Aptiv: From GM's Parts Bin to the Brain and Nervous System of the Car

The Most Unlikely Tech Transformation in Automotive History

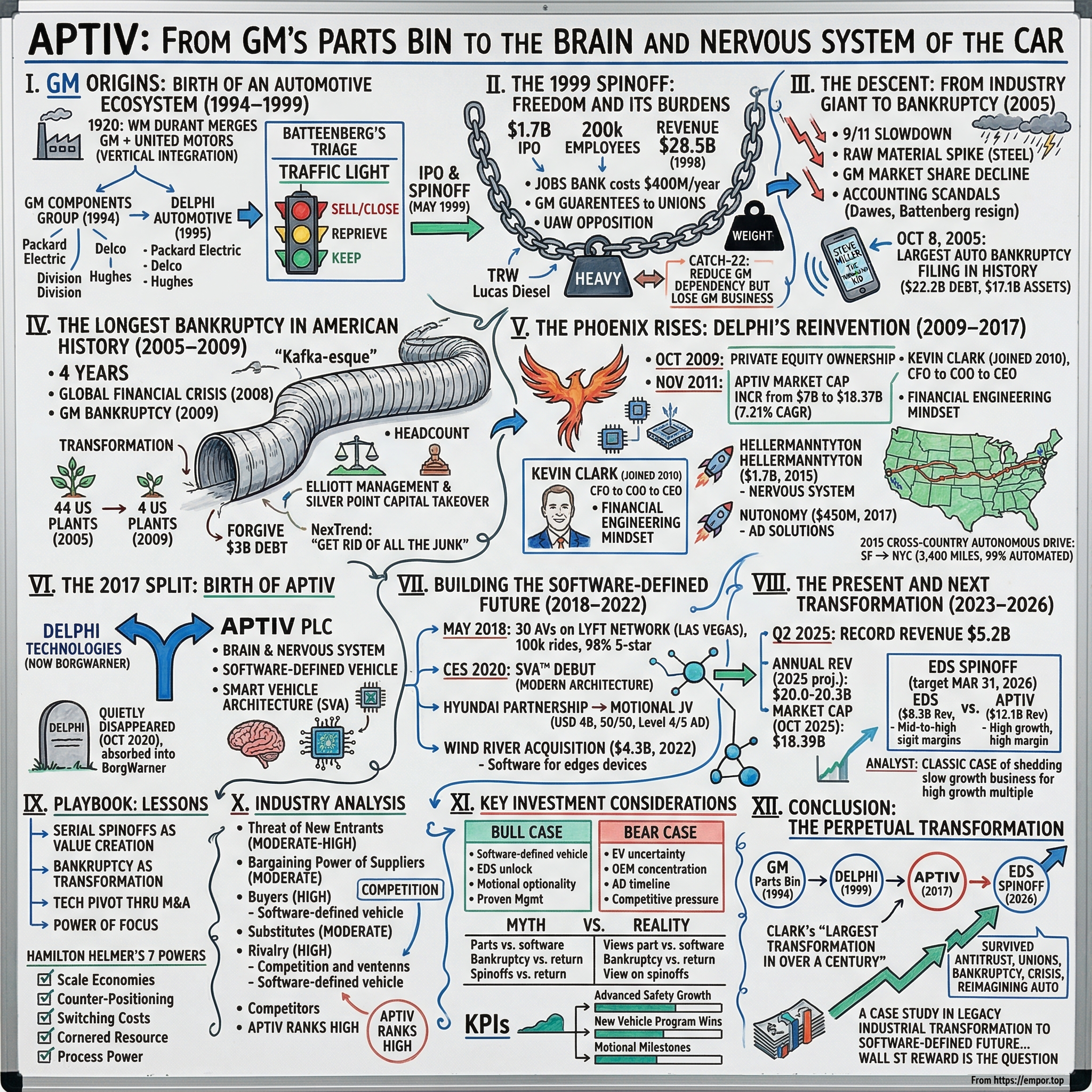

Picture the scene: October 8, 2005, a Saturday morning in Troy, Michigan. Inside the headquarters of Delphi Corporation, the nation's largest auto parts supplier, CEO Steve Miller—known in industry circles as "The Turnaround Kid"—picks up the phone to authorize what would become the largest bankruptcy filing in automotive history. Delphi Corp., the largest U.S. auto supplier, filed for bankruptcy Saturday, sending shock waves through the nation's auto industry, already weakened by high labor costs and falling market share.

Few could have imagined that from this corporate wreckage would emerge one of the most remarkable transformations in business history. Today, Aptiv—the phoenix that rose from Delphi's ashes—stands as a $20 billion technology company with approximately 141,000 employees across the globe, positioned at the intersection of automotive's most powerful megatrends: electrification, autonomy, and software-defined vehicles.

"Automakers will need to adopt a new vehicle architecture to unlock software innovation and actually bring to market the innovative concepts on display across CES," said Kevin Clark, President and Chief Executive Officer, Aptiv. "As a full systems solutions provider, uniquely positioned with both the brain and nervous system of the vehicle, we know that Smart Vehicle Architecture is the right approach to enable the future of mobility."

This is the story of how a collection of GM's castoff parts divisions—burdened with legacy labor costs, pension obligations, and commodity businesses—transformed itself through serial spinoffs, the longest bankruptcy in American history, and relentless strategic repositioning into a company that now competes head-to-head with Silicon Valley's finest for the soul of the software-defined automobile.

I. The GM Origins: Birth of an Automotive Ecosystem (1994–1999)

To understand Aptiv, one must first understand the paradox of vertical integration that shaped the American auto industry for nearly a century. In 1920, William Durant's General Motors merged with United Motors, creating the most vertically integrated manufacturing enterprise the world had ever seen. GM made everything—from spark plugs to steering wheels, from wiring harnesses to window glass.

For decades, this made strategic sense. Control the supply chain, control the quality, control the costs. But by the early 1990s, the calculus had shifted dramatically. Japanese competitors with leaner supply chains were eating GM's lunch. The company's internal parts operations, protected from competition by their captive parent, had grown bloated and inefficient.

General Motors formed the Automotive Components Group in 1994, renamed it Delphi Automotive a year later, and folded in Delco Electronics, which developed the first auto self-starter for the 1912 Cadillac, and Hughes Electronics, in 1997.

The company was established as General Motors' Automotive Components Group in 1994, which changed its name to Delphi Automotive Systems in 1995. G.M. also renamed the various divisions within the newly created Delphi unit. Packard Electric became Delphi Packard Electric Systems; Delco Chassis became Delphi Chassis Systems; Inland Fisher-Guide became Delphi Interior and Lighting Systems; Saginaw became Delphi Saginaw Steering Systems; Harrison Radiator became Delphi Harrison Thermal Systems, and AC Delco became Delphi Energy and Engine Management Systems.

The name "Delphi" itself carried symbolic weight—a reference to the ancient Greek oracle, suggesting wisdom and foresight. Whether the choice proved prophetic or ironic would depend on your vantage point over the next quarter century.

It organized a large chunk of its parts and components business into the new Automotive Components Group, assigning executive J.T. Battenberg III to figure out how to either salvage those operations or get rid of as many as possible. Battenberg, once considered a contender for GM's top spot, knew he was being sidelined. But, as he said in an interview at the time, he saw "an opportunity" to create something bigger than initially perceived. Battenberg's first step with what, in 1995, was renamed Delphi Automotive Systems, was to divide the parts-making empire into three groups.

Those operations given a red light were destined for sale or closure; those given a green light were deemed worth keeping. Yellow gave a reprieve, but only if a turnaround seemed feasible. By 1999, a pared-back Delphi was spun off through an IPO, with Battenberg as its first chief executive.

This traffic-light system of triage—ruthless in its simplicity—would become the template for corporate restructuring that Aptiv's leaders would apply again and again over the ensuing decades. The ability to distinguish between businesses worth fighting for and those destined for the dustbin would prove to be the company's most valuable capability.

For investors, the key insight from this era is foundational: Aptiv's DNA contains the corporate genes of both massive scale (it was the world's largest auto supplier at birth) and ruthless portfolio management. Both traits remain visible today as the company prepares yet another transformative spinoff.

II. The 1999 Spinoff: Freedom and Its Burdens

The February morning of the Delphi IPO marked both liberation and imprisonment for the newly independent company. GM conducted an initial public offering (IPO) of 17.7 percent of Delphi's shares in February 1999, which raised $1.7 billion. The IPO had been delayed about a year while Delco was being combined with Delphi.

By this time, Delphi had spent six years preparing for its independence, selling off 14 lines of business with sales of $6 billion a year, and closing or selling 62 unprofitable plants. When GM completed Delphi's spinoff in May 1999, the newly independent company was twice as large as Visteon Corporation, the parts maker that was being spun off from Ford.

The numbers were staggering. Revenues were about $28.5 billion in 1998, when the company posted a net loss of $93 million. Delphi, which had 200,000 employees, had its share of strikes.

General Motors Corp., the world's largest automaker, completed its separation from No. 1 auto-parts maker Delphi Automotive Systems Corp. with the distribution of $9.3 billion in Delphi shares. GM, which handed its investors an 80.1 percent stake in Delphi and gave another 2.2 percent to a pension trust, now owns no Delphi shares.

But freedom came with chains. The spinoff agreement contained provisions that would haunt Delphi for years to come.

In 1999, Delphi was spun off from General Motors as an independent auto parts supplier. At the time of the spin-off, GM agreed to provide a guarantee to its union (UAW, IAM, and USW) employees who were going to Delphi. The agreements specified that if the Delphi Hourly plan terminated, GM would pay the difference between the plan's benefits and the PBGC's guaranteed benefits.

Delphi also blamed its spinoff agreement with GM for saddling it with high labor costs. Under the agreement, Delphi is required to pay GM wages of $27 an hour to most of its 24,000 UAW-represented workers. That's double the level of competing suppliers, according to Standard & Poor's Ratings Services.

Delphi also had to pay full wages and benefits to 4,000 laid-off workers in jobs banks, which cost it $400-million each year.

The Jobs Bank—a program designed to prevent layoffs by paying workers not to work—became Delphi's albatross. As GM shifted business to lower-cost suppliers, Delphi couldn't reduce its workforce proportionally. The math was devastating: paying workers to sit idle while losing the business that should have employed them.

Union workers protested the loss of jobs and benefits likely to come from outsourcing and globalization; the United Auto Workers had always opposed Delphi's separation from GM, believing this would lead to wage concessions.

Despite these structural challenges, Battenberg and his team pushed aggressively to diversify away from their GM dependency. Delphi sought to expand its core businesses via acquisition soon after its spinoff. Several companies were acquired in the first year, including TRW Inc.'s Lucas Diesel parts unit, bought for $871 million in November 1999. Delphi also bought a wiring harness plant in Asia and entered a number of joint ventures.

But while looking to expand its business apart from its old parent, Delphi also risked having GM assign its business elsewhere. DENSO Corporation, Toyota's parts spinoff firm, quadrupled its business with GM in four years, attaining sales of $1 billion with the automaker by 2001. Delphi was scheduled to lose its right of last refusal for replacement business in North America with GM on January 1, 2002.

This was the catch-22 that would ultimately prove fatal: Delphi needed to reduce its GM dependency to survive long-term, but losing GM business meant paying workers not to work, which accelerated its path to insolvency. The spinoff had created a structural trap from which there was no elegant escape.

III. The Descent: From Industry Giant to Bankruptcy (2005)

The early 2000s brought a cascade of problems that would have tested any management team. The 9/11 attacks triggered an economic slowdown. Raw material costs—particularly steel—spiked. And most importantly, GM's market share continued its inexorable decline, taking Delphi's captive business down with it.

The company announced plans to reduce its worldwide workforce by 11,500 jobs, or 5.5 percent, mostly through attrition. The automobile industry as a whole was experiencing a slowdown. Sales slipped a bit to $29.1 billion in 2000. Slowing auto sales in the fall of 2001 resulted in Delphi's customers making fewer cars and ordering fewer parts.

Then came the accounting scandals. Delphi disclosed some irregular accounting practices in 2005. Many executives, including CFO Alan Dawes, resigned. Delphi Chairman J.T. Battenberg retired. Delphi then filed for Chapter 11 bankruptcy protection to reorganize its struggling U.S. operations. As a result of this action, the Securities and Exchange Commission granted an application by the New York Stock Exchange to delist Delphi's common stock and bonds.

Robert S. "Steve" Miller first made a name for himself helping to orchestrate the improbable 1981 bailout of Chrysler Corp. The author of The Turnaround Kid: What I Learned Rescuing America's Most Troubled Companies, Miller went on to replicate his magic at Waste Management and Bethlehem Steel. And when he joined Delphi Corp. in July 2005, its course was obvious.

Even so, Miller was intent on crafting a consensual resolution, one in which all the relevant stakeholders would agree to make the necessary concessions on wages, debt, and the other impediments holding Delphi back. But it quickly became clear no one was willing to budge. On Oct. 8, 2005, Delphi voluntarily filed for Chapter 11 in New York bankruptcy court — at the time, the biggest auto industry filing ever.

Delphi, No. 63 on the 2005 Fortune 500 list of the country's largest corporations, listed $17.1-billion in assets and $22.2-billion in debt in Saturday's bankruptcy petition.

The scale was staggering—a Fortune 100 company with 200,000 employees worldwide and 50,000 in the United States. Delphi is a global company. It employs 185,000 people around the world. Of these, about 50,000 are employed in the U.S. Delphi makes a wide range of auto parts, including dashboards, air conditioning systems, electronics, and batteries.

Delphi will finance its operations with $4.5-billion in loans, including as much as $2-billion in debtor-in-possession financing from a group of lenders led by JPMorgan Chase Bank and Citigroup Global Markets Inc. Based in the Detroit suburb of Troy, Delphi has struggled to make a profit since GM spun it off in 1999. It lost $4.8-billion in 2004 and nearly $750-million in the first half of this year.

Miller promised a quick, surgical restructuring. He envisioned emerging from bankruptcy within 18 months. Reality would prove far more stubborn.

IV. The Longest Bankruptcy in American History (2005–2009)

So instead of the quick, surgical restructuring envisioned by former Delphi CEO Steve Miller, the supplier's trip through the courts began to take on Kafka-esque tones that started to suggest a permanent existence in bankruptcy hell. By the time the courts finally signed off on the last legal documents four years later, what had been envisioned as a surgical strike turned out to be the longest corporate bankruptcy in American history.

Giant parts maker Delphi, once one of the world's largest automotive suppliers, voluntarily plunged itself into bankruptcy in 2005. Giant parts maker Delphi voluntarily plunged itself into bankruptcy in 2005 as the only way to hammer out a painful restructuring.

The company faced what industry observers called a "double-feature" of catastrophe: just as it was struggling to reorganize, the global financial crisis of 2008 triggered the near-collapse of the entire auto industry. GM itself would file for bankruptcy in 2009.

Delphi nearly emerged from Chapter 11 last year, but was forced to redraw its reorganization plan after a group of investors, led by the Appaloosa Management LP hedge fund, pulled out of an investment deal in April 2008. After that, Delphi struggled to find the financing it needed to restructure. Those troubles were complicated by the collapse of investment banks in the fall and the drop-off in new vehicle sales.

The transformation that occurred during bankruptcy was radical. From being a catch-all conglomeration of myriad GM component suppliers, Delphi has shrunk to being a purveyor of overseas-made climate control systems, powertrain systems, and automotive electronics. Over 50,600 people worked for Delphi in the United States when it filed for bankruptcy in 2005, but because of plant closures and buyouts it now employs only about 14,000 personnel. The company had 44 plants in the United States when it entered bankruptcy; it possesses only four now, and one of those is earmarked for closure.

A group of private investors purchased Delphi's core assets to create a new Delphi Corporation in October 2009. Some of its non-core steering operations were sold to General Motors Company, the successor to the bankrupt Motors Liquidation Company that was formerly General Motors Corporation. The stock was cancelled. The old Delphi Corporation was renamed DPH Holdings Corporation.

On July 30, the bankruptcy judge overseeing Delphi's case approved the auto supplier's plan to hand control of the company to its lenders in exchange for the forgiveness of a combined more than $3 billion in debt. That paved the way for Delphi to emerge from Chapter 11. Elliott Management and Silver Point Capital, the senior lenders that spearheaded the acquisition, said they believe the deal "will provide a solid financial foundation for the company's growth."

"They've finally gotten rid of all the junk," says NexTrend automotive analyst Joe Phillippi, referring to the truly ancient 20th-century legacy businesses that had collectively become Delphi's corporate albatross. But that's only one of myriad reasons why Phillippi and other industry analysts are so bullish about the Troy-based supplier. The slimmed-down Delphi that's emerged from bankruptcy is effectively debt-free and operating largely without the legacy labor costs and holdover wages that made it increasingly noncompetitive. And although it's barely half the size of the company that entered Chapter 11, what remains offers Delphi the opportunity to tap into some of the industry's most promising trends.

Yet, after all the miscues and false moves, industry analysts suggest the new Delphi bears a striking resemblance to the company that Miller and O'Neal envisioned when they first filed for court protection.

V. The Phoenix Rises: Delphi's Reinvention (2009–2017)

The Delphi that emerged from bankruptcy in October 2009 bore little resemblance to the bloated conglomerate that had entered Chapter 11 four years earlier. Under private equity ownership—principally Elliott Management and Silver Point Capital—the company had been ruthlessly streamlined into a focused technology business.

November 2011 marked another pivotal moment. Since November 17, 2011, Aptiv's market cap has increased from $7.00B to $18.37B, an increase of 162.38%. That is a compound annual growth rate of 7.21%.

But the real story of this period is the arrival of the man who would architect Aptiv's transformation into a technology company: Kevin Clark.

Joined Aptiv in July 2010 as Vice President and Chief Financial Officer, advanced to Chief Operating Officer in October 2014, then became President and CEO in March 2015, and assumed the role of Chairman of the Board and CEO in April 2022.

Clark began his career in the financial organization of Chrysler Corporation. He has both a bachelor's degree in financial administration and a master's degree in finance from Michigan State University.

Clark joined Delphi in 2010 as Chief Financial Officer, responsible for all financial activities including strategic planning, corporate development, financial planning and analysis, treasury, accounting, and tax. Before coming to Delphi, he was a founding partner of Liberty Lane Partners, LLC, a private equity investment firm focused on investing in and building and improving middle-market companies. Prior to that, Clark held a number of senior management positions at Fisher-Scientific International Inc., a manufacturer, distributor and service provider to the global healthcare market. He served as Fisher-Scientific's Chief Financial Officer from the company's initial public offering in 2001 through the completion of its merger with Thermo Electron Corporation in 2006.

Clark's background—straddling private equity, financial restructuring, and operating experience at a successful healthcare company—proved ideal for Delphi's next act. He brought the financial engineering mindset of private equity combined with operational chops from running complex global businesses.

Under Clark's leadership, Delphi pursued an aggressive acquisition strategy to build out its technology capabilities:

In the same month, Delphi bought HellermannTyton for $1.7 billion. This December 2015 acquisition strengthened Delphi's position in cable management and connection systems—the "nervous system" of the vehicle that would become central to Aptiv's value proposition.

The company then bought the self-driving startup NuTonomy for $450 million in October 2017.

The transaction brings together the leading start-up and Tier 1 in autonomous driving (AD) and further accelerates Delphi's commercialization of AD and Automated Mobility on-Demand (AMoD) solutions for automakers and new mobility customers worldwide. Founded in 2013 by Dr. Karl Iagnemma and Dr. Emilio Frazzoli and recently named a World Economic Forum Technology Pioneer, nuTonomy is developing a proprietary full-stack AD software solution for the global AMoD market.

Perhaps most symbolically powerful was the 2015 cross-country autonomous drive—a statement moment that demonstrated Delphi's transformation from a parts supplier to a technology innovator:

The SQ5 covered nearly 3400 miles in the coast-to-coast road trip, with 99 percent of the drive in fully automated mode. The SQ5 started the trip at the Golden Gate Bridge in San Francisco, and over the course of nine days, it crossed 15 states before making it to its final destination in New York.

An autonomous car created by Delphi Automotive completed a 3,400-mile trip across the country this week, arriving in New York City nine days after its departure from San Francisco.

This wasn't just a publicity stunt—it was a technological proof point that put Delphi on the map as a serious autonomous vehicle player, years before most traditional suppliers had even begun developing such capabilities.

VI. The 2017 Split: Birth of Aptiv

By 2017, Clark and his team had reached a strategic inflection point. Delphi now housed two fundamentally different businesses under one roof: a technology-forward portfolio focused on autonomous driving, connectivity, and software; and a traditional powertrain business focused on internal combustion engines.

The strategic logic for separation was compelling. Delphi Automotive PLC announced it was splitting into two, with Delphi Technologies taking the advanced vehicle propulsion side of the business, specializing in combustion, software and controls and electrification, and the other spinoff, Aptiv, providing software, advanced computing platforms, and networking architecture for active safety and autonomous driving.

If the sorts of technologies that Delphi Technologies sells still has an uncertain future going into 2030 and beyond, the technologies from spinoff Aptiv do not. It's pretty easy to predict which of the two new companies Wall Street financial analysts and Silicon Valley venture capitalists will favor. Aptiv is working on automotive electrics for the autonomous/connected future that depart from hardware-based systems in favor of software-based systems, as Tesla has used pretty much since the beginning.

The company divested its powertrain division and aftermarket related businesses (now Borg Warner's Delphi Technologies division) in December 2017 and changed its name to Aptiv PLC.

The name "Aptiv" was deliberately chosen to signal a break with the past—apt for a new chapter, evoking adaptability and aptitude. The new company would focus exclusively on what Clark called "the brain and nervous system of the vehicle."

Two years ago, Dephi split itself into two companies. Aptiv Plc focuses on autonomous and connected vehicles. Delphi Technologies retained components for internal combustion engines and some electrification applications. "They knew that the powertrain side of the business was never going to be a growth business," Abuelsamid said.

The fate of Delphi Technologies proved prescient. On October 2, 2020, BorgWarner Inc. today announced it has completed its acquisition of Delphi Technologies. The combination of BorgWarner and Delphi Technologies is expected to strengthen BorgWarner's electronics and power electronics products, capabilities.

BorgWarner completed its $3.3 billion takeover of Delphi Technologies, the last vestige of the once-vast General Motors Co. BorgWarner Inc. has completed its takeover of Delphi Technologies, the last vestige of the once-vast General Motors Co.

The Delphi name—which had graced one of the largest bankruptcies in American history and one of the most remarkable corporate transformations—quietly disappeared from public markets, absorbed into BorgWarner. Aptiv, the technology-focused spinoff, traded on, its stock unburdened by the legacy associations of its former parent.

VII. Building the Software-Defined Future (2018–2022)

With the 2017 split complete, Aptiv moved aggressively to establish itself as a technology leader. In May 2018, the company took a bold step into commercial autonomous operations:

Aptiv PLC, a global technology leader in mobility, announced the launch of a fleet of 30 autonomous vehicles in Las Vegas on the Lyft network. A product of Aptiv's Mobility and Services group, these vehicles will operate on Aptiv's fully-integrated autonomous driving platform and be made available to the public in partnership with Lyft. On an opt-in basis, passengers will have the ability to hail a self-driving vehicle equipped with Aptiv technology to and from high-demand locations. This partnership is a multiyear agreement between the two companies and a clear step toward generating revenue for Aptiv's autonomous driving business.

We're proud to share that in partnership with Lyft, Aptiv has successfully provided 100,000 commercial robotaxi rides in Las Vegas. Notably, 98% of these paying passengers have rated their Aptiv self-driving rides 5-out-of-5 stars, with most stating this first-of-a-kind experience is something they are eager to try again.

This wasn't just testing—this was commercial autonomous vehicle deployment, generating real revenue and real consumer feedback. Aptiv was operating at the frontier of what was technologically possible.

But Clark recognized that autonomous driving represented only part of the software-defined vehicle opportunity. At CES 2020, Aptiv unveiled its comprehensive vision:

SVA™ is a modern, sustainable vehicle architecture that enables automakers to improve safety, increase vehicle efficiency, and deliver the intelligently connected, software-defined experiences consumers want. Aptiv's Smart Vehicle Architecture (SVA) debuts at the Consumer Electronics Show 2020.

Aptiv PLC, a leading technology company committed to making mobility safer, greener, and more connected, unveiled today a modern, sustainable vehicle architecture that enables automakers to improve safety, increase vehicle efficiency, and deliver the intelligently connected, software-defined experiences consumers want. Aptiv's Smart Vehicle Architecture (SVA) debuts at the Consumer Electronics Show 2020 as today's vehicle architectures have reached an impasse and are no longer able to handle the rapidly increasing software and hardware complexity.

Later in 2019, Aptiv forged what would become its most significant strategic partnership:

Joint venture advances the development of production-ready autonomous driving systems for commercialization of Level 4 and 5 self-driving technologies. This partnership brings together one of the industry's most innovative vehicle technology providers and one of the world's largest vehicle manufacturers. The joint venture will advance the design, development and commercialization of SAE Level 4 and 5 autonomous technologies.

As part of the agreement, Hyundai Motor Group and Aptiv will each have a 50 percent ownership stake in the joint venture, valued at a total of USD 4 billion.

The autonomous driving joint venture between Hyundai Motor Group and Aptiv PLC unveiled today its official name and brand identity: Motional. Launched virtually to its employees around the world, the self-driving pioneer is making driverless vehicles a safe, reliable, and accessible reality. The joint venture was established in March 2020 to advance the development and commercialization of the world's highest-performing and safest autonomous vehicles.

Aptiv will contribute its autonomous driving technology, intellectual property, and approximately 700 employees focused on the development of scalable autonomous driving solutions. Hyundai Motor Group affiliates — Hyundai Motor, Kia Motors and Hyundai Mobis — will collectively contribute USD 1.6 billion in cash at closing and USD 0.4 billion in vehicle engineering services, R&D resources, and access to intellectual property.

The Wind River acquisition in 2022 represented perhaps the boldest statement of Aptiv's software ambitions:

Aptiv PLC today announced a definitive agreement to acquire Wind River from TPG Capital, the private equity platform of global alternative asset management firm TPG, for $4.3 billion in cash.

The transaction is valued at $3.5 billion, instead of the initial purchase price of $4.3 billion agreed to in January 2022. Aptiv and the seller agreed to the amended purchase price, in part, as a result of certain changes in Wind River's current operating structure required to bring the regulatory approval process to a satisfactory conclusion.

Wind River software enables the secure development, deployment, operations and servicing of mission-critical intelligent systems. The company's technology is in over two billion edge devices across more than 1,700 customers in high-value industries, including aerospace and defense, telecommunications, industrial, medical and automotive.

"The automotive industry is undergoing its largest transformation in over a century, as connected, software-defined vehicles increasingly become critical elements of the broader intelligent ecosystem," said Kevin Clark, president and chief executive officer of Aptiv.

VIII. The Present and Next Transformation (2023–2026)

In January 2025, Aptiv announced yet another strategic separation—the spinoff of its Electrical Distribution Systems (EDS) business:

Aptiv PLC today announced that its Board of Directors has unanimously approved a plan to separate its Electrical Distribution Systems business from Aptiv, creating two independent companies, each optimally positioned to serve their customers and create value for their shareholders.

"We have a long track record of transforming Aptiv through operational changes and organic and inorganic portfolio shifts to best position our businesses in a dynamic environment. Today's separation announcement represents the next step in our transformation journey. By enhancing strategic and operating focus, we are positioning both Aptiv and EDS to more effectively address the evolving needs of our customers and to further capitalize on market opportunities."

The separation transaction is expected to be effected through a spin-off of EDS, under which Aptiv shareholders will retain their current shares of Aptiv stock and receive a pro-rata dividend of shares of the new EDS company stock. The transaction is expected to be tax-free to Aptiv and its shareholders for both Swiss and U.S. federal income tax purposes. Aptiv is targeting completion of the separation by March 31, 2026, subject to final approval by Aptiv's Board of Directors and other customary conditions.

The Company estimates that Aptiv had $12.1 billion in revenues, including intercompany sales to EDS that are currently eliminated in consolidation, U.S. GAAP operating income, and $2.3 billion in Adjusted EBITDA for 2024, excluding the EDS business to be separated.

In the medium term, Aptiv is targeting pro forma EDS to generate mid-single digit revenue growth, mid-to-high single digit GAAP operating income margins, high-single to low-double digit Adjusted EBITDA margins, and solid free cash flow. The Company estimates that EDS had $8.3 billion in revenues, $0.4 billion in U.S. GAAP operating income, and $0.8 billion in Adjusted EBITDA for 2024, excluding the Aptiv business from which it will be separated.

This appears to be a classic case of a company shedding a business with slim margins and slow growth, leaving behind a high growth, high margin business that they hope will be rewarded with a bigger multiple.

The company's recent financial performance has been solid despite challenging automotive market conditions. Aptiv revenue for the twelve months ending September 30, 2025 was $20.152B, a 2.16% increase year-over-year. Aptiv annual revenue for 2024 was $19.713B, a 1.69% decline from 2023.

Aptiv reported strong Q2 2025 financial results with record revenue of $5.2 billion, up 3% year-over-year. The company achieved U.S. GAAP earnings of $1.80 per diluted share and adjusted earnings of $2.12 per diluted share. Key highlights include Adjusted Operating Income of $628 million with a 12.1% margin, and $510 million cash generated from operations. For full-year 2025, Aptiv projects revenue of $20.0-20.3 billion and adjusted earnings per share of $7.30-7.60.

IX. Playbook: Business & Investing Lessons

The Aptiv story offers several profound lessons for students of corporate strategy and long-term investors:

Serial Spinoffs as Value Creation

From GM to Delphi to Aptiv plus Delphi Technologies to Aptiv plus EDS—this company has used separation as its primary tool for value creation. Each spinoff forced management to confront what businesses truly belonged together and which were better off independent. The upcoming EDS separation represents the fourth major corporate restructuring in the company's history.

Bankruptcy as Transformation

Yet, after all the miscues and false moves, industry analysts suggest the new Delphi bears a striking resemblance to the company that Miller and O'Neal envisioned when they first filed for court protection.

The Delphi bankruptcy demonstrates that Chapter 11 can be a powerful tool for corporate renewal—not just financial restructuring, but fundamental business model transformation. The company that emerged from bankruptcy in 2009 was radically different from the one that entered.

Technology Pivot Through M&A

Clark's acquisition strategy—HellermannTyton, NuTonomy, Wind River—systematically built the technology capabilities that Aptiv needed to compete with Silicon Valley. Each deal targeted specific capability gaps in the company's portfolio.

The Power of Focus

By spinning off Delphi Technologies and now EDS, Aptiv has consistently traded revenue for focus. The post-separation Aptiv will be smaller but more concentrated in high-growth, high-margin segments.

X. Competitive Landscape & Industry Analysis

Porter's Five Forces

Threat of New Entrants (MODERATE-HIGH): In the electrical architecture and connectivity space, primary competitors include Bosch, Continental AG, and TE Connectivity. These companies compete on product innovation, manufacturing scale, and global reach to serve major automotive OEMs worldwide.

The traditional barriers—scale, certification requirements, OEM relationships—remain formidable. However, Competition among Suppliers in ADAS and Autonomous Driving is getting stronger. Emerging Chinese Suppliers and technology giants, such as Baidu and Huawei, threaten the leadership of major Tier-1s in ADAS, such as Bosch, Continental, Valeo and ZF.

Bargaining Power of Suppliers (MODERATE): The semiconductor shortage exposed supply chain vulnerabilities. Aptiv's Wind River acquisition reduces dependency on external software suppliers, representing vertical integration in key technology areas.

Bargaining Power of Buyers (HIGH): Aptiv's customer base is concentrated among major OEMs. However, as vehicles become more software-defined, suppliers like Aptiv gain leverage through their technical expertise.

Threat of Substitutes (MODERATE): Traditional wiring can potentially be replaced by wireless technologies in some applications, though vehicle safety requirements limit this substitution.

Competitive Rivalry (HIGH): Aptiv's top 18 competitors are Autoliv, Valeo, DENSO Auto Parts, Marelli, HARMAN, Bosch Auto Parts, Veoneer, Visteon, DENSO, Delphi Technologies, ZF, Bosch, Continental, AISIN, Lear, Eaton, AAM and Magna.

APTIV ranks high as a competent supplier for Lv.3-4 for carmakers. Bosch and Continental lag behind in Level 3 and Level 4 offerings compared to APTIV.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Aptiv's 141,000 employees and global manufacturing footprint create significant scale advantages in wiring harness production.

Network Effects: Limited direct network effects, though Aptiv's SVA platform could develop switching costs as OEMs build their software stacks on it.

Counter-Positioning: Aptiv's bet on software-defined vehicles represents counter-positioning versus traditional suppliers focused on hardware.

Switching Costs: High switching costs exist once OEMs design vehicles around Aptiv's electrical architecture.

Branding: Limited consumer-facing brand, though strong B2B brand with OEMs.

Cornered Resource: Wind River's VxWorks RTOS and Aptiv's autonomous driving IP represent defensible technology assets.

Process Power: Aptiv's automotive-grade software development and safety certification capabilities are difficult to replicate.

XI. Key Investment Considerations

Bull Case

- Software-defined vehicle transition: Aptiv is uniquely positioned with both hardware (electrical architecture) and software (Wind River, SVA) capabilities

- EDS spinoff unlocks value: Separation of lower-margin business could result in multiple expansion for remaining high-growth segments

- Motional optionality: Joint venture provides exposure to autonomous driving upside with limited capital commitment

- Proven management: Kevin Clark's track record of successful transformations provides confidence in execution

Bear Case

- EV adoption uncertainty: Slower-than-expected EV adoption could pressure growth in high-voltage systems

- OEM concentration risk: Heavy dependence on major automakers creates customer concentration risk

- Autonomous driving timeline: Fully autonomous vehicles remain elusive, potentially limiting Motional's value creation

- Competitive pressure: Tech giants and Chinese competitors are investing heavily in automotive software

Myth vs. Reality

| Myth | Reality |

|---|---|

| "Aptiv is just a parts supplier" | Aptiv's Wind River acquisition makes it a significant automotive software company |

| "The Delphi bankruptcy destroyed all value" | Post-bankruptcy Delphi/Aptiv generated returns far exceeding the S&P 500 |

| "Spinoffs are desperate moves" | Aptiv's serial spinoffs have consistently unlocked shareholder value |

Key KPIs to Monitor

-

Revenue Growth in Advanced Safety & User Experience Segment: This segment represents Aptiv's highest-growth, highest-margin business. Track year-over-year growth and margin expansion.

-

Win Rate on New Vehicle Programs: Aptiv's future revenue depends on winning electrical architecture and ADAS contracts for new vehicle platforms. Track announced wins and their expected revenue contribution.

-

Motional Milestones: Watch for commercial robotaxi deployments, partnership expansion, and any change in Aptiv's ownership stake following Hyundai's increased investment.

XII. Conclusion: The Perpetual Transformation

From GM's parts bin in 1994 to the brain and nervous system of tomorrow's vehicles, Aptiv's journey embodies the perpetual transformation that defines successful companies in periods of technological disruption. The company has survived antitrust concerns, union negotiations, the longest bankruptcy in American history, a global financial crisis, and the fundamental reimagining of the automobile itself.

As the automotive industry undergoes what Kevin Clark calls "its largest transformation in over a century," Aptiv has positioned itself at the intersection of the three megatrends reshaping mobility: electrification, connectivity, and automation. The upcoming EDS spinoff represents yet another chapter in a story that has been defined by reinvention.

For investors, Aptiv offers a compelling case study in how legacy industrial companies can transform themselves for the software-defined future—not through revolutionary breakthroughs, but through patient, disciplined portfolio management and strategic M&A.

As of 30-Jun-2025, Aptiv has a trailing 12-month revenue of $19.8B. As of October 2025 Aptiv has a market cap of $18.39 Billion USD. This makes Aptiv the world's 1182th most valuable company according to our data.

The question for the next chapter is whether Aptiv can complete its transformation from automotive supplier to technology company—and whether Wall Street will reward that transformation with a technology multiple rather than an auto parts multiple. The company's history suggests it knows how to navigate radical change. Whether that skill translates into sustained value creation in an increasingly software-defined automotive world remains the central investment thesis.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube