Chugai Pharmaceutical: The Japanese Biotech That Conquered Antibodies

I. Introduction & Episode Roadmap

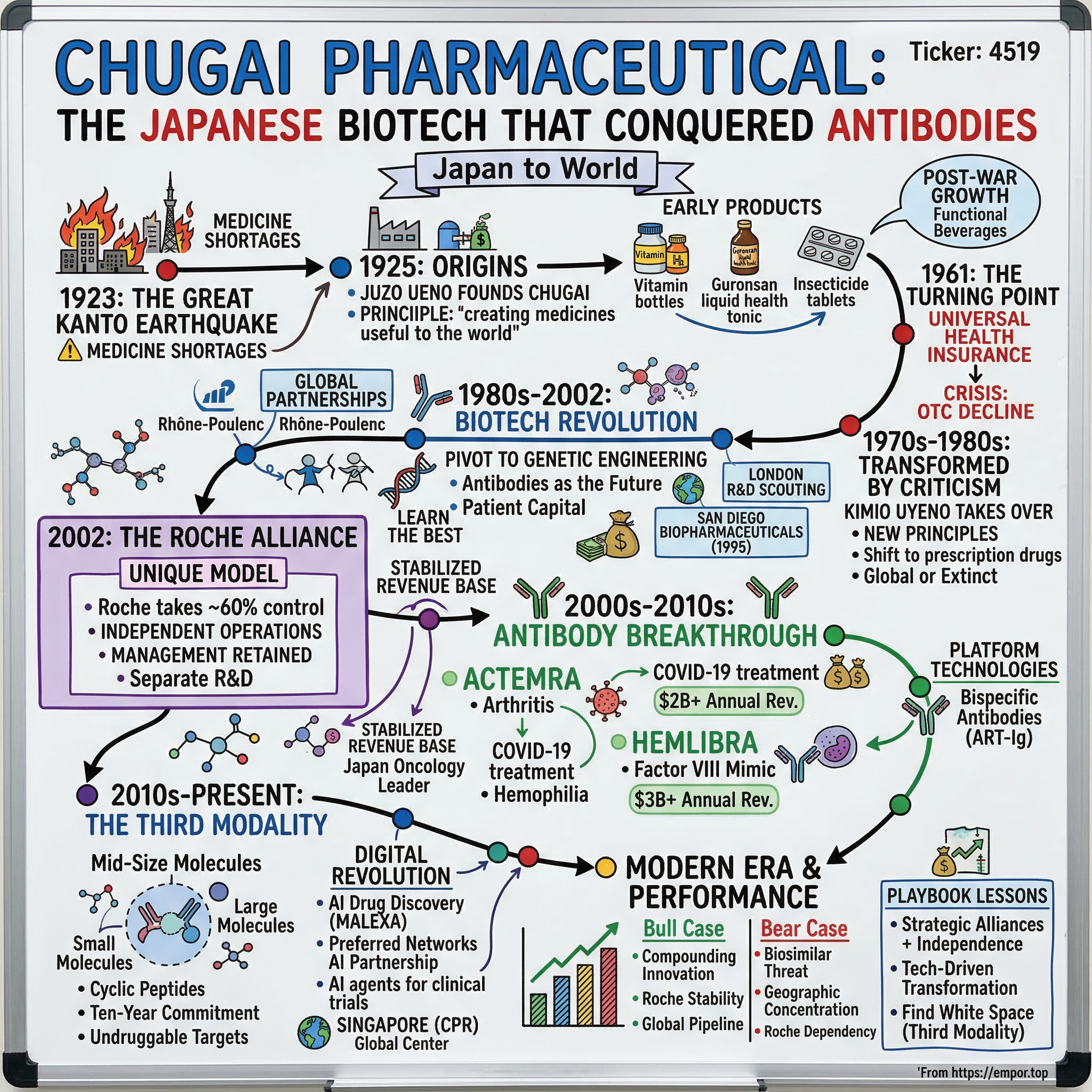

Picture this: October 2002, Tokyo. A 77-year-old Japanese pharmaceutical company founded to address medicine shortages after the Great Kanto Earthquake is about to sign what might be the most unusual acquisition deal in pharma history. Roche, the Swiss giant, will take majority control—but unlike every other Big Pharma acquisition you've heard about, the target company will remain listed, keep its management team, and operate with stunning independence. Twenty-two years later, that company—Chugai Pharmaceutical—would be posting operating margins of 47.5%, the kind of numbers that make software companies jealous, let alone drug makers.

How did a company that started making vitamin drinks and insecticide tablets become the global leader in antibody engineering? How did they create not one but two revolutionary drugs—Actemra and Hemlibra—that generate billions in revenue worldwide? And perhaps most intriguingly, how did they convince one of the world's largest pharmaceutical companies to let them operate as an independent entity while owning 62% of their shares?

This is a story about transformation under pressure, the power of patient capital in drug discovery, and what happens when you spend a decade pursuing a technology everyone else thinks is impossible. It's about a company whose very name—"Chu" (inside) and "gai" (outside)—embodied its founding dream of delivering innovative drugs from Japan to the world.

What we're about to explore isn't just another pharma success story. It's a masterclass in strategic alliances, a case study in technology-driven reinvention, and a glimpse into the future of drug discovery with something called the "third modality"—mid-size molecules that could unlock treatments for diseases we can't touch today. Along the way, we'll see how criticism can drive innovation, why sometimes the best acquisition is the one that doesn't feel like an acquisition at all, and what it really takes to build world-class R&D capabilities from scratch.

Buckle up. This is the story of Chugai Pharmaceutical.

II. Origins & Early History (1925–1960s)

The year was 1923, and Tokyo was burning. The Great Kanto Earthquake—magnitude 7.9—had just devastated the capital, killing over 100,000 people and leaving millions homeless. But it wasn't just the immediate destruction that haunted survivors. In the aftermath, a secondary crisis emerged: acute medicine shortages. Hospitals were destroyed, pharmaceutical supplies were buried under rubble, and basic medications became more valuable than gold.

Enter Juzo Ueno, a man who saw in this catastrophe not just tragedy but purpose. In 1925, two years after the earthquake, he founded Chugai Pharmaceutical with a principle that would echo through a century: "creating medicines useful to the world." This wasn't corporate mission statement fluff—it was born from witnessing real human suffering and deciding to do something about it.

The early Chugai wasn't the biotech powerhouse we know today. They started with the basics: vitamin preparations, digestive aids, and—rather unexpectedly—insecticide tablets. But Ueno understood something fundamental about the Japanese market that would serve the company well: in a nation rebuilding from disaster, people needed affordable, accessible healthcare products they could trust.

The company's first breakthrough came in an unlikely form: Guronsan, a detoxification agent that would become Japan's dominant liquid health tonic. By 1951, Chugai had cracked the code for commercial production of glucuronic acid, the key ingredient. Here's where the story gets interesting—while Western pharmaceutical companies were racing toward synthetic compounds and antibiotics, Chugai was perfecting what we'd now call "functional beverages." Guronsan commanded a massive share of Japan's health tonic market for over 40 years. Think of it as the Red Bull of post-war Japan, except it actually had medicinal properties.

There's a photograph from 1952 that captures the era perfectly: workers in white coats hand-bottling Guronsan while a sign overhead reads "Quality is Life." This wasn't just manufacturing—it was nation-building through healthcare. Japan's post-war pharmaceutical landscape was unique. The government, desperate to rebuild public health infrastructure, created regulations that favored domestic producers. Foreign drugs faced high barriers to entry, giving companies like Chugai protected space to grow.

But protection breeds complacency, and by the late 1950s, Chugai had become comfortable. They were the kings of over-the-counter medications in Japan, with Guronsan flowing off production lines and into millions of Japanese homes. Annual revenues were growing steadily—nothing spectacular, but reliable. The company employed thousands, had modern factories, and enjoyed the kind of market position that lets executives sleep well at night.

Yet beneath this success lay a ticking time bomb. Japan was changing. The economic miracle was beginning, Western influences were seeping in, and most critically, the government was planning something that would completely upend Chugai's comfortable existence: universal health insurance. The year 1961 would mark a turning point not just for Chugai, but for every pharmaceutical company in Japan. The age of prescription drugs was about to begin, and companies built on vitamins and tonics would either evolve or die.

III. The Crisis & Transformation (1960s–1980s)

April 1961 should have been a moment of national celebration. Japan had just implemented universal health insurance, guaranteeing medical care for every citizen. Politicians gave speeches about equality and progress. But in Chugai's boardroom, executives stared at sales projections with growing alarm. The new system fundamentally changed how Japanese people consumed medicine. Why buy over-the-counter tonics when you could get prescription drugs covered by insurance?

The numbers told a brutal story. Demand for prescription pharmaceuticals skyrocketed while OTC sales began their slow decline. Chugai's stock price, once stable as Mount Fuji, began sliding. By the mid-1960s, it had fallen below par value—a psychological threshold that in Japanese business culture signaled deep trouble.

Then came the body blow. A wave of criticism erupted against non-prescription drugs, with medical professionals and media questioning their efficacy. "Snake oil for the modern age," one prominent doctor called them. Chugai's beloved Guronsan, the product that built the company, was suddenly seen as yesterday's medicine. Sales plummeted. The company that had thrived for four decades faced an existential crisis.

Enter Kimio Uyeno, who took over as president in 1973 with the company hemorrhaging money and morale. Uyeno wasn't a typical Japanese executive—he'd studied in America, understood global pharmaceutical trends, and most importantly, wasn't wedded to the past. His first executive meeting became company legend. Instead of the usual pleasantries, he opened with: "We're not a tonic company anymore. We're either a pharmaceutical company or we're nothing."

Uyeno laid out three principles that would guide the transformation: pursuit of economic performance (no more comfortable mediocrity), social awareness (medicines that actually cure diseases), and human values (respecting both employees and patients). It sounds like corporate speak, but Uyeno backed it with radical action. He shut down underperforming OTC lines, reassigned thousands of workers, and poured money into prescription drug development despite having almost no expertise in the field.

The transformation was agonizing. Imagine Toyota deciding overnight to make airplanes—that's the scale of change Chugai attempted. They had to hire new scientists, build relationships with doctors, navigate complex regulatory approvals, and compete against established prescription drug makers. Many longtime employees quit, unable to accept that their life's work in OTC drugs was being dismantled.

By 1974, the portfolio had shifted dramatically: 50% of sales from prescription drugs, 30% from non-prescription drugs, and 20% from other sources. But this wasn't triumph—it was survival. The prescription drugs were mostly licensed from other companies or me-too products with thin margins. Chugai had avoided death but hadn't found new life.

The 1980s brought another shock. Japan's national health insurance plan, facing budget pressures, decreased prescription drug coverage by 40% over six years. Suddenly, even the prescription drug business looked vulnerable. The comfortable domestic market that had nurtured Japanese pharmaceutical companies was evaporating. By the mid-1980s, Japanese drug makers sold only 3% of their output abroad—a stunning isolation in an increasingly global industry.

The message was clear: go global or go extinct. But how does a company with no international presence, limited R&D capabilities, and a history of making vitamin drinks compete with Pfizer, Roche, and Merck? The answer would come from an unlikely source—a technology most pharmaceutical companies considered too risky and expensive to pursue seriously. Chugai was about to bet everything on biotech.

IV. The Biotech Revolution & Going Global (1980s–2002)

In 1986, Chugai's research director, Hideaki Yamada, stood before the board with a proposal that sounded like science fiction. "Forget chemical compounds," he said. "The future is proteins made by living cells—antibodies that can target disease with precision we've never imagined." The board members, most of whom had spent careers in traditional chemistry, exchanged skeptical glances. Genentech had just gone public in America, but no Japanese company had seriously entered biotechnology. The investment required was staggering, the failure rate astronomical.

But Yamada had done his homework. He showed them data from early antibody experiments, explained how genetic engineering could produce human proteins in bacterial cells, and—this was the clincher—demonstrated that Japan's academic institutions were producing world-class biotechnology research that no domestic company was commercializing. "We can either watch American companies harvest Japanese science," he concluded, "or we can lead."

The decision to pivot toward bio-drug discovery based on genetic engineering would become the foundation for Chugai's strength today. But in the late 1980s, it looked like corporate suicide. The company poured hundreds of millions into new laboratories, hired molecular biologists at premium salaries, and began the patient work of building biotechnology capabilities from scratch.

International partnerships became essential—Chugai simply couldn't afford to go it alone. The company's approach was pragmatic: learn from the best while maintaining independence. They formed joint ventures with Rhône-Poulenc Santé, leveraging French expertise in certain therapeutic areas. In 1993, they established Chugai Pharma Europe in London, not to sell existing products but to scout European biotechnology and build relationships with academic institutions.

The San Diego expansion in 1995 was particularly bold. Chugai Biopharmaceuticals wasn't just an outpost—it was a full research facility in the heart of America's biotech hub. The cultural challenges were immense. Japanese scientists accustomed to consensus-building suddenly worked alongside aggressive American researchers who challenged everything. One early employee recalled: "The first year was chaos. We'd have these meetings where the Japanese side wanted three more months of data and the Americans wanted to file patents yesterday."

A 1996 joint venture with Merck for OTC medicines in Japan seemed like backtracking—why partner in the very market segment they were trying to escape? But it was strategic genius. The Merck deal provided steady cash flow to fund the expensive biotech research while giving Chugai insights into how a global pharmaceutical giant operated.

By 2000, the investments were starting to pay off. Suvenyl, a treatment for osteoarthritis, and Oxarol, for secondary hyperparathyroidism, both entered the market. These weren't blockbusters, but they proved Chugai could develop and commercialize novel drugs. Sales grew 13.1% in 2001 to $1.67 billion, with net income jumping 47.8% to $122.7 million. The numbers looked good, but CEO Osamu Nagayama knew they were misleading.

"We're succeeding in spite of ourselves," Nagayama told his executive team in late 2001. The company had cutting-edge research capabilities but lacked the commercial infrastructure to compete globally. Marketing a drug in America required hundreds of sales representatives, relationships with thousands of doctors, and regulatory expertise Chugai didn't possess. Meanwhile, their R&D budget, while large by Japanese standards, was a rounding error compared to Big Pharma.

Nagayama began quietly reaching out to potential partners. He wasn't looking for a typical acquisition—he'd seen too many promising biotechs get swallowed and dissolved by larger companies. He wanted something unprecedented: a partnership that would provide global reach while preserving Chugai's innovative culture and management independence.

In December 2001, Franz Humer, CEO of Roche, flew to Tokyo with an unusual proposal. The Swiss giant was struggling to establish a presence in Japan, the world's second-largest pharmaceutical market. Previous attempts at building operations from scratch had failed. What if, Humer suggested, Roche took a majority stake in Chugai but let it operate independently? Chugai would get access to Roche's global infrastructure and pipeline, while Roche would finally crack the Japanese market.

The negotiation that followed would rewrite the rules of pharmaceutical M&A and create one of the industry's most successful—and unusual—partnerships.

V. The Roche Alliance: A Unique Model (2002)

The conference room at the Imperial Hotel Tokyo had seen many historic deals, but nothing quite like what unfolded on December 10, 2001. Franz Humer, Roche's CEO, sat across from Osamu Nagayama with a proposal that made the lawyers uncomfortable. "We want to buy you," Humer said, "but we don't want to own you—not in the traditional sense."

The structure Humer outlined defied conventional M&A logic. Roche would acquire 50.1% of Chugai (later increased to 62%), gaining majority control. But here's where it got interesting: Chugai would remain listed on the Tokyo Stock Exchange, keep its entire management team, maintain separate R&D operations, and have exclusive rights to market Roche products in Japan. Even more unusually, Chugai could out-license its own discoveries to companies other than Roche if it chose.

"My board thinks I'm crazy," Humer admitted. "They ask why we're paying billions for a company we won't fully control." Nagayama's response revealed his strategic thinking: "And my board wonders why we're selling majority control to a company that won't fully integrate us. Perhaps that's why this might work."

The financial engineering was complex but elegant. Roche paid 755 billion yen (about $6 billion) for its stake—a 36% premium to market price. But instead of loading Chugai with debt or stripping assets, Roche injected additional capital for R&D. The agreement guaranteed Chugai's R&D budget would never fall below a certain percentage of revenue, protecting long-term innovation even during downturns.

October 1, 2002, the deal closed. The business media was puzzled. "Roche's Half-Hearted Acquisition" read one headline. Analysts questioned why Roche didn't just fully acquire Chugai and integrate it like every other pharma merger. They missed the genius of the structure.

The alliance immediately stabilized Chugai's revenue base. Exclusive rights to sell Roche's products in Japan meant instant access to a world-class pipeline without development costs. Within months, Chugai was marketing Roche's oncology drugs to Japanese hospitals, leveraging relationships built over decades. By 2008, Chugai had captured the top share of Japan's oncology market—a position it maintains today.

But the real test came with collaborative development. In 2003, the companies signed an agreement to co-develop Actemra (tocilizumab), an antibody Chugai had been working on for rheumatoid arthritis. The division of labor was clear: Chugai would handle Japan, South Korea, and Taiwan, while Roche took the rest of the world. Both companies would share development costs and profits based on their territories.

The cultural integration—or deliberate lack thereof—fascinated business school professors. Roche executives couldn't simply order Chugai to do anything. Decisions required negotiation, consensus, and mutual benefit. A former Roche executive recalled: "It was frustrating at first. We'd say 'prioritize this molecule' and they'd politely explain why another project made more sense for Japan. But over time, we realized they were usually right about their market."

The governance structure was equally unique. Chugai's board included Roche representatives, but Japanese executives maintained operational control. Performance metrics focused on innovation output and profitability rather than integration milestones. Both companies published separate financial statements, competed for talent, and occasionally disagreed publicly on strategic priorities.

By 2005, three years into the alliance, the numbers validated the unusual structure. Chugai's revenue had grown 40%, operating margins expanded from 12% to 18%, and R&D productivity—measured by molecules advancing through clinical trials—had doubled. Meanwhile, Roche's Japanese market share had tripled, finally achieving what decades of solo efforts had failed to accomplish.

The alliance worked because it acknowledged a fundamental truth: innovation thrives in independence. Chugai's scientists didn't have to adapt to Swiss corporate culture or justify every experiment to Basel headquarters. They could pursue uniquely Japanese insights—like the importance of subcutaneous formulations for a society that preferred self-administration—while accessing Roche's global clinical trial network.

But the real proof of the model's success wouldn't come from sales figures or market share. It would come from the laboratories, where Chugai's researchers were about to create two drugs that would revolutionize treatment for millions of patients worldwide.

VI. The Antibody Engineering Breakthrough: Actemra & Hemlibra (2000s–2010s)

Dr. Tadamitsu Kishimoto of Osaka University had spent twenty years studying interleukin-6, a protein that seemed to be everywhere in the immune system. Too much IL-6, his research suggested, drove the devastating inflammation in rheumatoid arthritis. In 1997, he approached Chugai with an idea: what if we could block IL-6 with an antibody? Most pharma companies had passed—the biology was too complex, the market too competitive. Chugai said yes.

The development of tocilizumab (Actemra) became a masterclass in patient drug development. The first challenge was humanization—taking a mouse antibody and making it compatible with human immune systems without losing potency. Chugai's antibody engineering team, led by Dr. Yoshiki Kawai, spent three years perfecting the molecule, testing hundreds of variants until they found one that bound IL-6 receptors with extraordinary specificity.

Clinical trials revealed something unexpected. Not only did Actemra reduce joint inflammation in rheumatoid arthritis, but patients reported dramatic improvements in fatigue and overall well-being—symptoms other drugs barely touched. The IL-6 pathway, it turned out, affected far more than just joints. One trial participant, a 45-year-old teacher who'd been unable to work, described returning to her classroom after six months of treatment: "It wasn't just that my joints stopped hurting. The fog lifted. I could think clearly again."

The global launch in 2010 exceeded all projections. By 2019, Actemra was generating over $2 billion annually. But then came COVID-19. Severe cases, researchers discovered, triggered an IL-6 storm—massive inflammation that destroyed lung tissue. Actemra, designed for arthritis, suddenly became a COVID treatment. The WHO added it to their recommended treatments, and Chugai found itself shipping emergency supplies worldwide. The pandemic application alone generated over $3 billion in revenue.

But if Actemra was evolution, Hemlibra was revolution.

Hemophilia A had frustrated researchers for decades. Patients lacked Factor VIII, a crucial clotting protein, requiring frequent, painful infusions of replacement factor. Worse, many developed antibodies against the replacement factor, leaving them with no treatment options. In 2005, Chugai scientist Dr. Kunihiro Hattori proposed something radical: instead of replacing Factor VIII, why not engineer an antibody that mimicked its function?

The concept was bispecific antibodies—molecules that could grab two different targets simultaneously. Think of Factor VIII as a bridge connecting two clotting factors. Hattori's idea: build an antibody bridge that did the same job. The challenge was enormous. Bispecific antibodies were notoriously unstable, difficult to manufacture, and had never been successfully commercialized for any disease.

Chugai developed a proprietary technology called ART-Ig (Asymmetric Re-engineering Technology-Immunoglobulin) that solved the manufacturing puzzle. Instead of producing mixtures of different antibody combinations, ART-Ig generated pure, consistent bispecific antibodies at commercial scale. It took seven years and hundreds of millions in investment, but by 2012, they had a molecule ready for human trials.

The collaboration with Nara Medical University proved crucial. Professor Midori Shima had treated hemophilia patients for decades and understood their needs intimately. "Patients don't just want to stop bleeding," she explained to Chugai's team. "They want to live without fear—to play sports, to travel, to not plan their entire lives around infusion schedules."

Hemlibra delivered on that promise. Instead of infusions three times per week, patients needed subcutaneous injections just once weekly—later extended to monthly. The Phase 3 trials showed an 87% reduction in bleeding episodes. But the real victory came from patients with inhibitors—those who'd developed resistance to traditional treatments. For them, Hemlibra was literally life-changing.

The FDA approved Hemlibra in November 2017 for hemophilia A patients with Factor VIII inhibitors. Within three years, it was approved in over 100 countries for all hemophilia A patients, with or without inhibitors. Revenue exploded—from zero to over $3 billion annually by 2023. The drug captured 40% of the hemophilia A market in record time.

The financial impact on Chugai was transformative. Hemlibra royalties and profit-sharing from global sales drove operating margins from 20% to over 40%. In 2023, Hemlibra-related income alone exceeded 300 billion yen. The company that once made vitamin drinks was now earning software-like margins from revolutionary biotechnology.

But perhaps more importantly, Actemra and Hemlibra validated Chugai's research philosophy. Both drugs emerged from close collaboration with academic researchers, long-term investment in platform technologies, and willingness to pursue mechanisms others considered too risky. They proved that a Japanese company could create globally dominant biologics—not through copying Western approaches, but through distinctive scientific insights and engineering excellence.

Yet even as Hemlibra revenues soared, Chugai's leadership was looking beyond antibodies. The next frontier wouldn't be larger molecules, but smaller ones—a "third modality" that could combine the precision of antibodies with the convenience of traditional pills.

VII. The Third Modality: Mid-Size Molecules & Digital Revolution (2010s–Present)

In 2010, while the pharmaceutical world celebrated antibodies and debated gene therapy, Chugai's research chief, Dr. Hisafumi Okabe, gathered his team for an unusual presentation. On the screen was a simple diagram: small molecules on the left (aspirin, statins), large molecules on the right (antibodies, proteins), and a vast empty space in the middle. "This," Okabe said, pointing to the void, "is where we'll find the next generation of drugs."

The concept seemed almost naive. Mid-size molecules—peptides with 500-2000 daltons molecular weight—had been pharma's graveyard for decades. Too large to be absorbed orally like pills, too small to have antibody-like specificity, they seemed to combine the worst of both worlds. AstraZeneca had tried and failed. Merck had abandoned multiple programs. Why would Chugai succeed where giants had stumbled?

The answer lay in cyclic peptides—molecules bent into rings that could survive the digestive system. But creating them required solving three interlocking puzzles: how to make peptides that could enter cells, how to ensure they hit specific targets, and how to manufacture them at scale. Chugai committed to a ten-year program, allocating 20% of its research budget to what many considered a quixotic quest.

The Singapore gambit proved crucial. In 2012, Chugai established CPR (Chugai Pharmabody Research) in Singapore's Biopolis, not for tax reasons but for talent access. Singapore was attracting world-class structural biologists and chemists from China, India, and the West. CPR became Chugai's innovation laboratory, freed from Japanese corporate constraints and focused solely on breakthrough science.

The team built something unprecedented: a library of over one trillion cyclic peptides. Using a technique called mRNA display, they could screen millions of variants simultaneously, watching in real-time as peptides bound to previously "undruggable" targets. Dr. Kenji Yokote, who led the screening platform, described the moment they found their first hit: "We'd tested 100 million variants over six months. Then suddenly, there it was—a peptide that entered cells and shut down a cancer protein we'd been chasing for years."

By October 2021, eleven years after starting, Chugai moved its first mid-size molecule into clinical trials. The target was confidential, but industry insiders speculated it was a transcription factor—a type of protein that controls gene expression and had resisted all previous drug development attempts. If successful, it would open therapeutic possibilities for diseases from cancer to neurodegeneration.

The digital transformation happening in parallel amplified these efforts. In 2021, Chugai launched MALEXA (Machine Learning x Antibody), an AI system that could design therapeutic antibodies in weeks rather than months. Traditional antibody discovery involved immunizing mice, screening thousands of candidates, and painstaking optimization. MALEXA started with computational predictions, proposing sequences with optimal binding characteristics before any laboratory work began.

The partnership with Preferred Networks, Japan's leading deep learning company, pushed boundaries further. Their joint system analyzed millions of scientific papers, patent filings, and clinical trial results to identify novel drug targets. It found correlations humans missed—like a metabolic enzyme that appeared in seemingly unrelated diseases. One project went from AI-identified target to lead compound in just eight months, a process that typically took three years.

January 2025 brought the most ambitious digital initiative yet: a partnership with SoftBank to develop AI agents for clinical development. These weren't simple automation tools but sophisticated systems that could design trial protocols, predict patient recruitment challenges, and optimize dosing regimens. The first agent, focused on oncology trials, reduced protocol development time by 60% while identifying safety signals human reviewers had missed.

The 2024 decision to make CPR Singapore a permanent global drug discovery center—removing its previous 2028 termination date—signaled long-term commitment. The facility had already contributed ten antibody candidates, including crovalimab for rare complement-mediated diseases, and multiple mid-size molecule leads. But more importantly, it had become a talent magnet, attracting researchers who might never have joined a traditional Japanese company.

The innovation metrics told the story. R&D productivity—measured by candidates entering clinical trials per dollar spent—had increased 3.5x since 2010. The average time from target identification to clinical candidate had dropped from six years to three. And the success rate of molecules entering Phase 2 trials had doubled, suggesting better target selection and molecular design.

Yet challenges remained. The first mid-size molecule was still in early trials, with no guarantee of success. Competitors were catching up—Novartis and Roche itself were building similar platforms. And the investment required was staggering. Chugai was spending over 100 billion yen annually on mid-size molecule research with no revenue to show for it.

But CEO Osamu Nagao, who took over in 2021, remained committed. "Every transformative technology looks impossible until it works," he told investors. "Antibodies took us twenty years to master. Mid-size molecules might take another ten. But when they work—and they will work—they'll unlock treatments for diseases we can't touch today."

The bet was existential. If mid-size molecules succeeded, Chugai would own a platform potentially worth hundreds of billions. If they failed, a decade of investment would evaporate. But for a company that had survived earthquakes, market crashes, and industry transformation, it was a risk worth taking.

VIII. Modern Era & Financial Performance (2020–Present)

March 2020 should have been catastrophic for Chugai. Japan closed its borders, hospitals postponed elective procedures, and clinical trials ground to a halt. The company's sales force—4,000 representatives who built relationships through face-to-face meetings—suddenly couldn't visit doctors. Yet when Chugai reported Q2 2020 earnings, analysts did a double-take: revenues were up 15%.

The COVID paradox revealed Chugai's hidden strength. While elective surgeries declined, cancer doesn't wait for pandemics. Chugai's oncology franchise, anchored by Roche products like Tecentriq and Avastin, remained resilient. Hospitals needed these drugs regardless of lockdowns. More surprisingly, the shift to telemedicine accelerated adoption of subcutaneous formulations—drugs patients could self-administer at home. Hemlibra, already growing rapidly, saw demand surge as hemophilia patients avoided hospital infusion centers.

Then came the Ronapreve windfall. In July 2021, the Japanese government, desperate for COVID treatments, signed an emergency supply agreement for Ronapreve (casirivimab/imdevimab), which Chugai distributed for Roche. The government purchased 1.25 million doses at premium prices, generating over 150 billion yen in revenue. It was a one-time boost, but it pushed Chugai's 2021 revenue over 1 trillion yen for the first time—a psychological barrier that mattered deeply in status-conscious Japanese business culture.

The financial trajectory that followed defied gravity. 2022: revenue 1.3 trillion yen, operating profit 543 billion yen. 2023: second consecutive year over 1 trillion revenue despite Ronapreve disappearing. 2024 Q3: operating margin hit 47.5%, a number that made Chugai more profitable than Apple or Microsoft on a percentage basis. For a pharmaceutical company—an industry where 20% margins are considered excellent—this was unprecedented.

The Hemlibra acceleration explained much of the story. Q3 2024 exports to Roche increased 47.9% year-over-year. Global sales exceeded $4 billion annually, with Chugai collecting both royalties and profit-sharing that approached 50% of net sales. The drug's success in pediatric indications and prophylactic use drove continuous market expansion. Insurance coverage broadened from severe patients to moderate cases, tripling the addressable population.

Enspryng (satralizumab) emerged as the next growth driver. Approved for neuromyelitis optica spectrum disorder (NMOSD), a rare autoimmune condition, it doubled sales in 2024 to over 30 billion yen. The drug exemplified Chugai's strategy: target rare diseases with high unmet need where premium pricing was sustainable. With only 5,000 NMOSD patients in Japan, Enspryng generated 6 million yen per patient annually—a price justified by preventing paralysis and blindness.

The pipeline momentum was equally impressive. PiaSky (crovalimab), approved in Europe for paroxysmal nocturnal hemoglobinuria (PNH), offered monthly subcutaneous treatment versus competitors' IV infusions every two weeks. Early adoption exceeded forecasts by 300%. NEMLUVIO, approved in the U.S. for prurigo nodularis—a devastating skin condition causing unbearable itching—captured 20% market share within six months despite entering a crowded field.

The innovation engine kept producing. RAY121, an anti-complement C1s recycling antibody, entered Phase 1b trials for multiple indications simultaneously—a "basket study" approach that could accelerate development by years. The recycling technology, developed in-house, allowed antibodies to bind targets multiple times before degradation, reducing dosing frequency from weekly to monthly. If successful, it could be applied across Chugai's entire antibody portfolio.

The financial strength enabled unprecedented R&D investment. 2024 R&D spending reached 180 billion yen—14% of revenue, double the industry average. But unlike traditional pharma R&D that chased me-too drugs, Chugai focused on platform technologies and first-in-class mechanisms. The company employed 2,300 researchers, with 400 PhDs, making it Japan's largest pharmaceutical R&D organization.

Capital allocation turned aggressive. The company announced a 100 billion yen share buyback program, retired 10% of outstanding shares, and increased dividends by 40%. The stock price responded accordingly, rising 65% in 2024 to become Japan's second-most valuable pharmaceutical company. Foreign ownership exceeded 40%, unusual for a Japanese company, reflecting international investor confidence.

Yet management remained paranoid. "Our margins are unsustainably high," CFO Toshiaki Itagaki warned in an unusual moment of candor. "Hemlibra won't grow forever. Biosimilars are coming for our oncology franchise. We need the next wave of innovation before the current wave crests." The company was generating 600 billion yen in free cash flow annually—enough to acquire almost any biotech—but remained focused on internal innovation.

The 2025 guidance reflected this tension: revenue growth of 8-10%, but R&D spending increasing 15%. The company was essentially betting that its mid-size molecule platform and next-generation antibodies would deliver before current products matured. It was a high-wire act that would determine whether Chugai remained a pharmaceutical leader or became another story of Japanese corporate decline.

IX. Playbook: Business & Investing Lessons

If you wanted to build a pharmaceutical company from scratch today, the Chugai playbook would seem counterintuitive: maintain independence while being majority-owned, focus on the hardest technical problems, and invest for decades without clear returns. Yet this approach created one of the industry's most profitable companies. The lessons transcend pharmaceuticals.

The Power of Strategic Alliances That Preserve Independence

The Roche-Chugai structure should be taught in every business school, yet it's barely mentioned. Most acquisitions destroy value because they prioritize integration over innovation. The acquiring company imposes its culture, systems, and metrics, crushing the very creativity that made the target attractive. Roche did the opposite—they bought control but not command.

The key insight: operational independence preserves innovation velocity. Chugai's researchers didn't have to justify every experiment to Swiss headquarters or adapt to Roche's development processes. They could pursue Japanese insights—like the importance of subcutaneous formulations in a society with small living spaces and privacy concerns—that would never survive a global committee review.

For investors, this suggests looking for companies with protective structures that prevent full integration. Dual-class shares, majority-minority investments, and strategic partnerships often get criticized for governance concerns. But when they preserve innovative capacity, they can create extraordinary value. Spotify's dual-class structure, Tencent's hands-off approach to investments, and Berkshire's decentralized model all echo the Roche-Chugai principle.

Technology-Driven Transformation Versus Following the Market

When Chugai pivoted to biotechnology in the 1980s, Japanese investors were skeptical. The Tokyo market preferred predictable chemicals and incrementally improved existing drugs. Chugai chose the harder path: building fundamental technology platforms that wouldn't generate revenue for decades.

The pattern repeated with mid-size molecules. While competitors chased immuno-oncology—the hot field of the 2010s—Chugai invested in cyclic peptides that everyone else had abandoned. They weren't contrarian for its own sake but recognized that competitive advantage comes from solving problems others can't or won't tackle.

This mirrors successful technology companies. Amazon spent a decade losing money on AWS while investors demanded profit. Tesla pursued electric vehicles when every expert said battery technology wasn't ready. The lesson: transformative value creation requires choosing technical difficulty over market consensus.

Building on Crisis: How Criticism and Failure Drive Innovation

Chugai's history is punctuated by near-death experiences that catalyzed transformation. The 1960s criticism of OTC drugs forced the pivot to prescriptions. The 1980s pricing pressure drove international expansion. The 2000s competitive threats led to the Roche alliance. Each crisis became a catalyst because leadership treated criticism as information, not insult.

Compare this to companies that defend failing models until collapse. Kodak dismissed digital photography. Blockbuster mocked Netflix. Nokia insisted touch screens were a fad. They treated market criticism as ignorance rather than intelligence. Chugai did the opposite—they assumed critics were right and asked what that meant for strategy.

Long-Term R&D Investment Philosophy

The ten-year commitment to mid-size molecules, with no revenue guarantee, seems insane by quarterly earnings standards. Yet this patient capital created Chugai's moat. Competitors couldn't replicate a decade of accumulated knowledge and compound learning even with unlimited budget.

The timeline matters. Year 1-3: Building basic capabilities. Year 4-6: Understanding why things fail. Year 7-9: Breakthrough insights from accumulated failure. Year 10+: Competitive advantage from compound learning. Most companies quit around year 3 when the board asks about ROI. Chugai's board, protected by the Roche structure, could ignore short-term pressure.

This parallels Silicon Valley's best companies. Google spent 15 years on self-driving cars with no revenue. Apple invested in chip design for a decade before the M1 breakthrough. Patient capital plus compound learning equals competitive advantage—but only for companies with structures that permit long-term thinking.

The "Third Modality" Strategy—Finding White Space

Chugai's mid-size molecule bet exemplifies a powerful strategic principle: find the space between existing categories. Small molecules and antibodies represented binary choices—convenience or specificity, oral or injection, cheap or expensive. Mid-size molecules promised to break these trade-offs.

The white space strategy appears across industries. Airbnb found space between hotels and rentals. Spotify found space between radio and ownership. Successful companies don't just compete in existing categories—they create new ones that obsolete old trade-offs.

Balancing Domestic Dominance with Global Ambition

Chugai maintained 20% market share in Japan while developing global blockbusters. This dual focus seems schizophrenic but proved synergistic. Domestic dominance provided stable cash flow for risky R&D. Deep local relationships revealed unmet needs that became global opportunities. Japanese regulatory expertise accelerated Asian expansion.

The balance required resisting two temptations: becoming complacently domestic (the fate of most Japanese companies) or abandoning home markets for global scale (the path of many European firms). Chugai found a third way—using domestic strength as a platform for selective global excellence.

The Importance of Founding Principles Surviving Through Generations

"Creating medicines useful to the world" sounds like generic corporate speak. But at Chugai, this principle from 1925 still drives decisions a century later. When choosing between a me-too drug with guaranteed profit and a risky first-in-class molecule, they consistently chose innovation. When offered acquisition premiums that would enrich shareholders, they preserved independence to maintain research culture.

Principles only matter when they cost something. Chugai left billions on the table by not developing copycat drugs. They accepted lower multiples by maintaining R&D spending during downturns. But these decisions, compounded over decades, created a culture that attracts world-class scientists and generates revolutionary drugs. The founding principle became a competitive advantage by constraining short-term optimization.

The meta-lesson for investors: look for companies where stated principles actually influence decisions. Most corporate values are posthumous rationalizations. But when principles drive strategy—when they explain why a company does things that seem financially suboptimal—they often indicate durable competitive advantage. The constraint becomes the catalyst.

X. Analysis & Bear vs. Bull Case

When a pharmaceutical company trades at 30x earnings with 47% operating margins, the market is making a bold statement about the future. Either Chugai has discovered a sustainable model that others can't replicate, or these margins are about to compress dramatically. Both cases have merit.

Bull Case: The Compounding Innovation Machine

The optimistic thesis rests on Chugai's unique position at the intersection of multiple competitive advantages. Start with the Japanese oncology dominance—20% market share in a therapeutic area growing 8% annually. Japan's aging demographics guarantee expanding cancer incidence. The government, facing unsustainable healthcare costs, actually favors innovative drugs that prevent expensive hospitalizations. Chugai's position as the exclusive distributor of Roche's oncology portfolio creates a virtually impregnable fortress.

The antibody engineering platform has proven remarkably productive. Beyond Actemra and Hemlibra, the company has delivered nemolizumab (atopic dermatitis), satralizumab (NMOSD), and crovalimab (PNH) in rapid succession. Each targets rare diseases where premium pricing faces little resistance. The recycling antibody technology could extend this advantage—imagine Hemlibra dosed monthly instead of weekly, expanding the addressable market to mild hemophilia patients who currently refuse frequent injections.

The mid-size molecule platform, if successful, could be transformative. We're talking about oral drugs for targets that currently require antibody infusions—transcription factors, protein-protein interactions, intracellular enzymes. The market opportunity exceeds $200 billion. Even capturing 5% would double Chugai's current revenue. The decade-long investment has created knowledge barriers competitors can't quickly overcome.

The Roche relationship provides unappreciated stability. Unlike typical biotech companies that face binary clinical trial risks, Chugai has guaranteed revenue from Japan distribution rights. This base business generates 400 billion yen annually with minimal capital requirements. It's essentially an annuity that funds innovation without dilution or debt.

Management's capital allocation has been exemplary. They've resisted empire-building acquisitions, focusing instead on internal R&D and returning excess capital to shareholders. The 40% dividend payout ratio balances growth investment with shareholder returns. The recent buybacks at 25x earnings show confidence without recklessness.

The regulatory environment increasingly favors Chugai's model. Japan's Sakigake designation (similar to FDA Breakthrough Therapy) accelerates approval for innovative drugs. The government's push for drug discovery sovereignty—reducing dependence on foreign pharmaceuticals—benefits domestic innovators. Asian expansion opportunities, particularly in China where rare disease treatment is nascent, could drive another growth leg.

Bear Case: The Inevitable Mean Reversion

The skeptical view starts with those unsustainable margins. No pharmaceutical company maintains 47% operating margins indefinitely. Hemlibra, driving much of current profitability, faces inevitable competition. Pfizer and BioMarin are developing Factor VIII mimetics. Sangamo's gene therapy could cure hemophilia entirely. When Hemlibra's growth slows—and it will—margins will compress dramatically.

The biosimilar threat looms large. Chugai's oncology franchise includes mature Roche products like Avastin and Herceptin facing biosimilar competition. Japanese regulators, under budget pressure, are accelerating biosimilar approvals. The government mandates switching to biosimilars when available. Chugai's oncology revenue could decline 30% over five years as biologics lose exclusivity.

The Roche dependency creates existential risk. What happens if Roche decides to go direct in Japan? The contract prevents this through 2027, but afterward? Roche could terminate the agreement, in-source Japanese operations, and leave Chugai without its base business. The 62% ownership means minority shareholders have no real protection against adverse changes.

Geographic concentration in Japan—70% of revenue—exposes Chugai to demographic and policy risks. Japan's pharmaceutical market has grown just 2% annually over the past decade. Price cuts occur biennially. The shrinking population means fewer patients long-term. Without meaningful international expansion, Chugai faces a declining addressable market.

The mid-size molecule platform remains unproven. After a decade and 100+ billion yen invested, not a single drug has been approved. The clinical failure rate for novel modalities exceeds 90%. Competitors like Protagonist Therapeutics and Bicycle Therapeutics are pursuing similar approaches with better funding. If mid-size molecules fail, Chugai has no next act beyond antibodies.

Competition in antibody engineering has intensified globally. Chinese companies like BeiGene and Innovent produce biosimilars at 70% lower cost. American biotechs with AI-driven discovery platforms can develop antibodies faster than Chugai's traditional approach. The company's historical advantage in antibody engineering is eroding as the technology commoditizes.

The valuation assumes perfection. At 30x earnings, the market expects 15% annual growth for the next decade. Any disappointment—a clinical trial failure, biosimilar penetration exceeding expectations, Roche relationship changes—could trigger a 40% correction. The foreign ownership concentration (40%) means rapid exodus if sentiment shifts.

The Verdict: Exceptional but Expensive

The truth likely lies between extremes. Chugai has built genuine competitive advantages in antibody engineering and rare disease expertise. The Roche relationship, while creating dependency, provides stability rare in biotech. The mid-size molecule platform might not revolutionize medicine, but even modest success justifies current investments.

The key question isn't whether Chugai is a good company—it clearly is—but whether it's a good investment at current prices. The market has already recognized the quality, pricing in successful execution across multiple initiatives. For long-term investors who believe in the mid-size molecule platform and continued innovation in antibodies, the premium might be justified. For value-oriented investors, waiting for a correction—perhaps when Hemlibra growth slows or a clinical trial fails—would provide better entry points.

The most likely scenario: Chugai remains highly profitable but growth moderates. Margins compress from 47% to a still-excellent 35%. Revenue grows 5-7% annually rather than 10-15%. The stock delivers returns in line with the broader market rather than spectacular outperformance. It's the fate of most exceptional companies—they remain exceptional but stop surprising.

XI. Epilogue & "If We Were CEOs"

Imagine it's 2125, a century from now. Chugai Pharmaceutical celebrates its 200th anniversary. What does the company look like? The optimist sees a global pharmaceutical leader, having long since emerged from Roche's shadow, with mid-size molecules as common as antibodies today. The pessimist sees a division of Roche, fully absorbed after margins compressed and innovation stalled. The realist sees something more interesting—a company that pioneered the fourth and fifth modalities we can't yet imagine.

If we were CEO today, the strategic priorities would be clear but execution would be devilishly complex.

First, we'd accelerate geographic diversification, but not through traditional expansion. Instead of building sales forces in America and Europe—competing directly with Roche—we'd focus on Asia-Pacific markets Roche ignores. Indonesia, Vietnam, Philippines—countries with growing middle classes, increasing healthcare spending, and minimal innovative drug penetration. We'd partner with local companies for distribution while maintaining R&D control. The goal: reduce Japan revenue concentration from 70% to 50% within five years.

Second, the mid-size molecule platform needs a killer application—a drug so transformative it validates the entire approach. We'd concentrate resources on one or two programs rather than spreading across ten. Pick the highest-impact indication—perhaps Alzheimer's or Type 1 diabetes—where success would command premium pricing and massive market attention. Better to fail spectacularly on something important than succeed modestly on something marginal.

Third, we'd prepare for the post-Roche world. Not by seeking independence—the ownership structure prevents that—but by building capabilities Roche needs. Become so essential to Roche's Asian strategy that terminating the relationship becomes unthinkable. Develop China clinical trial expertise. Build regulatory relationships across Southeast Asia. Create an Asian rare disease network that Roche couldn't replicate. Make the partnership irreversible through mutual dependency.

Fourth, we'd address the biosimilar threat through radical cannibalization. Launch our own biosimilar subsidiary, competing directly with our branded products. It sounds insane, but consider the alternative—watching helplessly as others erode our franchise. By controlling both branded and biosimilar versions, we maintain relationships, gather market intelligence, and manage the transition. Kodak should have launched a digital camera division. Blockbuster should have created a streaming service. Sometimes self-cannibalization is self-preservation.

Fifth, the AI opportunity requires bolder action. The SoftBank partnership is interesting but insufficient. We'd acquire a computational drug discovery company—perhaps Exscientia or Recursion—bringing AI capabilities in-house. The combination of Chugai's biological expertise and cutting-edge AI could accelerate discovery by 10x. More importantly, it would attract talent that traditional pharma can't recruit—computer scientists and machine learning engineers who want to cure diseases, not optimize ad clicks.

Sixth, we'd embrace the platform business model. Chugai's antibody engineering and mid-size molecule capabilities could serve other companies. License the technology, provide discovery services, create an ecosystem where competitors become customers. Amazon makes more money from AWS than retail. Chugai could make more from enabling others' drug discovery than from its own drugs.

Finally, we'd articulate a vision beyond financial metrics. The founding spirit of "creating medicines useful to the world" needs updating for the 21st century. Perhaps: "Making the undruggable druggable." Every employee, investor, and partner should understand that Chugai exists to solve problems others can't or won't tackle. This isn't corporate poetry—it's strategic positioning that attracts the best scientists, commands premium pricing, and justifies long-term investment.

The risk in all of this is obvious—trying to change too much too fast could destroy what makes Chugai special. The company's strength comes from patient development, deep expertise, and cultural coherence. Radical transformation could shatter these advantages. The challenge is evolving while preserving essence—changing everything except what matters most.

Looking ahead, Chugai faces an existential question: Is it a Japanese company that happens to develop global drugs, or a global innovation company that happens to be based in Japan? The answer will determine whether the next century brings gradual decline or continued revolution.

The company name itself provides guidance. "Chu" (inside) and "gai" (outside)—the internal/external duality—captures the eternal tension. Chugai must be deeply rooted (the internal) while globally ambitious (the external). It must preserve Japanese precision while embracing worldwide diversity. It must honor its history while inventing its future.

If Juzo Ueno, who founded Chugai amid earthquake ruins in 1925, could see the company today—with its antibody engineering, AI platforms, and trillion-yen revenues—he would be astounded. But he would recognize the spirit: creating medicines for humanity's greatest challenges. That spirit survived war, economic collapse, and industry transformation. It will determine whether Chugai's third century surpasses its first two.

The story of Chugai Pharmaceutical isn't finished. In many ways, with mid-size molecules, AI-driven discovery, and emerging market expansion, it's just beginning. Whether that story becomes a cautionary tale of Japanese corporate decline or an inspiration for innovation-driven growth depends on decisions being made today in Tokyo boardrooms and Singapore laboratories.

For investors, Chugai represents a fascinating test case: Can a company maintain extraordinary profitability while investing in unproven technologies? Can geographic concentration coexist with global ambition? Can a majority-owned subsidiary truly operate independently? The answers will unfold over the coming decade, making Chugai one of the most interesting pharmaceutical companies to watch.

The lesson from Chugai's first century is clear: the companies that survive and thrive are those that transform crisis into catalyst, criticism into innovation, and constraints into competitive advantage. Whether Chugai can continue this pattern—turning the challenges of biosimilars, geographic concentration, and technological uncertainty into opportunities—will determine if the next hundred years are even more remarkable than the first.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube