Allegro.eu: Central Europe's E-Commerce Champion

How a basement startup in Poznań fended off eBay, Amazon, and Chinese giants to become the region's dominant online marketplace

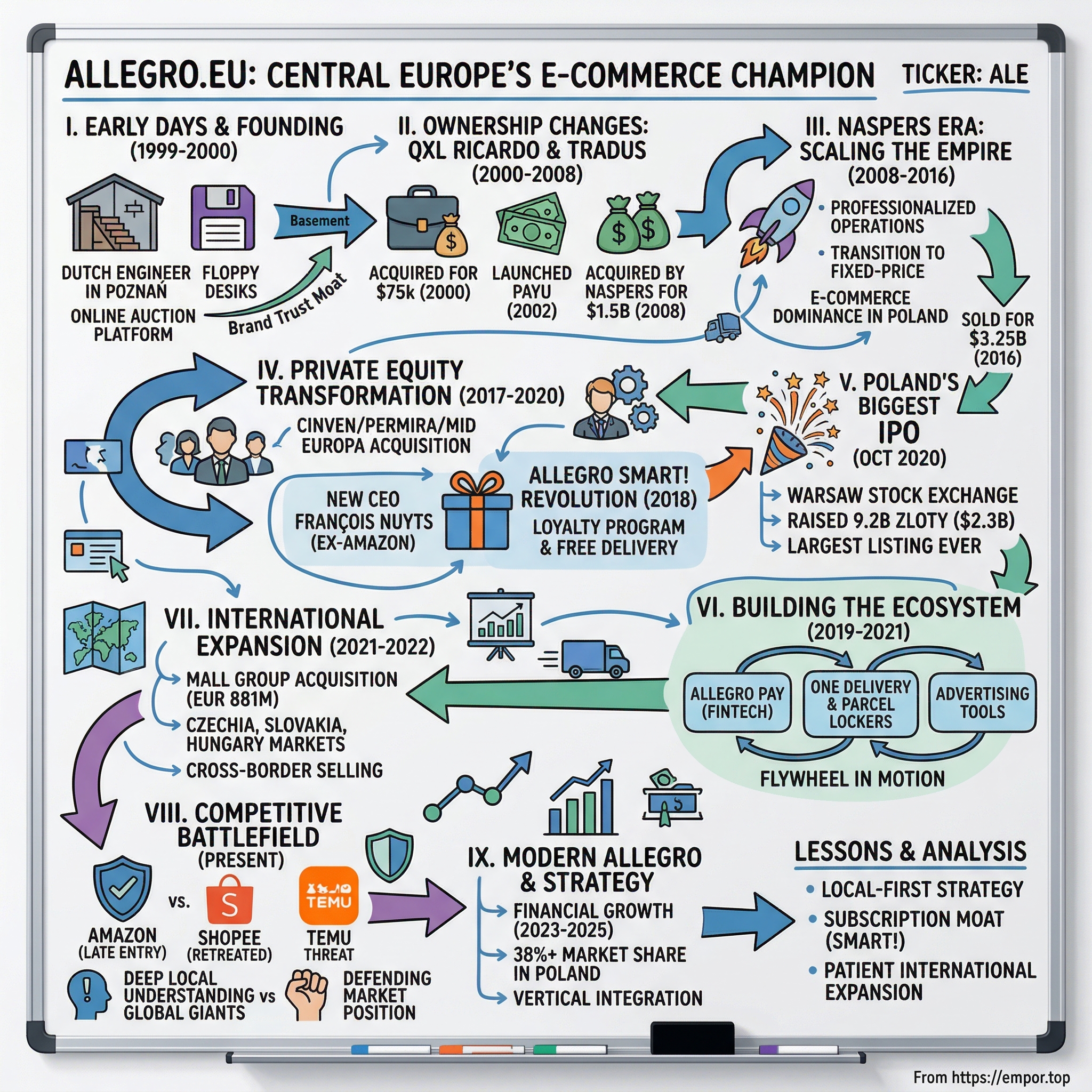

I. Introduction: The Polish Amazon Nobody Saw Coming

Picture this: It's 2025, and Poland—a country of 38 million people in the heart of Europe—hosts one of the world's top ten e-commerce platforms by traffic. A marketplace that has successfully repelled eBay, watched Shopee retreat after just 15 months, kept Amazon to less than 4% market share despite a four-year head start, and is now locking horns with Temu, the hyperaggressive Chinese newcomer backed by billions in marketing spend.

Allegro has been developing its platform since 1999 and remains the go-to online shopping place for millions of Poles despite growing competition from international players. Its share of the Polish retail e-commerce market was 38.8% at the end of 2024, according to Euromonitor International. Amazon held a 3.9% share, followed by AliExpress with 3.4% and Temu with 1.5%.

Those numbers tell only part of the story. Allegro is Central and Eastern Europe's largest and most trusted e-commerce platform and the largest e-commerce player of European origin. Founded in Poland in 1999, it has grown into a regional leader, connecting over 20.8 million active buyers with more than 160,000 merchants across Poland, Czechia, Slovakia, Hungary, Croatia, and Slovenia.

The central question that makes Allegro's story so compelling for business students and investors alike: How did a platform born in a basement in post-communist Poland not only survive but dominate against some of the most well-capitalized and sophisticated competitors in global e-commerce?

Poland entered e-commerce later than Western Europe. This gave local platforms time to establish themselves before Amazon showed up—unlike Germany or France, where Amazon dominated early. But timing alone doesn't explain Allegro's resilience. The answer lies in a combination of first-mover advantage, deep local understanding, strategic ecosystem building, multiple ownership transitions that paradoxically strengthened rather than weakened the company, and a subscription loyalty program that would make Amazon Prime blush with envy.

This is the story of five inflection points: the founding vision that anticipated eBay's model, the Naspers era that professionalized operations, the private equity transformation that launched Allegro Smart!, the pandemic-fueled IPO that became Warsaw's largest ever, and the Mall Group acquisition that opened the gates to Central European expansion. Along the way, we'll explore why global giants have struggled in Poland, what the Temu threat really means, and whether Allegro can successfully export its playbook beyond its home market.

Let's dive in.

II. Origins: Poland's Internet Frontier (1999–2000)

A Dutch Engineer in Poznań

Allegro was founded in 1999 in Poznań by Dutch entrepreneur Arjan Bakker as an online auction platform. Bakker had never been involved in IT before. Being a chemical engineer, he worked in marketing and sales in the chemical company DSM in the Netherlands.

The origin story reads like an unlikely tech fairy tale. When he was 25, Bakker was invited to Poland by his friend to establish their own firm that imported office equipment, wooden items and then distributed software for finance and computer hardware. Poland in the late 1990s was a nation in transition—emerging from decades of communist rule, hungry for Western goods and business models, with a young population eagerly discovering the internet.

The history of the largest e-commerce platform in Poland dates to 1999, with Arjan Bakker as its originator and Tomasz Dudziak as its first programmer. The company took steps in the basement of a computer warehouse in Poznan.

Bakker aimed to replicate the eBay model in the Polish market by creating an online auction platform for private individuals. The site launched on December 13, 1999, with its inaugural auction for a USB camera, marking the beginning of operations as a digital alternative to traditional flea markets.

The development timeline was remarkably compressed. The initial version of the software was developed in just three weeks by programmers Łukasz Ćwikła and Robert Marciniak, enabling rapid deployment despite limited resources. The software was so compact it fit on a single floppy disk—a quaint detail that speaks to both the technical simplicity of the era and the scrappy, resource-constrained nature of the founding team.

The Right Moment in Polish History

To understand why Allegro succeeded where others might have failed, you need to understand Poland at the millennium's turn. The country was experiencing rapid economic transformation. Internet penetration was growing, but still low enough that early movers had room to establish dominant positions. Poland's large, educated population was developing purchasing power for the first time in generations.

In the early 2000s, Allegro experienced swift adoption amid Poland's growing internet penetration, transitioning from a niche auction service to the country's leading e-commerce site by outcompeting entrants like eBay, which failed to gain significant traction locally. The platform's user-friendly interface and focus on local needs, such as support for Polish language and payment methods, drove organic growth.

Bakker felt instinctively that here was a nation that would like an online journey through hundreds of listings. He set Christmas time of 1999 for the launch of his auction website.

The timing proved prescient. While Western European markets were being contested by well-funded American players, Poland represented virgin territory. eBay, which would later attempt to enter, was focused on more developed markets. Amazon was years away from even considering Poland. The window was open, and Bakker walked through it.

Early Chaos and Opportunity

Various mistakes and failures of the service did not disrupt the development, and users were snooping around Allegro, as in their own drawers. They were constantly selling and buying something, from millions of auctions. Some scandals happened, such as the auction with a minimum price of 1 PLN for a sea yacht listed, which was bid by one buyer and for this amount went under the hammer—in accordance with the rules and the law, the new yacht was passed to the lucky buyer.

These early mishaps, far from damaging the platform, became part of its folklore. Polish internet users embraced Allegro as their marketplace—chaotic, occasionally unpredictable, but authentically local. After his first 10,000 users registered, British investment group QXL Ricardo became interested in investing in ingenious Bakker.

For investors evaluating Allegro today, the founding story matters because it established something that would prove remarkably durable: brand trust. Unlike platforms that entered Poland later as foreign entities, Allegro was born Polish. It spoke Polish, understood Polish consumers, and grew organically with the Polish internet generation. This native authenticity would become its most formidable competitive moat.

III. Early Ownership Changes: QXL Ricardo & Tradus (2000–2008)

The First Exit

In 2006, after a year of its establishment, a price comparison website Ceneo.pl became a part of Allegro. After that, in 2008, both companies were acquired by global South African internet group Naspers for $1.5 billion.

But before Naspers, there was QXL Ricardo. Almost immediately after launching, in March 2000, Allegro was purchased by the British online auction site QXL Ricardo plc for $75,000. The company was formed in 1999 and subsequently purchased by QXL Ricardo plc in March 2000. QXL Ricardo plc changed its name to Tradus plc in 2007.

For Bakker and his small team, this represented validation—and capital. For QXL Ricardo, Allegro was a bet on Central European e-commerce at a time when few understood its potential. The acquisition price of $75,000 seems laughably small in hindsight, but reflected both the nascent state of the business and the broader skepticism about internet valuations following the dot-com crash.

Building the Ecosystem Early

The period between 2000 and 2008 saw Allegro evolve from a simple auction platform into something more sophisticated. In 2002, when the number of auctions exceeded 1 million, Allegro launched its online payment system PayU—a move that would prove strategically brilliant.

The first transaction with PayU occurred on June 3, 2002 in Poland—a phone top-up for 20 PLN by card. From 2005, PayU was available on Allegro under the name "Płatności Allegro" (Allegro Payments).

This early integration of payments created something that few competitors could match: a seamless, trusted transaction environment tailored to Polish consumer preferences. Polish consumers at the time were wary of credit cards and distrustful of cross-border payment systems. PayU offered local bank transfers and payment methods that Poles actually used.

The Ceneo.pl acquisition in 2006 added another strategic layer. Price comparison sites were becoming increasingly important in e-commerce, and Ceneo gave Allegro control over a critical consumer touchpoint—the research phase before purchase. Together, Allegro, PayU, and Ceneo formed an early flywheel: consumers researched on Ceneo, shopped on Allegro, and paid through PayU.

The Tradus Years

QXL Ricardo's transformation into Tradus plc in 2007 reflected broader consolidation in European e-commerce. But for Allegro, little changed operationally. The platform continued growing, adding users and merchants, deepening its hold on Polish e-commerce.

After the dot-com bubble burst, the company fell into conflict between Allegro's founders and QXL Ricardo, with the dispute resolved by settlement only in 2006. This conflict, while disruptive, ultimately didn't prevent Allegro from growing—evidence of the platform's inherent momentum and the strength of its market position.

By 2008, when Naspers came calling, Allegro was no longer a scrappy startup. It was Poland's dominant marketplace, with millions of users, a proven business model, and an ecosystem of payments and price comparison tools that competitors couldn't easily replicate. The question was no longer whether Allegro would survive—but how big it could become.

IV. The Naspers Era: From Auction Site to E-Commerce Empire (2008–2016)

A South African Giant's Emerging Markets Playbook

In 2008, both companies were acquired by global South African internet group Naspers for $1.5 billion. According to the Cape Town-based company, Allegro was bought to establish other fast-growing businesses in Poland, such as e-commerce website OLX and to continue the scaling of payment platform PayU.

Naspers, the Cape Town-based media and internet conglomerate, had developed a remarkable playbook for emerging market internet investments. Its legendary investment in Tencent (buying one-third of the Chinese gaming and messaging giant for $32 million in 2001) had made Naspers one of the most successful technology investors in history. Now it was applying similar thinking to Central and Eastern Europe.

The $1.5 billion acquisition price represented a stunning return for QXL Ricardo/Tradus shareholders—and signaled that sophisticated global investors saw Poland as a major opportunity. For Naspers, Allegro represented a platform onto which it could build complementary businesses.

Professionalizing the Operation

Under Naspers ownership, Allegro underwent significant professionalization. The company invested in technology infrastructure, expanded its product range, and began the transition from a primarily auction-based model to one that increasingly featured fixed-price transactions.

This shift was crucial. While auctions had driven Allegro's early growth, they were inherently limiting. Fixed-price listings allowed for greater seller participation (particularly from businesses rather than individuals), more predictable shopping experiences, and better integration with the emerging logistics infrastructure.

The platform evolved from a primarily auction-based model to a hybrid marketplace emphasizing fixed-price transactions, broader product categories, and enhanced user features, capitalizing on Poland's burgeoning internet penetration and rising online shopping adoption. This period saw steady expansion in active users and transaction volumes, driven by investments in technology and logistics integrations.

Why Naspers Sold

In 2016, Naspers sold its Polish e-commerce businesses Allegro and Ceneo to funds advised by a consortium of private equity firms that includes Cinven, Permira and Mid Europa for $3.253 billion, keeping OLX and PayU. It was the largest transaction in Poland's digital sector and one of the largest transactions of this kind in Europe.

The decision to sell is worth examining. Naspers retained OLX (the classifieds business) and PayU (the payments platform)—both assets with broader international application. Allegro, while dominant in Poland, was fundamentally a local marketplace without obvious paths to global scale.

This strategic decision meant Allegro would get new owners with a different orientation: private equity firms focused on operational improvement, efficiency gains, and eventual exit. The stage was set for the next transformation.

For investors considering Allegro today, the Naspers era demonstrates something important: the company has successfully navigated multiple ownership transitions without losing its market position. Each transition brought new capital, new management perspectives, and new strategic priorities—but Allegro's core competitive advantages remained intact.

V. Private Equity Transformation: The Cinven/Permira/Mid Europa Chapter (2017–2020)

New Owners, New Playbook

At the IPO price of PLN 43 per share, the implied market capitalisation was PLN 44 billion (€9.8 billion). Funds advised by Cinven, Permira, and MidEuropa (together "the Sponsors") acquired Allegro.eu in January 2017 for US$3.25 billion (€2.75 billion).

The private equity consortium that acquired Allegro in January 2017 faced a familiar PE challenge: take a good business and make it great. The $3.25 billion purchase price was substantial, meaning significant operational improvements would be required to generate acceptable returns.

David Barker, Partner of Cinven, said: "When we originally invested in Allegro in 2017, it was a good business with a good reputation. We brought in a new management team, led by the highly experienced Chair, Darren Huston, and CEO, François Nuyts."

The Management Upgrade

The decision to bring in Darren Huston as Chairman and François Nuyts as CEO proved transformative. Huston, a former CEO of Booking.com and Expedia, understood marketplace dynamics at scale. Nuyts joined from Amazon where he was responsible for establishing Amazon in Southern Europe, as Vice President & Managing Director of Amazon Spain and Italy.

Think about what that meant: Allegro's new CEO had literally built Amazon's presence in two European markets. He understood Amazon's playbook, its strengths, and its weaknesses. He knew what it took to compete with—and defend against—the world's largest e-commerce company.

Przemyslaw Budkowski had been CEO of Allegro for more than seven years. During this time, Allegro continued to expand, becoming Poland's leading eCommerce engine. The transition from Budkowski to Nuyts represented a shift from organic local growth to professional, internationally-minded marketplace management.

The Allegro Smart! Revolution

The value creation strategy involved investing in the experience and convenience of Allegro's services to both consumers and merchants. Initiatives included the development of a best-in-class mobile app, improved logistics solutions and pricing tools, and the launch of Allegro SMART!

The launch of Allegro Smart! in 2018 was the single most important strategic move of the private equity era. Modeled explicitly on Amazon Prime, the subscription-based loyalty program offered unlimited free deliveries to subscribers. But unlike Prime, which was layered onto an existing Amazon ecosystem, Smart! was designed specifically for the Polish market and its unique logistics infrastructure.

Allegro Smart is a dedicated e-commerce subscription model operating within Poland's leading marketplace. It was launched in 2018 and has grown to become a hallmark of fast, free delivery and returns for subscribers. The programme allows registered buyers to pay a fixed fee and in return enjoy "free shipping" across many offers marked with the Smart badge.

The strategic brilliance of Smart! lay in its alignment of incentives. For consumers, it eliminated the friction of delivery costs—a significant barrier in price-sensitive Poland. For merchants, Smart! eligibility became a competitive advantage; products displaying the Smart badge received increased visibility and measurably better sales metrics. For Allegro, the subscription created predictable revenue, increased purchase frequency, and most importantly, switching costs.

By the Numbers

Over the lifetime of the Sponsors' investment, GMV grew by 99%, net revenue by 102% and adjusted EBITDA by 113% on a last-twelve month basis. Most recently, GMV growth increased further to 54% (LTM to 30 June 2020) as consumers turned to Allegro to provide them with goods during the ongoing COVID-19 pandemic.

In addition to the significant business growth and value creation, Allegro has seen a substantial increase in employees from 1,380 at the end of 2016 to nearly 2,300 as at 30 June 2020.

These metrics demonstrate textbook private equity value creation: operational improvement, strategic investment, and headcount expansion focused on growth. The consortium didn't just cut costs—they invested aggressively in capabilities that would drive long-term competitive advantage.

33% of Allegro's customers in Poland are also users of "Smart!". This increases loyalty towards the company and is beneficial for both Allegro and the customer. By the time of the IPO, Smart! had become so embedded in Polish shopping behavior that competitors couldn't easily replicate it—even with similar offerings, they lacked the network of merchants and the consumer trust that made Smart! work.

VI. Poland's Biggest IPO: October 2020

Perfect Timing

Shares in Allegro, Poland's number one commerce platform and the most recognized e-commerce brand in the country with over 12.3 million active buyers and over 117,000 merchants as of 30 June 2020, began trading on the Warsaw Stock Exchange, marking the completion of Poland's largest ever IPO.

October 12, 2020 was a watershed moment for Polish capital markets. E-commerce platform Allegro raised about 9.2 billion zloty ($2.3 billion) in Warsaw's largest-ever listing after selling more shares than planned thanks to strong demand for technology-related stocks in Europe. Allegro sold 213.5 million shares at 43 zloty each, the top end of a marketed range.

The timing could not have been better. COVID-19 had accelerated e-commerce adoption globally, and investors were hungry for exposure to digital commerce. With its sales model, Allegro survived a critical moment in the history of many companies in Poland—the COVID-19 pandemic. When the retail market was in lockdown, e-commerce was undergoing a revival. At that time, Allegro was recording sales increases.

As elsewhere, Polish online retailers had seen a boost during coronavirus lockdown. Allegro's sales rose by 52%, reaching 1.77 billion zloty in the first half of the year.

First Day Pop

The IPO exceeded all expectations. On October 12, Allegro went public on the Warsaw Stock Exchange. Its listing price leapt more than 60% in the first hours of trading, making it the biggest listed company in Warsaw with a market value of about $19 billion.

The immediate price appreciation told investors two things: first, that demand for Allegro shares was substantial and genuine; second, that the IPO had been priced conservatively—good for new investors, but suggesting the PE sponsors left money on the table (a common criticism of successful IPOs).

"[Allegro] could become the largest company to be listed on our exchange," Marek Dietl, CEO of the Warsaw Stock Exchange, had told the press. That title previously belonged to Polish gaming company CD Projekt, maker of The Witcher franchise.

The PE Returns

For the PE consortium, the numbers were impressive. At the IPO price of PLN43 per share, the implied market capitalisation was PLN44 billion (EUR9.8 billion). Funds advised by Cinven, Permira and Mid Europa Partners acquired Allegro.eu in January 2017 for USD3.25 billion (EUR2.75 billion).

The math is straightforward: a roughly 3x return on invested capital in under four years, not including ongoing ownership stakes. Due to the strength of investor demand the original offer of shares was up-sized, with c.182.6 million shares sold by the Sponsors in the IPO (in aggregate), raising PLN 7.85 billion (€1.76 billion) while retaining an aggregate equity stake in the Group of c.73 per cent post-listing.

For investors studying private equity value creation, Allegro offers a masterclass in the playbook: acquire a good business with defensible market position, bring in world-class management, invest in strategic initiatives (Smart!), and exit at the right moment (pandemic e-commerce boom) through a well-executed IPO.

A CEO's Reflection

"Allegro's story started over 20 years ago in a garage in Poznan. It's normally the story you hear in different continents. But to have this story be such a success in Poland is actually amazing," CEO François Nuyts said at the opening ceremony in Warsaw.

The statement captured something important: Allegro had become not just a successful company, but a symbol of Polish technological capability. In a country that had spent decades under communist rule and then years catching up economically to Western Europe, Allegro represented proof that Polish entrepreneurs and companies could compete on a global stage.

VII. Building the Ecosystem: Allegro Pay, One Delivery & Acquisitions (2019–2021)

The Fintech Play

In 2019, Allegro acquired online ticketing platform eBilet, and in 2020 it acquired Polish fintech start-up FinAi, which ultimately enabled the company to launch Allegro Pay. In 2021, the company also acquired Opennet as part of its focus on fulfilment capabilities, allowing Allegro to inhouse its last-mile software.

At launch, access to Allegro Pay was granted to a group of tens of thousands of customers and was extended through 2020. Clients who logged in to Allegro and saw Allegro Pay among the payment methods could activate the service and receive up to PLN 4,000 to pay for purchases made on the platform. It sufficed to fill out a simple application once, and the funds would be granted based on an individual analysis, primarily involving data from external databases and the history of purchases on Allegro.

The Allegro Pay launch represented a strategic shift. Rather than relying solely on external payment providers like PayU (which, remember, Naspers had retained when selling Allegro), the company was building its own financial services capability. This vertical integration would prove increasingly important.

Allegro Pay loan origination grew at a steady 41% over the past two years. Advertising growth accelerated by 31.3% year-on-year, indicating strong potential for future revenue streams. Allegro Pay demonstrated robust growth with a 41% increase in loan origination over the past two years.

Allegro Pay serves multiple strategic purposes. It increases conversion by removing payment friction. It generates interest income from deferred payments. Most importantly, it creates another layer of switching costs: users with Allegro Pay credit lines are less likely to shop elsewhere.

Financial options like Allegro Pay are crucial for many shoppers. This service originated PLN 2.8 billion (approximately $745 million USD) in loans in Q1 2025, increasing its financed GMV share to nearly 17%.

Building Logistics Infrastructure

The Allegro Delivery network includes around 33,000 parcel lockers and 37,000 pick-up points, including those operated by Orlen Paczka, DHL and DPD, its most recent collaborator. Thanks to the program, the share of parcels handled directly by Allegro rose to 34% in Q2 2025.

The logistics buildout represents one of Allegro's most capital-intensive and strategically important initiatives. Allegro started to roll out its own network of parcel lockers, One Box by Allegro, beginning in November 2021. To start with, Allegro planted more than 600 green lockers, planning to bring the number to at least 3,000 by the end of 2022.

The company is adding 2,500 lockers in 2025, bringing its own One Box footprint past 8,000 units by year's end. Lockers shorten the distance between parcel and customer, enabling late-night orders to be available by the next morning.

The strategic logic is compelling. By controlling more of the delivery infrastructure, Allegro can: reduce per-parcel costs, guarantee delivery quality, differentiate from competitors who rely on shared logistics providers, and potentially offer services (like same-day delivery) that wouldn't be economical through third parties.

The DPD Polska agreement extends Allegro's reach dramatically. With 12,000 additional lockers and 21,000 pick-up/drop-off points, Allegro can handle surges and serve rural areas more efficiently. The contract runs until April 2030 and allows Allegro to direct flows based on performance rather than quotas.

The Flywheel in Motion

The ecosystem pieces fit together: marketplace → payments → logistics → advertising → loyalty → more GMV. Each element reinforces the others. Smart! subscribers shop more frequently. Allegro Pay users convert at higher rates. Controlled logistics enables faster delivery, which drives more Smart! subscriptions. Advertising tools help merchants succeed, attracting more selection, which drives more buyers.

Allegro's Smart! loyalty programme, with more than 8 million subscribers, drives repeat purchases and higher spend, which is a major advantage for sellers. Allegro combines marketplace reach with fintech and advertising tools.

For long-term investors, this flywheel is the core thesis. Unlike simpler e-commerce businesses that compete primarily on price or selection, Allegro has built an integrated ecosystem with multiple reinforcing competitive advantages. Breaking into this ecosystem requires not just competitive pricing, but matching Allegro's logistics infrastructure, payment capabilities, and subscriber base—all simultaneously.

VIII. International Expansion: The Mall Group Acquisition (2021–2022)

The Big Bet

Allegro, the most popular shopping platform in Poland and one of the world's top ten e-commerce websites, announced in November 2021 that it had agreed to acquire 100% of Mall Group a.s. and WE|DO CZ s.r.o. from selling shareholders PPF, EC Investments, and Rockaway Capital.

Mall Group and WE|DO were acquired for a price amounting to EUR 881 million, based on a firm valuation of EUR 925 million adjusted for debt and debt-like items of EUR 44 million. The final price might be increased by a price adjustment of up to EUR 50 million based on specific short-term objectives.

The acquired business comprises the e-commerce assets of MALL Group and the logistics assets of WE|DO based across the Czech Republic, Slovakia, Hungary, Slovenia, Croatia and Poland.

The Mall Group acquisition represented Allegro's most aggressive move yet—and its riskiest. For the first time, the company was betting seriously on markets outside Poland, where it would need to replicate its playbook against established local competitors.

The Strategic Rationale

The merger between Allegro, Mall Group, and WE|DO was designed to strengthen the companies' position as a leading marketplace platform for European customers and merchants, propelling the group's international expansion. The move aimed to improve the shopping experience and provide the broadest selection at best prices and maximum convenience for 70m potential customers across the region.

The transaction nearly doubled the group's total addressable market in countries with highly attractive fundamentals and growth potential. The combination would also enable efficient international merchants' sourcing and onboarding.

The theory made sense. Central and Eastern European markets share cultural similarities, growing middle classes, and relatively underdeveloped e-commerce infrastructure. A platform that succeeded in Poland might well succeed in neighboring countries—especially with an existing asset base (Mall Group) to accelerate market entry.

The group's 135k merchants across Central and Eastern Europe would benefit from the ability to list once and sell everywhere, gaining wider access to a 240-billion euro addressable retail market.

Execution Challenges

The acquisition closed on April 1, 2022, but integration has proved challenging. Allegro is working to complete the Mall transformation in 2025, aiming for a lean merchant model. This is expected to contribute positively to group results by 2026.

Allegro expanded into the Czech Republic in 2023, followed by Slovakia and Hungary in 2024. These new Allegro marketplaces in Czechia, Slovakia, and Hungary have increased the group's addressable market by an additional 26 million potential customers. As of Q1 2025, active buyers in these three international markets reached 3.7 million, with their Gross Merchandise Volume (GMV) totaling $128 million.

The numbers reveal both progress and the scale of the challenge. International GMV of $128 million compares to Polish GMV exceeding $14 billion—international operations remain tiny relative to the home market.

Allegro launched in Slovakia early last year, and Hungary followed in October 2024. Allegro now serves 4.2 million customers across the three international marketplaces, compared to 2.8 million a year earlier.

Merchants welcome Allegro's powerful cross-border selling opportunity and expand their exportable selection. The group's new marketplaces hit 4.2 million active buyers, a surge of over 50% as Allegro.hu exceeded expectations in its inaugural year.

The 50%+ growth in international active buyers is encouraging, but investors should recognize that international expansion remains a work in progress. The company has paused further geographic expansion to focus on improving existing international operations—a pragmatic decision that prioritizes execution over ambition.

IX. The Competitive Battlefield: Amazon, Temu & Chinese Giants (2021–Present)

Amazon's Late Entry

Allegro resisted Amazon, eBay, and the Shopee platform. The latter withdrew its operations from Poland after a year and a half of operation. Although Amazon launched a Polish platform in 2021 and China's AliExpress is building logistics centers in Poland, Allegro remains the country's most popular e-commerce platform. It outclasses its competitors regarding the number of users, reach, and brand awareness.

Amazon's 2021 entry into Poland was widely anticipated. The question was never whether Amazon would come, but whether it could dislodge Allegro's dominant position. Three years later, we have an answer: not easily.

Allegro's share of the Polish retail e-commerce market was 38.8% at the end of 2024. Amazon held a 3.9% share, followed by AliExpress with 3.4% and Temu with 1.5%.

Amazon's 3.9% market share after three years in Poland contrasts sharply with its typical dominance in Western European markets. Poland entered e-commerce later than Western Europe. This gave local platforms time to establish themselves before Amazon showed up—unlike Germany or France, where Amazon dominated early.

The Shopee Lesson

In autumn 2021, Shopee, the Singaporean e-commerce company that is part of SEA, announced that it was going to enter the Polish market. Following nearly two decades of relatively limited competition in Poland, the country's e-commerce market turned into a battlefield of well-funded foreign entrants.

Shopee's entry was aggressive. The company onboarded tens of thousands of local merchants by offering them 0% commissions for the first six months, which further helped to keep prices competitive. This made Shopee popular with consumers; within less than a year, the company's website reached over 10m monthly active users.

But Shopee's Polish experiment ended abruptly. It all turned out to be a mere flash in the pan. 15 months after launching in Poland and despite seemingly strong metrics, Shopee closed its Polish operation. As it turned out, there is a difference between throwing cash at a market to show fast growth, and building a sustainable, profitable business.

The Shopee failure offers a lesson that investors should note: in e-commerce, user acquisition is relatively easy if you're willing to burn money. Sustainable market position requires something more—logistics infrastructure, merchant relationships, consumer trust, and unit economics that work without subsidies.

The Temu Threat

In April 2025, Temu became the most visited e-commerce platform in Poland, dethroning local marketplace Allegro.eu SA after two years of expansion fueled by lavish spending on marketing.

The Chinese giant owned by PDD Holdings Inc. had 18.1 million real users in Poland in March 2025, compared with 17.8 million for Allegro, according to research company Gemius Mediapanel. It's the first time the Polish incumbent has been surpassed by its rivals.

These headlines sound alarming. But the reality is more nuanced. While Temu is leading in user volume, Allegro still holds an edge in user engagement. Data from May 2025 shows that the average user spent 1 hour, 48 minutes, and 55 seconds on Allegro—an increase from April's 1 hour, 45 minutes, and 38 seconds.

Traffic and transactions are different things. Allegro is still dominating the market in Poland. Management stated: "And we're still seeing when we look at share of transactions, our estimates based on these surveys are that the 2 together, Shein and Temu, are in the mid single digits in terms of the segment share in the market at this point in time."

Allegro's Response

E-commerce platform Allegro is doubling down on its local offering in a bid to differentiate itself from Asian competitors like Temu, its finance chief said. Allegro, which has been developing the platform since 1999, remains the go-to online shopping place for millions of Poles despite growing competition from international players.

Allegro said it had in recent months removed offers with long shipping times, mostly from East Asia, from its international marketplaces. Eastick said removing most of the long delivery time Asian selection helped Allegro distinguish itself from the Asian competitors and the shopping frequency was improving a lot.

This strategic choice—removing Asian sellers with long delivery times—represents Allegro betting on quality over price. The company is positioning itself as the fast, reliable, local alternative to Chinese platforms that may offer lower prices but with unpredictable delivery times and uncertain product quality.

"There was fairly rapid progress from zero in 2023 and early part of 2024, but it's slowed down dramatically now," Eastick said about the performance of Asian platforms in its markets. "We'll continue to defend our position in terms of marketing spend," he added.

X. Modern Allegro: Financials, Strategy & Current State (2023–2025)

The Numbers

Allegro saw revenue rise by 6.7% year on year to PLN10.9 billion ($2.8 billion U.S.) in 2024. During the same period, its adjusted EBITDA increased by 17.9% to PLN3.0 billion.

GMV reached PLN64 billion for the group, a growth of 9.6% year-on-year. Revenue increased by 6.7% year-on-year. Adjusted EBITDA grew by 17.9% to approximately PLN3 billion.

The key metrics reveal a maturing but still-growing business. GMV growth of nearly 10% is solid for a dominant platform in a developed market. More impressive is the EBITDA margin expansion—adjusted EBITDA growing faster than revenue indicates improving operational efficiency despite competitive pressures.

Take rate increased by 33 basis points, reaching 12.01% in Q4 2024. Average annual spend per buyer in Poland exceeded PLN4,000.

The rising take rate is particularly noteworthy. It suggests merchants continue to see value in Allegro's platform despite the availability of alternatives—a sign of pricing power that reflects strong market position.

Forward Guidance

For 2025, Allegro anticipates its GMV to reach 16.7 billion euros and revenue to total 2.85 billion euros.

Following H1 2025, management raised revenue and EBITDA guidance while keeping GMV growth stable. Revenue growth was nudged up from 9% to 9.5%, while EBITDA expectations climbed from 13.5% to 15%. The stronger outlook reflects advertising momentum, fintech, and logistics upside, as well as disciplined capex.

The guidance raise mid-year signals management confidence. More importantly, the sources of the upside—advertising, fintech, logistics—represent the higher-margin, higher-growth segments of the business that differentiate Allegro from simpler marketplace operators.

Active Buyer Trends

The incoming CEO Marcin Kuśmierz stated: "Not only is the number of active buyers rising in Poland and internationally, but they also continue to spend more with us on average." Allegro, which runs third-party marketplace platforms in the Czech Republic, Slovakia and Hungary, said it had 21 million active buyers across the group, a 5.4% rise from a year earlier, including nearly 6 million outside of Poland.

The group's active buyers' base grew by almost 600,000 YoY, with 15.2 million active buyers in Poland spending on average 8% more than a year earlier.

The combination of rising active buyers and increasing spend per buyer creates compound GMV growth. This pattern—existing customers spending more while new customers are added—is the hallmark of a healthy marketplace flywheel.

Smart! Progress

The number of Allegro Smart! users in Poland now exceeds 7 million.

Allegro Smart! added nearly 1 million subscribers YoY in Poland thanks to the rollout of special bonuses and promotions. Smart! subscriptions beyond Poland more than doubled.

With 7+ million Smart! subscribers in Poland—representing roughly 45% of active buyers—the loyalty program has achieved critical mass. The doubling of international Smart! subscriptions, while from a smaller base, suggests the program can successfully translate to new markets.

XI. Business & Investing Lessons: The Allegro Playbook

Lesson 1: Local-First Strategy Beats Global Scale

Allegro's success against eBay, Amazon, and Shopee demonstrates that in e-commerce, local knowledge can trump global resources. Understanding Polish payment preferences, logistics infrastructure, and consumer psychology allowed Allegro to create experiences that foreign competitors couldn't easily replicate.

Every international company entering Poland quickly learns they can't ignore Allegro. It's like trying to sell in Germany without Amazon. But this dominance creates gaps. Smart international players are finding ways in.

For investors evaluating e-commerce platforms, the lesson is clear: dominant local position matters more than global footprint. Markets that already have an entrenched local champion are difficult to crack, even for well-capitalized global players.

Lesson 2: Subscription as Strategic Moat

Over time, the Smart! programme has evolved—as of 2024 it had saved buyers over 13 billion PLN in delivery/returns costs.

Allegro Smart! isn't just a revenue stream—it's a competitive moat. 33% of Allegro's customers in Poland are also users of "Smart!". This increases loyalty towards the company and is beneficial for both Allegro and the customer.

Competitors can match Allegro's product selection. They can match its prices. But matching the embedded behavioral patterns of 7+ million subscription customers is exponentially harder. Smart! creates switching costs that simple marketplace competition cannot overcome.

Lesson 3: Vertical Integration Timing

Allegro's strategic investments in payments (Allegro Pay), logistics (One Box), and advertising demonstrate sophisticated understanding of vertical integration timing. The company didn't try to build everything at once; it sequenced investments based on market maturity and competitive need.

Early on, external payments (PayU) and external logistics made sense—the company needed to focus resources on core marketplace growth. As Allegro matured and competitors threatened, bringing capabilities in-house became both possible and necessary.

Lesson 4: Private Equity Can Add Value

The Cinven/Permira/Mid Europa ownership period offers a counterexample to narratives about private equity strip-and-flip. The sponsors brought in world-class management, invested in strategic initiatives, and grew the business substantially—all while generating attractive returns.

"When we originally invested in Allegro in 2017, it was a good business with a good reputation. We brought in a new management team, led by the highly experienced Chair, Darren Huston, and CEO, François Nuyts. Together with management and our co-shareholders, we focused on improving the experience for both customers and merchants."

Lesson 5: International Expansion Requires Patience

Allegro's struggles to rapidly scale internationally—despite clear strategic logic and substantial capital—remind investors that geographic expansion is hard. The company's decision to pause further expansion and focus on existing markets shows disciplined prioritization over empire-building.

It's part of Allegro's philosophy to only enter a new market if the company can provide value to customers. "We want to go to places where we are welcome."

XII. Analysis: Strategic Position & Investment Considerations

Porter's Five Forces

Threat of New Entrants: MODERATE-HIGH Every international company entering Poland quickly learns they can't ignore Allegro. It's like trying to sell in Germany without Amazon. But this dominance creates gaps. Smart international players are finding ways in.

Barriers include brand trust, logistics infrastructure, and Smart! subscriber lock-in. However, well-capitalized entrants (Temu, Amazon) can absorb losses to gain share. The threat is moderated by Shopee's failure, which demonstrated that money alone isn't sufficient.

Bargaining Power of Suppliers (Merchants): LOW-MODERATE Allegro connects over 20.8 million active buyers with more than 160,000 merchants.

With 160,000+ merchants dependent on Allegro's reach, individual seller bargaining power is limited. However, large brand partners and exclusive merchant relationships require ongoing attention.

Bargaining Power of Buyers: MODERATE Switching costs exist (Smart! subscription, Allegro Pay credit lines, purchase history) but aren't prohibitive. Price-sensitive Polish consumers will compare alternatives.

Competitive Rivalry: HIGH AND INTENSIFYING Amazon, Temu, AliExpress, and local players all compete for Polish e-commerce spending. However, competitive intensity hasn't yet translated to significant share losses for Allegro.

Threat of Substitutes: LOW Online shopping has become behavioral default for many product categories. Substitutes (physical retail) are actually losing share to e-commerce, benefiting all digital players.

Hamilton Helmer's Seven Powers

Scale Economies: Allegro benefits from scale in logistics, technology, and marketing. Larger GMV enables investment in One Box infrastructure that smaller players can't match.

Network Effects: Classic two-sided marketplace dynamics—more buyers attract more merchants, which attract more buyers. The density of this network in Poland is Allegro's core advantage.

Counter-Positioning: Allegro's local-first approach represents counter-positioning against global players. Amazon and Temu are unwilling (or unable) to match Allegro's deep Polish integration.

Switching Costs: Smart! subscriptions, Allegro Pay credit, and embedded shopping habits create meaningful switching costs. These aren't prohibitive but require competitors to offer substantial improvement to overcome.

Branding: The portal is the first choice for 12.3 million active shoppers and 117,000 sellers, resulting in as much as 98% of Allegro's brand recognition. This brand equity took decades to build and can't be replicated quickly.

Cornered Resource: Allegro's 160,000+ merchant relationships represent a cornered resource—these partnerships, built over two decades, give Allegro selection advantages that new entrants must painstakingly recreate.

Process Power: Allegro's operational expertise in Polish e-commerce—understanding local logistics, payments, and consumer behavior—represents process power that competitors can theoretically copy but practically struggle to match.

Key KPIs to Monitor

For ongoing investment evaluation, focus on these metrics:

-

GMV Growth Rate: The fundamental health indicator. Growth below 5% would signal saturation or competitive pressure; growth above 10% indicates continued momentum.

-

Smart! Subscriber Count and Retention: The loyalty moat. Rising subscriptions with high retention signal sustainable competitive advantage; declines would be concerning.

-

Take Rate Trend: Allegro's ability to monetize GMV through advertising, fintech, and commissions. Rising take rate indicates pricing power; declining take rate suggests competitive pressure.

Regulatory and Risk Considerations

EU Digital Markets Act: As a major European marketplace, Allegro faces potential regulatory scrutiny. Increased compliance costs are possible, though the company's European domicile may prove advantageous relative to non-EU competitors.

Chinese Competition Regulatory Risk: Temu and other Chinese platforms face increasing EU scrutiny regarding product safety, customs duties, and subsidy practices. Regulatory action against Chinese competitors could benefit Allegro, but could also lead to retaliatory measures affecting all e-commerce players.

InPost Dispute: InPost remains one of the parcel locker operators used by Allegro, but the marketplace has also built its own parcel locker network and partnered with other logistics providers. As a result, the Allegro Delivery network now includes around 33,000 parcel lockers and 37,000 pick-up points.

InPost has accused Allegro of steering customers away from its parcel lockers and towards Allegro Delivery and has taken the case to arbitration. Allegro countered that its delivery programme is open to all major logistics players and aims to give consumers more choice. A ruling in the arbitration case is expected next year.

This dispute bears watching—an adverse ruling could affect logistics strategy and costs.

Bull Case vs. Bear Case

The Bull Case

Structural Growth Runway: Central and Eastern Europe remains underpenetrated in e-commerce relative to Western Europe. As Polish incomes rise and e-commerce adoption increases, Allegro should benefit as the dominant local platform.

Flywheel Acceleration: Smart! subscriptions, Allegro Pay, and advertising all show strong growth. These high-margin businesses should drive profit expansion even as GMV growth moderates.

Competitive Moats Holding: Despite Amazon's entry, Shopee's attempt, and Temu's marketing blitz, Allegro retains 38%+ market share in Poland. The competitive threats that concerned investors in 2021-2022 have largely failed to materialize.

International Optionality: While international expansion has been challenging, the 50%+ growth in international active buyers shows the model can translate. Success in Czech Republic, Slovakia, and Hungary would meaningfully expand the addressable market.

Valuation: At current levels, Allegro trades at a discount to global marketplace peers despite dominant market position and solid growth trajectory.

The Bear Case

Competitive Pressure Intensifying: Temu's traffic leadership, even if not yet translating to transaction share, signals consumer willingness to try alternatives. Continued Chinese marketing spend could erode Allegro's position over time.

International Execution Risk: Mall Group integration has been slower and costlier than anticipated. International profitability remains elusive, and management attention spent on challenging markets detracts from defending Poland.

Logistics Investment Burden: Building 8,000+ parcel lockers requires substantial capital investment. If take-up disappoints or competitors match capabilities, these investments may not generate adequate returns.

Macro Sensitivity: Polish consumer spending correlates with economic conditions. An economic downturn would pressure GMV growth and potentially trigger aggressive discounting that damages profitability.

Single Market Concentration: Despite international expansion efforts, Poland still accounts for the vast majority of Allegro's business. Regulatory changes, competitive disruption, or macro shocks specific to Poland would disproportionately impact the company.

Conclusion: Central Europe's Digital Champion

From a basement in Poznań to Poland's largest listed company, Allegro's 25-year journey offers a masterclass in building durable competitive advantage. The company successfully navigated multiple ownership transitions, beat back global competitors, and built an integrated ecosystem that creates genuine switching costs.

CEE is home to ~140M online users, of which Allegro already reaches 69M—comparable to the entire digital population of France or the UK. Poland contributes 37M, with Czechia, Hungary, Slovakia, Croatia, and Slovenia adding another 32M.

The challenges ahead are real. Chinese competitors have demonstrated willingness to lose billions to gain market share. Amazon's presence, while limited, represents a persistent threat. International expansion has proved harder than anticipated.

But the core thesis remains intact: Allegro has built something that competitors can't easily replicate—deep local trust, an integrated ecosystem of payments, logistics, and advertising, and a loyalty program with millions of subscribers. Whether that proves sufficient to sustain dominance in an increasingly competitive landscape will determine Allegro's investment case for the decade ahead.

Darren Huston, Allegro's Chairman, summarized: "Since 2018, François has steered Allegro to what it is today—a European ecommerce champion and a leading global marketplace. Not only did he continue to lead efforts to improve our business, but he also oversaw the company's bourse debut—the largest listing Warsaw has ever seen. François also led our entry into international markets with the acquisition of Mall, laid the groundwork for a company-owned package distribution network, and successfully launched Allegro Pay."

For investors seeking exposure to Central European consumer growth, Allegro offers something rare: dominant market position in a growing market, multiple reinforcing competitive advantages, and optionality on international expansion. The story isn't perfect—execution challenges persist, competition is intensifying, and international markets remain works in progress.

But then again, no great business story ever is.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube