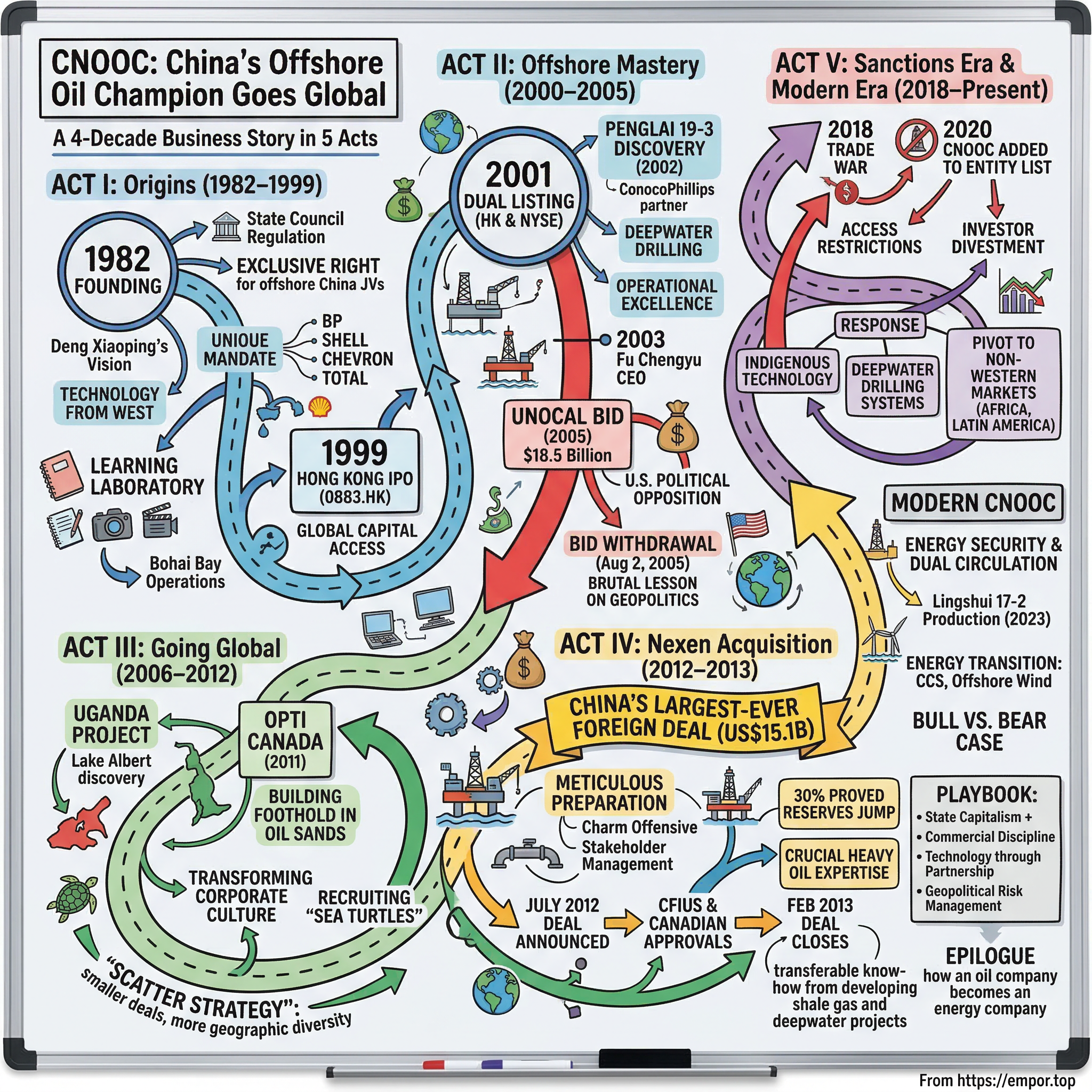

CNOOC: China's Offshore Oil Champion Goes Global

I. Introduction & Episode Roadmap

Picture this scene: It's July 2012, and in the gleaming boardrooms of Calgary's corporate towers, executives at Nexen Inc. are weighing an offer that would make history. On the table: $15.1 billion in cash from a Chinese state-owned oil company most Canadians had never heard of. The premium? A staggering 61% above Nexen's stock price. This wasn't just another energy deal—it was China's largest offshore oil and natural-gas explorer paying $27.50 for each common share, making it the biggest overseas takeover by a Chinese company.

The company making this audacious bid was CNOOC Limited, and its journey from a fledgling state enterprise founded in the early days of China's economic reforms to a $100 billion global energy powerhouse encapsulates one of the most dramatic transformation stories in modern business history.

Here's the paradox that makes CNOOC fascinating: Among China's three oil giants—CNPC, Sinopec, and CNOOC—it was always the "baby," the smallest, the one with the most limited domestic resources. Through its parent company, it has exclusive rights to partner with foreign companies in offshore China projects, but that monopoly came with a catch: China's offshore fields were technically challenging and required expertise the country didn't possess. Yet somehow, this constraint became CNOOC's greatest strength, forcing it to become the most internationally minded, technologically sophisticated, and commercially aggressive of China's energy champions.

What you're about to discover is how a company born from Deng Xiaoping's vision of opening China to the world became a master class in state capitalism—learning from Western partners, acquiring cutting-edge technology, and ultimately challenging those same partners on the global stage. It's a story of geopolitical chess moves, multi-billion dollar gambles, and the delicate dance between commercial ambition and national strategy.

We'll trace CNOOC's evolution through five distinct acts: from its origins as China's designated offshore explorer, through its failed attempt to buy America's Unocal (a defeat that taught it invaluable lessons about Western politics), to its eventual triumph with Nexen, and finally to its current position navigating sanctions, energy transition pressures, and its role in China's quest for energy security.

Along the way, we'll explore fundamental questions: Can a state-owned enterprise truly operate by market principles? How does a company balance shareholder returns with national strategic objectives? And what happens when energy security collides with geopolitical tensions?

II. Origins: China Opens Up (1982–1999)

The rain was coming down in sheets on that February morning in 1982 when a small group of Chinese officials gathered in Beijing to sign documents that would fundamentally reshape China's energy landscape. When the State Council implemented the regulation on petroleum resources in cooperation with foreign enterprises on January 30, 1982, CNOOC was incorporated and authorized to assume overall responsibility for the exploitation of oil and gas resources of offshore China in cooperation with foreign partners, which ensured monopoly status for CNOOC in offshore oil and natural gas.

This wasn't just another bureaucratic reorganization. It was Deng Xiaoping's strategic masterstroke—a carefully designed gateway for Western technology to flow into China while maintaining state control over critical resources. The timing was no accident. Deng had just consolidated power after the tumultuous Cultural Revolution, and his reforms were gaining momentum. Economic reforms began in earnest during the "Boluan Fanzheng" period, especially after Deng and his reformist allies rose to power with Deng replacing Hua Guofeng as the paramount leader in December 1978.

The genius of CNOOC's creation lay in its unique mandate. Unlike CNPC, which controlled onshore resources, or Sinopec, which dominated refining, CNOOC was given something seemingly less valuable: the right to explore China's offshore waters. But here's what the planners understood: offshore drilling required advanced technology China didn't have. By giving CNOOC monopoly rights to partner with foreign companies, they created a learning laboratory.

The early days were humble, almost comically so. CNOOC's first headquarters was a repurposed hotel in Beijing, its staff a mix of petroleum engineers transferred from other ministries and young graduates who barely knew the difference between a drill bit and a drill pipe. The company's first CEO, Qin Wencai, was a petroleum veteran who understood that CNOOC's success depended not on competing with Western oil majors but on making them partners.

And partners came calling. BP was among the first, followed by Shell, Chevron, and Total. These weren't charity missions—China's offshore basins, particularly the Bohai Bay near Beijing and the South China Sea, showed promising geology. But the production-sharing contracts CNOOC negotiated were masterpieces of asymmetric learning. Foreign companies brought technology and expertise; CNOOC provided access and absorbed knowledge like a sponge.

Consider the Bohai Bay operations in the mid-1980s. When Chevron's engineers arrived to drill the first exploratory wells, they found their CNOOC counterparts taking detailed notes on everything—from drilling mud compositions to crew shift patterns. One Chevron executive later recalled: "They photographed our equipment from every angle, asked questions about things we took for granted, like why we torqued bolts in a specific sequence. We thought they were just being thorough. They were building a university."

By the early 1990s, this learning strategy was paying dividends. CNOOC engineers weren't just observing anymore; they were making improvements. When Phillips Petroleum encountered unexpected high-pressure zones in the Xijiang field, it was a young CNOOC engineer who suggested a modified well design that solved the problem. The Western partners began to realize they weren't just training potential competitors—they were creating them.

The Asian Financial Crisis of 1997-1998 became CNOOC's crucible moment. As currencies collapsed across Southeast Asia and capital fled emerging markets, China's leadership faced a choice: retreat into protectionism or double down on market reforms. For CNOOC, the crisis presented an unexpected opportunity. The company was incorporated in 1999 and is based in Hong Kong. By 1999, CNOOC was incorporated in Hong Kong and subsequently became publicly traded on the Hong Kong Stock Exchange under the stock code 0883.HK.

The decision to incorporate in Hong Kong rather than mainland China was deliberate and revealing. Hong Kong offered access to international capital markets, a familiar legal framework for Western investors, and—critically—a degree of operational independence from Beijing's day-to-day political interference. This structure would become CNOOC's secret weapon: Chinese when it needed to be, international when it suited its purposes.

As the 1990s drew to a close, CNOOC had transformed from a novice player learning from Western partners to a competent operator running its own offshore platforms. Production from Bohai Bay was ramping up, early exploration in the South China Sea showed promise, and the company had built a technical team that could hold its own with international peers. The student was ready to graduate.

III. The Offshore Mastery Phase (2000–2005)

The turn of the millennium marked CNOOC's coming-out party. On February 27-28, 2001, in a carefully orchestrated dual listing, CNOOC Limited raised $1.4 billion on the Hong Kong and New York stock exchanges. The company's initial public offering raised approximately US$3 billion at that time, making it one of the largest IPOs in Asia. The roadshow had been a revelation—Western fund managers, initially skeptical of a Chinese state-owned enterprise, were won over by CEO Wei Liucheng's presentation: disciplined capital allocation, transparent governance, and production growth that would make any Houston-based independent envious.

The IPO proceeds immediately went to work. CNOOC embarked on an aggressive drilling campaign in Bohai Bay that would have seemed like science fiction just a decade earlier. The company wasn't just drilling more wells; it was pushing the technical envelope. In 2002, the Penglai 19-3 field discovery in Bohai Bay proved to be a game-changer—China's largest offshore oil field at the time, with reserves exceeding 1 billion barrels.

But here's where CNOOC showed its evolving sophistication: instead of developing Penglai alone, it brought in ConocoPhillips as a partner, not because it needed the capital or technology anymore, but because it wanted to learn best practices for managing a field of this scale. The partnership was structured so that CNOOC engineers were embedded in every aspect of the development, from reservoir modeling to platform construction.

The real technical leap came with deepwater drilling. China's offshore geology presented a cruel irony—the most promising reserves lay in deep waters that required technology CNOOC didn't yet possess. In 2003, the company made a strategic decision that would define its future: it would leapfrog intermediate steps and go straight for ultra-deepwater capability.

The company produces offshore crude oil and natural gas primarily in Bohai, the Western South China Sea, the Eastern South China Sea, and the East China Sea in offshore China. It also holds interests in various oil and gas assets in Asia, Africa, North America, South America, Oceania, and Europe. This wasn't just about drilling deeper; it was about mastering the entire value chain—from seismic interpretation in complex geology to managing production facilities in typhoon-prone waters.

The company's engineers developed an almost obsessive culture around safety and operational excellence. When a minor gas leak occurred on a platform in 2003, CNOOC didn't just fix it—they conducted a systematic review of every valve, fitting, and weld across their entire offshore infrastructure. This attention to detail earned grudging respect from Western partners who had initially viewed Chinese operators as cutting corners.

By 2004, CNOOC was hitting its stride. Production had reached 500,000 barrels of oil equivalent per day, the company was generating substantial free cash flow, and its technical capabilities were approaching international standards. Management, led by the ambitious Fu Chengyu who became CEO in 2003, began looking beyond China's waters.

Then came the Unocal opportunity.

In early 2005, Unocal Corporation—a mid-sized American oil company with attractive Asian assets—announced it was for sale. For Fu Chengyu, this was the perfect target: Unocal's oil and gas properties in Thailand, Indonesia, and Myanmar would complement CNOOC's offshore expertise, while its technical teams could accelerate CNOOC's deepwater learning curve.

In April 2005, Chevron made an offer to acquire Unocal for US$16.6 billion, which was followed, after the companies had agreed to the transaction, by a competing unsolicited bid from the Chinese firm CNOOC Limited of US$18.5 billion on June 22. CNOOC's all-cash offer represented a 67% premium to Chevron's initial bid—a stunning display of financial firepower that shocked American boardrooms.

But CNOOC had catastrophically misread the political environment. Within days of the bid's announcement, American politicians across the spectrum erupted in opposition. The Chinese offer had sparked considerable resistance from members of Congress, who worried that the Chinese buyout would compromise national security. Representative Joe Barton called it an attempt by "a front company for the communist Chinese to purchase a strategic asset." The rhetoric grew increasingly heated, with some lawmakers suggesting CNOOC's acquisition would threaten American energy security and transfer sensitive deepwater drilling technology to China's military.

In response to potential objections, CNOOC stated that it was fully prepared to participate in a CFIUS review of the transaction and had made assurances to Unocal to "address concerns relating to energy security and ownership of Unocal assets located in the United States." CNOOC was prepared to sell or take other actions with respect to Unocal's minority pipeline interests and storage assets. The company even offered to maintain all American employees and place U.S. assets under American management.

But the political tide was unstoppable. Congressional opponents managed to insert a requirement into new energy legislation that would have forced a four-month impact study of the Chinese takeover. The delays and uncertainty made the deal untenable.

On August 2, 2005, CNOOC withdrew its bid. In a strongly worded statement, Hong Kong-based CNOOC said it might have raised its bid even higher, if not for the political backlash. "The unprecedented political opposition...was regrettable and unjustified," CNOOC said.

The Unocal failure was a searing experience for CNOOC's leadership. Fu Chengyu returned to Beijing humiliated but educated. The company had learned a brutal lesson about the intersection of energy and geopolitics. In internal meetings following the withdrawal, Fu reportedly told his team: "We understood oil and gas, we understood finance, but we didn't understand America."

IV. Going Global: The International Expansion (2006–2012)

The scars from Unocal ran deep, but they also catalyzed a fundamental strategic shift. If CNOOC couldn't buy its way into the American energy market, it would go everywhere else—Africa, Southeast Asia, Canada, South America. The company adopted what internally became known as the "scatter strategy": smaller deals, less political visibility, more geographic diversity.

Uganda became the unlikely launching pad for CNOOC's African ambitions. Waraga-1 test commenced 22nd June 2006 and flowed at a combined rate in excess of 12,000 bopd. This was the first flow of oil to surface in Uganda and East Africa. The discovery at Lake Albert wasn't just oil—it was validation that CNOOC could operate successfully in frontier markets.

The Uganda project showcased a different CNOOC, one that had learned from Unocal. Instead of swooping in with a massive acquisition, the company partnered with Tullow Oil and Total, taking a minority stake initially and gradually increasing its presence. CNOOC's engineers worked alongside local teams, training Ugandan technicians while adapting to operating conditions that were radically different from offshore China—think blazing heat, limited infrastructure, and complex stakeholder management involving local communities, environmental groups, and government officials at multiple levels.

Meanwhile, in Canada, CNOOC was quietly building a foothold in the oil sands. In 2011, Chinese oil company CNOOC Ltd. agreed to purchase struggling Calgary-based oilsands producer Opti Canada Inc. for $2.1 billion US. The troubled Long Lake oilsands project has found new backing in a Chinese suitor. The OPTI acquisition was strategically brilliant—a distressed asset that wouldn't trigger political antibodies, yet provided CNOOC with critical oil sands expertise and a 35% stake in the Long Lake project.

What made the OPTI deal particularly clever was its structure. Rather than a hostile takeover, CNOOC positioned itself as a white knight, rescuing a bankrupt Canadian company and preserving local jobs. "CNOOC Ltd. is a technically experienced and well-capitalized company that is equipped to support further development at Long Lake and future expansions in the Canadian oil sands," said Opti president and CEO Chris Slubicki.

Throughout this period, CNOOC was also transforming its corporate culture. The company began recruiting Western-educated Chinese nationals who could navigate both worlds. These "sea turtles" (as Chinese who studied abroad and returned were called) brought not just technical knowledge but cultural fluency. They could negotiate with Houston lawyers in the morning and Beijing bureaucrats in the afternoon.

The company's operational performance during these years was remarkable. By 2010, production had surpassed 800,000 barrels of oil equivalent per day, with international assets contributing nearly 30%. More importantly, CNOOC had developed genuine technical expertise in areas like deepwater drilling, where it was now competing for acreage against Western majors on equal terms.

The financial metrics told a compelling story: return on equity consistently above 20%, finding and development costs below $15 per barrel, and a balance sheet strong enough to fund major acquisitions without dilution. Wall Street analysts, initially skeptical of Chinese corporate governance, grudgingly admitted that CNOOC was one of the best-run oil companies globally.

But Fu Chengyu, still CEO and still smarting from Unocal, wanted a defining transaction—something that would announce CNOOC's arrival as a truly global player. Throughout 2011 and early 2012, investment bankers pitched various opportunities. Most were too small, too risky, or too politically sensitive.

Then Nexen appeared on the radar.

Nexen was perfect: a mid-sized Canadian independent with world-class assets in the North Sea, Gulf of Mexico, and West Africa. It had cutting-edge deepwater expertise, exactly what CNOOC needed. And critically, it was Canadian—a country that, unlike the United States, had historically been open to Chinese investment.

The approach to Nexen was methodical, almost surgical in its precision. CNOOC had learned from Unocal not to surprise anyone. Months before any formal offer, CNOOC's representatives were in Ottawa, meeting with government officials, addressing concerns, making commitments about jobs and investment. They hired the best Canadian law firms, brought in public relations experts who had worked on previous Chinese investments in Canada, and most importantly, secured Nexen management's support before going public.

V. The Nexen Acquisition: China's Largest Foreign Deal (2012–2013)

The call came at 3 AM Beijing time on July 23, 2012. Fu Chengyu, unable to sleep, was already in his office when the phone rang. "It's done," said the voice from Calgary. "The Nexen board has approved. We're announcing in three hours."

China's largest offshore oil and natural-gas explorer is paying $27.50 for each common share, a premium of 61 percent to Calgary-based Nexen's closing price on July 20. Nexen's board recommended the deal to its shareholders. The numbers were staggering: CNOOC's acquisition of Nexen was completed on February 25, 2013. Total consideration of approximately US$15.1 billion has been paid for Nexen's common and preferred shares.

But the real story wasn't the price—it was the execution. CNOOC had assembled a dream team for this transaction. Leading the charge was Wang Yilin, CNOOC's chairman, a petroleum engineer turned diplomat who understood that this deal would be won or lost in the political arena, not the boardroom.

The company's preparation was meticulous. CNOOC's success in navigating the CFIUS approval process "is likely to be viewed as a positive development," said Joshua Zive, senior counsel at Bracewell & Guiliani. They had learned from Unocal that technical merit meant nothing if the politics were wrong.

The charm offensive began immediately. Unlike the Unocal bid, where CNOOC executives remained largely invisible, this time they were everywhere—op-eds in Canadian newspapers, meetings with labor unions, presentations to environmental groups. The message was consistent: CNOOC wasn't coming to strip assets and ship them to China; it was investing in Canada's future.

At the outset, CNOOC had tried to assuage nationalist anxieties. It had accepted management and employment conditions set by the government, agreed to list its shares on the Toronto Stock Exchange, said that Calgary would be its North American hub and that it would maintain Nexen staffing and capex levels.

The technical fit was compelling. Macquarie's oil and gas analysts described the "strategic fit" of the Nexen acquisition as "overwhelmingly compelling". They pointed to a better balance to CNOOC's upstream portfolio, the bigger scale of its operations, an extension of its reserves life, a cash-cow base from the UK North Sea and the material presence that CNOOC would have at every step in a trans-Pacific integrated LNG chain. The company would also have a springboard into Africa and would gain transferable know-how from developing shale gas and deepwater projects.

What CNOOC really bought went far beyond reserves and production. Nexen's Buzzard field in the North Sea was one of the most technically complex offshore developments in the world—experience directly applicable to China's own deepwater ambitions. The Long Lake oil sands project, despite its troubles, provided crucial heavy oil expertise. And Nexen's positions in the Gulf of Mexico gave CNOOC a front-row seat to the world's most advanced deepwater plays.

The regulatory approval process was a masterclass in stakeholder management. In Canada, Endorsement by the Canadian industry ministry and Prime Minister Stephen Harper on Friday came after months of argument in Canada and concern in the US. But CNOOC had done its homework.

The real test came with U.S. approval. Nexen had significant Gulf of Mexico assets, meaning CFIUS review was mandatory. This time, CNOOC was ready. Nexen said that CFIUS had given the green light and that it expects the deal to close the week of Feb. 25, seven months after China's top offshore oil and natural gas producer made its bid.

The contrast with Unocal couldn't have been starker. Where that bid triggered congressional hearings and xenophobic rhetoric, Nexen proceeded relatively smoothly. Part of this was timing—by 2012, Chinese investment in North America had become more common. But mostly it was CNOOC's sophisticated approach. They had learned to speak the language of Western capitalism while never forgetting they represented Chinese interests.

On February 25, 2013, the deal closed. Fu Chengyu, who had overseen the entire process, permitted himself a rare moment of public emotion. At the closing ceremony in Calgary, he said: "This isn't just a transaction. It's a bridge between East and West, a model for how Chinese companies can be responsible global citizens."

The numbers validated the strategy. The acquisition closed in February 2013; representing China's largest-ever foreign acquisition. Post-Nexen, CNOOC's proved reserves jumped by 30%, production increased by 20%, and most importantly, the company had acquired capabilities that would have taken decades to develop organically.

VI. The Sanctions Era: Geopolitical Headwinds (2018–2021)

The celebration over Nexen was still fresh when the geopolitical weather began to change. The first warning signs came in 2018 with the U.S.-China trade war, but few at CNOOC anticipated how dramatically their fortunes would shift.

By 2020, the company that had spent two decades cultivating Western partnerships found itself in the crosshairs of Washington's new Cold War with Beijing. The Trump administration's perspective was blunt: Chinese state-owned enterprises were not commercial entities but extensions of the Communist Party's power.

The Trump administration is poised to add China's top chipmaker SMIC and national offshore oil and gas producer CNOOC to a blacklist of alleged Chinese military companies, according to a document and sources, curbing their access to U.S. investors and escalating tensions with Beijing weeks before President-elect Joe Biden takes office. Reuters reported earlier this month that the Department of Defense (DOD) was planning to designate four more Chinese companies as owned or controlled by the Chinese military, bringing the number of Chinese companies affected to 35. A recent executive order issued by President Donald Trump would prevent U.S. investors from buying securities of the listed firms starting late next year.

The designation was devastating in its simplicity. CNOOC was added to the Entity List, a tool utilized by Commerce's Bureau of Industry and Security (BIS) to restrict the export, re-export, and transfer (in-country) of items to persons reasonably believed to be involved in activities contrary to the national security or foreign policy interests of the United States.

The official justification was CNOOC's activities in the South China Sea. According to the Department of Commerce, "CNOOC has repeatedly harassed and threatened offshore oil and gas exploration and extraction in the South China Sea, with the goal of driving up the political risk for interested foreign partners, including Vietnam".

Inside CNOOC's Beijing headquarters, the sanctions triggered soul-searching and scrambling in equal measure. The immediate impact was dramatic: CNOOC, on the other hand, is believed to be one of the earliest Chinese state-owned enterprises to have taken a hit from Washington, having also been added to a Pentagon blacklist in 2021. American institutional investors, who held approximately 16% of CNOOC's Hong Kong-listed shares, were forced to divest.

But the real damage went beyond share prices. Suddenly, CNOOC's carefully cultivated Western partnerships were toxic. American service companies like Halliburton and Schlumberger faced restrictions on providing technology and equipment. Joint ventures in the Gulf of Mexico came under scrutiny. Even routine commercial transactions required legal review.

The company's response revealed how much it had evolved since its founding. Instead of retreating into economic nationalism, CNOOC doubled down on commercial pragmatism. Management's message to employees was clear: "We are not politicians. We are an energy company. Our job is to find oil and gas efficiently and safely."

Behind the scenes, CNOOC accelerated efforts to develop indigenous technology. If American companies wouldn't sell them advanced drilling equipment, they would build it themselves. The company established research partnerships with Chinese universities, recruited overseas Chinese engineers, and poured billions into R&D.

The results were impressive. Within two years, CNOOC had developed its own deepwater drilling systems, seismic processing software, and even specialized drilling fluids that had previously been sourced from Western suppliers. The irony wasn't lost on industry observers: sanctions designed to cripple CNOOC had instead accelerated its technological independence.

The period also saw CNOOC pivot more decisively toward non-Western markets. In Africa, the company expanded its presence in Uganda, Nigeria, and Gabon. In Latin America, it acquired assets in Brazil and Guyana. The message was clear: if the West didn't want Chinese investment, others would gladly take it.

VII. Modern Era: Energy Security & The Dual Circulation Strategy (2021–Present)

Today's CNOOC is a study in contradictions—a commercial enterprise that must serve national interests, a global company operating in an increasingly fragmented world, an oil producer talking about carbon neutrality. Understanding modern CNOOC requires grasping China's "dual circulation" strategy: developing domestic capabilities while maintaining selective international engagement.

The numbers tell a story of resilience. Production for 2020 averaged 1.44 million barrels of oil equivalent per day (79% oil), and year-end proven reserves were 5.37 billion barrels of oil equivalent, or boe, (73% oil). Despite sanctions and geopolitical headwinds, CNOOC has maintained its position as a major global energy player.

The company's domestic operations have reached new technical heights. In 2023, CNOOC announced first production from Lingshui 17-2, China's first 1,500-meter ultra-deepwater gas field. The project, entirely developed with Chinese technology, would have been impossible without the decades of learning from Western partners—a perfect encapsulation of CNOOC's journey.

But perhaps the most intriguing development is CNOOC's approach to the energy transition. CNOOC Limited (the "Company", SEHK: 00883, SSE: 600938) today announces the official commissioning of China's first offshore CCS demonstration project. The company is experimenting with offshore wind, utilizing its marine engineering expertise for renewable energy. It's developing carbon capture and storage projects, leveraging its understanding of subsurface geology.

The international strategy has evolved too. The crown jewel remains the Uganda project, where At peak plateau, upstream partners—TotalEnergies (56.67%), CNOOC (28.33%), and UNOC (15%)—expect to produce 230,000 B/D basinwide. The East African Crude Oil Pipeline, despite environmental opposition, represents CNOOC's ability to execute complex international projects even in a hostile geopolitical environment.

Meanwhile, CNOOC Limited announces today that Buzios5 Project has commenced production safely. The Brazilian deepwater project showcases CNOOC's technical capabilities—operating in 2,000 meters of water in one of the world's most challenging offshore environments.

The financial performance remains robust. CNOOC is highly regarded as one of the best oil price proxies, with a very competitive all-in cost of ~USD30/bbl and a steady growth strategy. The company's ability to generate profits at $30 per barrel gives it remarkable resilience in volatile oil markets.

For investors, CNOOC presents a unique proposition. The stock offers a very attractive dividend yield of 7% with management committed to a payout of at least 45% during 2025-2027. This combination of growth and income, rare among international oil companies, reflects CNOOC's confidence in its business model.

VIII. Playbook: The CNOOC Model

After four decades, CNOOC has developed a distinctive playbook that offers lessons for both state-owned enterprises and private companies operating in complex geopolitical environments.

State Capitalism with Commercial Discipline: CNOOC proves that state ownership doesn't necessarily mean inefficiency. The company operates with the financial discipline of a private corporation while maintaining the long-term perspective that state backing provides. Investment decisions are based on economic returns, not political considerations—at least most of the time.

Technology Acquisition Through Partnership: CNOOC's greatest innovation wasn't technical but strategic: using joint ventures as universities. Every partnership was structured to maximize learning. Western companies got access to Chinese resources; CNOOC got access to Western knowledge. Over time, the student became the master.

The "Going Out" Strategy: CNOOC embodies China's "going out" policy—not as crude resource grab but as sophisticated portfolio construction. The company's international assets provide diversification, technical learning, and strategic options. When Western markets closed, CNOOC had alternatives.

Capital Allocation Excellence: Despite state ownership, CNOOC's capital allocation rivals the best private companies. The company maintains strict return thresholds, regularly divests underperforming assets, and has avoided the empire-building that plagues many state enterprises.

Managing Geopolitical Risk Through Diversification: CNOOC operates in over 40 countries, reducing dependence on any single market. This geographic spread provides resilience against sanctions, political upheaval, and market disruptions.

The Three-Body Problem: CNOOC must simultaneously satisfy three masters: the Chinese government (energy security), international shareholders (returns), and host countries (local development). Balancing these competing demands requires constant negotiation and occasional compromise.

IX. Bull vs. Bear Case

The Bull Case:

Start with China's energy reality: the country imports 75% of its oil and this dependence is growing. In this context, CNOOC isn't just another oil company—it's a strategic asset critical to national security. The Chinese government will support CNOOC through any crisis because the alternative—energy insecurity—is unthinkable.

The production economics are compelling. At $30 per barrel all-in costs, CNOOC is profitable at oil prices that would bankrupt many competitors. The company's offshore focus provides a natural moat—these are long-life, high-margin assets that can't be easily replicated.

Technology capabilities now rival Western majors. CNOOC's ultra-deepwater expertise, developed through decades of learning and recent indigenous innovation, positions it to capture high-value opportunities globally. The company is no longer dependent on Western technology—a crucial advantage in an era of technological decoupling.

The natural gas pivot aligns perfectly with China's energy transition. As China shifts from coal to gas, CNOOC's domestic gas resources become increasingly valuable. The company's LNG import infrastructure and trading capabilities provide additional growth vectors.

Valuation remains undemanding. Despite strong operational performance, CNOOC trades at significant discounts to Western peers—a function of geopolitical risk that may already be fully priced in.

The Bear Case:

CNOOC's earnings is sensitive to oil prices, which would be dictated by output by the Organization of the Petroleum Exporting Countries (OPEC) and the US. With OPEC+ managing supply and U.S. shale providing a ceiling on prices, CNOOC's earnings remain hostage to forces beyond its control.

The geopolitical risk is structural, not cyclical. The U.S.-China rivalry is a generational conflict that will likely intensify. CNOOC will remain a target for Western sanctions, limiting its access to capital, technology, and markets. The Pentagon designation as a military-linked company is unlikely to be reversed.

Peak oil demand looms. Electric vehicle adoption in China is accelerating faster than anywhere globally. CNOOC's core product faces obsolescence within decades—a particular challenge for long-life offshore assets that require huge upfront investment.

Capital allocation in state-owned enterprises inevitably suffers from political interference. While CNOOC has maintained discipline so far, pressure to support national objectives—regardless of returns—will likely intensify as geopolitical tensions rise.

The technology gap in certain areas remains real. Despite progress, CNOOC still lacks capabilities in some specialized areas like floating LNG and advanced subsea processing. Without access to Western technology, closing these gaps will be expensive and time-consuming.

X. Epilogue: The Energy Transition Dilemma

As we sit here in 2025, CNOOC faces an existential question that would have seemed absurd at its founding: how does an oil company survive the end of oil?

China's 2060 carbon neutrality pledge isn't just rhetoric—it's driving fundamental policy changes that will reshape CNOOC's market. The company's response has been pragmatic rather than transformational. Unlike European oil majors making bold pivots to renewables, CNOOC is taking measured steps: offshore wind projects that leverage existing capabilities, carbon capture projects that extend the life of oil and gas assets, and hydrogen experiments that may or may not scale.

The company's renewable energy investments remain modest—perhaps 5% of capital expenditure. Management's view, expressed privately, is that CNOOC's comparative advantage lies in complex marine engineering and subsurface expertise, not in manufacturing solar panels or operating wind farms. Better to focus on what they do well than chase fashionable narratives.

Yet the energy transition creates opportunities too. Natural gas will be a bridge fuel for decades, and CNOOC's gas resources become more valuable as China phases out coal. The company's LNG infrastructure—import terminals, storage facilities, distribution networks—provides options regardless of whether that LNG comes from conventional or renewable sources.

The deeper question is whether a state-owned enterprise designed for energy security can adapt to a world where energy security means something fundamentally different. In 1982, energy security meant finding oil. In 2050, it might mean managing intermittent renewables, hydrogen supply chains, or technologies we haven't imagined.

CNOOC's journey from a startup learning basic offshore drilling to a global energy major mirrors China's own transformation. Both have succeeded through pragmatism, learning, and strategic patience. Both now face futures that will require different capabilities than those that brought them success.

The next decade will determine whether CNOOC can execute one more transformation—from oil company to energy company. The track record suggests not betting against them. After all, this is a company that learned to drill in 3,000 meters of water by watching others, acquired the West's best petroleum assets despite political opposition, and survived sanctions designed to cripple it.

For investors, CNOOC represents a unique proposition: exposure to China's energy security imperative, world-class offshore assets, and a management team that has navigated every crisis thrown at it. The risks are real—geopolitical, technological, and existential. But then again, CNOOC has been managing exactly these kinds of risks for four decades.

The company that Deng Xiaoping's reforms created to bring Western technology to China has become something nobody anticipated: a Chinese company teaching the world how state capitalism can work. Whether it can teach one more lesson—how an oil company becomes an energy company—remains to be seen.

In the end, CNOOC's story isn't just about oil or China or even energy. It's about adaptation, learning, and the constant balance between commercial logic and national interest. It's about how companies and countries evolve, sometimes in harmony, sometimes in tension, but always in response to forces larger than themselves.

As Fu Chengyu, the CEO who led CNOOC through both its greatest triumph and most humbling defeat, once said: "We didn't choose to be at the intersection of energy and geopolitics. But since we're here, we might as well learn to navigate it better than anyone else."

Four decades after its founding, that navigation continues.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube