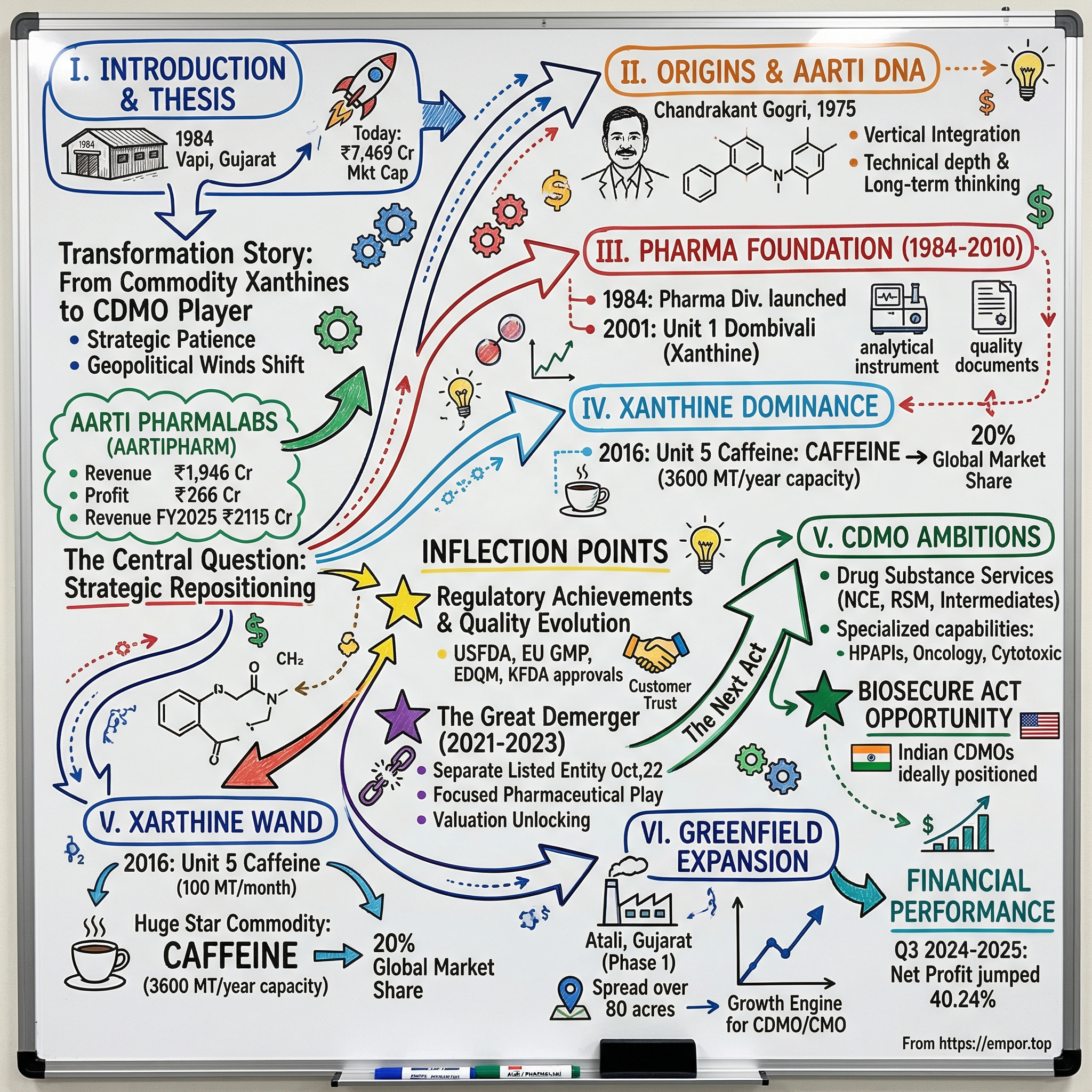

Aarti Pharmalabs: India's Xanthine Champion and the CDMO Transformation Play

I. Introduction & Episode Roadmap

Picture a can of cola sliding across a convenience-store counter somewhere in suburban America. Picture the energy drink a graduate student cracks open at 2 a.m. before an exam. Picture the bottle of theophylline a pharmacist hands to an asthmatic grandmother in São Paulo. These three moments have nothing in common—except that, with surprising frequency, the molecule doing the work inside each of them was synthesized not in China, not in Germany, but in a cluster of reactors in Gujarat and Maharashtra, India, by a company most Western consumers have never heard of.

That company is Aarti Pharmalabs Limited, and its story is one of the more quietly remarkable industrial transformations to come out of India's chemicals belt. Here is the hook that animates this entire episode: how did a sleepy, commodity-focused chemicals-and-pharma division buried inside a sprawling Indian conglomerate spin itself out, quietly capture somewhere between fifteen and twenty percent of the entire global caffeine market, and then use that boring, dependable cash engine to fund an audacious bet on the high-margin frontier of contract pharmaceutical manufacturing?15

Let us anchor the scale before we go any further, because the numbers tell you immediately that this is not a hobby business. In fiscal year 2025, Aarti Pharmalabs reported consolidated revenue of roughly ₹2,115 crore—a little over a quarter of a billion US dollars.[^7] Net profit after tax came in at ₹272 crore, and standalone EBITDA margins ran at around twenty-two percent.[^7] For a company born from the unglamorous world of benzene chemistry, those are margins that look more like a specialty pharma player than a bulk chemicals shop. That gap—between what the business looks like on the surface and what it is quietly becoming—is the heart of our story.

The central question we are going to wrestle with today is this: in a world where Chinese chemical giants dominate on raw cost and established Indian pharma behemoths like Divi's Laboratories command premium valuations, how does a mid-market player carve out a durable moat? How do you build something defensible around a molecule as old and as commoditized as caffeine, while simultaneously pivoting toward oncology APIs, complex corticosteroids, and custom synthesis for the world's drug innovators?

Our thesis is that Aarti Pharmalabs represents something close to the platonic ideal of a "cash cow to high-growth star" transition. It is a case study in vertical integration taken to an almost obsessive degree, in opportunistic capital deployment that occasionally borders on the audacious, and in riding one of the largest geopolitical tailwinds of our era—the great "China + 1" supply-chain diversification that has reshaped how the world thinks about where its medicines and ingredients come from.

Here is the roadmap for the next couple of hours. First, we will trace the Aarti conglomerate DNA and the Gogri family legacy that produced it. Second, we will get our hands dirty with the secret chemistry of the xanthine dominance and the strange global beverage oligopoly it serves. Third, we will dissect the 2022 demerger that set this business free. Fourth, we will analyze a masterclass in capital allocation through the curious case of the Ganesh Polychem joint venture. Fifth, we will examine the high-stakes pivot into small-molecule CDMO and the regulatory fortress that protects it. And finally, we will run the whole thing through the analytical machinery of Porter's Five Forces and Hamilton's Seven Powers before weighing the bull and bear cases. Let us begin where every good industrial story begins—with a family and a single, stubborn philosophy.

II. The Aarti Group DNA & Chemical Foundations (1984–2010)

In 1984, India was still a closed economy. The License Raj governed who could manufacture what, in what quantity, and where. Importing a chemical feedstock meant navigating a thicket of permits, foreign-exchange controls, and the perpetual uncertainty of whether your supplier on the other side of an ocean would actually deliver. It was in this environment—scarcity, control, and chronic dependence on imports—that the Gogri family planted the seed of what would become Aarti Organics, operating under the larger umbrella of Aarti Industries Limited.1

The founding insight was almost monastic in its simplicity, and it has echoed down through four decades of the company's decision-making: never rely on anyone else for your raw materials. In a country where the chemicals and pharmaceutical industry was structurally addicted to Chinese Key Starting Materials—the so-called KSMs that form the first link in any drug's supply chain—the Aarti philosophy was to build backward, relentlessly, into one's own feedstock. If you needed an intermediate, you learned to make the intermediate. If that intermediate required a precursor, you learned to make the precursor too. The family's chemistry was anchored in benzene-based value chains, the aromatic backbone from which a staggering variety of dyes, agrochemicals, and pharmaceutical building blocks are derived.

Why does this forty-year-old origin story matter to an investor sizing up the company in 2026? Because vertical integration is not a slogan you can bolt on later—it is an accumulated capability, built reaction by reaction, plant by plant, over decades. When global pharmaceutical buyers in the 2020s went looking for suppliers who were genuinely insulated from Chinese feedstock shocks, the companies that could credibly say "we make our own starting materials" were vanishingly rare. Aarti could. That is not a strategy that was invented in a boardroom during the pandemic; it was the literal founding genome of the firm.

The transition from industrial chemicals into pharmaceuticals came in stages, and each stage was a deliberate climb up the value ladder. The company commissioned its first active pharmaceutical ingredient manufacturing unit in Dombivali—Unit 1—in 2001.1 This was the moment the firm stopped being purely a chemicals supplier and started learning the far more demanding discipline of making molecules that go inside human bodies. The difference is not trivial. Manufacturing an industrial dye and manufacturing an API are separated by an enormous chasm of documentation, purity control, batch traceability, and regulatory scrutiny. Then, in 2005, the company took the next decisive step by launching Unit 4 in Tarapur, explicitly built to serve regulated markets—the United States, Europe, and the other jurisdictions where the bar for quality is set by the most demanding pharmaceutical regulators on earth.1

This is where the chemical history stops being a quaint origin tale and becomes the foundation of the modern moat. Aarti's deep, almost instinctive understanding of basic organic synthesis—of how to run multi-step reactions safely, of how to handle hazardous intermediates, of how to treat industrial waste streams, of how to wring efficiency out of a process—became the bedrock on which everything pharmaceutical was later built. A company that has spent forty years learning the unglamorous craft of making benzene derivatives at industrial scale has internalized a kind of process intelligence that a pure-play pharma startup simply cannot buy or hire its way into quickly. That accumulated know-how, paired with a non-Chinese-dependent starting-material chain, is the company's ultimate margin shield—the thing that lets it hold price and protect profitability when raw-material markets convulse. With that foundation laid, the question becomes: who, today, is steering the ship, and how aligned are they with the shareholders along for the ride?

III. Current Management, Ownership & Incentives

There is a moment in the life of every family-controlled industrial group when the question of succession and stewardship moves from polite drawing-room conversation to hard operational reality. For Aarti Pharmalabs, that moment arrived with the demerger, when the pharma business was handed the keys to its own future and a specific cast of family members and professional managers had to prove they could run it as a standalone enterprise. Understanding who these people are, and—crucially—how they are paid, tells you almost everything about whether minority shareholders are riding alongside the insiders or quietly being taken for a ride.

At the top sits Rashesh C. Gogri, Chairman and Non-Executive Director. A production engineer trained at Mumbai University, Rashesh occupies the role of strategic and group-level guide rather than day-to-day operator. He holds an individual stake of roughly 4.23 percent of the company, equivalent to some 3,834,404 shares.[^11] His function is the one you want a family chairman to play in a maturing business: the keeper of long-term capital-allocation discipline and the connective tissue back to the broader Aarti group's institutional knowledge, without micromanaging the operating engine.

The genuine operational force, however, is Hetal Gogri Gala, Vice Chairperson and Managing Director. She is the executive most directly responsible for driving the demerged entity forward, and she holds an individual stake of approximately 2.89 percent, or around 2,615,548 shares.[^11] But the stake is not the interesting part of her compensation story. The interesting part is the structure of her pay.

For fiscal year 2024, Hetal Gogri Gala's remuneration came to approximately ₹10.32 crore.2 On its own, that is an unremarkable number for a managing director of a profitable mid-cap. What is remarkable—genuinely unusual, even—is the composition. Roughly 89.4 percent of that compensation was variable: performance-linked commission and bonuses tied to how the company actually performed. Only about 10.6 percent was fixed base salary.2 Pause on that for a moment, because it is rare. In most companies, executive pay is dominated by guaranteed salary with a modest performance kicker on top. Here, the relationship is almost inverted. If the company stumbles, the managing director's income stumbles with it. This is one of the most highly aligned promoter-incentive structures you will find anywhere in the Indian mid-cap universe, and it means that Hetal's daily execution is wired directly into the same outcome that a minority shareholder cares about—profitable growth, not empty top-line vanity.

Alongside the family sits the professional backbone of the operation: Narendra J. Salvi, who serves as a Managing Director in his own right but as a non-promoter professional executive. Salvi brings more than thirty-six years of experience in the API sector and holds a Master of Science in Organic Chemistry.1 His remit is the unglamorous, mission-critical machinery of the business—daily operations, research and development, and the regulatory quality systems that span all six of the company's manufacturing plants. In a business where a single botched FDA inspection can vaporize years of carefully built customer trust, having a deeply technical chemist with nearly four decades of API-specific scar tissue running quality is not a luxury; it is the whole ballgame.

Step back and look at the ownership picture in aggregate. Total promoter-group holding stands robustly at around forty-five percent.[^11] That is the sweet spot many long-term investors look for: high enough that the insiders have profound skin in the game and every incentive to compound value patiently, but not so absolute that minority voices and institutional board representation become irrelevant. And institutions have been paying attention—in December 2024, Sunil Singhania's Abakkus fund acquired a stake in Aarti Pharmalabs via a bulk deal, a notable vote of confidence from one of India's more respected fundamental-value investors.[^8] With the human and incentive architecture established, we can finally turn to the engine that generates all the cash: the molecule that wakes up the world.

IV. Core Business Engine Part 1: The Xanthine Powerhouse (The Cash Cow)

Every morning, several billion people perform the same small ritual: they ingest a mild, naturally occurring stimulant to make the day bearable. They call it coffee, or tea, or an energy drink, or a cola. Chemists call it caffeine, and caffeine belongs to a family of compounds called xanthines—a cluster that also includes theophylline, used to relax the airways of people with asthma and chronic respiratory disease, and aminophylline, its close cousin. These molecules act on the central nervous system as stimulants and on the lungs as bronchodilators, and they have been doing so, commercially, for well over a century.1

Here is the part that surprises people. The caffeine in your energy drink is, more often than not, not extracted from coffee beans or tea leaves. It is synthesized—built up, molecule by molecule, in industrial reactors from simpler chemical starting materials. Synthetic caffeine is cheaper, purer, and far more consistent than the extracted kind, which is exactly what a beverage company wants when it is producing hundreds of millions of identical cans that must all taste precisely the same. And in the global business of synthesizing caffeine, Aarti Pharmalabs is India's undisputed king.

The scale is what makes it a genuine moat rather than a side hustle. The company operates xanthine capacity of roughly 5,000 metric tonnes per annum, and it has been expanding aggressively toward 9,000-plus metric tonnes per annum across two sites.[^2][^9] On the strength of that capacity, Aarti controls somewhere between fifteen and twenty percent of the entire global caffeine market.5 To put that in human terms: a meaningful slice of all the synthetic caffeine consumed on planet Earth passes through this one Indian company's reactors.

To appreciate how unusual that position is, you have to understand the competitive landscape, which historically looked less like a free market and more like a tight oligopoly. For decades, global synthetic caffeine was dominated by a handful of Chinese producers and a single ultra-high-purity German player. On the Chinese side stand the giants: 石药集团 CSPC Pharmaceutical Group, generally regarded as the world's single largest caffeine producer with something like forty percent of the market; 山东新华制药 Shandong Xinhua Pharmaceutical; and 吉林舒兰 Jilin Shulan Synthetic.5 Taken together, Chinese players have historically controlled on the order of seventy percent of global synthetic caffeine volume.5 Then there is the German anchor, BASF SE, operating out of its colossal Ludwigshafen complex with roughly thirty percent of the global market and a focus on the ultra-high-purity, pharmaceutical-grade end of the spectrum.5

Into this concentrated field, Aarti has inserted itself as the credible third pole—and here is where the strategy gets genuinely clever. Why would a global FMCG titan—Coca-Cola, PepsiCo, Monster, Celsius—choose to source caffeine from a mid-market Indian firm rather than simply buying the cheapest Chinese tonnage? The answer is a combination of grade and geopolitics.

Consider grade first. Sourcing caffeine for beverages is a game of obsessive consistency. The product is typically caffeine anhydrous, and the tolerance for impurity is brutally low. A trace contaminant that would be invisible in an industrial application can subtly alter the flavor profile of a soda—and when you are bottling hundreds of millions of cans that consumers expect to taste identical every single time, a flavor deviation is not a minor quality issue; it is a brand-threatening catastrophe. A supplier who can guarantee that level of purity, batch after batch, year after year, earns a kind of trust that is extraordinarily hard to win and easy to lose.

Now layer on the geopolitics—the "China + 1" procurement tailwind. The world's largest consumer brands learned a painful lesson over the past several years: a supply chain with a single point of failure is a liability waiting to detonate. If your entire caffeine supply runs through Chinese factories and a trade dispute, a regulatory crackdown, a port shutdown, or a pandemic interrupts that flow, your production lines stop and your shelves go empty. FMCG majors simply cannot tolerate that risk. And so they went looking for a high-quality, reliable, non-Chinese alternative to diversify into—and Aarti, with its clean regulatory record and integrated chemistry, was waiting. Global brands have, by various accounts, shifted somewhere in the range of fifteen to twenty-five percent of their caffeine sourcing toward Aarti specifically to build that supply-chain resilience.[^2]

The economics of all this are what make the xanthine business the beating heart of the company's financial model. It is high-volume and stable-margin—not a glamorous business, but a profoundly dependable one. Xanthines contribute somewhere between forty-three and forty-nine percent of total revenue, and they generate the steady, highly predictable cash flows that bankroll everything else.[^2] This is the cash cow in the truest sense: a mature, defensible, cash-generative engine whose profits are quietly funneled into the company's far more ambitious API and CDMO expansions. Which raises the natural next question—what exactly is the company building with all that caffeine cash? The answer begins in the regulated world of generic active pharmaceutical ingredients.

V. Core Business Engine Part 2: The Generic API Portfolio (The Regulatory Moat)

If the xanthine business is about volume and consistency, the API business is about something harder to acquire and far harder to take away: regulatory trust. To understand why, you have to understand what it actually takes to sell a pharmaceutical ingredient into a regulated market like the United States or the European Union. You do not simply manufacture a molecule, package it, and ship it. You need, in effect, a passport—a thick stack of regulatory approvals, audits, and filings that certifies your facility, your processes, and your quality systems to the satisfaction of the world's most demanding drug regulators.

Aarti's deliberate strategy over the past decade has been to climb out of the bloody, low-margin trenches of bulk generic APIs—where everyone competes on price and the cheapest tonne wins—and toward higher-value, more defensible molecules. The portfolio has shifted toward high-potency active pharmaceutical ingredients, the so-called HPAPIs that require specialized containment because they are biologically active at minute doses; toward oncology drugs used in cancer therapy; and toward complex corticosteroids, a notoriously finicky class of anti-inflammatory compounds whose multi-step synthesis rewards exactly the kind of process mastery Aarti spent forty years accumulating.1 Together, APIs and intermediates drive somewhere between thirty-nine and forty-four percent of total revenue, built on a foundation of more than fifty-five commercialized APIs and over 140 generic intermediates.[^2]

But the molecules themselves are only half the story. The other half—the half that actually constitutes the moat—is the regulatory fortress. Over the years, Aarti has accumulated accreditations from an alphabet soup of the world's toughest agencies: the United States Food and Drug Administration; EU GMP, the European Union's Good Manufacturing Practice standard; the EDQM, Europe's directorate for the quality of medicines; South Korea's KFDA; and Mexico's COFEPRIS.1 Each of those is a separate, grueling certification process. And on top of the facility approvals sit the product-level filings: Aarti holds more than fifty US Drug Master Files—the confidential dossiers that document exactly how a given API is manufactured—and more than thirty-one CEPs, the Certificates of Suitability that allow a product to be sold across Europe.[^2]

Why does this matter so much to the investment case? Because it is precisely the kind of barrier that money alone cannot quickly buy. A well-funded competitor could, in theory, build a chemical plant in eighteen months. What that competitor cannot do is conjure up a multi-year track record of clean USFDA inspections with zero major warning letters or import alerts. That record is a function of time, discipline, and institutional culture—it accrues slowly and can be destroyed overnight by a single serious compliance failure. For a global pharmaceutical major sourcing an API, the nightmare scenario is a supply halt triggered by a regulatory action against their supplier. They will pay a premium, and they will stay loyal for years, to avoid that risk. An immaculate regulatory record is therefore not a checkbox; it is a deep, durable institutional trust that compounds over time and forms a multi-year barrier to entry around the business.

This regulatory fortress is also the precise foundation on which the company's most ambitious bet is being built—because the same clean track record that makes you a trusted generics supplier is the price of admission to the far more lucrative world of contract manufacturing for innovators. But before we get to that pivot, we need to understand the corporate event that made the entire transformation possible: the great unbundling of 2022.

VI. The Greenfield Expansion & Capital Deployment: The Ganesh Polychem Bargain

Conglomerates are, in a sense, a bet against the market's ability to value things correctly. When a fast-growing, high-margin, regulatory-driven pharma business is bolted onto a capital-hungry, cyclical specialty-chemicals core, the stock market tends to do something frustrating: it values the combined entity at some muddy blended multiple that does justice to neither half. The pharma growth gets discounted by the chemicals cyclicality; the chemicals stability gets ignored amid the pharma volatility. The cure for this affliction is the demerger—the surgical separation of the two businesses so that each can be valued, capitalized, and managed on its own terms.

That is exactly what happened in October 2022, when Aarti Pharmalabs was formally spun off from its parent, Aarti Industries.[^4] The mechanics were straightforward: shareholders of Aarti Industries received one share of the newly independent Aarti Pharmalabs for every four shares of the parent that they held.[^4] The strategic logic was equally clear. Separating the high-margin, regulatory-driven pharma and CDMO business from the high-CAPEX, cyclical specialty-chemicals business allowed each to pursue its own growth path, raise its own capital, and—critically—be judged by the market on its own merits. For the pharma entity, it meant focus, an independent balance sheet, and the freedom to deploy capital into the opportunities that mattered most to it.

And deploy capital it did. The centerpiece of the post-demerger growth story is the greenfield expansion at Atali, in Bharuch, Gujarat—a massive program with a capital outlay in the range of ₹400 to ₹450 crore, spread across an eighty-acre site.[^9] Phase 1 came online with 440 kilolitres of reactor capacity across sixty-three reactors, and the site was deliberately designed with headroom to scale up to something like eight to ten times the company's current capacity.[^9] A greenfield site of this scale is not merely additional volume; it is a statement of intent. You do not build that much optionality into a plant unless you are planning to fill it with high-value work, and the work Aarti has in mind is the contract manufacturing we will turn to shortly.

But the most instructive capital-allocation story of the post-demerger era is not the headline-grabbing greenfield. It is a quieter, almost overlooked transaction: the Ganesh Polychem joint venture. This is the kind of deal that fundamental investors love to find, because it reveals how management thinks about value when no one is watching closely.

Here is what happened. Effective April 1, 2025, Ganesh Polychem Limited officially transitioned into a fifty percent joint venture of Aarti Pharmalabs, formalized in March 2025.4 Aarti held its fifty percent equity stake in GPL at a historical cost of just ₹12.61 crore—a value that had been transferred during the demerger.4 Now, ₹12.61 crore is a small number, the kind of line item that disappears in a footnote. But look at what that small number actually controls. Ganesh Polychem generated EBITDA of approximately ₹14 crore in the third quarter of fiscal 2025 alone.[^7] Annualize even conservatively, and you arrive at an EBITDA run-rate somewhere in the range of ₹40 to ₹50 crore for the whole entity.

Now run the comparison that any analyst would run. Indian specialty-chemical companies typically trade at enterprise values of roughly twelve to eighteen times EBITDA. A fifty percent stake in GPL, representing perhaps ₹20 to ₹25 crore of Aarti's share of EBITDA, would on the open market plausibly be valued somewhere between ₹240 and ₹350 crore.4 In other words, an asset carried on the books at ₹12.61 crore may be worth twenty to thirty times that figure on a fair-value basis. By retaining and consolidating this joint venture for a book value that is almost a rounding error, Aarti executed an extraordinarily accretive piece of capital deployment with virtually zero cash outlay. This is what disciplined, opportunistic capital allocation looks like in practice—not a flashy billion-dollar acquisition, but a quiet retention of a hidden gem at a fraction of its intrinsic worth. And as we will see, GPL is not merely a financial curiosity; it is a strategic bridge into one of the most exciting corners of the company's future. Which brings us to the pivot that the entire transformation has been building toward.

VII. The CDMO Pivot: The Future Growth Engine

There is a fundamental difference between two ways of making money in pharmaceutical chemistry, and the entire future of Aarti Pharmalabs hinges on the company's ability to migrate from one to the other. In generic APIs, you compete on price. Your molecule is identical to your competitor's molecule, your buyer knows it, and every negotiation is a grind toward the lowest sustainable cost. In contract development and manufacturing—CDMO—you compete on something far richer and far stickier: chemistry, speed-to-market, and the protection of your customer's intellectual property.

Let us define the term plainly, because it gets thrown around loosely. A CDMO is a partner that an innovating drug company hires to develop and manufacture a proprietary molecule—often a brand-new compound still working its way through clinical trials. The innovator owns the intellectual property and the eventual drug; the CDMO supplies the process chemistry, the scale-up expertise, and the manufacturing muscle to turn a lab-bench discovery into commercial-scale production. It is a relationship built on trust, technical collaboration, and absolute discretion, and it commands far better economics than commodity work. EBITDA margins for CDMO services typically run between twenty-five and thirty-five percent, compared with the fifteen to eighteen percent that commodity chemicals deliver.[^2] That margin gap is the whole reason for the pivot.

Today, the CDMO business is still the smallest of Aarti's three engines, representing roughly twelve to thirteen percent of total revenue.[^2] But it is the fastest-growing by a wide margin, expanding at a projected thirty to forty percent year-over-year.[^2] More importantly, the pipeline that feeds it is maturing in exactly the right way. Aarti has built relationships with twenty-one active global customers, working across sixty projects—of which thirty-three are already in the commercial phase and twenty-seven remain in active development.[^2] That ratio matters enormously, because the development-stage projects are the seed corn: each one that successfully graduates into commercial manufacturing becomes a long-duration, high-margin annuity that can run for the life of the underlying drug.

There is also a fascinating "hidden" dimension to this story, and it runs straight back through the Ganesh Polychem joint venture we just discussed. Through GPL, Aarti has gained exposure to high-performance monomer intermediates—specifically compounds like DCDPS and DADPS, the building blocks of advanced sulfone polymers used in aerospace and other demanding high-performance applications.4 Why should a pharma investor care about aerospace polymer intermediates? Because this is genuine non-pharma optionality—a highly profitable, fast-growing specialty-chemicals business that leverages the very same chemical-engineering DNA the group has cultivated for four decades, sitting quietly inside the structure and barely reflected in how most observers value the company.

And then there is the macro tailwind, which may be the single most important external force acting on the business. The United States has been advancing the BioSecure Act, legislation aimed at restricting US companies from contracting with certain Chinese biotech and pharma service giants—names like 药明康德 WuXi AppTec and 药明生物 WuXi Biologics, which have long been dominant forces in global drug development and manufacturing services.6 If that legislation forces global innovators to migrate their CDMO contracts away from Chinese partners, those innovators need somewhere to go. They need partners with clean FDA track records, world-class chemistry, and the physical capacity to absorb the work. Aarti—with its immaculate regulatory record and its purpose-built greenfield site at Atali waiting to be filled—is positioned almost perfectly to capture a slice of what could be a multi-decade structural shift in where the world's medicines are made.6 Management has not been shy about the ambition, setting an aggressive medium-term target of ₹1,000 crore in CDMO and CMO revenue.[^2] Whether they can hit it is the central uncertainty of the entire investment case. To weigh that, we need to step back and analyze the business through the cold, structural lenses of competitive strategy.

VIII. Framework Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Strip away the narrative for a moment and run Aarti Pharmalabs through the two great frameworks of competitive analysis. Michael Porter's Five Forces tell you how attractive the structural battlefield is; Hamilton Helmer's Seven Powers tell you what, specifically, lets this company keep more of the spoils than its rivals. Together they form a kind of X-ray of durability.

Porter's Five Forces Applied to Aarti Pharmalabs

Start with the threat of new entrants, which is very low. To compete with Aarti on its own turf, a newcomer would have to build USFDA-approved plants, secure EDQM certification, and stand up integrated organic-synthesis reactor trains—a combination that demands massive capital, on the order of ₹400 crore or more, and three to five years of regulatory audit cycles before a single commercial gram can be sold into a regulated market.[^9] That time-plus-capital wall is the single most reliable protector of incumbent profits in this industry.

Next, the bargaining power of buyers, which is moderate. The high-volume caffeine buyers—the global beverage giants—are enormous and undeniably possess pricing leverage. But they temper their use of it because what they prize above raw price is supply-chain security and zero-impurity guarantees, both of which raise the cost of switching away from a proven supplier. In the CDMO segment, buyer power is even weaker once a relationship matures: the moment a drug is filed with regulators listing Aarti as the registered manufacturer, the customer is structurally locked in for years.

Third, the bargaining power of suppliers, which is low—and this is where forty years of backward integration pays off. Because Aarti makes so many of its own intermediates and key starting materials, it is far less exposed to the raw-material cost shocks and supply interruptions that whipsaw less-integrated competitors. The company is, to a meaningful degree, its own supplier.

Fourth, the threat of substitutes, which is very low. There is simply no chemical or functional substitute for caffeine in global beverage formulation—nothing else delivers that exact stimulant profile that consumers have been trained over generations to expect. The same is true of oncology APIs, where the specific molecule is the therapy and cannot be swapped for something else.

Finally, the competitive rivalry, which is high—the one force that genuinely bites. In caffeine, Aarti faces relentless low-cost Chinese volume players led by 石药集团 CSPC. In CDMO and APIs, it competes against premier Indian names like Divi's Laboratories, Syngene, and Neuland Labs, all of whom are chasing the same "China + 1" opportunity. This is the force that keeps management honest and prevents the business from ever growing complacent.

Hamilton's Seven Powers

Of Helmer's seven powers, four show up clearly here. The first is high switching costs, concentrated in the CDMO segment. Once a pharmaceutical innovator registers its drug substance with the FDA naming Aarti as the manufacturing partner, switching to a rival CDMO would require years of bioequivalence testing, fresh regulatory re-filings, and significant capital—a process so painful that customers rarely undertake it without overwhelming cause. This is the deepest and most valuable of Aarti's powers, and it is exactly the one the company is racing to accumulate.

The second is scale economies, concentrated in the xanthine segment. Operating at 5,000 metric tonnes per annum and climbing toward 9,000 lets Aarti spread its fixed regulatory, R&D, and compliance costs across an enormous volume base, keeping per-unit costs competitive even against Chinese manufacturers who enjoy other structural advantages.[^2]

The third is process power—the accumulated chemistry know-how. More than forty years of proprietary organic-synthesis expertise, multi-step reaction handling, and waste-treatment capability constitute a body of operational knowledge that competitors cannot simply hire or reverse-engineer in a hurry. It is embedded in people, procedures, and institutional muscle memory.

The fourth is brand and trust, expressed as the regulatory record. The company's clean, multi-decade history of compliance with the USFDA and other global agencies functions as an institutional trust moat—a reputation that buyers rely on and that takes years to build but only a single serious failure to destroy. Having mapped the structural defenses, the real value of these frameworks emerges only when we turn them into actionable lessons and then stress-test them against the risks.

IX. Playbook: Business & Investing Lessons

Step back from the specifics of caffeine and corticosteroids, and Aarti Pharmalabs offers a set of transferable lessons—the kind of patterns that recur across industries and decades, which is exactly what makes a business history worth studying rather than merely admiring.

The first is the conglomerate demerger playbook. When you separate a fast-growing, high-margin, regulatory-heavy business from a capital-intensive, cyclical core, you do two things at once. You unlock a valuation multiple, because the market can finally price each business on its own characteristics rather than smothering both in a blended average. And you furnish each business with its own independent pool of growth capital and its own focused management attention. The 2022 separation from Aarti Industries was a textbook execution of this move, and the subsequent freedom to pour capital into Atali and to opportunistically retain Ganesh Polychem is the direct dividend of that focus.

The second is the "China + 1" execution guide, and it is more subtle than it first appears. The naive version of "China + 1" is to try to out-China China—to beat the world's lowest-cost producers on pure price. That is a losing game; you will never win a cost war against entrenched scale and state support. The sophisticated version, the one Aarti actually runs, is to compete on the dimensions where Chinese dominance is a liability rather than an asset: supply-chain security, regulatory trust, and vertical integration. You do not ask the customer to pay less; you ask them to sleep better at night. That is a far more defensible value proposition, and it commands a premium rather than a discount.

The third is variable promoter compensation as an alignment engine. When roughly ninety percent of the managing director's pay is tied directly to company performance, you have engineered a structure in which the controlling family's day-to-day economic interest is almost indistinguishable from the minority shareholder's.2 This is the kind of governance signal that fundamental investors should weight heavily, because incentives, over long enough horizons, shape behavior far more reliably than mission statements do.

The fourth lesson is the one most likely to be dismissed as a soft factor and most likely to be underestimated: green, sustainable moats. Aarti Pharmalabs became the sixth pharmaceutical company in India to achieve approval under the Science Based Targets initiative, and it secured an EcoVadis Gold rating—a top-tier sustainability assessment.[^12] A decade ago, this would have been a public-relations footnote. Today it is an active procurement requirement. Global beverage and pharmaceutical majors increasingly screen their suppliers on verified environmental performance, and a supplier who cannot demonstrate credible sustainability credentials can find itself quietly excluded from tenders it would otherwise win. In a business where the entire pitch is supply-chain reliability and trust, sustainability has quietly become part of the price of admission. These lessons are the optimistic read; the discipline of investing demands that we now turn them over and examine the downside.

X. Financial Trajectory & Core KPIs

Numbers tell a story only when you read them as a sequence rather than a snapshot, so let us walk the consolidated trajectory across the four fiscal years since the demerger and listen to what the arc is actually saying.

Fiscal 2023 was the post-demerger baseline—the first full picture of the business as a standalone entity. Revenue came in at roughly ₹1,948 crore, EBITDA at ₹344 crore, and net profit at ₹193 crore.[^2] This was the starting line, the year against which everything subsequent would be measured.

Fiscal 2024 told a quietly encouraging story about quality over quantity. Revenue actually dipped slightly to about ₹1,853 crore, yet EBITDA rose to ₹386 crore and profit climbed to ₹217 crore.[^2] Read that carefully: the top line shrank while profitability expanded, with margins widening to roughly 20.8 percent. That is the fingerprint of a deliberate mix shift—the company selling proportionally less low-margin commodity volume and more high-margin, value-added product. It is exactly the kind of "less revenue, more profit" pattern that thoughtful investors should find reassuring rather than alarming.

Fiscal 2025 was the peak year, and it was a strong one. Revenue surged to ₹2,115 crore, EBITDA jumped to ₹464 crore, and net profit reached ₹272 crore, with margins touching twenty-two percent.[^7] The drivers were precisely the two engines the company most wants firing: robust CDMO growth and strong xanthine volume. For a moment, the transformation thesis looked like it was simply going to compound smoothly upward.

Then came fiscal 2026, and the headwinds. Revenue fell to around ₹1,819 crore and profit dropped to roughly ₹175 crore.[^7] Taken in isolation, that looks like a worrying reversal. But the narrative context matters enormously, and this is where an investor earns their keep by looking past the headline. The decline was not the symptom of a collapsing business. It was the product of a perfect storm of largely non-operating and one-time factors: roughly ₹33.2 crore of unrealized foreign-exchange derivative losses—mark-to-market hits on hedging positions rather than real cash going out the door; the implementation of new domestic labor codes that raised costs; and an accounting transition to equity-method consolidation for the Ganesh Polychem joint venture, which changed how GPL's contribution flows through the financials.[^7] None of those three is a sign that the underlying caffeine-and-CDMO engine is failing. They are, in the main, the kind of noise that obscures signal for a year or two before washing out. The thoughtful question is not "why did fiscal 2026 dip?" but "is the structural growth engine intact beneath the dip?"—and the operating evidence suggests it is.

Which leads to the genuinely useful exercise: of all the metrics one could track, which few actually matter for monitoring this company's progress? Three stand out, and an investor watching only these would understand the story far better than one drowning in the full financial statement.

The first is the CDMO active-project conversion rate—how many of those twenty-seven development-stage projects successfully graduate into commercial manufacturing.[^2] This is the leading indicator of the entire premium-margin transformation. Each conversion is a multi-year annuity locking in; a stall in conversions would be the earliest warning that the CDMO thesis is faltering.

The second is xanthine capacity utilization, particularly at the newly expanded Atali and brownfield sites. Building 9,000 metric tonnes per annum of capacity is only value-creating if global FMCG buyers actually absorb it. Watching how quickly that expanded capacity fills tells you whether the "China + 1" caffeine demand is real and durable or merely hoped-for.

The third is the standalone EBITDA margin, with management implicitly targeting the 22 to 24 percent band. This single number is the cleanest summary of the entire mix-shift thesis: as lower-margin generics give way to higher-margin CDMO services, the margin should grind upward. If it does, the transformation is working. If it flatlines or slips for non-transitory reasons, the thesis needs re-examination. With the scoreboard understood, we can finally stage the debate between the optimists and the skeptics.

XI. The Bull vs. Bear Case

Every compelling investment is, at its core, an unresolved argument between two plausible futures. Let us give each side its strongest case and let them fight it out across the same structural terrain we mapped earlier.

The Bear Case

The bears begin with the most direct threat: Chinese dumping. The xanthine business, for all its scale economies, sells a commodity, and the Chinese players led by 石药集团 CSPC command both the volume and the cost structure to wage aggressive pricing wars. If they choose to flood the market to defend share, global caffeine margins could compress, and Aarti's cash cow could give less milk precisely when the company most needs cash to fund its pivot. This is the rivalry force from Porter's framework asserting itself at its most dangerous.

Second, the bears point to execution risk at Atali. A ₹400-crore-plus greenfield facility is a complex undertaking, and any delay in commissioning or in commercializing the new capacity pushes out the returns on a very large capital commitment. Idle reactors earn nothing while depreciation and financing costs accrue. The bull case depends on a smooth ramp; the bear case asks what happens if the ramp stutters.

Third is forex and derivative volatility. With more than half of revenue coming from exports, the company is structurally exposed to currency swings, and the ₹33.2 crore unrealized derivative loss in fiscal 2026 is exhibit A for how that exposure can bruise reported earnings even when the operating business is healthy.[^7] A persistent run of adverse currency movements would be a recurring drag.

Fourth, the bears flag client concentration. The xanthine revenue rests heavily on a handful of global beverage giants. That is a double-edged sword: those relationships are sticky and high-quality, but the loss or pullback of even one major buyer would leave a conspicuous hole. Concentration is comfortable until, suddenly, it is not.

The Bull Case

The bulls counter with the structural tailwind that could dwarf every bear concern: the BioSecure windfall. If US legislation accelerates the migration of innovator CDMO contracts out of China, Aarti's clean FDA record and waiting Atali capacity position it as a prime beneficiary of a shift that could play out over a decade or more.6 This is not a cyclical kicker; it is a potential secular re-routing of global pharmaceutical manufacturing, and Aarti has spent forty years building exactly the credentials it requires.

Second, the bulls see the asset turnaround at Atali not as a risk but as the central value-creation engine. A successful ramp of that facility could drive a sustained revenue and EBITDA compounding rate in the mid-to-high teens over the coming years, exactly the kind of durable growth that re-rates a stock.

Third—and this is the bull's most ambitious claim—is valuation re-rating. Today the market tends to value Aarti somewhere in the range of an industrial chemicals multiple. But if the CDMO revenue share climbs past twenty-five percent of the total, the bulls argue, the market may come to view the company as a premium CDMO and pharma play, the way it values a Divi's or a Syngene. The gap between an industrial chemicals multiple and a premium CDMO multiple is enormous, and closing it would represent a substantial portion of the bull-case return—earnings growth and multiple expansion compounding together.

Fourth, the bulls hold Ganesh Polychem as free optionality. That high-margin specialty-polymer-intermediate JV, carried at a book value that is almost a rounding error, could scale meaningfully as its facilities are upgraded—a non-pharma kicker that most observers are not paying anything for.4

Weigh the two cases through Helmer's lens, and the crux becomes clear. The bear case is fundamentally about the xanthine cash cow being commoditized faster than the CDMO switching-cost moat can be built. The bull case is that the switching-cost and trust powers in CDMO compound faster than Chinese rivalry can erode the caffeine economics. Both can be partially true at once; the question is one of timing and degree. Which way the story resolves depends entirely on execution—and that, fittingly, is where we end.

XII. Conclusion & Epilogue

Trace the whole arc and the shape of the thing becomes unmistakable. A family of Mumbai chemists, operating in a closed and scarcity-bound economy in 1984, internalized a single stubborn principle—make your own raw materials, depend on no one—and spent four decades compounding it into genuine industrial mastery. That mastery let them conquer a global commodity that billions of people consume daily without ever wondering where it comes from. The caffeine cash cow, in turn, financed the patient construction of a regulatory fortress in generic APIs, and that fortress became the foundation for the company's most consequential bet: a pivot into the premium, innovator-led world of contract development and manufacturing, arriving at the precise moment that geopolitics is rewriting where the world chooses to make its medicines.

It is, in the end, a coherent and rather elegant blueprint—how a traditional Indian industrial family leveraged its basic chemical-engineering DNA to win in commodity caffeine, built a moat of regulatory trust, and is now executing a highly aligned, strategically positioned move up the value chain.

But blueprints are not buildings, and the epilogue is not yet written. The long-term bet on Aarti Pharmalabs reduces, finally, to a single human question: can Hetal Gogri Gala and Narendra Salvi take the Aarti group's historical scaling playbook—the one that worked so well in benzene chemistry and in caffeine—and successfully run it again in the far more complex, far more demanding, innovator-driven world of global small-molecule pharmaceuticals? The cash cow is real, the moat is real, and the tailwind is real. What remains uncertain, as it always is in business, is execution. The reactors at Atali are built. Now they have to be filled.

References

-

Aarti Pharmalabs Limited Credit Rating Report — ICRA, 2025 ↩

-

Ganesh Polychem Limited Corporate and Financial Profile — ICRA ↩↩↩↩↩

-

Global Caffeine Market Analysis and Major Competitors — Coherent Market Insights ↩↩↩↩↩

-

US BioSecure Act Impact on Indian CDMO and API Manufacturers — Reuters, 2024-05-15 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube