Klarna: The BNPL Pioneer That Bet Everything on AI

I. Introduction: From Stockholm Rejection to Wall Street Redemption

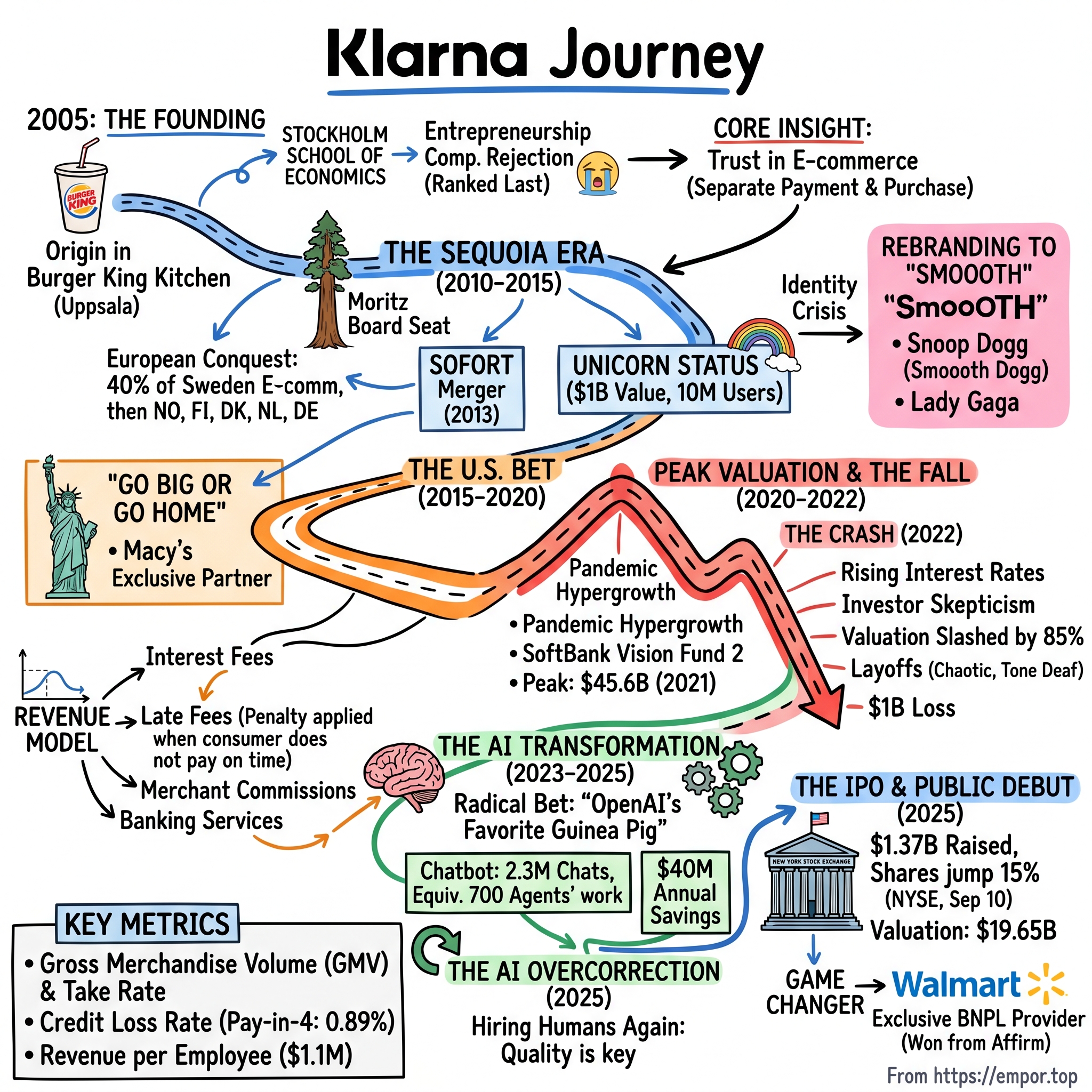

On a crisp September morning in 2025, Sebastian Siemiatkowski stood on the trading floor of the New York Stock Exchange, wearing his signature open-collared shirt instead of the banker's suit his younger self once thought necessary. Twenty years earlier, a panel of Sweden's business elite—including the chairman of H&M and even the king—had laughed his startup idea out of a pitch competition. Now, shares of Klarna rose 15% in their New York Stock Exchange debut Wednesday, closing at $45.82 after the Swedish fintech priced its IPO above its expected range at $40, raising $1.37 billion for the company and existing shareholders.

Klarna shares jumped 30% in their hotly anticipated New York debut, valuing the Swedish fintech at $19.65 billion, ending the company's years-long wait for a listing and underscoring a rebound in the broader U.S. IPO market. It was the largest IPO of 2025, a remarkable achievement for a company whose journey reads like a fintech Odyssey—complete with false starts, near-death experiences, and a villain in the form of rising interest rates.

The central question that any serious investor must ask is this: How did three Swedish business students who got laughed out of a pitch competition build Europe's most valuable startup—only to lose 85% of that value and claw their way back?

In its regulatory filing, Klarna said it was profitable for its first 14 years before expanding into the U.S. and other markets, and it hasn't recorded an annual profit since 2018. This admission raises crucial questions about the sustainability of Klarna's business model in an era where easy money is gone and consumers face mounting pressures.

This deep dive will examine the evolution of consumer credit itself, how BNPL emerged as a category that is reshaping global payments, the perils and promises of AI-first transformation, and what happens when hypergrowth meets market reality. Founded nearly 20 years ago by Swedish entrepreneurs Sebastian Siemiatkowski, Niklas Adalberth, and Victor Jacobsson when they themselves were in their 20s, Klarna over the years transformed from a provider of short-term loans into something more akin to a neobank. Last week's IPO, which saw shares jump 15% on opening day and gave Klarna a market cap of $17.3 billion, was a big win. Yet, the firm's long journey in the private markets, which included founder departures, a crushing down-round, and a perilous board fight, complicates the traditional venture narrative.

II. Origin Story: From Burger King to Business School

The Unlikely Immigrant Entrepreneur

The story of Klarna begins not in a gleaming startup incubator, but in the steamy confines of a Burger King kitchen in Uppsala, Sweden. Burger King is the kind of company that rarely, if ever, tops lists of inspirational wellsprings for tech entrepreneurs. Yet Sebastian Siemiatkowski, founder and CEO of Swedish fintech insurgent Klarna, discovered plenty to admire when he worked at the fast-food giant as a teenager. "These restaurant chains have incredibly meticulous processes," Siemiatkowski enthuses. "They don't have the advantages of a software firm; they are thin-margin businesses that are always squeezed."

Siemiatkowski's parents moved to Uppsala from Poland in the 1980s. He was born on 3 October 1981 in Sweden but his older sister was born in Poland. Siemiatkowski considers himself as a second generation immigrant. His early influences were Richard Branson and Ingvar Kamprad, founder of IKEA.

The immigration story was not easy. The family maintained strong ties to their Polish background, and Siemiatkowski grew up speaking Polish at home, eating Polish food and celebrating Polish Catholic holidays. Stories of the trials his ancestors endured during World War II, including relatives who suffered in German concentration camps, lingered in the background. Overall, the immigration experience was hard on Siemiatkowski's parents, especially his father Michal, who sacrificed his budding career as a veterinarian in Poland in exchange for a job driving a taxi. Siemiatkowski's parents had little money in his youth and struggled to provide the basics. "We would go a full week at a time eating meal after meal of Swedish pancakes, which are essentially nothing more than flour and milk," Siemiatkowski says. "My parents couldn't afford anything else."

Yet within this struggle lay opportunity. Siemiatkowski credits the Swedish digital policy of subsidizing the ownership of computers for his success because it allowed his family to acquire their first computer. That subsidized machine became his window to a larger world and, eventually, his toolkit for building one of Europe's most valuable companies.

The Burger King Brotherhood

If Siemiatkowski's two years flipping burgers gave him a taste for the rigors of a well-oiled corporate machine, it also helped crystallize a relationship that would prove pivotal—that with his Klarna co-founder, Niklas Adalberth. Although Adalberth would eventually leave the company in 2015, the two boys' formative experiences in the literal boiler room sparked a friendship that would evolve over the course of a round-the-world excursion, a failed entrepreneurship competition and the ultimate founding of Klarna in 2005. "Niklas gave me a fantastic gift: in my youth, I was always convinced that I was right, while Niklas was always able to show me when I was wrong," Siemiatkowski says. "He was this amazingly patient, focused, solid person, while I could be quite emotionally all over the place."

After their shifts flipping burgers ended, the two young men embarked on an adventure that would have broken less resilient spirits. They tried bartending, worked (unsuccessfully) on a Florida cruise ship, and waited tables at a Swiss ski resort. Still restless, they set off to hitchhike across the world. But a crisis arose when they missed the last monthly cargo ship to Los Angeles from Sydney, leaving them stranded.

When Siemiatkowski returned to Sweden, living on welfare checks while attending the Stockholm School of Economics, he landed a job at a factoring company—one that helps small companies cover unpaid invoices. It was this experience that planted the seed for what would become Klarna's revolutionary approach to consumer payments: buy now, pay later.

III. The Founding & Early Years: "Forget About It" (2005-2010)

The Pitch That Almost Wasn't

Siemiatkowski, Adalberth and Jacobsson had entered Kreditor into an entrepreneurship competition at their school presided over by Sweden's corporate elite, including Stefan Persson, chairman of H&M, and a member of the Wallenberg family, a prominent venture outfit. Even Sweden's king was in attendance. "Unfortunately, none of them was convinced," Siemiatkowski says with a laugh. "'It'll never work…why can't the banks just do it'…they had all kinds of arguments about why it wouldn't pan out." Siemiatkowski describes their loss—they ranked last out of three startups—as an "emotional" blow that nevertheless provided spiritual fodder for the harder fight ahead. "My reaction wasn't to give up and go home, it was to curl up my fist and say 'I'll show you'."

Reflecting on the experience, Siemiatkowski previously told Forbes Europe: "We presented our idea at an innovators pitch, and they said, 'forget about it. It's never going to work.' I didn't feel great." However, an observer approached Siemiatkowski and co during the competition and gave them some welcome encouragement. "He said, 'you know what, I don't care what those guys said. Just go for it, and the banks will never understand what happened'. I'm still on that mission."

The Core Insight: Trust in E-commerce

In the early 2000s, online shopping was embryonic—rife with fraud and scams, widely regarded as unsafe. Consumers were hesitant to share credit card information and bank details online. Klarna's insight was deceptively simple: separate the payment from the purchase. Let consumers receive goods first, then pay. This invoked trust and fundamentally changed the psychology of online shopping.

In an interview with Whiteboard, founder Niklas Adalberth explained: "The problem we faced was: we were three students, we had no money whatsoever, and no tech knowledge either. I mean, I did some homepages when I was younger, but no hardcore programming. We needed money and tech, which was hard to find. There was no commercial solution out there solving our need." Though the founders faced a real setback with their loss of the Entrepreneurship Award, they soldiered on. And by mid-2005, Klarna had launched operations in Sweden—thanks, in great part, to Swedish angel investor Jane Walerud.

Walerud not only invested capital but also put the founders in contact with the tech resources they'd need to get Klarna off the ground. Adalberth recounted how it all went down, saying: "Three weeks later, she gave us 60,000€ (in) seed money for 10% of the company and 5 techies to build our platform in exchange for 37% of the company." While some may argue that this was a great deal of stake to give up so early in the game, Adalberth explained that though it "was a tough decision", they realized that they "wanted to build something big".

Early Traction

The team started out in 2005 cold calling merchants, offering direct payments, installment plans, and pay-after-delivery options. The first company was named Kreditor—a name that would later be changed to Klarna, derived from the Swedish word "klar" meaning "clear."

Angel investor Jane Walerud invested in their company and connected them with a team of programmers. In 2007, venture capital firm Investment AB Öresund invested in the company. In 2010, Klarna started providing services in Norway, Finland, Denmark, Germany and the Netherlands. It also received an investment from Sequoia Capital, and increased its revenue by over 80% to US$54 million.

The Sequoia investment marked a turning point. The legendary Silicon Valley firm, known for backing Apple, Google, and countless other tech titans, saw in Klarna something the Swedish establishment had missed: a fundamental rethinking of how payments could work in the digital age.

IV. European Domination & The Sequoia Era (2010-2015)

The American Kingmakers Arrive

Klarna's previous round was a scant $9 million in May 2010 when it was discovered by Sequoia Capital and superstar partner Michael Moritz took a board seat (yes, he actually flies to Sweden for the board meetings).

Klarna is on track to double revenues to about $120 million this year, CEO Sebastian Siemiatkowski estimates. And it's been profitable on a pre-tax basis since 2005. It has 600 employees and clears $2.5 billion worth of e-commerce transactions through its payment system.

"I think overall it is better for businesses to stay private because you have more latitude," says Moritz, "more freedom. The inevitable mistakes made during the hurly burly of developing a business are not penalized by people who do not understand it." Moritz is a patient guy. He knows Sequoia will get its return down the line.

That patience would be tested over the next 15 years, through boom and bust, but ultimately vindicated. Sequoia's overall gain remains the highest of any investor in Klarna.

European Conquest

As of 2011, about 40% of all e-commerce sales in Sweden were through Klarna. This staggering market share demonstrated the power of Klarna's model in Nordic markets, where trust in institutions and technology adoption ran high.

In 2011, growth equity firm General Atlantic led a $155 million investment round joined by DST Global, and General Atlantic's managing director Anton Levy joined the board of directors. In May 2011, Klarna acquired Israeli company Analyzd, which provided risk management and fraud prevention services.

The service started in Sweden (where 20 percent of all e-commerce sales already go through Klarna), then spread to Norway, Finland, Denmark, the Netherlands, and most recently Germany (where it is growing at more than 1,000 percent annually). "When we started it, people said it was a Swedish phenomenon," recalls Siemiatkowski, "then a Nordic phenomenon, then a Nordic-German phenomenon."

The SOFORT Merger & Unicorn Status

In 2013, Klarna and German SOFORT AG merged to become Klarna Group. The merger brought together two complementary businesses: Klarna's post-purchase payment model and SOFORT's direct bank transfer technology. Together, they created a payments powerhouse with dominant positions across Northern Europe.

In 2013, Klarna became a unicorn company after reaching a market cap of over $1 billion, also reaching 10 million users—more than the population of Sweden at the time.

In 2015, Minister of Enterprise and Innovation Mikael Damberg dubbed Klarna one of Sweden's "five unicorns", by which he meant startup companies that had succeeded in growing and attracting international investments. The other four were Spotify, Mojang, Skype, and King.

The Strategic Road Not Taken

As Klarna celebrated its unicorn status, Siemiatkowski faced a fateful decision. The company was approaching dominance in its core European markets after a successful rollout in Germany. Siemiatkowski had established himself as a rising star in fintech and knew the landscape inside and out. He decided that the time was ripe to conquer an adjacent market: digital payments infrastructure.

Siemiatkowski presented his vision to the board, which endorsed it wholeheartedly. "We went over the competitive landscape and I kind of glossed over these other players—this company 'Stripe' founded by these two Irish brothers, and this other one, Adyen, founded by a few Dutch guys," Siemiatkowski recalls sheepishly.

That strategic pivot never fully materialized. Stripe went on to become the most valuable private company in fintech history at $95 billion; Adyen became a European payments giant worth tens of billions. Klarna stayed focused on BNPL—a decision that proved both blessing and curse.

Identity Crisis: Blue Suits to Pink Logos

By 2014, Klarna had become one of Europe's fastest-growing companies, with over 1,000 employees moving into a new headquarters in Stockholm. Klarna's massive success made them a renowned tech wonder, but we continued to embody the characteristics of the industry we wanted to disrupt. We were on the path to becoming just another boring blue bank.

In the early years we thought, as three twenty-something start-up founders, that we needed to act bigger than we were. We wore suits and ties and thought having business cards and phone numbers with as many zeros as possible would make people trust us. The more experienced we became, the less important we realized that those things were. It all comes down to the value that you create for your customers.

The company experienced a major crossroads, as leadership came to the realization that some of the industry practices they had digitalized were not always in the best interest of the consumer. Their first approach was to be honest about it, and their second approach was to transform the industry.

The new brand identity, Smoooth, did not only include a new logo, graphic identity, typeface and tonality—it marked the starting point towards creating a completely new user experience. We officially ditched the shirt and tie, and teamed up with world-famous celebrities. Snoop Dogg changed his name to 'Smoooth Dogg' and became an investor. Lady Gaga challenged outdated gender stereotypes. A$AP Rocky ensured consumers left lockdown in style.

V. The U.S. Bet: "Go Big or Go Home" (2015-2020)

America Calling

Klarna launched in the United States in 2015, and the US has become its principal focus for growth, after securing exclusive partnerships with luxury department store Macy's.

The strategic imperative was clear: to justify its growing valuation, Klarna needed America. The U.S. represented the world's largest consumer credit market, the global center of venture capital, and the ultimate proving ground for fintech ambitions. But it was also a market dominated by credit cards—a deeply entrenched system that had resisted disruption for decades.

"It's the largest consumer market in the world, and it's the biggest credit card market in the world. It's a tremendous opportunity, from our perspective," said CEO and co-founder Sebastian Siemiatkowski. Over the years and in multiple interviews, Siemiatkowski has made it clear that Klarna wants to steal away customers from the big credit card companies and sees credit cards as a high-interest, exploitative product that consumers rarely use correctly. Klarna's most popular product is what's known as a "pay-in-4" plan, where a customer can split a purchase into four payments spread over six weeks.

The Revenue Model Under the Microscope

By offering flexible e-commerce payments, Klarna makes money through several channels: interest fees, late fees, merchant commissions, and banking services. But the revenue model carried an ethical tension that would haunt the company.

Many customers had received reminder fees and threats about debt collection without having received a proper invoice. It was speculated if this was an unethical business model since the company made money on these reminder fees and Klarna also had a subsidiary dedicated to debt collection. The Swedish Consumer Agency found a reason to investigate how Klarna added credit fees for partial payments. In 2013, the co-founder Niklas Adalberth said in a presentation during the startup conference Arctic15 that: "That is one of our revenue streams... the best customer is the one that doesn't pay directly but actually [gets] a reminder and then also debt collection because we are able to add the legal fees."

This candid admission about Klarna's early revenue model reveals the fundamental tension at the heart of consumer finance: the incentive to profit from consumer mistakes versus building a sustainable, trust-based relationship. It's a tension Klarna has spent years trying to resolve—or at least rebrand.

BNPL Goes Mainstream

This BNPL value proposition has gained traction outside of the US as well, with Klarna leading in Europe and Afterpay (acquired by Square) in Australia. In 2022, BNPL accounted for 5% of global e-commerce payments, up from just 1% in 2015.

Klarna is Europe's leading BNPL provider, commanding 70% market share as of recent estimates. Klarna's BNPL model has proven especially beneficial to online retailers, reducing cart abandonment rates, which had plagued the industry due to complicated checkout processes. Klarna's higher-converting checkout experience allows shoppers to pay for purchases in four interest-free installments every two weeks. Klarna is said to process two million transactions daily, with big-name users including Nike, Adidas, and H&M.

In 2019, Klarna raised $460 million with plans to expand its operations in the US, with participation from Dragoneer Investment Group, Commonwealth Bank of Australia, HMI Capital, Merian Chrysalis Investment Company Limited, and others. This funding round valued the company at $5.5 billion, making Klarna the largest fintech start-up in Europe.

VI. Peak Valuation & The Fall (2020-2022)

Pandemic-Fueled Hypergrowth

The COVID-19 pandemic proved to be rocket fuel for Klarna. As consumers shifted en masse to online shopping, BNPL services exploded in popularity. Young consumers, in particular, embraced the flexibility of spreading payments over time without the perceived burden of credit card debt.

Atomico, Northzone, Permira, Silver Lake Partners, Technology Crossover Ventures, Sequoia Capital, BlackRock, Bestseller, Dragoneer Investment Group, GIC, Ant Group, Commonwealth Bank of Australia and Hmi Capital all backed Klarna in the round. The fundraise tripled Klarna's valuation to $31bn. But it's worth noting that despite 2020's revenue increases, Klarna's losses also accelerated 50% that year due to expansion costs. Its net losses came in at around $109m that year too. It's a wonder how the Klarna exec team managed to pause to catch their breath last year amid all the fundraising activity: just three months later, the company scored another $639m in fresh capital at a $45.6bn post-money valuation. SoftBank's Vision Fund 2 led the round, which gave Klarna the crown of second most valuable fintech startup in the world—second only to Stripe.

At its peak in 2021, Klarna commanded a private valuation of around $45.6 billion, becoming Europe's most valuable private tech company. Back in 2021, the Swedish BNPL giant was soaring in subsequent fundraises, first becoming Europe's startup champion and then coming only behind Stripe among fintechs globally.

The Crash

Then came 2022. Rising interest rates, tighter regulation of BNPL services, and investor skepticism toward profitless growth combined to create a perfect storm.

Klarna saw its valuation slashed by 85% in a new financing round announced Monday, reflecting grim investor sentiment surrounding high-growth tech stocks and "buy now, pay later" lenders. The Swedish fintech firm said it raised $800 million in fresh funding from investors at a $6.7 billion valuation—down sharply from the $45.6 billion value it secured in a 2021 cash injection led by Japan's SoftBank.

A $14 billion IPO represents a redemption arc for a company that could've easily been another cautionary tale—its valuation plunged by as much as 85%, to $6.7 billion by 2022.

Klarna lost $580 million between January and July 2022. In September 2022, it announced plans to lay off an additional 100 employees.

The 2022 Layoffs

In May 2022, Siemiatkowski revealed it would be laying off more than 10% of its employees. A former employee described the layoffs as "chaotic". When Siemiatkowski posted a list of the fired employees on LinkedIn, several users described his post as "tone deaf".

Sebastian Siemiatkowski, Klarna's CEO and co-founder, made the announcement to his employees in a pre-recorded video message Monday. The "vast majority" of Klarna employees won't be affected by the measures, he said, however some will be informed that they are being let go. "When we set our business plans for 2022 in the autumn of last year, it was a very different world than the one we are in today," Siemiatkowski said.

The Stockholm-based company showed that its full-year operating loss for 2022 grew 46.5% to 10.4 billion Swedish kronor (around $994 million) from 2021's 7.1 billion kronor. The first two quarters of 2022 accounted for 67.5% of that figure, with the loss narrowing in Q4. Klarna had a tough 2022 as investor sentiment shifted against high-growth, unprofitable startups. In July, the company lost its title as Europe's most valuable VC-backed company when its valuation fell 85.3% to $6.7 billion following its most recent round, in which Klarna raised $800 million from investors including Sequoia and Silver Lake. Later in the year, it also announced widespread layoffs.

The company posted a $1 billion loss for 2022—a stunning reversal for a company that had been profitable for its first 14 years.

VII. The AI Transformation: "OpenAI's Favorite Guinea Pig" (2023-2025)

The Radical AI Bet

Facing existential pressure to return to profitability, Klarna made what would become one of the most closely watched bets in corporate AI history. Rather than simply using AI to augment human workers, Siemiatkowski proposed something far more radical: replace them.

Klarna's OpenAI integration is doing the work of 700 live agents, the payments company announced on Feb. 27. In the month since the integration has launched, the chatbot has had 2.3 million conversations, handling two-thirds of the company's customer service queries. Workers are increasingly afraid of their workload being scooped up by AI. Gallup has noted an uptick in FOBO or the "fear of becoming obsolete" over the past two years. Klarna claimed that its chatbot's service is equally as satisfying as human interaction, based on ratings; the fintech company also said that its "AI assistant" has resolved customer issues more quickly and has led to "a 25% drop in repeat inquiries."

On its website, OpenAI featured a customer story in which Siemiatkowski proudly boasted, "we push everyone to test, test, test, and explore." The testimonial noted that, within the first month of the plug-in being live, the AI assistant "had 2.3 million conversations, two-thirds of Klarna's customer service chats, it is doing the equivalent work of 700 full-time agents, it is on par with human agents in regard to customer satisfaction score."

Workforce Transformation

The company's employee count dropped from over 5,500 in 2022 to just 3,400 by the end of 2023.

Klarna's cofounder and chief executive Sebastian Siemiatkowski indicated he hopes to shrink his workforce to a magic number of 2,000 in the coming years. The firm's AI-driven automation of customer service operations reportedly saved $40 million annually and reduced its workforce from 5,000 in 2023 to 3,500 by the end of 2024.

The company's average revenue per employee has increased by 73 percent in the past year. Klarna delivered its fifth consecutive quarter of operational profitability and reached major milestones, including $823m in revenue, 111 million active Klarna consumers, 790,000 merchant partners, and $1 million in revenue per employee, nearly triple the figure from two years ago ($369,000).

In December 2024, the CEO said how AI affected his company's hiring policies. According to him the company did not recruit last year because, "AI can do all of the jobs that we humans do."

The AI Overcorrection

Then came the reckoning. After aggressively pursuing an AI-first workforce reduction strategy, the company had to reverse course in 2025 due to quality issues with customer service.

After years of depicting Klarna as an AI-first company, the fintech's CEO reversed himself, telling Bloomberg the company was once again recruiting humans after the AI approach led to "lower quality." After months of boasting that AI has let it drop its employee count by over a thousand, Swedish fintech Klarna now says it's gone too far and is hiring people again.

Founder and CEO Sebastian Siemiatkowski told Bloomberg the company is in the midst of a recruitment drive to ensure customers always have a human to talk to. "[I]t's so critical that you are clear to your customer that there will be always a human if you want," he said. The apparent turnaround comes after years in which Klarna touted its all-in-on-AI strategy.

It now seems that, while chatbots are cheaper, they're just not as good as humans for some jobs, according to Siemiatkowski. "As cost unfortunately seems to have been a too predominant evaluation factor when organizing this, what you end up having is lower quality," he told Bloomberg this week. "Really investing in the quality of the human support is the way of the future for us."

People do not like talking to chatbots, no matter how advanced they may have become in recent years. A study conducted last year found that more than four in five people would choose waiting to talk to a human over getting immediately served by a bot.

Just one in four AI projects delivers on the return on investment it promised, according to a recent IBM survey of 2,000 CEOs. An even smaller portion, 16%, are scaled across the enterprise, the survey said. Despite this dismal success rate, companies are going all-in on AI, driven largely by the belief that everyone else is doing it.

Klarna's AI journey—from triumphalist proclamations to quiet reversal—may be the most instructive case study of the AI era thus far. It demonstrates both the genuine efficiency gains possible and the limits of automation in customer-facing roles that require empathy, nuance, and human judgment.

VIII. The IPO & Public Markets Debut (2025)

The Long Road to Public Markets

Klarna initially planned to file as an American initial public offering (IPO) in April 2025 and was projected to be valued at $15 billion. The valuation was about one-third of its peak of $45.6 billion in 2021. Klarna delayed its IPO filing as a result of market volatility amid tariff uncertainties under the Trump administration, but launched its IPO in September 2025 and raised $1.37 billion.

The company announced its intention to make its stock market debut in March of this year. But shortly after, President Trump's Liberation Day tariffs wreaked havoc on markets, causing Klarna to postpone its public offering plans. But earlier this month, Klarna began announcing details of its postponed IPO, suggesting a date was near. Klarna priced its shares on Tuesday and is expected to list today: Wednesday, September 10.

IPO Financials

Klarna made $2.8 billion revenue in 2024, a 22.8% year-on-year increase. Klarna made its first annual net profit in 2024, posting $21 million profit. It generated $105 billion in gross merchandise volume in 2024. 93 million people used Klarna in 2024, with approximately 65 million using the Klarna mobile app.

Klarna reported a 24% increase in revenue, reaching $2.81 billion in 2024, and a net profit of $21 million—its first profitable year after heavy losses in previous periods.

However, as one analyst noted, there was accounting nuance behind that profit. Here's a footnote explaining the "other income" line item in Klarna's consolidated profit and loss statement: Other income for the year ended December 31, 2024 primarily related to a net gain of $171 million as a result of the divestment of KCO. KCO is Klarna Checkout, which Klarna sold last year for $520 million. The reason given at the time was that KCO was creating competitive conflicts with Stripe and Adyen, which may very well be true. However, selling the business last year helped Klarna (barely) turn a profit, which has undoubtedly been helpful in positioning the business to go public this year.

Market Reception

Klarna stock opened at $52 a share Wednesday, a 30% premium to the company's $40 pricing. It took roughly three-and-a-half hours for the specialists on the floor of the NYSE to manually price the first batch of trades of the company. Over 34 million shares worth approximately $1.37 billion were sold to investors, making it the largest IPO this year, according to Renaissance Capital.

With Klarna going public, its co-founders are now billionaires. At Klarna's IPO price of $40, Siemiatkowski's 7% stake in the company is worth around $1 billion, while Victor Jacobsson, who left the company in 2012, owns an 8.4% stake in the company now worth $1.3 billion. Siemiatkowski said he did not sell shares as part of the IPO. But with Klarna's 20-year-long incubation period before going public, and several fundraising rounds, major parts of Silicon Valley are walking with a handsome return for their patience.

Sequoia, which first backed Klarna in 2010, has invested $500 million in total. The venture firm sold 2 million of its 79 million shares in the IPO, meaning it's generated an overall return of about $2.65 billion, based on the offer price. Andrew Reed, a partner at Sequoia, told CNBC that he was still in college when the firm made its first investment in an "alternative payments company in Stockholm."

The Walmart Partnership: A Game Changer

Just before the IPO, Klarna secured what may be its most significant merchant partnership to date.

Klarna shook up the fintech world in March with the announcement that it was becoming the exclusive buy now, pay later (BNPL) provider for Walmart, replacing its competitor Affirm in one of the most sought-after partnerships in the industry. "This is a game changer," Klarna CEO Sebastian Siemiatkowski said in a statement. "Millions of people in the US shop at Walmart every day—and now they can shop smarter with OnePay installment loans powered by Klarna." OnePay is the Walmart-backed finance app and digital wallet provider that is managing the partnership with Klarna.

Walmart will receive warrants to acquire up to 15 million shares in Klarna once it becomes public at a strike price of $34.

This partnership—won from rival Affirm—positions Klarna at the checkout of the world's largest retailer, potentially transforming its U.S. growth trajectory.

Post-IPO Performance

Klarna topped Wall Street's third-quarter revenue expectations in its first earnings report since its IPO on the NYSE in September. CEO Sebastian Siemiatkowski told CNBC that the company is benefitting from U.S. growth and growing adoption of Klarna Card and fair financing. Siemiatkowski said the company isn't yet seeing "material differences" in payback or spending habits due to the microenvironment. Klarna topped Wall Street third-quarter revenue expectations in its first earnings report after debuting on the New York Stock Exchange in September. Shares dropped 9%. Here's how the company performed compared to LSEG estimates: Revenues: $903 million vs. $882 million expected.

Klarna shares have shed more than one-third in value from their highs. Siemiatkowski told CNBC in May that the technology, along with attrition, has helped the fintech firm shrink its workforce by 40%. He said its natural attrition rate is as much as 20%.

Klarna also said Elliott Investment Management agreed to buy $6.5 billion of its fair financing loans so it can focus on the product's U.S. growth. Merchants grew 38% to 850,000 from 616,000 in the year-ago period, but average revenue per active customer declined. For the fourth quarter, Klarna expects gross merchandise volume to range between $37.5 and $38.5 billion and revenues between $1.065 million and $1.08 million. Both topped FactSet estimates.

IX. Competitive Landscape & Investment Framework

The BNPL Battlefield

The U.S. BNPL market is dominated by key players such as Affirm, Afterpay (owned by Block, Inc.), and Klarna, each securing strong partnerships with major retailers to offer installment payment solutions. These companies have expanded their services beyond traditional retail, integrating BNPL options into the travel, healthcare, and electronics sectors. Their widespread adoption has fueled the growth of BNPL as a mainstream payment method, particularly among younger consumers who seek flexible financing options.

Klarna's primary competitor is Affirm, founded by PayPal co-founder Max Levchin. Among the companies we analyzed, Klarna and Affirm generated about the same revenue in CY 2024. When it comes to revenue growth, Affirm was the fastest growing of the group at 46%, followed by Afterpay at 25% and Klarna at 24%. To put our growth rate in perspective, Affirm increased revenue by almost $900 million in 2024, exceeding Klarna's total U.S. revenue, their largest market.

Affirm has been aggressive in calling out what it sees as differences in business model. For example, in its F-1, Klarna claimed it has "minimized" late fees and that 99% of the consumer loans it extends are paid back on time. However, Klarna generates quite a lot of revenue from the junk fees it charges consumers. To be exact, these junk fees accounted for $472 million in 2024, and comprised 17% of Klarna's total revenue and roughly half of their margins when adjusting their reporting to match Affirm's on an apples-to-apples basis. These junk fees include: Reminder fees, which Klarna describes as a "penalty applied when a consumer does not pay on time" (aka late fees); Snooze fees, which is when a consumer pays a fee to move a payment date.

Porter's Five Forces Analysis

Threat of New Entrants: HIGH The BNPL space has attracted formidable new entrants. The entry of traditional financial institutions into the BNPL space is expected to reshape the competitive landscape, enhancing consumer trust and offering more regulated installment-based payment options. Established banks and credit card issuers are introducing BNPL features to retain existing customers and compete with fintech firms. Apple launched Apple Pay Later, PayPal has its Pay-in-4 product, and major banks like Chase and Citi have introduced their own installment offerings. The barriers to entry are relatively low for well-capitalized players with existing customer relationships.

Bargaining Power of Suppliers (Capital Providers): MODERATE BNPL companies require significant capital to fund their loan books. Klarna's recent $6.5 billion deal with Elliott Investment Management demonstrates the importance of capital markets access. In a higher-rate environment, the cost of capital directly impacts profitability.

Bargaining Power of Buyers (Merchants): HIGH Merchants hold significant leverage. The Walmart partnership switch from Affirm to Klarna—reportedly involving $500 million in warrants—shows how expensive it can be to win and retain major merchant relationships. Merchants can and do switch providers, and they negotiate aggressively on fees.

Threat of Substitutes: HIGH Traditional credit cards remain the dominant payment method, and their issuers are fighting back. Credit card companies are introducing their own installment features, and Apple's integration of BNPL into its ecosystem poses a significant threat. Consumer credit unions and traditional banks also offer personal loans that can substitute for BNPL.

Industry Rivalry: INTENSE Klarna will now be the second-largest buy-now-pay-later company by market capitalisation behind Affirm. The competition is fierce and growing fiercer. Price competition, merchant acquisition costs, and marketing expenses all pressure margins.

Hamilton Helmer's Seven Powers Framework

Scale Economies: MODERATE Klarna benefits from scale in technology development, risk assessment algorithms, and brand marketing. However, the unit economics of each transaction limit how much scale advantages compound. The company doesn't have the same scale economies as a payment network like Visa.

Network Effects: MODERATE-LOW Unlike a two-sided marketplace, BNPL has limited network effects. Consumers don't care much whether other consumers use Klarna, and merchants' adoption doesn't significantly increase consumer demand. There are some benefits from data accumulation for risk modeling, but these are acquirable rather than structural.

Counter-Positioning: WEAKENING Klarna's original counter-positioning—offering flexible payments that traditional banks couldn't or wouldn't provide—has eroded as incumbents have launched their own BNPL products. The "disruptor" positioning is less distinctive when JPMorgan and Apple offer similar services.

Switching Costs: LOW Consumers face almost no switching costs between BNPL providers. They can use multiple services simultaneously and often do. Merchants face moderate switching costs due to integration work, but these aren't prohibitive.

Branding: MODERATE-STRONG Klarna has invested heavily in brand, with celebrity partnerships and distinctive pink branding. There are over 43 million Klarna users in the US alone, making it Klarna's largest market. Brand awareness and trust are genuine assets in consumer finance, though they're expensive to maintain.

Cornered Resource: LOW Klarna doesn't possess any clearly cornered resource—no patents that block competition, no exclusive technology, no regulatory moat.

Process Power: MODERATE Klarna's 20 years of risk assessment data and algorithms represent accumulated process knowledge. Its operational experience in BNPL across multiple markets is difficult to replicate quickly. However, well-funded competitors can and are building similar capabilities.

The Bull Case

-

Massive TAM with Structural Growth: The U.S. BNPL market is projected to reach $184 billion by 2030, and Klarna has secured the world's largest retailer as an exclusive partner.

-

AI-Driven Efficiency Gains: Despite the recent reversal on pure AI customer service, Klarna's operational efficiency has improved dramatically. Revenue per employee has nearly tripled.

-

Platform Evolution: Klarna is transforming from a single-product BNPL provider into a comprehensive digital banking platform, with the Klarna Card, fair financing products, and banking services expanding its revenue opportunities.

-

First-Mover Advantage in Europe: With 70% market share in Europe, Klarna has a dominant position that would be extremely difficult for competitors to dislodge.

The Bear Case

-

Intense Competition: Apple, PayPal, Affirm, and traditional banks are all competing aggressively. Merchant acquisition costs are rising, and switching costs are low.

-

Regulatory Risk: The Consumer Financial Protection Bureau (CFPB) introduced new regulations in May 2024, applying credit card-like protections to BNPL providers. Increased regulatory scrutiny could increase compliance costs and limit growth.

-

Profitability Questions: The $21 million 2024 profit was aided by a one-time gain from the Klarna Checkout sale. Core profitability remains thin, and the company's reliance on late fees (despite messaging to the contrary) creates reputational risk.

-

Macroeconomic Sensitivity: BNPL is inherently sensitive to consumer credit conditions. In a recession, default rates could spike, and consumer spending would decline.

-

AI Strategy Uncertainty: The reversal on AI customer service raises questions about management's strategic judgment and the true limits of AI in consumer-facing roles.

X. Key Metrics to Watch

For investors tracking Klarna's ongoing performance, three metrics deserve particular attention:

1. Gross Merchandise Volume (GMV) Growth & Revenue Take Rate GMV measures the total value of transactions processed through Klarna's platform, while the take rate measures how much revenue Klarna extracts per dollar of GMV. The company achieved a revenue of $903 million, marking a 26% increase year-over-year, and GMV of $32.7 billion, up 23% like-for-like. Klarna's Fair Financing offering saw remarkable growth, particularly in the U.S., contributing to a strong transaction margin. Watch for whether Klarna can maintain GMV growth while improving take rates—or whether competitive pressure forces take rate compression.

2. Credit Loss Rate The delinquency rate on Klarna's "pay-in-4" loans is 0.89 percent, and on its longer-term loans for bigger purchases, the delinquency rate is 2.23 percent. Those figures are below the average 30-day delinquency rates on a credit card. Credit losses are the Achilles' heel of any consumer lending business. Klarna's short-duration loan book (83% refreshes within three months) provides some protection, but watch for any deterioration as the company expands into longer-term fair financing products.

3. Revenue Per Employee / AI Efficiency Metrics Klarna has made bold claims about AI-driven productivity gains. Klarna reported Q3 2025 revenue of $903 million with 51% U.S. growth, yet stock fell 8.97% to $33.4 amid profitability concerns. Operational efficiency improved with revenue per employee reaching $1.1 million, while the company saved $60 million through AI implementation. This metric will reveal whether AI investments are genuinely transforming Klarna's cost structure or whether the human workforce reductions simply masked underlying challenges.

XI. Regulatory & Accounting Considerations

Regulatory Overhangs: BNPL remains less regulated than traditional credit products, but that's changing. The CFPB has signaled intent to apply credit card-like protections to BNPL providers, which could require enhanced disclosures, dispute resolution processes, and potentially limit certain fee structures. State-level regulation adds additional complexity.

Revenue Recognition: Klarna's merchant fee revenue is recognized at the point of sale, while interest income from longer-term loans accrues over time. As Klarna shifts toward more fair financing (longer-term interest-bearing loans), the revenue profile will shift. Investors should watch how this mix evolves and how it affects quarterly results.

Loan Book Accounting: According to the F-1, 76% of the revenue that Klarna made in 2024 was "transaction and service revenue" (down from 77% in 2022), while the remaining 24% was interest income from interest-bearing loans (up from 23% in 2022). The growing proportion of interest income suggests Klarna is becoming more bank-like, which carries different risk and capital requirements.

XII. Conclusion: What 20 Years Teaches Us

The Klarna story is, at its core, a story about time. Twenty years from rejection at a student pitch competition to the largest IPO of 2025. Twenty years of building, expanding, crashing, and rebuilding. Twenty years of a founder's evolution from a Burger King employee to a billionaire CEO.

But time also teaches humility. Venture capitalists love to tell neat stories about their successes: an investor jumping in early with high conviction, a startup showing years of compounding growth under the dutiful stewardship of the founder, and then everyone getting a spectacular return when the company finally goes public. Klarna doesn't exactly fit that mold.

The company's journey illustrates several enduring truths about building technology businesses:

Persistence matters more than initial approval. The same idea that Sweden's establishment rejected became Europe's most valuable startup. Markets and experts are often wrong about what will work.

Growth without profitability is borrowed time. Klarna's 14 years of profitability were followed by years of losses during aggressive U.S. expansion. The market eventually demanded a return to sustainable economics.

AI is powerful but not magical. The most prominent corporate AI experiment of the 2020s resulted in a humbling reversal. AI can do the work of 700 agents—but not with the quality that customers demand.

Capital allocation defines destiny. The strategic decision not to pursue payments infrastructure—glossing over "these other players" like Stripe and Adyen—may have cost Klarna a chance at even greater scale.

For Klarna, the next chapter is being written in public. With 114 million users, 850,000 merchants, and the world's largest retailer as a partner, the company has significant scale. Whether it can translate that scale into durable competitive advantage and sustainable profitability remains the central question.

As Siemiatkowski himself might say, he's still on that mission—the one that stranger at the pitch competition encouraged him to pursue two decades ago: "Just go for it, and the banks will never understand what happened."

The banks understand now. The question is whether Klarna can stay ahead of them.

Myth vs. Reality Box

Myth: "Klarna's AI replaced 700 workers and proved AI can do human jobs." Reality: Klarna's AI handled customer service volume equivalent to 700 workers, but quality suffered, leading to a 2025 reversal and human rehiring. The 700 figure was a productivity metric, not actual layoffs.

Myth: "Klarna returned to profitability in 2024 through operational excellence." Reality: The $21 million 2024 profit included a $171 million gain from selling Klarna Checkout. Core operating profitability remains thin.

Myth: "BNPL companies don't charge interest or fees." Reality: While Klarna's signature pay-in-4 product is interest-free, the company generates significant revenue from late fees, reminder fees, and interest on longer-term financing products. These fees represented 17% of 2024 revenue according to competitor Affirm's analysis.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube