Zomedica: The $200 Million Meme and the Race for the Vet Clinic

I. Introduction: The "Tiger King" Inflection Point

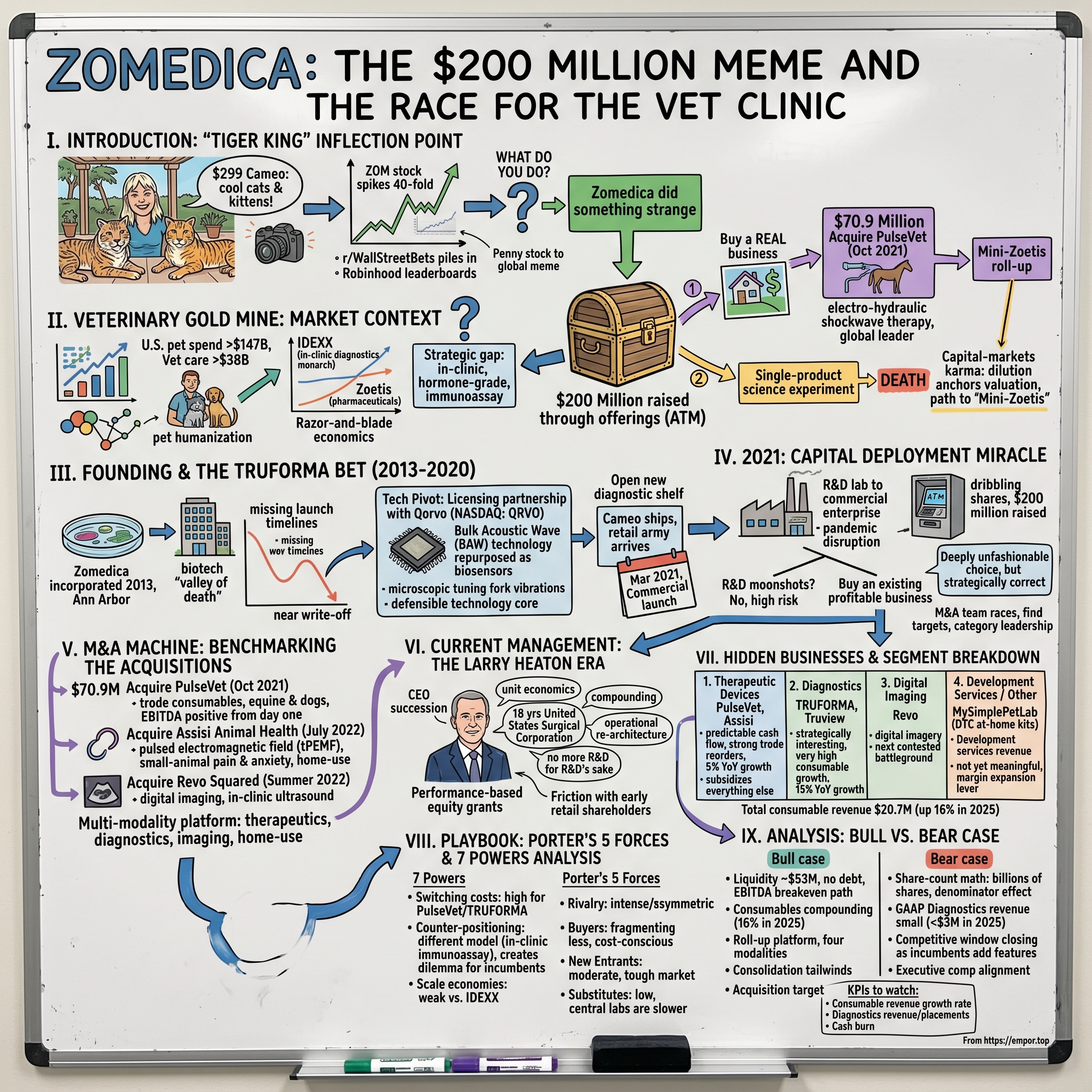

In early January 2021, somewhere between the COVID lockdowns and the GameStop short squeeze, a 59-year-old retired big-cat sanctuary operator from Tampa, Florida sat on a sunny patio, looked into a smartphone camera, and read out a $299 Cameo script for "all the cool cats and kittens" who were watching at home. Carole Baskin, freshly minted as a global meme thanks to Netflix's Tiger King, was casually plugging a small Michigan-based veterinary diagnostics company called Zomedica and its forthcoming point-of-care platform, TRUFORMA. The video posted to YouTube on January 8. Within four trading days, the stock had soared by triple digits.1

The company at the receiving end of that endorsement was not a household name. Zomedica Corp., listed on the NYSE American under the ticker ZOM, had been a $0.07 penny stock — a near-zombie biotech with no commercial revenue, an unproven hardware product, and a market cap that wouldn't have purchased a single mid-Manhattan office floor. Within weeks, ZOM was trading just shy of $3.00, a roughly 40-fold move from its 52-week low.2 Reddit's r/WallStreetBets piled in. Robinhood's "most actively traded" leaderboard featured Zomedica alongside AMC and BlackBerry. By mid-January 2021, penny stocks like ZOM accounted for as much as 18% of total U.S. equity volume on certain trading days.2

Now imagine you are the CFO of that company. You spent eight years grinding through the "valley of death" — the pre-revenue purgatory where biotech CEOs go to die. You have maybe nine months of cash. And then, almost overnight, the public market hands you a microphone, a moonshot multiple, and an open-ended ATM facility. What do you do?

If you are AMC, you use it to refinance debt. If you are GameStop, you let the chairman pivot the company into NFTs. If you are Hertz, you try to issue more shares before the SEC shows up. But Zomedica did something genuinely strange in the meme-stock pantheon: it took the money and bought a real business.

Over the course of 2021, Zomedica raised nearly $200 million through at-the-market offerings — capital that, in a normal universe, would have taken a company of its size a decade to assemble.3 Then, in October 2021, it deployed roughly a third of that war chest in a single move, paying $70.9 million to acquire PulseVet, the global leader in electro-hydraulic shockwave therapy for horses and dogs.4 In a span of nine months, ZOM transformed itself from a single-product science experiment into the unlikely nucleus of a diversified animal-health roll-up — a kind of Mini-Zoetis assembled almost entirely from retail-investor enthusiasm.

This is the story of how a "Tiger King" cameo became a strategic option, why veterinary medicine is one of the most under-appreciated growth markets in the developed world, and what happens when management treats a meme-induced bubble not as a windfall but as a one-shot, never-again chance to bootstrap a real company. It is also a study in capital-markets karma: the same dilution that gave Zomedica its lifeline now anchors its valuation, and the per-share math from 2021 will haunt every quarterly print for years to come.

We'll travel from a microfluidics lab in Ann Arbor, through a Bulk Acoustic Wave licensing deal with one of the largest semiconductor companies on the planet, into the buyout of a horse-shockwave franchise that most stock-pickers had never heard of, and end with a bull-versus-bear case for what ZOM has actually become. Strap in. The road from a $0.07 ticker to a $32-million-revenue point-of-care platform is more interesting than most things in the meme-stock graveyard.5

II. The Veterinary Gold Mine: Market Context

To understand why Zomedica's transformation matters, you have to first appreciate how unusual veterinary medicine is as a sector. There is a phrase that gets thrown around at every animal-health investor day: the "humanization of pets." It sounds like the kind of generic deck-slide cliché that dies the moment you press it. But unlike most marketing buzzwords, this one has the data to back it up.

Walk into a typical American household and you'll find a dog or cat treated with the kind of medical attention once reserved for grandparents — annual blood panels, dental cleanings, MRI scans, behavioral therapy, even targeted oncology treatment. U.S. consumers spent over $147 billion on their pets in 2023, with veterinary care alone exceeding $38 billion and growing in the high single digits annually.6 During the great inflation scare of 2022, vet spending didn't slow. During the regional banking crisis of 2023, vet spending didn't slow. There is something almost spiritual about the resilience of pet-care wallet share — owners cut their own dental visits before they cut Bella's.

The two giants who own this gold mine are 艾迪克斯 IDEXX Laboratories ($IDXX) and 硕腾 Zoetis ($ZTS). IDEXX, headquartered in Westbrook, Maine, is the in-clinic diagnostics monarch. Zoetis, spun out of Pfizer in 2013, dominates pharmaceuticals, vaccines, and parasiticides like Apoquel and Simparica Trio. Together they trade at multiples that would make most enterprise-software CFOs blush — IDEXX at low- to mid-double-digit revenue multiples through most of the past decade, Zoetis at high-twenties P/E ratios.7 Why? Because their economics resemble the most beautiful business model in capitalism: razor-and-blade.

When IDEXX places a Catalyst One chemistry analyzer or a ProCyte Dx hematology unit in a clinic, it isn't really selling a machine. It's planting a recurring-revenue annuity. The hardware is a customer-acquisition cost; the consumable test slides, reagents, and per-test cartridges are the actual product. Switching costs are brutal — once a clinic's veterinary technicians, software workflows, and reference range databases are calibrated around IDEXX's instruments, ripping them out is the operational equivalent of replacing the plumbing while the patient is on the table.

Now here's where it gets interesting. The veterinary diagnostics market splits into two universes. The first is the "send-out" world: a vet draws blood from a Labrador with suspected hypothyroidism, ships the sample to a central reference lab (typically IDEXX's or Antech's), and gets results back in 24 to 48 hours. The second is the "point-of-care" or POC world: the vet runs a test on equipment in the clinic and gets answers in 8 to 20 minutes, often before the dog has finished trembling on the exam table.

POC is the holy grail. It is faster, generates more billable visits, lets the vet prescribe on the spot, and dramatically improves the client experience. But POC has historically been limited to a narrow menu — basic chemistry panels, complete blood counts, urinalysis, and a handful of rapid antigen tests for parvovirus or feline leukemia. The hard stuff — endocrinology, hormone assays, allergy panels, exotic biomarkers — has stubbornly stayed in the central lab. The biology is too finicky, the antibody chemistry too sensitive, the engineering too hard to miniaturize.

Which leads us to the strategic gap. Every animal-health CEO in 2015 looked at the same map and saw the same blank quadrant: in-clinic, hormone-grade, immunoassay-class diagnostics. Whoever cracked that quadrant could potentially open a multi-hundred-million-dollar greenfield, untouched by the entrenched IDEXX moat — at least until IDEXX inevitably copied it. The technology problem looked like a moonshot. The commercial prize looked like the kind of opportunity that justified moonshot risk. And in 2013, in a small Michigan office, that is exactly the bet a microbiologist named Gerald Solensky Jr. set out to make.

III. Founding & The TRUFORMA Bet (2013–2020)

Zomedica was incorporated in Ann Arbor in 2013 — a stone's throw from the University of Michigan's veterinary medicine ecosystem and walking distance from one of the densest concentrations of biotech startups in the Midwest.8 Founder Gerald Solensky Jr. was not a glamorous figure in the mold of Theranos's Elizabeth Holmes or even of the typical med-tech serial founder. He was a microbiology-trained operator with a lifelong obsession around small-animal health. The company's earliest pitch decks framed the opportunity simply: vets needed better, faster diagnostic tools, and the existing cohort of test platforms had been designed for human medicine and grafted awkwardly onto animals.

The first few years were the classic biotech "valley of death." There was no product. There was no revenue. There were grant applications, prototype iterations, and the long, slow assembly of intellectual property around microfluidics-based detection. By 2016, the company needed real public-market capital, and Zomedica went public on what was then the Toronto Venture Exchange and shortly after on the NYSE American, raising a modest sum that bought roughly 24 to 30 months of runway.9

The technical pivot that defined the company's identity came not from biology at all but from an unlikely corner of the semiconductor industry. In 2018, Zomedica announced a licensing partnership with 致博 Qorvo (NASDAQ: QRVO), the multibillion-dollar radio-frequency chip maker whose components live inside almost every smartphone on Earth.10 The technology in question was Bulk Acoustic Wave, or BAW — the same thin-film resonator chemistry that filters out unwanted radio frequencies in 4G and 5G handsets. Qorvo's engineers, intrigued by the possibility that ultra-precise mechanical resonators could be repurposed as biosensors, had been quietly working on a diagnostic application of the technology for years.

Here is the simplest way to understand BAW: imagine a tiny, microscopic tuning fork that vibrates at a known frequency. Coat the surface of that fork with antibodies designed to grab a specific molecule — say, thyroid-stimulating hormone in a cat. When the molecule binds, it adds mass to the resonator, and the vibrational frequency shifts. Measure the shift, and you have measured the concentration of the molecule. It's a frequency-domain assay rather than a chemistry-and-color-change assay, which is why it can theoretically achieve laboratory-grade sensitivity in a hand-portable footprint. It's also why nobody else in veterinary medicine had it — you cannot invent BAW chemistry from scratch in a startup. You have to license it from a company like Qorvo whose RF business has spent half a billion dollars maturing the underlying physics.

That partnership turned out to be the single most important commercial decision in Zomedica's pre-meme history. It gave the company a defensible technology core, a credible Tier-1 industrial partner (the kind whose name reassures both regulators and capital markets), and a road map for an entire menu of in-clinic immunoassays — starting with thyroid (T4, TSH), adrenal (cortisol, eACTH), and inflammation markers like fPL/cPL pancreatic lipase. If it worked, Zomedica wouldn't have to compete with IDEXX on the chemistry it already owned. It could open an entirely new diagnostic shelf in the clinic.

But "if it worked" is doing a lot of heavy lifting. Between 2018 and 2020, Zomedica burned through capital at a clip that any biotech investor will recognize — clinical validation studies, USDA and FDA equivalence work, manufacturing scale-up, sales force pre-hiring. The company missed several launch timelines. By the back half of 2020, its share price was floating below a dollar, the bid-ask was wider than a Michigan pothole, and the prevailing narrative was that Zomedica was about to become another quiet write-off in the long graveyard of single-platform medical-device startups. A delisting warning from NYSE was a real possibility. The math of dilution looked ugly: you can only issue so many shares at $0.10 before there is no equity left for anyone.

The platform finally launched commercially in March 2021 — but by then, the entire context around the company had been violently rewritten. The Cameo had already shipped. The retail army had already arrived. And the company that had spent eight years trying to build a product from a base of technical merit suddenly found itself with a base of capital so large that the strategic question shifted overnight. It was no longer "will TRUFORMA work?" It was "what else can we buy?"

IV. 2021: The Capital Deployment Miracle

Most meme-stock stories follow the same arc. A struggling business catches an unjustified bid, management issues a token amount of stock to plug a balance-sheet hole, the stock retraces, and the brief window of mispricing closes with everyone roughly where they started. The pattern is so consistent that it's nearly a market law. The exception that makes the law worth restating is what Zomedica did in the first half of 2021.

The mechanics of the capital raise were almost surgical. Rather than rush a marketed follow-on offering — which would have signaled distress and capped the price — Zomedica leaned into an at-the-market (ATM) program. ATM facilities allow companies to dribble shares directly into the open market over time, taking the prevailing trading price. Done badly, ATMs are death by a thousand paper cuts. Done well — into a euphoric tape with deep retail liquidity — they can monetize a bubble without ever signaling that you know it's a bubble. Through Q1 and Q2 of 2021, Zomedica issued shares almost continuously into the meme-driven volume, ultimately raising approximately $200 million in fresh equity.11 To put that in perspective: the company's entire market capitalization a year earlier had been a fraction of that figure. They had, in effect, created a decade of R&D budget out of a single cycle of internet-driven enthusiasm.

The cultural transformation inside the company during those months is worth pausing on. Zomedica had been built like a research lab. Most of its hires had Ph.D.s. The marketing team was a handful of people. There were no regional sales managers, no key-account directors, no clinic-relationship specialists. Suddenly, the company had to flip from being a science project to being a commercial enterprise — and do so while a global pandemic disrupted clinic visits, supply chains, and trade-show schedules.

Then-CEO Robert Cohen, who had taken over leadership in 2020, made the call that most likely defined the next five years of the business. Rather than spend the windfall on doubling the R&D budget or chasing a second technology platform from scratch, he framed the decision as a portfolio question: would $200 million go further as twenty more years of internal product development, or as the down payment on an existing, profitable, channel-rich business? Internal R&D had a multi-year, low-probability conversion into commercial revenue. An acquisition would deliver instant cash flow, an installed base, a sales force, and — crucially — relationships with the very veterinarians Zomedica needed to sell TRUFORMA into.

If you have been around capital markets long enough, you'll recognize this as a deeply unfashionable choice in 2021. The era's playbook was the opposite. Companies were spinning out, not bolting on. Capital was supposed to fund organic moonshots. Yet the boring decision — buy something that already works — turned out to be the strategically correct one. The TRUFORMA hardware launch in March 2021, while encouraging, was generating consumable revenue in the low six figures per quarter. To grow into the cash position they had just raised, Zomedica needed an installed base they could not realistically build organically before the cash burned out.

The company also recognized something subtle about the meme-stock window: it was a one-shot. ATM offerings can only run while there is bid behind the stock. The day the meme energy dissipated, the door to dilution-at-favorable-prices would slam shut. So management raced. They built out an M&A team practically overnight, retained advisors, and went looking for targets that fit a very specific profile: profitable, vet-clinic-channel adjacent, with category leadership and limited overlap with the giants. The PulseVet thesis was forming, even before the deal terms were on the table.

The deeper lesson here, and the reason Acquired listeners should care, is that capital allocation and capital availability are different problems with different time scales. Most management teams, given an unexpected pile of cash, treat it as a permission slip to do more of what they were already doing. Zomedica's board treated it as a permission slip to do something fundamentally different. The willingness to abandon the founding identity — to stop being primarily an R&D bet and start being primarily a commercial roll-up — is the kind of decision that, in retrospect, looks obvious but in the moment requires a lot of organizational courage. By the time the leaves turned in October, the first shoe was about to drop.

V. The M&A Machine: Benchmarking the Acquisitions

If you were a veterinarian who treated horses in Texas, Kentucky, or the United Arab Emirates in 2021, there is a very good chance you knew the name PulseVet long before you knew the name Zomedica. PulseVet — the trade name of Pulse Veterinary Technologies, headquartered in Alpharetta, Georgia — built a global franchise on a deceptively simple proposition: a non-invasive shockwave device that accelerated tendon and ligament healing, addressed osteoarthritis pain, and reduced reliance on systemic anti-inflammatories in equine patients. The category is called electro-hydraulic shockwave therapy, and PulseVet was the unambiguous global leader, with an installed base in clinics, racing stables, and ambulatory equine practices across more than 30 countries.4

On October 1, 2021, Zomedica announced it had acquired PulseVet for approximately $70.9 million in a combined cash-and-stock transaction.4 The deal closed within weeks, an aggressive timeline for a transaction of that complexity. To appreciate the strategic logic, you have to understand what Zomedica was actually buying. PulseVet wasn't a product; it was a system: capital equipment installed in clinics, plus a recurring stream of "trode" consumables (the wearable applicators that contact the patient's body during treatment). It was, in other words, a textbook razor-and-blade business — exactly the model Zomedica was trying to replicate at TRUFORMA but had not yet fully proven.

Now to the benchmarking question every Acquired episode obsesses over: did they overpay? On a multiple of trailing revenue, the deal landed somewhere in the 5-to-6x neighborhood — material, but not absurd. For comparison, IDEXX traded at roughly 13-15x revenue through most of 2021, and Zoetis at high-single-digit revenue multiples for a substantially less-pure-play diagnostics business.7 More importantly, PulseVet was profitable at the EBITDA line on day one of being inside Zomedica. That single fact transformed Zomedica's financial profile: the consolidated entity was no longer a pure cash-burning R&D shop, it was a hybrid — a profitable therapeutic-device segment subsidizing a growth-stage diagnostics segment. For investors, the change was psychological as much as financial. The company suddenly had a floor.

The PulseVet deal also gave Zomedica something that no amount of hiring could have built: a sales force that already had relationships with thousands of equine, mixed-practice, and high-end small-animal clinics globally. When the time came to introduce TRUFORMA assays into those same clinics, the door was already open. Cross-selling into an installed channel is the single most powerful lever in healthcare distribution, and Zomedica had effectively bought a key into the building.

Round two came in July 2022 with the acquisition of Assisi Animal Health, a New York-based company specializing in targeted Pulsed Electromagnetic Field (tPEMF) therapy.12 If shockwave therapy is the equine and orthopedic flagship, tPEMF is the small-animal pain-and-anxiety play. Assisi's flagship products — the Assisi Loop for inflammation and pain, and Calmer Canine for separation anxiety — extended Zomedica's therapeutic-device franchise into the home-use and home-prescribed channel, an entirely different sales geometry from PulseVet's in-clinic capital-equipment model. Acquisition price terms were not fully disclosed but the deal was structured as an asset purchase, materially smaller than PulseVet.12

The third move, executed roughly in parallel during the summer of 2022, was the acquisition of Revo Squared, the developer of the MicroView digital imaging platform — Zomedica's beachhead into in-clinic ultrasound and digital imaging, the next contested battleground in vet-tech.13 Imaging, like diagnostics, is a hardware-plus-software-plus-services business with strong recurring revenue characteristics. By 2022, IDEXX, Heska (since acquired by Antech), and a handful of imaging specialists were all racing to bundle ultrasound, X-ray, and AI-driven image analysis into a single workflow tool for the modern clinic. Revo gave Zomedica a credible foothold without having to build a vendor platform from scratch.

Stepping back, the strategy rotates into focus. Each acquisition was small enough not to bet the company, yet meaningful enough to add a new modality. PulseVet brought regenerative therapy and recurring trode consumables. Assisi brought home-use anxiety and pain. Revo brought imaging optionality. TRUFORMA, the homegrown product, brought the in-clinic immunoassay platform. Together they form what management started calling a "multi-modality" platform — code, in plain English, for: we are no longer a one-product company, and we have multiple ways to win in a single clinic. This is the Zoetis playbook, scaled down by a factor of fifty. And it is the strategic frame that turns Zomedica from a meme-stock relic into something more interesting: a small-cap roll-up with a real shot at category relevance.

VI. Current Management: The Larry Heaton Era

If the meme cycle was the inflection point and the M&A spree was the strategic pivot, the operational re-architecture of Zomedica is largely the work of one man: Larry C. Heaton II. Heaton joined the company as President in October 2021 — the exact same month the PulseVet deal was announced — and was elevated to Chief Executive Officer shortly thereafter as part of a planned succession from Robert Cohen.14 The timing was not a coincidence. The board had decided that the company needed a different kind of leader for what came next, and they had quietly recruited him before the PulseVet ink was even dry.

Heaton's resume is the kind that doesn't fit on a single LinkedIn screen. He spent eighteen years at United States Surgical Corporation, the wound-closure giant, ending as President and Chief Operating Officer from 1998 to 2000.14 After USSC, he moved through a series of CEO roles at smaller medical device companies — VioOptix in tissue oximetry, Curon Medical in gastrointestinal devices, Response Genetics in oncology genomics, Cardiox in structural heart and liver diagnostics, and most recently Flowonix, an implantable drug-delivery business serving pain and spasticity patients.14 What unites those stops isn't a single therapeutic area; it is a single skill: commercializing a hardware-plus-consumable medical device into specialist clinical channels. That is exactly the muscle Zomedica needed to develop, and Heaton arrived already flexing it.

His operating style is, by all accounts, the polar opposite of the founder-CEO archetype. Where founder Solensky was the company's visionary, comfortable spending years validating biology and chemistry, Heaton is the kind of executive who reads a quarterly P&L the way a sommelier reads a wine label. He talks publicly about the company in the careful, sequenced cadence of someone who has run earnings calls for two decades — strategic priorities, near-term milestones, midterm targets, long-term vision. He doesn't promise revolution. He promises compounding.

The cultural shift inside the company, in the years following his arrival, has been substantial. Headcount in commercial roles expanded materially, with sales representatives realigned into modality-specific pods (PulseVet, Assisi, TRUFORMA, Imaging) but with cross-pollination KPIs that incentivize a single rep to introduce more than one Zomedica product into a single clinic. The R&D function, while still funded, is no longer setting the pace of the company — the commercial calendar is. Heaton has been quoted saying, in effect, that "no more R&D for R&D's sake" is the operating principle. Every new program now gets benchmarked against an explicit commercial milestone before it advances.[^15]

Compensation structure under Heaton has been reshaped to align with that philosophy. Recent proxy disclosures show executive equity grants that are increasingly weighted toward performance-based RSUs tied to revenue targets and milestones around adjusted EBITDA breakeven, rather than time-vested grants alone. The message to the executive team is unambiguous: you get paid when shareholders get paid, and you get paid more when the company hits specific commercial milestones, not when you simply show up.15

The non-founder, professional management style is occasionally a source of friction with longtime retail shareholders. Founder-led companies often command emotional loyalty from their early investor base, and when a meme-stock cohort transitions to professional management, there is invariably a period of "I miss the old vibe." Heaton's communications strategy seems calibrated to that audience — frequent investor outreach, regular video updates, accessible Q&A formats — without conceding any ground on the operational discipline. It is a balancing act that few CEOs of post-meme companies have managed to pull off without alienating either the institutional or the retail base.

What investors are really getting in Heaton is a CEO who thinks in unit economics. How many TRUFORMA placements per quarter? At what consumable attach rate? At what gross margin per assay? How does the PulseVet trode reorder cadence compare to industry benchmarks? These are the questions he grinds on, publicly and privately, and they are the questions the next chapter of the Zomedica story will be judged on.

VII. Hidden Businesses & Segment Breakdown

Spend an hour reading Zomedica's quarterly disclosures and a different company comes into view than the one most casual observers remember from the meme era.16 The 2021 narrative — single-product, pre-revenue, retail-driven — has been replaced by a segmented operating story with real cash flow, real growth, and several embedded option values that the market has not entirely priced.

The largest and most predictable segment is Therapeutic Devices, comprising PulseVet and Assisi. In fiscal 2025, this segment generated approximately $26.1 million of revenue, growing 5% year-over-year, with strong contribution from PulseVet's "trode" consumable reorders.5 Trodes — the disposable applicators that wear down over hundreds of treatments — are the textbook recurring-revenue lever. They generate ratable, predictable cash flow that compounds with the installed base. Every time PulseVet installs another shockwave system in a horse clinic, it is essentially planting an annuity that pays out for the next several years. The 5% growth rate looks slow until you remember that the segment is already mature, profitable, and globally distributed. It is the cash engine that subsidizes everything else.

The most strategically interesting segment, however, is Diagnostics — TRUFORMA, plus the more recently launched TRUVIEW digital cytology platform and VetGuardian remote vital-signs monitor. Diagnostics revenue was approximately $2.8 million in 2025, up 15% year-over-year, with very high underlying growth in TRUFORMA assay consumables.5 Across the entire company, total consumable revenue (PulseVet trodes plus TRUFORMA and Truview cartridges) reached $20.7 million in 2025, up 16%.5 Read that again. The recurring half of the business is now compounding at the mid-teens, off a base that is already meaningful. That is the Holy-Grail dynamic IDEXX investors have been paying mid-double-digit revenue multiples for over the past decade. Zomedica is, on a vastly smaller scale, beginning to print the same kind of metric.

The newer, less-discussed expansion lane is Digital Imaging, anchored by the Revo-derived MicroView platform. This is not yet a meaningful revenue contributor on its own, but it is the strategic optionality slot. Imaging is one of the few in-clinic categories where IDEXX has been historically weak, and where smaller specialists have accumulated customer relationships without the kind of overwhelming switching-cost moat that exists in chemistry and hematology. If Zomedica can credibly bundle imaging with diagnostics in a single clinic pitch, the cross-sell math becomes very interesting.

There is also a fourth segment — quietly emerging — that long-time ZOM watchers refer to as the "hidden play." It consists of MySimplePetLab, the direct-to-consumer at-home pet diagnostic kits offering, and the Development Services line item, which generated approximately $3.1 million in 2025 from contract research and platform-license arrangements.5 DTC vet diagnostics is a market that essentially didn't exist a decade ago and that has been growing in fits and starts as pet parents adopt the same self-care behaviors they've adopted for their own bodies — at-home cholesterol kits, microbiome panels, hormone monitors. If Zomedica's DTC offering achieves any meaningful scale, it will be the cherry on top of the in-clinic strategy and a margin-expansion lever rather than a strategic pivot.

The composite picture is of a company that has, almost without anyone noticing, assembled a four-modality animal-health platform on a sub-$200 million revenue base, with consumables compounding in the mid-teens and gross margins in the high 60s.5 There are not many small caps in the U.S. equity market that match that profile. Whether that ultimately translates into per-share value or gets diluted away is the central question of the next two sections.

VIII. Playbook: Porter's 5 Forces & 7 Powers Analysis

Step back from the company and put the whole thing on a strategy whiteboard. Acquired listeners will recognize the rhythm: through Hamilton Helmer's Seven Powers and Michael Porter's Five Forces, what does Zomedica actually have, what does it lack, and where does it rank against the industry's giants?

Start with Switching Costs. This is the most clearly earned of Zomedica's powers. A vet clinic that purchases a PulseVet shockwave system pays five-figure capital equipment dollars, trains its staff, integrates the device into treatment protocols, and starts billing patients on procedure codes built around that platform. Ripping it out to switch to a competitor would require not just buying new hardware but unlearning a workflow. Same dynamic, slightly weaker, applies to TRUFORMA: once a vet has a reagent panel, calibration history, and a TRUFORMA-trained technician, the cost to swap to a competing immunoassay platform is non-trivial. This is the same lock-in mechanic that has made IDEXX and Roche Diagnostics so durably valuable in their respective universes. Zomedica's footprint is much smaller, but the mechanic is real.

Second, Counter-positioning. This is a more subtle and arguably more interesting power for Zomedica. The Big Two — IDEXX and Zoetis — have built their entire businesses around two structural choices: send-out reference labs and centralized in-clinic chemistry. Their P&L, sales force compensation, capital base, and reagent supply chain are all optimized around those choices. When Zomedica enters with a different model — in-clinic immunoassay using BAW resonators — the incumbents face a classic innovator's dilemma. They could replicate the technology, but doing so cannibalizes their own send-out lab revenue. They could buy Zomedica, but at what price after another two years of compounding? The longer Zomedica grows in the gap that the incumbents are structurally reluctant to enter, the harder the competitive response becomes.

Third, Scale Economies. This is where Zomedica is structurally weak, and it is unlikely to ever rival IDEXX's purchasing power, R&D budget, or global service infrastructure. The "meme-induced scale" of 2021 helped enormously — the company has roughly $53 million in liquidity at year-end 2025 and effectively no debt, which is a rare and valuable position for a sub-$50 million revenue company.5 But financial liquidity is not the same as operating scale. In any drawn-out price war on consumables, Zomedica is at a structural disadvantage.

Fourth, Branding and Network Economies — both essentially absent at the parent level, though PulseVet has a meaningful brand among equine veterinarians.

Now Porter's Five Forces, applied to the segment.

Rivalry. Intense and asymmetric. IDEXX has placed analyzers in approximately 70% or more of U.S. companion-animal clinics. Zoetis competes on the pharmaceutical side. Antech (now under Mars), Heska (acquired by Antech in 2023), and a long tail of regional reference labs cover the rest. Zomedica is a mosquito at this party in absolute terms, though its share of relevant niches (equine shockwave, in-clinic endocrine assays) is materially higher.

Bargaining Power of Buyers. The buyers are veterinary clinics, and they are price-sensitive but desperate for labor-saving and revenue-enhancing technology. The buyer is also, importantly, fragmenting less than it once did — corporate consolidators like Mars Petcare's VCA, NVA (now part of JAB Holding), and Banfield are buying up independent clinics and centralizing purchasing decisions. That trend cuts both ways. Centralized buyers can squeeze on price, but they also award standardized contracts that, if Zomedica wins, dramatically accelerate placement.

Bargaining Power of Suppliers. Moderate. Qorvo is a key technology supplier on BAW chips and the relationship is contractual. Trode manufacturing for PulseVet has more than one source. Component supply has not historically been a binding constraint.

Threat of New Entrants. Moderate. Vet diagnostics is hard — regulatory clearance, antibody chemistry, channel access — and the three-letter incumbents have deep moats. But the "diagnostics-as-a-platform" world is now attracting human-health crossover entrants, and any disruption in that adjacent market could spill over.

Threat of Substitutes. Low for now. The substitute for in-clinic POC is the central reference lab, which is slower and more expensive per workflow.

The composite read: Zomedica has built a real, defensible niche on the back of switching costs and counter-positioning, but it operates inside a hostile ecosystem dominated by larger and better-capitalized rivals. The 2021 meme bubble bought it a seat at the table. Whether it can stay there is a function of execution and capital discipline.

IX. Analysis: Bull vs. Bear Case

Walk into a room of small-cap fund managers and mention ZOM, and you will almost immediately hear two diametrically opposed stories. Both are coherent. Both are supported by the same set of facts. The difference is in time horizon and in tolerance for share-count math. Let's lay them out cleanly.

The Bull Case, in its purest form, is a survivor's narrative. Zomedica has approximately $53 million in liquidity at the end of 2025, no debt, and a multi-segment business growing roughly 17% on the top line.5 That is enough cash to plausibly reach adjusted-EBITDA breakeven without further dilution — a remarkable achievement for a company that, only five years earlier, was a sub-dollar penny stock. Gross margins in the high 60s mean each incremental dollar of revenue carries strong incremental contribution, and the consumable mix is rising. Total consumable revenue compounded at 16% in 2025, which is the kind of figure investors pay premium multiples for in IDEXX or 罗氏 Roche Diagnostics.5

Zoom out and the strategic frame is even more bullish. The roll-up of PulseVet, Assisi, Revo, and TRUFORMA gives Zomedica a four-modality platform across therapeutics, diagnostics, imaging, and home-use that no other sub-billion animal-health company possesses. The pet-spending macro is structurally favorable. The corporate-clinic consolidation trend (Mars/VCA, JAB/NVA) raises the value of being a multi-modality vendor that can satisfy a chain's whole portfolio. And Zomedica is small enough to be an acquisition target — both Mars Petcare and Zoetis have consolidated similar bolt-ons in recent years, and the strategic logic of a Mars or Zoetis bid is not difficult to construct.

The Bear Case is a dilution story dressed in operating-margin anxiety. Yes, Zomedica raised $200 million at the meme peak, but it did so at the cost of issuing roughly a billion new shares. The current count of shares outstanding is the size of mid-cap corporations, and that share count anchors any per-share metric for the next several years. Even if Zomedica triples its revenue — an aggressive but not crazy assumption — the per-share earnings impact is muted by the denominator. Bears will also point out that the diagnostics segment, despite years of investment, generated less than $3 million of GAAP revenue in 2025, and that TRUFORMA's commercial momentum, while real, has not yet reached a flywheel that obviously threatens IDEXX.5

The other bear concern is competitive: IDEXX and Zoetis are not standing still. IDEXX has been progressively adding endocrine assays and exotic biomarker tests to its in-clinic menu, and there is no structural reason it cannot eventually replicate, at scale, anything Zomedica builds — at which point Zomedica's counter-positioning advantage erodes. The bear thesis essentially holds that the window of competitive immunity is shorter than the bull thinks, and that the dilution math is permanent.

Layered on top are the second-order diligence considerations that long-term investors should at least track: the proxy treatment of executive compensation in a long-tenured, post-meme company; the distribution of the share base across retail and institutional ownership (still heavily retail-skewed for a small-cap, which can produce volatility on news days); the auditor's commentary in the latest 10-K — clean, but with the standard discussion of going concern that any sub-scale med-device company carries; and the natural question of whether the cash position is being deployed at attractive risk-adjusted IRRs or held primarily for optionality.16 None of these are red flags. They are, however, the texture of the story that doesn't fit on a one-page summary.

The KPIs to actually watch — the metrics that will tell you whether the bull or the bear is winning — are narrower than most coverage implies. Zero in on three:

- Consumable revenue growth rate — the closest single number to a measure of installed-base health and razor-and-blade flywheel velocity.

- Diagnostics segment revenue growth and TRUFORMA placements — the leading indicator of the long-term strategic thesis (in-clinic immunoassay).

- Cash burn / liquidity runway — the inverse of the dilution risk, and the test of whether management can execute to breakeven without returning to the equity well.

Everything else — gross margin movement, segment mix, geographic expansion — flows downstream from those three.

X. Epilogue & Final Reflections

There is a passage in Hamilton Helmer's 7 Powers where he points out that durable competitive advantage is rarely the product of any single strategic decision; it is the accumulation of choices made under constraint, where each constraint shapes the next. Zomedica is a near-textbook case study of that idea. The constraint in 2013 was a lack of money, which forced the bet on a single-platform technology. The constraint in 2018 was a lack of credibility, which forced the Qorvo partnership. The constraint in 2020 was a lack of revenue, which forced the slow grind toward TRUFORMA's launch. The constraint in 2021 was, briefly and bizarrely, a lack of anything but money, which forced the lightning-fast pivot into M&A.

The first reflection — and the one founders should sit with — is that the willingness to take the money when it's offered is itself a form of strategic intelligence. Most of the meme-stock survivors of 2021 are diminished today, but Zomedica is bigger and more diversified, and the difference comes down to a board that recognized that retail enthusiasm was a window, not a regime. They took the money. They deployed it within nine months. They ignored the temptation to over-engineer the perfect deal and instead bought a profitable cash-generating asset that gave them immediate optionality. That sequence will be studied in business schools for years.

The second reflection is about the transformation of identity. There is something almost philosophical about a company changing what it is. Zomedica started as an R&D bet, became a meme, and has slowly metabolized into something neither of those labels capture: a diversified small-cap animal health platform with real recurring revenue, real channel relationships, real customer switching costs, and a real seat at the multi-modality table. The price the market pays for that company is governed by share count, growth rate, and competitive risk — but the kind of company it has become has a permanence that no amount of bear-case dilution math can erase.

The third reflection — and the question every Acquired episode ends with — is whether Zomedica is, in the end, an acquisition target. The strategic logic for a Mars Petcare or a Zoetis or a 玛氏 Mars-controlled veterinary platform to buy ZOM is reasonable: a four-modality bolt-on with established channel access and a complementary diagnostics platform is the kind of asset that looks attractive at a control premium. The strategic logic for IDEXX to do it is less obvious — the diagnostics overlap creates regulatory and customer-conflict considerations. But the fundamental answer is that Zomedica's near-term destiny is in its own hands. If management executes through the next two years and crosses the EBITDA breakeven line, the company has the optionality to remain independent and compound on its own. If execution stalls, the bid becomes more compelling.

What the Carole Baskin moment ultimately gave Zomedica was not a stock price. Stock prices come and go. What it gave the company was time — five extra years of runway, deployed into a real platform, by a management team that took the gift seriously. Whether that translates into per-share returns for the cohort of investors who bought ZOM at $2.50 in February 2021 is a different question, governed by share count and entry price. But the company those investors funded, almost by accident, is now a real business — a multi-segment, multi-modality, real-revenue veterinary technology platform, competing for one of the most resilient end-markets in the developed world.

The cool cats and kittens, it turns out, picked a stranger and more interesting horse than they realized. The race to the vet clinic continues, and Zomedica — improbably, durably — is still in it.

References

-

Zomedica's Stock Spikes 90% And 'Tiger King' Star Carole Baskin Could Be The Reason — Benzinga, 2021-01-11 ↩

-

Penny stock Zomedica jumps 250% after someone paid Netflix star Carole Baskin $299 for a mention — Yahoo Finance, 2021-01-12 ↩↩

-

Zomedica Announces Record Fourth Quarter Revenue of $10.5 Million and Full Year Revenue of $32.0 Million for 2025 — PharmiWeb, 2026-03-16 ↩↩↩↩↩↩↩↩↩↩

-

The Veterinary Diagnostic Market Outlook — Fortune Business Insights ↩

-

Analysis of the Vet Health Roll-up Strategy — Reuters, 2021-08-16 ↩↩

-

Zomedica 10-K Annual Report for Fiscal Year 2023 — SEC EDGAR ↩

-

Qorvo and Zomedica Partner on Point-of-Care Diagnostics — Qorvo Newsroom, 2018-08-30 ↩

-

Zomedica Acquires Assets of Leading tPEM Company Assisi Animal Health — Nasdaq/Globe Newswire, 2022-07-18 ↩↩

-

Zomedica Acquires Revo Squared — Veterinary Practice News, 2022-07-20 ↩

-

Zomedica Appoints Larry Heaton as President and Announces CEO Succession Plan — Globe Newswire, 2021-10-04 ↩

-

Zomedica Announces Third Quarter 2025 Financial Results — Access Newswire, 2025-11-04 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube