Lenovo Group Limited: From Beijing Garage to Global PC Titan

I. Introduction & Episode Roadmap

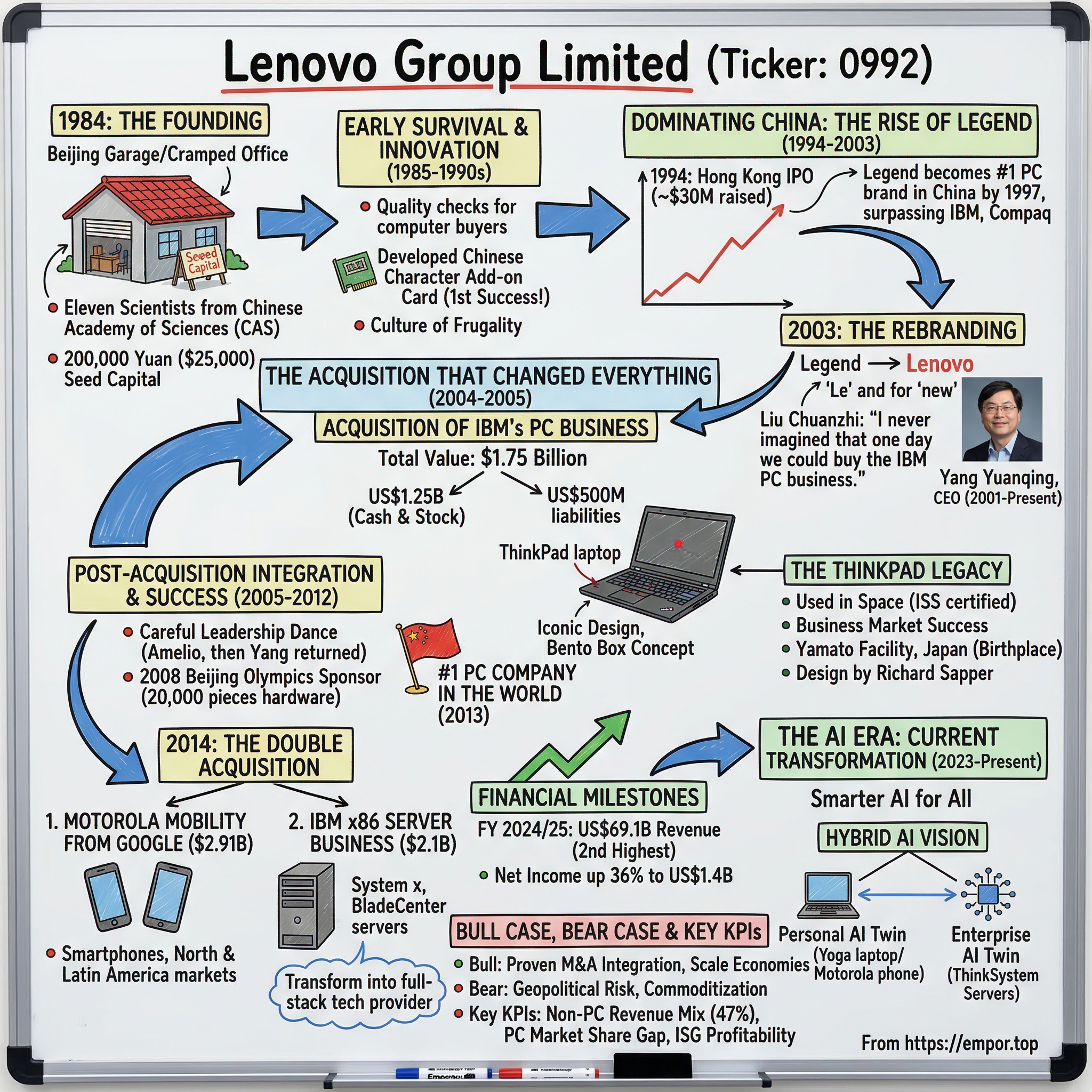

Picture this: It's 1984, and in a cramped 20-square-meter office in Beijing, eleven scientists from the Chinese Academy of Sciences pool together 200,000 yuan—roughly $25,000—to start a computer company. They have no business experience, no products, and in a country where entrepreneurship is still viewed with suspicion as bordering on immoral, they're betting their careers on an uncertain future. Fast forward four decades, and that modest startup has transformed into a $69 billion global technology powerhouse that ships more personal computers than any other company on Earth.

For the fiscal year 2024/25, Lenovo's revenue grew 21% year-on-year to US$69.1 billion, marking the Group's second-highest annual revenue in its history. In 2024, Lenovo led the global PC market with a 23.5% share, shipping 61.8 million units—a 4.7% increase from the prior year. This isn't just a story about market share and revenue figures. It's one of the most remarkable business narratives of the modern era—how a Chinese company, born from a government research institute, managed to acquire IBM's legendary PC business, integrate two vastly different cultures, and emerge as the undisputed global leader in personal computing.

The central question animating this story: How did eleven engineers with $25,000 from a Chinese government research institute end up acquiring IBM's legendary PC business and becoming the world's dominant computer maker?

"One of the great business stories of the last 10 years is how Lenovo, a Chinese company, was able to take IBM's PC unit and integrate it into its own, becoming a global technology powerhouse in the process. The story is one of the greatest case studies on how to merge massive international enterprises into a winning firm."

The themes that emerge from Lenovo's journey are instructive for any student of business strategy: the audacity to bet on M&A when organic growth isn't enough; the humility to let acquired talent lead; the discipline to integrate disparate cultures without destroying value; and the resilience to navigate geopolitical headwinds that would have sunk lesser companies. Today, as artificial intelligence reshapes the technology landscape, Lenovo finds itself at another inflection point—with non-PC revenue mix up nearly five points year-on-year to 47%—transforming from a hardware company into an AI-powered solutions provider.

II. The Origins: From Chinese Academy of Sciences to Legend (1984-1993)

The Founding Context

To understand Lenovo's origins, one must first understand the man who built it. Liu Chuanzhi (born 29 April 1944) is a Chinese entrepreneur and founder of Lenovo, the world's largest personal computer vendor by unit sales. Liu's path to entrepreneurship was anything but conventional. After graduating from high school in 1962, Liu applied to be a military pilot and passed all the associated exams. Despite his father's revolutionary credentials, Liu was declared unfit for military service because a relative had been denounced as a rightist. He entered the People's Liberation Army Institute of Telecommunication Engineering, now known as Xidian University, where due to his political and class background, he was assigned to study radar.

Liu was trained as an engineer at a military college and later went on to work at the Chinese Academy of Sciences. Like many young people during the Cultural Revolution, Liu was denounced and sent to the countryside where he worked as a laborer on a rice farm. This experience—the forced manual labor, the political persecution—shaped Liu's worldview and instilled in him both caution and ambition.

Liu Chuanzhi and his group of ten experienced engineers, teaming up with Danny Lui, officially founded Lenovo in Beijing on 1 November 1984, with 200,000 yuan. The Chinese government approved Lenovo's incorporation on the same day. Each of the founders was a member of the Institute of Computing Technology of the Chinese Academy of Sciences (CAS).

The founding came at a peculiar moment in Chinese history. Lenovo's founders, all scientists and engineers, faced difficulty from their lack of familiarity with market-oriented business practices, traditional Chinese ambivalence towards commerce, and anti-capitalist communist ideology. During this period many Chinese intellectuals felt that commerce was immoral and degrading. The fact that in the 1980s entrepreneurs were drawn from lower classes, and often dishonest as well, made the private sector even more unattractive. This was readily apparent to Liu and his collaborators due to their proximity to Zhongguancun, where the proliferation of fly-by-night electronics traders lead to the area being dubbed "Swindlers Valley."

Early Innovation & Survival

The early years were marked by failure and frugality. Their first significant transaction, an attempt to import televisions, failed. The group rebuilt itself within a year by conducting quality checks on computers for new buyers. Lenovo soon invested money in developing a circuit board that would allow IBM PCs to process Chinese characters.

This Chinese character add-on card became their first real product success—a modest innovation that solved a genuine problem. In a country where computing was exclusively the domain of foreign machines designed for Western alphabets, this circuit board opened the door to Chinese-language computing.

To save money during this period, Liu and his co-workers walked instead of taking public transportation. To keep up appearances, they rented hotel rooms for meetings. This culture of frugality—born of necessity—would later become a competitive advantage as Lenovo scaled.

In 1990, Lenovo started to manufacture and market computers using its own brand name. Some of the company's early successes included the KT8920 mainframe computer. It also developed a circuit board that allowed IBM-compatible personal computers to process Chinese characters.

Liu later reflected on the journey with characteristic understatement: "I remember the first time I took part in a meeting of IBM agents. I was wearing an old business suit of my father's and I sat in the back row. Even in my dreams, I never imagined that one day we could buy the IBM PC business."

III. Dominating China: The Rise of Legend (1994-2003)

Going Public and Market Leadership

The transformation from scrappy startup to domestic giant began in earnest with a crucial 1994 milestone. Legend listed on the Hong Kong Stock Exchange in 1994 and became the largest PC manufacturer in China and eventually in Asia; they were also domestic distributors for HP printers, Toshiba laptops, and others. Lenovo (known at the time as Legend) became publicly traded after a 1994 Hong Kong IPO that raised nearly US$30 million at HK$1.33 per share.

The IPO marked a transition from survival mode to growth mode. Legend's strategy was deceptively simple: combine local market knowledge with relentless focus on cost efficiency. While foreign competitors struggled with China's fragmented distribution landscape and unfamiliar consumer preferences, Legend built an extensive network that reached deep into second- and third-tier cities.

By 1997, Legend had achieved the unthinkable—Under Liu's leadership, Lenovo became the top PC brand in China by 1997, overtaking IBM and Compaq. For a domestic company to surpass the American giants who had invented the personal computer was nothing short of revolutionary.

The momentum continued. Lenovo brand PCs have been the best seller in China for seven consecutive years, commanding a 27.0 percent unit share of China's PC market in 2003. Lenovo PCs also ranked number one in the Asia Pacific (excluding Japan) market with a 12.6 percent market share in 2003.

The Rebranding: Legend to Lenovo

But dominance in China wasn't enough. Yang Yuanqing, who had risen through Legend's ranks with remarkable speed, had global ambitions. These qualities caught the attention of Liu Chuanzhi, who later promoted Yang to head Lenovo's personal computer business at just 29 years old. Yang was elevated to CEO of the whole company when Liu retired in 2001. Liu described Yang as "A man who moves forward, takes risks and aims to innovate."

In 1989, Yang joined Legend, as Lenovo was then known, at the age of 25. He was quickly promoted. Yang travelled to meet distributors throughout China and used his technical knowledge to achieve a strong sales record. Yang also stood out at Lenovo for being a quiet, deep thinker.

Yang was born on 12 November 1964 to parents both educated as surgeons. He spent his childhood in Hefei in Anhui province. He grew up poor, as his parents were paid the same salaries as manual laborers. Yang's father, Yang Furong, was a disciplined man with strict standards. Yang said of his father, "If he set a target, no matter what happened, he wanted to reach it." While his parents wanted him to pursue a career in medicine, and he had a budding interest in literature, Yang decided to study computer science on the advice of a family friend who was a university professor.

Yang's global ambitions hit an immediate roadblock: the Legend name was already trademarked in multiple international jurisdictions. It was renamed as Lenovo is 2003 amid a media blitz and large-scale branding campaign. The word is a portmanteau of the first two letters of the parent company's name and the Latin ablative for "new."

The rebranding wasn't cheap or quick. Lenovo spent over 200 million RMB on the effort—a massive investment that signaled its seriousness about going global. The question was: how would a Chinese company with no international presence become a true global competitor?

IV. The IBM PC Acquisition: The Deal That Changed Everything (2004-2005)

The Strategic Context

Prior to its acquisition of IBM's PC business in 2005, Lenovo ranked #9 in the worldwide PC industry with 2.3 percent market share and annual revenue of just $3 billion. To go from ninth to first through organic growth would take decades—time Lenovo didn't have as the global PC market consolidated around a handful of giants.

Meanwhile, IBM was wrestling with its own strategic dilemma. By 2004, IBM's business had changed, and it was looking to get out of the PC hardware business. So on May 1, 2005, IBM sold its PC business to Lenovo. The PC business that had once defined IBM had become a drag on the company's transformation into a services and software powerhouse.

Simply put, changing market dynamics and a new focus for IBM paved the way for the acquisition. IBM's PC business was experiencing significant challenges after the turn of the millennium. Heightened competition and an increasingly cramped market meant growth was slowing and revenue streams were drying up. For IBM, the future lay in enterprise solutions, particularly software and infrastructure, and under the leadership of CEO Samuel J. Palmisano took the company down a new path. As a 2012 Harvard Business Review article noted, Palmisano transformed IBM into a "globally integrated enterprise" – devices just weren't part of the equation.

The Deal Structure

The acquisition of IBM Personal Systems Group, the PC business arm of International Business Machines (IBM) Corporation, by Lenovo was announced on December 7, 2004, and was completed on May 3, 2005.

Under the terms of the transaction, Lenovo has paid IBM US$1.25 billion, comprised of approximately US$650 million in cash and US$600 million in Lenovo Group shares, based on the closing price on the last day of trading prior to the December 2004 announcement. IBM's ownership in Lenovo upon closing is 18.9 percent. Additionally, Lenovo will assume approximately US$500 million of net balance sheet liabilities from IBM.

The deal's total consideration of $1.75 billion transformed Lenovo overnight. Lenovo will have combined annual PC revenue of approximately US$12 billion and volume of 11.9 million units, based on 2003 business results — a fourfold increase in Lenovo's current PC business. Lenovo's new PC business will benefit from a powerful worldwide distribution and sales network covering 160 countries, global brand recognition through the combination of IBM's highly regarded "Think" brand notebook franchise and Lenovo's leading brand recognition in China.

In a transaction announced on March 31, 2005, Lenovo has agreed to the terms for a strategic investment of US$350 million from leading private equity investment firms Texas Pacific Group, General Atlantic Group and Newbridge Capital Group. Per the agreement, Lenovo will issue US$350 million worth of convertible preferred shares and unlisted warrants that can be converted into common shares of Lenovo.

The Security Review Drama

The deal immediately attracted scrutiny from Washington. A Chinese company acquiring a major American technology brand—one that supplied computers to the U.S. government—raised national security concerns. When Lenovo bought IBM's PC division in 2005, members of Congress openly fretted that the Chinese company would use its new asset to spy on American rivals – and the US government. One concern: IBM was (and still is) a major supplier of computers to the government. "Why would the US government be reliant on a Chinese company whose major shareholder is the Chinese government?" Rep. Don Manzullo told The Wall Street Journal. "That in itself sends a chill up and down the spines of members of Congress."

The deal was closed on May 3, 2005. Part of the deal included that Lenovo would move their global headquarters from Beijing to New York. This geographical compromise—headquarters in Purchase, New York, with principal operations in both Beijing and Raleigh, North Carolina—helped address some American concerns.

Skepticism and Execution

The business community was deeply skeptical. "At first, I was highly pessimistic about the success of this venture," noted analyst Tim Bajarin after being invited to Beijing to meet Lenovo's management team.

It turns out that Lenovo was able to coax most of IBM's top PC execs to join the new venture. They helped assure IBM's corporate customers as well as any consumers who bought their products that everything would be business as usual, and that Lenovo would honor all past warranties and service their needs well into the future. An initial hiccup came when some in the U.S. government were reluctant to give a Chinese company access to government data or contracts, but within a year the deal began to smooth out.

"Lenovo's success has to be credited to the hard work of the Chinese and American teams. The merging of these two business cultures alone is quite a feat. One thing I didn't expect is that the Chinese leadership took a hands-off approach to the U.S.-run PC company, fully trusting their leadership to keep the business moving forward. That was one of the assurances us analysts got during our trip to Beijing, but I wasn't sure that would hold true."

This hands-off approach—counterintuitive for many acquiring companies—proved to be Lenovo's masterstroke. By preserving IBM's operational autonomy while gradually integrating the businesses, Lenovo avoided the cultural clashes that have doomed so many cross-border acquisitions.

V. The ThinkPad Legacy & Integration Success (2005-2012)

What Lenovo Really Acquired

When Lenovo paid $1.75 billion for IBM's PC business, it wasn't just buying market share. It was acquiring an icon. ThinkPad is a line of business-oriented laptop and tablet computers produced since 1992. It was originally designed, created and manufactured by the American International Business Machines (IBM) Corporation. IBM sold its PC business to the Chinese company Lenovo in 2005 and since 2007 all ThinkPad models have been manufactured by them. The ThinkPad line was first developed at the IBM Yamato Facility in Japan; they have a distinct black, boxy design, which originated in 1990 and is still used in some models. Most models also feature a red-colored trackpoint on the keyboard, which has become an iconic and distinctive design characteristic associated with the ThinkPad line. It has seen significant success in the business market while certain models target students and the education market. ThinkPad laptops have been used in outer space and for many years were the only laptops certified for use on the International Space Station (ISS).

The design was based on the concept of a traditional Japanese bento lunchbox, which revealed its nature only after being opened. According to later interviews with Sapper, he also characterized the simple ThinkPad form to be as elementary as a simple, black cigar box and with similar proportions, with the same observation that it offers a 'surprise' when opened.

The ThinkPad's highly engineered innards — neatly segmented along the lines of a bento box, according to design chief David Hill — required an equally inspired exterior. Introduced in 1992, the ThinkPad marked a turning point for both the image of IBM and the prospects of mobile computing. With a simple design evocative of a black cigar box, a signature cursor pointing device, a vivid display and unprecedented processing power, the ThinkPad won favor among a rapidly expanding market of business travelers and became the world's most iconic notebook computer.

The ThinkPad represented something rare in the technology industry—a product with genuine brand loyalty. Business travelers swore by it. IT departments standardized on it. In 1993, PC Computing magazine gave its annual Most Valuable Product award to the 700C, calling it "a clear standout by its combination of speed, beauty, hard-nosed practicality and, yes, grace." The ThinkPad became a status symbol in both the C-suite and IT departments, selling more than USD 1 billion worth in its first year. It also supercharged IBM's PC business, which grew from USD 120 million a year to USD 3 billion within two years.

Leadership Evolution

The post-acquisition years saw a careful leadership dance. William Amelio served as the CEO and President of Lenovo from December 2005 to February 2009, tasked with overseeing the integration of IBM's PC business into Lenovo and driving the company's global growth. Under Amelio's leadership, Lenovo experienced revenue growth from $13 billion to $15 billion by 2008, expanded its brand internationally, and had sales profits greater than the market average for seven consecutive quarters. He implemented strategies to enhance Lenovo's operational efficiency and profitability, such as adopting Six Sigma practices. However, amid the global financial crisis, Lenovo posted a $97 million loss in Q4 2008, and Amelio's three-year contract was not renewed.

In early 2009, amid the global financial crisis and Lenovo's reported quarterly losses—including a pre-tax loss of US$90 million in the third quarter of fiscal 2008/09 with a gross margin of 9.8%—Yang was reappointed as chief executive officer on February 5, replacing Western executive William Amelio and restoring a Chinese-led management structure to address inefficiencies.

The Olympic Platform

Lenovo sponsored Beijing Olympics delivering 20,000 pieces of infrastructure and hardware; entered global consumer laptop and desktop markets; built ThinkPad X300, which BusinessWeek called "the best laptop ever" (2008).

The 2008 Beijing Olympics provided Lenovo with an unprecedented global stage. As the official computing equipment partner, the company demonstrated its capability to deliver on the world's largest sporting event—a powerful rebuttal to those who questioned whether a Chinese company could manage global-scale operations.

Rising to #1

The decade after the IBM acquisition validated every risk Lenovo had taken. Prior to its acquisition of IBM's PC business in 2005, Lenovo ranked #9 in the worldwide PC industry with 2.3 percent market share and annual revenue of just $3 billion. Fast forward to 2015 and Lenovo has risen to become #1 in worldwide PCs with market share at 20% and revenue growing roughly thirteen-fold over the past ten years to $39 billion.

In 2013, Lenovo became the world's largest personal computer vendor by unit sales for the first time, a position it still holds as of 2024. Yang Yuanqing was named to Barron's list of the world's best CEOs in 2013, 2014, and 2015, during a period when Lenovo under his leadership achieved significant market growth, including surpassing HP as the world's largest PC vendor by shipment volume in the second quarter of 2013 with a 16.7% market share compared to HP's 16.4%.

VI. The 2014 Double Acquisition: Motorola Mobility & IBM x86 Servers

The Motorola Mobility Acquisition

Emboldened by its success with IBM's PC business, Lenovo went shopping again in 2014—this time, making two major acquisitions within weeks of each other.

On January 29, 2014, Google announced it would, pending regulatory approval, sell Motorola Mobility to the Hong Kong based Chinese technology company Lenovo for US$2.91 billion in a cash-and-stock deal.

The context mattered: In May 2012, Google acquired Motorola Mobility for US$12.5 billion; the main intent of the purchase was to gain Motorola Mobility's patent portfolio, in order to protect other Android vendors from litigation. Google was selling Motorola for less than a quarter of what it paid—but it was keeping the patents it really wanted.

The total purchase price at close was approximately US$2.91 billion (subject to certain post-close adjustments), including approximately US$660 million in cash and 519,107,215 newly issued ordinary shares of Lenovo stock. The remaining US$1.5 billion will be paid to Google by Lenovo in the form of a three-year promissory note.

The transaction has satisfied all regulatory requirements and customary closing conditions, including clearance by competition authorities in the U.S., China, EU, Brazil and Mexico, and by the Committee on Foreign Investment in the United States (CFIUS). This is the fifth time since 2005 Lenovo has been cleared by CFIUS to acquire a U.S. business.

The IBM x86 Server Acquisition

Within days of announcing the Motorola deal, Lenovo struck again. Lenovo and IBM announced today that conditions for Lenovo's acquisition of IBM's x86 server business have been satisfied and the parties anticipate they will begin closing the transaction effective on October 1, 2014. The acquisition will make Lenovo the third-largest player in the $42.1 billion global x86 server market.

The purchase price is approximately US$ 2.1 billion. Approximately US$ 1.8 billion will be paid in cash at closing after estimated adjustments and approximately US$ 280 million will be paid in Lenovo stock.

Lenovo is acquiring System x, BladeCenter and Flex System blade servers and switches, x86-based Flex integrated systems, NeXtScale and iDataPlex servers and associated software, blade networking and maintenance operations. IBM will retain its System z mainframes, Power Systems, Storage Systems, Power-based Flex servers, PureApplication and PureData appliances.

Strategic Rationale

Lenovo's $2.91 billion purchase of Google's Motorola Mobility smartphone business, following its blockbuster $2.3 billion acquisition of IBM's x86 server business last week, means that customers can standardize on the Chinese manufacturer's platforms from PCs to servers to mobile phones. Boiled down it means Lenovo owns three critical end-points–and that alters the playing field quite a bit.

With this deal, Lenovo will not only be able to expand its current portfolio of handsets, add a rich heritage of mobile handset design, engineering and manufacturing expertise. Also gains Motorola's brand and access to key North America & Latin America markets. This instantly makes Lenovo almost the third largest smartphone player in the global smartphone segment competing head-on with Huawei.

The logic was compelling: transform from a PC company into a full-stack technology provider spanning devices, infrastructure, and services. The execution, as with the original IBM PC acquisition, would prove more challenging than the strategy.

VII. Navigating Geopolitics: The Security Challenges

The Ongoing Tension

Lenovo's success has come despite—or perhaps because of—relentless scrutiny from U.S. authorities and lawmakers. The company operates in one of the most geopolitically fraught spaces imaginable: a Chinese-origin technology company selling hardware to Western governments and corporations at a time of intensifying U.S.-China competition.

In 2006, the State Department said it would not use on classified networks 16,000 computers it had bought from Lenovo. The reason was security concerns. There was also an effort in 2011 to remove Lenovo hardware purchased for use at the Tobyhanna Army Depot in Pennsylvania, which was a site for IT repairs.

The accusations have continued. "[Lenovo's] links to state-run cyberespionage campaigns are well documented, and it is believed to have been complicit in installing Superfish spyware and potentially a BIOS backdoor on a number of its computer products," one congressional letter alleged. "We are concerned that [Chinese] actors could gain access to service members' sensitive personal information and exploit this access to compromise U.S. national security."

Lenovo's Defense

Lenovo has consistently and vigorously denied any connections to the Chinese government or military. "Lenovo is not affiliated with the People's Liberation Army in any way, is not invested in or controlled by the Chinese government or the Chinese Communist Party, and does not participate in or have links to Chinese state-run cyberespionage campaigns," a company spokesperson said. While Legend Holdings is a shareholder of Lenovo that owns a 36% stake, it only controls two out of 12 board seats and has no control over the company. Furthermore, Lenovo is a publicly traded company that adheres to global corporate governance requirements.

As a global and publicly traded company operating in 180 markets around the world, we continue to hold ourselves to the highest standards of transparency, corporate governance, and regulatory compliance and welcome all objective and professional assessments of our business, supply chain, and security practices. We've opened ourselves to 18 consecutive years of CFIUS audits which ensures we are a known and compliant entity to the U.S. government. Any suggestion that Lenovo is controlled by the Chinese government, or that our ties to China compromise our cybersecurity, is false. We have an international and independent board of directors and leadership team.

The Competitive Dimension

Perhaps more interesting than the security allegations themselves is Lenovo's claim about their origin. The article shines a spotlight on how a disinformation campaign secretly funded by our competitors is using front organizations like China Tech Threat to appear as real research and journalism. As Lenovo's Chief Security Officer outlined back in 2021, we were aware of detractors seeking to harm our business, but not the extent of the anti-competitive disinformation campaign waged against us. China Tech Threat repeatedly referred to reports that are outdated, unsubstantiated, or resolved years ago.

Responding to claims that Lenovo is a state-owned enterprise, CEO Yang Yuanqing said, "Our company is a 100% market oriented company. Some people have said we are a state-owned enterprise. It's 100% not true. In 1984 the Chinese Academy of Sciences only invested $25,000 in our company. The purpose of the Chinese Academy of Sciences to invest in this company was that they wanted to commercialize their research results. The Chinese Academy of Sciences is a pure research entity in China, owned by the government. From this point, you could say we're different from state-owned enterprises. Secondly, after this investment, this company is run totally by the founders and management team. The government has never been involved in our daily operation, in important decisions, strategic direction, nomination of the CEO and top executives and financial management."

Regardless of the merit of specific allegations, the geopolitical reality is that Lenovo must navigate a business environment where its Chinese heritage is viewed with suspicion in many Western markets—even as it operates what is arguably one of the most globally diverse technology companies in the world.

VIII. The AI Era: Lenovo's Current Transformation (2023-Present)

Financial Performance in the AI Age

For the full year 2024/25, revenue grew 21% year-on-year to US$69.1 billion, marking the Group's second-highest annual revenue in its history. Net income was up 36% year-on-year to US$1.4 billion on a non-Hong Kong Financial Reporting Standards basis. The Group's diversified growth engines continue to accelerate, with non-PC revenue mix up nearly five points year-on-year to 47%.

All business groups were healthy and strong and met their strategic intent and financial goals, and all sales geographies gained double-digit revenue growth year-on-year, reflecting the strength of the Group's diversified businesses and resilient global footprint.

CEO Yang Yuanqing stated: "This has been one of our best years yet, even in the face of significant macroeconomic uncertainty. We achieved strong top-line growth with all our business groups and sales geographies growing by double digits, and our bottom-line increased even faster. Our strategy to focus on hybrid AI has driven meaningful progress in both personal and enterprise AI, laying a strong foundation for leadership in this AI era. With 20 years of leading a global business and navigating challenges, I'm confident that our operational excellence and continued investment in innovation will not only sustain but strengthen our competitiveness."

AI PC Leadership Strategy

Lenovo is betting heavily on the AI PC transition. Lenovo expects the AI PC to represent approximately 80 percent of the PC industry landscape by 2027.

The company reported that AI PCs now make up more than 30% of their total PC shipments, and they claim a 31% market share in the global Windows AI PC segment. This is a powerful signal. It suggests that the promise of AI PCs is not just marketing hype; it's a tangible driver of sales, giving customers a real reason to upgrade their hardware.

Putting Lenovo's AI PC progress into perspective, so far in 2025, global AI PC penetration has hit roughly 5%. Lenovo's share of that is about 30%, and Rossi claims that the percentage will likely rise to 50% in a year or a year and a half.

Business Diversification

ISG delivered an almost 60% increase in revenue year-on-year for the quarter, achieving break-even with revenue of US$3.9 billion. The results were driven by continued hyper-growth in the Cloud Services Provider (CSP) business, as well as steady growth in the enterprise and SMB (E/SMB) business. Revenue from ISG's AI server business and industry-leading Lenovo Neptune liquid cooling solutions made strong contributions in the quarter, with AI server revenue growing steadily and Neptune expanding beyond supercomputing and academia to wider vertical industries. Looking ahead, ISG expects greater demand for hybrid infrastructure given the wider growth of AI, in particular demand for public clouds as well as on-premises data centers, private clouds, and edge computing.

AI benefited the SSG unit with hardware-attached services, although revenue from non-hardware systems and services remained SSG's strong profit engine, as it has been for 15 straight quarters. The company said more than 46 percent of its revenues now come from non-PC sources, meaning smartphones, infrastructure, and services, up from 42 percent a year ago.

The Hybrid AI Vision

Instead of fragmenting, Lenovo's effort has been unifying. Its "Smarter AI for All" vision is predicated on a "hybrid AI" model. The masterstroke of this strategy is its Personal AI Twin and Enterprise AI Twin concepts—persistent, learning AI models that represent you. It understands your workflow, manages your preferences, and proactively assists you. Crucially, it isn't tethered to your laptop, making Lenovo's ecosystem an existential threat to Dell. Lenovo, through its ownership of Motorola, has the very piece Dell is missing: a globally recognized smartphone brand. Lenovo's vision is an AI Twin that starts the day with you on your Motorola phone, seamlessly transfers to your Yoga laptop when you sit down at your desk, interacts with the ThinkPad at your office, and is backed by AI models running on Lenovo's own ThinkSystem servers in the cloud. Dell simply cannot compete with that vision.

IX. Bull Case, Bear Case & Competitive Analysis

Bull Case: The Integration Machine

The bull case for Lenovo rests on several pillars:

-

Proven M&A Execution: No company in tech history has demonstrated Lenovo's ability to acquire Western technology assets and successfully integrate them. The IBM PC deal was supposed to fail—it became a case study in how to do cross-border M&A right. This institutional capability is a genuine competitive advantage.

-

Scale Economics: Lenovo led the global PC market with a 23.5% share in 2024, shipping 61.8 million units. In a volume business with thin margins, scale matters enormously for procurement leverage, R&D efficiency, and channel relationships.

-

AI Transition Timing: The Windows 10 end-of-support in October 2025, combined with emerging AI PC capabilities, creates a potential upgrade super-cycle that plays to Lenovo's strengths in commercial accounts.

-

Ecosystem Integration: Unlike Dell (no mobile), or HP (limited infrastructure), Lenovo spans devices, smartphones (via Motorola), servers, storage, and services—positioning it uniquely for enterprise AI deployments that touch all layers of the stack.

Bear Case: Structural Challenges

The bear case is equally compelling:

-

Geopolitical Risk: The ongoing U.S.-China tensions represent an existential threat to Lenovo's business model. Further restrictions on Chinese technology companies could materially impact revenue, particularly in government and defense verticals.

-

Commoditization Pressure: PCs remain a commodity business where brand loyalty is weak and switching costs are low. HP retained its somewhat distant second position with 53.0 million shipments, growing 0.1%, while Dell shipped 39.1 million units—the competition remains fierce.

-

Infrastructure Business Struggles: Lenovo's full year results for FY24 saw ISG report a nine percent retreat in revenue to $8.9 billion and a $248 million loss. The business unit made a $93 million profit in the previous year. The foundation of the ISG is the IBM x86 server business that Lenovo acquired in 2014 – a move the PC builder hoped would propel it from its existing desktop business into more lucrative datacenter sales.

-

Mobile Margins: While Motorola provides strategic value for ecosystem completeness, it operates in an even more brutally competitive market than PCs.

Porter's Five Forces Analysis

-

Threat of New Entrants (Low): The PC and server markets require massive scale, established supply chains, and brand recognition. Barriers to entry are substantial.

-

Bargaining Power of Suppliers (Moderate): Intel, AMD, and Nvidia hold significant power as key component suppliers. However, Lenovo's scale provides negotiating leverage.

-

Bargaining Power of Buyers (High): Enterprise customers have significant leverage and can easily switch between major vendors. Consumer price sensitivity is high.

-

Threat of Substitutes (Moderate to High): Smartphones and tablets continue to cannibalize some PC use cases. Cloud computing reduces server hardware needs.

-

Competitive Rivalry (Very High): Dell, HP, Apple, and numerous Asian competitors fight intensely for share in a slowly growing market.

Hamilton Helmer's 7 Powers Framework

-

Scale Economies: Lenovo benefits from procurement leverage and manufacturing efficiency across 60+ million annual PC shipments.

-

Network Effects: Limited in hardware, but potentially emerging in ecosystem play (devices + infrastructure + services).

-

Counter-Positioning: Lenovo's willingness to integrate Chinese and Western operations distinguishes it from both American competitors (unable to leverage Chinese manufacturing as deeply) and Chinese competitors (lacking global brand credibility).

-

Switching Costs: Low for consumers; moderate for enterprise customers with standardized IT environments (particularly ThinkPad-heavy deployments).

-

Branding: ThinkPad remains one of tech's most valuable brands in the enterprise segment.

-

Cornered Resource: The Yamato R&D facility in Japan (birthplace of ThinkPad) represents unique engineering capabilities.

-

Process Power: Lenovo's M&A integration capabilities represent genuine process know-how that competitors cannot easily replicate.

X. Key KPIs for Investors

For investors tracking Lenovo's ongoing performance, three metrics stand out as most critical:

-

Non-PC Revenue Mix: Currently at 47%, this metric captures Lenovo's success in diversifying beyond its core PC business into higher-margin infrastructure and services. The company's stated goal is to continue growing this percentage, which insulates the business from PC market cyclicality.

-

PC Market Share Gap vs. #2: IDG gained a top 24.3 percent share of the PC business, almost five points clear of the number-two player (Dell), its highest share in 5 years. Maintaining and expanding this lead demonstrates competitive positioning and scale advantages.

-

Infrastructure Solutions Group (ISG) Profitability: ISG delivered an almost 60% increase in revenue year-on-year for the quarter, achieving break-even. The turnaround of this business—after years of losses—is essential for Lenovo's enterprise ambitions. Sustained profitability here would validate the 2014 server acquisition and demonstrate Lenovo can compete beyond PCs.

XI. Conclusion: The Next Forty Years

From a cramped Beijing office in 1984 to a $69 billion global technology leader in 2025, Lenovo's journey represents one of the most remarkable business stories of the past half-century. The company has defied skeptics at every turn—those who said Chinese companies couldn't compete globally, those who said the IBM acquisition would fail, those who said the PC market was dying.

At a 2012 award ceremony, Yang said, "I have a dream that Lenovo will become the pride of China in the IT industry. Lenovo is my life's struggle and career, I have invested all of my energy into it. I firmly believe that Lenovo, a product of China, will stand atop the world's stage."

That dream has been realized—and then some. The question now is whether Lenovo can navigate the AI transition while managing unprecedented geopolitical complexity. The company's track record suggests investors should not underestimate its ability to adapt, integrate, and grow.

But risks remain substantial. The U.S.-China technology decoupling shows no signs of abating. The AI infrastructure market is fiercely competitive. And transformation from a hardware company to a solutions provider is never guaranteed to succeed.

What seems certain is that Lenovo will continue to occupy a unique position in the global technology landscape—neither purely Chinese nor fully Western, drawing on both heritages while belonging completely to neither. In a world increasingly defined by technological nationalism, that may be either Lenovo's greatest vulnerability or its most distinctive strength.

Key Metrics Summary

| Metric | FY 2024/25 |

|---|---|

| Total Revenue | US$69.1 billion |

| Net Income (non-HKFRS) | US$1.4 billion |

| Revenue Growth YoY | 21% |

| Non-PC Revenue Mix | 47% |

| Global PC Market Share | ~24% |

| IDG Revenue | US$13.8 billion (Q3) |

| ISG Revenue | US$3.9 billion (Q3) |

| SSG Revenue | US$2.3 billion (Q3) |

| R&D Investment (Q3) | US$621 million |

| Employees | ~77,000 |

| Markets Served | 180 |

Leadership Timeline

| Period | CEO | Notable Events |

|---|---|---|

| 1984-2001 | Liu Chuanzhi | Founding, IPO, China market leadership |

| 2001-2004 | Yang Yuanqing | Rebranding to Lenovo, IBM negotiations |

| 2004-2005 | Stephen M. Ward Jr. | IBM PC integration |

| 2005-2009 | William Amelio | Global expansion, financial crisis |

| 2009-Present | Yang Yuanqing | #1 PC position, Motorola/Server acquisitions, AI transformation |

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube