Sika Interplant Systems: India's Hidden Aerospace & Defence Champion

I. Introduction & Episode Roadmap

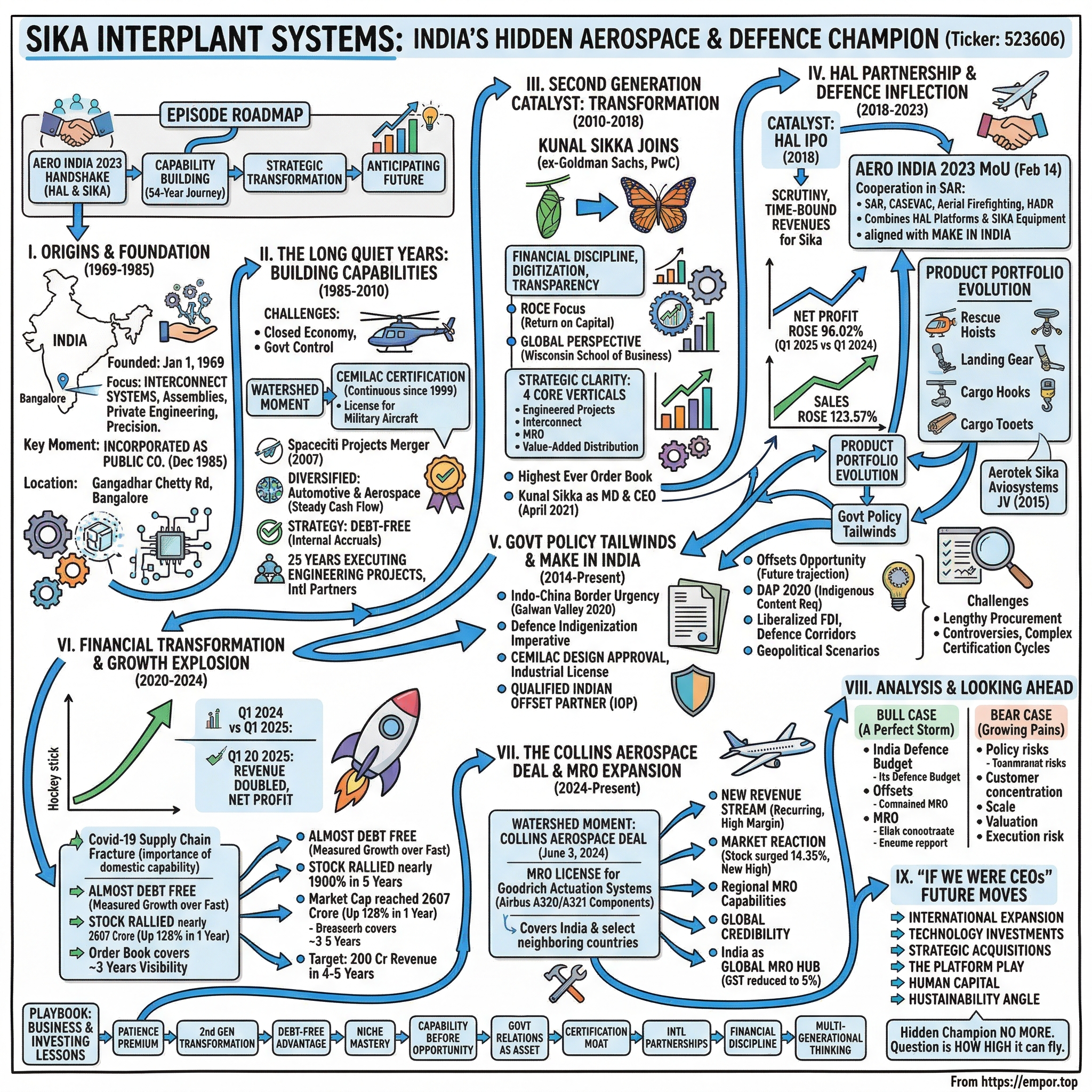

Picture this scene: It's February 2023 at the Aero India exhibition in Bengaluru. Two men shake hands over a document that will reshape India's aerospace maintenance capabilities. Nikhil Dwivedi, General Manager of HAL Helicopter Division, and Kunal Sikka, Managing Director & CEO of SIKA Interplant Systems Limited, sign a memorandum of understanding on February 14th, 2023 during the ongoing Aero India 2023. This wasn't just another corporate handshake—it marked the culmination of a 54-year journey from a modest engineering shop to becoming India's critical aerospace and defence player.

How does a company founded in 1969, decades before India's defence indigenization push gained momentum, position itself perfectly for the current boom? The answer lies in patient capability building, strategic second-generation transformation, and an uncanny ability to anticipate where the puck was going, not where it had been.

Founded in 1969, the Company is headquartered in Bangalore, where it has also established a greenfield technology park, and maintains a sales office in Mumbai. Today, Sika Interplant boasts a market cap of 2,607 Crore with revenue of 185 Cr and profit of 31.6 Cr—numbers that barely hint at the transformation story underneath.

What makes this narrative particularly compelling isn't just the financial turnaround. It's the timing. As India pushes for defence self-reliance under the "Make in India" initiative, as geopolitical tensions with China create urgency for domestic capabilities, and as global aerospace giants seek reliable partners in Asia, Sika Interplant Systems finds itself at the perfect intersection of capability and opportunity.

This is the story of how a company spent five decades preparing for a moment that's just arriving—and why the next decade could transform it from a hidden champion into a global aerospace powerhouse.

II. Origins & Foundation Story (1969–1985)

The year was 1969. Neil Armstrong had just walked on the moon, Boeing's 747 was making its first flight, and in Bangalore—then a quiet pensioner's paradise, not yet India's Silicon Valley—an engineering enterprise was taking shape that would eventually touch the skies in its own way.

Founded on January 1, 1969, Sika began not as a grand aerospace venture but as a private engineering operation focused on what seemed mundane at the time: interconnect systems and assemblies. The founders understood something fundamental about India's industrial landscape—before you can fly, you need to master the basics of precision engineering.

For sixteen years, the company operated as a private enterprise, slowly building its reputation in a market dominated by government-owned behemoths. This wasn't glamorous work. While Hindustan Aeronautics Limited (HAL) was assembling MiG fighters, Sika was perfecting wire harnesses and electrical assemblies. But every complex system needs these unglamorous components, and Sika was learning to make them with a precision that would later prove invaluable.

The pivotal moment came in 1985. Sika Interplant Systems Limited was incorporated as a Public company on 20 December 1985. It is classified as Non-government company and is registered at Registrar of Companies, Bangalore. This wasn't just a legal formality—it represented a strategic decision to formalize operations and prepare for larger ambitions.

The timing of this incorporation was no accident. The mid-1980s marked a subtle shift in India's approach to defence procurement. The Bofors scandal hadn't yet erupted, but there were already whispers about the need for greater transparency and private sector participation in defence. The founders of Sika, operating from NO.3, GANGADHAR CHETTY ROAD, BANGALORE, sensed an opportunity that wouldn't fully materialize for another two decades.

What distinguished Sika in these early years wasn't rapid growth or flashy contracts—it was the deliberate cultivation of engineering DNA. While others chased quick profits in trading or simple manufacturing, Sika invested in understanding the complexities of aerospace-grade components. They weren't building rockets, but they were mastering the art of building the nervous systems that make rockets work.

The company's approach was distinctly contrarian for its time. In an era when Indian private companies typically acted as traders or assemblers of imported components, Sika focused on developing indigenous engineering capabilities. This meant slower growth, lower margins, and long periods of patient investment. But it also meant that when India's defence sector eventually opened up, Sika would be ready—not as a latecomer trying to catch up, but as a veteran with decades of relevant experience.

By the time Sika Interplant Systems Limited completed its incorporation formalities in 1985, it had already established the three pillars that would define its future: technical competence in critical components, a presence in Bangalore's emerging aerospace ecosystem, and most importantly, the patience to play a long game in a sector where success is measured not in quarters but in decades.

The foundation was set. The next phase would test whether a small private company could survive—and eventually thrive—in the shadow of India's defence giants.

III. The Long Quiet Years: Building Capabilities (1985–2010)

If business success were a movie, the period from 1985 to 2010 in Sika's history would end up on the cutting room floor. No dramatic acquisitions, no exponential growth curves, no headlines. Yet these 25 years of apparent quietude would prove to be the company's most important investment—an investment in capabilities that money couldn't buy when the market eventually exploded.

The late 1980s and early 1990s were particularly challenging. India's economy was closed, defence procurement was entirely government-controlled, and private companies were viewed with suspicion in strategic sectors. Sika persisted, slowly building relationships with public sector units, learning their exacting standards, understanding their bureaucratic rhythms. The company became fluent in a language that would later prove invaluable: the complex dialect of Indian defence procurement.

The watershed moment came in 1999, though few recognized its significance at the time. Sika obtained continuous approval from the Indian MoD's Center for Military Airworthiness and Certification (CEMILAC) since 1999. In the aerospace and defence world, CEMILAC certification is not just a quality stamp—it's a license to play in the big leagues. This certification meant that Sika's products could fly on Indian military aircraft, a privilege that separated serious players from aspirants.

Obtaining CEMILAC certification wasn't simply about meeting technical standards. It required building sophisticated quality systems, establishing traceability for every component, and creating a culture where failure wasn't just expensive—it could be fatal. The certification process took years of preparation, significant investment in equipment and training, and most challenging of all, changing the mindset from commercial to aerospace-grade precision.

The early 2000s brought new complexities. Sika's most recent deal was a Merger/Acquisition with Spaceciti Projects for . The deal was made on 01-Jan-2007. While the details of this transaction remain opaque, it represented Sika's first major corporate action, suggesting that the company was beginning to think beyond organic growth.

Throughout this period, Sika maintained a deliberately diversified approach, serving both automotive and aerospace sectors. The automotive work, while less prestigious, provided steady cash flow and allowed the company to refine its manufacturing processes without the extreme regulatory overhead of pure defence work. This dual focus would later prove prescient when aerospace opportunities finally materialized.

The company also made a strategic decision during these quiet years that would define its future: remaining debt-free. While competitors leveraged themselves to chase growth, Sika chose the harder path of self-funded expansion. This wasn't just financial conservatism—it was a recognition that in defence contracting, where payments could be delayed by years and contracts could be cancelled overnight, financial independence was a strategic asset.

SIKA has a successful track-record of nearly twenty-five years in executing advanced engineering projects, in collaboration with international technology partners, for A&D customers in India. These partnerships weren't just about technology transfer; they were about learning global best practices, understanding international quality standards, and most importantly, building trust with foreign OEMs who would later become crucial partners.

By 2010, Sika had quietly assembled an impressive set of capabilities: CEMILAC certification for over a decade, relationships with international partners, a debt-free balance sheet, and deep expertise in aerospace-grade manufacturing. The company had spent 25 years preparing for an opportunity that hadn't yet fully materialized. But the winds were beginning to shift. India's defence procurement policies were evolving, the private sector was gaining acceptance, and a new generation was about to take charge at Sika—one that would transform these carefully built capabilities into explosive growth.

The quiet years were ending. The transformation was about to begin.

IV. The Second Generation Catalyst: Transformation Begins (2010–2018)

Every family business faces a moment of truth when the second generation takes charge. Will they preserve the old ways or chart a new course? For Sika Interplant Systems, this moment arrived with someone who brought an unusual combination: the Sikka family DNA and the Goldman Sachs playbook.

The metamorphosis of SIKA started when the young blood (the present CFO and second generation of founder) joined the company a few years back after completing his stint at Goldman Sachs. He brought in the required financial discipline, built capability and laid foundation for futuristic work. Kunal Sikka, based in Karnataka, India, is currently Chief Executive Officer at SIKA Interplant Systems Ltd, bringing experience from previous roles at Goldman Sachs, Deutsche Bank and PricewaterhouseCoopers.

The transformation wasn't immediate or dramatic—that's not how aerospace companies change. Instead, Kunal Sikka began with the fundamentals: financial discipline. Coming from Goldman Sachs, he understood something his father's generation perhaps couldn't fully appreciate: in the modern aerospace industry, financial engineering was as important as mechanical engineering.

The first changes were subtle but profound. Manual processes were digitized. Financial reporting became more transparent. The company began thinking in terms of return on capital employed, not just revenue growth. Kunal Sikka completed his undergraduate degree at the University of Wisconsin, specifically holding a 2002-2006 Bachelor of Business Administration in Real Estate, Management, Finance from Wisconsin School of Business, bringing a global perspective to what had been a decidedly local operation.

But Kunal's most important contribution wasn't financial sophistication—it was strategic clarity. He recognized that Sika couldn't compete with the HALs and BELs of the world in scale. Instead, it needed to find niches where its agility and private sector efficiency could shine. The strategy that emerged was elegant in its simplicity: focus on four core verticals where Sika could build genuine competitive advantages.

SIKA's main lines of business comprise: engineered projects & systems; interconnect solutions & electrical module integration, maintenance, repair & overhaul (MRO); and value-added distribution. Each vertical was chosen carefully. Engineered projects leveraged decades of design expertise. Interconnect solutions built on the company's original DNA. MRO represented a massive future opportunity as India's military fleet aged. Value-added distribution provided steady cash flow while maintaining customer relationships.

The transformation also brought a cultural shift. The old Sika was content to be a reliable supplier. The new Sika wanted to be an indispensable partner. This meant moving up the value chain—from simply manufacturing to specifications to actually helping design solutions. It meant investing in certifications like AS 9100D, the latest aerospace quality standard. It meant thinking globally while executing locally.

By 2015, the results were becoming visible. The company was winning more complex contracts. Customers were beginning to see Sika not just as a vendor but as a capability partner. The transformation was working, but the real catalyst was still to come.

Kunal Sikka was appointed as Managing Director and CEO of the company, with effective from 1, April 2021, though his influence had been transformative long before the formal title. The appointment represented not just a generational transition but a strategic inflection point. The company that had spent decades building capabilities now had leadership that knew how to monetize them.

As a result of which today SIKA is sitting on its highest ever order book and is probably one of the very few growing debt free private defense companies. The patient capital approach of the earlier generation combined with the financial sophistication of the new created a powerful combination.

The period from 2010 to 2018 wasn't just about internal transformation. The external environment was changing too. The Modi government's "Make in India" initiative was gathering steam. The standoffs with China were creating urgency around defence indigenization. Global OEMs were being mandated to meet offset obligations. Every trend pointed in Sika's direction, and thanks to the second-generation transformation, the company was ready to capitalize.

The stage was set for the next act: the HAL partnership and the defence inflection point that would transform Sika from a capable supplier into a strategic partner in India's aerospace ambitions.

V. The HAL Partnership & Defence Inflection Point (2018–2023)

Sometimes a single event can illuminate years of patient preparation. For Sika Interplant Systems, that moment came with an IPO—but not their own. It was Hindustan Aeronautics Limited's public listing in 2018 that unexpectedly became the catalyst for Sika's transformation.

For Sika's defense business, a notable structural change happened last year, when one their largest customer – HAL came out with its IPO. Their projects are now getting scrutiny of investors (like BEL and BEML) and their time bound completion is now in focus, which in-turn would ensure sustained and time bound revenues for Sika.

The HAL IPO was more than a financial event—it was a fundamental shift in how India's premier aerospace company operated. Suddenly, HAL faced quarterly earnings calls, analyst scrutiny, and pressure to deliver projects on time. The days of indefinite delays and cost overruns were ending. For suppliers like Sika who could deliver on schedule, this represented an unprecedented opportunity.

But Sika wasn't content to remain just another supplier. The company's product portfolio had evolved dramatically. The company has presence in businesses like search and rescue (Rescue hoists/ winches; air ambulance/ EMS modules), Landing gear & hydraulics, interconnection systems (harness & looms, electro mechanical assemblies, etc.), handling systems (cargo hooks, cargo and marine winches, sonar winch, etc.). These weren't commodity products—they were sophisticated systems critical to aircraft operation and mission success.

The relationship with HAL reached a new level on February 14, 2023, during the Aero India exhibition. SIKA Aerospace, a division of SIKA Interplant Systems Limited entered into a memorandum of understanding (MoU) with Hindustan Aeronautics Limited (HAL) to pursue strategic business cooperation in the Airborne Search & Rescue (SAR), Casualty/Medical Evacuation (CASEVAC/MEDEVAC), Aerial Firefighting and Humanitarian Assistance & Disaster Relief (HADR) domains.

The MoU intends to leverage the existing business relationship between HAL and SIKA, utilising each company's respective strengths, to generate mutually beneficial business outcomes while providing state-of-the-art solutions to customers. Further, the MoU envisages combining HAL's experience in manufacture, integration, and upgrades of platforms together with SIKA's expertise in supply and integration of SAR, CASEVAC, MEDEVAC and HADR equipment, and is consistent with the goals of the Government of India's "Make in India" initiative.

This wasn't just a supply agreement—it was a strategic partnership. HAL brought platform expertise and government relationships. Sika brought specialized systems knowledge and private sector agility. Together, they could address opportunities neither could tackle alone.

The financial impact was dramatic and immediate. Net profit of Sika Interplant Systems rose 96.02% to Rs 10.35 crore in the quarter ended June 2025 as against Rs 5.28 crore during the previous quarter ended June 2024. Sales rose 123.57% to Rs 68.01 crore in the quarter ended June 2025 as against Rs 30.42 crore during the previous quarter ended June 2024.

But the numbers only tell part of the story. What was really happening was a fundamental shift in Sika's position in the value chain. The company was moving from being a component supplier to becoming a systems integrator. This meant higher margins, stronger customer relationships, and most importantly, greater strategic importance.

The period also saw Sika building partnerships beyond HAL. In partnership with Aerotek Aviation Engineering Ltd (AAE) of the UK, Aerotek Sika Aviosystems Private Limited was incorporated on 26th June 2015 in partnership with Aerotek Aviation Engineering Limited, UK, with equity holding in the ratio of 51:49 between your Company (including subsidiaries) and Aerotek UK (including its promoters), to undertake the manufacture and maintenance, repair and overhaul of aeronautical products and systems.

The order book told the story of transformation. Sika Interplant is now sitting on its highest ever order book which roughly gives us three years visibility and the good part is nothing of it is from offset. In the coming years once they start getting offset contracts, the revenues could go to altogether another trajectory. The fact that this growth came without offset obligations was particularly significant—it meant Sika was winning on merit, not mandates.

The HAL partnership also opened doors to other opportunities. When HAL's Dhruv helicopters needed search and rescue equipment, Sika was there. When the Indian Coast Guard required specialized maritime systems, Sika had the capability. When the Indian Army needed air ambulance modules, Sika could deliver. Each success built credibility for the next opportunity.

By 2023, the transformation was complete. Sika was no longer just a component supplier hoping for contracts. It was a strategic partner to India's aerospace champions, with unique capabilities in critical systems. The HAL IPO had indeed created a structural change in the industry—and Sika had positioned itself perfectly to benefit.

VI. Government Policy Tailwinds & Make in India (2014–Present)

Every industry has moments when government policy aligns perfectly with corporate capability. For Sika Interplant Systems, that alignment began in 2014 with the Modi government's "Make in India" initiative and has only intensified since.

The stand-offs seen in recent years on the Indo-China border have renewed the urgency to build capability and capacity for India's defense industry. The Galwan Valley clash of 2020 wasn't just a military confrontation—it was a wake-up call about India's continued dependence on imported defence equipment. Suddenly, indigenization wasn't just economic policy; it was national security imperative.

The government has given priority to this sector and is pivotal to their 'Make in India' plans which has acted as a tailwind. But Sika had an advantage that many companies rushing into defence didn't: it had already been there for decades. The Company is one of the select private enterprises with design approval from the Center for Military Airworthiness and Certification (CEMILAC). Sika has also been granted an Industrial License for Defence production from the Government of India, and also a qualified Indian Offset Partner with a license for Defence production from the Government of India.

The Indian Offset Partner (IOP) qualification was particularly strategic. When India buys fighter jets from Dassault or helicopters from Boeing, these companies must invest 30-50% of the contract value back in India. A number of international OEMs have significant offset obligations outstanding, and so it is expected that the opportunity from offsets in the coming years will be significant, with avenues likely to be available both in manufacturing and services. For these global giants, partners like Sika—with proven capabilities and certifications—were invaluable.

Yet remarkably, Sika's current growth wasn't dependent on offset contracts. The company had built its order book through competitive wins, not mandated partnerships. This organic growth validated the company's capabilities in ways that offset-driven revenues never could.

The policy environment created multiple growth vectors. The Defence Acquisition Procedure (DAP) 2020 introduced an Indigenous Content (IC) requirement, mandating that Indian defence equipment contain increasing percentages of local content. For system integrators like HAL, partners like Sika became essential to meeting these requirements.

The government's push extended beyond just procurement policies. The liberalization of FDI in defence, the creation of defence corridors, and the simplification of licensing procedures all created an ecosystem where private players could thrive. Sika, with its decades of experience navigating defence bureaucracy, was perfectly positioned to capitalize.

The geopolitical environment added another layer of urgency. India's geopolitical scenario and compulsions, real or perceived, are continuing to drive the development of its A&D industry. The stand-offs seen in recent years on the Indo-China border have renewed the urgency to build capability and capacity for India's defense industry. The geopolitical situation in South Asia and the Indian Ocean region, as well as the wider theater of Southeast Asia and South China Sea, has important implications for defence preparedness.

This wasn't just about land borders. India's growing maritime interests, the need to project power in the Indian Ocean, and the requirement to support humanitarian missions across the region all created demand for the specialized systems Sika produced—search and rescue equipment, medical evacuation modules, maritime handling systems.

The policy tailwinds also brought challenges. Most of the threats to the domestic A&D industry are rooted on the policy front, such as lengthy procurement and evaluation processes, controversies related to corruption, and disputes over shortlisting in competitive bids. These will serve to delay acquisition plans of the armed forces and impact the timing of execution of already long-dated projects. In A&D business, the products and systems involved are typically of complex advanced technologies, often resulting in the approval and certification cycle extending for materially longer than originally planned. This can result in delays in production orders and consequent deliveries, affecting the timing of revenues.

But for patient players like Sika, these challenges were also barriers to entry. Not every company could afford to wait years for certifications or navigate the complex world of defence procurement. Those that could—and had—found themselves in an increasingly exclusive club.

By 2024, the policy environment had fundamentally transformed India's aerospace and defence sector. What had been a government monopoly was becoming a vibrant ecosystem with private players taking increasingly important roles. Sika hadn't just benefited from these changes—it had positioned itself over decades to capitalize when the moment arrived. The company that had patiently built capabilities during the quiet years was now perfectly aligned with national priorities.

VII. Financial Transformation & Recent Growth Explosion (2020–2024)

Numbers tell stories, but in Sika's case, they practically shout. The financial transformation from 2020 to 2024 reads like a hockey stick graph that every startup dreams of—except this "startup" had been preparing for 50 years.

The COVID-19 pandemic, which devastated many industries, became an unexpected catalyst for defence companies. Following the Covid-19 pandemic induced downgrade in the growth of the global A&D industry in 2020-21, the sector is steadily—if tentatively improving—following a bottoming out in early 2021 and a moderate improvement in the second half of 2021-22. As global supply chains fractured, the importance of domestic defence capabilities became undeniable.

The numbers from recent quarters tell a story of explosive growth. The revenue for Sika Interplant Systems Ltd in the Q1 results 2024 was ₹31.57Cr. The net profit for Sika Interplant Systems Ltd in the Q1 results 2024 was ₹5.28Cr. Fast forward just one year, and The revenue for Sika Interplant Systems Ltd in the Q1 results 2025 was ₹69.74Cr. The net profit for Sika Interplant Systems Ltd in the Q1 results 2025 was ₹10.35Cr. That's more than a doubling of revenue and profit in just twelve months.

But here's what makes these numbers truly remarkable: Company is almost debt free. In an industry where companies routinely leverage themselves to win large contracts, Sika achieved explosive growth while maintaining financial discipline. The company plans to remain debt free and grow on internal accruals. It wants measured growth rather than fast unprofitable growth.

The stock market noticed. Shares of Sika Interplant Systems have rallied nearly 1,900 per cent in the last five years from Rs 26.21 levels. For long-term investors who had the patience to stick with this seemingly sleepy engineering company, the rewards were extraordinary. The company that had spent decades under the radar was suddenly on everyone's watchlist.

The order book provided visibility into future growth. In FY24, Sika Interplant has secured significant new orders for advanced engineering products and services in the recent past. With these recent contracts, the cumulative of new orders received by Sika since the start of FY 2023-24 is Rs 117 crore (approx.) as on August 11, 2023. This order book, representing nearly three years of revenue visibility, provided the kind of certainty that's rare in the volatile defence sector.

The company's ambitions were clearly stated. The company plans to take revenues to INR 200 crore in the next 4-5 years. Given the current revenue run rate and order book, this seemed conservative rather than ambitious. The Q3 FY24 results showed continued momentum, with Sika Interplant Systems reporting a 51.06 per cent rise on a year-on-year (YoY) basis to Rs 7.14 crore in the December 2024 period, driven by higher demand and improved operational performance. Its revenue increased 46.11 per cent YoY to Rs 37.98 crore for the quarter under review.

The financial metrics showed a company firing on all cylinders. Debtor days have increased from 64.7 to 80.3 days, suggesting strong bargaining power with customers—in the defence sector, getting paid quickly is often a sign of how essential you are. The company was growing rapidly while maintaining operational efficiency.

What's particularly impressive is the profitability of this growth. Sika Interplant Systems Ltd's net profit margin fell -11.26% since last year same period to 14.84% in the Q1 2025-2026. While the margin compression might concern some investors, it reflected the company's strategic shift toward larger, more complex projects that would ultimately provide better absolute returns.

The market capitalization told the story of transformation. Sika Interplant's market cap reached 2,607 Crore (up 128% in 1 year). The company had graduated from micro-cap to small-cap status, attracting institutional attention for the first time in its history. The top shareholders of Sika Interplant are Ultraweld Engineers LLP with 70.1%, followed by Rimo Capital Fund LP at 2.8%, showing that while the promoter family maintained control, sophisticated investors were beginning to take notice.

The financial transformation wasn't just about growth—it was about quality of growth. Revenue was diversifying across product lines, customer concentration was decreasing, and the company was moving up the value chain. This wasn't a company riding a single wave; it was building sustainable competitive advantages that would compound over time.

VIII. The Collins Aerospace Deal & MRO Expansion (2024–Present)

June 3, 2024, marked a watershed moment in Sika's evolution. The company's stock price surged, but more importantly, it signaled Sika's entry into the exclusive club of global aerospace MRO providers.

SIKA Interplant Systems (SIKA) has entered into a License Agreement with Goodrich Actuation Systems SAS (France) and Goodrich Actuation Systems Limited (UK), each a part of Collins Aerospace (Collins). Under this agreement, SIKA will be licensed to undertake maintenance, repair and overhaul (MRO) of specific primary flight control actuation part numbers (the Components) for which Collins is the original equipment manufacturer (OEM). These Components are standard installations on all Airbus A320/A321 series aircraft.

The significance of this agreement cannot be overstated. Collins Aerospace, a unit of Raytheon Technologies, doesn't hand out MRO licenses casually. These are critical flight control components—the systems that keep aircraft safely in the air. For Collins to trust Sika with maintaining these components spoke volumes about how far the company had come from its origins as a simple component manufacturer.

As per the License Agreement, SIKA is authorised to service Components from aircraft registered in India and select neighbouring countries as defined in the agreement. This geographical scope was strategic. India's aviation market was exploding, with airlines adding hundreds of A320 family aircraft. The "select neighbouring countries" clause potentially opened markets like Bangladesh, Sri Lanka, and Nepal—countries whose airlines often looked to India for MRO services.

The market reaction was immediate and dramatic. Sika Interplant Systems surged 14.35% after the company announced that it has entered into a license agreement, with some reports showing the stock hitting a new 52-week high of ₹956.90 before settling around ₹945, lifting the company's market capitalization to ₹2,003 crore.

The deal allows SIKA to carry out maintenance, repair, and overhaul (MRO) services for key flight control components used in Airbus A320/A321 aircraft. The license applies to aircraft registered in India and select neighboring countries, reinforcing SIKA's focus on expanding its regional MRO capabilities. This wasn't just about servicing aircraft—it was about becoming an integral part of the aviation ecosystem.

The MRO market represented a fundamentally different business model from Sika's traditional manufacturing. MRO provided recurring revenue, higher margins, and deeper customer relationships. An airline that trusts you to maintain its flight controls becomes a partner, not just a customer. The switching costs are high, the relationships are sticky, and the revenue streams are predictable.

"This collaboration aligns with SIKAs strategic objective of expanding its MRO capabilities to better serve aviation and aerospace customers in India and the region," the company said in a statement. The language was corporate, but the implications were transformational. Sika was no longer just an Indian defence supplier—it was becoming a regional aerospace services provider.

The Collins partnership also provided something invaluable: global credibility. When other OEMs saw that Collins trusted Sika with critical flight control maintenance, doors would open. Boeing might consider them for 737 components. Airbus might explore direct partnerships. The Collins deal was both a destination and a launching pad.

This move is more than just a commercial agreement—it represents a significant step toward localizing critical aerospace capabilities. Moreover, the MRO space is becoming increasingly attractive in India due to policy support, cost efficiencies, and geographic advantages. Sika's entry into this space with a high-value licensing deal provides it with an early-mover advantage that could pay off significantly in the coming years.

The timing was perfect. India was positioning itself as a global MRO hub, leveraging its large aviation market, skilled workforce, and cost advantages. The government had reduced GST on MRO services from 18% to 5%, making India competitive with Dubai and Singapore. For Sika, with its new Collins license and existing capabilities, the opportunity was enormous.

The deal also validated Sika's strategic evolution. The company had spent years moving from component supplier to systems integrator. Now it was adding services to its portfolio—the highest margin, most defensible part of the aerospace value chain. This wasn't just growth; it was intelligent growth that built on existing capabilities while opening entirely new revenue streams.

IX. Playbook: Business & Investing Lessons

After chronicling Sika's 55-year journey, certain patterns emerge that transcend this specific company. These aren't just lessons about aerospace or Indian business—they're insights about how patient capital, strategic positioning, and multi-generational thinking can create extraordinary value.

The Patience Premium

Sika's story demolishes the myth of overnight success. The company's shares rallied nearly 1,900 per cent in five years, but those five years were preceded by fifty years of capability building. The lesson? In industries with high barriers to entry—whether regulatory, technical, or capital—time can be your greatest competitive advantage. While others chase quick returns, patient players accumulate capabilities that become increasingly valuable as markets mature.

Second-Generation Transformation Blueprint

The infusion of fresh perspective through Kunal Sikka, who brought experience from Goldman Sachs, Deutsche Bank and PricewaterhouseCoopers, offers a masterclass in family business evolution. The key wasn't replacing the old with the new, but combining foundational strengths with modern capabilities. The engineering DNA from the first generation merged with financial sophistication from the second created something neither could achieve alone.

The Debt-Free Advantage

In an era of cheap money and financial engineering, Sika's commitment to remain debt free and grow on internal accruals seemed almost quaint. Yet this conservatism became a strategic weapon. In defence contracting, where payments can be delayed and contracts canceled, financial independence meant Sika could take calculated risks others couldn't afford. The company could walk away from bad deals, invest in long-term capabilities, and weather downturns without existential risk.

Niche Mastery Over Diversification

While conglomerates chased growth through diversification, Sika doubled down on aerospace and defence. But within this focus, they built four complementary verticals that reinforced each other. The lesson: horizontal diversification often dilutes competitive advantage, while vertical integration within a domain can create compounding moats.

Capability Before Opportunity

Perhaps the most counterintuitive lesson: Sika built capabilities before clear opportunities existed. The CEMILAC certification in 1999 came years before private sector participation in defence became viable. The international partnerships preceded the offset opportunities. The MRO capabilities were developed before the Collins deal materialized. This "build it and they will come" approach only works with patient capital and deep conviction—but when it works, the returns are extraordinary.

Government Relations as Strategic Asset

Unlike tech companies that can scale globally from day one, defence companies must master local regulations and relationships. Sika spent decades learning the language of Indian defence procurement, understanding government priorities, and building trust with public sector units. This knowledge became a moat that money couldn't buy when markets opened up.

The Certification Moat

In regulated industries, certifications aren't just compliance requirements—they're competitive moats. Sika's continuous CEMILAC approval since 1999 meant that when opportunities arose, they were already qualified while competitors were just starting the multi-year approval process. Each additional certification—AS 9100D, Industrial License, Indian Offset Partner qualification—added another layer to this moat.

International Partnerships as Capability Accelerators

Rather than trying to develop all capabilities internally, Sika strategically partnered with international players. The Aerotek JV for landing gear, the Collins license for MRO—each partnership brought capabilities that would have taken years to develop independently. The key was maintaining majority control while leveraging foreign expertise.

Financial Discipline in Growth

Even during explosive growth, Sika wanted measured growth rather than fast unprofitable growth. This discipline meant saying no to opportunities that didn't meet return thresholds, maintaining focus on core competencies, and avoiding the trap of growth for growth's sake.

Multi-Generational Thinking

Perhaps the most important lesson: Sika thought in decades, not quarters. The founders accepted slow growth to build capabilities. The second generation leveraged these capabilities for explosive growth. This multi-generational perspective is rare in public markets but essential in industries where success is measured over long time horizons.

X. Analysis & Bear vs. Bull Case

Every investment thesis has two sides, and Sika Interplant Systems is no exception. After examining the company's journey and current position, let's weigh the arguments that bulls and bears might make.

The Bull Case: A Perfect Storm of Tailwinds

Bulls see Sika as a coiled spring, with decades of patient capability building ready to deliver explosive growth. The numbers support their optimism—revenue more than doubled year-over-year in recent quarters, the order book provides three years of visibility, and the company remains debt-free despite rapid expansion.

The macro environment couldn't be more favorable. India's defence budget continues to grow, with increasing allocation for domestic procurement. The China threat ensures defence spending remains a priority regardless of political changes. India's geopolitical scenario and compulsions are continuing to drive the development of its A&D industry. The stand-offs on the Indo-China border have renewed the urgency to build capability and capacity.

The offset opportunity remains largely untapped. Sika's order book contains nothing from offset, yet international OEMs have significant offset obligations outstanding. As these obligations come due, Sika's certifications and track record position it as an obvious partner. This represents potentially billions in additional revenue over the coming decade.

The MRO expansion opens an entirely new market. With the Collins Aerospace license, Sika enters a high-margin, recurring revenue business with massive growth potential. India's aviation market is expected to become the world's third-largest by 2030, creating enormous MRO demand that Sika is now positioned to capture.

Bulls also point to valuation. Despite the recent run-up, Sika trades at reasonable multiples compared to global aerospace peers. If the company achieves its revenue target of 200 crore in 4-5 years while maintaining margins, the current valuation could prove cheap in hindsight.

The Bear Case: Growing Pains and Structural Challenges

Bears acknowledge Sika's progress but worry about several structural challenges that could limit future growth.

Most threats to the domestic A&D industry are rooted on the policy front, such as lengthy procurement and evaluation processes, controversies related to corruption, and disputes over shortlisting in competitive bids. These delays impact the timing of execution of already long-dated projects. A single cancelled contract or delayed payment could significantly impact Sika's financials given its size.

Customer concentration remains a concern. Despite diversification efforts, HAL remains a critical customer. Any deterioration in this relationship or delays in HAL's own projects could cascade to Sika. The company's dependence on government-controlled entities makes it vulnerable to policy changes and bureaucratic delays.

Scale remains a challenge. At 185 crore in revenue, Sika is tiny compared to global aerospace suppliers. This limits its bargaining power with both customers and suppliers. As opportunities grow larger, Sika might struggle to compete with international giants who can offer complete solutions and global support.

The stock's valuation reflects perfection. After rising 1,900% in five years, much of the good news appears priced in. Any execution stumbles, contract delays, or margin compression could trigger significant corrections. The high promoter holding of 71.7% also limits float, potentially exacerbating volatility.

Bears also worry about execution risk. Scaling from 185 crore to the targeted 200 crore requires not just winning contracts but delivering on them. The aerospace industry is unforgiving—a single quality issue could destroy decades of reputation. As Sika takes on more complex projects, execution risk multiplies.

The Balanced View

The truth, as always, likely lies between these extremes. Sika has clearly positioned itself well for India's aerospace opportunity. The capabilities built over decades are real, the certifications are valuable, and the partnerships are strategic. The company has demonstrated an ability to win contracts and deliver growth.

However, the journey from small-cap to mid-cap won't be linear. There will be quarters of disappointment, contracts that don't materialize, and execution challenges. The key question for investors: Is the long-term opportunity large enough to justify riding through this volatility?

The answer depends on one's view of India's aerospace future. If India successfully builds a domestic aerospace industry comparable to its IT or pharmaceutical sectors, early champions like Sika could generate multi-bagger returns from here. If progress remains slow and government-dependent, returns might be more modest.

What's clear is that Sika has earned its place at the table. Whether it becomes a feast or merely a meal remains to be seen.

XI. Epilogue & "If We Were CEOs"

Standing at this inflection point in Sika's journey, it's tempting to imagine what the next decade might bring. If we were sitting in Kunal Sikka's chair, looking out from that Bangalore headquarters at an aerospace industry on the cusp of transformation, what moves would we make?

International Expansion: Beyond South Asia

The Collins Aerospace deal authorizes Sika to service aircraft in "select neighbouring countries," but why stop there? Southeast Asia represents a massive aviation growth market. Countries like Vietnam, Indonesia, and the Philippines are adding aircraft rapidly but lack developed MRO ecosystems. Sika could establish partnerships or facilities in these markets, leveraging its Collins certification and Indian cost advantages.

The Middle East presents another opportunity. While Dubai and Abu Dhabi have established MRO hubs, there's room for specialized players. Sika's expertise in military systems and search-and-rescue equipment could find ready markets among Gulf nations modernizing their forces.

Technology Investments: The Digital Layer

Aerospace is becoming increasingly digital. Predictive maintenance, digital twins, and IoT-enabled components are transforming how aircraft are maintained and operated. Sika needs to add a digital layer to its mechanical expertise. This might mean acquiring a software company, partnering with tech firms, or building internal capabilities. The company that combines physical expertise with digital intelligence will win the next decade.

Strategic Acquisitions: Building Scale

At 185 crore revenue, Sika lacks the scale to compete for mega-contracts. Strategic acquisitions could accelerate growth while adding complementary capabilities. Targets might include distressed aerospace suppliers with valuable certifications, complementary product lines, or customer relationships. The debt-free balance sheet provides firepower for such moves.

Consider acquiring a composites manufacturer as aircraft increasingly shift from metal to composite materials. Or a sensors company as aircraft become more automated. Each acquisition should add not just revenue but strategic capability that reinforces Sika's competitive position.

The Platform Play

Rather than remaining just a supplier, Sika could evolve into a platform that connects India's fragmented aerospace supply chain. Many small manufacturers have capabilities but lack certifications, quality systems, or customer access. Sika could become their gateway to aerospace markets, providing quality oversight, certification support, and customer relationships while taking a margin for platform services.

Human Capital: The Talent Imperative

The constraint on Sika's growth might not be capital or contracts but talent. Aerospace engineering requires specialized skills that remain scarce in India. Sika should consider establishing partnerships with engineering colleges, creating apprenticeship programs, or even establishing its own training academy. The company that solves the talent constraint will have a significant competitive advantage.

The Sustainability Angle

Environmental concerns are reshaping aerospace. Electric aircraft, sustainable aviation fuels, and carbon-neutral operations are moving from nice-to-have to must-have. Sika should position itself at the forefront of this transition. This might mean developing electric systems for aircraft, creating lighter components that improve fuel efficiency, or establishing carbon-neutral manufacturing processes.

Building for the Next 50 Years

The most important strategic decision might be maintaining the long-term perspective that brought Sika this far. In a market obsessed with quarterly results, the temptation to chase short-term growth could be overwhelming. But Sika's success came from patient capability building, strategic positioning, and waiting for the right opportunities.

The next decade will bring opportunities the founders couldn't have imagined. Urban air mobility, space commercialization, hypersonic travel, autonomous aircraft—each represents a potential market measured in billions. The company that builds capabilities today for markets that don't yet exist will capture extraordinary value when those markets materialize.

Sika Interplant Systems spent 55 years becoming an overnight success. The next chapter of this story is being written now, in the contracts being signed, capabilities being built, and partnerships being forged. Whether Sika becomes India's aerospace champion or remains a profitable niche player depends on decisions being made today in that Bangalore headquarters.

The foundation is solid. The opportunity is massive. The capabilities are proven. What happens next will determine whether Sika's story becomes a case study in building an aerospace champion or merely another example of unrealized potential. Given the company's track record of patient excellence and strategic timing, betting against them would be unwise.

The hidden champion is hidden no more. The question now is how high it can fly.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube