Alior Bank: Poland's Digital Banking Disruptor

How a startup bank founded during the worst financial crisis in modern history became one of Poland's most innovative financial institutions—and what lies ahead

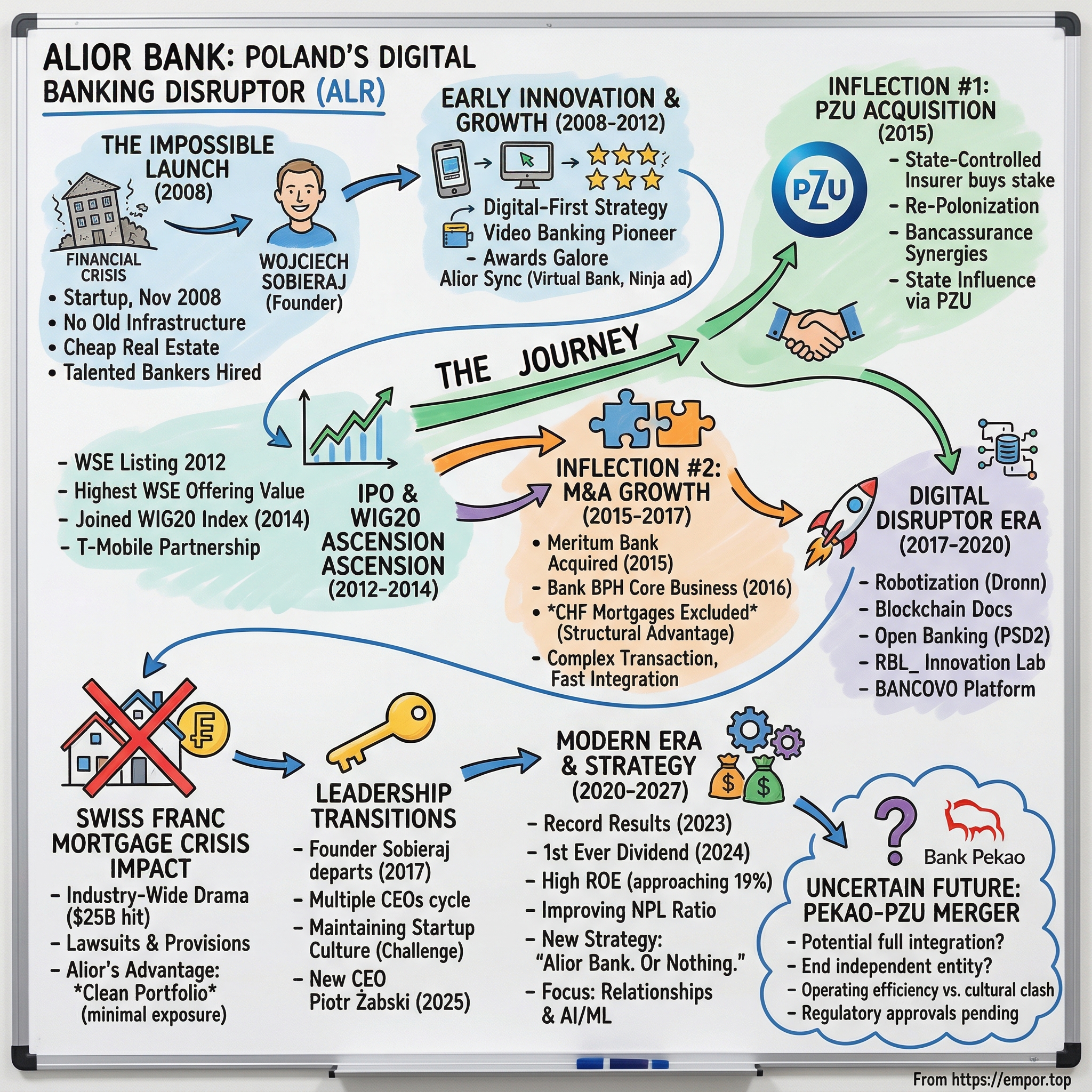

Introduction: The Impossible Launch

Warsaw, November 2008. Lehman Brothers had collapsed just weeks earlier. Global financial markets were in freefall. Banks around the world were being nationalized, merged in desperation, or simply shuttered. Against this apocalyptic backdrop, a 42-year-old Polish-American banker named Wojciech Sobieraj walked into what appeared to be professional suicide: launching a brand-new bank from scratch.

The institution he created, Alior Bank SA, is now a universal bank in Poland founded in 2008. It debuted on the Warsaw Stock Exchange in 2012 with an offering valued at 2.1 billion Polish złoty—the highest in the exchange's history at that time. By 2014, just six years after opening its doors during the worst financial crisis in modern memory, Alior's stock joined the elite WIG20 index, Poland's blue-chip benchmark. Today, the bank serves over four million retail customers and approximately 180,000 corporate clients.

The central question that this story addresses is both simple and profound: how did a bank born during a financial apocalypse become one of Europe's most innovative financial institutions? The answer involves a masterclass in contrarian timing, digital disruption before "digital disruption" was a buzzword, aggressive M&A execution, and the complex dance of operating within a state-controlled insurance conglomerate.

Alior Bank has been a subsidiary of insurance company PZU SA since 2015 and forms the 10th largest banking group in the country, with more than 8,143 employees as of the end of 2019. The themes running through Alior's journey—digital innovation in traditional banking, the "build vs. buy" growth strategy, surviving industry-wide crises, and navigating state ownership—offer insights relevant to any investor analyzing European financial services.

The Polish Banking Context: Market Opportunity in the 2000s

To understand why Alior Bank could exist at all, one must first understand the peculiar structure of Poland's banking sector in the early 2000s. Poland's post-communist economic transformation had created a banking landscape unlike anything in Western Europe.

After the fall of communism in 1989, Poland embarked on one of the most successful economic transformations in modern history. The banking sector was rebuilt almost from scratch. Over 30 years, it went from 100% state ownership through privatisation, with nearly 77% of foreign ownership in 2008, to "repolonization." The breakthrough year was 2020 when government-owned banks constituted nearly 48% of commercial banks' assets.

When Poland joined the European Union in 2004, the banking sector entered a period of extraordinary growth. The FX mortgage became a big business in 2004, when Poland joined the European Union, with hundreds of thousands of Poles taking mortgages in foreign exchange, mainly in Swiss francs. The country was in full development, and in 2004, the future looked bright. The overall belief back then was that the Polish economy could only go up faster than the old economies like Switzerland.

The competitive landscape was dominated by giants. State-controlled PKO BP, the country's largest bank, had never been fully privatized. Bank Pekao, initially sold to Italian UniCredit, represented foreign capital's deep penetration into Polish finance. Foreign capital accounts for more than half of the sector's assets, while state capital makes up slightly less than a third, with the remainder coming from Polish private capital.

As of 2023, the number of commercial banks controlled by Polish capital (including State Treasury) was still 8, whose assets are equal to 56.4% of the sector's total assets, while 43.6% were controlled by foreign entities. The concentration at the top has only intensified over time, with the five largest lenders—PKO BP, Bank Pekao, Santander Bank Polska, ING Bank Śląski, and mBank—holding a combined market share exceeding 55%.

For a would-be disruptor in the mid-2000s, the question was whether there was room for a digitally-native challenger bank. The incumbents were large but often technologically stagnant. Branch networks had been built for a different era. Customer service, by many accounts, was mediocre. The conditions, in retrospect, were perfect for disruption.

For Investors: Poland's banking sector remains relatively concentrated but competitive. Understanding the ownership structure—the interplay between state capital, foreign capital, and domestic private capital—is essential for analyzing any Polish bank. Regulatory and political dynamics around "re-Polonization" continue to shape the sector.

The Founding Vision: Building a Bank from Scratch (2008)

The Alior Bank history began on October 24, 2008. Wojciech Sobieraj founded it with a vision to transform the Polish financial market. He aimed to achieve this through technological innovation and a customer-focused approach.

Sobieraj's biography reads like a template for the globalized Polish executive of the transition era. He graduated from the Warsaw School of Economics in 1990, then in 1993 enrolled at New York University's Stern School of Business, obtaining an MBA in 1995. In 1991–1994, he was the owner of Central European Financial Group in New York, dealing with analysis of the capital markets of Eastern Europe. In that same period, he obtained a license as a broker on Wall Street and worked as an assistant in the Department of Finance and Operations at New York University.

His consulting credentials were equally impressive. From 1997 to 2002, he was an employee, manager and partner at The Boston Consulting Group in Boston and London, and was one of the founders of BCG's office in Warsaw. The combination of Wall Street experience, top-tier consulting pedigree, and deep Polish market knowledge was rare.

Before founding Alior, Sobieraj had already proven he could build banking operations. At Bank BPH, he was part of a team that Józef Wancer assembled with a specific mandate: "build a bank he wouldn't be ashamed of" and "put 40-year-olds in charge." This experience gave Sobieraj both the operational knowledge and the conviction that Poland could support a new kind of bank.

The funding came from an unusual source. Founded in 2008 by an Italian group Carlo Tassara, the bank debuted on Warsaw Stock Exchange in 2012. The Carlo Tassara Group was a holding company controlled by Romain Zaleski, a financier with Polish roots. The investor ready to put money into building a bank from scratch in Poland was found in France—the Carlo Tassara holding, belonging to financier Romain Zaleski with Polish roots. At the end of December 2007, Sobieraj announced his plans and noted in the media that the group's investment in Poland "is not just sentiment to the old country."

The Carlo Tassara group spent over 400 million euros to launch Alior. But the key managers—including Sobieraj—also invested their own money. "We had to commit capital, because that is the principle of a start-up: the investor agrees to enter the project if its creators put everything they have into it. And we did that," the departing president recalled.

Alior Bank officially commenced operations on November 17, 2008, with first branches opened on October 28, 2008. The Carlo Tassara group received permission from the Polish Financial Supervision Authority to establish the bank on April 18, 2008, and on September 1, 2008, Alior Bank SA received permission to begin operations.

In a three-year perspective, Alior Bank intended to acquire 2 to 4% market share depending on segment and gain the trust of approximately one million customers, achieving profitability in its third year of operations. In that period, the bank planned to open 200 branches, 400 agencies, and 300 additional sales points.

The timing—launching during the epicenter of a global financial crisis—appeared insane. But Sobieraj understood something counterintuitive: crisis creates opportunity. Alior Bank could offer what customers needed precisely because it was built from scratch—not burdened by old infrastructure or employee routines. Building IT infrastructure from the ground up allowed keeping costs low, and therefore offering many products and services at competitive prices.

Real estate was cheap. Talented bankers were being laid off elsewhere. Customers, burned by incumbent banks, were desperate for alternatives. High equity capital of 1.5 billion PLN placed Alior Bank among the ten largest banks in Poland from the very beginning of operations.

For Investors: Alior's founding story illustrates a classic venture principle: the best time to build can be during a crisis, when competitors are retrenching and resources are abundant. The founder's skin-in-the-game—with key managers investing their own capital—aligned incentives from day one.

Early Innovation & Rapid Growth (2008-2012)

The first years of Alior Bank's existence demonstrated that the founding thesis was correct. The early growth and expansion of Alior Bank was marked by rapid development. The bank quickly established itself through a digital-first strategy, attracting customers with user-friendly online services and competitive rates. This period saw significant investment in technology and strategic acquisitions.

The bank was a pioneer in adopting new technologies to enhance customer experience and operational efficiency. Early adoption of video banking and advanced mobile banking applications set it apart in the Polish banking landscape.

The awards began accumulating almost immediately. In May 2009, the Alior Bank MasterCard Silver credit card was recognized as the best credit card on the market in the Open Finance ranking. In May 2009, Alior Bank was awarded the title "Best Workplace 2009." In July 2009, Alior Bank introduced Poland's first Debit MasterCard enabling online payments.

In September 2009, Alior Bank received three main awards in the "Newsweek Friendly Bank 2009" ranking in the categories: "Best Retail Bank," "Best Bank on the Internet," and "Best Bank for Seniors." Also in September 2009, Forbes magazine awarded Alior Bank the title "Best Bank for Companies."

The pattern would repeat year after year: best bank for this, most innovative product for that. The cumulative effect was to establish Alior as the go-to option for customers who wanted something different from the staid incumbents.

In June 2012, Alior Sync debuted on the Polish market—the first fully virtual bank in the world. Beyond modern product offerings, the new bank offered services previously unavailable on the market—like transfers on Facebook, Financial Manager, or Virtual Branch, where customers could contact a banker at any time via audio, video, or chat.

This was Alior Sync, a fully digital banking platform that predated many of the fintech "neobanks" that would capture headlines years later. The brand, operated by Alior Bank, was famous for its characteristic advertising campaign featuring a ninja image, symbolizing agility and effectiveness. Fully remote service using chat, voice communication, and video calls with advisors, service in innovative, transparent online banking, and above all, an attractive offer of a completely free account were meant to win Alior the trust of new customers.

In September 2009, Alior Bank entered into an agreement with HSBC regarding the purchase of a portfolio of loans, installment credits, and credit cards. This early acquisition demonstrated an appetite for inorganic growth that would become a defining characteristic of the bank's strategy.

For Investors: Alior's early years established two patterns that would persist: technology leadership and acquisition capability. The awards and customer growth validated the model, while the HSBC portfolio purchase showed the bank could execute on inorganic opportunities.

The IPO & WIG20 Ascension (2012-2014)

Despite the difficult economic environment, Alior Bank quickly established itself in the Polish banking sector through a combination of organic growth and strategic acquisitions. The bank went public on December 14, 2012, with its initial public offering (IPO) on the Warsaw Stock Exchange, which was one of the largest IPOs in Poland's history at that time. The successful IPO provided the bank with capital to fuel its expansion strategy.

The IPO price for institutional investors, who bought the most shares, was 57 PLN, representing nearly a doubling of the amount invested at the beginning. For the original investors and management team who had bet their capital on a startup bank during a financial crisis, the IPO represented vindication—and substantial returns.

In 2014, Alior's stock price became part of the WIG20 index. For a six-year-old bank to join Poland's blue-chip index was remarkable. The WIG20 comprises the largest and most liquid companies on the Warsaw Stock Exchange. Inclusion meant institutional buying, increased visibility, and validation of Alior's emergence as a major player.

Not everything was smooth sailing. In 2013, the bank attracted controversy when its deputy president mentioned that the bank considers collecting big data of its customers, pulling information from online social networks. The privacy concerns were prescient of debates that would consume the tech industry years later, but they also showed Alior was thinking ahead—perhaps too far ahead—of prevailing norms.

Alior Bank received numerous awards for its outstanding customer service, such as being named the best bank in Poland by Bloomberg in 2014 and 2015. The Bloomberg recognition from one of the world's most prestigious financial media companies confirmed that Alior had transcended its startup origins.

The T-Mobile partnership represented another innovation milestone. In May 2014, as part of a strategic alliance between Alior Bank and T-Mobile operator, the T-Mobile Banking Services delivered by Alior Bank brand appeared on the market. This first project of cooperation between a bank and a telecommunications company realized on this scale in Europe provided modern banking services to T-Mobile Poland customers and customers of the former Alior Sync. The partnership allowed offering innovative solutions in internet and mobile technology as well as products and services combining unique benefits from cooperation that no bank could offer alone. After one year from the market launch, T-Mobile Banking Services served half a million people.

T-Mobile and Alior wanted their joint bank to acquire 2 million customers within five years. The agreement was signed for five years with an option to extend for another five. The model was innovative: a telecommunications company and a bank combining their customer bases and technology capabilities.

For Investors: The IPO-to-WIG20 trajectory in just four years demonstrated execution capability. The T-Mobile partnership showed creative thinking about distribution and customer acquisition. Both would become templates for later initiatives.

Inflection Point #1: The PZU Acquisition & "Re-Polonization" (2015)

In June 2015, state-controlled PZU, Poland's largest insurer, agreed to buy a 25.3-percent stake in Alior Bank. Currently, the PZU SA Group holds 31.94% of shares in Alior Bank.

In 2015, a significant change in ownership occurred when PZU Group (Powszechny Zakład Ubezpieczeń), Poland's largest insurance company, acquired a controlling stake in Alior Bank. This acquisition was part of PZU's strategy to build a financial group that would combine insurance and banking services.

In May 2015, PZU reached a preliminary agreement to acquire a 25.3% stake in Alior Bank from Italian investor Carlo Tassara for 1.63 billion Polish zloty (approximately 431 million USD) at 89.25 zloty per share, aiming to consolidate banking operations and form a top-five Polish banking group by assets. The transaction was completed in March 2016, granting PZU a 25.2% holding and positioning it as Alior's anchor shareholder.

The transaction must be understood in the broader context of Polish politics. Since coming to power in late 2015, Poland's nationalist Law and Justice Party (PiS) embraced public-sector banking with enthusiasm. In its first two years in government, PiS sponsored the acquisition of three banks by state-controlled insurer PZU, including the successful challenger bank Alior and second-place player Bank Pekao. As market leader, PKO BP was never fully privatized—this means around 30% of banking assets in Poland are now under state control.

State influence on Alior Bank derives indirectly through PZU, whose largest shareholder is the Polish State Treasury with a 34.2% direct stake as of May 2025, conferring effective governmental oversight. PZU acquired its initial 25.19% stake in Alior in 2015, later increasing it to a controlling position amid a broader Polish government push under the then-ruling Law and Justice party to enhance national control over banking assets previously dominated by foreign entities.

PZU SA's CEO Andrzej Klesyk told reporters that PZU's goal is to "create one of Poland's top five lenders." The Alior purchase is the "first step for us to consolidate the Polish banking industry."

This investment marked a shift from Alior's earlier private-led growth model toward state-backed scaling, enabling synergies in bancassurance—cross-selling PZU's insurance products through Alior's branch network—and cost efficiencies estimated at over 160 million zloty annually from integrated operations.

For Alior, the PZU acquisition brought both advantages and challenges. On one hand, it provided a deep-pocketed owner capable of supporting aggressive expansion. On the other, it introduced the complexities of operating within a state-controlled conglomerate, with potential for political influence over commercial decisions.

A major element of the PZU Group's business model is the banking business. The tightening of cooperation with the banks within the PZU Group (with Alior Bank and Bank Pekao acquired by the Group in 2015 and 2017, respectively) has opened up tremendous growth opportunities, especially in terms of integrating and focusing services on clients at every stage of their personal and professional development.

For Investors: The PZU acquisition fundamentally changed Alior's ownership dynamics. Investors must understand that the bank operates within a state-influenced ecosystem, with both synergies (insurance cross-selling, capital support) and risks (political interference, competing priorities with sister bank Pekao).

Inflection Point #2: The M&A Growth Strategy (2015-2017)

Since 2015, the bank commenced a series of mergers and acquisitions, most notably acquiring Meritum Bank (2015) and Bank BPH (2016).

The Meritum Bank Acquisition

In autumn 2014, Alior Bank purchased 97.9% of Meritum Bank. On February 19, 2015, the transaction was finished. On June 23, 2015, the Polish Financial Supervision Authority authorized the merger of Alior Bank S.A. and Meritum Bank ICB S.A. by transferring all of Meritum Bank's assets to Alior Bank. The banks merged on October 24–26, 2015.

The Meritum acquisition for approximately 352 million PLN added scale and customers to Alior's platform. But the main event was yet to come.

The Bank BPH Core Business Acquisition

Under PZU's ownership, Alior Bank continued its expansion, most notably with the acquisition of Bank BPH's core business from GE Capital in 2016, which significantly increased Alior's market share in the Polish banking sector.

GE announced that on November 4, 2016, it completed the spin-off and merger of Bank BPH's Core Bank to Alior Bank, representing aggregate ending net investment (ENI) of approximately $3.6 billion at the end of the third quarter 2016.

On March 31, 2016, Alior Bank concluded with GE Capital group an agreement regarding the purchase of the demerged part of Bank BPH. The transaction excludes the mortgage loan portfolio (in CHF, other currencies and Polish złoty) as well as BPH TFI. The acquisition of the demerged part of Bank BPH is in line with the development strategy of Alior Bank and will be an important step in the consolidation of the banking sector.

The structure of this deal was critical. The transaction does not carry to Alior Bank any risk connected with the potential CHF mortgage conversion. By explicitly excluding the Swiss franc mortgage portfolio—which would become an industry-wide nightmare—Alior protected itself from a time bomb that would detonate at other banks.

Greenberg Traurig advised Alior Bank in an agreement to acquire Bank BPH's core business from affiliates of GE Capital. The agreement was signed on March 31, 2016. Alior Bank valued Bank BPH's core business at PLN 1.5 billion.

This transaction is now widely recognized as the most complex transaction in the field of financial institutions M&A in Poland. It involved several complex parts that the Greenberg team welded together in order for the deal to go through.

Upon the merger, Alior Bank assets reached approximately PLN 60 billion, placing Alior Bank at 9th position in the banking sector. The experience of both banks' employees will form a solid basis for the development of innovative products and service offering. Alior Bank expects to benefit from pre-tax annual synergies of approximately PLN 300 million, before including PLN 160 million of synergies resulting from the implementation of the Remedy Plan. The full run-rate synergies were envisaged to be achieved in 2019.

The target synergies generated by the merger with Core Bank BPH at PLN 381 million were achieved already in 2018, one year earlier than initially expected. The merger with Core Bank BPH was the fastest and one of the most efficient acquisitions in the Polish banking sector, completed within months.

For Investors: The BPH acquisition demonstrated sophisticated M&A execution—particularly the exclusion of CHF mortgages that would burden competitors for years. The synergy realization ahead of schedule suggested strong operational integration capabilities.

The "Digital Disruptor" Strategy Era (2017-2020)

The banking industry was going through a technological revolution as clients used products and processes over digital channels on a mass scale. With fewer visits to bank branches and fewer transactions made over the counter, financial operations went digital. To address these trends, Alior Bank launched a "Digital Disruptor" strategy for 2017-2020 to become even more innovative and customer-friendly and to strengthen its capital position. The strategy aimed to maintain the highest net interest margin in the industry (4.5%), reduce C/I to 39%, and provide shareholders with return on equity rising from 8% in 2016 to 14% in 2020.

"The objective of Alior Bank is to remain a Polish innovation leader and to become a top five innovative bank in Europe. The Bank will invest another PLN 400 million in innovative technological projects in the next four years on top of the originally planned investment in IT development and system maintenance."

According to the Digital Disruptor strategy, innovation is the foundation of Alior Bank's competitive advantage. Alior Bank's capabilities of in-house incubation of fintech business models came to fruition in 2017 with the launch of the BANCOVO platform, a fully digital transactional intermediary in the cash loan market.

The strategy involved multiple pillars:

Robotization: development of Dronn functionalities and continuously thinking about adopting them to other areas. Robo Factory, which has automatized processes of repetitive activities, helped Alior's employees to focus on more complicated challenges. 70 processes had already been changed, and by 2020 Alior Bank would have robotized almost 120. Blockchain: as one of the first banks in the world, Alior Bank implemented open blockchain for document authentication. The Bank adopted this technology as it benefits customers and lowers costs. Open Banking: PSD2 revolution will give the Bank a place among market leaders.

In 2018, Alior Bank established RBL_, an innovation laboratory, which was named one of 25 Best Financial Innovation Labs in 2019 by Global Finance magazine.

The innovation lab has nearly 50 people. Global Finance Magazine awarded Alior Lab—for the second time—as being one of 25 best financial innovation labs in the world.

Efma-Accenture's Banking Innovation of the Month award for June 2019 went to Alior Bank for Smartphonisation, a new mobile way of working. Alior Bank was the first bank in Poland to equip its employees with ready-to-use smartphones to put them at the heart of the bank's digital transformation. The devices came with a tailored, preinstalled set of applications, including cloud collaboration, video chats, and messenger utilities. These tools enhanced the employee experience. This move was part of Alior's 'Digital Disruptor' strategy and denoted a shift from customer-centric to employee-centric experience.

In response to the EU's requirement to store terms, tariffs, and pricing tables on a "durable medium" such as paper, Alior unveiled a document authentication feature built on top of the public Ethereum blockchain. In 2021, it launched an AI voice assistant named InfoNina which is a customer's first point of contact when they call the bank. If InfoNina can't help them, the bot sends the customer to a human rep. InfoNina also proactively calls customers if any of their information on record isn't accurate or needs updating. Alior also implemented a bill consolidation service called BillTech into their mobile app.

In 2018, the bank became a member of the Blockchain and New Technologies Chamber and had been actively supporting initiatives aimed at developing blockchain technology in the country.

For Investors: The Digital Disruptor strategy positioned Alior as a technology leader, not just a traditional bank with a mobile app. The innovation lab, blockchain implementations, and AI initiatives created competitive differentiation that could support premium pricing and customer retention.

Inflection Point #3: The Swiss Franc Mortgage Crisis Impact

The Swiss franc mortgage crisis represents one of the most significant regulatory and financial events in Polish banking history—and Alior's positioning relative to it has been a structural advantage.

The number of franc mortgage loans peaked in 2008, when almost 70% of all outstanding mortgages were issued in the franc.

In 2008, for example, the annual interest rate in Zlotys was around 8.7%, compared to the one in Swiss francs at 4.4%. On January 15, 2015, Switzerland announced scrapping its currency peg with the euro. The Swiss franc jumped 20%. The Polish Zloty to Swiss franc exchange rate jumped from 3.5 to 5 Zloty overnight.

It was a societal drama for many, leading to a revolt of close to 20% of customers who started claims against their bank. The ruling means that Polish banks are facing a $25 billion hit on the ongoing Swiss franc mortgage case, equal to 50% of own funds held by local commercial banks. Despite the ruling, the financial regulator stressed that Polish lenders were safe.

By the end of Q3 2024, Polish banks had reported a staggering 120,500 active lawsuits—an increase of over 14,000 cases compared to the end of 2023. Polish common courts ruled in favour of consumers in approximately 97% of verdicts.

KNF chair Jastrzębski told an economic conference that while banks could afford to absorb the full cost of the Swiss-franc mortgage debacle, it would reduce their ability to finance other activities. "Banks have sufficient capital for the time being but not sufficient to invest also in the green transition, our security and help companies in the reconstruction of Ukraine," he said.

Alior's Advantaged Position

Here is the critical point: The BPH transaction did not carry to Alior Bank any risk connected with the potential CHF mortgage conversion. The bank was founded in 2008, precisely when the CHF mortgage boom was at its peak—meaning Alior largely avoided building this legacy problem into its loan book.

Regarding provisions for the CHF portfolio in Q4 2025 and 2026: "It depends on how fast new cases are opened. In Q4, we expect a slightly higher number, similar to Q3, but these numbers should be lower in the coming quarters. Our CHF portfolio is disproportionately lower than other banks, so it's a fractional number."

This represents a structural advantage versus older competitors. Foreign-currency mortgages contributed to the collapse of Getin Noble Bank SA in 2022. Bank Millennium has the highest percentage of Swiss franc mortgages among Poland's largest banks at 9.4%, followed by mBank SA with 5.4%. Alior's minimal exposure means capital that competitors must reserve for CHF litigation can instead be deployed for growth or returned to shareholders.

For Investors: The CHF mortgage crisis is the gift that keeps on giving—for Alior. While competitors face ongoing litigation costs, provisioning requirements, and management distraction, Alior operates largely unencumbered. This structural advantage should persist for years as the litigation plays out.

Founder Departure & Leadership Transitions (2017-Present)

The idea for Alior Bank arose in 2007 and quickly came to life as a specific business plan. The originator and founder of the institution was Wojciech Sobieraj, who led the bank from its inception until June 2017.

From 2008 to 2017, Wojciech Sobieraj served as CEO of Alior Bank, which at the time was Europe's largest banking startup, employing over 10,000 people at the end of 2016.

After nearly a decade at the helm, Sobieraj stepped down in 2017. His departure marked the end of an era—the founder who had built the institution from scratch, surviving the financial crisis and navigating through IPO, acquisitions, and the PZU ownership transition.

In 2018, together with Wojciech Sass and a group of other managers, Sobieraj founded Aion Bank and Vodeno, offering banking-as-a-service across Europe. Alior Bank founder Wojciech Sobieraj launched a bank in Belgium—Aion Bank—one of the most modern banks on the continent and in the world.

Interestingly, Sobieraj once again launched a bank in the middle of a crisis. In November 2008—at the epicenter of the financial crisis—Alior Bank launched, which focused on high quality customer service. The pattern repeated with Aion, founded during the COVID-19 crisis.

The post-Sobieraj era brought leadership instability. Multiple CEOs cycled through the position, reflecting the challenges of maintaining startup culture within a state-controlled insurance conglomerate.

Following a competition announced in May 2024, Piotr Żabski was appointed CEO of Alior Bank as of January 1, 2025. The positions of Vice Presidents were taken by Jacek Iljin, Wojciech Przybył, Marcin Ciszewski, and Zdzisław Wojtera.

Alior Bank S.A. announced the appointment of Piotr Zabski as the new CEO of Alior Bank as of January 1, 2025. From August 15, 2024, until Piotr Zabski took over, the work of Alior Bank's management board was headed by Jacek Iljin.

The new leadership team brings experience from across the Polish financial sector—Euro Bank, Credit Agricole's EFL, mBank, and others—suggesting a focus on operational excellence and integration capabilities.

For Investors: Leadership stability has been a challenge post-Sobieraj. The new management team's ability to execute on strategy while navigating the complex PZU-Pekao-Alior relationship will be critical to watch. Key question: can hired managers maintain the innovation culture that a founder created?

Modern Era: Technology, Results & Record Performance (2020-2025)

Despite leadership transitions and the COVID-19 pandemic, Alior delivered strong performance in the 2020s.

At the end of 2023, Alior Bank achieved record results. Net profit amounted to PLN 2.03 billion, an increase of PLN 1.35 billion compared to the 2022 result. In April 2024, the General Meeting of Alior Bank decided to pay the first-ever dividend from the 2023 profit of PLN 577 million (PLN 4.42 per share).

The first-ever dividend marked a milestone: Alior had transitioned from a growth-focused startup to a mature, capital-returning institution.

Alior Bank SA reported a strong return on equity (ROE) close to 19%, aligning well with strategic goals. The bank's net profit in Q3 2025 amounted to 563 million PLN, contributing to a year-to-date profit of 1.679 billion PLN. The number of relationship customers grew by 100,000 year on year, reaching 1.68 million, indicating successful customer acquisition strategies. Alior Bank SA achieved a significant increase in mortgage sales, with a 111% year-on-year growth, contributing to portfolio stability.

Total assets grew 7% to nearly 100 billion PLN, and deposits rose 8% to exceed 80 billion PLN. The customer base continued to expand, with 1.68 million relationship clients, up by 100,000 year-on-year, and mobile app users increasing 15% to 1.59 million.

Alior Bank was awarded a total of 55 times in nationwide competitions and industry rankings in the first half of 2025. The most important awards included: Top Employer 2025, 2nd place in the Banking Star ranking, the Golden Grand Prix in the Polish Contact Center Awards, and 5 individual distinctions in the Polish National Sales Awards. The bank was also recognized in the Institution of the Year competition (6 categories), the Golden Banker plebiscite, Invest Cuffs 2025, and by the Polish Association of Developers.

In 1Q 2025, Alior Bank achieved very good financial results. The number of mobile app users was 1.33 million (16% more than at the end of 1Q 24). The number of customers with a main relationship was 1.05 million (56k more than at the end of 1Q 24). Very strong and safe capital position with Tier 1 and TCR at 17.37%. High surplus over regulatory minimums: for Tier 1 it's 8.86 pp. (PLN 5.0 billion), for TCR it's 6.86 pp. (PLN 3.9 billion).

While a one-off corporate default affected quarterly results, the non-performing loan (NPL) ratio improved to 6.29%, down 0.81 percentage points from the previous year. The bank expects the ratio to decline further to below 5% by 2026.

For Investors: Alior's financial performance has been strong, with ROE approaching 19% and improving credit quality. The first dividend payment and declining NPL ratio suggest a maturing business with capacity for ongoing capital returns.

The 2025-2027 Strategy: "Alior Bank. Or Nothing"

The Bank's 2025–2027 strategy ("Alior Bank. All or nothing.") guides current operations, with the Alior Bank Group recording a net profit of PLN 1,117 million in H1 2025 and achieving strong return on equity.

The new strategy emphasizes customer relationships and fee income diversification to prepare for an anticipated interest rate decline.

As at the end of June 2025, the Tier 1 and TCR capital ratios significantly exceeded the regulatory minimums by 846 bp (PLN 4.9 billion) and 646 bp (PLN 3.8 billion) respectively. Strategic priorities include an agile distribution model and digital channel expansion, implementing modern analytics tools and developing AI/ML capabilities.

The strategy targets ambitious metrics: ROE above 18% by 2027, dividend payout exceeding 50% of net income, and profit targets of 2.6 billion zlotys by 2027.

But the most significant strategic development is the potential integration with Bank Pekao.

The Pekao-PZU Merger: Alior's Uncertain Future

Poland's biggest insurer PZU SA plans to sell a nearly $1 billion stake in Alior Bank SA to Bank Pekao SA in the first major corporate transaction overseen by Prime Minister Donald Tusk's year-old government. PZU and Pekao—the country's second-largest lender—signed a non-binding letter of intent regarding the sale. The planned deal involving three government-controlled firms seeks to eliminate a situation where an insurer effectively controls two major commercial banks.

On June 1, 2025, PZU SA and Bank Pekao SA signed a memorandum of understanding aimed at reorganizing and enhancing the efficiency of the capital group. The potential transaction outlined in the memorandum—subject to a number of conditions and required approvals—could release a capital surplus of up to PLN 20 billion. The merged banking and insurance group will become one of the largest financial institutions in Europe.

The memorandum of understanding outlines a plan of actions preparing the transaction, which is initially expected to be finalized in mid-2026. Its implementation is still dependent on many factors, including the agreement of the relevant transaction documentation, entry into force of appropriate legislative changes, obtaining a number of regulatory approvals, and granting appropriate corporate approvals. In the course of further work, the parties also want to develop an optimal strategy for the future of Alior Bank.

A merger with Alior Bank would strengthen Bank Pekao's position as Poland's second-largest lender by assets, loans and deposits, narrowing the gap with sector leader PKO Bank Polski SA. A deal could reduce operating costs and improve efficiency for both banks, while expanding Bank Pekao's operations and creating economies of scale. "But we are skeptical about obtaining significant revenue synergies." "Additionally, both banks complement each other in their product offerings: Pekao excels in corporate banking and mortgages, while Alior specializes in cash products."

Both brands will maintain their "identity, distinctiveness and autonomy of activity" in their respective business areas, but the group would be led by a bank, not an insurer. The companies also plan to develop an optimal strategy for Alior Bank, in which Pekao will have a 32% stake.

For Investors: The PZU-Pekao merger creates fundamental uncertainty about Alior's future. Scenarios range from full integration with Pekao (eliminating Alior as a separate listed entity) to continued independent operation under new ownership. This uncertainty may weigh on valuation until resolution.

Competitive Position & Strategic Analysis

Porter's Five Forces Analysis

Threat of New Entrants (Moderate): Banking licenses remain difficult to obtain, but digital neobanks and foreign entrants (like Revolut) are increasingly active in Poland. Alior's digital heritage provides some insulation.

Bargaining Power of Suppliers (Low): Technology vendors and deposit providers have limited bargaining power given multiple alternatives and the bank's scale.

Bargaining Power of Customers (Moderate-High): Polish consumers are price-sensitive and switching costs have decreased with open banking. However, Alior's digital experience creates some stickiness.

Threat of Substitutes (Increasing): Payment apps, buy-now-pay-later services, and cryptocurrency platforms are nibbling at traditional banking services. Alior's digital positioning helps defend against some of these threats.

Industry Rivalry (High): The Polish banking sector is competitive, with PKO BP, Pekao, Santander, ING, and mBank all vying for customers. Both banks have delivered strong return on equity over the past five quarters, with Alior Bank's ratio consistently exceeding 20%. But Alior's nonperforming loan ratio remains higher than Pekao's, though it has been trending downward.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Alior has achieved meaningful scale but remains smaller than the top banks. The potential Pekao combination would significantly enhance scale advantages.

Network Economies: Limited in traditional banking; the T-Mobile partnership attempted to create network effects but ultimately ended.

Counter-Positioning: Alior's founding thesis was counter-positioned against stodgy incumbents. This advantage has eroded as competitors have improved their digital offerings.

Switching Costs: Moderate and declining with open banking mandates.

Branding: The "Alior" brand carries positive associations with innovation and customer service, validated by numerous awards.

Cornered Resource: The absence of CHF mortgage exposure could be considered a cornered resource—a structural advantage competitors cannot easily replicate.

Process Power: Alior's technology infrastructure and integration capabilities represent potential process power, evidenced by the rapid BPH integration.

Bull and Bear Case Analysis

Bull Case

-

CHF Mortgage Advantage Persists: As competitors continue absorbing CHF mortgage litigation costs, Alior's clean portfolio enables investment in growth or capital returns.

-

Pekao Acquisition Premium: If Pekao acquires Alior outright, shareholders may receive a premium to current trading prices.

-

Digital Leadership Pays Off: Investments in AI, mobile, and automation translate into superior cost efficiency and customer acquisition.

-

Interest Rate Tailwind: While rates are expected to decline, any slower-than-expected path would benefit net interest income.

-

Poland Economic Growth: As one of Europe's fastest-growing economies, Poland offers secular tailwinds for banking.

Bear Case

-

Integration Risk: A Pekao merger could be value-destructive, with execution challenges, cultural clashes, and customer attrition.

-

Interest Rate Decline: Lower rates compress net interest margins, the bank's primary income source.

-

Competitive Pressure: Intensifying competition from fintechs and aggressive incumbents erodes market share.

-

Political Risk: State ownership introduces potential for political interference in commercial decisions.

-

NPL Deterioration: Economic stress could reverse the improving NPL trend, requiring increased provisioning.

Key Performance Indicators to Track

For investors monitoring Alior Bank, three metrics deserve particular attention:

-

Net Interest Margin (NIM): Currently among the highest in the Polish banking sector. Tracks the bank's ability to maintain spread income as rates decline. The bank anticipates a further drop in net interest margin (NIM) by about 10 basis points in the next quarter, indicating ongoing pressure on interest income.

-

NPL Ratio: Currently at 6.29% and declining, but still higher than peers. A key indicator of credit quality evolution and provisioning needs.

-

Cost-to-Income Ratio: Measures operational efficiency. The Digital Disruptor strategy targeted 39% C/I—tracking progress against this benchmark reveals execution success.

Regulatory and Legal Considerations

CHF Mortgage Litigation: While Alior's exposure is minimal, sector-wide developments could affect sentiment and regulatory responses. Landmark court rulings from the CJEU and Polish Supreme Court have strengthened borrowers' positions, and anticipated procedural reforms in 2025 are expected to improve judicial efficiency and provide consumers with faster, more effective legal remedies.

PZU-Pekao Merger Approvals: The proposed merger requires regulatory approvals, legislative changes, and shareholder consent. Timeline and structure remain uncertain.

Capital Requirements: Evolving European banking regulations (CRR3, MREL requirements) affect capital planning and dividend capacity.

Conclusion: The Next Chapter

Alior Bank's story is one of improbable success—a startup bank founded during the worst financial crisis in modern history that became one of Poland's largest and most innovative financial institutions. The digital-first strategy, aggressive M&A execution, and fortunate avoidance of the CHF mortgage crisis have created a bank with strong fundamentals and distinctive positioning.

The coming years will test whether this success can persist. The PZU-Pekao merger dynamics create fundamental uncertainty about Alior's future as an independent entity. Leadership transitions post-Sobieraj raise questions about cultural continuity. Interest rate declines threaten the net interest income that drives profitability.

Yet the bank enters this period of transition from a position of strength. Capital ratios significantly exceed regulatory minimums. Credit quality is improving. Digital capabilities remain industry-leading. The first-ever dividend demonstrated the business had matured enough to return capital to shareholders.

For long-term investors, Alior represents a play on Polish financial sector consolidation, with the added optionality of either remaining independent with strong fundamentals or receiving an acquisition premium. The key risks—execution on any integration, interest rate pressure, and political interference—are real but manageable given the bank's capitalization and competitive position.

Wojciech Sobieraj's original thesis—that Poland could support a digitally-native, customer-focused challenger bank—has been validated beyond any reasonable doubt. The question now is whether the institution he built can write the next chapter of its story without its founder and potentially without its independence. That answer will determine whether "Alior Bank. Or Nothing" becomes aspirational vision or ironic epitaph.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube