Antero Resources: The Shale Revolution's Serial Entrepreneurs

I. Introduction & Episode Roadmap

The Appalachian Basin stretches across the eastern United States like an ancient geological fingerprint—layers of rock deposited over 400 million years, hiding what would become the world's second-largest natural gas deposit. In the heart of West Virginia and Ohio, drilling rigs now punctuate the rolling hills where coal once reigned supreme. At the center of this transformation stands Antero Resources, a Denver-based company that has quietly become one of America's most important natural gas producers.

Antero Resources Corporation is an independent exploration and production company focused on the development and production of natural gas, natural gas liquids (NGLs), and oil in the Appalachian Basin of the United States. Founded in 2002, the company has grown into one of the largest U.S. producers of natural gas and NGLs, ranking as the sixth-largest natural gas producer and fourth-largest NGL producer in the country.

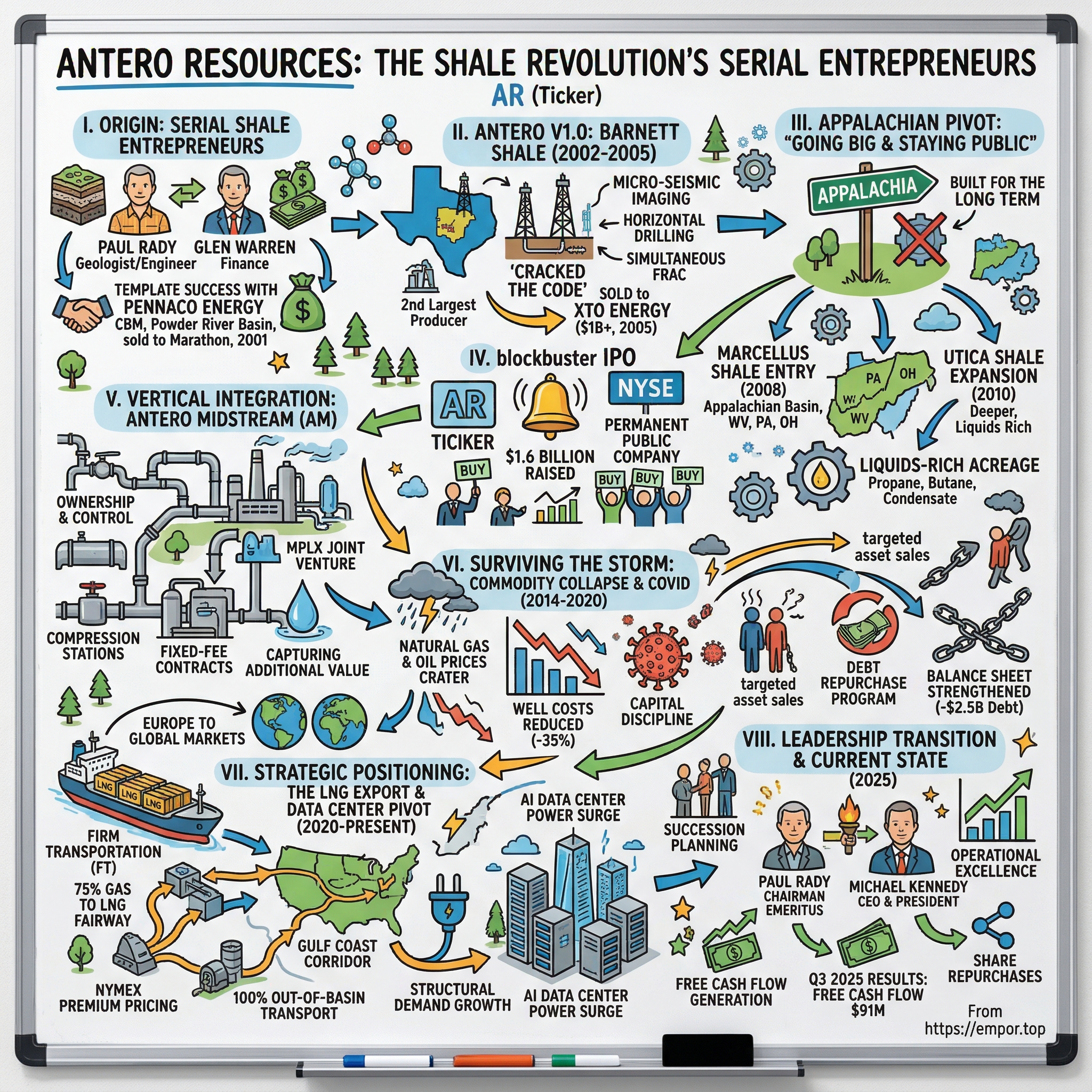

But here's what makes the Antero story genuinely fascinating: this is not the founders' first rodeo. Paul Rady and Glen Warren didn't just build one successful shale company—they built three. The question that animates this deep dive is deceptively simple: How did a pair of serial entrepreneurs repeatedly build and flip shale companies, then finally decide to go big and stay public?

The answer illuminates something profound about the American energy business: in an industry notorious for boom-and-bust cycles, management matters enormously. The founders' playbook—partner with private equity, identify undervalued geology, execute with operational excellence, and exit profitably—worked spectacularly until they encountered an opportunity so compelling they broke their own pattern.

Antero Resources Corporation is the most integrated natural gas and NGL business in the US and one of the largest suppliers to the country's LNG market. Through its firm transportation agreements, the company delivers the bulk of its production to premium Gulf Coast markets where LNG export terminals are hungry for molecules. This strategic positioning, combined with over 20 years of drilling inventory, has transformed Antero from a scrappy shale developer into a structural beneficiary of the global energy transition.

This episode traces Antero's journey through several distinct phases: the founders' origin story as serial shale entrepreneurs; the Barnett Shale build-and-sell that proved the model; the transformative pivot to Appalachia that created lasting value; the blockbuster IPO that marked a strategic inflection; the near-death experience during the commodity collapse; and the remarkable positioning for the LNG export megatrend that defines the company today. Along the way, we'll examine how vertical integration through Antero Midstream created a competitive moat, how capital discipline saved the company during the darkest days of the pandemic, and what the August 2025 leadership transition means for the next chapter.

The themes that emerge—founder-led execution, geological contrarianism, operational intensity, and strategic patience—offer lessons that extend far beyond the oil and gas sector.

II. The Founders' Origin Story: Serial Shale Entrepreneurs

To understand Antero Resources, you must first understand Paul Rady and Glen Warren—two men who spent decades learning to read the subtle geological signals that separate mediocre acreage from world-class reserves.

Prior to founding Antero, Rady was chairman, president and CEO of Pennaco Energy Inc., which was sold to Marathon Oil. Warren was executive vice president and CFO of Pennaco. Rady and Warren led Pennaco from its start as a small acreage-holder in the Powder River Basin play in Wyoming into a public company with net production of over 50 million cubic feet per day.

The Pennaco story set the template. In the late 1990s, coalbed methane in Wyoming's Powder River Basin was considered a marginal resource—expensive to develop and technically challenging. Rady, an engineer with deep expertise in unconventional reservoirs from his years at Amoco and Barrett Resources, saw something others missed: the right combination of geology, technology, and market timing could unlock enormous value.

Pennaco only produces coalbed methane gas from the Powder River Basin of northern Wyoming and southern Montana. It is one of the largest leaseholders in the area with more than 400,000 net acres and net production of over 50 MMcfgd. Net proven reserves are 200 bcf, with over 800 bcf of upside potential.

Within just two and a half years, the duo transformed Pennaco from a small acreage holder into one of the basin's dominant producers. Marathon Oil came calling, and in early 2001, Marathon put together a $500 million deal to acquire Pennaco Energy Inc. To make the deal, Marathon paid about $19 a share—$446 million in cash, including $54 million for Pennaco's debt. The deal represented a 30% premium to Pennaco's price.

This exit crystallized the playbook: identify an emerging unconventional play before it becomes conventional wisdom, assemble a dominant land position, prove up the resource through aggressive drilling, and sell to a larger company seeking proven reserves. The approach required equal parts geological insight, operational excellence, and financial discipline.

Prior to Pennaco, Rady was president and CEO of Barrett Resources Corp., which was sold to The Williams Companies. The Barrett experience had taught Rady the importance of scale and operational control. The Pennaco exit taught both founders that private equity partnerships could accelerate the model dramatically.

Paul Rady noted: "For more than 20 years, Glen and I have been partners across a number of successful plays and organizations. We were some of the first successful players in unconventional resources, initially in coal bed methane in the Powder River Basin, then in the Barnett Shale where we were early adopters of horizontal drilling and multi-stage completions."

The partnership between Rady and Warren proved remarkably durable—a rarity in an industry where ego clashes and strategic disagreements frequently fracture executive teams. Their complementary skills created a powerful combination: Rady brought the geological vision and technical credibility, while Warren contributed financial engineering and capital markets expertise. "It has been one of the greatest honors of my career to partner with Paul Rady and to help lead the growth of the Antero entities from the ground floor," Warren later reflected. "I have so many great memories over the years, from the multitude of relationships built to the countless milestones achieved."

The team's continuity was remarkable: Paul M. Rady, Chairman and CEO, and Glen C. Warren, Jr., President and CFO, formed Antero Resources Corporation in 2002 and funded the company in early 2003 with the current investor group. The majority of management had worked together for over 30 years across multiple ventures—Amoco Production Company, Barrett Resources Corporation, Pennaco Energy Inc., and now Antero Resources. This institutional knowledge and proven chemistry became a competitive advantage that's difficult to replicate.

With the Pennaco proceeds in hand and their reputations established, Rady and Warren were ready to deploy the playbook again—this time in a formation that would reshape American energy: the Barnett Shale.

III. Antero Version 1.0: Barnett Shale & First Exit (2002-2005)

The year 2002 marked a pivotal moment in American energy history. Deep in the Fort Worth Basin of North Texas, a stubborn wildcatter named George Mitchell had finally cracked the code on the Barnett Shale after two decades of experimentation. His breakthrough—combining horizontal drilling with hydraulic fracturing—would eventually liberate trillions of cubic feet of natural gas locked in tight shale formations. But in 2002, the Barnett was still considered a curiosity, not a revolution.

Paul Rady and Glen Warren saw opportunity where others saw uncertainty. Fresh from their Pennaco success, they founded Antero Resources Corporation with a singular focus: become a dominant Barnett Shale producer before the rest of the industry woke up.

Beginning in February 2003, Warburg Pincus invested over $1.5 billion into the company and at one time held a controlling stake. This partnership with one of the world's most sophisticated private equity firms provided not just capital, but strategic credibility and operational support. Warburg's energy team had backed numerous successful E&P companies and understood the unconventional resource development model that Rady and Warren proposed.

The execution was breathtaking in its speed. The company was focused on the Barnett shale, eventually becoming the second-largest producer and second-most-active operator until its sale in April 2005 to XTO Energy Inc. for more than $1 billion in cash and stock.

In less than three years, Antero had grown from a startup to the Barnett's second-largest producer. The company wasn't just drilling wells—it was innovating. Antero pioneered the use of micro-seismic imaging technology, which allowed operators to visualize fracture propagation in real-time, dramatically improving well placement and completion design. The team also performed the first simultaneous fracture stimulation in the play, a technique that would become standard practice across the shale industry.

The company's early efforts centered on the Barnett Shale in Texas, where it rapidly expanded operations to become the second-largest producer in the play within three years, drilling hundreds of horizontal wells and pioneering advanced completion techniques.

The sale to XTO Energy validated every element of the playbook. XTO, led by the legendary Bob Simpson, was building a shale empire through strategic acquisitions of proven assets. Antero's Barnett position offered exactly what XTO needed: core acreage, proven reserves, and operational excellence. The billion-dollar transaction represented a spectacular return for Warburg Pincus and the management team—and confirmed that their approach could be repeated.

The lessons from Barnett were clear: speed to scale mattered enormously in land-based plays; operational innovation could differentiate seemingly similar geology; and the right exit partner valued execution as much as reserves. But there was another lesson too: knowing when to sell. The Barnett was getting crowded, drilling costs were rising, and the easy gains had been captured. Better to monetize the position and redeploy capital into the next opportunity.

The company's fast growth (production was up 121% in the second quarter) and experienced management team (the founders sold XTO in 2005 for $1.0 billion) helped establish the company's reputation.

What makes the Barnett chapter instructive is how decisively Rady and Warren executed their exit. Many operators struggle to sell successful assets—the temptation to keep drilling, to capture one more well's worth of returns, proves irresistible. But the Antero team understood that timing the cycle was as important as geological selection. They sold at or near the peak of Barnett enthusiasm, freeing capital and management attention for the next opportunity.

IV. Antero Version 2.0: Arkoma, Piceance & Setting the Stage (2005-2008)

With XTO's check clearing and their reputation enhanced, Rady and Warren immediately pivoted to the next opportunity. The Antero name lived on, but the company's geographic focus shifted dramatically.

The current Antero group has been focused on developing properties in the Arkoma Basin of Oklahoma and the Piceance Basin of Colorado. Antero currently operates 11 rigs and has more than 120,000 net leasehold acres with more than 2,800 proved, probable and possible gross drilling locations. Gross operated production in the Woodford shale play of the Arkoma Basin is 34 million cubic feet of gas per day and in the Piceance Basin is 20 million cubic feet per day.

The Woodford Shale in Oklahoma's Arkoma Basin represented the next frontier in unconventional development. Rady and Warren applied the same formula: acquire land aggressively, prove up the resource, and operate at industry-leading efficiency. By 2007, Antero had assembled 100,000 net acres in the Woodford and 46,000 acres in the Piceance.

Antero has drilled over 200 horizontal wells in the Barnett Shale and Woodford Shale and is currently operating six rigs drilling horizontally on its 100,000 net acres in the Arkoma Basin Woodford Shale play in eastern Oklahoma and four rigs on its 46,000 net acres in the Piceance Basin in western Colorado. In August 2007, shareholders including Warburg Pincus, Yorktown Partners and Lehman Brothers Merchant Banking committed $1 billion of equity to support Antero's growth.

The $1 billion equity commitment from Warburg Pincus, Yorktown Partners, and Lehman Brothers represented extraordinary confidence in the management team. This wasn't seed capital—it was growth capital, earmarked for rapid land acquisition and aggressive drilling programs. The timing would prove fortuitous for reasons nobody anticipated.

But even as Antero built its Arkoma and Piceance positions, Rady was watching something remarkable unfold 1,500 miles to the east. In the Appalachian Basin of Pennsylvania and West Virginia, a formation called the Marcellus Shale was generating buzz among geologists and early-mover operators. The Devonian-age rock extended nearly 100,000 square miles and appeared to contain gas in quantities that defied conventional thinking.

The strategic discipline that defined Antero's approach became evident in 2010. In 2010, Antero sold its midstream assets in the Woodford Shale area of the Arkoma Basin for $268 million, streamlining operations toward upstream activities in higher-return areas. Rather than spreading resources across multiple basins, the team recognized that the emerging Appalachian opportunity demanded total focus. The Arkoma midstream sale demonstrated the founders' willingness to exit perfectly good assets when superior opportunities beckoned.

This period also revealed something important about the Antero approach to capital allocation. Unlike many E&P companies that diversified across multiple basins as a hedge, Rady and Warren preferred concentration. They believed that operational excellence came from deep familiarity with specific geology, and that spreading management attention diluted returns. The decision to exit non-core assets and redeploy capital into Appalachia would prove to be among the most consequential in company history.

V. The Appalachian Pivot: Entering Marcellus & Utica (2008-2012)

The Marcellus Entry (2008)

September 2008 was an extraordinary moment to be making multi-hundred-million-dollar bets on shale gas. Lehman Brothers had just collapsed, credit markets were frozen, and the global financial system teetered on the edge of collapse. Dominion Resources, the Virginia-based utility, had agreed to sell Marcellus Shale drilling rights on approximately 205,000 acres for $552 million—but the deal had to be restructured as financing conditions deteriorated.

The Denver-based, privately held Antero Resources Corp., has closed its acquisition of Marcellus shale rights only from integrated energy company Dominion for approximately $347 million, resulting in after-tax proceeds of approximately $205 million to Dominion. The assets include 114,259 acres largely in western Pennsylvania and West Virginia. When announced in June, the deal was to involve 205,000 acres for $552 million. Dominion scaled back the sale "due to Antero's difficulty in obtaining follow-on financing in the current market turmoil."

The market turmoil that forced the deal's restructuring also created the opportunity. Antero paid approximately $3,037 per acre—a price that would soon look like one of the great bargains in energy industry history. Within a few years, Utica Shale leases in similar core areas would trade at nearly double that price.

When Antero acquired its initial Marcellus acreage from Dominion in 2008, natural gas prices were at an all-time high, from $8 to $12 per Mcf. "We didn't have processing at first, and we were going for the dry gas initially," Warren said. The company drilled 142 dry gas wells primarily in Harrison County with an average 30-day rate of 6 million cubic feet per day on an average 6,900-foot lateral.

The entry into Appalachia represented more than a geographic shift—it was a strategic commitment to what would become North America's most prolific natural gas region. The Marcellus Shale extends nearly 100,000 square miles across the Appalachian basin and contains approximately 410 trillion cubic feet of natural gas, making it the world's second-largest natural gas find after the South Pars field in Iran.

Antero Resources entered the Appalachia Basin in 2008 and drilled its first Marcellus Shale wells in 2009.

Utica Shale Expansion (2010)

Having established a beachhead in the Marcellus, Antero expanded aggressively into the underlying Utica Shale beginning around 2010. The Utica, slightly deeper than the Marcellus, offered additional drilling targets and exposure to natural gas liquids that commanded premium prices.

The decision around 2008 to enter the Marcellus Shale, followed by the Utica Shale in 2010, and the subsequent divestiture of non-Appalachian assets, fundamentally reshaped the company.

Key acquisitions bolstered this expansion. In September 2011, Antero announced that it had acquired a 7% overriding royalty interest from CONSOL Energy in approximately 115,000 net acres located in the southwestern core of the Marcellus Shale play for $193 million. The cash transaction closed on September 21, 2011 with an effective date of July 1, 2011. The acquisition of the CONSOL ORI increases Antero's average net revenue interest to 87% in the 115,000 net Marcellus acres that the company acquired from Dominion Resources in September 2008.

By 2012, Antero had secured high-value Utica Shale leases in eastern Ohio at record rates of up to $5,900 per acre—nearly double what the company paid for its original Marcellus position. But more importantly, the company had assembled a vast, contiguous acreage position in the core of both plays. Following the closing of the acquisition and the clearing of ownership discrepancy on the 5,000 net acres mentioned previously, Antero now owns over 200,000 net acres of leasehold in the Marcellus Shale play.

Why the Bet on Appalachia Was Transformative

The Appalachian pivot concentrated the company's resources on what would become North America's most prolific natural gas region. Several factors made this bet transformative:

Scale Advantages: The contiguous nature of Antero's acreage enabled operational efficiencies impossible with scattered positions. Drilling rigs could move from pad to pad with minimal mobilization time. Infrastructure could be built once and utilized across thousands of wells.

Decades of Inventory: The large land position provided drilling locations for 20+ years, creating visibility into long-term production and cash flows that attracted institutional investors.

Liquids Richness: The southwestern core of the Marcellus and portions of the Utica contained significant natural gas liquids—propane, butane, and natural gasoline—that commanded premium prices relative to dry natural gas.

Infrastructure Proximity: Unlike some remote shale plays, Appalachia sat relatively close to major population centers and existing pipeline networks, reducing the build-out costs required to bring production to market.

Paul Rady knows unconventional gas plays. In the late 1990s he, along with wingman Glen Warren, built Pennaco Energy, a Powder River Basin coalbed methane producer, into the highest-return public E&P of its day before selling in 2001. Next, they formed Antero Resources in the upstart Barnett Shale, forging the second-largest producer in the play in advance of its 2005 sale. Rady refocused in the Woodford Shale, again growing to No. 2 in total production. He ultimately sold the asset for nearly a half billion dollars in 2012.

The decision not to sell Appalachia marked a profound departure from the build-to-sell playbook. For the first time, Rady and Warren were building to keep. The opportunity was simply too large, too promising, and too strategically important to hand off to another operator. The Appalachian pivot wasn't just a geographic shift—it was the moment Antero Resources transformed from a serial asset flipper into a company built for the long term.

VI. The IPO & Becoming a Public Company (2013)

By the fall of 2013, Antero Resources had transformed from a private E&P with a decade of history into a pure-play Appalachian juggernaut. The company had sold its Arkoma and Piceance assets, concentrated entirely on the Marcellus and Utica, and was drilling at a pace that demanded access to the public capital markets.

In 2013, Antero Resources transitioned to a publicly traded company through an initial public offering on the New York Stock Exchange under the ticker symbol AR. The IPO, completed on October 16, 2013, involved the sale of 41,083,750 shares of common stock at $44.00 per share, raising approximately $1.6 billion in net proceeds, which were primarily used to repay borrowings under the company's credit facility.

The initial $1.5 billion deal value is the largest U.S.-listed E&P IPO since Statoil ASA's $2.9 billion opening in June 2001. The Denver-based E&P has become a "must-own" name because of its dominance in the Marcellus and Utica shales.

The IPO wasn't just large—it was extraordinarily well-received. Antero Resources raised $1.6 billion by offering 35.7 million shares (19% above the 30 million originally planned) at $44, above the range of $38 to $42. It is the second largest US IPO of the year, behind only Zoetis.

Investors poured into onshore operator Antero Resources in its debut Thursday on the New York Stock Exchange, gaining more than 18% to close at $52.01. "AR," the most heavily traded stock of the day, saw more than 28.4 million shares trade hands. Based on investor interest, Antero was estimated to be worth about $11 billion.

What drove such intense investor enthusiasm? Several factors converged:

Proven Management Team: The company's fast growth (production was up 121% in the second quarter) and experienced management team (the founders sold XTO in 2005 for $1.0 billion) helped the stock rise 21%.

Prime Acreage Position: With approximately 329,000 net acres in the Marcellus, 102,000 in the Utica, and 170,000 in the Upper Devonian, Antero had assembled one of the largest and most contiguous positions in the core of Appalachia.

Operational Momentum: Since initiating the drilling program with one rig in 2009, Antero had invested over $3.9 billion in land and drilling in the Appalachian Basin. With 15 rigs running in the Marcellus Shale, it was the most active driller in the area.

The company was formerly known as Antero Resources Appalachian Corporation and changed its name to Antero Resources Corporation in June 2013.

The IPO proceeds allowed Antero to accelerate drilling dramatically. The company increased its drilling and completion capital budget to $1.8 billion in 2014, up from prior years, to support an expanded program that included an average of 21 rigs across both plays.

Private equity continued to exert significant control over Antero, with Warburg affiliated funds holding more than 38% of the voting interests in Antero Resources Investment LLC, which owned 87% of the producer. Yorktown Partners LLC and Trilantic Capital Partners also own stakes.

For Warburg Pincus, the IPO represented the beginning of an exit from an investment that had delivered spectacular returns. But for Antero's management team, going public meant something different: permanent access to public capital markets, the ability to make acquisitions using stock, and a currency for management compensation. Most importantly, it signaled that Rady and Warren intended to run Antero for the long term—a dramatic departure from their previous build-and-sell pattern.

The decision to become a permanent public company carried risks. Public market investors would demand consistent quarterly performance. Short-term pressures could conflict with long-term value creation. And the cyclical nature of commodity prices meant that Antero would inevitably face periods when its stock traded far below intrinsic value.

But the opportunity in Appalachia was simply too large to capture as a private company. The capital requirements for drilling hundreds of wells per year, building out midstream infrastructure, and securing firm transportation capacity demanded the scale that only public markets could provide. Antero's management team had spent a decade proving they could create value—now they would attempt to compound it indefinitely.

VII. Midstream Integration: Creating Antero Midstream (2013-2019)

One of the most strategic decisions in Antero's history occurred almost simultaneously with the IPO: the creation of a dedicated midstream subsidiary to own, operate, and develop the infrastructure required to move the company's rapidly growing production to market.

Antero Midstream was formed by Antero Resources in 2012 to own, operate and develop midstream energy infrastructure to service Antero Resources' increasing production.

The rationale was straightforward but far-reaching. Natural gas doesn't move itself from wellhead to market. It requires gathering pipelines to collect production from individual well pads, compression stations to boost pressure for transportation, processing facilities to separate liquids from the gas stream, and fractionation plants to divide the liquids into component products. Without this infrastructure, even the most prolific wells are worthless.

Most E&P companies contract with third-party midstream providers for these services, paying per-unit fees that can consume a significant portion of wellhead revenue. Antero's founders recognized that owning the infrastructure could capture additional value and provide operational control that third-party arrangements couldn't match.

On November 4, 2014, Antero announced the pricing of the Antero Midstream Partners LP initial public offering of 40,000,000 common units representing limited partner interests in the Partnership at $25.00 per common unit. The Partnership was initially offering 37,500,000 common units at an estimated price range of $19.00 to $21.00 per common unit. The Partnership has granted the underwriters a 30-day option to purchase up to an additional 6,000,000 common units.

Antero Midstream Partners completed a $1.15 billion IPO, the lowest-yielding and largest MLP IPO to date.

The Antero Midstream IPO was remarkable for several reasons. The $1.15 billion raised exceeded Shell Midstream Partners' then-record offering by a slim margin. More importantly, the "lowest-yielding" characterization signaled investor confidence that Antero Midstream's distribution would grow substantially over time—investors were willing to accept a lower current yield in exchange for growth prospects.

The year 2014 saw two notable movements in the space: the largest MLP IPOs ever (from Antero Midstream Partners LP and Shell Midstream Partners, L.P.) as well as the mega merger of one of the MLP pioneers—Kinder Morgan—in August.

The structure worked as follows: Antero Resources would dedicate substantially all of its current and future Appalachian production to Antero Midstream under long-term, fixed-fee contracts. This guaranteed throughput provided revenue visibility that supported Antero Midstream's debt and equity costs. In return, Antero Midstream would build and operate the gathering, compression, and processing infrastructure the E&P required.

Key milestones included: 2014: Completed IPO as Antero Midstream Partners LP, raising approximately $1.15 billion. 2015: Acquired Antero Resources' water handling business for $1.05 billion. 2016: Formed joint venture with MPLX (MarkWest) for processing and fractionation services.

The 2016 joint venture with MPLX proved particularly strategic. By partnering with an established midstream operator for processing and fractionation—capital-intensive facilities that benefit from scale—Antero Midstream could expand capacity without bearing the full capital burden. Antero Midstream Partners forms a 50/50 processing & fractionation joint venture with MLPX with $800 million of new project inventory.

In 2019, Antero Resources simplified the midstream structure. In 2019, Antero Resources simplified its midstream operations by supporting the acquisition of Antero Midstream Partners LP by Antero Midstream Corporation, a controlled subsidiary, which integrated the entities and eliminated the master limited partnership structure. This transaction, completed in March 2019, allowed for streamlined governance and reduced administrative complexities while maintaining dedicated midstream infrastructure for Antero's upstream activities.

Antero Resources holds approximately 29% ownership in Antero Midstream, enabling efficient gathering, processing, and transportation of its production under long-term fixed-fee contracts.

The formation and development of Antero Midstream proved critical to Antero Resources' success. Building dedicated pipelines and processing facilities ensured efficient transport and processing for the company's growing production, particularly its significant NGL volumes. This integration provided operational control and captured additional value that would otherwise flow to third-party infrastructure owners.

Today, Antero Midstream Corporation is a growth-oriented midstream energy company that owns, operates, and develops midstream energy infrastructure primarily to service Antero Resources Corporation's increasing production in the Appalachian Basin. Headquartered in Denver, Colorado, Antero Midstream provides gathering, compression, processing, and fractionation services through its extensive network of pipelines and compressor stations.

VIII. Surviving the Storm: 2014-2020 Commodity Collapse & COVID

The all-time high Antero Resources stock closing price was 64.91 on March 25, 2014.

That high-water mark came less than six months after Antero's triumphant IPO. What followed would test every assumption about the company's business model, management capability, and financial resilience.

Natural gas prices, already pressured by the shale production boom, collapsed from over $4 per million BTUs to below $2 by early 2016. Oil prices, which had traded above $100 per barrel in mid-2014, cratered below $30 in early 2016. The entire energy sector entered a multi-year depression that eliminated companies, destroyed capital, and forced a fundamental rethinking of how E&P businesses should be run.

For Antero, the timing was particularly challenging. The company had just completed an aggressive IPO, committed to rapid production growth, and begun building midstream infrastructure that required continued drilling to justify. The stock price, which had touched nearly $65 in early 2014, would eventually trade below $5 during the darkest days of 2020.

The turnaround strategy centered on three pillars: capital discipline, operational efficiency, and opportunistic debt management.

Facing depressed commodity prices during the 2020–2022 period, Antero prioritized debt reduction through targeted asset sales, midstream fee renegotiations, and operational cost efficiencies. In late 2019, the company announced a non-core asset divestiture program expected to generate over $1 billion in proceeds, which funded substantial debt paydowns.

The asset sale program proved transformative. By selling non-core properties—acreage outside the liquids-rich fairway where drilling economics were less compelling—Antero generated proceeds to reduce debt while concentrating on its highest-return locations. The discipline required to sell assets during market weakness, when buyers demanded discounts, revealed management's commitment to balance sheet improvement over production growth.

By 2022, these efforts culminated in approximately $1 billion of debt reduction that year alone, contributing to a cumulative $2.5 billion decrease since 2019, with net debt-to-EBITDAX dropping to 0.4x.

Well costs became a critical focus. Through design optimization, drilling efficiency improvements, and completion innovation, Antero drove unit costs dramatically lower. The 2021 capital budget reflected a shift to maintenance-level capital plans and well cost savings initiatives launched in 2019. Total well costs were targeted at $635 per lateral foot for the second half of 2021, a 35% reduction from $970 in the initial 2019 budget.

The debt repurchase strategy deserves particular attention. When Antero's bonds traded at discounts to par value—reflecting market skepticism about the company's ability to survive—management bought back debt at prices that captured meaningful savings. As Michael Kennedy, then CFO, noted: "Antero's investment grade credit rating reinforces the strength of our company, driven by the success of our development program and commitment to debt reduction over the last several years. Since the start of our debt reduction program in the fourth quarter of 2019, we have reduced debt by more than $2 billion."

Under Glen Warren's co-leadership, Antero Resources reset its balance sheet and cost structure, generated significant free cash flow, and expected to reduce leverage below 2.0x in 2021. In addition, Antero Midstream became one of the only midstream companies in the industry with the optimum combination of c-corp governance, a self-funding business model after dividends, long-term growth and a declining leverage profile with already one of the strongest balance sheets in the midstream industry.

The turnaround wasn't just about survival—it was about positioning for the recovery. By maintaining core operations while competitors went bankrupt or slashed activity to bare minimums, Antero preserved its operational capabilities and drilling inventory. When commodity prices eventually recovered, the company would be positioned to generate substantial free cash flow.

The period also marked Glen Warren's departure from day-to-day management. In April 2021, Glen Warren retired as President and Chief Financial Officer of Antero Resources and President of Antero Midstream. Mr. Warren also stepped down from the board of both companies as of the same date.

Warren noted: "Going forward, the Antero entities are very well positioned with the lowest debt levels since being public and one of the strongest, most integrated teams in the industry with the continued outstanding leadership of Paul."

IX. The LNG Export Pivot: Positioning for Global Markets (2020-Present)

As Antero emerged from the commodity collapse, management recognized that the company's greatest strategic asset wasn't just its acreage or operational capabilities—it was something less visible but potentially more valuable: a portfolio of firm transportation agreements that could move the company's production to premium markets.

As Michael Kennedy explained: "Looking ahead to 2025, our firm transportation portfolio delivers 75% of our natural gas to the LNG corridor along the Gulf Coast, and is expected to result in higher premium price realizations to NYMEX following the recent start-up of two large LNG export terminals in the Gulf."

This positioning was no accident. While most Appalachian producers sold their gas at regional delivery points—where persistent pipeline constraints often caused prices to trade at significant discounts to national benchmarks—Antero had systematically assembled transportation capacity that reached the Gulf Coast LNG corridor. The strategy required years of advance planning and substantial financial commitments for pipeline capacity that might not be fully utilized until export demand materialized.

Justin Fowler, senior vice president of natural gas marketing, emphasized Antero's transportation portfolio, "which delivers 100% of natural gas out of the Appalachian Basin—75% destined for the LNG fairway and into Tier 1 Gulf Coast pricing points."

"This firm transportation delivers 100% of our natural gas out of basin, including 75% that is delivered to the LNG fairway and is tied directly to Nymex Henry Hub pricing." This compared to only 13% Henry Hub-linked production on average for Appalachian peers.

The contrast with competitors is stark. Most Appalachian producers receive prices indexed to local hubs like Dominion South or Eastern Gas South, which frequently trade $0.30 to $0.50 per thousand cubic feet below Henry Hub. Antero's firm transportation agreements essentially allow the company to "import" Gulf Coast pricing into Appalachia, adding that differential directly to realized prices.

Antero holds 2.3 Bcf/d of firm transportation to LNG export areas, including Cove Point in Maryland and the Gulf Coast. Approximately 75% of Antero's first-quarter 2022 gas volumes were sold into hubs that serve LNG export terminals.

The LNG export thesis rests on a simple observation: U.S. natural gas is the cheapest major source of natural gas in the world, while European and Asian prices are substantially higher. The spread between Henry Hub (around $3) and international benchmarks (often $10-15 or higher) creates enormous value for any U.S. producer who can access the LNG export market. And Antero, through its transportation agreements, has essentially reserved a seat at the table.

Remaining LNG projects would result in more than 10 Bcf of natural gas demand by the end of 2027, bringing the current 14.5 Bcf/d of U.S. LNG capacity to 25 Bcf/d. And by 2025, total exports, including LNG and Mexico pipeline flows, are expected to increase by nearly 8 Bcf/d. "This is a substantial demand increase that we expect to tie U.S. natural gas prices more closely to the higher international prices," Fowler said.

The company has chosen to remain largely unhedged on natural gas prices, betting that the structural growth in LNG demand will support pricing. As Kennedy explained the strategy: "We see the optionality around that as being substantial for Antero because you just don't know where that's going to go with the next wave of LNG being built and there's going to be a lot of competition for that gas, and we're the ones with transport."

Paul Rady emphasized: "Looking ahead, natural gas demand is expected to grow by more than 25% by 2030 driven by LNG export growth and increasing power demand fueled by AI Data Centers. With firm transportation capacity to the Gulf Coast LNG corridor and over 20 years of premium drilling inventory, Antero is uniquely positioned to benefit from both the significant new LNG capacity and the strong regional power demand growth that is anticipated by the end of the decade."

The AI data center demand thesis adds another dimension. Antero anticipates as much as 5 Bcf/d of incremental natural gas demand across Appalachia by 2030, driven by power plants and AI data center projects. In-basin gas demand has grown by 2 Bcf/d in just the past quarter.

Paul Rady stated that the industry now expects natural gas demand to soar 25% by 2030, led by LNG growth and then by data center power thirst.

X. Modern Era: Leadership Transition & Current State (2021-2025)

On August 14, 2025, Antero Resources Corporation and Antero Midstream Corporation announced that Michael N. Kennedy will serve as Chief Executive Officer and President of Antero Resources and Antero Midstream, and serve on each company's Board of Directors. Mr. Kennedy's promotion comes in connection with the announcement that Paul M. Rady will transition from his roles as Chief Executive Officer and President and member and Chairman of the Boards of Directors of Antero Resources and Antero Midstream to Chairman Emeritus.

This leadership transition marked the end of an era. Paul Rady had led Antero since its founding in 2002, building the company from a private equity-backed startup into a publicly traded producer worth roughly $10 billion. Rady co-founded Antero and has served as CEO and chairman since its inception. Under his direction, the Antero chain of companies grew to a combined enterprise value of about $24 billion.

The choice of Kennedy as successor reflected careful succession planning. Mr. Kennedy joined Antero in 2013, and his impact has been felt throughout the organization. Mr. Kennedy has served as Chief Financial Officer of Antero Resources since 2021 and SVP—Finance of Antero Resources and Antero Midstream since 2016.

Kennedy joined Antero in 2013 and has held financial leadership roles at both Antero Resources and Antero Midstream. He previously worked as CFO at Forest Oil Corp. and began his career as an auditor at Arthur Andersen.

"Mike Kennedy is an inspirational leader with extensive oil and gas industry and financial experience," said Benjamin A. Hardesty, Lead Independent Director of Antero Resources. "Mike was the obvious choice to succeed Paul, and I can think of nobody better to lead Antero Resources into its next phase. I have seen Mike and Paul work together seamlessly for years making operational and financial decisions for the company, and with Mike taking over as CEO and President, I believe Antero Resources is well-positioned to capitalize on the highly-visible natural gas demand growth from LNG and data centers."

As part of the transition, the companies are separating the roles of chairman and CEO. Hardesty was appointed chairman of Antero Resources' board, while David Keyte, currently lead independent director of Antero Midstream, will be chairman there.

Current Financial Position

Antero continues to strengthen its balance sheet, reducing net debt to $1.1 billion as of June 30, 2025, down from $1.5 billion at the end of 2024. This represents a continuation of the company's long-term debt reduction strategy, with approximately $2.7 billion in debt reduction since 2019.

Antero Resources reported strong Q2 2025 financial results, with net income of $157 million and Free Cash Flow of $262 million. The company achieved net production of 3.4 Bcfe/d and realized a premium price of $0.41 per Mcfe above NYMEX.

Antero reduced its debt by $187 million during Q2 2025, bringing total debt to $1.1 billion. Year-to-date debt reduction was approximately $400 million or 30% of total debt. Antero increased its 2025 production guidance to 3.4-3.45 Bcfe/d while reducing drilling and completion capital guidance to $650-675 million due to efficiency gains.

The capital efficiency improvements have been remarkable. Maintenance production increased by 5% from 2023 guidance to 2025 guidance, while maintenance capital decreased by 26% over the same period. This efficiency translates to a capital efficiency metric of $0.53, substantially better than the peer average of $0.73.

From April 1 to July 30, 2025, Antero purchased 3.6 million shares at an average price of $34.49, totaling $126 million in share repurchases.

The company's environmental performance has also improved substantially. Antero reduced absolute methane emissions by 77% and methane intensity by 79% since 2019, while reducing overall Scope 1 emissions by 63%.

XI. Playbook: Business & Investing Lessons

The Antero story offers several enduring lessons for operators and investors in commodity businesses:

Serial Entrepreneurship in Commodities

The build-to-sell versus build-to-keep decision reveals a fundamental tension in resource development. Rady and Warren mastered the build-to-sell model—identifying undervalued plays, proving up the resource, and exiting to deep-pocketed acquirers. But they recognized that Appalachia represented something different: an opportunity so large and so strategic that selling would leave enormous value on the table. The decision to break their own pattern and go public with Antero required intellectual flexibility and long-term conviction.

Management Alignment

The founder-led model and long-tenured team created remarkable strategic consistency. Rady and Warren were partners across a number of successful plays for more than 20 years. This continuity allowed for patient capital allocation decisions that might be difficult for management teams facing shorter-term performance pressures. The transition to Kennedy, who has worked at Antero since 2013 and alongside Rady for years, suggests institutional knowledge will be preserved.

Basin Selection as Competitive Advantage

How contrarian bets on geology create value is perhaps the central lesson. Entering the Marcellus in September 2008—during the financial crisis—required conviction in geological analysis when market conditions screamed caution. The subsequent focus on the liquids-rich fairway within the Marcellus, rather than dry gas areas, reflected geological insight that differentiated returns.

Vertical Integration

When to own infrastructure versus outsource remains one of the most important capital allocation decisions for E&P companies. Antero's creation of Antero Midstream captured value that would otherwise flow to third parties, provided operational control over critical infrastructure, and created a currency for accessing capital markets. The integration proved particularly valuable during the commodity collapse, when third-party midstream providers might have prioritized other customers.

Capital Discipline

Surviving commodity cycles through cost management separates winners from losers in the energy business. Antero's willingness to sell non-core assets, reduce drilling activity, and repurchase debt at discounts demonstrated discipline that many E&P management teams struggle to maintain. The $2.7 billion of debt reduction since 2019 transformed the company's risk profile.

Strategic Positioning

Securing premium pricing through transportation assets represents a form of competitive advantage that's difficult for competitors to replicate. Years before LNG export demand materialized, Antero was assembling firm transportation capacity to the Gulf Coast. This long-term thinking created optionality that now defines the bull case for the stock.

Patience and Optionality

Building 20+ years of drilling inventory creates flexibility that short-cycle operators lack. Antero can accelerate drilling when prices are attractive and slow activity when economics deteriorate, without worrying about acreage expirations or infrastructure commitments. The company's dry gas inventory, largely undeveloped to date, provides additional optionality should regional power demand from data centers materialize.

XII. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's 5 Forces

1. Threat of New Entrants: LOW-MEDIUM

The barriers to replicating Antero's position are substantial. As of December 31, 2024, the company had approximately 521,000 net acres in the Appalachian Basin; and approximately 170,000 net acres in the Upper Devonian Shale. Its gathering and compression systems also comprise 708 miles of gas gathering pipelines in the Appalachian Basin.

Core Marcellus and Utica acreage was assembled over a decade when land costs were lower and lease competition less intense. New entrants would face significantly higher acquisition costs for comparable positions. The capital intensity of shale development ($650-700M annual drilling budgets), regulatory complexity and permitting challenges, and integrated midstream infrastructure requirements create meaningful barriers.

2. Bargaining Power of Suppliers: MEDIUM

Oilfield services providers have some leverage during boom cycles when drilling activity outpaces equipment and crew availability. However, Antero's scale and operational efficiency reduce dependence on any single supplier. The company's well cost reductions—from $970 per lateral foot in 2019 to below $700 currently—demonstrate ability to extract efficiencies from the supply chain.

3. Bargaining Power of Buyers: MEDIUM-HIGH

Natural gas is a commodity with transparent pricing at liquid trading hubs. Producers have limited ability to differentiate their molecules. However, Antero offers the purest exposure to rising Nymex natural gas prices with an unhedged production profile and an extensive firm transportation position. This firm transportation delivers 100% of natural gas out of basin, including 75% delivered to the LNG fairway tied directly to Nymex Henry Hub pricing. This transportation portfolio provides some insulation from the basis discounts that plague Appalachian peers.

LNG export facilities becoming key buyers adds buyer diversification. Multiple export terminals competing for supply creates optionality for producers with Gulf Coast access.

4. Threat of Substitutes: MEDIUM-HIGH

Renewable energy competition for power generation represents a long-term threat to natural gas demand. Electric vehicles could eventually reduce oil-linked NGL demand. However, natural gas maintains advantages as a transition fuel due to its lower emissions profile relative to coal and its ability to provide reliable baseload power when renewables are intermittent.

The AI data center demand narrative suggests sustained near-term demand growth that could extend natural gas's runway even as renewable capacity expands.

5. Competitive Rivalry: HIGH

Multiple well-capitalized E&P players compete in Appalachia, including EQT (the basin's largest producer), Range Resources, Expand Energy, and Coterra. Differentiation comes through operational efficiency, capital discipline, and market access rather than product differentiation.

Antero differentiates through its capital efficiency metric of $0.53, substantially better than the peer average of $0.73. This cost advantage creates sustainable profitability advantages across commodity cycles.

Hamilton's 7 Powers Framework

1. Scale Economies: PRESENT

Antero's 521,000 net acres provides operational scale advantages. The integrated relationship with Antero Midstream creates gathering and processing efficiencies unavailable to smaller operators. Fixed costs like corporate overhead are spread across substantial production volumes, lowering unit costs.

2. Network Effects: LIMITED

Traditional network effects don't apply to E&P businesses in the way they do to technology platforms. However, the integrated midstream infrastructure creates some network-like benefits: each new well connected to Antero Midstream's gathering system increases that system's utilization and economics.

3. Counter-Positioning: PRESENT

Antero's transportation portfolio delivers 100% of natural gas out of the Appalachian Basin—75% destined for the LNG fairway and into Tier 1 Gulf Coast pricing points. Most Appalachian peers (averaging only 13-31% Henry Hub-linked) would face significant cost and lead time to replicate this positioning. The years of advance commitment required to secure firm transportation capacity creates a durable positioning advantage.

4. Switching Costs: MODERATE

Long-term midstream contracts with Antero Midstream create stickiness. Firm transportation commitments lock in market access for years. However, the underlying commodity is fungible, and buyers face minimal switching costs in purchasing gas from different suppliers.

5. Branding: LIMITED

Commodity businesses offer limited brand power. However, Antero's reputation with capital providers—demonstrated through the Warburg Pincus partnership and successful capital markets transactions—has value in accessing financing on favorable terms.

6. Cornered Resource: STRONG

The company holds more than 20 years of premium drilling inventory to meet demand. As of December 31, 2024, the company's estimated proved reserves totaled 17.9 trillion cubic feet equivalent (Tcfe), consisting of 59% natural gas, 40% natural gas liquids (NGLs), and 1% oil.

This reserve base, combined with the core positioning within the Marcellus and Utica fairways, represents a cornered resource that would be expensive and time-consuming for competitors to replicate. The liquids-rich nature of the acreage—40% NGLs—provides exposure to higher-value products.

7. Process Power: PRESENT

Antero's operational improvements—driving well costs down 35% since 2019, achieving completion speeds that exceed peer records—reflect accumulated learning and process optimization that creates sustainable cost advantages. Antero showcased significant improvements in drilling and completion efficiencies, achieving a 15% increase from 2023 to Q1 2025. The company completed 2,452 feet per day in the first quarter, substantially outperforming the peer quarterly record of 1,600 feet per day.

Key Metrics for Investors to Track

For investors following Antero Resources, three KPIs provide the clearest window into the company's ongoing performance:

1. Maintenance Capital per Mcfe

This metric captures how much capital Antero must invest simply to maintain current production levels. The company's current $0.53/Mcfe is significantly below the peer average of $0.73/Mcfe. Continued improvement here directly translates to higher free cash flow for any given commodity price environment. Deterioration would signal operational issues or inventory quality concerns.

2. Price Realization Premium/Discount to NYMEX

Antero's firm transportation portfolio is designed to capture Gulf Coast pricing rather than discounted Appalachian hub prices. The company's Q2 2025 realization of $0.41/Mcfe premium to NYMEX validates this strategy. Tracking this differential over time reveals whether the transportation advantage is being maintained or eroding. Any sustained discount to NYMEX would indicate structural issues.

3. Free Cash Flow Yield (Unhedged Breakeven)

Given Antero's largely unhedged posture, understanding the gas price required to achieve free cash flow breakeven is critical. The company's current breakeven around $2.29/Mcf is among the lowest in the industry. This provides substantial downside protection while preserving full upside exposure to rising prices.

Myth vs. Reality: Fact-Checking Consensus Narratives

Myth: Antero is just another over-leveraged E&P

Reality: This narrative reflected 2019-2020 reality but is now outdated. Net debt has been reduced to $1.1 billion as of June 30, 2025, down from $1.5 billion at the end of 2024, representing approximately $2.7 billion in debt reduction since 2019. With leverage at 0.8x EBITDAX, Antero's balance sheet now ranks among the strongest in the sector.

Myth: LNG export exposure is just marketing hype

Reality: The transportation portfolio is real and verifiable. 75% of production is delivered to the LNG fairway tied directly to Nymex Henry Hub pricing—confirmed through quarterly pricing disclosures. The $0.41/Mcfe premium to NYMEX in Q2 2025 demonstrates the value is flowing to realized results, not just investor presentations.

Myth: The leadership transition signals strategic uncertainty

Reality: Kennedy's promotion was well-telegraphed and reflects continuity rather than change. He has worked at Antero since 2013, served as CFO since 2021, and worked side-by-side with Paul Rady for many years. The separation of Chairman and CEO roles aligns with governance best practices.

Material Risks and Accounting Considerations

Regulatory Risk: The Biden administration's pause on LNG export permits created uncertainty, though most near-term projects proceed under existing authorizations. Changes in federal energy policy could impact the long-term LNG demand thesis.

Commodity Price Volatility: Antero's largely unhedged posture amplifies both upside and downside exposure to natural gas prices. A sustained period of sub-$2.50 gas would pressure cash flows despite low breakevens.

Midstream Accounting: Antero's 29% ownership in Antero Midstream is accounted for under the equity method, meaning only Antero's proportionate share of midstream income flows through the income statement. The intercompany arrangements between upstream and midstream entities require scrutiny to ensure arm's-length pricing.

Reserve Estimation: Proved reserves of 17.9 Tcfe involve significant judgment regarding future commodity prices, development costs, and recovery factors. Annual reserve audits provide external validation, but estimates can change materially with commodity price movements.

Environmental Liabilities: While Antero has made substantial emissions reductions, the upstream E&P business carries inherent environmental risks. Any major incident could result in regulatory penalties, cleanup costs, and reputational damage.

The Antero Resources story is ultimately about the power of patience, execution, and strategic positioning in a commodity business. Paul Rady and Glen Warren spent decades learning to read geology, operate drilling rigs, and navigate capital markets. They built and sold multiple companies, honing a playbook that created billions of dollars in value.

When they encountered Appalachia—a formation so prolific and strategically important that it demanded a different approach—they adapted. Instead of building to sell, they built to keep. Instead of diversifying, they concentrated. Instead of maximizing near-term production growth, they prioritized long-term positioning through transportation investments that wouldn't pay off for years.

As Michael Kennedy takes the helm in August 2025, Antero Resources stands as the most capital-efficient developer in the Appalachian Basin, with peer-leading transportation access to premium markets and over two decades of drilling inventory. The natural gas demand growth from LNG exports and AI-driven power consumption represents a structural tailwind that could define the next chapter of the company's story.

For investors, the key questions center on commodity price assumptions, the pace of LNG capacity additions, and whether the operational execution that defined the Rady era will continue under new leadership. The company's track record suggests the answer is yes—but in commodity businesses, nothing is certain except that cycles will turn and discipline will be tested.

What remains constant is the strategic asset base that Rady, Warren, and their team assembled over two decades: core acreage in America's most prolific gas basin, integrated midstream infrastructure, and transportation capacity to the markets that matter most. In an industry where assets frequently outlive the managements that develop them, Antero has positioned itself to thrive regardless of who occupies the corner office.

Now I have enough information to continue the article. Let me pick up where it left off and complete the remaining sections.

Recent Developments: Q3 2025 and Beyond

On October 29, 2025, Antero Resources announced its third quarter 2025 financial and operating results. CEO Michael Kennedy commented, "Antero's third quarter results yet again raised the bar for operational performance, as we set numerous drilling and completion records during the period."

The company realized a pre-hedge natural gas equivalent price of $3.59 per Mcfe, representing a $0.52 per Mcfe premium to NYMEX. Net income reached $76 million, with Adjusted EBITDAX of $318 million and Free Cash Flow of $91 million.

Operational efficiencies reached new highs, with the company setting records for the longest lateral drilled—over 22,000 feet—and the highest quarterly completion rate at 14.5 stages per day.

Kennedy noted, "We completed several bolt-on acquisitions located in our core Marcellus acreage position in West Virginia. The transactions increase Antero's production and inventory and enhance our ability to capitalize on the significant demand increases expected for natural gas."

CFO Brendan Krueger added, "Our best-in-class low maintenance capital requirements has led to substantial Free Cash Flow in 2025. During the year, we used this Free Cash Flow to finance several bolt-on acquisitions, pay down $182 million of debt, and purchase $163 million of stock."

Perhaps most significantly, Kennedy announced, "We are excited to return to our dry gas acreage, where we have not drilled in over a decade. We spud a pad during the fourth quarter of 2025, which highlights our ability to quickly increase dry gas production to supply power for datacenters, other power generation projects or to sell into the local market if local basis were to tighten meaningfully."

The company now anticipates Q4 2025 production to increase to the range of 3.5-3.525 Bcfe/d, with full-year 2025 production expected at the high end of the 3.4-3.45 Bcfe/d range.

The acquisitions secured 79 high-quality drilling locations at an average cost of $900,000 per location, which management projects will yield a free cash flow return exceeding 20% in 2026.

XIII. The Structural Demand Thesis: LNG and Data Centers

The investment case for Antero Resources increasingly rests on two structural demand drivers that extend far beyond traditional seasonal heating patterns: the buildout of U.S. LNG export capacity and the explosive growth in power demand from artificial intelligence data centers.

The LNG Export Wave

Between 2025 and 2030, more than 300 billion cubic meters per year of new LNG export capacity is expected to come online from projects that have already reached final investment decision and are under construction, marking the largest wave of capacity additions to date.

The United States, already the world's largest LNG exporter with 15.4 Bcf/d of capacity, continues to expand rapidly. LNG exporters in the U.S. plan to more than double the country's liquefaction capacity by adding an estimated 13.9 Bcf/d between 2025 and 2029.

After being largely flat in 2024, U.S. LNG exports surged by 21% in the first half of 2025, accounting for the vast majority of incremental global volumes.

With 96 billion cubic meters per year of new liquefaction capacity sanctioned between January and October, 2025 is already the second-highest year for LNG final investment decisions on record. The United States is projected to account for approximately 75% of LNG supply final investment decisions for 2025 and 2026, and would more than double its market share by 2030, growing from 90 million metric tons in 2024 to 185 million metric tons by 2030.

U.S. natural gas prices tend to be lower than global prices, making U.S. LNG attractive on the international market. Favorable economics for U.S.-supplied natural gas leads to LNG exports growing through 2040 in most EIA cases.

This export growth creates sustained demand for domestic natural gas that fundamentally alters the supply-demand dynamics that have historically kept U.S. prices depressed relative to international benchmarks. For Antero, with its firm transportation capacity to Gulf Coast LNG corridors, this structural shift translates directly into realized pricing advantages.

The Data Center Power Surge

After a couple of decades during which U.S. power demand remained relatively stagnant, domestic electricity consumption is expected to surge by 25% from 2023 to 2035 and roughly 60% from 2023 to 2050, driven largely by AI and data centers, according to the International Energy Agency.

The Appalachian Basin, the largest natural gas production region in the United States, extends from central Alabama to the Adirondack Mountains in New York. It is known for its rich natural resources, including oil and gas, particularly from formations like the Marcellus and Utica shales.

The growing data center hub in Northern Appalachia sits on top of the Marcellus Shale, a major natural gas producing region in the world. As Penn State's Seth Blumsack noted, "we are basically sitting on just a gold mine of...pretty easily accessible, fairly low-cost fuel for power plants."

Range Resources, another major Appalachian producer, is forecasting combined demand and takeaway capacity to reach 38-40 Bcf/d by 2028 compared with about 34 Bcf/d in 2023. Coal-fired power plant retirements could drive 0.9-1.8 Bcf/d of power sector gas demand growth in Appalachia by 2028, while data center projects could add about 0.7 Bcf/d.

EQT demonstrated the growth opportunities by finalizing two supply agreements in July for more than 1 Bcf/d from its Marcellus output to serve two restarted Pennsylvania power plants and co-located data centers.

As Tradition Energy's Gary Cunningham explained, energy demand from data centers, particularly in Appalachia, provides tremendous benefits to producers "looking for ways to increase output without overloading regional pipelines and causing stronger negative basis."

The Appalachian Basin, powered by the Marcellus and Utica shales, has become one of the nation's largest natural gas-producing regions. The area's industrial heritage, abundant brownfield sites, and extensive pipeline corridors make it a natural fit for data center development.

For Antero, the data center thesis provides a dual benefit: incremental in-basin demand that improves regional pricing dynamics, plus the strategic value of holding dry gas inventory that can be quickly activated to serve power generation needs. The company's Q4 2025 decision to spud a dry gas pad for the first time in over a decade demonstrates this optionality in action.

XIV. Wall Street Perspective

One equities research analyst has rated the stock with a Strong Buy rating, eleven have assigned a Buy rating and six have given a Hold rating to the company's stock. Based on data from MarketBeat, Antero Resources presently has a consensus rating of "Moderate Buy" and an average target price of $44.00.

Citigroup raised shares of Antero Resources from a "neutral" rating to a "buy" rating and boosted their target price for the company from $37.00 to $39.00 in September 2025. Wells Fargo raised Antero Resources from an "equal weight" to an "overweight" rating and set a $39.00 price target in early November 2025.

CFO Brendan Krueger demonstrated insider confidence by purchasing 5,000 shares of Antero Resources stock on November 7, 2025, at an average price of $33.35 per share. Following the completion of the acquisition, the insider owned 295,917 shares in the company.

Institutional ownership remains robust, with 83.04% of the stock currently owned by institutional investors and hedge funds.

Many of the nation's top gas producers, including Expand Energy, EQT, Range Resources, and Antero Resources, all have major Appalachian footprints and market cap values that have spiked by 25% to 75% over the past 12 months.

XV. Conclusion: The Value of Patience in Commodity Markets

The Antero Resources story defies the conventional narrative of the oil and gas industry as a sector dominated by short-term thinking, boom-and-bust cycles, and management teams more interested in empire-building than shareholder returns.

Paul Rady and Glen Warren spent two decades developing a playbook that combined geological insight with operational excellence and capital discipline. They built and sold multiple companies, proving their ability to create value in unconventional resource plays. When they encountered Appalachia—a basin so prolific that it demanded a different approach—they adapted their strategy without abandoning their principles.

The result is a company uniquely positioned for the structural shifts reshaping global energy markets. Antero's firm transportation portfolio, assembled over years of patient investment, now provides access to the premium LNG export corridor along the Gulf Coast. The company's liquids-rich acreage generates higher realized prices than dry gas competitors. And the 20+ years of drilling inventory provides optionality to respond to emerging demand sources like AI-powered data centers.

The Q3 2025 acquisitions, which secured 79 high-quality drilling locations at an average cost of $900,000 per location with projected free cash flow returns exceeding 20% in 2026, demonstrate that the acquisition discipline and operational focus that characterized the company's early years remain intact under new leadership.

As CFO Brendan Krueger noted, "Looking ahead, we will continue to focus on opportunistically adding to our position in the core of the West Virginia Marcellus, maintaining low absolute debt levels and repurchasing our stock."

The transition from Paul Rady to Michael Kennedy marks the end of one chapter and the beginning of another. Kennedy inherits a company with a fortress balance sheet, premium market positioning, and structural tailwinds from LNG exports and data center power demand. The question for the next decade is whether the operational and strategic excellence that defined the founder era can be sustained and extended.

For students of business history, Antero offers lessons that transcend the energy sector: the value of management continuity and institutional knowledge; the importance of concentrating resources on highest-return opportunities rather than diversifying into mediocrity; the discipline required to exit good assets in pursuit of great ones; and the strategic patience to build infrastructure advantages that take years to materialize but create durable competitive moats.

In an industry where many companies chase the latest hot play and exhaust themselves on the commodity price treadmill, Antero has demonstrated that thoughtful positioning and relentless operational improvement can generate returns through the cycle. The founders built something designed to endure—and the structural demand growth from LNG exports and AI-driven power consumption suggests the next chapter may be even more compelling than the one that came before.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube