Spotify: The Sound of Disruption

I. Introduction & Episode Roadmap

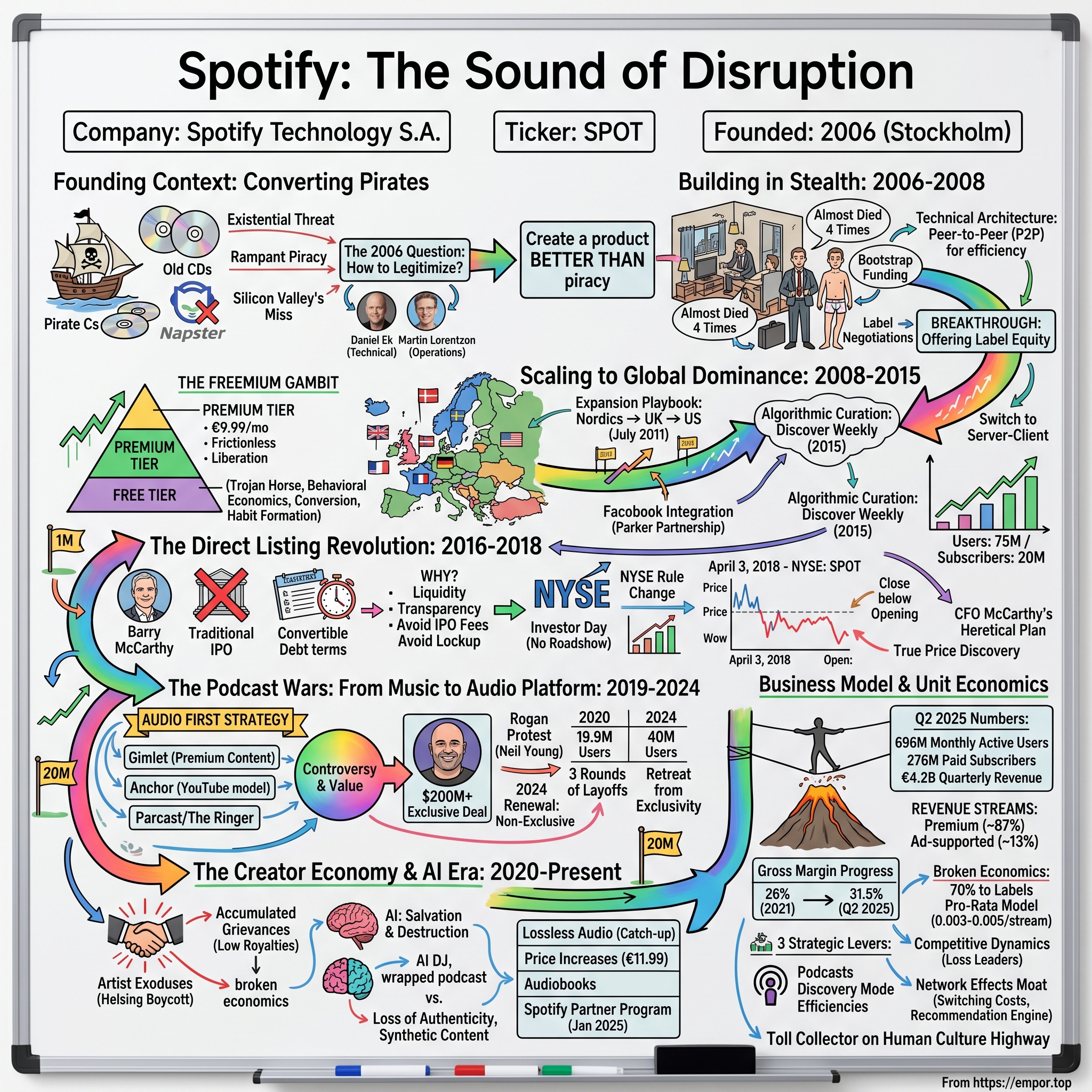

Picture this: It's 2006 in Stockholm, and two Swedish entrepreneurs are sitting in a cramped apartment, wrestling with a question that Silicon Valley had already answered with lawsuits and cease-and-desist letters. How do you convince an industry that just spent five years fighting Napster in court to hand over their entire catalog to yet another tech startup? The music industry had been burned—badly. CD sales were cratering, digital piracy was rampant, and labels viewed technology companies as existential threats, not partners.

Yet somehow, Daniel Ek and Martin Lorentzon pulled off what seemed impossible. Today, Spotify commands 696 million monthly active users and 276 million paid subscribers, making it the world's largest audio streaming platform. The company that started as a pirate's dream of legitimate music has transformed into a $90 billion audio empire that fundamentally rewired how humanity consumes sound. The company that started as a pirate's dream of legitimate music has transformed into a $145 billion audio empire that fundamentally rewired how humanity consumes sound.

But here's what makes the Spotify story particularly fascinating for students of business strategy: This is fundamentally a story about converting pirates into paying customers—a behavioral economics masterclass executed at planetary scale. It's about two Swedes who understood something Silicon Valley missed: that the solution to piracy wasn't better DRM or more lawsuits, but creating a product so seamless, so frictionless, that paying for music became easier than stealing it.

The European tech success story angle matters too. While American tech giants were building social networks and search engines, Spotify emerged from Stockholm's tech scene to dominate a category that should have belonged to Apple or Google. The company's journey illuminates how geography, timing, and regulatory environments can create unexpected competitive advantages.

This is also a platform economics case study in real-time. Spotify operates a three-sided marketplace connecting listeners, artists, and advertisers—each with conflicting interests that the company must perpetually balance. Every strategic decision ripples through this ecosystem, from playlist algorithms to podcast exclusivity deals to artist compensation models.

What you'll learn from Spotify's story extends far beyond streaming. It's a playbook for building in heavily regulated industries, for turning existential threats into growth opportunities, and for maintaining independence while surrounded by tech giants with infinite resources. Most importantly, it's about understanding when to pivot—from peer-to-peer to client-server, from music to audio, from licensing to owning content, and knowing when to reverse course entirely.

The numbers tell part of the story, but the real lessons lie in the decisions behind them. How do you negotiate with an industry that views you as the enemy? When do you choose growth over profitability? How do you build a moat when your product is essentially a commodity? These questions drive our exploration of Spotify's remarkable ascent.

As we trace this journey from a Stockholm apartment to the New York Stock Exchange, we'll uncover the strategic pivots, near-death experiences, and counterintuitive decisions that transformed a simple idea—"what if paying for music was easier than pirating it?"—into one of the defining companies of the streaming era.

II. The Pirates Who Saved Music: Founding Context

The fluorescent lights of Rågsved's computer lab flickered as thirteen-year-old Daniel Ek hunched over a keyboard in 1996. This wasn't Silicon Valley or even central Stockholm—Rågsved was a working-class suburb where immigrant families like Ek's (his mother fled Yugoslavia) carved out modest lives. While his classmates played football, Ek was discovering he could turn HTML into cash. His first website fetched 5,000 Swedish kronor—about $600. "I thought it was a mistake," he later recalled. Within months, he was charging $100-200 per site, earning more than his teachers by age fourteen.

By sixteen, Ek was running a web development business with twenty-five employees, operating out of his high school. He'd arrive at school in a suit, conduct meetings during lunch breaks, and somehow maintained straight A's while managing developers twice his age. The teenage CEO was making serious money—enough to buy a red Ferrari he was too young to legally drive. But the glossy success masked deeper questions. "I had all this money, but I was miserable," Ek would later reflect. The Ferrari collected dust. The business felt hollow. After selling a web consultancy to Tradera (later acquired by eBay), Ek founded Advertigo, an online advertising company. In 2006, TradeDoubler acquired Advertigo, netting the 23-year-old Ek approximately $1.25 million. Fresh off this exit, Ek did something unexpected: he briefly became CEO of μTorrent, working with founder Ludvig Strigeus until the company was sold to BitTorrent in December 2006. This μTorrent stint would prove pivotal—not just because Strigeus would later become Spotify's lead developer, but because it gave Ek an insider's view of how piracy actually worked.

The epiphany came in 2002, watching the Napster shutdown unfold. "I realized that you can never legislate away from piracy. The only way to solve the problem was to create a service that was better than piracy and at the same time compensates the music industry", Ek would later explain. This wasn't naive optimism—it was cold calculation from someone who'd just run a BitTorrent client and understood the user experience intimately.

Enter Martin Lorentzon, a different breed of Swedish entrepreneur. Where Ek was the technical prodigy, Lorentzon was the seasoned operator who'd already built and sold TradeDoubler for serious money. In 2005, Lorentzon sold his TradeDoubler options for $70 million, making him one of Sweden's most successful tech entrepreneurs. When TradeDoubler bought Advertigo in March 2006, Lorentzon left the board and gave one million euros to Ek. The two men discovered an instant chemistry—they claim there hasn't been a day since 2006 when they didn't speak at least once.

On April 23, 2006, they incorporated Spotify AB in Stockholm, though the company was officially registered in June 2006. The name itself was supposedly a mishearing of "spot" and "identify," though that origin story feels almost too perfect. What mattered more was their complementary skill sets: Ek brought technical vision and product intuition; Lorentzon brought operational excellence and the credibility that comes from having built a publicly traded company.

The Swedish ecosystem provided unexpected advantages. Stockholm in 2006 wasn't Silicon Valley, but that was precisely the point. Sweden had already given the world Skype, demonstrating that world-class consumer technology could emerge from Scandinavia. The country's progressive IP laws, strong social safety net, and culture of consensus-building created an environment where a radical reimagining of music distribution could take root. Plus, Sweden had another crucial asset: The Pirate Bay. The country was simultaneously ground zero for music piracy and home to some of the world's best engineers—many of whom had cut their teeth building file-sharing systems.

Lorentzon's financial cushion proved critical. He spent his own money on developers' salaries, offices, and renting music licenses, allowing Spotify to operate in stealth mode without venture capital pressure. They tried to attract investor money, but Lorentzon wasn't satisfied with the terms offered. Because of these unplanned expenses, Lorentzon's share in Spotify turned out to be the largest.

The founding context reveals something profound about Spotify's DNA. This wasn't a company built by music industry insiders trying to save their business model, nor was it created by Silicon Valley disruptors looking to "move fast and break things." Instead, it emerged from two Swedish entrepreneurs who understood both sides of the equation—the technical elegance of peer-to-peer systems and the business realities of building sustainable companies. They weren't trying to destroy the music industry or perpetuate piracy. They were trying to build a bridge between two worlds that had declared war on each other. The pirates who would save music had found their mission.

III. Building in Stealth: The Pre-Launch Years (2006–2008)

The apartment above a Stockholm coffee shop looked more like a college dorm than a tech startup. Pizza boxes stacked in corners, engineers sleeping under desks, and the perpetual smell of Red Bull permeating everything. This cramped three-bedroom flat became Spotify's first headquarters in 2006, where a handful of developers worked in secrecy while Daniel Ek jetted around the world on what seemed like a fool's errand: convincing record labels to trust yet another tech company with their entire catalog.

The company only had a handful of engineers working in a three-bedroom apartment above a coffee shop when the platform was founded, while Ek traveled the globe trying to secure licenses from record labels. The contrast was stark—while Ek wore suits in boardrooms facing hostile executives, his team coded in their underwear during Stockholm's sweltering summer, building what would become the fastest music streaming service on the planet.

The technical architecture decision came first, and it was controversial. Spotify's initial approach leveraged peer-to-peer technology—the same underlying system that powered BitTorrent and, by extension, music piracy. The irony wasn't lost on anyone. Here was a company trying to legitimize music consumption, using the very technology that had terrorized the industry. But Ek and his team, including μTorrent founder Ludvig Strigeus who joined as a Spotify developer, understood something crucial: P2P wasn't inherently evil—it was just incredibly efficient.

The peer-to-peer model meant that users' computers would share songs with each other, reducing Spotify's server costs and, more importantly, creating near-instantaneous playback. Click a song, and it started playing in under 200 milliseconds—faster than iTunes could load a file already on your hard drive. This speed wasn't a nice-to-have feature; it was existential. If legal music was even slightly more cumbersome than piracy, the entire project would fail. Meanwhile, the real battle was happening in conference rooms around the world. The company only had a handful of engineers working in a three-bedroom apartment above a coffee shop when the platform was founded, while Ek traveled the globe trying to secure licenses from record labels. Ek told Bartlett that Spotify "almost died four times" during the 18-month period he was trying to secure licenses—because it almost ran out of money. He added that for a two-year period, he thought "once every month or two" that Spotify was going to fail.

The physical toll was brutal. "In the beginning of that process, I had hair and then at the end of it, I lost all of the hair. I probably gained 30 pounds in weight during that period of time. It was awful." The stress wasn't just about rejection—it was about the fundamental mismatch between what labels wanted and what Spotify needed to offer. Labels wanted to kill the free tier entirely, viewing it as cannibalizing sales. Spotify knew that without a free option, they'd never convert pirates.

The breakthrough came through equity. Rather than just licensing deals, Spotify offered the major labels ownership stakes in the company. This aligned incentives in a way that pure licensing never could. If Spotify succeeded, the labels would profit not just from royalties but from appreciation of their equity. It was financial jujitsu—turning adversaries into stakeholders.

Self-funding became crucial during this period. Lorentzon spent his own money on developers' salaries, offices, and renting music licenses. They tried to attract investor money, but Lorentzon was not satisfied with the terms with which they were offered to cooperate. Because of these unplanned expenses, Lorentzon's share in Spotify turned out to be the largest. This bootstrapping period, painful as it was, gave the founders extraordinary control over their destiny.

When Daniel and Martin presented their demo of Spotify in early 2007, I was totally blown away. But there was something entirely different going on at the tiny offices at Riddargatan than anything we as venture capitalists had seen before in Sweden. The best talent was attracted to Spotify like bees to honey and the buzz wasn't constrained to the environs of Stockholm, as Northzone's Pär-Jörgen Pärson would later recall.

The beta testing strategy was deliberately constrained. Rather than launching widely and risking server overload or label backlash, Spotify created artificial scarcity. The invite-only system generated buzz while allowing the team to gradually scale infrastructure. Each new user became an evangelist, desperately sharing invites with friends. The product was so good that access itself became social currency.

By 2008, the pieces were finally in place. In 2008, Spotify secured a Series A investment led by Northzone, a European venture capital firm. The funding round also included participation from Creandum, a Swedish venture capital firm, and notable angel investors such as Shakil Khan and Li Ka-shing. The October 2008 launch in select European markets—Sweden, Finland, Norway, France, Spain, and the UK—was deliberately conservative. No fanfare, no massive marketing campaign. Just a product so compelling that word-of-mouth would do the work.

The pre-launch years revealed Spotify's core insight: The music industry's problem wasn't technology—it was trust. By spending two years in stealth, burning through personal fortunes, and nearly killing themselves with stress, Ek and Lorentzon had done something remarkable. They'd convinced an industry scarred by Napster that maybe, just maybe, technology could be an ally rather than an enemy. The impossible had become merely improbable, setting the stage for one of the most audacious scaling stories in tech history.

IV. The Freemium Gambit: Scaling to Global Dominance (2008–2015)

The October 2008 launch timing couldn't have been worse—or better, depending on your perspective. Lehman Brothers had collapsed weeks earlier, the global economy was in freefall, and venture capital was drying up faster than you could say "subprime mortgage." Yet here was Spotify, launching a service that asked people to pay for something they'd been getting free for a decade. The audacity was breathtaking.

But Spotify's freemium model was more sophisticated than it appeared. The free tier wasn't charity—it was a Trojan horse designed to infiltrate the pirates' den. Users could access millions of songs instantly, legally, with ads every few tracks. The genius lay in the constraints: lower bitrates, no offline listening, limited skips on mobile. These weren't bugs; they were carefully calibrated friction points designed to make the €9.99 monthly premium subscription feel like liberation rather than expense.

The early growth numbers validated the approach. Within a year of launch, Spotify had hit one million users across Europe. But the real metric that mattered was conversion rate: roughly 10% of free users upgraded to premium, a figure that would remain remarkably consistent as the company scaled. This wasn't accident—it was behavioral economics executed with surgical precision. The free tier created habit formation, the limitations created desire, and the price point hit the sweet spot between impulse purchase and considered decision.

In February 2009, Spotify opened public registration for the free service tier in the United Kingdom. Registrations surged following the release of the mobile service, leading Spotify to halt registration for the free service in September, returning the UK to an invitation-only policy. Spotify launched in the United States in July 2011, and offered a six-month, ad-supported trial period.

The UK launch in February 2009 became a masterclass in market entry. Rather than competing head-to-head with iTunes on downloads, Spotify positioned itself as complementary—a discovery engine that could actually drive iTunes sales. The message to the British music industry was clear: we're not here to cannibalize your business; we're here to grow the pie.

Geographic expansion followed a deliberate playbook. Start in smaller, tech-forward markets where music piracy was rampant (Nordics). Move to larger European markets with strong rule of law (UK, France, Germany). Only then tackle the US—the graveyard of European tech ambitions. Each market taught lessons that informed the next. The UK taught them about playlist culture. France taught them about local content requirements. Germany taught them about privacy concerns.

The US launch in July 2011 was different. The price of the US licensing deal was that Spotify had to massively scale back its free service in the US. Originally, the majors wanted to shut it down altogether, but Spotify successfully fought back. The compromise was that users could only use the ad-funded free service for ten hours and could only repeat a track five times in total. The restrictions were painful but necessary—without US labels on board, global dominance was impossible.

Facebook integration, launched in September 2011, turned Spotify into a social phenomenon. Suddenly, your music choices were broadcasting to your entire social graph. The partnership was so deep that Facebook's Sean Parker, an early Spotify investor and board member, essentially became Spotify's ambassador to Silicon Valley. The integration drove massive user acquisition—at one point, Spotify was adding a million users every week.

But not everything was smooth sailing. Taylor Swift's high-profile catalog removal in 2014 created a PR crisis. Her argument—that Spotify's free tier devalued music—struck at the heart of the freemium model. Spotify's response was telling: they didn't cave. Instead, they published data showing that 70% of their revenue went to rights holders, arguing that streaming was growing the overall pie rather than cannibalizing sales.

The real innovation during this period wasn't just user acquisition—it was product evolution. In 2012, Spotify realized they had a discovery problem. As one insider put it, Spotify was "great when you know what to listen to, but not when you don't". The solution came through algorithmic curation. Discover Weekly, launched in 2015, used collaborative filtering and natural language processing to create personalized playlists that felt almost telepathic. Within 10 weeks, 40 million people were listening.

The technical infrastructure evolution was equally dramatic. Initially, Spotify ran on a peer-to-peer distribution model, similar to μTorrent, but switched to a server-client model in 2014. This wasn't just a technical decision—it was strategic. P2P had served its purpose during the bootstrap phase, but as Spotify scaled, the legal and technical complexities weren't worth the cost savings. The transition happened so smoothly that most users never noticed.

Competition during this period was fierce but fragmented. Pandora dominated US radio-style streaming but couldn't offer on-demand. Rdio had a better interface but lacked Spotify's catalog depth. Deezer was strong in France but struggled globally. Apple seemed content to milk iTunes downloads rather than embrace streaming. This fragmentation gave Spotify a crucial window to establish itself as the default streaming choice.

The numbers by 2015 told the story: 75 million active users, 20 million paying subscribers, available in 58 countries. Revenue had grown from virtually nothing to €1.95 billion. But profitability remained elusive—the company lost €173 million that year. The bearish view was that Spotify was simply buying growth at unsustainable prices. The bullish view was that they were building an unassailable network effect in a winner-take-all market.

What the critics missed was the platform dynamic emerging beneath the growth numbers. Every playlist created, every song saved, every friend followed—these weren't just engagement metrics. They were switching costs, incrementally raising the barrier for users to leave. The freemium gambit had worked: Spotify had converted millions of pirates into paying customers. Now came the hard part—convincing Wall Street that a money-losing Swedish streaming service was worth tens of billions of dollars.

V. The Direct Listing Revolution: Going Public (2016–2018)

Barry McCarthy, Netflix's former CFO, walked into Spotify's Stockholm headquarters in late 2016 with a radical proposition. "Why do you need investment bankers?" he asked Daniel Ek. It was the question nobody in the room had dared to voice, but everyone had been thinking. Spotify didn't need to raise capital—they had just secured $1 billion in debt financing. They didn't need price discovery—the private markets had been trading Spotify shares for years. What they needed was liquidity for employees and early investors who'd been locked up for a decade. McCarthy's solution was heretical: skip the IPO entirely and list directly on the NYSE.

The traditional IPO process is financial theater at its most expensive. Investment banks typically take 3-7% of proceeds, lockup periods trap insiders for 180 days, and the "IPO pop"—when shares surge on the first day—represents money left on the table by the company. For Spotify, with private market valuations already exceeding $20 billion, this could mean leaving billions with Wall Street rather than the company.

But the real motivation ran deeper. Spotify issued stock options in January 2016 at an interest rate of 4 per cent, raising US $500 million in venture capital. Buyers could exercise the option at a 17.5 per cent discount if Spotify went public within a year. If it did not, the discount would have increased by a further 2.5 percentage points every six months. The convertible debt came with a ticking clock—every month Spotify delayed going public, the terms got worse.

The path to direct listing required rewriting the rules—literally. The NYSE had to change its regulations to accommodate a listing without an underwriter setting an initial price. The SEC had to be convinced that Spotify could provide adequate disclosure without the traditional IPO roadshow. Even Spotify's own lawyers were skeptical. "There's no precedent for this," they warned. Ek's response was characteristically Swedish: "Good. We'll set one."

The preparation was meticulous. Instead of the typical two-week roadshow, Spotify held an investor day on March 15, 2018, streamed live to anyone who wanted to watch. The presentation was a masterclass in transparency: 300 slides detailing everything from churn rates to playlist engagement metrics. They even published their entire financial model—something unheard of in traditional IPOs.The 2017 financials painted a complex picture: nearly $5 billion in revenue, but an operating loss of $461 million. Revenue growth was accelerating—up 39% year-over-year—but so were content costs. The company was essentially buying market share, betting that scale would eventually bring pricing power and operational leverage. Wall Street had to decide: was this Amazon circa 2000, or MoviePass circa never?

April 3, 2018, arrived with unusual calm for such a momentous occasion. Daniel Ek deliberately chose not to ring the opening bell—a statement that this wasn't about pageantry but about democratizing access. The NYSE set a reference price of $132 based on private market trades. When trading opened at 11:35 AM, after more than three hours of price discovery, the first trade printed at $165.90—a 25% premium to the reference price.

The music streaming service traded on the New York Stock Exchange under the ticker symbol SPOT. Unlike a traditional IPO, Spotify conducted a direct listing, meaning no banks underwrote the offering and no price was set ahead of the debut. The NYSE set a reference price of $132 on Monday night based on previous trades on private markets, but ultimately the publicly listed price was based on investor demand.

The first day's trading told a nuanced story. Spotify's shares closed at $149.01 per share after its first day of trading, up from its initial reference price of $132 per share, but more than 10% below its opening price of $165.90 per share and its high price of the day of $169 per share. Volume was lighter than expected—only about 30 million shares traded, roughly 17% of outstanding shares. This wasn't the feeding frenzy of a hot IPO; it was measured, almost cautious.

The immediate reaction was mixed. Critics pointed to the intraday volatility and closing below the opening price as evidence that investment banks served a purpose after all. Without underwriters to stabilize the price, Spotify experienced more volatility than a typical IPO might have seen. But supporters noted that this was exactly the point—true price discovery, not artificial support.

The financial impact was significant. Spotify reportedly paid roughly $35 million in fees. Had they gone the traditional IPO route and floated 10% of the company at a 7% fee (standard for tech IPOs), they would have paid nearly $200 million. The savings were substantial, but the real victory was philosophical. Spotify had proven that companies didn't need Wall Street's permission to go public.

The ripple effects were immediate. Within months, the NYSE and Nasdaq were updating their rules to make direct listings easier. Slack announced plans to follow Spotify's path. Venture capitalists started discussing direct listings as exit strategies. Investment banks, sensing the threat, began offering "IPO-lite" products with lower fees and more flexibility.

But the direct listing also revealed uncomfortable truths about Spotify's business model. Without the typical IPO roadshow narrative of "growth at all costs is temporary," investors had to confront the reality: Spotify's unit economics were challenging. The company paid out roughly 70% of revenue to rights holders, leaving little room for margin expansion. Unlike software companies with 80% gross margins, Spotify was essentially a toll collector, taking a small cut of each transaction.

The market's initial verdict was cautiously optimistic. The stock settled into a trading range between $140-180 for the rest of 2018, suggesting investors were willing to bet on Spotify's growth but not at any price. The "growth over profits" narrative held, but barely. The company would need to prove it could expand beyond music, improve its margins, or achieve such scale that even thin margins would generate substantial profits.

The direct listing revolution wasn't just about saving fees or avoiding lockups. It was a statement about the maturation of private markets and the democratization of capital access. Spotify had proven that with sufficient brand recognition, transparent financials, and existing liquidity, companies could bypass the traditional gatekeepers. The revolution wouldn't apply to every company—most still needed the capital and credibility that came with a traditional IPO. But for a select few unicorns, Spotify had shown there was another way. The Pirates of Stockholm had pulled off their greatest heist yet—stealing the IPO process itself from Wall Street.

VI. The Podcast Wars: From Music to Audio Platform (2019–2024)

The PowerPoint slide that changed everything contained just three words: "Audio First Strategy." It was February 6, 2019, and Daniel Ek stood before investors in New York, about to announce the biggest strategic pivot in Spotify's history. "We aren't just in the music streaming business," he declared. "We're in the business of being the world's audio platform." Within hours, Spotify would announce $340 million in podcast acquisitions, sending shockwaves through both Silicon Valley and Hollywood.

The timing wasn't accidental. Apple Music had been gaining ground, leveraging its iPhone install base to add subscribers at an alarming rate. Amazon was bundling music with Prime, essentially giving it away for free. YouTube commanded more music listening hours than anyone but generated minimal revenue for artists. Spotify needed differentiation, and fast. The answer lay in a medium that was simultaneously ancient and nascent: spoken word audio. The February 2019 acquisitions were surgical strikes. Spotify paid €300 million, or about $337 million, to buy podcasting companies Gimlet Media and Anchor FM Inc. Gimlet brought premium content—shows like "Reply All" and "Homecoming" that had already proven their worth. Anchor offered the YouTube model for audio: let anyone create, monetize at scale. Together, they represented both sides of the content equation: supply and demand, creation and consumption.

But these were just the opening salvos. Within months, Spotify acquired Parcast (true crime podcasts) for $56 million and The Ringer (Bill Simmons' sports and pop culture empire) for up to $250 million. The message was clear: Spotify wasn't dabbling in podcasts—it was declaring war on the entire audio landscape. Then came the deal that changed everything. In May 2020, Spotify announced it had secured exclusive rights to "The Joe Rogan Experience" in a multi-year deal. "The Joe Rogan Experience" became exclusive to Spotify under a 2020 deal, which sources confirmed was worth more than $200 million over 3.5 years. The number was staggering—for context, this was more than Spotify had spent on some entire companies. But Rogan brought something priceless: 11 million listeners per episode, demographic diversity that spanned from tech bros to soccer moms, and cultural relevance that transcended traditional media boundaries.

The impact was immediate and dramatic. Spotify's stock surged from around $150 in May 2020 to over $360 by February 2021—a gain that added roughly $46 billion to the company's market value. The math was beautiful: spend $200 million, gain $46 billion in market cap. Even if the correlation wasn't perfect causation, the signal to the market was clear: Spotify was no longer just aggregating content; it was creating differentiation that competitors couldn't match.

But the Rogan deal also brought something Spotify hadn't fully anticipated: controversy at scale. In January 2022, the platform faced its biggest crisis since launch. Neil Young demanded his music be removed from Spotify, protesting what he called vaccine misinformation on Rogan's show. Joni Mitchell followed. Then India. Arie. Suddenly, Spotify was caught between its biggest content investment and some of music's most respected artists.

The internal turmoil was even more intense. Spotify employees demanded editorial oversight of Rogan's content. Some threatened to quit. Daniel Ek found himself in an impossible position, ultimately declaring: "I do not believe that silencing Joe is the answer." The company removed 70 episodes where Rogan had used racial slurs, added content advisories, but fundamentally stood by their star. The stock plummeted from $245 to $150 in the first half of 2022, though macroeconomic factors also played a role.

The celebrity podcast strategy had mixed results. The Obamas' Higher Ground production company delivered prestige but not massive numbers. Prince Harry and Meghan Markle's Archewell Audio produced exactly one series before Spotify executive Bill Simmons publicly called them "fucking grifters" after their $20 million deal ended. The lesson was brutal: fame didn't automatically translate to podcast success.

By 2023, Spotify began a strategic retreat from exclusivity. The economics had shifted. Exclusive content was expensive and limited advertising inventory. The new strategy: wider distribution, focus on advertising technology, and creator tools. In February 2024, Spotify renewed Rogan's deal for up to $250 million but crucially made it non-exclusive. Rogan could now post on YouTube and other platforms while Spotify handled distribution and ad sales. The results spoke volumes. During Rogan's exclusivity period from 2020 to 2024, Spotify saw a 232% increase in podcast consumption. The platform's monthly active podcast user base grew from 19.9 million in 2020 to 40 million in 2024. By 2025, Spotify had approximately 7 million podcast titles on its platform, making it the go-to platform for podcast listeners worldwide, with 37% choosing it as their favorite.

The layoffs that followed told a different story. Three rounds of cuts between 2022 and 2024 eliminated roughly 25% of Spotify's workforce, with podcast-related divisions bearing the brunt. The company wrote down nearly $400 million in podcast investments. The strategy pivot was clear: away from expensive exclusivity deals, toward technology and advertising infrastructure that could scale across millions of creators.

The broader impact on the audio landscape was undeniable. Spotify had successfully repositioned itself from music streamer to audio platform. Podcasts now represented a growing share of listening time, with higher engagement rates and more valuable advertising inventory than music. The company's Spotify for Podcasters platform gave creators analytics and monetization tools that rivaled YouTube's creator ecosystem.

But the real victory was strategic positioning. Apple, despite inventing podcasting, had been caught flat-footed. Amazon had the resources but lacked focus. YouTube dominated video podcasts but struggled with audio-only content. Spotify had carved out a unique position: the default home for audio-first content, whether music or spoken word.

The podcast wars revealed fundamental truths about content strategy in the streaming age. First, exclusivity is a double-edged sword—it drives subscriptions but limits reach and advertising potential. Second, celebrity doesn't guarantee success in audio—authenticity and consistency matter more than fame. Third, owning the creator tools and advertising infrastructure is more valuable than owning the content itself.

By 2024, the strategy had evolved from "Netflix for podcasts" to something more nuanced: Spotify as the operating system for audio. The company wasn't trying to own all the best content; it was trying to be the platform where all audio content lived, was discovered, and was monetized. The shift from exclusive content to open distribution with superior monetization tools reflected this evolution.

The numbers validated the approach. Podcast advertising on Spotify was growing at 50% annually. Creator sign-ups were accelerating. Time spent listening was increasing. The podcast bet hadn't played out exactly as planned, but it had achieved its core objective: differentiation in an increasingly commoditized streaming market. The pirates had become platform builders, and audio—not just music—was their kingdom.

VII. The Creator Economy & AI Era (2020–Present)

The exodus began with a tweet. On January 27, 2025, Massive Attack announced they were pulling their catalog from Spotify, citing Daniel Ek's investment in Helsing, an AI defense company supplying military technology to Ukraine. Within days, the trickle became a flood—hundreds of artists joining what they called a "conscience boycott." The irony was palpable: the company that had saved artists from piracy was now losing them to principles. The backlash wasn't just about weapons. It represented years of accumulated grievances reaching a breaking point. As Deerhoof put it in their departure statement: "We don't want our music killing people. We don't want our success being tied to AI battle tech." The band called Spotify a "data-mining scam masquerading as a music company" and predicted that "eventually artists will want to leave this already widely hated data-mining scam."

The timing couldn't have been worse for Spotify. Just as the company was trying to rebuild artist relations after the podcast controversies, it faced a new existential question: Could a platform built on creative content survive when creators viewed it as morally compromised? Ek's response to The Financial Times was characteristically blunt: "Personally, I'm not concerned about it. I focus more on doing what I think is right and I am 100 per cent convinced that this is the right thing for Europe."

But the creator economy challenges extended far beyond ethical concerns. The fundamental economics of streaming remained broken for most artists. Spotify's pro rata model meant that if an artist's catalog accounted for 1% of streams, it earned 1% of royalties. This sounded fair in theory but was devastating in practice. A MusiCares survey in 2024 found that 69% of musicians cannot cover expenses from working in music alone, despite record-breaking profits for both the recording industry and streaming services.

The AI revolution promised both salvation and destruction for creators. On one hand, Spotify's AI DJ and personalized playlists drove discovery, helping unknown artists find audiences. The Wrapped AI podcast, using Google's NotebookLM, turned listening data into personalized audio experiences that went viral annually. AI-powered mastering tools democratized production quality. On the other side, AI threatened to flood the platform with synthetic content. Ghost artists—AI-generated musicians creating background music for playlists—became a controversial reality. The fear wasn't just about authenticity; it was about economics. If AI could generate infinite content at zero marginal cost, what happened to human creators?

The September 2025 launch of lossless audio—finally delivering on a promise made in 2021—felt like too little, too late. Spotify Premium subscribers could now stream tracks in up to 24-bit/44.1 kHz FLAC, but Apple had been offering this for free since 2021. The feature rollout to over 50 markets was smooth, but it highlighted a fundamental challenge: Spotify was playing catch-up on quality while trying to lead on discovery.

The price increases told their own story. Premium rose to €11.99 in multiple regions throughout 2024 and 2025, testing the limits of consumer tolerance. Each increase sparked cancellations, but the majority stayed—testament to the switching costs Spotify had built through playlists, social features, and algorithmic recommendations.

The vision Daniel Ek articulated—"one billion subscribers"—seemed both inevitable and impossible. The path required threading multiple needles: keeping artists happy enough to stay while maintaining margins, innovating fast enough to stay ahead of tech giants while not alienating users with constant changes, expanding globally while respecting local content preferences.

The creator tools ecosystem represented Spotify's best hope for sustainable differentiation. Spotify for Artists provided analytics that helped musicians understand their audience. The Spotify Partner Program, launched in January 2025, offered monetization options beyond streaming royalties. Discovery Mode let artists accept lower royalty rates in exchange for algorithmic promotion—controversial but effective.

The audiobooks expansion, accelerated in 2024, opened a new front in the content wars. With 15 hours of audiobook listening included in Premium subscriptions, Spotify was directly challenging Amazon's Audible dominance. Early results were promising—audiobook consumption grew 45% quarter-over-quarter—but the economics remained challenging.

The AI integration went beyond features to fundamental platform architecture. Machine learning models now predicted not just what users wanted to hear, but when and why. The "daylist" feature, which created different playlists for different times of day, showed AI's potential to create genuinely novel experiences. The annual Wrapped became a cultural phenomenon, with the 2024 AI-generated podcast feature garnering billions of social media impressions.

Yet for all the technological innovation, the human element remained paramount. The artist exodus over Helsing exposed a fundamental tension: Spotify needed creators more than creators needed Spotify. Bandcamp, despite its clunky interface, was seeing record sales. Physical media was experiencing a revival. Direct-to-fan platforms were proliferating.

The creator economy era revealed Spotify's greatest strength and weakness: scale. With 675 million monthly active users, it was too big to ignore but also too big to satisfy everyone. Every decision—from royalty rates to content moderation to feature prioritization—affected millions of stakeholders with competing interests.

The path forward required acknowledging uncomfortable truths. Streaming economics would never satisfy all artists. Platform capitalism created winners and losers. Technology could enhance but not replace human creativity. The company that had disrupted the music industry now faced disruption from all sides—AI, social media, gaming, and creators themselves.

As 2025 progressed, Spotify stood at a crossroads. It could double down on being a utility—the pipes through which audio flowed—or try to become something more: a creative platform, a social network, a cultural arbiter. The choice would determine whether the pirates who saved music would themselves need saving, or whether they'd chart a course to that billion-subscriber horizon, ethics and economics be damned.

VIII. Business Model & Unit Economics Deep Dive

Imagine running a restaurant where you pay 70 cents of every dollar that comes in the door directly to your suppliers, before accounting for rent, staff, or utilities. Now imagine those suppliers—in this case, three major record labels—essentially control what you can serve and at what price. Welcome to Spotify's economic reality, where the path to profitability resembles less a runway and more a tightrope walk over an active volcano.

The three-sided marketplace Spotify operates is deceptively complex. On one side sit 675 million monthly active users, 263 million of whom pay roughly €12 per month. On another side perch millions of artists and rights holders, expecting fair compensation. On the third side lurk advertisers, seeking engaged audiences. Spotify sits in the middle, trying to extract value while keeping all parties just happy enough not to revolt. The revenue streams break down with brutal simplicity. Premium subscriptions generate roughly 87% of revenue—€3.7 billion in Q2 2025. Ad-supported revenue contributes the remaining 13%, split between music and podcast advertising. But here's the rub: that €4.2 billion in quarterly revenue translates to a gross margin of just 31.5% as of Q2 2025—impressive progress from the mid-20s a few years ago, but still anemic compared to software companies sporting 80% margins.

The pro rata payout model sounds equitable but creates perverse incentives. If an artist's catalog accounts for 1% of total streams, it earns 1% of the royalty pool. This means a sleep meditation playlist on repeat all night generates the same revenue per stream as a meticulously crafted album played with focused attention. The system rewards quantity over quality, background music over foreground artistry.

Consider the math from an artist's perspective. Spotify pays out roughly $0.003-0.005 per stream. To earn minimum wage in the US ($15,000 annually), an artist needs approximately 3-5 million streams per year. That sounds achievable until you realize that 98% of artists on Spotify have fewer than 1,000 monthly listeners. The pyramid is steep, and the peak is narrow.

The gross margin evolution tells a story of incremental victories. From 26% in 2021 to 31.5% in Q2 2025, each basis point fought for through a combination of price increases, renegotiated label deals, and efficiency gains. The company finally achieved consistent profitability in 2024, posting its first full year in the black. Operating income reached €406 million in Q2 2025—real money, but modest relative to a €145 billion market cap.

Three strategic levers have driven margin improvement. First, the podcast investment, despite its controversies, diversified content costs. Podcast content typically commands 40-50% gross margins versus 25-30% for music. Second, marketplace initiatives like Discovery Mode—where artists accept lower royalties for algorithmic promotion—directly improve unit economics. Third, operational efficiency from the layoffs reduced operating expenses by 16% year-over-year.

The competitive dynamics add another layer of complexity. Apple Music operates as a loss leader, subsidized by iPhone profits. Amazon bundles music with Prime, essentially giving it away. YouTube Music leverages its video platform for near-zero customer acquisition costs. Only Spotify must survive on streaming alone, without a hardware ecosystem or e-commerce empire to lean on.

Network effects provide the primary defense. Every playlist created, every friend followed, every algorithmic recommendation accepted increases switching costs. A typical Spotify user has 50+ playlists, follows dozens of artists, and has trained the algorithm through years of listening. Recreating this on another platform requires effort most users won't expend.

But the moat has limits. Music catalogs are largely identical across platforms. Exclusive content proved too expensive to sustain. The user interface, while refined, isn't dramatically superior to competitors. The real differentiation lies in the recommendation engine and social features—defensible but not impregnable.

Capital allocation reveals management's priorities. Despite achieving profitability, Spotify announced a $1 billion share buyback program in 2024, signaling confidence in the business model. R&D spending continues at 10-12% of revenue, focused on AI and personalization. Marketing spend has actually decreased as a percentage of revenue, from 14% to 11%, as organic growth and word-of-mouth became primary acquisition channels.

The path to sustainable profitability requires threading multiple needles. Music costs must continue declining as a percentage of revenue, likely through direct artist deals that bypass labels. Advertising revenue must grow faster than the user base, requiring better targeting and higher CPMs. Price increases must continue without triggering mass defections. New revenue streams—live events, merchandise, artist services—must mature.

The bear case remains compelling. Spotify operates in a commodity business with powerful suppliers and well-funded competitors. The company generates roughly €25 in revenue per user per quarter but keeps less than €8 after content costs. Marketing, technology, and overhead consume most of what remains. The math is unforgiving.

Yet the bull case has merit too. With 696 million users and growing, Spotify has achieved unprecedented scale in audio. Every 1% improvement in gross margin drops roughly €170 million to the bottom line annually. The platform is becoming essential infrastructure for the music industry, too important to squeeze too hard.

The unit economics reveal a fundamental truth: Spotify isn't really a tech company in the traditional sense. It's a toll collector on the highway of human culture, taking a small cut of each transaction while bearing the costs of building and maintaining the road. Whether that toll generates sufficient returns for shareholders remains an open question. The pirates may have saved music, but whether they can save themselves financially is still being written in the quarterly earnings reports.

IX. Playbook: Lessons in Platform Building

The conference room in Stockholm, 2007. Martin Lorentzon slams his fist on the table: "We're not competing with iTunes. We're competing with piracy!" This fundamental insight—that the enemy wasn't other legitimate services but illegal alternatives—shaped every strategic decision that followed. The lesson: identify your true competition, not the obvious one.

Converting pirates to paying customers required understanding a counterintuitive truth about human behavior. Pirates weren't stealing music because they were criminals; they were stealing because the experience was superior to buying. Instant access to everything, no DRM restrictions, perfect portability. Spotify's genius was recognizing that you couldn't compete with free on price—you had to compete on experience.

The Swedish advantage extended beyond progressive IP laws. Sweden in 2006 had 90% broadband penetration, compared to 60% in the US. The population was tech-literate, English-speaking, and culturally predisposed to consensus-building rather than litigation. Spotify couldn't have started in Silicon Valley because Silicon Valley would have attracted lawsuits before users. The lesson: geography is destiny for regulatory-sensitive startups.

Consider the road not taken. If Spotify had launched in the US first, it would have faced immediate legal challenges from labels still traumatized by Napster. The RIAA would have sought injunctions. Artists would have organized boycotts. The press would have framed it as "Napster 2.0." Instead, by proving the model in smaller, more receptive markets, Spotify arrived in the US with momentum, credibility, and leverage.

The freemium wedge deserves its own MBA case study. In winner-take-all markets, the temptation is to go premium-only—higher margins, cleaner positioning, simpler operations. But Spotify understood that in a market with near-zero marginal costs, controlling distribution mattered more than maximizing revenue per user. The free tier wasn't charity; it was customer acquisition cost brilliantly disguised as product.

The numbers validate the strategy. Customer acquisition cost through the free tier: essentially zero. Conversion rate to premium: 10-15% consistently. Lifetime value of a premium subscriber: over €1,000. The math was beautiful—let users acquire themselves, convert the most engaged, monetize for years. Compare this to Netflix spending hundreds of dollars to acquire each subscriber through marketing.

Timing the market required patience bordering on masochism. Spotify incorporated in 2006 but didn't launch publicly until 2008. Two years of negotiations, development, and preparation. The post-Napster era had created a unique window: labels desperate enough to try anything, consumers trained on digital music by iPods, broadband finally ubiquitous. Too early, and the infrastructure wouldn't support streaming. Too late, and Apple or Google would have locked up the market.

The direct listing playbook rewrote the rules of going public. Traditional IPOs serve three purposes: raise capital, provide liquidity, generate publicity. Spotify needed only liquidity—it had capital and publicity. By eliminating investment banks from the equation, Spotify saved hundreds of millions in fees and avoided the typical first-day pop that transfers value from the company to traders. The lesson: question every "standard" process, especially expensive ones.

Content strategy pivots revealed strategic flexibility. The exclusive podcast bet from 2019-2023 was ultimately a failed experiment, but the speed of recognition and reversal was impressive. Rather than doubling down on a losing strategy (the corporate default), Spotify acknowledged reality and pivoted to open distribution with better monetization tools. The lesson: strategy is hypothesis; be prepared to falsify your own theories.

Managing multi-stakeholder complexity required a delicate balance. Labels wanted higher royalties but needed Spotify's reach. Artists wanted more money but benefited from discovery. Users wanted everything free but valued the service enough to pay. Advertisers wanted engaged audiences but not at the expense of user experience. Spotify became a master of giving each stakeholder just enough to stay engaged without giving away the store.

The platform versus aggregator distinction matters enormously. Aggregators like Netflix create or license content exclusively. Platforms like YouTube let anyone contribute. Spotify tried to be both—aggregating music from labels while platforming podcasts from creators. The hybrid model is harder to execute but more defensible once established. You get the quality control of curation with the scale economics of user-generated content.

Technical architecture decisions had strategic implications. The shift from peer-to-peer to client-server in 2014 wasn't just about reliability—it was about control. P2P was faster and cheaper but legally questionable and technically complex. Client-server was expensive but defensible. The lesson: sometimes the technically inferior solution is strategically superior.

The creator tools ecosystem represents platform building at its most sophisticated. Spotify for Artists, Spotify for Podcasters, the Spotify Partner Program—these aren't just features but switching costs. Every artist who depends on Spotify's analytics, every podcaster who uses Spotify's hosting, becomes locked into the ecosystem. The tools are free, but the dependency is priceless.

International expansion followed a counterintuitive sequence. Instead of targeting the largest markets first (US, China, India), Spotify expanded in concentric circles from Sweden. First Nordics, then Western Europe, then English-speaking countries, finally emerging markets. Each market's learnings informed the next. The slow rollout built operational muscle and negotiating leverage.

Price discrimination through family plans, student discounts, and regional pricing extracted maximum consumer surplus without appearing predatory. A US family plan at $20/month for six users equals $3.33 per user. A student plan in India at $0.80/month. Same product, 4x price difference. The lesson: price based on willingness to pay, not cost to serve.

The Spotify playbook ultimately teaches that platform building is about managing paradoxes. Be open but controlled. Be cheap but valuable. Be global but local. Be tech but media. Be innovative but reliable. The companies that successfully navigate these contradictions don't just build products—they build ecosystems that become too essential to abandon. The pirates didn't just save music; they created a blueprint for how to transform any industry held hostage by its own business model.

X. Bear vs. Bull Case & Future Scenarios

The elevator pitch for both cases fits on a napkin. Bulls see the TAM: 8 billion humans with ears, only 700 million using Spotify. Bears see the margins: 31% gross, 10% operating on a good day. Bulls point to pricing power finally emerging after 15 years. Bears note that every price increase sparks cancellations and artist defections. Both are right. That's what makes Spotify fascinating—and frustrating—as an investment.

The Bull Case: Path to Global Audio Domination

Start with the inexorable math of streaming adoption. In 1999, zero humans streamed music. In 2015, 68 million paid for streaming globally. Today, that number exceeds 700 million and is growing 15% annually. Spotify owns roughly 31% market share—double its nearest competitor. In any other industry, this would be called dominance.

The billion-user target isn't fantasy—it's arithmetic. India has 1.4 billion people and 3% streaming penetration. Southeast Asia has 700 million people and 5% penetration. Africa has 1.4 billion people and virtually no penetration. As smartphones proliferate and data costs plummet, these markets will stream. The question isn't if but when, and Spotify is already present in 184 markets, waiting.

AI-powered personalization creates a compounding moat. Every stream trains the algorithm. Every skip refines recommendations. After 18 years and trillions of data points, Spotify's recommendation engine is approaching telepathy. The Discover Weekly playlist has a 70% completion rate. The DJ feature feels genuinely conversational. This isn't easily replicable—it's the product of time, scale, and continuous refinement.

Podcast advertising is finally delivering on its promise. CPMs for podcast ads are 3-5x higher than music ads. Engagement rates exceed 80%. The Spotify Audience Network allows advertisers to buy across podcasts programmatically. As podcast listening grows from 20% to 40% of total platform time, advertising revenue could triple without adding a single user.

The platform is becoming essential infrastructure for creators. Spotify for Artists has 5 million active users. The Spotify Partner Program is distributing millions to creators monthly. Canvas (the moving artwork feature) has been used on 100 million tracks. Discovery Mode is driving billions of streams to emerging artists. This isn't just a streaming service—it's becoming the operating system for audio creators.

Pricing power is finally materializing. After years of being stuck at $9.99, Spotify has successfully raised prices three times since 2023 without significant churn. The service has become habitual—part of daily routine like coffee or commuting. Users grumble but don't leave. Each 10% price increase drops roughly €1.5 billion straight to gross profit.

Live events and merchandise represent untapped billions. Spotify knows what 700 million people listen to, when, and where. That data is worth fortunes to concert promoters, merchandise companies, and artists planning tours. The company is just beginning to monetize this intelligence through Spotify Live and artist partnerships.

The Bear Case: Structural Challenges and Existential Threats

The fundamental economics remain broken. Spotify pays out 70% of revenue to rights holders—a percentage that hasn't materially changed since 2008. Every dollar of revenue growth generates only 30 cents of gross profit. This isn't a software company; it's a utility with tech company valuations.

Major labels hold Spotify hostage. Universal, Sony, and Warner control 68% of recorded music. They can demand higher royalties, threaten to pull content, or launch competing services. The labels learned from the iTunes experience—never again will they let a tech company have too much power. Spotify's negotiating position weakens as alternatives proliferate.

Artist relations are deteriorating, not improving. The Helsing controversy is just the latest grievance. Musicians increasingly view Spotify as exploitative—a necessary evil rather than a partner. The platform that saved the industry from piracy is now viewed as the new oppressor. Taylor Swift's return was pragmatic, not an endorsement.

Big Tech competitors have infinite resources and patience. Apple doesn't need Apple Music to be profitable—it's a feature to sell iPhones. Amazon bundles music with Prime. YouTube leverages its video dominance. Google has YouTube Music. These companies can operate at losses indefinitely. Spotify must generate returns or die.

Regulatory risks are mounting globally. The EU's Digital Markets Act forces interoperability. The US Congress is investigating anticompetitive practices. India mandates local content quotas. Each market adds compliance costs and operational complexity. The regulatory burden only increases with scale.

Content fragmentation is accelerating. Podcasts are re-fragmenting across platforms. Artists are experimenting with direct-to-fan models. NFTs and Web3 promise (however dubiously) to eliminate intermediaries. The grand unified platform for all audio may be impossible to sustain.

AI commoditizes both creation and distribution. If AI can generate infinite background music at zero cost, why pay royalties? If AI assistants can perfectly curate from any source, why need Spotify's recommendations? The same technology that enhances Spotify's product also threatens to obsolete it.

Future Scenarios

Scenario 1: The Winner-Take-Most Victory (30% probability) Spotify reaches 1.5 billion users by 2030, achieves 40% gross margins through direct artist deals and AI optimization, and becomes the definitive global audio platform. The company vertically integrates into live events, merchandise, and artist financing. Market cap exceeds $500 billion. Daniel Ek becomes the richest person in Europe.

Scenario 2: The Profitable Niche (40% probability) Spotify plateaus at 800-900 million users but achieves sustainable 15% operating margins through cost discipline and price optimization. The company remains the leader in music streaming but cedes podcasts to YouTube and audiobooks to Amazon. It generates steady cash flows, buys back shares, and trades at a reasonable multiple. A boring but successful business.

Scenario 3: The Slow Bleed (20% probability) Competition intensifies, margins compress, and growth stalls. Spotify becomes the BlackBerry of streaming—once dominant, gradually irrelevant. Apple or Amazon acquires it for $50-75 billion to eliminate a competitor. Daniel Ek starts another company, claiming he was always more interested in healthcare anyway.

Scenario 4: The Platform Revolution (10% probability) Spotify successfully transforms into a true platform where creators capture most value. The company becomes the AWS of audio—providing infrastructure while creators build businesses. Web3 integration enables direct artist-to-fan monetization. Spotify takes a small percentage of massive transaction volume. The stock either 10xs or goes to zero trying.

The future remains radically uncertain. Spotify has survived piracy, fought Apple, tamed labels, and achieved impossible scale. Yet profitability remains fragile, competition intense, and stakeholders increasingly hostile. The bull case requires everything going right. The bear case needs only a few things to go wrong. The truth, as always, lies somewhere in between—in the messy middle where great companies either transcend their constraints or succumb to them. The pirates saved music once. Whether they can save themselves remains the question worth €145 billion.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube