Grupo ACS: How a Failing Spanish Contractor Became a Global Infrastructure Titan

I. Introduction & Episode Roadmap

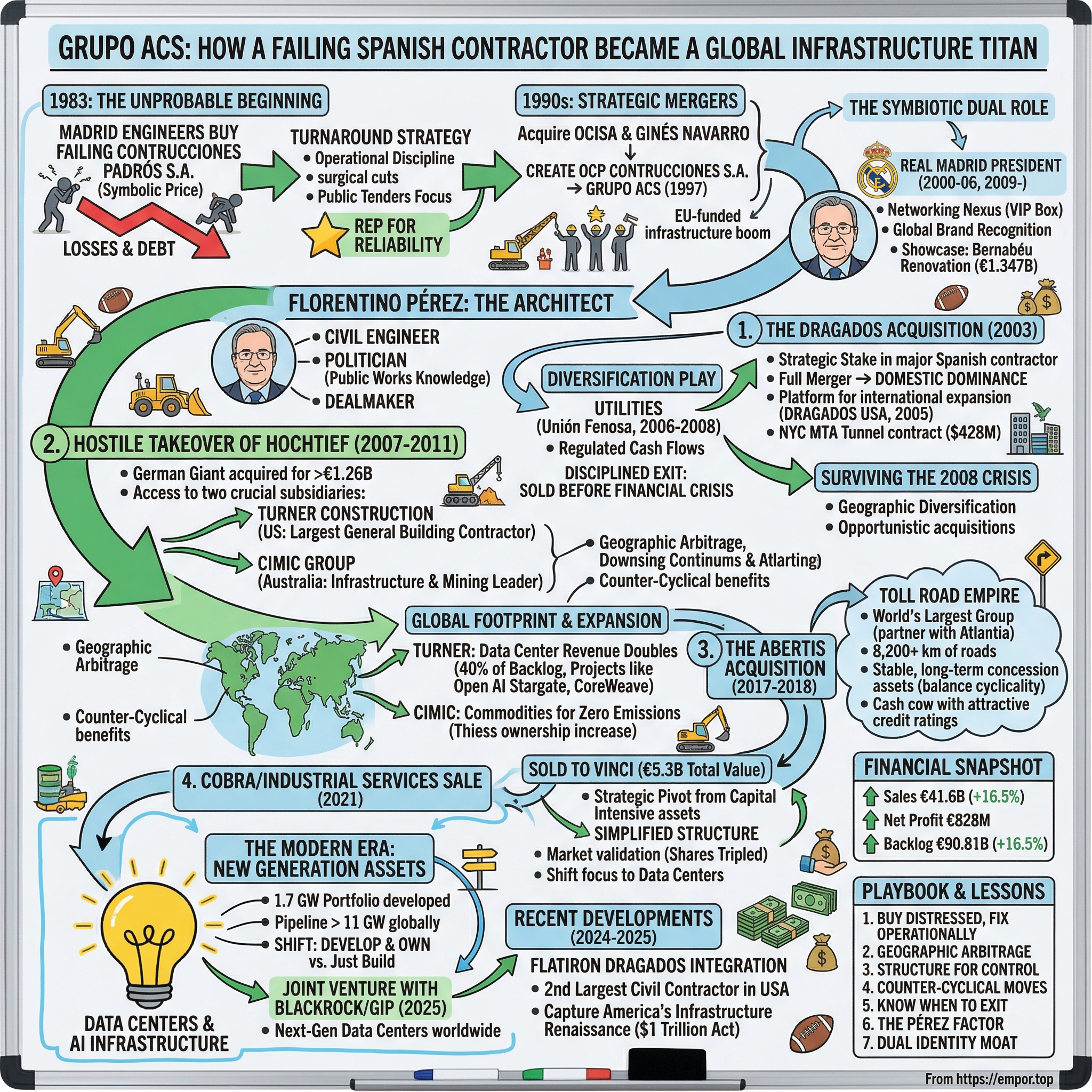

In the labyrinthine world of global construction, one company stands out as an improbable empire-builder. Picture Madrid in 1983: Spain was emerging from decades of dictatorship, the economy was sputtering, and a group of civil engineers had just bought a failing construction firm called Construcciones Padrós S.A. for a symbolic price. The company was hemorrhaging money. Its reputation was in tatters. Most observers would have given it six months before bankruptcy.

Four decades later, that same company—now called Grupo ACS—generates over €41 billion in annual revenue, employs approximately 134,000 people across more than 30 countries, and sits at the center of a web of subsidiaries that includes America's largest general building contractor, Germany's most international construction firm, Australia's dominant infrastructure player, and the world's largest toll road operator. Sales in 2024 grew by 16.5% to €41,633 million. The company employs approximately 134,321 people worldwide and has a market capitalization of $20.072B.

The central question driving this analysis: How did a group of engineers buying a failing Spanish construction company in 1983 create a €40+ billion revenue global empire and make its chairman—who also happens to run the world's most successful football club—a billionaire?

The scale today is staggering. At the end of March 2025, the backlog stood at €90.81 billion, which represents a growth of 16.5% with respect to the first quarter of the previous year. EBITDA was up 28.7% to €2,456 million. Operating profit (EBIT) was €1,590 million, 17.1% higher than in the previous period on a comparable basis.

This is a story of serial acquisitions executed with ruthless discipline. Of geographic arbitrage—taking Spanish management expertise to German, American, and Australian markets. Of the genius of acquiring distressed assets. And of Florentino Pérez, a civil engineer turned politician turned businessman turned football legend, who created one of the most complex and successful conglomerate structures in modern business history. The journey from Padrós to global titan illuminates timeless principles about value creation, capital allocation, and the art of the deal.

II. The Protagonist: Florentino Pérez—Civil Engineer, Politician, Dealmaker

Before understanding ACS, one must understand the singular figure who shaped it. Florentino Pérez Rodríguez was born in Madrid on March 8, 1947. Florentino was born into a middle-class family of businessmen. His father, Eduardo Pérez del Barrio, was the owner of Shangai perfumeries and president of the company Coperlim.

Florentino was the third of five siblings, with two older sisters and two younger brothers. From a young age, Florentino was known to be an outgoing and mischievous child, highly esteemed by his environment. Although he did not stand out as a brilliant student, he never failed and was characterized by his effort and responsibility, values instilled by his parents.

The choice of career proved fateful. Although he initially entered a film school, he finally decided to study Civil Engineering at the Polytechnic University of Madrid, a discipline that combines technical precision with large-scale planning, which would lay the foundations for his successful career in business and sports. Civil engineering in Spain during the 1960s and 1970s wasn't just an academic exercise—it was training for managing the massive public works that would define Spain's modernization. Roads, dams, tunnels, bridges: these were the currency of national development, and engineers who understood both the technical and political dimensions of such projects wielded enormous influence.

This training not only provided him with a solid foundation in technical knowledge, but also shaped his approach to problem solving and complex project management. The rigor and analysis that characterize this branch of engineering are reflected in the way Florentino Pérez approaches his challenges in business and sport. His engineering education was crucial in developing key skills such as strategic vision, long-term planning and efficient resource management.

Pérez's path took an unusual detour through politics. Florentino Pérez began his political career in 1976, entering the public arena through the Unión de Centro Democrático (UCD), a key party in Spain's transition to democracy. During his time in politics, which lasted until approximately 1983, he held several important positions that allowed him to have a significant impact in different areas.

Among his most prominent roles, he served as delegate of Sanitation and Environment in the Madrid City Council. This position gave him the opportunity to work on projects focused on improving the quality of life of the people of Madrid through waste management and the promotion of sustainable environmental practices. In addition, he was deputy director general for promotion at the CDTI (Center for Industrial Technological Development) in the Ministry of Industry and Energy, where he contributed to the development and promotion of technological innovation in the country.

Pérez began his professional career in the private sector in 1971 and was a member of the Spanish Union of the Democratic Center and the secretary-general of the Spanish Democratic Reformist Party, from 1979 to 1986.

This political experience proved invaluable. Pérez learned how public works contracts were awarded. He understood the Byzantine nature of Spanish bureaucracy. He developed relationships across party lines that would serve him for decades. Most importantly, he saw firsthand which construction companies performed well and which were struggling—knowledge that would prove decisive when he returned to the private sector.

The return to private business in 1983 represented a pivotal choice. Spain's Socialist government under Felipe González was embarking on a massive infrastructure program, fueled by European Union accession subsidies that would soon flood the country. Pérez could have stayed in politics, but he recognized that the real opportunity lay in building the physical infrastructure of modern Spain.

Pérez's dual identity—chairman of one of the world's largest construction companies while simultaneously serving as president of Real Madrid—creates a unique positioning in global business. He has been president of Real Madrid from 2000 to 2006 and from 2009 onwards. Pérez is the most successful president in the history of Real Madrid, winning 37 titles during his presidency, surpassing Santiago Bernabéu, who won 32.

The relationship between these two roles is more symbiotic than it appears. The Santiago Bernabéu VIP box became a networking nexus where business deals were discussed alongside football strategy. The renovation of the Bernabéu stadium—the total investment amounting to €1.347 billion as of June 30, 2025—showcased the kind of ambitious, complex project management that defines ACS's capabilities.

III. Origins: The Construcciones Padrós Turnaround (1983–1993)

In 1983, Spain's construction industry was in turmoil. The global oil crisis had rippled through the Spanish economy. Several traditional construction firms found themselves overleveraged and underperforming. Among them was Construcciones Padrós S.A., a Madrid-based contractor that had accumulated losses and lost major contracts to better-capitalized competitors.

The company was formed when a team of engineers acquired Construcciones Padrós S.A., a construction business which had been in financial difficulty, in 1983.

This wasn't a glamorous deal. The engineers who acquired Padrós were essentially betting that their operational expertise could extract value from a distressed asset that others had written off. The purchase price was nominal—Padrós was worth more dead than alive to its previous owners. But Pérez and his colleagues saw something others missed: a valid construction license, existing relationships with subcontractors and suppliers, and a team that could be reorganized.

By 1987, Pérez had assumed the chairmanship of Construcciones Padrós. His approach was surgical: cut overhead, renegotiate supplier contracts, focus on competitive public tenders rather than speculative private development, and build a reputation for delivering projects on time and within budget. In an industry plagued by cost overruns and delays, reliability became Padrós's calling card.

The playbook crystallized further with the acquisition of another struggling entity. The company acquired a majority holding in Cobra, a support services business, and merged with OCISA S.A. to create OCP Construcciones, S.A. OCISA (Obras y Construcciones Industriales S.A.) was bought at symbolic prices, bringing industrial and civil construction capabilities that complemented Padrós's existing strengths.

The merger logic was straightforward: two struggling companies, combined, could achieve scale advantages that neither possessed alone. Shared back-office functions, joint bidding on larger contracts, cross-selling of services—the synergies were real and substantial. By eliminating duplicate costs and combining complementary capabilities, OCP Construcciones emerged as a viable mid-sized player.

In 1993, he was named vice chairman of OCP Construcciones. The timing coincided with Spain's EU-funded infrastructure boom. European structural funds were financing highways, high-speed rail, urban renewal, and modernization projects across the country. OCP positioned itself to capture this wave, moving from regional contractor to national player.

In 1993, it went on to merge with Ginés Navarro Construcciones, S.A. to create Grupo ACS in 1997. By 1994, OCP ranked as Spain's eighth-largest public works contractor—an astonishing rise for a company that had been essentially worthless a decade earlier.

The decade from 1983 to 1993 established what would become the ACS playbook: buy distressed assets with valid operating licenses and existing relationships, apply operational discipline to restore profitability, then use the healthier platform for further acquisitions. It was textbook turnaround investing, executed by engineers who understood construction economics at a granular level.

IV. The Birth of ACS & The Merger Years (1997–2002)

The company was founded in 1997 through the merger of OCP Construcciones, S.A. and Ginés Navarro Construcciones, S.A. The combination created Actividades de Construcción y Servicios, S.A.—ACS.

After a merger in 1997, he became chairman of Actividades de Construcción y Servicios, S.A. (ACS). Pérez now led a company with national scale and the financial capacity to pursue much larger deals.

The name itself—"Construction and Services Activities"—signaled strategic intent. ACS wasn't positioning itself as a traditional construction company. The "Services" component reflected understanding that the most valuable infrastructure businesses combined building with ongoing operation and maintenance. A highway constructor earns fees once; a highway operator earns tolls for decades.

The late 1990s saw ACS executing a diversification strategy that would define its business model. It subsequently bought Onyx SCL, an environmental contractor in 1999 and stakes in Xfera and Broadnet, telecommunications businesses in 2000.

The telecommunications investments were particularly bold. Spain was experiencing a wireless boom, and Pérez bet that infrastructure expertise could translate to telecommunications tower construction and network services. While the telecom bubble would eventually burst, the underlying logic—that ACS could manage any complex infrastructure project—proved prescient.

ACS's listing on the Madrid Stock Exchange and inclusion in the IBEX 35 provided access to capital markets at a critical moment. The company could now use publicly traded shares as acquisition currency, finance larger deals through equity issuances, and benefit from the prestige of blue-chip status.

The parallel story of Pérez's life added another dimension. In 2000, the same year ACS was consolidating its position in Spanish construction, Pérez launched his campaign for the presidency of Real Madrid. In 2000, he made a dramatic move into the football world by running for president of Real Madrid. His campaign promise was to bring high-profile players to the club, including the legendary Luís Figo. When he won the presidency, Pérez's leadership immediately changed the landscape of the club.

During his first six years as president, he implemented the Galácticos policy of bringing the world's best players to Real Madrid. In his first four seasons in charge, he bought Luís Figo from arch-rivals Barcelona, Zinedine Zidane for a then-world record transfer fee, Ronaldo, and David Beckham.

The dual role seemed impossibly demanding, yet Pérez thrived in both. The business skills translated directly: negotiating player contracts wasn't so different from negotiating construction contracts; managing star egos resembled managing difficult subcontractors; building a championship team required the same organizational capabilities as building a billion-euro highway. And the visibility from Real Madrid enhanced ACS's brand recognition globally.

By 2002, ACS had established itself as a major Spanish construction company. But Pérez had larger ambitions. The next move would transform ACS from a Spanish champion into a European powerhouse.

V. INFLECTION POINT #1: The Dragados Acquisition (2003)

In 2003, ACS acquired Dragados S.A., a large contractor established during the Second World War to dredge the Port of Tarifa and which had subsequently gained extensive experience in hydro-electric and civil engineering work.

To understand why this deal mattered, consider Dragados's history. Dragados y Construcciones ("Dredging and Construction") was formed in 1941 as part of the effort to build the Port of Tarifa, in Cadiz, Spain. Dragados's work in that port consisted of constructing and placing reinforced concrete caissons. The company continued to build expertise in port and harbor dredging, construction, and services, becoming the leading Spanish group in that sector.

Over the following decades, Dragados's dam-building expertise helped it build a strong international component, with a portfolio of over 120 dam projects worldwide. By the turn of the next century, the company had completed more than 2,500 kilometers of highways (including toll roads), another 4,000 kilometers of other roadways, and more than 1,500 bridges, a portfolio that established the group as one of the world's leading infrastructure companies.

Dragados was everything ACS aspired to become: internationally experienced, technically sophisticated, diversified across civil engineering sectors. It had built some of Spain's most iconic infrastructure—the Guadarrama Tunnel, multiple major dams, the Cadiz Bay bridge. Its industrial construction division had expanded into offshore oil platforms and gas pipelines. Its services division managed water treatment and waste management facilities.

The deal structure revealed Pérez's tactical sophistication. In 2002, ACS made a surprise move to acquire a 23.5 percent stake in Dragados, just under the level at which Spanish law requires it launch a full takeover attempt. Nonetheless, the smaller ACS was able to gain a majority on Dragados's board of directors, giving it effective control of the company.

In 2003, ACS purchased an additional 10 percent and indicated its interest in completing a full merger with Dragados. The goodwill recognized from this merger—€554 million came from the ACS and Dragados Group merger in 2003—reflected the strategic premium ACS was willing to pay for domestic dominance.

With Dragados, ACS became the undisputed Spanish construction champion. But more importantly, Dragados provided the platform for international expansion. During 2005, ACS entered the US market via the establishment of Dragados USA, a wholly owned subsidiary of Dragados S.A. One of the first undertakings of the newly formed branch was a successful bid for the New York City's Metropolitan Transportation Authority (MTA) East Side Access Manhattan Tunnels project, being awarded an initial contract valued at $428 million.

The MTA contract represented a breakthrough. American infrastructure markets were notoriously difficult for foreign contractors to penetrate. Local relationships, union complexities, regulatory knowledge—these barriers had defeated many international entrants. Dragados USA cracked the code, demonstrating that Spanish construction expertise could compete and win in the world's most sophisticated infrastructure market.

VI. The Utility Play: Unión Fenosa & Diversification (2006–2008)

Pérez's strategic vision extended beyond construction. In 2006, ACS made a significant move into the utility sector. In 2003, ACS acquired Dragados, one of Spain's largest construction companies, significantly expanding its domestic operations and international presence.

ACS acquired a 22% stake in Unión Fenosa, one of Spain's major electric utilities, subsequently increasing its stake to 45%. The logic was compelling: utilities provided stable, regulated cash flows that could balance the cyclical volatility of construction. Infrastructure companies that combined building with operating assets could smooth earnings and generate more predictable returns for shareholders.

The timing proved fortuitous—and Pérez showed he knew when to exit. In 2008, just as the global financial crisis was intensifying, ACS sold its Unión Fenosa stake to Gas Natural, crystallizing substantial gains while the deal market remained functional. Weeks later, Lehman Brothers collapsed, and deal activity froze globally.

This transaction demonstrated a critical capability: disciplined capital allocation. Many conglomerates fall in love with their acquisitions and hold too long. Pérez recognized that Unión Fenosa was a financial investment, not a strategic platform, and exited when valuations peaked. The proceeds provided firepower for deals to come.

The financial crisis of 2008 devastated Spain's construction industry. Property developers collapsed. Banks withdrew financing. Unemployment in construction soared. Many of ACS's competitors faced existential threats.

ACS survived through geographic diversification (already generating significant international revenues through Dragados), operational discipline (maintaining stronger balance sheets than peers), and strategic opportunism (using distress to acquire assets at attractive prices). The crisis years would set up the most transformative deal in ACS history.

VII. INFLECTION POINT #2: The Hostile Takeover of Hochtief (2007–2011)

If the Dragados acquisition made ACS Spain's champion, the Hochtief acquisition made it a global titan. And it remains one of the most dramatic corporate takeovers in European construction history.

In March 2007, the Spanish construction group Actividades de Construcción y Servicios (ACS) purchased Custodia's shares for €72 per share, with the transaction amounting to over €1.26 billion. This initial stake of approximately 25% announced ACS's intentions to German financial markets.

Hochtief was no ordinary target. HOCHTIEF, a globally renowned infrastructure group, excels in construction, services, and concessions/PPP. With a century-long legacy, it shapes the world through iconic projects like the Gotthard Tunnel and Madison Square Garden.

Founded in 1873, Hochtief had built an extraordinary portfolio of landmark projects: the Munich Olympic Stadium, the Elbphilharmonie concert hall in Hamburg, and infrastructure across five continents. More importantly for ACS's strategy, Hochtief had made two crucial acquisitions that ACS coveted.

Crucial milestones in this regard were the acquisition of the Turner Corporation in the USA (100 percent since 2000) and Australia's Leighton Holdings (50.2 percent majority shareholding since 2001).

Turner Construction had become America's largest general building contractor—a remarkable achievement for a German-owned subsidiary. Leighton Holdings dominated Australian infrastructure and mining services. Through Hochtief, ACS could access the world's two most attractive developed-market construction sectors in a single deal.

The German resistance proved fierce. This acquisition was classified as a 'hostile takeover', a seldom occurrence in Germany. The first was registered as recently as 1997, and was a national affair when Krupp-Hoesch acquired and merged with Thyssen.

Hochtief's management deployed every defensive tactic available under German corporate law. They questioned ACS's financial capacity to complete the deal. They warned about job losses and cultural incompatibility. They attempted to rally German institutional investors behind a "German solution." German labor unions and politicians expressed concern about foreign ownership of a national industrial champion.

After improving the offer to nine ACS shares for five Hochtief shares, ACS announced in January 2011 that it held over 30% of Hochtief's shares following the conclusion of the takeover bid.

During April 2011, the firm raised its stake in Hochtief to 50.16%, effectively acquiring the company. Hochtief got acquired by Grupo ACS on Jun 18, 2011.

The acquisition goodwill of €1,144 million came from the acquisition of HOCHTIEF in 2011.

The deal transformed ACS's geographic profile virtually overnight. Through Hochtief's subsidiaries, ACS now had leading positions in North America (Turner), Asia-Pacific (Leighton/CIMIC), and Europe (Hochtief's German and pan-European operations). The combination created one of the world's most geographically diversified construction groups.

The integration unfolded over years rather than months. ACS installed its people in key management positions, beginning with Marcelino Fernández Verdes in November 2012. Under the stewardship of Mr Fernández, HOCHTIEF has undergone a process of transformation with its strategy now focused on sustainable cash-backed profit generation and an improved approach to risk management.

VIII. Global Footprint: The Turner, CIMIC & International Expansion Story

The acquisition of a controlling stake in Germany's HOCHTIEF in 2011 provided access to the North American market through HOCHTIEF's subsidiary Turner Construction, as well as to the Asia-Pacific region through CIMIC Group (formerly Leighton Holdings).

Turner Construction: America's Largest General Building Contractor

Turner's position in the American market is difficult to overstate. As the largest general contractor in the country, Turner is a leader in all major market segments, including healthcare, education, commercial, sports, aviation, pharmaceutical, retail and green building.

But it's Turner's recent pivot that tells the most compelling story. International construction services firm Turner Construction Company has more than doubled its data center revenue Year-on-Year (YoY), increasing from $3.6 billion in 2024 to $6.4bn in the first nine months of 2025. DC projects make up 40 percent of its $40.3bn order backlog.

According to financial results released this week, ACS has had a number of significant new data center projects in the first nine months of 2025. These include a $15bn data center complex in Wisconsin, part of OpenAI's Stargate program; a more than $6bn commitment to build a 100MW data center for CoreWeave in Pennsylvania, purpose-built for AI use cases.

Turner showed strong sales growth (+45%), driven by the organic growth (+34%) in the data center, healthcare, sports and education sectors, and by the first contribution from Dornan Engineering, the Irish electromechanical engineering firm acquired by the Group in 2024. Pre-tax profit increased by 62.3% over the same period last year to over €175 million, with a continued improvement in the margin to 3% thanks to specialization in advanced technology projects. In addition, contract awards grew by 10%, pushing the project backlog to more than 33 billion euros, the company's record.

CIMIC: The Asia-Pacific Powerhouse

CIMIC Group Limited is an Australian multinational corporation specializing in engineering-led construction, mining, services, and public-private partnerships, with operations focused on infrastructure, resources, and asset lifecycle management. Headquartered in North Sydney, New South Wales, it employs around 39,000 people.

CIMIC Group has increased its ownership of mining services company Thiess to 60 per cent. "Increasing our ownership of Thiess strengthens CIMIC's business profile, as it grows its commodities portfolio to include metals and minerals critical to the world's shift to zero emissions and develops services to enable sustainable mining."

CIMIC's pre-tax profit grew by 52.2% compared to Q1 2024, reaching €119 million. The project backlog exceeded €23 billion thanks to growth in all segments, especially in data centers, defense and sustainable mobility.

The geographic diversification strategy addresses a fundamental challenge in construction: cyclicality. Building activity follows economic cycles, which vary by region. When Australia's mining sector softens, American data center construction booms. When European infrastructure spending slows, Asian urbanization accelerates. A globally diversified construction company can shift resources and capital to wherever opportunities are strongest.

IX. INFLECTION POINT #3: The Abertis Acquisition (2017–2018)

Building the World's Largest Toll Road Empire

In October 2018, ACS Group joined with the Italian holding firm Atlantia to undertake a 16.5 billion euro ($19 billion) acquisition of Abertis as part of its ambition to build the world's largest toll road group.

This acquisition marked a strategic shift toward more stable, long-term concession assets to balance the cyclical nature of the construction business.

Abertis Infraestructuras, S.A. is a Spanish worldwide corporation engaged in toll road management. The company is headquartered in Madrid. The company runs over 8,600 kilometres of toll roads in the world.

The deal structure itself was sophisticated. Rather than acquiring Abertis outright, ACS partnered with Atlantia (now Mundys), creating a consortium that could pool capital and expertise. As of 2025, Abertis's ownership structure remains unchanged, with Mundys, ACS, and Hochtief retaining their respective stakes.

The strategic logic was elegant. Construction businesses are project-based: you win a contract, execute it, collect payment, and start hunting for the next contract. Revenue can swing dramatically based on backlog timing and project mix. Concession businesses—particularly toll roads—operate under multi-decade contracts with relatively predictable traffic patterns and regulated pricing. A toll road generates cash for 30-40 years; a construction project generates cash for 3-4 years.

Abertis showed a solid operating performance, with revenue growth of 9.8% and EBITDA growth of 10.3%, thanks to the geographical distribution of the backlog and the contribution of new assets in Puerto Rico and Spain. Average traffic growth reached 1.5%, supported by the strong evolution of heavy vehicle traffic (+3.4%).

Abertis is one of the leaders worldwide in tollroads motorways management and mobility solutions, managing over 8,200 kilometres of high-capacity and quality roads and mobility services in 15 countries in Europe, the Americas and Asia. Abertis is the first national operator of motorways in Chile and Brazil, and has a significant presence in France, Spain, Italy, Mexico, the US, Puerto Rico and Argentina.

X. INFLECTION POINT #4: The Cobra/Industrial Services Sale to Vinci (2021)

The Biggest Corporate Transaction in Spain's Year—A Strategic Pivot

In March 2021, as the world was still emerging from COVID-19 lockdowns, ACS announced a deal that would reshape its portfolio: the sale of its Industrial Services division (centered on Cobra) to French construction giant Vinci.

After announcing the agreement on 1 April 2021, VINCI's acquisition of ACS's energy business was completed this morning. The acquisition covers: Most of the contracting business of the ACS Industrial Services division; 9 greenfield concession projects under development or construction, mainly electrical transmission networks in Latin America; The renewable energy project development platform.

The final purchase price of €4.9 billion, financed entirely through VINCI's available cash, equates to the enterprise value of €4.2 billion initially agreed by the parties, plus €700 million relating to cash held by the new unit and various adjustments.

It should be noted that the total value of the acquisition of Cobra IS by VINCI – including Cobra IS' cash position at the time of the acquisition and various adjustments – amounts to €5.3 billion (of which the enterprise value at the time of the acquisition was €4.6 billion).

Why sell a profitable, growing business? The answer reveals Pérez's thinking about capital allocation and strategic focus.

First, the price was exceptional. Vinci paid a premium valuation that reflected both strategic value and scarcity—there weren't many industrial services platforms of Cobra's scale available globally. ACS crystallized gains at peak valuations.

Second, Cobra's business model was becoming more capital-intensive. The renewable energy development platform required significant upfront investment in project development before revenues materialized. While potentially lucrative, this tied up capital that ACS preferred to deploy elsewhere.

Third, selling Cobra simplified ACS's structure. Investors had long complained about the complexity of ACS's corporate architecture. Divesting a major division improved transparency and allowed investors to value the remaining businesses more clearly.

At the same time, ACS has been focusing its interest on new activities such as data centres and the promotion of private construction projects in the US in high-value sectors such as technology and pharmaceuticals, both of which are quite far removed from renewables. Since the sale of Cobra, ACS's share price has tripled, so it is clear that the new strategy has been backed by the market.

The market's response validated the decision. ACS shares tripled following the sale, as investors recognized that the remaining construction and concessions businesses were higher-quality, easier to analyze, and positioned for structural growth in infrastructure spending.

XI. The Modern Era: Data Centers, AI Infrastructure & New Generation Assets (2022–Present)

The Pivot That Could Define the Next Decade

If the first four decades of ACS's history were defined by traditional infrastructure—roads, tunnels, bridges, buildings—the next chapter centers on digital infrastructure. And the company has moved with remarkable speed.

ACS has a proven track record of delivering large-scale projects for global technology clients, having constructed more than 5.5 GW of data center capacity through its subsidiaries, including Turner Construction Company (and its recently acquired division Dornan Group) and Leighton Asia.

The company's Q3 2024 results presentation highlights an investment strategy for greenfield data centers. It noted 1.1GW of capacity (278MW in Spain, 220MW in Australia, 300MW in the US, and 300MW in Chile) totaling $3.4bn in equity.

In November 2025, ACS announced a transformative partnership. ACS Group and Global Infrastructure Partners (GIP), a part of BlackRock, have entered into an agreement to form a 50-50 joint venture dedicated to developing and operating next-generation data centers worldwide. The new platform combines ACS's advanced global technology capabilities and industrial expertise with GIP's investment leadership to deliver end-to-end, global solutions for hyperscalers, AI companies and enterprises seeking rapid, scalable, and sustainable data centers.

Upon closing, the new data center development platform will consist of ACS's existing 1.7 GW portfolio of data center assets under development across Europe, the United States, and Australia. The transaction values these assets (on 100% basis) at approximately EUR 2.0 billion, consisting of a cash payment of approximately EUR 1.0 billion, plus initial earn-outs of up to EUR 1.0 billion, contingent on achieving predefined commercial milestones.

In addition to the existing portfolio of assets contributed by ACS to the platform, ACS is reviewing a pipeline of potential projects exceeding 11 GW across North America, Europe, and Asia Pacific.

The shift represents something deeper than diversification. Traditionally focused on construction services for third-party clients, ACS has begun pivoting toward a model in which it develops and owns digital infrastructure that it can lease or sell. This new direction is reflected in its ambitious global development pipeline, which is reported to total 5 gigawatts (GW) of potential data center capacity.

Our General Shareholders' Meeting has been highlighted by the achievements of a historic 2024 and the great growth prospects in new generation markets, including digitalization, defense, energy transition, critical minerals, and sustainable mobility.

The strategic rationale is compelling. Data centers require exactly the capabilities ACS has developed over four decades: complex project management, technical engineering expertise, long-term client relationships, and access to global capital. The difference is that instead of building data centers for fees, ACS now develops data centers for ownership—capturing not just the construction margin but the ongoing operating returns.

XII. Recent Developments: Flatiron Dragados & North American Dominance (2024–2025)

In July 2024, ACS announced another structural simplification with significant strategic implications. On 30 July 2024, ACS Group and Hochtief announced that Dragados North America would be integrated with Flatiron. The combined company, Flatiron Dragados, would be held 61.8% by ACS and 38.2% by Hochtief.

The company has a long-standing presence in 24 states of the United States and eight Canadian provinces. At the end of the June, the integrated business reported a project a backlog of US$17.2 billion and revenue of US$3.1 billion.

"Bringing together Flatiron and Dragados creates a strong platform for organic growth in North America," Hochtief CEO Juan Santamaría said.

The logic is straightforward: Flatiron (owned by Hochtief) and Dragados North America (owned directly by ACS through Dragados S.A.) were both operating in the same market, sometimes competing against each other, sometimes partnering on major projects. Flatiron and Dragados have also been joint venture partners and currently are in a joint venture as prime contractor for Harbor Bridge in Corpus Christi, Texas, and for Construction Package 2-3 of the California High Speed Rail project.

The combination creates the second-largest civil engineering and construction company in the United States—a formidable platform for capturing America's infrastructure renaissance. The 2021 Infrastructure Investment and Jobs Act committed over $1 trillion to infrastructure spending. State and local governments are expanding transportation networks. Private capital is flooding into data centers, renewable energy facilities, and manufacturing plants. Flatiron Dragados is positioned to capture share across all these segments.

The integration between Flatiron and Dragados North America was completed in January 2025 and led to the creation of the second largest civil contractor in the United States, with sales of over $6,000 million and a joint backlog of approximately $17 billion.

XIII. Financial Deep Dive & Current State

The numbers tell a story of disciplined growth and strengthening financial position.

Sales in 2024 grew by 16.5% to €41,633 million. Net Profit reached €828 million, meanwhile Earnings Per Share rose 7.8% to €3.23.

Group Net Profit in 2024 amounted to €828 million, 6.1% higher than in the previous period.

The Group had a positive evolution of its financial position, with a net operating cash flow that reached €2,094 million in 2024.

The backlog figures reveal future visibility. At the end of March 2025, the backlog stood at €90.81 billion, which represents a growth of 16.5% with respect to the first quarter of the previous year. This growth was due to the increase in the volume of contracts awarded during the year, which exceeded €15 billion, especially driven by the new-generation infrastructure markets.

The balance sheet demonstrates conservative financial management. The Group maintains modest leverage relative to cash-generating capacity, providing flexibility for opportunistic acquisitions and investment in growth initiatives.

Segment performance shows diversification benefits:

Construction: The largest segment by revenue, driven by Dragados, HOCHTIEF, and Turner Construction. Sales grew by 4.9% year-on-year to €5,877 million and EBITDA reached €332 million (+13.5%). The improvement in financial results allowed Dragados to increase its pre-tax profit by 21.4% to €130 million. Dragados' backlog closed 2024 with a volume of €17,812 million, growing by 10% in 2024.

Concessions: Through ABERTIS, the segment provides stable cash flows and inflation protection. During 2024, Abertis reduced its net debt balance by more than €3,300 million, to €22,585 million, showing great financial strength, with attractive credit ratings (BBB in S&P and BBB- in Fitch) with a stable outlook.

Iridium and Data Center Development: The emerging growth engine. The joint venture with BlackRock's GIP signals the market's validation of ACS's digital infrastructure strategy.

XIV. Playbook: Business & Investing Lessons

The ACS Playbook for Serial Acquirers:

1. Buy Distressed, Fix Operationally

From Padrós to OCISA to Hochtief, the pattern repeats: acquire underperforming assets at attractive prices, apply operational discipline, and extract value that previous owners couldn't. This requires deep industry knowledge to distinguish fixable problems from terminal decline, and operational expertise to execute turnarounds.

2. Geographic Arbitrage

ACS has consistently applied Spanish management expertise to foreign markets. The engineering and project management skills developed in Spain's infrastructure boom translated directly to German, American, and Australian markets. Cultural and linguistic differences created opportunities for Spanish managers who could navigate complexity.

3. Structure for Control

The layered ownership through Hochtief → Turner/CIMIC/Flatiron creates complexity but also strategic optionality. ACS can consolidate subsidiaries, sell partial stakes, or reorganize holdings depending on market conditions. The structure enables tax efficiency and regulatory flexibility across multiple jurisdictions.

4. Counter-Cyclical Moves

Using construction cash flows to fund concession assets that provide stability represents textbook portfolio construction. When construction booms, reinvest profits in toll roads and infrastructure concessions. When construction slows, the concession cash flows support the organization through the cycle.

5. Know When to Exit

The Unión Fenosa and Cobra sales demonstrate discipline in capital reallocation. Pérez and his team don't fall in love with assets—they evaluate opportunities continuously and exit when valuations peak or strategic fit diminishes.

6. The Pérez Factor

One individual's network, relationships, and reputation enabled deals that might otherwise be impossible. Pérez's political experience, Real Madrid visibility, and decades of relationship building created access and credibility that competitors couldn't replicate.

7. Dual Identity as Moat

The Real Madrid connection provides global brand recognition and relationship capital. The Santiago Bernabéu VIP box has hosted countless deal discussions. The football club's global fan base creates awareness of ACS's brand in markets worldwide.

XV. Porter's Five Forces & Hamilton's 7 Powers Analysis

Porter's Five Forces for Global Infrastructure Construction:

| Force | Assessment | ACS Position |

|---|---|---|

| Threat of New Entrants | LOW | Massive capital requirements, bonding capacity, track record requirements, and regulatory expertise create enormous barriers. ACS has over 40 years of experience in managing and developing concession projects globally. |

| Supplier Bargaining Power | MODERATE | Materials (steel, cement, aggregates) are commoditized; specialized equipment and skilled labor can be constrained during boom cycles. ACS's scale provides negotiating leverage. |

| Buyer Bargaining Power | MODERATE-HIGH | Government contracts are competitive and politically influenced; private clients (data center hyperscalers) have significant leverage but also limited qualified supplier options. |

| Threat of Substitutes | LOW | Physical infrastructure cannot be easily substituted; modular construction and prefabrication are complements rather than substitutes. |

| Competitive Rivalry | HIGH | Competition from Vinci, Ferrovial, Bouygues, Skanska, and Chinese state-owned enterprises creates constant pressure on margins and contract terms. |

Hamilton Helmer's 7 Powers Framework:

Scale Economies: ACS benefits from purchasing power, shared services, and brand recognition across global operations. The ability to bid on projects that smaller competitors cannot bond creates natural advantages.

Network Effects: Limited in traditional construction, but potentially significant in concessions where interconnected toll road systems (like Abertis's European network) create operational efficiencies and data advantages.

Counter-Positioning: ACS's integrated model—combining construction with concessions and now digital infrastructure development—creates a business model that pure-play competitors cannot easily replicate without cannibalizingstheir existing relationships.

Switching Costs: High in concessions (multi-decade contracts) but low in construction (project-based relationships). The data center pivot could create recurring relationships with hyperscalers.

Branding: The Real Madrid association provides global awareness that pure construction companies cannot match. Turner's reputation in American markets and Hochtief's legacy in European markets provide localized brand power.

Cornered Resource: Pérez himself represents a partially cornered resource—his relationships, reputation, and strategic vision are not easily replaceable.

Process Power: Decades of operational discipline in executing complex projects create institutional knowledge that competitors cannot quickly replicate.

Competitive Positioning

ACS has entered the top 10, moving up from 11th to 10th place. In terms of companies with a higher proportion of their sales abroad, ACS remains second in total figures with $41.145 billion, behind only France's Vinci.

Against Vinci (France), Ferrovial (Spain), Bouygues (France), and other global peers, ACS differentiates through: - Greater geographic diversification through the Hochtief acquisition - Stronger North American presence through Turner - Asia-Pacific leadership through CIMIC - Integrated concessions model through Abertis - Aggressive pivot to digital infrastructure

XVI. Key Metrics for Ongoing Monitoring

For investors tracking ACS's ongoing performance, three metrics matter most:

1. Order Backlog Growth (by Segment and Geography)

The backlog represents future revenue visibility. Growth in backlog—particularly in high-margin segments like data centers—signals continued demand for ACS's services. Watch for backlog composition shifts toward "new generation" infrastructure versus traditional civil works.

2. Concession Traffic and Toll Revenue (Abertis)

Abertis's toll roads provide the stable cash flow foundation for ACS's business model. Traffic volumes and toll revenues indicate economic health in key markets (Spain, France, Latin America, United States). Inflation-linked pricing mechanisms should translate GDP growth into revenue growth.

3. Turner Data Center Backlog Percentage

Turner's data center business has emerged as the highest-growth, highest-margin opportunity. The percentage of Turner's backlog in data centers versus traditional building construction indicates whether the digital infrastructure pivot is accelerating or maturing. Currently at 40% of backlog, this metric should be watched closely.

XVII. Risk Factors and Regulatory Considerations

Regulatory and Legal Overhangs

In July 2022, the company was fined €57.1 million, along with five other contractors, by the Comisión Nacional de los Mercados y la Competencia (CNMC) for bidding collusion in public tenders for building and civil infrastructure works.

This fine, while manageable relative to ACS's scale, highlights the regulatory scrutiny that large infrastructure companies face. Government contract investigations, antitrust concerns, and compliance requirements create ongoing legal and reputational risks.

Accounting Considerations

The goodwill balance—€4,754 million, including €554 million from the ACS and Dragados Group merger in 2003, €1,144 million from the acquisition of HOCHTIEF in 2011, and €1,900 million from full consolidation of Thiess in Q2 2024—represents acquisitions at prices above book value. Investors should monitor for impairment risk if subsidiary performance deteriorates.

Concentrated Leadership Risk

Florentino Pérez has dominated ACS's strategy for over three decades. At 78 years old, succession planning becomes increasingly relevant. In January 2025, Pérez was re-elected as club's president until 2029. While Juan Santamaría serves as Group CEO and has demonstrated strong execution, Pérez's relationships and strategic vision are not easily transferred.

Cyclical Exposure

Despite diversification into concessions, construction remains the dominant revenue source. Economic downturns in key markets (United States, Australia, Germany, Spain) would pressure volumes and margins. The data center boom could reverse if technology companies pull back capital spending.

XVIII. The Real Madrid Dimension

No analysis of ACS is complete without addressing the Real Madrid connection—not as a curiosity, but as a genuine business asset.

Florentino Pérez delivered a long speech during the General Assembly of Real Madrid, highlighting the economic power of the club. "Two seasons ago, we were the first club to exceed a billion euros in turnover. And this season we reached 1.185 billion euros, an increase of 10%."

"Our net assets reached 598 million euros… We invested 1.347 billion euros in the Bernabéu… the club made a significant contribution to the public economy, paying 356 million euros."

The Santiago Bernabéu renovation demonstrates capabilities that apply directly to ACS's commercial strategy: complex urban construction, retractable roof engineering, integrated technology systems, stakeholder management. With a seating capacity of 83,186 following its extensive renovation completed in late 2024, the stadium has the second-largest seating capacity for a football stadium in Spain.

Forbes has recognized Real Madrid as the most valuable sports club in the world, with Los Blancos having a value of US$6.07 billion.

The cross-pollination is real. ACS engineers have worked on Bernabéu projects. The VIP relationships cultivated through football extend into business development. The global visibility from Real Madrid's 700 million fans creates awareness for ACS in markets where it operates.

XIX. Conclusion: The Building Never Stops

From a failing Spanish contractor purchased for symbolic value in 1983 to a global infrastructure titan generating over €40 billion in annual revenue, Grupo ACS represents one of the most successful corporate transformations in modern business history.

The playbook—buy distressed assets, apply operational discipline, acquire transformative platforms, diversify geographically, shift toward stable recurring revenues, and pivot toward emerging opportunities—has been executed with remarkable consistency across four decades.

Today, ACS stands at another inflection point. The data center boom represents an opportunity comparable in scale to the Spanish infrastructure buildout of the 1980s or the Hochtief acquisition of 2011. The BlackRock partnership validates ACS's positioning in this structural growth opportunity.

The risks are real: cyclical exposure, regulatory scrutiny, leadership concentration, and execution challenges in a rapidly evolving digital infrastructure market. But the track record suggests ACS knows how to navigate complexity and capitalize on transformational moments.

For Florentino Pérez—now 78 years old, still running both ACS and Real Madrid, still hunting for the next deal—the building never stops. And for investors seeking exposure to global infrastructure, ACS offers something few competitors can match: a proven playbook, global scale, and the adaptive capacity to pivot toward whatever infrastructure the world needs next.

Myth vs. Reality

MYTH: ACS is primarily a Spanish construction company. REALITY: Spain represents a minority of revenues. North America (through Turner and Flatiron Dragados), Asia-Pacific (through CIMIC), and Europe (through Hochtief) dominate the revenue base. ACS is a global infrastructure company headquartered in Spain.

MYTH: The Real Madrid connection is a distraction from ACS's business. REALITY: The dual role provides relationship capital, brand recognition, and demonstration projects (like the Bernabéu renovation) that create genuine business value.

MYTH: ACS is a traditional construction company facing disruption. REALITY: ACS has actively pivoted toward digital infrastructure, with data centers now representing 40% of Turner's backlog and a potential 11+ GW development pipeline globally.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube