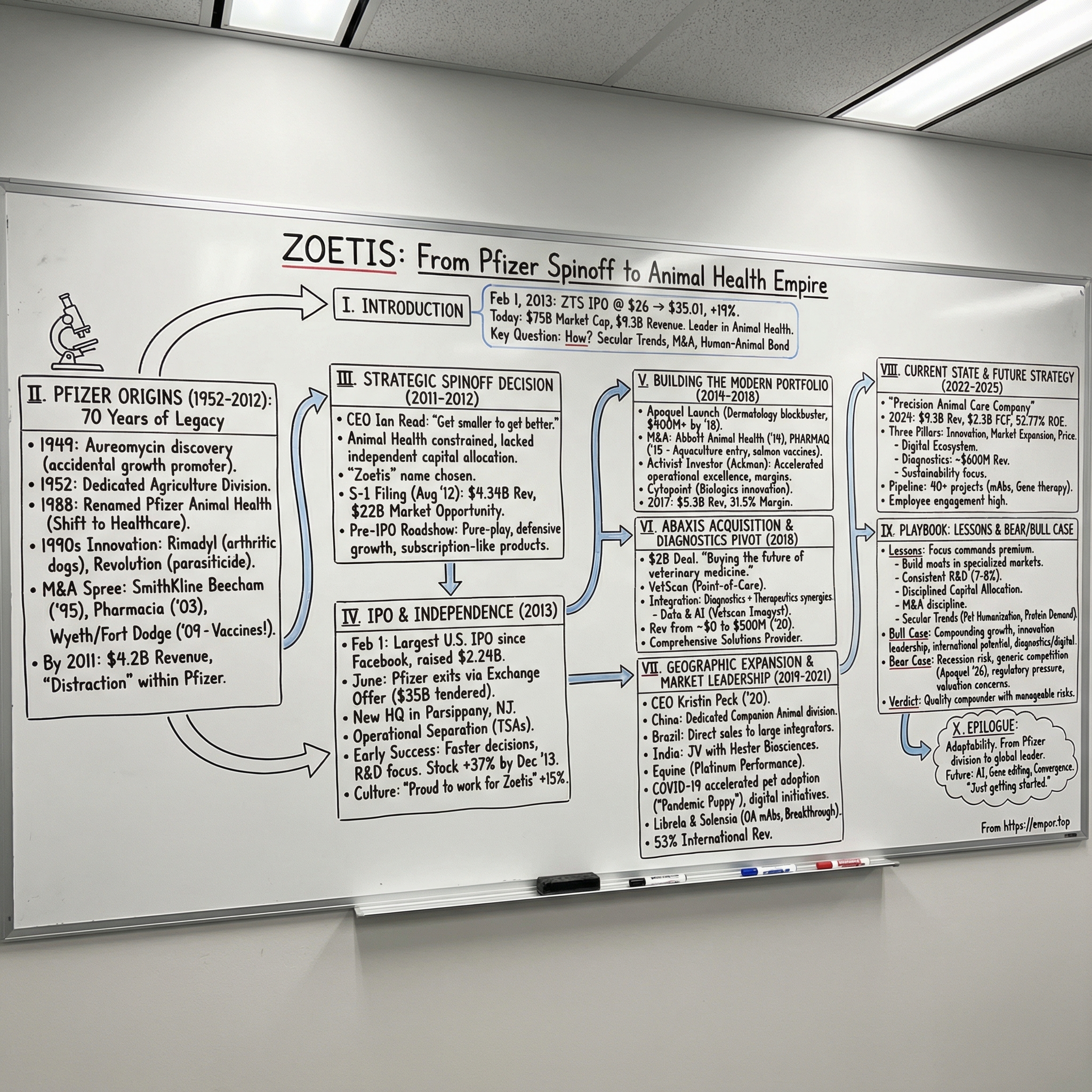

Zoetis: From Pfizer Spinoff to Animal Health Empire

On February 1, 2013, a Spanish-born executive who never expected to run an S&P 500 company stepped up to the podium at the New York Stock Exchange and rang the opening bell. Behind him stood a familiar cast for an IPO: Pfizer executives, investment bankers, and a crowd of employees wearing brand-new Zoetis badges. In front of them was something far rarer: a company that had been independent for, essentially, zero days.

The market didn’t care. When trading began, shares jumped about nineteen percent above the offering price. Overnight, a business that had spent decades inside Pfizer was being priced like a standalone category king.

Even the name sounded like a startup trying to will itself into existence. Zoetis. Pronounced zo-EH-tis. It comes from “zoetic,” a little-used English adjective rooted in the Greek zoe, meaning life. You can imagine how many people in that room had to double-check the spelling.

But the company behind the word was anything but small. This was the world’s largest animal health business, carved out of Pfizer’s roughly seventy-year veterinary legacy. And it was on its way to becoming the biggest U.S. IPO since Facebook.

Fast forward to today, and Zoetis looks less like a spinoff and more like an institution. It brings in nearly $9.5 billion a year in revenue, employs about 13,800 people, and sells more than 300 product lines spanning eight species across more than 100 countries. In companion animal health, it holds roughly a quarter of the market. The stock that opened at $31.50 on that first trading day sits around $130 in February 2026—one of the standout spinoff success stories of the last twenty years.

So the question at the heart of Zoetis is deceptively simple: how does a division tucked inside one of the world’s biggest pharmaceutical conglomerates turn into the dominant force in an entire industry?

The answer is a string of bets—on pet “humanization,” on monoclonal antibodies for dogs, on diagnostics as a recurring-revenue engine, and on the conviction that animal health should get the same innovation firepower as human health. Many of those wagers have paid off. One, in particular—a breakthrough osteoarthritis treatment called Librela—has also become one of the most closely watched risk factors in the portfolio.

This is the story of how a Pfizer castoff became an empire.

The Pfizer Origins: Building on 70 Years of Legacy

In 1950, deep inside Pfizer’s research labs, a discovery landed that would quietly bend the company’s trajectory for decades. Terramycin—oxytetracycline—was a broad-spectrum antibiotic that worked against a staggering range of infectious organisms. The FDA approved it on March 15, 1950, and it quickly became one of Pfizer’s most versatile medicines.

Then someone tried it in animals. And it worked just as well.

Terramycin proved highly effective in cattle, poultry, and swine—the same kinds of infections, the same basic biology, and a market that was hungry for reliable, affordable treatment. Pfizer hadn’t set out to build a veterinary business. But it had accidentally found a wedge into one.

The economics did the rest. Livestock producers needed medicines that were dependable and cheap at scale. The animal-drug regulatory pathway, while still rigorous, tended to move faster and cost less than human pharma. And once a producer found something that kept respiratory disease out of a herd, they didn’t casually switch. Not because of contracts, but because the “switching cost” was risk: you don’t experiment mid-season with thousands of animals on the line just to shave pennies off a dose.

By 1952, Pfizer had seen enough to make it real. The company established an Animal Agriculture Division and opened a roughly 700-acre farm and research facility in Terre Haute, Indiana—a rare kind of campus where lab science and real-world husbandry lived side by side. Researchers didn’t just run tests in controlled rooms; they walked out into barns, feedlots, and muddy pastures to observe disease and trial treatments under the conditions farmers actually faced.

That detail mattered. Terre Haute wasn’t simply an R&D site—it was a cultural imprint. Pfizer’s animal health teams learned, early, that a great drug on paper isn’t enough. It has to work in the messiness of real operations, with real constraints, and real economics. Decades later, that institutional muscle—understanding how veterinarians, ranchers, and producers actually used products—would become a quiet competitive advantage.

For the next thirty years, the division grew steadily without becoming a headline. Inside Pfizer, animal health was a solid business, but it wasn’t the main event. The blockbuster human medicines eventually associated with Pfizer—Lipitor, Viagra, Zoloft—captured the attention, the margin, and the prestige. Animal health sat in the background: profitable, predictable, and largely invisible to Wall Street.

In 1988, the unit was renamed Pfizer Animal Health. And in the 1990s, the pace changed.

The world around it was shifting. Pet ownership in the U.S. was rising, and the cultural framing of pets was moving from “property” to “family.” Veterinary medicine was professionalizing, clinics were getting better equipped, and owners were increasingly willing to pay for advanced care. Companion animals were turning into a serious market, not a side category.

Pfizer kept building in both worlds—livestock and pets. In 1993, it launched Dectomax, a broad-spectrum parasiticide for livestock that became one of its best-selling products and is still used today. In 1995, Pfizer acquired SmithKline Beecham’s animal health division, a deal that did something bigger than add revenue. It gave Pfizer a meaningful foothold in vaccines and companion animal care.

That was a strategic pivot. Up to then, Pfizer Animal Health leaned heavily livestock—cattle, swine, poultry. SmithKline brought dogs and cats into the center of the story. It also brought vaccine capabilities, which behave differently than pharmaceuticals: prevention becomes routine, logistics matter, and the revenue can be steadier. With therapeutics and biologics under one roof, Pfizer Animal Health now had a breadth that few competitors could match.

Then came a run of products that, in hindsight, read like the template for what Zoetis would later become.

In 1997, Pfizer launched Rimadyl, the first non-steroidal anti-inflammatory drug approved specifically for dogs. It gave vets a real option for chronic pain in aging pets—something far beyond aspirin and a resigned “he’s slowing down.” That same year also brought Clavamox, an anti-infective for dogs and cats.

In 1999, Revolution became the first FDA-approved topical medicine that combined heartworm protection, flea control, and ear mite treatment in one application. In 2004, Draxxin delivered a full course of antibiotic therapy for livestock in a single injection—an operational win for ranchers managing animals across huge acreages. In 2006, Convenia brought that same single-dose convenience to cats with bacterial skin infections.

And the category creation kept going. In 2007, Cerenia became the first antiemetic developed specifically for dogs—because yes, dogs get nausea and motion sickness, and no, there hadn’t been an approved veterinary solution before. In 2008, Palladia raised the bar again: the first FDA-approved cancer drug for dogs, targeting mast cell tumors with a tyrosine kinase inhibitor.

These weren’t me-too products. They were firsts. Pfizer Animal Health wasn’t just selling into existing demand; it was inventing new standards of care—giving veterinarians tools they simply hadn’t had. That instinct—solve a real clinical problem with something truly differentiated—would become a defining part of the Zoetis playbook.

At the same time, Pfizer’s dealmaking was reshaping the industry around it.

The most consequential transaction came in October 2009, when Pfizer acquired Wyeth for approximately $68 billion. The headline rationale was human pharma—vaccines and biologics. But inside Wyeth sat Fort Dodge Animal Health, and bringing it in helped make Pfizer Animal Health the global leader in veterinary vaccines and medicines. Regulators required Pfizer to divest certain Fort Dodge assets—primarily some cattle and small animal vaccines, along with the manufacturing facility in Fort Dodge, Iowa—to Boehringer Ingelheim. Even so, the outcome was unmistakable: Pfizer’s animal health division now held one of the broadest portfolios in the industry across beef, dairy, companion animals, swine, equine, and poultry.

A year later, Pfizer bought King Pharmaceuticals for $3.6 billion, and with it came Alpharma, a leader in feed additive products for food-producing animals. By 2011, Pfizer Animal Health was generating more than $4.2 billion in annual revenue and operating across virtually every corner of the global veterinary market. R&D headquarters had been established in Kalamazoo, Michigan in 2003, and Pfizer added more pieces through acquisitions including Embrex (poultry devices and vaccines, 2006), Catapult Genetics and Bovigen (animal genetics and DNA technology, 2007), and CSL Animal Health (Australian and New Zealand pipeline, 2003).

By the early 2010s, the division wasn’t a side business anymore. It was a powerhouse—arguably one of the strongest assets inside Pfizer that the market couldn’t clearly see.

And that was the tension. Inside Pfizer, animal health still had to compete for capital and attention against human drugs with far larger revenue pools. In R&D budget debates, animal health was almost always going to lose to the next potential Lipitor. In analyst models, it was a line item, not a thesis.

Pfizer Animal Health had become excellent—but it was also structurally undervalued and strategically constrained. The obvious question was starting to feel inevitable: would it be worth more on its own?

The Strategic Spinoff Decision

On July 7, 2011, Pfizer CEO Ian Read did something that, in retrospect, made the Zoetis story inevitable. He announced that Pfizer would explore “strategic alternatives” for its Animal Health and Nutrition businesses. That phrase is corporate code for a short menu: sell them, spin them, or take them public. But the real message was simpler: these businesses were probably worth more—and would operate better—outside the gravitational pull of a giant human-pharma company.

The timing wasn’t subtle. Pfizer was heading straight into the Lipitor patent cliff. Lipitor had been the most profitable drug in pharmaceutical history, and losing exclusivity meant Pfizer needed to shrink distractions, protect cash flow, and re-center the company around its next wave of human medicines. Meanwhile, Wall Street was newly enthusiastic about separations. Spinoffs and divestitures were surging, and the logic was easy to explain: conglomerate discounts are real. Focused companies often earn higher valuations than divisions buried inside diversified parents.

Read put it bluntly: “We are better positioned to focus on our core business as an innovative biopharmaceutical company by unlocking value from the animal health business.” Translation: animal health is excellent. It’s just no longer core to Pfizer’s identity.

Once that decision was in motion, the work became very practical, very fast. This division needed to become a real company—on paper and in the minds of investors. It needed a name, a board, leadership, a capital structure, and a narrative compelling enough to sell shares in a standalone entity that had never existed before.

The name came first. Pfizer brought in branding help—marketing consultants, linguists, the whole exercise—and landed on Zoetis, derived from “zoetic,” meaning “pertaining to life.” It was unusual. Many people didn’t know how to pronounce it. But it was distinctive, globally usable, and, crucially, it arrived with no history attached. For a business trying to step out from under Pfizer’s shadow after seven decades, a blank slate was exactly the point.

Next came the leadership question. Juan Ramón Alaix, who had led Pfizer Animal Health since 2006, was the obvious CEO choice. But “obvious” hides how unconventional his path was.

Alaix was born in Barcelona, moved to Madrid at age ten, and earned a graduate degree in economics from the University of Madrid. He started his career in finance roles in Spain—far from the traditional American pharma executive track. In the 1990s, he moved into general management at Rhône-Poulenc Rorer, eventually becoming general manager of the company’s Belgian operations in 1996. In 1998, he became country president for Pharmacia in Spain. When Pfizer acquired Pharmacia in 2003, Alaix relocated to the U.S. and took on a regional president role—usually the kind of career move that leads to a stable senior position, not the top job of a future S&P 500 company.

But he had a reputation for getting things done. In 2006, Pfizer made him President of Pfizer Animal Health, putting him in charge of strategy and performance for the whole division. Over the next six years, he expanded globally, integrated major acquisitions like Wyeth/Fort Dodge and Alpharma, and kept the product engine moving. He wasn’t flashy. He was an operator.

He was also candid about how little he’d planned for any of this. In Harvard Business Review, he later wrote: “It never crossed my mind to be a CEO of an S&P 500 corporation.” From 2011 to 2013, he also served as President of the International Federation for Animal Health, giving him a front-row seat to the industry’s global dynamics just as the business was preparing to step out on its own.

Behind the scenes, another Pfizer executive was instrumental in making the separation happen: Kristin Peck. At the time, she was Pfizer’s EVP of Worldwide Business Development and Innovation, and she was directly responsible for evaluating what Pfizer should do with Animal Health and Nutrition. Years later, she would follow the business to Zoetis, cycle through operating roles, and ultimately succeed Alaix as CEO. But in 2011 and 2012, her mandate was more fundamental: figure out whether this could be a viable independent company—and how to structure the exit.

The numbers made that case easier. Pfizer Animal Health generated $4.2 billion in revenue in 2011 and $4.34 billion in 2012. The global animal health industry was estimated at about $22 billion, which meant Pfizer Animal Health held roughly a fifth of the market—clearly the leader. The division employed around 9,300 people across dozens of countries. Margins were healthy. Growth was steady. And the business lacked one of the most punishing features of human pharma: the constant fear of a single patent expiration wiping out a giant chunk of revenue.

That last point matters because it helps explain why animal health businesses often command premium valuations. In human pharma, a blockbuster can throw off enormous revenue for years and then collapse almost overnight when generic competition arrives. Lipitor is the classic example: it fell dramatically within a couple of years of losing exclusivity. Animal health tends to decay more slowly. Veterinary generics face a more fragmented set of regulatory approvals across countries. Individual product markets are smaller, which can reduce the incentive for copycats. And veterinarians, like physicians, develop strong preferences based on what works in practice—preferences reinforced by longstanding relationships with sales reps and the habit of sticking with trusted brands.

By August 2012, Pfizer had made the call. On August 10, it filed to register Zoetis Class A stock with the SEC. The spinoff was no longer a concept—it was a process with deadlines. The pitch to investors leaned on the same themes that had made the division so valuable inside Pfizer: durable demand, rising spend on companion animals, and a livestock portfolio that behaved like a steady backbone.

The question wasn’t whether Zoetis would happen anymore. It was what the market would decide it was worth.

The IPO and Independence

The pricing call came on January 31, 2013. Pfizer’s bankers—JPMorgan Chase, Bank of America Merrill Lynch, and Morgan Stanley—had gone out with an expected range of $22 to $25 per share. Then the orders started piling up. The IPO was reportedly between ten and twenty times oversubscribed, a signal that the market wasn’t just interested—it was fighting for allocation. The banks priced the deal at $26, above the top end of the range.

Investors were eager because Zoetis offered something the IPO market rarely does: a grown-up business. Decades of operating history. Real profits. A leadership position in a category with attractive tailwinds. And for institutional investors—especially healthcare-focused funds—it was a long-awaited way to buy animal health directly, not as a footnote inside a pharma conglomerate.

The next morning, February 1, Juan Ramón Alaix rang the NYSE opening bell. Zoetis shares opened at $31.50—about twenty-one percent above the IPO price—and finished the day at $35.01, up roughly nineteen percent. The offering raised about $2.2 billion at the initial pricing, and about $2.57 billion after underwriters exercised their overallotment option, for a total of 99 million shares sold. It was the biggest U.S. IPO since Facebook nine months earlier. And unlike Facebook, which notoriously struggled out of the gate, Zoetis looked like it had been public for years.

But there was a catch—one that mattered a lot if you were thinking about what this meant for Zoetis as a company. Zoetis didn’t get the money. Every dollar of IPO proceeds went to Pfizer. This was Pfizer turning the crank on a monetization plan, not Zoetis raising growth capital.

At the same time, Zoetis took on real financial weight of its own. To fund the separation, the company issued $3.65 billion in senior notes in a private placement. In other words: Zoetis started its public life with substantial debt and without the comfort of Pfizer’s balance sheet behind it. No parental backstop, no easy bailouts—just a new ticker symbol and an immediate need to perform.

Pfizer also wasn’t done. After the IPO, it still held 414 million Class B shares—roughly eighty percent of Zoetis. So Zoetis was public, but not truly independent. Pfizer controlled governance, had board influence, and could still shape major decisions. If you bought Zoetis stock in the IPO, you were betting on Zoetis’s future while Pfizer still had its hands on the wheel.

That awkward in-between period didn’t last long. On May 21, 2013—less than four months later—Pfizer announced it would exit through an exchange offer. Pfizer shareholders could swap Pfizer shares for Zoetis shares at a seven percent discount, capped at 0.9898 Zoetis shares per Pfizer share. The design was clever: it gave Pfizer shareholders an incentive to participate, and it let Pfizer unwind its stake without simply dumping shares into the open market.

The exchange was massively oversubscribed. About 868 million Pfizer shares were tendered, far more than the roughly 405 million that could be accepted. On June 24, 2013, Pfizer exchanged all 401 million of its Zoetis shares and fully severed ownership.

Just like that, Zoetis was actually on its own. From IPO to full separation took less than five months—remarkably fast for a deal of this size, and a sign of two forces pulling in the same direction: Pfizer’s urgency to simplify, and the market’s appetite for a pure-play animal health leader.

With Pfizer executives off the board, Zoetis reshaped its leadership. Michael McCallister became Non-Executive Chairman, and new independent directors, including Sanjay Khosla and Robert Scully, joined—fresh eyes, and fewer inherited reflexes from Pfizer’s culture.

Then came another milestone that basically stamped Zoetis as “fully mainstream” overnight. S&P Dow Jones Indices announced Zoetis would join the S&P 500, replacing First Horizon National Corporation. For a company that had been a division months earlier, it was a startlingly fast arrival. And it mattered mechanically: index funds tracking the S&P 500 had to buy the stock, creating structural demand and expanding the shareholder base beyond the healthcare specialists who had crowded into the IPO.

Alaix’s first job as CEO of an independent company was less about products and more about identity. Zoetis had about 9,300 employees who’d grown up inside Pfizer—Pfizer systems, Pfizer benefits, Pfizer ways of working. Alaix talked about creating “new corporate DNA.” And he pushed on three fronts at once: prove the company could deliver near-term results, build a culture that was distinct from Pfizer’s, and keep investing in innovation that could separate Zoetis from every other player in the category.

The early numbers suggested the plan was working. Revenue rose from $4.34 billion in 2012 to $4.6 billion in 2013 and $4.8 billion in 2014. Zoetis wasn’t merely surviving the split—it was gaining momentum.

And the clearest proof point was about to arrive in the form of a small tablet that would redraw the veterinary dermatology market.

Building the Modern Portfolio

In late 2013 and into early 2014, veterinarians around the U.S. started hearing the same rumor from colleagues and Zoetis reps: there was a new drug for allergic dermatitis in dogs that worked almost immediately.

If you’ve ever lived with a dog that can’t stop itching, you know how brutal this condition is. The constant scratching isn’t just annoying—it’s self-injury. Skin breaks down, infections follow, antibiotics enter the picture, and the whole cycle repeats. For years, vets had been stuck with a handful of imperfect tools: steroids that worked but came with real long-term side effects, antihistamines that usually didn’t do much in dogs, and cyclosporine that could be slow and expensive. None of it felt like a clean, modern solution designed for the canine immune system.

Apoquel was different. It was the first Janus Kinase inhibitor approved for veterinary use, and it went straight at the signaling pathway that drives itch. The result was what made it famous: speed. Many dogs got relief within hours—often within about four. It didn’t feel like incremental progress. It felt like a new standard of care.

When Apoquel launched in 2014, demand hit so hard that Zoetis ran into supply shortages. The company had to ration product and scramble to expand manufacturing capacity—an early, unmistakable signal that this was more than a niche win.

Apoquel also crystallized Zoetis’s emerging identity as an independent company: it was willing to do real pharma innovation for animals, not just adapt human drugs for veterinary use. And it landed right as the companion animal market was changing shape. Pet owners—especially younger ones—were increasingly treating dogs and cats like family, which pulled spending and expectations upward. At the clinic, the conversation was shifting from “Is this worth it?” to “What’s the best option?”

The veterinary business model amplified that shift. In human pharma, insurance companies and pharmacy benefit managers sit between the drug and the patient, negotiating prices and controlling access. In animal health, it’s far more direct: the veterinarian recommends a treatment and the owner pays. That dynamic rewards products with obvious, visible results. Apoquel had that in spades. When a dog that’s been scratching itself raw stops the same day, you don’t need an advertising campaign. The outcome sells the product.

Zoetis doubled down on dermatology the next year. In 2015, the USDA granted a conditional license for Cytopoint, a monoclonal antibody that targets canine interleukin-31—the key cytokine involved in sending itch signals. Cytopoint received its full USDA license in December 2016.

The pairing was elegant. Apoquel was a daily oral tablet. Cytopoint was an injection administered by a veterinarian every four to eight weeks. They weren’t head-to-head substitutes so much as different answers for different dogs and different owners. Some patients did well with daily home dosing. Others benefited from a longer-acting injection that didn’t depend on perfect owner compliance. Veterinarians liked having both tools. Zoetis liked something else: two differentiated products in the same high-value category, with different delivery formats and mechanisms—built-in diversification if one ever faced competition or scrutiny.

By 2025, Apoquel and Cytopoint together would be generating about $1.7 billion in annual revenue. What started as “a new itch drug” became a franchise bigger than many entire pharmaceutical companies.

But Zoetis wasn’t planning to rely on organic growth alone. Alaix and his team pursued a disciplined M&A program—mostly targeted deals meant to widen the portfolio, add new capabilities, and open up new species and geographies.

In November 2014, Zoetis bought a portfolio of pet drugs from Abbott Laboratories for $255 million, a bolt-on acquisition designed to fill gaps in the companion animal lineup. That same month, activist investor Bill Ackman revealed that Pershing Square had built an 8.5% stake—about 42 million shares. The stock jumped to its highest price since the IPO. Ackman’s presence did two things at once: it validated Zoetis as a serious value-creation story, and it raised the bar for management on operational execution, capital returns, and strategic ambition.

The boldest acquisition of this stretch came in November 2015, when Zoetis paid $765 million for PHARMAQ, a Norwegian company and the global leader in vaccines for farmed fish. On the surface, a fish vaccine business looked worlds away from dog dermatology. Strategically, it fit. Aquaculture was the fastest-growing protein category globally, and fish farming—like cattle or poultry—runs on industrial scale, tight margins, and relentless disease-management needs. PHARMAQ’s market was growing around ten percent annually, and the company had been compounding revenue at about seventeen percent a year for a decade. Its $80 million of 2014 revenue was small inside Zoetis, but the growth and the margins were the point. And Zoetis’s core strengths—regulatory navigation, manufacturing quality, global distribution—translated well.

Then, in April 2017, Zoetis made a bet that was small in purchase price but massive in implications: it acquired Nexvet Biopharma for about $85 million, a roughly 66% premium to the prior closing share price. Nexvet was headquartered in Tullamore, Ireland, with R&D operations in Melbourne, Australia, and it brought a platform with a memorable name: PETization.

Here’s why it mattered. Monoclonal antibodies are engineered proteins designed to bind to specific targets in the body. In human medicine, they became one of the most important classes of drugs in the world—think Humira, Keytruda, Herceptin. But you can’t simply take a human monoclonal antibody and give it to a dog. The dog’s immune system would see it as foreign, mount a response, and potentially neutralize it or cause safety issues. Nexvet’s PETization platform was built to solve that problem by engineering antibodies that were “caninized” or “felinized,” designed to be recognized as “self” by the animal’s immune system.

That technology became the biological foundation for what would eventually become Librela and Solensia, Zoetis’s monoclonal antibody treatments for osteoarthritis pain in dogs and cats. At the time, the chronic pain market in companion animals was estimated around $400 million annually—large enough to justify a push. But the bigger prize was the platform: a way to create a whole new class of veterinary biologics, potentially across multiple diseases.

By 2018, the transformation was obvious in the results. Revenue had risen from about $4.3 billion at the IPO to nearly $5.8 billion. Adjusted EPS increased from roughly $1.77 in 2015 to $3.13 in 2018. The stock had tripled from its IPO price. And Alaix won the Deming Cup for Operational Excellence from Columbia Business School—recognition that the quiet operator who never expected to run a public company had built one the market couldn’t ignore.

But he wasn’t finished. The next move would take Zoetis into an entirely new line of business.

The Abaxis Acquisition and the Diagnostics Pivot

On the morning of May 16, 2018, Zoetis announced it would acquire Abaxis, a California-based maker of veterinary diagnostic instruments, for $83 per share in cash—about $2 billion. It was, by a wide margin, the largest acquisition in Zoetis’s history. And it wasn’t just “buying another product line.” It was Zoetis deliberately stepping into a new kind of business.

To see why, zoom in on how a veterinary clinic actually makes money. A dog comes in for a routine visit. The vet does the exam, gives vaccines, and sends the owner home with preventives—flea and tick, heartworm, maybe a daily allergy medication. That’s the pharmaceutical side.

But the engine of modern veterinary care is increasingly diagnostics. Blood chemistry panels. Complete blood counts. Urinalysis. Rapid tests for heartworm and tick-borne diseases. Diagnostics give the vet the data to make better decisions, but they also generate high-value revenue for the clinic. And they come with a powerful business model: once a clinic installs a diagnostic machine, it keeps buying the proprietary consumables that run on that machine.

At the time, the veterinary diagnostics market was estimated at more than $3 billion and had been growing at roughly ten percent annually for the prior three years. IDEXX Laboratories was the heavyweight in the space, but Abaxis had built a meaningful position with its VetScan portfolio of point-of-care diagnostic instruments and consumables. VetScan, in particular, fit smaller clinics and many international settings well, where portability and simplicity weren’t nice-to-haves—they were the product.

For Zoetis, the attraction was that diagnostics could change the relationship with the customer. Pharmaceuticals are episodic: prescribe a drug, fill a prescription, revenue is booked, and the moment ends. Diagnostics can be structural. When a clinic installs a VetScan instrument, it becomes part of daily workflow. The clinic reorders chemistry discs, hematology cartridges, and rapid test kits on a steady cadence. The switching costs are real because those consumables are tied to the platform, and the platform is tied to how the clinic operates. It’s the razor-and-blade model applied to veterinary medicine, and it can produce annuity-like revenue that drug sales alone don’t.

Alaix framed the ambition in language that matched how vets think about care: “Together we can bring more veterinarian customers comprehensive solutions to predict, prevent, detect and treat disease in animals.” That first word—predict—was the tell. It signaled Zoetis’s intent to move upstream, from treating what’s already obvious to identifying risk before symptoms fully show up.

Abaxis, founded in 1989 and headquartered in Union City, California, reported $245 million in revenue for its fiscal year ending March 2018, with about twenty percent coming from international markets. It was also investing in the connective tissue of modern practice. Recent launches included the VetScan FLEX4 Rapid Test for heartworm, Lyme, Ehrlichia, and Anaplasma, and the VetScan FUSE connectivity system, which integrated diagnostic instruments with practice management software. Zoetis funded the acquisition with existing cash and new debt, and the deal closed on July 31, 2018. Integration moved faster than planned, and Zoetis began using its global distribution muscle to place VetScan instruments in markets where Abaxis had been relatively underpenetrated.

Over time, the strategic logic got even sharper. Diagnostics didn’t just add revenue—it created a hub inside the clinic. A vet who prescribes Apoquel has a transactional relationship with Zoetis: recommendation, purchase, done. A vet running VetScan has an operational relationship: the machine is used every day, consumables are reordered constantly, and the resulting data shapes treatment decisions that can lead directly to prescriptions—including Zoetis prescriptions. Abaxis gave Zoetis a way to embed itself into the workflow of veterinary medicine, not just the pharmacy shelf.

Then Zoetis widened the diagnostic footprint beyond in-clinic machines. Over the following years it expanded into reference labs through acquisitions: Phoenix Lab in Seattle (acquired October 2019, with more than thirty years of diagnostic experience serving twenty states), ZNLabs in Louisville (November 2019, with satellite facilities in six cities), and Ethos Diagnostic Science with locations in Boston, Denver, and San Diego (February 2020). Now Zoetis could offer both point-of-care testing in the clinic and send-out testing through a growing U.S. lab network—two complementary pieces of the same diagnostics strategy. By 2025, companion animal diagnostics was growing at thirteen percent operationally—faster than any other segment in the portfolio, with U.S. diagnostics up fourteen percent and international up eleven percent. The razor-and-blade bet was working.

In a way, Abaxis also felt like the closing move of Zoetis’s first era. Alaix had taken a division inside Pfizer and, in just a few years, turned it into a standalone company with leadership positions in pharmaceuticals, biologics, and now diagnostics. The CEO who never expected to run a Fortune 500-caliber business had built one of the defining spinoff success stories of modern corporate history.

Geographic Expansion and Market Leadership

In January 2020, Kristin Peck became CEO of Zoetis. Her timing was, to put it mildly, dramatic. Within weeks, a novel coronavirus began spreading around the world, setting off lockdowns, supply chain chaos, and the sharpest economic shock since the Great Depression.

Peck’s path to the top didn’t look like the typical animal health résumé. She studied at Georgetown, earned her MBA at Columbia, and started out in a mix of strategy and finance—Boston Consulting Group, private equity, and real estate finance at J.P. Morgan. She joined Pfizer in 2004 in business development, eventually becoming EVP of Worldwide Business Development and Innovation—the job that put her at the center of the decision to spin animal health out in the first place. In other words, she had helped architect Zoetis’s independence. Now she was inheriting the operating reality.

After moving over to Zoetis in 2012, she ran a deliberately broad gauntlet of roles—global manufacturing and supply, global poultry, diagnostics, corporate development, U.S. operations. It read like succession planning in real time. When the board named her CEO, she became one of fewer than forty women leading a Fortune 500 company.

Her style also marked a shift from Juan Ramón Alaix. Where Alaix was measured and private—results first, always—Peck was more visible and explicitly culture-driven. She pushed the idea of being “customer obsessed” and anchored management around five principles: customer focus, ownership mentality, doing the right thing, valuing colleagues, and acting as one company.

She also tightened the company’s posture on capital allocation. Under her leadership, dividends and buybacks scaled up, and Zoetis grew more willing to use the balance sheet to fund shareholder returns. The clearest example came later, in December 2025, with a convertible bond offering that helped fund $1.75 billion in repurchases.

Externally, Peck became a face of the business in a way Zoetis hadn’t really had before. She later landed on TIME’s list of the 100 Most Influential People in Health in 2025, Barron’s top CEO list, and Fortune’s Businessperson of the Year rankings. She also took board seats at BlackRock, the Mayo Clinic, and Columbia Business School—signals that animal health was no longer being treated as a pharmaceutical side quest.

Then, oddly, the pandemic delivered Zoetis a tailwind.

Lockdowns triggered a surge in pet adoption across the developed world. People stuck at home wanted companionship. Shelters that had struggled for years suddenly had waiting lists. Breeders couldn’t keep up. The American Pet Products Association estimated that U.S. pet ownership rose from sixty-seven percent of households to seventy percent during the pandemic—millions of new pet-owning households in a single year.

Those new owners then did what new owners do: they went to the vet. Vaccinations. Wellness visits. Preventives. The demand wave lifted companion animal spending for years, and it skewed toward exactly the customer Zoetis served best—owners treating pets like family, comfortable paying for premium care, and increasingly willing to research options and ask for the “best” version of treatment.

But Peck’s most consequential early win wasn’t just riding that demand. It was getting Zoetis’s monoclonal antibody franchise across the regulatory finish line.

The science traced back to the 2017 Nexvet acquisition. The target was Nerve Growth Factor, a protein central to pain signaling. Block NGF with a species-specific monoclonal antibody, and you could deliver sustained osteoarthritis pain relief without the gastrointestinal and renal issues that can limit long-term use of traditional NSAIDs like Rimadyl.

Solensia—the cat formulation—won EU approval in May 2021 and FDA approval in January 2022. That FDA decision made Solensia the first monoclonal antibody new animal drug approved for use in any animal species. It was a landmark for the entire industry.

Monoclonal antibodies had already reshaped human medicine—Humira, Keytruda, and Herceptin alone sit in a class of therapies that collectively generate more than $50 billion a year and have rewritten standards of care across autoimmune disease and cancer. But veterinary medicine had never truly cracked the category. Part of that was technical: engineering antibodies that an animal’s immune system won’t reject is hard. And part of it was economic: pet owners pay out of pocket, so pricing has to work without the cushioning effect of insurance. Solensia proved Zoetis could make the science work.

Librela—the dog formulation—followed with FDA approval on May 5, 2023. Together, Librela and Solensia went after one of the biggest, most chronic problems in companion animal medicine: osteoarthritis pain. It affects an estimated forty percent of dogs and ninety percent of cats over age twelve. For decades, the toolkit was limited—NSAIDs that weren’t appropriate for many long-term cases, plus pain approaches adapted from human medicine that weren’t built for the realities of veterinary practice. Librela and Solensia offered something cleaner: a purpose-built, once-monthly injection using a fundamentally different mechanism.

While that franchise moved through approvals, Peck kept widening Zoetis’s footprint—especially in companion animals and diagnostics—through targeted acquisitions.

In August 2019, Zoetis acquired Platinum Performance, a California-based maker of premium nutritional products for horses, dogs, and cats. Founded in 1996 and based in Buellton, Platinum Performance had built a loyal following—especially among horse owners and veterinarians—around omega-3-based wellness supplements. Deal terms weren’t disclosed, but the strategic intent was clear: a small bet on the growing overlap between nutrition, prevention, and everyday pet health.

The reference lab roll-up also continued through 2019 and into 2020. Phoenix Lab, ZNLabs, and Ethos Diagnostic Science were folded in, extending Zoetis’s diagnostics presence across the U.S. and complementing the in-clinic Abaxis footprint with send-out testing capability.

And then came the product launch that, commercially, defined this era: Simparica Trio.

The FDA approved Simparica Trio on February 27, 2020. It became the first and only combination product offering all-in-one protection against heartworm disease, ticks, fleas, roundworms, and hookworms in a single monthly chewable for dogs.

The pitch was almost embarrassingly simple—and that’s why it worked. Before Trio, parasite protection often meant multiple products: heartworm, flea and tick, and deworming for intestinal parasites. That’s multiple prescriptions, multiple compliance talks, and multiple chances for an owner to miss a dose. Trio collapsed it into one chewable. One conversation. One monthly routine.

The original Simparica—a monthly flea and tick chewable—had been on the market since 2016. Trio added moxidectin for heartworm prevention and pyrantel for intestinal worms. In January 2022, it picked up an additional indication for prevention of Lyme disease. In April 2025, it added another for flea tapeworm prevention.

By 2025, the Simparica franchise was generating about $1.5 billion in annual revenue, growing twelve percent operationally, used by more than fifteen million dogs, and ranked as the number-one veterinarian-prescribed combination parasiticide. What’s striking is the durability: many pharma products slow down as they mature, but Trio kept taking share from older, single-purpose options.

Put it all together—pandemic-driven pet adoption, blockbuster launches, and steady geographic and capability expansion—and Zoetis’s revenue rose from $6.3 billion in 2019 to $8.1 billion in 2022. The company wasn’t just growing. It was widening the gap.

That gap shows up when you look at the competitive set. Zoetis fights three major rivals: Merck Animal Health (inside Merck), Boehringer Ingelheim Animal Health (inside the privately held German pharma giant), and Elanco Animal Health (spun out of Eli Lilly in 2018). All are credible, global competitors. But Zoetis has one structural advantage the others can’t easily reproduce: it’s the only large-cap company that is one hundred percent animal health.

When Merck allocates R&D dollars, animal health competes with Keytruda and the rest of human pharma. When Boehringer makes big bets, animal health sits alongside human pharma and biopharmaceutical priorities. Zoetis doesn’t have that internal fight. Every R&D debate, every management meeting, every strategic initiative is about animals. That focus shows up in the breadth of the portfolio—more than 300 product lines across eight species—and in the speed at which Zoetis keeps turning innovation into market leadership.

Current State and Future Strategy

Zoetis entered 2026 looking like the kind of business Wall Street loves: dominant share, sticky customers, premium margins, and a portfolio built around recurring, routine care. It also entered 2026 with one very real problem child. Start with the good news.

On February 12, 2026, Zoetis reported full-year 2025 results. Revenue came in at $9.47 billion, up six percent on an organic operational basis. About two-thirds of that growth came from pricing, with the rest from volume—an important signal. Zoetis wasn’t just riding a bigger pet population; it was capturing more value per dose and per visit.

Profitability stayed in rare air. Adjusted net income reached $2.8 billion, or $6.41 per diluted share, up seven percent organically. Adjusted gross margin expanded again, to 71.9 percent. And in the U.S., gross margin hit 83.5 percent—an almost absurd number in any healthcare category. It’s what you get when you combine differentiated, branded products with limited generic pressure and a distribution model that’s still largely driven by a trusted intermediary: the veterinarian.

Zoetis also leaned hard into shareholder returns. In 2025, it sent more than $4 billion back through $3.2 billion of share repurchases— including a $1.75 billion buyback funded by a convertible bond offering in December 2025—and about $800 million in dividends.

If you want the simplest read on where the company is, look at the mix. Companion animal—dogs, cats, and horses—made up roughly seventy percent of revenue and grew five percent. Livestock accounted for about twenty-nine percent.

Inside companion animal, the growth engines were exactly the modern Zoetis core: parasiticides, dermatology, and diagnostics. The Simparica franchise delivered $1.5 billion and grew twelve percent. Apoquel and Cytopoint together did $1.7 billion, up six percent. Diagnostics grew thirteen percent. These are products and services tied to routines—monthly protection, chronic conditions, repeat testing—not one-off interventions. That’s the annuity model Zoetis has been quietly building for a decade.

The species breakdown makes the strategic shift even more obvious. Dogs and cats generated $6.3 billion—about two-thirds of total revenue. Horses added $304 million. Cattle, the historical foundation of the business, contributed $1.5 billion. Swine brought in $466 million, poultry $432 million, and fish $286 million. The company that started in the barn now makes its money in the living room.

And yet livestock still matters. At $2.8 billion, the segment grew eight percent organically in 2025, even though reported results were weighed down by divestitures and currency effects. Cattle alone was nearly $1.5 billion, making Zoetis one of the largest cattle health suppliers in the world. Fish—powered by PHARMAQ—kept expanding as aquaculture scales globally. Analysts often gloss over livestock because it’s lower margin and usually slower growing than companion animal, but it brings real advantages: diversification by geography and species, a massive installed base of producer relationships, and exposure to emerging markets where protein demand is rising fastest.

Looking ahead, Zoetis guided to 2026 revenue of $9.825 billion to $10.025 billion—three to five percent organic operational growth—and adjusted diluted EPS of $7.00 to $7.10. Both midpoints were above Wall Street expectations when the company announced them.

Then there’s the headache: Librela.

When Librela launched in 2023, it looked like a classic Zoetis breakout—something that could become the next Apoquel. A once-monthly monoclonal antibody injection for osteoarthritis pain in dogs, with a novel mechanism and no direct competitor. It ramped quickly, reaching hundreds of millions of dollars in revenue within its first full year.

And then the adverse event reports began to mount.

In December 2024, the FDA issued a “Dear Veterinarian” letter, a form of communication that carries real weight in the profession. The FDA’s Center for Veterinary Medicine said it had identified 3,674 reports as of April 2024. The reported events included ataxia, seizures, and other neurologic signs such as paresis and recumbency; urinary incontinence; and, in some cases, death including euthanasia. The agency identified eighteen distinct safety signals.

Zoetis responded forcefully. It emphasized that more than 21 million doses had been distributed globally, and that no individual adverse event sign was reported at a rate higher than “rare” under the European Medicines Agency’s definition—fewer than ten per ten thousand treated animals. Zoetis framed the FDA letter as an informational update rather than a warning, and said it had the utmost confidence in Librela’s safety and efficacy.

In February 2025, Zoetis updated Librela’s label to add a post-approval experience section listing neurological side effects including ataxia, seizures, paresis, and paralysis. Veterinarians were advised to discuss potential adverse effects with pet owners before treatment.

Then, in May 2025, a study published in Frontiers in Veterinary Science raised a different kind of concern. It documented musculoskeletal adverse events—ligament and tendon injuries, polyarthritis, fractures, and suspected cases of rapidly progressing osteoarthritis—occurring about nine times more frequently in dogs receiving Librela than in dogs receiving NSAIDs. The study also noted that total musculoskeletal adverse events over forty-five months exceeded those of Rimadyl, the top-ranking NSAID, by roughly twentyfold. Librela is supposed to treat osteoarthritis pain. Any suggestion that it might, in some cases, worsen joint outcomes strikes at the heart of the product’s promise.

The commercial impact showed up in the numbers. Zoetis’s OA pain franchise—Librela plus Solensia—generated $568 million in 2025 and declined three percent operationally. Librela itself fell six percent, with a much sharper drop in Q4. Meanwhile, the European Commission opened an investigation into possible anticompetitive conduct related to Librela, adding a second layer of uncertainty: regulatory, not just clinical.

Zoetis’s response has been two-speed.

In the near term, it has focused on stabilizing Librela—more veterinary education, updated labeling, and a steady drumbeat around overall benefit-risk. On the most recent earnings call, management described monthly sales trends as stabilizing—not rebounding, but no longer falling at the late-2024 pace.

In the longer term, Zoetis is building the next wave of the franchise. It is developing Lenivia, a next-generation monoclonal antibody for OA pain in dogs designed to provide up to three months of relief from a single injection. Lenivia received Canadian approval in Q3 2025 and a positive opinion from the European Medicines Agency’s CVMP committee. EU and Canadian launches were expected in the first half of 2026, with U.S. approval anticipated in 2027. Zoetis is also advancing Portela, a long-acting formulation for cats.

Kristin Peck used that February 2026 earnings call to flag another issue investors can’t ignore: the customer. She pointed to “greater price sensitivity and tighter household budgets” for routine care among Gen Z and Millennial pet owners—the same cohorts that drove much of the pandemic-era adoption boom. The concern isn’t whether people love their pets; it’s whether economic pressure nudges them to delay wellness visits and routine prevention. That’s where Zoetis’s demand begins.

The pet humanization thesis doesn’t require unlimited spending. It requires that spending per pet rises over time as care becomes more medicalized: more vet visits, earlier diagnostics, more chronic-condition treatment. Zoetis is built for that world. Apoquel turns “itchy dog” from a nuisance into a treated condition. Simparica Trio makes comprehensive parasite prevention a simple monthly habit. Diagnostics catch problems earlier, which tends to pull more treatment through the system. But if routine care gets deferred, the whole flywheel slows.

Zoetis does have some insulation. Roughly forty percent of Simparica Trio and Apoquel sales already come through alternative channels like retail and e-commerce rather than directly through clinics, which can soften the blow if vet visit frequency wobbles.

Even with those cross-currents, the company’s innovation machine kept running. Zoetis said it advanced about 185 geographic expansion and lifecycle innovations in 2025 and had twelve potential blockbusters in development, each with the potential to exceed $100 million in annual revenue. In November 2025, it launched Vanguard Recombishield, a recombinant kennel cough vaccine featuring the first and only vaccine with pertactin protein—proof that even the “legacy” biologics side of the house can still produce real innovation.

And Zoetis kept reinforcing its diagnostics bet. In November 2025, it acquired the Veterinary Pathology Group in the UK and Ireland, extending its diagnostics laboratory network into Europe. It was another step toward the same endgame that motivated Abaxis: make Zoetis not just the company that sells the drug, but the company embedded in the daily workflow of veterinary medicine.

Playbook: Business and Investing Lessons

The Zoetis story offers lessons that reach far beyond animal health.

First: spinoffs can be one of the cleanest forms of value creation. Inside Pfizer, Animal Health was just that—an “other” business, buried in a conglomerate and priced like one. Investors couldn’t buy it directly, management couldn’t set its own priorities, and the market applied the standard conglomerate discount.

Independence flipped the switch. Zoetis suddenly got valued on its own merits—and animal health has a fundamentally different profile than human pharma. Demand is steadier. The industry is less defined by single patent cliffs. Growth is more predictable. When investors could finally underwrite those characteristics directly, the standalone multiple was meaningfully higher than what Pfizer’s structure ever allowed.

You can see it in the math. Around the IPO, Zoetis had roughly $4.3 billion in revenue and a valuation around $13 billion—about three times revenue. About twelve years later, revenue had grown to roughly $9.5 billion, but the market cap had climbed to about $57 billion—around six times revenue. The re-rating—investors deciding this is a higher-quality, more durable business than they once assumed—created as much or more value than the growth itself.

That’s what happens when a great business gets the right corporate wrapper. And it’s exactly why conglomerates sitting on “hidden” category leaders should pay attention.

Second: moats in healthcare aren’t one thing—they’re layers that reinforce each other. Zoetis’s first layer is innovation. The company has repeatedly launched first-in-class products that created, or reshaped, categories: Apoquel as the first JAK inhibitor for dogs, Cytopoint as a monoclonal antibody for atopic dermatitis, Solensia as the first FDA-approved monoclonal antibody new animal drug for any species, and Simparica Trio as the first all-in-one combination parasiticide. When you’re first, you don’t just win share—you set the default standard of care.

Then come relationships. Animal health is a relationship business in a way most investors underestimate. Veterinarians are the gatekeepers, and their preferences harden over time through clinical experience, trust, sales-rep support, and continuing education. Zoetis has one of the industry’s largest dedicated animal health sales forces, with direct marketing operations in about forty-five countries. That footprint isn’t just a distribution engine; it’s a feedback loop. It keeps Zoetis close to clinic-level reality and lets it spot shifts in demand and competitive behavior early.

Add regulatory expertise. Getting an animal drug approved in one country is difficult. Getting it approved across a hundred—each with its own framework, data expectations, and timeline—is a capability that takes decades to build. That institutional know-how becomes a real barrier to entry, and it compounds over time.

And then there’s diagnostics, where the moat looks more like software than pharma. Once a clinic installs VetScan equipment, integrates it into workflow, and trains the team, switching becomes painful. Consumables become routine reorders. That makes the revenue base more predictable and harder for competitors to pry loose.

Third: capital allocation matters more when the core business is already great. Zoetis throws off substantial free cash flow, in part because it doesn’t require massive capital expenditure to keep growing. In 2025, it returned more than $4 billion to shareholders while still funding R&D and selective acquisitions. The framework is simple and repeatable: invest in innovation first, buy capabilities when it makes strategic sense, and return excess cash through buybacks and dividends. The company’s return on equity has consistently topped fifty percent—a signal not just of operating strength, but of a balance sheet and capital-return approach built to maximize per-share outcomes.

That same discipline shows up in M&A. Alaix and Peck largely avoided empire-building deals and instead chose targeted bolt-ons that filled specific gaps: Abbott’s pet drug portfolio for $255 million, PHARMAQ for $765 million to enter aquaculture, Nexvet for about $85 million to secure monoclonal antibody technology, and Abaxis for roughly $2 billion to build a diagnostics platform. Even the biggest one—Abaxis—was about capability expansion, not size for its own sake. The deals were meaningfully strategic, absorbable operationally, and funded without equity dilution, preserving the economics for existing shareholders.

The final lesson is the most foundational: the human-animal bond is a secular driver, not a cyclical one.

Pet humanization—the shift from “pet” to “family member”—has been building for decades and hasn’t shown signs of reversing. The U.S. spends more on pets than ever. And while the pandemic accelerated adoption, the deeper forces are demographic and cultural: smaller families, delayed parenthood, urbanization, and more people living alone. In that world, pets aren’t a nice-to-have accessory. They’re a central source of companionship, and that changes how owners respond to medical decisions.

Zoetis positioned itself right in the middle of that shift by building a portfolio that spans prevention, diagnosis, and treatment—and now chronic pain management, too. As veterinary care becomes more medicalized and more data-driven, more of the spend flows through products like Zoetis’s. That’s the flywheel the company has been building since the day it stepped out of Pfizer’s shadow.

Analysis: Bear vs. Bull Case

The Bull Case

The bull case for Zoetis comes down to three things: structural demand growth, innovation leadership, and the quiet compounding of an unusually high-quality business model.

Start with demand. The global animal health market was valued at about $48 billion in 2024 and is projected to grow around ten percent a year through the end of the decade, potentially reaching $113 billion by 2033. That growth is being pulled by two long-running forces. In developed markets, pets keep moving up the family hierarchy, and spending per animal rises with it. In emerging markets, more protein consumption means larger, more industrial livestock systems—and more spending to keep herds and flocks healthy.

Zoetis is positioned to benefit from both. Its companion animal portfolio rides the pet humanization wave in the U.S., Europe, and Japan. Its livestock portfolio tracks rising protein demand in regions like Latin America, Southeast Asia, and Africa. And aquaculture—built through PHARMAQ—puts Zoetis in what is often described as the fastest-growing protein category in the world. The breadth matters. But so does the structure: Zoetis is the only large-cap company that is entirely focused on animal health, without an internal competition for capital against a Keytruda or a diabetes franchise.

Then there’s innovation. Zoetis consistently invests around seven percent of revenue into R&D—roughly $660 million—and it has said it has twelve potential blockbusters in development, defined as products that can exceed $100 million in annual revenue. That pipeline sits on top of a track record that’s hard to overstate: Zoetis has repeatedly launched products that didn’t just win share, they reset standards of care. Apoquel is still a defining drug in canine dermatology more than a decade after launch. Simparica Trio became the combination parasiticide leader in just a few years.

And the pipeline isn’t only about incremental tweaks. Lenivia, the next-generation long-acting monoclonal antibody for osteoarthritis pain in dogs, is designed to provide up to three months of relief from a single injection, versus Librela’s monthly dosing. If it reaches broad approval and adoption, it could do two things at once: expand the market by making treatment even easier, and potentially soften some of the concerns that have complicated Librela’s rollout.

Finally, diagnostics gives Zoetis a second growth engine with a different economic shape than drugs. Diagnostics can be platform-based and repeatable: instruments installed in clinics, consumables reordered continuously, high switching costs once workflow is built around the system. If Zoetis keeps expanding its point-of-care footprint and reference lab network, diagnostics can become strategically central, not just additive.

Through the lens of Hamilton Helmer’s 7 Powers, Zoetis checks multiple boxes. It has scale economies as the biggest pure-play, with global manufacturing and distribution that can run at lower unit costs than smaller competitors. It has meaningful switching costs in diagnostics via installed instruments and consumable lock-in. It has brand and relationship depth with veterinarians built over decades of clinical education and sales support. And it has a cornered resource in regulatory and market-access know-how across 100+ countries—institutional capability that takes years to replicate.

Porter’s Five Forces also looks favorable.

Barriers to entry are high. Animal drugs still require years of development, clinical data, regulatory submissions across geographies, and pharmaceutical-grade manufacturing. A new entrant can spend heavily for a long time before earning its first dollar—and it would still be up against incumbents with decades of data, relationships, and distribution.

Buyer power is fragmented. Zoetis sells into thousands of veterinary clinics, producers, and retailers, with no single buyer dominating revenue. That fragmentation limits aggressive pricing pressure from any one customer.

Supplier power is moderate. The manufacturing demands are specialized, but Zoetis has invested in integration and scale over time, reducing dependence on any single external supplier.

Threat of substitutes is low in innovative biologics, where veterinary generic and biosimilar pathways are less mature than in human pharma. There isn’t a direct veterinary equivalent of the Hatch-Waxman framework that streamlined human generics.

Competitive rivalry is real, but generally rational. With a growing market, the fight tends to show up in innovation, lifecycle management, and geography more than all-out price wars.

The Bear Case

The bear case also reduces to three themes: Librela, competitive erosion, and normalization.

Librela is the most immediate and emotionally charged risk. Adverse event reports, FDA scrutiny, and the European Commission investigation have placed a cloud over what was meant to be Zoetis’s next category-defining launch. If the safety debate intensifies—or if regulators impose additional restrictions—it could hit Librela’s revenue, but also spill into confidence around the broader monoclonal antibody platform, including Solensia and next-generation products like Lenivia and Portela.

Generic and biosimilar competition is the longer-burn concern. Veterinary products have often enjoyed longer lifecycles than human drugs, but that advantage isn’t guaranteed forever. As products like Apoquel age, the question becomes not whether competitive pressure arrives, but how quickly it ramps and how much pricing power it takes with it. Biosimilar pathways for veterinary biologics are still less established than in human medicine, but they are evolving. Faster-than-expected erosion would pressure the premium margins that help fund Zoetis’s R&D engine.

Normalization is the subtlest risk—and potentially the most important over the next several years. The pandemic pet adoption boom pulled demand forward from 2020 through 2023. As that cohort of new owners matures, and as cost-conscious younger owners become a larger share of the market, growth could cool. Kristin Peck’s February 2026 comments about greater price sensitivity and tighter budgets among Gen Z and Millennial pet owners suggested Zoetis was already seeing early signs.

Livestock adds another layer of uncertainty. Even with solid growth, it remains exposed to agricultural cycles, trade dynamics, and regulatory pressure to reduce antibiotic use in food-producing animals—especially in the EU, and increasingly elsewhere. Over time, those trends can reshape demand across meaningful parts of the livestock pharmaceutical portfolio.

Competition isn’t standing still either. Elanco, the Eli Lilly spinoff that acquired Bayer Animal Health in 2020, has been investing heavily in its companion animal pipeline. Boehringer Ingelheim acquired Saiba Animal Health in 2024 to strengthen its pet therapeutics portfolio. And IDEXX remains the dominant diagnostics player, with far greater scale than Zoetis’s still-growing diagnostics business. Taking share in diagnostics while simultaneously funding leadership in pharmaceuticals, biologics, and livestock is a multi-front execution challenge—and those are hard to sustain indefinitely.

Finally, valuation raises the stakes. At a trailing P/E of roughly twenty-two times, the market is paying for continued premium performance. That means less room for error: a growth miss, margin compression, or a re-acceleration of Librela concerns can trigger a meaningful reset in expectations.

Key KPIs to Watch

For anyone tracking Zoetis from here, two metrics matter most:

First, companion animal organic revenue growth. It’s the clearest read on whether the pet humanization thesis is still translating into durable demand for Zoetis’s highest-margin products. And the mix matters: healthy growth should come from both price and volume, not price alone.

Second, Librela and the broader OA pain franchise trajectory. This is Zoetis’s flagship bet for the next chapter of growth. Whether that franchise stabilizes, recovers, or continues to slip will be a real-time verdict on the company’s monoclonal antibody platform—and on whether the Nexvet-derived biologics strategy can deliver another Apoquel-sized win.

Epilogue

On a February morning in 2013, a Spanish-born economist rang the opening bell at the New York Stock Exchange and sent a brand-new public company into the world. Twelve years later, that company had more than doubled its revenue, multiplied its market value several times over, and become the clear global leader in animal health.

What makes Zoetis so fascinating isn’t just the growth. It’s the mechanism. This is a story about focus—about what happens when a great business gets separated from a structure that quietly holds it back. Inside Pfizer, animal health was strong but perpetually competing: for capital against blockbuster human drugs, for management attention against higher-profile priorities, for strategic oxygen against the next patent cliff. Independence changed the incentives overnight. Zoetis could invest like an animal health company, plan like an animal health company, and—crucially—be valued like an animal health company. The market rewarded that clarity with a premium that Pfizer’s conglomerate wrapper was never going to unlock.

There’s an irony here that corporate finance people love: Pfizer created tremendous shareholder value by letting this asset go. The IPO and exchange offer helped Pfizer navigate the Lipitor era and strengthen its balance sheet. At the same time, Zoetis—freed from the “other” bucket—went on to create far more value as a standalone than it ever could have as a line item inside a pharma giant. It wasn’t a zero-sum breakup. It was a rare case where both sides won, which is usually the signature of a spinoff done right.

The choices that shaped that outcome aren’t hard to trace.

Pfizer chose to spin Zoetis rather than sell it outright, preserving the culture, talent, and institutional memory built over seven decades. Zoetis chose innovation over harvesting—building new standards of care with products like Apoquel, Cytopoint, and Simparica Trio instead of simply squeezing the legacy portfolio. It chose to push into diagnostics, betting that being embedded in clinic workflow—with instruments and consumables reordered every day—could be more strategic, and more durable, than episodic drug sales alone. And it chose to pioneer monoclonal antibodies in animals, reaching for a new therapeutic frontier even though that kind of leap inevitably brings new kinds of risk.

The next chapter will be shaped by forces both within and outside management’s control. Librela will resolve one way or another, and that outcome will shape how the industry thinks about monoclonal antibodies for chronic pain in pets. Diagnostics will either scale into a major, defensible platform or remain an important but secondary business alongside pharmaceuticals and biologics. Emerging markets may deliver the livestock growth that demographics suggest—or they may continue to be slowed by infrastructure gaps and fragmented regulation. And pet humanization, the secular engine under so much of the last decade, will face its next test: not whether people love their pets, but how spending holds up when budgets tighten.

There’s also a convergence story hiding in plain sight. The boundary between human and animal health keeps getting blurrier. Diseases jump species. Antimicrobial resistance doesn’t care whether the antibiotic was prescribed in a hospital or a barn. And the biologics playbook Zoetis used for dogs and cats draws directly from the toolchain of human pharma. A company that sits at that intersection—disease biology, global regulation, high-quality manufacturing, and population-scale logistics—may find its strategic importance rising in ways that aren’t fully captured in a quarterly model.

What does seem clear is that animal health is no longer a pharmaceutical afterthought. It’s a large, growing, strategically important industry in its own right. And Zoetis—more than any other company—helped pull it into that reality. The business Pfizer cast off didn’t just survive on its own. It became something bigger than its parent ever needed it to be.

Recent News

Zoetis reported Q4 2025 results on February 12, 2026. Revenue came in at $2.39 billion, ahead of consensus estimates, and adjusted EPS of $1.48 also topped expectations. Even so, the stock fell about five percent after CEO Kristin Peck warned that U.S. companion animal spending remained under pressure and competition was heating up.

The Librela story kept getting more complicated through late 2025 and into 2026. After the FDA’s December 2024 “Dear Veterinarian” letter and the May 2025 research documenting musculoskeletal adverse events, Zoetis updated Librela’s label and ramped up veterinarian education efforts. Management said monthly sales trends were stabilizing, but the near-term damage was visible: Q4 Librela revenue declined thirty-two percent.

Zoetis’s next attempt at expanding the osteoarthritis franchise is Lenivia, a long-acting monoclonal antibody designed to provide up to three months of relief per injection in dogs. Lenivia received Canadian approval in Q3 2025 and a positive opinion from the European Medicines Agency. Launches in Canada and the EU were expected in the first half of 2026, with U.S. approval anticipated in 2027.

In November 2025, Zoetis launched Vanguard Recombishield in the U.S., a recombinant kennel cough vaccine featuring what the company described as the first and only vaccine with pertactin protein for an optimized immune response.

That same month, Zoetis completed its acquisition of Veterinary Pathology Group, a leading diagnostic laboratory group in the UK and Ireland, extending its diagnostics footprint in Europe.

In December 2025, Zoetis completed a convertible bond offering that supported a $1.75 billion stock repurchase program, a clear signal that management viewed the shares as attractive long-term value.

For fiscal 2026, the company guided revenue of $9.825 billion to $10.025 billion—three to five percent organic operational growth—and adjusted diluted EPS of $7.00 to $7.10.

Sources and References

Company Filings and Investor Materials

Zoetis Inc. Annual Report (Form 10-K), filed with the U.S. Securities and Exchange Commission, fiscal years 2013–2025

Zoetis Inc. Quarterly Reports (Form 10-Q), various quarters

Zoetis Inc. IPO Prospectus (Form S-1), filed August 10, 2012

Zoetis Inc. Q4 and Full Year 2025 Earnings Release, February 12, 2026

Zoetis Inc. Q4 and Full Year 2024 Earnings Release

Zoetis Investor Day presentations, various years

Key Articles and Analysis

Juan Ramón Alaix, “The CEO of Zoetis on How He Prepared for the Top Job,” Harvard Business Review, June 2014

FDA Center for Veterinary Medicine, “Dear Veterinarian Letter: Librela (bedinvetmab injection),” December 16, 2024

Frontiers in Veterinary Science, research on Librela musculoskeletal adverse events, May 9, 2025

Industry Research

Grand View Research, “Animal Health Market Size & Trends Analysis Report,” 2024

MarketsandMarkets, “Veterinary Pharmaceuticals Market,” 2026

American Pet Products Association (APPA), National Pet Owners Survey, various years

Regulatory Filings

FDA approval letter for Solensia (frunevetmab injection), January 13, 2022

FDA approval letter for Librela (bedinvetmab injection), May 5, 2023

FDA approval letter for Simparica Trio, February 27, 2020

USDA license for Vanguard Recombishield, March 4, 2025

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube