Novo Nordisk: The Danish Titan That Conquered Obesity

I. Introduction & Episode Roadmap

Picture this: A Danish pharmaceutical company worth more than Denmark's entire economy. Novo's market capitalization of more than $570 billion is bigger than the Danish economy. The company's market capitalization of $570 billion remained larger than the entire economy of Denmark, its $2.3 billion income tax bill for 2023 made it the largest taxpayer in the country, and its rapid growth was driving nearly all of the expansion of Denmark's economy.

It sounds like something out of a business fiction novel, but this is the reality of Novo Nordisk in 2024—a company that began in a Copenhagen villa experimenting with animal pancreases and now commands the global obesity treatment market with drugs that have become household names: Ozempic and Wegovy.

How did two feuding Danish insulin makers, born from a bitter betrayal between mentor and protégés, transform into Europe's most valuable company? How did a century-old diabetes company pivot to create what could become the best-selling drugs of all time?

This is the story of scientific breakthroughs, corporate rivalries, and strategic patience. It's about a company structure that prioritizes long-term thinking over quarterly earnings, a small Scandinavian nation that bet its economic future on biotechnology, and a discovery that transformed obesity from a lifestyle choice into a treatable disease.

What you're about to learn goes far beyond the headlines of celebrity weight loss and TikTok trends. This is the untold business story of how Novo Nordisk built a pharmaceutical empire on the foundation of a hormone called GLP-1, creating drugs that not only treat diabetes and obesity but also reduce cardiovascular risk and potentially reshape how we think about metabolic health entirely.

From insulin wars in 1920s Denmark to a $600 billion market cap in 2024, from laboratory breakthroughs to manufacturing crises, from scientific Nobel prizes to Wall Street's obsession—this is how Novo Nordisk conquered chronic disease and, in the process, became bigger than the country that created it.

II. The Danish Insulin Wars: Origins & Founding Drama (1920s–1980s)

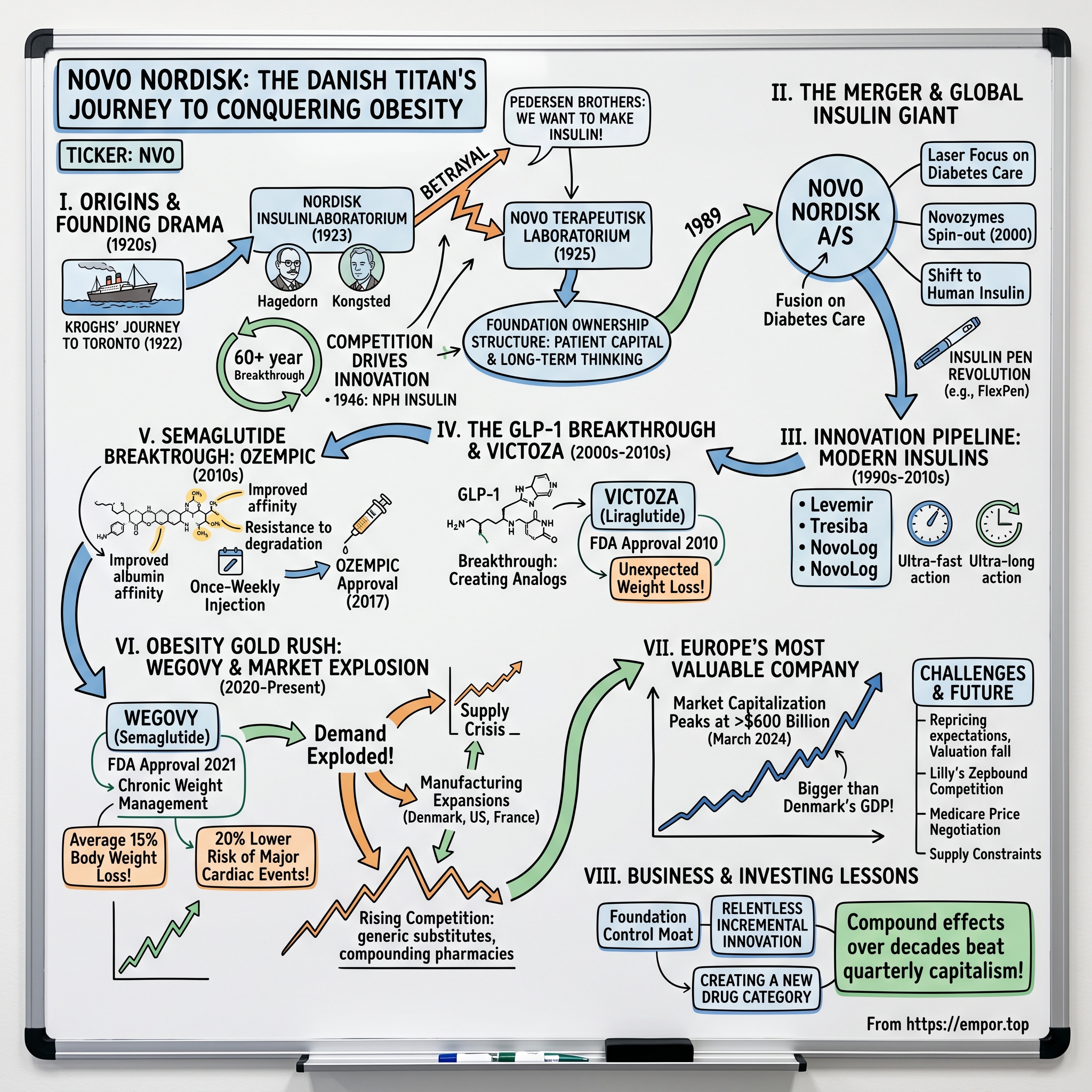

The story begins with love, disease, and a lecture tour that would change medical history. Marie and August Krogh were no ordinary couple. She was among Denmark's first female medical graduates, while he was a renowned physiologist and Nobel laureate. Marie also had diabetes – a disease considered a death sentence at the time. After hearing of the discovery of insulin in 1921, August and Marie were intrigued. At Marie's urging, August travelled to Canada to seek permission from the researchers to produce this life-saving medicine in Denmark.

The Kroghs' 1922 journey to Toronto wasn't just a scientific expedition—it was a desperate mission to save Marie's life. At a private dinner, Marie Krogh was told by the renowned American diabetologist Eliot P. Joslin that insulin had just been discovered and purified in Toronto. August and Marie Krogh therefore extended their journey and spent the November 23-25 in Toronto as John Macleod's guests. During his stay in Toronto, Krogh obtained a license which allowed him to use the protocol for insulin purification developed there. Production was started immediately upon his return to Copenhagen on December 12. The first patient was treated as early as March 13, 1923.

Working alongside physician Hans Christian Hagedorn and pharmacist August Kongsted, Krogh established Nordisk Insulinlaboratorium in 1923. Upon his return, Marie also convinced the scientist Hans Christian Hagedorn to join her husband and August Kongsted from Løvens Kemiske Fabrik. In March 1923, the first patients were treated with their insulin, kicking off a century of innovation within diabetes.

But success breeds competition—and in this case, betrayal.

The Pedersen brothers, Harald and Thorvald, were integral to Nordisk's early insulin production. Harald had built a revolutionary machine that could shave frozen pancreases into ice-cold acid alcohol, dramatically improving extraction efficiency. Thorvald, a talented chemist, worked on purifying the insulin to unprecedented levels. Together, they were helping Nordisk approach the mass production levels of American giant Eli Lilly.

Then came the rupture that would define Danish pharmaceutical history for the next 65 years.

In 1924, tensions between Thorvald Pedersen and Hans Christian Hagedorn reached a breaking point. In 1924, a disagreement led Christian Hagedorn to dismiss Thorvald Pedersen, a talented chemist working in his lab. Thorvald's brother Harald, who also worked at Nordisk but on Krogh's team, handed in his resignation in solidarity. According to the people involved in what we can only assume was a somewhat tense exit interview, this is what was said: August Krogh: "What are you going to do?" Harald Pedersen: "We want to make insulin." August Krogh: "Well, you'll never manage that." Harald Pedersen: "We will show you!"

Those five words—"We will show you!"—would echo through Danish business history.

Brothers Harald and Thorvald Pedersen, who were former employees of Nordisk, formed their own company, Novo Terapeutisk Laboratorium. Novo and Nordisk competed vigorously until they merged in 1989 to become Novo Nordisk A/S. The brothers established their competing insulin company in 1925, setting up shop just a few kilometers away from their former employer.

What followed was six decades of fierce competition that, paradoxically, drove both companies to excellence. Each breakthrough by one company spurred innovation at the other. When Nordisk developed longer-acting insulins, Novo responded with improved purification techniques. When Novo pioneered new delivery mechanisms, Nordisk countered with enhanced formulations.

NPH (Neutral Protamine Hagedorn) insulin was developed in 1946 and soon accounted for much of the world's consumption of longer-acting insulin. With NPH, people with diabetes require fewer injections. This innovation, named after Hagedorn himself, represented a massive quality-of-life improvement for diabetes patients worldwide.

The competition wasn't just about products—it extended to every aspect of the business. Novo and Nordisk each established diabetes hospitals in Denmark to provide specialised diabetes care and lifestyle guidance while gaining a better understanding of patients' needs. In 1992, the two hospitals merged to become the Steno Diabetes Center, and Novo Nordisk continues to build on this holistic approach to care today.

Perhaps most significantly, both companies adopted a foundation ownership structure that would prove crucial to their long-term success. Nordisk's foundation was established in the 1920s and Novo followed in 1951. The foundations merged in 1989 and today the Novo Nordisk Foundation continues to award research and humanitarian grants while enabling Novo Nordisk to do what is best in the long term for patients, employees and shareholders.

This structure wasn't just about governance—it was about philosophy. The foundations ensured that profits would flow back into scientific research and humanitarian causes, creating a virtuous cycle of innovation and social responsibility that continues to this day. August Krogh's words to Harald Pedersen in 1924, "You'll never manage that", and Pedersen's reply, "We will show you", were perhaps no longer prominently displayed in the corridors of the respective companies, but the voices of the past and the fierce competition between them had not been forgotten.

By the 1980s, both Novo and Nordisk had grown from small Danish laboratories into significant players in the global insulin market. Novo had built an impressive campus in the Copenhagen suburb of Bagsværd, while Nordisk operated from nearby Gentofte—two pharmaceutical powerhouses separated by just 15 minutes' drive and 60 years of rivalry.

The stage was set for one of the most significant mergers in pharmaceutical history.

III. The Merger & Becoming a Global Insulin Giant (1989–2000s)

January 1989. The boards of two foundations that had spent 65 years in bitter competition issued a joint press release that sent shockwaves through Denmark's business community. Nevertheless, in January 1989, the boards of the two foundations with corporate interests, Novo Foundation and Nordisk Insulinlaboratorium, issued a press release that unleashed tremendous external attention on the two companies and was the equivalent of a palace revolution internally. The press release was short and sweet: "The Boards of the Novo Foundation and Nordisk Insulinlaboratorium have agreed to merge the two foundations into the Novo Nordisk Foundation."

The brevity of that announcement belied the seismic shift it represented. In 1989, Novo Industri A/S (Novo Terapeutisk Laboratorium) and Nordisk Gentofte A/S (Nordisk Insulinlaboratorium) merged to become Novo Nordisk A/S, the world's largest producer of insulin with headquarters in Bagsværd, Copenhagen.

The merger made immediate strategic sense, even as it shocked employees who had spent their careers viewing the other company as the enemy. The merger instantly created the world's largest insulin producer that could now leverage Novo's strong marketing and manufacturing with Nordisk's best-in-class research. The combined company had annual revenues of more than DKr 6 billion ($835 million) and 7,350 employees. It was estimated to control up to half of the market for insulin in the Western world.

But this wasn't just a business combination—it was a philosophical fusion that would define modern Novo Nordisk. The merged foundation structure created something unique in global pharma: a company with patient capital, freed from the quarterly earnings pressure that drives short-term thinking at most pharmaceutical giants.

Novo Nordisk is controlled by majority shareholder Novo Holdings A/S (wholly owned by the Novo Nordisk Foundation) which holds approximately 28.1% of its shares and a majority (77.1%) of its voting shares. This structure would prove invaluable as the company embarked on decades-long research programs that might never have survived the scrutiny of quarterly earnings calls.

The 1990s saw Novo Nordisk systematically streamline its operations to focus on its core competency: diabetes care. The company made strategic divestitures that would seem prescient in hindsight. Novo's enzymes business, Novozymes A/S, was spun-out in 2000. This wasn't abandoning a profitable business—it was laser-focusing on where Novo Nordisk could dominate globally.

The company also pioneered the shift from animal-derived to human insulin through recombinant DNA technology. This wasn't just a scientific achievement; it was a strategic masterstroke that eliminated supply constraints and ethical concerns while dramatically improving product consistency and safety.

Building beyond just drugs, Novo Nordisk created an entire diabetes care ecosystem. The company invested heavily in patient education, established specialized diabetes centers, and developed innovative delivery devices that made insulin therapy less burdensome. The Steno Diabetes Center, formed from the merger of Novo and Nordisk's respective diabetes hospitals, became a model for integrated diabetes care worldwide.

The insulin pen revolution exemplified Novo Nordisk's approach to innovation. While competitors focused solely on the insulin molecule, Novo Nordisk recognized that how patients administered insulin was just as important as the drug itself. The development of pre-filled, disposable insulin pens transformed diabetes management from a medical procedure into something patients could discretely handle in their daily lives.

By the late 1990s, Novo Nordisk commanded significant global market share in insulin, but the company's leadership saw something others missed: the future wasn't just in better insulin, but in entirely new approaches to metabolic disease. Research teams were already investigating a curious gut hormone called GLP-1 that seemed to regulate blood sugar in ways insulin couldn't match.

Competition with Eli Lilly intensified during this period, but Novo Nordisk's foundation structure allowed it to take a longer view. While Lilly had to satisfy Wall Street every quarter, Novo Nordisk could invest in research programs that might not pay off for a decade or more. This patience would prove crucial as the company began developing what would become the most valuable drugs in its history.

The merger also brought unexpected benefits in terms of talent and culture. The best researchers from both companies now worked together, their former rivalry channeled into competing with external competitors rather than each other. The combined R&D capabilities, coupled with the financial strength of the merged entity, created a innovation powerhouse.

The company had started to move away from its traditional focus on diabetes care towards a more ambitious mission to "defeat serious chronic diseases", and towards that end, hired over 10,000 people in 2023 alone. This expansion of vision—from treating diabetes to addressing metabolic disease more broadly—would position Novo Nordisk perfectly for the obesity epidemic that was just beginning to be recognized as a medical crisis.

IV. The Innovation Pipeline: Modern Insulins & Device Evolution (1990s–2010s)

While the world focused on the internet boom and bust, Novo Nordisk was quietly revolutionizing diabetes care through incremental innovations that, collectively, transformed patient lives. The company makes several drugs under various brand names, including Levemir, Tresiba, NovoLog, Novolin R, NovoSeven, NovoEight, and Victoza.

The evolution from human insulin to insulin analogues represented a quantum leap in diabetes management. Ultra-long action insulins reduce the number of injections and the risk of hypoglycaemia by releasing the medication very slowly, while ultra-fast action insulins offer convenience by reducing the need for planning around mealtimes. These weren't just minor improvements—they fundamentally changed how people with diabetes could live their lives.

Tresiba, launched in the 2010s, exemplified this innovation. With a half-life of over 25 hours, it provided unprecedented flexibility in dosing time—patients no longer had to structure their entire lives around rigid injection schedules. For shift workers, parents with unpredictable schedules, or anyone living a non-routine life, this was revolutionary.

But Novo Nordisk understood that the best drug in the world is useless if patients can't or won't take it properly. The company's device innovation matched its pharmaceutical development stride for stride. The FlexPen, NovoPen, and later smart insulin pens didn't just deliver insulin—they transformed the entire experience of diabetes management.

The smart pen evolution deserves particular attention. By the late 2010s, Novo Nordisk's connected pens could track doses, timing, and even remind patients when to inject. This wasn't just convenience—it was addressing one of the biggest challenges in diabetes care: adherence. Studies showed that even motivated patients often forgot doses or couldn't remember if they'd already injected. Smart pens solved this with elegant simplicity.

The company's approach to innovation was distinctly different from Silicon Valley's "move fast and break things" ethos. Each new insulin formulation underwent years of testing, not just for efficacy but for real-world usability. Engineers worked alongside endocrinologists, designers collaborated with patients, and manufacturing experts ensured each innovation could be produced at scale without compromising quality.

Market dominance during this period wasn't achieved through monopolistic practices but through relentless focus on patient outcomes. When competitors launched new products, Novo Nordisk's response was invariably to innovate further rather than simply compete on price. This created a virtuous cycle: higher margins funded more R&D, which produced better products, which commanded premium prices.

The pricing power Novo Nordisk accumulated during this period would later become controversial, but it's important to understand the value proposition. A patient using Tresiba needed fewer injections, experienced fewer dangerous low blood sugar episodes, and could live a more flexible life than someone using older insulins. For many, this wasn't just a medication upgrade—it was life-changing.

By the early 2010s, Novo Nordisk's insulin portfolio covered every possible patient need: ultra-rapid for mealtime coverage, long-acting for baseline control, and premixed formulations for simplicity. The company had also expanded beyond insulin into other diabetes-related hormones and proteins, building expertise that would prove crucial for its next act.

In practice, Novo Nordisk typically reinvests about 13–15% of its annual revenue into R&D programs. This consistent investment, maintained even during economic downturns, created a deep pipeline of innovations. While other pharmaceutical companies might slash R&D during tough times to maintain earnings, Novo Nordisk's foundation structure allowed it to think in decades, not quarters.

The company was also building capabilities beyond traditional pharmaceuticals. Protein engineering, formulation science, device development, and even digital health—Novo Nordisk was assembling the tools for a transformation that few saw coming.

In research laboratories in Denmark, scientists were working on something that had nothing to do with insulin but everything to do with diabetes: a gut hormone that seemed to not just control blood sugar but also affect appetite and weight. The GLP-1 story was about to begin.

V. The GLP-1 Discovery & Development of Victoza (2000s–2010s)

The conference room at Novo Nordisk's Bagsværd headquarters must have been electric with possibility when researchers first presented their findings on GLP-1 receptor agonists. This wasn't just another insulin improvement—this was an entirely new paradigm for treating type 2 diabetes.

GLP-1, or glucagon-like peptide-1, had been known to scientists since the 1980s. But understanding a hormone and turning it into a medicine are vastly different challenges. Native GLP-1 is broken down by the body in minutes, making it useless as a therapeutic. Novo Nordisk's breakthrough was in creating analogues that could survive in the body long enough to be effective.

The development of liraglutide, which would become Victoza, represented years of painstaking molecular engineering. Scientists had to solve multiple puzzles simultaneously: How to prevent the rapid breakdown of the hormone, how to make it bind effectively to receptors, and how to ensure it could be manufactured at scale. The solution involved attaching a fatty acid side chain that allowed the drug to bind to albumin in the blood, dramatically extending its half-life.

Victoza received FDA approval in 2010, entering a diabetes market that Novo Nordisk already knew intimately. But this wasn't just another diabetes drug—it represented a fundamental shift in treatment philosophy. Semaglutide, a glucagon like peptide-1 (GLP-1) receptor agonist, is available as monotherapy in both subcutaneous as well as oral dosage form (first approved oral GLP-1 receptor agonist). It has been approved as a second line treatment option for better glycaemic control in type 2 diabetes and currently under scrutiny for anti-obesity purpose.

The clinical trials for Victoza revealed something unexpected that would reshape Novo Nordisk's entire strategy: patients were losing weight. Not just a few pounds, but meaningful, sustained weight loss. This wasn't entirely surprising to scientists who understood GLP-1's role in appetite regulation, but the magnitude of the effect caught everyone's attention.

However, the path wasn't without obstacles. In September 2017, Novo Nordisk agreed to pay $58.7 million to end a United States Department of Justice probe into the lack of FDA disclosure to doctors about the cancer risk for their diabetic drug, Victoza. The controversy around potential cancer risks cast a shadow over GLP-1 drugs that would take years of additional research to fully address.

Despite these challenges, Victoza became a blockbuster, generating billions in revenue and establishing Novo Nordisk as the leader in GLP-1 therapies. But more importantly, it provided proof of concept for what would come next. The company's researchers were already working on a next-generation GLP-1 drug that would only need to be injected once weekly instead of daily.

The success of Victoza also validated Novo Nordisk's strategy of moving beyond insulin. While the company maintained its insulin market leadership, it was clear that GLP-1 drugs represented the future. The global diabetes epidemic was accelerating, driven by obesity and sedentary lifestyles. Traditional treatments could manage blood sugar, but GLP-1 drugs offered something more: they addressed multiple aspects of metabolic disease simultaneously.

Competition in the GLP-1 space intensified quickly. Eli Lilly, Novo Nordisk's perpetual rival, was developing its own GLP-1 drugs. Other pharmaceutical giants were entering the space. But Novo Nordisk had a crucial advantage: years of experience with the GLP-1 pathway and a deep understanding of how to engineer these complex molecules for maximum effectiveness.

The development costs were staggering—hundreds of millions of dollars for each clinical trial, years of regulatory reviews, and massive investments in manufacturing capabilities. But the potential reward justified the risk. The diabetes market was worth tens of billions annually, and GLP-1 drugs were capturing an increasing share.

By the mid-2010s, Novo Nordisk's scientists had achieved something remarkable: a GLP-1 drug that was even more potent than Victoza, lasted even longer in the body, and could be injected just once per week. They called it semaglutide, and it would change everything.

The lessons learned from Victoza's development and commercialization informed every decision about semaglutide. The molecule was optimized not just for efficacy but for manufacturing efficiency. The clinical trial program was designed to demonstrate benefits beyond blood sugar control. And perhaps most importantly, the weight loss effects that had been a pleasant surprise with Victoza were now a primary focus of investigation.

VI. The Semaglutide Breakthrough: Ozempic Development (2010s)

In the molecular engineering labs at Novo Nordisk, scientists had created something extraordinary. Semaglutide has 94% sequence homology with native GLP-1 and three key structural differences that confer improved albumin affinity and resistance to dipeptidyl peptidase-4 degradation. That 94% similarity to human GLP-1 was crucial—close enough to activate the body's natural systems, different enough to last in the bloodstream for a week instead of minutes.

The development of semaglutide represented the culmination of decades of expertise in protein engineering. Semaglutide (C187H291N45O59; 4113.58 g/mol) has 31 amino-acid containing peptidic structure which is 94% homologous to the native GLP-1 for avoiding immunogenicity. The alanine residue at 8th position is substituted with Aib (2-aminoisobutyric acid) which protects semaglutide from enzymatic degradation by DPP-4. Similar to liraglutide, the lysine residue at 34th position in native GLP-1 was replaced by arginine in semaglutide too. The arginine substitution at 34th position was helpful in production of GLP-1 analogue through semi-recombinant process. Lysine residue at 26th position was acylated for attachment with a C18 fatty diacid through a hydrophilic linker "γGlu-2xOEG", which prolonged the systemic half-life through enhanced albumin binding and reduced renal clearance.

This might read like impenetrable scientific jargon, but each modification represented years of research and hundreds of failed attempts. The result was a molecule that could survive in the human body for an entire week while maintaining its therapeutic effect—a feat of molecular engineering that shouldn't be understated.

The SUSTAIN clinical trial program for Ozempic was massive in scope and ambition, encompassing more than 8,000 adults with type 2 diabetes across eight phase 3a trials. Bagsværd, Denmark, 5 December 2017 - Novo Nordisk today announced that the US Food and Drug Administration (FDA) has approved Ozempic® (semaglutide injection). Ozempic® is indicated as an adjunct to diet and exercise to improve glycaemic control in adults with type 2 diabetes mellitus. Ozempic®, the approved brand name for once-weekly semaglutide in the US, is a glucagon-like peptide 1 (GLP-1) receptor agonist. The approval of Ozempic® is based on the results from the SUSTAIN clinical trial programme and follows a positive recommendation from an FDA Advisory Committee meeting on 18 October 2017. In people with type 2 diabetes, Ozempic® produced clinically meaningful and statistically significant reductions in HbA1c compared with placebo, sitagliptin, exenatide extended-release and insulin glargine U100. Furthermore, in the trials, treatment with Ozempic® resulted in statistically significant reductions in body weight.

December 5, 2017, marked a watershed moment: FDA approval of Ozempic for type 2 diabetes. But even as champagne corks popped in Bagsværd, Novo Nordisk's leadership knew this was just the beginning. The weight loss signal in the clinical trials was too strong to ignore. Patients weren't just losing a few pounds—they were experiencing transformative weight reduction that rivaled dedicated weight-loss medications.

The mechanism behind semaglutide's effectiveness was elegant in its mimicry of natural processes. By activating GLP-1 receptors in the pancreas, brain, and gastrointestinal tract, the drug orchestrated a complex symphony of metabolic effects: increased insulin production when blood sugar rose, decreased glucagon release, slowed gastric emptying, and crucially, reduced appetite through direct action on brain centers controlling hunger and satiation.

What made Ozempic particularly revolutionary was its demonstration that treating diabetes and addressing weight weren't separate challenges but interconnected aspects of metabolic health. The traditional medical approach had been to treat each condition independently, often with medications that worked at cross-purposes. Ozempic offered a unified solution.

The early commercial success of Ozempic was solid but not spectacular. Diabetes specialists appreciated the once-weekly dosing and superior efficacy, but the drug was entering a crowded market. Novo Nordisk priced it at parity with other weekly GLP-1 drugs, focusing on gaining market share rather than maximizing initial revenues.

Behind the scenes, however, Novo Nordisk was preparing for something much bigger. The company had initiated clinical trials testing higher doses of semaglutide specifically for weight loss in people without diabetes. The STEP trial program would evaluate semaglutide in obesity treatment, and early signals suggested the results would be extraordinary.

The development of an oral formulation of semaglutide, eventually branded as Rybelsus, represented another breakthrough. Glucagon-like peptide-1 receptor agonists (GLP-1RA) are effective agents for achieving glycemic control. Oral semaglutide is the first oral formulation of a GLP-1RA to be approved in the USA. This agent may lead to earlier initiation of GLP-1RA therapy in the type 2 diabetes continuum of care, and represents a valuable treatment option for patients with a preference for oral therapy.

Creating an oral version of a peptide drug is extraordinarily difficult—the stomach's acidic environment and digestive enzymes are designed specifically to break down proteins. Novo Nordisk solved this puzzle by combining semaglutide with an absorption enhancer called SNAC that protected the drug and facilitated its absorption through the stomach lining. It was a technical tour de force that opened GLP-1 therapy to the millions of patients who refused injectable medications.

By 2020, as the world grappled with COVID-19, Novo Nordisk was sitting on clinical trial data that would soon transform the company—and potentially society's entire approach to obesity. The STEP trials had concluded, and the results exceeded even the most optimistic projections.

VII. The Obesity Gold Rush: Wegovy & Market Explosion (2020–Present)

June 4, 2021. The FDA approval of Wegovy for chronic weight management sent shockwaves through the pharmaceutical industry and beyond. FDA Approved: Yes (First approved June 4, 2021) Brand name: Wegovy Generic name: semaglutide Dosage form: Injection Company: Novo Nordisk Treatment for: Weight Loss (Obesity/Overweight), Cardiovascular Risk Reduction This wasn't just another drug approval—it was the validation of obesity as a treatable chronic disease and the beginning of what would become the most dramatic pharmaceutical market expansion in recent history.

The clinical trial results were unprecedented. In 2021, the FDA gave the green light to Wegovy to help people with obesity or overweight lose weight. In the STEP trials, participants lost an average of 15% of their body weight—results that approached what had previously only been achievable through bariatric surgery. For context, previous obesity medications celebrated achieving 5% weight loss. Wegovy had tripled that benchmark.

But the real game-changer came in 2023 with the SELECT trial results. In addition to having a 20% lower risk overall of major cardiac events, such as heart attack, stroke, or cardiovascular death, participants who took Wegovy had a 28% reduction in heart attacks (for those already taking heart medications, such as statins, to reduce cholesterol), a 7% decrease in non-fatal strokes, and a 15% drop in cardiovascular-related deaths. Suddenly, Wegovy wasn't just a weight-loss drug—it was a cardiovascular medication that happened to cause dramatic weight loss.

The market response was extraordinary and immediate. Demand exploded beyond anything Novo Nordisk had anticipated or prepared for. Most of the growth occurred from its weight loss drugs, Wegovy and Ozempic, which accounted for 55% of the company's 2023 revenue. Pharmacies couldn't keep the drug in stock. Patients formed waiting lists. Insurance companies scrambled to develop coverage policies for a drug that cost over $1,000 per month.

The supply crisis that emerged wasn't a simple manufacturing bottleneck—it reflected the complexity of producing semaglutide at unprecedented scale. On completion, Novo Nordisk said it would acquire three manufacturing facilities from its parent for $11 billion to scale up production to meet the massive demand for Wegovy and Ozempic. The company revealed in April 2024 that to meet demand, it was running its production facilities 24 hours a day, 365 days per year.

The cultural impact of Wegovy and Ozempic transcended typical pharmaceutical marketing. The drugs became a social media phenomenon, with "Ozempic face" entering the vernacular and celebrities openly discussing their use. This wasn't just medical treatment—it had become a cultural moment, sparking debates about body image, medical equity, and the medicalization of obesity.

Competition from compounding pharmacies added another layer of complexity. During the shortage, these pharmacies began producing their own versions of semaglutide, arguing that FDA shortage declarations allowed them to compound copies of branded drugs. By July 2025, Novo Nordisk had fallen to become the fifth most valuable drug company amid rising competition from generic weight loss substitutes. The company established a new pharmacy, called NovoCare, which would charge customers $499 per month for access to the drug, less than half the cost of the drug through other pharmaceutical distribution networks.

Novo Nordisk's response to the supply crisis was multifaceted and expensive. Beyond the $11 billion acquisition of Catalent manufacturing facilities, the company announced massive expansions of its existing facilities in Denmark, France, and the United States. In June 2024, the company announced plans to build a new production plant in Clayton, North Carolina, at a cost of $4.1 billion. It will be the company's fourth in the state of North Carolina and used for production of semaglutide products Ozempic and Wegovy. The company also announced plans to acquire three US-based Catalent sites in to increase production supply.

The financial performance during this period was nothing short of spectacular. Sales of Obesity care products, Wegovy® and Saxenda®, increased by 56% measured in Danish kroner and by 57% at CER to DKK 65,146 million. Sales growth was driven by both North America Operations and International Operations. The volume growth of the global branded obesity market was 119%. Novo Nordisk is the global market leader with a volume market share of 70.4%.

But success brought scrutiny. In February 2024, the United States Judicial Panel on Multidistrict Litigation ordered that 55 lawsuits pending in federal courts be consolidated into a multidistrict litigation. The majority of the cases were against Novo Nordisk, but some were brought against Eli Lilly. Patients reported side effects ranging from mild nausea to severe gastroparesis. Questions emerged about long-term safety, the sustainability of weight loss after stopping treatment, and the societal implications of medicalizing obesity on such a massive scale.

The transformation of Novo Nordisk during this period extended beyond just financial metrics. The company had started to move away from its traditional focus on diabetes care towards a more ambitious mission to "defeat serious chronic diseases", and towards that end, hired over 10,000 people in 2023 alone. This wasn't just growth—it was metamorphosis from a diabetes company that happened to make weight-loss drugs into a metabolic disease powerhouse addressing some of society's most pressing health challenges.

VIII. The Business of Being Europe's Most Valuable Company

The numbers are staggering, almost incomprehensible in their scale. In March 2024, Novo Nordisk reached a $604 billion market capitalization and became the 12th most valuable company in the world. To put this in perspective, a Danish pharmaceutical company focused primarily on diabetes and obesity had become more valuable than most of the world's tech giants, oil majors, and financial institutions.

But with great power came great responsibility—and concern. The drugmaker's income tax bill in Denmark last year was $2.3 billion, and its massive investments and heightened production helped the domestic economy expand almost 2% — more than four times the EU average. Without Novo's contribution, the Danish economy would have stagnated. Economists began using a term typically reserved for oil-dependent nations: Dutch disease.

The fear was real and justified. That's triggered worries about the small nation's reliance on the company, and that Denmark — if the drugmaker were to face serious challenges — could suffer like Finland did when Nokia Oyj slumped in the early part of the 2000s. Denmark's economy had become so intertwined with Novo Nordisk's success that any stumble by the company could trigger a national recession.

Net sales in 2024 were US$42.121 billion. This represented a remarkable growth trajectory—Novo Nordisk annual revenue for 2024 was $42.108B, a 24.86% increase from 2023. Novo Nordisk annual revenue for 2023 was $33.724B, a 34.59% increase from 2022. Novo Nordisk annual revenue for 2022 was $25.057B, a 11.85% increase from 2021.

The company's influence extended far beyond direct economic impact. The foundation backs 27% of Denmark's medical research. It sponsors the work and salaries of 9,500 scientists — almost as many as work at Novo itself. Last year, the foundation gave away its first Obesity Prize for Excellence in collaboration with the European Association for the Study of Obesity. The winner was a researcher from the Novo Nordisk Foundation Center for Basic Metabolic Research at the University of Copenhagen.

This concentration of power raised legitimate questions about academic independence and research priorities. When one company funds over a quarter of a nation's medical research, how independent can that research truly be? The Novo Nordisk Foundation, now the world's largest philanthropic foundation with assets twice those of the Gates Foundation, wielded enormous influence over Denmark's scientific agenda.

The manufacturing expansion required to meet global demand was reshaping entire regions. Capital expenditure for property, plant and equipment was DKK 47.2 billion compared with DKk 25.8 billion in 2023, primarily reflecting investments in additional capacity for active pharmaceutical ingredient (API) production and fill-finish capacity for both current and future injectable and oral products. Capital expenditure related to intangible assets was DKK 4.1 billion in 2024 compared with DKK 13.1 billion in 2023 reflecting business development activities.

The company's strategic decisions rippled through global markets. When Novo Nordisk announced it would establish NovoCare, a direct-to-consumer pharmacy offering Wegovy for $499 per month—less than half the typical cost—it sent shockwaves through the pharmaceutical distribution industry. This wasn't just pricing strategy; it was a potential reshape of how expensive medications reach patients.

The human capital transformation was equally dramatic. The company had started to move away from its traditional focus on diabetes care towards a more ambitious mission to "defeat serious chronic diseases", and towards that end, hired over 10,000 people in 2023 alone. To effectively manage the rapid expansion of its workforce while maintaining its traditional corporate culture, the Novo Nordisk Way, the company put over 400 senior executives through a leadership development program.

Managing this growth while maintaining the company's distinctive culture—rooted in Danish values and the foundation's long-term perspective—became a critical challenge. The Novo Nordisk Way, the company's governing philosophy, emphasized patient focus, business ethics, and sustainable thinking. But could these values survive the transition from Danish diabetes specialist to global pharmaceutical titan?

The financial markets watched every move with intense scrutiny. By September 2025, reality had set in: As of September 2025 Novo Nordisk has a market cap of $247.78 Billion USD. This makes Novo Nordisk the world's 52th most valuable company according to our data. The dramatic fall from the $604 billion peak reflected multiple challenges: intensifying competition from Eli Lilly, supply chain constraints, and questions about the long-term sustainability of the GLP-1 market's growth.

Yet even at this "reduced" valuation, Novo Nordisk remained a colossus. The company's influence on Denmark's economy hadn't diminished—if anything, the volatility highlighted the risks of such dependence. It paid $3.8 billion in taxes last year, its ecosystem now accounts for roughly 10% of Denmark's GDP when indirect effects are included, and around 40% of the country's exports.

IX. Competition, Challenges & The Future of GLP-1s

The battle for obesity market supremacy between Novo Nordisk and Eli Lilly has become the pharmaceutical industry's most watched rivalry since the statin wars of the 1990s. But unlike those earlier competitions, this fight involves drugs that don't just treat disease—they fundamentally alter how society thinks about weight, health, and medical intervention.

Eli Lilly said its obesity drug Zepbound led to more weight loss than its main rival, Novo Nordisk's Wegovy, in the first head-to-head clinical trial on the two weekly injections. The findings suggest Zepbound may be a superior treatment for weight loss, helping patients with obesity or who are overweight lose 20.2% of their body weight on average after 72 weeks. Wegovy helped people lose 13.7% of their weight on average after the same time period. Zepbound's greater weight loss is a huge advantage for Eli Lilly, helping obese or overweight patients lose 20.2% of their body weight, or roughly 50 pounds, on average after 72 weeks in the phase three trial.

The SURMOUNT-5 trial results, released in December 2024, sent shockwaves through the industry. Lilly's tirzepatide (Zepbound) had definitively proven superior to Novo's semaglutide (Wegovy) in head-to-head comparison—a 47% greater relative weight loss. This wasn't a marginal victory; it was decisive.

But Novo Nordisk wasn't sitting idle. The company's response came through the STEER real-world study, which showed Wegovy (semaglutide) at 2.4 mg cut the risk of heart attack, stroke and cardiovascular-related death or death from any cause by 57% in patients without substantial treatment gaps compared to Lilly's Zepbound (tirzepatide). That translated to 15 recorded cardiovascular events in the study's Wegovy arm versus 39 reported in the Zepbound cohort.

This highlighted a crucial distinction: while Zepbound might deliver superior weight loss, Wegovy appeared to offer better cardiovascular protection. For many patients and physicians, this presented a genuine dilemma—what mattered more, maximum weight loss or optimal heart protection?

The competitive landscape was also complicated by mechanism of action differences. While Novo's semaglutide regulates the GLP-1 incretin hormone, Lilly's tirzepatide acts on both the GLP-1 and the gastric inhibitory polypeptide (GIP) hormones. Both are involved in the production of insulin and the control of appetite. This dual-action approach gave Lilly's drug theoretical advantages that were now being proven in clinical practice.

Legal challenges mounted alongside commercial competition. In February 2024, the United States Judicial Panel on Multidistrict Litigation ordered that 55 lawsuits pending in federal courts be consolidated into a multidistrict litigation. The majority of the cases were against Novo Nordisk, but some were brought against Eli Lilly. Patients alleged inadequate warnings about side effects, particularly gastroparesis and gallbladder problems.

The supply chain challenges that had plagued both companies throughout 2023-2024 showed signs of easing, but at enormous cost. Lilly seems to have gotten a better handle on its supply challenges. Last week, the FDA's drug shortage database indicated that all doses of Mounjaro and Zepbound are now available in the U.S. Meanwhile, Novo is also making strides in boosting the supply of semaglutide with only Wegovy's lowest dose of 0.25 mg tagged as having "limited availability" by the FDA.

Looking ahead, the pipeline competition intensified. Novo Nordisk's CagriSema, combining semaglutide with cagrilintide, showed promising results with 23% weight loss in trials, matching Zepbound's efficacy. But the real game-changers might come from outside the current duopoly. Viking Therapeutics, Pfizer, Amgen, and others had GLP-1 drugs in development that could reshape the market by 2026-2027.

The pricing and access battles were just beginning. One snag for Novo is the inclusion of semaglutide on CMS' list for its Medicare price negotiation program. All three of Novo's semaglutide products were included in the second wave of the program, with negotiated prices set to go into effect in 2027. This government intervention could fundamentally alter the economics of the GLP-1 market in the United States.

Perhaps most significantly, the societal questions around these drugs were becoming impossible to ignore. Were GLP-1 drugs addressing a medical crisis or creating a new form of pharmaceutical dependency? As data emerged showing rapid weight regain after stopping treatment, critics questioned whether these drugs solved obesity or simply created lifetime customers.

The international expansion opportunities remained massive. All these companies could come together to battle for a market Pitchbook estimates could reach $200 billion annually by 2031. Yet penetration outside the US remained limited, constrained by pricing, cultural attitudes toward obesity treatment, and healthcare system readiness.

X. Playbook: Business & Investing Lessons

The Novo Nordisk story offers a masterclass in long-term value creation that challenges conventional business wisdom. Here are the key lessons that transcend pharmaceuticals:

The Power of Foundation-Controlled Governance

Novo Nordisk is controlled by majority shareholder Novo Holdings A/S (wholly owned by the Novo Nordisk Foundation) which holds approximately 28.1% of its shares and a majority (77.1%) of its voting shares. This structure, often criticized by Wall Street for lack of accountability, enabled Novo Nordisk to invest in research programs with 10-20 year horizons. The semaglutide development program took over a decade from concept to market—a timeline that would have been terminated multiple times at a quarterly earnings-driven company.

The foundation structure also aligned incentives in unique ways. Since the foundation's mission includes funding scientific research and humanitarian causes, Novo Nordisk's profitability directly translates into societal benefit. This creates a virtuous cycle where commercial success enables more research, which drives more innovation, which generates more profit for philanthropic purposes.

Long-term Thinking vs. Quarterly Capitalism

When competitors were slashing R&D during economic downturns, Novo Nordisk maintained its investment at 13-15% of revenue, regardless of economic cycles. This consistency created compound advantages: institutional knowledge accumulated, research teams remained intact, and multi-year programs proceeded uninterrupted.

The contrast with American pharmaceutical companies is stark. While US competitors often grow through acquisition—buying innovation rather than developing it—Novo Nordisk built capabilities organically over decades. The expertise in protein engineering that enabled semaglutide's development wasn't purchased; it was cultivated through generations of scientists working on incremental improvements.

Dominating Through Incremental Innovation

Novo Nordisk's path to dominance wasn't marked by singular breakthroughs but by relentless incremental improvement. From NPH insulin in 1946 to Tresiba in the 2010s, each innovation built on the previous one. This approach created multiple advantages: - Deep technical expertise that competitors couldn't quickly replicate - Strong physician relationships built over decades of reliable innovation - Manufacturing excellence from producing similar molecules for generations - Regulatory expertise from hundreds of successful submissions

Creating Category-Defining Drugs

The transformation of obesity from a lifestyle choice to a chronic disease requiring medical intervention represents one of the most successful medical reframings in history. Novo Nordisk didn't just develop obesity drugs; they helped create the obesity drug category itself. This involved: - Funding research demonstrating obesity's biological basis - Supporting physician education about obesity as a disease - Lobbying for insurance coverage of obesity treatments - Conducting long-term outcome studies showing mortality benefits

Managing Supply/Demand Imbalances at Scale

The Wegovy shortage crisis could have destroyed the product's launch and handed the market to competitors. Instead, Novo Nordisk turned it into a demonstration of commitment, investing over $20 billion in manufacturing expansion while maintaining product quality and avoiding the quality issues that plagued competitors' rapid scaling efforts.

The Compound Effect of R&D Investment

In 2024, for instance, it spent around $3.5B on R&D. But the real story isn't the absolute number—it's the consistency and focus. By concentrating R&D spending on metabolic disease for decades, Novo Nordisk built cumulative advantages that generalist pharmaceutical companies couldn't match.

Building Moats in Pharma

Novo Nordisk's competitive advantages extend far beyond patents: - Manufacturing complexity: Producing semaglutide at scale requires expertise in protein production, purification, and formulation that takes years to develop - Regulatory relationships: Decades of successful interactions with FDA and EMA created trust and expertise - Physician networks: Relationships with endocrinologists built over a century - Patient data: Millions of patient-years of real-world evidence - Supply chain: Vertical integration from active ingredients to finished products

The lesson for investors and operators: true competitive advantages in complex industries come from the accumulation of many small edges rather than single breakthrough innovations.

XI. Analysis & Bear vs. Bull Case

Bull Case: The Trillion-Dollar Trajectory

The optimistic case for Novo Nordisk rests on multiple expanding opportunities. The obesity epidemic affects over 650 million adults globally, yet less than 2% currently receive pharmaceutical treatment. At current prices, treating just 10% of the eligible population would create a $500 billion annual market.

Beyond obesity, semaglutide's demonstrated cardiovascular benefits open entirely new markets. Ozempic® (semaglutide) injection 0.5 mg, 1 mg, or 2 mg as the most broadly indicated glucagon-like peptide-1 receptor agonist (GLP-1 RA) in its class. Every major cardiovascular outcome trial has shown benefits, suggesting GLP-1 drugs could become standard of care for anyone with metabolic syndrome—potentially 30-40% of adults in developed countries.

The international opportunity remains largely untapped. While the US generates the majority of revenues, penetration in Europe, Asia, and emerging markets remains minimal. As healthcare systems recognize the long-term cost savings from preventing diabetes complications and cardiovascular events, reimbursement should expand globally.

Manufacturing scale advantages are becoming insurmountable. The billions invested in production capacity create barriers competitors will struggle to match. Even if patents expire, the complexity of manufacturing these biologics at scale means generic competition will be limited and delayed.

Bear Case: Peak GLP-1 and Competitive Threats

The bearish perspective starts with valuation. As of September 2025 Novo Nordisk has a market cap of $247.78 Billion USD. This makes Novo Nordisk the world's 52th most valuable company according to our data. The dramatic fall from $604 billion to $248 billion in 18 months suggests the market is repricing growth expectations.

Competition is intensifying dramatically. Zepbound's greater weight loss is a huge advantage for Eli Lilly, helping obese or overweight patients lose 20.2% of their body weight, or roughly 50 pounds, on average after 72 weeks in the phase three trial. Some analysts expect the space to be worth $150 billion a year by the early 2030s. Lilly's superior efficacy data could drive market share shifts, while next-generation competitors could leapfrog both companies.

Pricing pressure is inevitable and intensifying. Government intervention through Medicare negotiation, competition from compounding pharmacies, and eventual generic competition will compress margins. The current pricing of $1,000+ per month is unsustainable as volumes grow and political pressure mounts.

Safety concerns could emerge with broader use. As millions of patients use these drugs for years or decades, rare side effects could surface. The litigation consolidation already underway suggests legal risks are materializing. A single major safety issue could devastate the entire GLP-1 class.

The Denmark dependency creates unique risks. Higher U.S. tariffs and a slowdown in the rapid growth of its star pharma company, Novo Nordisk, contributed to the revision, the economy ministry said. Denmark on Friday slashed its annual growth forecast to 1.4% from 3%, in large part due to weaker expectations for pharmaceutical giant Novo Nordisk. The economy ministry noted that Denmark's U.S. exports fell significantly in early 2025 after a huge spike in late 2024, due to both inventory build-up and increased competition in the weight loss drug market, which has seen Novo lose market share. Pharmaceuticals are now expected to contribute just 1.3 percentage points to Denmark's goods exports growth this year, down from 8.1 percentage points in 2024.

The Question of Sustainability

The fundamental question facing Novo Nordisk is whether GLP-1 drugs represent a permanent shift in disease treatment or a bubble driven by social media hype and aggressive marketing. The answer likely lies somewhere between these extremes.

The biological efficacy is undeniable—these drugs work better than anything previously available for obesity. The cardiovascular benefits provide medical justification beyond cosmetic weight loss. But the need for continuous treatment, high costs, and side effects mean these aren't miracle cures but rather powerful tools with significant limitations.

For investors, the key insight is that Novo Nordisk doesn't need the most optimistic scenarios to play out to remain highly valuable. Even in a world where growth slows, competition intensifies, and prices decline, the company's established position, manufacturing scale, and pipeline depth should ensure continued profitability.

The real risk isn't that GLP-1 drugs stop working or that demand disappears—it's that the extraordinary margins and growth rates of 2023-2024 prove unsustainable as the market matures and competition increases.

XII. Epilogue & "If We Were CEOs"

The transformation of Novo Nordisk from a Danish insulin manufacturer to a global metabolic disease leader represents one of the most successful pivots in pharmaceutical history. But what comes next?

If we were running Novo Nordisk, three strategic priorities would dominate:

First, manufacturing must become a core competitive advantage, not just a necessary capability. The company should vertically integrate even further, controlling the entire supply chain from raw materials to patient delivery. This means not just building factories but developing proprietary manufacturing technologies that create insurmountable cost and quality advantages. The goal: make it economically impossible for biosimilar manufacturers to compete even after patent expiry.

Second, expand beyond injection into multiple modalities. While the oral semaglutide (Rybelsus) represents a start, the future lies in combination therapies, longer-acting formulations (monthly or quarterly), and entirely new delivery methods. Imagine a GLP-1 patch changed weekly or an implant lasting six months. The company that makes GLP-1 therapy as convenient as taking a daily vitamin will dominate the next decade.

Third, redefine the therapeutic scope from metabolic disease to human longevity. The cardiovascular benefits of GLP-1 drugs suggest broader anti-aging and protective effects. Novo Nordisk should investigate semaglutide's impact on cognitive decline, certain cancers, and inflammatory conditions. The goal isn't to become an everything drug but to recognize that metabolic health underlies many chronic diseases.

The biggest surprise in researching this story? The extent to which Novo Nordisk's success stems not from any single breakthrough but from patient, cumulative advantages built over a century. In an industry obsessed with blockbuster drugs and breakthrough innovations, Novo Nordisk won through consistency, focus, and the luxury of long-term thinking enabled by its foundation structure.

For founders, the lesson is powerful: in industries with long development cycles and complex products, patient capital and consistent focus beat brilliant pivots and aggressive growth hacking. The Novo Nordisk model—foundation control, long-term thinking, reinvestment in core capabilities—offers an alternative to the venture capital-driven, exit-focused model that dominates today's startup ecosystem.

For investors, Novo Nordisk demonstrates that the most valuable companies aren't always the fastest-growing or most innovative, but those that compound advantages over decades. The company's century-long focus on metabolic disease created knowledge, relationships, and capabilities that no amount of capital could quickly replicate.

Looking ahead, Novo Nordisk faces its greatest challenge not from competitors but from its own success. Can a company born from Danish insulin wars maintain its cultural cohesion while operating as a global giant? Can the patient, scientific culture survive the pressures of being a top 50 global company by market value? Can the foundation structure that enabled long-term thinking withstand the scrutiny that comes with controlling a significant portion of Denmark's economy?

The next decade will determine whether Novo Nordisk becomes the first trillion-dollar pharmaceutical company or whether the GLP-1 gold rush proves to be a spectacular but ultimately unsustainable bubble. Either way, the company has already achieved something remarkable: transforming how humanity thinks about and treats metabolic disease.

The Danish insulin wars that began a century ago have evolved into something far greater—a battle for the future of human health, with implications reaching far beyond medicine into how we conceptualize obesity, aging, and the role of pharmaceutical intervention in society. Whatever happens next, Novo Nordisk has already secured its place in business history as the company that made obesity a treatable disease and, in the process, became bigger than the nation that birthed it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube