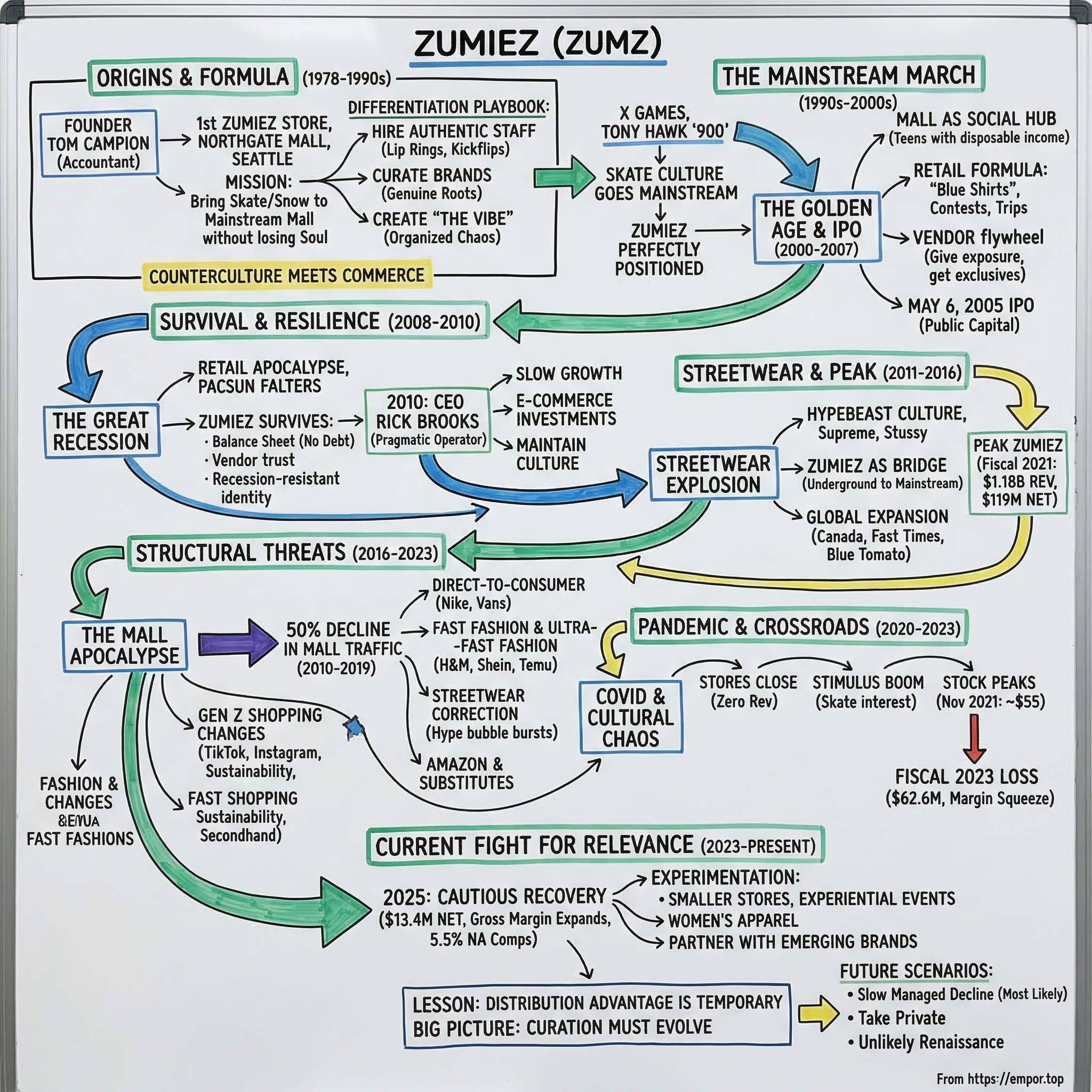

Zumiez Inc.: From Mall Rat Rebellion to Streetwear Survival

I. Introduction & Episode Roadmap

Picture a sixteen-year-old skater in 2004, baggy jeans dragging on the tile floor, Etnies on his feet, pushing through the double doors of a suburban mall somewhere outside Portland. He walks past the Abercrombie & Fitch with its cologne-soaked entrance, past the Gap with its khaki uniformity, past the food court where his mom is killing time with a Cinnabon. And then he sees it: Zumiez. The music is loud. The walls are covered in decks. A twenty-something employee with a lip ring is doing a kickflip on the demo rail by the entrance. The kid walks in, and for thirty minutes, he is not in a mall. He is somewhere else entirely. He is in a skate shop that happens to have a JCPenney next door.

That moment, replicated millions of times across hundreds of American malls throughout the 2000s, was the beating heart of Zumiez's business model. The company took something inherently anti-establishment, skateboarding and snowboarding culture, and packaged it for suburban consumption inside the most establishment place in America: the shopping mall. And for a while, it worked brilliantly.

Today, Zumiez operates roughly 700 stores across four countries, generating just under a billion dollars in annual revenue. The company just reported fiscal 2025 fourth quarter results on March 12, 2026, beating estimates with earnings per share of $1.16 and North American comparable sales growth of 5.5 percent. That sounds encouraging. But zoom out, and the picture gets complicated. The stock, which hit an all-time high of nearly $55 in November 2021, trades around $21 today. Revenue peaked above $1.18 billion in fiscal 2021 and has contracted sharply. The company posted a net loss of over $62 million in fiscal 2023. The most recent full fiscal year showed net income of just $13 million, a fraction of the $119 million earned during the stimulus-fueled peak.

The central question of this deep dive is deceptively simple: how did a single Seattle skate shop become a seven-hundred-store mall empire, and why is it now fighting for relevance in a world that has moved on from both malls and the version of youth culture that Zumiez monetized? This is a story about commodified counterculture, the fragility of authenticity as a business strategy, the death of the American mall, and the way the internet fundamentally rewired how teenagers discover brands, build identities, and spend money. It is also a story about remarkably disciplined operators who have managed to survive longer than almost anyone thought possible.

What makes Zumiez different from every other retail cautionary tale is the tension at its core. The company was never just selling clothes and skateboards. It was selling belonging, a sense of tribal identity, access to a subculture. And that worked beautifully right up until the internet gave every teenager in America unlimited access to every subculture simultaneously, no mall trip required.

The leadership team matters to this story as well. Tom Campion, the founder, remains Chairman of the board at age seventy-six, a steady hand connecting the company's countercultural origins to its corporate present. Rick Brooks, the CEO since 2010, has navigated the company through a recession, a pandemic, and a fundamental restructuring of the retail landscape. CFO Chris Work has managed a balance sheet that, remarkably, carries no long-term debt, a distinction that very few retailers of any size can claim. These are not flashy executives. They are operators, and the company's survival to this point is largely their story.

II. Origins: Counterculture Meets Commerce (1978-1990s)

In 1978, Tom Campion was an unlikely candidate to launch a skateboard shop. Born in 1949, Campion had trained as an accountant, the kind of buttoned-up career path that could not be further from the anarchic energy of late-1970s skate culture. But Campion had caught the bug. He had watched skateboarding evolve from a California sidewalk curiosity into something with genuine cultural momentum, and he saw an opportunity that the existing skate shops were missing: suburban kids wanted in, but they had nowhere to go.

The first Zumiez store opened in Seattle's Northgate Mall. The irony of this origin story is worth pausing on, because it defines everything that followed. This was not a gritty Venice Beach boardwalk shop or a DIY operation in a converted garage. From its very first day, Zumiez existed inside the belly of mainstream American retail. Campion's thesis was not that skateboarding should stay underground. His thesis was that it could be brought to the mainstream without losing its soul. Whether he succeeded in that mission, or whether the attempt was always doomed to eventually hollow out the culture it celebrated, is the central philosophical tension of the entire Zumiez story.

The early differentiation strategy was straightforward but fiercely executed. Campion insisted on hiring actual skaters and snowboarders as employees. This was not a cosmetic decision. In the late 1970s and 1980s, the entire credibility of a skate shop rested on whether the people behind the counter actually lived the lifestyle. A skater could walk into a store and within thirty seconds determine whether the staff was authentic or posing. Campion understood that this credibility was the single most important asset his business had.

He curated brands carefully, stocking the names that had genuine roots in skate and snow culture, and he invested in creating what he called "the vibe," a store environment that felt more like a community hangout than a retail transaction.

Throughout the 1980s and into the 1990s, Zumiez grew slowly. This was a deliberate choice. Campion kept the company private, resisted the urge to franchise or scale rapidly, and focused on perfecting the formula in the Pacific Northwest. The slow burn paid off in the form of deep vendor relationships, a genuine reputation within the action sports community, and a management team that understood the delicate balance between commercial growth and cultural authenticity.

The broader cultural context matters here. Skateboarding in the 1980s was still genuinely countercultural, associated with trespassing, property damage, and a general disregard for authority. Cities passed ordinances banning skating in public spaces. Parents viewed it as a gateway to delinquency. The Bones Brigade videos, featuring skaters like Tony Hawk, Rodney Mullen, and Steve Caballero, were passed around on VHS tapes like samizdat literature. The culture was tight-knit, tribal, and deeply suspicious of outsiders, particularly commercial outsiders.

But by the mid-1990s, with the launch of ESPN's X Games in 1995, the sport began its long march toward mainstream acceptance. Tony Hawk became a household name, culminating in his legendary 900 at the X Games in 1999. The Tony Hawk's Pro Skater video game series, launched that same year, sold millions of copies and introduced skateboarding culture to an entire generation of kids who had never set foot on a board. Thrasher Magazine, which had long been the bible of underground skate culture, began appearing on coffee tables alongside Sports Illustrated. And suddenly, the suburban teenager who had never touched a board in his life wanted to dress like he spent every afternoon at the skatepark. Zumiez was perfectly positioned for exactly this moment. The company had spent nearly two decades building credibility within the community, and now the community was about to explode in size.

This mainstreaming of skate culture was a double-edged sword that would recur throughout the Zumiez story. Broader adoption meant more customers and more revenue. But it also diluted the exclusivity that made the culture attractive in the first place. The core skaters, the ones who actually skated, began to feel that their culture was being appropriated by poseurs who bought the clothes but never learned an ollie. Zumiez navigated this tension by maintaining its commitment to hardgoods, hiring real skaters, and curating brands that had credibility with the core community. But the tension never fully resolved.

The name itself, Zumiez, deserves a moment of explanation. It was a made-up word, chosen precisely because it had no prior meaning. Campion wanted a brand name that would feel native to the culture without being derivative of it. It needed to sound like something a skater would say, even though no skater had ever said it. The name worked because it was authentic in spirit even if it was manufactured in origin, a paradox that would come to define the entire enterprise.

By the late 1990s, Campion had proven the concept regionally and was ready to go national. The company had grown to a few dozen stores concentrated in the Pacific Northwest and Mountain West, had established a small but loyal following, and had developed the operational playbook that would guide the coming expansion. The question was no longer whether suburban kids wanted access to skate culture. They obviously did. The question was whether you could scale that access to hundreds of locations without destroying the very thing that made it valuable.

III. The Mall Golden Age & IPO (2000-2007)

The early 2000s were, in retrospect, the last great era of the American mall. Teenagers did not have smartphones. Social media did not exist in any meaningful form. The mall was not just where you shopped; it was where you socialized, where you saw and were seen, where you figured out who you were. For a company like Zumiez, which was selling identity as much as merchandise, this was the perfect environment. Every Friday night, millions of American teenagers converged on their local malls with disposable income and a desperate need to signal which tribe they belonged to. Zumiez was there to help.

The Zumiez retail formula, perfected during this era, was genuinely distinctive. Walk into a store, and the first thing you noticed was what the company called "organized chaos." Unlike the clean, minimalist aesthetic of an Abercrombie or the clinical layout of a department store, a Zumiez store felt deliberately cluttered. Skateboards hung from the ceiling. Shoes were stacked in columns. T-shirts from a dozen different brands competed for wall space. Music blared. The effect was intentional: it made the store feel like a skater's bedroom, not a retail environment. It invited browsing and discovery rather than targeted shopping.

The employee culture was the secret weapon. Zumiez called its store associates "blue shirts," and they were not typical retail workers. They were hired because they skateboarded, snowboarded, or surfed. They were encouraged to be themselves, to talk to customers about the latest tricks or the newest board, to treat the store as an extension of the local skate scene. The company invested in employee engagement through things like skate contests, snowboard trips, and a culture that valued passion over polish. The result was a level of customer trust that was essentially impossible for a corporate competitor to replicate. When a Zumiez employee told a sixteen-year-old which deck was worth buying, that recommendation carried weight because the employee actually skated.

Vendor relationships were equally critical. The action sports industry in the early 2000s was a fragmented ecosystem of small, founder-led brands, many of which were deeply suspicious of mainstream retail. Zumiez navigated this tension by positioning itself as a bridge, not a sellout. The company gave emerging brands shelf space and exposure to a national audience, and in return, those brands gave Zumiez access to products and limited releases that department stores could never get. This created a powerful flywheel: authentic brands attracted credible customers, credible customers attracted more authentic brands, and the cycle reinforced itself.

On May 6, 2005, Zumiez went public on NASDAQ. The timing, though it seemed brilliant at the moment, would prove to be a double-edged sword. The IPO arrived at what would prove to be the absolute peak of mall-based specialty retail. Campion, who remains Chairman to this day, used the public offering to provide liquidity while retaining strategic control. The stock debuted strongly, and by late 2006, shares were trading above $33. The company used the IPO capital to accelerate its expansion strategy, opening new stores at a pace that would have been unthinkable during the cautious private-company era. From roughly a hundred stores at the time of the IPO, the fleet would eventually grow to over 700 locations. The formula was treated as cookie-cutter replicable: find a mid-tier mall with strong teenage foot traffic, build out a store with the signature organized chaos aesthetic, staff it with local skaters, and let the flywheel spin.

The expansion strategy carried an implicit assumption that was rarely examined at the time: that every American city of meaningful size had a population of teenagers who wanted what Zumiez was selling, and that the mall was the right place to reach them. Through the mid-2000s, this assumption held. But the expansion also created a fixed cost structure, hundreds of lease commitments, thousands of employees, warehouse and distribution infrastructure, that would prove extremely difficult to unwind when the underlying demand began to shift.

The golden era metrics were extraordinary. Same-store sales grew consistently. New stores reached profitability quickly. Revenue climbed from roughly $300 million at the time of the IPO toward the billion-dollar mark. By October 2007, the stock had climbed to nearly $42, reflecting investor enthusiasm for what appeared to be a perfectly scalable retail concept.

The competition was fierce but fragmented. Pacific Sunwear, known as PacSun, was the most direct competitor, chasing the same teenage surf-and-skate dollar with a California-inflected version of the same formula. Tilly's, founded in 1982 and based in Irvine, offered a similar action sports assortment but with a broader appeal that straddled the line between skate culture and general teen fashion. Journeys, owned by Genesco, focused on footwear but competed for the same mall traffic and teenage disposable income. Hot Topic went after the alternative-culture demographic from a different angle, emphasizing music, pop culture, and a darker aesthetic.

Each competitor had its own version of the teen-identity-through-retail playbook, and each would face similar structural challenges in the years ahead. But in the mid-2000s, the market was large enough to support multiple players, and the real competition was not between Zumiez and PacSun but between all of them collectively and the emerging digital alternatives that would eventually make the entire category irrelevant.

Behind these direct competitors, larger players like Urban Outfitters were beginning to eye the streetwear market with growing interest. Private equity firms and strategic acquirers circled Zumiez during this period, recognizing the value of a brand that had genuine cultural credibility with the most coveted demographic in retail. But Campion and his team resisted, believing they could build more value as a public company.

The hardgoods business, skateboards, snowboards, bindings, and components, was a smaller but strategically important part of the revenue mix. Hardgoods carried lower margins than apparel and footwear, but they served a critical purpose: they established authenticity. A store that sold actual skateboards, not just skate-inspired clothing, had more credibility with the core customer. The hardgoods section was the proof of concept, the thing that separated Zumiez from a Hot Topic or a PacSun that was merely borrowing the aesthetic. When a serious skater walked in and saw quality decks from brands like Element, Plan B, and Baker, he knew this was a real shop, even if most of the store's revenue came from the t-shirts and hoodies that his less committed friends were buying.

The pre-financial-crisis era was Zumiez at its most confident. The company had solved the puzzle of scaling counterculture, or so it seemed. Every new store opening was a validation of the thesis. Every quarter of same-store sales growth confirmed that the formula worked. What nobody could see, because nobody was looking in the right direction, was that the foundation upon which the entire model rested, the American shopping mall as the center of teenage social life, was about to begin its long, irreversible decline.

IV. The Great Recession & Unexpected Resilience (2008-2010)

The 2008 financial crisis hit American retail like a wrecking ball. Consumer spending collapsed. Credit markets froze. Mall traffic, which had already begun showing early signs of softness, fell off a cliff. For specialty retailers targeting teenagers, a demographic whose spending is almost entirely discretionary, the recession should have been an extinction event. PacSun would never fully recover. Countless smaller chains shuttered entirely. The first wave of what would become known as the "retail apocalypse" had arrived.

Zumiez survived, and the way it survived revealed something important about the business that would matter enormously in the years ahead. The stock cratered from that pre-crisis high of $42 all the way down to $6.12 in November 2008, a gut-wrenching decline of over eighty-five percent. But the business itself, while battered, remained fundamentally intact.

Three factors explained the resilience. First, inventory discipline. Unlike many specialty retailers that had loaded up on inventory during the boom years, Zumiez had maintained relatively conservative buying practices. When consumer spending collapsed, the company was not stuck with mountains of unsold merchandise that had to be liquidated at steep discounts. Second, vendor partnerships. Because Zumiez had built genuine relationships with its brands over decades, those vendors worked with the company during the downturn rather than cutting off supply or demanding punitive terms. Third, and most importantly, the balance sheet. Zumiez had gone public with modest debt and had resisted the temptation to leverage up during the expansion years. When the crisis hit, the company had the financial flexibility to weather the storm without taking on emergency financing or selling equity at distressed prices.

There was also something more subtle at work. Skate culture, it turned out, was partially recession-resistant. Not because skaters were wealthy, but because the core activity, skateboarding itself, was essentially free. You needed a board and a pair of shoes, and both lasted longer than a fashion trend. The identity associated with skate culture was durable in a way that fashion-driven identities were not. A kid who identified as a skater in 2007 still identified as a skater in 2009, even if he was buying fewer shirts. This meant that Zumiez's customer base contracted in spending but not in loyalty, a crucial distinction that kept the brand relevant through the downturn.

In 2010, Rick Brooks took over as CEO, a transition that would prove to be one of the most consequential in the company's history. Brooks, born in 1960 and a long-time Zumiez executive, was not a turnaround specialist brought in from outside. He was an operator who understood the culture of the company from the inside. His leadership style was pragmatic rather than visionary: slow store growth, obsessive focus on profitability, early investment in e-commerce, and a relentless attention to the metrics that actually drove the business.

Brooks' background shaped his approach. Unlike the founder-visionary archetype, Brooks was a career retail operator who had risen through Zumiez's ranks over many years. He understood the stores, the vendors, the customers, and the culture not from a strategic planning deck but from having worked in and around them. His compensation, at roughly $877,000 in base pay, was modest by public company CEO standards, reflecting the company's culture of frugality and its relatively small scale. The leadership team around him was similarly long-tenured: CFO Chris Work, Chief Legal Officer Chris Visser, and International President Adam Ellis all had deep institutional knowledge. This was not a company that brought in outsiders to shake things up. It was a company that promoted from within and valued continuity.

Brooks made several strategic choices during this period that would define the next decade. He slowed the pace of new store openings, recognizing that the pre-crisis expansion had outrun demand in some markets. He invested in the company's digital capabilities at a time when most specialty retailers still treated e-commerce as an afterthought. And he maintained the cultural hiring practices that had always been Zumiez's differentiator, even as cost-cutting pressure might have justified a shift toward cheaper, less specialized labor.

What nobody fully appreciated at the time was the emerging threat that would ultimately prove far more destructive than any recession. In 2007, Apple released the iPhone. By 2010, smartphones were becoming ubiquitous among teenagers. Social media platforms, Instagram would launch in October 2010, were beginning to reshape how young people discovered brands, built identities, and communicated with each other. The mall visit, once the centerpiece of teenage social life, was starting to compete with a device that offered unlimited social connection without leaving the house. The recession had been a temporary shock. The smartphone was a permanent structural change. And Zumiez, for all its operational excellence, was built entirely on the assumption that teenagers would keep showing up at the mall.

V. The Streetwear Explosion & Peak Zumiez (2011-2016)

Something unexpected happened in the early 2010s that gave Zumiez a second wind nobody anticipated. Streetwear, which had been percolating in underground fashion circles for years, exploded into the mainstream. Supreme, the New York skate brand founded in 1994, went from a single Lafayette Street shop to a global phenomenon. Stussy, which had been around since the 1980s, suddenly found itself relevant to a new generation. The "hypebeast" emerged as a cultural archetype: a young consumer obsessed with limited-edition drops, brand logos, and the social currency of wearing the right thing.

This was, in theory, perfect for Zumiez. The company had been stocking many of these brands for years, long before they became objects of mainstream desire. Zumiez had distribution relationships with emerging streetwear labels that department stores could not access and online-only retailers had not yet cultivated. For a brief, shining period, Zumiez's original competitive advantage, being the bridge between underground culture and mainstream retail, aligned perfectly with the cultural moment.

The company leaned into the opportunity. Under Brooks' leadership, Zumiez expanded internationally for the first time. The initial move was into Canada, a natural extension of the North American market. Then came a much more ambitious play: the acquisition of Blue Tomato, an Austrian action sports retailer, which gave Zumiez a foothold in Europe. The Blue Tomato deal was strategically clever. Rather than trying to export the Zumiez brand to a market where it had no recognition, the company acquired an established European player with its own cultural credibility and local knowledge. Later, the acquisition of Fast Times brought Zumiez into Australia. By the mid-2010s, international operations contributed over $100 million in annual revenue, providing geographic diversification that few specialty retailers of similar size could match.

The omnichannel push was equally aggressive. Zumiez invested in integrating its physical stores with its e-commerce platform, launching ship-from-store capabilities, building out its mobile presence, and creating a digital experience that complemented rather than cannibalized the in-store experience. The company recognized earlier than many peers that the customer journey was no longer linear, that a teenager might discover a brand on Instagram, research it on her phone, and then visit the store to try it on before buying.

The international revenue buildup was meaningful. By fiscal 2016, foreign operations contributed roughly $125 million, growing to over $150 million by fiscal 2017. This represented about fifteen to seventeen percent of total revenue, a significant diversification for a company that had been entirely domestic just a few years earlier. The European operation, in particular, gave Zumiez access to a different retail dynamic: European malls and shopping streets had not experienced the same degree of decline as their American counterparts, and the action sports culture in markets like Austria, Germany, and the Nordic countries was vibrant and growing.

Financially, the results were strong. Revenue grew steadily through this period, crossing the billion-dollar threshold. But the stock performance told a more complicated story. After recovering from the financial crisis lows, shares climbed into the mid-$40s by mid-2015, reflecting optimism about the streetwear tailwind and international growth. Then came a sharp correction. By early 2017, the stock had fallen to the low teens, despite the fact that the underlying business was still profitable. The market was beginning to price in the structural headwinds that would dominate the next chapter of the story.

The paradox of this era was that Zumiez's success was beginning to undermine its own foundation. The more mainstream streetwear became, the less differentiated Zumiez's product assortment appeared. When everybody from H&M to Zara started producing streetwear-inspired clothing at a fraction of the price, the value proposition of buying an authentic brand at an authentic retailer became harder to articulate. Why pay forty dollars for a graphic tee at Zumiez when you could get something visually similar at a fast-fashion chain for twelve?

More fundamentally, the way teenagers discovered and adopted brands was changing in ways that threatened the entire retail model. Instagram, which reached a billion users by 2018, became the primary discovery platform for fashion. A sixteen-year-old in 2015 did not need to walk into Zumiez to find out what was cool. She could follow the right accounts, see what influencers were wearing, and order directly from brand websites. The information advantage that physical retail had always provided, the ability to curate and introduce customers to new brands, was being eroded by an algorithm.

For investors watching Zumiez during this period, the critical question was whether the company's strengths, its vendor relationships, its employee culture, its operational discipline, could survive the transition from a world where physical stores were the primary discovery mechanism to one where they were increasingly optional. The stock market's answer, expressed through the steep decline from the 2015 highs, was: probably not.

VI. The Mall Apocalypse & Strategic Crossroads (2016-2019)

The numbers were brutal and unambiguous. Between 2010 and 2019, foot traffic at American shopping malls declined by an estimated fifty percent. Anchor tenants, the Sears and JCPenneys whose presence justified the entire mall ecosystem, were closing at an accelerating pace. For a retailer like Zumiez, which derived virtually all of its North American revenue from mall locations, this was not a cyclical headwind. It was a structural threat to the business model itself.

Zumiez's response was measured and disciplined, reflecting Brooks' operational temperament. The company began optimizing its store fleet, closing underperforming locations and renegotiating leases at others. This was not an easy process. Mall leases are long-term commitments, typically five to ten years, and breaking them early involves significant costs. But the alternative, continuing to pay rent on stores with declining traffic and negative four-wall contribution, was worse. The fleet, which had peaked at over 700 stores in North America, began a slow contraction.

Digital acceleration became a strategic priority, though the transition was far from seamless. Zumiez invested in its mobile app, improved the online shopping experience, and expanded its social media presence. The company's marketing shifted from traditional mall-based tactics, in-store events, window displays, flyer distributions, toward digital channels that could reach customers where they actually spent their time. Influencer partnerships, Instagram campaigns, and YouTube content replaced the grassroots marketing that had defined Zumiez's early decades.

But digital was not a simple substitute for physical. The economics were different: online customers could comparison-shop instantly, return rates were higher, and fulfillment costs ate into margins. The experience was different too. The organized chaos of a Zumiez store, the music, the employees doing kickflips, the sensory overload that made the space feel alive, could not be replicated on a website. E-commerce was a necessary evolution, but it was also a dilution of the core value proposition. The more revenue shifted online, the less distinctive Zumiez became relative to any other website selling the same brands.

The Blue Tomato private label strategy represented an interesting bet. By developing house brands through its European subsidiary, Zumiez could capture higher margins and reduce its dependence on third-party vendors who were increasingly tempted to go direct-to-consumer. Private label in action sports retail was a delicate proposition, since the entire value proposition rested on carrying authentic third-party brands, but the economic logic was compelling. When a brand like Vans decided to sell directly through its own stores and website, the margin Zumiez earned on that brand's products was zero. Private label was insurance against vendor defection.

The competitive landscape was intensifying from every direction simultaneously. Direct-to-consumer brands represented the most existential threat. Vans, owned by VF Corporation, was aggressively building out its own retail presence and e-commerce platform. Nike, which had long been a wholesale-dependent company, announced a dramatic shift toward direct-to-consumer sales, reducing its wholesale relationships and prioritizing its own stores and digital channels. When a brand that generated significant foot traffic for Zumiez decided to sell directly to consumers instead, the retailer lost not just that brand's margin but the traffic that brand had driven.

Amazon loomed as an ever-present threat, not because it was directly competing for the streetwear customer, but because it had trained an entire generation to expect free shipping, instant delivery, and unlimited selection. Every retailer, regardless of category, was now being benchmarked against Amazon's convenience standard. Urban Outfitters and similar lifestyle retailers were chasing the streetwear trend with their own curated assortments, bringing the financial muscle and marketing reach of larger companies to bear on Zumiez's core market.

Event marketing and community engagement became increasingly important as tools for driving traffic that no longer came organically. Zumiez invested in in-store events, brand demo days, and partnerships with local skate parks and music venues. The idea was to transform stores from transaction points into community hubs, places where teenagers would come not just to buy but to participate. The company's "Couch Tour" concert series, which brought live music performances into stores, was a creative attempt to generate foot traffic by offering an experience that could not be replicated online. These initiatives were genuinely innovative, but they were swimming against a tide of declining mall visits that no amount of event programming could fully reverse.

A symbolic moment arrived in 2017 when the International Olympic Committee announced that skateboarding would be included in the 2020 Tokyo Olympics. This was, depending on your perspective, either the ultimate validation of the sport or the final stage of its co-option by mainstream culture. For Zumiez, the implications were ambiguous. On one hand, Olympic inclusion brought new attention and potential new customers to skateboarding. On the other, it accelerated the mainstreaming that was already eroding Zumiez's differentiation. When skateboarding is an Olympic sport, the distinction between an authentic skate retailer and a general sporting goods store becomes harder to maintain.

The pre-pandemic financial performance was solid but uninspiring in the context of the company's prior trajectory. Fiscal 2018, ending February 2019, saw revenue of $979 million and net income of $45 million. Fiscal 2019, ending February 2020, pushed revenue above $1.03 billion with net income of $67 million and earnings per share of $2.62. These were respectable results, but they represented a company running hard to stay in place. Revenue growth was driven primarily by new store openings rather than same-store sales improvement, meaning the company was spending capital to maintain growth rather than generating it organically from its existing base.

The period was also defined by a question that the company's leadership addressed directly in earnings calls: can a mall-based specialty retailer survive the 2020s? Brooks and his team argued yes, pointing to their digital investments, their international diversification, and their unique cultural positioning. Skeptics argued that no amount of operational excellence could overcome the structural decline of the channel through which Zumiez reached its customers. The stock, trading in the low-to-mid twenties heading into 2020, reflected this uncertainty. The market was giving Zumiez credit for being a survivor but was not willing to bet on a comeback. Fiscal 2019's revenue of over a billion dollars and EPS of $2.62 translated to a stock price of roughly $31, meaning the market was valuing the company at roughly twelve times earnings, a below-market multiple that reflected the structural concerns that no operational result could fully assuage.

VII. COVID, Cultural Chaos, and Reinvention Attempts (2020-2023)

When the pandemic hit in March 2020, Zumiez closed all of its stores overnight. Every single one, across four countries. The stores that had been generating the vast majority of the company's revenue were now generating precisely zero revenue while continuing to incur lease costs, insurance, and other fixed obligations. For a company that derived the overwhelming majority of its sales from physical locations, this was as close to a business-ending event as you could get without actually going bankrupt.

The emergency response was immediate. E-commerce, which had been growing steadily but still represented a minority of sales, suddenly became the only sales channel. The company's previous investments in digital infrastructure, which had seemed like a hedge against a distant future, became mission-critical overnight. Curbside pickup was hastily implemented at stores that could partially reopen. The corporate team transitioned to remote work. Furloughs and layoffs reduced headcount to survival levels. The balance sheet, with its lack of debt and significant cash reserves, provided the oxygen the company needed to survive weeks and months without meaningful revenue.

The stock plunged to $17 in March 2020 as investors priced in the possibility that the mall apocalypse had just been compressed from a decade-long slow decline into a single catastrophic quarter.

What happened next defied every reasonable expectation. The combination of government stimulus checks, enforced boredom, and a sudden teenage interest in outdoor activities including skateboarding created a spending boom that lifted Zumiez to financial heights it had never previously reached. Fiscal 2020, the year ending January 2021, saw revenue of $991 million and net income of $76 million. Fiscal 2021, ending January 2022, was even more extraordinary: revenue surged to $1.184 billion, the highest in company history, and net income reached $119 million. Earnings per diluted share hit $4.85, nearly double the previous peak. The stock rocketed from that pandemic low to an all-time high of $54.63 in November 2021.

The stimulus era was a sugar high, and anyone paying attention knew it. Zumiez's management, to their credit, recognized this. On earnings calls during fiscal 2021, Brooks and CFO Chris Work repeatedly cautioned that the elevated spending levels were not sustainable, that consumers were spending stimulus dollars and savings accumulated during lockdowns, and that a normalization was inevitable. The question was not whether the boom would end but how far the pendulum would swing in the other direction. The answer, it turned out, was very far indeed.

The stock's journey during this period told a remarkable story of sentiment whiplash. From $17 in March 2020, shares climbed steadily as each quarterly report surprised to the upside. By June 2021, the stock was at $49. By November 2021, it touched $54.63, the all-time high. Zumiez was briefly valued at over a billion dollars, a staggering figure for a company that most investors had written off as a declining mall retailer just eighteen months earlier. The company used the strength to buy back shares aggressively, spending hundreds of millions on repurchases over fiscal 2020 and 2021. These buybacks would prove to be poorly timed, executed near the stock's peak and funded with cash that would later be missed during the downturn. But the peak lasted only weeks. As inflation surged, the Federal Reserve began signaling rate hikes, and consumer spending patterns normalized, the stock began a long descent. By mid-2022 it was at $26. By mid-2023, $17. The round-trip was nearly complete.

The meme stock era also briefly touched Zumiez, though the company was never a primary target of the Reddit-driven speculation that defined 2021. Short interest in the stock fluctuated, and the volatility attracted day traders who had no particular interest in skate culture or retail fundamentals. For a company whose identity was built on authenticity, becoming a ticker symbol in the Wall Street Bets casino was a strange and faintly humiliating experience.

The company had used the pandemic to accelerate several strategic initiatives. The Fast Ship program, which enabled stores to fulfill online orders from their own inventory, represented a genuine operational innovation. Rather than shipping everything from centralized warehouses, Zumiez could use its hundreds of store locations as mini-fulfillment centers, getting products to customers faster and reducing the cost of online fulfillment. The loyalty program was overhauled to capture better data on customer behavior and spending patterns. Social media strategies were expanded, with the company investing in TikTok content, influencer partnerships, and the kind of digital marketing that could reach Gen Z consumers on their own terms.

But the fundamental challenge remained unchanged: the customer was evolving faster than the business model. Gen Z, the cohort that was supposed to be Zumiez's next generation of loyal customers, shopped in ways that were fundamentally different from the Millennials who had driven the company's golden era. Gen Z discovered brands through TikTok and Instagram, not by wandering through a mall. They valued sustainability and social consciousness in ways that a legacy action sports retailer was not positioned to deliver. They cycled through trends at a pace that made the traditional retail buying cycle, where products were ordered months in advance, look hopelessly slow. And they were comfortable buying secondhand, through platforms like Depop and ThredUp, in a way that previous generations had not been.

The streetwear correction hit simultaneously, and it hit hard. The hype bubble that had inflated brands like Supreme to absurd valuations began to deflate. VF Corporation, which had acquired Supreme for over $2 billion in 2020, watched the brand's momentum stall. The resale market, which had boomed during the pandemic as speculators treated sneakers and streetwear like tradeable assets, crashed as supply exceeded demand and consumers became more price-sensitive. StockX, the leading resale platform, saw transaction volumes decline and was forced to lay off staff. GOAT, its main competitor, similarly retrenched. The cultural moment that had aligned so perfectly with Zumiez's assortment was passing.

This had a direct impact on Zumiez's business. When streetwear was hot, customers were willing to pay full price for branded products because those products had social currency. When the hype faded, the same products needed to be marked down to move. The promotional activity that followed compressed gross margins at precisely the moment when the company could least afford it. In fiscal 2023, cost of revenue consumed nearly 68 percent of sales, leaving a gross margin of just 32 percent, down from 39 percent during the peak year. That seven-point margin decline, on a nearly $900 million revenue base, represented roughly $60 million in lost gross profit, almost exactly the amount of the net loss that year.

The financial results after the stimulus peak told the story in stark numbers. Fiscal 2022, ending January 2023, saw revenue drop to $958 million with net income of $21 million, an eighty-two percent decline from the prior year. Fiscal 2023 was devastating: revenue fell to $875 million, and the company reported a net loss of $62.6 million, driven in part by impairment charges and a sharp contraction in gross margins. Comparable store sales declined for multiple consecutive quarters. The stock fell from its $55 high back to the mid-teens, essentially round-tripping the entire pandemic rally.

Rising costs compounded the revenue decline. Wages, driven by tight labor markets and minimum wage increases, pushed up the single largest expense in a retail operation. Rent, while negotiable in some locations, remained a substantial fixed cost across the fleet. Shipping costs, which had spiked during the pandemic, came down but did not return to pre-COVID levels. The combination of declining revenue and rising costs created a margin squeeze that turned modest operating profits into outright losses.

The company was caught in a painful bind. Its stores were expensive to operate but essential to the brand experience. Its digital business was growing but did not generate the same margins as physical retail. Its vendor partners were increasingly going direct-to-consumer, reducing both product availability and customer traffic. And the cultural credibility that had always been Zumiez's ultimate differentiator was being questioned by the very demographic it was trying to serve. To Gen Z, Zumiez was not a cool skate shop. It was a "mall brand," a term that carried roughly the same connotation as "your parents' music."

The goodwill impairment charges taken during fiscal 2023 were particularly telling. The company wrote down goodwill associated with its international acquisitions, an accounting acknowledgment that the assets it had purchased were no longer worth what it had paid for them. Goodwill impairment is, in accounting terms, the company's own admission that it overpaid for growth. Combined with inventory write-downs and restructuring costs, these charges pushed the fiscal 2023 net loss to $62.6 million, the worst annual result in company history. The operating loss for that year reached nearly $65 million, a stunning reversal from the $158 million operating profit generated just two years earlier.

Perhaps the most concerning metric during this period was the share count. The weighted average diluted shares outstanding fell from roughly 25 million during the peak years to under 19 million by fiscal 2024, reflecting aggressive share repurchases. In normal circumstances, buybacks are a sign of confidence and a mechanism for returning value to shareholders. But when a company is buying back shares while its business is contracting, there is a risk that it is merely shrinking the denominator to make per-share metrics look less terrible. The buyback program consumed capital that might have been invested in digital capabilities, new store formats, or brand partnerships.

VIII. The Current Chapter: Fighting for Relevance (2023-Present)

The most recent fiscal year, ending January 31, 2026, offered the first genuinely encouraging signs in several years. Revenue recovered to $929 million, up from $889 million the prior year. Net income turned positive at $13.4 million, a modest profit but a significant improvement from the losses of the preceding two years. The fourth quarter was particularly strong: earnings per share of $1.16 beat analyst estimates of $1.08, and North American comparable sales increased 5.5 percent. Gross margin expanded by 200 basis points to 38.2 percent, driven by better inventory management and fewer markdowns. The board authorized a new $40 million stock repurchase program, signaling confidence that the company was generating sufficient free cash flow to return capital to shareholders.

But the context around these improving numbers matters as much as the numbers themselves. Revenue of $929 million is still well below the $1.18 billion peak and roughly flat with fiscal 2017 levels. Net income of $13 million represents a return on equity of about four percent, a figure that would not excite any investor looking for growth. The stock, after rallying to above $31 in late 2025 on improving fundamentals, dropped sharply to around $21 following the earnings report, reflecting the market's skepticism that the recovery is sustainable.

The company is experimenting with its store format, testing smaller footprints and more experiential concepts that emphasize in-store events, product customization, and community engagement over pure merchandise display. The logic behind smaller formats is straightforward: a 3,000-square-foot store costs less to operate than a 5,000-square-foot store, and if you can generate similar revenue per square foot in the smaller space by curating a tighter assortment, the four-wall economics improve significantly. There has been a renewed focus on women's apparel and accessories, categories that had been underserved relative to the core men's streetwear and skateboard hardware business. Women's apparel represents a significant addressable market that Zumiez has historically underserved. Expanding into this category could broaden the customer base without requiring new store openings, essentially growing the same-store sales number by attracting customers who currently walk past the store because they do not see themselves reflected in the merchandise.

Partnership strategies with emerging brands have been refreshed, with Zumiez positioning itself as a launchpad for new labels that lack the resources to build their own retail presence. This is an attempt to recapture the discovery platform role that was Zumiez's original competitive advantage, updated for the current environment. The pitch to emerging brands: we will give you shelf space in hundreds of stores, exposure to our customer base, and a testing ground for your products. In return, we get exclusive or early access to your products, which gives our customers a reason to visit that they cannot get online. Whether this strategy can work at scale, given that most emerging brands today are built on Instagram and Shopify rather than wholesale retail, remains an open question.

The cost structure has been overhauled. Headcount has been reduced from what was once a larger workforce to approximately 2,400 full-time employees. Store-level expenses have been trimmed through renegotiated leases and more efficient staffing models. Corporate overhead has been cut.

These are the moves of a company in managed-decline mode, trying to right-size its cost structure to match a permanently lower revenue trajectory. The question is whether the cuts have gone deep enough. SGA expenses of $315 million in fiscal 2025 represent 34 percent of revenue, still above the levels that would support healthy profitability. Further cuts risk degrading the store experience that remains Zumiez's primary differentiator. It is the classic dilemma of a shrinking retailer: cut too little and you bleed cash; cut too much and you accelerate the decline by making the stores less interesting to visit.

Geographically, the story is mixed. The United States, which generated $708 million in fiscal 2025 revenue, remains the dominant market but has been the source of most of the weakness. Europe, operating under the Blue Tomato brand, contributed $148 million and has shown relative stability, benefiting from a less severe mall decline than the U.S. market. Canada, at $49 million, and Australia, at $24 million, are small but stable contributors.

The competitive landscape has only gotten more hostile. Shein and Temu have introduced ultra-fast fashion at price points that make even H&M look expensive. TikTok Shop has turned social media from a discovery platform into a direct sales channel, cutting out the retailer entirely. Sneaker and streetwear resale platforms like StockX and GOAT have created an alternative marketplace where brand-conscious consumers can buy and sell without ever touching a traditional retailer. And the direct-to-consumer movement continues to accelerate: Nike, Adidas, Vans, and virtually every other major brand that once relied on wholesale partners like Zumiez are now prioritizing their own channels.

What is working: the European business has proved more resilient than the U.S. operations, digital sales have grown as a percentage of total revenue, and the company's balance sheet remains clean with no long-term debt and over $160 million in cash and short-term investments. What is not working: the core U.S. mall business continues to face structural headwinds, gross margin remains under pressure from the shift toward digital, and the company has not yet articulated a compelling vision for what Zumiez looks like in five years.

One notable development in the most recent earnings report deserves attention. Short interest in Zumiez stock increased by roughly thirty percent in January 2026, reaching about 1.45 million shares, or approximately eleven percent of the float. This elevated short interest suggests that a significant number of professional investors are betting against the recovery narrative. The stock's sharp decline from above $31 to around $21 in the weeks following the earnings beat, a counterintuitive reaction to better-than-expected results, may reflect the market's view that the Q4 strength was seasonal and holiday-driven rather than indicative of a sustainable trend. The market, in other words, is saying: show us more than one good quarter before we believe the story has changed.

The broader context for Zumiez's current position is the ongoing bifurcation of American retail into winners and losers, with very little middle ground. The winners are either massive-scale players like Amazon, Walmart, and Costco, who compete on price, convenience, and selection, or premium brands with fierce customer loyalty and the ability to sell directly. The losers are the mid-tier specialty retailers caught between these poles, too small for scale advantages, too mass-market for premium positioning. Zumiez sits squarely in this endangered middle ground, and the question is whether operational excellence alone can defy the gravitational pull of structural decline.

IX. Business Model Deep Dive & Unit Economics

When the Zumiez flywheel worked, it was one of the most elegant machines in specialty retail. Authentic brand curation attracted credible teenage customers. Credible customers generated foot traffic. Foot traffic gave Zumiez leverage with vendors, who needed the exposure and distribution. Vendor leverage allowed Zumiez to secure exclusive products and favorable terms, which improved margins. Better margins funded more stores, which attracted more brands. The cycle reinforced itself beautifully for the better part of two decades.

Understanding why the math is breaking down requires looking at the unit economics of a Zumiez store. A typical store build-out cost somewhere in the range of $300,000 to $500,000, depending on size and location. During the golden era, a well-performing store could pay back that investment within two to three years and then generate positive four-wall contribution, meaning revenue minus direct store costs including rent, labor, and inventory, for the remainder of the lease. The metric that mattered most was revenue per square foot: a store needed to generate a certain minimum level of sales density to cover its fixed costs and contribute to corporate overhead and profit.

The problem is straightforward. When mall traffic declines by fifty percent, revenue per square foot declines with it unless the store can convert a dramatically higher percentage of visitors into buyers or increase the average transaction size. Zumiez has managed to improve both metrics through better merchandising and employee training, but not nearly enough to offset the traffic decline. A store that once generated $600 per square foot might now generate $400, and at that level, the fixed costs of rent and labor eat up most or all of the profit margin.

Digital sales add complexity rather than solving the problem. When a customer buys online, the gross margin is often similar to in-store, but the fulfillment cost is higher, the return rate is higher, and the competitive price pressure is more intense because the customer can comparison-shop with a single click. The ship-from-store program helps by reducing fulfillment costs and turning stores into distribution assets, but it does not fundamentally change the economics. A dollar of digital revenue is worth less to Zumiez's bottom line than a dollar of in-store revenue.

The vendor power shift is perhaps the most threatening dynamic. In the flywheel era, Zumiez needed brands and brands needed Zumiez. Today, that relationship is asymmetric. A brand like Vans can reach consumers directly through its own stores, its website, and its social media channels. It does not need Zumiez for distribution or discovery. But Zumiez absolutely needs Vans, because Vans drives customer traffic. This power shift shows up in the income statement as margin pressure: vendors can demand better terms, knowing that Zumiez has fewer alternatives.

The private label strategy is a logical response to this dynamic, but it carries its own risks. Zumiez's entire brand identity is built on curating other people's brands. If private label becomes too large a percentage of the assortment, the store risks losing the authenticity that differentiates it from a department store or a fast-fashion chain. It is a delicate balancing act: enough private label to protect margins, not so much that it dilutes the brand.

Inventory management remains a genuine competitive strength. The company has been disciplined about matching inventory levels to expected demand, avoiding the promotional spiral that has destroyed many specialty retailers. Days of inventory outstanding have remained relatively stable around ninety days, a reasonable figure for a seasonal apparel business. The cash conversion cycle of roughly sixty-five days indicates that the company is not tying up excessive capital in working goods.

The people challenge is real but less discussed. Zumiez built its culture on hiring passionate skaters and paying them to be authentic. As the company has been forced to cut costs, the question is whether it can maintain that culture with lower headcount, tighter budgets, and a more corporate approach to staffing. The answer may be that it cannot, and if the employee culture degrades, the last remaining differentiator goes with it.

There is a deeper structural issue buried in the unit economics that rarely gets discussed: the seasonal pattern. Zumiez, like most apparel retailers, is heavily dependent on the holiday quarter. The fourth quarter, which includes Black Friday and the Christmas shopping season, typically generates the majority of the company's annual profit. The other three quarters frequently run at or near breakeven. This means that any disruption to holiday spending, whether from recession, weather, competitive intensity, or shifting consumer preferences, has an outsized impact on the full-year result. The fiscal 2025 fourth quarter EPS of $1.16, which beat estimates, accounted for nearly all of the full-year EPS of $0.78, meaning the other three quarters combined were actually unprofitable. This seasonal dependency makes Zumiez an inherently fragile business, where one bad holiday season can turn a marginally profitable year into a loss.

X. Porter's Five Forces Analysis

Threat of New Entrants: Medium-Low but shifting. The barriers to opening a physical retail chain remain significant: capital requirements, vendor relationships, lease negotiations, and supply chain infrastructure all favor incumbents. But the relevant competitive threat to Zumiez is no longer another chain of mall stores. It is digital-native brands that can launch with a Shopify store, an Instagram account, and a small production run. The barriers for these entrants are essentially zero, and they can target Zumiez's exact customer demographic with surgical precision. Mall presence, once a barrier that protected incumbents, has become a liability that burdens them with fixed costs their digital competitors do not bear.

Supplier Power: High and rising. The direct-to-consumer movement has fundamentally shifted the power dynamic between brands and retailers. VF Corporation, which owns Vans, The North Face, and Timberland, has the scale and infrastructure to reach consumers directly. Nike's wholesale pullback set the template for the industry. When a brand decides to go direct, Zumiez loses not just that brand's products but the traffic those products generated. The consolidation of the vendor base, with a few large conglomerates controlling multiple important brands, makes the retailer even more vulnerable to individual supplier decisions.

Buyer Power: Very High. Gen Z consumers have more choices than any previous generation. They can shop online, in stores, through social media, on resale platforms, or directly from brands. Switching costs are zero. Brand loyalty among younger consumers is notably weak compared to previous generations, driven by the constant exposure to new options through social media. Price sensitivity is high, particularly given the availability of fast-fashion alternatives that offer visually similar products at a fraction of the cost.

Threat of Substitutes: Extremely High. This is arguably the most damaging force. Online pure-plays, brand DTC channels, resale platforms, fast-fashion chains, Amazon, and social commerce platforms like TikTok Shop all serve as substitutes for the Zumiez shopping experience. Fast fashion can replicate streetwear trends within weeks of their emergence, at dramatically lower price points. The resale market offers authentic branded products at used-item prices. The substitution is not just product-for-product but experience-for-experience: the social function that a mall visit once served, the hanging out, the identity signaling, is now served by social media.

Competitive Rivalry: Intense. Zumiez competes with Tilly's, PacSun, Urban Outfitters, and every other retailer targeting the youth fashion market, plus the DTC brands, plus the fast-fashion players, plus the marketplaces. The rivals are not just numerous but diverse in their business models, making it impossible for Zumiez to out-compete all of them simultaneously. Price competition is escalating, and differentiation is eroding as the cultural credibility that once set Zumiez apart becomes less relevant to its target customer.

The interaction between these forces is what makes the situation so challenging. High supplier power means Zumiez cannot negotiate better terms to offset the impact of high buyer power. Intense rivalry prevents price increases that might compensate for rising costs. Extremely high substitution risk means that any misstep in product assortment or customer experience sends shoppers to alternatives with zero friction. And the modest barriers to digital entry mean that new, nimble competitors can emerge constantly, each taking a small slice of the market that Zumiez once had largely to itself.

The structural verdict from Porter's framework is sobering. The industry is characterized by declining attractiveness across nearly every dimension. The forces that once protected Zumiez, supplier relationships, mall-based barriers to entry, and customer loyalty to the in-store experience, have weakened or reversed. The forces working against it, supplier power, buyer power, substitution, and rivalry, have intensified. This is not a cyclical challenge. It is a structural one.

A comparison with peers reinforces this assessment. Genesco, the parent company of Journeys, trades at a similar market capitalization of roughly $270 million and faces many of the same headwinds. Shoe Carnival, at roughly $500 million, has performed somewhat better by focusing on value-oriented footwear, a less culturally dependent positioning. The specialty apparel retail sector as a whole has seen massive value destruction over the past decade, with multiple bankruptcies, going-private transactions, and strategic pivots that have reshaped the competitive landscape beyond recognition.

XI. Hamilton's 7 Powers Framework Analysis

Hamilton Helmer's framework asks a more pointed question than Porter: does the company have a durable competitive advantage that can generate persistent differential returns? Applied to Zumiez, the answer is uncomfortable.

Scale Economies: Weak and declining. Seven hundred stores once provided meaningful buying power, the ability to negotiate better terms with vendors, spread fixed costs across a larger revenue base, and invest in systems and infrastructure that smaller competitors could not afford. But scale in physical retail is now as much a cost burden as an advantage. Each store carries fixed costs regardless of traffic. Digital retail does not provide winner-take-all scale economics in specialty apparel the way it does in marketplaces or platforms. Being big no longer means being cheap; it means being expensive.

Network Effects: Absent. There are no platform dynamics in Zumiez's business. Each customer shops independently. The company has attempted to create community through events, loyalty programs, and social media engagement, but none of these efforts have produced genuine network effects where the value of the platform increases with each additional user. A Zumiez loyalty member does not benefit from the existence of other loyalty members.

Counter-Positioning: Lost. This is the most painful assessment and arguably the most important dimension of the entire analysis. Counter-positioning, in Helmer's framework, exists when an incumbent cannot copy a challenger's approach because doing so would damage the incumbent's existing business. Zumiez was originally counter-positioned against department stores and mainstream retailers. It offered something they could not replicate, authentic skate culture credibility, because attempting to replicate it would have undermined their broader brand positioning. A Nordstrom could not credibly turn a corner of its store into a skate shop without confusing its core customer.

But the counter-positioning has flipped entirely. Today, the insurgents are the DTC brands and digital-native retailers, and Zumiez is the legacy incumbent. The very mall-based model that once felt rebellious now feels old-fashioned. When a new skate brand launches in 2026, it goes to Instagram and Shopify, not to Zumiez's buying team. The company has moved from insurgent to incumbent without ever becoming dominant, which is the worst possible position in Helmer's framework: all the disadvantages of incumbency with none of the advantages of scale.

Switching Costs: Minimal. There is zero cost to shopping elsewhere. The loyalty program offers modest rewards but does not create meaningful lock-in. A customer can walk out of Zumiez and into Tilly's, or open the Vans app on her phone, without any friction whatsoever.

Branding: Moderate but fading. The Zumiez brand carried real meaning for a generation of customers. "Skate and snow culture authority" was a positioning that translated into trust, repeat visits, and willingness to pay a premium. But brand perception among the current target demographic is less favorable. Gen Z consumers are more likely to associate Zumiez with "mall brand" than with authentic skate culture. The brand's regional strength persists in some markets, particularly in the Pacific Northwest where the company's heritage is strongest, but national brand equity is declining.

Cornered Resource: Previously held, now lost. The most valuable cornered resource Zumiez ever had was its relationships with emerging brands. For years, the company served as a discovery platform, giving new labels their first national retail exposure. This made Zumiez indispensable to the brand ecosystem. But brand discovery has migrated to social media, and vendor access is now commoditized. Any retailer with the right buyer can stock the same brands. And the store locations themselves, once valuable cornered resources in high-traffic malls, have become anti-resources in declining malls.

Process Power: Minimal. Zumiez's merchandising and curation capabilities were once genuinely distinctive, the product of decades of accumulated knowledge about what the skate customer wanted. But this process power has been replicated and in many cases surpassed by algorithm-driven discovery on social media platforms and by influencer-driven trend identification that moves faster than any buying team can react.

The 7 Powers verdict is stark: Zumiez exhibits no durable competitive advantage under Helmer's framework. The powers it once possessed, counter-positioning, cornered resources, and branding, have eroded. The powers it never had, network effects and switching costs, cannot be manufactured. This does not mean the company will immediately fail, but it does mean that any return to sustained above-market profitability would require building new sources of competitive advantage, a task that very few companies in structural decline have ever accomplished.

The contrast with companies that do possess durable powers is illuminating. Nike, which competes in the same broad market, has brand power, scale economies, and process power through its product innovation engine. Lululemon has counter-positioned itself against traditional athletic wear with a premium community-driven model. Even Supreme, before its acquisition by VF Corporation, had cornered resource power through its brand mystique and controlled scarcity model. Zumiez, as a multi-brand retailer rather than a brand owner, was always structurally disadvantaged in a framework that rewards proprietary assets. A retailer can lose its best vendors. A brand cannot lose its own identity in the same way.

The fundamental insight from applying both Porter and Helmer to Zumiez is that the company's historical success was driven not by structural competitive advantages but by a favorable alignment of cultural trends, channel dynamics, and demographic patterns that has now shifted. When the alignment was favorable, Zumiez looked like a great business. When it shifted, the underlying fragility became apparent. The company was always a surfboard rider, not a wave maker, and the wave has passed.

XII. Bull vs. Bear Case

The Bull Case

The most compelling bull argument starts with operational track record. Zumiez survived the Great Recession when competitors did not. It navigated the pandemic without taking on debt. It returned to profitability in fiscal 2025 after two very difficult years. The management team, led by Rick Brooks for over fifteen years, has demonstrated a capacity for disciplined cost management and strategic adaptation that is rare in specialty retail. Consider the comparison with PacSun, which went through bankruptcy in 2016, or with Wet Seal, which liquidated entirely. Zumiez has outlasted nearly every direct competitor from its golden era, and that longevity is not an accident. It reflects genuine operational skill.

The most recent quarter reinforced this point. Fourth quarter earnings per share of $1.16 represented 49 percent growth year over year. Gross margin expanded by 200 basis points, driven by disciplined inventory management and reduced promotional activity. The company generated positive operating income for the full fiscal year after two years of losses. These are the results of a management team that knows how to pull the right levers when the business gives them something to work with.

European growth still has runway. The Blue Tomato brand is well-established in the action sports market across the continent, and the European retail landscape, while facing its own challenges, has not experienced the same severity of mall decline as the United States. International revenue of roughly $220 million could continue to grow even if the U.S. business stagnates.

The balance sheet provides a margin of safety. With over $160 million in cash and short-term investments and no long-term debt, Zumiez has the financial flexibility to invest in its turnaround without the existential pressure that leverage creates. The new $40 million buyback authorization suggests management believes the stock is undervalued relative to the company's cash generation capacity.

There is a private equity takeout thesis. At a market capitalization of roughly $360 million, Zumiez could be attractive to a private equity buyer looking to take the company private, optimize the cost structure away from the scrutiny of quarterly earnings, and execute a longer-term transformation. The clean balance sheet and positive cash flow make it financeable. The company's $160 million in cash and investments means that the effective enterprise value, the amount a buyer would actually need to pay after netting out the cash on the balance sheet, would be even lower. A take-private at, say, a thirty percent premium to the current stock price would value the company at roughly $470 million, an enterprise value of around $310 million, or about eight times trailing EBITDA. That is within the range that private equity firms have historically found attractive for retail turnarounds.

There is also a streetwear durability thesis. Unlike many fashion trends that burn bright and disappear, streetwear and skate culture have proven remarkably persistent over four decades. The specific brands and styles change, but the underlying cultural energy, the fusion of sport, art, music, and fashion, shows no signs of fading. If Zumiez can maintain its position as a credible curator of this culture, there will always be a customer for what it sells.

Finally, there is the generational cycle argument. Retail trends are cyclical, and there are early signs that Gen Alpha, the generation after Gen Z, may be rediscovering physical retail. If the mall experience evolves to become more experiential and community-oriented, Zumiez's network of physical locations could become an asset again. There is something appealing about the idea of tactile, real-world shopping as a counterpoint to the screen-dominated lives of today's teenagers. If that pendulum swings, Zumiez has the physical infrastructure to benefit.

The Bear Case

The structural decline of American malls is irreversible. No amount of format innovation or experiential retail can offset the fundamental reality that teenagers do not go to malls the way they used to, and there is no reason to believe they ever will again. Zumiez is optimizing within a declining channel, which is like rearranging deck chairs on a ship that is slowly taking on water.

Gen Z shopping behavior is fundamentally incompatible with the Zumiez model. This generation discovers brands on social media, buys through digital channels, values sustainability and secondhand shopping, and cycles through trends too quickly for a traditional retail buying cycle to keep pace. Zumiez cannot change who its customer is, and its customer has moved on.

The competitive moat is gone. Brands will continue going DTC because the economics are better and the data is richer. Zumiez has no way to prevent its most important vendors from deciding that they no longer need a wholesale partner. Every brand that goes direct takes traffic and margin with it.

The "authenticity" brand positioning, once Zumiez's greatest asset, may be damaged beyond repair. When your target customer views you as a mall brand rather than a culture brand, the game is essentially over. Rebuilding that perception would require not just marketing but a fundamental reinvention of what Zumiez means, and it is not clear that the current leadership or business model can deliver that reinvention. Brand perception among teenagers is notoriously difficult to change once set. The brands that Gen Z considers authentic, whether it is Corteiz, Aimé Leon Dore, or Fear of God, share a common trait: they are not sold in malls. That association between authenticity and non-mall distribution is a structural headwind that no amount of store renovation can overcome.

The cost structure remains fundamentally challenged even after years of optimization. Selling, general, and administrative expenses consumed roughly 34 percent of revenue in the most recent fiscal year. For context, a healthy specialty retailer typically targets SGA below 30 percent. The difference, roughly four percentage points on a $929 million base, represents approximately $37 million in excess costs that must be eliminated or offset by revenue growth to achieve sustainable profitability. With over 700 stores still in operation, the fixed cost overhang of lease obligations, store labor, and utility costs creates a high breakeven point that leaves very little room for error.

Even a successful turnaround likely results in a much smaller, less profitable company. The bull case for Zumiez is not a return to billion-dollar revenue and hundred-million-dollar profits. It is a managed contraction to a fleet of four or five hundred stores generating adequate but not exciting returns. For investors, the question is whether the current stock price adequately compensates for the risk that even this modest outcome does not materialize.

Most Likely Scenario

The base case is a slow decline with periodic quarters of stabilization that give the appearance of a turnaround without fundamentally changing the trajectory. The store fleet likely shrinks to somewhere between 400 and 500 locations over the next five years as underperforming leases expire and are not renewed. The company becomes a smaller, more focused regional player rather than a national brand. Eventually, it is either taken private at a modest premium to the market price or merged with a competitor in a consolidation play that creates incremental cost savings but does not solve the underlying demand challenge.

This is not a story of management failure. Rick Brooks and his team have managed the decline with more skill and discipline than virtually any comparable company. This is a story of structural change: the business model that Zumiez was built on, selling youth culture through mall-based physical retail, is dying. Zumiez is just dying slower than most.

KPIs That Matter Most

For investors tracking this story, two metrics matter above all others.

North American comparable store sales growth is the single most important indicator of whether the core business is stabilizing or continuing to decline. Comparable sales, or "comps," measure revenue growth at stores that have been open for at least a year, stripping out the effect of new store openings and closures. This metric isolates the organic health of the business: are existing customers spending more, are new customers finding existing stores, or is the customer base eroding? The 5.5 percent comp growth in the most recent quarter was encouraging, particularly after multiple quarters of declines. But one quarter does not make a trend. Sustained comp growth above three percent for four or more consecutive quarters would be the most convincing signal that the traffic decline has genuinely reversed rather than merely paused.

Gross margin percentage tells the story of pricing power, inventory management, and the balance between third-party brands and private label. Gross margin is calculated as revenue minus the cost of goods sold, divided by revenue, essentially measuring how much of each sales dollar remains after paying for the products themselves. For Zumiez, this metric captures everything from vendor pricing power to promotional activity to the mix between full-price and markdown sales. The 200-basis-point improvement to 38.2 percent in the most recent quarter suggests that the company is regaining some control over its product economics. For context, gross margin was 39 percent at the peak and fell to 32 percent during the trough. If gross margin can stabilize above 36 percent on a full-year basis, the business can remain profitable at current revenue levels. If it falls back toward the 32-34 percent range that characterized the loss years, the path to sustainable profitability becomes much more difficult.

XIII. Lessons & Playbook

For Founders

The Zumiez story contains a masterclass in the lifecycle of culturally-driven businesses. Tom Campion proved that cultural authenticity can be monetized at scale: from a single Seattle skate shop to a seven-hundred-store international operation. But the story also demonstrates the fragility of that authenticity. When you build a business on the proposition that you are the authentic representative of a subculture, every step toward mainstream success erodes the very thing that made you distinctive. Fifty stores felt like an insider's network. Seven hundred stores felt like a corporation.