Corporación América Airports: How an Argentine Textile Family Built the World's Largest Private Airport Operator by Number of Airports

I. Introduction: Gateway to an Unlikely Empire

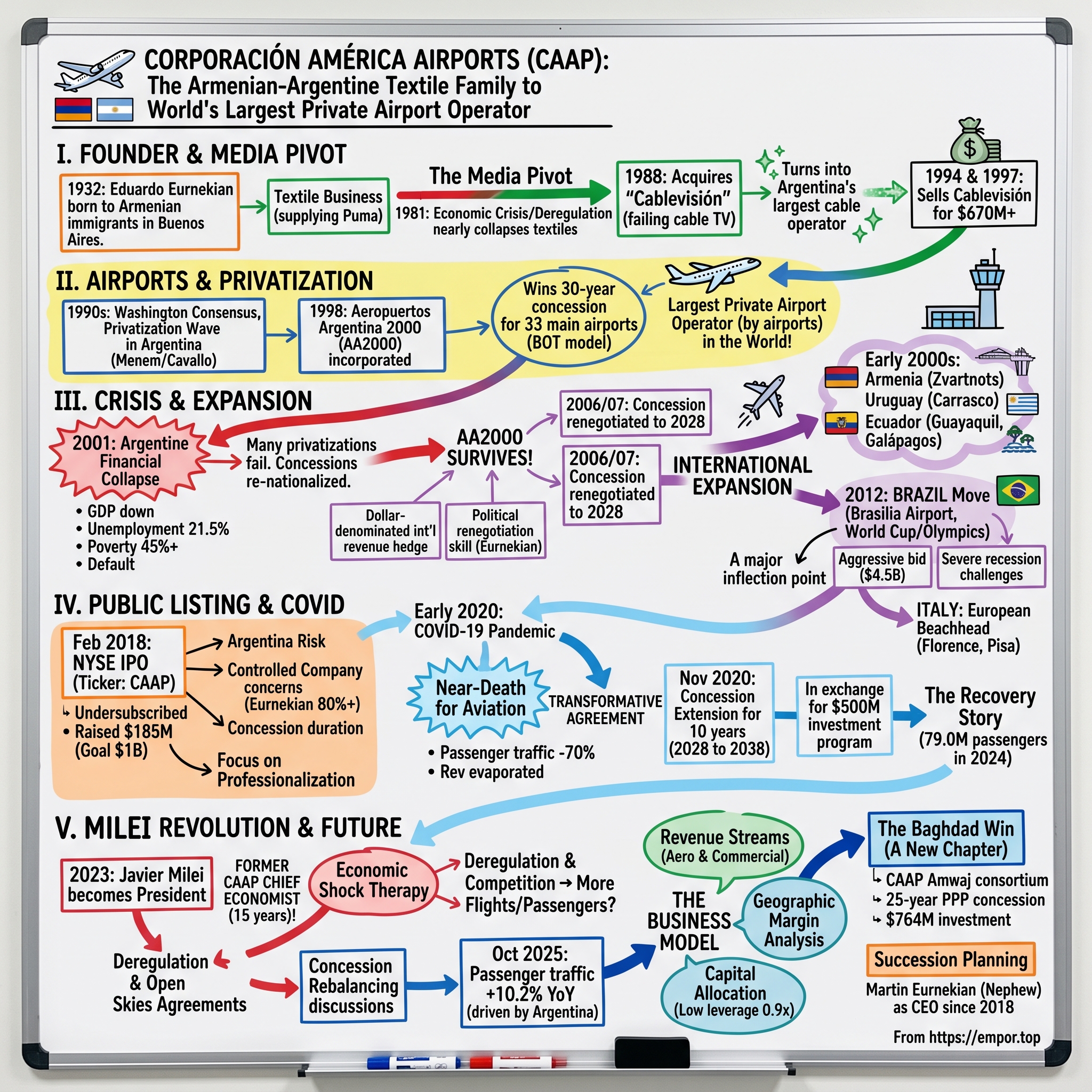

On a humid morning in Buenos Aires, an aging Soviet-era terminal groans under the weight of passengers shuffling through customs at Ezeiza International Airport. Outside, jets bearing the liveries of three continents line up for takeoff. Few travelers boarding their flights realize they're standing in the crown jewel of one of the most improbable business empires in Latin American history—built not by an airline or a construction giant, but by a family that once made textiles for Puma.

Corporación América Airports acquires, develops, and operates airport concessions. Currently, the company operates 52 airports in 6 countries across Latin America and Europe—Argentina, Brazil, Uruguay, Ecuador, Armenia, and Italy. The company trades on the New York Stock Exchange under the ticker "CAAP," a deceptively mundane symbol for what is arguably one of the most extraordinary corporate stories to emerge from Latin America's turbulent economic landscape.

The Company is the largest private sector airport operator in the world based on the number of airports under management and the tenth largest based on passenger traffic. That's right—a company with roots in an Argentine textile shop now controls more individual airports than any private operator on Earth.

The hook to this story isn't just the scale of operations. It's the question of how. How did an Armenian-Argentine family pivot from near-bankruptcy in textiles to cable television, then to airports across three continents? How did they survive not one, not two, but three catastrophic Argentine economic crises—each of which obliterated competitors and sent foreign investors fleeing? And how, in a twist that reads like fiction, did their former chief economist become the President of Argentina?

In 2024, Corporación América Airports served 79.0 million passengers, 2.7% (or 0.4% excluding Natal) below the 81.1 million passengers served in 2023, and 6.2% below the 84.2 million served in 2019. Post-pandemic recovery, while substantial, remains a work in progress—but the trend lines are unmistakable. In October 2025, the company reported a 10.2% year-on-year increase in passenger traffic.

This is a story of privatization as opportunity, crisis-tested resilience, the concession business model at its most complex, and the unique challenges of infrastructure investing in emerging markets. It's a case study in how family-controlled businesses can navigate political volatility that would paralyze publicly traded competitors. And it raises profound questions about the future of airport infrastructure in a world where private capital increasingly controls the gateways to nations.

II. The Founder: Eduardo Eurnekian and the Armenian-Argentine Business Dynasty

To understand Corporación América Airports, you must first understand its founder, Eduardo Eurnekian—a man whose biography reads like a novel spanning nearly a century of Argentine history.

Eduardo Eurnekian is an Argentine businessman who was born to immigrants from Armenia on December 4th, 1932, in Buenos Aires. Born during the aftermath of one of Argentina's earliest economic crises, Eurnekian grew up in a family that had fled the Armenian genocide, carrying with them the memory of catastrophic loss and the hard-won knowledge that survival often depends on adaptability.

Eurnekian was born in Argentina to Armenian immigrant parents. His family ran a textile business that thrived for years and supplied Puma. The family's textile manufacturing operation was typical of immigrant entrepreneurship in mid-century Argentina—modest origins, relentless work ethic, gradual accumulation of capital. For decades, it worked. The Eurnekians built a reliable business supplying athletic apparel to international brands.

Then came the first near-death experience.

However, in 1981, the company nearly collapsed due to Argentina's economic deregulation under Minister José Alfredo Martínez de Hoz. The "tablita" policy—an attempt to gradually devalue the peso against the dollar—combined with radical trade liberalization devastated Argentine manufacturing. Imported goods flooded markets. Textile businesses that had thrived for generations found themselves suddenly uncompetitive. The Eurnekian family business teetered on the edge of bankruptcy.

The Media Pivot: Cable Television and the Birth of a Fortune

What happened next would define Eurnekian's approach to business for the rest of his career: he didn't retreat. He pivoted—radically.

Eurnekian ventured into media by acquiring Cablevisión S.A in 1988, contributing to its growth amidst Argentina's financial stabilization in the 1990s. At the time, Cablevisión was a failing local cable TV station. Most observers saw a sinking ship. Eurnekian saw something else: an undervalued asset in a sector poised for growth, available for purchase precisely because everyone else was running away.

Taking his first steps in the family-established textile industry, in the late 70s he diversified his interests into communications and media by taking over "Cablevision" (then a failing local cable TV station) and turning it into the largest TV cable operator in Argentina.

The timing proved impeccable. When Economy Minister Domingo Cavallo implemented the Convertibility Plan in 1991, pegging the peso to the dollar at parity, Argentina experienced a period of remarkable financial stability. Foreign investment poured in. Consumer spending surged. Cable television subscriptions exploded as the middle class embraced new forms of entertainment.

Eurnekian didn't just ride the wave—he caught it perfectly. In 1994, Eurnekian sold 51% of the company's shares, which had become the second-largest in the country, to Tele-Communications Inc for $350 million. He later sold most of his remaining stake in 1997, netting an additional $320 million from CEI Citicorp Holdings.

The pattern was established: buy distressed assets at the bottom of the cycle, build them up during the recovery, sell at or near peak valuations. It's a playbook that sounds simple on paper but requires extraordinary timing, operational skill, and the nerve to buy when others are selling.

The Renaissance Man of Argentine Business

With capital in hand from the cable television exits, Eurnekian expanded into a bewildering array of businesses. Eurnekian also gained control of "América TV," four radio stations, and a Buenos Aires financial daily, El Cronista. He won a 30-year concession to run 33 of Argentina's main airports through "Aeropuertos Argentina 2000," and purchased the Howard Johnson's master franchise in Argentina from Cendant.

His business interests eventually came to include agricultural concerns, cattle ranches, biodiesel plants, upstream oil operations, wineries, home building, toll road concessions, and even semiconductor fabrication employing nanotechnology. He is, by any measure, a polymath of commerce.

Eduardo Eurnekian is a polyglot and speaks several languages, including Spanish, Armenian, English, and Italian. He is also a keen art collector and has a passion for classical music. Those who know him describe a man of unusual intellectual curiosity—someone who approaches business as both an art form and a puzzle to be solved.

As of 2024, he is Argentina's fourth-richest person, with a net worth of $3.4 billion. Yet the wealth alone doesn't capture the scope of his influence. Eurnekian has received multiple awards, including Businessman of the Year (1995), Italy's Leonardo Award (1999), and Armenia's highest honors. He was named National Hero of Armenia in 2017 and received the Oslo Business for Peace Award in 2012.

Now 92 years old, Eurnekian remains active in the business empire he built, though succession planning has advanced significantly. Eurnekian is single, and his "chosen successor" is his nephew Martin Eurnekian.

The question that loomed over Argentine business in 1998 was what Eurnekian would do with his cable television fortune. The answer would reshape Argentina's infrastructure and create an airport operator of global scale.

III. Argentina's 1990s Privatization Wave: The Washington Consensus Arrives

To understand why a cable television magnate suddenly found himself operating airports, you must understand the extraordinary transformation Argentina underwent in the 1990s.

The Washington Consensus Comes to Buenos Aires

Argentina in the early 1990s was a laboratory for economic experimentation. The country had emerged from hyperinflation so severe that prices could triple in a single month. When the peso was first linked to the U.S. Dollar at parity in February 1991 under the Convertibility Law, initial economic effects were quite positive: Argentina's chronic inflation was curtailed dramatically and foreign investment began to pour in, leading to an economic boom.

The policy toolkit came straight from Washington. Privatization. Deregulation. Trade liberalization. Foreign investment. The ideas had been codified by economist John Williamson as the "Washington Consensus"—a set of policy prescriptions that dominated emerging market economics throughout the decade.

Argentina embraced these policies with a fervor unmatched in Latin America. State oil company YPF was privatized. The telephone system was sold. Railroads, water utilities, power companies—all transferred to private hands. The centerpiece of Menem's policies was the Convertibility Law, which took effect on April 1, 1991. It ended the hyperinflation by establishing a pegged exchange rate with the U.S. dollar and backed money issued by the central bank substantially with dollars.

The transformation was breathtaking. Argentina's reforms were faster and deeper than any country of the time outside the former communist bloc. Real GDP grew more than 10 percent a year in 1991 and 1992, before slowing to a more normal rate of slightly below 6 percent in 1993 and 1994.

The Airport Opportunity: 1998

By 1997, the government turned its attention to airports. The significant increase in air traffic in Argentina during 1990s highlighted a need to upgrade the country's airport infrastructure. The existing facilities were aging, underfunded, and increasingly inadequate for a growing economy.

Aeropuertos Argentina 2000 S.A. ("AA2000" or the "Company") was incorporated in the Autonomous City of Buenos Aires on January 28, 1998, after the consortium of companies won the national and international bid for the concession rights for the use, management and operation of the "A" Group of the Argentine National Airport System. "A" Group includes 33 airports.

The bidding process was competitive. Eurnekian who has been a good friend of Argentine presidents won the Argentine airports privatization back in 1998, under the administration of former president Carlos Menem. His partners at the time were the US based company Ogden and Italy's SEA.

The concession was based on a build-operate-transfer (BOT) system with an investment commitment of $2.2 billion over the concession period and a $171.2 million annual license fee. The terms were ambitious—the government expected major infrastructure improvements in exchange for the right to operate Argentina's gateways to the world.

The Concession was granted pursuant to the concession agreement the Company entered into with the Argentine National Government on February 9, 1998. The Concession is for an initial period of 30 years through February 13, 2028.

Why airports? For Eurnekian, the logic was compelling. Unlike cable television, which faced increasing competition and technological disruption, airports were natural monopolies with high barriers to entry. Once you controlled an airport, competitors couldn't simply build another one across the street. The regulatory framework provided predictable revenue streams. International passengers paid in dollars, providing a natural hedge against peso volatility—a crucial consideration in a country with Argentina's currency history.

The airports operated by Aeropuertos Argentina concentrate more than 90% of the argentine air traffic. This wasn't just market dominance—it was effective monopoly control over Argentina's connections to the world.

The new private owner i.e., AA2000 carried out modernization of Argentine airports significantly. One of the most worked on airports was Ezeiza Airport. AA2000 built a new departure hall in Terminal A; a new parking area for over 500 cars and invested 138 Million Argentine pesos in development works of the airport.

The stage was set for what should have been a straightforward success story: private capital modernizing aging infrastructure under a stable regulatory framework. But Argentina being Argentina, the straightforward rarely stays that way for long.

IV. Crisis #1: The 2001 Argentine Financial Collapse

On December 21, 2001, as smoke rose from fires set by protesters in Buenos Aires and the government fell for the second time in two weeks, Eduardo Eurnekian was less than four years into his airport concession. What followed would test every assumption built into the original deal—and establish a template for how CAAP would navigate crises for decades to come.

The Perfect Storm

By the time of the default, Argentina's GDP was falling abruptly—the drop since the beginning of a recession in 1998 until the default was 15.7 percent (and from 1998 to 2002 the cumulative decline was –19.9 percent). The unemployment rate rose to 21.5 percent and the poverty rate reached a historical peak of above 45 percent.

The crisis was a perfect storm of accumulated vulnerabilities. The influx of foreign currency provided by the privatization of state companies had ended. Brazil, Argentina's largest trading partner, had devalued its currency in 1999, making Argentine exports uncompetitive. The peso's peg to the dollar—once the foundation of stability—became an economic straightjacket.

When the government finally abandoned the peg, chaos ensued. Bank accounts were frozen. Dollar-denominated contracts were forcibly converted to devalued pesos. Foreign investors fled. The country defaulted on roughly $100 billion in sovereign debt—at the time, the largest sovereign default in history.

The Concession Renegotiation Drama

For infrastructure concession holders like Eurnekian, the crisis presented an existential threat. As the economy crashed in 2001 and the local currency was devalued, a new government took office, which renegotiated all contracts. This resulted in re-privatization and re-nationalization of many services.

Proponents of private participation state that a freeze in tariffs at the time of the devaluation of the peso during the Argentinian economic crisis in 2001 substantially reduced the real value of tariff revenues and thus made it difficult to achieve the original targets.

Many privatizations from the 1990s did not survive. Water utilities were renationalized. Railroad concessions were abandoned. Telephone companies faced crushing regulatory battles. The great privatization experiment of the 1990s seemed to be unraveling entirely.

But AA2000 survived. How?

Several factors proved critical. First, unlike water utilities or domestic power companies, airports derived significant revenue from international passengers who paid fees denominated in dollars. This provided a natural hedge against peso devaluation that purely domestic utilities lacked. When the peso crashed, international revenue retained its value while peso-denominated costs collapsed.

Second, Eurnekian proved adept at navigating the political complexities of renegotiation. The Argentine government said it was willing to compensate for the forced 'pesification' of debts because of the 2001/02 Argentine economy meltdown, and Aeropuertos Argentina 2000 proposed paying a percentage of revenue. Finally in 2006 an agreement was reached: the concession was extended until 2028 and the Argentine state was entitled to a 15% stake option and a member in the board of directors which became effective with a 2007 decree.

The 2007 memorandum of agreement restructured the relationship between AA2000 and the government, essentially resetting the economics of the concession to reflect post-crisis realities while preserving the fundamental structure of private operation.

International Expansion as Diversification Strategy

While renegotiating in Argentina, Eurnekian did something counterintuitive: he expanded internationally, seeking geographic diversification as a hedge against Argentine political risk.

In 2001, Eurnekian's company, Corporación América, signed a 30-year contract to manage Armenia's Zvartnots International Airport. It later built a new terminal to meet international standards, a project costing over $50 million.

Why Armenia? The answer lies in Eurnekian's heritage. As a descendant of Armenian genocide survivors, he maintained deep connections to the Armenian diaspora and the Armenian state. These diaspora networks provided deal flow and access that purely financial investors couldn't replicate. The Armenia expansion wasn't just business—it was personal.

The Armenia deal also demonstrated a pattern that would characterize CAAP's expansion strategy: targeting markets where local expertise and relationships mattered as much as capital. In emerging markets, political navigation skills often determine success or failure more than pure operational efficiency.

The crisis had not destroyed Eurnekian's airport empire. It had taught him something invaluable: concentration in Argentina was dangerous. Geographic diversification wasn't just strategy—it was survival.

V. The Expansion Years: Building a Global Footprint (2002-2017)

The years between the 2001 crisis and the 2018 IPO saw Corporación América transform from an Argentine airport operator into a genuinely multinational enterprise. The expansion was methodical, targeting markets where CAAP's emerging market expertise could provide competitive advantage.

Latin American Consolidation

Uruguay came first. Eurnekian also has the concession of Uruguay's international airport of Carrasco. The Montevideo airport operation provided exposure to a smaller but more stable economy, with strong tourism flows from Argentina and Brazil.

Ecuador followed, with concessions at Guayaquil's José Joaquín de Olmedo International Airport and the Galápagos Islands' Seymour Airport. The Galápagos concession was particularly strategic—tourism to the famous islands provided stable, dollar-denominated revenue from international visitors.

The Brazil Move: World Cup Infrastructure

In 2012, as part of the Inframerica Concessionaria do Aeroporto do Brasilia S.A., we were awarded the concession to operate the Presidente Juscelino Kubitschek Airport located in Brasilia, Brazil's capital city. The Brasilia Airport has an annual traffic of 16.7 million passengers.

The Brazil entry was a major inflection point. Brazil's airport privatization program, launched in preparation for the 2014 World Cup and 2016 Olympics, presented an opportunity to enter Latin America's largest economy.

Brasilia was among the first Brazilian airports to be privatised in late 2012, with a 51% stake being awarded to Inframerica Aeroporos, a consortium of Infravix Participações SA and Argentina's Corporacion America SA. State-owned Infraero retains a 49% stake in the airport.

The InfrAmerica consortium won the right to run Brasilia's airport for 25 years. Argentina's Corporacion America SA holding company and Brazil's Engevix SA each have a 50 percent stake in that consortium.

The consortium paid aggressively for the privilege. InfrAmérica, a consortium of Engevix Participacoes SA (50%) and Corporación America SA (50%), won the concession for Brasilia. The consortium offered USD4.51 billion, which is 673.39% above the minimum price.

Since taking over management of Brasilia in December 2012, Inframerica has invested more than R1.2 billion ($464.5 million) to build a new terminal that now boasts 110,000m2 and 29 boarding points, in addition to expanded taxiways and apron space.

The Brazil investment would prove challenging. The country's economy entered a severe recession starting in 2014, and the anticipated traffic growth from World Cup and Olympics hosting proved temporary. CAAP later exited the Natal concession, but retained the strategically important Brasilia operation.

Italy: The European Beachhead

The Italian expansion represented a different strategic calculus entirely. CAI is the controlling entity of Toscana Aeroporti S.p.A. ("TA"), a publicly traded Italian company which manages and holds the concessions for the Florence and Pisa airports in Italy.

Florence and Pisa airports serve the heart of Italian tourism—Tuscany. Unlike the emerging market plays in Latin America or Armenia, Italy offered exposure to developed market dynamics: stable regulatory frameworks, predictable economic conditions, and high-value international tourism. The airports serve as gateways to one of the world's most visited regions.

The Italian operations also provided CAAP with a European footprint that would prove valuable in attracting institutional investors and demonstrating operational capabilities in developed markets.

Building Professional Management

As the empire grew, the challenges of professionalization became paramount. The founder, Eduardo Eurnekian, 85-year-old, owns 82% of the company and since, October 2017, the company has been headed by his nephew, Martin Eurnekian.

The transition from founder-led entrepreneurship to professional management is one of the most perilous passages for family-controlled enterprises. Many fail it. The Eurnekian family attempted to navigate this transition by combining family continuity with professional structures.

Succession planning has advanced with nephew Martín Eurnekian assuming key operational leadership, including as CEO of Corporación América Airports since 2018, ensuring continuity as Eduardo, now 92, steps back from day-to-day management.

Martin Eurnekian brought younger leadership to a company whose markets and competitive dynamics were evolving rapidly. The question of whether the company could maintain its entrepreneurial edge while institutionalizing operations would be tested in the public markets.

By 2017, the company operated airports across Argentina, Brazil, Uruguay, Ecuador, Armenia, Italy, and Peru. The foundation for public listing was in place—but the IPO itself would prove to be a humbling experience.

VI. The 2018 IPO: Going Public on the NYSE

In February 2018, Corporación América Airports rang the opening bell at the New York Stock Exchange. It should have been a triumphant moment—the culmination of two decades of empire-building, the validation of a unique business model, access to the world's deepest capital markets. Instead, the IPO became a sobering lesson in the gap between founder vision and investor reception.

The Road to Public Markets

The company was formerly known as A.C.I. Airports International S.à r.l. and changed its name to Corporación América Airports S.A. in September 2017. The company was founded in 1998 and is based in Luxembourg City, Luxembourg.

The Luxembourg domicile was not accidental. It provided tax efficiency and access to European legal frameworks that many emerging market companies find advantageous. The corporate structure positioned CAAP as an international company with Argentine operating roots—a distinction that mattered to institutional investors wary of Argentine political risk.

Corporación América Airports S.A. announced today the pricing of its initial public offering of 28,571,429 common shares of the Company at $17.00 per common share. The shares are expected to begin trading on the New York Stock Exchange on February 1, 2018 under the symbol "CAAP."

The Undersubscribed IPO

What happened next surprised the company's advisors. The company intended to raise as much as $1 billion in its IPO. In fact, it hired an all-star team including Bank of America Corp., Oppenheimer & Co., Goldman Sachs Group Inc. and Citigroup Inc. to raise at least $500 million. Frustratingly, it ended up with just $185 million, net of all fees, and unsurprisingly, at a price well below the initial expected range.

The deal raised roughly $486 million in gross proceeds, with approximately $202 million flowing to the company and the rest to selling shareholders. But this was far short of the billion-dollar aspiration.

Why the tepid reception? Several factors converged:

Argentina Risk: However diversified the portfolio had become, Argentina still dominated the business. Institutional investors maintained deep skepticism about Argentine assets, scarred by repeated defaults and policy reversals. The country's macroeconomic volatility was well-documented and persistent.

Emerging Market Discount: Latin American infrastructure assets generally traded at significant discounts to developed market peers. The Mexican airport operators commanded higher multiples despite similar underlying economics, largely because Mexico was perceived as more politically stable.

Controlled Company Concerns: With Eduardo Eurnekian retaining over 80% ownership post-IPO, minority shareholders had limited influence over corporate governance. The company is exempt from the requirement to have a majority of independent directors on the board and fully independent nominating and compensation committees within the first year after the IPO.

Concession Duration Questions: The Argentine concession ran through 2028 with a possible 10-year extension—but the extension wasn't guaranteed. Investors assigned minimal value to years beyond what was contractually certain.

Getting listed was an essential step in our company's history, being its main objective the professionalization of our operations and not the raise of capital. It is a commitment that not only the management but all our employees have taken to our investors from all over the world.

Eduardo Eurnekian framed the IPO as primarily about professionalization rather than capital raising—a positioning that acknowledged the underwhelming financial outcome while emphasizing the intangible benefits of public listing.

Strategic Partnerships Post-IPO

Following the IPO, CAAP moved to strengthen its position through strategic partnerships. Corporación América Airports S.A. and Investment Corporation of Dubai ("ICD"), the principal investment arm of the Government of Dubai announced today that they have entered into a share purchase agreement whereby CAAP will sell 25% of its wholly owned subsidiary Corporación America Italia S.p.A. ("CAI") to ICD. CAAP and ICD have also entered into a Memorandum of Understanding ("MOU") to jointly pursue new opportunities in the airport sector in Italy, Eastern Europe (exc. Russia) and the Middle East. The MOU aims to build upon CAAP's management capabilities and deep knowledge of the airport industry as well as ICD´s unique access to financing and the capital markets.

The ICD partnership signaled intentions to expand beyond Latin America and Armenia into new markets—though the MOU would take years to bear fruit.

What the IPO demonstrated most clearly was that CAAP's stock price would be hostage to Argentine macroeconomic conditions regardless of geographic diversification. From the $17 IPO price, the stock would face years of volatility driven less by operational performance than by the latest news from Buenos Aires.

VII. Crisis #2: The COVID-19 Pandemic

The pandemic that swept the globe in early 2020 presented CAAP with its second existential test in two decades. Unlike the 2001 Argentine crisis, which was country-specific, COVID-19 struck every market simultaneously. For airport operators worldwide, the impact was catastrophic.

The Near-Death Experience for Global Aviation

So bad was the impact in 2Q2020 that in that period the aeronautical revenues of Corporación América Airports amounted to just USD8 million.

The numbers were staggering. Passenger traffic collapsed by approximately 70% in 2020. Revenue evaporated. Fixed costs—maintenance, debt service, minimum staffing—continued regardless. Airport concessions, which had been reliable cash generators for decades, suddenly consumed cash at alarming rates.

For CAAP, the crisis was compounded by the company's emerging market exposure. While developed market airports could rely on government support programs, CAAP's Latin American operations faced the crisis largely without fiscal backstops.

The Concession Extension: A Crisis-Driven Opportunity

What happened next demonstrated CAAP's ability to turn crisis into opportunity. In November 2020, at the depths of the pandemic, the company secured a transformative agreement.

At a signing ceremony that took place at the office of the President of the Republic of Argentina Dr. Alberto Fernandez, Aeropuertos Argentina 2000 S.A. ("AA2000") represented by its Chairman Martín Eurnekian and the Organismo Regulador del Sistema Nacional de Aeropuertos ("ORSNA") represented by its Chairman Carlos Pedro Lugones Aignasse signed an agreement to extend the AA2000 concession for a ten-year period from 2028 to 2038, as provided for under the existing concession agreement. This extension is part of an agreement entered by AA2000 and ORSNA with an aim to mitigate the impact of COVID19 in its operations.

Extends the term of the AA2000 Concession for a ten–year period from 2028 to 2038, as provided for under the existing concession agreement: the extension is in connection with the 35 airports network operated by AA2000 in the country.

In exchange for the extension, AA2000 agreed to capital investment program for expansion projects of approximately $500 million to be undertaken in two phases: Phase 1: approximately $336 million to occur preferably in 2022 and 2023. Phase 2: annual investments of approximately $41 million between 2024 and 2027, for a total of approximately $164 million.

The extension transformed CAAP's investment case overnight. The day following the announcement shares in Corporacion America, parent company jumped to $US5.59 in Wall Street, up from the previous close of US$3.12.

The Recovery Story

The post-pandemic recovery proved the resilience of air travel demand. In 2023, Corporación América Airports served 81.1 million passengers, 23.7% above the 65.6 million passengers served in 2022 and 3.6% below the 84.2 million served in 2019.

By the end of 2023, passenger traffic had recovered to within 4% of pre-pandemic levels—a remarkable rebound that validated the fundamental thesis that air travel demand would return.

The lessons from COVID-19 reinforced conclusions from the 2001 crisis: geographic diversification matters, government relationships are crucial, and the concession model's stability depends on the willingness of governments to renegotiate terms during force majeure events.

VIII. Crisis #3 (and Opportunity?): The Milei Revolution (2023-Present)

If the story of CAAP were a novel, no editor would accept what happened next as plausible. The company's former chief economist—a man who had spent 15 years advising Eduardo Eurnekian—was elected President of Argentina on a platform of radical economic reform.

The Milei Connection

For 15 years, he worked at the private company Corporación América as the chief economist and financial adviser to Eduardo Eurnekian.

Before entering the public spotlight, Milei was chief economist at Corporación America, one of Argentina's largest business conglomerates that, among other things, runs most of the country's airports.

Javier Milei's biography reads like something invented for dramatic effect. That year Milei became an economist and financial analyst for Corporación América, the large conglomerate controlled by billionaire Eduardo Eurnekian, which has interests in the energy, infrastructure, and agribusiness sectors in addition to operating the majority of Argentina's airports.

During his time at Corporación América, Milei absorbed the frustrations of doing business in Argentina—the regulatory burdens, currency controls, inflation, bureaucratic obstacles. These experiences would inform his political philosophy and his prescriptions for reform.

Javier Gerardo Milei (born 22 October 1970) is an Argentine politician and economist who has served as President of Argentina since 2023. Milei also served as a national deputy representing the City of Buenos Aires for the party La Libertad Avanza from 2021 until his resignation in 2023 due to him being elected President of Argentina that same year.

Argentina's Economic Shock Therapy

Milei inherited an economy in crisis. Inflation exceeded 200% annually. The peso was in freefall. Poverty rates approached 50%. The prescription was radical: slash government spending, eliminate the fiscal deficit, deregulate vast sectors of the economy.

For CAAP, the Milei presidency has created both opportunities and uncertainties. On the opportunity side, aviation deregulation has opened Argentina's skies to competition in unprecedented ways.

Decree 844/2024 essentially deregulates domestic flights in Argentina, and allows flights to be operated by foreign airlines. The new decree came into force 60 days after it was issued.

The changes in policy included authorising foreign companies to provide internal or international air transportation, and more competition in ground handling. Over the course of his presidency Mr Milei has also forged open skies agreements with numerous countries, including Brazil, Canada, Chile, Ecuador, Peru, Uruguay, the Dominican Republic, Ethiopia, Mexico and Turkey.

More competition among airlines could mean more flights, more passengers, and higher airport utilization. Chile's JetSMART Airlines SpA is increasing its fleet of planes in Argentina as President Javier Milei seeks to deregulate the aviation industry. The low-cost carrier, backed by Bill Franke's Indigo Partners LLC and American Airlines Group Inc., has invested at least $160 million in Argentina this year.

The traffic data supports the optimism. Domestic passenger traffic rose by 10.9% year over year (YoY), largely driven by Argentina, along with strong performance in Brazil. Notably, Argentina accounted for more than 79% of the total YoY traffic growth in September. In Argentina, total passenger traffic increased by 13.3% YoY, driven by double-digit growth in both international and domestic segments.

The Concession Rebalancing Question

The uncertainty concerns what happens to the AA2000 concession economics under a government committed to market principles but also to fiscal austerity. In Argentina, we continue progressing through the AA2000 concession rebalancing process.

The "rebalancing" discussions involve adjusting the economic terms of the concession to reflect current market conditions—potentially including tariff adjustments that could improve CAAP's profitability. Under a government philosophically aligned with private enterprise and infrastructure investment, such discussions may find receptive ears.

However, the Milei presidency has not been without turbulence. The corruption scandal revealed in August 2025 had a profound impact on Milei's approval rating, shifting from a steady 48% just a month before to 39%.

For investors, the Milei factor creates a distinctive risk-reward profile. A former CAAP economist in the presidency, pursuing policies favorable to private infrastructure investment, represents an unusual alignment of interests. But Argentine politics remains volatile, and policy continuity beyond any single administration is never guaranteed.

IX. The Business Model Deep Dive

Understanding CAAP requires unpacking the economics of airport concessions—a business model that combines elements of regulated utilities, real estate, and retail operations.

Revenue Streams

Airport revenue divides into two primary categories:

Aeronautical Revenues: These include landing fees charged to airlines, passenger charges collected per departing traveler, and aircraft parking fees. These revenues are typically regulated under the concession agreements, with tariffs approved by government authorities. Importantly, fees charged to international passengers in Argentina are denominated in U.S. dollars, providing a natural hedge against peso depreciation.

Commercial Revenues: These include retail concessions (duty-free shops, restaurants, convenience stores), parking operations, cargo handling, advertising, and VIP lounges. Commercial revenues are generally less regulated and offer greater margin expansion potential through operational improvements.

The company's revenue concentration remains heavily Argentine. The primary sources of revenue come from Argentina's 37 airports (approximately 64% of total revenue), with Ezeiza and Aeroparque in Buenos Aires being the two largest individual contributors. Italy's two airports contribute approximately 10%, and Brazil's airport accounts for roughly 8%.

Geographic Margin Analysis

One of the striking features of CAAP's portfolio is the significant variation in profitability across geographies. As a group, CAAP's EBITDA margin (excluding construction accounting) runs approximately 29-38% depending on the period. By geography, Uruguay operates at the highest margins (approximately 47%), followed by Armenia (approximately 43.5%), Argentina (approximately 31%), Ecuador (approximately 31%), Italy (approximately 19%), and Brazil (approximately 13%).

The margin differential between CAAP and best-in-class airport operators is substantial. The Mexican airports have typically earned 65-70% EBITDA margins for many years. CAAP's lower margins reflect several factors: the economic volatility of Argentina, the regulatory constraints on tariffs, and operational challenges in emerging markets.

Corporacion America Airports Q3 2025 revenue ex-IFRIC12 $472.1M, up 16.6% YoY, Adjusted EBITDA ex-IFRIC12 of $194.3M, 41.2% margin and 23.3M passengers.

Adjusted EBITDA margin ex-IFRIC12 expanded 5.2 percentage points to 41.2% from 35.9% in 3Q24. The trend toward margin expansion is encouraging, suggesting operational improvements are taking hold.

Capital Allocation & Balance Sheet

The company has prioritized deleveraging following the pandemic stress. Net debt to LTM Adjusted EBITDA improved to 1.1x as of December 31, 2024, from 1.4x as of December 31, 2023.

Maintained strong liquidity position with $540.4 million in Cash & Cash equivalents as of September 30, 2025. Net debt to LTM Adjusted EBITDA remained at 0.9x as of September 30, 2025, reflecting continued financial discipline and solid Adjusted EBITDA growth.

For a company with significant capital expenditure requirements under its concession agreements, balance sheet strength provides crucial flexibility. The low leverage ratio provides room for both investment in existing concessions and pursuit of new opportunities.

The Baghdad Win: A New Chapter

The most significant recent development is the company's entry into Iraq. The Iraqi Council of Ministers has approved the award of a 25-year, approximately $764 million PPP concession to the CAAP Amwaj consortium, comprising Corporación América Airports (CAAP), the world's largest private airport operator, and Amwaj, a leading Iraqi development group.

According to a previous announcement, CAAP will invest approximately $764 million in the airport without any government expenditure during the concession term. The project includes the construction of a new passenger terminal with an initial capacity of 9 million passengers per year, expandable to 15 million.

Martin Eurnekian, CEO of Corporación América Airports, commented: "We are honored to have been selected to contribute to Baghdad's airport modernization efforts. Together with our partner Amwaj International, we are committed to developing world-class airport infrastructure that will enhance connectivity, promotes economic growth, and creates opportunities for local communities."

The Baghdad concession represents CAAP's entry into the Middle East—a region with significant infrastructure investment needs and growing air travel demand. It validates the company's strategy of leveraging emerging market expertise to access opportunities that more risk-averse developed market operators might avoid.

X. Competitive Analysis: Porter's Five Forces and Hamilton's Seven Powers

Porter's Five Forces Analysis

Threat of New Entrants: LOW Airport concessions represent one of the most defensible competitive positions in any industry. Physical airports cannot be replicated—you cannot build a competing facility next door. Concession agreements typically run for 20-40 years, creating extremely long-duration competitive moats. The barriers to entry are essentially absolute during concession periods.

Bargaining Power of Suppliers: MODERATE Airlines are the primary "suppliers" of passengers to airports. Large carriers have some negotiating leverage, particularly in markets with alternative airports. However, for gateway airports like Ezeiza or Brasilia, airlines have limited alternatives. Ground handling services and retail concessionaires have less bargaining power as airports control premium real estate access.

Bargaining Power of Buyers: MODERATE Passengers have limited choice in airport selection—they generally use the airport serving their origin or destination. Airlines, as the commercial customers, have more bargaining power but remain dependent on access to key gateways. Retail concessionaires compete for airport space, reducing their negotiating leverage.

Threat of Substitutes: LOW TO MODERATE For short distances, ground transportation (rail, buses, automobiles) represents a substitute. Argentina's vast geography makes this less relevant for domestic travel than in Europe or Asia. For international travel, air remains without meaningful substitute for most passengers.

Competitive Rivalry: LOW Within concession areas, rivalry is essentially non-existent—airports are regulated monopolies. The competition that matters occurs at the bidding stage for new concessions, where CAAP competes against other global airport operators.

Hamilton's Seven Powers Analysis

Economies of Scale: CAAP benefits from scale economies in centralized management, procurement, and expertise. Operating 52 airports allows shared learning and operational benchmarks that smaller operators cannot replicate.

Network Effects: Limited direct network effects, though reputation and track record create an indirect network benefit in winning new concessions.

Counter-Positioning: CAAP's emerging market specialization represents counter-positioning versus developed market operators who may lack expertise navigating volatile political and economic environments. Few competitors can claim the crisis-navigation credentials CAAP has earned through multiple Argentine economic catastrophes.

Switching Costs: Extremely high. Once a concession is awarded, the government faces enormous costs and political complications to change operators mid-concession.

Branding: Limited consumer-facing brand power, but strong B2G (business-to-government) reputation for airport management competence.

Cornered Resource: Long-term concession agreements represent legal cornered resources—exclusive rights to operate specific airports for decades.

Process Power: CAAP's process advantages include expertise in navigating emerging market regulatory environments, managing through economic crises, and negotiating with governments accustomed to nationalist economic policies.

Competitive Comparison: CAAP vs. Mexican Airport Operators

The natural comparables for CAAP are the Mexican airport operators: Grupo Aeroportuario del Pacífico (PAC), Grupo Aeroportuario del Centro Norte (OMAB), and Grupo Aeroportuario del Sureste (ASUR).

The differences are instructive:

| Factor | CAAP | Mexican Operators |

|---|---|---|

| EBITDA Margin | ~38-41% | 65-77% |

| Concession Duration | Through 2038 (Argentina) | Through 2048 |

| Country Risk | High (Argentina dominance) | Moderate (Mexico) |

| Currency Exposure | Mixed (peso/dollar) | Predominantly peso |

| Political Stability | Variable | More consistent |

EBITDA margins spiked to as high as 77% for OMAB. This was well above the average historical profitability of the airport sector and above what the government felt was in the spirit of the concession contract.

The margin gap reflects regulatory differences, operational scale, and country-specific dynamics. The Mexican operators benefit from longer concession durations and more predictable regulatory environments. CAAP's lower multiple relative to Mexican peers reflects this risk differential.

XI. Bull and Bear Cases: What Investors Should Consider

The Bull Case

1. Milei Policy Tailwinds With a former company economist as president, CAAP has unprecedented potential access to favorable policy treatment. Aviation deregulation is expanding flight options and passenger volumes. The concession rebalancing discussions may yield improved economics. Dollar-based fee structures align with government preferences for de-pesification.

2. Geographic Diversification Reduces Argentina Dependence The Baghdad concession, Italian operations, and ongoing international expansion are steadily reducing Argentina's share of the portfolio. Over time, this should narrow the country-risk discount in the valuation.

3. Traffic Recovery and Growth International passenger traffic in Argentina performed particularly well during the quarter, increasing by more than 11% year-over-year and driving hard-currency revenue streams.

Double-digit traffic growth translates to operating leverage and margin expansion. Latin American air travel remains underpenetrated relative to developed markets, providing secular growth tailwinds.

4. Balance Sheet Optionality Net debt to LTM Adjusted EBITDA remained at 0.9x as of September 30, 2025.

Sub-1x leverage provides capacity for both organic investment and M&A. The Baghdad win demonstrates CAAP can compete for and win international opportunities.

5. Valuation Discount CAAP trades at significant discounts to developed market peers and even to Mexican airport operators. If the company can demonstrate sustained margin improvement and political stability, multiple expansion could provide substantial returns independent of earnings growth.

The Bear Case

1. Argentina Remains Argentina Despite the Milei connection, Argentina's history suggests that policy reversals are always possible. Future governments may take different views on concession terms, tariff structures, or even the desirability of private airport operation. The 2001 crisis template—renegotiation, pesification, regulatory changes—could recur.

2. Concession Duration Limits Terminal Value Even with the 2038 extension, CAAP's Argentine concession has finite duration. Post-2038 value depends entirely on further extensions or successful rebidding. Competitors with 2048 or longer concession terms command higher multiples for good reason.

3. Emerging Market Execution Risk The Baghdad concession, while strategically attractive, exposes CAAP to a market with significant political and security risks. Iraq's history since 2003 includes periods of extreme instability. Execution risk on a $764 million project in such an environment is substantial.

4. Hyperinflation Accounting Complexity CAAP's Argentine operations require hyperinflation accounting under IAS 29, making financial statements difficult to interpret. Nominal results differ substantially from inflation-adjusted figures. This complexity may discourage institutional investors who prefer straightforward financial statements.

5. Controlled Company Governance With the Eurnekian family controlling over 80% of shares, minority shareholders have limited influence over corporate decisions. Related-party transactions, capital allocation decisions, and succession planning remain at the family's discretion.

XII. Key Performance Indicators to Track

For investors following CAAP, three metrics deserve priority attention:

1. Passenger Traffic Growth (Year-over-Year)

This is the fundamental driver of airport economics. Traffic growth translates directly to both aeronautical revenues (passenger fees) and commercial revenues (retail spending). Track both total traffic and the breakdown by geography to assess the sustainability of growth and progress on diversification.

Why it matters: Corporación América Airports reported 7.63M passengers in Oct 2025, up 10.2% YoY. Double-digit traffic growth demonstrates demand resilience and supports the margin expansion thesis.

2. Adjusted EBITDA Margin (ex-IFRIC12)

This metric strips out the noise from construction accounting and inflation adjustments to reveal underlying operational profitability. Track progression toward levels achieved by best-in-class operators (40%+ consistently).

Why it matters: Adjusted EBITDA margin ex-IFRIC12 expanded 5.2 percentage points to 41.2% from 35.9% in 3Q24. As a result, the Adjusted EBITDA margin expanded by more than 5 percentage points. Margin expansion demonstrates operational improvement and management execution.

3. Net Debt to Adjusted EBITDA

Balance sheet health determines CAAP's ability to invest in existing concessions, pursue new opportunities, and withstand economic shocks. Given the company's emerging market exposure, maintaining conservative leverage provides crucial shock absorption.

Why it matters: Net debt to LTM Adjusted EBITDA remained at 0.9x as of September 30, 2025. Sub-1x leverage positions the company well for both investment and potential stress scenarios.

XIII. Regulatory and Risk Considerations

Accounting Complexity

CAAP's financial statements require careful interpretation. The application of IAS 29 hyperinflation accounting to Argentine operations means that reported figures in U.S. dollars reflect inflation-adjusted peso results. Comparisons between periods require adjusting for both currency translation and inflation effects.

The IFRIC 12 accounting for construction services under concession agreements creates revenue and expense recognition that may not align with cash flows. Investors should focus on "ex-IFRIC12" metrics that strip out construction accounting noise.

Concession Risk

All of CAAP's value derives from concession agreements with governments. These agreements, while legally binding, exist within political systems where future administrations may take different views. The 2001 crisis demonstrated that Argentine governments will renegotiate terms when circumstances change dramatically.

The concession in Argentina runs until 2038, with Uruguay's until 2043/53, Italy's until 2045/48, and Armenia's deals last into the 2032.

Currency Risk

Despite efforts to denominate fees in dollars where possible, CAAP retains significant exposure to emerging market currencies. Peso depreciation, while partially hedged through dollar-denominated international fees, affects peso-denominated domestic revenues and the translation of local operating costs.

Controlled Company Status

CAAP qualifies as a "controlled company" under NYSE rules due to the Eurnekian family's majority ownership. This exempts the company from certain governance requirements applicable to widely held companies. Minority shareholders should evaluate whether the interests of controlling shareholders align with their own.

XIV. Conclusion: The Anatomy of Crisis-Proof Growth

The story of Corporación América Airports defies easy categorization. It is simultaneously a tale of emerging market entrepreneurship at its most ambitious, a case study in crisis navigation, and an object lesson in the complexities of infrastructure investing in volatile economies.

Eduardo Eurnekian's journey from near-bankruptcy in textiles to control of the world's largest private airport portfolio offers lessons that transcend the specifics of airport operations:

1. Distressed assets create fortunes—if you survive the distress. Eurnekian's pattern of buying failing cable television stations, struggling airports, and undervalued infrastructure consistently generated superior returns. But this strategy requires both capital and the ability to operate through difficult periods that destroy weaker competitors.

2. Geographic diversification is survival insurance, not just return enhancement. The 2001 Argentine crisis would have destroyed a pure-play Argentine airport operator. International expansion transformed an existential risk into a manageable challenge.

3. Government relationships matter as much as operational excellence in infrastructure. CAAP's ability to renegotiate concession terms through multiple crises reflects relationship capital that purely financial investors cannot replicate.

4. Family control can be an advantage in volatile environments. The Eurnekian family's long-term orientation and willingness to accept short-term volatility enabled patience that public market pressures might have precluded.

Looking forward, CAAP enters the late 2020s with the strongest positioning in its history. The Argentine concession runs through 2038. Traffic has recovered to near pre-pandemic levels. The balance sheet carries manageable leverage. The Baghdad concession opens an entirely new geographic frontier. And the Milei administration, whatever its ultimate trajectory, has created an unusually favorable policy environment for the aviation sector.

The risks remain substantial—Argentina will always be Argentina, concession politics are inherently unpredictable, and emerging market volatility is structural rather than episodic. But for investors who believe that the Eurnekian playbook of crisis navigation can continue to generate returns, CAAP offers exposure to one of the most distinctive infrastructure stories in the world.

From monsoon-season textile shipments to Puma, through cable television empires and corporate drama, to the runways of Buenos Aires, Florence, Brasilia, Yerevan, and now Baghdad—the Corporación América story continues to write new chapters. The question for investors is whether this particular page-turner has more upside ahead, or whether the best chapters have already been written.

Note: This analysis is for informational purposes only and does not constitute investment advice. Readers should conduct their own due diligence and consult appropriate financial advisors before making investment decisions. CAAP reports financial results in U.S. dollars but conducts operations in multiple currencies, creating translation effects that complicate period-over-period comparisons.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube