Bank of Communications: China's First Modern Commercial Bank & The State Banking Puzzle

Introduction: The Bank That Bridges Empires

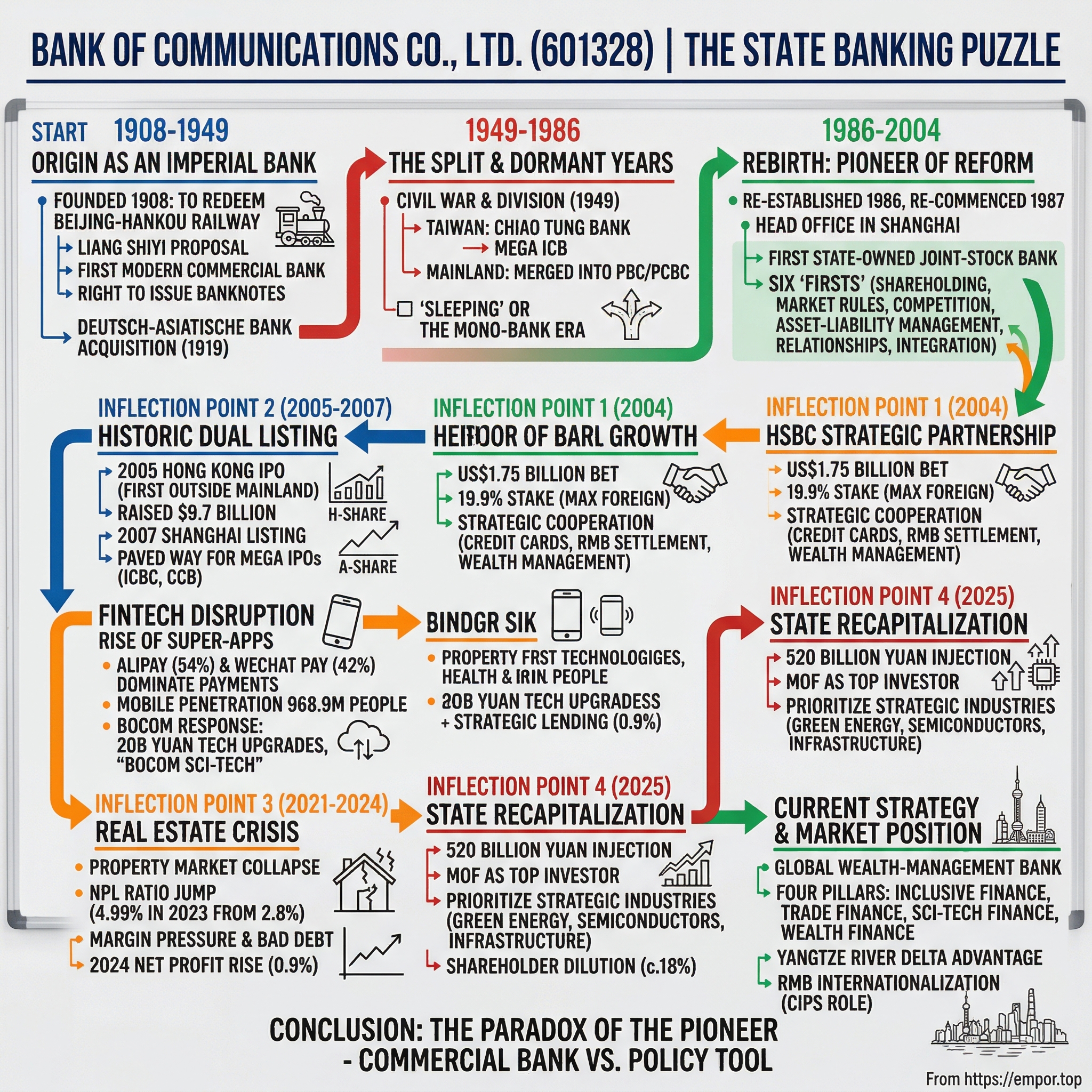

In 1907, a bureaucrat named Liang Shiyi stood before Qing Dynasty officials with an audacious proposal: create a new bank to buy back a Belgian-owned railway stretching from Beijing to Hankou. The plan was equal parts financial engineering and nationalist aspiration—an attempt to wrest control of China's critical infrastructure from foreign hands. In 1907, Liang Shiyi proposed the formation of a Bank of Communications to redeem the Beijing–Hankou Railway from its Belgian owners and place the railway under Chinese control. The Bank of Communications was formed in 1908 and provided more than half of the financing needed to buy the railway.

The name itself tells the story. The bank's name uses the word "communications" to refer to the linking of two points by a means of transportation—railways, shipping lines, the arteries of a modernizing nation. This wasn't meant to be a typical bank. It was conceived as an instrument of national industrial development, a vehicle for Chinese sovereignty in an age of imperial predation.

What followed over the next 117 years represents one of the most extraordinary institutional odysseys in global finance. The Bank of Communications—or BOCOM, as it's known today—has experienced civil war, communist revolution, four decades of dormancy, resurrection as China's reform laboratory, a transformational partnership with HSBC, a historic dual listing, the fintech revolution, a property crisis, and now, in 2025, a massive state recapitalization that raises fundamental questions about the future of Chinese banking.

Bank of Communications, or Bocom, is the only nationwide state-owned bank with its headquarters in Shanghai. As one of China's four oldest banks, Bocom became China's first state-owned shareholding commercial bank in 1987. By the end of FY24, BOCOM commanded approximately RMB 14.9 trillion in total assets—making it one of the world's largest banks and a Global Systemically Important Bank (G-SIB). Yet for all its heft, BOCOM occupies a peculiar position: too small to be a true "Big Four" giant, too state-controlled to be nimble, too Western-partnered to be purely Chinese, and too Chinese to be comfortable for foreign investors.

The central question animating this analysis: How did a 117-year-old bank that literally printed money in Imperial China become both a pioneer of Chinese banking reform AND a symbol of state-controlled finance's inherent tensions? The answer reveals as much about China's modern economic evolution as it does about BOCOM itself.

Origins: The Imperial Bank That Printed Money (1908-1949)

Birth From National Crisis

The late Qing Dynasty was an era of humiliation and awakening. Foreign powers had carved up China's most valuable assets—railways, ports, customs—through unequal treaties and concessions. The Beijing-Hankou Railway, completed in 1906 by Belgian investors backed by French capital, represented exactly the kind of foreign control that Chinese reformers found intolerable.

The Beijing–Hankou railway was completed in 1906. In the meantime, the Belgians had purchased a controlling stake in the American China Development company that held the concession for the Guangdong–Hankou railway. Most of the shares in the Belgian company were owned by Édouard Empain, and this move threatened to place the entire route between Beijing and Guangzhou under foreign control. Opposition to this state of affairs was especially strong in Hunan.

Liang Shiyi, a brilliant bureaucrat who would become one of the most influential figures in early Republican China, saw an opportunity. Rather than simply protest foreign ownership, he proposed a financial solution: create a bank specifically designed to mobilize Chinese capital for national infrastructure redemption.

The Bank of Communication was founded in 1908 and emerged as one of the first few major national and note-issuing banks in the early days of the Republic of China. It was chartered as "the Bank for developing the country's industries". This wasn't merely marketing language—the bank's founding charter explicitly tied its mission to industrial development, making it arguably China's first industrial development bank.

The Bank of Communications was formed in 1908 and provided more than half of the financing needed to buy the railway, the remaining coming from the Imperial Bank of China and the Ministry of Finance. The railway was placed under Chinese control on January 1, 1909, and the successful redemption enhanced the prestige of Liang's Communications Clique.

The Note-Issuing Bank

What distinguished BOCOM from ordinary commercial banks was its extraordinary privilege: the right to issue banknotes. It was originally established in 1908 and was one of a handful of domestic Chinese banks that issued banknotes in modern history. In an era before central banking monopolies were firmly established, this meant BOCOM functioned partly as a quasi-governmental monetary authority.

The bank's reach expanded rapidly through the turbulent years of dynastic collapse and Republican emergence. In order to expand the business into the overseas arena, the Bank opened its first Hong Kong Branch on 27 November 1934. This Hong Kong presence would prove crucial—it was the thread that kept the BOCOM name alive through decades of political upheaval.

By the 1920s and 1930s, BOCOM had grown into one of China's most important financial institutions, financing not just railways but shipping, manufacturing, and trade. It opened a Shanghai branch and expanded throughout the country's major commercial centers. The bank took a notable acquisition when In 1919, the Bank of Communications took over the holdings of the Deutsch-Asiatische Bank, including its properties in Shanghai—a symbolic turnabout given the bank's origins in reclaiming Chinese assets from foreign control.

But this golden era was about to end catastrophically.

War, Collapse, and Division

In late July 1942, it lost its note-issuance privilege simultaneously as the Bank of China and the Farmers Bank of China, whereas the Central Bank of China was granted the issuance monopoly in the territories still ruled by the Nationalist government. Japanese occupation, civil war, and finally communist victory in 1949 tore apart the institutional fabric BOCOM had woven over four decades.

For investors thinking about BOCOM today, this early history matters for understanding the bank's DNA: it was created as an instrument of national policy, not purely commercial enterprise. That founding mission—finance as a tool of national development—has never fully disappeared, even as the bank has adopted the outward forms of commercial banking.

The Split & The Dormant Years (1949-1986)

A Bank Torn in Two

The Chinese Civil War didn't just divide a nation—it cleaved institutions down the middle. After the Chinese Civil War ended in 1949, the Bank of Communications, like the Bank of China, was effectively split into two operations, with part of it relocating to Taiwan with the Kuomintang government. In Taiwan, the bank was also known as the Bank of Communications or Chiao Tung Bank.

This created two parallel institutional lineages. It eventually merged with the International Commercial Bank of China (中國國際商業銀行), the renamed Bank of China in Taiwan after its 1971 privatization, to become the Mega International Commercial Bank. The Taiwan branch evolved, privatized, merged, and ultimately became part of a different financial system entirely.

On the mainland, the story was dramatically different. The new People's Republic had little use for commercial banking as the concept was understood elsewhere. In the early years of the People's Republic, the bank's operations in the mainland were merged into the PBC and PCBC, while the Hong Kong branch continued to exist under the same name and was integrated in the so-called Bank of China Group.

The Mono-Bank Era

Under the communist system, the People's Bank of China became a "mono-bank" performing virtually all banking functions—commercial lending, monetary policy, and payment settlement—under direct state control. Independent commercial banks had no role to play. BOCOM as a distinct mainland institution essentially ceased to exist for over three decades.

This dormancy would have lasting implications. When China's reformers began reopening banking in the 1980s, they faced a landscape without modern commercial banking expertise, governance frameworks, or risk management culture. The skills and institutional memory accumulated during BOCOM's pre-1949 era had been lost. Everything would need to be rebuilt from scratch.

Yet one ember remained: the Hong Kong branch, which continued operating throughout this period under the Bank of China Group umbrella. This continuity of the BOCOM brand, however attenuated, provided a foundation for what came next.

Rebirth: The Pioneer of Chinese Banking Reform (1986-2004)

The 1987 Resurrection

By the mid-1980s, Deng Xiaoping's economic reforms were gathering momentum. The mono-bank system was clearly inadequate for a modernizing economy that needed commercial credit allocation, not just administrative fiat. The question was: how to build commercial banking from nothing?

The State Council decided to re-establish the Bank of Communication as a mainland commercial bank in 1986. The Bank was then restructured and re-commenced operations on 1 April 1987. Since then, its Head Office has been located in Shanghai.

This wasn't merely a rebranding exercise. The reconstituted BOCOM was designed as a laboratory for Chinese banking reform—a place to test commercial structures before rolling them out to the massive state banks. BoCom reopened after reorganization on April 1, 1987. It is the first nationwide state-owned joint-stock commercial bank in China, with Head Office located in Shanghai.

The Six "Firsts"

BOCOM's reformist credentials are real and documented. According to the bank's own history, BOCOM has achieved six "firsts" in China's banking reform and development: the first to implement shareholding system for its capital and mode of ownership form; the first to command an organizational structure based on market rules and cost/return rules; the first to introduce competition into the banking industry in China; the first to introduce assets/liability ratio management and apply it for regulating business operations and risk; the first to build new bank/enterprise relationships based on two-way selection; and the first commercial bank to integrate banking, insurance and securities businesses.

These firsts represented genuinely radical departures from communist-era banking practice:

Shareholding system: Instead of 100% state ownership, BOCOM was structured with multiple shareholders—a foundational shift toward corporate governance.

Market-based organization: The mono-bank had operated by administrative command. BOCOM organized itself around cost/return principles—revolutionary in a system where profit had been ideologically suspect.

Competition: BOCOM's mere existence meant Chinese enterprises could choose between lenders, a concept alien to centralized planning.

Asset-liability management: Rather than simply executing credit quotas, BOCOM managed its balance sheet according to prudential ratios—laying groundwork for future Basel compliance.

BOCOM's experience in reform and development paves the way for the development of shareholding commercial banks in China and exemplifies the banking reform of China.

Rapid Expansion

Through the 1990s, BOCOM grew aggressively, expanding its branch network and building out capabilities in corporate and trade finance. Headquartered in Shanghai—China's commercial capital—the bank was well-positioned to serve the explosion of private enterprise and foreign trade that characterized the reform era.

But this period was not without challenges. Non-performing loans (NPL) increased significantly: by the late 1990s the large state-owned banks' aggregate non-performing loan (NPL) ratio exceeded 30 per cent. While BOCOM was smaller than the "Big Four" state banks, it was not immune to the era's bad lending. Despite efforts to reform the SOEs through privatisation initiatives and to improve the asset-liability management of the banks, by 1997–1998 the largest four banks' NPLs had risen to between one-quarter and one-third of total assets. Although China's strong capital controls allowed it to weather the 1997–1998 Asian financial crisis, the concurrent NPL crisis heightened policymakers' concerns about domestic financial fragility.

The Late 1990s Banking Crisis

China's response to this crisis established patterns still visible today. The last time the Ministry of Finance undertook a large-scale capital injection was in the late 1990s when the entire banking system was struggling under high levels of bad debt. Back then, the MoF issued 270 billion renminbi (RMB) in special government bonds.

The government responded swiftly, recapitalising the state-owned banks, introducing debt-for-equity swaps, and creating four asset management companies to purchase banks' NPLs at face value and begin the process of their disposal. This cleanup set the stage for the next phase of reform: bringing in foreign expertise and accessing international capital markets.

For investors, BOCOM's reform-era history establishes two key characteristics. First, the bank genuinely does have reformist DNA—it was created to experiment with new structures. Second, that experimentation happens within bounds set by the state. BOCOM pioneered commercial banking within the Chinese system, not as an alternative to it.

Inflection Point #1: The HSBC Strategic Partnership (2004-2005)

Context: WTO and the Opening

China's 2001 accession to the World Trade Organization committed the country to opening its financial sector to foreign competition. When China joined the World Trade Organization in 2001, China agreed to a five-year timetable of changes aimed at opening up its banking system to foreign competition; by 2006, locally incorporated foreign-owned banks were allowed to apply for a licence to offer unrestricted local currency services to Chinese individuals.

This created both opportunity and urgency. Chinese banks needed to modernize quickly before facing full foreign competition. Foreign banks saw a once-in-a-generation chance to enter the world's largest untapped market.

The $1.75 Billion Bet

On 6 August 2004, HSBC announced that it would pay US$1.75 billion for a 19.9% stake in Shanghai-based Bank of Communications. At the time of the announcement, Bank of Communications was China's fifth-largest bank and the investment by HSBC was eight times bigger than any previous foreign investment in a Chinese bank.

When HSBC bought its 19% equity stake in Bank of Communications for $1.7 billion in 2004, it seemed like a smart way to bet on China's fast growing economy without the ethical minefield of direct lending within an authoritarian state. BoCom was China's fifth-largest lender, but only had $112 billion of assets, compared with $1.3 trillion at HSBC itself.

The 19.9% figure wasn't accidental—it represented the maximum stake foreign investors could hold in a Chinese bank under then-prevailing regulations. HSBC was pushing to the limit of what was legally permissible.

Strategic Cooperation Agreement

Beyond the capital, the partnership promised operational collaboration. In June 2004, with the banking reform in China well under way, the State Council approved BOCOM's general plan on deepening the reform of its shareholding structure. Through the reform, BOCOM completed financial reorganization, successfully introduced mainland and overseas strategic investors like HSBC, the national Social Security Fund and China SAFE Investment Ltd.

HSBC co-operates with Bank of Communications on over 60 initiatives, including joint credit card activities in China, renminbi (RMB) trade settlement and payments and cash management services. The joint credit card activities in China were launched in October 2004, with over 13 million cards now in issue.

What HSBC Got (and Didn't Get)

HSBC's operations in China include its own banking operations, its stake in BoCom, and an 8% stake in the Bank of Shanghai. HSBC also holds a 19.9% shares in Ping An Insurance through its wholly owned subsidiary HSBC Insurance Holdings.

The partnership created a template for subsequent foreign investments in Chinese banks, but it also highlighted the inherent limitations. HSBC gained exposure to Chinese growth, dividend income, and a partnership structure—but never management control. Strategic influence was constrained by political realities that no commercial agreement could override.

Today, China's economy is ten times bigger than it was in 2004, and BoCom's balance sheet is now $1.92 trillion, approaching two thirds of HSBC by size. Indeed, this rapid growth recently prompted the Financial Stability Board to classify BoCom as a G-SIB. Meanwhile, it pays an annual $730 million dividend to HSBC – which amounts to 12% of the global giant's profit before tax.

For investors evaluating BOCOM today, the HSBC relationship remains significant: it provides operational expertise, international credibility, and a consistent dividend stream to a major Western institution. But it also demonstrates the ceiling on foreign influence in China's state banking system.

Inflection Point #2: The Historic Dual Listing (2005-2007)

Hong Kong: The Groundbreaking IPO

On June 23, 2005, BOCOM was listed in Hong Kong, the first China based commercial bank of its kind to get listed outside of the Chinese mainland. On May 15, 2007, BOCOM was listed in Shanghai Stock Exchange.

In 2005, BoCom became publicly traded, listing its shares on the Hong Kong Stock Exchange, raising approximately $9.7 billion in its initial public offering (IPO). This IPO marked the largest ever for a Chinese bank at that time.

The Hong Kong listing was more than a capital-raising exercise. It forced BOCOM to meet international disclosure standards, adopt IFRS accounting, and subject itself to scrutiny from global investors and analysts. This disciplining effect was arguably as valuable as the capital raised.

Shanghai Listing

The subsequent Shanghai A-share listing gave domestic Chinese investors access to BOCOM stock for the first time and created what remains today: a dual-listed structure with H-shares trading in Hong Kong and A-shares in Shanghai. This structure provides liquidity in two major markets but also creates complexity around valuation differentials and currency exposure.

Pioneering Role

BOCOM's successful listings paved the way for the subsequent mega-IPOs of ICBC (2006) and others. All four banks underwent further recapitalisation and disposal of NPLs in the 2000s, and were subsequently listed on the Hong Kong and Shanghai stock exchanges. The four banks' initial public offerings (IPOs) raised a combined US$74 billion in return for around 15–25 per cent of these companies' equity.

By 2015, BOCOM's growth trajectory was impressive: By 2015, it reported total assets of approximately $1.82 trillion, making it the fifth-largest bank in China by total assets. The bank's net profit for the year was reported at $10.08 billion, reflecting its strong financial health and operational efficiency.

For investors, the dual listing creates both opportunity and complexity. H-shares typically trade at a discount to A-shares, reflecting differences in investor bases and currency considerations. The institutional quality associated with Hong Kong listing provides some comfort around governance, while the A-share listing ensures domestic policy support.

The Fintech Disruption & Digital Transformation Challenge

The Rise of the Super-Apps

No discussion of Chinese banking can ignore the elephant in the room: Alipay and WeChat Pay have fundamentally transformed how Chinese consumers interact with financial services.

Alipay dominates the market with a 54% share, making it the most widely used mobile payment platform. WeChat Pay follows closely with 42% market share, maintaining a strong position among Chinese consumers.

Together, Alipay and WeChat Pay control over 90% of China's mobile payment market, making them the backbone of the nation's cashless economy.

The implications for traditional banks are profound. By mid‑2024, nearly 92% of Chinese respondents reported using Alipay, and 85% used WeChat Pay. Mobile payment penetration reached 968.9 million people.

Competitive Threat Assessment

China's fintech revolution created new competitive dynamics. Digital financial platforms offer services at lower costs, put pressure on bank margins, and capture the customer relationship that banks traditionally owned. Young customers especially often interact with Alipay or WeChat Pay far more frequently than with their bank.

According to the iResearch Consulting Group report, in 2019, China's third-party mobile payment transactions reached 226.1 trillion Yuan representing year-on-year growth of 18.7%. China's third-party mobile payment market is highly concentrated: Alibaba's Alipay and Tencent's WeChat Pay are first-tier companies which accounted for nearly 93.8% of the market at the end of 2019.

BOCOM's Digital Response

BOCOM has responded with significant technology investments. The Bank of Communications has integrated digital transformation into its core operations, focusing on enhancing service efficiency and customer engagement through technology investments. In 2021, the bank committed over 20 billion yuan to technology upgrades specifically for advancing digital banking infrastructure and capabilities. This included the development of unified platforms for data processing and service delivery. A key initiative involved artificial intelligence integration, exemplified by a June 2021 partnership with 4Paradigm to construct a bank-level end-to-end AI platform.

BoCom is actively engaged in digital transformation, highlighted by its Fintech Development Plan for the 14th Five-Year Plan (2021-2025) and the Action Plan of BoCom for Digital Finance (2024-2025), focusing on digital infrastructure and innovative business drivers.

BOCOM presented a range of digital solutions, including the latest versions of its corporate online banking, mobile banking, open banking, and mini-program services. BOCOM's efforts have already shown measurable impact, with digital capital projects experiencing a 130 percent increase in transaction value in the first half of 2024.

The Structural Challenge

Despite these efforts, traditional banks face structural disadvantages against platform giants. Alipay and WeChat Pay benefit from network effects, platform economics, and customer data advantages that pure banking operations cannot easily replicate. BOCOM's digital initiatives are defensive—necessary for survival—but unlikely to fundamentally alter competitive dynamics.

For investors, the fintech challenge represents a persistent structural headwind. BOCOM must continuously invest in technology simply to maintain relevance, while the super-apps extract the most profitable customer touchpoints. The good news: regulatory crackdowns on fintech giants since 2020 have somewhat leveled the playing field.

Inflection Point #3: The Real Estate Crisis & NPL Exposure

Property Market Collapse

China's real estate sector, which accounts for roughly 25-30% of GDP including related activities, entered a prolonged downturn starting in 2021. Major developers defaulted, construction projects stalled, and home prices declined. This created direct exposure for all major Chinese banks through both developer loans and residential mortgages.

Bank of Communications Co. reported that its property bad loan ratio jumped to 4.99% at the end of 2023 from 2.8% a year earlier. While the balance of its overdue mortgages slipped, the special mention loans for the segment – a leading indicator of soured loans – jumped 23% to 9.88 billion yuan ($1.4 billion).

Real estate NPL ratios ranged from 4.99% at Bank of Communications to 5.64% at China Construction Bank. Overall nonperforming loan (NPL) ratios among the five G-SIBs ranged from 1.27% at Bank of China to 1.37% at China Construction Bank in 2023.

Headline NPLs vs. Reality

BOCOM's headline NPL ratio has remained relatively stable at around 1.31-1.33%—below the industry average. BOCOM's non-performing loan (NPL) ratio improved to 1.33% at the end of 2023 from 1.35% at the end of 2022, despite the real-estate NPL ratio rising to 4.99% from 2.80%. Its NPL ratio was compared favorably to the sector average of 1.59% but weaker than the state-owned peers' average of 1.25%.

However, skeptics note that Chinese banks have significant discretion in NPL classification and can use various techniques to manage reported numbers. The bank's domestic corporate loans overdue for more than 60 days have been included in non-performing loans, and the ratio of NPLs to loans overdue for more than 90 days has gradually increased from 87.5% in 2017 to 154.5% by the end of 2023. The bank's loan loss provisions have improved over the past three years, with a provision coverage ratio of 195.2% at the end of 2023.

2024 Results

The most recent results show incremental improvement but continued pressure. China's Bank of Communications Co Ltd reported a 0.9% rise in 2024 net profit, while warning of margin pressure and bad debt. The bank's net interest margin (NIM) - a key gauge of profitability - was 1.27% at the end of last year, slightly narrowed from 1.28% at the end of September. Its non-performing loan (NPL) ratio was 1.31% at the end of last year compared to 1.32% at end of September.

As of December last year, non-performing loans totaled around 111.7 billion yuan, up about 6 billion yuan year-on-year. The NPL ratio dropped by 0.02 percentage points to 1.31 percent.

Management has been forthright about ongoing challenges. Also of concern for the bank is the real estate business, which will continue to drag. Vice president Gu Bin said that there will be increasing bad debt among loans to property developers, while risks on retail loans have also risen. "In 2025, the external environment will be more complicated, challenging and uncertain," the bank said in the filing.

For investors, real estate exposure remains BOCOM's most significant risk factor. While reported metrics have held up better than many feared, the property market's extended weakness means the resolution process will take years, not quarters.

Inflection Point #4: The 2025 State Recapitalization

The Announcement

In March 2025, China unveiled a major recapitalization of its banking system—the first such large-scale injection in over two decades.

Bank of Communications Co., Bank of China Ltd., Postal Savings Bank of China Ltd. and China Construction Bank Corp. plan to raise up to a combined 520 billion yuan ($72 billion) through additional offerings of mainland-traded stocks, according to filings. The Ministry of Finance will be the top investor in all the proposed private placements, subscribing to 500 billion yuan in total.

China Construction Bank (CCB) plans to mop up as much as 105 billion yuan, Bank of China about 165 billion yuan, Bank of Communications (Bocom) at least 120 billion yuan and Postal Savings Bank of China about 130 billion yuan.

Why This Matters

The last time the Ministry of Finance undertook a large-scale capital injection was in the late 1990s when the entire banking system was struggling under high levels of bad debt. Back then, the MoF issued 270 billion renminbi (RMB) in special government bonds.

The timing and structure of this recapitalization reveals Beijing's priorities. The recapitalization is not an end in itself but a means to fund Beijing's broader economic agenda. The four banks are expected to prioritize lending to strategic emerging industries, including green energy, semiconductors, and infrastructure modernization.

The finance ministry will subscribe to the shares of all four banks, while China Tobacco will buy Bocom's shares, and China Mobile will acquire shares of Postal Savings Bank, with the proceeds to be used to replenish tier-one capital.

Dilution and Dividend Implications

The capital injection comes with shareholder dilution. Despite the c.18% share dilution after the MOF capital injection completes later in the year, we expect BOCOM to offer near 5% dividend yield at current valuation, which remains attractive to long-term funds such as China insurance companies.

The banks are issuing shares at between 66% and 76% of book value, the first time a major lender has sold below the regulatory minimum, according to analysts—suggesting the state has "limited confidence in the banks' share price performance". The risks are already peeking through: BoCom's ratio of non-performing personal loans rose by a third to 1.08% last year.

What It Signals

The state is injecting 520 billion yuan ($72 billion) of capital into four big lenders, hoping to spark consumer-driven economic growth. But doing Beijing's bidding is already starting to cause some stress.

For investors, the recapitalization is a double-edged sword. On one hand, it demonstrates explicit state support and improves capital ratios. On the other, it confirms that these banks face competing demands that commercial profitability alone cannot satisfy. BOCOM is being recapitalized partly to serve as a policy tool—not solely to maximize shareholder returns.

Current Strategy & Market Position

Strategic Pillars

Today, Bocom is amid a strategic transformation, building itself into a global wealth-management bank with wide-ranging financial operations, including insurance, brokerage, trust, and asset management.

The bank has articulated four major business characteristics it aims to develop: inclusive finance, trade finance, sci-tech finance, and wealth finance. The bank accelerated the digital transformation to build a New Digital BoCom with excellent experience, diverse ecology, intelligent control and efficient operation, and innovated the financial supply while highlighting four business features of inclusive finance, trade finance, sci-tech finance and wealth finance.

The Yangtze River Delta Advantage

BOCOM's Shanghai headquarters provides a crucial competitive position. At the end of June 2019, BOCOM's total financing in the Yangtze River Delta region amounted to nearly 2 trillion yuan, accounting for more than 30 percent of the total financing of the bank and its subsidiaries. About 37 percent of China's unicorn companies, tech startups valued at over $1 billion, are located in the Yangtze River Delta region, a major origin for technological innovation.

This regional concentration in China's most economically dynamic zone represents a genuine competitive advantage. The Yangtze River Delta—encompassing Shanghai, Jiangsu, Zhejiang, and Anhui—contributes nearly 20% of China's GDP and hosts the country's highest concentration of private enterprise and technology innovation.

Personal Lending Pivot

BOCOM is one of the few major banks where personal loan growth is outpacing corporate loans. Mortgage balance was largely flat y/y as of Dec 24 while personal business and personal consumption loans grew by 20%/90%.

This strategic shift toward retail lending reflects both opportunity (consumer credit underpenetration) and necessity (corporate lending margins under pressure). Personal loans typically carry higher yields, though they also bring higher credit risk—a tradeoff that BOCOM's rising personal NPL ratio demonstrates.

Sci-Tech Finance Initiative

BOCOM introduced its "BOCOM Sci-Tech" brand to provide tailored financial services for tech companies throughout their development. In collaboration with several tech investment firms, BOCOM launched a new fund of funds focused on innovative Shanghai-based companies, as well as sub-funds targeting industries such as integrated circuits, advanced manufacturing, photonic chips, and commercial space exploration.

RMB Internationalization Role

Bocom is known for its strategic importance in the process of RMB internationalization, particularly with its role as one of the first banks involved in the Cross-Border Interbank Payment System, or CIPS.

As China promotes international use of the RMB, BOCOM's cross-border capabilities position it to benefit from trade settlement and offshore financing growth.

Ownership Structure & Governance

State Control Architecture

This concentrated state dominance facilitates direct governmental influence over strategic decisions, though BoCom maintains operational independence as a commercial entity. The ownership model reflects China's hybrid financial system, where state control prioritizes systemic stability and policy objectives over pure market-driven governance.

The government's willingness to support BOCOM in times of need is very strong, given the government holdings of 23.9% under the Ministry of Finance (MOF) and 15.5% under the National Council for Social Security Fund (SSF). Being one of the six large state-owned banks, the bank has high systemic importance to China and the global banking industry. It is also tasked with policy functions and sovereign mandates for promoting economic growth and facilitating industry development.

The HSBC Question Revisited

Twenty years after the original investment, HSBC's stake has evolved. In 2024, HSBC recognised an impairment loss of $3.0bn in respect of the Group's investment in BoCom.

The HSBC relationship illustrates the limits of strategic partnerships in China's state banking system. Despite two decades of collaboration, board seats, and operational cooperation, HSBC remains a minority investor without control—subject to the same political and regulatory constraints as any other shareholder.

Governance Reality

For investors, the governance reality is straightforward: BOCOM operates as a commercial entity within parameters set by state policy. Major strategic decisions—capital allocation priorities, lending sector targets, dividend policy—reflect both commercial logic and policy directives. The bank cannot be evaluated purely through commercial metrics.

Playbook: Business & Investing Lessons

Lesson 1: The "First Mover" Template

BOCOM's 1987 reconstitution as China's first joint-stock commercial bank created a template that subsequent reforms followed. Being first meant absorbing the learning curve, making mistakes, and developing institutional capabilities that could be exported elsewhere in the system. This reformist heritage provides genuine cultural and operational advantages.

Lesson 2: Strategic Partnerships in Controlled Markets

The HSBC partnership demonstrates both the potential and limitations of foreign strategic investment in China. Capital, expertise, and credibility can be imported; control cannot. Foreign investors seeking China exposure through minority stakes in state banks must accept policy risk as an embedded feature.

Lesson 3: State Banks as Policy Tools

The 2025 recapitalization crystallizes a fundamental tension. BOCOM exists simultaneously as a commercial enterprise (maximizing shareholder returns) and as a policy instrument (supporting national development priorities). When these objectives conflict, policy wins.

Lesson 4: Regional Concentration as Competitive Advantage

BOCOM's Shanghai headquarters and Yangtze River Delta focus represent a differentiated position relative to Beijing-headquartered giants. Regional specialization can be a moat when that region is China's most dynamic economic zone.

Lesson 5: Digital Disruption Response

Traditional banks can invest heavily in technology and still lose the most valuable customer touchpoints to platform companies. BOCOM's digital efforts are necessary for survival but insufficient for transformation.

Lesson 6: Capital Allocation Under Political Constraints

Good reported metrics don't tell the whole story when a bank faces directed lending mandates, policy rate compression, and societal stability obligations alongside commercial objectives.

Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's Five Forces

Threat of New Entrants: LOW China's banking sector has extremely high barriers to entry. Regulatory licensing requirements are stringent, capital requirements enormous, and the state maintains tight control over who can operate. Foreign banks face even higher hurdles, limited to minority stakes and restricted branch networks. This protects incumbents like BOCOM.

Bargaining Power of Suppliers (Depositors): MODERATE Depositors can move funds to fintech money market products (Yu'e Bao and competitors) that offer superior yields and convenience. However, deposit insurance and state backing provide comfort that smaller institutions cannot match. The central bank's benchmark rate setting also limits deposit rate competition.

Bargaining Power of Buyers: MIXED Retail customers have significant alternatives through digital platforms and can easily switch for routine transactions. Corporate borrowers, especially private enterprises, have growing options. However, state-owned enterprises often have relationships directed by policy rather than pure price competition.

Threat of Substitutes: HIGH This is BOCOM's greatest competitive challenge. Alipay and WeChat Pay have evolved into full-service financial platforms offering payments, lending, insurance, and wealth management. For many Chinese consumers, the super-app is now the primary financial relationship.

Competitive Rivalry: HIGH Among the Big Five state banks plus joint-stock banks, competition for quality corporate clients and retail deposits is intense. Margin compression reflects this competitive intensity. However, the competitive field is somewhat managed by state ownership and policy coordination.

Hamilton's Seven Powers Analysis

Scale Economies: BOCOM benefits from scale in technology infrastructure, regulatory compliance, and risk management systems. However, it's smaller than the Big Four, so scale advantages are relative.

Network Effects: Limited in traditional banking. BOCOM doesn't benefit from the user-to-user network effects that power Alipay and WeChat Pay.

Counter-Positioning: BOCOM is positioned between the massive state giants and nimble fintech players. Its counter-position as a reform-oriented, Shanghai-based, internationally-partnered bank is distinct but not strongly defensible.

Switching Costs: Moderate for corporate relationships involving complex credit facilities and treasury services. Low for retail transactions increasingly conducted through third-party platforms.

Branding: The century-old heritage provides brand equity, particularly with older and more conservative customers. Less resonant with younger, digitally-native consumers.

Cornered Resource: BOCOM's most defensible position is its Yangtze River Delta franchise and Shanghai headquarters—geographic advantages that cannot be replicated.

Process Power: BOCOM has genuine operational capabilities in trade finance, cross-border services, and corporate banking developed over decades. These capabilities take years to build and represent real process power.

Investment Considerations

Key Metrics to Watch

For investors tracking BOCOM's ongoing performance, three metrics deserve close attention:

1. Net Interest Margin (NIM): Currently at 1.27%, among the lowest in the sector. NIM compression reflects both policy-directed rate cuts and competitive pressure. Stabilization or recovery would signal improved profitability fundamentals.

2. Real Estate NPL Ratio: The sector-specific NPL ratio for property exposure (4.85% at year-end 2024) is more revealing than headline NPLs. Watch for whether this stabilizes as property markets find a floor, or continues deteriorating.

3. Personal Loan Growth vs. Personal Loan NPLs: BOCOM is strategically pivoting toward retail lending. The ratio of personal loan growth (currently outpacing corporate growth) to personal loan NPL formation (rising to 1.08%) will indicate whether this strategy creates value or concentrates risk.

Bull Case Elements

- State backing provides explicit capital support and implicit guarantee

- Yangtze River Delta regional concentration offers superior growth exposure

- ~5% dividend yield attractive for income-focused investors

- Reform heritage may allow faster adaptation than larger state peers

- International HSBC partnership provides operational expertise

Bear Case Elements

- Policy mandates subordinate commercial returns to national priorities

- Real estate exposure risks remain elevated despite stable headline NPLs

- Fintech competition erodes retail banking franchise value

- 18% dilution from 2025 recapitalization reduces per-share value

- NIM compression appears structural rather than cyclical

Regulatory and Legal Considerations

BOCOM operates under China's regulatory framework, which provides less transparency and fewer minority shareholder protections than Western markets. The bank's status as a G-SIB subjects it to additional capital requirements but also provides systemic importance that makes state support virtually certain. U.S.-China tensions create potential sanctions risk for international investors, though this has not materialized significantly to date.

Conclusion: The Paradox of the Pioneer

Bank of Communications embodies the contradictions of Chinese state capitalism. It was created to reclaim national sovereignty from foreign capital, then welcomed foreign capital as a strategic partner. It pioneered market-based banking reform, then remained firmly under state control. It adopted international governance standards for listing, then operates according to domestic policy priorities.

For 117 years, BOCOM has survived—and often thrived—by navigating between these contradictions rather than resolving them. The bank that Liang Shiyi created to buy back a railway has become a $2 trillion institution ranking among the world's largest. Yet it remains, fundamentally, what it was at birth: an instrument of national development that happens to be organized as a commercial bank.

The 2025 recapitalization marks another inflection point. Beijing is explicitly asking its major banks to support economic transformation—green energy, semiconductors, infrastructure modernization—while simultaneously managing legacy real estate exposure and maintaining dividend payments. These demands may prove compatible, or they may conflict. BOCOM's ability to serve multiple masters while generating acceptable returns for shareholders will determine whether the next chapter of this extraordinary institutional story is one of continued adaptation or structural decline.

For investors, the proposition is nuanced: BOCOM offers exposure to China's growth potential with explicit state backing, but only through a vehicle whose primary purpose is not maximizing shareholder value. Understanding this trade-off is essential to any investment thesis. The bank that pioneered Chinese banking reform remains, ultimately, a bank that exists to serve China's development—whatever that means in any given era.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube