ACC Limited: The Story of India's Cement Pioneer

I. Introduction & Episode Roadmap

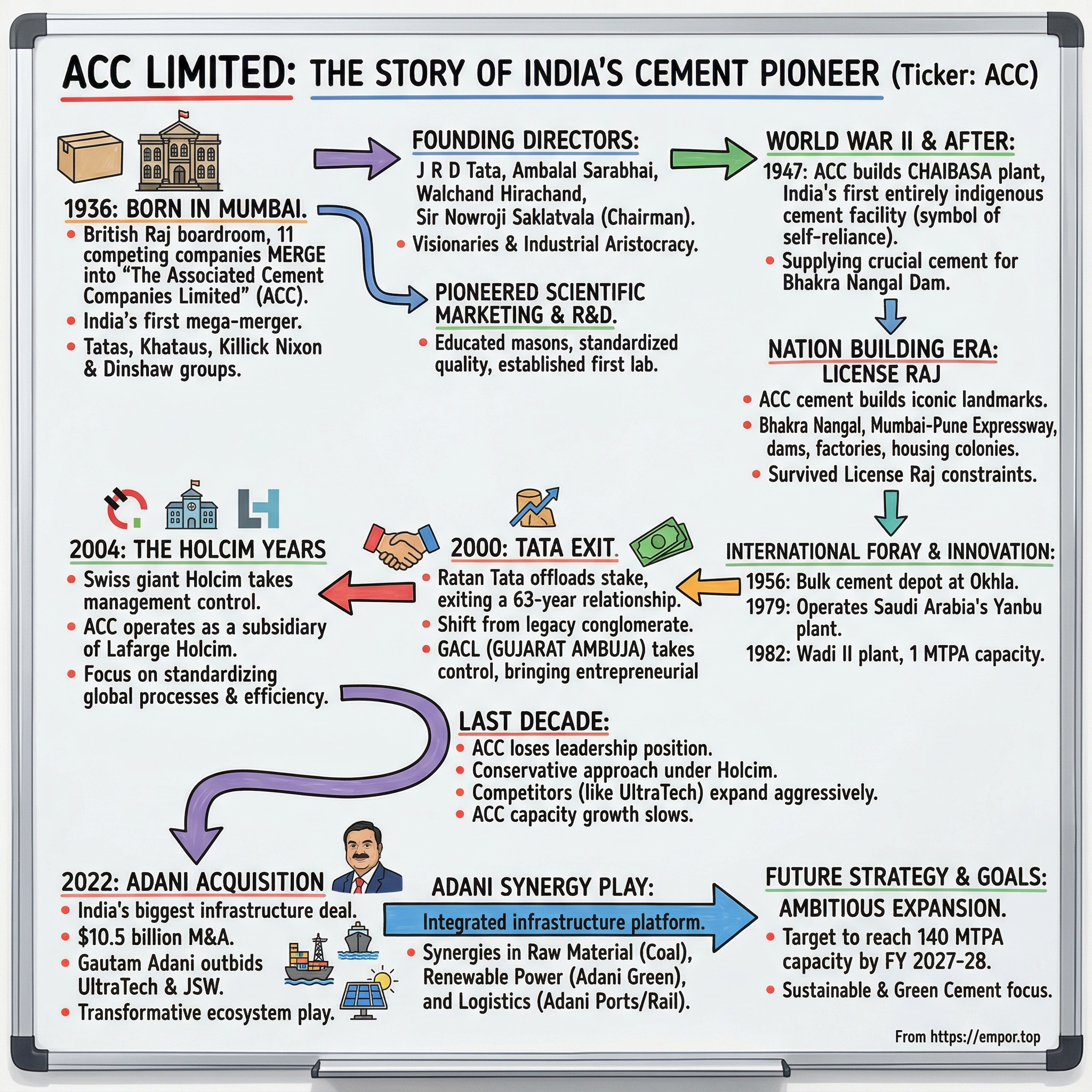

The year is 1936. In the bustling commercial heart of Mumbai, representatives from eleven cement companies gather in a wood-paneled boardroom. Outside, the British Raj still governs India, but inside this room, something unprecedented is happening. These fierce competitors—backed by the Tatas, Khataus, Killick Nixon, and the Dinshaw groups—are about to merge into a single entity. It's colonial India's first mega-merger, creating The Associated Cement Companies Limited, or ACC. No one in that room could have imagined that 86 years later, their creation would become the centerpiece of India's largest-ever infrastructure acquisition.

Fast forward to May 2022. Gautam Adani, India's infrastructure czar, sits across from Holcim's leadership in Switzerland. On the table: a $10.5 billion deal that will instantly transform Adani from a cement outsider to India's second-largest player. The Swiss are eager sellers after years of regulatory scrutiny. Adani outbids Kumar Mangalam Birla's UltraTech and Sajjan Jindal's JSW Group. Within months, ACC—once the crown jewel of the Tata empire, then a prized asset for global cement giant Holcim—becomes part of the Adani infrastructure ecosystem.

This is a story of industrial evolution spanning nine decades. From ACC's birth as India's first cement conglomerate through its role in building post-independence India, from the surprising Tata exit to Swiss ownership, and finally to its dramatic acquisition by Adani. It's a tale that mirrors India's own economic journey—from colonial industry to socialist planning, from liberalization to global integration, and now to the age of infrastructure super-conglomerates. Today, ACC Limited is a part of the diversified Adani Group and one of India's leading producers of cement and ready-mix concrete, with 18 cement manufacturing units, 82+ ready mix concrete plants spread across India. The company that began as colonial India's industrial experiment has evolved into a modern infrastructure powerhouse with ambitious plans to reach 140 MTPA cement capacity by FY 2027-28.

What makes ACC's story particularly compelling is how it reflects every major transition in Indian capitalism. The company has survived and adapted through colonialism, socialism, liberalization, and globalization. Each ownership change—from the founding families to the Tatas, from Indian conglomerates to Swiss multinationals, and now to the Adani empire—tells us something profound about how India's business landscape has evolved.

This deep dive will explore how eleven fierce competitors created India's first industrial mega-merger in 1936. We'll examine why the Tatas, after nurturing ACC for 63 years, suddenly exited in 2000. We'll unpack how Swiss giant Holcim's ambitious India plans unraveled, leading to their hasty exit. And we'll analyze what Adani's record-breaking acquisition means for India's infrastructure future.

Along the way, we'll discover how ACC built the Bhakra Nangal Dam, pioneered bulk cement transportation, operated Saudi Arabia's cement plants, and survived the License Raj. We'll see how a company that once dominated with over 20% market share gradually lost ground to nimbler competitors. And we'll understand why, despite these challenges, ACC remains one of India's most valuable cement assets.

This isn't just a corporate history—it's a masterclass in industrial evolution, M&A dynamics, and the enduring value of infrastructure assets. Let's begin where it all started: a humid Mumbai boardroom in 1936, where India's cement industry was about to change forever.

II. The Great Merger: Birth of a Cement Giant (1936)

The monsoon had just broken over Bombay when F.E. Dinshaw's car pulled up to the grand colonial building on Esplanade Road. It was July 1936, and inside, representatives of India's most powerful business houses were gathering for what would become the subcontinent's first mega-merger. The British Raj still ruled India, Gandhi's independence movement was gaining momentum, and here, in this mahogany-paneled boardroom, eleven cement companies were about to do something unprecedented.

In 1936, eleven cement companies belonging to Tata, Khatau, Killick Nixon and FE Dinshaw groups merged to form a single entity, The Associated Cement Companies. Think about the audacity of this move. In an era when the very concept of mergers and acquisitions was foreign to Indian business—the term itself barely existed in the Indian commercial lexicon—these fierce competitors decided to pool their resources.

The catalyst was economics, but the vision was transformative. India's cement consumption in 1936 was a mere 2 million tonnes annually, with imports comprising nearly 30% of demand. British and other foreign manufacturers dominated quality perceptions. Indian producers, operating sub-scale plants with outdated technology, were bleeding cash competing against each other while foreign giants picked them off one by one.

Sir Nowroji B Saklatvala was the first chairman of ACC, a Parsi industrialist who understood both British commercial culture and Indian business realities. The first board meeting must have been extraordinary—imagine The first board of directors including prominent industrialists—J R D Tata, Ambalal Sarabhai, Walchand Hirachand, Dharamsey Khatau, Sir Akbar Hydari, Nawab Salar Jung Bahadur and Sir Homy Mody. This wasn't just a business merger; it was a coalition of India's industrial aristocracy.

J.R.D. Tata, just 32 years old but already running Tata Sons, brought operational excellence and long-term vision. Walchand Hirachand, the shipping and aviation pioneer, understood logistics and scale. Ambalal Sarabhai, the textile magnate from Ahmedabad, knew how to build distribution networks across India's vast geography. Each brought complementary strengths, but also massive egos and competing visions.

The integration challenges were staggering. The eleven companies operated 14 cement plants scattered from Dwarka in Gujarat to Shahabad in Bihar. Each had different production processes—some used wet process technology, others semi-dry. Quality standards varied wildly. The Katni plant, originally built in 1923, was producing just 200 tonnes per day, while the newer Shahabad facility could manage 600 tonnes. Labor practices, procurement systems, and even accounting methods had to be standardized.

But the real genius was in the market strategy. Instead of competing on price—a race to the bottom that had decimated profitability—ACC created India's first truly national cement brand. They standardized quality across plants, ensuring that ACC cement from Dwarka performed identically to cement from Shahabad. This was revolutionary in a market where quality varied not just between companies but between batches from the same plant.

The company introduced scientific marketing to Indian cement. ACC's engineers traveled to construction sites, educating contractors and masons about proper cement usage. They published technical manuals in regional languages. They established India's first cement research laboratory in 1937, just a year after formation, focusing on developing cement grades suitable for Indian conditions—high temperatures, monsoon moisture, and saline coastal environments.

The financial engineering was equally sophisticated. The merged entity had an authorized capital of Rs 7 crores—massive for that era. More importantly, it created India's first professionally managed industrial enterprise where ownership was separated from management. While the founding families held equity, day-to-day operations were run by professional managers, a model that would later inspire other Indian conglomerates.

ACC also pioneered labor relations in Indian industry. At a time when industrial workers were treated as expendable, ACC introduced health insurance, housing colonies, and schools for workers' children. The Shahabad plant colony, built in 1938, had running water, electricity, and a hospital—amenities that many Indian towns wouldn't see for decades. This wasn't altruism; it was strategic. Skilled cement plant operators were scarce, and ACC needed to retain talent.

The competitive response from foreign players was swift and brutal. Kesoram Industries, backed by British capital, slashed prices. Japanese cement began flooding the Calcutta market. But ACC had an advantage its foreign competitors couldn't match: indigenous intelligence networks. Through the vast business networks of the Tatas, Sarabhais, and others, ACC knew about construction projects before tenders were floated. They could pre-position inventory, offer credit to contractors, and lock in orders before competitors knew opportunities existed.

By 1939, just three years after formation, ACC had captured 35% of India's cement market. Production had increased from 600,000 tonnes to nearly 900,000 tonnes. More importantly, imports had dropped from 30% to less than 15% of consumption. The company was generating returns on capital of over 12%—exceptional for a capital-intensive industry.

World War II transformed ACC from a large company into a strategic asset. The British military needed massive quantities of cement for airfields, bunkers, and ports. ACC's plants ran at over 100% capacity. The company innovated on the fly—when German U-boats made imported coal scarce, ACC's engineers modified kilns to burn inferior domestic coal. When rail wagons were requisitioned for military use, ACC pioneered bullock cart distribution networks that could reach remote construction sites.

The war years also saw ACC's first international foray. In 1944, the company sent engineers and equipment to Burma to help rebuild infrastructure destroyed by Japanese occupation. This experience—operating in difficult conditions with minimal support—would prove invaluable when ACC later expanded internationally.

But perhaps the most important legacy of ACC's founding was cultural. The merger created India's first truly merit-based industrial organization. Engineers from modest backgrounds could rise to run plants. The company's scholarship program, started in 1942, sent promising Indian engineers to study at MIT and Imperial College London. Many would return to lead not just ACC but India's broader industrialization. By 1945, as World War II ended and India's independence loomed, ACC stood as a testament to what Indian enterprise could achieve. From eleven squabbling companies had emerged a unified force that not only survived but thrived against foreign competition. The merger had created something greater than the sum of its parts—a company with the scale, technology, and management depth to help build a new nation. Little did anyone know that ACC's greatest contributions to India were still ahead.

III. Nation Building Era: Independence to Liberalization (1947–1991)

The midnight hour of August 15, 1947, found ACC's engineers not celebrating but working. At Chaibasa in Bihar, they were racing to commission India's first entirely indigenous cement plant. No foreign consultants, no imported drawings—just Indian engineers building with Indian hands. The ACC established India's first entirely indigenous cement plant at Chaibasa in Bihar in 1947, a symbolic achievement for a newly independent nation.

The timing was no coincidence. J.R.D. Tata, still on ACC's board, had insisted that independent India needed industrial self-reliance. The Chaibasa plant became ACC's declaration: we don't just make cement; we make our own destiny. Every component—from the kiln design to the control systems—was developed in-house. When it fired up successfully, producing 600 tonnes per day, it sent a message across the subcontinent: India could industrialize on its own terms.

But independence brought unexpected challenges. The partition had severed ACC from its plants in what became Pakistan. The Rohri plant in Sindh, one of ACC's most modern facilities, was lost overnight. Supply chains were disrupted. The refugee crisis meant skilled workers disappeared without warning. Yet ACC adapted with remarkable agility, shifting production patterns and creating new distribution networks almost overnight.

The 1950s saw ACC become the backbone of Nehru's vision of modern India. When construction began on the Bhakra Nangal Dam in 1948—what Nehru called a "temple of modern India"—ACC was there. From the Bhakra Nangal Dam in 1960 to the Mumbai-Pune Expressway, ACC cement is at the heart of iconic landmarks across the country. The dam required 4.5 million tonnes of cement over its construction period. ACC not only supplied the cement but stationed engineers on-site to ensure optimal concrete mixing for this engineering marvel that would become Asia's second-tallest dam.

The scale of nation-building was staggering. The five-year plans demanded cement for everything—dams, factories, housing colonies, airports. ACC's production jumped from 1.1 million tonnes in 1947 to 2.8 million tonnes by 1960. But this wasn't just about volume. ACC pioneered specialized cements for India's diverse needs—sulfate-resistant cement for coastal projects, low-heat cement for massive dams, rapid-hardening cement for defense installations.

The company set up a bulk cement depot at Okhla, Delhi, in 1956, revolutionizing cement distribution. Until then, cement moved in jute bags that often tore, leading to massive wastage. ACC's bulk transport system—using specially designed rail wagons and pneumatic unloading—reduced wastage from 5% to less than 1%. It was logistics innovation that would be copied globally.

The socialist era brought its own peculiarities. The License Raj meant ACC needed government permission for everything—expanding capacity, importing equipment, even pricing decisions. The Monopolies and Restrictive Trade Practices Act of 1969 specifically targeted ACC, viewing its market dominance suspiciously. ACC was forced to help competitors by sharing technical knowledge and even training their engineers.

Yet ACC turned these constraints into opportunities. Unable to expand freely domestically, the company looked abroad. In 1979, ACC bagged an international contract for operating and managing a new one million tonne cement plant in Yanbu-Ras Biridi, Saudi Arabia. This wasn't just running a plant; ACC provided complete technical and management services, earning valuable foreign exchange when India desperately needed it.

The Saudi experience was transformative. ACC engineers learned to operate in 50°C heat, manage multicultural workforces, and meet international quality standards. They brought back knowledge of automated process control, energy optimization, and preventive maintenance that would modernize ACC's Indian operations. The Yanbu project alone earned ACC over $100 million in fees over five years—massive for that era.

Back home, ACC was navigating the complexities of industrial relations in socialist India. The company employed over 20,000 workers by 1975, making it one of India's largest industrial employers. Labor unions were powerful, strikes common. But ACC pioneered progressive practices—profit-sharing schemes, worker education programs, company townships with schools and hospitals. The ACC township at Jamul became a model, with worker productivity 40% higher than the industry average.

The 1970s oil crisis hit cement manufacturing hard—energy costs comprised 40% of production costs. ACC responded with India's first comprehensive energy conservation program. They modified kilns to use agricultural waste as fuel, installed heat recovery systems, and optimized grinding processes. Energy consumption per tonne dropped by 22% between 1974 and 1980, keeping ACC profitable when competitors struggled.

The company acquired Cement Marketing Company of India (CMI) in 1973, gaining a nationwide distribution network overnight. CMI's 10,000 dealers gave ACC unprecedented market reach. But more importantly, it provided market intelligence—ACC knew about construction projects before they were announced, allowing strategic inventory positioning.

Technology remained ACC's differentiator. The company's R&D center, established in 1975 at Thane, became India's premier cement research facility. They developed blended cements using fly ash from thermal power plants—turning industrial waste into a resource. By 1985, ACC's Portland Pozzolana Cement comprised 30% of production, reducing costs and environmental impact simultaneously.

Three years later the company commissioned its first 1 MTPA plant in India at Wadi, Karnataka in 1982. This wasn't just another plant; it represented a technological leap. The Wadi facility used Japanese dry-process technology, consuming 30% less energy than older wet-process plants. Its computerized control room, the first in Indian cement, became a training ground for the industry.

The 1980s brought subtle liberalization. Rajiv Gandhi's government eased some licensing restrictions. ACC immediately launched an ambitious modernization program—investing Rs 500 crores over five years. Old wet-process plants were converted to dry-process. Capacity utilization improved from 65% to 85%. Production costs dropped by 18% in real terms.

But ACC's greatest achievement in this era wasn't measured in tonnes or rupees. The company had created India's cement industry ecosystem. ACC-trained engineers ran competing companies. ACC's quality standards became industry benchmarks. ACC's vendor development programs created a supply chain that supported the entire sector. When liberalization finally arrived in 1991, India's cement industry was ready to compete globally—thanks largely to foundations ACC had laid.

The numbers tell only part of the story. By 1991, ACC had grown from 11 merged companies to an industrial giant with 16 plants, 35,000 employees, and 4.5 million tonnes annual capacity. But more importantly, it had helped build modern India—every major dam, every expressway, every industrial complex bore ACC's imprint. The company had survived the License Raj not by working around it but by finding purpose within constraints.

As 1991 dawned, bringing economic liberalization, ACC faced a paradox. The company that had thrived under socialism now had to reinvent itself for capitalism. The protective walls were coming down. Foreign technology was arriving. New competitors were emerging. The next chapter would test whether ACC's institutional strength could adapt to market forces.

IV. The Tata Exit & The Ambuja-Gujarat Era (1996–2004)

The boardroom at Bombay House was unusually quiet that October morning in 1999. Ratan Tata, now chairman of Tata Sons, was about to sign papers that would end a 63-year relationship. Outside, Mumbai's humidity was oppressive, but inside, the atmosphere was even heavier. The Tatas were selling their remaining stake in ACC to Gujarat Ambuja Cements Limited (GACL), walking away from the company they had nurtured since 1936.

The journey to this moment had been building since liberalization. In November 1996, the company was listed on the National Stock Exchange (NSE), opening ACC to broader market scrutiny. The listing revealed uncomfortable truths—ACC's return on capital employed had dropped to 8%, well below the 15% that new entrants like Gujarat Ambuja were achieving. Market share had eroded from 22% in 1991 to 14% by 1998.

The problem wasn't operational—ACC's plants ran well. It was strategic. While ACC had spent the 1980s perfecting large integrated plants, nimbler competitors were building smaller, regional grinding units close to markets. Gujarat Ambuja, founded only in 1983 by Narotam Sekhsaria and Suresh Neotia, had grown to 15 million tonnes capacity in just 15 years—a pace ACC couldn't match under its consensus-driven board structure.

Ratan Tata faced a dilemma. ACC needed massive capital investment—at least Rs 2,000 crores—to modernize and expand. But Tata Sons itself was transforming, focusing on technology, automobiles, and services. Cement, despite ACC's heritage, didn't fit the new vision. Meanwhile, other Tata companies needed capital. The decision was pragmatic but painful.

In 1999, the Tata Group offloaded 7.2% of its stake in ACC to Ambuja Cement Holdings Ltd and exited the cement company the next year by selling its remaining stake to the GACL group. The transaction valued ACC at Rs 3,600 crores—good value, but for Tata old-timers, it felt like selling family silver.

Gujarat Ambuja's interest wasn't accidental. Sekhsaria, a Marwari entrepreneur who'd built his fortune in cotton trading before entering cement, saw what others missed. ACC had unmatched assets—limestone reserves for 100+ years, established brands, and deep technical expertise. What it lacked was entrepreneurial aggression. Sekhsaria believed he could provide that.

The cultural clash was immediate. ACC executives, used to long deliberations and committee decisions, suddenly faced Sekhsaria's trademark urgency. He would call plant managers directly at 6 AM, questioning yesterday's production numbers. Investment decisions that took months now happened in days. The message was clear: ACC's leisurely pace was over.

But Sekhsaria was no asset stripper. He recognized ACC's institutional knowledge was invaluable. Instead of mass layoffs, he initiated knowledge transfer programs. Ambuja managers learned ACC's technical excellence; ACC absorbed Ambuja's commercial aggression. Joint procurement leveraged combined volumes. Technology sharing improved both companies' operations.

In 2001, the company commissioned a new plant of 2.6 MTPA capacity at Wadi, Karnataka, but this expansion revealed deeper challenges. While ACC built large plants with cutting-edge technology, regional players were capturing market share with smaller, more flexible operations. L&T's cement division, Grasim, and dozens of regional players were eating into ACC's traditional markets.

The competitive landscape had transformed dramatically. By 2003, India had over 130 cement companies, up from 30 in 1991. Pricing power had evaporated—cement that sold for Rs 200 per bag in 1995 was down to Rs 160 by 2003, despite inflation. ACC's high-cost structure, built for a different era, struggled with these new realities.

Yet the Ambuja partnership brought unexpected benefits. GACL's port infrastructure—they pioneered coastal shipping of cement—gave ACC access to new markets. Joint ventures in ready-mix concrete leveraged ACC's brand with Ambuja's execution. Combined R&D efforts produced new products faster than either could alone.

The period also saw ACC's first serious cost-reduction drive. Layers of management were eliminated. Voluntary retirement schemes reduced workforce from 28,000 in 1999 to 19,000 by 2004. Energy costs were attacked systematically—alternative fuels usage increased from 2% to 8%. These weren't popular decisions, but they were necessary.

Market dynamics were shifting toward consolidation. International cement giants were eyeing India—Lafarge had entered through Tata Steel's cement division, Italcementi had bought Zuari Cement. The logic was compelling: India's per capita cement consumption at 100 kg was a fraction of the global average of 250 kg. Growth was inevitable; the question was who would capture it.

For ACC, independence was ending. The company that had begun as India's first industrial consolidation was about to be consolidated itself. Sekhsaria, despite his success with Ambuja, recognized that competing against global giants required global partnerships. Negotiations with Switzerland's Holcim began in 2004, setting the stage for ACC's next transformation.

The Tata exit marked more than ownership change—it symbolized Indian business evolution. The industrial houses that built India's economy were giving way to focused corporations and global partnerships. ACC, born from consolidation, raised under protection, and matured through competition, was about to enter its most challenging phase yet. The Swiss were coming, bringing capital, technology, and global ambitions. Whether they understood India's unique cement market remained to be seen.

V. The Holcim Years: Global Ambitions Meet Indian Reality (2004–2022)

Thomas Schmidheiny looked out from his Zurich office at the Swiss Alps, contemplating a memo about India. It was late 2004, and Holcim, the cement giant his family had built over a century, needed growth. Europe was saturated, America consolidated. But India—with its billion-plus population and infrastructure deficit—promised decades of expansion. The strategy seemed obvious: acquire a strong local player, apply Swiss efficiency, and dominate. Reality would prove far messier.

The management control of the company was taken over by Swiss cement manufacturer Holcim Group in 2004. ACC operated as a subsidiary of Lafarge Holcim. The deal structure was elegant: In 2005, Switzerland's Holcim group formed a strategic alliance with Ambuja Group by picking up the majority stake in Ambuja Cements India Ltd. (ACIL) which at the time owned a 13.8% stake in ACC. Through this indirect route, Holcim gained control of both Ambuja and ACC—instantly becoming India's largest cement producer with combined capacity exceeding 40 million tonnes.

The Swiss brought radical changes. On 1 September 2006, the name of The Associated Cement Companies Limited was changed to ACC Limited—a seemingly minor change that symbolized major transformation. The elaborate name that had represented Indian industrial collaboration for 70 years was replaced by a corporate acronym. Old-timers saw it as erasure of heritage; Holcim saw it as modernization.

Holcim's initial investments were impressive. They pumped in Rs 3,500 crores over three years, upgrading technology across ACC's plants. Swiss-designed vertical roller mills replaced old ball mills, improving energy efficiency by 25%. German automation systems modernized control rooms. Environmental compliance, previously an afterthought, became central—ACC installed India's first cement plant electrostatic precipitators to control emissions.

But cultural integration proved challenging. Swiss managers, accustomed to punctual trains and predictable systems, struggled with Indian complexity. A plant expansion that would take 18 months in Switzerland stretched to 36 months in India, tangled in land acquisition, environmental clearances, and local politics. Holcim's standardized global processes collided with India's relationship-based business culture.

The first major crisis came in 2008. The global financial crisis had Holcim reeling—their stock price halved, debt mounted. Suddenly, Indian operations needed to generate cash, not consume capital. Expansion plans were frozen. Just as India's infrastructure boom was taking off, ACC was told to maximize margins, not market share.

This conservative approach opened doors for competitors. Kumar Mangalam Birla's UltraTech Cement, aggressive and well-capitalized, launched a massive expansion. From 23 million tonnes in 2004, UltraTech grew to 65 million tonnes by 2015. Regional players like Shree Cement and Dalmia Bharat expanded rapidly. ACC, constrained by Holcim's global priorities, watched market share slip away.

In the last decade, compared to other key cement companies who at least doubled their capacity, Holcim did not increase ACC capacity as aggressively as its competitors and as a result, ACC lost its leadership position. The numbers were stark: ACC's capacity grew from 18 million tonnes in 2004 to just 34 million tonnes by 2020. UltraTech, over the same period, had quadrupled capacity.

Yet Holcim brought valuable contributions. Their "Leadership Journey" management development program created a cadre of professional managers. Safety standards improved dramatically—accident rates dropped by 70%. ACC became India's first cement company to publish sustainability reports, setting industry benchmarks for environmental disclosure.

The ready-mix concrete business, neglected under previous managements, flourished under Holcim. They expanded from 15 plants in 2004 to 85 by 2020, making ACC India's largest RMX player. The logic was compelling—ready-mix offered 40% margins versus 25% for cement, provided customer stickiness, and utilized cement capacity. But execution remained challenging in a market where most construction still mixed concrete on-site.

Holcim's global procurement leverage delivered cost advantages. ACC accessed equipment at 20% lower costs through Holcim's global contracts. Technical knowledge transfer was substantial—Swiss experts improved ACC's clinker factor from 72% to 65%, significantly reducing production costs. Best practices from Holcim's 70-country operations were systematically implemented.

But regulatory challenges mounted. The Competition Commission of India grew increasingly suspicious of ACC-Ambuja coordination. Despite being sister companies under Holcim, they were required to compete independently—a legal fiction that hampered operational synergies. Holcim was planning to exit India following intense scrutiny of its India operations by the Competition Commission of India (CCI) which opened its second investigation against the company in December 2020.

The cement cartel investigation of 2012 was particularly damaging. CCI imposed Rs 1,100 crore penalty on ACC for alleged price-fixing. Though legally contested, the reputational damage was severe. Holcim's country CEO was transferred; senior executives faced personal scrutiny. The Swiss board grew increasingly uncomfortable with Indian regulatory complexity.

Meanwhile, the Indian cement industry was consolidating rapidly. Lafarge India merged with Birla Corp. Jaypee Group, crushed by debt, sold assets to UltraTech. Binani Cement's bankruptcy saw a fierce battle between UltraTech and Dalmia. ACC, hamstrung by Holcim's cautious approach, participated in no major acquisitions. Each missed opportunity strengthened competitors.

Technology disruption added pressure. Digital sales platforms were changing cement distribution. Small players used mobile apps to reach customers directly, bypassing traditional dealer networks. ACC's 56,000-dealer network, once an asset, became a costly legacy. Holcim's global digital initiatives, designed for developed markets, proved inappropriate for India's fragmented retail landscape.

The 2014-2019 period saw temporary revival. The Modi government's infrastructure push drove demand. ACC's capacity utilization improved from 65% to 78%. Prices firmed up. Profits reached record levels—Rs 1,500 crores in 2018. But this masked structural issues. ACC's cost per tonne remained 15% higher than efficient producers like Shree Cement. Market share continued declining, from 11% in 2014 to 8% by 2020.

Environmental pressures intensified. The National Green Tribunal's limestone mining restrictions affected ACC disproportionately—many mines operated on expired leases awaiting renewal. While competitors had secured long-term mining rights, ACC's regulatory compliance focus, while ethically sound, disadvantaged them commercially.

COVID-19 became the final catalyst. The pandemic's first wave devastated cement demand—sales dropped 40% in Q1 2020. But recovery was swift and uneven. Smaller, nimbler players captured the rebound. ACC's large plants, optimized for steady demand, struggled with volatility. Working capital ballooned as inventory management systems, designed for predictable markets, failed.

By late 2021, Holcim's board reached a conclusion: India was too complex, too competitive, and too capital-intensive for their global strategy. The company that had entered India expecting to dominate was now seeking exit. ACC, despite strong brand equity and valuable assets, had become a subscale player in a consolidating industry.

On 14 April 2022, Holcim announced that it would exit from the Indian market after 17 years of operations as part of a strategy to focus on core markets and listed its stakes in ACC and Ambuja Cements for sale. The announcement triggered India's most dramatic M&A battle. ACC's future hung in balance—would it find an owner who understood both its heritage and potential?

The Holcim years were neither failure nor success but a complex lesson in globalization's limits. Swiss efficiency couldn't overcome Indian complexity. Global best practices needed local adaptation. Financial engineering couldn't substitute for entrepreneurial aggression. ACC had survived another ownership transition, but at a cost. The company that once defined Indian cement was now struggling to remain relevant. The stage was set for the most dramatic acquisition in Indian infrastructure history.

VI. The Adani Acquisition: India's Biggest Infrastructure Deal (2022)

Gautam Adani's private jet touched down at Zurich Airport on a crisp April morning in 2022. Unlike his usual entourage-heavy visits, this trip was deliberately low-key—just Adani, his son Karan, and two trusted advisors. They were about to make the biggest bet in Adani Group's history, and secrecy was paramount. Across the table at Holcim's headquarters, CEO Jan Jenisch was equally eager. After months of regulatory battles and board pressure, Holcim needed out of India—fast.

The Adani Family, through an offshore special purpose vehicle, announced that it had entered into definitive agreements for the acquisition of Switzerland-based Holcim Ltd's entire stake in two of India's leading cement companies – Ambuja Cements Ltd and ACC Ltd. Holcim, through its subsidiaries, holds 63.19% in Ambuja Cements and 54.53% in ACC (of which 50.05% is held through Ambuja Cements).

The bidding process had been intense. Kumar Mangalam Birla's UltraTech, already India's cement king with 120 MTPA capacity, desperately wanted to consolidate further. JSW group chairman Sajjan Jindal had recently said his group has offered $7 billion to Holcim for its Ambuja stake which includes $4.5 billion of his own money and $2.5 billion investment from the private equities. But Adani had three advantages his rivals couldn't match: speed, structure, and synergy.

The group outbid Ultratech and JSW group to enter the cement industry and also emerge as the country's second-largest cement manufacturer, with 70 million tonnes of capacity annually. The final price was staggering: The value for the Holcim stake and open offer consideration for Ambuja Cements and ACC is USD ~10.5 billion, which makes this the largest ever acquisition by Adani, and India's largest ever M&A transaction in the infrastructure and materials space.

But the real genius was in the deal structure. Instead of a straightforward Indian acquisition that would trigger regulatory scrutiny and tax implications, Adani structured it offshore. A Mauritius-based special purpose vehicle, Endeavour Trade and Investment Limited, would acquire Holcim's Netherlands-based holding company. This wasn't just tax efficiency—it was about speed. The Adani group, on the other hand, had assured to close the deal as early as possible to the bankers – making them win the transaction.

The financing was equally innovative. Rather than burden the Adani Group's listed entities with debt, the acquisition was initially funded through offshore borrowings by family members. The plan was elegant: acquire first, then refinance using the target companies' own cash flows and assets. This structure allowed Adani to move fast without lengthy approvals from Indian lenders or shareholders.

For Holcim, the timing was perfect. Holcim was planning to exit India following intense scrutiny of its India operations by the Competition Commission of India (CCI) which opened its second investigation against the company in December 2020. The Swiss faced continuing regulatory headaches, with appeals against CCI penalties stuck in courts. Their global strategy had shifted toward asset-light solutions and products, away from capital-intensive emerging markets.

But for Adani, this wasn't just about buying cement capacity. This was about ecosystem play at its finest. Both Ambuja and ACC will benefit from synergies with the integrated Adani infrastructure platform, especially in the areas of raw material, renewable power and logistics, where Adani Portfolio companies have vast experience and deep expertise.

Consider the synergy mathematics. Adani Ports, with 15 facilities handling 350 million tonnes annually, could revolutionize cement logistics. Coastal shipping costs were 40% lower than rail transport. Adani's ports could provide limestone imports, coal handling, and finished cement exports. The logistics savings alone could improve EBITDA margins by 200-300 basis points.

Power was another game-changer. Cement manufacturing consumed 80-100 kWh per tonne, comprising 25% of production costs. Adani Green Energy, with 20 GW renewable capacity and plans for 45 GW by 2030, could provide captive green power. This wasn't just cost savings—it was about decarbonization, increasingly critical for global customers and ESG-focused investors.

Mr Adani added, "Holcim's global leadership in cement production and sustainability best practices brings to us some of the cutting-edge technologies that will allow us to accelerate the path to greener cement production. This wasn't corporate speak. European cement technology was 10-15 years ahead in carbon capture, alternative fuels, and green cement formulations. ACC and Ambuja would leapfrog Indian competitors in sustainability.

The regulatory approvals moved with unprecedented speed. The Competition Commission of India (CCI) has given its approval for the acquisition of Holcim's stake in Ambuja Ltd and ACC Ltd by the Adani Group. In a tweet on Friday, the watchdog said it has approved the "acquisition of the stake in Holderind Investments, Ambuja Cements and ACC by Endeavour Trade and Investment". CCI clearance came in just three months—remarkable for a deal creating India's second-largest cement player.

The open offer, mandatory under Indian takeover regulations, was another masterpiece of execution. Adani group on Friday launched its Rs 31,000-crore open offer to acquire 26 per cent additional stake from the public shareholders of Swiss firm Holcim's two Indian listed entities ACC Ltd and Ambuja Cements. The open offer is estimated at over Rs 31,000 crore if fully subscribed.

Market reaction was euphoric. Shares of Ambuja Cement and ACC rallied up to 8 per cent on the BSE in Monday's intra-day trade after the Adani Group announced the acquisition of Swiss cement major Holcim's stake. Investors saw what Adani saw—massive synergies, aggressive expansion potential, and an owner with deep pockets and deeper ambitions.

The cultural transformation began immediately. Adani management, known for execution speed, descended on ACC and Ambuja plants. Debottlenecking studies identified quick capacity additions. Procurement was centralized, leveraging group-wide contracts. Digital initiatives, languishing under Holcim, were fast-tracked. The message was clear: the Swiss conservatism era was over.

But challenges emerged quickly. ACC and Ambuja's combined debt of Rs 3,000 crores, while manageable, limited immediate expansion capital. The acquisition debt, though held offshore, needed servicing. More concerning was the market structure—UltraTech's dominance meant pricing discipline was essential, limiting margin expansion opportunities.

Employee integration proved delicate. ACC's veteran engineers, many with 20+ years experience, were skeptical of Adani's aggressive targets. The ready-mix concrete business, built painstakingly over decades, didn't fit Adani's bulk infrastructure focus. Some senior executives, comfortable with Holcim's deliberate pace, struggled with Adani's entrepreneurial chaos.

Yet the strategic logic remained compelling. India's cement demand, at 250 million tonnes annually, was projected to reach 550 million tonnes by 2030. Infrastructure spending under the National Infrastructure Pipeline would drive demand. Affordable housing, metro projects, and industrial corridors needed massive cement quantities. ACC and Ambuja, with established brands and distribution, were perfectly positioned.

The financing strategy evolved post-acquisition. Switzerland's Holcim has closed the sale of Ambuja Cement and ACC (Ambuja's subsidiary) to the Adani Group, resulting in cash proceeds of $6.4 billion. The initial acquisition debt was refinanced through a combination of promoter funding, strategic investors, and eventual capital market raises. The structure, while complex, maintained Adani family control while optimizing capital costs.

International investors watched carefully. This wasn't just another Adani acquisition—it was a test case for the group's ability to integrate large, complex businesses outside their core infrastructure domain. Success would validate Adani's conglomerate model; failure would question the group's ambitious diversification.

For ACC specifically, the Adani acquisition marked a pivotal moment. After 86 years and four major ownership changes, the company was back under Indian entrepreneurial control. The question wasn't whether Adani could run cement plants—that was operational. The question was whether Adani could transform ACC from a heritage brand into a modern, efficient, growth machine capable of challenging UltraTech's dominance. The announcement sent shockwaves through the industry. How could a group with zero cement experience bid more than established players? But this revealed Adani's key insight: cement wasn't about making clinker—it was about infrastructure ecosystems. And no one in India understood infrastructure ecosystems better than Adani.

VII. Business Model & Operational Deep Dive

Inside ACC's Wadi plant in Karnataka, the morning shift change reveals the scale of ambition. At 12,500tpd, ACC's new cement kiln at Wadi is the world's largest with a capacity of 12,500 tonnes per day creating new landmarks for cement industry. This single kiln produces more cement than many entire companies managed a generation ago. But size alone doesn't capture ACC's operational complexity—it's the intricate dance of chemistry, logistics, and market dynamics that makes this business fascinating.

ACC Ltd owns and operates 17 cement manufacturing units and 85 ready-mix concrete plants in various states across India with an Installed cement manufacturing capacity of 36.05 MTPA, though post-Adani acquisition, expansion plans target 140 MTPA by 2028. The company's footprint spans from the limestone quarries of Rajasthan to the urban markets of Mumbai, from the coalfields of Jharkhand to the ports of Gujarat.

The operational model begins with limestone—the soul of cement. ACC controls limestone reserves sufficient for over 100 years of production at current rates. But not all limestone is equal. The calcium carbonate content varies from 48% to 52% across ACC's mines. This seemingly small variation dramatically impacts energy consumption—each percentage point reduction in CaCO3 increases fuel consumption by 2-3%. ACC's geologists constantly map and blend limestone from different quarry faces to maintain optimal chemistry.

The manufacturing process itself is energy-intensive alchemy. Limestone, clay, and iron ore are ground to powder fineness—particles smaller than 90 microns. This raw meal enters the preheater tower at ambient temperature and exits at 850°C. The precalciner, where 60% of the calcination occurs, operates at 900°C. Finally, the rotary kiln, the heart of the plant, reaches 1,450°C—hot enough to melt steel. Here, the raw meal transforms into clinker, small grey nodules that are cement's precursor.

Commercial production at ACC Ltd's Wadi II plant, situated in India's southern state of Karnataka, commenced on 1 May 2011. This integrated cement project comprised a clinker line expanded to 12,500tpd as well as two satellite cement grinding works (both in Karnataka) to manufacture Portland slag cement and fly-ash based Portland pozzolana cement. This configuration represents modern cement economics—centralized clinker production for efficiency, distributed grinding for market proximity.

Energy comprises 35-40% of cement production costs, making efficiency paramount. ACC's specific energy consumption has dropped from 95 kWh/tonne in 2004 to 68 kWh/tonne today through systematic improvements. Variable frequency drives on motors save 8% energy. Waste heat recovery systems generate 35 MW of power from exhaust gases. Alternative fuels—industrial waste, biomass, refuse-derived fuel—now substitute 8% of coal consumption, targeting 25% by 2025.

But the real innovation is in product strategy. ACC's product portfolio: Gold range vs. Silver range strategy isn't just marketing—it's sophisticated price discrimination. The Gold range—comprising premium products like ACC Gold water shield (water-resistant), ACC F2R (rapid-setting), and ACC Concrete+ (high-strength)—commands 15-20% price premiums. These aren't cosmetic differences; each variant has specific chemical compositions and performance characteristics.

The Silver range—ACC Suraksha, ACC HPC—targets price-sensitive segments. Here, the game is cost optimization. Higher fly ash content (up to 35% versus 25% in premium products) reduces clinker consumption. Regional sourcing minimizes logistics costs. Simplified packaging reduces material costs. Yet quality remains consistent—Indian Standards allow wide specification ranges, which ACC exploits expertly.

Ready-mix concrete (RMX) represents ACC's most ambitious diversification. From 15 plants in 2004, ACC expanded to 85 plants by 2020, becoming India's largest RMX player. The economics are compelling: RMX offers 40% gross margins versus 25% for cement. Customer stickiness is higher—switching RMX suppliers mid-project is practically impossible. Technical support requirements create entry barriers.

Yet RMX in India faces unique challenges. Unlike developed markets where 70-80% of cement flows through RMX, India's penetration is below 10%. Construction sites prefer on-site mixing—it's cheaper, allows payment flexibility, and suits the informal economy. ACC's response has been targeted: focus on commercial projects, infrastructure contracts, and premium residential developments where quality premiums are valued.

It caters to its customers through a large distribution network of 56,000 dealers and retailers and a countrywide spread of sales offices. This network, built over decades, is ACC's moat. But it's also expensive—dealer margins, credit costs, and logistics eat into profitability. The average dealer holds 15-20 days inventory, tying up Rs 2,000 crores of working capital across the system.

Digital transformation, much discussed but slowly implemented, is finally gaining traction under Adani. The 'ACC Connect' app allows dealers to place orders, track shipments, and manage credit. Dynamic pricing algorithms adjust rates based on local demand-supply. GPS-tracked trucks optimize delivery routes. Early results are promising—logistics costs have dropped 8%, inventory turns have improved by 15%.

The company has installed the world's largest kiln having the capacity to produce 12,500 tonnes per day at its cement plant in Wadi, Karnataka, but technology leadership extends beyond scale. ACC's Technical Services team, 150 engineers strong, provides on-site support for major projects. They optimize concrete mix designs, troubleshoot quality issues, and train contractors. This isn't altruism—technical support creates specifications that favor ACC products, building long-term demand.

Sustainability initiatives, once CSR window-dressing, now drive operational strategy. With an investment of over ₹10,000 crore in green power projects, the Company aims to power 60% of its planned 140 MTPA cement capacity through 1 Giga Watt of solar and wind power and 376 MW of Waste Heat Recovery System by FY 2027-28. This isn't just environmental compliance—renewable power at Rs 2.50/unit beats grid power at Rs 7/unit, improving margins substantially.

The circular economy approach transforms waste into resources. Fly ash from power plants, blast furnace slag from steel plants, and synthetic gypsum from fertilizer plants substitute virgin raw materials. ACC consumes 6 million tonnes of industrial waste annually—avoiding disposal costs for waste generators while reducing ACC's material costs. It's a win-win that improves both economics and sustainability.

Water management, critical in water-stressed India, showcases operational excellence. ACC's specific water consumption has dropped from 125 liters/tonne to 65 liters/tonne through recycling, rainwater harvesting, and process optimization. Zero liquid discharge systems, mandatory at new plants, recover 95% of water. Air-cooled condensers replace water-cooled systems. These investments, totaling Rs 200 crores, pay back through reduced water costs and regulatory compliance.

Quality control, often overlooked, differentiates ACC in a commoditized market. Each plant tests 200+ samples daily across 30 parameters. Automated sampling eliminates human error. X-ray fluorescence provides real-time chemical analysis. Particle size analyzers ensure consistent fineness. This obsession with quality reduces customer complaints to less than 0.1%—industry-leading performance that justifies premium pricing.

The maintenance philosophy—predictive, not reactive—minimizes downtime. Vibration analysis detects bearing failures before they occur. Thermal imaging identifies insulation degradation. Oil analysis predicts gearbox failures. This approach has improved plant availability from 85% to 92%, adding effective capacity without capital investment.

Logistics, the final frontier, determines delivered cost competitiveness. ACC moves 50 million tonnes annually—by rail (45%), road (50%), and sea (5%). Rail transport, at Rs 1.20/tonne-km, beats road transport at Rs 2.50/tonne-km, but requires scale and infrastructure. ACC's 18 railway sidings and 500 owned wagons provide this advantage. GPS tracking and RFID tags monitor movement, reducing pilferage from 2% to 0.3%.

The human element remains crucial despite automation. ACC employs 10,000+ people directly and 50,000+ indirectly. The skill profile is shifting—from manual operators to process engineers, from mechanical maintenance to predictive analytics. ACC's training programs, investing Rs 50 crores annually, prepare workers for this transition. The Jamul Technical Institute trains 500+ engineers annually, creating industry-ready talent.

Procurement, often 60% of revenues, offers massive optimization potential. Centralized procurement under Adani has delivered immediate benefits—coal costs down 12%, power costs down 18%, logistics costs down 15%. But integration challenges remain. ACC's established vendor relationships, some decades old, resist change. Quality specifications, developed over years, don't always align with group standards.

The technology roadmap under Adani is ambitious. Artificial intelligence for demand forecasting, blockchain for supply chain transparency, IoT for plant optimization. A Rs 500 crore digital transformation budget aims to make ACC India's most technologically advanced cement company by 2025. Early pilots show promise—AI-based kiln optimization has improved fuel efficiency by 3%, potentially saving Rs 100 crores annually if scaled.

Market positioning remains ACC's challenge and opportunity. In a fragmented market with 100+ players, ACC's 8% share seems modest. But in premium segments—special applications, infrastructure projects, branded retail—ACC commands 15-20% share with superior realizations. The strategy is clear: concede commodity volumes to regional players while dominating profitable niches.

The operational transformation under Adani is just beginning. Capacity expansion plans include 20 MTPA brownfield additions at existing sites and 30 MTPA greenfield plants in new markets. But the real transformation is operational—from a manufacturing company that sells cement to an integrated infrastructure partner that provides building solutions. This shift, if successful, could restore ACC's industry leadership. But execution, in India's hypercompetitive cement market, will determine whether ambition translates to results.

VIII. The Adani Synergy Play & Future Strategy

At Adani Group's Ahmedabad headquarters, the war room walls are covered with maps, charts, and flowcharts showing the integration masterplan. Red pins mark ACC plants, blue ones show Adani Ports, green indicates renewable energy projects, and yellow highlights coal mines. The overlap is striking—almost every ACC facility sits within 200 kilometers of an Adani asset. This isn't coincidence; it's the foundation of India's most ambitious industrial integration.

Both Ambuja and ACC will benefit from synergies with the integrated Adani infrastructure platform, especially in the areas of raw material, renewable power and logistics. This will enable higher margins and return on capital employed for the two companies. But the real story is in the execution details that transform paper synergies into operational reality.

Start with logistics, where the impact is immediate and measurable. Adani Ports and Special Economic Zone (APSEZ), India's largest private port operator, handles 350 million tonnes of cargo annually. ACC's coastal plants in Gujarat, Maharashtra, and Karnataka can now access imported coal, gypsum, and fly ash through Adani facilities at 30% lower handling costs. More importantly, Adani's port infrastructure enables cement exports to Middle East and Africa—markets where Indian cement enjoys 20-25% cost advantages.

The numbers tell the story. During the reporting year, the Company has improved and optimised its logistics cost by leveraging Group synergy. Pre-acquisition, ACC paid Rs 180/tonne for coal handling at third-party ports. Through Adani Ports, this drops to Rs 125/tonne. With 8 million tonnes of annual coal consumption, that's Rs 440 crores in savings—straight to the bottom line. But it's not just about rates; it's about reliability. Adani Ports guarantees 24-hour turnaround for ACC vessels versus 48-72 hours at other ports.

The rail logistics transformation is equally dramatic. Adani's rail logistics arm operates 100+ rakes and has India's largest private railway network. ACC can now move cement from plants to ports using dedicated trains, avoiding Indian Railways' congestion. Transit time from Wadi to Mumbai port drops from 7 days to 3 days. Inventory carrying costs reduce proportionally. Working capital requirements drop by Rs 300 crores.

Power integration represents the most transformative synergy. Cement plants consume 100 kWh per tonne; at ACC's 36 MTPA capacity, that's 3.6 billion units annually. With an investment of over ₹10,000 crore in green power projects, the Company aims to power 60% of its planned 140 MTPA cement capacity through 1 Giga Watt of solar and wind power and 376 MW of Waste Heat Recovery System by FY 2027-28. This isn't just cost reduction—it's competitive transformation.

Consider the mathematics. Grid power costs Rs 7-8/unit. Adani Green Energy can supply renewable power at Rs 2.50-3/unit through group captive arrangements. That's Rs 4.50/unit savings, or Rs 1,620 crores annually at full implementation. This transforms ACC from a high-cost producer to one of India's most competitive. But beyond economics, it's about sustainability—ACC can claim to produce India's greenest cement, commanding premium pricing from environmentally conscious customers.

Integration with ports business, power transmission (fly ash), and coal from Australian mines allows him to manage costs at two key levels—logistics and power. With his foray into renewable energy—which is known to have a long gestation period—the acquisition opens up one more way to knock off costs and set him up well for the decarbonisation story.

The fly ash synergy is particularly elegant. Adani Power's thermal plants generate 15 million tonnes of fly ash annually—a disposal headache that costs Rs 100/tonne. ACC can consume 8 million tonnes, converting waste into valuable input. Adani Power saves disposal costs; ACC gets free raw material that replaces costly clinker. The environmental benefit—reduced CO2 emissions—attracts carbon credits worth Rs 50 crores annually.

Raw material security, often overlooked, provides strategic advantage. Adani's Australian coal mines guarantee fuel supply at predictable prices, hedging against market volatility. Indian coal, with 35% ash content, requires blending with imported coal (15% ash) for optimal kiln performance. Adani's Indonesian coal assets provide this blend component, ensuring quality and availability.

The digital integration leverages Adani's technology investments across the group. The Adani Command and Control Centre in Ahmedabad, originally built for ports, now monitors ACC plants in real-time. Artificial intelligence algorithms, trained on port logistics data, optimize cement distribution. Predictive maintenance systems, developed for power plants, prevent cement plant breakdowns. This technology transfer, worth Rs 200 crores if purchased independently, comes free through group synergies.

During the reporting year, the Company has improved and optimised its logistics cost by leveraging Group synergy. ACC has implemented advanced logistics and fleet management digitalisation for real-time vehicle tracking, enhancing efficiency and leading to optimised logistics expenditure. The Company has also adopted integrated excellence projects for logistics cost rationalisation.

Customer synergies, though less tangible, offer significant value. Adani's infrastructure projects—airports, roads, data centers—consume 2 million tonnes of cement annually. These captive volumes, supplied at premium prices due to technical specifications, provide baseload demand. More importantly, ACC becomes the preferred vendor for Adani's Rs 2 lakh crore infrastructure pipeline, ensuring decades of growth.

Green cement ambitions represent the boldest synergy play. Traditional cement emits 0.9 tonnes CO2 per tonne produced. Using renewable power, alternative fuels, and carbon capture, ACC targets 0.4 tonnes CO2 by 2030—industry-leading performance. Adani Green's expertise in carbon credits, renewable energy certificates, and sustainability financing accelerates this transition. Green cement commands 20-30% premiums in export markets and attracts ESG-focused investors.

The circular economy integration is comprehensive. Adani's ports handle 30 million tonnes of industrial waste—steel slag, copper slag, phosphogypsum. ACC can consume 40% of this as alternative raw materials. Adani's city gas distribution generates biogas from waste; ACC's kilns can use this as fuel. Adani's solar panel recycling yields silicon; ACC incorporates this in specialized cements. Every waste stream becomes a resource, improving both economics and sustainability.

Capacity expansion under Adani follows a different philosophy. Rather than greenfield mega-plants that take 5 years and Rs 5,000 crores, the focus is brownfield debottlenecking. Following the acquisition, plant capacity utilisation rose from 28% to 52% between December 2023 and March 2024. Each existing plant can add 20-30% capacity through focused investments—new grinding mills, additional silos, logistics infrastructure. This approach adds 10 MTPA capacity with Rs 2,000 crores investment versus Rs 6,000 crores for greenfield equivalent.

The market approach is equally transformed. Instead of competing across all segments, ACC focuses on profitable niches where Adani synergies provide advantage. Infrastructure projects, where technical specifications and timely delivery matter more than price, become priority. Coastal markets, accessible through Adani Ports, get emphasis. Export markets, enabled by port infrastructure, open new revenue streams.

Competition with UltraTech takes a different dimension. Rather than matching UltraTech's 120 MTPA capacity, ACC leverages Adani ecosystem advantages. Lower power costs, superior logistics, and captive demand create competitive advantage without capacity wars. The strategy is profitability, not volumes—earning 15% EBITDA margins on 70 MTPA versus 12% on 120 MTPA.

The ESG transformation under Adani is substantive, not cosmetic. The Companies will also benefit from Adani's focus on ESG, Circular Economy and Capital Management Philosophy. The businesses will continue to be deeply aligned to UN Sustainability Development Goals with clear focus on SDG 6 (Clean Water and Sanitation), SDG 7 (Affordable and Clean Energy), SDG 11 (Sustainable Cities and Communities) and SDG 13 (Climate Action). Water-positive operations by 2025, carbon neutrality by 2050, zero waste to landfill by 2030—these aren't just targets but operational imperatives driven by customer demands and regulatory requirements.

The innovation agenda, backed by Adani's deep pockets, is ambitious. 3D printing concrete for construction automation, graphene-enhanced cement for super-strength applications, self-healing concrete for infrastructure longevity. The Rs 500 crore R&D budget, 5x pre-acquisition levels, aims to make ACC India's most innovative cement company.

International expansion, dormant under Holcim, revives under Adani. Middle East markets, accessible through Adani's port network, offer premium pricing for Indian cement. Africa, where Adani has mining and port investments, provides growth opportunities. The target: 10 million tonnes of exports by 2030, generating 25% of revenues from international markets.

The financial engineering mirrors Adani's broader strategy. Asset-light models through grinding unit franchises expand market presence without capital. Infrastructure Investment Trusts (InvITs) monetize logistics assets, recycling capital for growth. Green bonds fund sustainability investments at competitive rates. The objective: double asset turnover while maintaining conservative leverage.

Supply chain integration extends beyond direct synergies. Adani's vendor ecosystem—equipment suppliers, service providers, contractors—now serves ACC at group-negotiated rates. Maintenance contracts cost 20% less, insurance premiums drop 15%, equipment leasing improves 25%. These indirect benefits, totaling Rs 150 crores annually, demonstrate ecosystem value.

The human capital strategy leverages Adani's leadership development programs. High-potential ACC managers rotate through Adani businesses, gaining diverse experience. Adani's aggressive, entrepreneurial culture gradually replaces ACC's bureaucratic legacy. Performance incentives, linked to group objectives, align individual goals with organizational success.

Risk management under Adani is proactive, not reactive. Commodity hedging strategies, developed for Adani Enterprises, protect against input cost volatility. Currency hedging, critical for imported coal, leverages group treasury expertise. Credit insurance, essential in construction markets, benefits from portfolio scale. These risk management tools, unavailable to standalone cement companies, provide stability in volatile markets.

The technology roadmap is revolutionary. Blockchain for supply chain transparency, ensuring customers receive genuine ACC cement. Internet of Things sensors monitor plant performance, predicting failures before they occur. Artificial intelligence optimizes everything from quarry planning to customer delivery. Digital twins simulate plant operations, testing improvements virtually before implementation.

IX. Playbook: Business & Investing Lessons

The boardroom at Holcim's headquarters in Switzerland, 2019. The presenter clicks through slides showing ACC's declining market share, rising costs, and regulatory challenges. The board members, seasoned executives who've overseen cement operations from Brazil to Vietnam, exchange worried glances. How did ACC, once India's cement crown jewel, become such a challenge? The answer reveals timeless lessons about conglomerate ownership, industry consolidation, and capital allocation that every investor and operator must understand.

The Power and Perils of Conglomerate Ownership Structures

ACC's journey through multiple conglomerate owners—from the founding families to Tata, from regional players to global giants, and finally to Adani—illustrates a fundamental truth: ownership structure determines strategic direction. Each owner brought different capabilities, constraints, and cultures that shaped ACC's trajectory.

The Tata era (1936-2000) demonstrated benevolent conglomerate ownership. Tatas provided patient capital, technical expertise, and reputational benefits. But they also imposed conservative growth—consensus decision-making slowed expansion, social obligations limited profitability focus, and diverse stakeholder interests prevented aggressive competition. The lesson: legacy conglomerates excel at building institutions but struggle with entrepreneurial agility.

Holcim's ownership (2004-2022) showcased global conglomerate challenges. Despite superior technology and deep pockets, Holcim failed because they viewed ACC through a European lens. Standardized processes that worked in Switzerland failed in India's relationship-driven market. Global capital allocation priorities starved ACC of growth capital during India's infrastructure boom. The lesson: multinational conglomerates often misread local market dynamics, applying universal solutions to particular problems.

Adani's approach represents modern conglomerate synergy. Unlike financial conglomerates that seek portfolio diversification, Adani builds operational synergies. Ports feed logistics advantages, power provides cost benefits, and ecosystem integration creates competitive moats. The lesson: successful modern conglomerates create value through operational integration, not financial engineering.

How Industry Consolidation Creates Value (and When It Doesn't)

The Indian cement industry's consolidation journey—from 100+ players to meaningful concentration among top 5 players controlling 55% market share—offers nuanced lessons about value creation through M&A.

Consolidation creates value when it generates genuine synergies. UltraTech's serial acquisitions worked because they systematically eliminated subscale players, optimized logistics networks, and achieved procurement economies. Each acquisition strengthened the core. ACC's acquisition by Adani promises value through ecosystem synergies unavailable to standalone players.

But consolidation destroys value when financial engineering substitutes for operational improvement. The 2000s saw numerous debt-funded acquisitions where buyers paid premium multiples expecting price increases that never materialized. Jaypee Group's cement empire, built through leveraged acquisitions, collapsed when pricing power didn't materialize. The lesson: consolidation without integration is speculation.

The timing of consolidation matters enormously. Early consolidators like UltraTech paid reasonable multiples for subscale assets. Late consolidators like Holcim paid peak multiples for mature businesses. The lesson: in consolidating industries, move early or don't move at all.

The Importance of Timing in M&A: Why 2022 Was Perfect for Adani

Adani's acquisition timing was masterful, revealing how external factors create M&A opportunities. Three forces converged in 2022: Holcim's strategic shift toward asset-light models created a motivated seller. Post-COVID infrastructure spending ensured demand growth. Rising ESG pressure made Adani's renewable energy capabilities valuable.

The financing environment was equally favorable. Despite rising global rates, Indian infrastructure assets attracted capital. Adani's strong equity markets performance enabled favorable financing. Competition from UltraTech and JSW validated valuations, preventing lowball offers. The lesson: great M&A requires not just strategic fit but temporal alignment of seller motivation, market dynamics, and financing availability.

Capital Allocation in Capital-Intensive Industries

Cement manufacturing requires enormous capital—Rs 7,000 per tonne for greenfield capacity. This capital intensity creates specific allocation challenges that ACC's history illuminates.

The maintenance versus growth capital dilemma is acute. ACC under Holcim prioritized maintenance, ensuring world-class plant efficiency but sacrificing market share. UltraTech chose growth, accepting lower utilization for greater market presence. The lesson: in capital-intensive industries with economies of scale, growth investment often trumps efficiency optimization.

The technology investment paradox emerges clearly. ACC invested heavily in environmental compliance and energy efficiency—admirable but financially unrewarding in markets where customers won't pay premiums. Meanwhile, nimbler competitors invested in market presence and customer relationships. The lesson: technology investments must align with customer value perception, not engineering excellence.

The working capital trap caught multiple players. Cement's seasonal demand, credit sales culture, and inventory requirements tie up enormous capital. ACC's 56,000-dealer network requires Rs 2,000 crores of working capital—dead money that could fund capacity expansion. The lesson: in capital-intensive industries, working capital efficiency matters as much as fixed asset productivity.

Managing Legacy Businesses Through Ownership Transitions

ACC's multiple ownership transitions reveal how to manage legacy businesses during ownership changes. Successful transitions preserve institutional knowledge while injecting new capabilities.

Cultural integration proves more important than financial integration. When Ambuja acquired ACC, they preserved ACC's technical excellence while adding commercial aggression. When Holcim acquired both, they imposed global standards that alienated local talent. The lesson: respect what works, change what doesn't, and distinguish between the two.

Brand preservation matters enormously. Despite ownership changes, ACC maintained brand consistency—the name, logo, and quality promise remained constant. This brand equity, built over 86 years, commands price premiums and customer loyalty that no acquisition can create. The lesson: heritage brands are irreplaceable assets that require careful stewardship through transitions.

Stakeholder management during transitions determines success. ACC's relationships with dealers, contractors, and communities, cultivated over decades, survived ownership changes because new owners recognized their value. The lesson: in legacy businesses, relationships are assets as valuable as plants and equipment.

The Role of Regulatory Pressure in Forcing Exits

Holcim's exit, triggered by regulatory pressure, demonstrates how regulation shapes industry structure. Holcim was planning to exit India following intense scrutiny of its India operations by the Competition Commission of India (CCI) which opened its second investigation against the company in December 2020. An appeal filed against an earlier penalty imposed by the CCI is currently pending in the Supreme Court.

Regulatory scrutiny increases with market dominance. As ACC-Ambuja's combined market share grew, CCI attention intensified. Penalties, compliance costs, and management distraction made India unattractive for Holcim. The lesson: regulatory costs scale non-linearly with market share—dominance attracts scrutiny that erodes profitability.

Regulatory arbitrage creates opportunities for local players. Adani, understanding Indian regulatory nuances, could operate more efficiently than Holcim. Local knowledge of regulatory processes, relationships with officials, and cultural alignment reduce compliance costs. The lesson: in heavily regulated industries, local players enjoy structural advantages over multinationals.

Leverage Buyouts in Infrastructure Assets

Adani's leveraged acquisition structure—initial offshore debt refinanced through target company cash flows—exemplifies modern infrastructure LBO dynamics.

Infrastructure assets enable leverage because of predictable cash flows. Cement demand correlates with GDP growth, providing revenue visibility. High barriers to entry protect margins. Essential product nature ensures demand resilience. These characteristics support 4-5x debt/EBITDA leverage that would be dangerous in cyclical industries.

The refinancing strategy matters more than initial financing. Adani's genius wasn't in securing acquisition financing but in the refinancing plan—using target company assets, bringing strategic investors, and eventually accessing capital markets. The lesson: in leveraged deals, exit strategy from leverage matters more than entry leverage.

Operational improvements must service debt. Unlike financial engineering LBOs that rely on multiple expansion, infrastructure LBOs require operational improvements to generate cash for debt service. Adani's synergy plan—logistics savings, power cost reduction, and volume growth—creates the cash flow for deleveraging. The lesson: infrastructure LBOs work when operational synergies are real and achievable.

The ecosystem advantage in infrastructure investing becomes clear through ACC's story. Standalone infrastructure assets struggle with input costs, logistics challenges, and market access. Integrated infrastructure platforms solve these challenges systematically. Adani's ports-power-logistics ecosystem creates competitive advantages no standalone cement company can match. The lesson: in infrastructure, ecosystem players increasingly dominate point solution providers.

X. Analysis & Bear vs. Bull Case

The research analyst adjusts her screen, preparing for the video call with the portfolio manager in Singapore. It's 6 AM in Mumbai, and she's been modeling ACC's scenarios since 4 AM. "What's your take?" the PM asks. She pauses. After months of analysis, site visits, and management meetings, ACC remains one of the most complex calls in Indian infrastructure. The bull case is compelling, but the bear case keeps her awake at night.

Bull Case: The Infrastructure Decade Thesis

India's infrastructure story is not hypothesis—it's happening. The National Infrastructure Pipeline commits Rs 111 lakh crores through 2025. The PM Gati Shakti program coordinates infrastructure development across ministries. These aren't political promises; contracts are being awarded, construction has begun. ACC, positioned at infrastructure's heart, captures this growth disproportionately.

India continues to be the world's second largest cement market and yet has less than half of the global average per capita cement consumption. China's cement consumption is over 7x that of India's. The mathematics is compelling: India's per capita cement consumption at 250 kg must reach at least 500 kg to support urbanization. That's a doubling of demand—from 350 million tonnes to 700 million tonnes—over the next decade.

But the real bull case isn't about volume—it's about value. Infrastructure projects require specialized cements—sulfate-resistant for marine structures, low-heat for mass concrete, rapid-hardening for repairs. These premium products command 30-40% higher realizations. ACC's technical capabilities, honed over 86 years, position it perfectly for this high-value demand.

Both Ambuja and ACC will benefit from synergies with the integrated Adani infrastructure platform, especially in the areas of raw material, renewable power and logistics, where Adani Portfolio companies have vast experience and deep expertise. This will enable higher margins and return on capital employed for the two companies. These aren't theoretical synergies—they're operational realities delivering immediate benefits.

Consider the renewable energy advantage. While competitors pay Rs 7-8/unit for grid power, ACC accesses renewable power at Rs 2.50-3/unit through Adani Green Energy. That's Rs 1,600 crores annual savings at full implementation—pure margin expansion. As carbon taxes inevitable arrive, this green power advantage becomes a competitive moat.

The logistics transformation is equally powerful. Adani Ports' coastal shipping reduces transportation costs by 40% versus rail. With cement transportation comprising 30% of delivered costs, this advantage is decisive in coastal markets. ACC can now compete in Mumbai, Chennai, and Kolkata—markets previously uneconomical from inland plants.

Strong brand equity and distribution network provide the foundation for growth. ACC's 56,000 dealers aren't just distribution points—they're relationships built over decades. In India's relationship-driven market, these connections are irreplaceable. New entrants can build plants; they can't build trust.

The ready-mix concrete opportunity remains massive. India's RMX penetration at 7% compares to 60-70% in developed markets. As construction becomes more organized, quality-conscious, and time-sensitive, RMX adoption accelerates. ACC's 85 plants position it to capture this structural shift.

Export potential adds another growth vector. Middle Eastern construction, recovering from the oil price collapse, needs 50 million tonnes of imported cement annually. Indian cement, competitive at $40/tonne FOB, can capture significant share. Adani's port infrastructure makes ACC a natural export champion.

The consolidation opportunity is far from over. India still has 50+ subscale cement producers struggling with environmental compliance, working capital, and market access. As regulations tighten and capital becomes scarce, distressed assets will emerge. ACC, backed by Adani's balance sheet, can acquire selectively, adding capacity at attractive valuations.

ESG leadership, often dismissed as compliance cost, becomes competitive advantage. Global construction companies increasingly mandate sustainable materials. European infrastructure funds require carbon-neutral cement. ACC's renewable power usage and carbon reduction roadmap position it for these premium markets.

The financial flexibility under Adani transforms growth potential. Unlike Holcim's capital rationing, Adani provides unlimited growth capital for profitable projects. The plan to reach 140 MTPA by 2028—quadrupling current capacity—is aggressive but achievable given ecosystem advantages.

Bear Case: The Structural Challenges