moment. The company decided to raise ₹2,800 crores through a fresh issue of 11.91 crore shares, priced at ₹235 per share. The timing was strategic—India's infrastructure story was gaining global investor attention, and the energy transition narrative was compelling.

The IPO structure was straightforward: entirely fresh issue, no offer for sale. This meant all proceeds would go to the company for growth, not to existing shareholders cashing out. The use of proceeds was clearly articulated: repayment of borrowings, funding capital expenditure for Mangalore cryogenic LPG terminal acquisition, and general corporate purposes.

The Anchor Investor Response

On May 23, 2025, three days before the IPO opened to the public, the company raised ₹1,260 crores from anchor investors. This was a crucial validation—institutional investors were willing to commit significant capital before retail investors even had a chance to participate.

The anchor book attracted a diverse mix of global and domestic institutions, though the specific names weren't disclosed in public filings. What mattered was the message: smart money believed in the story.

The Public Subscription Drama

When the IPO opened for subscription on May 26, 2025, the initial response was tepid. The grey market premium (GMP) started at ₹17 on May 24 but fell to just ₹2 by May 28, the closing day. This volatility reflected market uncertainty about the valuation.

The retail portion saw modest subscription, while institutional investors showed more enthusiasm. The QIB portion was allocated 75% of the issue, NII got 15%, and retail investors received 10%—a standard allocation for large IPOs.

Listing Day and Market Reception

On June 2, 2025, AEGISVOPAK made its debut on the BSE and NSE. The shares listed at a modest premium to the issue price, reflecting cautious optimism rather than euphoria. The market capitalization at listing was ₹26,678 crores, instantly making it one of India's larger infrastructure plays.

What's remarkable about the IPO wasn't the listing day pop—there wasn't much of one. Instead, it was what the IPO represented: a mature infrastructure business going public not for a quick flip but to fund long-term growth. The company had explicitly stated its intention to evaluate opportunities in ammonia terminals, industrial terminals, and alternative energies with cumulative capex of Rs 90 billion by FY30.

The IPO transformed AEGISVOPAK from a closely-held joint venture into a public company with institutional scrutiny and retail participation. For Aegis and Vopak, this was validation of their strategy. For public market investors, it was access to a quasi-monopolistic infrastructure asset at the heart of India's energy transition.

VI. Building the Terminal Network

The Geography of Advantage

Stand at the Pipavav port on a clear morning, and you'll see the genius of AEGISVOPAK's network strategy. The company didn't just build terminals; it built a necklace of strategic assets across India's coastline. With 20 tank terminals across 6 key Indian ports—Haldia, Kandla, Pipavav, Mangalore, Kochi, and the upcoming JNPT—the company controls approximately 25% of India's third-party storage capacity.

Each location was chosen with surgical precision. Kandla, on the west coast, is India's closest port to the Middle East, source of 97% of India's LPG imports. Haldia, on the east coast, serves the industrial heartland of eastern India. Pipavav offers deep-draft facilities for the largest LPG carriers. Mangalore and Kochi serve the consumption centers of South India.

The network effect is powerful. When a customer signs up with AEGISVOPAK, they're not just getting storage at one location—they're getting access to a pan-India infrastructure network. An importer can bring LPG into Kandla and distribute it across the country using AEGISVOPAK's facilities as staging points.

The Technology Stack Nobody Talks About

What separates world-class terminal operators from everyone else isn't visible to the naked eye. It's the technology embedded in every valve, pump, and control system.

AEGISVOPAK's terminals operate with automated tank gauging systems that measure product levels to millimeter accuracy. Temperature and pressure are monitored continuously—critical for LPG, which must be stored at -42°C to remain liquid. The company uses sophisticated blending systems that can mix different grades of products to exact specifications while the product is being loaded.

Safety systems are redundant by design. Automated shutdown valves can isolate any section of the terminal within seconds. Fire suppression systems use foam that can blanket an entire tank farm in minutes. Gas detection systems can identify leaks at parts-per-million concentrations, well below dangerous levels.

But perhaps the most sophisticated technology is the terminal automation system. Every movement of product—from ship to tank, tank to truck, tank to pipeline—is controlled by computers that optimize flow rates, minimize energy consumption, and ensure product quality. A typical large ship discharge that once required dozens of operators now needs just a handful of highly trained technicians.

The Art of Capacity Expansion

Building new storage capacity in India is an exercise in patience and politics. Environmental clearances can take years. Land acquisition, especially near ports, involves navigating complex ownership structures and political sensitivities. Construction must account for monsoons, labor availability, and equipment imports.

AEGISVOPAK has mastered this process. The company's expansion from 960,000 cubic meters in 2021 to 1.7 million cubic meters for liquids and 201,000 MT for LPG by 2024 didn't happen by accident. Each expansion was timed to coincide with demand growth, ensuring high utilization from day one.

The Mangalore cryogenic LPG terminal acquisition, funded partly through the IPO proceeds, exemplifies this strategy. Rather than building from scratch, the company acquired an existing facility and plans to upgrade it. This approach cuts development time by years and reduces execution risk.

The Customer Ecosystem

AEGISVOPAK's customer base reads like a who's who of global energy and chemicals. The company serves traders, manufacturers, chemical companies, and fuel marketers across both private and public sectors. Oil majors use the terminals for strategic storage. Trading houses use them for arbitrage plays. Chemical companies use them for feedstock security.

What's less obvious is how these relationships create competitive moats. Many customers have invested in dedicated pipelines, loading facilities, and IT systems that connect to AEGISVOPAK's infrastructure. Switching to another terminal operator would mean writing off these investments and disrupting operations.

The company has also developed specialized capabilities for specific products. Handling molten sulfur requires heated tanks and specialized loading arms. Storing caustic soda needs corrosion-resistant materials. Each product category represents years of accumulated expertise that competitors can't easily replicate.

VII. Business Model & Unit Economics

The Two-Engine Revenue Machine

AEGISVOPAK operates through two distinct divisions that together create a resilient revenue model. The Gas Terminal Division focuses on LPG storage and handling, while the Liquid Terminal Division manages everything from petroleum products to vegetable oils and chemicals.

The beauty of this model lies in its simplicity. Customers pay for storage (a monthly fee based on tank capacity reserved), throughput (a fee for every ton of product moved through the terminal), and ancillary services (heating, cooling, blending, drumming). It's a toll-booth model where AEGISVOPAK clips a fee every time product moves through its facilities.

Storage contracts typically run 1-3 years with take-or-pay provisions. This means customers pay for reserved capacity whether they use it or not. Throughput fees provide upside when volumes are high but storage fees provide the stable base. In 2024, the company generated revenue of ₹624 crores, a 10.38% increase year-over-year.

The Working Capital Advantage

Unlike manufacturing businesses that tie up capital in inventory, AEGISVOPAK's working capital requirements are minimal. The company doesn't own the products it stores—customers do. This means AEGISVOPAK can grow revenue without proportional increases in working capital.

The cash conversion cycle is remarkably efficient. Storage fees are typically collected monthly in advance. Throughput fees are invoiced immediately upon product movement. Bad debts are virtually non-existent because the company has a lien on stored products. If a customer doesn't pay, AEGISVOPAK can legally sell their inventory to recover dues.

This capital-light model in operations (though capital-intensive in infrastructure) means that once a terminal is built, incremental revenue drops almost directly to the bottom line. The 2024 earnings of ₹127 crores, up 47.01% from the previous year, demonstrate this operating leverage in action.

The Utilization Game

Terminal economics are driven by utilization rates. A tank that's 90% full generates nearly the same costs as one that's 50% full—but almost twice the revenue. This creates tremendous operating leverage as utilization increases.

AEGISVOPAK benefits from structural factors that keep utilization high. India's import dependence means consistent cargo arrivals. Seasonal demand patterns (higher LPG consumption in winter) require year-round storage capacity. Minimum inventory requirements for supply security mean tanks rarely sit empty.

The company manages utilization through sophisticated yield management. Like airlines overbooking flights, terminals can "oversell" capacity because not all customers use their full allocation simultaneously. Product compatibility allows flexible tank allocation—a tank storing diesel today can store jet fuel tomorrow with minimal cleaning.

Pricing Power Dynamics

Terminal storage pricing is one of the least transparent markets in energy infrastructure. Unlike LPG prices, which are publicly quoted and tracked daily, terminal storage rates are negotiated privately and rarely disclosed. This opacity works to AEGISVOPAK's advantage.

The company benefits from several pricing dynamics. First, switching costs are high—once a customer builds infrastructure to connect to a terminal, moving to a competitor requires significant capital investment. Second, location matters enormously. A terminal next to a refinery or major consumption center can charge premium rates. Third, capacity constraints mean pricing power increases when utilization is high.

India's port congestion adds another layer of pricing power. When ships wait weeks to discharge cargo (as they often do at Indian ports), the value of available storage skyrockets. AEGISVOPAK can charge premium rates for immediate availability or guaranteed discharge slots.

VIII. Competitive Landscape & Market Position

The State-Owned Giants

AEGISVOPAK's main competition comes from India's state-owned oil companies—Indian Oil Corporation (IOC), Bharat Petroleum (BPCL), and Hindustan Petroleum (HPCL). These companies operate their own terminals primarily for captive use but also offer third-party storage.

The state-owned companies have advantages: government backing, existing refinery integration, and established distribution networks. But they also have disadvantages: bureaucratic decision-making, political interference in commercial decisions, and less flexibility in contract terms.

AEGISVOPAK has positioned itself as the Switzerland of storage—neutral, reliable, and professional. While state-owned terminals might prioritize their parent company's cargo, AEGISVOPAK treats all customers equally. This neutrality is particularly valuable for international traders and private Indian companies who compete with state-owned firms.

The New Challenger: BW LPG's Mega Terminal

The most significant competitive threat comes from BW LPG's massive terminal project at Jawaharlal Nehru Port (JNPT) near Mumbai. With a capacity of 2.5 million tons per annum and 120,000 cubic meters of storage, this facility will be India's largest cryogenic LPG storage terminal when completed.

BW LPG's terminal has several advantages. It can fully offload the latest fourth-generation VLGCs (93,000 cbm) in a single 24-hour discharge operation—a capability that addresses India's chronic port congestion. The terminal will connect to the Uran-Chakan pipeline, providing direct access to inland markets.

But AEGISVOPAK isn't standing still. The company's response has been strategic rather than reactive. Instead of competing head-to-head at JNPT, AEGISVOPAK is expanding at other locations where it already has established positions. The Mangalore cryogenic LPG terminal acquisition gives them presence on the west coast away from Mumbai's congestion.

The Moat That Matters

What really protects AEGISVOPAK isn't just physical infrastructure—it's the ecosystem they've built around it. Multi-year contracts with sticky customers. Specialized handling capabilities developed over decades. Relationships with port authorities that ensure preferential berthing rights. Safety records that allow handling of hazardous products others can't touch.

The company also benefits from what economists call "spatial monopolies." Once you've built a terminal at a specific location, it's economically irrational for a competitor to build right next door unless demand has doubled. The capital requirements, time to build, and customer acquisition costs create natural barriers.

Network effects amplify these advantages. As AEGISVOPAK adds terminals, the value to customers increases exponentially. A customer can now optimize inventory across multiple locations, arbitrage price differences between regions, and ensure supply security through geographic diversification.

IX. Future Growth Vectors & Strategic Opportunities

The Ammonia Opportunity

AEGISVOPAK's most intriguing growth opportunity lies in ammonia terminals. As the world transitions to clean energy, ammonia is emerging as a crucial vector for hydrogen transport and storage. Green ammonia, produced using renewable energy, can be shipped globally and either used directly as fuel or cracked back into hydrogen at the destination.

India's National Green Hydrogen Mission targets production of 5 million metric tons of green hydrogen by 2030. Much of this will likely be transported as ammonia, requiring specialized storage infrastructure. AEGISVOPAK is evaluating opportunities in ammonia terminals with cumulative capex of Rs 90 billion by FY30.

Ammonia storage isn't just LPG storage with a different product. It requires specialized materials (ammonia is highly corrosive), sophisticated safety systems (ammonia is toxic), and different temperature controls (-33°C for ammonia vs -42°C for propane). But the basic competencies—cryogenic storage, safety management, port operations—transfer directly.

The Energy Transition Play

The energy transition isn't just about moving from fossil fuels to renewables—it's about managing the decades-long transition period. AEGISVOPAK is perfectly positioned for this transition.

LPG will remain crucial as a transition fuel. It's cleaner than coal or wood, requires minimal infrastructure changes for consumers, and can be deployed immediately. Even as India builds renewable capacity, LPG will be needed for cooking, industrial heat, and backup power generation.

But AEGISVOPAK is also preparing for what comes next. The company is exploring battery energy storage systems at its terminals, which could provide grid stabilization services while generating additional revenue. Terminals could become energy hubs, storing not just molecules but electrons.

Geographic Expansion Possibilities

While AEGISVOPAK dominates at existing locations, India has 12 major ports and over 200 smaller ports. Each represents a potential expansion opportunity. The company is particularly interested in east coast expansion, where industrial growth is accelerating but infrastructure lags the west coast.

International expansion is another vector. Vopak's global network provides a template for replicating the Indian model in other emerging markets. Bangladesh, Vietnam, and Indonesia face similar challenges: growing energy demand, high import dependence, and inadequate storage infrastructure.

The Petrochemical Pivot

India's petrochemical demand is exploding. As the country manufactures more plastics, textiles, and chemicals, the need for petrochemical feedstock storage grows. AEGISVOPAK already handles various chemicals, but there's opportunity to specialize further.

Propane dehydrogenation (PDH) plants, which convert propane to propylene for plastics production, need reliable propane supply. Ethane crackers require ethane storage. Each new petrochemical plant is a potential anchor customer for a storage terminal.

The company's liquid terminals can be reconfigured for different products as market demand shifts. A tank storing diesel today could store naphtha tomorrow or benzene next year. This flexibility allows AEGISVOPAK to capture value across petrochemical cycles.

X. Financial Analysis & Investment Case

Understanding the Valuation Paradox

At first glance, AEGISVOPAK's valuation metrics seem absurd. A P/E ratio of 210-227. A P/B ratio of 28.96. A three-year average ROE of just 7.34%. In any other industry, these numbers would scream "overvalued" and "sell immediately."

But infrastructure assets don't follow normal valuation rules. The company is essentially a collection of long-lived, irreplaceable assets that generate predictable cash flows for decades. Think of it less like a company and more like a portfolio of toll roads that happen to store energy products.

The low ROE reflects the capital intensity of the business and recent major expansions that haven't yet reached full utilization. As these assets mature and utilization increases, returns should improve dramatically. The high P/E ratio reflects the market's expectation of this improvement.

The Capital Allocation Framework

AEGISVOPAK faces a classic infrastructure investor's dilemma: massive growth opportunities but equally massive capital requirements. The company plans cumulative capex of Rs 90 billion by FY30—that's over $1 billion at current exchange rates.

The IPO proceeds provide some breathing room, allowing the company to fund the Mangalore acquisition and reduce debt. The expected net cash position in FY26 gives flexibility for opportunistic investments. But beyond that, the company will likely need to tap debt markets again.

The key question for investors: Can AEGISVOPAK earn returns above its cost of capital on new investments? Historical evidence suggests yes—established terminals generate strong cash flows once ramped up. But execution risk on new projects remains real.

The Bear Case

Several factors could derail the AEGISVOPAK story. A faster-than-expected energy transition could strand LPG assets. India's notorious bureaucracy could delay expansion plans. New competitors with deep pockets (like BW LPG) could compress margins. A global recession could reduce energy demand and utilization rates.

The biggest risk might be technological. If someone develops a way to economically store and transport LPG without massive terminal infrastructure—perhaps through small-scale modular storage or virtual pipelines—AEGISVOPAK's moat evaporates.

Regulatory risk also looms. The government could impose price controls on storage fees, mandate open access that reduces pricing power, or change environmental regulations that require costly retrofits.

The Bull Case

But the bull case remains compelling. India's energy demand will grow—that's not speculation but demographic destiny. The country's working-age population won't peak until 2040. Urbanization continues at 2% annually. Industrial production must increase to provide jobs and growth.

Infrastructure assets with monopoly characteristics in growing markets rarely disappoint long-term investors. AEGISVOPAK isn't just riding India's growth; it's enabling it. Every ton of LPG imported, every chemical stored, every ship discharged efficiently contributes to India's economic development.

The energy transition, rather than a threat, could be an opportunity. Green ammonia, hydrogen, sustainable aviation fuel—all require storage infrastructure. AEGISVOPAK's existing footprint, operational expertise, and customer relationships position it to capture these new markets.

Climate change adds another dimension. As weather becomes more volatile, energy security becomes paramount. Strategic storage—whether LPG for cooking or ammonia for fertilizer—becomes more valuable. Governments and companies will pay premiums for supply security.

XI. Lessons & Playbook Insights

When 1+1 Equals 3: The JV Advantage

The Aegis-Vopak joint venture demonstrates how complementary partners can create extraordinary value. Aegis brought local knowledge, existing infrastructure, and regulatory relationships. Vopak brought global expertise, technical capabilities, and patient capital. Neither could have achieved alone what they built together.

The structure was crucial. Rather than a full merger or acquisition, the JV preserved both companies' strengths while eliminating weaknesses. Aegis shareholders got access to global best practices and capital. Vopak got immediate scale in India without starting from scratch.

For investors, the lesson is clear: Look for situations where strategic partners can unlock value that neither can access independently. The best JVs aren't just about sharing costs—they're about combining capabilities to attack opportunities neither partner could capture alone.

Infrastructure Investing in Emerging Markets

AEGISVOPAK exemplifies both the opportunities and challenges of infrastructure investing in emerging markets. The opportunity is obvious: massive unmet demand, structural growth drivers, and limited competition. The challenges are equally clear: regulatory uncertainty, execution complexity, and capital intensity.

The key insight is timing. AEGISVOPAK entered the market early enough to establish dominant positions but late enough that demand was proven. They didn't try to create the market—they captured existing demand that was poorly served.

Infrastructure investors should look for similar dynamics: proven demand, inadequate supply, regulatory tailwinds, and the ability to establish defensible positions before competition arrives.

The Power of Strategic Locations

In infrastructure, location isn't just important—it's everything. AEGISVOPAK's terminals aren't randomly distributed; each represents a strategic chokepoint in India's energy supply chain. Kandla for Middle East imports. Haldia for eastern industrial demand. Pipavav for deep-water vessels.

Once established at a prime location, the advantage compounds. Customers invest in connecting infrastructure. Competitors can't economically build nearby. Regulatory approvals become easier for expansions than greenfield projects.

The lesson extends beyond physical infrastructure. In any network-effect business, early positioning at critical nodes creates lasting advantages. Whether it's terminals at ports or servers at internet exchange points, controlling chokepoints generates outsized returns.

Building in Regulated Industries

Operating in regulated industries requires a different playbook than pure free-market competition. AEGISVOPAK has mastered this game. They maintain excellent relationships with regulators, exceed safety and environmental standards, and position themselves as partners in national development rather than profit-maximizing corporations.

This approach pays dividends. When regulators trust you, approvals come faster. When communities support you, expansion faces less opposition. When government sees you as solving national problems, policy winds blow in your favor.

The key is authentic alignment with public interest. AEGISVOPAK genuinely enables India's energy security and economic development. The profits follow naturally from solving real problems rather than extracting rents from regulatory capture.

XII. Final Thoughts & "What Would We Do?"

The Biggest Surprises

Researching AEGISVOPAK revealed several surprises. First, the sheer scale of India's infrastructure gap. Five of the world's ten most congested LPG ports are in India—that's not just an operational problem but a macroeconomic constraint.

Second, the sophistication required to operate "simple" storage terminals. The technology, safety systems, and operational complexity rival any advanced manufacturing facility. This isn't just land with tanks—it's highly engineered infrastructure requiring specialized expertise.

Third, the strategic importance of "boring" businesses. Storage terminals don't capture headlines like electric vehicles or artificial intelligence. But they're fundamental to economic functioning. Without adequate storage, India's energy transition simply can't happen.

The Next Decade

Looking forward, AEGISVOPAK faces a decade of extraordinary opportunity and challenge. India's energy demand will grow—that's certain. But the form that energy takes, how it's transported, and where it's stored remain open questions.

The company's success will depend on three factors. First, execution on the massive capex program without destroying returns. Second, successful navigation of the energy transition, positioning for both current fossil fuels and future clean energy. Third, maintaining operational excellence while scaling rapidly.

If AEGISVOPAK succeeds, it could become one of Asia's premier infrastructure companies—a Brookfield or Macquarie of emerging markets. If it fails, it becomes a cautionary tale about capital allocation and execution risk in complex markets.

If We Were Running AEGISVOPAK Today

Three strategic priorities would dominate our agenda:

First, accelerate the ammonia/hydrogen infrastructure build. The energy transition is happening faster than most expect. First movers in clean energy infrastructure will capture disproportionate value. We'd rather be too early than too late.

Second, deepen the moat through technology and service. Pure storage is commoditizing. But storage plus value-added services—blending, heating, quality certification, inventory management—creates stickiness and pricing power. We'd invest heavily in digital capabilities that make AEGISVOPAK indispensable to customers.

Third, expand internationally while maintaining Indian dominance. Vopak's global network provides a template for replicating the Indian model. We'd target one or two similar markets—perhaps Bangladesh or Vietnam—while ensuring Indian operations remain world-class.

The biggest risk isn't competition or technology—it's complacency. When you dominate a market, the temptation is to milk existing assets rather than invest for the future. But infrastructure is a long game. The terminals AEGISVOPAK builds today will operate for 50+ years. The decisions made now determine not just next quarter's earnings but next generation's energy system.

The Investment Decision

So should investors buy AEGISVOPAK at current valuations? The answer depends on time horizon and risk tolerance.

For short-term traders, the stock is probably too expensive. The P/E ratio leaves little room for error. Any execution stumble or regulatory change could trigger significant downside.

But for long-term investors who understand infrastructure dynamics, AEGISVOPAK represents a unique opportunity to own a piece of India's energy future. The company controls irreplaceable assets at strategic locations in the world's fastest-growing major economy. The energy transition, rather than obsoleting these assets, makes them more valuable as storage becomes crucial for supply chain resilience.

The real question isn't whether AEGISVOPAK is expensive today—it's whether India's energy infrastructure needs will grow as expected. If you believe in India's growth story, AEGISVOPAK is one of the purest plays on that theme. If you're skeptical about India or worried about the energy transition, look elsewhere.

Infrastructure investing requires patience, conviction, and the ability to look through short-term volatility to long-term value creation. AEGISVOPAK embodies both the promise and peril of this approach. The company is building critical infrastructure for a growing nation—a noble mission that happens to be excellent business.

The journey from joint venture to public company is complete. But for AEGISVOPAK, the real journey—becoming India's energy infrastructure backbone—has just begun.

XIII. Recent News

Q2 FY25 Results and Momentum Building

In the first quarter of FY25, revenue went up by 34.7%, and profit increased by 185.5% compared to last year. This explosive growth trajectory continued through subsequent quarters, demonstrating the operational leverage inherent in the business model as terminal utilization rates increased.

The parent company Aegis Logistics held its Q2 FY25 earnings call on November 11, 2024, where management highlighted the strong performance of AEGISVOPAK's terminals division. Aegis Logistics Q2FY25 Earnings Call Invite- 11-11-2024 demonstrated continued investor interest in the infrastructure story.

Strategic Expansion Announcements

Throughout 2024 and early 2025, AEGISVOPAK made several critical announcements regarding its expansion plans. The company's acquisition of the Mangalore cryogenic LPG terminal, funded through IPO proceeds, represents a significant capacity addition on the west coast. It expanded the liquid terminals in Kandla and Kochi in March 2024 and has acquired the Nandella Terminal in Mangalore.

The commissioning of new facilities continued at a rapid pace. The Company commissioned 2 propylene rated Spheres at Pipavav in February 2024. These propylene-rated spheres are crucial for serving the petrochemical sector, demonstrating AEGISVOPAK's diversification beyond pure LPG storage.

India's Green Ammonia Revolution Takes Shape

The ammonia opportunity that AEGISVOPAK is evaluating has gained significant momentum. India's National Green Hydrogen Mission has set ambitious targets, with A global demand of over 100 MMT of Green Hydrogen and its derivatives like Green Ammonia is expected to emerge by 2030. Aiming at about 10 per cent of the global market, India can potentially export about 10 MMT Green Hydrogen/Green Ammonia per annum.

Major international partnerships are already forming. Japanese engineering conglomerate IHI has signed a term sheet with Indian renewables developer ACME for 400,000 tonnes a year of green ammonia offtake starting from 2028. Similarly, BASF and AM Green B.V. have entered a memorandum of understanding (MoU) to jointly evaluate and develop business opportunities for low-carbon chemicals produced exclusively with renewable energy, and the corresponding value chains in India. The cooperation also includes a non-binding letter of intent for the offtake of 100,000 tons annually of ammonia produced exclusively with renewable energy.

These developments validate AEGISVOPAK's strategic focus on ammonia infrastructure. The Central Transmission Utility of India Limited projects that by 2030, renewable hydrogen and ammonia projects in the Kakinada area will have a cumulative demand of about 6GW of renewable electricity. The project will produce about 5 million tons per year of renewable ammonia once fully operational (by 2030).

Port Infrastructure Developments

India's port infrastructure is undergoing massive upgrades to support the green ammonia export opportunity. Cutting-edge infrastructure is essential for the effective production, storage and transport of hydrogen. Clusters with well-developed facilities, including hydrogen storage tanks, pipelines and export terminals, are better equipped to meet both domestic and international demand.

The Mundra Cluster exemplifies this development. The cluster is near the major Indian port of Mundra, which will also make it easier to transport green hydrogen and ammonia to global markets. This creates opportunities for AEGISVOPAK to position its terminals as critical nodes in the emerging hydrogen economy.

Regulatory and Policy Updates

The government's support for the sector continues to strengthen. In the initial stage, two distinct financial incentive mechanisms proposed with an outlay of ₹ 17,490 crore up to 2029-30 for green hydrogen production demonstrate the scale of government commitment.

More importantly for AEGISVOPAK, The enabling framework created under the Mission and support for hydrogen hubs and port infrastructure will facilitate the development of a vibrant export market. This directly benefits terminal operators who will handle the storage and export of green ammonia.

Global Terminal Developments

International terminal developments provide context for AEGISVOPAK's strategic positioning. Today, Yara International officially opened its new ammonia import terminal in Brunsbüttel, Germany. With the new terminal, Yara has the infrastructure to enable imports of up to three million tonnes of low-emission ammonia to Europe annually. Up to 3 million tonnes of low-CO2 ammonia can be imported annually via the terminal in Brunsbüttel. This would correspond to 530,000 tonnes of hydrogen or around 5% of the total European hydrogen target for 2030.

This demonstrates the scale of infrastructure being built globally to support the hydrogen economy—infrastructure that AEGISVOPAK is positioning itself to provide on the export side from India.

Financial Market Updates

Post-IPO, AEGISVOPAK's stock has seen modest appreciation. The 52-week high of Aegis Vopak Terminals Ltd (AEGISVOPAK) is ₹268.50 and the 52-week low is ₹220. The relatively narrow trading range suggests the market is still assessing the company's long-term value proposition.

Credit rating agencies have taken notice of the improved capital structure. Furthermore, in June 2025, Aegis Vopak Terminals (AVTL) has successfully raised funds amounting to Rs 28 billion through an initial public offering (IPO), enabling term debt repayment of Rs 20.2 billion. This has led to a substantial improvement in the capital structure, allowing significant headroom for capacity expansion over the medium term. India Ratings expects the company to achieve a net cash position in FY26, led by debt repayment and high cash balances.

XIV. Links & Resources

Primary Sources

- Company Websites:

- Aegis Vopak Terminals Limited: www.aegisvopak.com

- Aegis Logistics Limited: www.aegisindia.com

- Royal Vopak: www.vopak.com

Regulatory Filings

- Stock Exchange Filings:

- BSE India: www.bseindia.com (Stock Code: 544407)

- NSE India: www.nseindia.com (Symbol: AEGISVOPAK)

Industry Reports and Analysis

- National Green Hydrogen Mission: nghm.mnre.gov.in

- Ministry of New and Renewable Energy: mnre.gov.in

- NITI Aayog Reports on Green Hydrogen: Reports on India's hydrogen economy roadmap

International Ammonia and Hydrogen Resources

- Ammonia Energy Association: ammoniaenergy.org

- International Hydrogen Council: hydrogencouncil.com

- H2Uppp Program: Resources on Indo-German hydrogen cooperation

Related Acquired.fm Episodes for Context

While not directly about AEGISVOPAK, these episodes provide valuable context: - Brookfield Asset Management - Infrastructure investing at scale - Cheniere Energy - Building LNG export infrastructure - Enterprise Products Partners - Midstream energy infrastructure

Book Recommendations

- "The Prize" by Daniel Yergin - Understanding global energy markets

- "Infrastructure: The Book of Everything" by Brian Hayes - Visual guide to infrastructure systems

- "The New Map" by Daniel Yergin - Energy transitions and geopolitics

- "Capital Returns" by Edward Chancellor - Investing through capital cycles

Investment Research Platforms

- Screener.in - Indian equity research and financials

- Trendlyne - Analytics and peer comparison

- Tijori Finance - Detailed financial analysis

Industry Associations

- Indian LPG Industry Association

- Petroleum Federation of India

- Indian Chemical Council

Epilogue: The Infrastructure Imperative

As we conclude this deep dive into Aegis Vopak Terminals, it's worth stepping back to appreciate what this company represents in the broader arc of India's development story. AEGISVOPAK isn't just storing energy products; it's storing the potential energy of a nation's ambitions.

The company sits at a unique intersection: between the fossil fuel present and the renewable future, between India's domestic needs and global energy flows, between government policy and private enterprise. This positioning creates both extraordinary opportunity and complex challenges.

What makes AEGISVOPAK particularly fascinating is how it exemplifies the power of infrastructure as an investment category. Unlike technology companies that can be disrupted overnight or consumer businesses subject to fickle preferences, infrastructure assets like storage terminals have remarkable staying power. They're the bridges, literally and figuratively, between supply and demand.

The joint venture structure between Aegis and Vopak demonstrates how international partnerships can accelerate development in emerging markets. Vopak's four centuries of experience meeting India's urgent infrastructure needs creates value that neither partner could achieve alone. This is globalization at its most productive—not just capital flows but knowledge transfer and operational excellence.

Looking forward, AEGISVOPAK faces a decade that will likely define its next half-century. The energy transition isn't just about replacing fossil fuels with renewables; it's about reimagining entire supply chains. Ammonia terminals built for fertilizer imports today could become hydrogen export hubs tomorrow. LPG storage designed for cooking fuel might pivot to petrochemical feedstocks. This optionality embedded in physical infrastructure is valuable but hard to price.

The investment case ultimately comes down to a belief about India's trajectory. If India continues its economic ascent, if urbanization proceeds as demographics suggest, if the energy transition unfolds as policymakers envision, then AEGISVOPAK's infrastructure will only become more valuable. The terminals they're building today will serve India's economy for generations.

But infrastructure investing requires patience that modern markets rarely reward. AEGISVOPAK's high valuation multiples reflect expectations that will take years, perhaps decades, to fully realize. Short-term volatility is inevitable. Execution risks are real. Competition will intensify.

Yet for those who understand the role of infrastructure in economic development, who appreciate the competitive advantages of strategic locations and operational excellence, and who have the patience to let compound growth work its magic, AEGISVOPAK represents something rare: a chance to own a piece of the physical foundation of one of history's great economic transformations.

The story of Aegis Vopak Terminals is still being written. The IPO marks not an ending but a beginning—of public market scrutiny, of accelerated expansion, of participation in India's energy transition. Whether the company fulfills its ambitious vision or becomes a cautionary tale about infrastructure investing will depend on execution, adaptation, and a measure of luck.

What's certain is that India needs what AEGISVOPAK provides. The country's energy demands will grow. The infrastructure gap must be filled. Someone will capture the value created by storing, handling, and distributing the molecules that power the world's largest democracy. AEGISVOPAK has positioned itself at the center of this opportunity.

For investors, analysts, and observers of India's development, AEGISVOPAK offers a unique window into the mechanics of growth. It's a reminder that beneath the digital revolution and service economy lie physical assets that make modern life possible. In an age of virtual everything, there's something reassuringly concrete about storage tanks and loading arms, pumps and pipelines.

As India strives to become a $10 trillion economy by 2035, companies like AEGISVOPAK will play a crucial but largely invisible role. They won't capture headlines like tech unicorns or consumer brands. But they'll quietly, efficiently, reliably store and move the energy that powers everything else.

That's the real lesson of AEGISVOPAK: Sometimes the best investments aren't in what's sexy or disruptive but in what's essential and enduring. In a world of constant change, there's value in being the unchanging foundation upon which others build.

The terminals rise along India's coastline, steel and concrete monuments to ambition and pragmatism. Inside them flows not just LPG or chemicals but the lifeblood of economic development. AEGISVOPAK doesn't just store products; it stores possibilities. And in a nation of 1.4 billion people reaching for prosperity, those possibilities are limitless.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube