Medtronic: Engineering Tomorrow's Health

I. Cold Open & Episode Setup

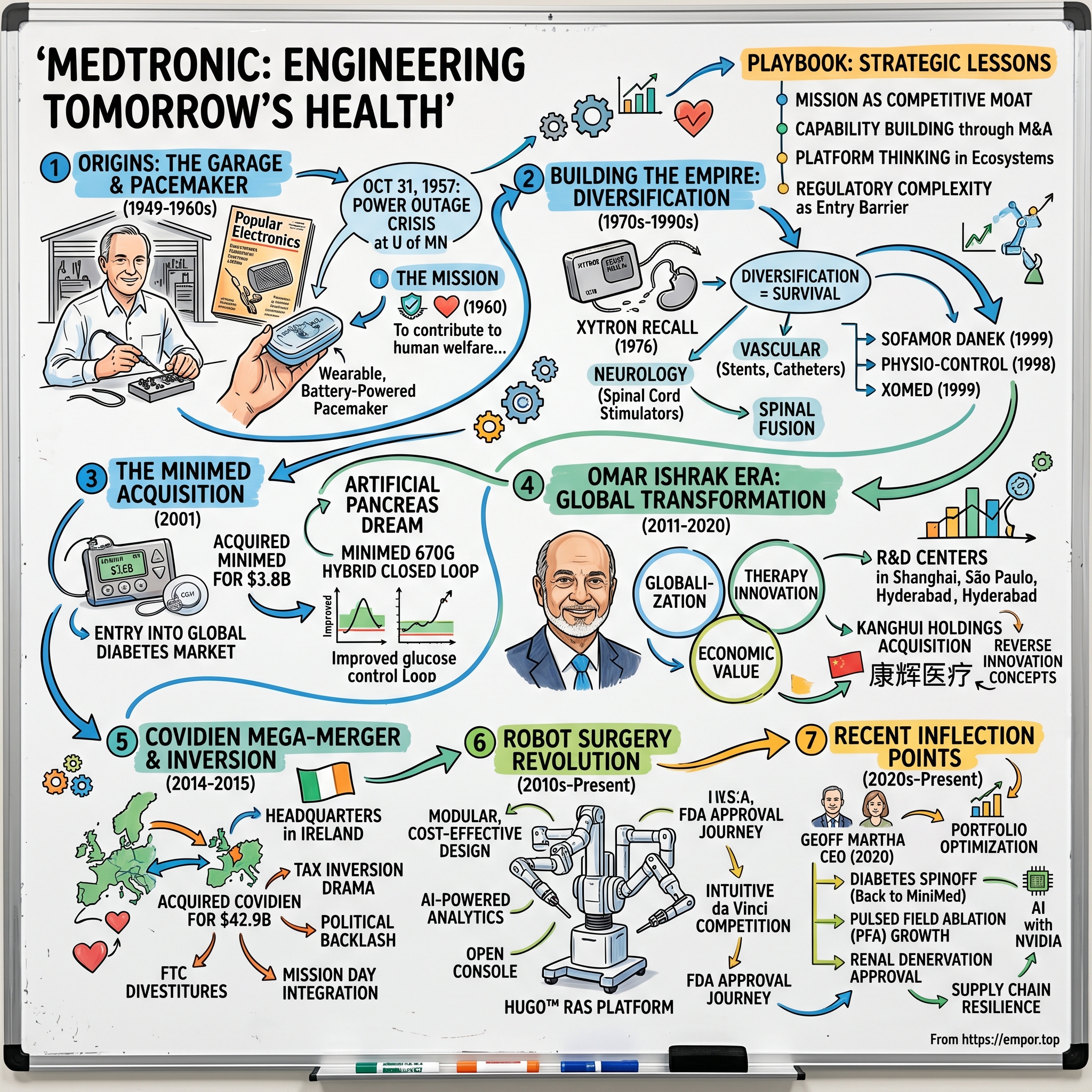

Picture this: Minneapolis, 1949. A young electrical engineer named Earl Bakken sits in his sister's garage, soldering iron in hand, fixing hospital equipment that most manufacturers have written off as irreparable. He charges $4 for house calls. Seven decades later, that garage operation has morphed into Medtronic—a $90 billion healthcare colossus that touches 75 million lives annually and generates more revenue than the GDP of dozens of countries.

How does a medical equipment repair shop become the world's largest medical device company by revenue? The answer isn't just about inventing the battery-powered pacemaker, though that's where the legend begins. It's about something far more audacious: the systematic engineering of an entire industry, one acquisition, one breakthrough, and one regulatory battle at a time.

Medtronic today isn't just American or Irish—it's both, thanks to one of the most controversial tax inversions in corporate history. It operates in 150 countries, employs 95,000 people, and maintains a portfolio spanning everything from spinal implants to surgical robots to insulin pumps. The company holds over 46,000 patents and pumps 8% of revenue back into R&D—a staggering $2.4 billion annually.

But here's what makes Medtronic truly fascinating for students of business history: it's a company that has reinvented itself completely at least four times. From garage startup to pacemaker monopolist. From pacemaker company to diversified medical device conglomerate. From device manufacturer to integrated healthcare solutions provider. And now, attempting perhaps its most ambitious transformation yet—from traditional medtech giant to AI-powered, robotics-driven healthcare platform.

This is a story about relentless innovation meeting ruthless capital allocation. About a "Mission" culture that survived countless mergers. About how a Minnesota nice company learned to play hardball in Washington and Dublin. And ultimately, about whether a $90 billion giant can stay nimble enough to compete with both scrappy startups and tech titans eyeing healthcare's $4 trillion prize.

The roadmap ahead takes us from Earl Bakken's garage through the creation of the Minneapolis medical device cluster, the building of a global empire through serial acquisitions, the controversial Covidien merger that relocated the company to Ireland, and the current inflection point as Medtronic prepares to spin off its diabetes business while betting billions on surgical robotics. Along the way, we'll decode the playbook that turned a repair shop into a healthcare powerhouse—and examine whether that playbook still works in an era of value-based care, AI disruption, and activist investors.

II. Origins: The Garage and the Pacemaker

The story begins not in a boardroom but in a movie theater. Eight-year-old Earl Bakken sits transfixed watching "Frankenstein" in 1932, mesmerized by electricity bringing life to the lifeless. That childhood fascination with electrical animation would, decades later, revolutionize cardiac care and spawn an industry.

By 1949, Bakken had returned from World War II service as a radar technician, armed with electrical engineering knowledge and entrepreneurial hunger. Post-war America was experiencing a medical equipment crisis: hospitals desperately needed sophisticated devices, but manufacturers often refused repairs, preferring to sell new units. Bakken saw opportunity in this service gap. Along with his brother-in-law Palmer Hermundslie, he launched Medtronic in a 600-square-foot garage in northeast Minneapolis, offering repair services for medical equipment that others wouldn't touch.

The business model was simple but revolutionary for its time: exceptional service, fast turnaround, and a willingness to tackle anything electrical in a hospital. They fixed centrifuges, incubators, even dental chairs. Revenue in the first month: $8. But Bakken understood something fundamental—relationships with physicians and hospital staff were more valuable than any single repair job. He cultivated these connections obsessively, often working for free to build trust.

Everything changed on October 31, 1957. A power outage at the University of Minnesota Hospital killed a young patient dependent on a wall-powered pacemaker. Dr. C. Walton Lillehei, the pioneering heart surgeon, approached Bakken with an urgent request: create a battery-powered pacemaker that could keep patients alive during power failures. Lillehei wasn't just any surgeon—he was performing groundbreaking open-heart surgeries on children, procedures considered impossible just years earlier. But his patients kept dying when the power failed.

Bakken's response demonstrated the ingenuity that would define Medtronic's culture. Rather than spending years on development, he grabbed a circuit diagram from Popular Electronics magazine for a transistorized metronome, modified it to deliver electrical pulses to the heart, and housed it in a aluminum soap dish with a leather strap. Four weeks later, he delivered the world's first wearable, battery-powered external pacemaker. Cost to build: about $50. Impact on medicine: priceless.

The device wasn't pretty—patients carried it like a purse, with wires running directly to their hearts—but it worked. The first patient to use it, a child, survived. Word spread through the medical community like wildfire. Orders poured in from hospitals worldwide. Medtronic's revenue jumped from $181,000 in 1958 to $500,000 in 1960.

But this wasn't just about one invention. Minneapolis in the 1950s was becoming the Silicon Valley of medical devices, and the ecosystem was unique. The University of Minnesota Medical School, under the leadership of Dr. Owen Wangensteen, encouraged an unprecedented collaboration between physicians and engineers. Wangensteen gave engineers like Bakken access to operating rooms, autopsies, and most importantly, direct feedback from surgeons about what they needed. This cluster produced other pioneers: St. Jude Medical, Cardiac Pacemakers Inc., and dozens of smaller firms. The ecosystem was unique—nowhere else did surgeons invite engineers into operating rooms to watch procedures and iterate designs in real-time. This collaborative culture would become Medtronic's secret weapon.

But Bakken's most enduring contribution wasn't technological—it was cultural. In 1960, facing near-bankruptcy and pressure from investors, Bakken developed the Medtronic Mission to help the company stay focused after a near-miss with bankruptcy. Written in 1960, the mission statement has remained intact, word for word, reading in part: "To contribute to human welfare by application of biomedical engineering" in the research, design, and manufacture of instruments that "alleviate pain, restore health and extend life."

This wasn't corporate pablum—it was operational doctrine. When interviewing executives, Bakken would spend hours discussing the Mission and values, never asking about qualifications. He instituted an annual holiday party where patients told employees how Medtronic devices changed their lives. Every employee who reaches a service milestone receives a medallion inscribed with the mission's six tenets. The culture was so strong that when acquiring Covidien for nearly $50 billion, CEO Omar Ishrak insisted the deal conform to every one of the mission's six key points, successfully integrating 40,000 new employees.

Early challenges tested this mission-driven approach. The FDA, established in 1962, brought regulatory complexity that garage startups weren't equipped to handle. Medtronic had to professionalize rapidly, hiring quality engineers and regulatory specialists. Market education proved equally challenging—convincing hospitals to trust electronic devices implanted in human hearts required not just clinical data but emotional persuasion. Bakken excelled at both, bringing patients to medical conferences to share their stories.

The transition from external to implantable pacemakers marked another inflection point. In 1960, Medtronic licensed the implantable pacemaker design from Wilson Greatbatch and William Chardack, giving them exclusive rights. This device, powered by mercury-zinc batteries and hermetically sealed, could function inside the body for years. It transformed pacemakers from emergency interventions to permanent solutions. Revenue exploded from $500,000 in 1960 to $12 million by 1968.

By the late 1960s, Medtronic controlled 40% of the global pacemaker market. But success brought competition—former Medtronic engineers left to start Cardiac Pacemakers Inc., introducing lithium batteries that lasted three times longer than Medtronic's mercury cells. The garage startup had become an industry, and the industry was getting crowded. To survive, Medtronic would need to evolve beyond its pacemaker roots—setting the stage for decades of strategic diversification.

III. Building the Empire: Diversification and Global Expansion (1970s–1990s)

The morning of February 12, 1976, began like any other at Medtronic headquarters. Then the phone calls started. Doctors were reporting failures of the Xytron pacemaker—the device was shorting out prematurely, leaving patients vulnerable. The Xytron-model pacemakers began to short out early, featuring older mercury batteries rather than the latest lithium ones. Although the several hundred Xytrons that failed did not cause any deaths, they seriously damaged Medtronic's reputation. For a company whose mission centered on reliability and trust, this was an existential crisis.

The Xytron recall became a defining moment. Rather than minimize the issue, Medtronic launched an unprecedented response: tracking down every single implanted device, offering free replacements, and establishing a patient registry system that would become the industry standard. The financial hit was substantial, but the reputational recovery was swift. More importantly, the crisis catalyzed a strategic revelation: Medtronic was too dependent on pacemakers. Diversification wasn't optional—it was survival.

The pivot began with neurological devices. If electrical stimulation could regulate heartbeats, why not pain signals or muscle spasms? Medtronic's engineers began developing spinal cord stimulators, devices that intercepted pain signals before they reached the brain. The technology was crude initially—imagine wearing a car battery-sized device on your belt—but for patients with chronic pain, it offered hope where opioids had failed.

Spinal fusion represented another frontier. Working with orthopedic surgeons, Medtronic developed titanium cages and bone growth proteins that could stabilize damaged vertebrae. The acquisition of Sofamor Danek in 1999 for $3.7 billion would later cement this position, but the groundwork was laid in these experimental years when engineers literally stood in operating rooms, modifying devices between procedures.

The vascular business emerged from an observation: the same catheter technologies used to place pacemaker leads could deliver other therapies. Medtronic began developing stents, balloon catheters, and eventually drug-eluting devices that could prop open arteries while releasing medication to prevent re-blockage. Each new product line required not just R&D investment but entirely new sales forces, regulatory pathways, and manufacturing capabilities.

The company experienced impressive growth in the 1970s; sales surpassed $100m in 1975, then exceeded $200m by the end of the decade, and it was listed on the New York Stock Exchange for the first time in 1977. But growth came with growing pains. By 1980, Medtronic's earnings were on the decline. The company needed to develop more innovative and diverse products to restore their reputation and compete with newer firms. They launched a line of programmable pacemakers but were no longer the technology leaders.

The solution came through aggressive R&D investment and strategic acquisitions. Throughout the 1980s, Medtronic routinely reinvested more than 8% of annual revenues into research and development. By 1981, annual sales reached $300 million—a 50% increase in just two years. When Winston Wallin took over as CEO in 1985, he doubled the company's research spending to push innovation.

The acquisition strategy accelerated in the 1990s. In 1998, Medtronic acquired Physio-Control for $538 million, entering the external defibrillator market. This wasn't just about adding products—it was about building ecosystems. A hospital that bought Medtronic pacemakers might also need defibrillators, and eventually spinal implants. The sales force became consultants, helping hospitals design entire cardiac care units.

In November 1999, Medtronic acquired Xomed Surgical Products for approximately $800 million, adding ear, nose, and throat surgical tools to its portfolio. Each acquisition brought not just products but relationships—surgeon champions who could influence purchasing decisions and provide feedback for next-generation devices.

The international expansion during this period was equally strategic. Rather than simply exporting American products, Medtronic established local R&D centers in Japan, Europe, and eventually China. They learned that a pacemaker designed for a 200-pound American might need modification for a 120-pound Japanese patient. Cultural sensitivity extended beyond product design—in Japan, Medtronic sales reps removed their shoes when entering hospitals, a small gesture that built enormous goodwill.

By 2000, Medtronic had transformed from a pacemaker company into a diversified medical technology conglomerate with revenue approaching $5 billion. The company operated in over 120 countries, held thousands of patents, and touched millions of patients annually. But the most ambitious acquisition was yet to come—one that would thrust Medtronic into an entirely new therapeutic area and test whether its integration capabilities could handle a true merger of equals.

IV. The MiniMed Acquisition & Diabetes Revolution (2001)

Alfred Mann was not your typical entrepreneur. A physicist-turned-businessman who'd already built and sold several companies for billions, Mann had become obsessed with a problem that affected millions yet seemed technologically solvable: managing Type 1 diabetes. His company, MiniMed, had pioneered the insulin pump—a beeper-sized device that delivered precise insulin doses throughout the day, freeing diabetics from multiple daily injections. When Medtronic acquired MiniMed in 2001 for $3.8 billion, it wasn't just buying a product line. It was buying entry into a $30 billion global diabetes market and, more ambitiously, pursuing the dream of an "artificial pancreas."

The insulin pump revolution that Mann championed was elegantly simple in concept, fiendishly complex in execution. Instead of diabetics guessing their insulin needs and injecting large boluses that created dangerous peaks and valleys in blood sugar, the pump delivered a continuous basal rate with additional boluses for meals. Users could finally eat pizza at 10 PM without risking a 3 AM hypoglycemic crisis. For children with diabetes, it meant parents could sleep through the night without fear.

But pumps were only half the equation. Without knowing blood glucose levels in real-time, users were still flying blind—pricking their fingers 6-10 times daily for snapshots of a constantly changing landscape. Medtronic's next move was acquiring the continuous glucose monitoring (CGM) technology that could provide readings every five minutes. Suddenly, patients could see not just where their blood sugar was, but where it was heading. The CGM would alarm before dangerous highs or lows, giving users time to intervene.

Building this ecosystem required overcoming staggering technical challenges. The human body actively rejects foreign objects, coating implanted sensors with proteins that degrade accuracy within days. Medtronic's engineers developed biocompatible membranes and algorithmic corrections that extended sensor life to a week. They miniaturized electronics to the point where the entire system—pump, CGM, and wireless communication—weighed less than a smartphone.

The integration challenges were equally daunting. MiniMed had its own culture, distribution network, and rabidly loyal customer base who viewed their pumps as life-sustaining partners, not mere medical devices. Medtronic couldn't simply absorb MiniMed; it had to preserve what made it special while leveraging Medtronic's global scale and regulatory expertise. The breakthrough came in September 2016 when the FDA approved Medtronic's MiniMed 670G hybrid closed loop system—the first FDA-approved "artificial pancreas" device for people with type 1 diabetes. The MiniMed 670G calculates how much insulin to infuse using a sensor that takes blood sugar readings every five minutes, adapting to blood sugar changes during exercise and illness. The device represented the culmination of 15 years of development since the MiniMed acquisition.

The clinical results were impressive: Medtronic's results show that the MiniMed 670G kept people with type 1 diabetes within their target blood sugar range 72% of the time compared with 67% without the system, with overall glucose control improving as shown by a drop in HbA1c levels from 7.4% to 6.9%. Of the 124 people in the trial, a striking 80% opted to continue using the device through the FDA's continued access program—demonstrating remarkable patient satisfaction.

But success brought scrutiny. The device still required manual bolusing for meals, making it a "hybrid" rather than fully closed-loop system. Competitors like Tandem, Insulet, and Beta Bionics were developing their own automated insulin delivery systems. Most concerning, continuous glucose monitors remained the weak link—requiring multiple daily calibrations and failing unpredictably, forcing the system back to manual mode.

The business model challenges were equally complex. Unlike a one-time pacemaker implant, diabetes management required continuous supplies—sensors every week, infusion sets every three days, insulin daily. This created predictable recurring revenue but also meant managing complex supply chains and insurance reimbursements across thousands of payers with different coverage policies.

By 2024, the diabetes business had grown to over $2 billion in annual revenue but faced mounting pressures. Digital health startups were unbundling the market, offering standalone CGMs and smart insulin pens at lower prices. The very success of continuous glucose monitoring had commoditized the technology, with competitors offering longer-lasting, more accurate sensors that didn't require fingerstick calibrations.

The strategic response would be dramatic: spinning off the entire diabetes business as a standalone company, returning to the MiniMed name. This wasn't retreat but recognition that diabetes care had evolved into a consumer-driven, software-centric market requiring different capabilities than Medtronic's traditional device business. The spinoff, planned for completion in fiscal 2025, would allow the new MiniMed to move at startup speed while Medtronic focused on its higher-margin surgical and cardiac businesses. The artificial pancreas dream lived on, just under different ownership.

V. The Omar Ishrak Era: Global Transformation (2011–2020)

When Omar Ishrak walked into Medtronic headquarters in June 2011, he faced a paradox. The company was wildly successful—$16 billion in revenue, market leadership across multiple categories—yet somehow stuck. Growth had slowed to low single digits. The stock price had flatlined for a decade. Most troubling, Medtronic was losing relevance in emerging markets that would drive healthcare's future. Omar Ishrak, who became CEO in 2011, is the strongest advocate for the mission. When the company was acquiring Covidien for nearly $50 billion, he insisted that first the deal had to conform to every one of the mission's six key points

Ishrak came from General Electric Healthcare with a clear mandate: transform Medtronic from an American medical device company that happened to sell internationally into a truly global healthcare solutions provider.

The numbers told the story. Since joining Medtronic, Omar focused the company on three core strategies of Therapy Innovation, Economic Value and Globalization. These weren't just buzzwords—they represented a fundamental reimagining of how a $16 billion company would compete in a rapidly consolidating, cost-conscious healthcare market.

Ishrak restructured his executive team: the heads of Medtronic's global operating regions now report directly to the CEO, putting seven non-Americans on the executive committee. This wasn't window dressing. For the first time, decision-makers from Europe, Asia, and Latin America had equal seats at the table with their American counterparts. Product development shifted from Minneapolis-centric to globally distributed, with R&D centers established in Shanghai, São Paulo, and Hyderabad.

Medtronic acquired a Chinese orthopedics company, which became its first fully integrated business unit outside the U.S. This acquisition, Kanghui Holdings, wasn't about importing American products to China—it was about developing products in China for China and eventually the world. The trauma devices designed in Beijing cost 40% less than their American equivalents while maintaining comparable quality, creating a reverse innovation model that could eventually disrupt Medtronic's own premium products.

The value-based healthcare pivot represented perhaps Ishrak's boldest strategic shift. Ishrak led Medtronic through the largest acquisition in med-tech history, redefined the company's growth strategy, inspired it to embrace value-based healthcare (VBHC), and strengthened its position in emerging markets. Rather than simply selling devices, Medtronic began partnering with hospitals to manage entire service lines. In diabetic care, they guaranteed outcomes—if patients didn't achieve target HbA1c levels, Medtronic would refund device costs. This required not just selling pumps but providing education, monitoring, and intervention services.

The economic value strategy meant competing on total cost of ownership, not just device price. A Medtronic spinal implant might cost more upfront, but if it reduced surgical time by 30 minutes and hospital stays by two days, the total economic benefit was compelling. Sales representatives became health economics consultants, armed with spreadsheets showing five-year ROI calculations.

During his time as CEO, Medtronic established prominent research and development centers in regions such as China. These weren't just assembly plants but true innovation hubs. The Shanghai facility developed a pacemaker specifically for Asian physiology—smaller, with different pacing algorithms optimized for lower body mass. Within three years, it captured 30% of the Chinese market previously dominated by local competitors.

By 2014, Ishrak's transformation was gaining momentum but faced a ceiling. Organic growth remained stubbornly in the mid-single digits. Breaking through would require something dramatic—a transformation so bold it would fundamentally alter Medtronic's DNA. That opportunity would come in the form of Covidien, setting the stage for the most controversial deal in medtech history.

VI. The Covidien Mega-Merger: Tax Inversion Drama (2014–2015)

Back in 2014, Medtronic was three years into the leadership of Omar Ishrak and looking at what was coming down the pipeline. There were enough problems in the healthcare space that Medtronic leaders felt they couldn't solve them with the company as it was. That model was still very transactional, and "we wanted to get at something much deeper in terms of meeting patient needs."

The courtship began over dinner. Covidien CEO Joe Almeida called Ishrak and said he was going to be in the area and wanted to go to dinner. Both companies had independently concluded that scale was destiny in the new healthcare landscape. Hospitals were consolidating, demanding bundled pricing across entire procedures. Standalone device companies couldn't compete with integrated solutions providers.

Medtronic announced that it has agreed to acquire Irish medtech firm Covidien for $42.9 billion in cash and stock. The purchase is the largest acquisition of a foreign firm by a U.S. company. The scale was staggering—creating a company with combined revenues approaching $30 billion, 87,000 employees, and market leadership across cardiac, spinal, surgical, and vascular markets.

But the structure of the deal ignited a firestorm. It was purchased by Medtronic in a transaction that closed in 2015. The now-merged company is headquartered in Ireland, where Covidien was based. This "inversion"—where an American company redomiciles abroad through acquisition—would lower Medtronic's tax rate from 35% to approximately 20%, saving billions over time.

Martha approached Medtronic's board and began laying out the possibilities of making an acquisition of a large medical company that would provide the needed breadth. "The board had started to warm to the idea, but we hadn't settled on anything." Covidien, he noted, was on the top of the list.

The political backlash was swift and brutal. By early August it was becoming increasingly obvious that President Barack Obama and other progressive politicians didn't approve of the Medtronic deal. It is but another indication that President Obama clearly doesn't like Medtronic's plan to move its headquarters to Ireland through the purchase. Senator Carl Levin called it "outrageous," accusing Medtronic of abandoning the country that nurtured its growth.

News came out that Medtronic had paid $200,000 to lobbyists including former U.S. Sens. Trent Lott and John Breaux to handle issues in Congress over the deal. In the first half of 2014, Medtronic has spent $2.84 million on lobbying fees--placing it on track to beat the $5.02 million it spent on lobbying last year.

The company desperately tried to reframe the narrative. Medtronic CEO Omar Ishrak defended the Covidien purchase: "the structure with Covidien was first and primarily driven by strategy from a healthcare perspective, in that together we could provide more value to the healthcare system and be a much more effective combination."

Indeed, the strategic logic was compelling. Covidien brought surgical staplers, energy devices, and respiratory products that complemented Medtronic's portfolio perfectly. A cardiac surgeon could now get pacemakers, surgical tools, and monitoring equipment from a single vendor. The combined company could offer hospitals complete "solutions"—from diagnosis through treatment to monitoring.

But shareholders faced their own drama. The deal would cause the shareholders to exchange their present stock for stock in the new Ireland-based Medtronic plc, and in the process they would be stuck with a surprise capital gains tax on all the extra value the stock gained over the decades. Long-term investors who'd held stock since the 1970s faced massive tax bills, creating revolt at the annual meeting.

The integration challenges proved equally complex. Martha said he thinks they took Medtronic and Covidien employees by surprise by announcing that every job was up for discussion. "We were looking for ambassador behavior, and we had a lot of respect for both teams." "To be frank, we didn't want people who took their positions for granted."

Rather than forcing Covidien into Medtronic's culture, leadership took an unprecedented approach. Instead of making big announcements, Medtronic's leadership presented "Mission Day," where it broke into groups and talked about the Medtronic mission statement. "That first day was a day of reflection and contemplative thought," Wall said. "We knew we wanted to retain the Medtronic name and the mission. What we really cared about was sharing that sense of purpose."

The two companies outlined more than $850 million in annual savings to be fully achieved by the end of Medtronic's 2018 fiscal year. These synergies would come from eliminating duplicate functions, optimizing supply chains, and leveraging combined purchasing power.

The regulatory scrutiny was intense. Global medical technology company Medtronic, Inc. has agreed to divest the drug-coated balloon catheter business of Ireland-based medical products company Covidien plc, in order to settle Federal Trade Commission charges that its $42.9 billion acquisition of Covidien would likely be anticompetitive. The FTC required this divestiture to preserve competition in the emerging drug-coated balloon market.

When the deal finally closed in January 2015, Medtronic had fundamentally transformed. The combined entity was now the undisputed leader in medical devices, with number one or two positions in virtually every market it competed in. The tax savings, while controversial, provided billions for R&D investment. Most importantly, the scale and scope positioned Medtronic to compete with anyone—from J&J to emerging tech giants eyeing healthcare.

But the inversion would cast a long shadow. Political pressure led to Treasury rule changes making future inversions nearly impossible. Medtronic faced ongoing scrutiny about its tax practices and "American-ness." The company that Earl Bakken built in a Minneapolis garage was now, legally at least, Irish. The strategic benefits were clear, but the reputational costs would linger for years.

VII. The Robot Surgery Revolution: Hugo's Long Journey

The conference room at Medtronic's Minneapolis campus fell silent as executives watched the video feed from Milan. On the screen, a surgeon manipulated controls while robotic arms performed delicate sutures on a patient hundreds of miles away. It was 2019, and Medtronic's Hugo robotic surgery system was finally becoming reality—nearly a decade after the company first identified surgical robotics as a must-win battlefield.

The journey to Hugo began with a sobering realization: Intuitive Surgical's da Vinci system had achieved something rare in medical devices—a true monopoly. With over 5,000 systems installed globally and surgeons trained exclusively on their platform, da Vinci had created switching costs so high that hospitals couldn't abandon them even when cheaper alternatives emerged. Medtronic needed a robot, but more importantly, it needed a strategy to crack Intuitive's fortress.

The company further expanded into minimally invasive surgical robotics with its Hugo™ RAS platform, strengthening its footprint across multiple specialties. Hugo's design philosophy was deliberately different from da Vinci. Where Intuitive built a massive, integrated system, Hugo was modular—individual robotic arms that could be positioned independently around the patient. This wasn't just about flexibility; it was about economics. Hospitals could start with two arms for simple procedures and add more as volumes grew.

The technology challenges were staggering. Robotic surgery demands sub-millimeter precision, zero latency between surgeon movement and robot response, and fail-safes that prevent any possibility of unintended movement. Medtronic's engineers spent years perfecting haptic feedback systems that could transmit the sensation of tissue resistance back to the surgeon's hands—something da Vinci still lacked.

The company was awarded a CE mark for Hugo in October 2021. The European launch became Medtronic's proving ground. Rather than competing head-to-head with da Vinci in prostatectomies where Intuitive dominated, Medtronic targeted hernia repairs and colorectal procedures where robotic adoption was still nascent.

The data that emerged was compelling. Hugo demonstrating a 98.5% surgical success rate and favorable complication data in the Expand URO study. Surgeons reported that Hugo's open console design—unlike da Vinci's enclosed viewer—allowed better communication with surgical teams. The system's AI-powered analytics could track every movement, creating personalized training programs that accelerated the learning curve.

But the U.S. market remained the prize, and the FDA approval process proved grueling. Medtronic submitted its Hugo™ robotic-assisted surgery system to the FDA in Q1 2025, with an initial focus on urologic procedures like prostatectomies and nephrectomies. The submission represented seven years of development, thousands of procedures in international markets, and an investment approaching $1 billion.

Hugo is positioned as a modular, cost-effective alternative to Intuitive Surgical's da Vinci®, offering AI-powered analytics, flexible system setup, and an open console for greater surgeon communication. The value proposition extended beyond hardware. Medtronic's Touch Surgery digital platform could simulate procedures, track outcomes, and connect surgeons globally for training and collaboration. This ecosystem approach—combining robots, software, and services—aimed to lower the total cost of robotic surgery by 20-30%.

The competitive dynamics were shifting rapidly. While Medtronic developed Hugo, Johnson & Johnson partnered with Google's Verily for their Ottava system, CMR Surgical raised hundreds of millions for their Versius robot, and Intuitive launched their smaller, single-port SP system. The robotic surgery market, monopolistic for two decades, was suddenly crowded.

Medtronic's strategy relied on leveraging its unique advantages: global scale, existing hospital relationships, and complementary products. A hospital buying Hugo could bundle it with Medtronic's surgical staplers, energy devices, and monitoring systems—creating economic incentives Intuitive couldn't match. The company's 5,000-person surgical sales force, already calling on every major hospital globally, provided distribution muscle that startups couldn't replicate.

The international rollout data provided reasons for optimism. In India, where price sensitivity limited da Vinci adoption, Hugo procedures grew 300% year-over-year. European teaching hospitals began incorporating Hugo into residency programs, creating a new generation of surgeons not locked into the da Vinci ecosystem. Most tellingly, several large American hospital systems signed letters of intent pending FDA approval, signaling pent-up demand for competition.

Yet challenges remained formidable. Intuitive's installed base generated recurring revenue from instruments and service contracts exceeding $3 billion annually—cash flow they could deploy to defend their position. Their newest Xi system incorporated many of Hugo's advantages while maintaining backward compatibility with the thousands of surgeons already trained on da Vinci. Most dauntingly, Intuitive had filed over 3,000 patents covering everything from robotic wrist mechanics to surgical visualization, creating a legal minefield for competitors.

The stakes for Medtronic couldn't be higher. Robotic surgery represents one of the fastest-growing segments in medical devices, expected to reach $20 billion by 2030. Success with Hugo would validate Medtronic's ability to disrupt entrenched markets and innovate at the technological frontier. Failure would confirm critics' views that the company had become too large and bureaucratic to compete with focused innovators.

As 2025 progresses, Hugo stands at an inflection point. FDA approval appears imminent, major hospital systems are preparing for installations, and the surgical community watches eagerly for a viable alternative to da Vinci's monopoly. Whether Hugo becomes Medtronic's next billion-dollar platform or an expensive lesson in the challenges of late entry remains to be determined. But one thing is certain: the robot surgery revolution that Intuitive started alone will be completed by an increasingly crowded field, with Medtronic determined to claim its share.

VIII. Recent Inflection Points & Strategic Pivots (2020–Present)

We have doubled the size of the company across many measures and have more than tripled its valuation. Today, we have far exceeded that goal, improving the lives of more than 75 million patients last year alone — that's two people every second. These were among Omar Ishrak's parting words as he handed leadership to Geoff Martha in April 2020—a transition that would mark the beginning of Medtronic's most ambitious restructuring in decades.

Martha inherited a paradox: a company that dominated multiple markets yet consistently underperformed investor expectations. The stock had barely moved in five years despite revenues growing to $30 billion. The diagnosis was clear: Medtronic had become too complex, too slow, and too wedded to mature markets growing at GDP rates. Martha's prescription would be radical surgery on the company itself.

The pandemic provided both crisis and clarity. Ventilator demand spiked 10-fold overnight, testing Medtronic's manufacturing agility. The company partnered with Tesla and SpaceX to increase production, sharing ventilator designs open-source—a decision that cost nothing but generated enormous goodwill. More importantly, COVID exposed healthcare's fragility and accelerated trends Martha had been tracking: procedure backlogs, hospital financial distress, and the desperate need for efficiency.

Martha's strategic pivot centered on three decisions that would have been unthinkable under previous leadership. First, portfolio optimization—admitting that not all businesses deserved equal investment. Second, embracing external innovation through partnerships rather than acquisitions. Third, and most dramatically, spinning off underperforming assets even if they were historically core to Medtronic's identity.

The diabetes spinoff announcement shocked the industry. MiniMed had been Medtronic's entry into chronic disease management, a $2 billion business with millions of loyal patients. But continuous glucose monitoring had commoditized, and digital health competitors were unbundling the market. Rather than pour resources into a battle against Dexcom and Abbott, Martha chose to set the business free as a standalone company, allowing it to move at startup speed while Medtronic focused on higher-margin surgical and cardiac businesses.

The cardiac ablation transformation demonstrated what focused execution could achieve. Pulsed field ablation (PFA) technology had languished in development for years, but Martha accelerated investment and streamlined decision-making. The result: Medtronic's cardiac ablation solutions became a $1 billion business in fiscal 2025, with clear line of sight to $2 billion as physicians embraced PFA over traditional radiofrequency and cryoablation for treating atrial fibrillation. The technology reduced procedure times by 40% while improving safety profiles—exactly the type of value proposition hospitals demanded.

Another breakthrough came from an unexpected source: renal denervation. After a decade of false starts, Medtronic's Symplicity system finally demonstrated that ablating nerves around kidney arteries could reduce blood pressure in patients resistant to medication. When CMS announced coverage for renal denervation in October 2025, it opened a $5 billion market opportunity. The therapy could help 20% of hypertension patients who don't respond to drugs—potentially preventing thousands of strokes and heart attacks annually.

The appearance of Elliott Investment Management as an activist investor initially seemed like Martha's nightmare scenario. The hedge fund, known for aggressive tactics, had taken a significant position and was reportedly preparing to demand board seats and asset sales. But Martha's preemptive moves—the diabetes spinoff, operational improvements yielding 50 basis points of margin expansion, and clear communication about long-term strategy—largely defused Elliott's critiques. The appointment of Megan Groetelaars, with her three decades of operational experience, to the board signaled responsiveness to shareholder concerns without capitulating to short-term pressures.

Digital transformation, long discussed but slowly implemented, suddenly accelerated. The FDA's pandemic-era flexibility around remote monitoring created opportunities Medtronic seized aggressively. The company's cardiac devices now transmit data continuously to physicians, with AI algorithms detecting anomalies before patients experience symptoms. Surgical planning software could simulate procedures on patient-specific anatomy, reducing OR time and improving outcomes. These weren't just features—they were becoming competitive requirements.

Supply chain resilience, exposed as a critical vulnerability during COVID, received massive investment. Medtronic diversified suppliers, regionalized production, and built strategic inventory buffers. The company's ability to maintain device availability while competitors faced shortages became a powerful differentiator, particularly in critical care products where switching costs were high.

The financial results validated Martha's strategy. In fiscal 2025, Medtronic raised diluted non-GAAP EPS guidance to represent growth in the range of 4.6% to 5.8%—exceeding analyst expectations despite currency headwinds and inflation. More importantly, the company's multiple began expanding as investors recognized improving capital allocation and clearer strategic focus.

But challenges remained formidable. Integration of AI and machine learning into medical devices faced regulatory uncertainty—the FDA struggled to create frameworks for continuously learning algorithms. Competition from tech giants intensified as Apple's health features, Google's AI capabilities, and Amazon's healthcare ambitions encroached on traditional medtech territory. Most concerning, procedure volumes hadn't fully recovered to pre-pandemic levels as patients deferred elective surgeries and hospitals faced staffing shortages.

The partnership with Nvidia on AI-powered surgical video analysis demonstrated Medtronic's evolved innovation approach. Rather than spending years developing proprietary computer vision, Medtronic licensed Nvidia's Clara platform and focused on clinical applications. Early results showed AI could reduce surgical errors by identifying critical structures and alerting surgeons to potential complications—capabilities that could fundamentally change surgical training and quality assurance.

As 2025 progresses, Martha's transformation appears to be gaining momentum. The company that once tried to be everything to everyone in medical devices is becoming more focused, more agile, and more profitable. The upcoming Hugo U.S. launch, renal denervation commercialization, and continued PFA adoption provide near-term catalysts. But the ultimate test remains whether a $90 billion company can consistently innovate at the pace of startups while maintaining the quality and reliability that defined Medtronic for 75 years.

IX. Playbook: Strategy & Investment Lessons

The Medtronic story offers a masterclass in how to build, scale, and continuously reinvent a technology company in one of the world's most regulated industries. The playbook that emerged from 75 years of evolution contains lessons that transcend medical devices, offering insights for any company navigating complex markets, technological disruption, and stakeholder capitalism.

The Mission as Competitive Moat

Medtronic's mission—written in 1960 and unchanged since—serves as more than inspirational decoration. It functions as an operational filter for decision-making at every level. When evaluating the $43 billion Covidien acquisition, executives spent months ensuring alignment with all six mission tenets before discussing financials. This mission-driven culture creates unique advantages: lower employee turnover (saving hundreds of millions in training costs), deeper physician relationships (doctors trust Medtronic's motivations), and resilience during crises (employees accept short-term sacrifice for long-term purpose).

The mission also provides strategic clarity in portfolio decisions. When activist investors push for higher margins through R&D cuts, management can point to the mission's mandate to "maintain good citizenship." When choosing between markets, those serving underserved populations receive priority even if returns are lower. This consistency builds trust with stakeholders who know Medtronic's decisions, while profit-motivated, consider broader impact.

Serial Acquisition as Capability Building

Medtronic has completed over 100 acquisitions, from small technology tuck-ins to massive transformational deals. The company's M&A playbook has evolved into a sophisticated capability that few can match. Due diligence goes beyond financials to assess cultural fit—deals have been killed despite compelling economics because values didn't align. Integration begins before closing, with teams identifying key talent to retain and planning system migrations.

The company learned expensive lessons about acquisition integration. Early deals often destroyed value by forcing acquired companies into Medtronic's processes, losing entrepreneurial energy. Modern acquisitions maintain operational independence longer, allowing innovation to flourish before gradual integration. The Covidien merger's "merger of equals" approach—where every position was reconsidered regardless of legacy company—became the model for maintaining meritocracy during integration.

Critical to acquisition success is Medtronic's ability to globalize products rapidly. A technology acquired from an Israeli startup can be manufactured in Puerto Rico, distributed through European channels, and serviced by teams in Asia within 18 months. This global infrastructure multiplies the value of acquisitions by 3-5x compared to standalone growth potential.

Platform Thinking in Ecosystem Age

Medtronic's evolution from product to platform thinking represents a fundamental strategic shift. Rather than selling individual devices, the company builds ecosystems where products, services, and software reinforce each other. The cardiac rhythm management platform includes pacemakers, defibrillators, monitoring systems, and AI-powered analytics—each component increasing the value of others.

This platform approach creates powerful network effects. Hospitals investing in Medtronic's surgical robots want compatible staplers and energy devices. Physicians trained on one Medtronic system are more likely to adopt others. Data from millions of devices feeds algorithms that improve future products. Competitors can match individual products but struggle to replicate entire ecosystems.

The economic model of platforms differs fundamentally from products. Initial devices might be sold at breakeven to establish installed base, with profits coming from consumables, software subscriptions, and services. This razor-and-blade model provides predictable, recurring revenue that smooths cyclical device purchases. It also increases switching costs—hospitals won't abandon platforms requiring extensive retraining and system integration.

Regulatory Complexity as Competitive Advantage

Operating in 150+ countries means navigating thousands of regulatory requirements, from FDA's 510(k) process to CE marking in Europe to NMPA approval in China. What seems like burden becomes barrier to entry—startups can't easily replicate Medtronic's regulatory expertise built over decades. The company maintains relationships with regulators globally, often helping shape new frameworks for emerging technologies.

Medtronic's regulatory affairs team of 2,000+ professionals doesn't just ensure compliance—they accelerate innovation. By engaging regulators early in development, the company can influence standards and clear pathways for novel technologies. When developing Hugo, Medtronic worked with European regulators to establish robotic surgery guidelines that became industry standards, advantaging their own submission while appearing collaborative.

The company's quality systems, refined through recalls and warning letters, now represent best practices. ISO 13485 certification, once table stakes, becomes differentiator when executed at Medtronic's scale and consistency. Hospitals and group purchasing organizations increasingly require supplier quality certifications that eliminate smaller competitors unable to meet standards.

Capital Allocation Discipline

Managing capital allocation for a $30 billion revenue company requires sophisticated frameworks balancing growth investment, shareholder returns, and strategic flexibility. Medtronic's approach segments investments into three categories: sustaining (maintaining existing franchises), emerging (scaling new platforms), and disruptive (long-term bets). Each category has different return thresholds and time horizons.

The company maintains R&D intensity around 8% of sales—roughly $2.4 billion annually. This seemingly fixed percentage actually represents dynamic allocation as management shifts resources between therapeutic areas based on opportunity. Surgical robotics received increased investment by reducing spending on mature pacemaker lines. Digital health initiatives funded by optimizing manufacturing efficiency.

Shareholder returns follow clear principles: dividend growth matching earnings growth, share buybacks when valuations compress, and major acquisitions only when strategic rationale overwhelming. The company's 45-year dividend growth streak provides stability that attracts long-term investors, reducing stock volatility and cost of capital. This patient capital enables long-term investments in platforms like Hugo that require years before profitability.

The Scale Paradox

At $90 billion market cap, Medtronic faces the classic innovator's dilemma: size provides resources but reduces agility. The company addresses this through portfolio management—divesting subscale businesses (like diabetes) to focus resources on leadership positions. "Big enough to win, focused enough to innovate" becomes the strategic filter.

Organizational structure balances global scale with local autonomy. Business units operate independently with P&L responsibility while sharing global functions like manufacturing and distribution. This hub-and-spoke model captures economies of scale without bureaucratic paralysis. Innovation happens at edges (business units) while core (corporate) provides infrastructure.

The company increasingly partners rather than acquires, recognizing that ownership isn't required for value creation. Collaborations with Nvidia (AI), IBM (quantum computing), and various startups provide access to innovation without integration complexity. These partnerships move at startup speed while leveraging Medtronic's commercialization capabilities—combining entrepreneurial innovation with corporate execution.

X. Bear vs. Bull Case Analysis

Bear Case: The Incumbent's Dilemma

The bearish perspective on Medtronic begins with a sobering reality: the company's stock has underperformed the S&P 500 for the past decade despite operating in supposedly high-growth medical technology markets. This isn't a temporary setback but potentially a structural problem reflecting fundamental challenges that no amount of restructuring can solve.

Size has become Medtronic's anchor. At $30 billion in revenue, generating even 5% organic growth requires adding $1.5 billion in new sales annually—equivalent to creating a mid-sized medtech company every year. The law of large numbers makes maintaining historical growth rates mathematically impossible. Worse, the company's breadth across dozens of product lines means management attention is perpetually divided, preventing the focused execution that drives breakthrough innovation.

Competition has intensified from every direction. Nimble startups unbundle Medtronic's integrated offerings with point solutions—Dexcom in CGM, Inspire Medical in sleep apnea, Nevro in spinal cord stimulation. These focused competitors move faster, iterate quicker, and capture the most attractive segments of markets Medtronic once dominated. Meanwhile, tech giants bring unlimited resources and software expertise that makes Medtronic's engineering prowess less differentiated. When Apple can turn a watch into a medical device that captures cardiology data, what's the value of Medtronic's traditional hardware?

The regulatory environment that once protected incumbents now accelerates disruption. FDA's Digital Health Software Precertification Program allows software-based competitors to update products continuously while Medtronic navigates traditional device pathways. European MDR regulations increase compliance costs disproportionately for companies with broad portfolios. China's volume-based procurement drives commoditization of once-profitable products.

Healthcare system evolution threatens Medtronic's business model. Value-based care shifts focus from selling devices to delivering outcomes—a transition requiring capabilities in data analytics, care coordination, and risk management that Medtronic lacks. Hospital consolidation creates mega-systems with procurement power that compresses margins. Ambulatory surgery centers prefer lower-cost alternatives to Medtronic's premium products designed for hospital operating rooms.

Integration challenges from serial acquisitions compound these pressures. The Covidien merger, five years later, still hasn't delivered promised synergies. Cultural integration remains incomplete with parallel organizations maintaining separate systems and processes. The diabetes spinoff admission that integration failed suggests similar issues lurk in other acquisitions. How many billions in acquired revenue are actually destroying value through complexity costs?

Technological disruption looms larger than ever. AI-driven drug discovery might eliminate the need for many medical devices by curing rather than managing diseases. 3D printing enables hospitals to manufacture certain implants on-site, disintermediating device companies. Robotics commoditization—as happened with industrial robots—would destroy Hugo's premium pricing power. Most threateningly, the convergence of technology and healthcare favors software-native companies over hardware-centric Medtronic.

Bull Case: The Platform Advantage

The bullish thesis rests on a different interpretation of the same facts: Medtronic's challenges are temporary while its advantages are structural. The company sits at the intersection of powerful secular trends that virtually guarantee long-term growth regardless of short-term volatility.

Demographics alone make Medtronic's growth inevitable. By 2050, the global population over 65 will triple to 2.1 billion people. These aging populations don't just need more healthcare—they need exactly the interventions Medtronic specializes in: cardiac rhythm management, spinal surgery, diabetes care. In the U.S. alone, 10,000 people turn 65 daily, entering peak years for device-intensive procedures. This demographic tsunami will drive procedural volumes regardless of economic cycles or competitive dynamics.

Medtronic's scale, rather than burden, provides unmatched competitive advantages. The company's global footprint allows geographic diversification that smooths regional volatility. Its broad portfolio enables bundled contracting that standalone competitors can't match. Most importantly, Medtronic's infrastructure—regulatory expertise, manufacturing capabilities, distribution networks—would cost competitors tens of billions and decades to replicate.

The innovation pipeline suggests acceleration, not stagnation. Hugo's entry into the $20 billion robotic surgery market could add $2-3 billion in revenue within five years. Renal denervation opens an entirely new $5 billion therapeutic area. The company's cardiac ablation solutions would become a $1 billion business in its fiscal 2025 year, with "line of sight" to $2 billion as the PFA portfolio grows. These aren't incremental improvements but platform-level innovations that create new markets.

Value-based healthcare, while challenging, ultimately favors integrated solution providers like Medtronic. Hospitals need partners who can guarantee outcomes across entire care pathways, not just provide point products. Medtronic's ability to combine devices, software, and services into outcome-based contracts creates competitive moats that pure-play device companies can't cross. The company's 95,000 employees include clinical specialists, health economists, and data scientists—capabilities that took decades to build and can't be easily replicated.

Financial strength provides strategic flexibility that bears underestimate. With investment-grade credit ratings and $10 billion in free cash flow annually, Medtronic can invest through cycles, acquire breakthrough technologies, and return cash to shareholders simultaneously. The dividend, raised annually for 45 years, attracts patient capital that enables long-term thinking. This financial fortress means Medtronic can weather any storm while competitors struggle for survival.

The guidance raise tells the real story. The company raised its FY25 diluted non-GAAP EPS guidance representing growth in the range of 4.6% to 5.8%. This isn't the guidance of a company in structural decline but one hitting inflection points across multiple growth drivers. Management's confidence in raising guidance despite macro headwinds suggests underlying business momentum that bearish narratives miss.

Most compellingly, healthcare's $4 trillion global spending remains radically inefficient, creating massive opportunities for companies that can drive better outcomes at lower costs. Medtronic's combination of clinical expertise, technological innovation, and global scale positions it uniquely to capture this value creation. While bears focus on quarterly misses, bulls see a company engineering solutions for humanity's most pressing health challenges—and getting paid handsomely for it.

XI. Epilogue: The Next Chapter

As Earl Bakken's garage fades into history and Medtronic approaches its 80th anniversary, the company stands at perhaps its most pivotal crossroads. The decisions made in the next few years will determine whether Medtronic remains a defining force in global healthcare or becomes a cautionary tale of how giants fall.

The MiniMed spinoff represents more than portfolio optimization—it's an acknowledgment that Medtronic's future requires focus rather than breadth. By liberating the diabetes business to compete as a standalone entity, management signals willingness to sacrifice sacred cows for strategic clarity. This won't be the last divestiture. Businesses that can't achieve market leadership or generate returns above cost of capital will find new owners, regardless of historical significance.

Hugo's U.S. launch in 2025-2026 will test whether Medtronic can still disrupt established markets. Success would validate the company's innovation capabilities and provide a platform for decades of growth. Failure would confirm skeptics' views that Medtronic has become too slow and bureaucratic to compete with focused innovators. The stakes—both financial and reputational—couldn't be higher.

AI transformation will separate tomorrow's winners from losers. Medtronic's partnership approach—collaborating with Nvidia, Microsoft, and others rather than building proprietary AI—shows pragmatic recognition that competitive advantage comes from clinical application, not algorithmic development. The company's vast data assets—billions of hours of surgical footage, decades of patient outcomes, real-world device performance—become invaluable training sets for AI systems that could revolutionize everything from surgical planning to predictive diagnostics.

The value-based care transition accelerates regardless of regulatory changes. Medtronic's evolution from device manufacturer to healthcare solutions provider positions it to capture value in this new paradigm. Imagine Medtronic guaranteeing stroke reduction rates for health systems, with payment tied to population outcomes rather than device sales. This transformation requires capabilities beyond engineering—risk management, care coordination, behavioral change—that Medtronic is building through partnerships and acquisitions.

Geographic expansion, particularly in emerging markets, offers the clearest growth pathway. As China, India, and Southeast Asia build healthcare infrastructure, they need partners who can provide not just products but entire systems. Medtronic's ability to train surgeons, design hospitals, and finance equipment purchases makes it indispensable to healthcare development. These markets will drive the next decade of growth as developed markets mature.

Yet fundamental questions remain unanswered. Can a $90 billion company maintain the innovation velocity needed to compete with startups? Will Medtronic's mission-driven culture survive as financial pressures intensify and activist investors demand higher returns? How will the company navigate the increasing politicization of healthcare as governments worldwide grapple with unsustainable costs?

The answer likely lies not in choosing between competing priorities but in transcending them. Medtronic must be both global and local, both innovative and reliable, both profitable and purposeful. This isn't corporate doublespeak but recognition that 21st-century healthcare demands paradoxical capabilities. Companies that can't hold multiple truths simultaneously will be forced to choose—and any single choice will prove insufficient.

Looking ahead, three scenarios seem plausible. In the optimistic case, Medtronic successfully transforms into a platform-based, AI-powered healthcare solutions company that leads the value-based care revolution while maintaining innovation leadership. The stock re-rates to reflect this transformation, potentially doubling within five years.

The pessimistic scenario sees continued share loss to focused competitors, failed product launches like Hugo disappointing expectations, and activist investors forcing breakup into separate companies that are acquired by private equity or strategic buyers. Medtronic as an independent entity ceases to exist by 2030.

The most likely path lies between these extremes. Medtronic muddles through—growing slowly but steadily, innovating incrementally rather than disruptively, generating solid if unspectacular returns. The company remains important but not essential, profitable but not transformational. This wouldn't be failure, but it wouldn't be the kind of success that Earl Bakken envisioned when he wrote about "alleviating pain, restoring health, and extending life."

The ultimate judgment of Medtronic's next chapter won't come from Wall Street analysts or technology journalists but from the patients whose lives hang in the balance. Every day, two people per second are touched by a Medtronic device. Whether that number grows or shrinks, whether those touches become more meaningful or more routine, whether Medtronic engineers tomorrow's health or simply manages today's diseases—these are the questions that will define not just a company but an industry's ability to serve humanity's most fundamental need.

The garage startup that became a global giant has proven remarkably adaptable across seven decades of technological and social change. Whether that adaptability extends into an eighth decade depends on choices being made today in boardrooms from Minneapolis to Dublin, in operating theaters from Mumbai to São Paulo, and in research labs from Shanghai to Tel Aviv. The story of Medtronic's future is still being written, and its ending remains gloriously uncertain.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube